controlling in the wood products industry - boku · z.b. tanz der vampire 3310512 profit center...

TRANSCRIPT

Controlling in the Wood Products Industry

SS 2016 Albert Sickl

26/2/2016 2

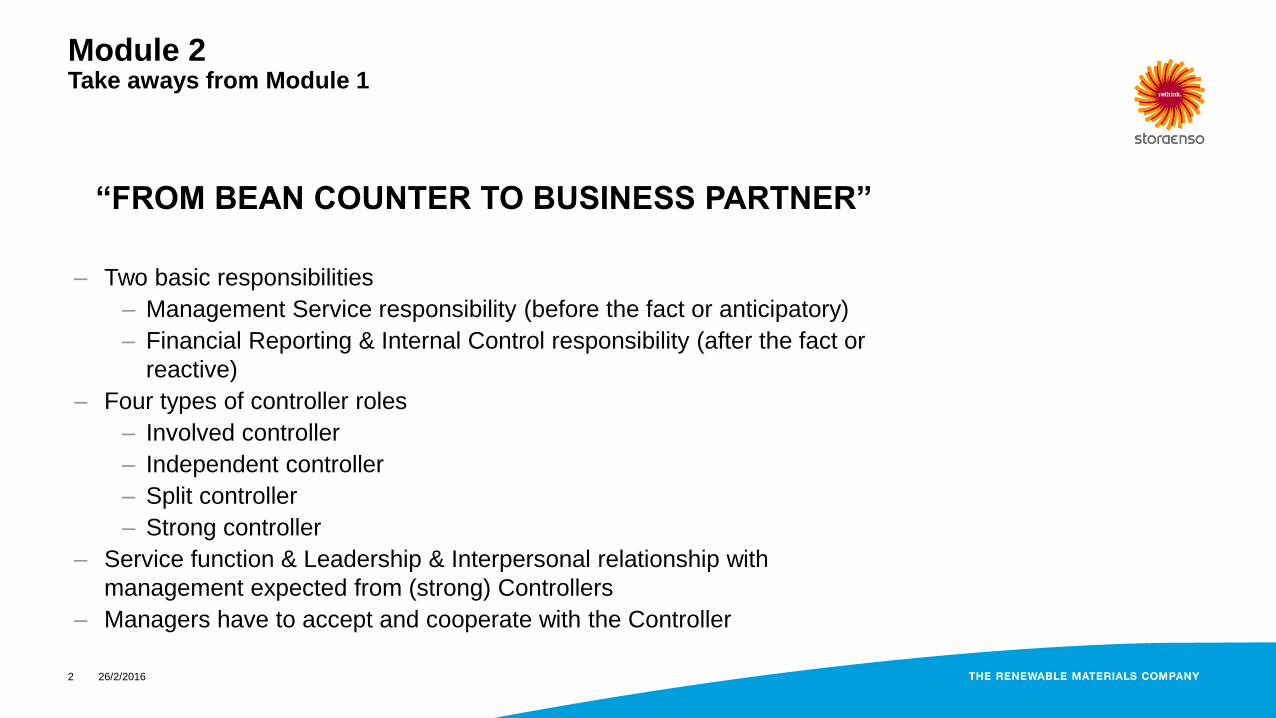

Module 2 Take aways from Module 1

“FROM BEAN COUNTER TO BUSINESS PARTNER”

– Two basic responsibilities

– Management Service responsibility (before the fact or anticipatory)

– Financial Reporting & Internal Control responsibility (after the fact or

reactive)

– Four types of controller roles

– Involved controller

– Independent controller

– Split controller

– Strong controller

– Service function & Leadership & Interpersonal relationship with

management expected from (strong) Controllers

– Managers have to accept and cooperate with the Controller

26/2/2016 3

Module 2 Basic Tools

Financial Concepts:

– Efficiency in value creation (ROCE > WACC)

– Strength to cope with uncertainty (D/E, Equity ratio)

– Ability to reward stakeholders (Cash)

MUST: Ability to cope with all three dimensions

26/2/2016 4

Module 2 Basic Tools

The magic triangle regarding the financial body:

Profit & Loss Statement (…the muscles)

Balance Sheet (…the bones) Cash Flow (…the blood)

KPIs

26/2/2016 5

Module 2 Basic Tools – Income Statement or P&L

– One of the major financial statements beside Balance Sheet and

Cash Flow Statement.

– “Muscles” of the financial body.

– Shows the profitability of a company during a PERIODE of time.

– It does not show cash receipts (money you receive) nor cash

disbursements (money you pay out). The profit-&loss statement

measures profitability, not cash flow!

– Prepared monthly, quarterly and / or annually.

– Two formats:

– Total Expenditure Format (Gesamtkostenverfahren)

– Cost of Sales Format (Umsatzkostenverfahren)

26/2/2016 6

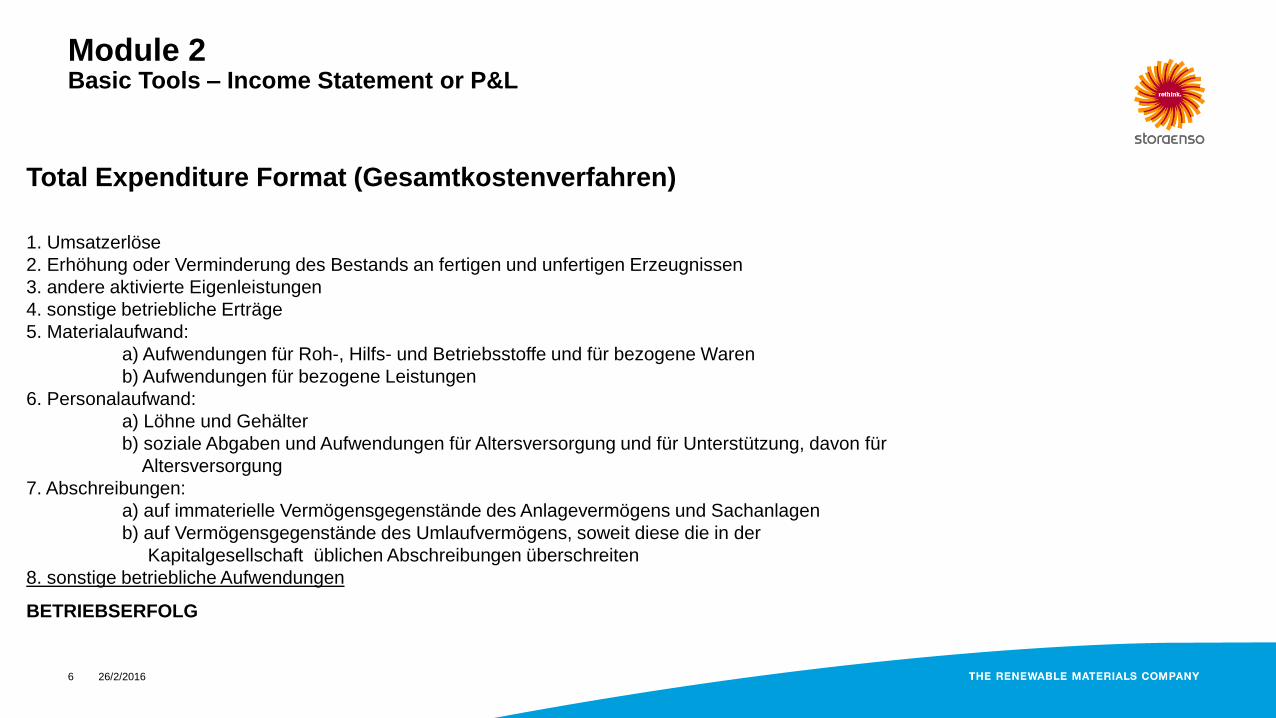

Module 2 Basic Tools – Income Statement or P&L

Total Expenditure Format (Gesamtkostenverfahren)

1. Umsatzerlöse

2. Erhöhung oder Verminderung des Bestands an fertigen und unfertigen Erzeugnissen

3. andere aktivierte Eigenleistungen

4. sonstige betriebliche Erträge

5. Materialaufwand:

a) Aufwendungen für Roh-, Hilfs- und Betriebsstoffe und für bezogene Waren

b) Aufwendungen für bezogene Leistungen

6. Personalaufwand:

a) Löhne und Gehälter

b) soziale Abgaben und Aufwendungen für Altersversorgung und für Unterstützung, davon für

Altersversorgung

7. Abschreibungen:

a) auf immaterielle Vermögensgegenstände des Anlagevermögens und Sachanlagen

b) auf Vermögensgegenstände des Umlaufvermögens, soweit diese die in der

Kapitalgesellschaft üblichen Abschreibungen überschreiten

8. sonstige betriebliche Aufwendungen

BETRIEBSERFOLG

26/2/2016 7

Module 2 Basic Tools – Income Statement or P&L

Cost of Sales Format (Umsatzkostenverfahren)

1. Umsatzerlöse

2. Herstellungskosten der zur Erzielung der Umsatzerlöse erbrachten Leistungen

3. Bruttoergebnis vom Umsatz

4. Vertriebskosten

5. allgemeine Verwaltungskosten

6. sonstige betriebliche Erträge

7. sonstige betriebliche Aufwendungen

BETRIEBSERFOLG 8. Erträge aus Beteiligungen,

davon aus verbundenen Unternehmen

9. Erträge aus anderen Wertpapieren und Ausleihungen des Finanzanlagevermögens,

davon aus verbundenen Unternehmen

10. sonstige Zinsen und ähnliche Erträge, davon aus verbundenen Unternehmen

11. Abschreibungen auf Finanzanlagen und auf Wertpapiere des Umlaufvermögens

12. Zinsen und ähnliche Aufwendungen, davon an verbundene Unternehmen

13. Ergebnis der gewöhnlichen Geschäftstätigkeit

14. außerordentliche Erträge

15. außerordentliche Aufwendungen

16. außerordentliches Ergebnis

17. Steuern vom Einkommen und vom Ertrag

18. sonstige Steuern

19. Jahresüberschuß/Jahresfehlbetrag

26/2/2016 8

Module 2 Basic Tools – Income Statement or P&L

Total Expenditure Format (Gesamtkostenverfahren)

• Shows the total performance and all costs for a selected period

with change in inventories

• Expenses are shown according to their origin (material,

personnel, maintenance, etc.)

Cost of Sales Format (Umsatzkostenverfahren)

• Shows the cost of goods sold (COGS) for a selected period

• Expenses are shown according to functions (production,

general & administration, sales)

Regarding 1) Financial result, 2) extraordinary items and 3)

taxes, both methods have the same structure and results.

26/2/2016 9

Module 2 Basic Tools – Income Statement or P&L

– Contribution margin: The contribution margin is the amount that

remains of our sales after deducting all variable costs. It is used to cover

fixed costs and eventually to make profits.

Gross Sales

- Sales deductions (rebates, cash discounts,..)

Net sales

- Freight costs, Commissions,..

- Variable Costs .

Contribution margin

– Can also be expressed as %-age of sales, i.e. a contribution margin of

15% indicates that out of 1Euro sales, 15 cents remain for coverage of

fixed costs

– Contribution margin can also be shown in several steps by allocating fixed

costs to articles, article groups, business areas,…

26/2/2016 10

Module 2 Basic Tools – Income Statement or P&L

Practical Example VBW:

Opern- und Musicalproduktionen in drei Häusern: Theater a.d. Wien (TAW),

Raimund Theater (RAI), Ronacher (RON)

Besucher: RON: 150.000; RAI 250.000; TAW 80.000

Kosten Intendanz: Musical: 600.000€; Oper: 500.000€

Leading Team Kosten: RON: 300T€; RAI: 350T€; TAW: 500T€

Produktionsausstattung:

RON: Bühne (450T€); Ton (50T€); Licht (50T€); Kostüm (200T€)

RAI: Bühne (500T€); Ton (50T€); Licht (50T€); Kostüm (200T€)

TAW: Bühne (600T€); Ton (50T€); Licht (50T€); Kostüm (300T€)

Personalkosten Haustechnik: RON: 25 Personen; RTH: 30 Personen; TAW: 20

Personen (durchschnittliche Kosten: 60.000€ / Person)

Orchester: RON: 10 Personen; RAI: 15 Personen; TAW: 20 Personen

(Durchschnittskosten pro Person: 60.000€)

26/2/2016 11

Module 2 Basic Tools – Income Statement or P&L

Practical Example VBW:

Opern- und Musicalproduktionen in drei Häusern: Theater a.d. Wien (TAW),

Raimund Theater (RAI), Ronacher (RON)

Technik (produktionsbezogene Überstunden): RON: 10.000h; RAI: 12.000h;

TAW: 6.000h (durchschnittliche Kosten: 30€/h)

Marketing (produktionsbezogen): RON: 300T€; RTH: 450T€; TAW: 600T€

Hausbezogener Materialaufwand: RON: 400T€; RTH: 350T€; TAW: 300T€

Durchschnittlicher Ticketpreis: RON: 45€; RAI: 50€; TAW 60€

Personalkosten FM Haus: RON: 25 Personen; RTH: 30 Personen; TAW: 20

Personen (durchschnittliche Kosten: 40.000€ / Person)

Cast: RON: 2.750T€; RAI: 3.125T€; TAW: 2.000T€

Overhead: Sonstiger Aufwand (Material, bezogene Leistungen): 2.500T€;

Zentrale Technik: 1.000T€; Zentrales FM: 700T€; Generaldirektion: 1.500T€

26/2/2016 12

Module 2 Basic Tools – Income Statement or P&L

1000 CUR

Sales, sawngoods Ext

Sales, sawngoods Int Prod unit

Sales, sawngoods Int Sales unit

Sales, distribution Ext

Sales, distribution Int

End Product Sales

Sales, by-products Ext

Sales, by-products Int

Sales, logs Ext

Sales, logs Int

Wood Sales

Energy Sales

FX on Sales and Operative Receivables

Sales of Stora Enso Products

Transportation & Freight Sales

Commission Income

Maintenance Materials & Services Income

Other Sales

FX cashflow hedge derivatives

Sales of Stora Enso Services and other

Sales non Stora Enso products

SALES

Transportation & Freight Costs, sawn

Transportation & Freight Costs, by-products

Transportation & Freight Costs, other

Transportation & Commissions Costs

Commission costs, sawn

Commission costs, other Total

Commission costs

SALES AT MILL PRICE

Change in Finished Goods Inventory & WIP

Change in net value of biological assets

Other Operating Income, other Ext

Other Operating Income, other Int

Wood costs

By-product purchases Total

Energy costs TOT

Supplied sawn goods Total

Other purchases, production Total

Other purchases, distribution Total

End Product Purchases

Chemicals & fillers costs

Packaging material

Other Operating Variable Costs

Total variable costs, CUR

Practical example – Stora Enso:

1) How big is the contribution

margin?

2) How big is the margin %-age?

24.849

1.450

67

0

0

26.366

868

0

0

0

868

0

3

27.237

0

0

0

0

0

0

0

27.237

-9

-24

0

-33

0

0

0

27.205

6

0

48

0

0

0

-357

-14.471

0

0

-14.471

-1.269

-96

0

-16.193

26/2/2016 13

Module 2 Basic Tools – Income Statement or P&L

– Break-Even Analysis: The break-even point defines the sales

volume which is needed to cover all costs, i.e. neither produces a

profit nor a loss.

Break Even Point means:

Profit = 0

Fixed costs = Total contribution margin

Revenues = Total costs

Profitability increase by:

– Increase of Sales

– Improvement of Contribution Margin (price increase, reduction of

variable costs, improved product mix)

– Reduction of Fixed costs

– Capacity Reduction

26/2/2016 14

Module 2 Basic Tools – Income Statement or P&L

– Break-Even Analysis:

Break Even Point (Vol) = Fixed costs / Contribution margin per piece

Break Even Point (Value) = Fixed costs / Contribution margin %-age

Safety margin [value] = (Planned sales-Minimum sales) / Planned sales * 100

Safety margin [volume] = (Planned volume-Minimum volume) / Planned volume * 100

Targeted Turnover = (Fixed costs + Profit) / Contribution margin %-age

26/2/2016 15

Module 2 Basic Tools – Income Statement or P&L

Example 2:

A company has the following planned parameters:

Sales volume: 2.000 bicycle shoes

Production volume: 2.300 shoes

Variable costs/shoe: 120EUR

Net sales / shoe: 180EUR

Fixed costs: 110.000EUR

1) How big is the minimum sales value?

2) How big is the minimum sales volume?

3) What are the safety margins?

4) Return of Sales?

5)The owner's target is a profit of 9TEUR. Which turnover is necessary?

6) How much additional sales are necessary if a new sales rep is employed for 25.000EUR p.a.?

7) The head of sales suggests a 5% price decrease. How many % more sales is the minimum requirement?

26/2/2016 16

Module 2 Basic Tools – Income Statement or P&L

Practical example – Stora Enso:

1) Minimum sales value?

2) Minimum sales volume?

3) Safety margins?

4) ROS?

Wages and Salaries, Production

Wages and Salaries, Maintenance

Wages and Salaries, Admin

Personnel costs

Maintenance Materials Total

Maintenance Services

Maintenance materials & services costs

Other fixed costs, excl. production cost Total

Other fixed costs, incl. in production cost Total

Contractors costs (log/truck/other)

Other fixed costs, admin

Other fixed costs, cost pool

Bad debts and credit losses

Wood proc related fixed

Other fixed costs total

Total fixed costs, CUR

-254

-44

-27

-324

-45

-3

-48

-8

-257

0

-8

-115

-66

0

-454

-826

Total invoicing, m3 6.814

Mill net price Total wo hedging CUR/m3 (ext) 429,38

Total variable costs, CUR -306,69

26/2/2016 17

Module 2 Basic Tools – Income Statement or P&L

Plan P&L Example 3:

A company has the following planned parameters:

Production volume: 8.100 aero-helmets

Sales volume: 8.000 aero-helmets

Net sales / helmet: 240EUR

Production time / helmet: 15min

Production wages / hour: 130EUR

Overhead production costs: 100%

Production materials / helmet: 28EUR

Overhead production materials / helmet: 3EUR

Basis for overhead material costs are production materials and for overhead production

costs the production wages.

Fixed costs: Personnel 150.000EUR

Other fixed costs 100.000EUR

Depreciation 190.000EUR

Interest costs 60.000EUR

1)Establish a plan P&L (Gesamtkostenverfahren)

2)Calculate the ROS

26/2/2016 18

Module 2 Basic Tools – Kostenarten (Cost elements), Kostenstellen (Cost centers), Kostenträger (Cost unit)

Kostenarten (Cost Elements): Kategorisierung nach der Natur der Kosten

Exkurs: Österreichischer Kontenrahmen

Kontenklasse:

0 Anlagevermögen

1 Vorräte und unfertige Aufträge Bestandskonten

2 Sonstiges UV und RAP

3 Verbindlichkeiten, RSt, RAP

4 Betriebliche Erträge

5 Materialaufwand und Aufwand für bez Leistungen

6 Personalaufwand Erfolgskonten

7 Abschreibungen und sonst betr Aufwendungen

8 Finanzkonten, Ao Erträge / Aufwendungen, Steuern

9 Kapitalkonten, Abschlußkonten

26/2/2016 19

Module 2 Basic Tools – Kostenarten (Cost elements), Kostenstellen (Cost centers), Kostenträger (Cost unit)

Kostenstellen (Cost Centers): Wo sind die Kosten angefallen?

6871206 Management

6871211 Construction

6871212 Post & Beam

6871213 Sales office CE

6871214 Light Frame

6871215 Joinery

6871216 Sales SEA

6871217 BL Trading

6871218 Sales administration team

2600 Marketing

2612 Publikationen (Printwerbung)

2613 Aussenwerbung (Plakate)

2614 Medien

2601 Grafik

2604 Kooperationen

2605 Hilfskräfte / Verteiler

2606 Marktforschung

26/2/2016 20

Kostenträger (Cost Units): Wofür sind die Kosten angefallen?

RON

Produktion mit der Endung

12 - bis zur Premiere inkl. Audition

13 - ab (einschließlich) Premiere

51 - Premieren- und Dernièrefeiern

52 - Merchandising

54 - Tonträger

z.B. Tanz der Vampire 3310512

Profit Center Mapping

Stora Enso Wood Products CEU

SAP Company code Profit Center

160 68037 Brand Mill

68038 Brand Post

68237 Ybbs Mill

68238 Ybbs Post

68239 Ybbs CLT

68537 Sollenau Mill

68780 Wood Products Head Office

161 68837 BSL Sawn

68838 BSL CLT

162 68938 SE WP Holzverarb.

Module 2 Basic Tools – Kostenarten (Cost elements), Kostenstellen (Cost centers), Kostenträger (Cost unit)

26/2/2016 21

1)Im Februar 2014 besuchten 32.141 Besucher im Ronacher die Vorstellungen zu "Der Besuch der alten

Dame". Der durchschnittliche Kartenpreis betrug 58,1 €.

2) Im Raimundtheater benötigte der Leiter der Tonabteilung 2.500 € für allgemeines Bühnenmaterial.

3) Für das Ronacher wurde im Jänner Beleuchtungsmaterial i. H. v. 5.000 € angeschafft.

4) Die Versicherung hat für einen Wasserschaden im Theater a.d. Wien 25.000 € überwiesen.

5)Für die Produktion "Der Besuch der alten Dame" wurde in das Bühnenbild investiert (Aufwand: 40.000

€)

6) Die Kostüme der Produktion "Elisabeth" wurden endgereinigt. Kostenpunkt 13.000 €

7)Das Ensemble der Produktion "Der Besuch der alten Dame" bekam im Jänner Probegagen in Höhe von

150.000 € ausbezahlt. (Lohnnebenkosten 30%)

8)Für den Aufbau der Lichtanlage für die neue Opernproduktion im Theater an der Wien wurde

Fremdpersonal benötigt (13.000 €)

9) Im Ronacher wurden neue Saiten für Streichinstrumente angeschafft. 2.500 €

10)Die Versicherung hat die Jahresbeträge für die Feuerversicherung für alle drei Häuser vorgeschrieben

(50.000 € je Haus)

11) Für die Produktion "Der Besuch der alten Dame" mußten 10 Lautsprecher zu je 2.500 € im Februar

angeschafft werden.

12) Die Verpachtung der Kantine brachte 2.100 € ein.

13) Die Wien Energie AG hat dem Raimund Theater eine Stromrechnung übermittelt (10.000 €).

14)Für die Produktion "Der Besuch der alten Dame" mußten 5 weiße Scheinwerfer zu je 5.000 €

angeschafft werden.

15) Im Februar wurden 13.598 Programmhefte (Der Besuch der alten Dame) zu je 6,5 € verkauft.

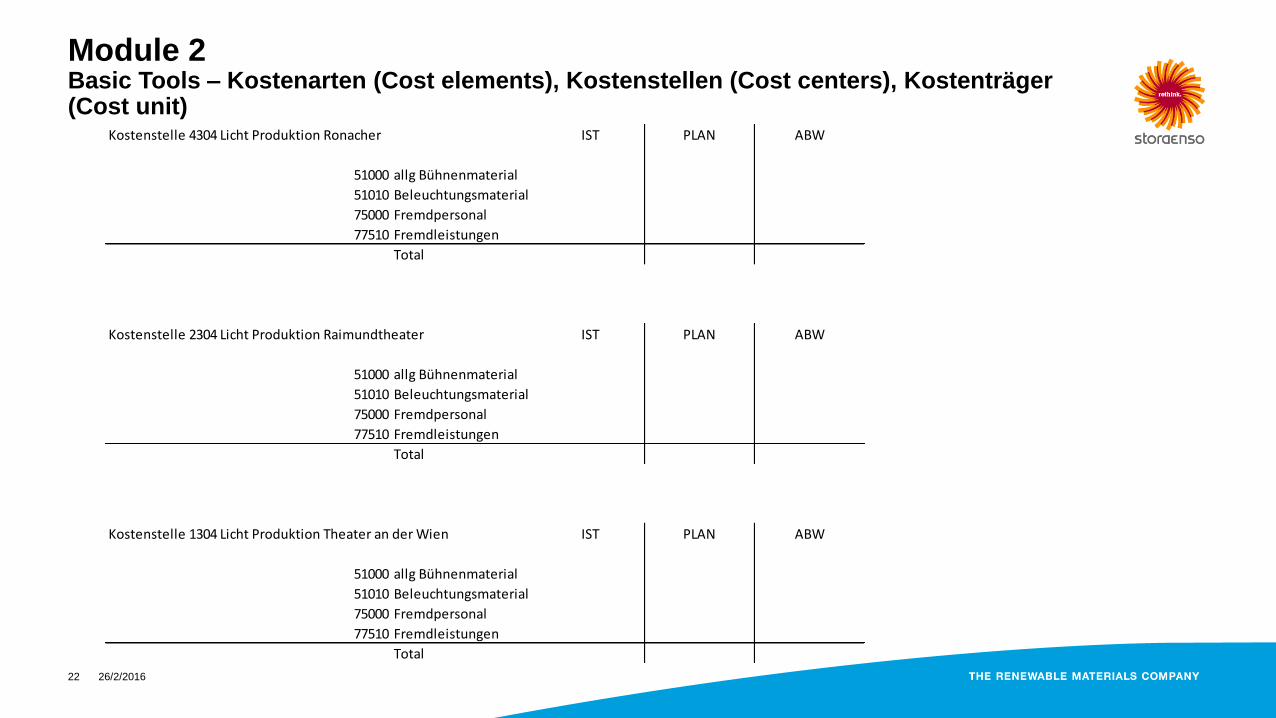

Module 2 Basic Tools – Kostenarten (Cost elements), Kostenstellen (Cost centers), Kostenträger (Cost unit)

26/2/2016 22

Kostenstelle 4304 Licht Produktion Ronacher IST PLAN ABW

51000 allg Bühnenmaterial

51010 Beleuchtungsmaterial

75000 Fremdpersonal

77510 Fremdleistungen

Total

Kostenstelle 2304 Licht Produktion Raimundtheater IST PLAN ABW

51000 allg Bühnenmaterial

51010 Beleuchtungsmaterial

75000 Fremdpersonal

77510 Fremdleistungen

Total

Kostenstelle 1304 Licht Produktion Theater an der Wien IST PLAN ABW

51000 allg Bühnenmaterial

51010 Beleuchtungsmaterial

75000 Fremdpersonal

77510 Fremdleistungen

Total

Module 2 Basic Tools – Kostenarten (Cost elements), Kostenstellen (Cost centers), Kostenträger (Cost unit)

26/2/2016 23

IST 2014 PLAN 2014 ABW

Erlöse

Kartenerlöse

Sonstige Umsatzerlöse

Total

Ausstattung

Bühne

Ton

Licht

Kostüm

Maske

Total

Musik

Orchester

Musikdirektion

Total

Cast

Solisten / Ensemble

Kinder

Total

Marketing

Marketing

Corporate Communications

Sales Department

Total

Gesamtkosten

Ergebnis

Kostenträger 3313412 Der Besuch der alten Dame

Module 2 Basic Tools – Kostenarten (Cost elements), Kostenstellen (Cost centers), Kostenträger (Cost unit)

26/2/2016 24

Module 2 Basic Tools – Income Statement or P&L – Value Creation and Value Capturing

Perceived Value Costs Value Comp. Profit

benefit created created discount

Quality

Functions/

Reliability

Services

Logs

Personnel

Maintenance

Other

Price

26/2/2016 25

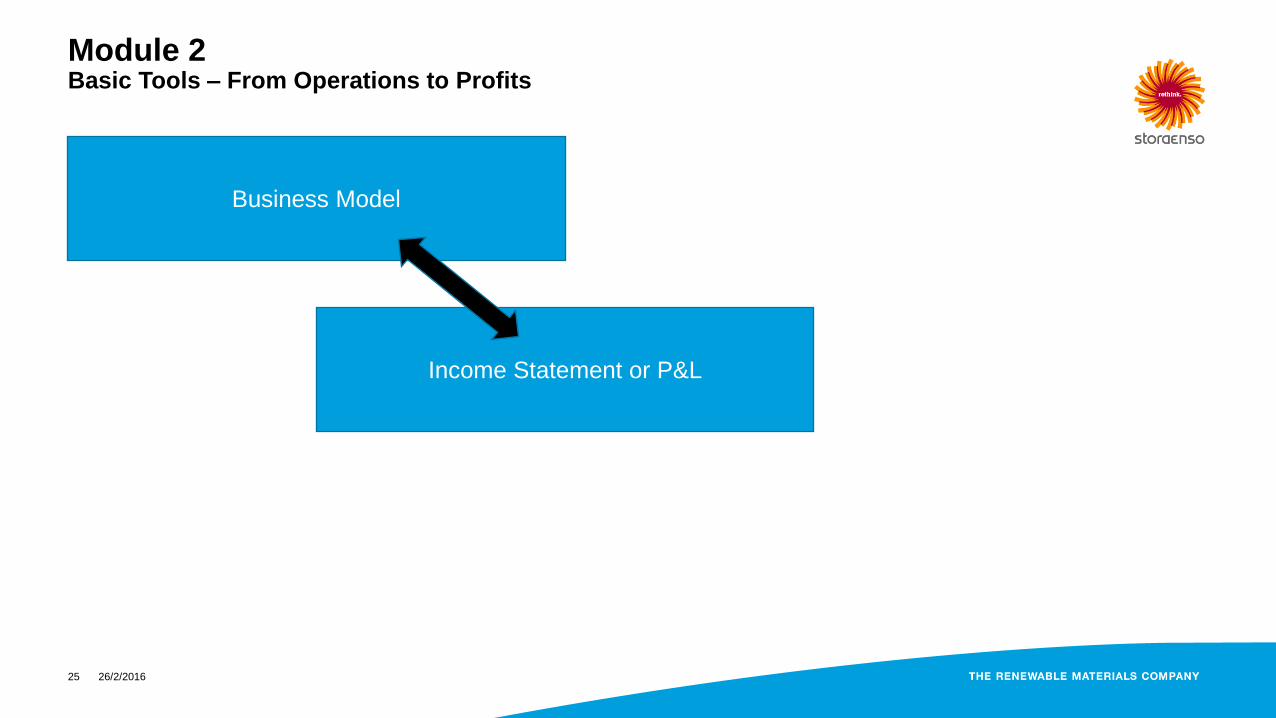

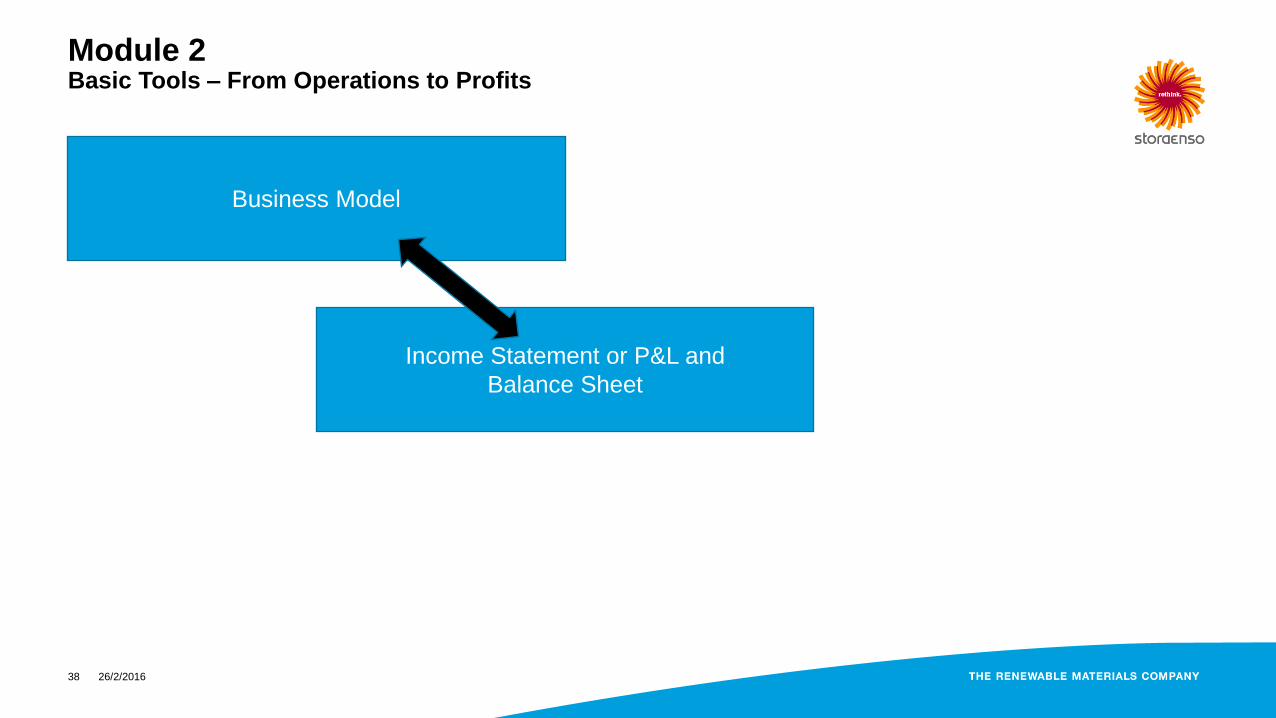

Module 2 Basic Tools – From Operations to Profits

Business Model

Income Statement or P&L

26/2/2016 26

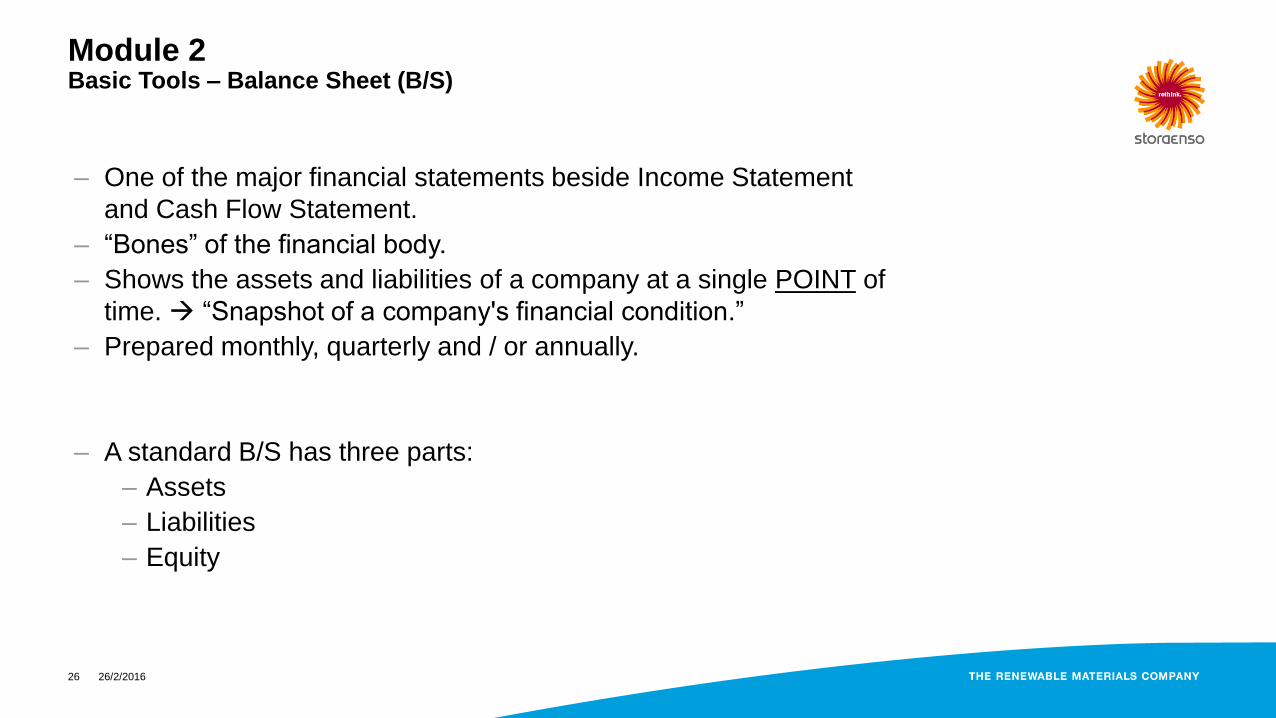

Module 2 Basic Tools – Balance Sheet (B/S)

– One of the major financial statements beside Income Statement

and Cash Flow Statement.

– “Bones” of the financial body.

– Shows the assets and liabilities of a company at a single POINT of

time. “Snapshot of a company's financial condition.”

– Prepared monthly, quarterly and / or annually.

– A standard B/S has three parts:

– Assets

– Liabilities

– Equity

26/2/2016 27

Module 2 Basic Tools – Balance Sheet (B/S)

– ASSETS:

– The left-hand side of a B/S shows how a company uses the

capital given by owners (equity) or external sources (debt). The

assets represent things of value that a company owns and has

in its possession or something that will be received.

– Fixed assets are expected to remain in the use of the

company for a longer period of time (> 1 year).

– Current assets are not expected to remain long in the use

of the company (consumed within 1 year).

26/2/2016 28

Module 2 Basic Tools – Balance Sheet (B/S)

26/2/2016 29

Module 2 Basic Tools – Balance Sheet (B/S)

– EQUITY & LIABILITIES:

– The right-hand side of a B/S shows where the capital of a

company comes from or in other words how the assets are

financed (equity, debt).

– Liabilities are those funds that a company owes to other

external sources. They are used to finance operations and

pay for expansions.

– Equity represents retained earnings and funds contributed

by the company's shareholders.

26/2/2016 30

Module 2 Basic Tools – Balance Sheet (B/S)

26/2/2016 31

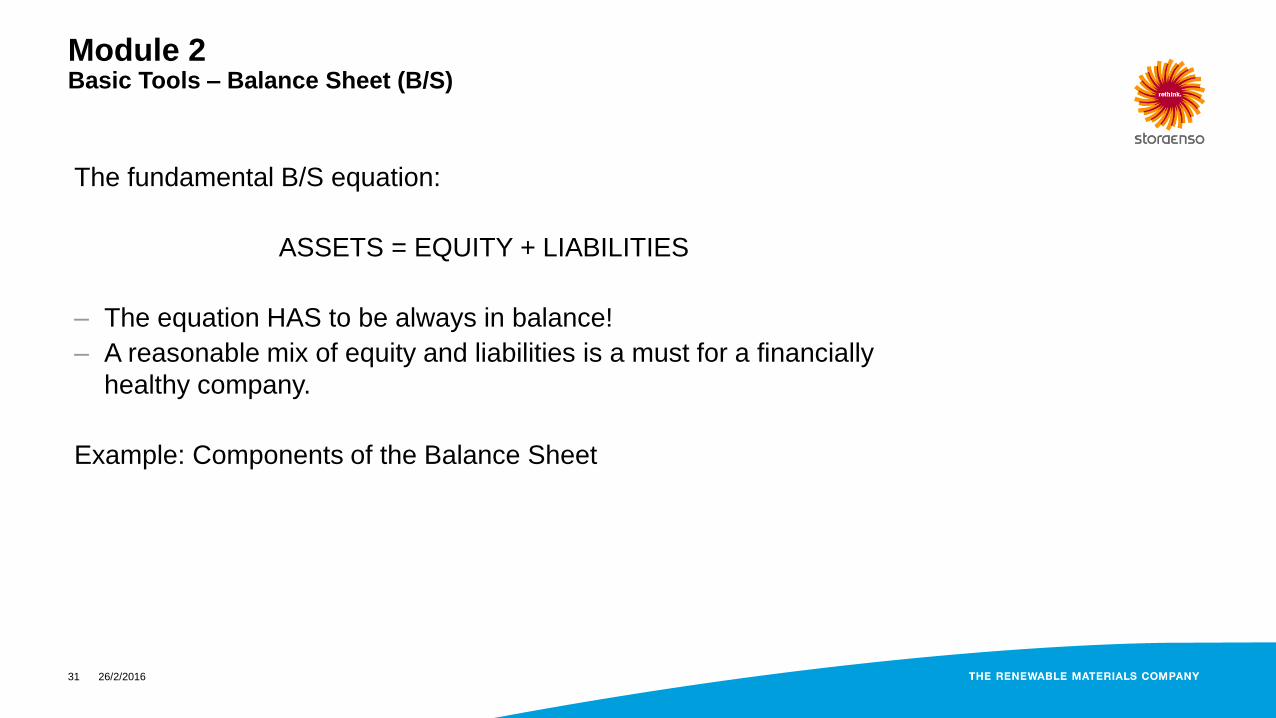

Module 2 Basic Tools – Balance Sheet (B/S)

The fundamental B/S equation:

ASSETS = EQUITY + LIABILITIES

– The equation HAS to be always in balance!

– A reasonable mix of equity and liabilities is a must for a financially

healthy company.

Example: Components of the Balance Sheet

26/2/2016 32

Module 2 Basic Tools – Balance Sheet (B/S)

Current

Assets

Invest-

ments

Fixed

Assets

Current

Liabilities

Lt

Liabilities

Equity

How we use our money Where the money comes from

Land

Plant

Equipment

Replacement / Development

Strategic

Accounts receivables

Inventories

Cash

Share Capital

Retained Earnings

Lt Accruals (Pensions,..)

Lt Loans

Accounts payables

St Borrowings

26/2/2016 33

Module 2 Basic Tools – Balance Sheet (B/S)

– Working Capital:

Delta between current assets and current liabilities.

Liquidity indicator: Shows the ability of a company to cover current liabilities

out of its current assets.

– Management approach:

Inventories

+ Accounts receivables

- Accounts payables

Working Capital

Lean working capital management means among others:

decreased costs (inventory space,…)

reduced bad debts

increased cash flow

26/2/2016 34

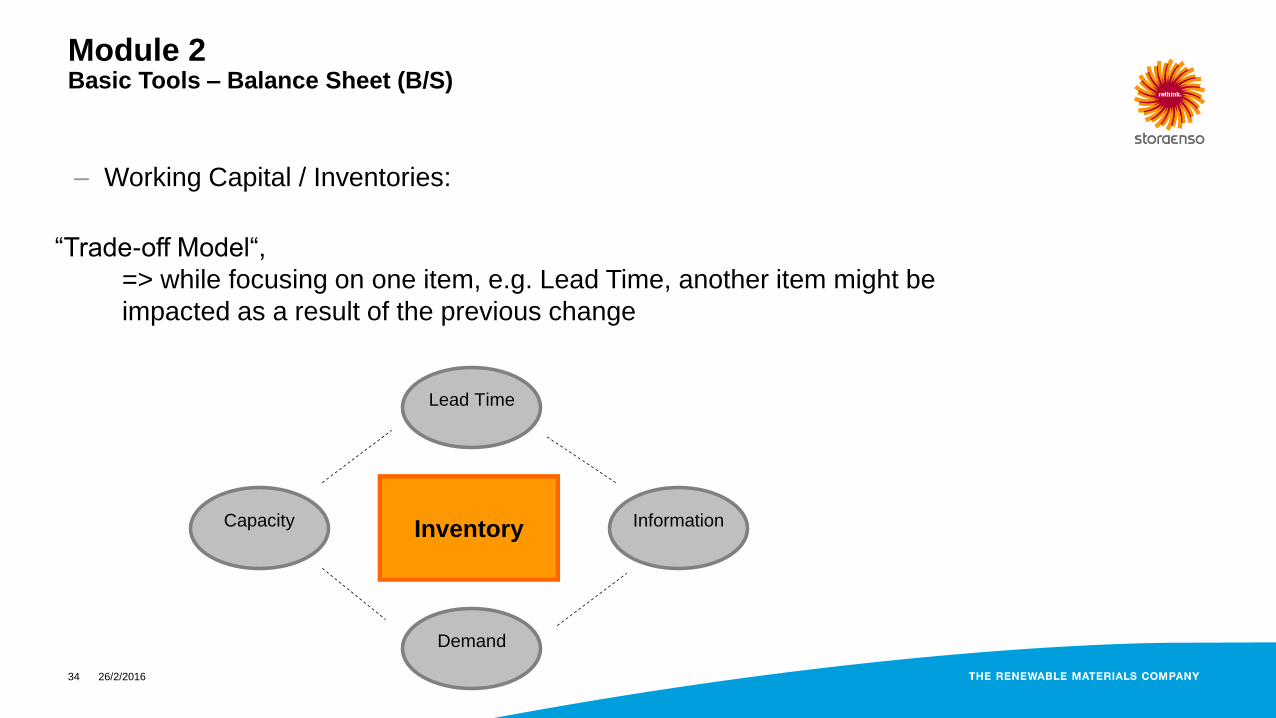

Module 2 Basic Tools – Balance Sheet (B/S)

– Working Capital / Inventories:

“Trade-off Model“,

=> while focusing on one item, e.g. Lead Time, another item might be

impacted as a result of the previous change

Inventory InformationCapacity

Lead Time

Demand

26/2/2016 35

Module 2 Basic Tools – Balance Sheet (B/S)

– Working Capital / Inventories:

26/2/2016 36

Module 2 Basic Tools – Balance Sheet (B/S)

– Working Capital / Accounts receivables:

– A tight receivables management is more than ever important to

prevent revenue leakage and bad debts to occur!

– Sales is interested in selling (and not in administration of

outstanding receivables…).

– Payment terms need to be managed efficiently and reviewed

periodically.

– Cash discounts are expensive tools and need to be handled

restrictively. Example:

Effective cash discount rate = Cash discount rate * 360 / (Term for payment – Cash discount period)

26/2/2016 37

Module 2 Basic Tools – Balance Sheet (B/S)

– Working Capital / Accounts receivables:

WP overdues by days31.12.2015 € thousand

Month 1 - 3 4 -14 15 - 30 31 - 60 61 - 90 91 - 120 + 120 Total O/D All rec O/D %Dec 14 3.367 6.332 3.429 1.863 2.187 367 0 17.551 119.778 14,65%

Jan 15 3.137 3.826 3.352 3.882 820 510 0 15.533 118.592 13,10%

Feb 15 2.588 2.467 3.586 1.830 2.843 651 420 14.402 143.567 10,03%

Mar 15 2.974 2.665 2.269 2.937 1.302 2.602 696 15.448 144.817 10,67%

Apr 15 931 2.868 1.138 1.293 1.886 1.100 26 9.244 144.601 6,39%

May 15 4.915 7.105 2.584 846 468 1.785 944 18.645 161.986 11,51%

Jun 15 2.194 2.949 1.498 837 212 8 2.401 10.088 155.490 6,49%

Jul 15 3.288 2.702 1.235 730 306 158 1.239 9.661 135.976 7,10%

Aug 15 3.968 3.902 1.040 1.152 152 20 441 10.678 123.062 8,68%

Sep 15 2.769 2.773 974 1.033 98 6 450 8.104 135.488 5,98%

Oct 15 3.891 2.437 1.181 1.137 241 1 454 9.349 138.390 6,76%

Nov 15 2.846 2.641 1.337 875 148 16 444 8.303 139.249 5,96%

Dec 15 2.713 4.238 1.813 1.191 197 73 115 10.334 108.931 9,49%

AVG 15 3.018 3.381 1.834 1.479 723 578 636 11.649 137.512 8,47%

AVG 14 4.075 4.735 3.563 1.768 917 229 216 15.102 155.478 9,71%

AVG 13 3.847 4.890 2.776 1.758 744 223 482 14.726 163.754 8,99%

26/2/2016 38

Module 2 Basic Tools – From Operations to Profits

Business Model

Income Statement or P&L and

Balance Sheet

26/2/2016 39

Module 2 Basic Tools – Cash Flow (CF)

– One of the major financial statements beside Income Statement

and Balance Sheet.

– “Blood” of the financial body.

– Shows the flow of cash in and cash out of the business. It reflects

a company's liquidity during a PERIODE of time.

– Prepared monthly, quarterly and / or annually.

– A standard Cash Flow statement has three parts:

– CF from operating activities

– CF from investing activities

– CF from financing activities

26/2/2016 40

Module 2 Basic Tools – Cash Flow (CF)

26/2/2016 41

Module 2 Basic Tools – Cash Flow (CF)

Jahresüberschuss/-fehlbetrag nach Steuern

+ Abschreibungen auf das Anlagevermögen

- Zuschreibungen zum Anlagevermögen

+/- Gewinn (-) / Verlust (+) aus dem Abgang von Anlagevermögen

+/- Zunahme (+) / Abnahme (-) lfr Rückstellungen

= Cash Flow aus dem Ergebnis (cash earnings)

+/- Zunahme (-) / Abnahme (+) der Vorräte

+/- Zunahme (-) / Abnahme (+) der Forderungen LuL

+/- Zunahme (-) / Abnahme (+) sonstiger Aktiva und ARA

+/- Zunahme (+) / Abnahme (-) der kfr Rückstellungen

+/- Zunahme (+) / Abnahme (-) der Verbindlichkeiten LuL

+/- Zunahme (+) / Abnahme (-) sonstiger Passiva und PRA

= Cash Flow Operating Activities

- Investitionen

- Aktivierte Eigenleistungen

+ Buchwert abgegangener Anlagen

+/- Gewinn (+) / Verluste (-) aus dem Abgang von Anlagevermögen

+/- Erhöhung (-) / Verminderung (+) der Finanzdarlehen an verbundene Unternehmen

= Cash Flow Investing Activities

+ Einzahlungen von den Gesellschaftern

- Auszahlungen an die Gesellschafter

+/- Erhöhung (+) / Tilgung (-) von Finanzkrediten und Anleihen

= Cash Flow Financing Activities

Veränderung des Finanzmittelbestandes

26/2/2016 42

Module 2 Basic Tools – Cash Flow (CF)

“Cash is King!”

A lot of capital is usually tied up in receivables and inventory.

Importance to optimize working capital level becomes more evident than

in the past.

Longer term, companies need to create a culture in which everyone takes

responsibility for the balance sheet!

There are six common mistakes that companies make in managing cash:

1. Don't manage to the income statement.

2. Don't reward the sales force for growth alone.

3. Don't overemphasize production quality.

4. Don’t tie receivables to payables.

5. Don’t manage by current and quick ratios.

6. Don’t benchmark competitors.

26/2/2016 43

Module 2 Basic Tools – From Operations to Profits

Business Model

Income Statement or P&L and

Balance Sheet and Cash Flow Statement

26/2/2016 44

Module 2 Basic Tools – Cash Flow (CF)

– A CF-statement is tied to the P&L and B/S via net earnings and

depreciation (P&L) on the one side and via working capital, fixed asset

investments, etc. (B/S) on the other side.

P&L:

Sales

+/- Change in inv

- Variable costs

- Fixed costs

- Depreciation

= Operating Profit

B/S:

Fixed Assets Equity

Inventories Accruals

Trade Receivables Trade payables

CF:

Operating Profit

+ Depreciation

+/- Change in inventories

+/- Change in Receivables

+/- Change in Payables

26/2/2016 45

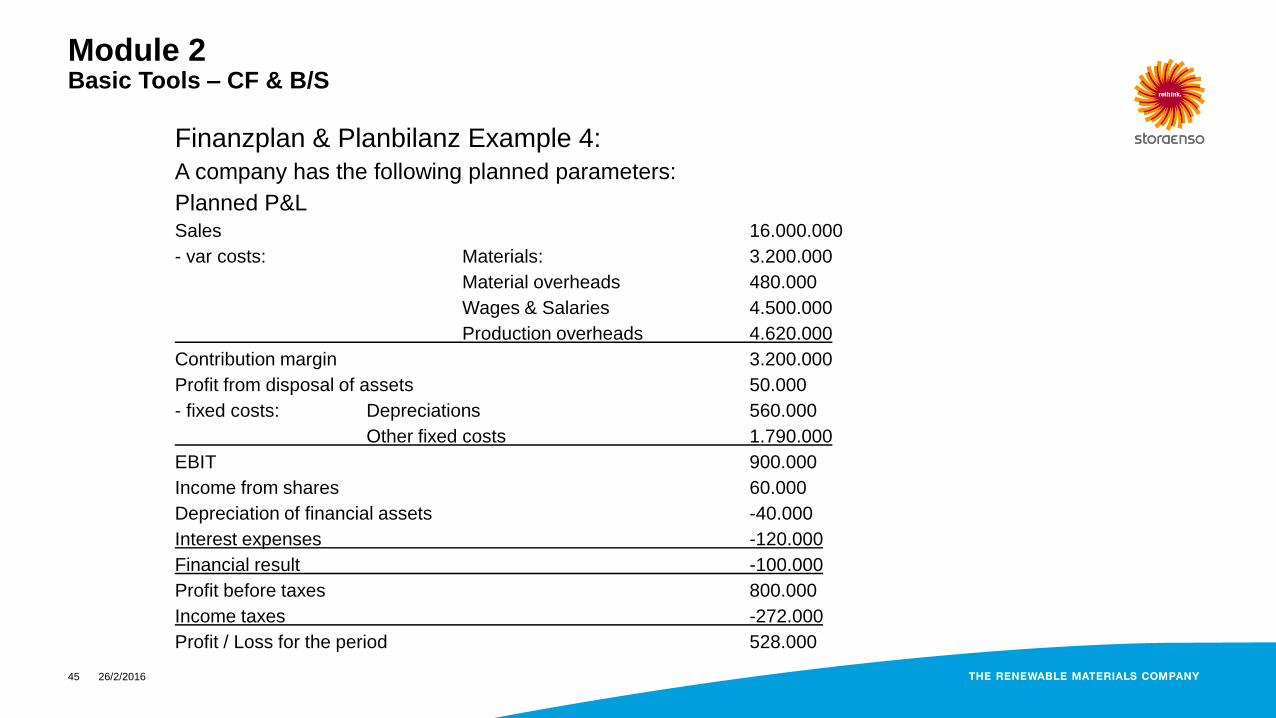

Module 2 Basic Tools – CF & B/S

Finanzplan & Planbilanz Example 4:

A company has the following planned parameters:

Planned P&L Sales 16.000.000

- var costs: Materials: 3.200.000

Material overheads 480.000

Wages & Salaries 4.500.000

Production overheads 4.620.000

Contribution margin 3.200.000

Profit from disposal of assets 50.000

- fixed costs: Depreciations 560.000

Other fixed costs 1.790.000

EBIT 900.000

Income from shares 60.000

Depreciation of financial assets -40.000

Interest expenses -120.000

Financial result -100.000

Profit before taxes 800.000

Income taxes -272.000

Profit / Loss for the period 528.000

26/2/2016 46

Module 2 Basic Tools – CF & B/S

Finanzplan & Planbilanz Example 4: A company has the following planned parameters:

B/S: 31.12. prior year

Fixed Assets 5.750.000 Equity 4.000.000

Inventory

Raw mat

Fin goods

1.200.000

900.000

Retained

earnings

890.000

Accounts

receivables

1.500.000 Profit of the

year

420.000

Cash /

banks

230.000 Accruals 880.000

Accounts

payables

1.200.000

Liab banks LT 2.100.000

Liab banks ST 90.000

Total Assets 9.580.000 Total Liabilities 9.580.000

26/2/2016 47

Module 2 Basic Tools – CF & B/S

Finanzplan & Planbilanz Example 4: A company has the following planned parameters:

•Raw material purchases: 3.100.000

•Trade receivables turnover: 13,33 (including 20% VAT)

•Trade payables are reduced by 150.000EUR

•The plan P&L includes a LT accrual of 80.000EUR (Abfertigung &

Pensionen)

•The B/S includes a tax accrual of 80.000EUR which is used as

planned.

•Tax prepayments (Köstvorauszahlung) are 250.000EUR.

•An investment of a machine (900.000EUR) is planned. 1/3 is financed

by a new loan. Depreciations are included in the plan P&L.

•LT Loans of 130.000EUR have to be paid back in the planning period.

•Retained earning (Gewinnrücklage) of 48.000EUR should be booked.

•A dividend of 400.000EUR is to be paid.

•A positive or negative liquidity should be used to balance ST bank

accounts. LT…long-term

ST…short-term

26/2/2016 48

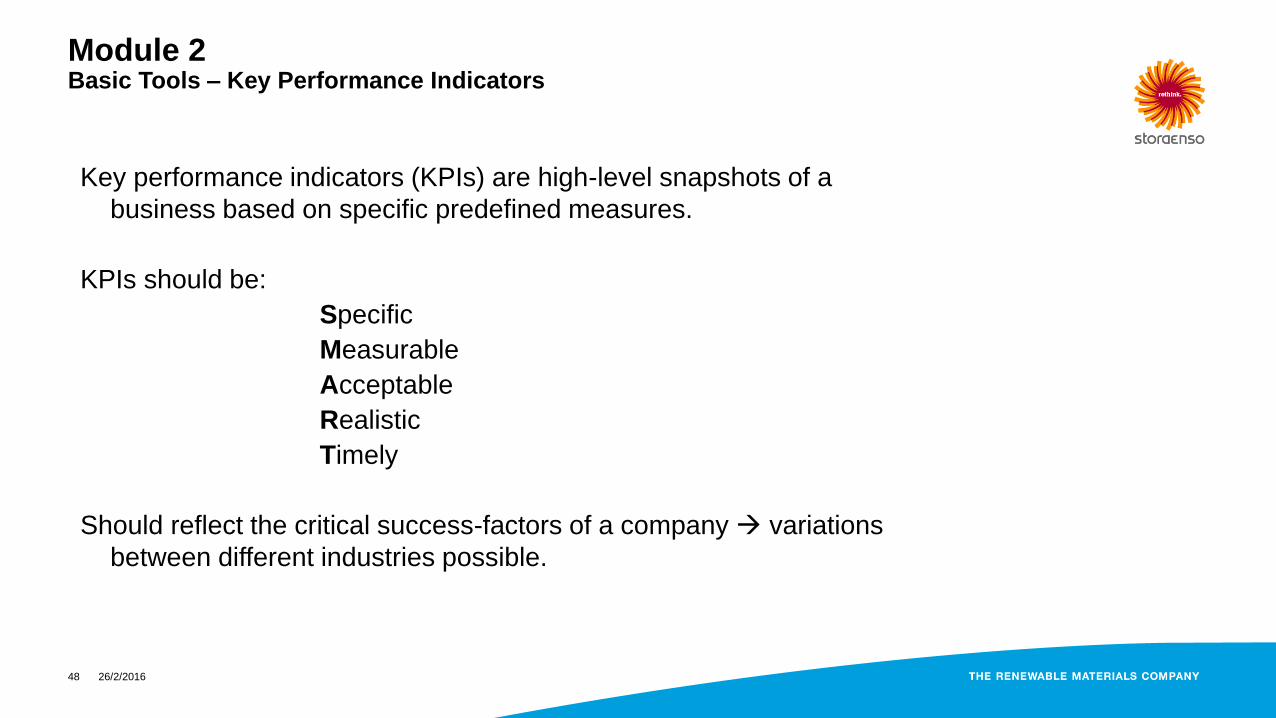

Module 2 Basic Tools – Key Performance Indicators

Key performance indicators (KPIs) are high-level snapshots of a

business based on specific predefined measures.

KPIs should be:

Specific

Measurable

Acceptable

Realistic

Timely

Should reflect the critical success-factors of a company variations

between different industries possible.

26/2/2016 49

Module 2 Basic Tools – Key Performance Indicators

Key performance indicators (KPIs) in the wood-products industry (example

Stora Enso):

KPIs connected to the P&L:

Return on Sales (ROS) = Operating Profit / Sales *100

Return on Capital Employed (ROCE) = Operating Profit / Operating capital *100

Personnel intensity = Personnel costs / Sales *100

Maintenance intensity = Maintenance costs / Sales *100

Raw material intensity = Raw material costs / Sales * 100

26/2/2016 50

Module 2 Basic Tools – Key Performance Indicators

Key performance indicators (KPIs) in the wood-products industry (example

Stora Enso):

KPIs connected to the B/S:

Inventory turnover ratio = Sales or COGS / (Average) Inventory

Inventory turnover days = 365/ Inventory turnover ratio (also called DIOH)

Receivables turnover ratio = Net Sales / (Average) Accounts receivables

Receivables turnover days = 365 / Receivables turnover ratio (also called DSO)

Payables turnover ratio = Purchases / (Average) Accounts payables

Payables turnover days = 365 / Payables turnover ratio (also called DPO)

Working Capital turnover = Sales / Working Capital

Relationship between the money used to fund operations

and the sales generated from these operations.

26/2/2016 51

Module 2 Basic Tools – Key Performance Indicators

Key performance indicators (KPIs) in the wood-products industry (example

Stora Enso):

KPIs connected to the B/S (continued):

Equity ratio = Owners equity / Total assets (Eigenkapitalquote)

Fixed Assets usage = accumulated depreciation / acquisition costs

(Anlagenabnützungsgrad)

Golden B/S rule: Fixed assets should be financed by equity (narrow) or equity +

long term liabilities (wider) (Goldene Bilanzregel)

26/2/2016 52

Module 2 Basic Tools – Key Performance Indicators

Key performance indicators (KPIs) in the wood-products industry (example

Stora Enso):

KPIs connected to the CF:

Cash Flow margin = Operating Cash Flow / Sales * 100

Gearing ratios:

Debt / Cash Flow

Debt / Equity (also known as debt to equity ratio)

Cash Flow KPIs are currently not used in monthly reporting.

26/2/2016 53

Module 2 Basic Tools – From Operations to Profits to Asset based Profitability

Business Model

Income Statement or P&L and

Balance Sheet and Cash Flow Statement

ROE and ROCE

26/2/2016 54

Module 2 Basic Tools – From Operations to Profits to Asset based Profitability

Return on

Equity

Profit

Margin

Capital

Turnover

Leverage

Ratio

Net income

Equity

Net income

Revenues

Revenues

Assets

Assets

Equity

How good are

we in translating

revenues into

profits?

How many units

of sales can we

squeeze out of

one unit of

assets?

How much debt

(i.e. borrowed

resources) do we

use?

26/2/2016 55

Module 2 Basic Tools – From Operations to Profits to Asset based Profitability

Operational

ROCE

Operating

Profit

Operating

Capital

100 Higher ROCE means more efficient

use of Assets to generate earnings.

26/2/2016 56

Module 2 Basic Tools – Value Creation

Provide Capital

Providers with a

reasonable rate of

return - WACC

Buy Capital

Assets ROCE

For each € Pay WACC Get ROCE

EVA = (ROCE – WACC) * IC

26/2/2016 57

Module 2 Basic Tools – From Operations to Profits to Asset based Profitability

Operating

Profit

Sales

Operating

Profit

Operating

Capital

ROCE

Sales

Operating

Capital

Sales

Assets

Sales

EBIT

Sales

Total Costs

Prices

Volume

Mix

Working

Capital

Fixed

Assets

Cash

Inventories

A/R

A/P

Var Costs

Fixed Costs

Strategic Drivers!!!

26/2/2016 58

Module 2 Basic Tools – From Operations to Profits to Asset based Profitability

Operating

Profit

Sales

Operating

Profit

Operating

Capital

ROCE

Sales

Operating

Capital

Sales

Assets

Sales

EBIT

Sales

Total Costs

Prices

Volume

Mix

Working

Capital

Fixed

Assets

Cash

Inventories

A/R

A/P

Var Costs

Fixed Costs

Increase EBIT

Decrease Capital Employed

26/2/2016 59

Module 2 Basic Tools

Financial Concepts:

– Efficiency in value creation (ROCE > WACC)

– Strength to cope with uncertainty (D/E, Equity ratio)

– Ability to reward stakeholders (Cash)

MUST: Ability to cope with all three dimensions

26/2/2016 60

Module 2 Basic Tools – Key Performance Indicators