corporate presentation september...

TRANSCRIPT

Corporate Presentation September 2014

Rev. 0914

2 | Page

Forward Looking Statement

This presentation contains forward-looking statements. Such forward-looking statements include but are not limited to that Cesca Therapeutics Inc. will provide unmatched world-class capability and service to its clients. These statements involve risks and uncertainties that could cause actual outcomes to differ materially from those contemplated by the forward-looking statements. A more complete description of risks that could cause actual events to differ from the outcomes predicted by our forward-looking statements is set forth under the caption "Risk Factors" in ThermoGenesis annual report on Form 10-K and other reports we file with the Securities and Exchange Commission from time to time, and you should consider each of those factors when evaluating the forward-looking statements. Contact: Cesca Therapeutics Inc. Website: http://www.cescatherapeutics.com Contact: Investor Relations +1-916-858-5107, or [email protected]

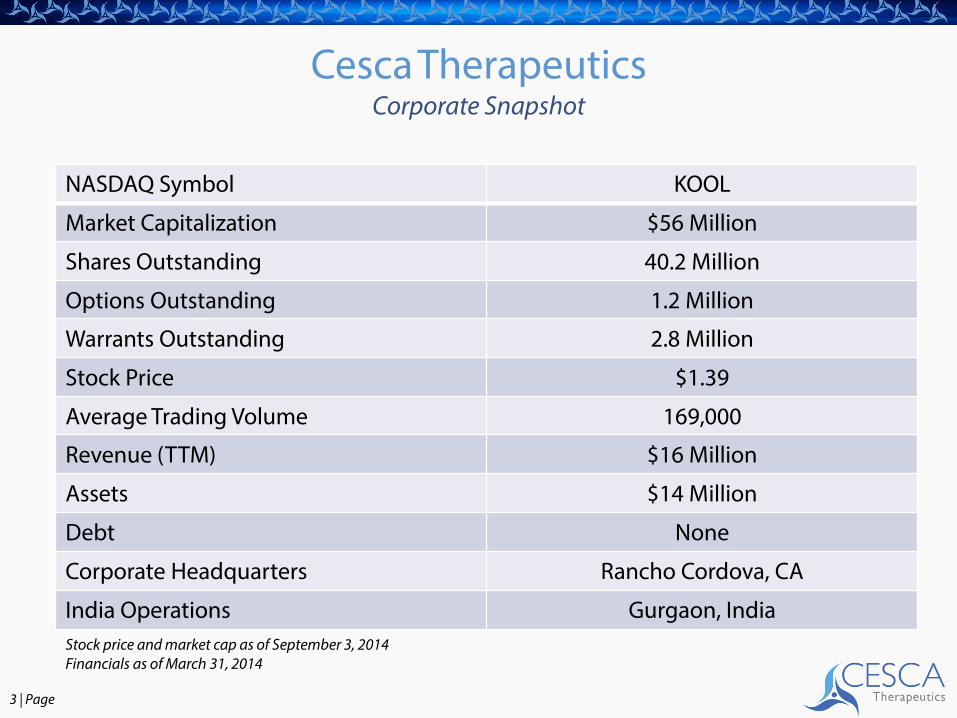

3 | Page

Cesca Therapeutics Corporate Snapshot

NASDAQ Symbol KOOL

Market Capitalization $56 Million

Shares Outstanding 40.2 Million

Options Outstanding 1.2 Million

Warrants Outstanding 2.8 Million

Stock Price $1.39

Average Trading Volume 169,000

Revenue (TTM) $16 Million

Assets $14 Million

Debt None

Corporate Headquarters Rancho Cordova, CA

India Operations Gurgaon, India Stock price and market cap as of September 3, 2014 Financials as of March 31, 2014

4 | Page

Cesca Therapeutics Regenerative Medicine Investor Checklist

• Safe? • Clinically effective? • Large markets? • Regulatory hurdles? • Cost effective/reimbursable?

5 | Page

Cesca Therapeutics An integrated regenerative medicine company

Uniquely positioned to be a best in class Integrated Regenerative Medicine Company

− Clinical Research Organization (Fortis embedded)

− Proprietary cell formulations

− Devices; patented platform technology

First commercially viable autologous cell therapy

− Safe & Effective; in the regulatory “sweet spot”

− Rapid; 60 minute bedside protocol

− Low cost delivery

Opportunity to create substantial shareholder value − Multiple therapies - 8 pilot & Phase 1b clinical trials

− Unlocks intrinsic value of multiples in regenerative medicine sector

− M&A/bolt on opportunities to help us further fill out our tools capabilities

6 | Page

Cesca Therapeutics Go-to-Market Success Formula

Autologous Cells, Minimally Manipulated

Naturally Safest, Regulatory Fast track

=

Bedside, Single Procedure 60 min

Total Process Control, +

CT Development Approach CT Product Attributes

Embedded CRO > 600 Trial Patients

+ =

+ Low COGS

= +

Proven Curative

Rapid CT Development & Commercialization

Multiple Shots on Goal

Blockbuster CT Treatments =

SurgwerksTM

1

2

3

7 | Page

Cesca SurgwerksTM

Indication specific POC process control

SurgWerks POC Advantages: • “Smart” cell formulation & verification

• Autologous (safe and fast)

• Data validated

• Structured, protocol driven

• Highly consistent

• Dose controlled

• FDA approved & practice of medicine friendly

• 600 patients treated across eight clinical indications

8 | Page

Fortis Partnership CRO embedded in New Delhi facility

Cesca is exclusive regenerative medicine provider to Fortis

• 72 hospitals (6 countries)

• 10,000 inpatient beds

• 15,000 outpatients per day

• Experienced clinical research staff

• 2x as many sites as Kaiser

Physician/patient access

World class clinical facilities and equipment

Lobby partner with government

Embedded CRO Benefits • Only global cell therapy CRO

• US FDA registered; FDA accepted foreign trial

• Over 600 patients treated

• Control over trial management

• Speed to completion

• 1/5 cost of US/ Europe patient related clinical trials

Rx Clinical Trial Advantage ($M) Pilot P1/P1b Total

Cesca Investment $2 $7 $9

US Equivalent Investment $17 $28 $45

Non-Dilutive Clinical Trial Funding Benefit $36

9 | Page

Clinical Trial Pipeline Blockbuster therapy candidates

$.7B

10 | Page

Clinical Trial Pipeline Major Milestones Substantial clinical value drivers

CLI Milestones Time Period

FDA IDE/PMA Pivotal Trial Approval March Qtr. 2015

Pivotal Phase Complete Late 2016

CLI PMA Approval/Commercialization Early 2017

BMT Milestones Time Period

ABO Mismatch FDA 510(K) Approval March Qtr. 2015

DCGI Haplo Phase I/II Trial Approval June Qtr. 2015

Haplo Full Market launch/Commercialization 2016

AMI Milestones Time Period

DCGI Phase II Trial Approval June Qtr. 2015

Phase II completed/Data Reported 2016

11 | Page

Critical Limb Ischemia Compelling clinical vascular results

All patients “no option” and near term leg amputation recommended

12 Month F/U Data

• Major Amputation Free Rate post SurgWerks™ Therapy = 82.4%

• Reduction in VAS Pain Score from 7.8±0.97 to 0.2±0.58

• Improvement in 6 minute walk test from 14.5m to 157m

• N=17 patients

Major Revascularization Trial Results

Completed Phase I/II

IDE PMA

Pivotal

Begin March 2015 Day 0 Day 365

12 | Page

• LVEF improvement = from 36% to 60%

• Stroke volume improvement = from 39.7cc to 80cc

• Scar remains 11% of total heart mass

• Normal life resumed

• N=1 patient (24 Mo F/U)

Cardiac Tissue Repair Trial Results

Acute Myocardial Infarction Compelling clinical cardiac results

Pilot Completed

Ph II

Begin June Qtr. 2015 (IDE PMA)

13 | Page

Bone Marrow Transplant Automating clinical major mismatch & haploidentical transplant

Improves Pediatric BMT (40% are mismatched)

• High - CD34 recoveries = 77.7%

• Low - hematocrit <12%

• Faster - Neutrophil engraftment = Day 18

• Faster - Platelet engraftment = Day 35

Haploidentical Clinical Results

Major ABO Clinical Results

Faster, Lower Cost,

Higher Cell Recovery

510(k) March Qtr. 2015

6,000 = new patients WW

$1,500 = Price of treatment

$9 M = Addressable market

• Reduces Expensive Reagent Usage

• Enables Cell Washing

6,000 = new patients India

$25,000 = Price of treatment

$150 M = Addressable market

Enabling 6k annual patient market in India

Plan to commercialize globally

Phase I/II June Qtr. 2015

14 | Page

Cesca Therapeutics Commercialization Advantage

15 | Page

Cesca Regulatory “Sweet Spot” Lower risk = speed to market

• IND/BLA • 3 Phase Trial • Higher Trial Patient Pop

• IDE/PMA • 2 Phase Trial • Lower Trial Patient Pop

16 | Page

Cesca SurgwerksTM

Sustainable differentiation

Significant commercial experience, proven technical reliability • Over 20,000 patients treated @ POC with Cesca Cell Technologies

• Over 600,000 cord samples processed (laboratory)

• Near six-sigma disposable quality levels

Clinically validated, proprietary protocols & method patents • Proprietary, smart platforms

• Proprietary cell formulations addressing multiple disease indications

• Pioneering with regulatory strategy to be first cell therapy in a box

IP Suite (device and algorithm patents) • 43 Design and device patents

• Three protocol provisional patents (6 indications)

• 8 pilot & phase 1b clinical trials

• 7 clinical algorithms

17 | Page

Cesca Therapeutics Market Cap Snapshot

Cell Therapy Peer Company TCKR Market Capitalization (000’S)

Aastrom Biosciences Inc. ASTM $27,000

Athersys ATHX $107,000

BioTime, Inc. BTX $220,000

Cytomedix, Inc. CMXI $47,000

Neuralstem, Inc. CUR $329,000

Cytori Therapeutics Inc. CYTX $104,000

Dendreon Corporation DNDN $216,000

NeoStem Inc. NBS $195,000

Osiris Therapeutics, Inc OSIR $474,000

Pluristem Therapeutics Inc. PSTI $195,000

StemCells Inc. STEM $102,000

Average Market Cap $183,000

Cesca Therapeutics KOOL $56,000

18 | Page

Management Highlights Chief Executive Officer & Director

Matthew T. Plavan - Leading Cesca since 2012, effected merger with TotipotentRX in 2014, served as COO and EVP Business Development, 2008-2010, CFO from 2005. Prior experience includes McKesson/Ernst & Young.

President & Director Kenneth L. Harris - Joined Cesca in February 2014 pursuant to merger. Prior experience includes Chairman and CEO of TotipotentRX /MK Alliance, Inc, and Corporate Senior Vice President and Global President of Biosciences of Pall Corporation.

Chief Financial Officer Dan T. Bessey - Joined Cesca in March 2013. Prior experience includes CFO of SureWest Communications and Vice President of Finance, Controller and Director of Corporate Finance.

Chief Biologist Mitch Sivilotti – Joined Cesca in February 2014 pursuant to merger. Prior experience includes President, Director and Chief Biologist of TotipotentRX/MK Alliance, Inc. and Pall Corporation.

VP, Quality & Regulatory Affairs

Raymond DeGrella – Consulted for Cesca as VP of Quality and Management Representative since 2012. In March 2014 assumed current role. Former experience includes Vice President Advanced Supply Chain of Beckman Coulter, and Abbott Laboratories.

VP, Operations Ken Pappa – Joined Cesca in April 2006 as Director of Finance and has held several managerial roles until October 2012 when he took on his current role. Prior experience includes Manufacturing Controller and Senior Operations Manager for Hewlett Packard-Agilent Technologies.

19 | Page

Cesca Therapeutics Regenerative Medicine Investor Checklist

Safe - Autologous Clinically effective - Yes Large markets - Multiple Regulatory hurdles - Lower Cost effective - Very Reimbursable – Well positioned

Thank you