cooking sauces & food seasonings - brand licensing

TRANSCRIPT

Market Report 2006

Second Edition September 2006Edited by Isla Gower

ISBN 1-84729-016-7

Cooking Sauces & Food Seasonings

Cooking Sauces & Food Seasonings Foreword

Key Note Ltd 2006

In today’s competitive business environment, knowledge and understanding of your marketplace is essential. With over 25 years’ experience producing highly respected off-the-shelf publications, Key Note has built a reputation as the number one source of UK market information. Below are just a few of the comments our business partners and clients have made on Key Note’s range of reports.

“The Chartered Institute of Marketing encourages the use of market research as an important part of a systematic approach to marketing. Key Note reports have been available in the Institute’s Information and Library Service for many years and have helped our members to build knowledge and understanding of their marketplace and their customers.”

The Chartered Institute of Marketing

“We have enjoyed a long-standing relationship with Key Note and have always received an excellent service. Key Note reports are well produced and are always in demand by users of the business library.”

“Having subscribed to Market Assessment reports for a number of years, we continue to be impressed by their quality and breadth of coverage.”

The British Library

“Key Note reports cover a wide range of industries and markets — they are detailed, well written and easily digestible, with a good use of tables. They allow deadlines to be met by providing a true overview of a particular market and its prospects.”

NatWest

“Accurate and relevant market intelligence is the starting point for every campaign we undertake. We use Key Note because they have a report on just about every market sector you can think of, and the information is comprehensive, reliable and accurate.”

J Walter Thompson

“Market Assessment reports provide an extremely comprehensive source of information for both account handling and new business research, with excellent, clear graphics.”

Saatchi & Saatchi Advertising

James DonovanManaging DirectorKey Note Limited

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

Contents

Executive Summary 1

1. Market Definition 2

REPORT COVERAGE.......................................................................................................................2

MARKET SECTORS..........................................................................................................................2

MARKET TRENDS............................................................................................................................2Attitudes Towards Cooking .............................................................................................................2Growth in Smaller Households ........................................................................................................2Staggered Eating Occasions.............................................................................................................3Lighter Eating Occasions ..................................................................................................................3Lack of Cooking Confidence ............................................................................................................3International Eating .........................................................................................................................3Supplier Activity................................................................................................................................3New Flavours and Cuisines...............................................................................................................3Provenance........................................................................................................................................4Packaging..........................................................................................................................................4Retailer Activity ................................................................................................................................4Healthy Eating ..................................................................................................................................4Barbecue Opportunities ...................................................................................................................5ECONOMIC TRENDS.......................................................................................................................5Gross Domestic Product....................................................................................................................5Table 1: UK Gross Domestic Product at Current and Annual Prices (£m), 2001-2005 ..................5Inflation.............................................................................................................................................6Table 2: UK Rate of Inflation (%), 2001-2005 .................................................................................6Household Disposable Income.........................................................................................................7Table 3: UK Household Disposable Income Per Capita (£), 2001-2005..........................................7MARKET POSITION ........................................................................................................................7The UK...............................................................................................................................................7Table 4: Consumer Expenditure on Food, Cooking Sauces and Food Seasonings (index 2001=100), 2001-2005.......................................................................8Figure 1: Consumer Expenditure on Food, Cooking Sauces and Food Seasonings (index 2001=100), 2001-2005.......................................................................8

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

2. Market Size 9

THE TOTAL MARKET......................................................................................................................9Table 5: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (£m at rsp), 2001-2005 .........................................................9Figure 2: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (£m at rsp), 2001-2005 .......................................................10BY MARKET SECTOR....................................................................................................................10Figure 3: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (%), 2005 ............................................................................11Cooking Sauces ...............................................................................................................................11Table 6: The UK Cooking Sauces Sector by Value at Current Prices (£m at rsp), 2001-2005 .......................................................................................12Pasta Sauces ....................................................................................................................................12Indian Sauces ..................................................................................................................................13Chinese and Oriental Sauces..........................................................................................................13British Recipes .................................................................................................................................13Other Cuisines.................................................................................................................................13Chilled Sauces .................................................................................................................................13Food Seasonings .............................................................................................................................14Table 7: The UK Food Seasonings Sector by Value at Current Prices (£m at rsp), 2001-2005 .......................................................................................14Salt...................................................................................................................................................14Herbs ...............................................................................................................................................15Spices ...............................................................................................................................................15

3. Industry Background 16

RECENT HISTORY..........................................................................................................................16

NUMBER OF COMPANIES ...........................................................................................................16Table 8: Number of UK VAT-Based Enterprises Engaged in the Manufacture of Food and Beverages by Turnover Sizeband (number and %), 2005.......................................17EMPLOYMENT ..............................................................................................................................17Table 9: Number of UK VAT-Based Enterprises Engaged in the Manufacture of Food and Beverages by Employment Sizeband (number and %), 2005.................................18REGIONAL VARIATIONS IN THE MARKETPLACE ....................................................................18

DISTRIBUTION...............................................................................................................................19Table 10: Retail Sales of Cooking Sauces and Food Seasonings by Distribution Channel by Value (%), 2005.................................................................................19Figure 4: Retail Sales of Cooking Sauces and Food Seasonings by Distribution Channel by Value (%), 2005.................................................................................20HOW ROBUST IS THE MARKET?................................................................................................20

LEGISLATION .................................................................................................................................20

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

KEY TRADE ASSOCIATIONS........................................................................................................21Food and Drink Federation............................................................................................................21Salt Manufacturers’ Association ....................................................................................................22Seasoning and Spice Association...................................................................................................22

4. Competitor Analysis 23

THE MARKETPLACE .....................................................................................................................23

MARKET LEADERS........................................................................................................................23Campbell’s UK Ltd ..........................................................................................................................23G Costa and Co Ltd .........................................................................................................................24Discovery Foods Ltd ........................................................................................................................24General Mills UK Ltd.......................................................................................................................24HP Foods Ltd ...................................................................................................................................25JFC (UK) Ltd.....................................................................................................................................26Mars UK Ltd ....................................................................................................................................26McCormick (UK) Ltd........................................................................................................................27Premier International Foods UK Ltd..............................................................................................27RHM PLC..........................................................................................................................................28Sacla UK Ltd ....................................................................................................................................29Unilever UK Foods ..........................................................................................................................29Worldwing Investments Ltd...........................................................................................................30Other Companies............................................................................................................................31RH Amar & Co Ltd...........................................................................................................................31Dress Italian Ltd ..............................................................................................................................31English Provender Company Ltd....................................................................................................31Fiddes Payne Ltd .............................................................................................................................31Greencore Group PLC.....................................................................................................................32The Grocery Company Ltd..............................................................................................................32Maldon Crystal Salt Company Ltd .................................................................................................32The New Covent Garden Soup Co Ltd...........................................................................................32Princes Ltd .......................................................................................................................................32SHS Group Ltd.................................................................................................................................32Temple Foods Ltd ...........................................................................................................................33TRS Wholesale Co Ltd.....................................................................................................................33MARKETING ACTIVITY ................................................................................................................33Main Media Advertising Expenditure ...........................................................................................33Table 11: Main Media Advertising Expenditure on Cooking Sauces and Mixes (£000), Years Ending March 2005 and 2006..................................................................................33Recent Campaigns ..........................................................................................................................34JFC (UK) Ltd.....................................................................................................................................34Kikkoman .......................................................................................................................................34Mars UK Ltd ....................................................................................................................................34Dolmio ............................................................................................................................................34Uncle Ben’s .....................................................................................................................................34McCormick (UK) Ltd........................................................................................................................34

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

Schwartz .........................................................................................................................................34Prince’s Ltd ......................................................................................................................................35Lee Kum Kee ..................................................................................................................................35RHM PLC..........................................................................................................................................35Sharwood’s .....................................................................................................................................35Unilever UK Foods ..........................................................................................................................35Knorr ..............................................................................................................................................35Bertolli ............................................................................................................................................35Exhibitions.......................................................................................................................................35

5. Strengths, Weaknesses, Opportunities and Threats 36

STRENGTHS....................................................................................................................................36WEAKNESSES ................................................................................................................................36

OPPORTUNITIES............................................................................................................................37

THREATS.........................................................................................................................................37

6. Buying Behaviour 38

CONSUMER PENETRATION.........................................................................................................38Table 12: Penetration of Cook-In Sauces, and Packeted, Tinned and Pour-Over Sauces in the Last 12 Months (% of main shoppers), 2002 and 2005 .....................................................38By Sex ..............................................................................................................................................39Table 13: Penetration of Cook-In Sauces, and Packeted, Tinned and Pour-Over Sauces in the Last 12 Months by Sex (% of main shoppers), 2005 ..........................................................39By Age .............................................................................................................................................39Table 14: Penetration of Cook-In Sauces, and Packeted, Tinned and Pour-Over Sauces in the Last 12 Months by Age (% of main shoppers), 2005 .........................................................40By Social Grade ...............................................................................................................................40Table 15: Penetration of Cook-In Sauces, and Packeted, Tinned and Pour-Over Sauces in the Last 12 Months by Social Grade (% of main shoppers), 2005 ...........................................41By Presence of Children..................................................................................................................41Table 16: Penetration of Cook-In Sauces, and Packeted, Tinned and Pour-Over Sauces in the Last 12 Months by Presence of Children (% of main shoppers), 2005 .............................42

7. Current Issues 43

COMPANY AND BRAND ACTIVITY ...........................................................................................43Cardini’s...........................................................................................................................................43Filippo Berio....................................................................................................................................43Jim Beam.........................................................................................................................................43Simply UK........................................................................................................................................43Spice-N-Tice.....................................................................................................................................43Tiger Tiger.......................................................................................................................................44

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

SUDAN 1 SCARE ...........................................................................................................................44FOOD LABELLING.........................................................................................................................44

8. The Global Market 46

GLOBAL MARKETPLACE DEVELOPMENTS ..............................................................................46France ..............................................................................................................................................46Asian Amoy Sauce Business Sold ...................................................................................................46The UK.............................................................................................................................................46HP Ethnic Foods Sell-Off.................................................................................................................46The US .............................................................................................................................................46Kikkoman........................................................................................................................................46McCormick Restructure ..................................................................................................................46Organic Ragu from Unilever ..........................................................................................................46Vita Products and Budweiser Sauces .............................................................................................47

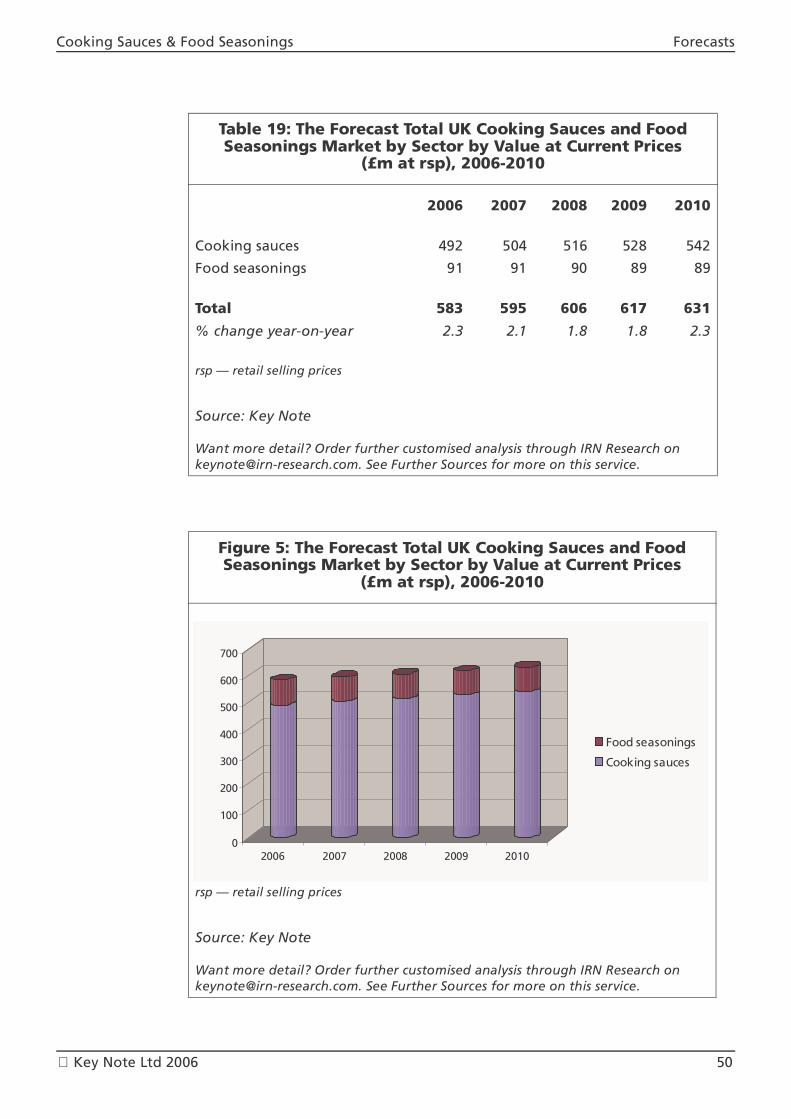

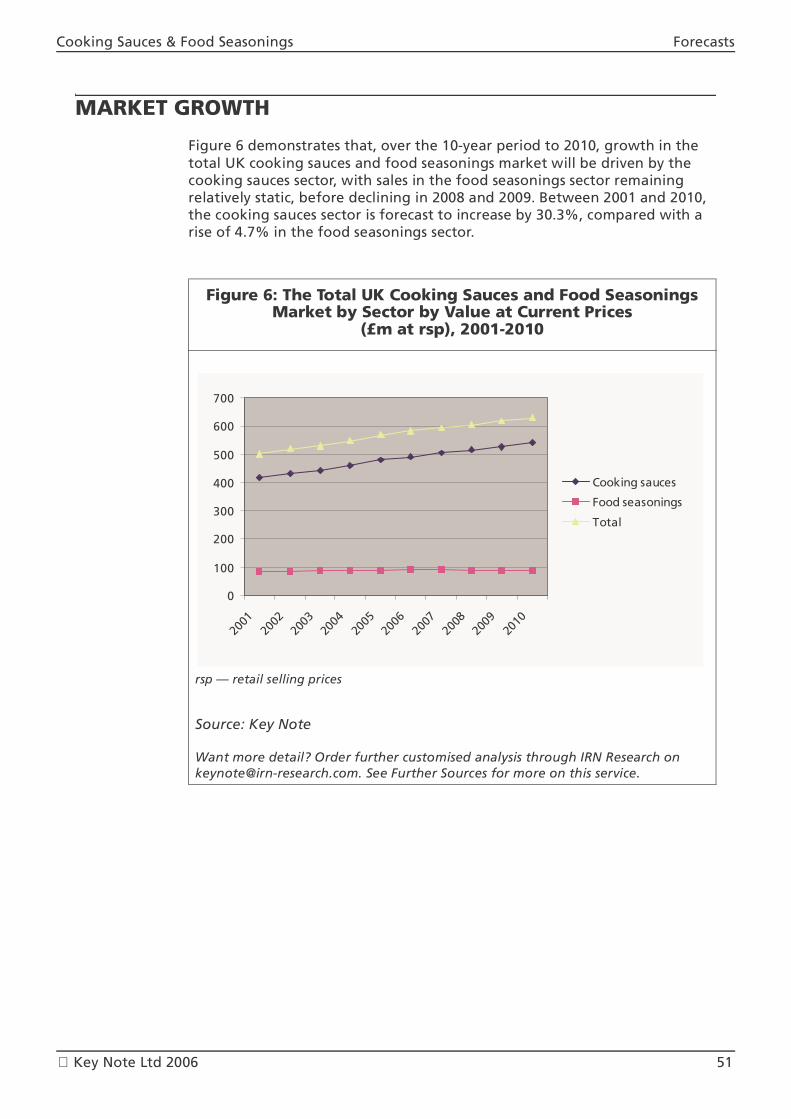

9. Forecasts 48

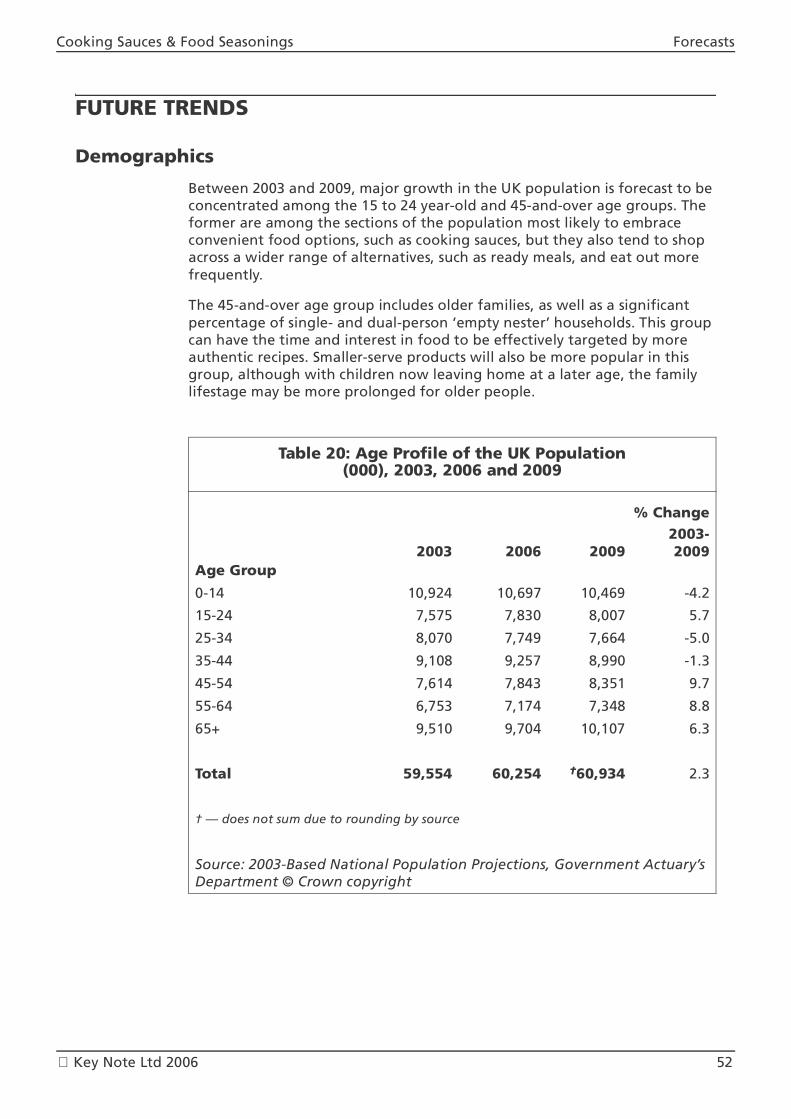

INTRODUCTION ............................................................................................................................48The Economy...................................................................................................................................48Gross Domestic Product..................................................................................................................48Table 17: Forecast UK Growth in Gross Domestic Product in Real Terms (%), 2006-2010 .........48Inflation...........................................................................................................................................48Table 18: Forecast UK Rate of Inflation (%), 2006-2010 ..............................................................49FORECASTS 2006 TO 2010 ..........................................................................................................49Table 19: The Forecast Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (£m at rsp), 2006-2010 .......................................................50Figure 5: The Forecast Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (£m at rsp), 2006-2010 .......................................................50MARKET GROWTH.......................................................................................................................51Figure 6: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (£m at rsp), 2001-2010 .......................................................51FUTURE TRENDS ...........................................................................................................................52Demographics .................................................................................................................................52Table 20: Age Profile of the UK Population (000), 2003, 2006 and 2009....................................52Market Segmentation ....................................................................................................................53Product Development ....................................................................................................................53

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

10. Company Profiles 54

HP Foods Ltd ...................................................................................................................................55Mars UK Ltd ....................................................................................................................................57Premier International Foods UK Ltd..............................................................................................59RHM PLC..........................................................................................................................................61Sacla UK Ltd ....................................................................................................................................63Worldwing Investments Ltd...........................................................................................................65

11. Consumer Confidence 67

METHODOLOGY...........................................................................................................................67KEY FINDINGS THIS QUARTER...................................................................................................67

THE WILLINGNESS TO BORROW ...............................................................................................68Confidence Declines Again ............................................................................................................68Table A: The Average Amount Consumers Are Willing to Borrow in Order to Purchase Expensive Items at Current and Constant November 2004 Prices (£ and £bn), May 2005, August 2005, November 2005, February 2006 and May 2006..............68Signs That the Decline Could be Bottoming Out .........................................................................70Table B: The Number of Adults Willing to Borrow in Order to Purchase Expensive Items (000 and %), May 2005, August 2005, November 2005, February 2006 and May 2006.............70THE WILLINGNESS TO SPEND FROM SAVINGS .......................................................................71Sharp Decline in Spending from Savings ......................................................................................71Table C: The Average Amount Consumers Are Willing to Spend from Savings in Order to Purchase Expensive Items at Current and Constant November 2004 Prices (£ and £bn), May 2005, August 2005, November 2005, February 2006 and May 2006..............72Table D: The Proportion of Adults Without Any Savings (%), May 2005, August 2005, November 2005, February 2006 and May 2006 ............................................................................73Borrowing Grows in Relative Importance.....................................................................................73Table E: The Average Amounts Adults are Confident Spending to Purchase Expensive Items (£ and %), May 2005, August 2005, November 2005, February 2006 and May 2006.........................................................................................................73

12. Further Sources 75

Associations.....................................................................................................................................75General Sources ..............................................................................................................................75Government Sources ......................................................................................................................75Other Sources..................................................................................................................................76Bisnode Sources ..............................................................................................................................76

Cooking Sauces & Food Seasonings Contents

Key Note Ltd 2006

Understanding TGI Data 80

Number, Profile, Penetration.........................................................................................................80Social Grade ....................................................................................................................................81Standard Region.............................................................................................................................81

Key Note Research 82

The Key Note Range of Reports 83

Key Note Ltd 2006 1

Cooking Sauces & Food Seasonings Executive Summary

Executive Summary

The total UK market for cooking sauces and food seasonings has experienced ongoing value growth since 2001, reaching £570m at retail selling prices (rsp) in 2005. This represents a growth of 4% on 2004, and a rise of 13.8% over the whole period. The main products covered in this report are ambient, packet and fresh chilled sauces, and mixes; and salt, pepper and other spices.

The shift towards more convenient food options has impacted on the market. Increasing sales of ready meals and prepared meal centres has meant that more ‘involved’ products, such as cooking sauces — seasonings, in particular — have experienced some decline in volume. The growth in foodservice and eating out has also had an adverse affect on the market.

More positively, the increasing variety of cuisines and flavours available through shortcuts such as sauces and marinades has made home cooking more accessible to some consumers. As the cookery media has become entertainment rather than education, there has been demand for simple ways to achieve more interesting meals. The endorsement of convenience food ranges by celebrities, such as Loyd Grossman, has added to the perceived legitimacy of such products.

Value has also been developed as consumers have traded up to more authentic ingredients. National dishes have given some ground to regional and local recipes, as consumers have become more interested in eating less anglicised versions. Healthy-eating options offering lower fat, salt or sugar recipes also command premium prices, as do organic sauces and seasonings.

The success of the barbecue market has provided another opportunity for products that can be used as marinades in the preparation of foods. This has aided some brands in gaining a year-round presence: previously, products for hot, cooked dishes might have languished in the warmer weather.

There are a number of international players in the market, such as Campbell’s, General Mills, Mars and McCormick. High-profile brands include Dolmio, Uncle Ben’s, Sharwoods, Homepride and Kikkoman. These have attracted some promotional and advertising support for the sector.

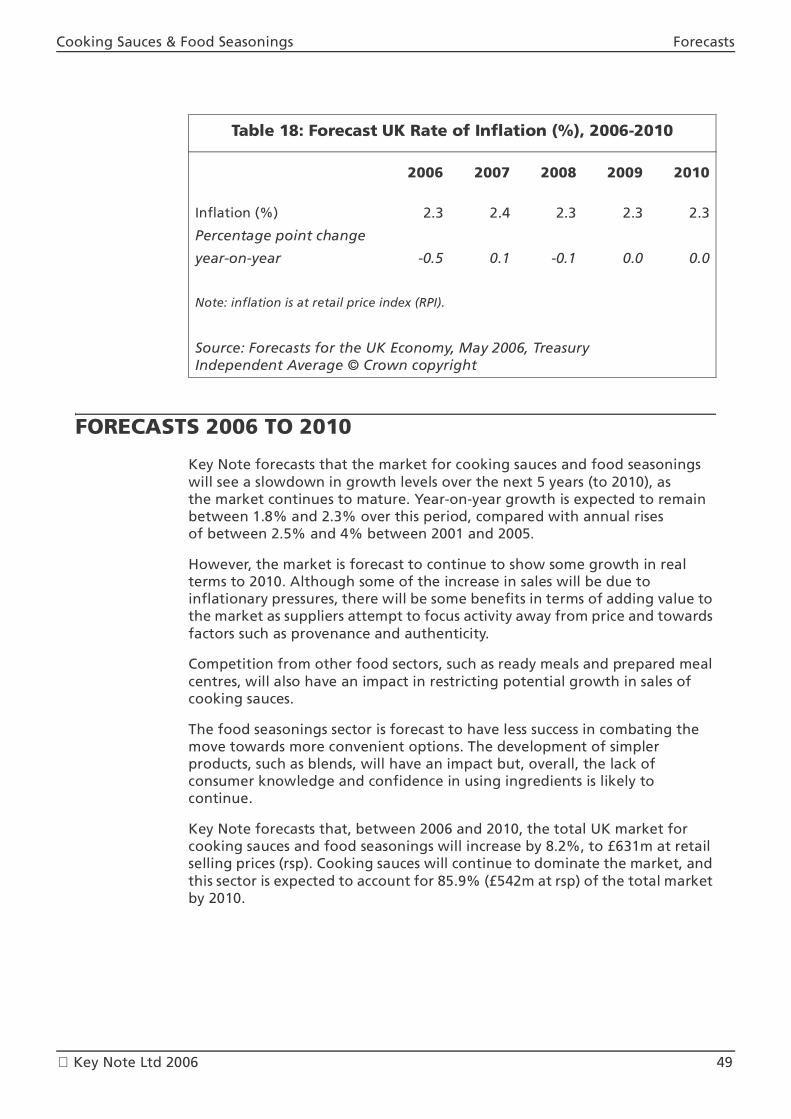

Despite value growth since 2001, the penetration levels for cooking sauces and food seasonings have fallen, with around three in ten consumers buying in either category in 2005. However, the outlook for the sector still has positive aspects, as suppliers look to focus on adding value to products and the market as a whole. Key Note forecasts that, over the 5-year period to 2010, the cooking sauces and food seasonings market will rise by between 1.8% and 2.3% year on year.

Key Note Ltd 2006 2

Cooking Sauces & Food Seasonings Market Definition

1. Market Definition

REPORT COVERAGE

This Key Note Market Report examines the UK retail market for cooking sauces, marinades and food seasonings. The report primarily focuses on ambient and chilled cooking sauces, and dried herbs and spices. Fresh herbs are excluded from the analysis.

MARKET SECTORS

The two main market sectors examined in this report are cooking sauces (including marinades) and food seasonings:

• Cooking sauces — this sector includes ambient, packet and fresh chilled sauces, and mixes. The products also vary according to usage, and can be divided broadly into those where foods are cooked in the sauce (cook-in sauces), and those that are poured over ingredients once they have been cooked (pour-over sauces). The range of cooking sauces available has been steadily expanding over the past decade, and a wide variety of recipes, from traditional to ethnic, are now available.

• Food seasonings — this sector covers salt, pepper and other spices. Food seasonings are used to enhance the flavours of foods. As consumers have become more educated about different foods and flavours, opportunities have arisen to offer a wider range of products. For example, salt is available in table, cooking, sea or flavoured variants. Herbs and spices have also become more widely available, and many products from international cuisines, such as Indian and Chinese spices, are now purchased.

MARKET TRENDS

Attitudes Towards Cooking

Cooking sauces are convenience products and, as such, have gained from changing attitudes towards cooking and eating in the UK. There has been a shift towards spending less time on food preparation or opting for more convenient options, as a result of a number of factors. These include the following:

Growth in Smaller Households

The average size of UK households is now 2.4 and, in 2005, 65% of households comprised just one or two people. The shift away from family households means that these homes are catering for fewer numbers, so they are more likely to minimise food-preparation times.

Key Note Ltd 2006 3

Cooking Sauces & Food Seasonings Market Definition

Staggered Eating Occasions

Similarly, in larger households, the range of activities undertaken by members may negate communal meals and lead to staggered eating occasions where meals are eaten in smaller numbers or alone. This too has driven the trend towards convenience products.

Lighter Eating Occasions

Trends towards smaller, and more frequent, meal and snack occasions have meant that the need to prepare an elaborate and timely evening meal is no longer such an important factor. This too can act against cooking from scratch.

The need to offer products for smaller eating occasions has been recognised through the development of products serving one or two people, or with longer in-home lives once opened. Both Sharwood’s and Knorr introduced such products in 2006.

Lack of Cooking Confidence

With cookery no longer being prioritised in school curriculums, and with more than a generation having been brought up without a traditional housewife role in the household, many consumers simply do not have the knowledge or skill to prepare meals from scratch.

International Eating

Even where consumers are able to prepare a range of meals, the shift towards more international eating means that there are likely to be gaps in knowledge. These gaps can be filled with cooking sauces and convenience products.

Supplier Activity

The demand for a range of convenient food-preparation options has been effectively targeted by manufacturers of cooking sauces.

New Flavours and Cuisines

Consumers are looking for a greater variety of products in order to change their meal portfolio. This has created the opportunity for suppliers to persuade consumers to trade up. For example, in 2006, Sharwood’s introduced a premium range of cooking sauces from Sri Lanka, Nepal and Malaysia. In addition, Patak’s introduced a range of regional recipe sauces.

As consumers have become more familiar with classic, established recipes, some are looking to trade up to more authentic products. These consumers are looking for something different, but they are anxious to remain within particular cuisines. As such, they might choose to opt for a pesto sauce rather than a tomato-based standard recipe.

Key Note Ltd 2006 4

Cooking Sauces & Food Seasonings Market Definition

Provenance

Provenance is gaining increasing importance in the food market as a whole. Consumers want some reassurance, not only about recipes but also about the ingredients, to confirm quality and authenticity. A further aspect of this has been expertise, with more suppliers offering products made in the recipe’s country of origin. For example, Sacla has launched a range of Classic Italian sauces made in Italy. In addition, consumers may look to media cookery shows that specify recipes and regionality, such as Jamie’s Italy. However, this is simpler for some cuisines than for others.

Packaging

Glass jars have taken the lead in packaging formats, as consumers are able to view contents easily while meeting safety and hygiene requirements, but there has been some development in pouch formats, particularly for ethnic recipes. Brands such as Amoy offer wet sauces in this format, often for smaller-serve products. It is easier to include this type of smaller product alongside items such as noodles in-store to prompt consumers to think in terms of meal solutions.

Retailer Activity

In the ethnic cuisines market, there has been particular activity on the part of retailers. For example, ASDA has created a new ‘ethnic manager’ role to ensure the continuous development of this category. In addition, Somerfield and Kwik Save have commented on the need to develop products for a wider consumer base, particularly in multicultural areas such as Birmingham, Bradford and key parts of London.

Healthy Eating

Healthy eating remains an important driver across the food market as a whole. The Government has prioritised the need to educate consumers on healthy-eating issues, and 2005/2006 saw particular activity relating to salt and food labelling (see Chapter 7 — Current Issues).

In 2005, the Government specifically targeted salt reduction with advertising featuring the Sid the Slug character. This was followed up with a campaign urging consumers to read ingredient labels on processed foods to find out about salt levels. At the same time, suppliers have been in talks with the Food Standards Agency (FSA) about salt levels in foods and specific targets for reduction have been set.

The introduction of clearer nutritional labelling on foods has already started to have an impact, with reports of falling sales of certain foods with higher fat, sugar or salt levels (see Chapter 7 — Current Issues). As consumers are beginning to act on this advice, suppliers are having to be more exacting in developing new products.

Key Note Ltd 2006 5

Cooking Sauces & Food Seasonings Market Definition

Barbecue Opportunities

The summer months can see a deterioration in sales of cooking sauces, as consumers opt for lighter and cold meals. However, the growth in outdoor eating, and barbecues in particular, has been effectively targeted by suppliers.

The rise of the barbecue market has been particularly important for marinades. As barbecue occasions have become more common, there has been a trading up from barbecue sauces to more exotic flavours, such as Chinese, Thai and Indian. Brands such as Nando’s have benefited from this trend. According to The Grocery Company Ltd, which distributes the brand, ‘consumers are happy to spend more on barbecuing because it is considered the new dinner party. Dining outside is seen as exciting’.

Brands such as Discovery Foods have also been targeting this market, encouraging consumers to use cooking sauces as well as condiments. However, the company has commented that it is difficult to educate consumers and get them to experiment, as it can be difficult to promote in-store.

Some brands, such as Kikkoman, have invested in television advertising. The company’s Teriyaki marinade gained exposure through television commercials from May 2006.

ECONOMIC TRENDS

Gross Domestic Product

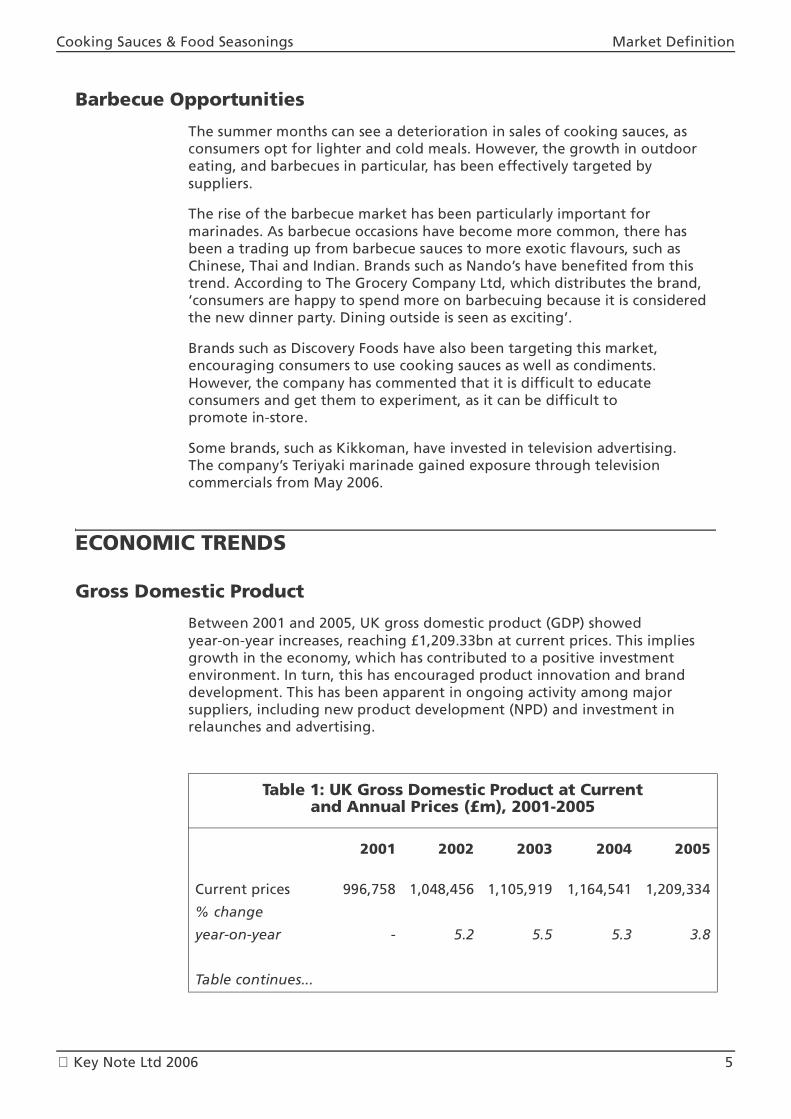

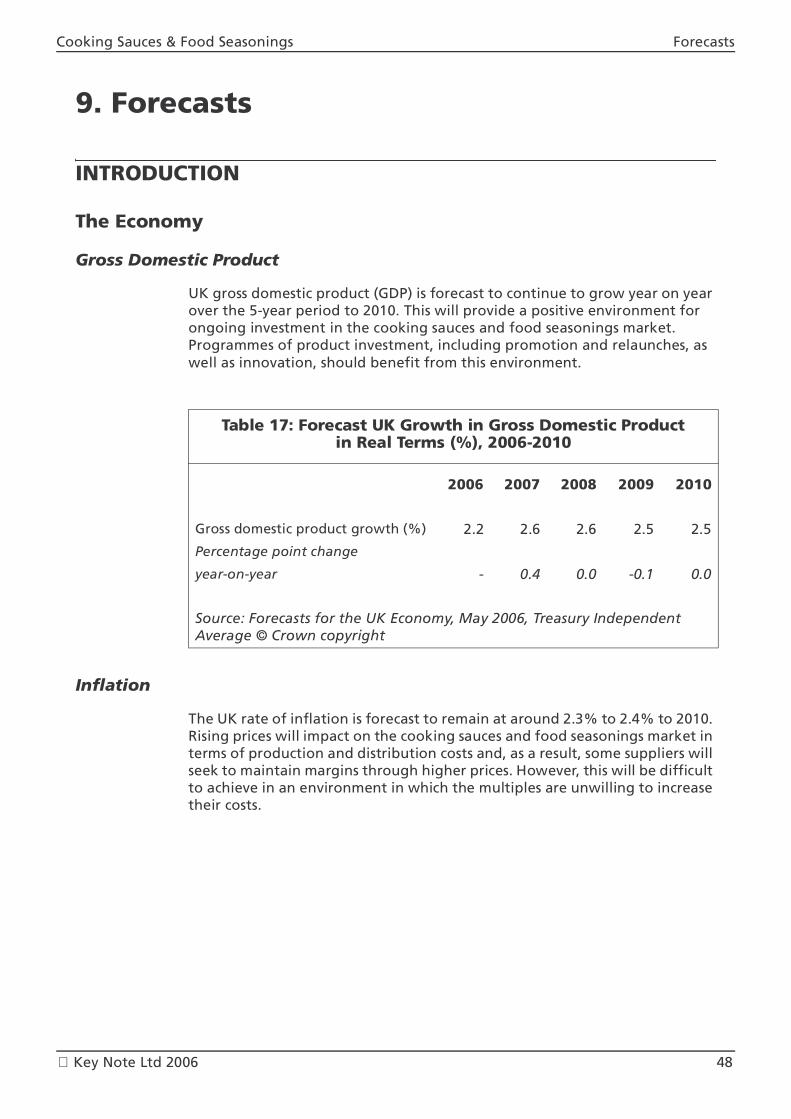

Between 2001 and 2005, UK gross domestic product (GDP) showed year-on-year increases, reaching £1,209.33bn at current prices. This implies growth in the economy, which has contributed to a positive investment environment. In turn, this has encouraged product innovation and brand development. This has been apparent in ongoing activity among major suppliers, including new product development (NPD) and investment in relaunches and advertising.

Table 1: UK Gross Domestic Product at Current and Annual Prices (£m), 2001-2005

2001 2002 2003 2004 2005

Current prices 996,758 1,048,456 1,105,919 1,164,541 1,209,334

% change

year-on-year - 5.2 5.5 5.3 3.8

Table continues...

Key Note Ltd 2006 6

Cooking Sauces & Food Seasonings Market Definition

Inflation

The UK rate of inflation has remained very low since the late 1990s. In fact, household disposable income levels (see Table 3) have been growing at a faster rate, meaning that consumers have been able to stretch their income further and purchase more in terms of volume or value items. This has been one of the factors behind higher spending in the food market as a whole.

...table continued

2001 2002 2003 2004 2005

Annual chain-linked

GDP 1,027,905 1,048,456 1,074,858 1,108,464 1,128,680

% change

year-on-year - 2.0 2.5 3.1 1.8

GDP — gross domestic product

Source: National Accounts, Main Aggregates 1948-2005, National Statistics website © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Table 1: UK Gross Domestic Product at Current and Annual Prices (£m), 2001-2005

Table 2: UK Rate of Inflation (%), 2001-2005

2001 2002 2003 2004 2005

Inflation (%) 1.8 1.6 2.9 3.0 2.8

Percentage point

change year-on-year - -0.2 1.3 0.1 -0.2

Note: inflation is at retail price index (RPI).

Source: Monthly Digest, May 2006, National Statistics website © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Key Note Ltd 2006 7

Cooking Sauces & Food Seasonings Market Definition

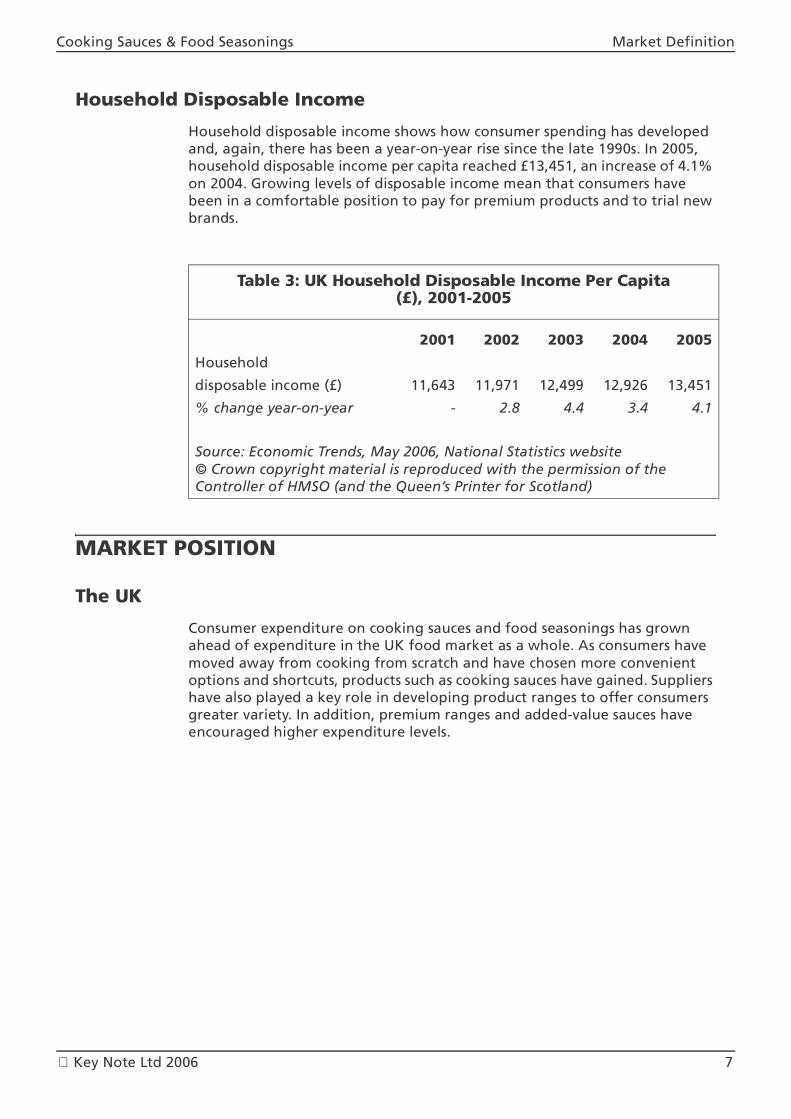

Household Disposable Income

Household disposable income shows how consumer spending has developed and, again, there has been a year-on-year rise since the late 1990s. In 2005, household disposable income per capita reached £13,451, an increase of 4.1% on 2004. Growing levels of disposable income mean that consumers have been in a comfortable position to pay for premium products and to trial new brands.

MARKET POSITION

The UK

Consumer expenditure on cooking sauces and food seasonings has grown ahead of expenditure in the UK food market as a whole. As consumers have moved away from cooking from scratch and have chosen more convenient options and shortcuts, products such as cooking sauces have gained. Suppliers have also played a key role in developing product ranges to offer consumers greater variety. In addition, premium ranges and added-value sauces have encouraged higher expenditure levels.

Table 3: UK Household Disposable Income Per Capita (£), 2001-2005

2001 2002 2003 2004 2005

Household

disposable income (£) 11,643 11,971 12,499 12,926 13,451

% change year-on-year - 2.8 4.4 3.4 4.1

Source: Economic Trends, May 2006, National Statistics website © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Key Note Ltd 2006 8

Cooking Sauces & Food Seasonings Market Definition

Table 4: Consumer Expenditure on Food, Cooking Sauces and Food Seasonings (index 2001=100), 2001-2005

Consumer Expenditure on

Consumer Expenditure Cooking Sauces and on Food Food Seasonings

2001 100 100

2002 103 103

2003 105 106

2004 107 109

2005 111 114

Source: National Statistics © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)/Key Note

Figure 1: Consumer Expenditure on Food, Cooking Sauces and Food Seasonings (index 2001=100), 2001-2005

Source: National Statistics © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)/Key Note

100

102

104

106

108

110

112

114

2001 2002 2003 2004 2005

Food

Cooking sauces and foodseasonings

Key Note Ltd 2006 9

Cooking Sauces & Food Seasonings Market Size

2. Market Size

THE TOTAL MARKET

The total UK cooking sauces and food seasonings market has managed to achieve growth ahead of inflation since 2001. This is largely attributable to the gains made in the cooking sauces sector, as sales of food seasonings have tended to stagnate.

The cooking sauces sector is beginning to mature and has a high level of consumer penetration. Many brands are centred on the middle market tier, and this has been the focus of price-based competition. Retailer policies focused on offering everyday low pricing have also been an issue in driving and keeping prices down. This has been exacerbated by ‘buy one, get one free’ (BOGOF) promotions, which may have led some consumers to stockpile at lower prices. This has countered the effects of a shift towards more premium recipes by some brands and has acted to depress potential market increases.

In 2005, the total UK cooking sauces and food seasonings market was worth £570m at retail selling prices (rsp), a rise of 4% on 2004. Between 2001 and 2005, the market grew by 13.8%. (It should be noted that the data in this report have been revised in line with the latest trade estimates.)

Table 5: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices

(£m at rsp), 2001-2005

2001 2002 2003 2004 2005

Cooking sauces 416 432 443 459 480

Food seasonings 85 86 88 89 90

Total 501 518 531 548 570

% change year-on-year - 3.4 2.5 3.2 4.0

rsp — retail selling prices

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

Key Note Ltd 2006 10

Cooking Sauces & Food Seasonings Market Size

BY MARKET SECTOR

Cooking sauces is the largest sector of the market, accounting for 84.2% of the total value in 2005.

Figure 2: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices

(£m at rsp), 2001-2005

rsp — retail selling prices

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

0

100

200

300

400

500

600

2001 2002 2003 2004 2005

Food seasonings

Cooking sauces

Key Note Ltd 2006 11

Cooking Sauces & Food Seasonings Market Size

Cooking Sauces

The cooking sauces sector comprises three main types:

• cook-in sauce — where foods are cooked in the sauce, e.g. stir-fry sauces

• pasta sauce — for use with pasta, e.g. bolognese or carbonara sauces

• pour-over sauce — where the sauce is poured over once the main ingredients have cooked, e.g. a red-wine sauce to be served with steak.

In addition to these, dry sauces can be mixed with water before using, and marinades are pastes and sauces that are used to coat meats and vegetables before cooking.

The cooking sauces sector has maintained growth in real terms since 2001. Although some subsectors are maturing, new product development (NPD) is ongoing and has been effective in targeting higher spending on some products. Much of the activity in the sector has centred on encouraging consumers to trade up.

In 2005, the cooking sauces sector was worth £480m at rsp, a rise of 4.6% on 2004 (see Table 6).

Figure 3: The Total UK Cooking Sauces and Food Seasonings Market by Sector by Value at Current Prices (%), 2005

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

Food seasonings15.8%

Cooking sauces84.2%

Key Note Ltd 2006 12

Cooking Sauces & Food Seasonings Market Size

According to Napolina, there are two main price points for ambient sauces — standard sauces retail at around the £1 mark, and premium sauces range from £1.49 to £1.70. It is anticipated that breaking the £2 mark will move the sector upmarket, with factors such as organics, healthy eating and premium ingredients all viewed as routes to achieving this.

The sector is aided by changing attitudes towards cooking and food preparation. With the amount of time spent preparing meals falling, options that offer simplicity and ease of preparation, such as cooking sauces, are seen as being vital by many households.

Pasta Sauces

The ambient wet cooking sauces sector is led by Italian pasta sauces, with brands such as Dolmio and Bertolli. These sauces are very easily combined with pasta to offer quick meals. The introduction of ‘with pasta’ products for the microwave has added further value to the market. Many consumers are looking at a window of less than half an hour to prepare meals, and pasta and sauce dishes fit this well.

Value-added activity has included the addition of vegetables, targeting consumer interest in healthy eating and offering a more complete meal solution. Increased authenticity has also been a factor. For example, the Loyd Grossman range of pesto sauces are made with traditional methods in Tuscany. This type of quality might push consumers upmarket.

The Italian sector also gains from substantial promotional investment. The major brands, led by Dolmio, keep these sauces in the public eye.

Table 6: The UK Cooking Sauces Sector by Value at Current Prices (£m at rsp), 2001-2005

2001 2002 2003 2004 2005

Value (£m) 416 432 443 459 480

% change year-on-year - 3.8 2.5 3.6 4.6

Sector share of total market (%) 83.0 83.4 83.4 83.8 84.2

rsp — retail selling prices

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

Key Note Ltd 2006 13

Cooking Sauces & Food Seasonings Market Size

Indian Sauces

Indian sauces are ranked second in the wet-sauces category. Suppliers such as Patak’s have been gearing recent product development towards more regional recipes. As consumers have become more educated in classic restaurant and takeaway-inspired recipes, they are becoming more adventurous. At the same time, the use of more authentic ingredients and specialised dishes offers the opportunity to trade up.

Chinese and Oriental Sauces

The oriental sauces subsector is seeing similar developments, with more regional offerings. This is evident across the entire product portfolio, including ready meals and accompaniments. Occasions such as Chinese New Year act as an ideal focus for promotional activity. In addition, suppliers are looking to events such as the Beijing Olympics to place a further spotlight on Chinese cuisine.

British Recipes

British recipes also form an important segment, with brands such as Homepride in the wet-sauces category and Colman’s in dry packet sauces. The revival of interest in traditional British dishes — engendered by media interest, including cookery books and television programmes such as Gary Rhodes’ Great British Classics and Rick Stein’s Food Heroes — has played a part. Although consumers watch such recipes being made from scratch as entertainment, they are happy to opt for shortcuts when it comes to preparing their own.

Many British-inspired recipes have a major presence in the pour-over sauces sector, including packet mixes, although these have lost ground to wet products.

Other Cuisines

Other cuisines that are making headway include Mexican, with television advertising by brands such as Old El Paso adding a focus. Thai is often listed alongside Chinese recipes and is gaining ground as an increasing number of restaurants offer ‘classics’, such as red and green curries. Malaysian, Korean and Jamaican sauces are also beginning to gain wider distribution.

Chilled Sauces

There has also been some development in chilled sauces. These products, which tend to centre on retailer own-brand offerings, are generally premium priced, tying with their added convenience and fresh positioning. Brands include New Covent Garden and Marks & Spencer’s Cook!. Patak’s also introduced a chilled range in 2005. Products in this category still account for a minority of sales, at around 10%, but chilled remains one of the fastest-growing sectors of the market.

Key Note Ltd 2006 14

Cooking Sauces & Food Seasonings Market Size

Food Seasonings

Food seasonings comprise primary products, such as salt, pepper, herbs and spices, that are used to flavour food in cooking.

There has been very limited growth in the food seasonings sector since 2001. A major factor in this has been the shift towards more convenient food options and away from cooking from scratch. The relatively long home life of dried products, in particular, has meant that they are not replenished often and have been phased out in some households.

Other factors affecting the sector include the following:

• the growing number of smaller households without the need or desire to cook from ingredients

• a rise in the number of meals taken outside the home

• the introduction of more meal kits, and other shortcuts and conveniences.

The food seasonings sector was worth £90m at rsp in 2005, an increase of 1.1% on 2004.

Salt

In the salt category, the most significant developments have been in sea and rock salt. The low-sodium sector has also made gains as a result of government activity encouraging consumers to reduce their salt intake. Although salt suppliers have been affected by such campaigning, the bulk of the reduction is being targeted on salt contained in processed foods.

Table 7: The UK Food Seasonings Sector by Value at Current Prices (£m at rsp), 2001-2005

2001 2002 2003 2004 2005

Value (£m) 85 86 88 89 90

% change year-on-year - 1.2 2.3 1.1 1.1

Sector share of total market (%) 17.0 16.6 16.6 16.2 15.8

rsp — retail selling prices

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

Key Note Ltd 2006 15

Cooking Sauces & Food Seasonings Market Size

Herbs

The dried herbs subsector has also suffered from the development of fresh products that have gained greater distribution at retail level. The branded presence of suppliers such as Schwartz and Barts has come under increasing pressure from retailer own labels. This has challenged not only price levels, but also in-store space.

Spices

Growth within the spices category tends to be focused on products such as preblended seasoning mixes and spice kits. For example, in the ethnic foods market, there has been a shift away from basic ‘curry powders’ towards recipe-specific blends, such as Rogan Josh. This move addresses more adventurous, but still fairly cautious, consumers.

Key Note Ltd 2006 16

Cooking Sauces & Food Seasonings Industry Background

3. Industry Background

RECENT HISTORY

The total UK cooking sauces and food seasonings market has developed strongly since the 1990s, driven by consumer demand for convenient products. This trend has been boosted not only by ‘time-poor, cash-rich’ purchasers, but also by those who do not have the knowledge or confidence to cook from scratch.

The basis for market development was the increasingly international UK food palate. With an established international restaurant and takeaway base, consumers were eager to extend their in-home meal repertoire in line with their eating-out experiences. While ready meals provided one route, the need to supply family meals was a more important factor in the development of cooking sauces, and brands such as Chicken Tonight emerged.

The shift towards a shorter food-preparation period also drove the rise in the Italian foods market, led by pasta and associated products. The entry and investment of major brands, such as Dolmio, did much to target and grow this demand.

With a number of major brands now competing in the market, pricing has become increasingly competitive. As a result, suppliers are looking to add further product differentials to avoid a price focus. This has given rise to growth in the premium market, with more sophisticated recipes and authentic ingredients.

NUMBER OF COMPANIES

There are no separate statistics available for cooking sauce and food seasoning manufacturers to gauge the scale of the market. As such, this market must be examined in the context of the food industry as a whole.

The food manufacturing industry in the UK comprises more than 6,000 companies. These vary greatly in size and include some of the largest, as well as the smallest, businesses in the country. As the food industry is made up of such a wide range of products, there is scope for many different types of business to operate.

The largest companies tend to be national operators, which are in a position to support their brand portfolio or supply retailer own-label products nationally. Smaller groups might specialise in terms of product type or confine their activities to local geographic markets.

In 2005, there were 6,310 UK VAT-based enterprises engaged in the manufacture of food and beverages. Of these, 33.8% had turnovers of £1m or more. The single largest category was enterprises with turnovers of between £100,000 and £249,000, which accounted for 20.6% of the total in 2005 (see Table 8).

Key Note Ltd 2006 17

Cooking Sauces & Food Seasonings Industry Background

EMPLOYMENT

The food industry is a major employer in the UK, with a large number of businesses involved in the market. For the most part, enterprises tend to be relatively small in terms of the number employed — in 2005, 58.9% of UK VAT-based enterprises engaged in the manufacture of food and beverages employed fewer than ten people (see Table 9). This is to be expected, given that many products are batch processed and, as a result, the manufacture of food tends to be capital intensive.

Table 8: Number of UK VAT-Based Enterprises Engaged in the Manufacture of Food and Beverages by Turnover Sizeband

(number and %), 2005

Number of Enterprises % of Total

Turnover Sizeband (£000)

0 -49 600 9.5

50-99 800 12.7

100-249 1,300 20.6

250-499 840 13.3

500-999 640 10.1

1,000-4,999 1,125 17.8

5,000+ 1,005 15.9

Total 6,310 †100.0

† — does not sum due to rounding

Source: UK Business: Activity, Size and Location 2005, National Statistics © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Key Note Ltd 2006 18

Cooking Sauces & Food Seasonings Industry Background

REGIONAL VARIATIONS IN THE MARKETPLACE

The cooking sauces and food seasonings market has limited regional variation. Strong brands and lines of distribution mean that the more prominent brands are nationally distributed through the grocery network. However, differences in population can mean that cities, for example, with international populations, are more likely to see specialist outlets for particular nationalities. In addition, the multiples have started to target in-store product offerings at local markets, which might also include more global foods.

Table 9: Number of UK VAT-Based Enterprises Engaged in the Manufacture of Food and Beverages by Employment Sizeband

(number and %), 2005

Number of Enterprises % of Total

Number of Employees

0-4 2,585 41.1

5-9 1,120 17.8

10-19 785 12.5

20-49 825 13.1

50-99 380 6.0

100-249 320 5.1

250+ 275 4.4

Total 6,290 100.0

Source: UK Business: Activity, Size and Location 2005, National Statistics © Crown copyright material is reproduced with the permission of the Controller of HMSO (and the Queen’s Printer for Scotland)

Key Note Ltd 2006 19

Cooking Sauces & Food Seasonings Industry Background

DISTRIBUTION

The distribution of cooking sauces and food seasonings is dominated by the major grocery multiples. Not only are these retailers able to offer a fuller range of products to consumers, but they have also been active in developing their own brands and products in the sector. The retailer own-label sector has evolved with a more tiered offering, including the following:

• value

• standard

• premium

• healthy eating.

This has contributed to differentiation in the market, with accompanying variations in price points and product offerings.

Independents and other outlets offer a narrower range of branded, as well as wholesaler-label, products. The restrictions on space in these outlets mean that the offerings centre on ambient items, with little scope for chilled sauces.

Specialist grocers, such as delicatessens and ethnic supermarkets, tend to have a much wider offering of both sauces and seasonings to cater for their clientele.

In 2005, grocery multiples accounted for the majority (87%) of retail sales of cooking sauces and food seasonings.

Table 10: Retail Sales of Cooking Sauces and Food Seasonings by Distribution Channel by Value (%), 2005

Grocery multiples 87

Independent grocers and co-operatives 9

Others 4

Total 100

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

Key Note Ltd 2006 20

Cooking Sauces & Food Seasonings Industry Background

HOW ROBUST IS THE MARKET?

The cooking sauces and food seasonings market is relatively robust, with a large number of brands and suppliers. As with many other food markets, a major potential threat is that of food scares. The sector weathered concerns surrounding Sudan 1 in 2005 relatively well (see Chapter 7 — Current Issues), indicating the level of stability in the market.

LEGISLATION

As part of the food and retail market, suppliers of cooking sauces and food seasonings are subject to a wide range of legislation in a number of areas. The list below is taken from Food Law (www.food.gov.uk) in June 2004. In cases where regulations specify England there is often equivalent regulation for Scotland and Wales.

• Trade Descriptions Act 1968

• Consumer Protection Act 1987

• Materials and Articles in Contact with Food Regulations 1987

• Weights & Measures Act 1988

Figure 4: Retail Sales of Cooking Sauces and Food Seasonings by Distribution Channel by Value (%), 2005

Source: Key Note

Want more detail? Order further customised analysis through IRN Research on [email protected]. See Further Sources for more on this service.

Independent grocers and

co-operatives9%

Others4%

Grocery multiples87%

Key Note Ltd 2006 21

Cooking Sauces & Food Seasonings Industry Background

• Food Safety Act 1990

• Flavourings in Food Regulations 1992

• Food Additives Regulations 1992

• General Product Safety Regulations 1994

• Colours in Food Regulations 1995 and amendments: 2000 and 2001

• Miscellaneous Food Additive Regulations and amendments: 1995, 1999, 2001 and 2003

• Sweeteners in Food Regulations 1995 and amendments: 1996, 1997, 1999, 2001, 2002 and 2003

• Food Labelling Regulations 1996

• Food (Lot Marking) Regulations 1996

• Food Premises Registration (Amendment) Regulations 1997

• Imported Food Regulations 1997

• Food Standards Act 1999

• Organic Products Regulations 2001

• Contaminants in Food (England) Regulations 2003

• Organic Products (Imports from Third Countries) Regulations 2003.

KEY TRADE ASSOCIATIONS

Food and Drink Federation

The Food and Drink Federation (FDF) represents the UK food and drink manufacturing industry.

The Federation helps its members to operate in an appropriately regulated marketplace, in order to maximise their competitiveness. The FDF communicates industry values and concerns to a range of audiences in the UK and abroad, including the Government, regulators, consumers and the media. In addition, it works in partnership with other major players in the food chain to help ensure that food is safe and that consumers can have confidence in it. Members include both large and small food and drink manufacturing companies, and trade associations dealing with specific food and drink sectors.

Key Note Ltd 2006 22

Cooking Sauces & Food Seasonings Industry Background

Salt Manufacturers’ Association

The Salt Manufacturers’ Association (SMA) is the trade association representing UK manufacturers of salt for domestic, catering, water-softening, industrial and de-icing uses.

The Association supports its members by:

• representing the views and objectives of the salt industry to relevant government and international organisations

• providing a forum where members can exchange knowledge and scientific information on research, legislation, diet and nutrition, technical training, and health and safety issues

• promoting balanced exposure for scientific research on salt and human health.

The SMA is a member of the European Salt Producers’ Association (ESPA) and subscribes to its code of practice, which promotes responsible care with the participation of employees, customers, users and communities. Concern for health, safety, environmental and quality issues forms an integral part of its business policy.

Seasoning and Spice Association

The mission of the Seasoning and Spice Association (SSA) is to be the leading voice of the UK food seasonings and spice industry in the interests of members, food manufacturers and consumers.

The SSA’s principal objective is to promote and protect the interests of its members in all matters relating to the trade in, and processing, marketing and distribution of, seasonings, herbs and spices, and similar products.

Key Note Ltd 2006 23

Cooking Sauces & Food Seasonings Competitor Analysis

4. Competitor Analysis

THE MARKETPLACE

The cooking sauces and food seasonings market is supplied by a diverse range of companies. With the drive for diversity and authenticity, there is scope for a number of smaller brands, including international names that might gain distribution through importers and distributors. However, the mass market is primarily catered for by the larger labels, such as Dolmio, Uncle Ben’s and others. Retailer own brands also take an important role, as with many other food markets.

MARKET LEADERS

Campbell’s UK Ltd

Company Structure

Campbell’s UK Ltd is a subsidiary of the US-based company most famous for its soup. Brands owned by the group that are relevant to the cooking sauces and food seasonings market include Oxo stock and Homepride cooking sauces. In March 2006, Campbell’s announced that it would consider selling its UK and Republic of Ireland businesses following a strategic review of its international assets. This would include brands such as Oxo and Homepride. In July 2006, Premier Foods bought the businesses for £450m.

Current and Future Developments

In September 2005, Homepride announced the introduction of five new varieties in its traditional cooking sauces jar range. The new varieties included: Creamy Stroganoff, Cheese Vegetable Bake, Smokey Barbecue and Fish Pie. The range was launched in September 2004.

Financial Results

In the year ending 31st July 2005, Campbell’s UK Ltd recorded a pre-tax profit of £3.5m on a turnover of £23,000. In the previous year, the company made a pre-tax profit of £13.9m.

Key Note Ltd 2006 24

Cooking Sauces & Food Seasonings Competitor Analysis

G Costa and Co Ltd

Company Structure

G Costa & Co Ltd imports and distributes fine foods, and supplies a range of retail food products under the Blue Dragon brand. The brand focuses on oriental foods. Other brands supplied by the group include Nong Shim, Maille and Tabasco.

Current and Future Developments

New products in the Blue Dragon range in 2005 included a Vietnamese meal kit and noodle products.

Financial Results

In the year ending 17th September 2005, turnover for G Costa and Co Ltd was £47.3m, a rise of 48.1% on 2004. The company made a pre-tax profit of £612,000 in 2005, compared with a pre-tax profit of £2m in 2004.

Discovery Foods Ltd

Company Structure

Discovery Foods Ltd, which is a family owned company, supplies mainly Mexican and US (e.g. Cajun) food products. The range includes dinner kits, seasonings and cooking sauces.

Current and Future Developments

Discovery Foods introduced two-step sauces from 2006. The Cajun Chicken, Chilli Con Carne and Fajita variants aimed to create stronger flavours, which are more commonly found in Mexican cooking.

Financial Results

Discovery Foods Ltd recorded a turnover of £32.1m and a pre-tax profit of £716,000 in the year ending 31st October 2004. This compares with a turnover of £28.5m and a pre-tax profit of £1.1m in 2003.

General Mills UK Ltd

Company Structure

General Mills UK Ltd supplies a wide range of food products, including the Old El Paso Mexican range.

Key Note Ltd 2006 25

Cooking Sauces & Food Seasonings Competitor Analysis

Current and Future Developments

In July 2006, the Old El Paso brand announced a revamp. Three new sauces were added to the range: Roasted Garlic & Chilli; Hot Chilli Con Carne; and Smoked Chilli & Sweet Peppers. The three existing sauces were reformulated to offer more ‘robust and authentic’ flavours. A new look, slimmer jar was also introduced and the brand will be supported with an advertising spend of £5m.

The Old El Paso brand was extended into grated cheese in 2006. The speciality blend of cheddar and mozzarella, Jalapeno peppers, red and green peppers, and capsicum seeds was developed following research indicating a gap in the market for cheese for specific eating occasions.

Financial Results

In the year ending 30th April 2005, turnover for General Mills UK Ltd was £136.5m, a decrease of 11.6% on 2004. Pre-tax profit fell by 9.7%, to £2.6m.

HP Foods Ltd

Company Structure

In February 2006, the Competition Commission provisionally cleared HJ Heinz’s £470m takeover of the HP Foods Group, which was previously owned by Groupe Danone. HP Foods Ltd supplies the Amoy brand, as well as Lea & Perrins Worcestershire sauce and the Rajah range of herbs and spices.

Current and Future Developments

In October 2005, Amoy announced the introduction of a premium soy sauce, seeking a similar positioning to balsamic vinegar in the vinegar market. Amoy Premium Soy Sauce is fermented from the first pressing of the soy bean, offering extra flavour. The packaging has a more contemporary feel, with a black glass bottle with square shoulders to stand out from the shelf.

Amoy Stir Fry Sensations were also introduced in 2005. Eight recipes were offered, packaged in clear plastic sachets with an outer card sleeve.

The Rajah Indian brand saw the addition of a ready meals offering in 2006. This formed part of the planned extension of the brand. The dishes are available in 300-gram (g) ambient pouches.

Financial Results

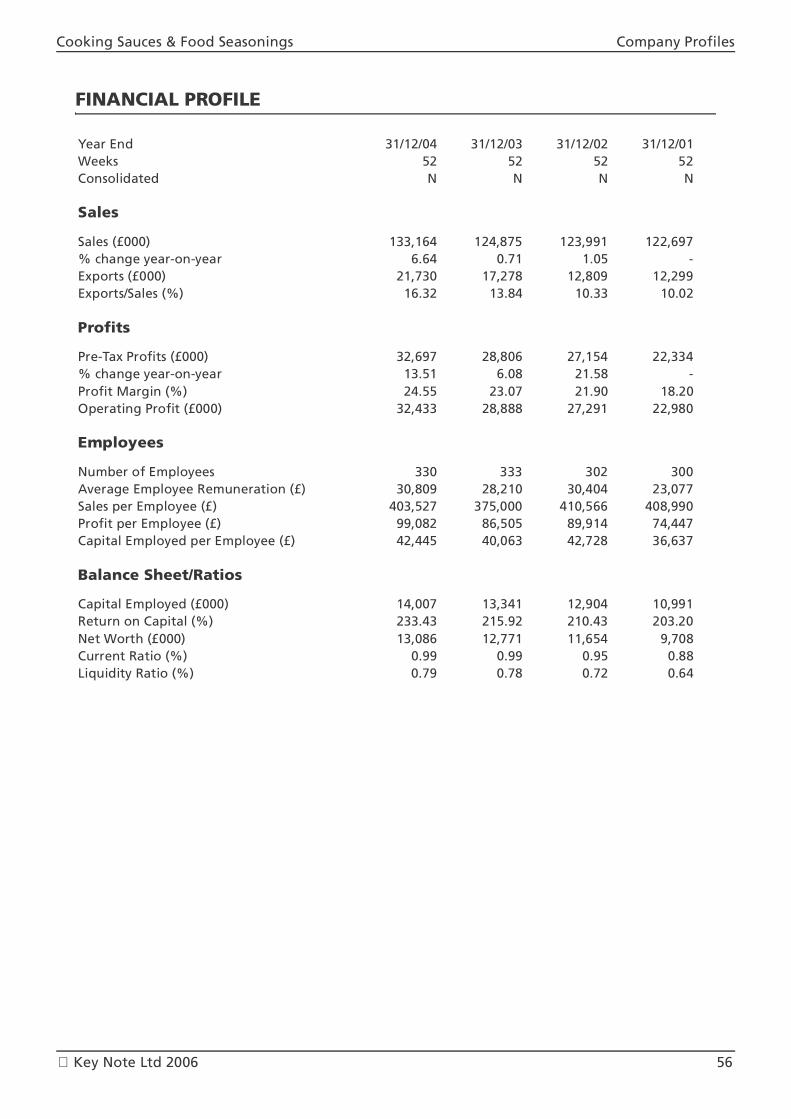

In the year ending 31st December 2004, HP Foods Ltd made a pre-tax profit of £32.7m on a turnover of £133.2m. This compares with a pre-tax profit of £28.8m on a turnover of £124.9m in 2003.

Key Note Ltd 2006 26

Cooking Sauces & Food Seasonings Competitor Analysis

JFC (UK) Ltd

Company Structure

JFC (UK) Ltd supplies the Kikkoman brand. The company is part of the Japan-based Kikkoman Corporation, which is the world’s largest producer of soy sauce.

Current and Future Developments

During 2005/2006, JFC invested in television advertising for the Kikkoman brand, as well as in-store activity.

Financial Results

In the year ending 31st December 2004, JFC (UK) Ltd recorded a turnover of £8m, a rise of 14.6% on 2003. The company made a pre-tax profit of £410,000 in 2004, compared with a pre-tax profit of £274,000 in 2003.

Mars UK Ltd

Company Structure

Mars UK Ltd is a widely based food group in US ownership. In the cooking sauces sector, its brands include Dolmio and Uncle Ben’s.

Current and Future Developments

From March 2005, Dolmio Chunky sauces — pasta sauces with additional chunks of vegetables — were introduced. The initial offering comprised Chunky Mediterranean Vegetables, Chunky Onion & Garlic, Chunky Mushroom & Courgette and Chunky Sweet Pepper. The tomato-based variants are colour coded to give shelf standout.

My Dolmio, an ambient range of sauces, was launched in May 2006. The range of pasta sauces and pastas target 8 to 12 year-olds, and come in easy-pour pouches for microwave cooking. The company commented that households with children were responsible for growth in the cooking sauces market, and that parents were increasingly looking for products designed specifically for children.

The Dolmio sauce range was revamped in 2006. Changes included a new logo in a leaf shape, incorporating the brand’s signature colour green.

Financial Results

Mars UK Ltd recorded a turnover of £1.56bn and a pre-tax profit of £171.5m in the 53 weeks ending 1st January 2005. This compares with a turnover of £1.55bn and a pre-tax profit of £146.1m in the year ending 27th December 2003.

Key Note Ltd 2006 27

Cooking Sauces & Food Seasonings Competitor Analysis

McCormick (UK) Ltd

Company Structure

McCormick (UK) Ltd, which is owned by the US-based McCormick & Co Inc, is the leader in the UK branded-seasonings market, with its Schwartz range of dried herbs and spices, and Real Pastes.

Current and Future Developments

Schwartz remains the leading player in the dried-seasonings market.

Six new Schwartz Shotz products were introduced in 2005. The products comprise blends of seasonings for added convenience and target less-experienced cooks.

Financial Results

In the year ending 30th November 2005, turnover for McCormick (UK) Ltd decreased by 3.4%, to £144.6m. The company made a pre-tax loss of £3m in 2005, compared with a pre-tax loss of £685,000 in 2004.

Premier International Foods UK Ltd

Company Structure

Premier International Foods UK Ltd supplies a range of foods, including the Loyd Grossman cooking sauces brand. The company acquired further brands, including Homepride, with the acquisition of Campbell’s UK and Republic of Ireland businesses in 2006.

Current and Future Developments

At the beginning of 2005, the Food Standards Agency (FSA) advised retailers and food manufacturers to withdraw from sale any products that may have contained Worcester sauce supplied to them from a specific batch manufactured by Premier Foods. This followed a Quality Assurance check, which revealed the presence of Sudan 1 in Worcester sauce, through the contamination of a batch of chilli powder. Sudan 1 is a colourant, which is not permitted for use in food products (see Chapter 7 — Current Issues).

During 2005, four creamy recipe sauces were added to the Loyd Grossman portfolio: Carbonara with Pancetta; Tomato & Mascarpone with Vodka; Porcini Mushroom with Amontillado Sherry; and Béchamel Sauce for Lasagne. Green and red pestos made in Tuscany using traditional methods were added to the Loyd Grossman range in 2006.

The Loyd Grossman range also saw the addition of Tomato, Green Olive and Roasted Red Chilli cooking sauce from April 2006. The aim of the seasonal aspect was to target more adventurous consumers seeking to try new flavours. For autumn 2005, the seasonal introduction was Tomato & Chargrilled Courgette.

Key Note Ltd 2006 28

Cooking Sauces & Food Seasonings Competitor Analysis

Financial Results

In the year ending 31st December 2004, turnover for Premier International Foods UK Ltd was £140.4m, a decrease of 1.8% on 2003. The company made a pre-tax profit of £28m in 2004, compared with a pre-tax profit of £26.1m in 2003.

RHM PLC

Company Structure

RHM PLC operates in a number of food sectors, including cooking sauces through its Sharwood’s brand. The company also supplies the Cerebos salt brand.

RHM was floated on the stock exchange in July 2005. In initial trading, around 63% of shares were sold to corporate investors, with the remainder of the business continuing to be owned by private equity firm Doughty Hanson.

Current and Future Developments

In March 2005, RHM announced a restructure from four business groupings into three. The new units are: Cake and Customer Partnerships; Culinary Brands (including Sharwood’s, Bisto, etc.); and Bread Bakeries.

During 2005, Sharwood’s introduced a range of products targeting the barbecue market. Sharwood’s Grill, BBQ or Bake sauces targeted summer eating and were introduced from May. Four flavours were introduced: Thai Sweet Chilli & Herb; Tandoori; Chinese BBQ; and Spicy Mango. The sauce can be brushed on to meat or vegetables before cooking and does not require marinading. The products also target lighter eating occasions.