corporate presentation (march)

TRANSCRIPT

1

Corporate PresentationMarch 2016

2

Disclaimer

The information contained in this presentation may include statements whichconstitute forward-looking statements, within the meaning of Section 27A of the U.S.Securities Act of 1933, as amended, and Section 21E of the U.S. Securities ExchangeAct of 1934, as amended. Such forward-looking statements involve a certain degree ofrisk and uncertainty with respect to business, financial, trend, strategy and otherforecasts, and are based on assumptions, data or methods that, although consideredreasonable by the company at the time, may turn out to be incorrect or imprecise, ormay not be possible to realize. The company gives no assurance that expectationsdisclosed in this presentation will be confirmed. Prospective investors are cautionedthat any such forward-looking statements are not guarantees of future performanceand involve risks and uncertainties, and that actual results may differ materially fromthose in the forward-looking statements, due to a variety of factors, including, but notlimited to, the risks of international business and other risks referred to in thecompany’s filings with the CVM and SEC. The company does not undertake, andspecifically disclaims any obligation to update any forward-looking statements, whichspeak only for the date on which they are made.

3

The Company

4

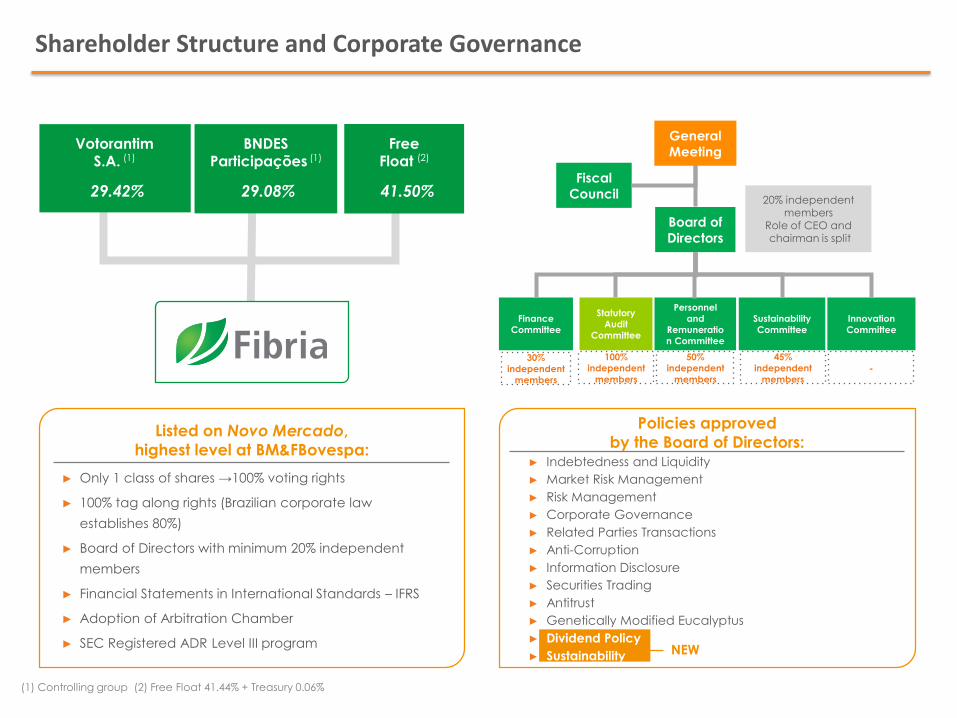

Shareholder Structure and Corporate Governance

(1) Controlling group (2) Free Float 41.44% + Treasury 0.06%

Votorantim S.A. (1)

29.42%

BNDESParticipações (1)

29.08%

FreeFloat (2)

41.50%

► Only 1 class of shares →100% voting rights

► 100% tag along rights (Brazilian corporate law

establishes 80%)

► Board of Directors with minimum 20% independent

members

► Financial Statements in International Standards – IFRS

► Adoption of Arbitration Chamber

► SEC Registered ADR Level III program

Listed on Novo Mercado,

highest level at BM&FBovespa:

Policies approved

by the Board of Directors:

Fiscal

Council

Board of

Directors

20% independent members

Role of CEO andchairman is split

Personnel

and

Remuneratio

n Committee

Statutory

Audit

Committee

Finance

Committee

Sustainability

Committee

Innovation

Committee

30%

independent

members

100%

independent

members

50%

independent

members

45%

independent

members-

General

Meeting

► Indebtedness and Liquidity

► Market Risk Management

► Risk Management

► Corporate Governance

► Related Parties Transactions

► Anti-Corruption

► Information Disclosure

► Securities Trading

► Antitrust

► Genetically Modified Eucalyptus

► Dividend Policy

► Sustainability NEW

5

A Winning Player

Port Terminal Pulp Unit

Três Lagoas

Santos

AracruzPortocel

Caravelas

BelmonteVeracel

Jacareí

Superior Asset Combination Main Figures – 2015

Pulp capacity million tons 5.300

Net revenues US$ billion 3.021

Total Forest Base(1) thousand hectares 969

Planted area(1) thousand hectares 568

Net Debt US$ billion 2.821

Net Debt/EBITDA (in Dollars)(2) X 1.78

Source: Fibria(1) Including 50% of Veracel, excluding forest partnership areas and forest bases linked to the sales of Losango and forest assets in Southern Bahia State. (2) For covenants purposes, the Net Debt/EBITDA ratio is calculated in Dollars.

6

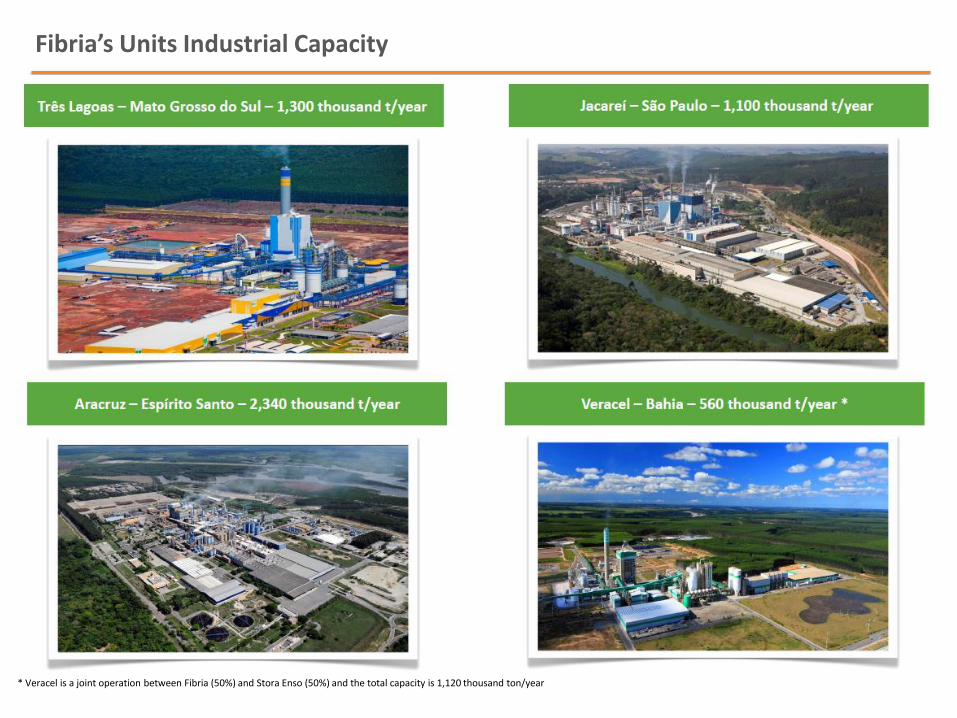

Fibria’s Units Industrial Capacity

* Veracel is a joint operation between Fibria (50%) and Stora Enso (50%) and the total capacity is 1,120 thousand ton/year

7

Fibria’s Strategy

8

Leadership Position

(1) Fiber Consumption, Recycled Fiber and Pulp: RISI | Market Pulp, Hardwood and Eucalyptus: PPPC Global 100 Report December 2015(2) Hawkins Wright – Outlook for Market Pulp, December 2015

Market Pulp Capacity Ranking 2015(2) (000t)

5,300

Recycled Fiber 242 million t

46% 54%

59%

18% 82%

59% 41%

41%

30% 70%

25%75%

Fiber Consumption412 million t

Pulp 169 million t

Chemical140 million t

Mechanical30 million t

Integrated Mills 83 million t

Market Pulp 57 million t

Hardwood31 million t

Other Eucalyptus Pulp producers:

16 million t

Softwood/Other 26 million t

Acacia/Other 9 million t

Eucalyptus21 million t

Industry Outlook(1)

0 2000 4000 6000

Canfor

Cenibra

Resolute Forest

Sodra

Domtar

Mercer

Eldorado

Weyerhaeuser

IP (excl. Ilim)

Ilim

Metsa Group

Georgia Pacific

Stora Enso

UPM-Kymmene

CMPC

Suzano

APRIL

APP

Arauco

Fibria

Bleached Softwood Kraft Pulp

Bleached Hardwood Kraft Pulp

Unbleached Kraft Pulp

Mechanical Pulp

9

Fibria’s Commercial Strategy

Source: Fibria – 4Q15

• Differentiation: Customized pulp products to specific paper grades

• Sole supplier to key customers

• Long term contracts

• Competitive logistics set up

Miami

Lustenau

Hong Kong

São Paulo

Net revenue by region

Fibria ‘s Offices

N.America

25%

L.America

8%

Europe

43%

Asia

24%

Fibria’s Pulp End Use

Tissue50%

Printing & Writing

35%

Speciatilies15%

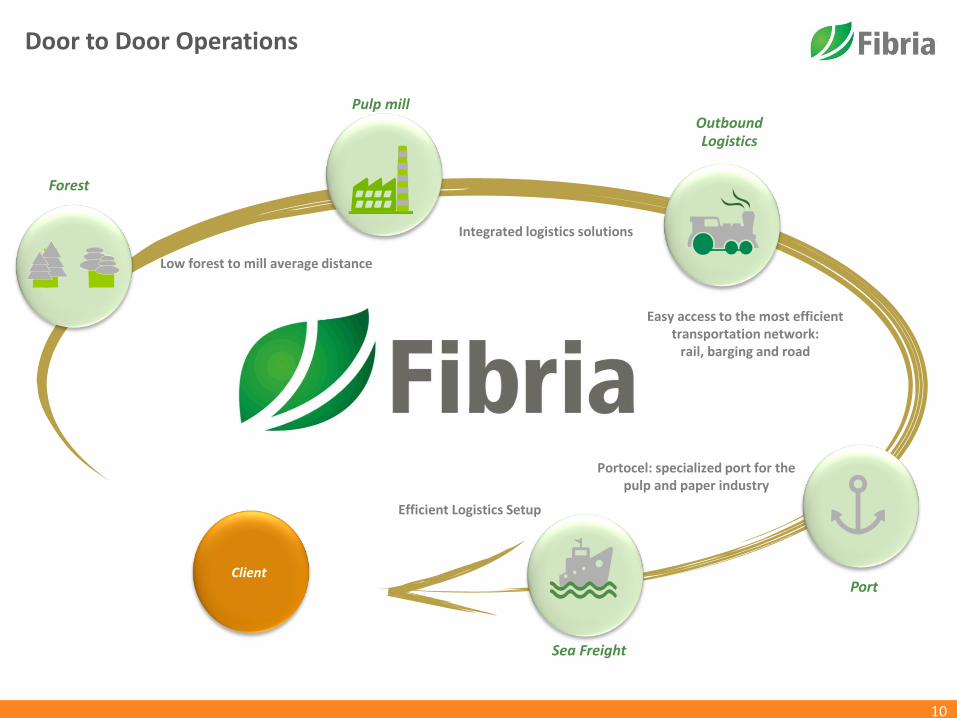

Forest

OutboundLogistics

Pulp mill

PortClient

Low forest to mill average distance

Easy access to the most efficienttransportation network:

rail, barging and road

Portocel: specialized port for the pulp and paper industry

Integrated logistics solutions

Efficient Logistics Setup

Sea Freight

Door to Door Operations

10

11

Pulp and Paper Market

12

Paper Consumption

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

CAGR 1996 – 2006Developed Markets: + 1.7%Emerging Markets : + 6.0%

85,291

117,611

15,548

37,474

P&W Consumption (000 tons)(1)

Tissue Consumption (000 tons)(1)

114,507

CAGR 2007 – 2016Developed Markets: - 4.0%Emerging Markets : + 4.1%

CAGR 1996 – 2006Developed Markets: + 2.4%Emerging Markets : + 6.9%

CAGR 2007 – 2016Developed Markets: + 1.4%Emerging Markets : + 6.7%

26,877

Source: RISI

13

Source: PPPC

Global Market Pulp Demand

Hardwood demand will continue to increase at faster pace than Softwood

Hardwood (BHKP) vs. Softwood (BSKP) (000 ton) Demand growth rate

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Hardwood Softwood

2014 - 2019 CAGR:Hardwood: +2.5%Softwood: +0.8% 000 ton 1999 2009 2019

Growth

1999-

2009

Growth

2009-

2019

Hardwood 16.3 24.8 33.8 52% 35%

Eucalyptus 6.0 15.9 24.1 165% 52%

Softwood 19.0 21.4 24.9 13% 16%

Market Pulp 35.3 46.2 58.7 30% 27%

Gross capacity addition should not be counted as the only factorinfluencing pulp price volatility….(1)

List Price bottoming at US$650/t in 2011 and US$724/t in 2014

Cap

acit

y (0

00

to

n)

BH

KP

pri

ces

-C

IF E

uro

pe

(U

S$/t

on

)

(1) Source: Hawkins Wright , Poyry and Fibria Analysis. Pulp price estimates according to Hawkins Wright (Dec/15), Brian McClay (Dec./15) and RISI (Jan/16)(2) Partially integrated production.

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

0

100

200

300

400

500

600

700

800

900

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Valdivia

APP Hainan

Veracel Nueva Aldea

Santa Fé

Mucuri

FrayBentos

KerinciPL3

Três Lagoas

Rizhao

APP Guangxi

ChenmingZhanjiang

EldoradoMontes del Plata

Maranhão

Guaíba II

APP South Sumatra(2)

Klabin

OjiNantong

Horizonte II

Source: PPPC and Fibria

Closures of Hardwood Capacity Worldwide(000 ton)

Capacity closures DO happen

-910

-85

-1,260

-1,180

-540-500

-105

-1,085

-445

-315

-580

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016-2017 E (1)

(1) As of January 2016 | 2016: -40kt Old Town (USA), -90kt Woodland (USA), -55kt Verso Wickliffe (USA), -120 April Kerinci (Indonesia) | 2017: -275kt Arauco Valdivia (Chile)

16

Tissue Market

(1) Source: RISI

Kg/capita/year

Per Capita Consumption of Tissue by Region, 2013(1)

Growth Potential

0

5

10

15

20

25

30

35

1991 1996 2001 2006 2009 2010 2011 2012 2013

N.America W.Europe E.Europe L.America Middle East

Japan China Asia FE Oceania Africa

LTM Growth of +4.2%

Million tons

World Tissue Consumption, 1991-2013(1)

24

15 15

12

76

5

1

0

5

10

15

20

25

30

N.America

WestEurope

Japan Oceania EastEurope

LatAm China Africa

17

Pulp Projects Backlog

Main Projects

Project Country Capacity Timing Status

Klabin Paraná Brazil 1.5 Mt* 2Q2016 Confirmed

APP South Sumatra Indonesia 1.5 Mt – 2.0 Mt 4Q2016 Confirmed

Fibria Três Lagoas II Brazil 1.75 Mt 4Q2017 Confirmed

• Minimum required return for new projects

• Closures due to increasing costs worldwide, reduction of maintenance capex (higher technical age of recovery boilers) and exchange rates

• Fiber substitution: Softwood x Hardwood and Recycled x Virgin Fiber

Main Questions About Capacity

Even though there is an extensive pulp projects backlog, there are important question marks regarding new projects

* 1.1 million tonnes of hardwood and 400 thousand tonnes of softwood

18

Financial Highlights

4Q15 Results

19

EBITDA (R$ million) and EBITDA Margin (%) – FX Sensitivity

906 1,007 1,1571,551 1,623

4Q14 1Q15 2Q15 3Q15 4Q15

EBITDA (R$ million)

EBITDA Margin

Average FX (BRL/USD)

Average pulp price - FOEX Europe (USD/t)

45%50% 50%

56% 54%734 749

779803 8032.54

2.87 3.073.54

3.84

Pulp Production and Sales (000 t) Pulp Net Revenues (R$ million)

1,982

2,761 2,962

4Q14 3Q15 4Q15

102% 102% 101%

1,381

1,275 1,297

1,410

1,298 1,308

4Q14 3Q15 4Q15Production Sales

Sales vs. production

20

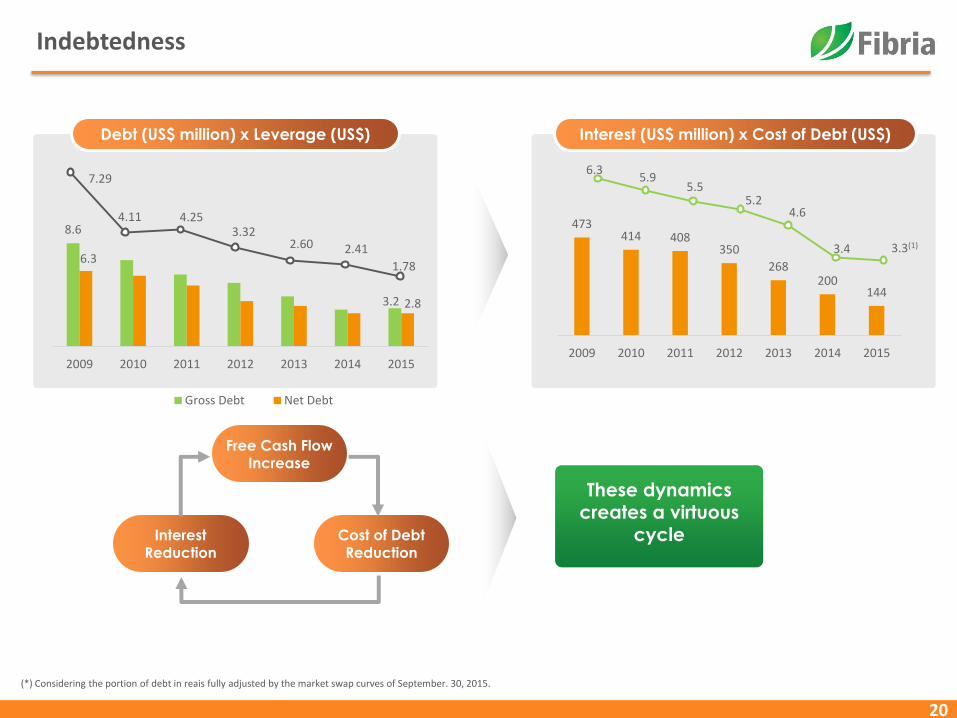

Indebtedness

Debt (US$ million) x Leverage (US$) Interest (US$ million) x Cost of Debt (US$)

Free Cash Flow Increase

Interest Reduction

Cost of Debt Reduction

These dynamics creates a virtuous

cycle

(*) Considering the portion of debt in reais fully adjusted by the market swap curves of September. 30, 2015.

8.6

3.2

6.3

2.8

2009 2010 2011 2012 2013 2014 2015

Gross Debt Net Debt

7.29

4.11 4.253.32

2.60 2.41

1.78

473414 408

350

268200

144

2009 2010 2011 2012 2013 2014 2015

6.35.9

5.55.2

4.6

3.4 3.3(1)

Debt Profile

Debt Amortization Schedule (US$ million)

Cost of Debt – Foreign Currency (% p.a.) Debt by Currency

3.7 % 3.8%

Dec/14 Dec/15

10%

90%

Local Currency

Foreign Currency

655

498

275274

477

812

299

485

25 11

606

Liquidity 2016 2017 2018 2019 2020 2021 2022 2023 2024

Pre-payment BNDES ECN ACC/ACE Voto IV Bonds ARC and Others Total

Cash on hand

Revolver

1,153

22

5,337

357

( 3,033 )

(830)(338)

518( 1,892 )595

AdjustedEBITDA

FX Debt MtMHedge

Net Interest Deprec., amortiz.and

depletion

Taxes Others Net Income

Non-recurringeffects

(1) Includes other exchange rate/monetary variations, other financial income/expenses and other operating income/expenses.

∆∆

Net Results (R$ million) – 2015

22

(1)

Dividend proposal of R$300 million, representing 87% of net income.