corporate finance v escp-eap - european executive mba 14-15 dec. 2005, london risk, return,...

TRANSCRIPT

CORPORATE FINANCEV

ESCP-EAP - European Executive MBA

14-15 Dec. 2005, London

Risk, Return, Diversification and CAPM

I. Ertürk

Senior Fellow in Banking

Capital Asset Pricing Model

Re = Rf + B ( Rm - Rf )

CAPM

Re = cost of equityRf = risk free rate (Current Treasury bill yield)B = beta (market risk)Rm = long-term return on market portfolio (stock market index)Rf = long-term return on risk free asset (Treasury bill)(Rm- Rf) = market risk premium

Capital Asset Pricing Model (CAPM)

Return

BETA

Rf

1.0

Security Market Line

Cost of equity (Re) = Rf + B ( Rm - Rf )

Betas

Company Beta

Shell 1.53

Tesco 0.43

Barclays 1.22

Vodafone 0.84

Glaxo 0.71

Man 1.59

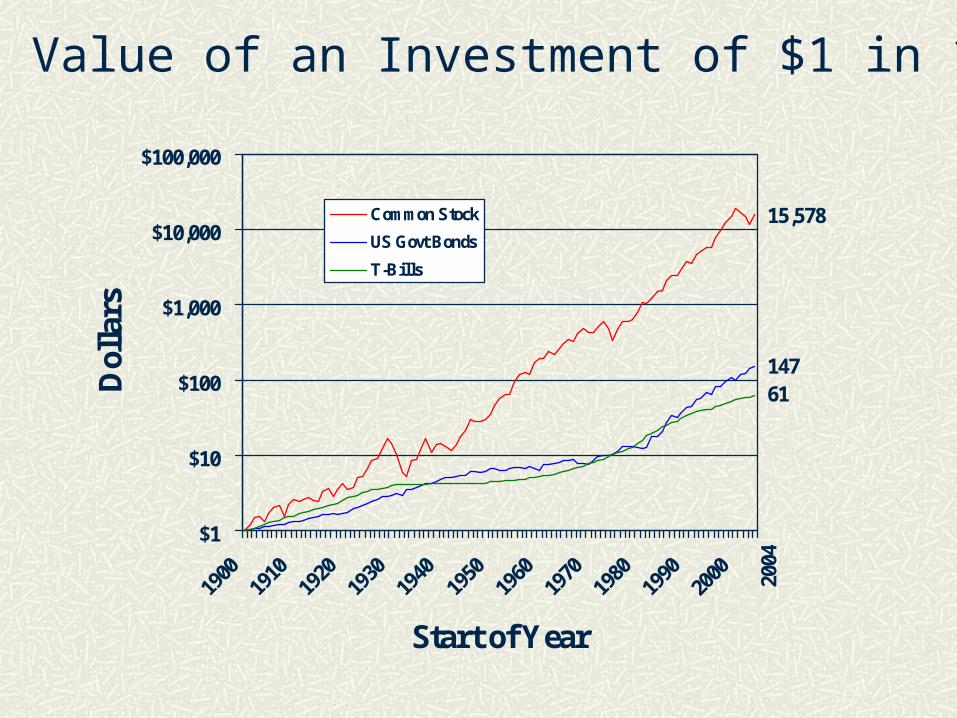

The Value of an Investment of $1 in 1900

$1

$10

$100

$1,000

$10,000

$100,000

1900

1910

1920

1930

1940

1950

1960

1970

1980

1990

2000

Start of Year

Dol

lars

Common Stock

US Govt Bonds

T-Bills

15,578

14761

2004

Rates of Return 1926-1997

Source: Ibbotson Associates

-60

-40

-20

0

20

40

60

26 30 35 40 45 50 55 60 65 70 75 80 85 90 95

Common Stocks

Long T-Bonds

T-Bills

Year

Per

cent

age

Ret

urn

Rates of Return 1900-2003

Source: Ibbotson Associates

-60%

-40%

-20%

0%

20%

40%

60%

80%

1900 1920 1940 1960 1980 2000

Year

Per

cent

age

Ret

urn

Stock Market Index Returns

Measuring Risk

1 14

1012

19

15

24

13

32

0

4

8

12

16

20

24

-50

to -

40

-40

to -

30

-30

to -

20

-20

to -

10

-10

to 0

0 to

10

10 t

o 20

20 t

o 30

30 t

o 40

40 t

o 50

50 t

o 60

Return %

# of Years

Histogram of Annual Stock Market ReturnsHistogram of Annual Stock Market Returns

Distribution of returns for Telus

0

1

2

3

4

5

6

7

-35% -30% -25% -20% -15% -10% -5% 0% 5% 10% 15% 20% 25% 30% 35%

Series1

-0.400

-0.300

-0.200

-0.100

0.000

0.100

0.200

0.300

0.400

0.500

04

/01

/19

99

04

/03

/19

99

04

/05

/19

99

04

/07

/19

99

04

/09

/19

99

04

/11

/19

99

04

/01

/20

00

04

/03

/20

00

04

/05

/20

00

04

/07

/20

00

04

/09

/20

00

04

/11

/20

00

04

/01

/20

01

04

/03

/20

01

04

/05

/20

01

04

/07

/20

01

04

/09

/20

01

04

/11

/20

01

04

/01

/20

02

04

/03

/20

02

04

/05

/20

02

04

/07

/20

02

04

/09

/20

02

04

/11

/20

02

04

/01

/20

03

04

/03

/20

03

04

/05

/20

03

04

/07

/20

03

04

/09

/20

03

04

/11

/20

03

XOM

HNZ

PFE

KO

Stock returns

Measuring Risk

Variance - Average value of squared deviations from mean. A measure of volatility.

Standard Deviation - Average value of squared deviations from mean. A measure of volatility.

Measuring Risk

Calculating variance and standard deviation

(1) (2) (3)

Percent Rate of Return Deviation from Mean Squared Deviation

+ 40 + 30 900

+ 10 0 0

+ 10 0 0

- 20 - 30 900

Variance = average of squared deviations = 1800 / 4 = 450

Standard deviation = square of root variance = 450 = 21.2%

Year Telus Market Index1973 -14.40% -0.51%1974 0.00% -22.57%1975 21.49% 15.35%1976 23.55% 8.80%1977 19.95% 9.64%1978 15.02% 29.10%1979 3.41% 43.94%1980 3.53% 29.70%1981 -6.12% -10.00%1982 18.36% 5.67%1983 32.17% 32.72%1984 3.77% -2.48%1985 24.36% 24.63%1986 7.02% 7.84%1987 -1.38% 6.24%1988 10.63% 10.88%1989 -32.63% 20.91%1990 12.61% -14.82%1991 24.57% 11.28%1992 -9.18% -1.70%1993 35.35% 31.90%1994 -0.59% -0.16%1995 9.46% 14.40%1996 23.84% 28.05%1997 54.64% 14.89%1998 -2.58% -1.58%1999 -12.87% 31.42%2000 22.19% 7.52%

Arithmetic average10.22% 11.82%STD 17.85% 15.82%correlation 73-2000 0.26

90-00 0.29

Beta 0.29

Markowitz Portfolio Theory

Combining stocks into portfolios can reduce standard deviation, below the level obtained from a simple weighted average calculation.

Correlation coefficients make this possible.

The various weighted combinations of stocks that create this standard deviations constitute the set of efficient portfolios.

Measuring Risk

Portfolio rate

of return=

fraction of portfolio

in first assetx

rate of return

on first asset

+fraction of portfolio

in second assetx

rate of return

on second asset

((

(())

))

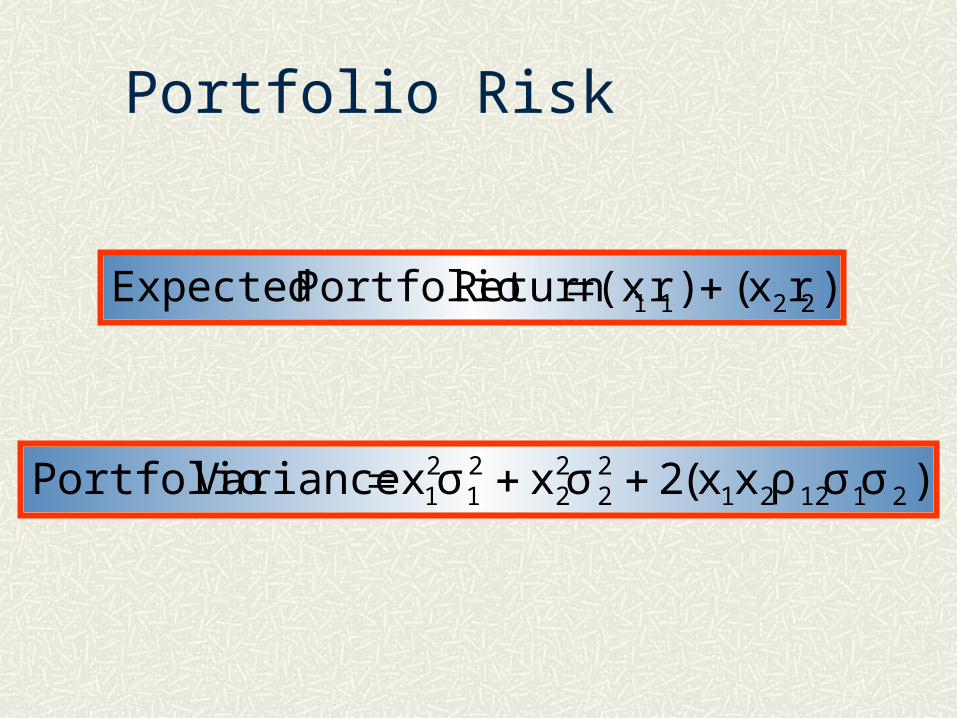

Portfolio Risk

)rx()r(x Return PortfolioExpected 2211

)σσρxx(2σxσxVariance Portfolio 21122122

22

21

21

Efficient FrontierExample Correlation Coefficient = .4

Stocks % of Portfolio Avg Return

ABC Corp 28 60% 15%

Big Corp 42 40% 21%

Standard Deviation = Portfolio = 28.1

Return = weighted avg = Portfolio = 17.4%

Let’s Add stock New Corp to the portfolio

Efficient FrontierExample Correlation Coefficient = .3

Stocks % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New CorpNew Corp3030 50%50% 19% 19%

NEW Standard Deviation = Portfolio = 23.43

NEW Return = weighted avg = Portfolio = 18.20%

Efficient FrontierExample Correlation Coefficient = .3

Stocks % of Portfolio Avg Return

Portfolio 28.1 50% 17.4%

New Corp 30 50% 19%

NEW Standard Deviation = Portfolio = 23.43

NEW Return = weighted avg = Portfolio = 18.20%

NOTE: Higher return & Lower risk

DIVERSIFICATION

Efficient Frontier

A

BN

Return

Risk

AB

Goal is to move up and left.

ABN

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

INTEGRATED MARKETS & DIVERSIFICATION BENEFITS C20A.WK1

F10 will graph the portfolio return-risk profile.

ASSUMPTION SET---------------- ---------------- ---------------- ----------------

Stock Return Risk Correlation---------------- ---------------- ---------------- ----------------

Boeing (US) 18.60% 22.80% 0.80Unilever (UK) 16.00% 24.00%

PORTFOLIO ANALYSIS---------------- ---------------- ---------------- ----------------

Weight of Weight of Expected ExpectedBoeing in Unilever in Return RiskPortfolio Portfolio (percent) (percent)

---------------- ---------------- ---------------- ----------------1.00 0.00 18.60% 22.80%0.95 0.05 18.47% 22.63%0.90 0.10 18.34% 22.49%0.85 0.15 18.21% 22.36%0.80 0.20 18.08% 22.27%0.75 0.25 17.95% 22.19%0.70 0.30 17.82% 22.15%0.65 0.35 17.69% 22.12%0.60 0.40 17.56% 22.12%0.55 0.45 17.43% 22.15%0.50 0.50 17.30% 22.20%0.45 0.55 17.17% 22.28%0.40 0.60 17.04% 22.38%0.35 0.65 16.91% 22.50%0.30 0.70 16.78% 22.65%0.20 0.80 16.52% 23.01%0.25 0.75 16.65% 22.82%0.20 0.80 16.52% 23.01%0.15 0.85 16.39% 23.23%0.10 0.90 16.26% 23.46%0.05 0.95 16.13% 23.72%0.00 1.00 16.00% 24.00%

---------------- ---------------- ---------------- ----------------

Benefits of Portfolio Diversification(two asset portfolio)

15.0

15.5

16.0

16.5

17.0

17.5

18.0

18.5

19.0

19.5

20.0

15.0 16.0 17.0 18.0 19.0 20.0 21.0 22.0 23.0 24.0 25.0

Risk (standard deviation, %)

Ret

urn

(%)

Measuring Risk

05 10 15

Number of Securities

Po

rtfo

lio

sta

nd

ard

dev

iati

on

Measuring Risk

05 10 15

Number of Securities

Po

rtfo

lio

sta

nd

ard

dev

iati

on

Market risk

Uniquerisk

Measuring Risk

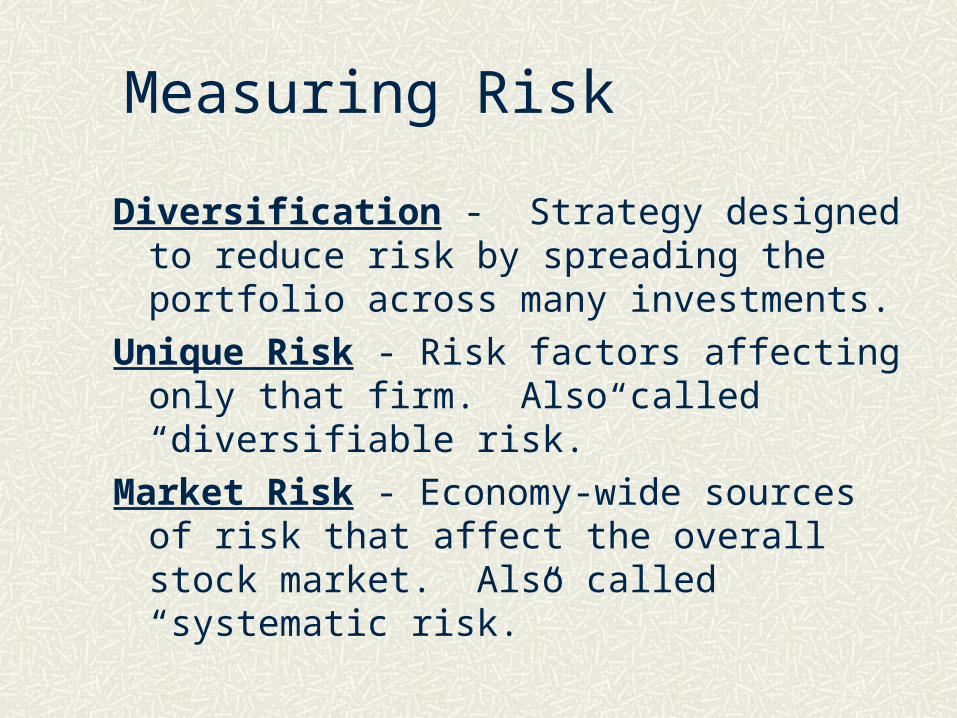

Diversification - Strategy designed to reduce risk by spreading the portfolio across many investments.

Unique Risk - Risk factors affecting only that firm. Also called “diversifiable risk.”

Market Risk - Economy-wide sources of risk that affect the overall stock market. Also called “systematic risk.”

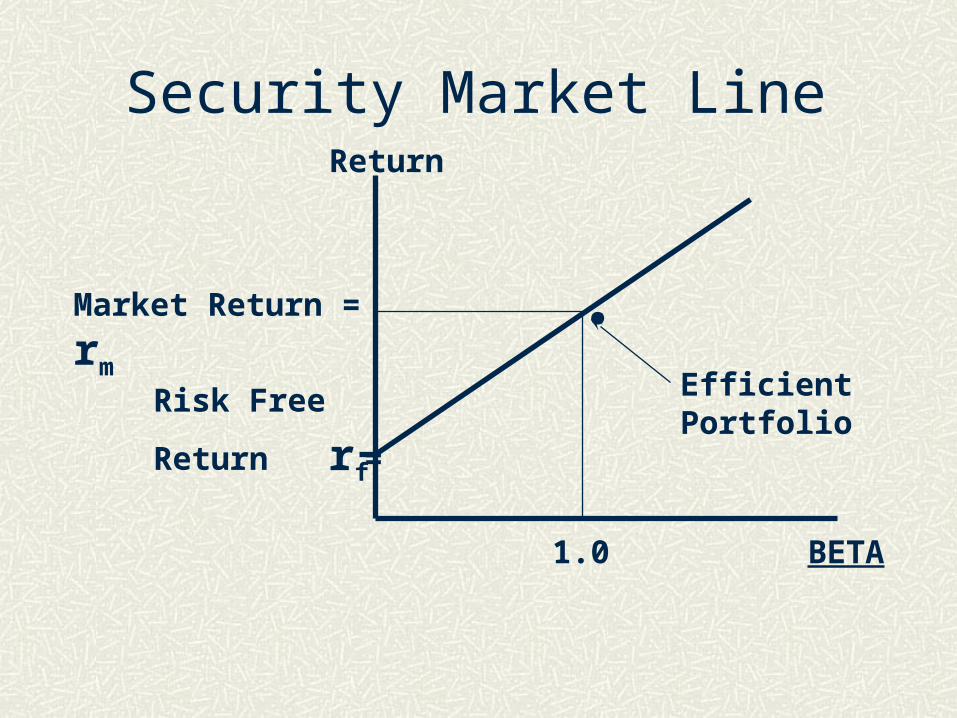

Security Market LineReturn

Risk

.

rf

Risk Free

Return =

Efficient Portfolio

Market Return = rm

0%

5%

10%

15%

20%

25%

30%

35%

40%

0% 10% 20% 30% 40% 50% 60%

Standard Deviation

Exp

ecte

d R

etu

rn

Stocks

Tangency Portfolio

Minimum Variance Frontier

Efficient Frontier (with rf)

Security Market LineReturn

.

rf

Risk Free

Return =

Efficient Portfolio

Market Return = rm

BETA1.0

Beta and Unique RiskMarket Portfolio - Portfolio of all assets in the economy. In practice a broad stock market index, such as the S&P Composite, is used to represent the market.

Beta - Sensitivity of a stock’s return to the return on the market portfolio.

Measuring Betas

The SML shows the relationship between return and risk.

CAPM uses Beta as a proxy for risk.

Beta is the slope of the SML, using CAPM terminology.

Other methods can be employed to determine the slope of the SML and thus Beta.

Regression analysis can be used to find Beta.

Beta and Unique Risk

beta

Expected

return

Expectedmarketreturn

10%10%- +

-10%+10%

stock

-10%

1. Total risk = diversifiable risk + market risk2. Market risk is measured by beta, the sensitivity to market changes

Beta and Unique Risk

2m

imiB

Covariance with the market

Variance of the market

Measuring Betas

Hewlett Packard Beta

Slope determined from 60 months of prices and plotting the line of best fit.

Price data - Jan 78 - Dec 82

Market return (%)

Hew

lett-Packard return (%

)

R2 = .53

B = 1.35

Measuring Betas

Hewlett Packard Beta

Slope determined from 60 months of prices and plotting the line of best fit.

Price data - Jan 83 - Dec 87

Market return (%)

Hew

lett-Packard return (%

)

R2 = .49

B = 1.33

Measuring Betas

Hewlett Packard Beta

Slope determined from 60 months of prices and plotting the line of best fit.

Price data - Jan 88 - Dec 92

Market return (%)

Hew

lett-Packard return (%

)

R2 = .45

B = 1.70

Measuring Betas

Hewlett Packard Beta

Slope determined from 60 months of prices and plotting the line of best fit.

Price data - Jan 93 - Dec 97

Market return (%)

Hew

lett-Packard return (%

)

R2 = .35

B = 1.69

Security Market LineReturn

BETA

rf

1.0

SML

SML Equation = rf + B ( rm - rf )

Capital Asset Pricing Model

R = rf + B ( rm - rf )

CAPM

Beta Stability % IN SAME % WITHIN ONE RISK CLASS 5 CLASS 5 CLASS YEARS LATER YEARS LATER

10 (High betas) 35 69

9 18 54

8 16 45

7 13 41

6 14 39

5 14 42

4 13 40

3 16 45

2 21 61

1 (Low betas) 40 62

Source: Sharpe and Cooper (1972)