corn starts to stir traders talk about slow planting, but tighter … · · 2018-04-25tota nl ext...

TRANSCRIPT

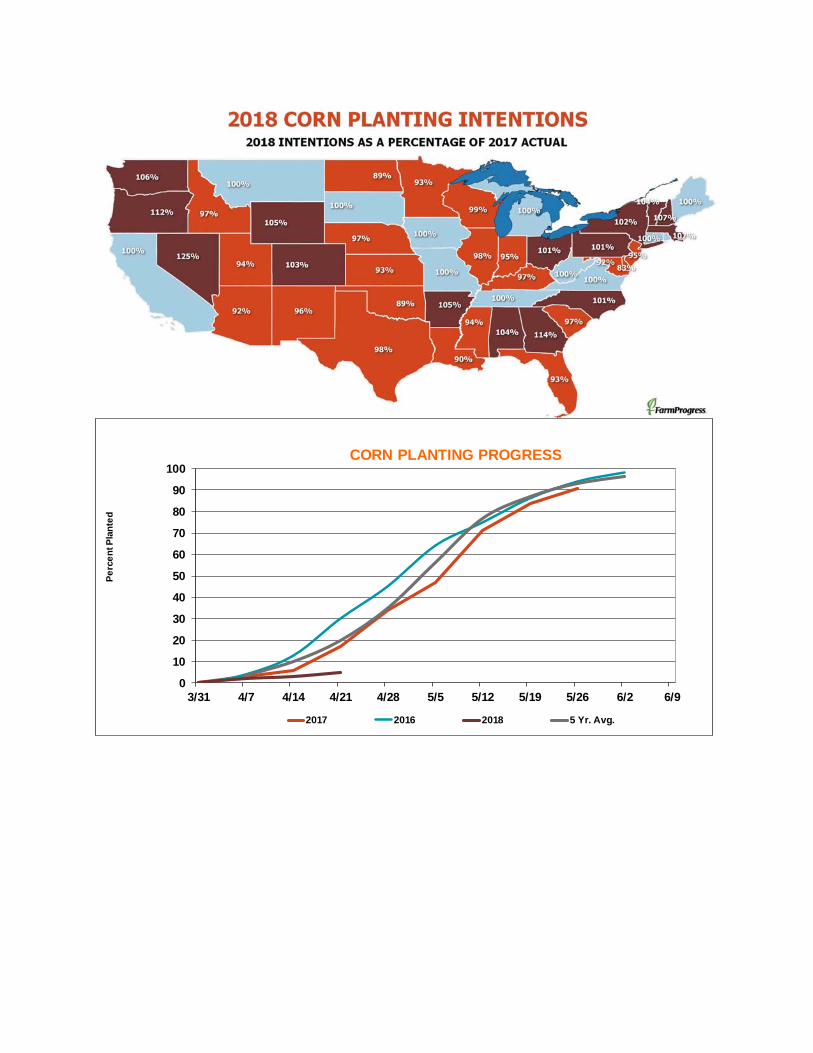

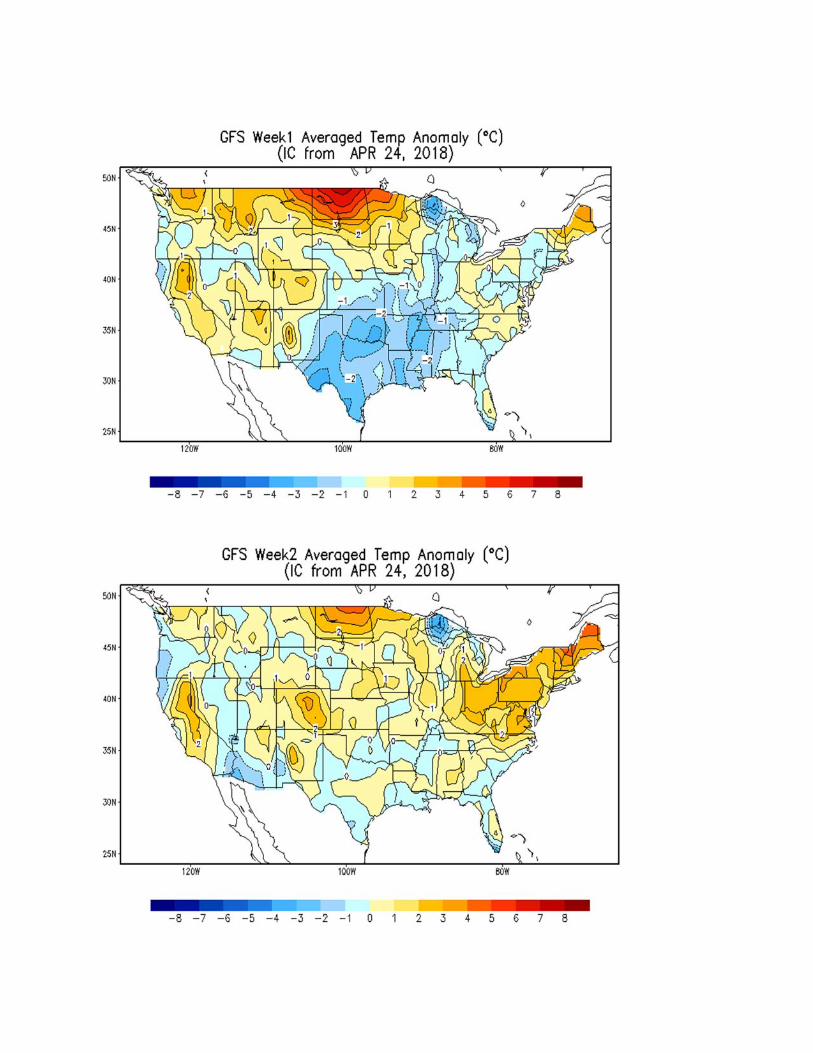

Corn starts to stir Traders talk about slow planting, but tighter carryout is key By Bryce Knorr, senior grain market analyst Growing a corn crop is a marathon, not a sprint. But so far the corn market is hitting all the paces to what could be a profitable year. A cold, wet start to the growing season has farmers talking about planting delays. The trade is talking about it too, but only a little. Tractors are starting to roll, for one thing, and forecasts look warmer for a week or so, and somewhat drier. But those who follow the markets also know about a weather model developed by USDA to predict corn yields. It’s not the be-all and end-all. But one of the factors it uses, in addition to June crop stress, and July rainfall and temperatures, is planting progress by mid-May. On average, around 85% of the crop is planted by the end of the third week of the month. That leaves a window of three weeks to get most of the crop in the ground. Moreover, some years slow progress makes a difference, some years it doesn’t. So while being idle in April frustrates farmers, it’s only a mild titillation for traders. Nonetheless, there are other good reasons to be optimistic about corn. Unless farmers plant significantly more acres than USDA forecast in its March report, production should be less than demand under normal yield and usage conditions. The balance sheet won’t be anywhere near squeaky tight. But it could support not only higher average cash prices, but rallies as well on any threat to yields. Forecasts for a warm June are already shaping up according to some models, adding further potential. But one of the most encouraging bits of hope comes from seasonal trend charts. December corn has a bullish pattern of higher highs and higher lows. Until that trend breaks down, the tendency is for higher prices into the approach of the window for pollination. This week’s pricing model puts the selling range for new crop futures from $4.37 to $4.77, levels that would be profitable for the average grower with average yields and basis. Don’t look for that price anytime soon, especially with geopolitical risk in outside markets lurking on a daily basis. In the meantime, growers should focus on winding down pricing of old crop inventory. Basis is firming, and pushes traditionally are possible when farmers are too busy in the field to sell. A record book of unshipped corn sales should support bids in the export pipeline, both along the river system and at rail terminals shipping out to the PNW and Mexico. Demand could grow if Brazil’s corn crop is hurt by dry conditions that appear to be developing, though it’s still too early to draw conclusions on yields. Ethanol may be more of a question mark, as production slowed to its lowest level since harvest. That’s not completely unusual seasonally, but it means corn usage to make the biofuel may not be any bigger than USDA currently estimates. Officially, I’ve recommended being 90% protected on 2017 production, hedging with futures or HTAs to wait for basis to keep firming. And being 100% set isn’t a bad idea, either for those with a profit who are ready to move on. Growers who are nervous about new crop can sell the carry to July 2019 to get closer to a profitable price. Otherwise, consider buying calls if the market breaks. Use rallies to consider bear-spreading December 2018 against July 2019 at 13 cents or better as a hedge for potential weak basis at harvest.

Corn Supply & Demand

USDA

Area 2016 2017 2018 2017 2018Planted 94,004 90,167 90,000 90,703 88,026 Harvested 86,748 82,703 82,700 82,703 80,885

Yield 174.6 176.6 174.0 176.6 172.6

Beginning stocks 1,737 2,294 2,352 2,294 2,181 Production 15,148 14,605 14,390 14,605 13,957 Imports 57 50 50 37 37 Supply, total 16,942 16,947 16,792 16,936 16,175 Feed and residual 5,472 5,500 5,475 5,427 5,226 Food, seed and ind. 6,884 7,040 7,145 7,048 7,119 Domestic, total 12,356 12,540 12,620 12,476 12,345 Exports 2,293 2,225 1,900 2,279 2,034 Use, total 14,649 14,766 14,520 14,755 14,379 Ending stocks 2,294 2,182 2,272 2,181 1,796 Ave. cash price $3.36 $3.35 $3.40 $3.41 $3.92

Stocks to use 15.7% 14.8% 15.6% 14.8% 12.5%Ave. nearby futures $3.69 $3.60 $3.76 $4.19

Top Third $3.76 $4.39 of Price Range to $4.09 to $4.77

Bryce's Forecast

0

10

20

30

40

50

60

70

80

90

100

3/31 4/7 4/14 4/21 4/28 5/5 5/12 5/19 5/26 6/2 6/9

Pe

rce

nt P

lan

ted

CORN PLANTING PROGRESS

2017 2016 2018 5 Yr. Avg.

0

10

20

30

40

50

60

707

0

73

76

79

82

85

88

91

94

97

00

03

06

09

12

15

18

sto

ck

s/u

se

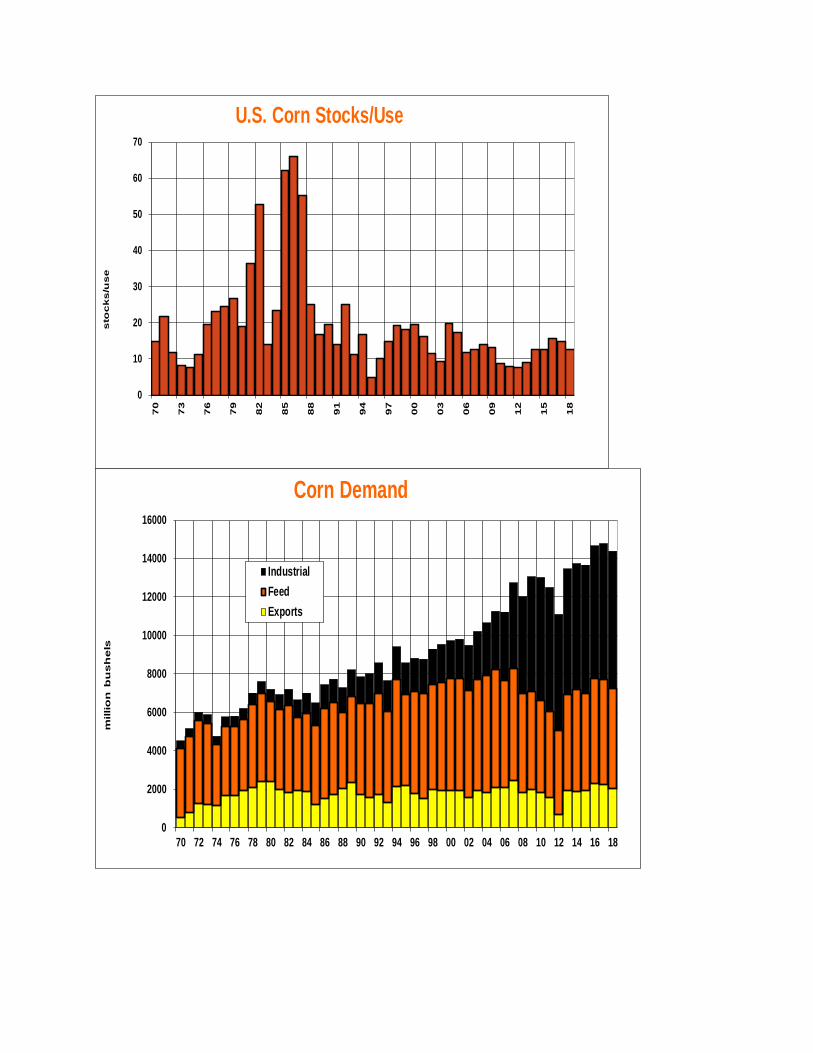

U.S. Corn Stocks/Use

0

2000

4000

6000

8000

10000

12000

14000

16000

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

millio

n b

us

he

ls

Corn Demand

Industrial

Feed

Exports

‐$1.00

‐$0.50

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Average Corn Belt Ethanol Plant Margins

2.65

2.70

2.75

2.80

2.85

2.90

2.95

Sep‐14 Jan‐15 May‐15 Sep‐15 Jan‐16 May‐16 Sep‐16 Jan‐17 May‐17 Sep‐17 Jan‐18

ETHANOL PRODUCTIONGALLONS FROM EACH BUSHEL USED

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2012 2013 2014 2015 2016 2017 2018

tho

usa

nd

ba

rre

ls

Source: USEIA, Farm Futures

Monthly U.S. ethanol production and stocks

Production Stocks

800

850

900

950

1000

1050

1100

1150

17000

18000

19000

20000

21000

22000

23000

24000

25000

9/1/16 11/1/16 1/1/17 3/1/17 5/1/17 7/1/17 9/1/17 11/1/17 1/1/18 3/1/18

thousand barrels/day

Production

thousand barrels

Stocks WEEKLY ETHANOL PRODUCTION AND STOCKS

Ending stocks Daily Production

0

20

40

60

80

100

120

2013 2014 2015 2016 2017

CHINESE CORN IMPORTS, SEPT-MARCH

(million bushels)Ukraine U.S. Total

Weekly Export Inspections

in million bushels For week of 04/19/18

This Week

Last Week

Average Trade Guess

This Week

Last Year

Rate Needed to Meet USDA

Forecast

Year-to-Date

Total This Year

Year-to-Date

Total Last Year

WHEAT 22.8 18.6 12-20 23.2 22.5 790 875

CORN 67.7 62.1 47-66 57.8 52.6 1,172 1,471

SOYBEANS 17.3 16.4 11-22 23.8 24.6 1,574 1,799

Source: USDA, Reuters

Weekly Export Sales (million bushels)AS OF WEEK ENDING 4/12/18

Wheat Corn SoybeansOld Crop Sales (2.5) 43.0 38.2 New Crop Sales 8.8 4.4 40.1Total Sales 6.4 47.4 78.3 Prior Week 6.9 35.3 90.6 Trade Estimates 11.9 41.3 66.2 Rate to reach USDA Forecast 12.1 14.2 4.0 Export Shipments 16.7 62.8 14.8Rate to reach USDA Forecast 32.4 56.7 25.4Commitments % of USDA est. 96% 86% 94%5-year average for this week 96% 84% 96%Shipments % of USDA est. 77% 59% 82%5-year average for this week 81% 56% 88%Source: USDA, Reuters

0%

20%

40%

60%

80%

100%

120%

0

500

1000

1500

2000

2500

Total Corn Sales & Shipments(Year to Date)

Total Commitments % of USDA Forecast

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0200400600800

10001200140016001800

Corn Shipments(Year to Date)

Total Shipments % of USDA Forecast

0

500

1000

1500

2000

2500

3000

0

20

40

60

80

100

120

140

160

Final exports

New crop sales

Total Next Year's Corn Sales (Year to Date)

New Crop Sales Final Exports

0

100

200

300

400

500

600

700

800

900

Mil

lio

n B

ush

els

Unshipped Corn Sales

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

S O N D J F M A M J J A

Th

ou

sa

nd

Bu

sh

els

Weekly Corn Export Inspections

5-Yr. Avg. 2016-17 2017-18

$3.00

$3.50

$4.00

$4.50

$5.00

-300000

-200000

-100000

0

100000

200000

300000

400000

1/15 3/15 5/15 7/15 9/15 11/15 1/16 3/16 5/16 7/16 9/16 11/16 1/17 3/17 5/17 7/17 9/17 11/17 1/18 3/18

ne

arb

y f

utu

res

ne

t p

osit

ion

in

co

ntr

acts

Source: CFTC

Commitment of Traders - Corn

Index funds Hedge funds Futures

250

260

270

280

290

300

310

320

300

320

340

360

380

400

420

440

11/1 1/1 3/1 5/1 7/1 9/1 11/1

DECEMBER CORN BULL VS BEAR YEARS

Bull Market 17-Dec Dec-18 Normal Year

255

260

265

270

275

280

285

290

295

300

300

350

400

450

500

550

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

July Corn Bull vs Bear Years

Bull Market Years July 2018 Normal Year

July Corn Futures Seasonal Trend

Start Date +1 Week +2 Weeks +3 Weeks +4 Weeks +5 Weeks +6 Weeks4/24 5/1 5/8 5/15 5/22 5/29 6/5Ave. Gain/Loss (3.6) (2.9) (4.5) (5.4) (3.3) (5.9)

% Up 20/43 16/43 19/43 15/43 20/43 20/43% Down 23/43 27/43 24/43 28/43 23/43 22/43Ave. Gain - Up year 5.5 12.1 9.8 15.1 13.3 11.1 Ave Loss - Down Year (11.6) (11.7) (15.8) (16.3) (17.7) (21.6) Biggest Gain 20.0 32.3 19.0 40.3 62.5 46.8 Biggest Loss (102.8) (103.3) (101.8) (90.8) (95.5) (94.5)

This table shows the typical seasonal pattern at weekly intervals from the start date, based onaverage daily futures prices from 1974-2016. Gains and losses are based on the difference between the closing price on the start date and the closing price on the weekly date shown.