corporate presentation aug10x - fibr.infoinvest.com.br at the time, ... eucalyptus pulp shipments...

TRANSCRIPT

1

Corporate PresentationAugust 2010

Disclaimer

The information contained in this presentation may include statements which constituteforward-looking statements, within the meaning of Section 27A of the U.S. Securities Actof 1933, as amended, and Section 21E of the U.S. Securities Exchange Act of 1934, asamended. Such forward-looking statements involve a certain degree of risk anduncertainty with respect to business, financial, trend, strategy and other forecasts, andare based on assumptions, data or methods that, although considered reasonable by thecompany at the time, may turn out to be incorrect or imprecise, or may not be possible torealize. The company gives no assurance that expectations disclosed in this presentationwill be confirmed. Prospective investors are cautioned that any such forward-looking

2

will be confirmed. Prospective investors are cautioned that any such forward-lookingstatements are not guarantees of future performance and involve risks and uncertainties,and that actual results may differ materially from those in the forward-looking statements,due to a variety of factors, including, but not limited to, the risks of international businessand other risks referred to in the company’s filings with the CVM and SEC. The companydoes not undertake, and specifically disclaims any obligation to update any forward-looking statements, which speak only for the date on which they are made.

Agenda

The Company

Market Positioning

Pulp and Paper Market

3

2Q10 Financials

Corporate Restructuring

4

The Company

VCP and Aracruz merged to create Fibria

Shareholder Structure

Votorantim Industrial S.A.

BNDESPar Free Float

29.34% 30.42% (1) 40.17%

Treasury

0.07%

5

Veracel Celulose S.A.

50.0%50.0%

Conpacel

(1) Position as of June 30, 2010. BNDESPar has 21% linked to a shareholder’s agreement with VID during the first 3 years, and 10.9% during the following 2 years.

Improved Corporate Governance

Board Advisory CommitteesBoard of Directors

Audit and Risks

Personnel and Remuneration

����

����

Alexandre Gonçalves Silva Indicated by Votorantim

Alexandre Silva D’Ambrosio Indicated by Votorantim

Armando Mariante Carvalho Junior Indicated by BNDES

Eduardo Rath Fingerl Indicated by BNDES

6

Finance

Sustainability

����

����

João Miranda Indicated by Votorantim

José Armando de Figueiredo Campos Independent Member

Jose Luciano Penido Chairman of the Board

Raul Calfat Indicated by Votorantim

Wang Wei Chang Indicated by Votorantim

7

Market Positioning

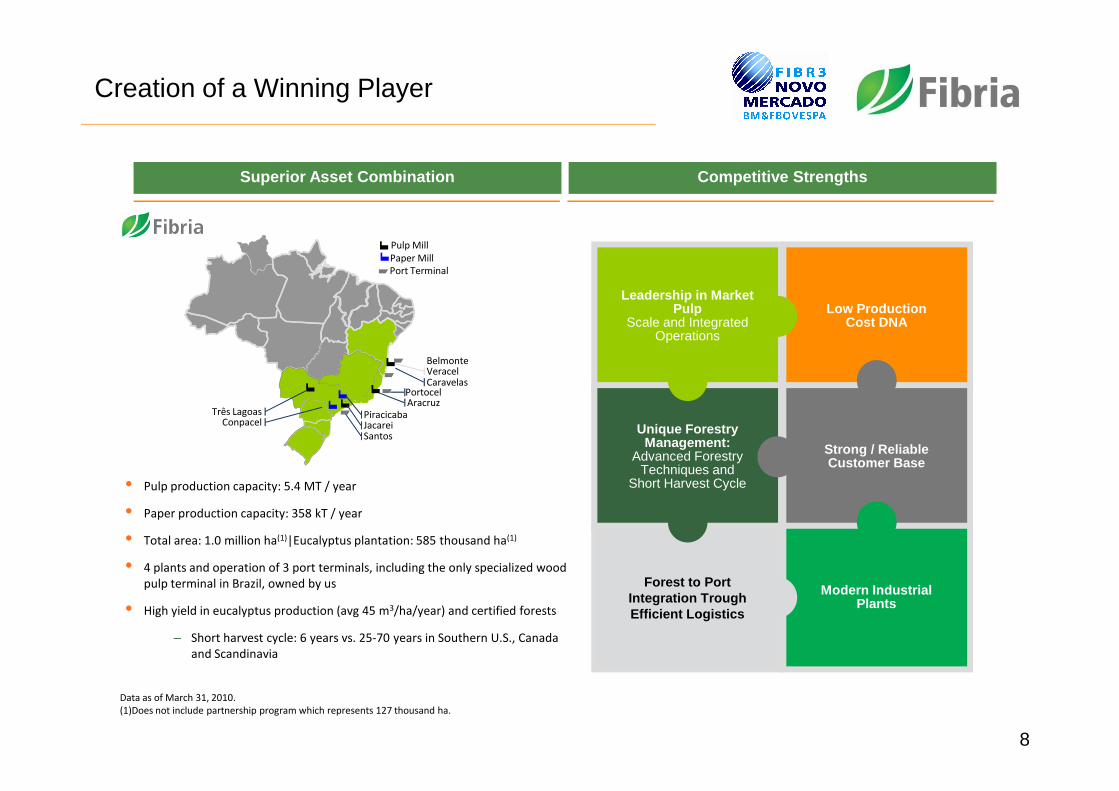

Creation of a Winning Player

Competitive Strengths

Pulp Mill

Paper Mill

BelmonteVeracelCaravelas

Portocel

Superior Asset Combination

Port Terminal

Leadership in Market Pulp

Scale and Integrated Operations

Low Production Cost DNA

8

• Pulp production capacity: 5.4 MT / year

• Paper production capacity: 358 kT / year

• Total area: 1.0 million ha(1)|Eucalyptus plantation: 585 thousand ha(1)

• 4 plants and operation of 3 port terminals, including the only specialized wood

pulp terminal in Brazil, owned by us

• High yield in eucalyptus production (avg 45 m3/ha/year) and certified forests

– Short harvest cycle: 6 years vs. 25-70 years in Southern U.S., Canada

and Scandinavia

PortocelAracruz

PiracicabaJacareiSantos

Três LagoasConpacel

Data as of March 31, 2010.

(1)Does not include partnership program which represents 127 thousand ha.

Unique Forestry Management:

Advanced Forestry Techniques and

Short Harvest Cycle

Forest to Port Integration Trough Efficient Logistics

Strong / Reliable Customer Base

Modern Industrial Plants

1.5

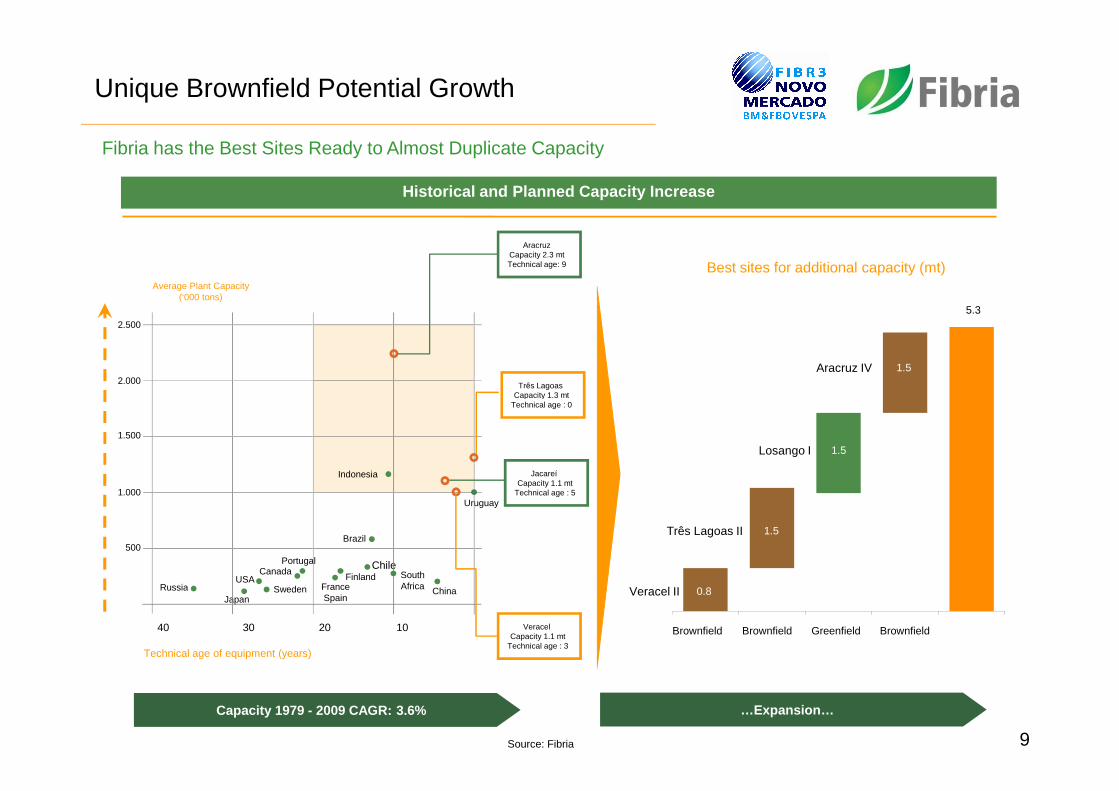

Unique Brownfield Potential Growth

Fibria has the Best Sites Ready to Almost Duplicate Capacity

Historical and Planned Capacity Increase

Aracruz IV

Best sites for additional capacity (mt)

AracruzCapacity 2.3 mtTechnical age: 9

Average Plant Capacity(‘000 tons)

2.500

2.000 Três LagoasCapacity 1.3 mt

5.3

9

Veracel II

Três Lagoas II

Losango I

Brownfield Brownfield Greenfield Brownfield

Source: Fibria

1.500

1.000

500

40 30 20 10

RussiaJapan

USASweden

CanadaPortugal

FinlandFranceSpain

ChileSouthAfrica China

Brazil

Indonesia

Uruguay

Technical age of equipment (years)

Capacity 1.3 mtTechnical age : 0

JacareíCapacity 1.1 mt

Technical age : 5

VeracelCapacity 1.1 mt

Technical age : 3

Capacity 1979 - 2009 CAGR: 3.6% …Expansion…

0.8

1.5

1.5

Undisputable Leadership in the Global Market Pulp

Pulp Production Capacity

2009E in ktons

5,400

Dominant Position in a Growing Market

1o

~ Twice The size

10Source: PÖYRY, 2007 / As for Market Pulp: Pulp and Paper Products Council (PPPC) 2009 and Fibria.(1) Market Share estimated considering 2009 nominal capacity.

2,44

2,18

2,00

Low Production Cash Cost DNA

Cash Costs (2)Fibria's Margin vc Macroeconomic Fundamentals (1)

155

243 238284 310

178232

178133 104 95

320225

199152 113

238 161

118133

151 155

468437 436 423

475

416393

296266 255 250(3)583

641

705

783

565

920

Average PriceBHKP (US$/ton) (1)

11

1,95 1,84

2,00

1,80

104 95

Iberia

(2) Source: Hawkins Wright Estimate 2Q10 (3) Fibria 2Q10 Cash cost without downtimes

Hardwood Cash Cost (US$/t) vs Capacity (kT)

0

100

200

300

400

500

600

0 2.000 4.000 6.000 8.000 10.000 12.000

US$/ton

Iberia

250

Capacidade (kT)

Exchange Rate Average(RS/US$)(1)

1.013 1.115880

2.196

1.697

730

35%38%

34%37%

28%

40%

2005* 2006* 2007* 2008 Pro Forma

2009 2Q10

(1) Average Price: FOEX | Exchange rate: Brazilian Central Bank

EBITDA Margin

EBITDA (R$ million)

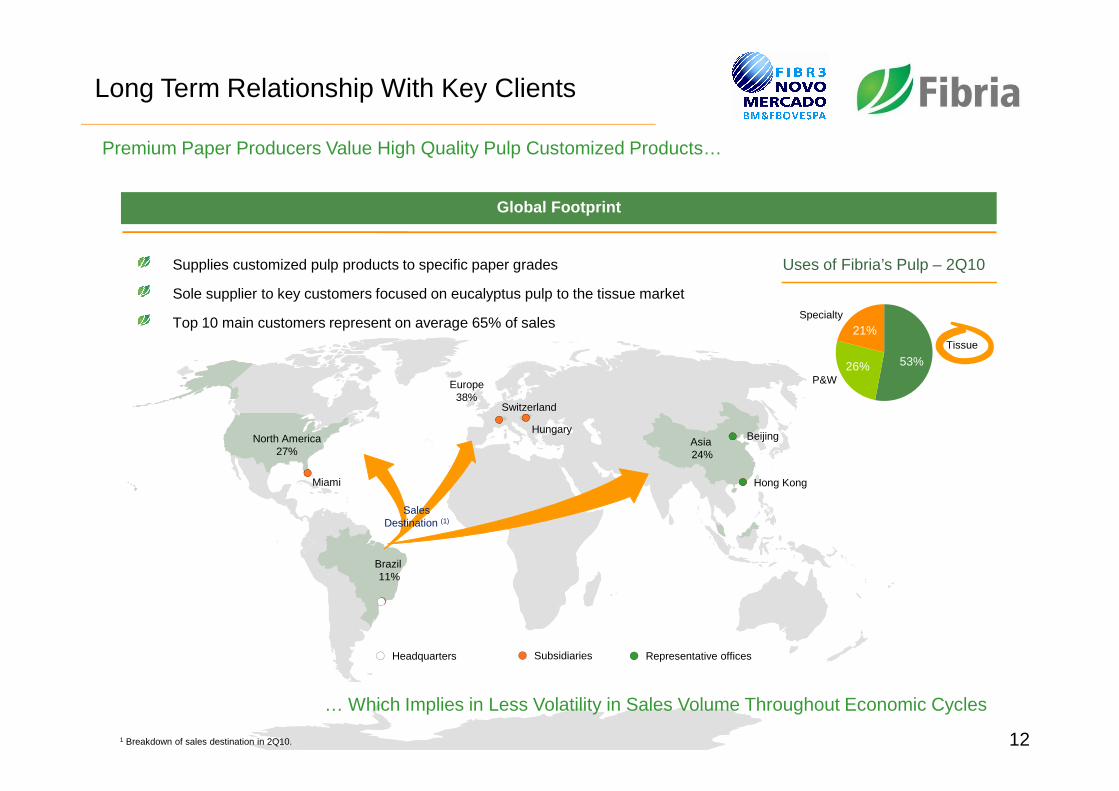

Long Term Relationship With Key Clients

Premium Paper Producers Value High Quality Pulp Customized Products…

Global Footprint

Supplies customized pulp products to specific paper grades

Sole supplier to key customers focused on eucalyptus pulp to the tissue market

Top 10 main customers represent on average 65% of sales

P&W

Tissue

Specialty

Uses of Fibria’s Pulp – 2Q10

Europe38%

53%26%

21%

12

NY004GAK_1.worNY004GAK_1.worNY004GAK_1.worNY004GAK_1.worNY004GAK_1.worNY004GAK_1.worNY004GAK_1.worNY004GAK_1.wor… Which Implies in Less Volatility in Sales Volume Throughout Economic Cycles

1 Breakdown of sales destination in 2Q10.

38%

North America27%

Asia 24%

Brazil 11%

Beijing

Switzerland

SalesDestination (1)

Miami Hong Kong

Hungary

Subsidiaries Representative officesHeadquarters

13

Pulp and Paper Market

Positive Commodity Cycle and Demand Recovery

World P&W paper shipments to capacityWorld market pulp shipments to capacity

91%89%

82%

86%

83%

79%

90%

77%

88%

92%

97%

86%

95%

92%93%

95%

90%92%

90%

86%

98%

91%

95%

87%87%

92%

89%

87%

97%

92%

85%

78%76%

79%79%77%

73%

79%79%78%

89%87%

86%

81%79%

88%87%

86%87%87%

14

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

World pulp consumers' days of supplyWorld pulp producers' average days of supply

Source: PPPC Global 100

Source: PPPC Global 100 Source: PPPC Global 100

Source: PPPC Global 100

1915

20

25

30

35

Mar

-05

Oct

-05

May

-06

Dec

-06

Jul-0

7

Feb

-08

Sep

-08

Apr

-09

Nov

-09

Jun-

10

25

10

20

30

40

50

60

Mar

-05

Oct

-05

May

-06

Dec

-06

Jul-0

7

Feb

-08

Sep

-08

Apr

-09

Nov

-09

Jun-

10

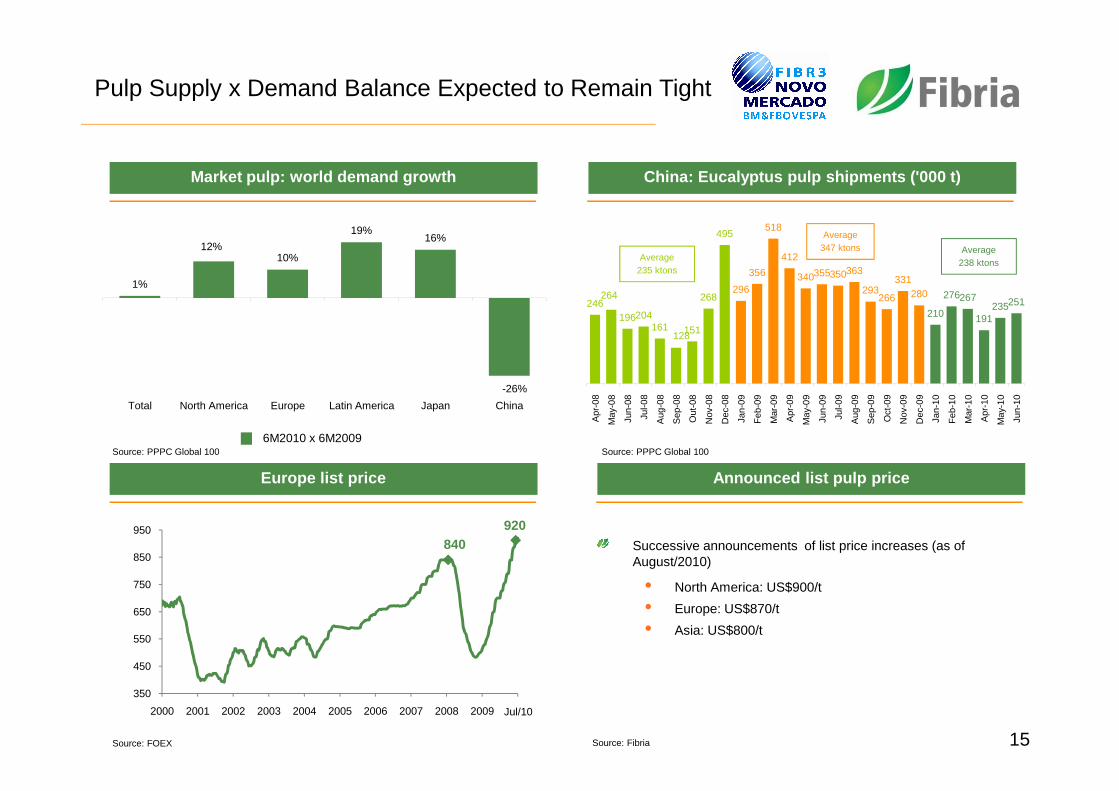

Pulp Supply x Demand Balance Expected to Remain Tight

China: Eucalyptus pulp shipments ('000 t)Market pulp: world demand growth

246264

196204161

128151

268

495

296

356

518

412

340355350363

293266

331280

210

276267

191235251

08 08 08 08 08 08 08 08 08 09 09 09 09 09 09 09 09 09 09 09 09 10 10 10 10 10 10

1%

12%10%

19%16%

-26%

Average235 ktons

Average347 ktons Average

238 ktons

15

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep

-08

Out

-08

Nov

-08

Dec

-08

Jan-

09

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Announced list pulp priceEurope list price

Source: Fibria

Source: PPPC Global 100 Source: PPPC Global 100

Source: FOEX

Total North America Europe Latin America Japan China

6M2010 x 6M2009

Successive announcements of list price increases (as of August/2010)

• North America: US$900/t

• Europe: US$870/t

• Asia: US$800/t

840920

350

450

550

650

750

850

950

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Jul/10

16

2Q10 Financials

2Q10 Performance

Pulp sales mixKey figures

2Q10 1Q10 2Q09 2Q10 vs1Q10

2Q10 vs2Q09

Pulp Production (1000t) 1,208 1,314 1,334 -8% -9%

Pulp Sales (1000t) 1,253 1,322 1,349 -5% -7%

Paper Producton (1000t) 79 77 94 3% -16%

Paper sales (1000t) 87 83 104 6% -16%

Net Revenue (R$ million) 1,809 1,675 1,471 8% 23%

Adjusted EBITDA (R$ million) 730 637 389 15% 87%

EBITDA Margin (%) 40% 38% 26% 2 p.p. 14 p.p.

21%

32%

37%

9%

2Q09

27%

39%

23%

11%

1Q10

North America Europe Asia Brazil/Others

27%

38%

24%

11%

2Q10

17

EBITDA (R$ million) and EBITDA Margin (%)Cash cost (R$/t)

389

637

730

2Q09 1Q10 2Q10

EBITDA Margin (%) 40% 38% 26% 2 p.p. 14 p.p.

Financial Income (R$ million) (315) (341) 1.369 - -

Net Income (R$ million) 130 9 920 1,341% -86%

26%

38% 40%

418

499

440

1Q10 2Q10 2010E

449

2Q10 w/ downtimes

Source: Fibria

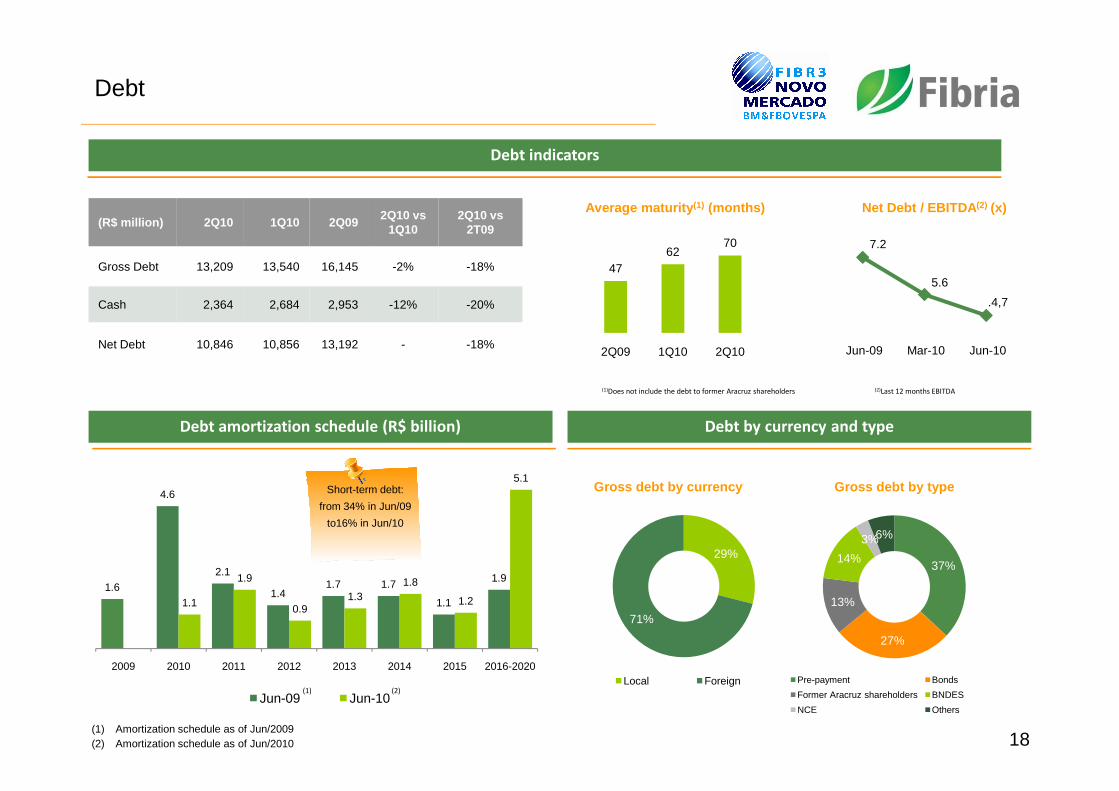

Debt

Debt indicators

(R$ million) 2Q10 1Q10 2Q092Q10 vs

1Q102Q10 vs

2T09

Gross Debt 13,209 13,540 16,145 -2% -18%

Cash 2,364 2,684 2,953 -12% -20%

Net Debt 10,846 10,856 13,192 - -18%

4762

70

2Q09 1Q10 2Q10

(1)Does not include the debt to former Aracruz shareholders

Average maturity (1) (months)

7.2

5.6

.4,7

Jun-09 Mar-10 Jun-10

Net Debt / EBITDA (2) (x)

(2)Last 12 months EBITDA

18

Debt amortization schedule (R$ billion) Debt by currency and type

1.6

4.6

2.1

1.41.7 1.7

1.1

1.9

1.1

1.9

0.91.3

1.8

1.2

5.1

2009 2010 2011 2012 2013 2014 2015 2016-2020

Jun-09 Jun-10

29%

71%

Gross debt by currency

Local Foreign

(1) Amortization schedule as of Jun/2009(2) Amortization schedule as of Jun/2010

(1) (2)

37%

27%

13%

14%

3%6%

Gross debt by type

Pre-payment Bonds

Former Aracruz shareholders BNDES

NCE Others

Short-term debt:

from 34% in Jun/09

to16% in Jun/10

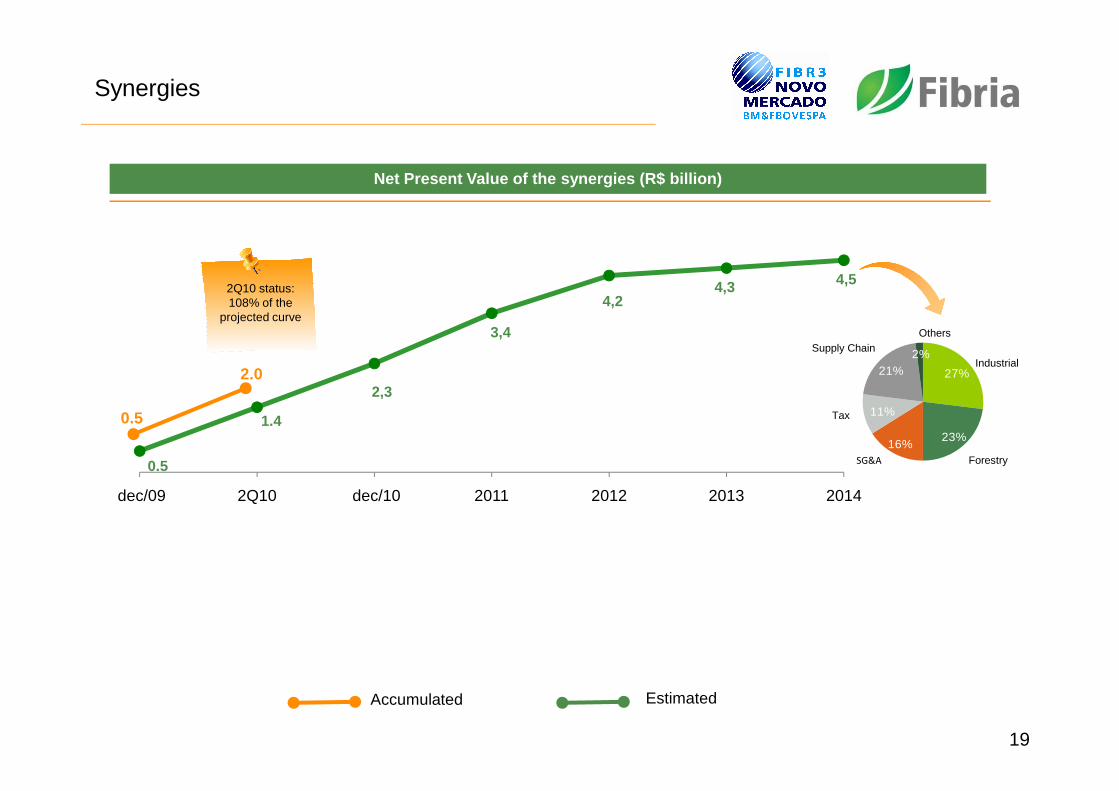

Synergies

Net Present Value of the synergies (R$ billion)

2,3

3,4

4,24,3 4,5

2Q10 status:108% of the

projected curve

27%21%2%

IndustrialSupply Chain

Others

2.0

19

Accumulated Estimated

0.5

1.4

2,3

dec/09 2Q10 dec/10 2011 2012 2013 2014

23%16%

11%

ForestrySG&A

Tax0.5

20

Corporate Restructuring

Corporate Restructuring

Event Date

Acquisition by VCP of additional 28% of Aracruz common shares Jan 20, 2009

VCP Capital Increase Apr 14, 2009

VCP conversion of prefered into common shares Jun 12, 2009

Tender Offer for Aracruz common shareholders Jul 02, 2009

Incorporation proposal for the 0.1347 ratio Aug 24, 2009

Merger of Aracruz shares into VCP approval Aug 24, 2009

21

Merger of Aracruz shares into VCP approval Aug 24, 2009

Shareholderes Agreement - VID and BNDES Oct 29, 2009

End of withdrawal rights period Nov 12, 2009

End of Aracruz trading Nov 17, 2009

Fibria trading start (Bovespa: FIBR3 / NYSE: FBR) Nov 18, 2009

Approval of the merger of Aracruz into Fibria Dec 22, 2009

Migration to Novo Mercado listing segment at BM&FBovespa May 20, 2010

2222

Investor Relations Team:

João Elek – IRO

André Gonçalves – General Manager

Fernanda Naveiro Vaz – Consultant

Anna Laura Linkewitsch – Specialist

Roberto Costa – Specialist

Email: [email protected]