corporate finance - m&a yanzhi wang. loughran and vijh (1997) using 947 acquisitions during...

TRANSCRIPT

Corporate Finance -M&A

Yanzhi Wang

Loughran and Vijh (1997) Using 947 acquisitions during 1970-1989, this article

finds a relationship between the post-acquisition returns and the mode of acquisition and form of payment.

During a five-year period following the acquisition, on average, firms that complete stock mergers earn significantly negative excess returns of -25.0 percent whereas firms that complete cash tender offers earn significantly positive excess returns of 61.7 percent.

Over the combined pre-acquisition and post-acquisition period, target shareholders who hold on to the acquirer stock received as payment in stock mergers do not earn significantly positive excess returns. In the top quartile of target to acquirer size ratio, they earn negative excess returns.

M&A and wealth gainMany researchers have addressed the

question of wealth gains from acquisitions. They typically find three patterns: ◦ Target shareholders earn significantly positive

abnormal returns from all acquisitions.◦ Acquiring shareholders earn little or no

abnormal returns from tender offers.◦ Acquiring shareholders earn negative abnormal

returns from mergers.This paper classifies a sample based on the

mode of acquisition (merger or tender offer) and the form of payment (stock or cash).

Mode of acquisition Mergers are usually friendly deals that enjoy the

cooperation of incumbent managers.◦ An acquisition is classified as a merger if some of the

following characteristics were present: the tone was friendly, the target’s managers were favorable, the board of directors and the shareholders voted and approved the deal.

Tender offers are made directly to target shareholders, often to overcome resistance from incumbent managers, and indicate greater confidence in the acquirer’s ability to realize efficiency gains from the acquisition.◦ An acquisition is classified as a tender offer if some of the

following characteristics were present the tone was aggressive, there was no shareholder meeting or approval, the word tender was used, a percentage of shares sought was mentioned (unlike mergers, tender offers may not be all or none type of deals).

Sometimes characteristics of both merger and tender offers are present.

Form of paymentFirms will issue stock only when it is

overvalued. It follows that firms will prefer to pay cash if their stock is undervalued.

Some firms adopt a mixed payment form.

DataTo identify the sample of acquisitions, we

search the CRSP tapes for all NYSE, AMEX, and Nasdaq firms delisted during 1970-1989. CRSP identifies firms delisted by reason of acquisition with a delisting code between 200 and 203 and a last dividend payment code starting with 32, 37, or 38. The delisting date is the effective date of acquisition.

They search the Wall Street Journal Index to identify whether an acquisition was a merger or a tender offer.

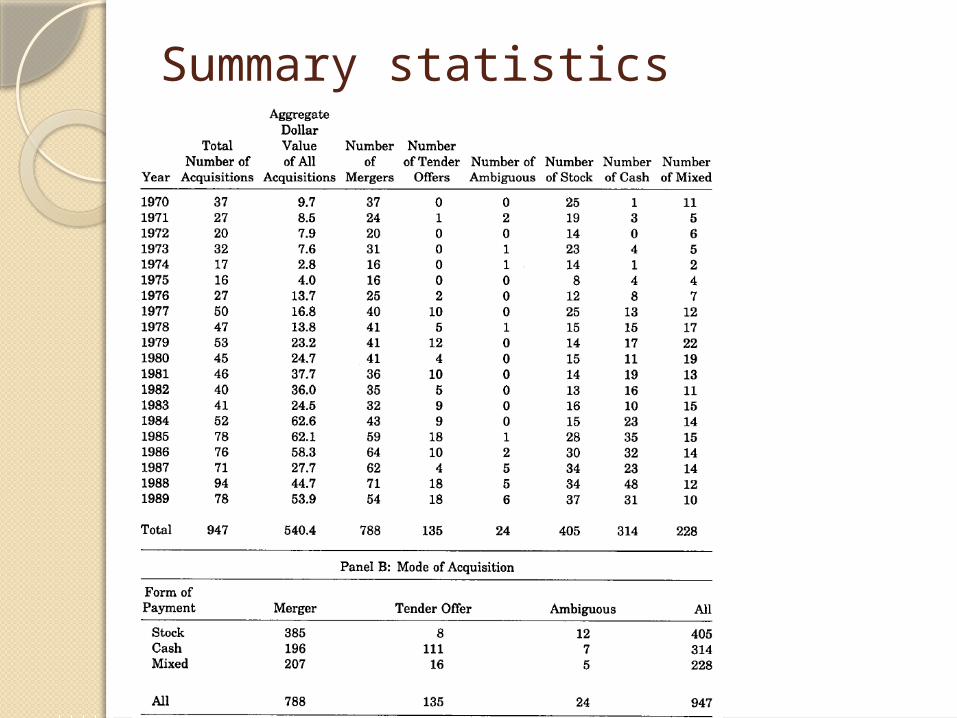

Summary statistics

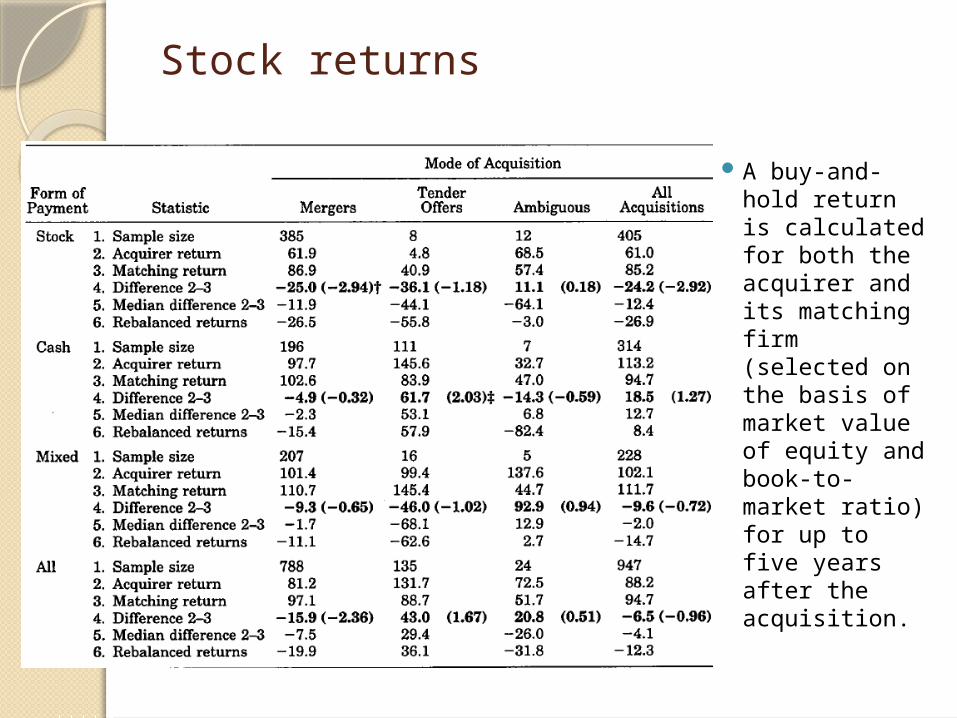

Stock returns

A buy-and-hold return is calculated for both the acquirer and its matching firm (selected on the basis of market value of equity and book-to-market ratio) for up to five years after the acquisition.

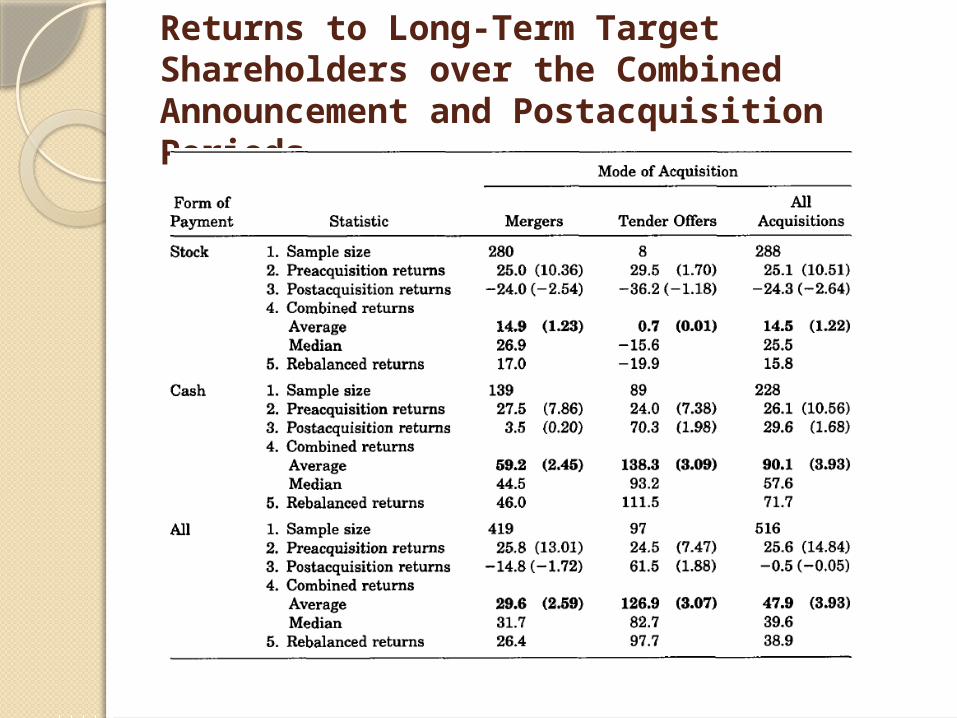

Returns to Long-Term Target Shareholders over the Combined Announcement and Postacquisition Periods

Dong, Hirshleifer, Richardson, and Teoh (2006) A summary:This paper uses pre-offer market valuations

to evaluate the misvaluation and Q theories of takeovers.

Both Q hypothesis and misvaluation hypothesis are supported while the evidence for the mispricing hypothesis is stronger in the 1990-2000 period than in the pre-1990 period.

Misvaluation hypothesis It implies the market inefficiency has

important effects on the takeover activity.Bidders can profit by buying undervalued

targets for cash at a price below fundamental value

Bidders can profit by buying equity for targets, even those overvalued targets, if bidders are more overvalued than the target.

The misvaluation hypothesis also implies that bidders will tend to be overvalued relative to targets.

Q hypothesisQ hypothesis focuses on how acquisitions

reallocate target assets. High market value is an indicator that a firm is well run or has god business opportunities.

Takeovers may be designed to eliminate wasteful target behavior or take advantage of better bidder investment opportunities.

Alternative, takeovers may be used by the managers of inefficient bidders to expand their domains of control.

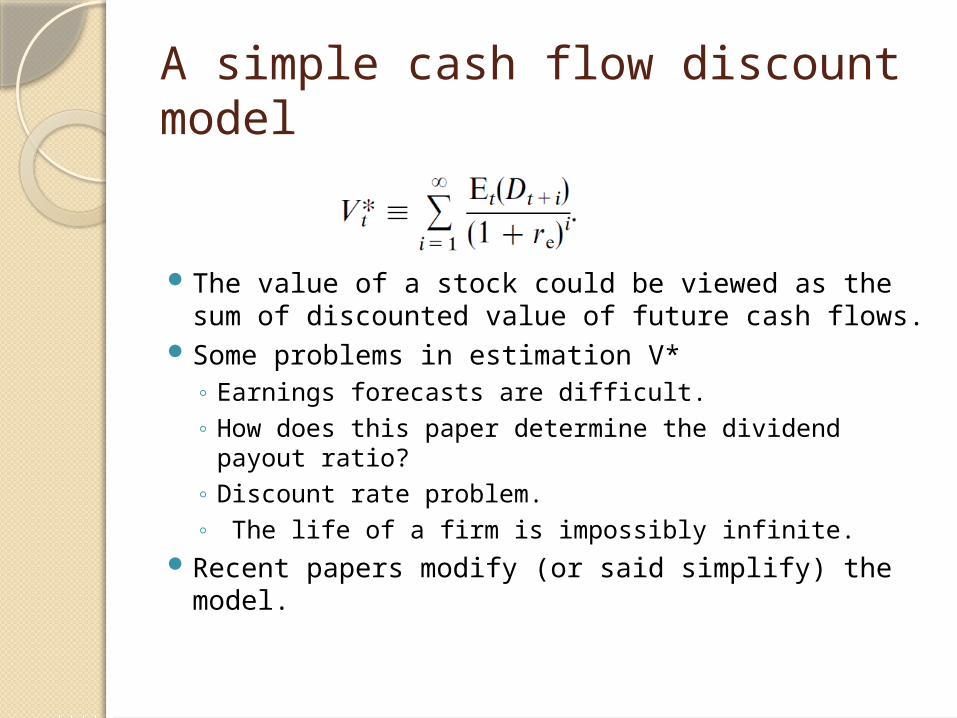

A simple cash flow discount model

The value of a stock could be viewed as the sum of discounted value of future cash flows.

Some problems in estimation V*◦ Earnings forecasts are difficult.◦ How does this paper determine the dividend

payout ratio?◦ Discount rate problem.◦ The life of a firm is impossibly infinite.

Recent papers modify (or said simplify) the model.

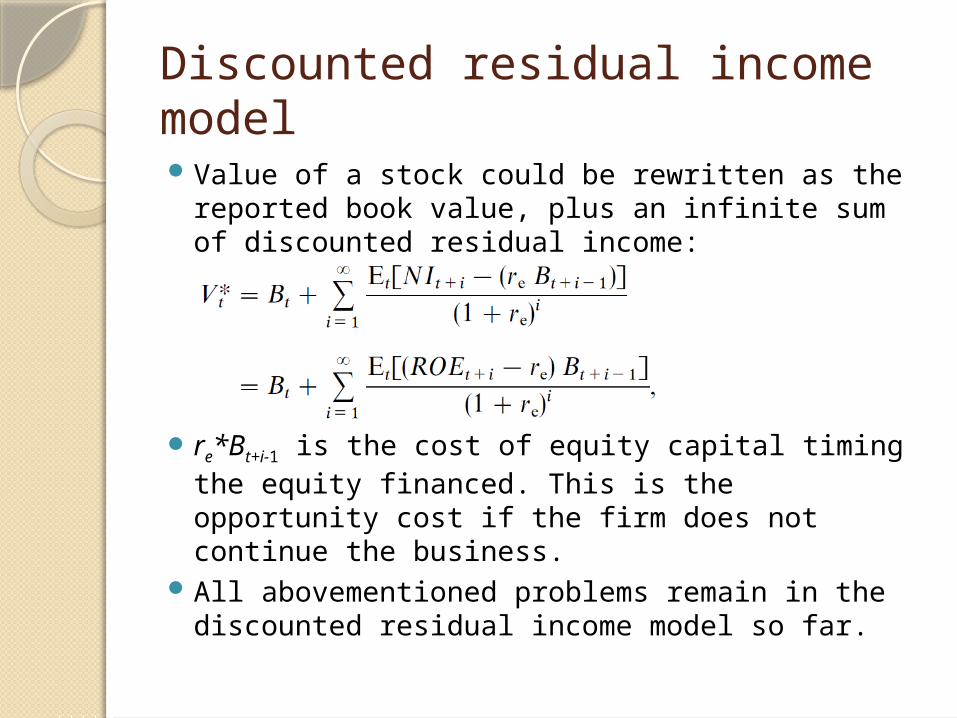

Discounted residual income modelValue of a stock could be rewritten as the

reported book value, plus an infinite sum of discounted residual income:

re*Bt+i-1 is the cost of equity capital timing the equity financed. This is the opportunity cost if the firm does not continue the business.

All abovementioned problems remain in the discounted residual income model so far.

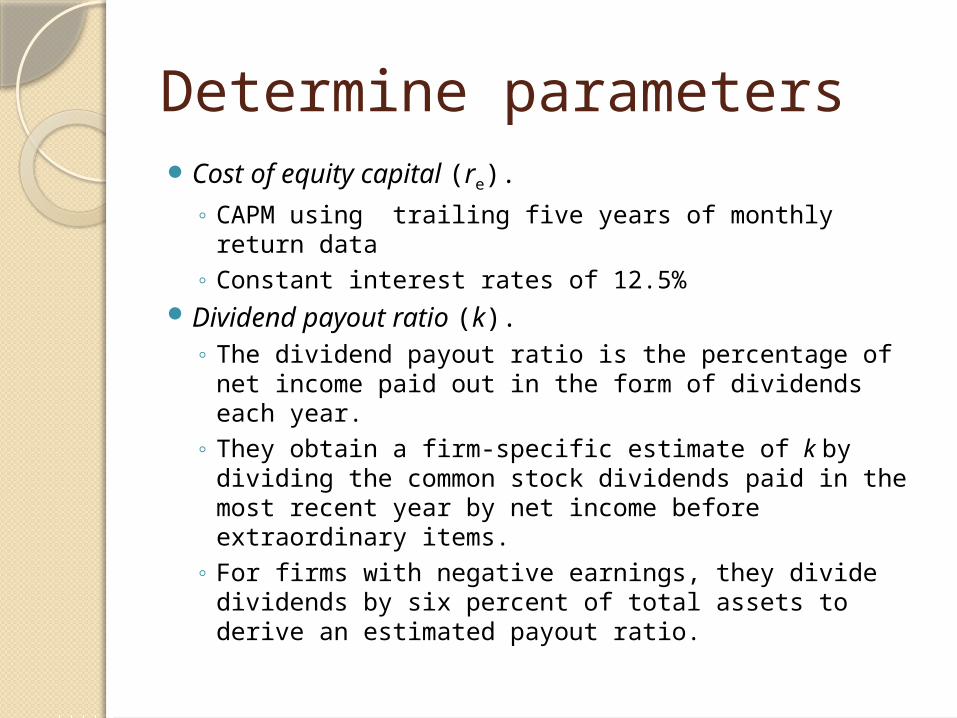

Determine parametersCost of equity capital (re).

◦ CAPM using trailing five years of monthly return data

◦ Constant interest rates of 12.5%Dividend payout ratio (k).

◦ The dividend payout ratio is the percentage of net income paid out in the form of dividends each year.

◦ They obtain a firm-specific estimate of k by dividing the common stock dividends paid in the most recent year by net income before extraordinary items.

◦ For firms with negative earnings, they divide dividends by six percent of total assets to derive an estimated payout ratio.

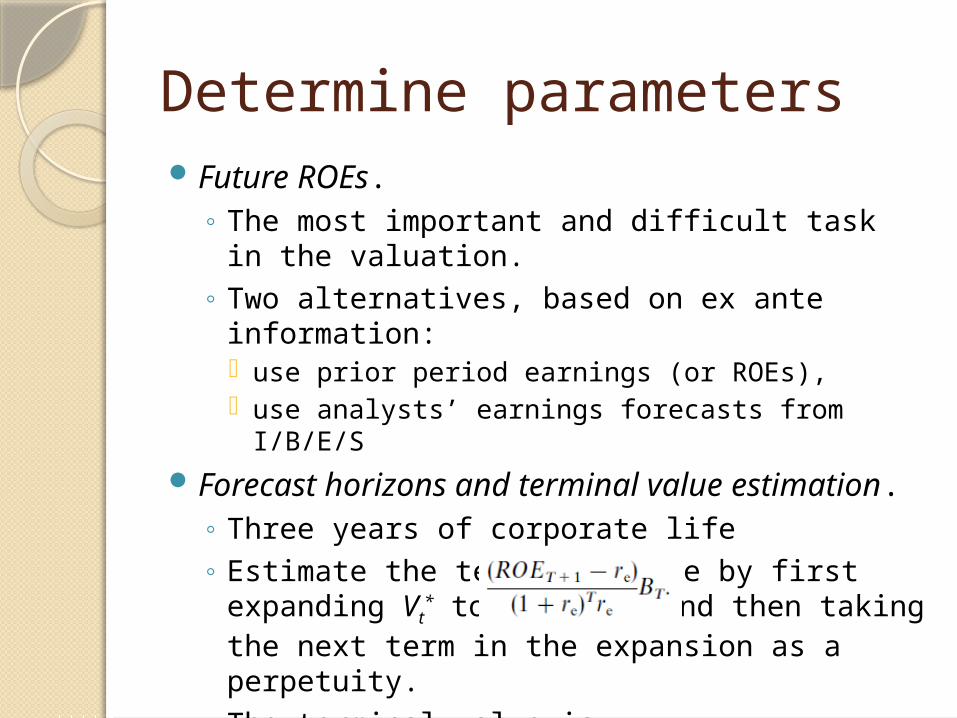

Determine parametersFuture ROEs.

◦ The most important and difficult task in the valuation.

◦ Two alternatives, based on ex ante information: use prior period earnings (or ROEs), use analysts’ earnings forecasts from I/B/E/S

Forecast horizons and terminal value estimation.◦ Three years of corporate life◦ Estimate the terminal value by first expanding

Vt* to 3 terms, and then taking the next term in

the expansion as a perpetuity.◦ The terminal value is

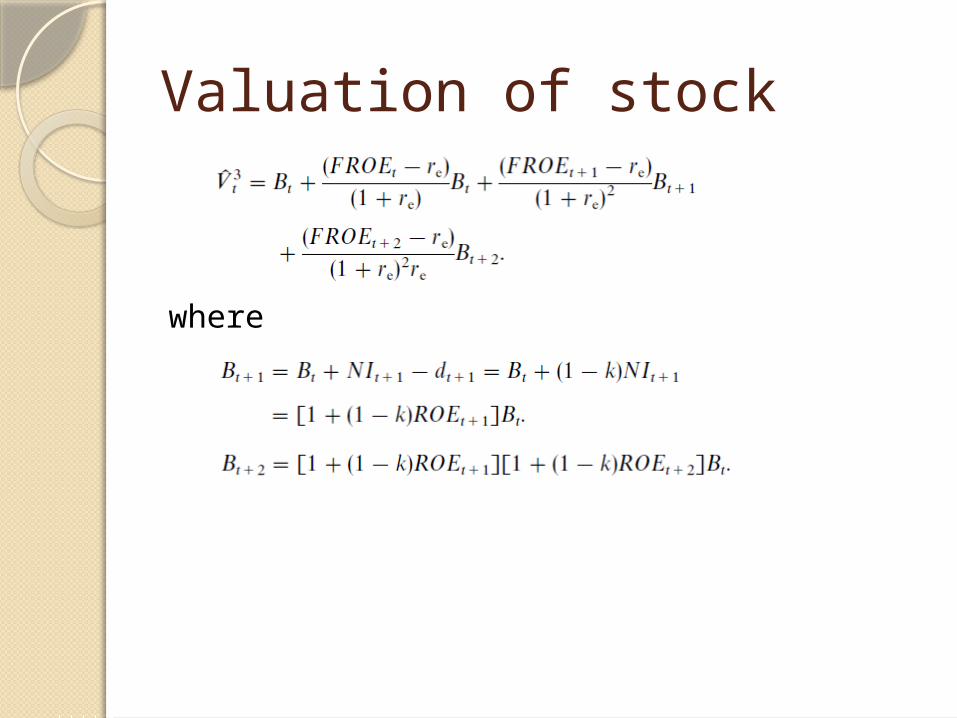

Valuation of stock

where

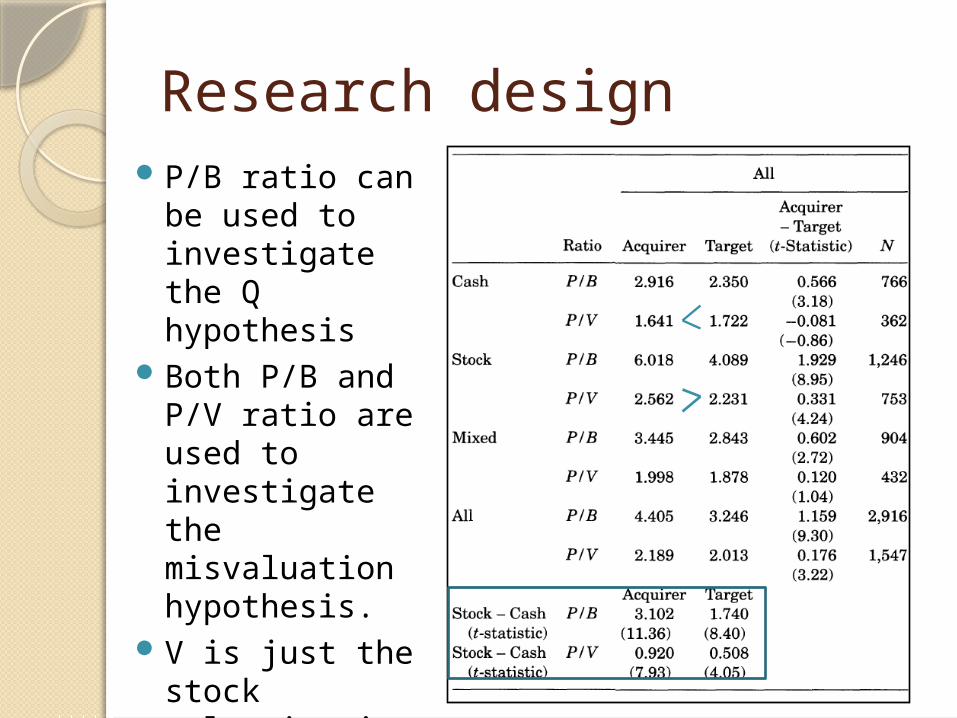

Research designP/B ratio can

be used to investigate the Q hypothesis

Both P/B and P/V ratio are used to investigate the misvaluation hypothesis.

V is just the stock valuation in Frankel and Lee (1998).

Payment method and CARWhat do you see from the table?

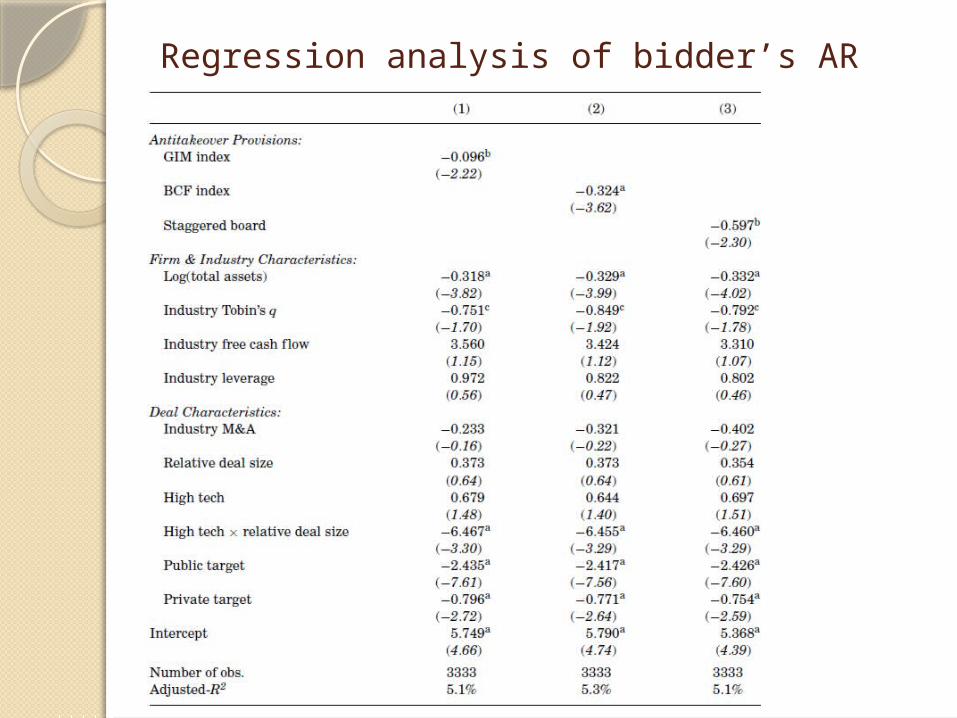

Masulis, Wang and Xie (2007)This paper examines whether corporate governance

mechanisms affect the profitability of firm acquisitions. Acquirers with more antitakeover provisions experience significantly lower announcement-period abnormal stock returns. This supports the hypothesis that managers at firms protected by more antitakeover provisions are less subject to the disciplinary power of the market for corporate control and thus are more likely to indulge in empire-building acquisitions that destroy shareholder value.

They also find that acquirers operating in more competitive industries or separating the positions of CEO and chairman of the board experience higher abnormal announcement returns.

Corporate control and ATPA series of recent studies by Gompers, Ishii,

and Metrick (GIM, 2003), Bebchuk, Cohen, and Ferrell (BCF, 2004), Bebchuk and Cohen (2005), and Cremers and Nair (2005) examine one important dimension of corporate governance, namely, the market for corporate control.

They document negative relations between various indices of antitakeover provisions (ATPs) and both firm value and long-run stock return performance.

M&A and agency problem Acquisitions are among the largest and most readily

observable forms of corporate investment. These investments also tend to intensify the inherent conflicts of interest between managers and shareholders in large public corporations (Berle and Means (1933) and Jensen and Meckling (1976)).

Jensen’s (1986) free cash flow hypothesis argues that managers realize large personal gains from empire building and predicts that firms with abundant cash flows but few profitable investment opportunities are more likely to make value-destroying acquisitions than to return the excess cash flows to shareholders.

Empirical studies including Lang, Stulz, andWalkling (1991) and Morck, Shleifer, and Vishny (1990) confirm this argument.

M&A and agency problemCeteris paribus, the conflict of interest

between managers and shareholders is more severe at firms with more ATPs, or equivalently, firms less vulnerable to takeovers. This leads to the following ATP value destruction hypothesis: Managers protected by more ATPs are more likely to indulge in value-destroying acquisitions since they are less likely to be disciplined for taking such actions by the market for corporate control.

Data This paper extracts the acquisition sample from

the Securities Data Corporation’s (SDC) U.S. Mergers and Acquisitions database. They identify 3,333 acquisitions made by 1,268 firms between January 1, 1990 and December 31, 2003 that meet the following criteria:◦ The acquisition is completed.◦ The acquirer controls less than 50% of the target’s shares

prior to the announcement and owns 100% of the target’s shares after the transaction.

◦ The deal value disclosed in SDC is more than $1 million and is at least 1% of the acquirer’s market value of equity measured on the 11th trading day prior to the announcement date.

◦ The acquirer has annual financial statement information available from Compustat and stock return data (210 trading days prior to acquisition announcements) from the University of Chicago’s Center for Research in Security Prices (CRSP) Daily Stock Price and Returns file.

◦ The acquirer is included in the Investor Responsibility Research Center’s (IRRC) database of antitakeover provisions.

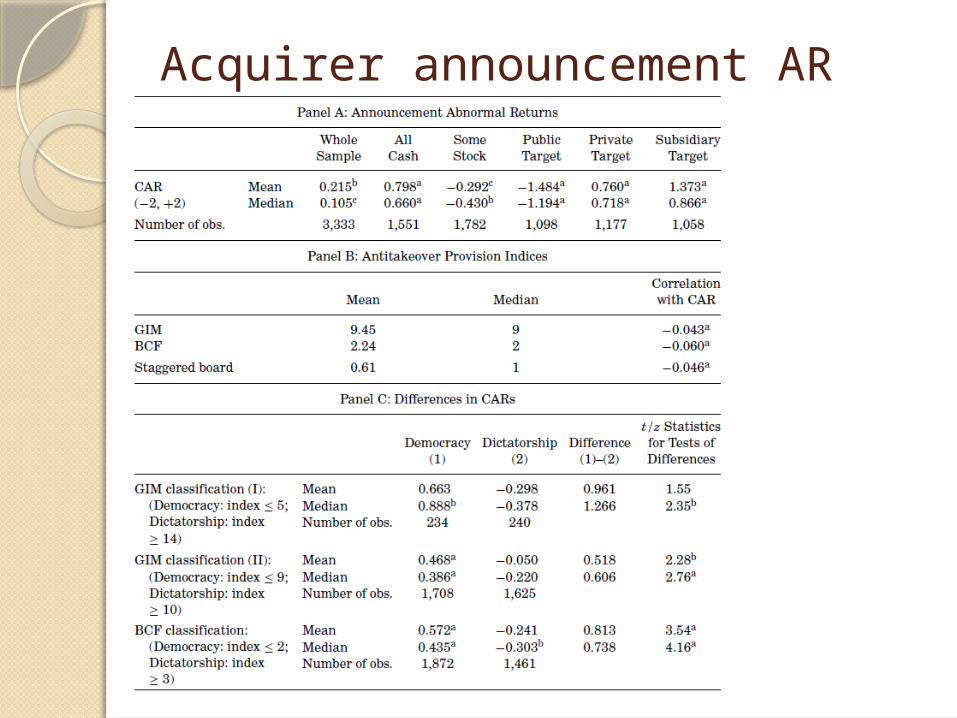

Acquirer announcement AR

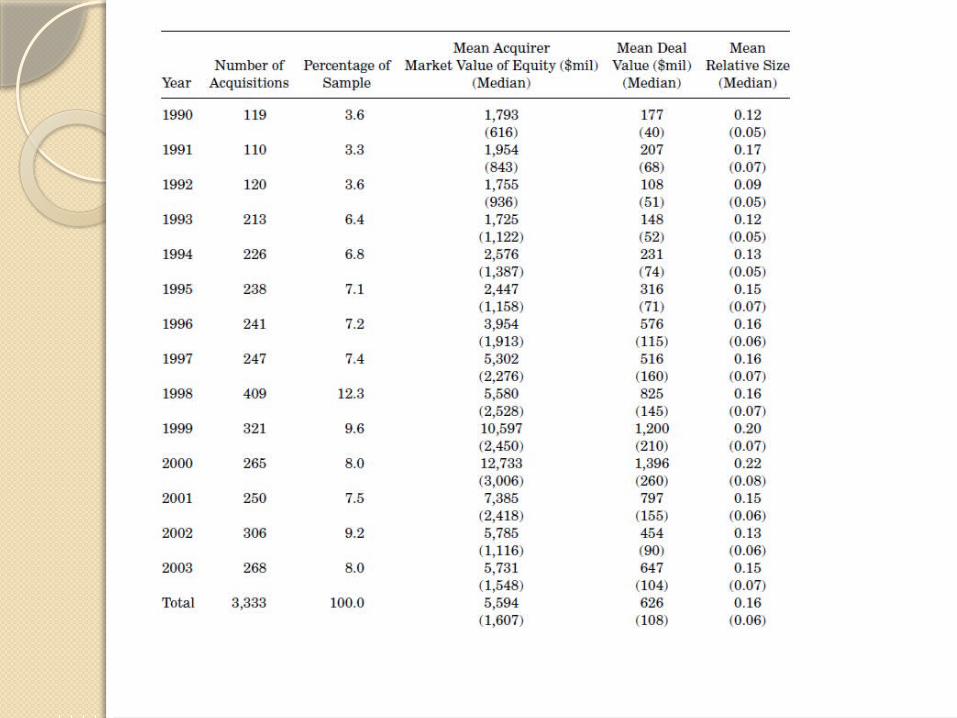

Summary statistics

Regression analysis of bidder’s AR

Other governance variablesSo far our results suggest that managers

who are more vulnerable to the market for corporate control make better acquisitions. However, previous tales have not controlled for other governance mechanisms that could mitigate the conflict of interest between managers and shareholders.

This omission is especially problematic given the possible interdependencies among various control mechanisms found in past studies.◦ Control for product market competition◦ Control for board characteristics

Regression analysis controlling for product market competition

Endogeneity- reverse causality

One form of the endogeneity problem is reverse causality, that is, managers planning to pursue empire building or make unprofitable acquisitions could first adopt ATPs to preclude being disciplined by the market for corporate control. To examine this possibility, they focus on a subsample of bidders that went public prior to 1990, after which institutional investors began to consistently vote against staggered boards and other takeover defenses (Bebchuk and Cohen (2005)).

Results are held under this subsample.

Endogeneity- omitted variableThe other form of the endogeneity problem is an

omitted variable bias. The concern is that some unobservable bidder

characteristics could be responsible for both the level of takeover protection in a firm and the profitability of its acquisitions. One factor that may have this property is management quality. It is conceivable that bad CEOs make poor acquisitions and adopt ATPs to entrench themselves.

Morck, Shleifer, and Vishny (1990) measure bidder CEO quality by industry-adjusted operating income growth over the 3 years prior to the acquisition announcement.

Controlling for management quality