contents page - whatdotheyknow.com · contents page explanatory foreword 3 main financial...

TRANSCRIPT

Contents Page Explanatory Foreword 3 Main Financial Statements Consolidated Revenue Account 17 Consolidated Balance Sheet 19 Statement of Total Movements in Reserves 20 Cashflow Statement 21 Notes to the Main Financial Statements 23 Additional Financial Statements 51 Group Accounts for Related Companies 55 Pension Fund Accounts 67 Statement of Accounting Policies and Valuation Certificate 79 Glossary of Financial Terms 91

3

EExxppllaannaattoorryy FFoorreewwoorrdd

4

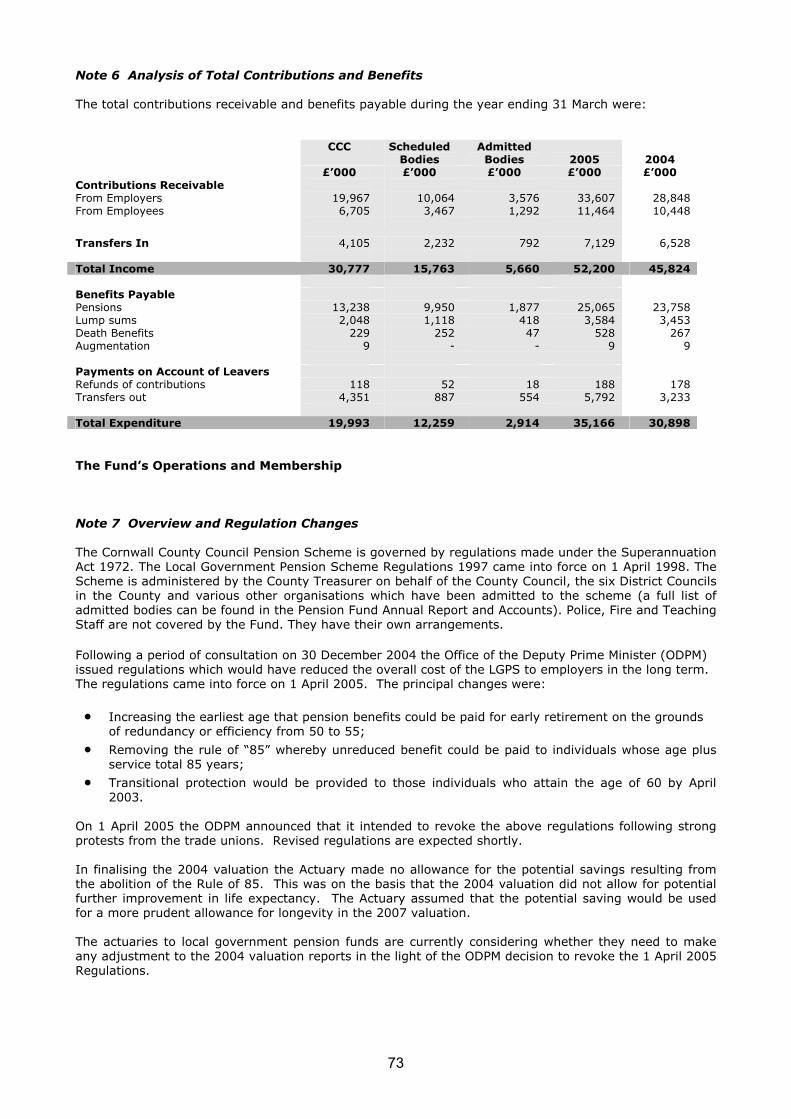

1 Introduction from the Responsible Finance Officer I am pleased to introduce the Council’s Statement of Accounts for 2004-2005. Cornwall County Council is a large and wide-ranging organisation committed to continuing improvement in performance and standard of services. This publication incorporates all the financial statements and disclosure notes required by statute. Explaining the Main Accounting Statements The accounts are split into five sections:

i) The Main Financial Statements. The main financial statements comprise the consolidated revenue account, the consolidated balance sheet, the statement of total movement in reserves and the cashflow statement. The consolidated revenue account shows how much the Authority has spent during the year on each of its services along with any corporate income or expenditure, which relates to the Authority as a whole. It also shows how much of this cost has been met by local taxpayers and how much has been funded by central government through the revenue support grant. Any surplus or deficit on this account is transferred to the Authority’s general fund reserve. The consolidated balance sheet shows a snap shot at the financial year end of all the Authority's assets and liabilities. Assets include both the value of our fixed assets such as buildings, land, equipment etc, and our current assets such as money owed to the Authority, stocks and investments. Liabilities mainly relate to money owed by the Authority. The balance of the assets and liabilities is represented on the balance sheet by the Authority’s reserves. The statement of total movement in reserves brings together all of the movements in the Authority’s reserves. The statement also splits the reserves between those which can be used to support future revenue expenditure and those which are of a capital nature. The cashflow statement shows the Authority’s cash transactions over the year, indicating the sources of cash income received and actual cash spent. The cash transactions are split between those which are of a revenue nature, those which are capital, and those which are in respect of the Authority’s borrowing.

ii) Notes to the Main Financial Statements. The second section covers the requirement under the Accounting Code Of Practice to produce certain additional financial information by way of disclosure notes. The aim of this additional information is to inform the reader of specific financial issues, which are not readily identifiable from the other financial statements.

iii) Additional Financial Statement.

Group Accounts for Related Companies.

The final sections cover the accounts of the following bodies:

iv) Extract from the Accounts of the Pension Fund, which show the operation of the Fund run by the Council for its own employees and for those of admitted authorities and other organisations.

v) Statement of Accounting Policies and Valuation Certificate.

Statement of Accounting Policies This section explains the accounting principles used to produce the figures in the accounts. These accounting principles are set nationally and ensure accounts from different organisations are consistent and comparable. Valuation certificate The Valuation Certificate relates to the value of certain fixed assets.

5

��

�.����������+"�������������,�������)�����������.//01.//2�

� �!�����������������(����#����������������!������������� �2� ���������������������������� ������� ,������ *����� 3� �����!� ��� �(������� *����� ���� �������� ���� (����#��,�������

.� (�������"�4� 5��16� ����������������7�������������0� ������ ���!��� ���� ��������� ��� � ��� ���&��������������� ����� ������� ������

2� ,������*��������

,������*����

�.48

������

(���!����

,�����9�

���������

�:8

(�������"�

..8

5��1

6� �����

�����

�:8

�������

,������*����

�.;8

���!�������!���� ������ ����� ������ ���� ���� ���!������ ����"������������������!��������������������+������� ,������� ������ ,����� 7�!�����,������+�����������������+���������(������� +������ ���� ���� )������!� ,�������������� �������� ��� ��� ����(��� #�� '�������������� ,������� ��������!���� ,������ �����(���� �����,��������(���� ,������� �����(�������� (��� �(����#�������� ��� ���� ����� ��� 6����� ���� (��������<�!���������(� ��������(������� ,������� ����� ������!���� �� ����������������������!����������������������� �

,�����,������

�.;8

�����,�����

�48

=�!��� ���

������9�

����������

,�������

;8

(����,������

�.8

(�������

+������ ���

9�)������!�

,������

�;8

(�������

,������

�.8

+�������

,�����

2.8

�!�������������������� ����� ������ ���� ����������� ��� (������"����������������>��������������+ ��� ��� ����� ����� ���� 248� ��� �������"��������������������������������!��������������� � �������� ���� ������� � ������ ��� �������� ����� �� ������� ��� ��� ������������!� ������ ��� ����(������������!��"�������������������� ��������&������ ���������� ��� ������!��� ������� ����� ��� ����������� ����������� �������������� ����������������������+"����������������(���!������������������������������ � �������� �"������� � ��� ���� ���� ����������!�� ���

+ ��� ���

�248

�����!�(����

028

+"�������

���������

(���!��

�.8

6

3 The 2004-2005 Budget 2004-2005 Original Budget

The net budget agreed by the County Council on 27 February 2004 for the 2004-2005 financial year was £472.466m. As a result, the County Council’s element of the Council Tax increased by 7.19%. This was above the average increase of the shire counties, which was 6.5%. The shire counties are a group of counties which are, like Cornwall, essentially rural in nature. The County Council’s three year strategy allowed budget increases for Education and Social Services equivalent to the Government’s funding increases (which were all above the general inflation rate), the provision of 3.5% pay and 3.0% price increases for all other services plus provision for some ‘unavoidable’ increases in other services. Within the overall net budget, a sum of £1.0m was set aside as a contingency to fund emergency items. The budget has been monitored throughout the year with variances being reported to members. Portfolio holders and chief officers have managed their service budgets throughout the financial year through the use of reserves and a number of self-balancing adjustments between portfolios and the central contingency. The most significant variation at year end was within the Corporate Support Portfolio, where significant surpluses were generated through the Council’s Treasury Management operations. These surpluses led to a net underspend of £1.908m on the interest receipts and capital financing budgets combined, plus an additional £0.758m income relating to PFI reserves. This reflected exceptional performance in minimising borrowing costs and maximising investment returns when benchmarked against other public bodies. The Lifelong Learning Portfolio also underspent its budget, by £1.317m, reflecting savings across a number of the Education Budgets, including a relatively small underspend of £0.256m against Schools’ delegated budgets. The overspends on the Economy, Environment & Heritage and Social Care & Health portfolios reflected spending from the Objective 1 Reserve, significant costs incurred in relation to the Integrated Waste Management Project and significant pressures on the Social Services budget from unavoidable residential placements and pressure on the Domiciliary budget, respectively.

Comparison of 2004-2005 Net Revenue Expenditure with the Original Budget

Actual Expenditure

Original Budget

Variation Above/(Below) Original Budget

Portfolio Budget

£'000 £’000 £’000

Leader 5,629 5,814 (185)

Corporate Support

35,894 38,969 (3,075)

Lifelong Learning

240,484 241,801 (1,317)

Economy

4,800 4,189 611

Strategic Planning & Transport

32,930 32,765 165

Environment & Heritage

18,749 17,897 852

Public Protection

19,718 20,084 (366)

Social Care & Health

80,686 80,113 573

Children & Young People

32,932 32,716 216

Children’s Bill Transition Costs

182 250 (68)

Total including Budgeted Use of Reserves 472,004 474,598 (2,594)

Budgeted Use of Reserves

(2,132)

(2,132)

-

Total Net Revenue Expenditure 469,872 472,466 (2,594)

7

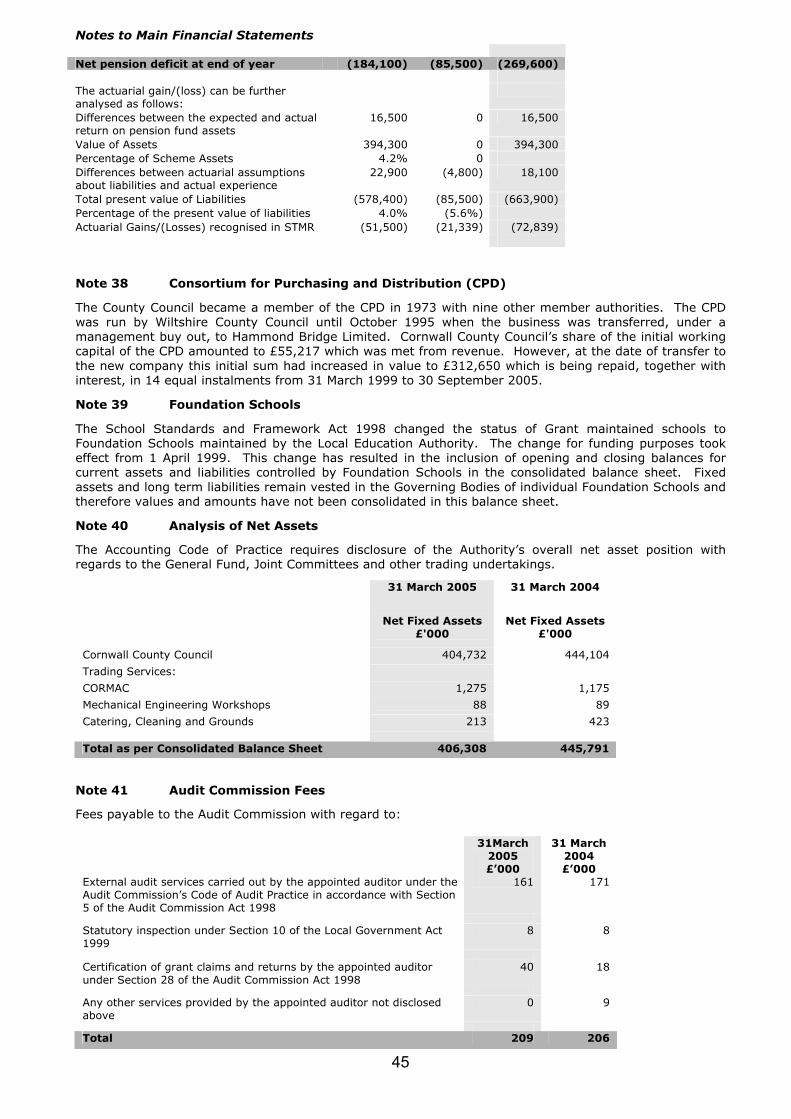

4 Reserves and Balances The County Council’s general balances, currently £13.999m, are used to meet general rather than specific future expenditure requirements, although £4.441m of this is earmarked to individual Portfolios in the form of Budget Equalisation Reserves (BERs). The total of the County Fund balance increased by £1.211m – being a decrease in Portfolio BER’s of £0.061m and an increase in the General Reserve of £1.272m following the repayments of £1m loan by the Objective One Reserve and due to the ongoing review of the Council’s existing reserves by the Resource Management Policy Development and Scrutiny Committee – Single Issue Panel. In addition, there is a Capital Reserve balance of £12.542m used to fund capital spending, including commitments from current schemes. Reserves held by Portfolios for specific purposes, such as equipment replacement, amount to £47.977m and schools hold balances of £19.196m. The schools balances are controlled by school governors and are not available to the County Council for general use. These reserves are described in the notes to the Consolidated Balance Sheet. A PFI Reserve is reported separately in the Accounts. Grant is received from the Government for PFI schemes which in the early years of projects is more than the amount needed to pay the contractor. This situation is reversed in the latter years of projects. The policy of the Council is to place the early surpluses in a reserve to be invested until such time as the funds are needed. The PFI Grant Equalisation Reserve holds the surplus from the Fire Stations scheme and the two Schools’ schemes. Because of the prudent approach to PFI affordability this represents, and because of the large sums involved which are increasing at this stage of the schemes, the PFI Reserve is being controlled and reported separately. 5 Capital Capital Spending

There is a continuing need for the Council to invest in capital spending on schools, roads, and other service assets. Capital expenditure for 2004-2005 totalled £101.457m (2003-2004 £79.295m) as detailed below.

Examples of Major Capital Schemes in 2004-2005

£’000

Highways Structural Maintenance of Roads 11,094 Bridge Strengthening & Assessment 3,539 CTO – Vehicles & Plant 2,403 Local Area Based Initiatives 2,939 Education New Deal for Schools Devolved Capital 5,696 New Deal for School Condition Funding 4,032 Major secondary school schemes 1,665 Surestart Schemes 1,024 Individual School Schemes 2,050

Capital Receipts and Revenue Financing

The ability of the Council to make significant inroads into the backlog of priority capital schemes depends very much on the generation of additional funds and capital receipts from the sale of surplus assets. In 2004-2005 capital receipts totalling £2.388m were used to finance capital spending. In total, £26.107m was funded from within the revenue budget rather than from borrowing. A substantial part of this sum was supported by reserve contributions (£9.723m advanced from the Central Capital reserve) and the balance came from Portfolios’ own earmarked reserves and from external bodies such as the Lottery funds. Capital grants received by the County Council amounted to £22.372m, this total included amounts received from European Union funding sources. Borrowing

Total external borrowing in support of the capital programme in 2004-2005 amounted to £47.205m (2003-2004 £39.418m).

8

6 Treasury Management Proactive treasury management continues to ensure that the Authority minimises its interest payable on external borrowings, and invests any temporary cash surpluses to generate investment income. The graph below illustrates how the Authority’s average borrowing rate has been steadily reduced over recent years.

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

1999-2000 2000-2001 2001-2002 2002-2003 2003-2004 2004-2005

%

Over the last two years, the Treasury Manager has actively sought to utilize market aberrations to restructure the Council’s debt portfolio. Over the period, £144m has been successfully and cost effectively restructured, reducing the average cost of the portfolio by over 1.10%. The numbers of opportunities in this area are a function of market conditions and consequently it is extremely difficult to predict the rate at which future savings may be made. 7 Statement of Internal Control 1. Scope of Responsibility Cornwall County Council is responsible for ensuring that its business is conducted in accordance

with the law and proper standards, and that public money is safeguarded and properly accounted for, and used effectively. We also have a duty under the Local Government Act 1999 to make arrangements to secure continuous improvement in the way in which our functions are exercised, having regard to a combination of economy, efficiency and effectiveness.

In discharging this overall responsibility, we are also responsible for ensuring that there is a

sound system of internal control which facilitates the effective exercise of the County Council’s functions and which includes arrangements for the management of risk.

2. The Purpose of the System of Internal Control The system of internal control is designed to manage risk to a reasonable level rather than to

eliminate all risk of failure to achieve policies, aims and objectives; it can therefore only provide reasonable and not absolute assurance of effectiveness. The system of internal control is based on an ongoing process designed to identify and prioritise the risks to the achievement of the Council’s policies, aims and objectives, to evaluate the likelihood of those risks being realised and the impact should they be realised, and to manage them efficiently, effectively and economically.

The current system of internal control described in this statement has been further redeveloped

during the last 12 months and the enhancements were in place for the year ended 31 March 2005.

3. The Internal Control Environment

The Council’s internal control environment is a dynamic process, which is designed to:

o establish and monitor the achievement of the Council’s objectives o facilitate policy and decision-making o ensuring compliance with established policies, procedures, laws and regulations

9

o ensure the economical, effective and efficient use of resources and secure continuous improvement in the way functions are exercised

o facilitate the financial management of the Council o facilitate the performance management of the authority and its reporting

The control environment has developed over many years, responding to changing needs as required. It follows therefore that it comprises a large number of different but related elements. Historically these had been managed in an individual way – the introduction of this statement last year led us to look at the operating of these elements in a more coherent manner. There are 3 key elements to the framework now in place:

• Departmental Controls – These comprise all the processes chief officers have in place within their departments and in particular include departmental approaches (based on the corporate strategy) to risk management. These also now include individual signed Statements of Assurance from each Chief Officer.

• The Independent View – of Internal and Computer Audits, External Audit and the various inspection regimes. All these agencies comment upon the operation of the Council. The Council is proactive in its dealings with all these agencies, and responsive to findings and rectifying any issues raised.

• Corporate Controls – These comprise a large number of policies, processes and strategies by which the Council exercises control over the operation of all activities within its remit. The most significant of these have been drawn together and reviewed, so we can ensure they are disseminated appropriately and monitored and reviewed regularly. These include the Council’s Constitution, its financial and service planning processes, performance management and codes of conduct for members and officers.

4. Review of Effectiveness

The Council now has a responsibility for conducting, at least annually, a review of the effectiveness of the system of internal control. The review is informed by the work of the internal auditors and the service managers within the Council who have responsibility for the development and maintenance of the internal control environment. It will also be informed by comments made by the external auditors and other review agencies and inspectorates. The Council has a comprehensive Service Planning process with a Performance Management Framework which regularly monitors achievement against priorities.

External Audit and Inspection

The Comprehensive Performance Assessment update in 2004 scored the Council four out of four for use of resources which demonstrates a commitment by the Council to manage its affairs wisely. The assessment covered:

• financial standing

• internal financial control

• standards of financial conduct and prevention of fraud

• financial statement

• legality of financial transactions

During 2004 we asked the Audit Commission to review over progress against the issues raised by the CPA in 2002. Their report has been used to re-target efforts and a Comprehensive Improvement Plan has now been implemented.

The Audit Commission’s Annual Audit and Inspection Letter for 2004 was very positive and did not identify any significant weaknesses in our internal control arrangements. The letter has been discussed with members and approved by the Audit Committee.

Internal and Computer Audit

The Council’s Internal Audit and Computer Audit Plans are risk based and are discussed with Chief Officers before approval by the Audit Committee annually. They provide the basis for the review of internal control within the Council. Achievement of the plan is monitored by the Audit Committee.

The Code of Practice (COP) requires internal and computer auditors to provide a written report to those charged with governance timed to support the statement on internal control (COP 9.1.6). Also under the COP (para 9.3) they are required to:

10

• include an opinion on the overall adequacy and effectiveness of the Council’s control environment

• disclose any qualification to that opinion, together with the reasons for the qualification • present a summary of audit work undertaken to formulate that opinion, including reliance

placed upon work by other assurance bodies • draw attention to any issues they judge particularly relevant to the preparation of the

statement of internal control • compare the work actually undertaken with the work that was planned and summarise the

performance of the function against our performance measures and criteria • comment on compliance with the standards set out in the Code of Practice and communicate

the results of our quality assurance programme. In addition they are required to make provision to form an opinion where:

• key systems are being operated, or key systems provided, on behalf of other organisations • key systems are being operated, or key services provided, by other organisations on behalf of

the Council

Notwithstanding any review by our auditors, the prime responsibility for ensuring that adequate internal control exists over all systems rests with management.

Audit’s role is to periodically test the effectiveness of those management systems and controls. Their selection of audits is risk-based but also includes those areas they would be expected to cover by the Audit Commission (specifically the key financial systems). The scope of each audit is risk-based. They cannot give absolute assurance but, given the coverage of their work, both internal audit and computer audit are of the opinion that, generally:

• Cornwall County Council has an adequate and effective control environment

• agreed policies, regulations and Standing Orders are complied with.

This opinion includes the Council’s key financial systems and the auditors are of the opinion that the County Treasurer is fulfilling his legal responsibilities under S151 of the Local Government Act 1972 and the 1996 Finance Act. In the course of their work, both planned and unplanned audits, they have not found any areas of such significant fundamental weakness that would affect this opinion. Where areas of weakness have been identified, action has been proposed or agreed to address those weaknesses. Specific areas of concern where action is still needed have been outlined to the Chief Executive and the County Treasurer and have been incorporated into section 5 below.

5. Significant Internal Control Issues

We drew attention to six areas in last years’ statement where further improvement was needed. There were a mixture of short and longer term issues, some of which continue into this statement. In general we have made good progress in all the areas raised last year. Where they remain a control issue, the notes below reflect the action taken to date.

• Risk Management – we have made significant progress in this area. We have a corporate risk

register, and all departments now have their own risk registers. Actions to mitigate risks are being built into service and business plans. This will remain a significant control issue until we are happy it is fully embedded into our processes, which is planned to be completed during 2005/06.

• Performance Management – again we have made good progress, but this is a longer term issue

about changing people’s attitudes as well as processes. Further improvement is needed if we are to have appropriate assurance from our processes.

• Partnerships – this is an ever developing area, with continued pressure from government

towards partnership-based service delivery. Our progress to date has been recognised by the Audit Commission. Nevertheless we intend to supplement this area with a review of the arrangements in place for each of the most significant partnerships during the coming year.

• Malware (or unwanted software) – the computer auditors identified that our security

arrangements did not protect our systems and network against “malware”, “spyware” and other such unwanted software. This is now being widely recognised as a common threat to all such computer systems which current virus checking software did not provide protection

11

against. This is now being rectified with the deployment of additional protective software over the next two months.

• Capacity – the Council’s capacity, particularly at the centre, to respond to government and

other initiatives, was highlighted in the CPA report in 2002. Since then we have taken a number of steps to improve our capability in this area. Longer term, we envisage resolving this issue through the implementation of the People Strategy. This contains a number if developments which will all help improve the Council’s capacity to respond to change, at both departmental and corporate levels.

• Children’s service – we are required to draw together all services for children into a single

service. This will combine activities from both the education and social services fields, and represents a significant change for the Council. We have a co-ordination team responsible for overseeing this development and have recently appointed a new ‘head of service’.

• Property Capital Programme – the Council have identified concerns over the way capital

schemes are controlled. In practice, all the costs relating to a scheme must be funded, and the source of that funding properly approved. Following a review, it became apparent that staff were using two sources of information to control the matching of approved funding to fund scheme cost. The two sources of information were not regularly compared, which led to confusion, increasing likelihood of incorrect management information being provided. The current arrangements have been reviewed and the agreed way forward rationalises the information holding to a single set of records, using temporary measures to rectify the immediate concerns over control. It is planned to have a new monitoring system for capital schemes in place by April 2006.

• Treasury Management – the Council has identified some concerns over the accounting support

to the Treasury Management function. The Council has external investments totalling almost £160m and borrowing of almost £292m. The Council is very active in exercising its Treasury Management function and there are a large number of transactions throughout the year. It is planned to have appropriate accountancy support in place, to provide regular reconciliations of the balances to the main accounting system and produce monthly reports for management over the next two months.

John Lobb Peter Stethridge Leader Chief Executive

12

8 Statement of Responsibilities & Certification of the Statement of Accounts The following statement describes the respective responsibilities of the County Council and the County Treasurer for the accounts. The County Treasurer is responsible for:

• the preparation of the Council’s statement of accounts and the accounts of the Cornwall County Council Pension Fund so as to present fairly the financial position at the accounting date and its income and expenditure for the year;

• making reasonable and prudent judgements and estimates;

• complying in all material aspects with the Code of Practice on Local Authority Accounting in Great Britain and applying accounting policies consistently;

• keeping proper, up to date, accounting records;

• taking reasonable steps for the prevention and detection of fraud and other irregularities. The County Council is responsible for:

• securing appropriate arrangements for the proper administration of its financial affairs ensuring that the nominated officer, namely the County Treasurer, has responsibility for them;

• managing its affairs so as to ensure the economic, effective and efficient use of resources and the safeguarding of assets.

Certification by Treasurer I certify that, in my opinion, the Statement of Accounts presents fairly the financial position of Cornwall County Council at 31 March 2005, and its income and expenditure for the year then ended.

Frank Twyning MBA, FCCA, CPFA County Treasurer Date 14 June 2005 Certification by Chairman of Standards Committee I confirm that these accounts were approved by the Standards Committee as Agenda Item Number 7 dated 27 June 2005. Chairman of Standards Committee Date 27 June 2005 Further Information Further information about the accounts is available from the Treasurers’ Department, Cornwall County Council, New County Hall, Truro, TR1 3AY. Interested members of the public have a statutory right to inspect the accounts before the audit is completed. For the 2004-2005 accounts the inspection period was 4 July 2005 to 29 July 2005. These dates were advertised in the local press and on the Council’s website.

13

9 Auditors’ Report to Cornwall County Council

I have audited the financial statements on pages 16 to 66 and 81 to 88 which have been prepared in accordance with the accounting policies applicable to local authorities as set out on pages 81 to 88 and the Pension Fund Accounts, on pages 69 to 78 which have been prepared in accordance with the accounting policies applicable to pension funds set out on page 71.

This report is made solely to Cornwall County Council in accordance with part II of the Audit Commission Act 1998 and for no other purpose, as set out in paragraph 54 of the Statement of Responsibilities of Auditors and of Audited Bodies, prepared by the Audit Commission.

Respective Responsibilities of County Treasurer and Auditor

As described on page 12 the County Treasurer is responsible for the preparation of the Statement of Accounts in accordance with the Statement of Recommended Practice on Local Authority Accounting in the United Kingdom 2004. My responsibilities, as independent auditor are established by statute, the Code of Audit Practice issued by the Audit Commission and my profession’s ethical guidance.

I report to you my opinion as to whether the financial Statement of Accounts present fairly: • the financial position of the Council and its income and expenditure for the year, • the financial transactions of its Pension Fund during the year and the amount and disposition of

the Fund’s assets and liabilities, other than liabilities to pay pensions and benefits after the end of the scheme year.

I review whether the Statement on Internal Control on page 8 reflects compliance with CIPFA’s guidance `The Statement on Internal Control in Local Government: Meeting the Requirements of the Accounts and Audit Regulations 2003’ published on 2 April 2004. I report if it does not comply with proper practices specified by CIPFA or if the Statement is misleading or inconsistent with other information I am aware of from our audit of the financial statements. I am not required to consider whether the Statement on Internal Control covers all risks and controls, or to form an opinion on the effectiveness of the Council’s corporate governance procedures or its risk and control procedures. My review was not performed for any purpose connected with any specific transaction and should not be relied upon for any such purpose.

I read the other information published with the Statement of Accounts and consider the implications for my report if I become aware of any apparent misstatements or material inconsistencies with the Statement of Accounts.

Basis of Opinion

I conducted my audit in accordance with the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission, which requires compliance with relevant auditing standards issued by the Accounting Practices Board.

An audit includes examination, on a test basis, of evidence relevant to the amounts and disclosures in the financial statements. It also includes an assessment of the significant estimates and judgements made by the Council in the preparation of the financial statements, and of whether the accounting policies are appropriate to the council’s circumstances, consistently applied and adequately disclosed. I planned and performed our audit so as to obtain all the information and explanations which I considered necessary in order to provide us with sufficient evidence to give reasonable assurance that the Statement of Accounts is free from material misstatement, whether caused by fraud or other irregularity or error. In forming my opinion, I evaluated the overall adequacy of the presentation of the information in the financial statements.

Opinion on the Authority’s Accounts

In my opinion the Statement of Accounts present fairly the financial position of Cornwall County Council as at 31 March 2005 and its income and expenditure for the year then ended.

In my opinion the financial statements present fairly the financial transactions of Cornwall County Council Pension Fund during the year ended 31 March 2005, and the amount and disposition at that date of its assets and liabilities, other than liabilities to pay pensions and benefits after the end of the scheme year.

14

9 Auditors’ Report to Cornwall County Council (continued)

Certificate

I certify that I have completed the audit of the accounts in accordance with the requirements of the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission.

Alun Williams 19 September 2005 District Auditor Audit Commission 5-6 Blenheim Court Matford Business Park Lustleigh Close Exeter EX2 8PW

15

MMaaiinn FFiinnaanncciiaall SSttaatteemmeennttss

16

Main Financial Statement

17

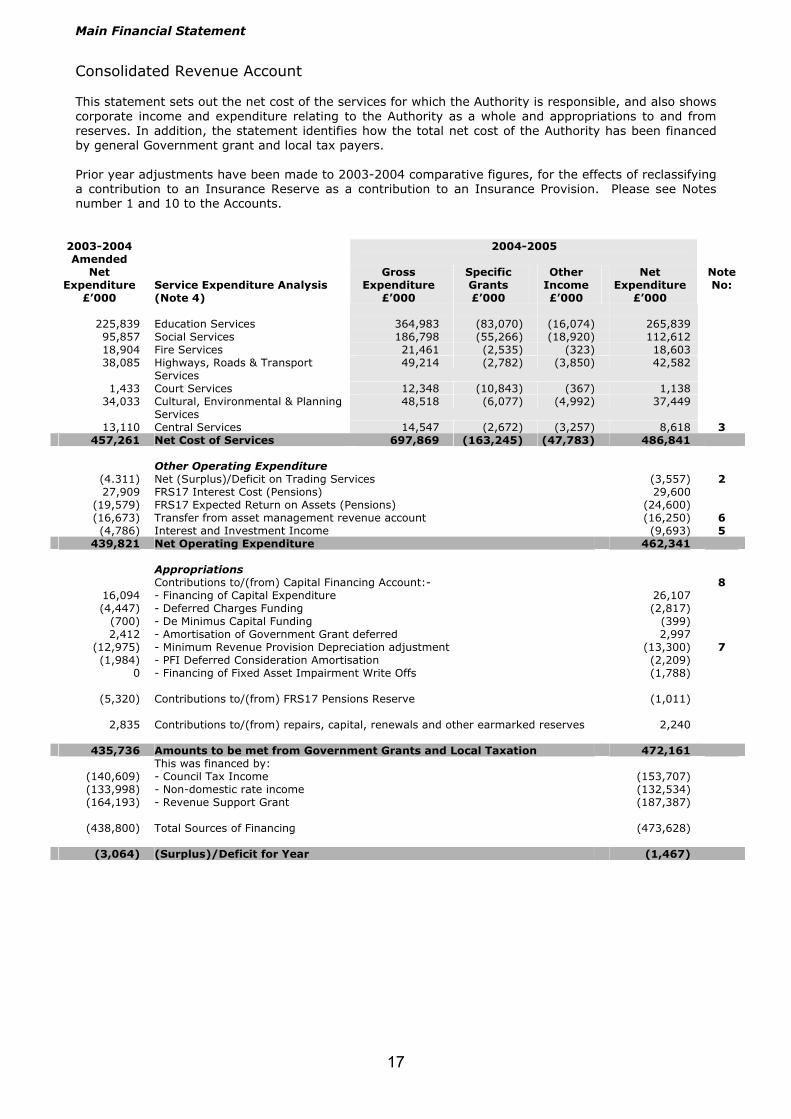

Consolidated Revenue Account This statement sets out the net cost of the services for which the Authority is responsible, and also shows corporate income and expenditure relating to the Authority as a whole and appropriations to and from reserves. In addition, the statement identifies how the total net cost of the Authority has been financed by general Government grant and local tax payers. Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying a contribution to an Insurance Reserve as a contribution to an Insurance Provision. Please see Notes number 1 and 10 to the Accounts.

2004-2005

2003-2004 Amended

Net Expenditure

£’000

Service Expenditure Analysis (Note 4)

Gross Expenditure

£’000

Specific Grants £’000

Other Income £’000

Net Expenditure

£’000

NoteNo:

225,839 Education Services 364,983 (83,070) (16,074) 265,839 95,857 Social Services 186,798 (55,266) (18,920) 112,612 18,904 Fire Services 21,461 (2,535) (323) 18,603 38,085 Highways, Roads & Transport

Services 49,214 (2,782) (3,850) 42,582

1,433 Court Services 12,348 (10,843) (367) 1,138 34,033 Cultural, Environmental & Planning

Services 48,518 (6,077) (4,992) 37,449

13,110 Central Services 14,547 (2,672) (3,257) 8,618 3 457,261 Net Cost of Services 697,869 (163,245) (47,783) 486,841

Other Operating Expenditure

(4.311) Net (Surplus)/Deficit on Trading Services (3,557) 2 27,909 FRS17 Interest Cost (Pensions) 29,600

(19,579) FRS17 Expected Return on Assets (Pensions) (24,600) (16,673) Transfer from asset management revenue account (16,250) 6 (4,786) Interest and Investment Income (9,693) 5

439,821 Net Operating Expenditure 462,341 Appropriations Contributions to/(from) Capital Financing Account:- 8

16,094 - Financing of Capital Expenditure 26,107 (4,447) - Deferred Charges Funding (2,817)

(700) - De Minimus Capital Funding (399) 2,412 - Amortisation of Government Grant deferred 2,997

(12,975) - Minimum Revenue Provision Depreciation adjustment (13,300) 7 (1,984) - PFI Deferred Consideration Amortisation (2,209)

0 - Financing of Fixed Asset Impairment Write Offs (1,788)

(5,320) Contributions to/(from) FRS17 Pensions Reserve (1,011)

2,835 Contributions to/(from) repairs, capital, renewals and other earmarked reserves 2,240

435,736 Amounts to be met from Government Grants and Local Taxation 472,161 This was financed by:

(140,609) - Council Tax Income (153,707) (133,998) - Non-domestic rate income (132,534) (164,193) - Revenue Support Grant (187,387)

(438,800) Total Sources of Financing (473,628)

(3,064) (Surplus)/Deficit for Year (1,467)

Main Financial Statement

18

2003-2004

£’000 Treatment of (Surplus)/Deficit 2004-2005

£’000 i) Contributions to/(from) County Fund Balances:

832 - Contributions to/(from) General Reserve 1,272 1,569 - Contributions to/(from) Portfolios Budget Equalisation Reserves (61)

663 ii) Contributions to/(from) Schools Reserve 256 3,064 1,467

Changes in County Fund & School Balances County Fund – Usable Reserve Balances: (a) General Reserve

7,454 Balance as at 1 April 2004 8,286 832 Net Contribution (to)/from Revenue Account 1,272

8,286 Balance as at 31 March 2005 9,558 (b) Budget Equalisation Reserves

2,933 Balance as at 1 April 2004 4,502 1,569 Net Contribution(to)/from Revenue Account (61) 4,502 Balance as at 31 March 2005 4,441

12,788 Total County Fund Balances 13,999 Schools Reserves

18,277 Balance as at 1 April 2004 18,940 663 Net Contribution (to)/from Revenue Account 256

18,940 Balance as at 31 March 2005 19,196 (see additional disclosed notes to balance sheet)

31,728 Total 33,195

Main Financial Statement

19

Consolidated Balance Sheet The Consolidated Balance Sheet summarises the financial position of the whole Council. It shows the value of the Council’s assets and liabilities at the end of the financial year (31 March 2005). Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying a contribution to an Insurance Reserve as a contribution to an Insurance Provision and reclassifying Receipts in Advance as Capital Grant Unapplied. Please see Notes 1 and 10 to the Accounts.

2005 Amended

2004 Note

£’000 £’000 £’000 No: Net Fixed Assets 11 Intangible Fixed Assets - - Tangible Fixed Assets Operational Assets Other land and buildings 536,591 529,987 Vehicles, plant, furniture & equipment 18,209 16,940 Infrastructure 181,385 157,938 Community Assets 2,289 1,611 Non-operational assets Surplus Assets, held for disposal 6,671 4,192 Assets under construction 34,311 22,321 Total Net Fixed Assets 779,456 732,989 PFI Scheme Deferred Consideration 45,953 42,082 12 PFI Scheme Residual Values 8,984 5,394 13 Long Term Investments 93,791 12,984 15 Long Term Debtors 12,154 18,197 17 Total Long Term Assets 940,338 811,646 Current Assets Stocks and Work in Progress 2,263 2,421 16 Debtors and Payments in advance 41,909 30,461 17 Short Term Temporary Investments 65,479 117,150 15 Cash in hand and in transit 128 94 Total Current Assets 109,779 150,126 Current Liabilities Short Term Borrowing (18,818) (270) Creditors (57,146) (71,091) 18 Cash Overdrawn (18,145) (12,094) Total Current Liabilities (94,109) (83,455) 15,670 66,671 Total Assets less Current Liabilities 956,008 878,317 Long Term Borrowing (273,262) (230,568) 19 FRS17 Pensions Liability (269,600) (195,750) 37 Creditors due after one year (548) (123) 20 Provisions (6,290) (6,085) 21 (549,700) (432,526) Total Assets less Liabilities 406,308 445,791 Represented by: Government Grants Deferred Account 98,317 78,942 22 Capital Grant Unapplied 7,549 8,283 22 FRS17 Pensions Reserve (269,600) (195,750) 37 Fixed Asset Restatement Account 321,346 318,489 22 Capital Financing Account 150,871 140,288 22 Reserves - Other Specific 79,715 77,220 22 - Usable Capital Receipts 4,111 5,531 22 Revenue Balances County Fund – Usable Reserves 13,999 12,788 22 Total Equity 406,308 445,791

Main Financial Statement

20

Statement of Total Movements in Reserves The statement of total movements in reserves brings together all the recognised gains and losses of the authority during the period and identifies those which have and have not been recognised in the Consolidated Revenue Account. The statement separates the movements between revenue and capital reserves. 2004-05 2003-04 Note Original Prior Year

Adjustment Amended

£’000 £’000 £’000 £’000 £’000 No: Surplus/(deficit) for the year 1,467 3,064 - 3,064 Add back movements on specific revenue reserve

2,240 3,835 (1,000) 2,835

Movement on FRS17 Pension Reserve

(1,011) (5,320) - (5,320)

Total increase/(decrease) in revenue resources

2,696 1,579 (1,000) 579 22

Increase/(decrease) in usable capital receipts

(1,420) (10) - (10)

Increase/(decrease) in unapplied capital grants and contributions

(734) 1,571 608 2,179

Total increase/(decrease) in realised capital resources (note i)

(2,154) 1,561 608 2,169 22

FRS17 Actuarial gains/(losses) (72,839) 31,773 - 31,773 Gains/(losses) on revaluation of fixed assets

3,279 3,156 - 3,156

Impairment losses on fixed assets due to general changes in prices

0 0 - 0

Total increase/(decrease) in unrealised value of fixed assets (note ii)

(69,560) 34,929 - 34,929 22

Value of assets sold, disposed of or decommissioned (note iii)

(422) (798) - (798) 22

Capital receipts set aside 2,388 1,669 - 1,669 Revenue resources set aside 8,195 (1,600) - (1,600) Movement on Grants in year 19,375 13,308 - 13,308 Total Increase/(decrease) in amounts set aside to finance capital investment (note iv)

29,958 13,377 - 13,377 22

Total recognised gains and losses

(39,482) 50,648 (392) 50,256

Main Financial Statement

21

Cash Flow Statement 2005 2004 Note £’000 £’000 £’000 No: Revenue Activities Cash Outflows Cash Paid on behalf of employees 366,529 340,662 Other operating costs 392,083 320,434 758,612 661,096 Cash inflows Council Tax (153,707) (140,609) Non-Domestic Rates (132,534) (133,998) Revenue Support Grant (187,387) (164,193) Other Government Grants (163,245) (130,983) Cash Received from Goods or Services (142,339) (143,254) (779,212) (713,037) Revenue Activities net cash flow (20,600) (51,941) 26 Servicing of Finance Cash Outflows Interest paid 12,567 12,341 Cash Inflows Interest Received (13,186) (5,364) (619) 6,977 (21,219) (44,964) Capital Activities Cash Outflows Purchase of fixed assets 87,507 79,295 Other capital cash payments 0 0 87,507 79,925 Cash Inflows Sale of fixed assets (572) (1,659) Other capital cash income 0 (144) Capital grants received (27,593) (20,247) (28,165) (22,050) 59,342 57,245 Net Cash outflow before financing 38,123 12,281 Financing Cash Outflows Repayments of amounts borrowed 53,108 33,646 Short Term Investments (51,671) 6,300 Long Term Investments 80,807 9,880 Cash Inflows New Loans Raised (114,350) (58,600) (32,106) (8,774) Decrease in cash 6,017 3,507

Main Financial Statement

22

23

NNootteess ttoo MMaaiinn FFiinnaanncciiaall

SSttaatteemmeennttss

24

Notes to Main Financial Statements

25

The following notes provide more detailed information in order to assist in the interpretation of the main Financial Accounts. Note 1 Prior Year Adjustments to Consolidated Revenue Account Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying a contribution to an Insurance Reserve as a contribution to an Insurance Provision. Note 2 Trading Services The Council’s main Trading Services are: • CORMAC – who provide construction and maintenance of the County’s highways and footpaths. • Planning, Transportation & Estates Consultancies – who provide design services and engineering

services for road schemes, bridges etc. • Workshops – who repair and maintain the Council’s vehicles and plant. • Commercial Services – who provide cleaning and grounds maintenance for schools and other parts of

the Council. • Central Transport Organisation – who provide fleet management of the Council’s vehicles and plant. • Education Business Units – providing specialist services (for example music lessons and outdoor

education) and advisory support to front line education services.

Other Trading Services include the following: • Notter Bridge Training Unit • Tremorvah Industries Trading Unit Trading Services Turnover

£’000

Expenditure

£’000

(Surplus)/deficit

2004-2005 £’000

(Surplus)/ deficit

2003-2004 £’000

CORMAC 42,479 42,088 (391) (777) Planning, Transport & Estates Consultancies 22,513 22,118 (395) (572) Workshops 2,997 2,970 (27) (52) Commercial Services 10,802 10,880 78 (82) Central Transport Organisation 9,627 6,755 (2,872) (2,664) Education Business Units 10,822 10,865 43 (54) Other Trading Services 3,990 3,997 7 (110) Total 103,230 99,673 (3,557) (4,311)

Note 3 Central Services An analysis of Central Services expenditure is shown in the table below. 2004-2005

£’000

Original 2003-2004

£’000

Contribution to Provision Adjustment

£’000

Amended 2003-2004

£’000

Corporate & Democratic Costs Democratic Representation 1,811 1,642 - 1,642 Corporate Management 2,348 2,283 - 2,283 Non Distributable Costs 910 5,255 - 5,255 Central Services to the Public 878 780 - 780 Other Income & Expenditure 2,671 2,150 1,000 3,150 8,618 12,110 1,000 13,110

Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying a £1.0m contribution to an Insurance Reserve as a £1.0m contribution to an Insurance Provision. From 1 April 2002 the past service element of employer’s pension costs has been increased significantly by the Pension Fund actuary from 0.8% to 2.1%.

Notes to Main Financial Statements

26

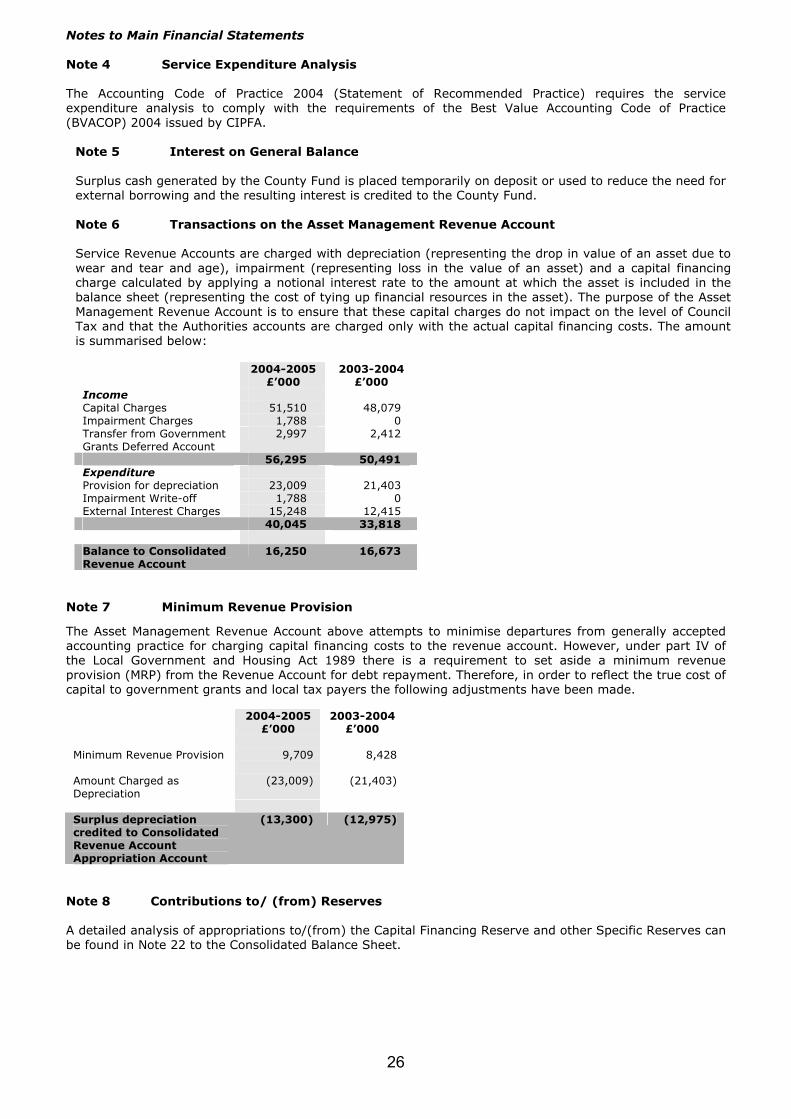

Note 4 Service Expenditure Analysis The Accounting Code of Practice 2004 (Statement of Recommended Practice) requires the service expenditure analysis to comply with the requirements of the Best Value Accounting Code of Practice (BVACOP) 2004 issued by CIPFA.

Note 5 Interest on General Balance Surplus cash generated by the County Fund is placed temporarily on deposit or used to reduce the need for external borrowing and the resulting interest is credited to the County Fund. Note 6 Transactions on the Asset Management Revenue Account Service Revenue Accounts are charged with depreciation (representing the drop in value of an asset due to wear and tear and age), impairment (representing loss in the value of an asset) and a capital financing charge calculated by applying a notional interest rate to the amount at which the asset is included in the balance sheet (representing the cost of tying up financial resources in the asset). The purpose of the Asset Management Revenue Account is to ensure that these capital charges do not impact on the level of Council Tax and that the Authorities accounts are charged only with the actual capital financing costs. The amount is summarised below:

2004-2005 2003-2004

£’000 £’000 Income Capital Charges 51,510 48,079 Impairment Charges 1,788 0 Transfer from Government Grants Deferred Account

2,997 2,412

56,295 50,491 Expenditure Provision for depreciation 23,009 21,403 Impairment Write-off 1,788 0 External Interest Charges 15,248 12,415 40,045 33,818 Balance to Consolidated Revenue Account

16,250 16,673

Note 7 Minimum Revenue Provision

The Asset Management Revenue Account above attempts to minimise departures from generally accepted accounting practice for charging capital financing costs to the revenue account. However, under part IV of the Local Government and Housing Act 1989 there is a requirement to set aside a minimum revenue provision (MRP) from the Revenue Account for debt repayment. Therefore, in order to reflect the true cost of capital to government grants and local tax payers the following adjustments have been made. 2004-2005

£’000 2003-2004

£’000 Minimum Revenue Provision 9,709 8,428 Amount Charged as Depreciation

(23,009) (21,403)

Surplus depreciation credited to Consolidated Revenue Account Appropriation Account

(13,300) (12,975)

Note 8 Contributions to/ (from) Reserves A detailed analysis of appropriations to/(from) the Capital Financing Reserve and other Specific Reserves can be found in Note 22 to the Consolidated Balance Sheet.

Notes to Main Financial Statements

27

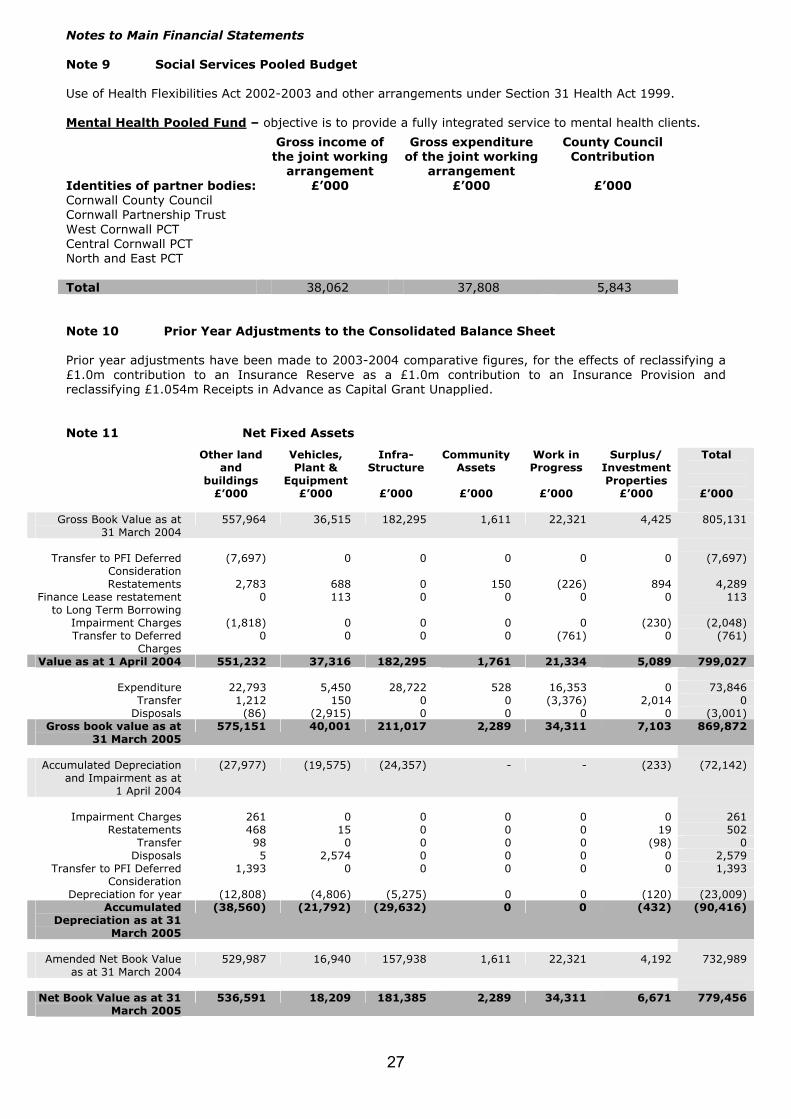

Note 9 Social Services Pooled Budget Use of Health Flexibilities Act 2002-2003 and other arrangements under Section 31 Health Act 1999. Mental Health Pooled Fund – objective is to provide a fully integrated service to mental health clients.

Gross income of the joint working

arrangement

Gross expenditure of the joint working

arrangement

County Council Contribution

Identities of partner bodies: £’000 £’000 £’000 Cornwall County Council Cornwall Partnership Trust West Cornwall PCT Central Cornwall PCT North and East PCT

Total 38,062 37,808 5,843 Note 10 Prior Year Adjustments to the Consolidated Balance Sheet Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying a £1.0m contribution to an Insurance Reserve as a £1.0m contribution to an Insurance Provision and reclassifying £1.054m Receipts in Advance as Capital Grant Unapplied. Note 11 Net Fixed Assets

Other land and

buildings £’000

Vehicles, Plant &

Equipment £’000

Infra-Structure

£’000

Community Assets

£’000

Work in Progress

£’000

Surplus/ Investment Properties

£’000

Total

£’000

Gross Book Value as at 31 March 2004

557,964 36,515 182,295 1,611 22,321 4,425 805,131

Transfer to PFI Deferred

Consideration (7,697) 0 0 0 0 0 (7,697)

Restatements 2,783 688 0 150 (226) 894 4,289 Finance Lease restatement

to Long Term Borrowing 0 113 0 0 0 0 113

Impairment Charges (1,818) 0 0 0 0 (230) (2,048) Transfer to Deferred

Charges 0 0 0 0 (761) 0 (761)

Value as at 1 April 2004 551,232 37,316 182,295 1,761 21,334 5,089 799,027

Expenditure 22,793 5,450 28,722 528 16,353 0 73,846 Transfer 1,212 150 0 0 (3,376) 2,014 0

Disposals (86) (2,915) 0 0 0 0 (3,001) Gross book value as at

31 March 2005 575,151 40,001 211,017 2,289 34,311 7,103 869,872

Accumulated Depreciation

and Impairment as at 1 April 2004

(27,977) (19,575) (24,357) - - (233) (72,142)

Impairment Charges 261 0 0 0 0 0 261

Restatements 468 15 0 0 0 19 502 Transfer 98 0 0 0 0 (98) 0

Disposals 5 2,574 0 0 0 0 2,579 Transfer to PFI Deferred

Consideration 1,393 0 0 0 0 0 1,393

Depreciation for year (12,808) (4,806) (5,275) 0 0 (120) (23,009) Accumulated

Depreciation as at 31 March 2005

(38,560) (21,792) (29,632) 0 0 (432) (90,416)

Amended Net Book Value

as at 31 March 2004 529,987 16,940 157,938 1,611 22,321 4,192 732,989

Net Book Value as at 31

March 2005 536,591 18,209 181,385 2,289 34,311 6,671 779,456

Notes to Main Financial Statements

28

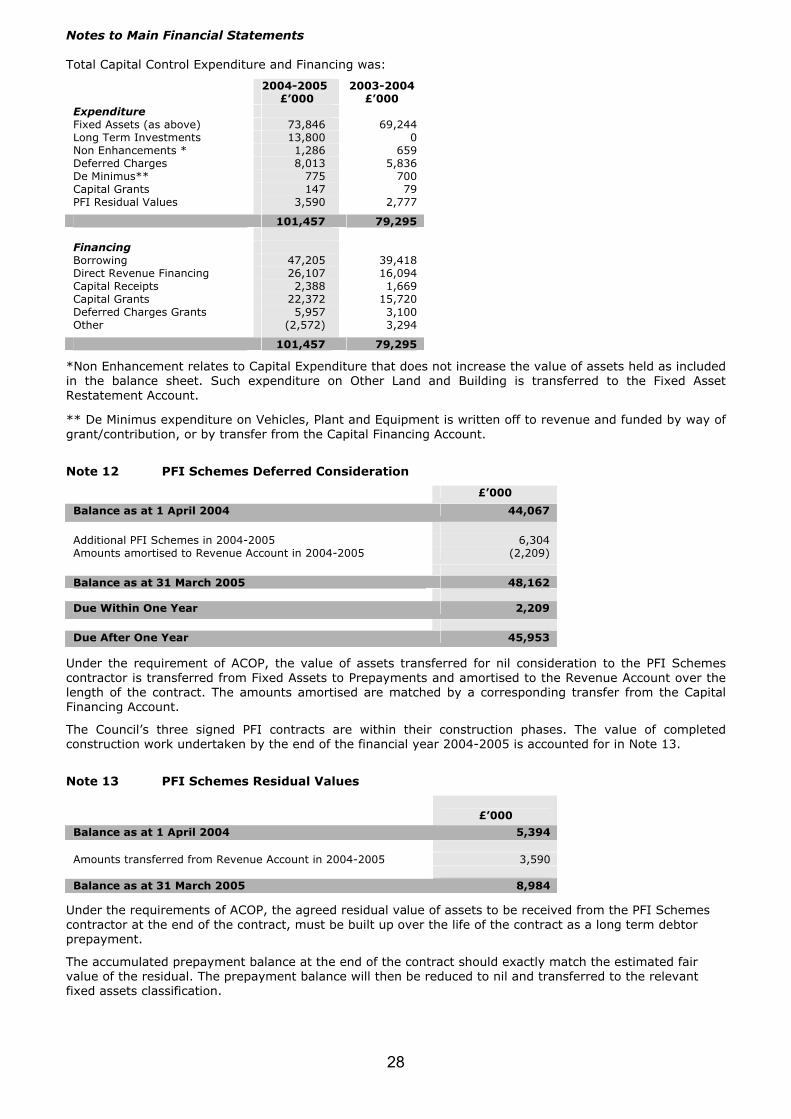

Total Capital Control Expenditure and Financing was:

2004-2005 £’000

2003-2004 £’000

Expenditure Fixed Assets (as above) 73,846 69,244 Long Term Investments 13,800 0 Non Enhancements * 1,286 659 Deferred Charges 8,013 5,836 De Minimus** 775 700 Capital Grants 147 79 PFI Residual Values 3,590 2,777

101,457 79,295 Financing Borrowing 47,205 39,418 Direct Revenue Financing 26,107 16,094 Capital Receipts 2,388 1,669 Capital Grants 22,372 15,720 Deferred Charges Grants 5,957 3,100 Other (2,572) 3,294

101,457 79,295

*Non Enhancement relates to Capital Expenditure that does not increase the value of assets held as included in the balance sheet. Such expenditure on Other Land and Building is transferred to the Fixed Asset Restatement Account.

** De Minimus expenditure on Vehicles, Plant and Equipment is written off to revenue and funded by way of grant/contribution, or by transfer from the Capital Financing Account.

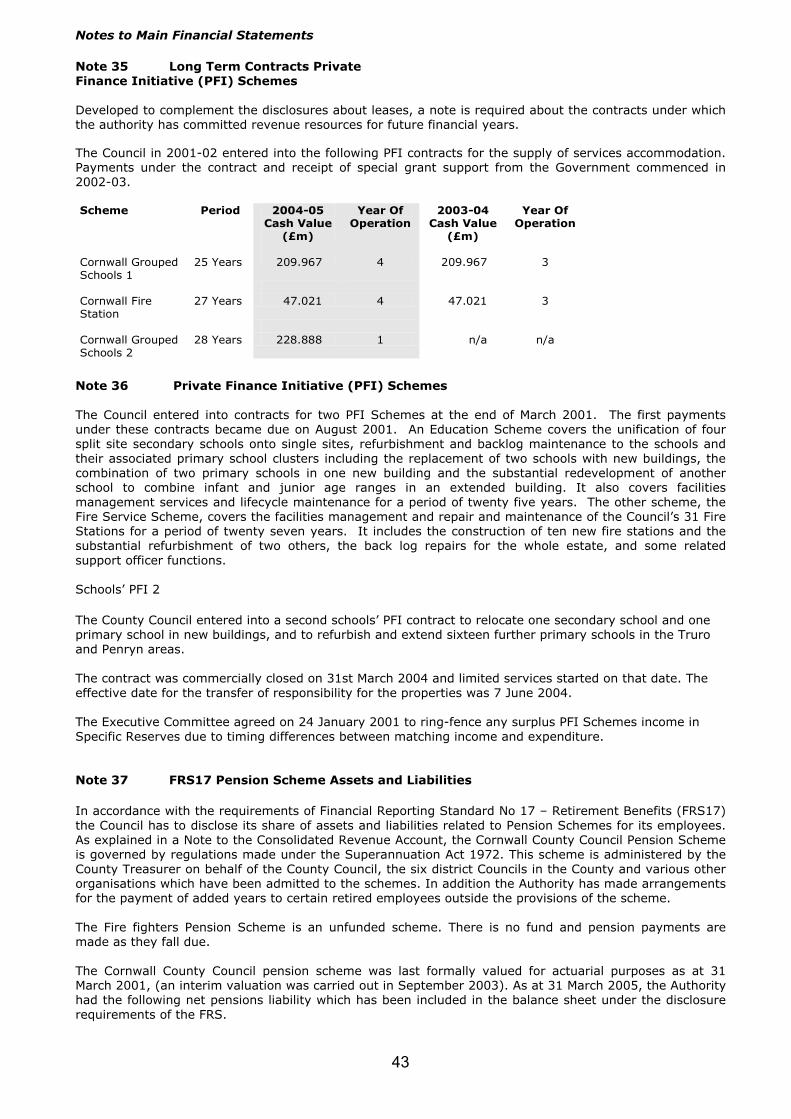

Note 12 PFI Schemes Deferred Consideration

£’000

Balance as at 1 April 2004 44,067

Additional PFI Schemes in 2004-2005 6,304 Amounts amortised to Revenue Account in 2004-2005 (2,209)

Balance as at 31 March 2005 48,162 Due Within One Year 2,209

Due After One Year 45,953

Under the requirement of ACOP, the value of assets transferred for nil consideration to the PFI Schemes contractor is transferred from Fixed Assets to Prepayments and amortised to the Revenue Account over the length of the contract. The amounts amortised are matched by a corresponding transfer from the Capital Financing Account.

The Council’s three signed PFI contracts are within their construction phases. The value of completed construction work undertaken by the end of the financial year 2004-2005 is accounted for in Note 13.

Note 13 PFI Schemes Residual Values

£’000

Balance as at 1 April 2004 5,394 Amounts transferred from Revenue Account in 2004-2005 3,590 Balance as at 31 March 2005 8,984

Under the requirements of ACOP, the agreed residual value of assets to be received from the PFI Schemes contractor at the end of the contract, must be built up over the life of the contract as a long term debtor prepayment.

The accumulated prepayment balance at the end of the contract should exactly match the estimated fair value of the residual. The prepayment balance will then be reduced to nil and transferred to the relevant fixed assets classification.

Notes to Main Financial Statements

29

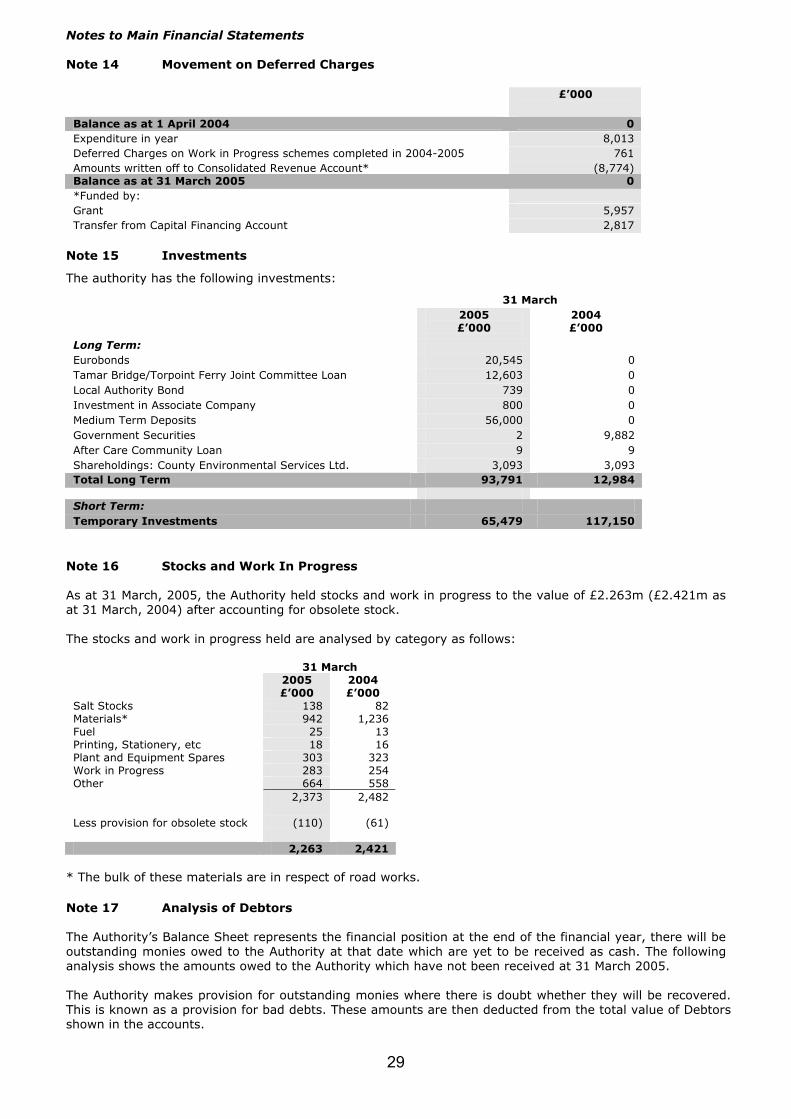

Note 14 Movement on Deferred Charges

£’000

Balance as at 1 April 2004 0 Expenditure in year 8,013 Deferred Charges on Work in Progress schemes completed in 2004-2005 761 Amounts written off to Consolidated Revenue Account* (8,774) Balance as at 31 March 2005 0 *Funded by: Grant 5,957 Transfer from Capital Financing Account 2,817

Note 15 Investments

The authority has the following investments:

31 March 2005

£’000 2004 £’000

Long Term: Eurobonds 20,545 0 Tamar Bridge/Torpoint Ferry Joint Committee Loan 12,603 0 Local Authority Bond 739 0 Investment in Associate Company 800 0 Medium Term Deposits 56,000 0 Government Securities 2 9,882 After Care Community Loan 9 9 Shareholdings: County Environmental Services Ltd. 3,093 3,093 Total Long Term 93,791 12,984 Short Term: Temporary Investments 65,479 117,150

Note 16 Stocks and Work In Progress As at 31 March, 2005, the Authority held stocks and work in progress to the value of £2.263m (£2.421m as at 31 March, 2004) after accounting for obsolete stock. The stocks and work in progress held are analysed by category as follows:

31 March 2005

£’000 2004 £’000

Salt Stocks 138 82 Materials* 942 1,236 Fuel 25 13 Printing, Stationery, etc 18 16 Plant and Equipment Spares 303 323 Work in Progress 283 254 Other 664 558 2,373 2,482 Less provision for obsolete stock (110) (61)

2,263 2,421

* The bulk of these materials are in respect of road works. Note 17 Analysis of Debtors The Authority’s Balance Sheet represents the financial position at the end of the financial year, there will be outstanding monies owed to the Authority at that date which are yet to be received as cash. The following analysis shows the amounts owed to the Authority which have not been received at 31 March 2005. The Authority makes provision for outstanding monies where there is doubt whether they will be recovered. This is known as a provision for bad debts. These amounts are then deducted from the total value of Debtors shown in the accounts.

Notes to Main Financial Statements

30

31 March 2005

£’000

2004

£’000

Short Term: Amounts falling due in one year Government Departments 4,540 5,269 Sundry Debtors 30,317 19,535 Payments in advance* 8,090 6,615 42,947 31,419 Less Provision for bad debts (1,038) (958) 41,909 30,461 Long Term: Amounts falling due after one year

Car loans to employees 229 205 Other** 11,925 17,992 12,154 18,197

* Includes £2.209m relating to PFI Schemes Deferred Consideration (see note 12) ** This balance includes: • An amount of £1.545m (2002-03 £2.156m) that the Council has advanced to the Millennium Project.

This is being repaid in instalments commencing October 2001 • An amount of £0.283m (2002-03 £0.283m) relating to the Cornwall Enterprise Loan (£0.266m) and

Brussel’s Office Bond (£0.017m). • Amounts totalling £0.741m relating to Education Services (2003-04 £2.953m) • Amounts totalling £1.309m relating to Social Services (2003-04 £1.045m) • Amounts totalling £7.762m relating to premiums on debt rescheduling (2003-04 £11.555m)

Note 18 Analysis of Creditors The Authority’s Balance Sheet represents the financial position at the end of the financial year, there will be outstanding monies that the Authority owes at that date which have yet to be paid. For example for goods received at the end of March where invoices have not been paid. The following analysis shows the amounts owed by the Authority which have not been paid as at 31 March 2005. 31 March 2005

£’000

Original2004

£’000

Receipts in Advance

Adjustment £’000

Amended2004

£’000

Inland Revenue 9,599 9,165 - 9,165 Sundry Creditors 34,642 33,453 - 33,453 Receipts in Advance 12,895 11,374 (1,054) 10,320 57,136 53,992 (1,054) 52,938 Long Term Borrowing Repayable within one year (see note 19)

10 18,153 - 18,153

57,146 72,145 (1,054) 71,091

Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying £1.054m Receipts in Advance as Capital Grant Unapplied.

Notes to Main Financial Statements

31

Note 19 Long term Borrowing The table below shows the Authority’s borrowing by lender, and by maturity. Total Outstanding as at 31 March

Range of Interest rates

payable %

2005 £’000

2004 £’000

Source of Loan External Borrowing Lawn Tennis Association 0 100 0 Other Local Authorities 4.00 - 4.13 0 7,350 Public Works Loan Board-Maturity 4.00 – 7.125 168,960 170,960 Public Works Loan Board-Instalment 3.00 – 4.25 12,612 10 Market Loans 3.30 – 4.25 91,600 70,401 Total Long Term Borrowing 273,272 248,721 An analysis of loans by maturity: External Borrowing * Maturing within one year 10 18,153 Maturing within 1-2 years 10 5,003 Maturing within 2-5 years 30 5 Maturing within 5-10 years 57 7,000 Maturing in more than 10 years 273,165 218,560 273,272 248,721 Payable within one year (see note 18) 10 18,153 Payable after one year 273,262 230,568 273,272 248,721

Note 20 Creditors Due After One Year 31 March 2005

£’000 2004 £’000

Sundry 548 123 548 123

Note 21 Provisions Provisions are required for any financial liabilities or losses which are likely or certain to be incurred but the amounts or the dates on which they will arise is uncertain. All provisions are charged to the appropriate service and can be used only for the purpose for which they were established, except where a review to determine the appropriateness of the level of the charge and the balance of the provision requires a change. Original

Balance as at 1 April,

2004 £’000

Insurance Reserve

Adjustment

£’000

Amended Balance as at 1 April,

2004 £’000

Additions

£’000

Deductions

£’000

Balance as at 31 March,

2005

£’000 Insurance Claims 3,990 1,000 4,990 437 (170) 5,257 FEFC Grant Clawback 341 0 341 0 0 341 Parts Initiative 10 0 10 0 0 10 Unused Leave 0 0 0 31 0 31 Contract Penalties 75 0 75 0 (12) 63 Future Liabilities 669 0 669 25 (106) 588 5,085 1,000 6,085 493 (288) 6,290

32

Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying a £1.0m contribution to an Insurance Reserve as a £1.0m contribution to an Insurance Provision. Insurance Claims

When an insurance claim is received the possible cost of the claim is estimated by the claims handler and a provision for that cost placed in the Insurance Fund. Insurance claims can take up to 10 years to finalise, during which time the potential cost to the Authority remains. When the claim is finalised the actual cost is met from the provision. Education FEFC Grant Clawback

The Adult Education Service receives FEFC funding (approximately £1.5m p.a.) for Vocational Adult Education schedule 2 courses. This funding is measured by a complex formula which determines a number of units by which authorities are funded. This provision is to allow for variations in funding in future years and for the increased participation in schedule 2 courses.

Future Liabilities

Consultancies:

The provision of £0.070m for potential losses due to disputed items in external contracts was fully utilised in 2004-2005.

Education:

The provision of £0.034m for variations in the Schools Meals Contract was fully utilised in 2004-2005. A provision of £0.025m for Student Awards agreed but not yet paid out was made in 2004-2005.

CORMAC:

This provision of £0.563m relates to the major works area of the Council’s Trading Organisation (CORMAC) such as surfacing/surface dressing, major road schemes, basic highway maintenance and the reinstatement of waste disposal sites. Contract Penalties

This provision of £0.063m relates to PFI contract penalty deductions for non-performance of certain tasks by the Council’s Commercial Services. Parts Initiative

Cornwall County Council workshops will have to pay a one off payment to Hendy Lennox Ltd, or bear any loss of the parts venture, which terminated on 31/03/03. A provision of £0.010m has therefore been made.

Unused Leave

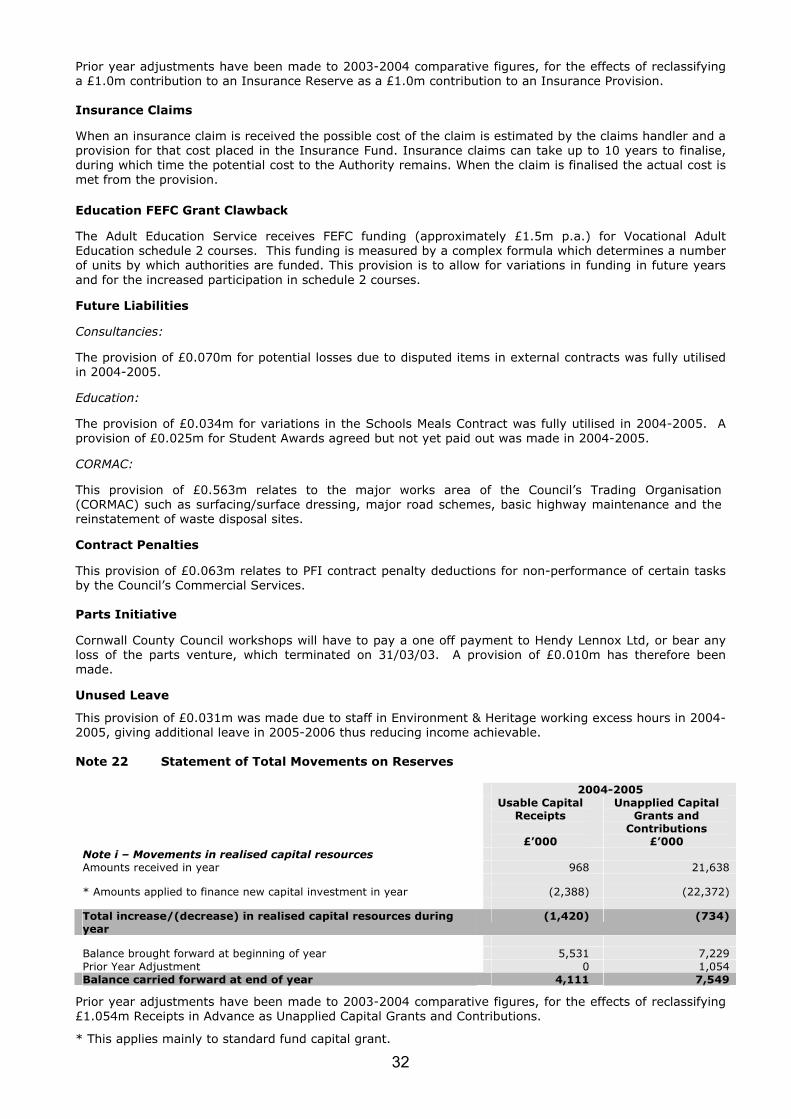

This provision of £0.031m was made due to staff in Environment & Heritage working excess hours in 2004-2005, giving additional leave in 2005-2006 thus reducing income achievable. Note 22 Statement of Total Movements on Reserves 2004-2005 Usable Capital

Receipts

£’000

Unapplied Capital Grants and

Contributions £’000

Note i – Movements in realised capital resources Amounts received in year 968 21,638 * Amounts applied to finance new capital investment in year (2,388) (22,372) Total increase/(decrease) in realised capital resources during year

(1,420) (734)

Balance brought forward at beginning of year 5,531 7,229 Prior Year Adjustment 0 1,054 Balance carried forward at end of year 4,111 7,549

Prior year adjustments have been made to 2003-2004 comparative figures, for the effects of reclassifying £1.054m Receipts in Advance as Unapplied Capital Grants and Contributions.

* This applies mainly to standard fund capital grant.

Notes to Main Financial Statements

33

2004-2005 2004-2005 Capital

Financing Account £’000

Government Grants

Deferred £’000

Totals

£’000 Note iv – Movements in amounts set aside to finance capital investment

Capital receipts set aside in year: - reserved receipts 0 0 0 - useable receipts applied 2,388 0 2,388 Total capital receipts set aside in year 2,388 0 2,388 PFI Deferred Consideration Amortised (2,209) 0 (2,209) Revenue resources set aside in year: - capital expenditure financed from revenue 23,704 0 23,704 - reconciling amount for provisions for loan repayment (13,300) 0 (13,300) Total revenue resources set aside in year 8,195 0 8,195 Grants applied to capital investment in year 0 22,372 22,372 Amounts credited to the Asset Management Revenue Account

0 (2,997) (2,997)

Total movement of grants in year 0 19,375 19,375 Total increase/(decrease) in amounts set aside to finance capital/investment

Total movement on Account in year 10,583 19,375 Balance brought forward at begininning of year 140,288 78,942 Balance carried forward at end of year 150,871 98,317

Revenue Reserves The Revenue Reserves can be used to meet capital or revenue expenditure. However, the sum of £79.715m under the heading of “specific reserves” has been earmarked for specific purposes. A more detailed analysis of these reserves is shown against note (d). For additional information, a detailed analysis of the transactions against the Fixed Asset Restatement Account, Capital Financing Account and Usable Capital Receipts Reserve appear below:

2004-2005 Fixed Asset

Restatement Account £’000

Note ii – Movements in unrealised value of fixed assets Gains/losses on revaluation of assets in year 3,279 Impairment losses due to general changes in prices in year 0 Total increase/(decrease) in unrealised capital resources in year 3,279

Note iii – Value of assets sold, disposed of or decommissioned

Amounts written off asset balances for disposals in year (422) Total movement on reserve in year 2,857 Balance brought forward at beginning of year 318,489 Balance carried forward at end of year 321,346

Notes to Main Financial Statements

34

Note (a) Fixed Asset Restatement Account

Note (b) Capital Financing Account The Capital Financing Account contains the amounts of capital expenditure financed from revenue, capital receipts and capital grants, relating to non depreciable assets, e.g. land. It also contains appropriations from the revenue account for differences between the authority’s MRP and depreciation charges.

Note (c) Usable Capital Receipts Reserve Income from the sale of fixed assets for example land and buildings is credited to the Usable Receipts Reserve. These receipts can be used to pay for new capital expenditure. Any balance remains in this account.

Note (d) Specific Reserves Insurance Original Reserve Amended 2004-2005 2003-2004 Adjustment 2003-2004 £’000 £’000 £’000 £’000 Usable: Capital Reserve 12,542 16,788 - 16,788 Other Specific Reserves* 23,316 27,728 (1,000) 26,728

(excluding P.F.I.)

Non Usable: LMS School** 19,196 18,940 - 18,940 Sub-total 55,054 63,456 (1,000) 62,456 P.F.I. Reserve 24,661 14,764 - 14,764 Total 79,715 78,220 (1,000) 77,220

* These reserves are for specific purposes such as repairs and renewals, I.T. and computing renewals and upgrades, economic regeneration and corporate objectives (see Note (e)). ** This amount includes a sum £0.273m representing an amalgamation of overspend at 13 schools.

£’000 Balance as at 1 April 2004 318,489 Non Enhancement Capital Expenditure (1,512) Restatments & Revaluations 4,791 Disposal of Fixed Assets (422) Balance as at 31March 2005 321,346

£’000 Balance as at 1 April 2004 140,288 2004-2005 Capital Financing :

- Capital Receipts (Usable) 2,388 - Revenue Contributions 26,107 - Deferred Charge Financing (2,817) - De Minimus Financing (399) - PFI Deferred Consideration Amortisation (2,209)

Fixed Asset Impairment Write Off Financing (1,788) Amortisation of Government Grants deferred 2,997 2004-2005 Minimum Revenue Provision (MRP) (less depreciation provision) (13,300) Long Term Loan Write Off Financing (396) Balance as at 31 March 2005 150,871

£’000 Balance as at 1 April 2004 5,531 Capital receipts in year 968 Capital receipts applied to finance capital expenditure (2,388) Balance as at 31 March 2005 4,111

Notes to Main Financial Statements

35

Prior Year Adjustment relates to the reclassification of the Insurance Premium Reserve balance of £1.0m as part of the Insurance Claims Provision balance. Note (e) Other Usable Specific Reserves 2004-2005 Original

2003-2004 Insurance Reserve

Adjustment

Amended 2003-2004

£’000 £’000 £’000 £’000 Waste Disposal 73 1,355 - 1,355 Renewals and Repairs 3,372 4,177 - 4,177 Computers and IT 1,928 3,076 - 3,076 Consultancy 194 250 - 250 Matched Funding 1,151 890 - 890 Objective One 1,571 3,422 - 3,422 Premises and Accommodation 229 260 - 260 Redundancy 1,100 1,012 - 1,012 Social Services: - Doubletrees 50 350 - 350 - Autism - 300 - 300 - Mental Health 175 378 - 378 Capital Related 493 426 - 426 Democratic Representation 499 416 - 416 Partnerships/Joint Arrangements 703 662 - 662 Schools: - Small Loans Scheme 282 224 - 224 - Nursery Schools 93 93 - 93 Adult FEFC 2,833 2,833 - 2,833 School and Post 16 Transport 448 347 - 347 Fire Service Pensions 820 588 - 588 Insurance Premium - 1,000 (1,000) - Interest Receipts Fluctuations 658 658 - 658 Pay & Grading 795 1,549 - 1,549 Local Committees 91 740 - 740 Fire Service Transitional Funding Loan 304 - - - Revenue Support Grant Repayment 1,161 - - - Customer Services Centre 380 - - - Special Education 250 - - - Children’s Service Transition 996 - - - Other Usable Specific Reserves 2,667 2,722 - 2,722 Sub-total 23,316 27,728 (1,000) 26,728 P.F.I: - Development 250 250 - 250 - Grant Income Equalisation 24,279 14,291 - 14,291 - Contract Equalisation 132 223 - 223 Total 47,977 42,492 (1,000) 41,492

Prior Year Adjustment relates to the reclassification of the Insurance Premium Reserve as an Insurance Provision.

Note (f) County Fund - Usable Reserves General

Reserve

£’000

Budget Equalisation

Reserves £’000

Total

£’000 Balance as at 1 April 2004 8,286 4,502 12,788 Transfers (to)/from Revenue Account 1,272 (61) 1,211 Balances as at 31 March 2005 9,558 4,441 13,999

Notes to Main Financial Statements

36

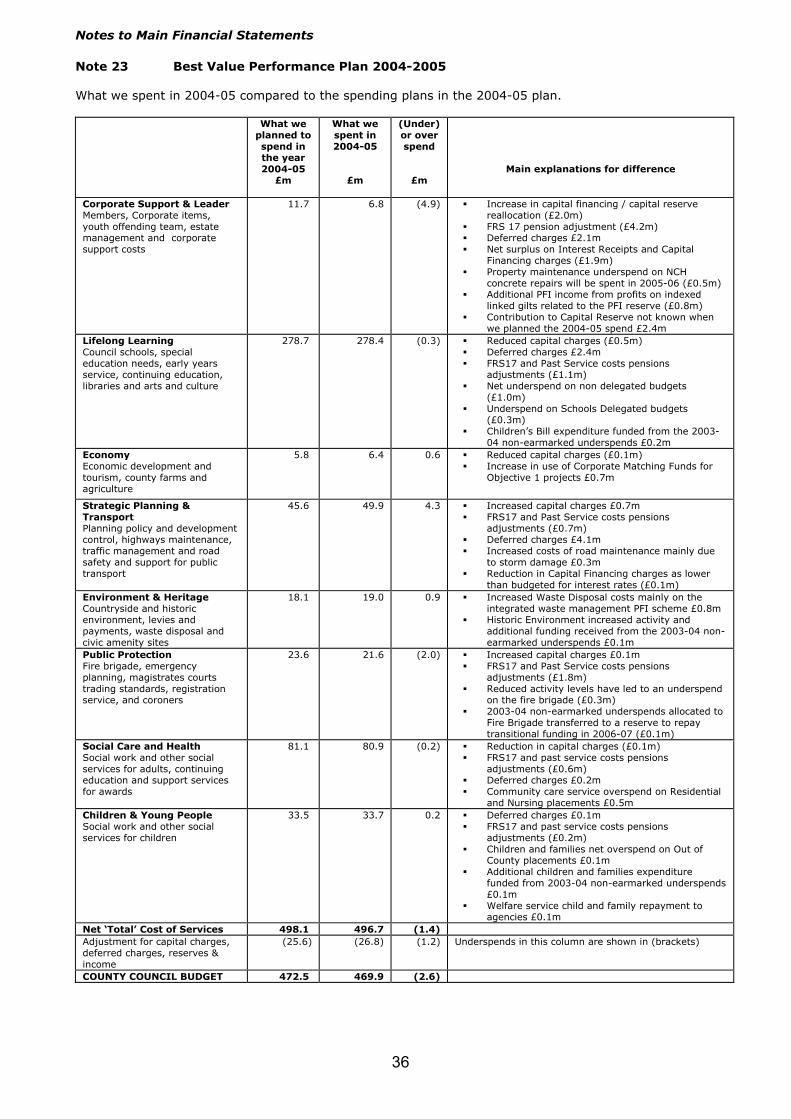

Note 23 Best Value Performance Plan 2004-2005 What we spent in 2004-05 compared to the spending plans in the 2004-05 plan.

What we planned to spend in the year 2004-05

£m

What we spent in 2004-05

£m

(Under) or over spend

£m

Main explanations for difference

Corporate Support & Leader Members, Corporate items, youth offending team, estate management and corporate support costs

11.7 6.8 (4.9) Increase in capital financing / capital reserve reallocation (£2.0m)

FRS 17 pension adjustment (£4.2m) Deferred charges £2.1m Net surplus on Interest Receipts and Capital

Financing charges (£1.9m) Property maintenance underspend on NCH

concrete repairs will be spent in 2005-06 (£0.5m) Additional PFI income from profits on indexed

linked gilts related to the PFI reserve (£0.8m) Contribution to Capital Reserve not known when

we planned the 2004-05 spend £2.4m Lifelong Learning Council schools, special education needs, early years service, continuing education, libraries and arts and culture

278.7 278.4 (0.3) Reduced capital charges (£0.5m) Deferred charges £2.4m FRS17 and Past Service costs pensions

adjustments (£1.1m) Net underspend on non delegated budgets

(£1.0m) Underspend on Schools Delegated budgets

(£0.3m) Children’s Bill expenditure funded from the 2003-

04 non-earmarked underspends £0.2m Economy Economic development and tourism, county farms and agriculture

5.8 6.4 0.6 Reduced capital charges (£0.1m) Increase in use of Corporate Matching Funds for

Objective 1 projects £0.7m

Strategic Planning & Transport Planning policy and development control, highways maintenance, traffic management and road safety and support for public transport

45.6 49.9 4.3 Increased capital charges £0.7m FRS17 and Past Service costs pensions

adjustments (£0.7m) Deferred charges £4.1m Increased costs of road maintenance mainly due

to storm damage £0.3m Reduction in Capital Financing charges as lower

than budgeted for interest rates (£0.1m) Environment & Heritage Countryside and historic environment, levies and payments, waste disposal and civic amenity sites

18.1 19.0 0.9 Increased Waste Disposal costs mainly on the integrated waste management PFI scheme £0.8m

Historic Environment increased activity and additional funding received from the 2003-04 non-earmarked underspends £0.1m

Public Protection Fire brigade, emergency planning, magistrates courts trading standards, registration service, and coroners

23.6 21.6 (2.0) Increased capital charges £0.1m FRS17 and Past Service costs pensions

adjustments (£1.8m) Reduced activity levels have led to an underspend

on the fire brigade (£0.3m) 2003-04 non-earmarked underspends allocated to

Fire Brigade transferred to a reserve to repay transitional funding in 2006-07 (£0.1m)

Social Care and Health Social work and other social services for adults, continuing education and support services for awards

81.1 80.9 (0.2) Reduction in capital charges (£0.1m) FRS17 and past service costs pensions

adjustments (£0.6m) Deferred charges £0.2m Community care service overspend on Residential

and Nursing placements £0.5m Children & Young People Social work and other social services for children

33.5 33.7 0.2 Deferred charges £0.1m FRS17 and past service costs pensions

adjustments (£0.2m) Children and families net overspend on Out of

County placements £0.1m Additional children and families expenditure

funded from 2003-04 non-earmarked underspends £0.1m

Welfare service child and family repayment to agencies £0.1m

Net ‘Total’ Cost of Services 498.1 496.7 (1.4) Adjustment for capital charges, deferred charges, reserves & income

(25.6) (26.8) (1.2) Underspends in this column are shown in (brackets)

COUNTY COUNCIL BUDGET 472.5 469.9 (2.6)

Notes to Main Financial Statements

37

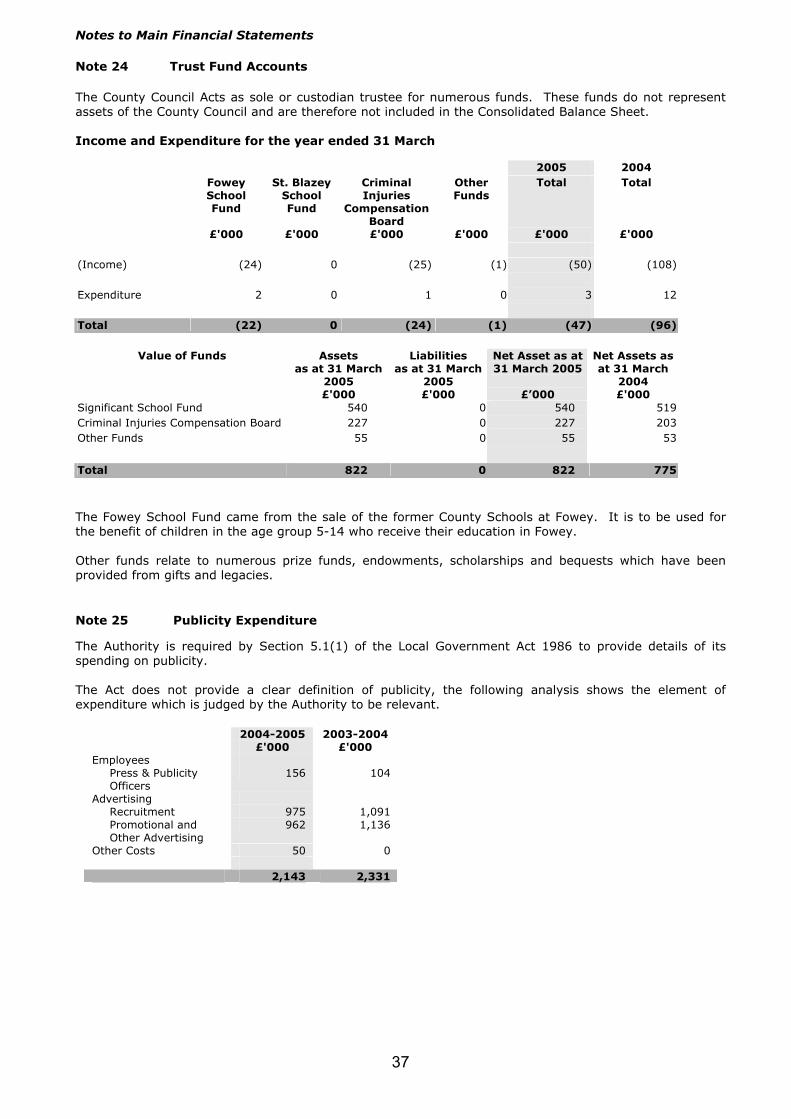

Note 24 Trust Fund Accounts The County Council Acts as sole or custodian trustee for numerous funds. These funds do not represent assets of the County Council and are therefore not included in the Consolidated Balance Sheet. Income and Expenditure for the year ended 31 March

2005 2004 Fowey

School Fund

St. Blazey School Fund

Criminal Injuries

Compensation Board

Other Funds

Total Total

£'000 £'000 £'000 £'000 £'000 £'000 (Income) (24) 0 (25) (1) (50) (108) Expenditure 2 0 1 0 3 12 Total (22) 0 (24) (1) (47) (96)

Value of Funds Assets

as at 31 March 2005 £'000

Liabilities as at 31 March

2005 £'000

Net Asset as at 31 March 2005

£’000

Net Assets as at 31 March

2004 £'000

Significant School Fund 540 0 540 519 Criminal Injuries Compensation Board 227 0 227 203 Other Funds 55 0 55 53

Total 822 0 822 775

The Fowey School Fund came from the sale of the former County Schools at Fowey. It is to be used for the benefit of children in the age group 5-14 who receive their education in Fowey. Other funds relate to numerous prize funds, endowments, scholarships and bequests which have been provided from gifts and legacies. Note 25 Publicity Expenditure

The Authority is required by Section 5.1(1) of the Local Government Act 1986 to provide details of its spending on publicity. The Act does not provide a clear definition of publicity, the following analysis shows the element of expenditure which is judged by the Authority to be relevant.

2004-2005 2003-2004 £'000 £'000

Employees Press & Publicity

Officers 156 104

Advertising Recruitment 975 1,091 Promotional and

Other Advertising 962 1,136

Other Costs 50 0

2,143 2,331

Notes to Main Financial Statements

38

Note 26 Cashflow Statement

(i) Reconciliation of revenue cash flow

2004-2005 2003-2004 £’000 £’000 £’000 Surplus for the year (1,467) (3,064) Deduct Interest Paid (15,248) (12,415) Contributions (to)/from provisions and reserves (2,445) (4,269) Deduct contributions to capital outlay (26,107) (16,094) Deduct depreciation (23,009) (21,403) Add minimum revenue provision adjustment 13,300 12,975 (53,509) (41,206) Increase/(decrease) in debtors 14,717 (2,110) Increase/(decrease) in long term debtors (6,043) 6,418 (Increase)/decrease in creditors 16,167 (17,184) Increase/(decrease) in stock and Work in Progress (158) 419 24,683 (12,457) Deduct: Interest received 9,693 4,786 Revenue Activities net contributions (20,600) (51,941)

(ii) Reconciliation of net cash flow to the movement in net debt

£’000 Decrease in cash in the period (6,017) Cash inflow from increase in debt financing (61,242) Cash outflow from decrease in liquid resources 29,136 (38,123) Movement in net debt in the period Net debt at 1 April 2004 (112,704) Net debt as at 31 March 2005 (150,827)

(iii) Analysis of net debt

Balance as at 1 April 2004 £’000

Cash Flow

£’000

Balance as at 31 March 2005 £’000

Cash in hand and in transit 94 34 128 Cash overdrawn (12,094) (6,051) (18,145) Debt due after one year (230,568) (42,694) (273,262) Debt due within one year (270) (18,548) (18,818) Short term investments 117,150 (51,671) 65,479 Long term investments 12,984 80,807 93,791 (112,704) (38,123) (150,827)

(iv) Other Government Grants and Contributions

2004- 2005 2003-2004 £'000 £'000 £'000 £'000

Education Services Standards Fund 32,381 21,742 Special Grant 8,228 7,170 Learning Skills Council 19,279 12,392 } Further Education Funding Council 5 5,840 } Private Finance Initiative Grant 13,915 6,738 Other 9,262 12,294

83,070 66,176

Notes to Main Financial Statements

39

Note 26 Cash Flow Statement (continued)

(iv) Other Government Grants and Contributions (continued)

Social Services Supporting People 15,350 14,010 Preserved Rights 5,780 6,581 Access & System Capacity 5,090 1,884 Health Services delivered by County Council 13,934 8,346 Residential Allowances 5,572 2,552 Other 9,540 13,185 55,266 46,558 Fire Service 2,535 1,842

Highways, Roads & Transport Services 2,782 2,895

Court Services Magistrates Courts 10,843 7,954

Cultural, Environmental & Planning Services 6,077 3,409

Central Services 2,672 2,149

163,245 130,983

Note 27 Officer Emoluments Under the Accounts and Audit Regulations, the Authority is required to disclose the number of staff, including teachers, whose remuneration falls within the following ranges.

Remuneration includes all amounts paid to or receivable by an employee including sums due by way of expense allowances and the estimated monetary value of any other benefits received by an employee otherwise than in cash (for example through a leased car).

The increase in staff numbers shown in this table is mainly due to the annual pay awards moving staff into the static remuneration bands. The numbers shown in the table will continue to grow each year because the remuneration levels are statutory and not adjusted to take into account the effects of inflation. Variations are also due to employees starting or leaving employment within the financial year.

Note 28 Income & Expenditure Under The Local Authority (Goods & Services) Act 1970

The Authority is required to provide details of work carried out by Service Departments for other Public Bodies. The purpose of this disclosure is to show the extent to which the Authority is engaged in trading activities which would not otherwise be part of its function as a Local Authority. All Local Authorities are allowed to supply goods and services to a number of prescribed Public Bodies by the 1970 Act. The income and expenditure in respect of these activities is included in the Authority’s Consolidated Revenue Account. Details are shown below.

2004-2005 2003-2004

Remuneration: No. of staff No. of staff

£50,001 - £60,000 59 39

£60,001 - £70,000 28 21

£70,001 - £80,000 13 7

£80,001 - £90,000 3 2

£90,001 - £100,000 1 3

£100,001 - £110,000 2 1

£110,001 - £120,000 1 0

107 73

Notes to Main Financial Statements

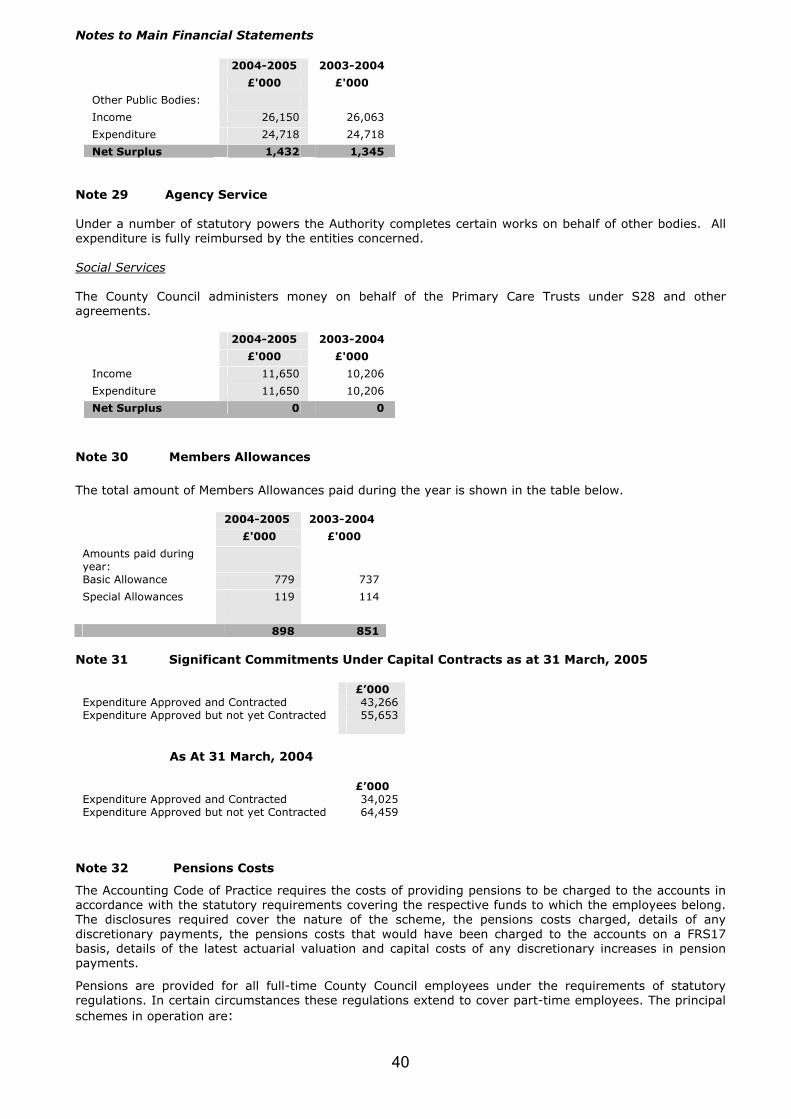

40

2004-2005 2003-2004

£'000 £'000

Other Public Bodies:

Income 26,150 26,063

Expenditure 24,718 24,718