corn & wheat take a beating; livestock futures slip late ... · june 5, 2010 • vol. 38, no....

TRANSCRIPT

June 5, 2010 • Vol. 38, No. 23

United We Stand

Corn & wheat take a beating; livestock futures slip late-week — Favorable weather, rising crop condition ratings and outside markets all combined to hit corn futures last week, producing a downside breakout below the April low. That and no additional corn sales reported to China gave market bears the upper hand. Wheat futures also took a beating, with new contract lows scored in both Chicago and Kansas City as HRW wheat harvest moved northward (see News page 2). With fundamentals bearish and spillover pressure from corn, wheat couldn’t catch a break. Soybeans, however, saw cash-market strength keep futures at least choppy for the week and above key support levels. For livestock, cattle futures found support early in the week on firmer cash bids and strong beef movement — expectations were meat-case clearance was good for the opening grilling weekend of the summer. But Friday saw gains evaporate as jobs data disappointed and outside markets turned negative. Similar influences kept a lid on lean hog futures along with weaker cash bids.

profarmer.comWhen you see the icon with the PF shield and the “link cursor,” go to

www.profarmer.comfor more on that story!

Antibiotics and ethanol.Anxiety with DDG users and ethanol pro-ducers is rising over a coming congressional look at antibiotics use in the livestock and dairy sector and the ethanol byproduct. FDA has been sampling DDGs to check for anti-biotic residues.

CSP signup extended.USDA published the final rule for the Conservation Stewardship Program last week and length-ened signup to June 25.

See you in Minnesota!We will hold a Profit Briefing Seminar, spon-sored by Pioneer, at Jackpot Junction near Redwood Falls June 29. Doors open at 8 a.m. and we'll get you on the road by 3 p.m. Options to sign up:Call 800-772-0023 orvisit www.profarmer.comto reserve your spot!

Are price trends for June set?How traders come out of a holiday like Memorial Day can set the tone for futures trade in coming weeks. Of course, there’s always wild cards that can affect how trade actually plays out. And there are plenty, including flare ups in Iran, Israel and North Korea; any potential terrorist activity (especially since some fret Al Qaeda could eye July 4 for a potential U.S. strike); the Gulf oil spill could worsen and affect shipping; and the ongoing debt struggles in Europe. Bottom line: Any of these potential wild cards could be price-negative for grains. Canada planting challenges remainWhile U.S. spring planting has progressed with minimal hitches, Canada hasn’t been as lucky. Indications are up to 1 million acres could be unplanted in Saskatchewan due to rain (crop insurance deadlines have been extended there) and there is some concern for canola in Manitoba. And U.S. govern-ment weather forecasts for June have above- normal precip and below-normal temps for areas of the U.S. Northern Plains, and those conditions won’t stop at the border. See News page 2 for more on weather.

Export sales slow for corn, wheat & beansMarketing-year low corn sales, and below-expectation sales tallies for wheat and soy-beans gave weekly export sales data from USDA for the week ended May 27 a bearish read to close out the week.

China failed to show up as a buyer of corn (and was listed for just 100 metric tons of soy-bean business!!) but they were the lead buyer for cotton, helping to push sales above trade expec-tations. Now there are reports out of China that their hefty bean import pace has jammed ports and left boats waiting to unload. This could explain their absence as a soybean buyer.

Markets eye shifts in June S&D dataWe'll get USDA’s second look at 2010-11 pro-jections June 10, and there's been a lot of speculation on whether it will adjust the corn yield projection. Some say the non-survey-based yield peg could be hiked, but history says they won’t. Most doubt conditions war-rant any shift. So the focus will be on what happens within balance sheets.

Informa sees uptick in winter wheat Closely followed Informa Economics reportedly expects USDA will raise the 2010 U.S. winter wheat crop estimate 23 million bu. in the June 10 Crop Production Report to 1.481 billion bushels. Contacts advise the firm sees the uptick coming in HRW. Trade expectations will help dictate market action this week ahead of the data.

Farmers have aggressive land viewsRabobank released a survey reporting farm-ers say they’re getting back in the land acqui-sition game — either buying or renting. LandOwner Editor Mike Walsten says that’s a sign the land market has found its footing. Data indicate good-quality ground is still moving, but he thinks lower-quality ground will eventually see a boost in sales.

Private sector job growth slow in MayWhile non-farm payrolls rose 431,000 in May — the highest monthly growth since March 2000 — only 41,000 private-sector jobs were added. Hiring of temporary Census workers wasn’t enough to push new jobs past expecta-tions of 500,000 or more new jobs. As for the decline in the unemployment rate to 9.7% (from 9.9% in April), Vince Malanga of LaSalle Economics said, “The only reason the jobless rate fell was because of a decline in the labor force.” He says the Fed still needs to stay “friendly” in the current environment.

News this week...Page 2: La Niña in position to hit June-August.Page 3: Euro and dollar still market factors.Page 4: Schedule full in DC for rest of 2010.

June 5, 2010 / News page 2

Be sure to download your Pro Farmer

newsletter atwww.profarmer.com!More and more PF

Members arediscovering the

ease of accessing their newsletter each week from

the “Subscription Services” area at

www.profarmer.com! To get your PF by

12:45 CT each Friday afternoon,

just register on your Membership

site — access is included in your

Membership fees.

Sherman (NE), Texas:“Wheat is coming

along nicely. Earliest planted

wheat should be ready in just a few

more days. Finishing up get-

ting the combines/trucks/grain carts

serviced and ready to hit the field. Approximately

1,500 acres planted this year.

Expecting a pretty good wheat crop

this year. Probably will not be a record

breaker, but will definitely be better

than last year.”

Vernon (NC), Texas:“We have had a wet, cool spring which has been

good for the wheat, but bad for diseas-

es. Wheat looks pretty good. I am a little worried about

the rust, but it came so late we

didn’t think we could justify a fun-gicide application.

Wheat was already flowering when it

showed up. I think yields will be aver-age — between 40 to 50 bu. per acre

unless the rust dings it pretty bad. Harvest should be the first couple of

weeks of June.”

NWS shifts June forecastThe National Weather Service shuttled above-normal temps in for Plains HRW wheat areas in their May 31 update to their June forecast, and moved odds for above-normal precip mostly into the heart of the Corn Belt. Also, the PNW and areas of the Northern Plains are now forecast to see above-normal rains and below normal temps — not the best conditions for spring wheat to get toward the finish line.

NWS Temp OutlookJune 9-13

NWS Precip OutlookJune 9-13

The darker the brown, the higher the odds of above-normal temps. The darker the blue, the higher the odds of below-normal temps.

The darker the brown, the higher the odds of below-normal precipitation. The darker the green, the higher the odds of above-normal precip.

Gov’t: ‘Favorable conditions’ for La Niña by June-AugustWarmer-than-normal sea surface temps (SSTs) in the equatorial Pacific have disappeared and gov-ernment weather forecasters have issued a “La Niña watch” — issued when conditions are favorable for the development of La Niña within the next three months.

In their latest update, the Climate Prediction Center (CPC) says models now “indicate the onset of La Niña conditions dur-ing June-August 2010.” Given recent observations of cooling trends in Pacific SSTs and “atmo-spheric circulation,” CPC con-cludes, “conditions are favorable for a transition to La Niña condi-tions during June-August 2010.”

And this shift has some weather watchers noting corn yield con-cerns. Iowa State University’s Elwynn Taylor said La Niña arriv-ing in June would bring a “sub-stantial increase in corn yield risk for the U.S. (primarily the eastern and central Corn Belt), shifting the likelihood of a below-trend yield from about 50/50 to 70%.”

Bottom line: Timing and severity of the shift remain the keys to whether La Niña will have a negative impact on U.S. corn or soybean yields. But tim-ing is starting to look like there is another factor to watch rela-tive to the 2010 growing season in the Midwest.

Corn progress stays ahead of average; CCI risesA combination of warmer temps and precip has kept the U.S. corn crop running ahead of the average pace relative to emer-gence — 85% for the week ended May 30 compared to a five-year average of 80%.

Condition ratings also improved for the week, with 76% now rated “good” to “excellent” compared to 71% the previous week.

When those weekly crop rat-ings are plugged into our weight-ed Pro Farmer Crop Condition Index (CCI; 0 to 500 point scale), the corn crop improved 10 points to 386. While there are some replant areas due to too much moisture, our checks with pro-ducers in frost-affected areas indicate the crop has come through the early May cold snap in mostly decent shape.

“There are some places where fields were nipped, but the high plant populations we’re plant-ing now mean there’s still enough left in most places to provide potential for optimum yields,” says a south-central Minnesota agronomist.

Soybeans closer to ‘average’While corn is running typically ahead of the five-year average, soybeans reflect the varied weather conditions that have been seen since planting focus shifted from corn. Still, growers had 74% of the crop planted as of May 30, just behind the 75% five-year average.

Emergence shot ahead with 46% out of the ground — a 22-percentage point jump — compared to a 44% average. Several states have emergence running double-digits ahead of their average pace.

We’ll get the first soybean con-dition ratings of the growing season June 7. But there won’t be a year-ago comparison — the first soybean condition rating wasn’t done until the week ended June 14, 2009.

Winter wheat harvest works into OklahomaOverall U.S. winter wheat harvest is running 10 points behind the average pace, with sluggish development the main culprit keep-ing combines rolling at a slower-than-normal pace.

Harvest moved into southwest Oklahoma last week, still behind in part due to cool temps that have dominated the region. But warmer readings last week also helped to push harvest ahead.

As combines roll, the focus is on quality, especially after protein levels were off in 2009. So far, officials with the Fort Worth Grain Exchange say protein levels have been around 11.3% to 11.5% on newly harvested supplies. While yields have been coming in around 30 bu. to 50 bu. per acre in Oklahoma, contacts say late-emerged fields in north-central Texas and far southwest Oklahoma are 20 to 30 bu. per acre below fields that emerged in mid-October.

As for Kansas, the crop remains behind (USDA said 0% was har-vested compared to an average of 11% and 2% in 2009) but could get a boost with warm temps. Some warn, though, hot temps could pose issues for the behind crop. “There is still a ways to go with this crop,” according to Kansas State University agronomist Jim Shroyer.

June 5, 2010 / News page 3

Shelby Co.,(WC) Iowa:“Rain! The first good rain over 0.25 inch in 30 days — 1.25 inch-es. Both corn and soybeans are looking good.”

East central Illinois:“Still raining (6/2) and more rain in the forecast. There are still fields unplanted and we are beginning to see more and more ponding in the fields.”

Adams Co., (NE) Indiana:“Two-and-one-half inches of rain yes-terday (6/1). Just fin-ished replanting beans which were drowned out from earlier rains. Many fields of corn replanted and under water again. What started out as a good spring in April has sure changed.”

Williams Co., (NW) Ohio:“Started back up on Thursday, May 27, with corn and beans still abouttwo days away from ready. Then rain on Monday morning (5/31) — 0.8 to 0.9 inch in about 20 minutes. Still raining (6/1). About 20% of corn to plant and 60% of beans in the area yet to be planted.”

Montana:“I think most of Montana picked up some pretty good precipitation this Memorial Day week. The crops in general look good, but late. Our early seeded spring wheat looks as far along as the win-ter wheat. I would estimate the win-ter wheat in our area to be a good 10 days behind normal maturity.”

Outside Market AnalysisU.S. Dollar Index: The focus on the woes in Europe were temporarily dis-placed by the resignation of Japan’s prime minister, bolstering the euro and the dollar. But the dollar remains well below long-term highs. Export flows are the main factor which are affected by the dollar, and there are concerns U.S. economic performance could be hindered if foreign demand is shut off. And there are further worries about Europe in the wake of recent economic news as euro-zone retail sales data remain weak. By contrast, the dollar has been buoyed by euro pessimism but also improving economic data here. That could keep the dollar climbing with some key resistance tests ahead.

Monthly Dollar IndexTrend is sideways.

Currency moves continue to impact export expectationsJust days after USDA raised its forecast for the value of U.S. ag exports in fiscal year (FY) 2010, the U.S. dollar continued to rise and continued to increase the level of potential pessimism about U.S. export competition.

Europe’s woes have been well documented, but the hammering the euro has taken puts them in potentially good shape to capital-ize on export demand.

As June started, one euro bought approximately $1.23; a month before, the euro bought $1.32 and six months ago, the euro commanded $1.50. The potential double whammy: Some European Union (EU) countries have lost 18% of their purchas-ing power in just six months.

While 9% of U.S. ag exports go to the 27 EU countries, for some products it’s a sizable per-centage. For example: 45% of tree nuts, 43% of tobacco and 39% of wine. Also, 9% of U.S. soybeans go to the EU, primari-ly headed to Germany, Spain and the Netherlands.

Bottom line: Even though the dollar has shown strength, it is still far below levels of recent years. But further appreciation in the greenback, especially if Europe’s woes worsen, could raise still more questions about the global economic recovery.

China updates 2009 corn crop; corn auctions stay activeChina’s National Bureau of Statistics put the 2009 Chinese corn crop at 163.97 million metric tons (MMT), down 1.16% from 2008, but well above USDA’s 155 MMT estimate and most private estimates.

Their stats bureau also says the 2010 Chinese winter wheat crop should be just above year-ago, although no specific figure was men-tioned by the Xinhua News Agency. USDA’s first peg of China’s 2010-11 wheat crop was 112.0 MMT. In 2009, Chinese data puts the crop at 115.21 MMT versus 114.5 MMT from USDA.

China corn auction activity remains heavyChina sold 1.369 MMT out of 1.549 MMT of corn that was auc-

tioned last week at slightly lower prices. Given strong demand for corn, especially in northeast provinces, the Chinese government will continue to auction state-owned reserves although the auctions aren’t driving domestic prices lower. That continues to support thoughts of additional purchases of U.S. corn. The first ship with U.S. corn left for China last week while the second should follow shortly.

Beef export developmentsHere’s a quick update on recent meat-trade developments:

Japan: With the country’s prime minister resigning and the government struggling to gain control of the foot-and-mouth disease (FMD) situation, addi-tional talks with the U.S. on beef trade are on hold.

Brazil: Brazilian officials will come to the U.S. as they are seek-ing additional clarification from the U.S. on testing procedures which found higher-than-accepted levels of Ivermectin in processed meat. Reports say the Brazilian meat industry is questioning whether the test used by the U.S. was okayed for processed meats.

Since March 2009, the dollar is still down 9%. Compared

to the average over the 1997-2003 period, the

greenback remains around 21% below that area.

While off the lows from the depths of the economic recession, the dollar still remains below resistance at 92.630 — the 2005 high.

China, Argentina still talking on soyoil situationBeijing-based talks last week between Argentine and Chinese officials over Chinese soyoil standards didn’t make much progress. While more talks are on tap, no dates have been set for the next sessions.

“This is a long negotiation pro-cess,” said chief Argentine nego-tiator and International Economic Relations Secretary Alfredo Chiaradía. “We were not expect-ing definitive decisions at the bilateral meeting.”

Estimates are if Argentina remains shut out of the Chinese soyoil market, it could cost the Argentine government $600 mil-lion in lost export duties.

92.63092.630

June 5, 2010 / News page 4

News alert and analysis exclusively for Members of Professional Farmers of America® P.O. Box 36, Cedar Falls, Iowa 50613-9985Sr. Vice President, Chuck Roth • Publisher/Editor, Chip Flory • Editor Emeritus, Jerry Carlson • News Editor, Roger Bernard

• Sr. Market Analyst, Brian Grete • Sr. Markets Editor, Julianne Johnston Member Relations Manager, Shelley Eilderts • Washington Consultant, Jim Wiesemeyer, Informa Economics

Subscription Services: 1-800-772-0023 • Editorial: 319-277-1278 • To record your news alert for PF editors: 1-800-PFA-NEWS (1-800-732-6397)©2010 Professional Farmers of America, Inc. • E-mail address: [email protected]

CEO, Andrew Weber • President, Jeff Pence

Agenda heating up as summer arrives in DCby News Editor Roger Bernard and Washington consultant Jim Wiesemeyer

Temperatures — and potentially tempers — will rise as Washington starts the summer work period leading

up to the August recess. Plenty of important issues are on the decision docket that can have an impact on how action in Washington plays out this summer and the balance of this election year.

Senate Democratic runoff in Arkansas Tuesday will tell whether Senate Ag Committee

Chair Blanche Lincoln (D-Ark.) will still be on the cam-paign in November. June 8 brings the runoff election in Arkansas against Lt. Gov. Bill Halter for the Democratic nod for Lincoln's Senate seat. If she loses, she doesn't lose her ag panel chair but becomes a lame duck.

Already an impact? Some believe the recent announce-ment by Lincoln that her panel will start hearings on the new farm bill June 30 was potentially an effort to under-score how important the ag panel is for Arkansas.

Tax extenders planAfter the House managed to approve the tax extend-

ers package before exiting Washington for the Memorial Day break, attention turns to the Senate this week. There, the future for the bill will not result in an imme-diate decision. Lawmakers in the Senate will bristle more than Blue-Dog Democrats did on the extra add-to-the-deficit spending in the bill.

What will happen? The bill will play out over poten-tially several weeks as Senate Majority Leader Harry Reid (D-Nev.) hasn’t committed to when that chamber will even consider the bill. Plus, he warns there are a lot of amendments in the wings. That means it could poten-tially be sent back through the House for another vote.

Bottom line: The final outcome is murky, but sup-port is there for the biodiesel tax credit to be restarted retroactive to Jan. 1, 2010.

Climate-change legislation pushPresident Obama last week renewed the push for

climate-change legislation, insisting the measure is not dead in the Senate. “The votes may not be there right now, but I intend to find them in the coming months,” he said. The Gulf oil spill is the catalyst behind this new push for climate legislation that has been written off in Washington as something that will have to wait for another day — or year.

And the president is getting help in this latest push. Within hours of Obama declaring he’d find the votes, Majority Leader Reid got involved, too. In a letter to key committee chairs, Reid said, “It is extremely impor-tant that you each examine what could be included in a comprehensive energy bill that would address the unfolding disaster in the Gulf of Mexico.” Who received the letter? Sens. Max Baucus (D-Mont.), Jeff Bingaman

(D-N.M.), Barbara Boxer (D-Calif.), Chris Dodd (D-Ct.), Patrick Leahy (D-Vt.), Joe Lieberman (ID-Ct.), Lincoln and Jay Rockefeller (D-W.V.).

What will happen? With Nov. 2 elections, another con-troversial measure will be too much to ask lawmakers from both parties up for re-election to confront. Instead, the Senate will initially vote on a resolution by Sen. Lisa Murkowski (R-Ak.) June 10 to significantly limit EPA’s role in regulating greenhouse gases. The vote outcome of that measure in the Senate will be the best litmus test for the near-term fate of the climate change bill.

EPA and E15EPA has been met in recent weeks with some who

have been seeking to sway the agency when it comes to the request to allow up to 15% ethanol in the nation’s fuel supply. As we noted via the interview with House Ag Committee Chairman Collin Peterson (D-Minn.), the decision time on this may have already slipped to late summer.

What will happen? A likely percentage boost could be limited to cars made in 2001 and later. Also, with court challenges to the Renewable Fuels Standard-2 rules already piling up, a decision to go to a 15% ethanol blend would see lawyers getting involved at some point, potentially reducing the positive impact of boosting the ethanol blend percentage.

Concentration workshop, round 3Dairy and cattle folks are next in line to tell their

stories to USDA and Dept. of Justice officials at the competition in ag workshops. Dairy is June 25 in Wisconsin and beef issues will get explored in a Colorado session in August. Then, results of the four sessions will be melded together for a post-election December wrap-up session in Washington, DC, where retailer price margins will also be under focus.

Impacts? These sessions won’t bring immediate changes from the Justice Dept. until after that final confab in December. And even then, it could take months before any plans emerge. There’s more near-term impact from soon-to-come concentration rules from USDA it was called on to develop as part of the 2008 Farm Bill.

Lame ducks in December?The Nov. 2 elections could turn more than a few law-

makers to lame ducks and that could bring a flurry of activity to close out the year by Congress. That especially will be the case if Democratic numbers dwindle to the point of holding reduced margins in the new Congress. But if Republicans regain control of any chamber, that could delay action on some matters until the next, new Congress is seated in early 2011.

Game plan: The pre-Me-morial Day low is key support. Fed cattle producers should be prepared to add defensive hedges on a close below that level despite the discount futures hold to the cash market.

Corn II’10 50% III’10 0% IV’10 0% I’11 0%Meal II’10 50% III’10 0% IV’10 0% I’11 0%

Analysis page 1

June 5, 2010

HOGS

CATTLE

FEEDFeed Monitor

Position Monitor

Game plan:Hog futures are showing signs of a price recovery, although buyers have been slow to surface as they wait on a low in the cash market. Be pre-pared to add short-term hedge coverage if support at the May low is violated.

Fundamental analysisRetailer beef purchases picked up coming out of Memorial Day week-end, which suggests holiday clear-ance was strong. That gives traders hope retailers will actively feature beef for Father’s Day. The stronger beef movement also encouraged packers to pay steady to firmer prices for cash cattle in the Plains, breaking the recent string of cash weakness. With market-ready cattle supplies tightening, a pickup in beef demand would rebuild a solid fundamental floor of support under cattle futures. But there’s more than just fundamen-tals at play in the cattle market. Concerns euro-zone debt problems will spread remain a market factor. With funds still heavily long cattle futures, risk of sharp liquidation pressure remains a real threat to the market.

Position MonitorLean Hogs

II’10 0% III’10 0% IV’10 0% I’11 0%

Corn game plan: Stay hand-to-mouth on corn needs for now as corn futures are threatening a downside breakout from the two-month choppy range. Extended cash coverage would be advised if there are signs of a strong price recovery.Meal game plan: Stay hand-to-mouth on meal needs for now as prices are trending lower. Be prepared to extend cash coverage if value buy-ing returns to the market.

Daily July MealTrend is choppy.

Fundamental analysisThe big discount summer-month lean hog futures held to the cash market has been erased after three weeks of sharp pressure on cash hog bids. While cutting margins were strong for much of the past three weeks, many plants took extended down-time ahead of the Memorial Day holiday due to tight market-ready supplies. Now that plants are run-ning again and margins are very deep in the black, near-term price strength is expected to rebuild in the cash hog market. And if cash hog bids firm, futures will be supported as market-ready hog supplies will remain tight through summer. The only real concern in the hog market is with investor confidence and the threat of sharp fund selling if the move to risk aversion heightens.

Feds FeedersII’10 0% 0%

III’10 0% 0%IV’10 0% 0% I’11 0% 0%

The downtrend from the February and March highs is support again.

CME Feeder Cattle Index

CME Lean Hog Index

Daily August Live CattleShort-term trend is down.

Daily August Lean HogsUptrend is being challenged.

Key near-term support lies at the May low of $81.25. A drop below that level would leave the March low

at $77.95 as the next level of strong support.

If the contract can reestablish the uptrend from the February low, it would open the door to a challenge of contract-high resistance at $87.35.

Support at $89.00 remains intact for now. A drop below that level would open downside risk to $86.63. For bulls to regain control, they must reestablish the uptrend from the December low.

$86.63

$72.60

The big price spike June 3 completed a 38% retracement of the price decline from the

April high to the June 1 low. Followthrough buying would confirm a short-term low.

$77.95

$95.55

$89.00

$259.70

$296.70

$87.35

$251.00

$81.25

Position Monitor — All Wheat ’09 crop ’10 cropCash-only: 100% 50%

Hedgers (cash sales): 100% 50% Futures/Options 0% 0%

Game plan: Get current with advised sales. An extended price recovery would be incentive to increase 2010-crop sales as the upside is limited to corrective buying.

June 5, 2010 / Analysis page 2

CORN

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

-0.35

-0.30

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

3-year avg. 2010

Daily December Corn

Aug

Sep

tO

ctN

ovD

ec Jan

Feb

Mar

Apr

May Jun

Jul

Aug

0102030405060

'08-09

'09-10

USDA

Total Corn Export Bookings

Average Corn Basis

Trend is down.Daily Chicago July Wheat

Daily July CornTrend is choppy to lower.

Trend is choppy.

Position Monitor ’09 crop ’10 cropCash-only: 80% 35% Hedgers (cash sales): 90% 40% Futures/Options 0% 0%

WHEAT

Fundamental analysisFavorable weather coming out of the Memorial Day weekend put pressure on corn futures. With the corn crop off to a strong start and plentiful soil moisture across much of the Corn Belt, yield expectations are high — and in many cases climbing. That has allowed traders to ignore increased talk of the likely development of La Niña this summer. Outside markets also continue to put pressure on corn. Ongoing concerns with the euro-zone debt situation are driving inves-tors toward more risk aversion, which is causing liquidation pressure on commodities, including corn. As long as weather and outside markets are price-negative, corn futures are at risk of additional selling pressure. It’s likely going to take fresh positive Chinese demand news and/or a sud-den shift in the weather to hot and dry before corn puts in a low.

Fundamental analysis

SRW: Bearish fundamentals, technical-based selling and a move toward more risk aversion continue to eat away at wheat futures. With the path of least resistance being down and nothing for bulls to dig their heels into, the down-side remains open, while the upside is limited to corrective buying.

Game plan: Hedgers should be pre-pared to add short-term, defensive hedges as the July contract closed below the April low. That opens fresh downside price risk and means the market is searching for a new level of value. With additional near-term price pressure, get current with advised 2009- and 2010-crop cash sales. But additional sales will wait as La Niña talk is building.

Basis July futures

The contract must close back above $4.60 1/2 and the downtrend from the

May high just to open the possibility of a rebound to the long-term downtrend.

A bounce from support at $3.67 1/4 could set up a near-term test of

resistance at $3.94 3/4.

$3.51 1/2

Position Monitor

$4.02 1/4

The close below $3.51 1/2 leaves the contract low at $3.33 3/4 as the only strong chart support.

$3.94 3/4

Million metric tons

$4.15 1/2

Building layers of flat resistance signal bears have the upper hand technically. But a

quick rebound back above $3.51 1/2 could trigger a recovery to the May high at $3.74 3/4.

$3.67 1/4

$4.60 1/2

$3.33 3/4

$3.74 3/4

$3.87 1/2

Support at $3.67 1/4 has been spiked, but the contract has not yet closed below that level. Support under that level is at the Sept. 2009 low at $3.52 3/4.

The contract violated two levels of support last week — the previous contract low at $4.60 1/2 and initial weekly chart support at $4.47. Next support is at the 2009 low of $4.39 1/4 and the 2007 low at $4.12.

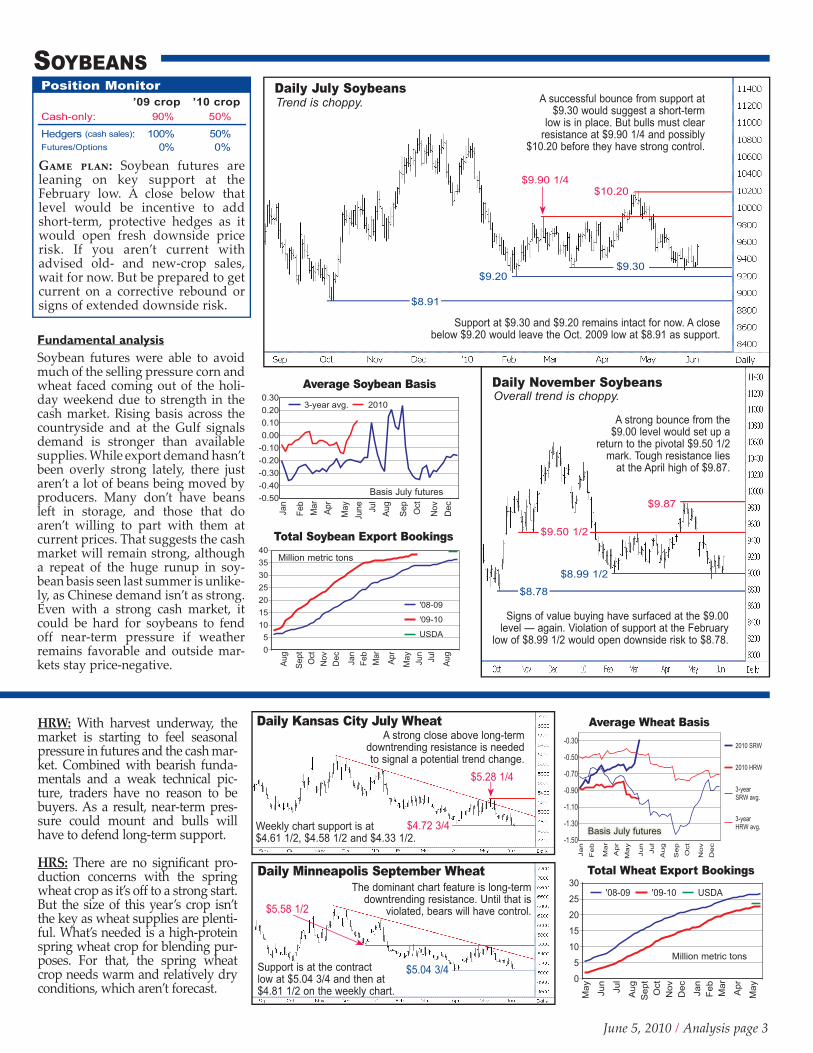

Game plan: Soybean futures are leaning on key support at the February low. A close below that level would be incentive to add short-term, protective hedges as it would open fresh downside price risk. If you aren’t current with advised old- and new-crop sales, wait for now. But be prepared to get current on a corrective rebound or signs of extended downside risk.

June 5, 2010 / Analysis page 3

Trend is choppy.Daily July Soybeans

Daily November SoybeansOverall trend is choppy.

Jan

Feb

Mar

Apr

May

June Ju

lAu

g

Sep

Oct

Nov

Dec

-0.50-0.40-0.30-0.20-0.100.000.100.200.30

3-year avg. 2010

Average Soybean Basis

Position Monitor ’09 crop ’10 cropCash-only: 90% 50% Hedgers (cash sales): 100% 50% Futures/Options 0% 0%

Fundamental analysisSoybean futures were able to avoid much of the selling pressure corn and wheat faced coming out of the holi-day weekend due to strength in the cash market. Rising basis across the countryside and at the Gulf signals demand is stronger than available supplies. While export demand hasn’t been overly strong lately, there just aren’t a lot of beans being moved by producers. Many don’t have beans left in storage, and those that do aren’t willing to part with them at current prices. That suggests the cash market will remain strong, although a repeat of the huge runup in soy-bean basis seen last summer is unlike-ly, as Chinese demand isn’t as strong. Even with a strong cash market, it could be hard for soybeans to fend off near-term pressure if weather remains favorable and outside mar-kets stay price-negative.

SOYBEANS

Aug

Sept

Oct

Nov

Dec Jan

Feb

Mar

Apr

May Jun

Jul

Aug0

510152025303540

'08-09

'09-10

USDA

Total Soybean Export Bookings

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

-1.50

-1.30

-1.10

-0.90

-0.70

-0.50

-0.30 2010 SRW

2010 HRW

3-yearSRW avg.

3-yearHRW avg.

Average Wheat Basis

May Jun

Jul

Aug

Sep

tO

ctN

ovD

ec Jan

Feb

Mar

Apr

May

0

5

10

15

20

25

30'08-09 '09-10 USDA

Total Wheat Export Bookings

HRW: With harvest underway, the market is starting to feel seasonal pressure in futures and the cash mar-ket. Combined with bearish funda-mentals and a weak technical pic-ture, traders have no reason to be buyers. As a result, near-term pres-sure could mount and bulls will have to defend long-term support.

HRS: There are no significant pro-duction concerns with the spring wheat crop as it’s off to a strong start. But the size of this year’s crop isn’t the key as wheat supplies are plenti-ful. What’s needed is a high-protein spring wheat crop for blending pur-poses. For that, the spring wheat crop needs warm and relatively dry conditions, which aren’t forecast.

Daily Kansas City July Wheat

Daily Minneapolis September Wheat

Basis July futuresBasis July futures

Basis July futures

A strong close above long-term downtrending resistance is needed to signal a potential trend change.

The dominant chart feature is long-term downtrending resistance. Until that is

violated, bears will have control.

$8.78

$10.20$10.20

Signs of value buying have surfaced at the $9.00 level — again. Violation of support at the February

low of $8.99 1/2 would open downside risk to $8.78.

A successful bounce from support at $9.30 would suggest a short-term

low is in place. But bulls must clear resistance at $9.90 1/4 and possibly

$10.20 before they have strong control.

Million metric tons

Million metric tons

A strong bounce from the $9.00 level would set up a

return to the pivotal $9.50 1/2 mark. Tough resistance lies

at the April high of $9.87.

$5.58 1/2

$5.28 1/4

$8.99 1/2

$9.20

$9.90 1/4$9.90 1/4

$4.72 3/4

$5.04 3/4

$9.50 1/2

$9.30$9.30

$9.87$9.87

$8.91

Support at $9.30 and $9.20 remains intact for now. A close below $9.20 would leave the Oct. 2009 low at $8.91 as support.

Weekly chart support is at $4.61 1/2, $4.58 1/2 and $4.33 1/2.

Support is at the contract low at $5.04 3/4 and then at $4.81 1/2 on the weekly chart.

June 5, 2010 / Analysis page 4

Read Pro Farmer on Friday!Put the profit-building news, analysis and insight of Pro Farmer newsletter

to work for you as early as Friday afternoon — before it hits the mail. Get Pro Farmer newsletter via email. Call 1-800-772-0023 for details!

Key Market Items on My ‘To Watch’ List

1) USDA Crop Progress/Condition Rpt. — Monday, June 7, 3:00 p.m. CTGiven generally favorable weather con-ditions and strong crop condition rat-ings, there are no major concerns with the corn crop.

2) USDA Crop Production/S&D Rpts. — Thursday, June 10, 7:30 a.m. CTReaction should be relatively limited unless there are surprises, as traders await the Acreage Report at the end of June.

3) USDA Weekly Export Sales Report — Thursday, June 10, 7:30 a.m. CTChinese purchases of corn, soybeans and cotton are the focal point.

FROM THE BULLPEN

Jan

Feb

Mar Apr

May Jun Jul

Aug

Sep

Oct

Nov

Dec-800.00

-700.00

-600.00

-500.00

-400.00

-300.003-year avg. 2010

Average Cotton BasisCOTTONPosition Monitor ’09 crop ’10 cropCash-only: 75% 50% Hedgers (cash sales): 100% 50% Futures/Options 0% 0%

Fundamental analysisWith planting moving into the final stages and no reason for traders to be concerned with the crop, funds are trimming their long exposure. Unless funds are active sellers, however, the downside should be relatively limit-ed as the demand side of the market remains price-supportive.

Domestic Cotton Use

GENERAL OUTLOOK

Game plan: Get current with advised sales. Be prepared to add hedge cov-erage if Dec. cotton futures close below the last reaction low.

Basis July futuresBasis July futures

by Senior Market Analyst, Brian Grete

Profit Briefing Seminar June 29 Join us in Redwood Falls, Minnesota, Tuesday, June 29, for our popular one-day seminar where you’ll hear what’s ahead for commodity prices, farm policy, land prices and the economy.

Call 1-800-772-0023 for details

Odds of increased price volatility in the corn and soybean markets this summer are rising. Weather is likely to be at the forefront of potentially sharp price movement.

While weather conditions are currently deemed “near ideal” by most traders and yield expectations are high, there’s a potential threat on the horizon — La Niña. (See News page 2 for more on weather.)

As we’ve noted many times over the last several weeks, when La Niña develops will be the key. The sooner a La Niña pattern appears, the greater the potential yield risk; the later, the less potential harm to yields.

History has proven traders will respond sharply to summer weather — positively or negatively. And they will likely respond even more aggressively if there’s a dramatic shift in the weather pattern during the middle of the

growing season. That’s the primary reason price volatility could be extreme this year.

While weather is likely to be the primary price driver this summer, the list of market-moving factors definitely doesn’t stop there.

Chinese demand, for corn and soybeans, will also be key. China carries so much weight they have the ability to sharply move prices. And you can bet there will be some activity from China — purchases and/or can-cellations — this summer.

The “forgotten” factor which will help move prices is the cash market. Strength in the cash soybean market is currently getting the most attention as prices are rising across the countryside and at the Gulf. But the cash corn market could also become a factor down the road, depending on how new-crop produc-tion potential shapes up this summer.

Weekly Crude Oil FuturesOn the bearish side, traders are concerned the euro-zone debt crisis will spread and turn into a contagion, which would slash global oil demand. Plus, domestic oil supplies are more than plentiful at near 19-year highs.

Most of the market headwinds are bearish and the path of least resis-tance remains down. But there is enough fodder for both bulls and bears to trigger choppy near-term trade — although price action could be volatile within a choppy range.

Energies: After the big price decline from the early May high, crude oil prices are showing signs of settling into a choppy trading range.

On the bullish side, there continues to be signs of gradual U.S. economic recovery. And with economic recovery comes hope for greater oil/gas demand. Plus, there is talk OPEC is likely to cut oil production if prices spend an extended period below $70 per barrel. Those factors are likely to attract buy-ing interest on price breaks.

Daily December CottonTrend is higher.

68.55¢A close below support at 74.06¢ would leave

68.55¢ as the next level of strong chart support.

The quick drop back below 78.25¢ signals the breakout attempt was a bull trap. The May high at 79.20¢ is tough resistance.

74.06¢

1985

-86

1986

-87

1987

-88

1988

-89

1989

-90

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

3

5

7

9

11

13Million bales

Longer-term trend is choppy to higher. Strong near-term

resistance lies at the May high at $87.15.

78.25¢79.20¢

$87.15$65.05

$58.32

The spike of support at $65.05 attracted value buying. Additional support is at $58.32.