corporate governance regulation: assessing the ... · corporate governance regulation: assessing...

TRANSCRIPT

i

Corporate Governance

Regulation: Assessing the Effectiveness of Soft Law in

relation to the Contemporary Role of the Board of Directors

Alice Louise Klettner

A Thesis Submitted for the Degree of Doctor of Philosophy

Faculty of Law

University of Technology, Sydney 2014

ii

Certificate of Original Authorship

I certify that the work in this thesis has not previously been submitted for a

degree nor has it been submitted as part of requirements for a degree except as

fully acknowledged within the text.

I also certify that the thesis has been written by me. Any help that I have received

in my research work and the preparation of the thesis itself has been

acknowledged. In addition, I certify that all information sources and literature

used are indicated in the thesis.

Signature of Student:

Alice Louise Klettner

Date:

iii

Acknowledgements

Thank you to my supervisors, Professor Paul Redmond and Professor Thomas

Clarke for their remarkable patience and support during the many months that

this thesis lingered mostly in my mind rather than on paper. You have not only

served as supervisors but as mentors, role models and confirmation that

academia can provide the freedom and opportunity to subtly make a difference.

Thank you to my twins Zoe and Harris who were born and lived their first six years

during the creation of this thesis. They have overcome so many hurdles and bring

joy and inspiration to every day.

My husband Mark also deserves an enormous thank you for supporting this

endeavour, giving up his pottery classes, getting up extremely early and taking on

Tuesday dinner and bedtime so that I could work late.

Thank you colleagues Marie and Martijn for your pep talks from the corner desk.

Lastly, thank you to my parents for offering to proof read and more importantly

for providing the love, support and opportunity that got me to this stage.

iv

Corporate Governance Regulation: Assessing the Effectiveness of Soft Law in relation to the

Contemporary Role of the Board of Directors

Chapter 1 Introduction to Thesis

Chapter 2 Corporate Governance Regulation

Chapter 3 Research Design and Methodology

Chapter 4 Theoretical Review

Chapter 5 Findings - Board Composition and Structure

Chapter 6 Findings - Board Evaluation and Effectiveness

Chapter 7 Findings - Gender Diversity on Boards

Chapter 8 Findings – Governance and Corporate Responsibility

Chapter 9 Soft Regulation and Board Performance

Chapter 10 Conclusions and Recommendations

v

Contents

1 Introduction to Thesis 1

1.1 The Role of the Board ............................................................................... 3

1.2 Soft Corporate Governance Regulation .................................................... 4

1.3 Research Methodology ............................................................................. 6

1.4 Thesis Structure ........................................................................................ 9

2 Corporate Governance Regulation 13

2.1 Definitions ............................................................................................... 13

2.1.1 Corporate Governance .................................................................... 13

2.1.2 Corporate Governance Regulation ................................................. 16

2.1.3 Corporate Responsibility ................................................................. 17

2.2 Development and Reform of Corporate Governance Regulation .......... 21

2.2.1 Phase 1: Early Corporate Governance Standards and Codes ......... 25

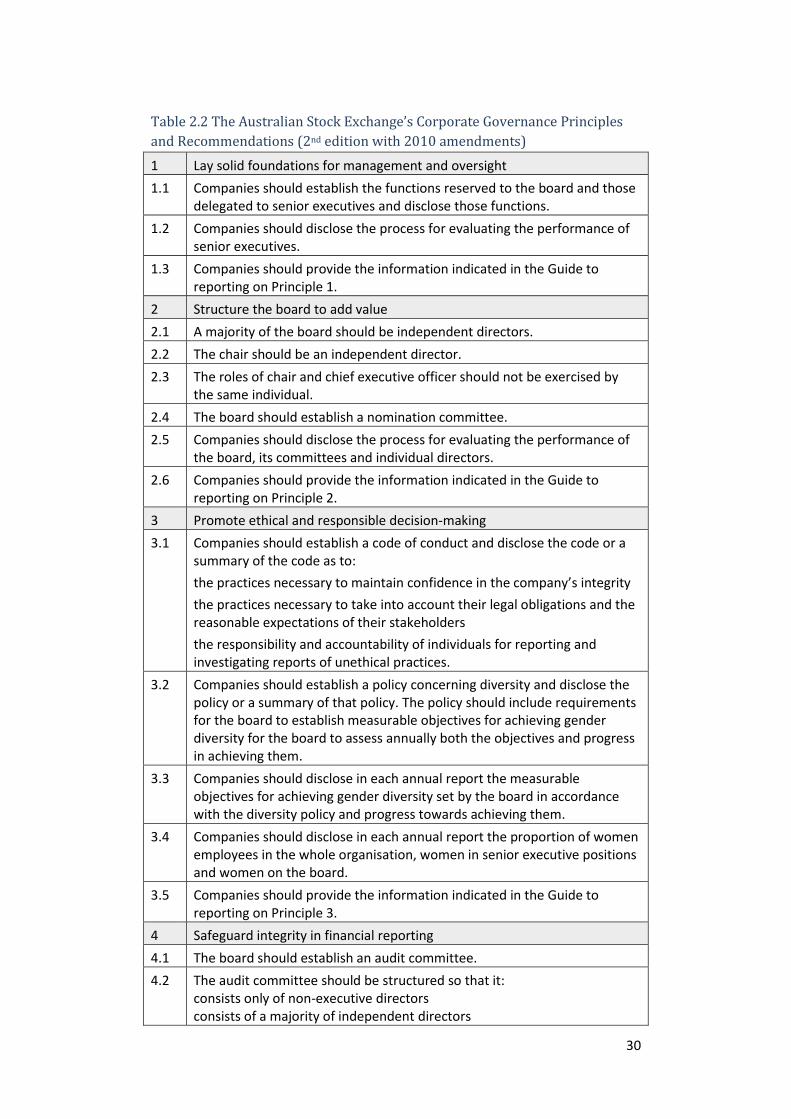

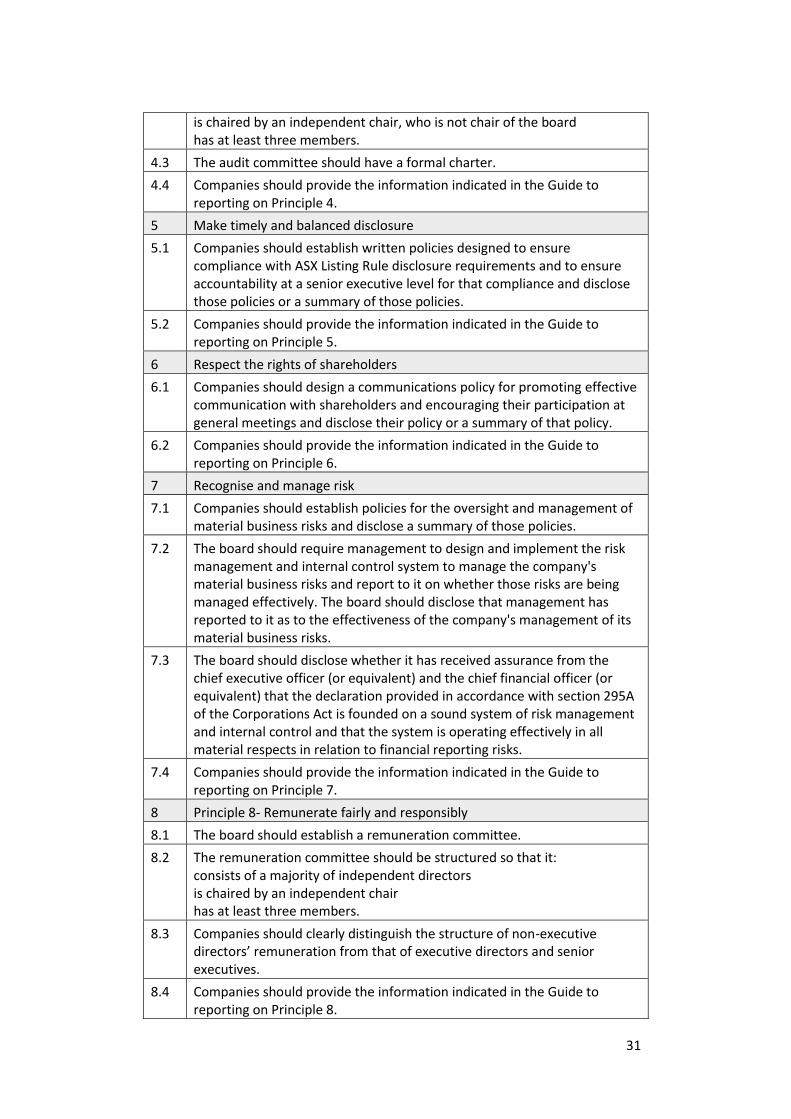

2.2.2 Phase 2: Strengthening Corporate Governance Regulation ........... 28

2.2.3 Phase 3: Reform Post-Global Financial Crisis .................................. 40

2.3 Summary of Chapter 2 ............................................................................ 47

3 Research Design and Methodology 48

3.1 Aims and objectives ................................................................................ 49

3.2 Call for research ...................................................................................... 49

3.2.1 Empirical Legal Research ................................................................. 50

3.2.2 Qualitative board research ............................................................. 57

3.2.3 Multi-theoretic research ................................................................. 62

3.2.4 Empirical research into regulatory mechanisms ............................. 63

3.2.5 Interdisciplinary research................................................................ 67

3.3 Research Objectives ................................................................................ 68

3.4 Research Design ...................................................................................... 70

3.4.1 Data collection ................................................................................ 70

3.4.2 Data analysis ................................................................................... 72

3.4.3 Research Limitations ....................................................................... 74

3.5 Summary ................................................................................................. 74

4 Theoretical review 76

4.1 Introduction ............................................................................................ 76

vi

4.1.1 The Role of the Board ..................................................................... 76

4.1.2 Regulatory Content ......................................................................... 77

4.1.3 Regulatory Mechanisms .................................................................. 78

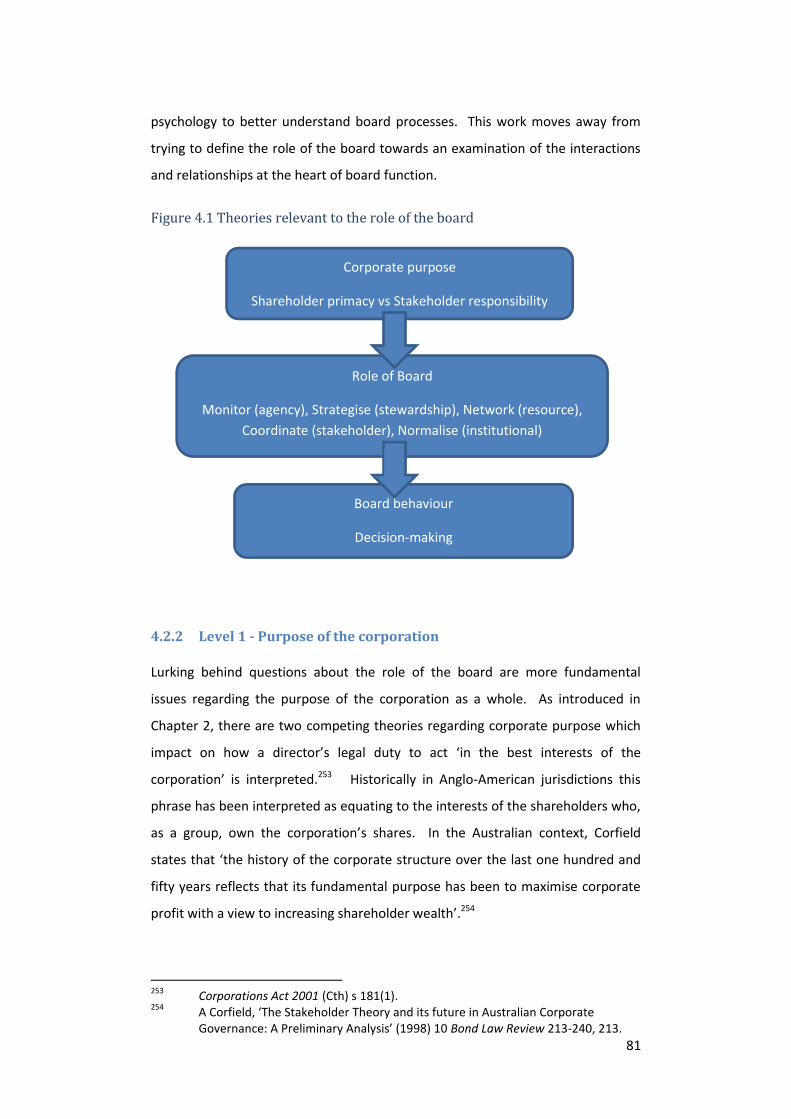

4.2 The Role of the Board ............................................................................. 79

4.2.1 Multiple board roles and theories .................................................. 79

4.2.2 Level 1 - Purpose of the corporation .............................................. 81

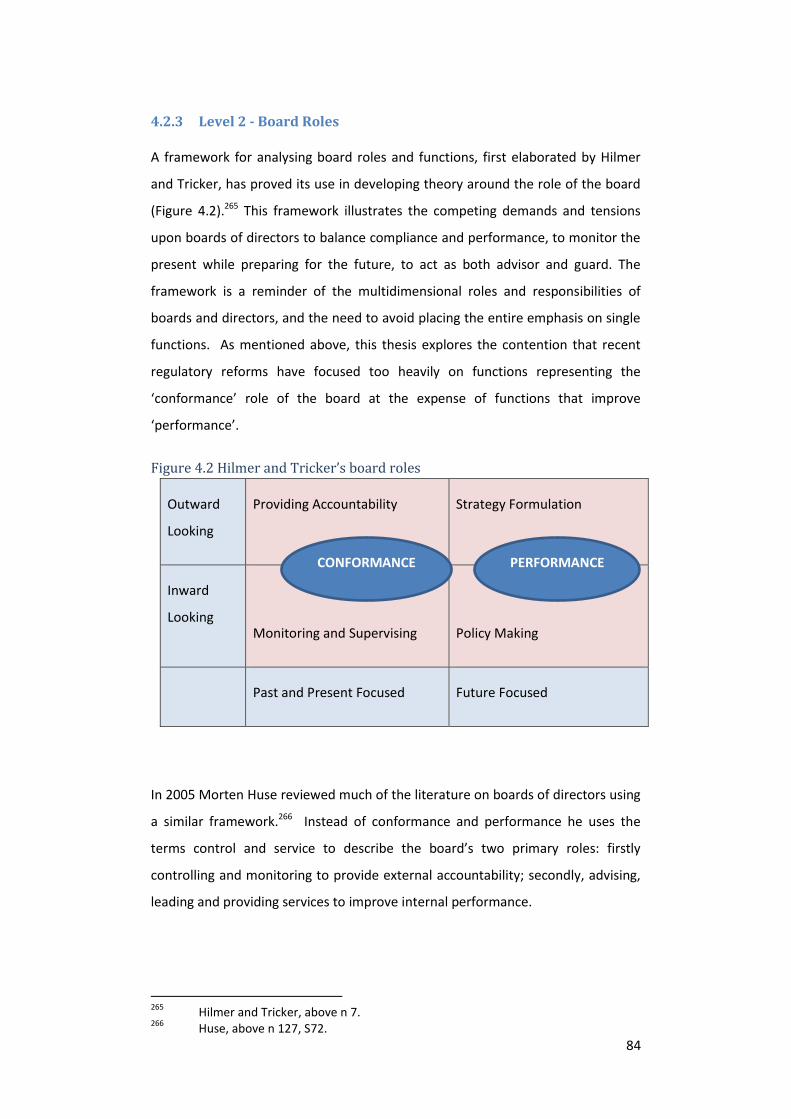

4.2.3 Level 2 - Board Roles ....................................................................... 84

4.2.4 Level 3 - Board behaviour ............................................................... 86

4.2.5 Agency Theory ................................................................................. 88

4.2.6 Stakeholder theory ......................................................................... 91

4.2.7 Stewardship Theory ........................................................................ 94

4.2.8 Resource-dependency theory ......................................................... 98

4.2.9 Institutional Theory ....................................................................... 100

4.2.10 Summary – theories on the role of the board .............................. 102

4.3 Regulatory Mechanisms ........................................................................ 103

4.3.1 Corporate governance regulation ................................................. 104

4.3.2 Regulatory theories ....................................................................... 106

4.3.3 New Governance ........................................................................... 107

4.3.4 Meta-regulation ............................................................................ 110

4.3.5 Responsive regulation ................................................................... 111

4.3.6 Disclosure as regulation – comply or explain ............................... 113

4.3.7 Soft law and norms ....................................................................... 115

5 Board Composition and Structure 122

5.1 Introduction .......................................................................................... 122

5.2 Board composition and structure ......................................................... 122

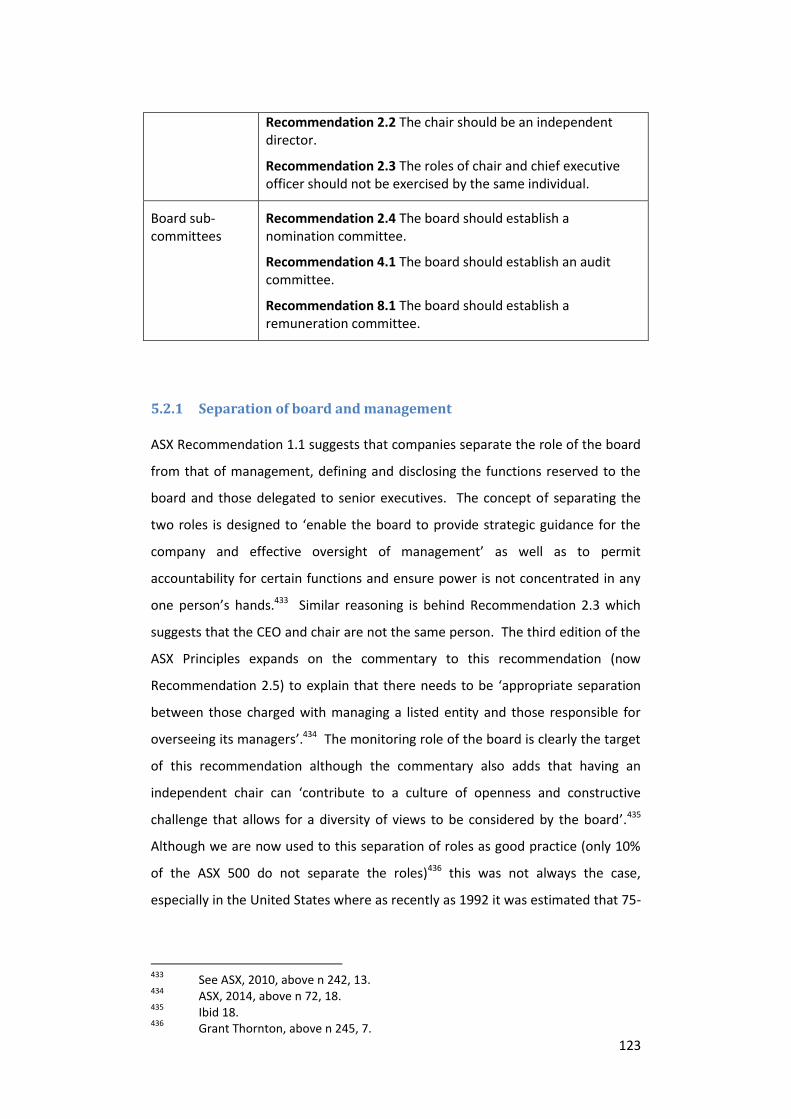

5.2.1 Separation of board and management ......................................... 123

5.2.2 Independent directors .................................................................. 124

5.2.3 Board sub-committees .................................................................. 126

5.3 Methodology ......................................................................................... 129

5.3.1 Target sample................................................................................ 130

5.3.2 Interviews ...................................................................................... 132

5.3.3 Interview preparation ................................................................... 135

5.3.4 Interview process .......................................................................... 136

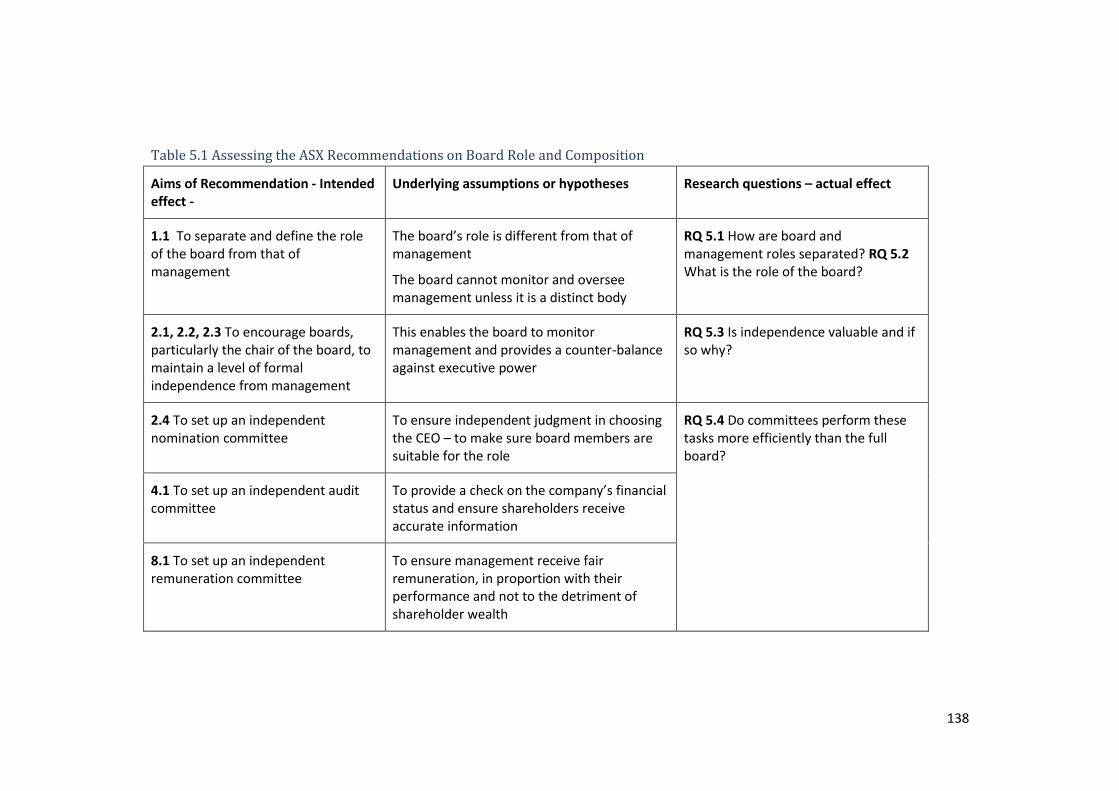

5.3.5 Thesis analysis ............................................................................... 137

vii

5.4 Findings ................................................................................................. 139

5.4.1 Separation of board and management ......................................... 139

5.4.2 The roles of the board ................................................................... 142

5.4.3 Changing role over time ................................................................ 148

5.4.4 Independence ............................................................................... 149

5.4.5 Non executives and independence ............................................... 152

5.4.6 Board committees ......................................................................... 153

5.4.7 Smaller companies’ boards ........................................................... 162

5.4.8 Division of responsibility ............................................................... 165

5.4.9 Regulation – the comply or explain mechanism ........................... 167

5.5 Summary of Chapter 5 .......................................................................... 174

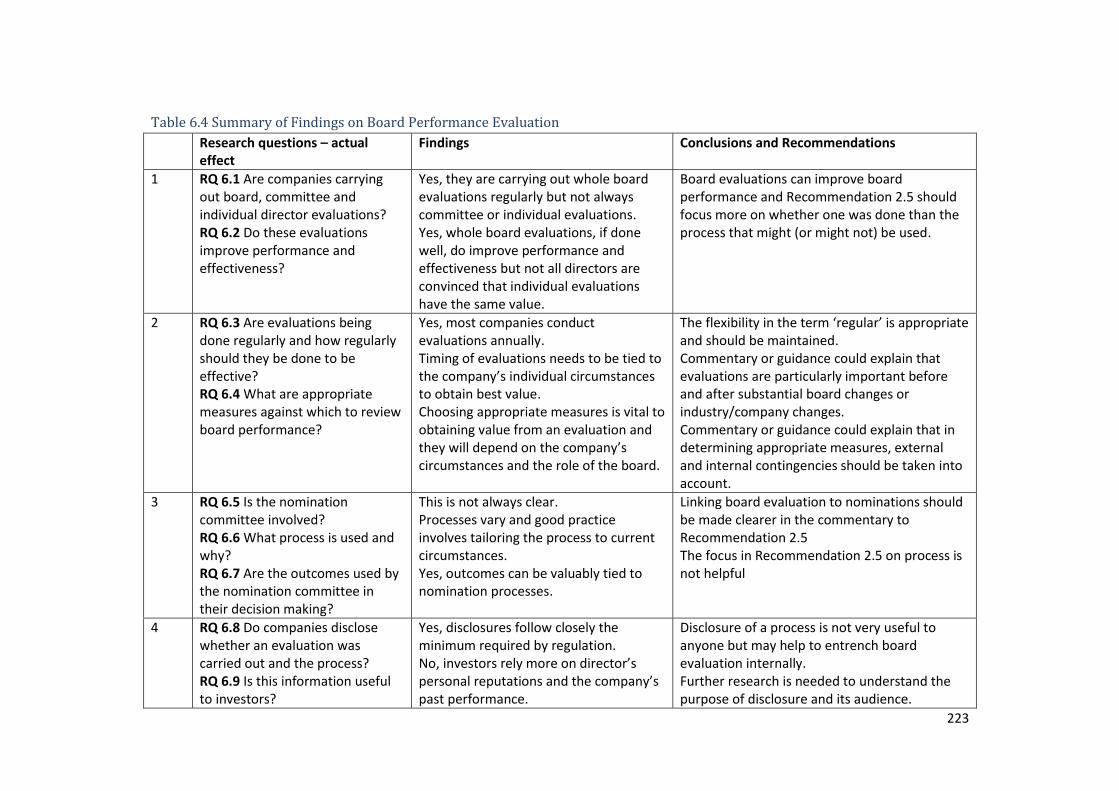

6 Board Evaluation and Effectiveness 177

6.1 Introduction .......................................................................................... 177

6.2 Board performance evaluations ........................................................... 177

6.3 Methodology ......................................................................................... 181

6.4 Findings ................................................................................................. 187

6.4.1 Board evaluations ......................................................................... 187

6.4.2 Individual director evaluations ..................................................... 188

6.4.3 Improved performance and effectiveness .................................... 190

6.4.4 Frequency of evaluation ............................................................... 192

6.4.5 Appropriate measures of effectiveness ........................................ 193

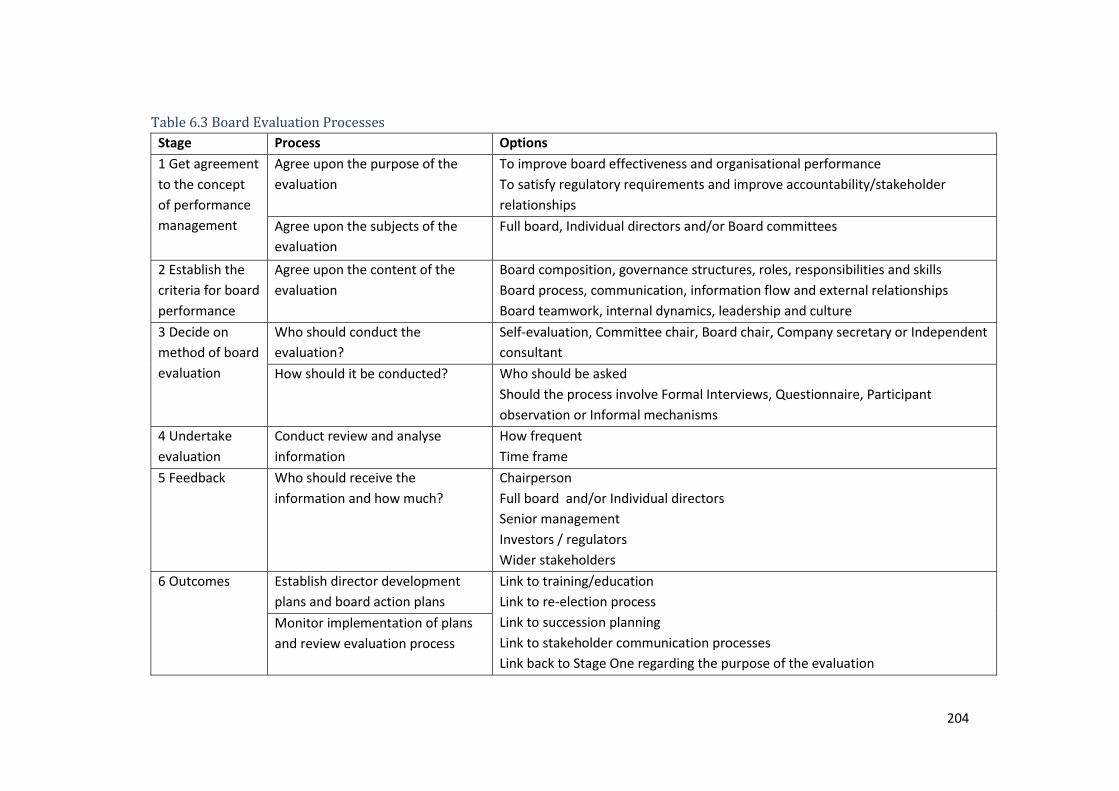

6.4.6 Process of board evaluation.......................................................... 202

6.4.7 Disclosure ...................................................................................... 214

6.5 Discussion .............................................................................................. 218

6.6 Summary of Chapter 6 .......................................................................... 220

7 Gender Diversity on Boards 224

7.1 Introduction .......................................................................................... 224

7.2 Gender diversity .................................................................................... 226

7.3 Research Objectives and Methodology ................................................ 231

7.4 Findings ................................................................................................. 234

7.4.1 Diversity Policies ........................................................................... 234

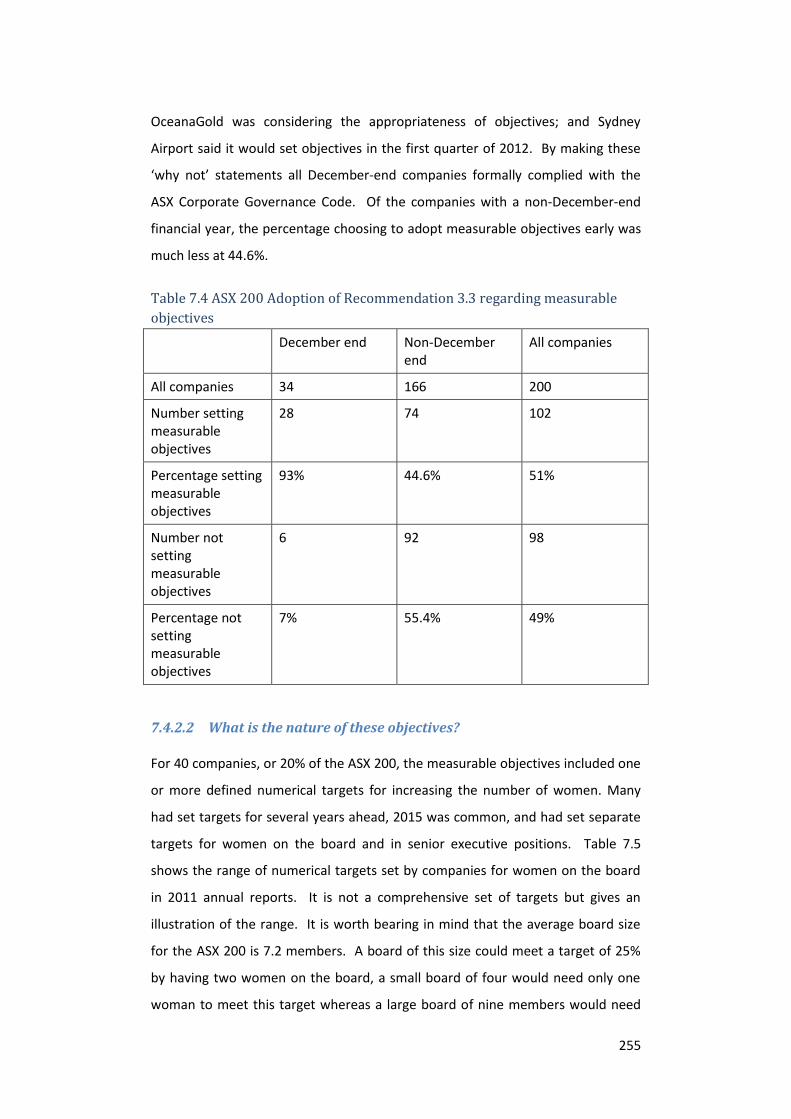

7.4.2 Measurable Objectives ................................................................. 254

7.4.3 Gender Statistics ........................................................................... 259

viii

7.5 Summary of Chapter 7 .......................................................................... 261

8 Governance and Corporate Responsibility 269

8.1 Introduction .......................................................................................... 269

8.2 Corporate Responsibility ....................................................................... 269

8.3 Regulation of CSR .................................................................................. 274

8.3.1 Hard law ........................................................................................ 275

8.3.2 Domestic soft law: ASX Principles ................................................. 278

8.3.3 International initiatives ................................................................. 282

8.4 Research Objectives and Methodology ................................................ 285

8.5 Findings ................................................................................................. 292

8.5.1 Communication - Reporting Frameworks ..................................... 292

8.5.2 Stakeholder Engagement .............................................................. 299

8.5.3 Leadership - Committees .............................................................. 302

8.5.4 Implementation – Remuneration incentives ................................ 308

8.6 Summary of Chapter 8 .......................................................................... 316

9 Soft regulation and board performance 324

9.1 Introduction .......................................................................................... 324

9.2 Theoretical/Academic Contribution ..................................................... 324

9.2.1 Theory-Building ............................................................................. 325

9.2.2 Links between theory and practice ............................................... 327

9.3 Summary of findings ............................................................................. 329

9.3.1 Chapter 5 - Board roles ................................................................. 329

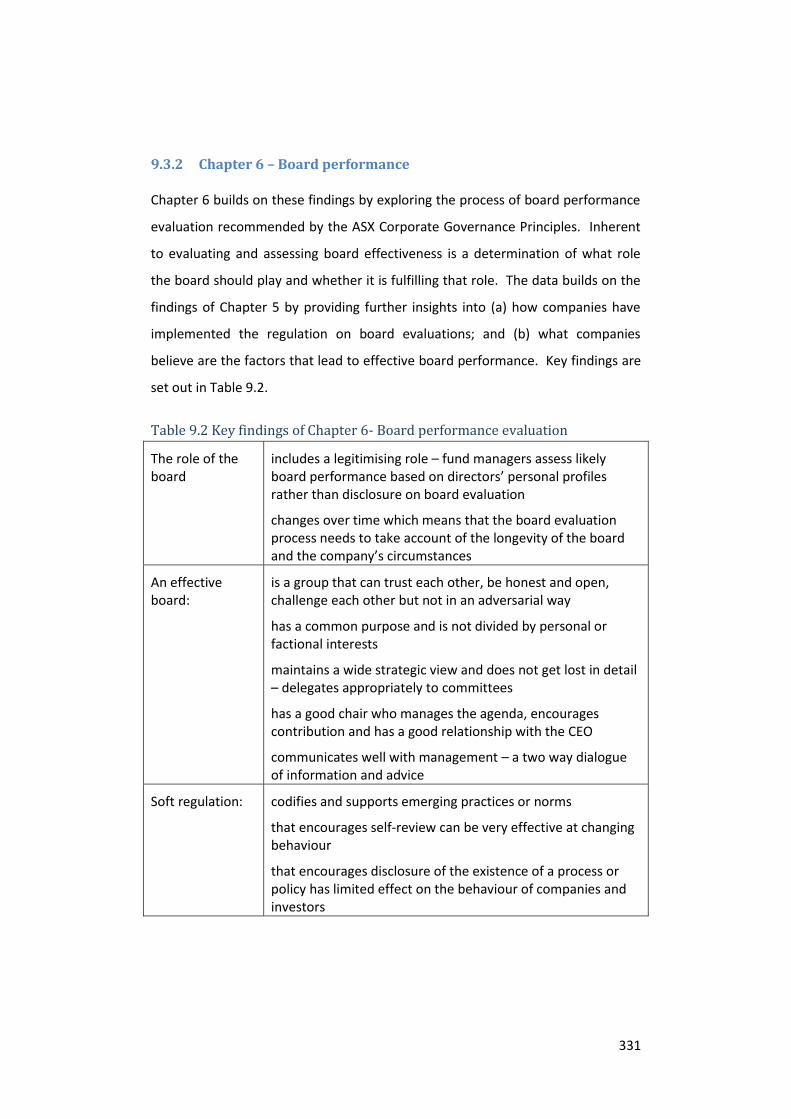

9.3.2 Chapter 6 – Board performance ................................................... 331

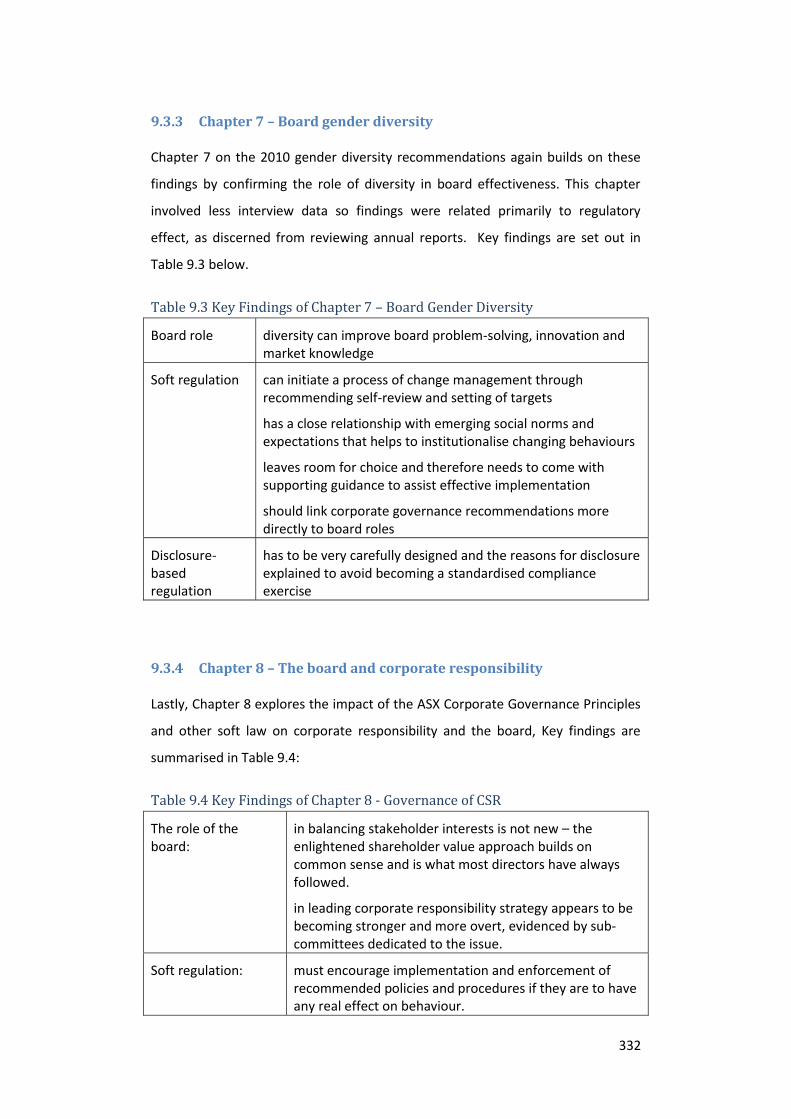

9.3.3 Chapter 7 – Board gender diversity .............................................. 332

9.3.4 Chapter 8 – The board and corporate responsibility .................... 332

9.3.5 Common themes ........................................................................... 333

9.4 The Modern Role of the Board ............................................................. 333

9.4.1 The Changing Role of the Board ................................................... 334

9.4.2 Flexible regulation ......................................................................... 336

9.4.3 The Collaborative Role of the Board ............................................. 337

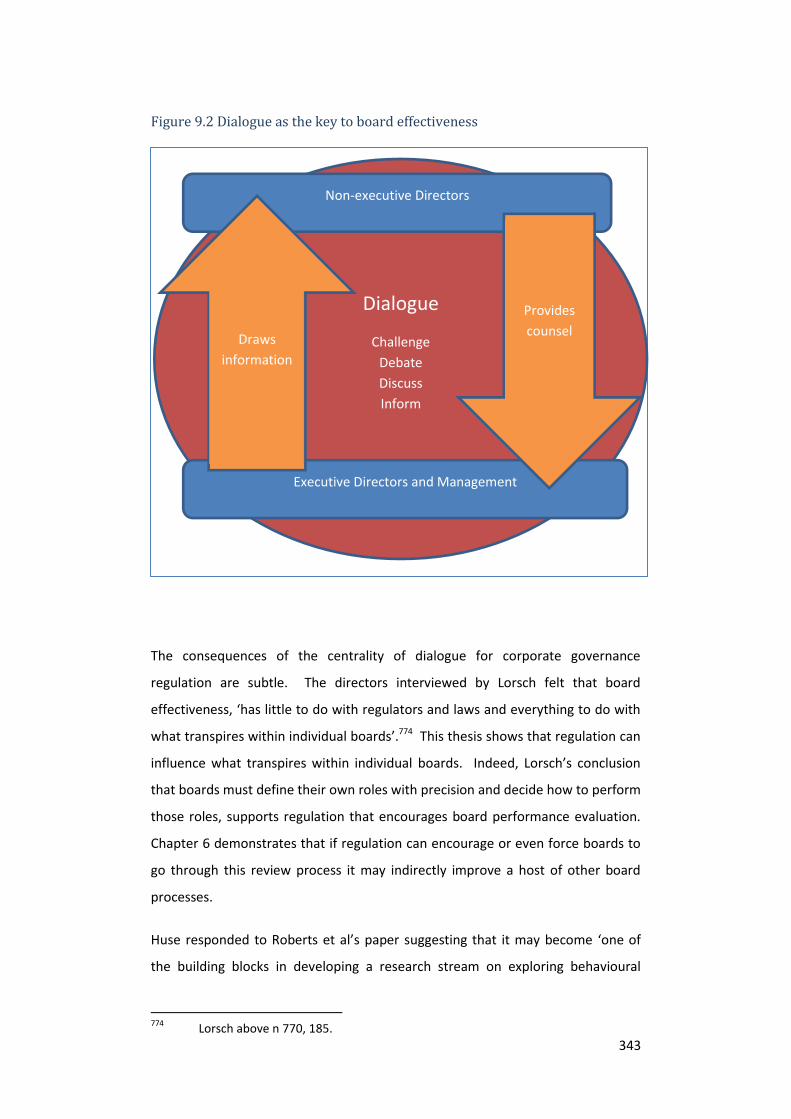

9.4.4 Trust and the Board ...................................................................... 344

9.4.5 The Mediating Role of the Board .................................................. 346

9.5 New Governance Regulation ................................................................ 348

ix

9.5.1 When to use New Governance ..................................................... 350

9.5.2 Why New Governance regulation changes behaviour ................. 355

9.5.3 How to make New Governance effective ..................................... 359

9.6 Summary ............................................................................................... 371

10 Conclusions and Recommendations 376

10.1 The contemporary role of the board .................................................... 376

10.2 Corporate governance regulation ......................................................... 377

10.3 Theoretical contribution ....................................................................... 378

10.4 Practitioner and policy implications ..................................................... 380

10.5 Future research ..................................................................................... 381

10.6 Concluding comments .......................................................................... 382

References 384

Appendix 1 406

Dibbs Study: The Changing Role and Responsibilities of Company Boards and Directors ............................................................................................................ 406

Interview Template ....................................................................................... 406

Appendix 2 409

ACSI Study: Board Performance and Effectiveness .......................................... 409

Interview Template for Directors .................................................................. 409

Appendix 3 410

ACSI Study: Board Performance and Effectiveness .......................................... 410

Interview Template for Fund Managers ....................................................... 410

x

List of Figures and Tables

Figure 1.1 Thesis Research Framework .................................................................. 12

Figure 2.1 Farrar’s Circles of Corporate Governance Regulation ........................... 17

Figure 2.2 Carroll’s Pyramid of Corporate Responsibility ....................................... 19

Table 2.1 Australian Corporate Governance Developments (and important

international influences) ......................................................................................... 23

Table 2.2 The Australian Stock Exchange’s Corporate Governance Principles and

Recommendations (2nd edition with 2010 amendments) ...................................... 30

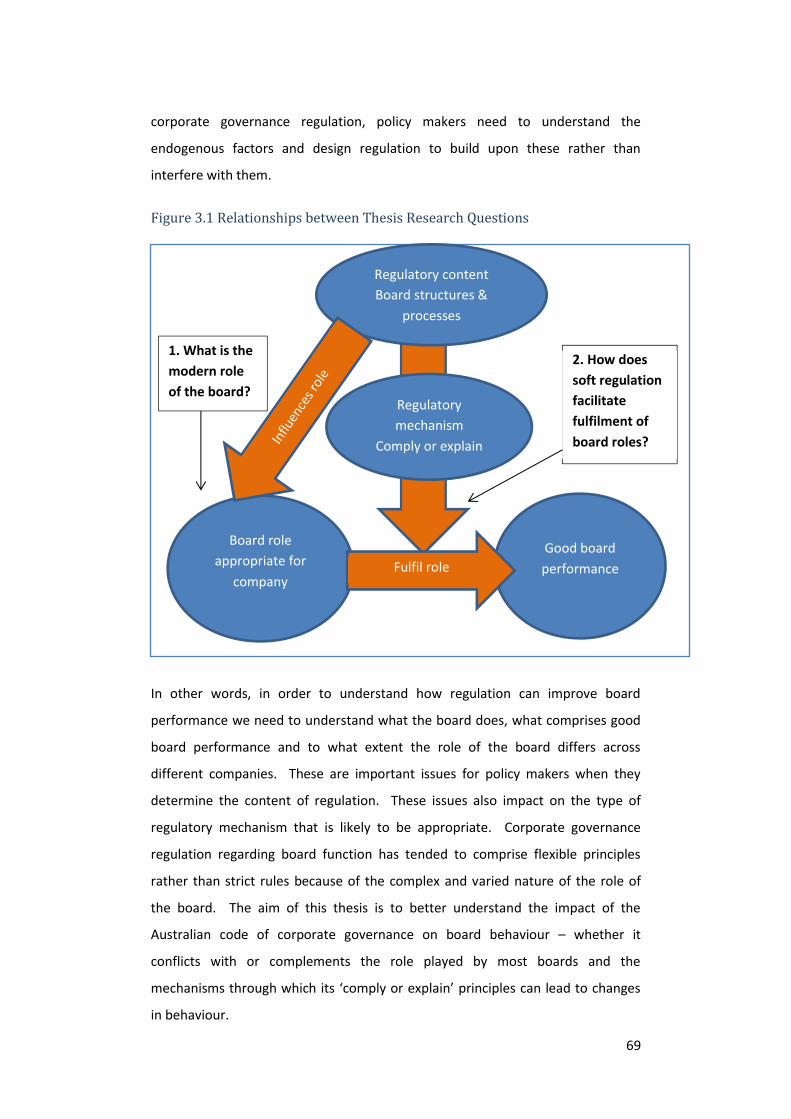

Figure 3.1 Relationships between Thesis Research Questions ............................... 69

Table 3.1 Thesis Database ....................................................................................... 71

Figure 3.2 Framework for analysis .......................................................................... 72

Figure 4.1 Theories relevant to the role of the board ............................................ 81

Figure 4.2 Hilmer and Tricker’s board roles ............................................................ 84

Figure 4.3 Board roles and corresponding theories ............................................... 86

Figure 4.4 Regulatory theories .............................................................................. 104

Box 5.1 ASX Recommendations regarding board composition and structure ..... 122

Table 5.1 Assessing the ASX Recommendations on Board Role and Composition

.............................................................................................................................. 138

Table 5.2 Summary of Findings on Board Role and Composition ......................... 176

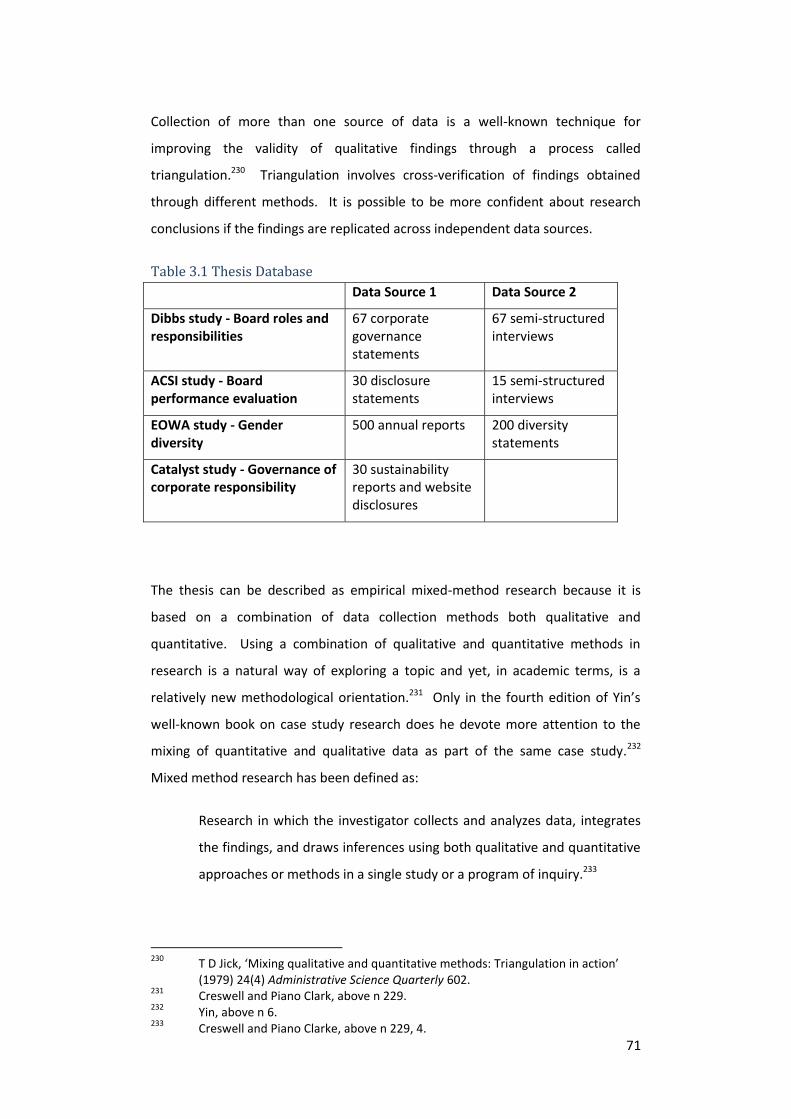

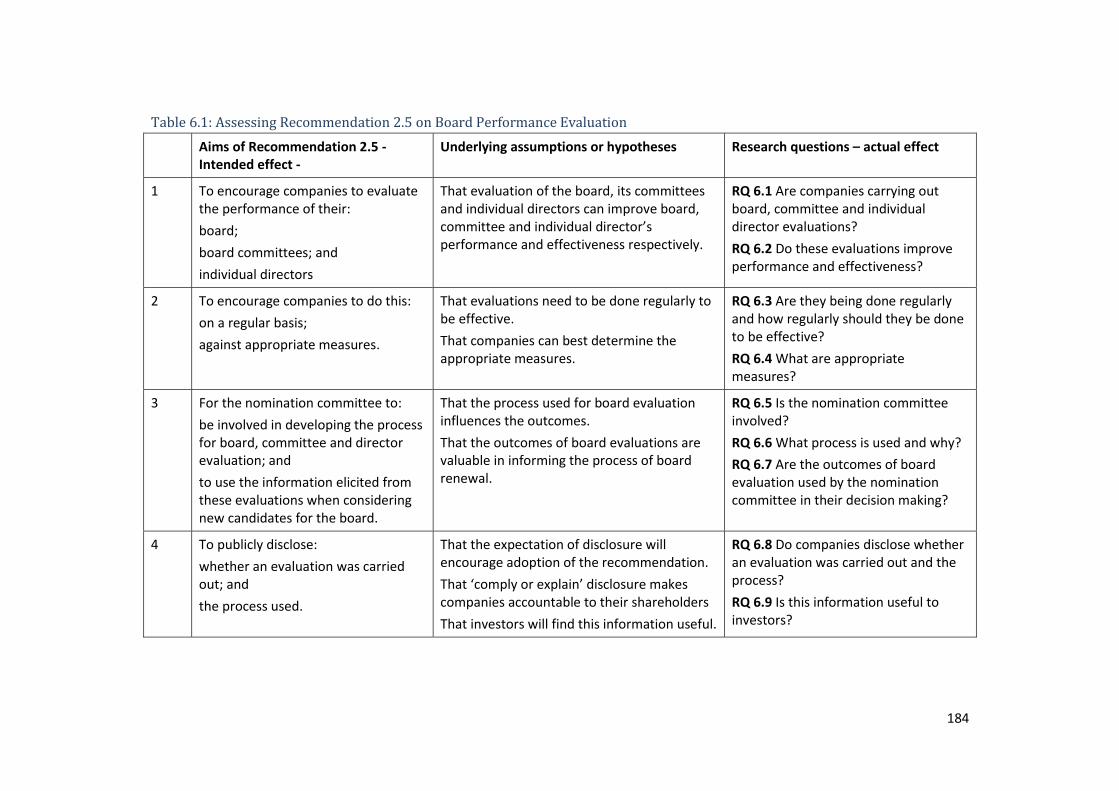

Table 6.1: Assessing Recommendation 2.5 on Board Performance Evaluation ... 184

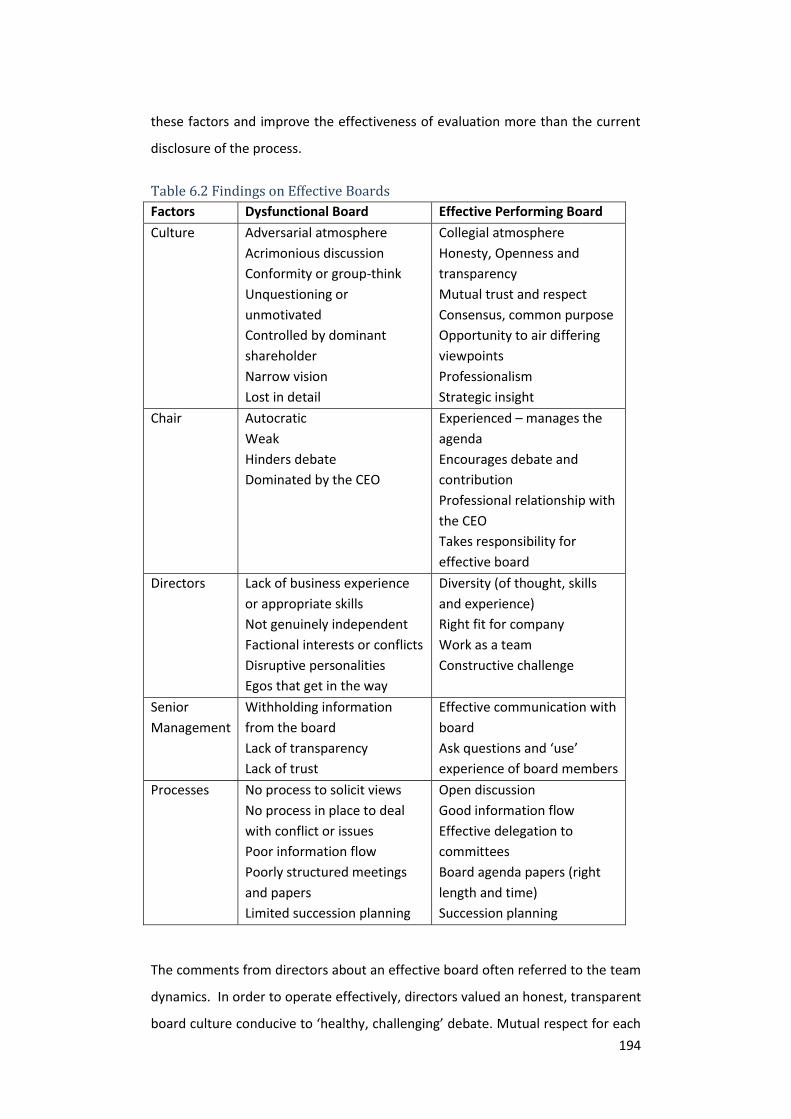

Table 6.2 Findings on Effective Boards ................................................................. 194

Table 6.3 Board Evaluation Processes .................................................................. 204

Table 6.4 Summary of Findings on Board Performance Evaluation ..................... 223

Box 7.1 ASX Recommendations on Diversity ........................................................ 224

Table 7.1 Assessing Recommendations 3.2-3.5 on Gender Diversity ................... 232

Box 7.2 ASX Suggestions for the content of a diversity policy .............................. 234

Table 7.2 ASX 200 Adoption of Recommendation 3.2 .......................................... 236

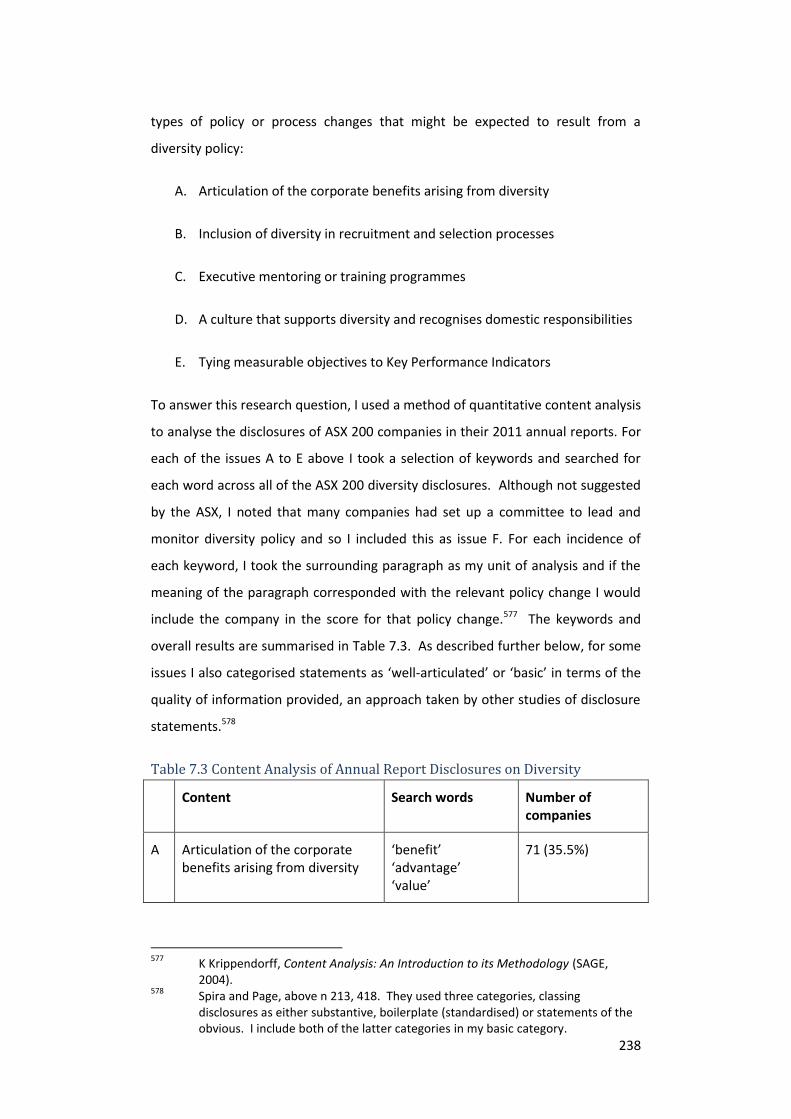

Table 7.3 Content Analysis of Annual Report Disclosures on Diversity ................ 238

Table 7.4 ASX 200 Adoption of Recommendation 3.3 regarding measurable

objectives .............................................................................................................. 255

Table 7.5 Targets for Women on the Board ......................................................... 256

Table 7.6 Targets for Female Senior Executives/Management ............................ 257

Table 7.7 Adoption of Recommendation 3.4 regarding Gender Statistics ........... 260

Figure 7.1 Process of implementing diversity recommendations ........................ 263

xi

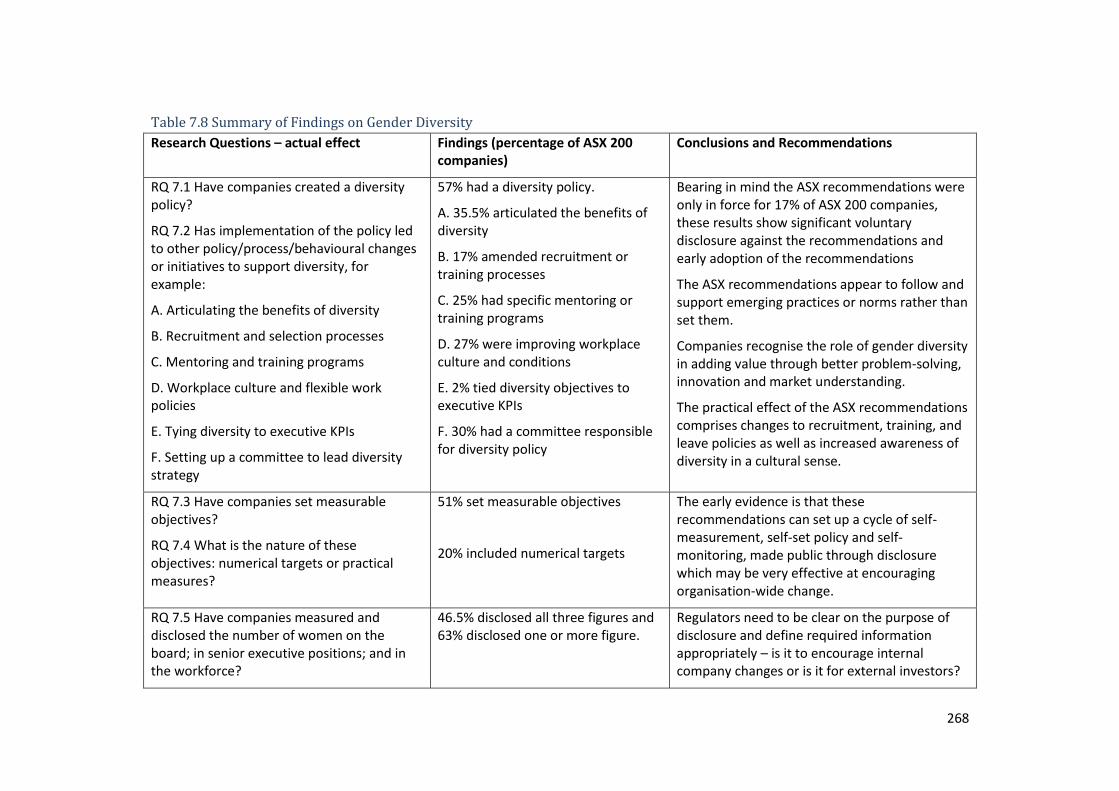

Table 7.8 Summary of Findings on Gender Diversity ............................................ 268

Box 8.1 ASX Recommendations relating to stakeholder interests ....................... 279

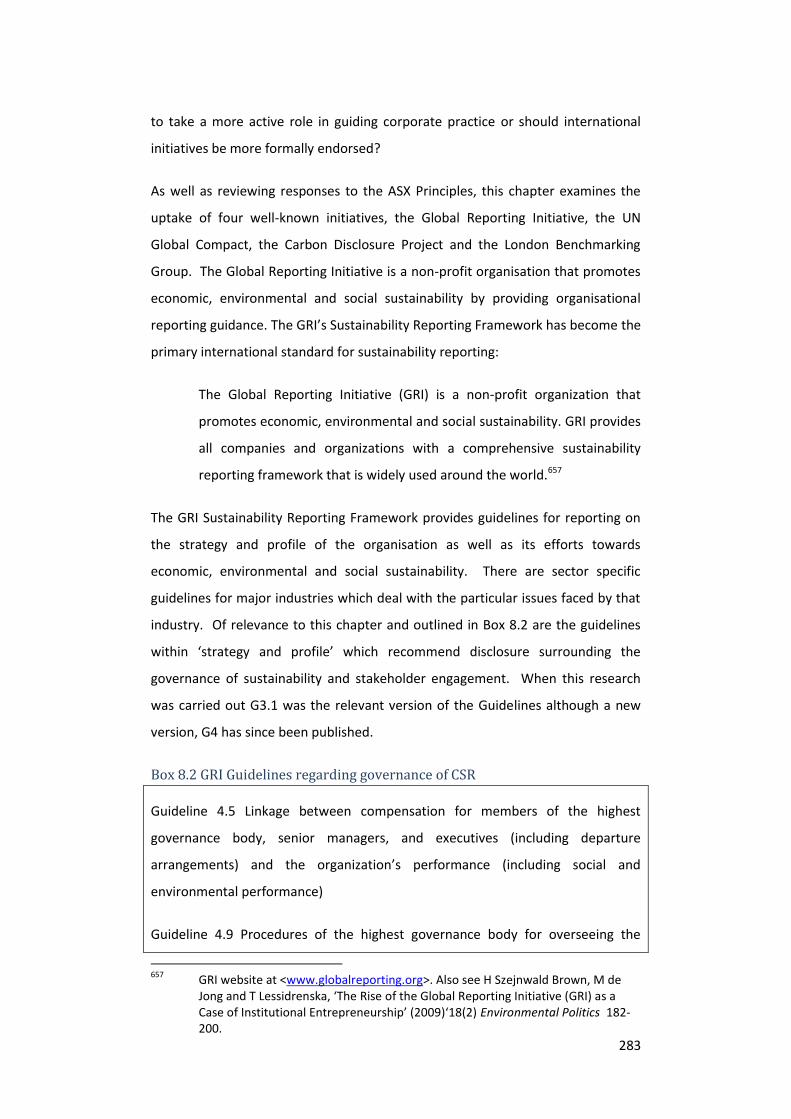

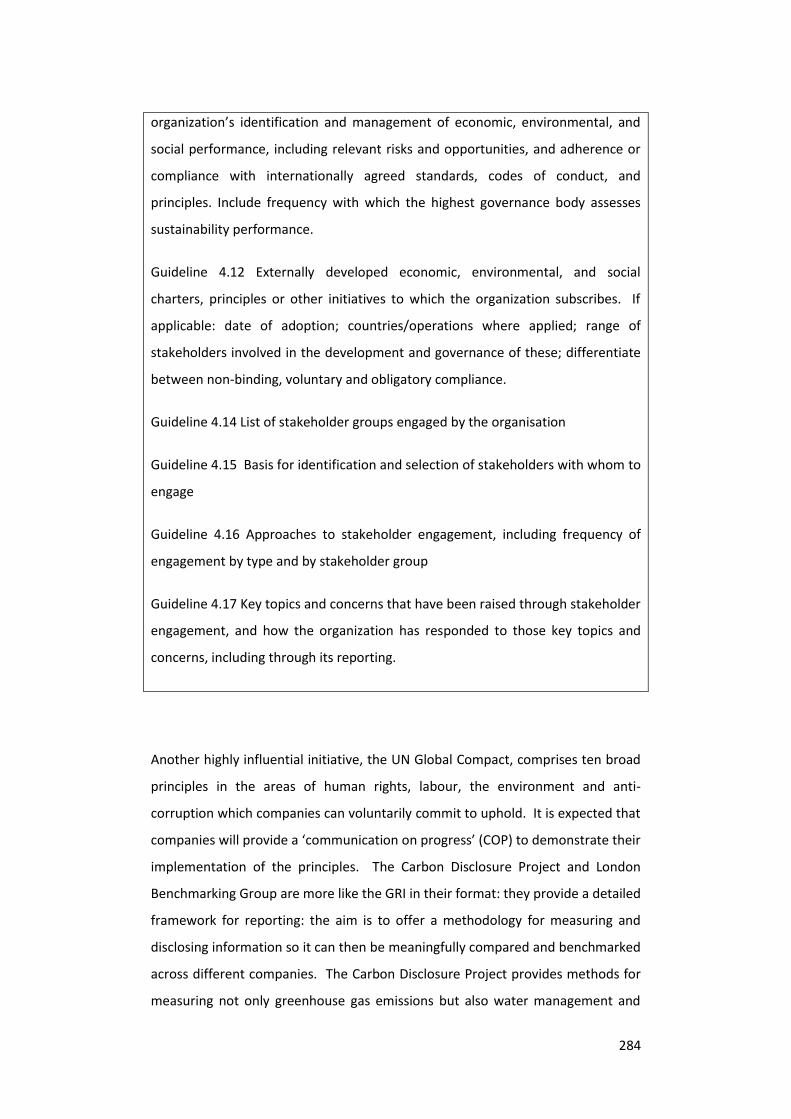

Box 8.2 GRI Guidelines regarding governance of CSR .......................................... 283

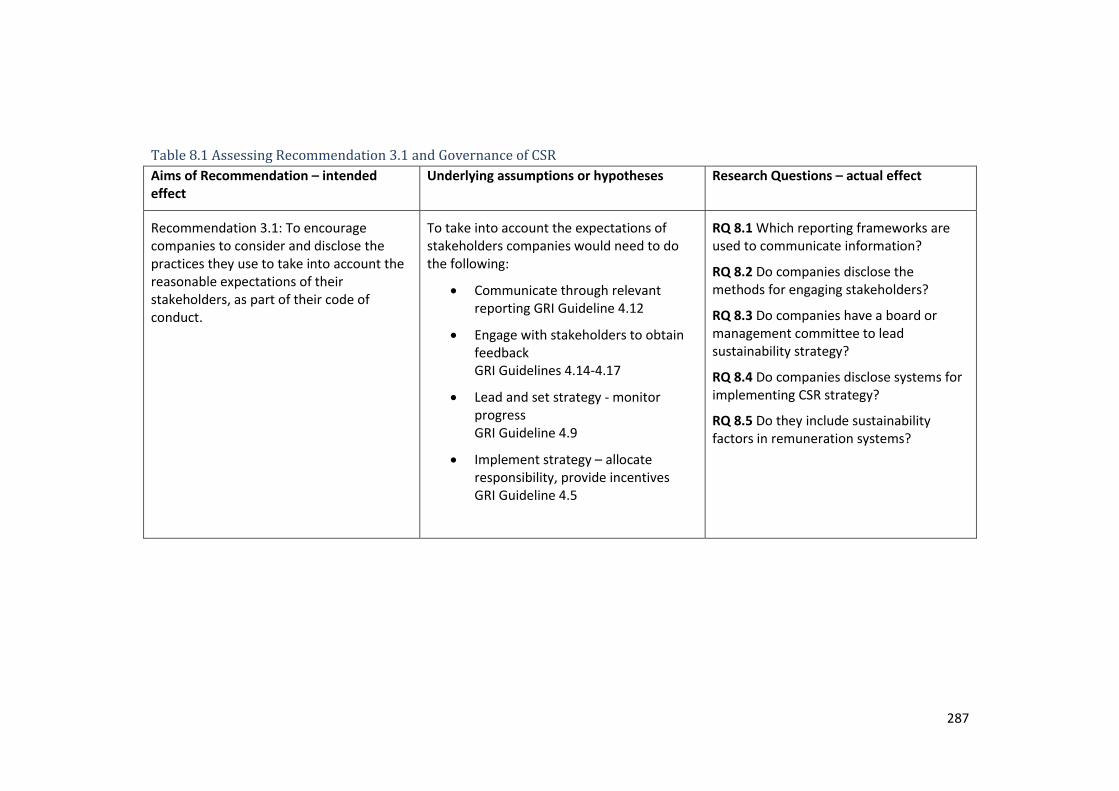

Table 8.1 Assessing Recommendation 3.1 and Governance of CSR ..................... 287

Table 8.2 Sample Companies ................................................................................ 289

Table 8.3 Assessment Criteria – Governance of CSR ............................................ 291

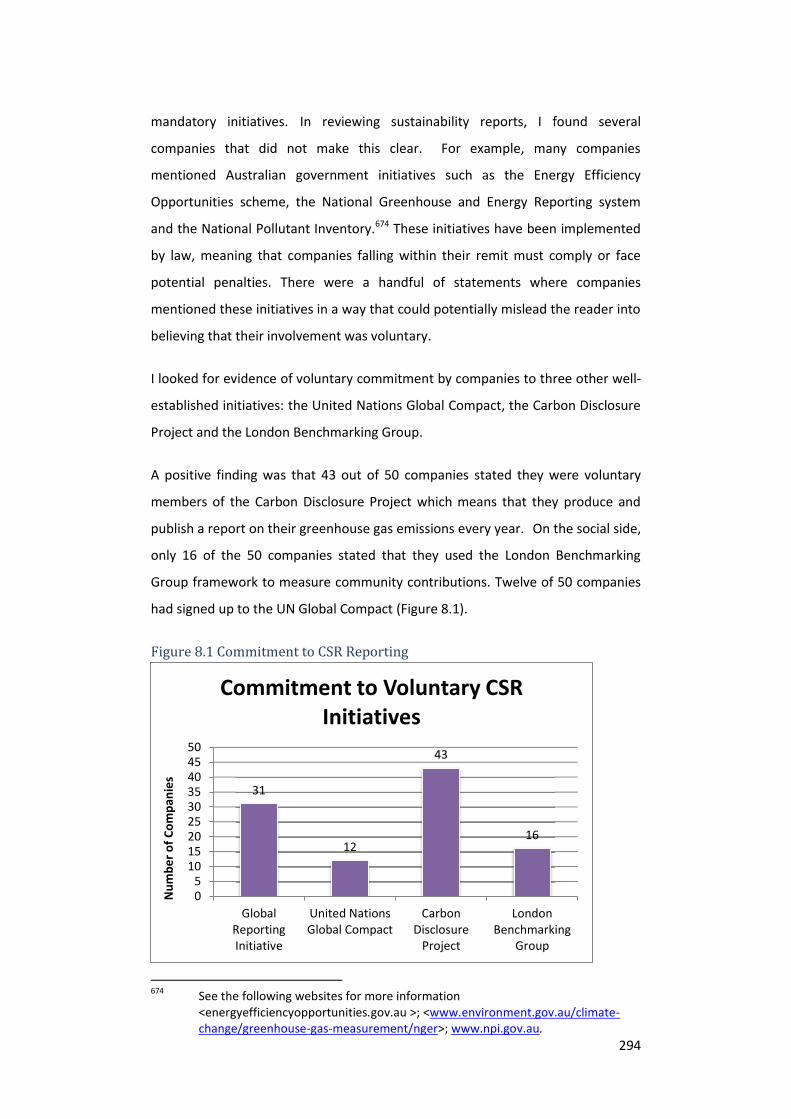

Figure 8.1 Commitment to CSR Reporting ............................................................ 294

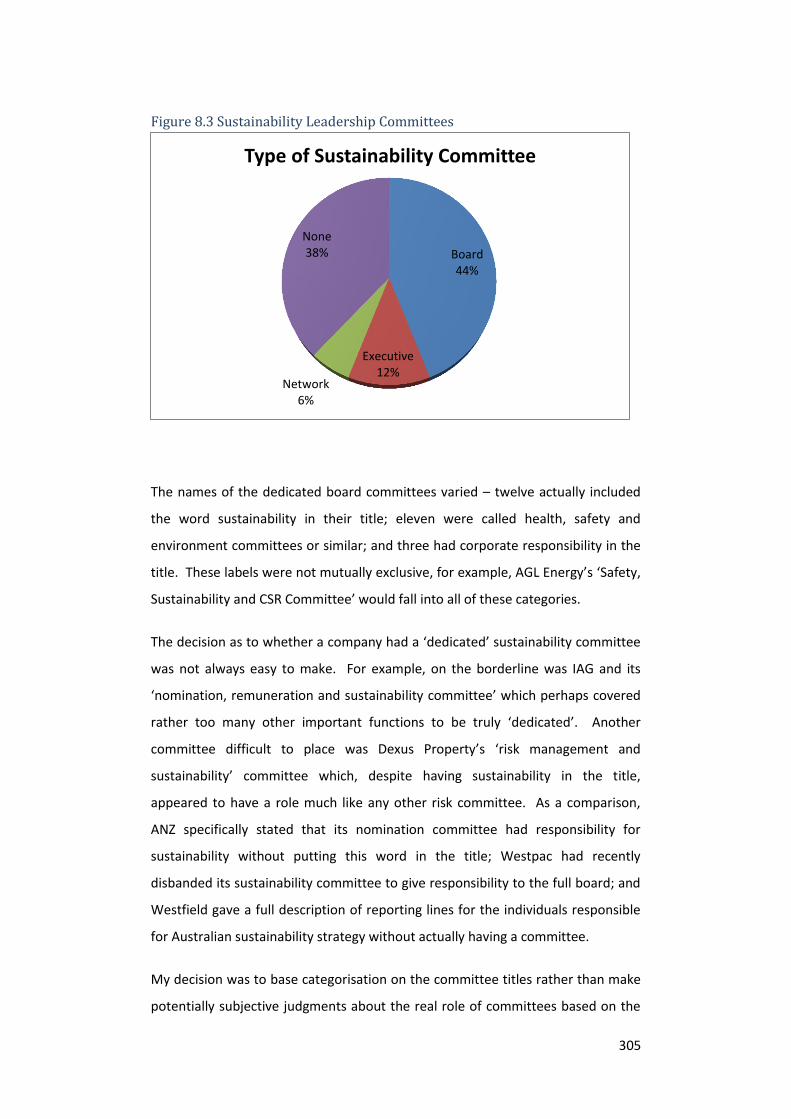

Figure 8.3 Sustainability Leadership Committees ................................................. 305

Figure 8.4 Sustainability Performance Indicators linked to Executive Remuneration

.............................................................................................................................. 314

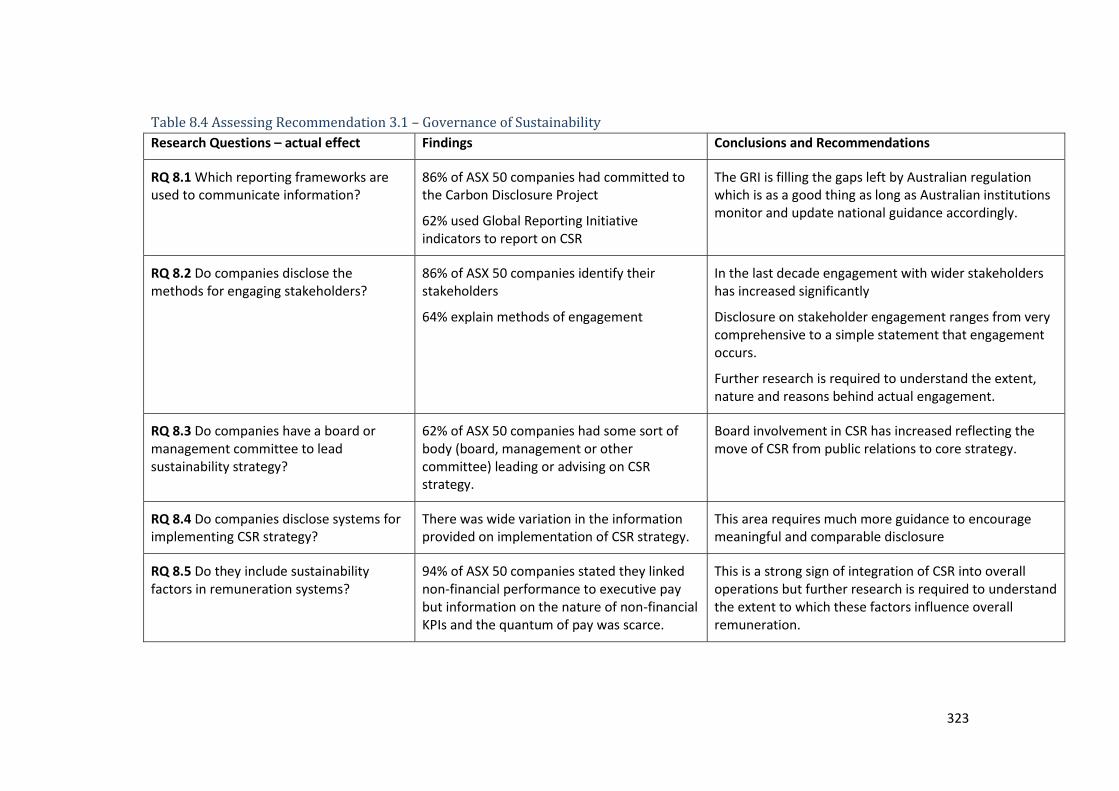

Table 8.4 Assessing Recommendation 3.1 – Governance of Sustainability.......... 323

Table 9.1 Key findings of Chapter 5 – Board roles ................................................ 330

Table 9.2 Key findings of Chapter 6- Board performance evaluation ................... 331

Table 9.3 Key Findings of Chapter 7 – Board Gender Diversity ............................ 332

Table 9.4 Key Findings of Chapter 8 - Governance of CSR .................................... 332

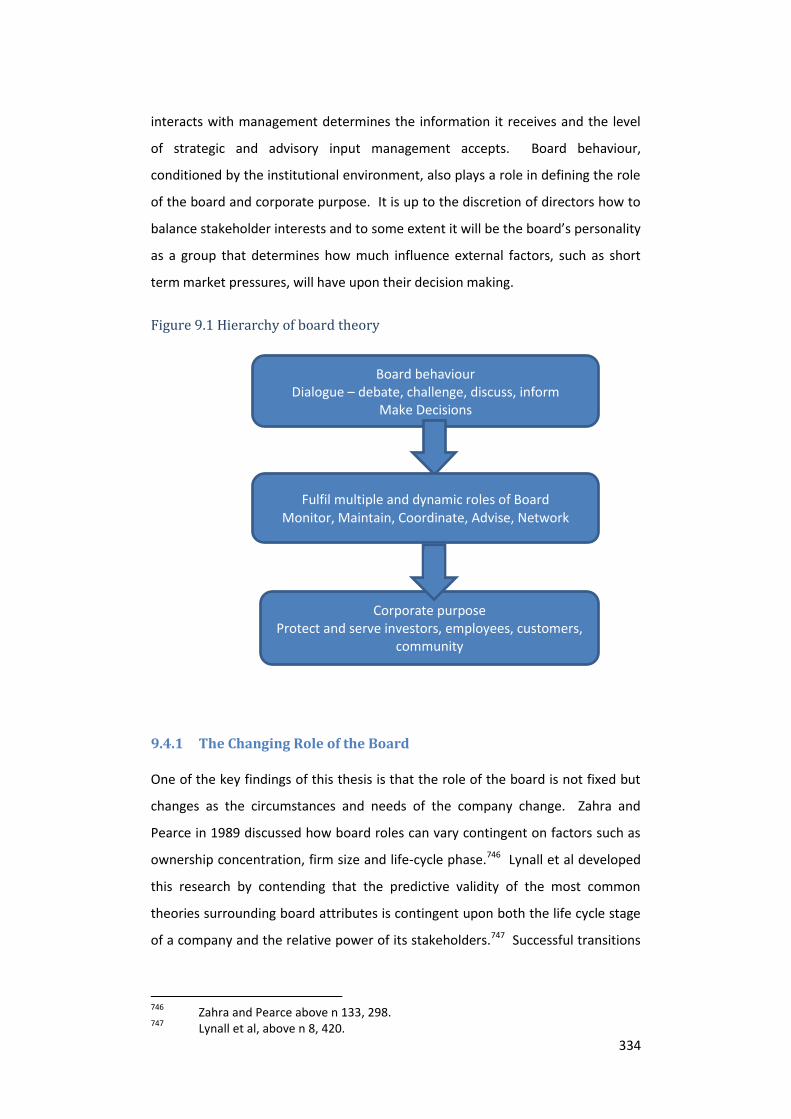

Figure 9.1 Hierarchy of board theory.................................................................... 334

Figure 9.2 Dialogue as the key to board effectiveness ......................................... 343

Figure 9.3 New governance regulation ................................................................. 350

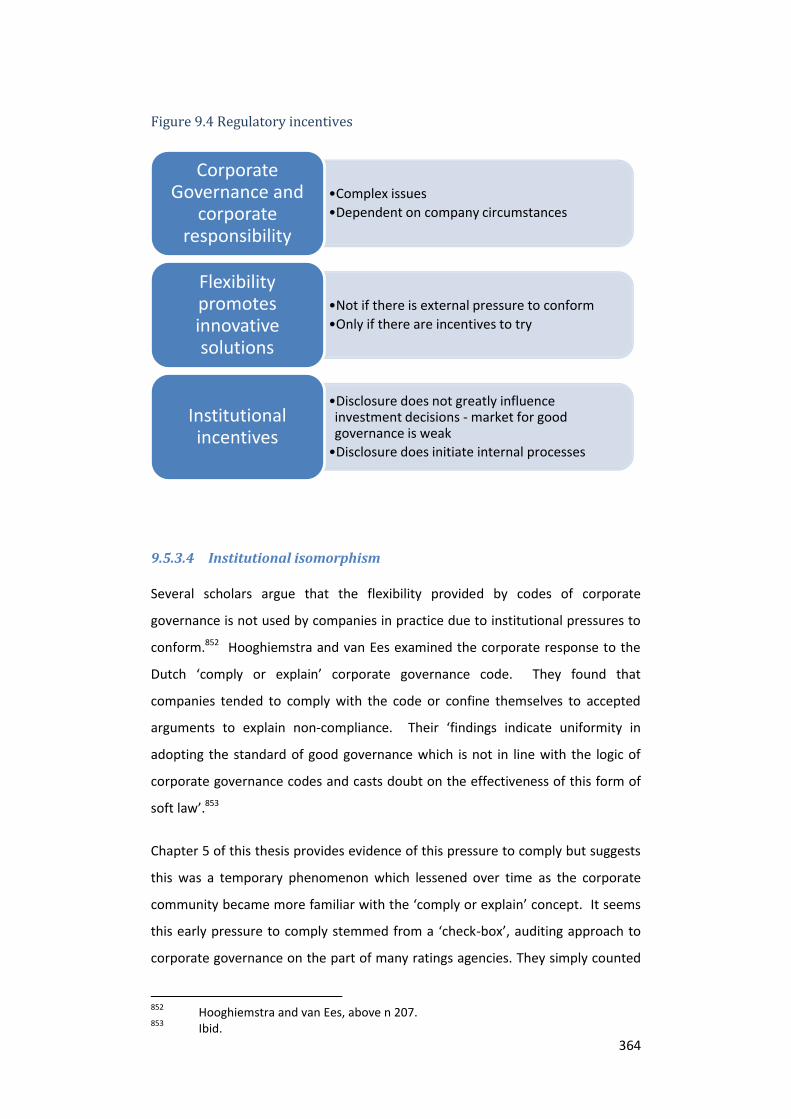

Figure 9.4 Regulatory incentives ........................................................................... 364

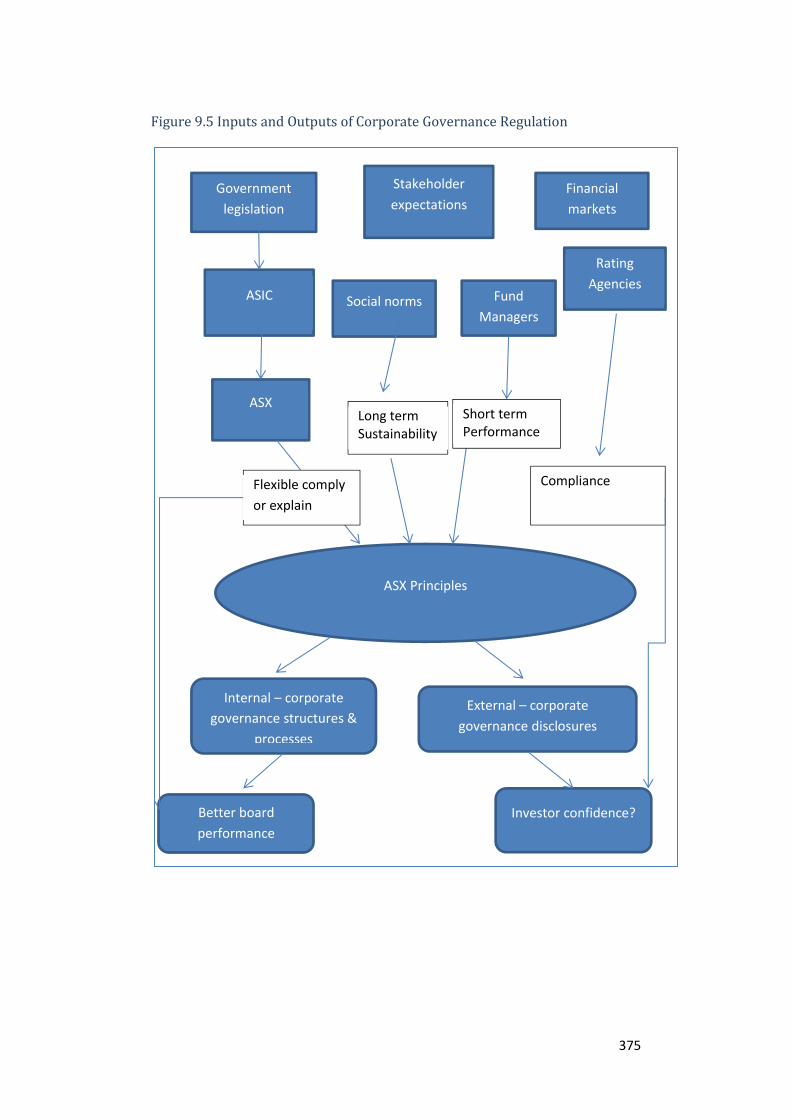

Figure 9.5 Inputs and Outputs of Corporate Governance Regulation .................. 375

xii

Abstract

The objective of this thesis is to explore, using empirical evidence, the effect of

recent corporate governance reforms in Australia. The Australian Securities

Exchange (ASX) implemented a code of corporate governance in 2003 which has

been regularly revised. The thesis focuses on this semi-voluntary code of

corporate governance, exploring how it has resulted in changes in corporate

behaviour and its effectiveness at improving board performance. By interviewing

directors and other company officers, as well as reviewing published evidence of

companies’ corporate governance systems, the thesis builds theory regarding

corporate governance and its regulation founded closely upon empirical data.

The thesis finds that the contemporary role of the board is complex: collaboration

with management may be more important to effective board function than

monitoring. Open dialogue between board and management is the key to an

effective board, a process that enables it to fulfil its multiple roles. The role of the

board can change over time and is dependent on company circumstances.

Directors, in fulfilling their legal duty to act in the best interests of the company

balance the interests of different stakeholders. This involves incorporating these

interests into operational strategies to improve long-term sustainability.

Using specific recommendations of the Australian corporate governance code as

regulatory case studies, the thesis finds that the flexibility of the ASX corporate

governance code is vital in permitting companies to create tailored solutions to

their governance needs. The provisions of the code that require regular review of

corporate governance and setting of targets are some of the most effective

because they keep corporate governance structures and processes alive and

relevant. Corporate governance codes appear to influence behaviour through the

internalisation of processes rather than through external pressure based directly

on corporate disclosures. Indeed, understanding the interplay between soft

regulation and its institutional environment is essential to effective policy making.

Voluntary regulation relies on tapping into this institutional environment to

provide incentives for desired behaviour. In doing so it builds on and enforces

emerging norms of behaviour and entrenches them into corporate culture

through a slow process of change management.

1

1 Introduction to Thesis

Recent years have shown that large and powerful companies can collapse very

suddenly causing great damage to national economies and the livelihoods of the

people who work and invest in them. As a consequence, corporate governance

has become a regular issue on most government policy agendas. Corporate

governance regulation, which can include both hard law and softer forms of

regulation, has been through several cycles of reform and yet collapses continue

to occur. Codes of corporate governance have been implemented in most

developed countries recommending detailed governance frameworks for

publically listed companies.1 The latest reforms, post-global financial crisis,

provide renewed focus on the board of directors and its role in corporate

governance.2

The objective of this thesis is to explore, using empirical evidence, the effect of

recent corporate governance reforms in Australia. The Australian Securities

Exchange (ASX) implemented a code of corporate governance in 2003 which has

been regularly revised, the third edition published in March 2014. The thesis

focuses on this semi-voluntary code of corporate governance, exploring how it

has resulted in changes in corporate behaviour and its effectiveness at improving

board performance. By interviewing directors and other company officers, as well

as reviewing published evidence of companies’ corporate governance systems,

the thesis builds theory regarding corporate governance and its regulation

founded closely upon empirical data.

An understanding of the role of the board across different contexts is essential in

both setting regulatory policy and assessing regulatory effectiveness. This thesis

proceeds on the assumption that to be effective, regulation should facilitate and

1 D Seidl, P Sanderson and J Roberts, ‘Applying the ‘comply-or-explain’ principle:

discursive legitimacy tactics with regard to codes of corporate governance’ (2013) 17(3) Journal of Management and Governance 791-826; Weil, Gotshal & Manges, Comparative Study of Corporate Governance Codes Relevant to the European Union and its Member States (European Commission, 2002) 22.

2 G Kirkpatrick, ‘Corporate Governance Lessons from the Financial Crisis’ (OECD, 2009).

2

encourage good board performance as well as deter poor practices.3 In exploring

what directors do day-to-day and the structures and processes they use to fulfil

their responsibilities, the thesis develops theory regarding the modern role of the

board of directors. It also develops theory regarding the mechanisms of soft

regulation by throwing light on the processes through which corporate

governance codes can lead to changes in behaviour.

I chose this topic for my thesis because I am interested in the practicalities of

corporate governance and the impact of law and regulation on society. As a

solicitor in London in the late 1990s I reviewed the 1998 Hampel Report and

became interested in the concept of voluntary regulation and the question of

whether and how it can be persuasive enough to change corporate behaviour.

My early research at the Centre for Corporate Governance at UTS required me to

read numerous corporate governance statements in annual reports and left me

sceptical as to their usefulness to investors. When I started this thesis, academic

research on the theory behind ‘comply or explain’ corporate governance codes

was very scarce, as was academic justification of their content.4 Other than

several surveys of compliance rates, it is still true that ‘very little scholarly

research has been carried out on how the comply-or-explain mechanism functions

in practice’5. As my research career progressed and I interviewed corporate

directors, the leading theory behind corporate governance and its regulation,

agency theory, appeared to have little in common with the realities of board

practice.

This thesis aims to review the theories behind corporate governance codes and

the role of the board by exploring how one such code (the ASX Principles of

Corporate Governance) functions in practice. The aim of the thesis is to explore

the following research questions:

3 R Adams, B E Hermalin and M S Weisbach, ‘The Role of Boards of Directors in

Corporate Governance: A Conceptual Framework and Survey’ (Working Paper Series, Center for Responsible Business, UC Berkley, 2008) 44.

4 At the time I could only find a working draft of I MacNeil and X Li, ‘Comply or explain: Market discipline and non-compliance with the combined code’ (2006) 14(5) Corporate Governance: An International Review 486–496.

5 Seidl et al, above n 1, 792; R V Aguilera and A Cuervo-Cazurra, ‘Codes of Good Governance’ (2009) 17(3) Corporate Governance: An International Review 376-387.

3

1. What is the modern role of the board in corporate governance

and

2. How does soft regulation facilitate fulfilment of that role?

The first research question is exploratory - it asks ‘what is the role of the board’,

an open question but also a theoretical question which may be answered

descriptively. This broad exploratory research has a specific purpose – its

conclusions as to the modern role of the board have direct consequences for the

effectiveness of corporate governance regulation. If the objective of corporate

governance regulation is to facilitate the board in fulfilling its role in directing the

company, understanding the nature of the role of the board is vital in setting

effective regulatory policy. The second thesis research question follows directly

from the first but is more explanatory and policy-focused - it is searching for

operational links between the role of the board and corporate governance

regulation. 6

1.1 The Role of the Board

This thesis explores the modern role of the board of directors against a

background of regulatory reforms designed to improve board performance.

Boards exist to manage, direct, supervise and advise. They lead and represent the

company and ensure that it is accountable to its shareholders and other relevant

stakeholders. This thesis explores the many different theories behind these board

roles and their consequences for regulatory design.

Agency theory posits the board as the shareholders’ agent, protecting

shareholders from managerial misbehaviour in circumstances where they are not

in a position to monitor and control management themselves. In contrast,

stewardship theory paints managers as trustworthy individuals who need to be

empowered to act on behalf of the organisation. Other theories, discussed in

more detail in Chapter 4, focus on the board’s role in providing skills, resources

and strategic direction. Many scholars have noted the potentially competing

demands placed on directors: to balance compliance and performance, to

monitor the present while preparing for the future, to act as both advisor and 6 R K Yin, Case Study Research: Design and Methods (SAGE Publications, 4th ed,

2009).

4

guard.7 The dilemma for regulatory policy-makers is how to facilitate the

fulfilment of these different roles when they may conflict with each other.

Certainly it is clear that the role of the board is multi-faceted and may change

over time and in different circumstances.8 The argument behind this thesis is that

we need to better understand the dynamic nature of the role of the board, if we

are to design effective regulation that will enhance board performance.

In response to board failures, regulatory reforms have proliferated across many

countries and yet some of their provisions remain controversial in terms of their

effectiveness.9 There is little empirical backing for many of these reforms. Indeed

it is argued that the strong focus on agency theory and improving the monitoring

capacity of the board may be detrimental to other important board functions.10

The aim of this thesis is to better understand the conditions that foster good

board performance and the role of regulation, particularly codes of corporate

governance, in creating those conditions.

1.2 Soft Corporate Governance Regulation

Most developed countries now have a corporate governance code that applies to

companies listed on the national stock exchange.11 The legal status of these codes

varies from country to country but in most cases they would not be classed as

hard law, rather they exist as forms of ‘soft law’ such as stock exchange rules,

7 F G Hilmer and R I Tricker, An Effective Board, From the company director manual

(Pearson/Prentice Hall 1991 Sydney) cited in T Clarke, International Corporate Governance: A comparative approach (Routledge, 2007) 34.

8 M D Lynall, B R Golden and A J Hillman, ‘Board Composition from Adolescence to Maturity: A Multitheoretic View’ (2003) 28(3) Academy of Management Review 416, 416.

9 C M Dalton and D R Dalton, 'Boards of Directors: Utilizing Empirical Evidence in Developing Practical Prescriptions' (2005) 16 British Journal of Management S91-S97; R Romano, ‘The Sarbanes-Oxley Act and the Making of Quack Corporate Governance’ (2005) 114(7) The Yale Law Journal 1521-1611.

10 D C Langevoort, ‘The Human Nature of Corporate Boards: Law, Norms and the Unintended Consequences of Independence and Accountability’ (2001) 89(4) Georgetown Law Journal 797-832.

11 Eg, in 2004, the OECD reported that ‘since the [OECD] Principles were agreed in 1999, some 30 codes or principles have been established in the OECD area’, see OECD, Corporate Governance: A Survey of OECD Countries (2004) 43-51. The European Corporate Governance Institute maintains a list of corporate governance codes that includes codes applicable to over 90 nations, available at <http://www.ecgi.org/codes/all_codes.php>.

5

codes, standards or recommendations.12 They deal with the practical aspects of

corporate governance such as the composition of the board of directors; its role

and responsibilities; and communications with shareholders. Scholars have

recognised that academic research has lagged behind the development of codes

of corporate governance meaning that codes are not necessarily based on a sound

understanding of the role of the board and its influence on company

performance.13 There is only scattered academic work questioning the substance

and content of corporate governance codes and whether, and in what

circumstances, adoption of recommended practices has valuable outcomes for

corporations and their stakeholders.14 As Finegold et al put it, ‘there is, at best,

weak guidance for policymakers on what governance practices will lead to more

effective firm performance’.15 One of the practical aims of this thesis is to develop

recommendations to assist future policy-making.

The thesis explores two factors impacting on the effectiveness of regulation (1) its

content; and (2) its mechanism. Even if all of the recommended structures and

processes in a corporate governance code were guaranteed to improve board

performance, is a voluntary ‘comply or explain’ mechanism strong enough to

instigate change? Seidl states: ‘Although codes of corporate governance have

come to be widely used as a mode of regulating corporations, our understanding

of how they function is still rather limited’.16 The Organisation for Economic Co-

operation and Development (OECD) made the statement that:

12 See A Keay, ‘Comply or Explain: In need of Greater Regulatory Oversight’ (2014)

34(2) Legal Studies 279-304. 13 Eg, Seidl et al, above n 1; D Seidl, ‘Standard Setting and Following in Corporate

Governance: An Observation-Theoretical Study of the Effectiveness of Governance Codes’ Organization (2007) 14(5) 705-727; Aguilera and Cuervo-Cazurra above n 5, 376.

14 D Finegold, G S Benson and D Hecht, ‘Corporate Boards and Company Performance: review of research in light of recent reforms’ (2007) 15(5) Corporate Governance: An International Review 865-878; Romano, above n 9; L E Ribstein, ‘Market vs Regulatory Responses to Corporate Fraud: A Critique of the Sarbanes-Oxley Act of 2002’ (2002) 28 Journal of Corporate Law 1.

15 Finegold et al, above n 14, 865. 16 D Seidl, ‘Regulating Organizations through codes of corporate governance’

(Working Paper No. 338, Centre for Business Research, University of Cambridge, December 2006).

6

Although voluntary codes and principles have the advantage of

maintaining flexibility and avoiding excessive and costly legal and

regulatory measures, the question of their effectiveness does arise.17

This sums up the balance that most corporate governance regulation is aiming to

achieve between permitting flexibility and yet encouraging change. It is generally

acknowledged that corporate governance is an area where it is not appropriate to

take a ‘one-size fits all’ approach. This is because the optimal structures and

processes for any particular company will depend on contingencies such as size,

ownership structure, industry and maturity.18 As a consequence, regulation is

designed to give a high level of discretion to companies in terms of whether or not

they adopt recommended practices. Most codes of corporate governance

operate on the basis of requiring disclosure rather than mandating specific

practices. Companies must explain if they do not adopt a particular practice but

are permitted to choose, a mechanism known as ‘comply or explain’ or ‘if not,

why not’. Corporate governance regulation is an area where the regulatory ‘rules

versus principles’ debate is often aired. Some countries take a more prescriptive,

rules based approach and others rely on voluntary or semi-voluntary principles.

This thesis will explore some of the theories behind the different methods of

regulating corporate governance, particularly the use of codes of best practice. Its

aim is to develop through empirical study, knowledge of how some of these new

soft regulatory mechanisms come to change behaviour.

1.3 Research Methodology

Many researchers have attempted to draw a relationship between corporate

governance practices and financial performance with inconclusive results.19 This

is not surprising considering the complex interaction of factors that lead to a

firm’s financial results. As a result, there have been repeated calls for ‘the use of

17 OECD, above n 11, 52. 18 Lynall et al, above n 8. 19 See, eg, A Levrau and L Van den Berghe, ‘Corporate Governance and Board

Effectiveness: Beyond Formalism’ (Vlerick Leuven Gent working Paper Series 2007/03); G C Kiel and G J Nicholson, ‘Board Composition and Corporate Performance: how the Australian experience informs contrasting theories of corporate governance’ (2003) 11 Corporate Governance: An International Review 189-205, 190.

7

a more in-depth, qualitative approach involving the direct study of boards and

contact with corporate directors’.20

This thesis builds on this stream of mostly management research into board

process and dynamics by taking a novel approach of viewing board function

through a regulatory lens. It focuses on the ASX Corporate Governance Principles

and Recommendations (ASX Principles) and takes specific code recommendations

as case studies to explore their implementation across a sample of Australian

corporations. It compares the intended effect of the recommendations with their

actual effect, in doing so comparing the role of the board envisaged by the

regulator against the actual role carried out in practice. The thesis takes the view

that code effectiveness should be measured, not through compliance levels, but

by assessing whether positive changes in corporate behaviour can be identified

that improve the governance of corporations.

The thesis takes an in-depth look at the effect of four areas of Australia’s

corporate governance code: (1) board structure and composition; (2) board

evaluations; (3) gender diversity; and (4) corporate responsibility, by exploring

how companies implement specific code recommendations and why. The four

topic areas were chosen because they reflect the trajectory of my work at the UTS

Centre for Corporate Governance. In my nine years as a Research Associate at the

Centre I personally managed several research projects which raised questions

about the effectiveness of corporate governance regulation:

The Changing Roles and Responsibilities of Company Boards and Directors

– a linkage project funded by the Australian Research Council and law firm

Dibbs Abbott Stillman which explored the role of the board following the

publication of the first edition of the ASX Principles.21

Board Performance and Effectiveness – commissioned by the Australian

Council of Superannuation Investors which examined the use of board

20 R Leblanc and M S Schwartz, ‘The Black Box of Board Process: gaining access to a

difficult subject’ (2007) 15(5) Corporate Governance: An International Review 843-851, 844. See also Langevoort, above n 10, 832.

21 See A Klettner, T Clarke and M Adams, ‘Corporate governance reform: An empirical study of the changing roles and responsibilities of Australian boards and directors’ (2010) 24 Australian Journal of Corporate Law, 148-176.

8

performance evaluations in Australian companies and the value to

investors of disclosures about board evaluation;22

Steering Sustainability – commissioned by Catalyst Australia which

explored the board’s role in leading and implementing corporate

responsibility strategy;23 and

The 2012 Australian Census of Women in Leadership – commissioned by

the Australian Government’s Equal Opportunity in the Workplace Agency

and sponsored by Australia New Zealand Bank - which surveyed the

number of women on boards and in executive teams in light of the 2010

amendments to the ASX Principles promoting gender diversity.24

Each project received funding from an external partner who led the direction of

the research. I was the core researcher for each project, guided by my supervisor

Professor Thomas Clarke.25 For each project, I personally collected a large amount

of empirical data. It was the collection of this data and the parallels that I could

see emerging between these distinct projects that inspired me to write this thesis.

In this thesis I draw on some of the raw data collected for each project to inform

my own research questions. Where necessary, I have the permission of each

external partner to use the raw data in this way. Some but not all of the data has

been published within the research reports for each project. However, the

interpretation of the data in this thesis is entirely original as the data is being used

22 See T Clarke and A Klettner, ‘Board Performance and Effectiveness’ (Australian

Council of Superannuation Investors, 28 October 2010) available at <http://www.acsi.org.au/research/research-reports.html>. Also A Klettner and T Clarke, ‘Board Evaluation Post-Financial Crisis’ (2011) 63(4) Keeping Good Companies 200-206.

23 A Klettner, Steering Sustainability (Catalyst Australia, December 2012) available at <http://www.catalyst.org.au/campaigns/full-disclosure/126-steering-sustainability>. See also A Klettner, T Clarke and M Boersma, ‘The Governance of Corporate Sustainability: Empirical Insights into the Development, Leadership and Implementation of Responsible Business Strategy’ (2014) 122(1) Journal of Business Ethics 145-165.

24 T Clarke, B B Nielsen, S Nielsen, A Klettner and M Boersma, 2012 Australian Census of Women in Leadership (Australian Government, Equal Opportunity for Women in the Workplace Agency, Sydney, 2012); A Klettner, T Clarke and M Boersma, ‘Strategic and Regulatory Approaches to Increasing Women in Leadership: Multi-level Targets and Mandatory Quotas as Levers for Cultural Change’ (2014) Journal of Business Ethics, published online 16 January 2014.

25 Professor Clarke is my supervisor both in relation to my employment and for this thesis.

9

to inform my research questions which are different from the research questions

set for each project. The findings in Chapters 5-8 do not simply relate to the four

research projects completed. They take a particular topic of the ASX Principles as

a focal point, and use all relevant evidence, across all four projects, to attempt to

answer the research questions. Thus the different data sources are combined in a

novel way to inform the thesis research questions.

For each of the ASX Recommendations under review, the thesis makes

assumptions about their intended effect and then uses interview and annual

report data to draw conclusions about the extent to which that effect has been

achieved. The aim is that, in drawing these findings together, it will be possible to

1. Contribute to corporate governance theory in terms of better

understanding the contemporary role of the board of directors in listed

companies;

2. Contribute to regulatory theory through understanding the processes

through which corporate governance codes affect corporate behaviour;

3. Make recommendations for regulators about how to make corporate

governance codes more effective.

1.4 Thesis Structure

This Chapter 1 introduces the aims and objectives of the thesis, its structure and

methodology.

Chapter 2 provides the practical and factual context to the thesis by providing an

account of the background to Australia’s corporate governance regulation; the

reasons for its development; and its reform over recent years including the

influence of developments overseas.

Chapter 3 describes in more detail the thesis research design and methodology,

explaining the need for research based on empirical evidence, particularly

qualitative, process-based studies which explore corporate governance in terms

of board behaviour and evaluate the impact of law and regulation on boards, their

companies and wider society.

10

Chapter 4 provides the theoretical context for the thesis by providing a review of

relevant literature. The thesis purposely aims to be cross-disciplinary, integrating

literature based in the disciplines of both law and management on the role of the

board of directors and corporate governance regulation. Chapter 4 reviews

common theories regarding the role of the board and discusses the consequences

of each theory for corporate governance regulation. It also reviews some of the

literature on the theories behind modern use of soft regulation including

voluntary codes of corporate governance.

Chapters 5 to 8 then present the empirical findings. Each chapter focuses on a

particular topic covered by the ASX Principles and explores the implementation of

specific corporate governance recommendations in Australian corporations.

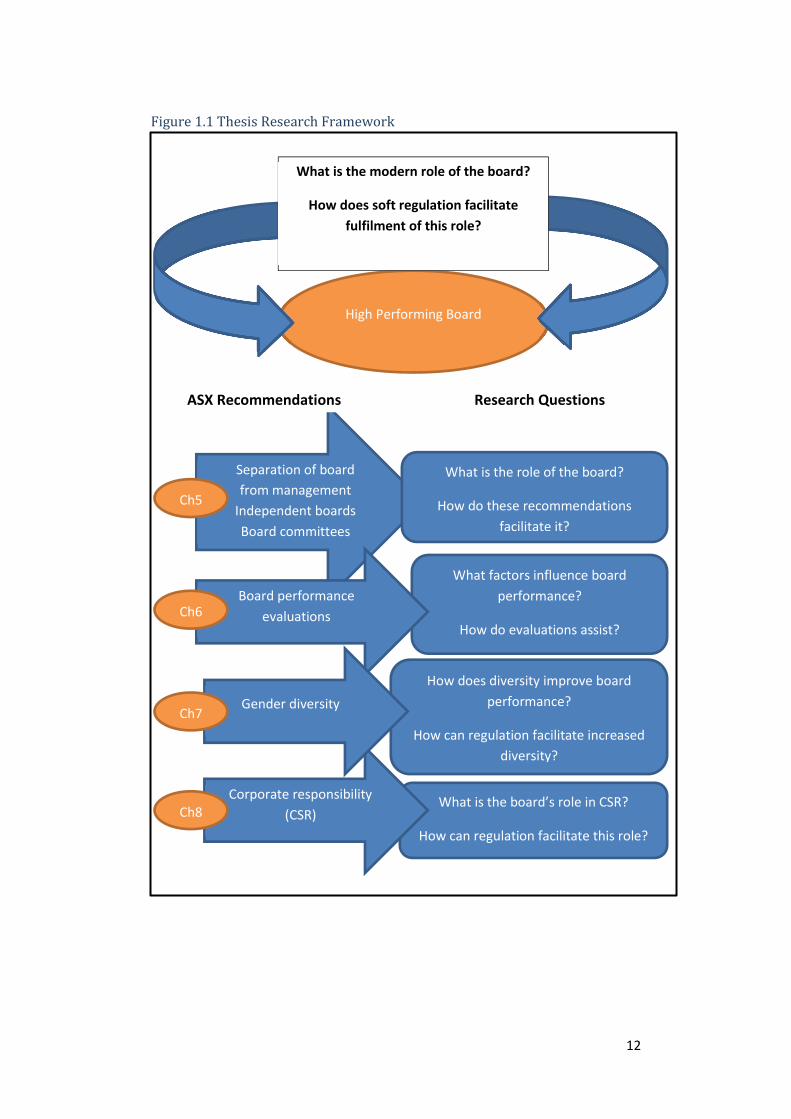

Figure 1.1 shows the topics covered and how they relate to the broader thesis

research questions.

Chapter 5 deals with the role of the board and the ASX recommendations that

suggest separation of board and management roles and director independence. It

also deals with the role of board committees and the ASX recommendations that

suggest that listed companies should set up audit, nomination and remuneration

committees. It provides evidence, obtained from both annual reports and

interviews with corporate officers, regarding the contemporary role of the board

as well as the adoption of committees and their value in improving corporate

governance.

Chapter 6 examines the effectiveness of the ASX recommendation suggesting that

listed companies should conduct board performance evaluations regularly and

disclose the process used. It presents evidence, from both annual reports and

interviews with directors, of the extent of adoption of this recommendation and

its value in improving board performance.

Chapter 7 examines the issue of gender diversity on boards following the

introduction, in 2010, of ASX recommendations encouraging the measurement

and promotion of diversity. It provides evidence, obtained from annual reports

and interviews with company officers, of the adoption of these recommendations

and the perceived value of diversity on boards.

11

Chapter 8 explores the role of the board in corporate responsibility by examining

how companies have implemented the ASX recommendations that refer to acting

ethically and responsibly in terms of taking into account the reasonable

expectations of stakeholders such as shareholders, employees, customers,

suppliers, and the broader community. It provides evidence, obtained from

annual reports and interviews with company officers, of the different methods

that companies use to implement corporate responsibility strategies and their

value to the firm.

Chapter 9 then draws together the findings of Chapters 5-8 by way of a discussion

of the contemporary role of the board and the mechanisms through which

regulation can facilitate board performance. It draws out the common themes of

Chapters 5-8 and analyses what they mean in the context of the literature on

board roles, corporate governance and soft law regulation.

Chapter 10 concludes with recommendations for regulators and companies on

how to implement the ASX Principles most effectively and how regulation might

be improved to better facilitate board performance.

12

Separation of board from management

Independent boards Board committees

What is the role of the board?

How do these recommendations facilitate it?

What factors influence board performance?

How do evaluations assist?

What is the board’s role in CSR?

How can regulation facilitate this role?

Board performance evaluations

Corporate responsibility (CSR)

How does diversity improve board performance?

How can regulation facilitate increased diversity?

Gender diversity

ASX Recommendations Research Questions

Ch5

Ch6

Ch7

Ch8

High Performing Board

What is the modern role of the board?

How does soft regulation facilitate fulfilment of this role?

13

2 Corporate Governance Regulation

This chapter provides the context to this thesis by describing the background to

Australia’s current corporate governance regulation. This includes reference to

development of corporate governance regulation internationally, particularly in

the United Kingdom (UK) and United States (US) because these regimes have had

a strong influence in Australia. As the aim of the thesis is to explore the

effectiveness of specific regulatory provisions it is important to understand the

wider purpose of corporate governance regulation and how it has developed to

be what it is today. As a relatively new and dynamic area of regulation, the aims

and objectives of corporate governance have expanded over time as the overall

corporate environment has become increasingly complex. Despite international

agreement on the broad nature of corporate governance through organisations

such as the United Nations and Organisation for Economic Co-operation (OECD)26

corporate governance systems vary across countries reflecting cultural, political

and economic differences. The problems that any regulation is designed to

resolve and the mechanisms likely to be effective at initiating change will also

depend on these national differences.27 Having said this, in the last two decades,

most developed countries have introduced a code of corporate governance for

companies listed on their national stock exchange.28

2.1 Definitions

2.1.1 Corporate Governance

First it is important to define corporate governance and hence corporate

governance regulation. Early attempts to define the concept of corporate

governance appear in the United Kingdom Cadbury Report (1992) and the South

26 The OECD Principles of Corporate Governance were first released in May 1999;

revised in 2004; and at the time of writing in 2014 were going through another review process. They are one of the 12 key standards used by the international Financial Stability Board and World Bank Group available at <http://www.oecd.org/corporate/oecdprinciplesofcorporategovernance.htm>.

27 See, eg, A Cuervo, ‘Corporate Governance Mechanisms: a plea for less code of good governance and more market control’ (2002) 10(2) Corporate Governance: An International Review 84-93; N K Cankar, S Deakin and M Simoneti, ‘The Reflexive Properties of Corporate Governance Codes: The Reception of the ‘Comply-or-Explain’ Approach in Slovenia’ (2010) 37(3) Journal of Law and Society 501-525.

28 Seidl et al, above n 1.

14

African King Report (1994), defined at its simplest as ‘the system by which

companies are directed and controlled’.29 Since then, there have been many

attempts to elucidate the concept in more detail. The second edition of the ASX

Corporate Governance Principles and Recommendations (ASX Principles), the

provisions of which this thesis will test, defines corporate governance as follows:

Corporate governance is ‘the framework of rules, relationships, systems

and processes within and by which authority is exercised and controlled in

corporations’. It encompasses the mechanisms by which companies, and

those in control, are held to account. Corporate governance influences

how the objectives of the company are set and achieved, how risk is

monitored and assessed, and how performance is optimised. Effective

corporate governance structures encourage companies to create value,

through entrepreneurialism, innovation, development and exploration,

and provide accountability and control systems commensurate with the

risks involved.30

Thus corporate governance is a broad topic – it covers the structures and

processes that define and guide the roles and relationships of the key players in a

corporation – shareholders, directors, managers and wider stakeholders such as

employees and creditors. As Justice Owen has commented ‘the expression

‘corporate governance’ embraces not only the models or systems themselves but

also the practices by which that exercise and control of authority is in fact

effected’.31 Tomasic et al define corporate governance as ‘the structures,

processes and systems, both formal and informal, by which power is exercised,

constrained, monitored and accounted for in the management of a corporation’.32

As the ASX definition suggests, corporate governance is aimed at both creating

value and maintaining control. This is reflected in the well-known framework

29 J J du Plessis, A Hargovan and M Bagaric, Principles of Contemporary Corporate

Governance, (Cambridge University Press, 2nd ed, 2010) 3. 30 ASX Corporate Governance Council, Corporate Governance Principles and

Recommendations (ASX, 2nd ed, August 2007) 3, available at <http://www.asx.com.au/regulation/corporate-governance-council.htm> citing N Owen, The Failure of HIH Insurance Volume 1: A Corporate Collapse and Its Lessons (Commonwealth of Australia, April 2003) xxxiii.

31 Owen, ibid xxi. 32 R Tomasic, S Bottomley and R McQueen, Corporations Law in Australia

(Federation Press, 2nd ed, 2002) 262.

15

developed by Hilmer and Tricker which depicts the role of the board as balancing

conformance (monitoring and accountability) with performance (strategy and

policy).33 Chapter 4 discusses in more detail some of the theories behind the role

of the board in corporate governance. The empirical evidence reviewed in this

thesis then explores the reality of the modern role of the board and its interaction

with corporate governance regulation.

Mechanisms of corporate governance are often distinguished as either internal or

external.34 Internal corporate governance concerns the relationships and balance

of powers within a corporation, primarily between the board, managers and

shareholders but also other key stakeholders such as employees and creditors.35

External corporate governance refers to outside forces that exercise a disciplining

influence on managers, such as takeover markets, financial markets and

regulatory intervention.36 This is an important distinction that raises its head at

several points in this thesis because regulatory initiatives can be aimed at both

improving internal processes and disclosing information about those processes.

One aim is to create the internal structures and processes necessary for good

corporate governance. Another aim is to improve information flow out of the

company to enable external forces to exert an influence. As Kingsford Smith

comments, corporate governance codes, as well as being an external influence

ideally have an internal effect - their incorporation into the company’s internal

rules, norms and culture.37 This dual objective is one of the features of corporate

governance codes discussed in more detail in Chapter 9. The findings of this

thesis throw light on the effectiveness of the ASX Principles at both causing

internal change and facilitating external market forces through disclosure of

information.

33 See Hilmer and Tricker, above n 7, 34. 34 K J Hopt, ‘Comparative Corporate Governance: The State of the Art and

International Regulation’ (2011) 59(1) The American Journal of Comparative Law 1-73, 4. See also D Kingsford Smith ‘Governing the Corporation: The Role of ‘Soft Regulation’’’ (2012) 35(1) University of New South Wales Law Journal 378-403, 382.

35 Hopt, above n 34, 4. 36 Ibid. 37 Kingsford Smith, above n 34, 382.

16

2.1.2 Corporate Governance Regulation

Corporate governance regulation, at its broadest, encompasses any law, rule,

standard or recommendation that is directed at influencing the way companies

are controlled and held to account. This includes most corporate law (in Australia,

the Corporations Act 2001) but also the codes and standards set by stock

exchanges, prudential regulators and accounting bodies which may be mandatory

or voluntary. Corporate governance regulation spans jurisdictional boundaries

and includes a burgeoning body of international initiatives – principles,

frameworks and standards, many of which would be classified as soft law.38

Corbett and Bottomley claim that it is useful to think of corporate governance

regulation as a body or category of law as well as a body of governance practices,

processes and structures.39

The focus of this thesis is the ASX Principles, Australia’s code of corporate

governance for companies listed on the Australian Securities Exchange. A code of

corporate governance can be defined generally as ‘a non-binding set of principles,

standards or best practices, issued by a collective body and relating to the internal

governance of corporations’.40 . This would fall squarely within most definitions of

‘soft law’, for example, Karmel and Kelly’s simple definition of soft law as ‘non-

binding standards and principles of conduct’ which they distinguish from hard law,

‘statutes, regulations and treaties’ that are binding.41 In reality, the divide

between hard and soft law is much less clear and there is a continuum of

instruments with varying degrees of obligation, precision and delegation.42

Branson comments that ‘at the level of large publicly held and multinational

corporations, a principal determinant of corporate behaviour has become ‘soft

38 Soft law tends to refer to quasi-legal instruments which do not have any legally

binding force. 39 A Corbett and S Bottomley, ‘Regulating Corporate Governance’ in C Parker, C

Scott, N Lacey and J Braithwaite (eds), Regulating Law (Oxford University Press, 2004) 60, 61.

40 Weil, Gotshal and Manges, International Comparison of Selected Corporate Governance Guidelines and Codes of Best Practice, (New York, 2003) cited in Seidl above n 16.

41 R S Karmel and C R Kelly, ‘The Hardening of Soft Law in Securities Regulation’ (2009) 34 Brooklyn Journal of International Law 883-951.

42 See, eg, S I Karlsson-Vinkhuyzen and A Vihma, ‘Comparing the legitimacy and effectiveness of global hard and soft law: An analytical framework’ (2009) 3 Regulation and Governance 400-420.

17

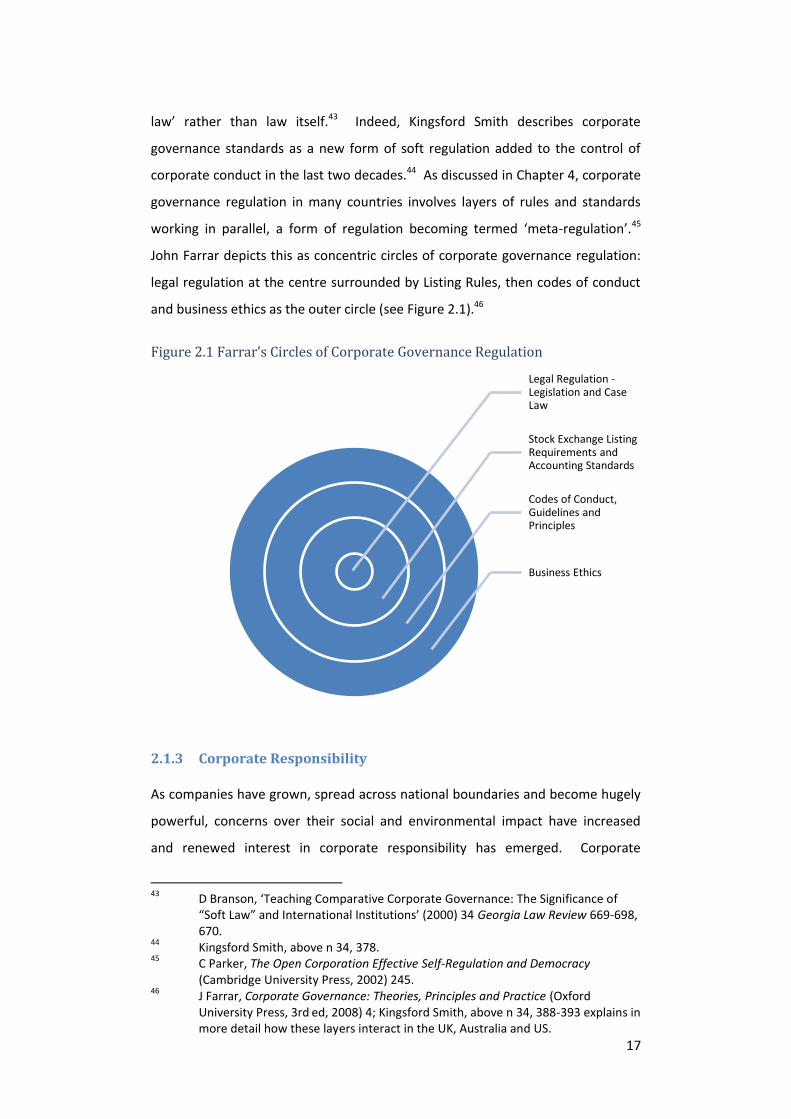

law’ rather than law itself.43 Indeed, Kingsford Smith describes corporate

governance standards as a new form of soft regulation added to the control of

corporate conduct in the last two decades.44 As discussed in Chapter 4, corporate

governance regulation in many countries involves layers of rules and standards

working in parallel, a form of regulation becoming termed ‘meta-regulation’.45

John Farrar depicts this as concentric circles of corporate governance regulation:

legal regulation at the centre surrounded by Listing Rules, then codes of conduct

and business ethics as the outer circle (see Figure 2.1).46

2.1.3 Corporate Responsibility

As companies have grown, spread across national boundaries and become hugely

powerful, concerns over their social and environmental impact have increased

and renewed interest in corporate responsibility has emerged. Corporate

43 D Branson, ‘Teaching Comparative Corporate Governance: The Significance of

“Soft Law” and International Institutions’ (2000) 34 Georgia Law Review 669-698, 670.

44 Kingsford Smith, above n 34, 378. 45 C Parker, The Open Corporation Effective Self-Regulation and Democracy

(Cambridge University Press, 2002) 245. 46 J Farrar, Corporate Governance: Theories, Principles and Practice (Oxford

University Press, 3rd ed, 2008) 4; Kingsford Smith, above n 34, 388-393 explains in more detail how these layers interact in the UK, Australia and US.

Legal Regulation - Legislation and Case Law

Stock Exchange Listing Requirements and Accounting Standards

Codes of Conduct, Guidelines and Principles

Business Ethics

18

responsibility has as its theoretical base the notion that the responsibility of a

corporation extends beyond the traditional Anglo-American objective of providing

financial returns to its shareholders. Instead, proponents of corporate

responsibility have argued that the legitimate concerns of a corporation should

include such broader objectives such as sustainable growth, equitable

employment practices, and long-term social and environmental well-being.47

Chapter 8 of this thesis explores the links between corporate governance and

corporate responsibility, particularly, how corporate governance processes and

structures can assist companies in developing and implementing corporate

responsibility strategies. Like corporate governance, corporate responsibility is

difficult to define. In fact, the confusion is even greater as there is no universally

agreed term for the concept let alone a definition. The Australian Parliamentary

Joint Committee Report on corporate responsibility (PJC Report) commented that

the terms ‘corporate responsibility’, 'corporate social responsibility (CSR)',

'corporate social transparency', 'triple bottom line', 'corporate sustainability' and

'social and environmental responsibility' are all used to refer to the same

concept.48 The working definition adopted by the PJC was:

Corporate responsibility is usually described in terms of a company

considering, managing and balancing the economic, social and

environmental impacts of its activities. It is about companies assessing

and managing risks, pursuing opportunities and creating corporate value,

in areas beyond what would traditionally be regarded as a company’s core

business. It is also about companies taking an ’enlightened self-interest’

approach to considering the legitimate interests of a company’s

stakeholders.49

In this wider interpretation corporate responsibility encompasses not only

compliance with legal obligations (environmental and employment legislation for

example), but also voluntary commitment to ethical and sustainable practices that

47 J M Conley and C A Williams, ‘Engage, Embed and Embellish: Theory versus

Practice in the Corporate Social Responsibility Movement’ (2005) 31 Iowa Journal of Corporation Law 1-38, 1.

48 Parliamentary Joint Committee on Corporations and Financial Services, Report on Corporate Responsibility’ (PJC Report) (June 2006) 4.

49 PJC Report, ibid 4.

19

benefit both society and the long-term success of the company. Carroll, in 1991,

provided a definition of CSR depicting a pyramid of responsibilities of increasing

priority (see Figure 2.2).50 At the base is the company‘s economic responsibility to

be profitable, upon which the other responsibilities rest. These are legal

compliance, ethical responsibility and, at the top of the pyramid, philanthropic

responsibility. Although philanthropy has somewhat lost favour (not as a laudable

activity but as a core aspect of long-term sustainability) this pyramid still

represents the basic tenets of corporate responsibility in terms of a company‘s

obligations to its stakeholders. It is the layer of the pyramid comprising ethical

responsibilities that makes up what we think of as corporate responsibility today:

a corporation going over and above its legal obligations to operate in an equitable

and responsible manner. Redmond defines CSR as ‘voluntary measures

undertaken by companies to integrate social, environmental and business

concerns in their operations and their interaction with stakeholders’.51

50 A B Carroll, Corporate social responsibility – evolution of a definitional

construction’ (1999) 38(3) Business and Society 268-295. 51 P Redmond, ‘Directors’ Duties and Corporate Social Responsiveness’ (2012) 35

University of New South Wales Law Journal 317-340, 320.

Philanthropic Responsibilities

Be a good corporate citizen

Ethical Responsibilities Do what is right, just

and fair and avoid harm

Legal Responsibilities Obey the law

Economic Responsiblities Be profitable

20

In 2001 Douglas Branson described the emergence of a ‘new corporate social

responsibility movement, different from previous efforts because of its

convergence with good corporate governance.52 Corporate governance and

corporate responsibility were for many years seen as different issues but the

overlap between the two is becoming increasingly evident as corporate

responsibility becomes more mainstream. Corporate responsibility has moved

from being a marketing response to specific events towards being a key element

of business strategy. This change requires leadership from the top and

integration of corporate responsibility across all aspects of the business. In 2006,

John Elkington, co-founder of SustainAbility, wrote about the merging of

corporate social responsibility with corporate governance that was then

occurring, the two having been thought for some time to be separate issues: ‘The

centre of gravity of the sustainable business debate is in the process of shifting

from public relations to competitive advantage and corporate governance – and,

in the process, from the factory fence to the boardroom’.53 Confirming this

development, a 2008 report by the Conference Board of Canada suggested that

‘good corporate governance will be redefined over this decade to include ways in

which a board provides oversight and strategic direction on the firm's social and

environmental performance’.54 KPMG’s 2011 report on the state of sustainability

reporting concluded that the integration of sustainability into core business

strategy and reporting was the next major development in the field.55 Chapter 8

of this thesis uses empirical evidence to explore the role of the board in corporate

responsibility and the role of the ASX Principles and other soft law regulation in

encouraging ethical behaviour.

52 D Branson, ‘Corporate Governance “Reform” and the New Corporate Social

Responsibility’ (2001) 62 University of Pittsburgh Law Review 605, 647. His paper provides a vivid and helpful history of corporate governance reform and efforts to make companies more responsible.

53 J Elkington, ‘Governance for sustainability’ (2006) 14(6) Corporate Governance: An International Review 522-529, 524.

54 Conference Board of Canada, The role of boards of directors in corporate social responsibility (2008).

55 KPMG, International Survey of Corporate Responsibility Reporting (2011).

21

2.2 Development and Reform of Corporate Governance Regulation

Henry Bosch, who produced one of the first reports on corporate governance in

Australia, refers to the fact that corporate governance is a modern term, nearing

30 years old: ‘Before the crash of 1987 the term corporate governance was rarely

used in Australia and few people gave much thought to the concepts now covered

by it’.56 Consequently, the development of corporate governance regulation is a

relatively recent phenomenon and has tended to be a reactive process responding

to bouts of corporate scandals and fear of economic downturn. It has involved

both a strengthening of legislated hard law but also development of rules,

standards and recommendations by many different organisations at national and

international levels. Indeed in most countries, corporate governance reform

tends to be cyclical, following the boom and bust of the business cycle.57 When

the economy is good, corporate regulation will be left alone but when the

economy falters, governments are placed under pressure to strengthen regulation

in order to reduce the risk of similar problems in future.

There have been three notable economic downturns relevant to the development

of corporate governance regulation in Australia and the pattern is similar

internationally. Each economic crisis has involved significant corporate collapses

and then a wave of investigations followed by regulatory reform. As corporations

and their markets have become more globalised so has the economic effect of

their failure. Thus the last of these crises, although originating in the United

States’ housing market, had impacts that were felt worldwide.58

It is difficult to decide on the best way to discuss the development of corporate

governance in Australia as reforms have been strongly influenced by international

developments. As Australian law grew from a mix of English and American

influences it is not surprising that corporate governance reforms in both the

56 H Bosch, ‘The changing face of corporate governance’ (2002) 25(2) University of

New South Wales Law Journal 270–293, 273. 57 T Clarke, ‘Cycles of Crisis and Regulation: the enduring agency and stewardship

problems of corporate governance’ (2004) 12(2) Corporate Governance: An International Review 153-161.

58 T Clarke, ‘Markets Regulation and Governance: The Causes of the Global Financial Crisis’ in D Branson and T Clarke (eds) The SAGE Handbook of Corporate Governance (SAGE, 2012) 533-555, 535.

22

United Kingdom and United States have been highly influential. The work of

international bodies such as the OECD, G-20 and European Union has also been

taken into account in Australian regulatory reform. At times Australia has been at

the forefront of corporate governance innovation and at other times Australian

institutions have been slower to react, benefiting from the lessons learnt

elsewhere.

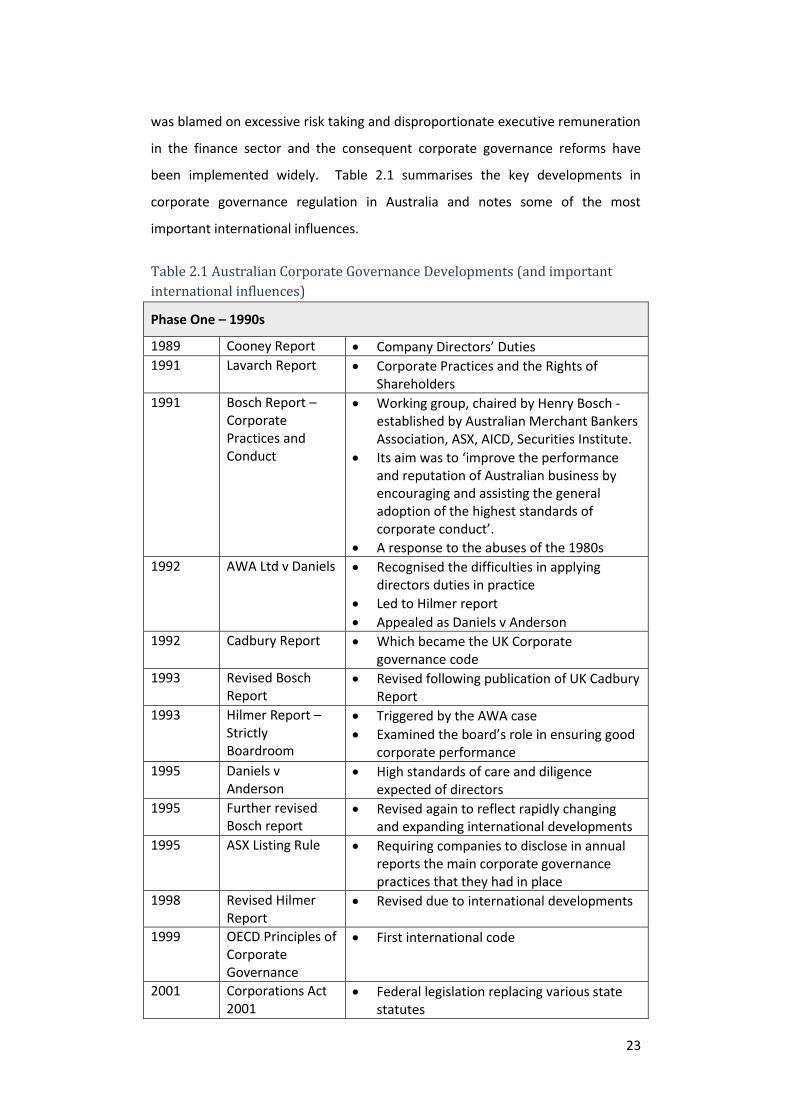

On this basis, this chapter takes a chronological journey through corporate

governance reform. Starting with the emergence of the term corporate

governance in the 1980s it charts Australia’s course of regulatory developments,

drawing on relevant international developments along the way. The disadvantage

of this approach is that it involves leaping from country to country, the advantage

is that it avoids moving back and forth in time. Australian corporate governance

reform is divided into three phases. The first phase, triggered by the corporate

misbehaviour of the 1980s, resulted in possibly the first ever report dedicated to

the topic of corporate governance, published in 1991, and a consolidated

Corporations Act in 2001. However, although Australia may have been at the

forefront in expressing some of the key concepts of corporate governance, it was

the United Kingdom that led the way in implementing these ideas in the form of a

‘comply or explain’ corporate governance code for listed companies published in

1992.

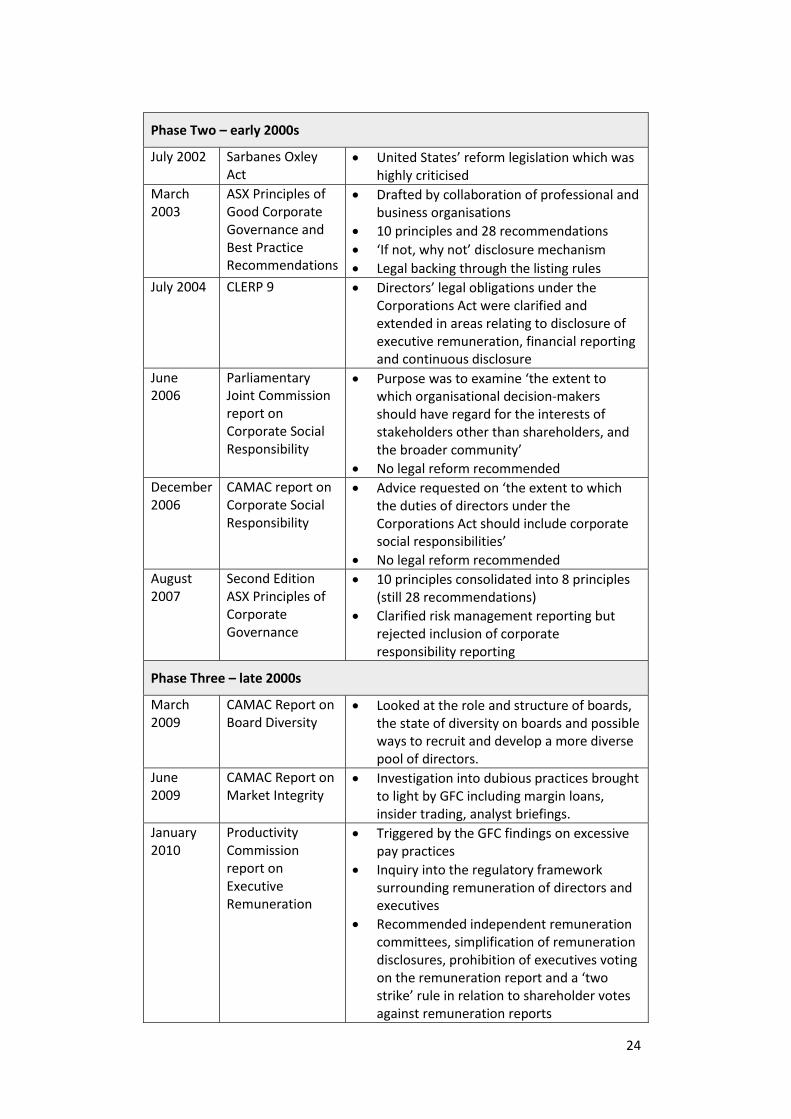

It was not until 2003 that Australia published its own corporate governance code.

This marked the start of a second phase of corporate governance reform,

triggered by the collapse of HIH insurance as well as American giants Enron and

Worldcom in 2001. At this stage it became clear that the United States was taking

a different regulatory path from that of the United Kingdom and Australia by

using prescriptive legislation (the Sarbanes Oxley Act of 2004) to implement

governance changes rather than a voluntary code. Also at this time, Australia

witnessed the anti-social behaviour of James Hardie Industries in underfunding its

compensation fund for asbestos-related injuries. This led to an important legal

debate over the role of the corporation in society and the links between

corporate governance and corporate responsibility.

The third phase of corporate governance reform was triggered by the global

financial crisis (GFC) that started to spread across the world in 2008. This crisis

23

was blamed on excessive risk taking and disproportionate executive remuneration

in the finance sector and the consequent corporate governance reforms have

been implemented widely. Table 2.1 summarises the key developments in

corporate governance regulation in Australia and notes some of the most

important international influences.

Phase One – 1990s

1989 Cooney Report Company Directors’ Duties 1991 Lavarch Report Corporate Practices and the Rights of

Shareholders 1991 Bosch Report –

Corporate Practices and Conduct

Working group, chaired by Henry Bosch - established by Australian Merchant Bankers Association, ASX, AICD, Securities Institute.

Its aim was to ‘improve the performance and reputation of Australian business by encouraging and assisting the general adoption of the highest standards of corporate conduct’.

A response to the abuses of the 1980s 1992 AWA Ltd v Daniels Recognised the difficulties in applying

directors duties in practice Led to Hilmer report Appealed as Daniels v Anderson

1992 Cadbury Report Which became the UK Corporate governance code

1993 Revised Bosch Report

Revised following publication of UK Cadbury Report

1993 Hilmer Report – Strictly Boardroom

Triggered by the AWA case Examined the board’s role in ensuring good

corporate performance 1995 Daniels v

Anderson High standards of care and diligence

expected of directors 1995 Further revised

Bosch report Revised again to reflect rapidly changing