consumer survey 2018 - european commission

TRANSCRIPT

CONSUMERS ATTITUDES TOWARDS

CROSS-BORDER TRADE AND CONSUMER PROTECTION

2018

Final Report

Specific contract No 2017 85 02

implementing Framework contract No EAHC 2013CP03 Lot 1

GfK Belgium

Final Version

14022019

Consumers Health Agriculture and

Food

Executive Agency

EUROPEAN COMMISSION

Produced by Consumers Health Agriculture and Food Executive Agency (Chafea) on behalf of

Directorate-General for Justice and Consumers

Unit JUST03 (Economic analysis amp evaluation)

E-mail JUST-03eceuropaeu

European Commission

B-1000 Brussels

EUROPEAN COMMISSION

Directorate-General for Justice and Consumers EU Consumer Programme

2019 3 EN

Consumers attitudes towards cross-border trade and

consumer protection 2018

Final Report

This report was produced under the EU Consumer Programme (2014-2020) in the frame of a service contract with the Consumers Health Agriculture and Food Executive Agency (Chafea)

acting under the mandate from the European Commission

The content of this report represents the views of the contractor and is its sole responsibility it

can in no way be taken to reflect the views of the European Commission andor Chafea or other body of the European Union

The European Commission andor Chafea do not guarantee the accuracy of the data included in this report nor do they accept responsibility for any use made by third parties thereof

More information on the European Union is available on the Internet (httpeuropaeu)

More information on the European Union is available on the Internet (httpeuropaeu)

Luxembourg Publications Office of the European Union 2019

Project number 20191119

Title Survey on consumers attitudes towards cross-border and consumer-related issues 2018 ndash Final Report

Language version

SupportVolume Catalogue number ISBN DOI

EN PDF PDFVolume_01

EB-01-19-185-EN-N 978-92-9478-091-1 102818209599

copy European Union 2019

Reproduction is authorised provided the source is acknowledged

Europe Direct is a service to help you find answers

to your questions about the European Union

Freephone number ()

00 800 6 7 8 9 10 11

() The information given is free as are most calls (though some operators phone boxes or hotels may charge

you)

Consumer Survey 2018

5

TABLE OF CONTENTS

TABLE OF CONTENTS 5

1 INTRODUCTION 7

Introduction to the 2018 wave of the Consumer Survey 7

Sampling methodology 7

121 Countries covered 8

122 Core questionnaire 9

123 Socio-demographic and background questions 9

124 Analysis and reporting of statistically significant differences 10

125 Weighting and wave to wave comparisons 11

2 EXECUTIVE SUMMARYKEY FINDINGS 13

3 DOMESTIC AND CROSS-BORDER SHOPPING 16

Domestic and cross-border online purchases 16

Offline cross-border purchases 23

4 THE EVOLUTION OF ONLINE PURCHASE BEHAVIOUR 28

5 KNOWLEDGE OF CONSUMER RIGHTS 35

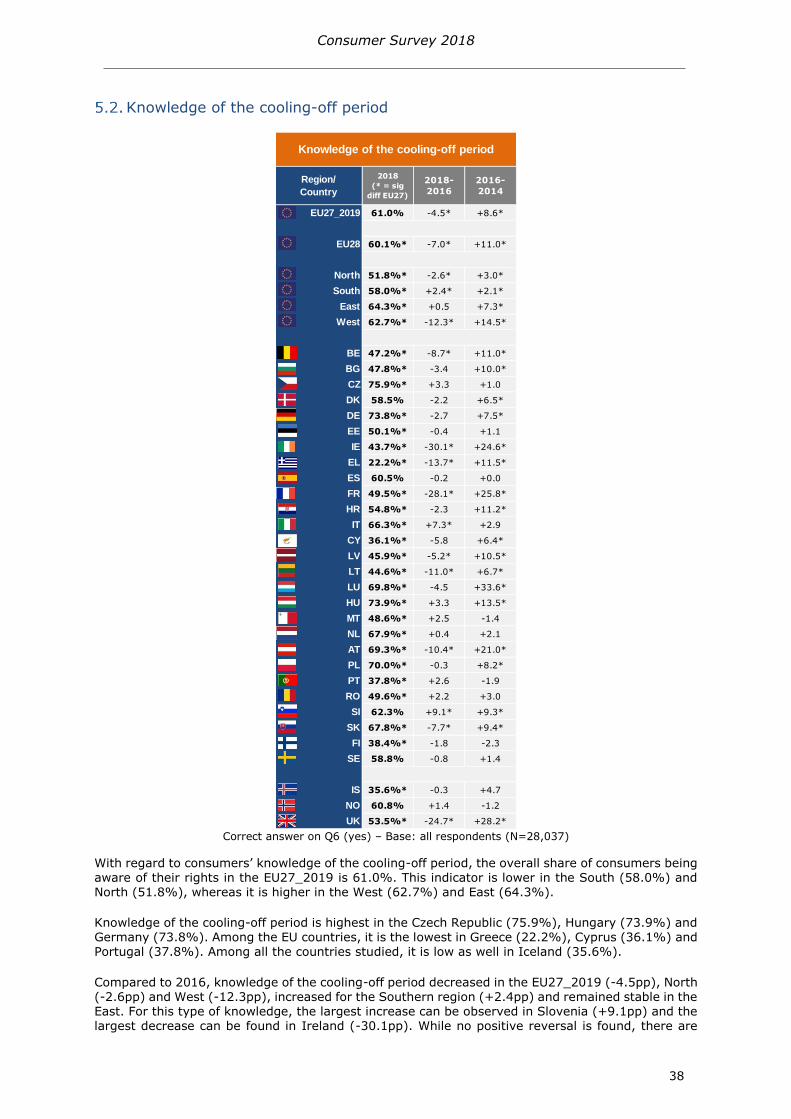

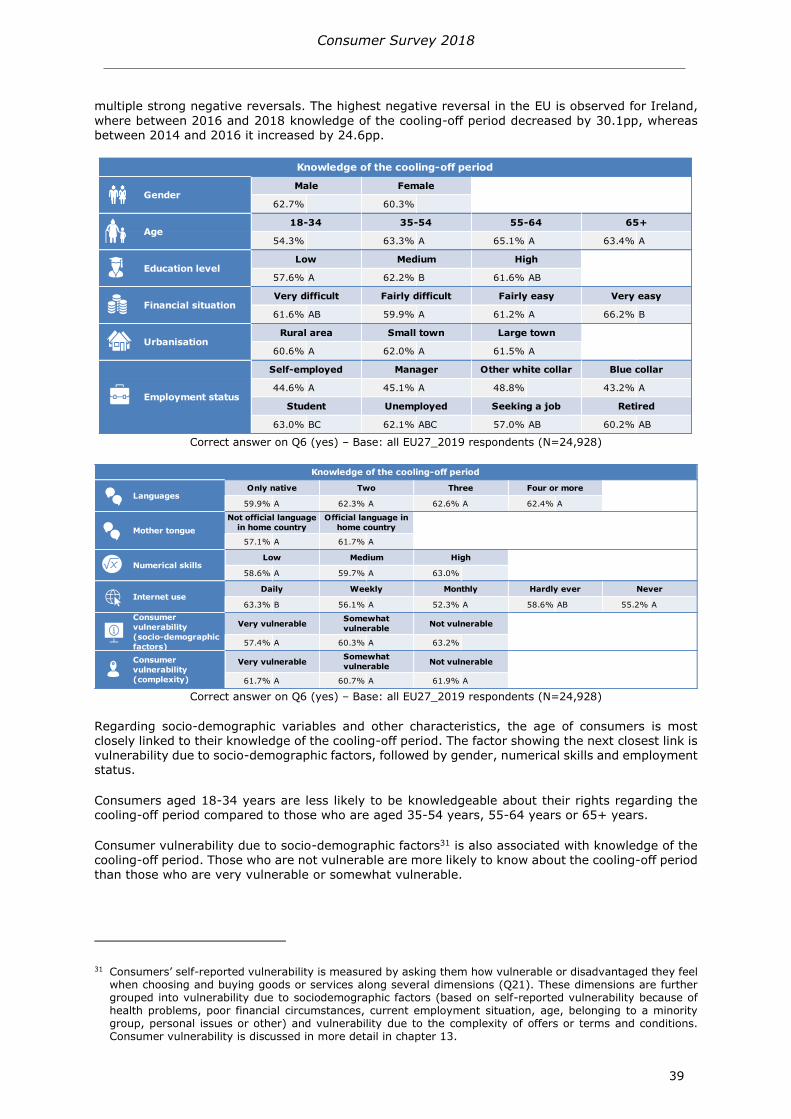

General level of knowledge about consumer rights 35

Knowledge of the cooling-off period 38

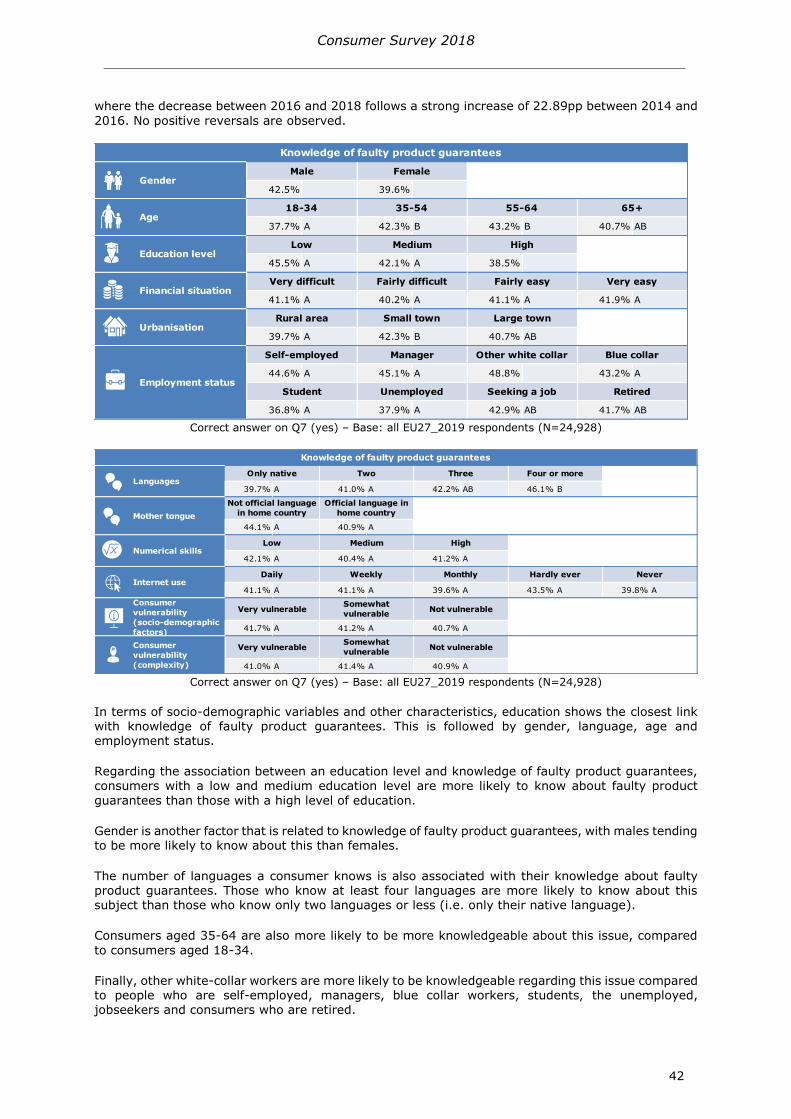

Knowledge of faulty product guarantees 41

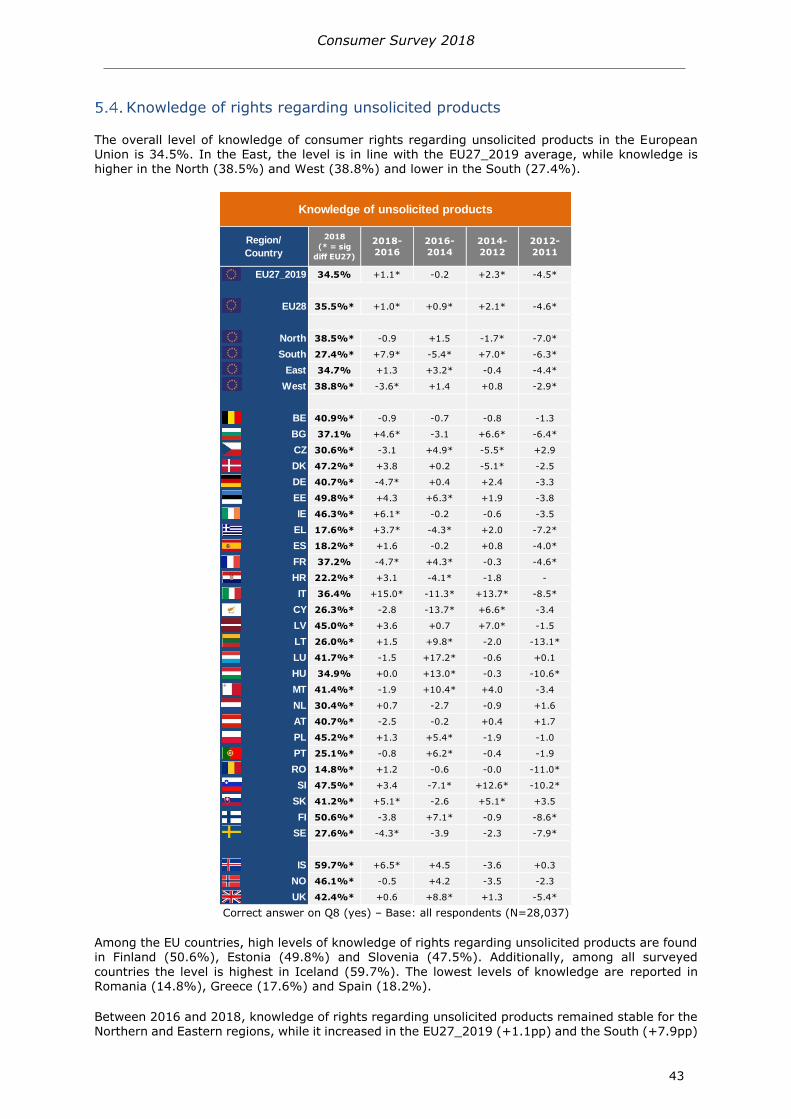

Knowledge of rights regarding unsolicited products 43

6 TRUST IN CONSUMER PROTECTION 46

Trust in organisations 46

611 Public authorities 49

612 Retailers and service providers 51

613 NGOs 54

Trust in redress mechanisms 56

621 ADR 59

622 Courts 61

7 TRUST IN PRODUCT SAFETY 63

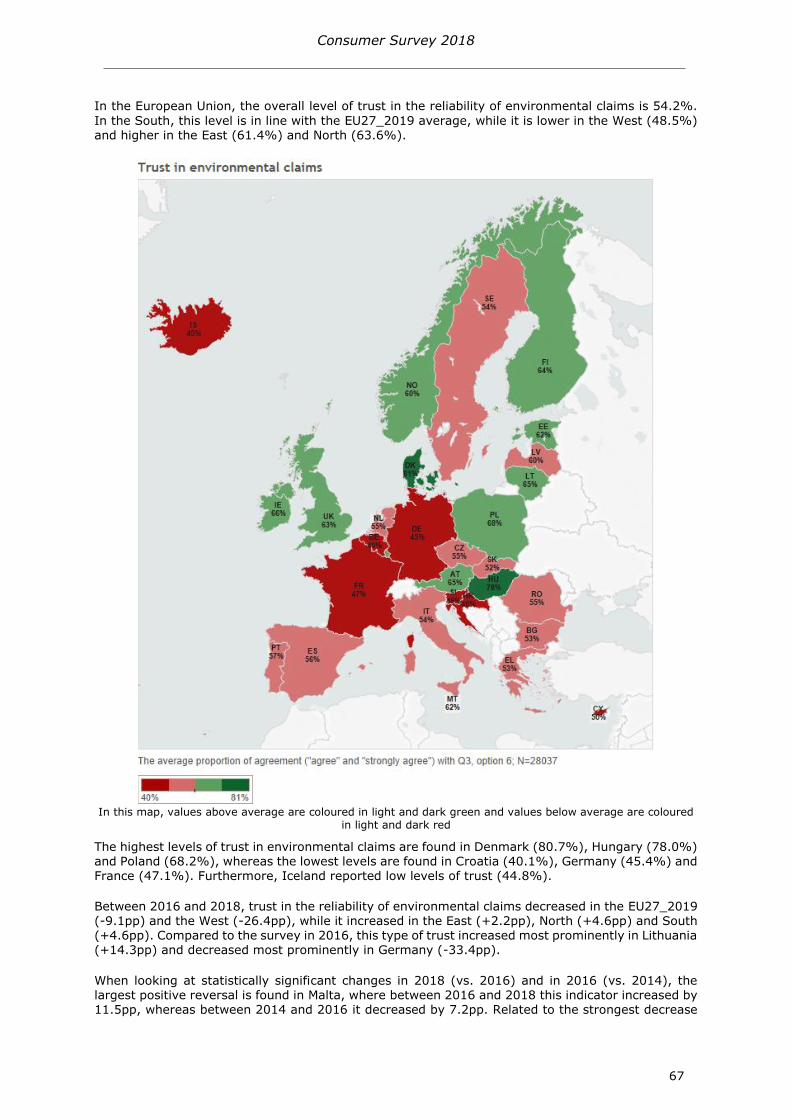

8 TRUST IN ENVIRONMENTAL CLAIMS 66

Reliability of environmental claims 66

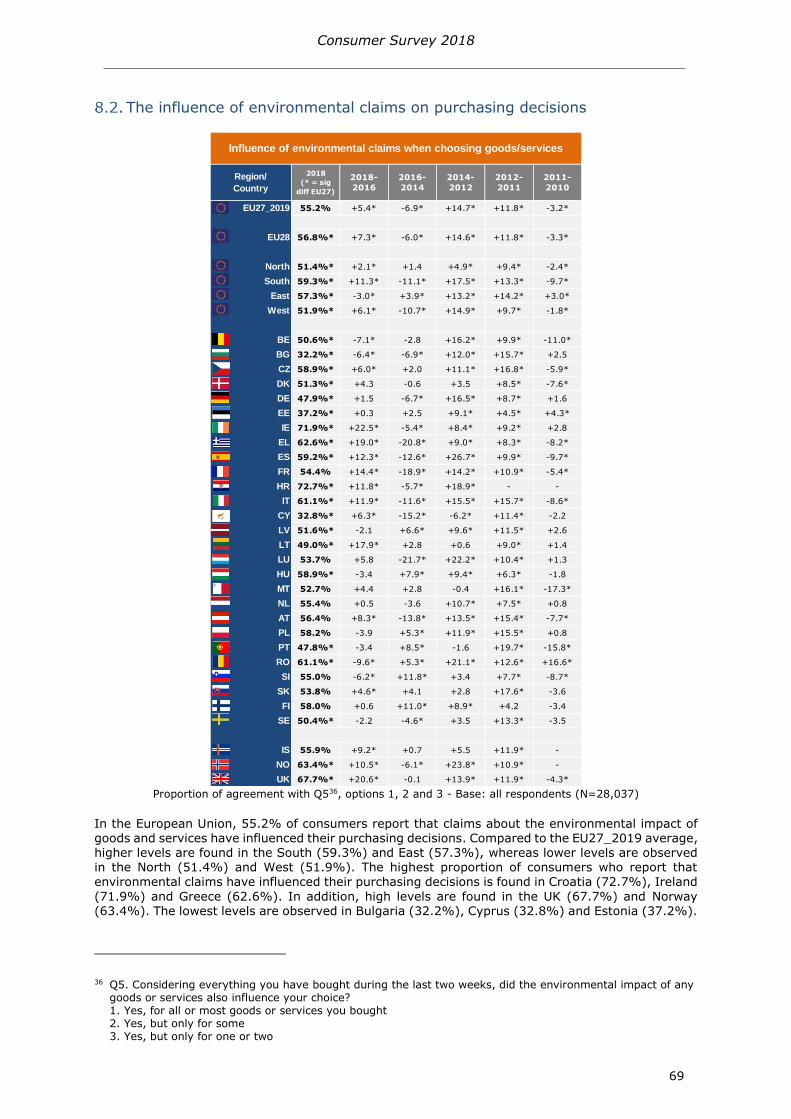

The influence of environmental claims on purchasing decisions 69

9 CONSUMER CONFIDENCE IN ONLINE PURCHASES 72

Domestic online purchases 72

Cross-border online purchases 75

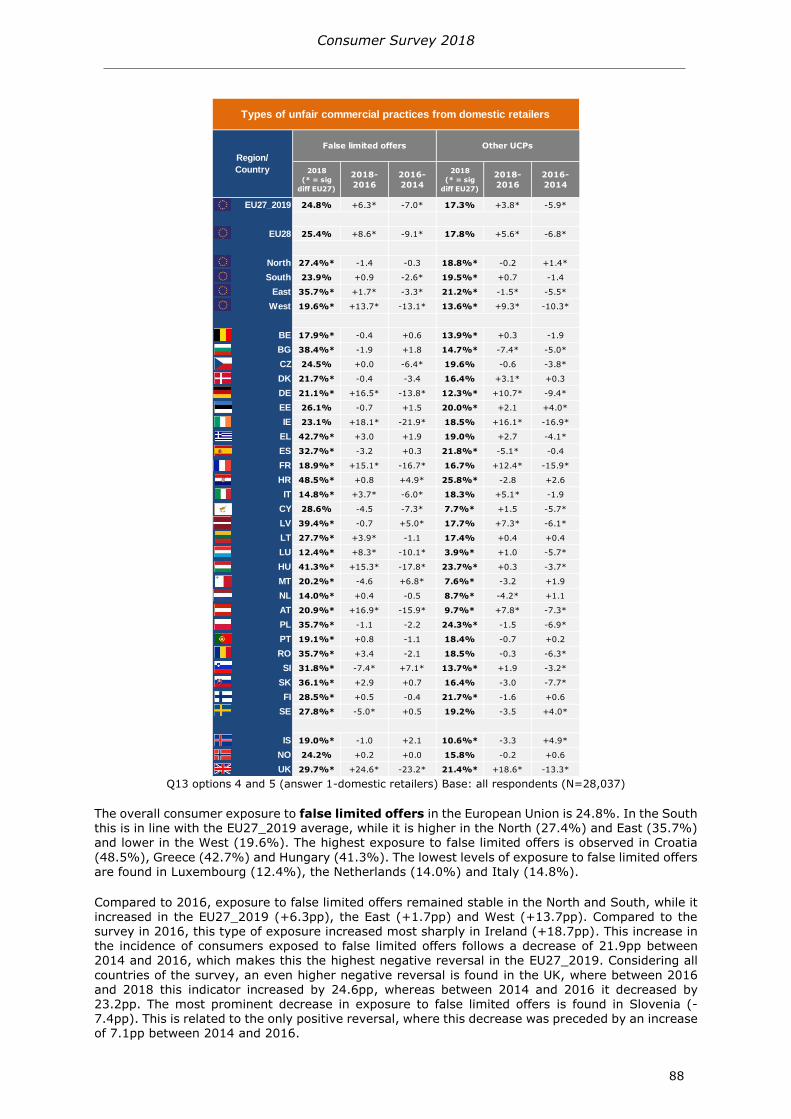

10 UNFAIR COMMERCIAL PRACTICES 78

Unfair commercial practices from domestic retailers 78

1011 Exposure to UCPs from domestic retailers 78

1012 Types of UCPs from domestic retailers 82

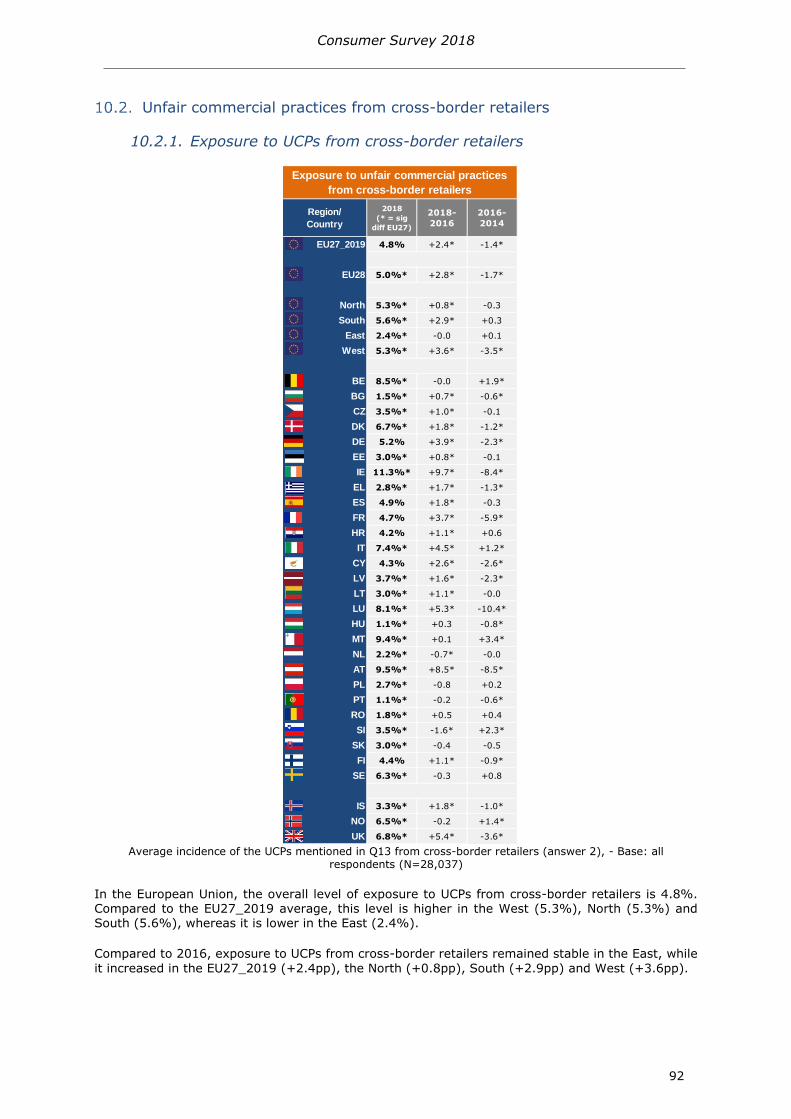

Unfair commercial practices from cross-border retailers 92

1021 Exposure to UCPs from cross-border retailers 92

1022 Types of UCPs from cross-border retailers 95

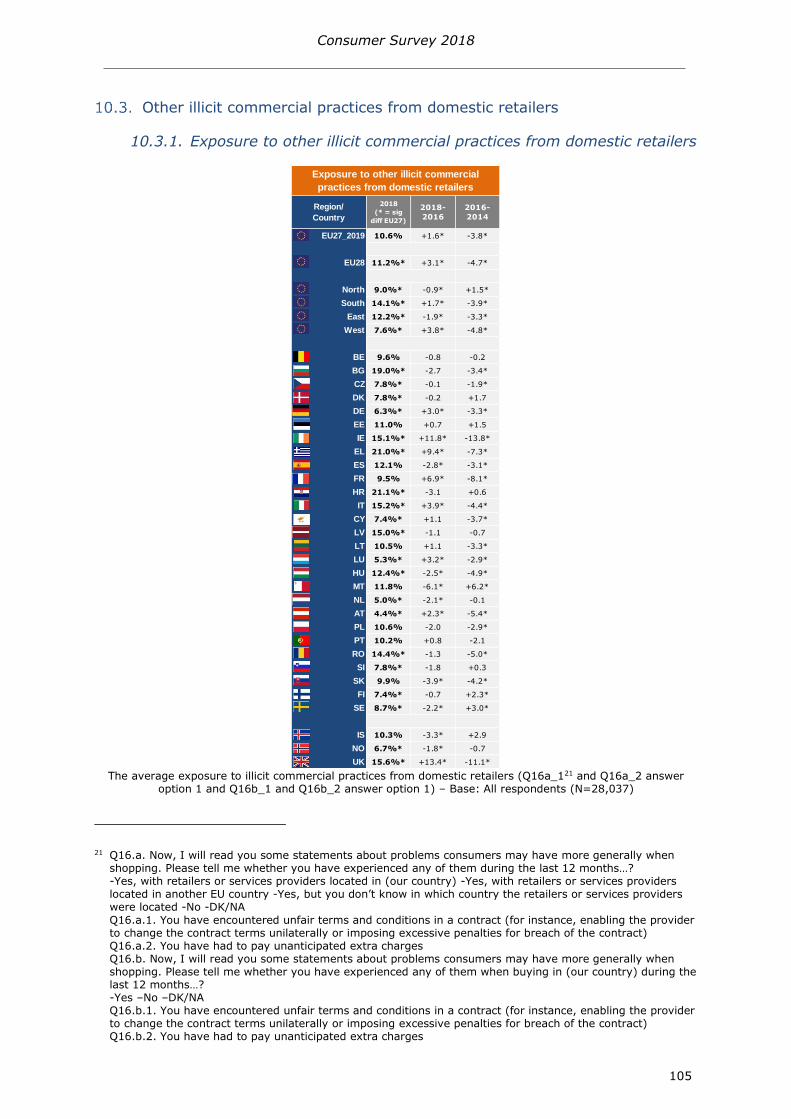

Other illicit commercial practices from domestic retailers 105

1031 Exposure to other illicit commercial practices from domestic retailers 105

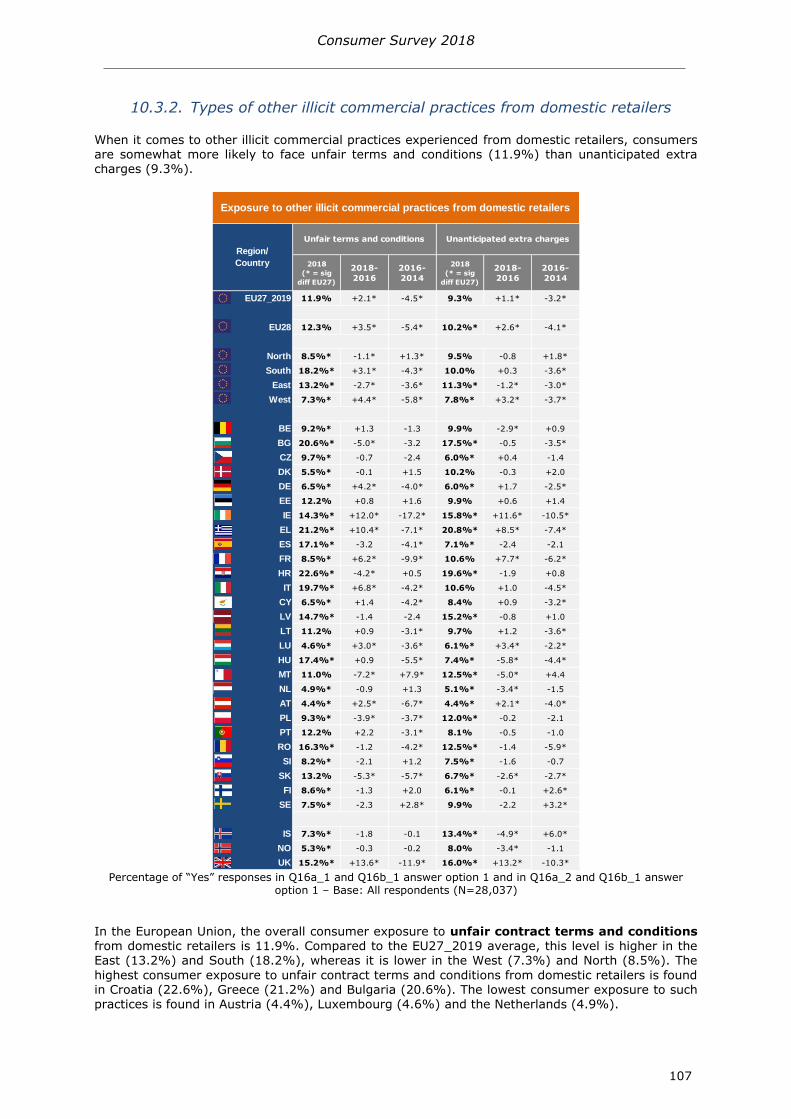

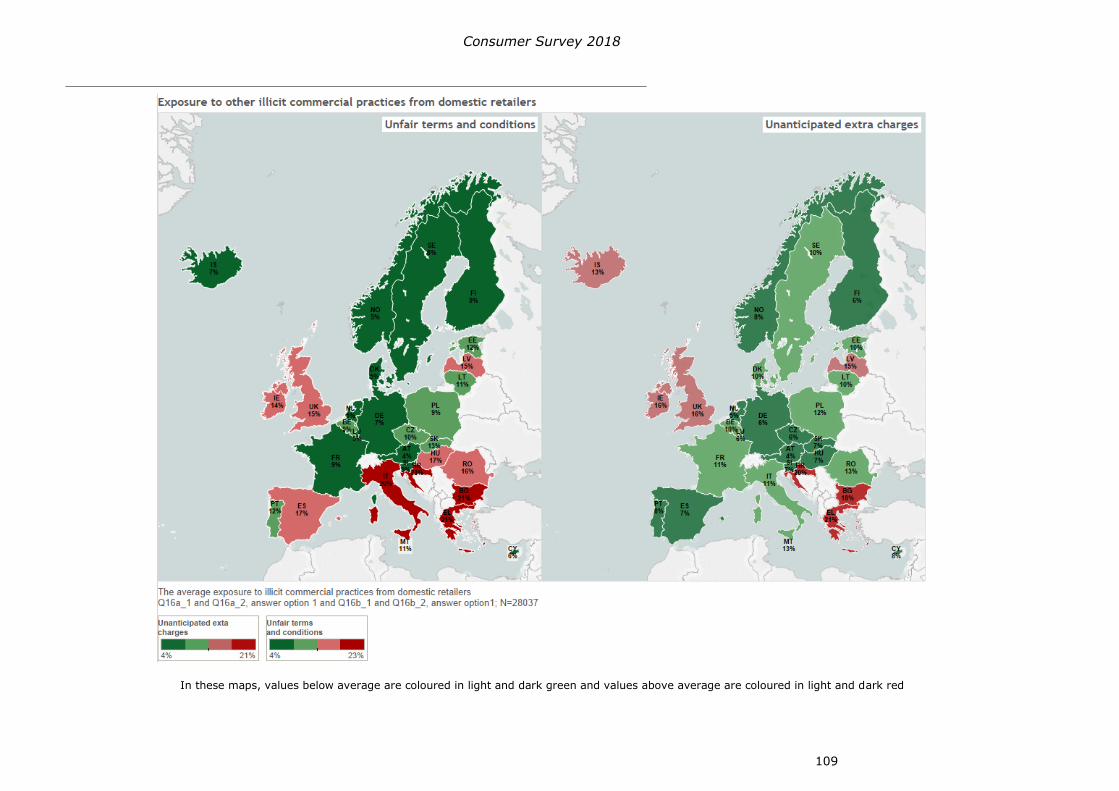

1032 Types of other illicit commercial practices from domestic retailers 107

1033 Exposure to other illicit commercial practices from cross-border retailers 113

Consumer Survey 2018

6

1034 Types of other illicit commercial practices from cross-border retailers 114

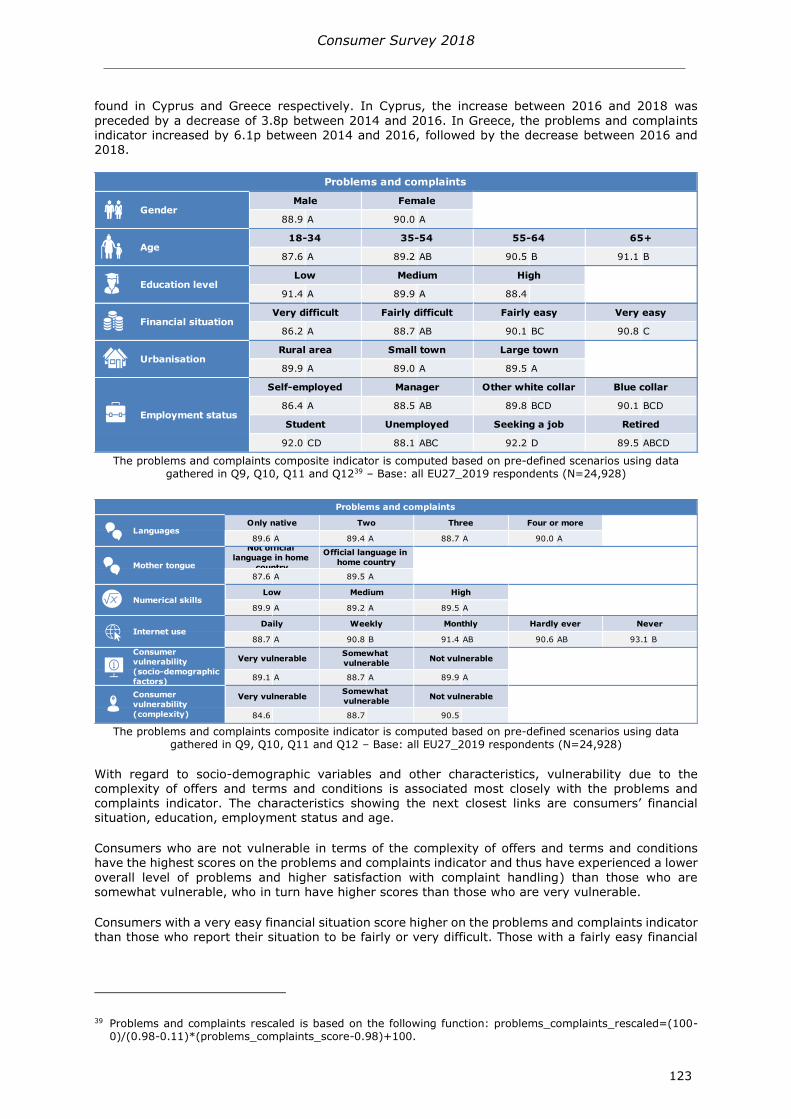

11 OVERALL PROBLEMS AND DISPUTE RESOLUTION 120

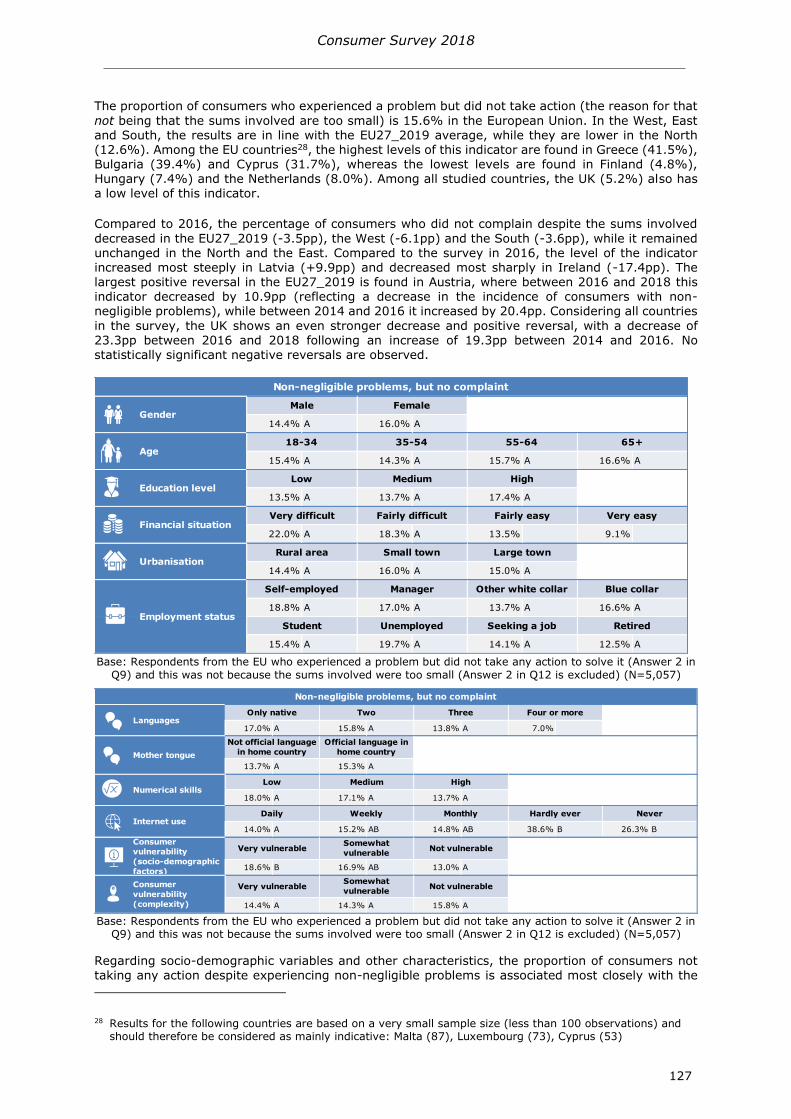

The problems and complaints indicator 120

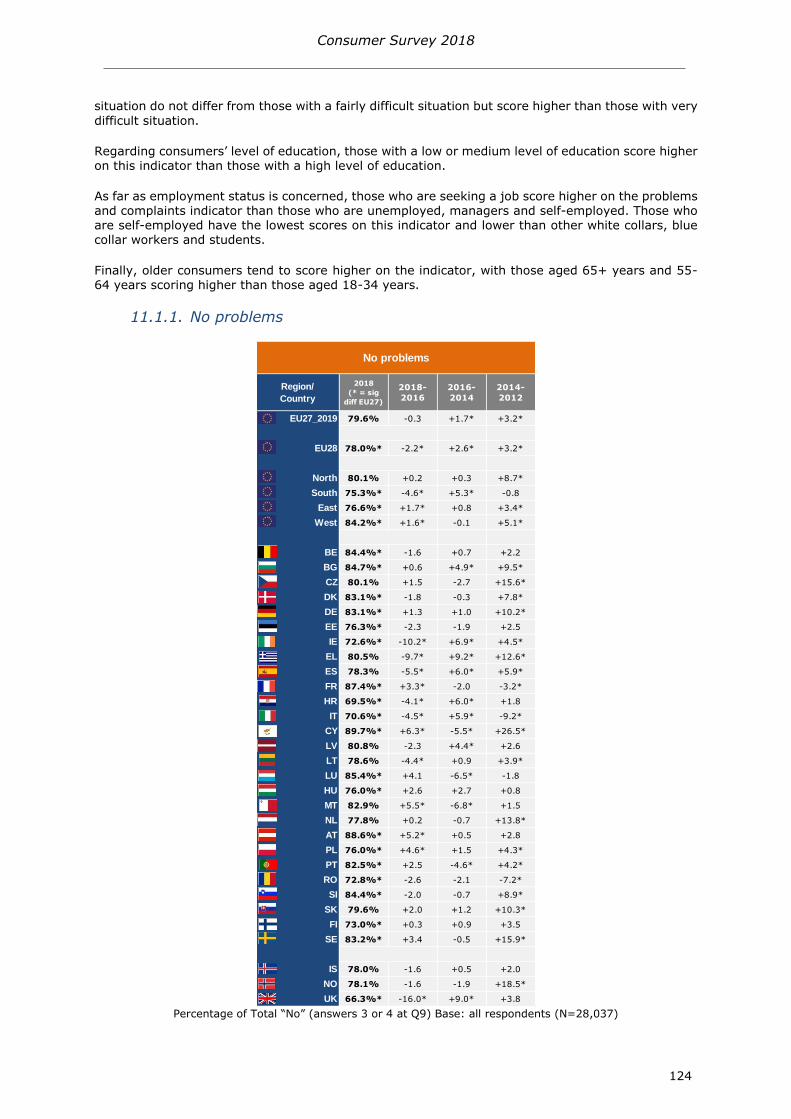

1111 No problems 124

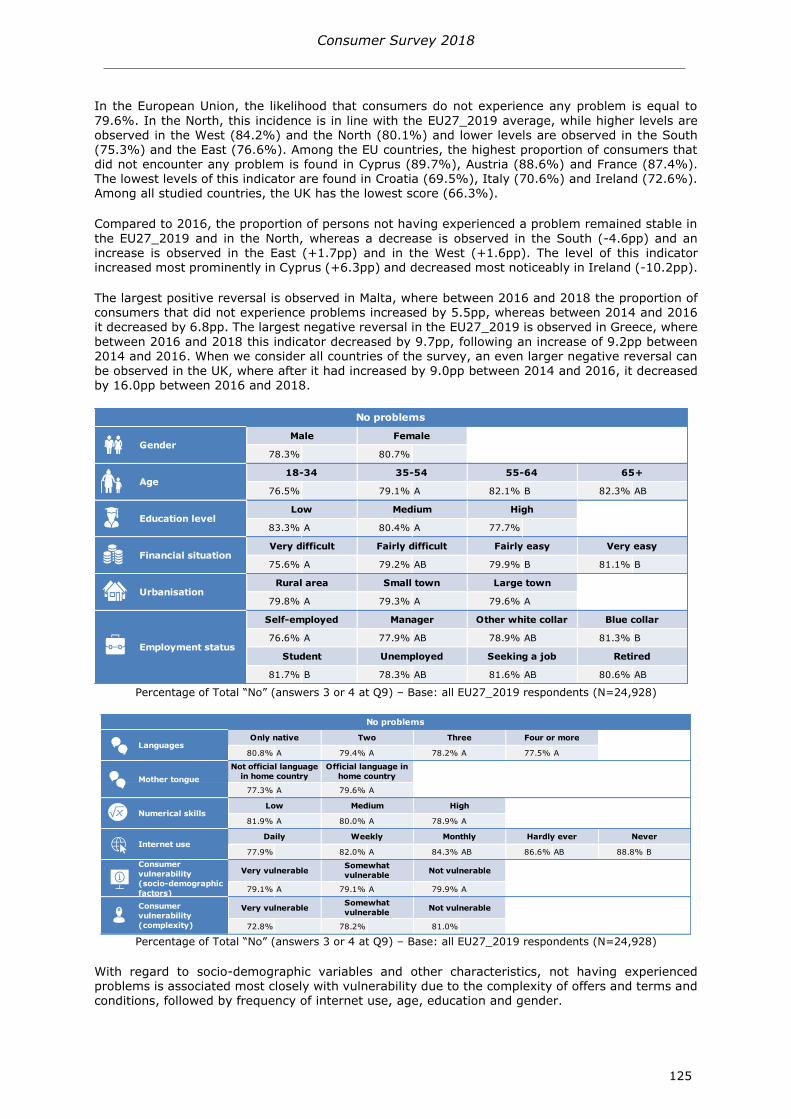

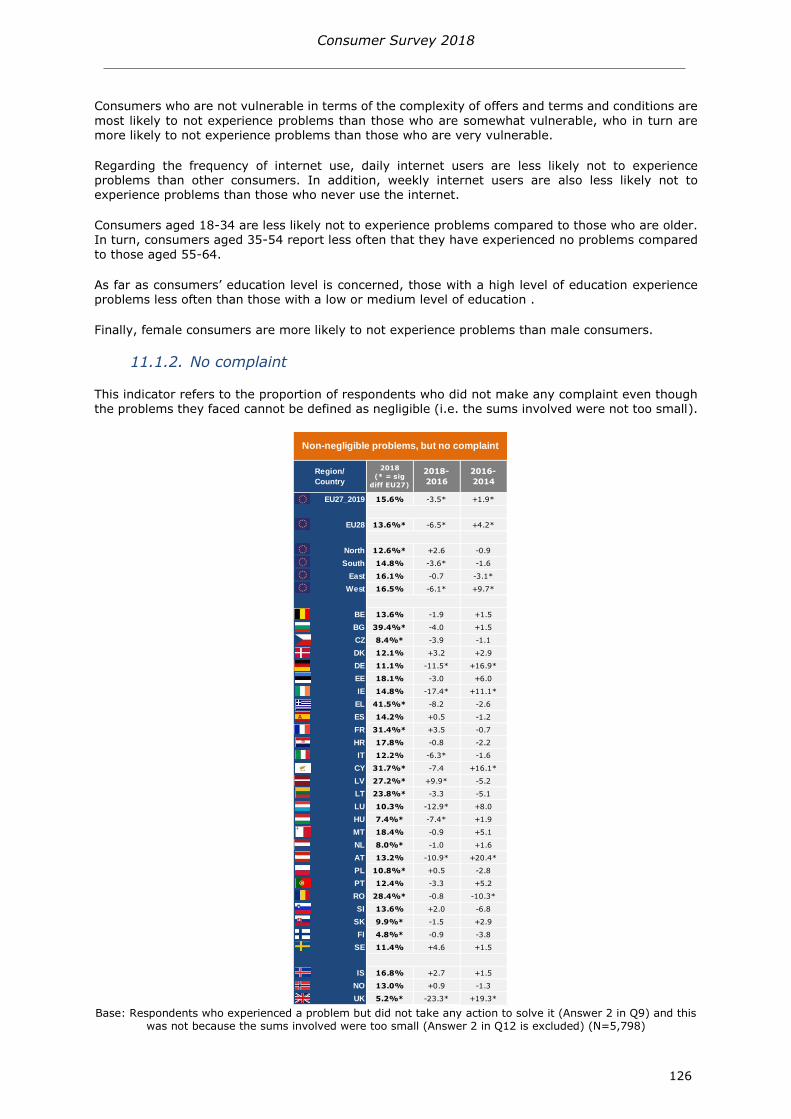

1112 No complaint 126

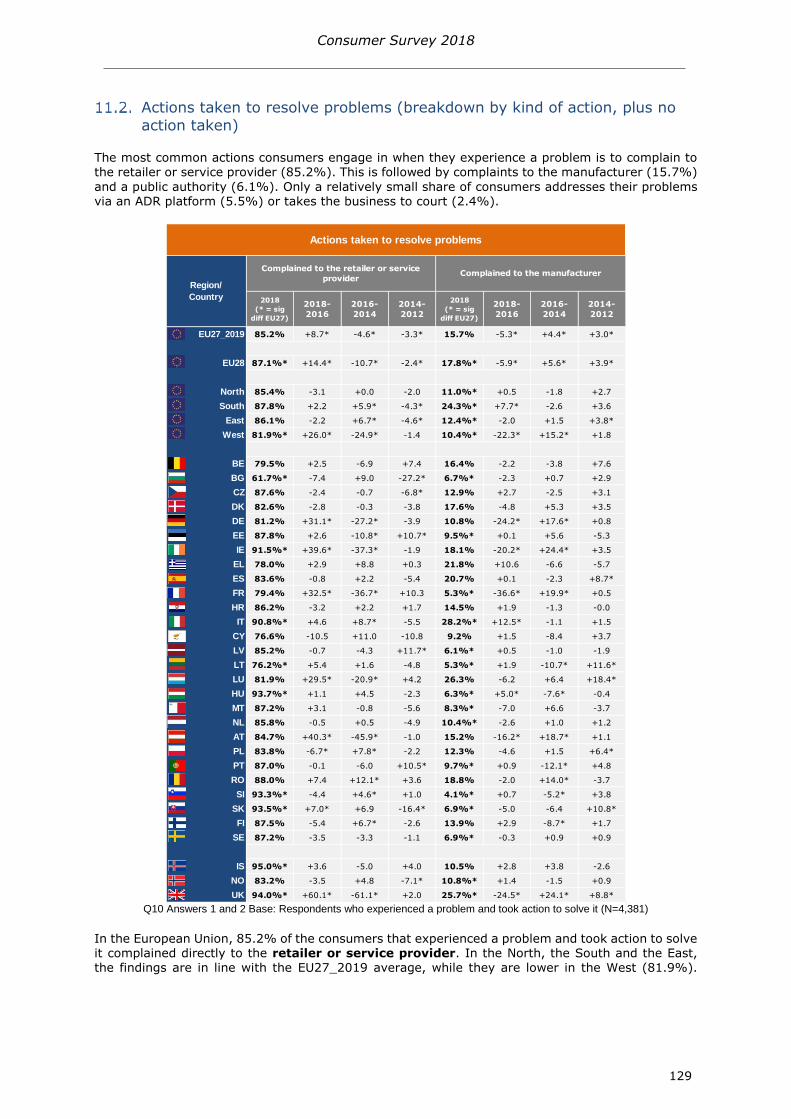

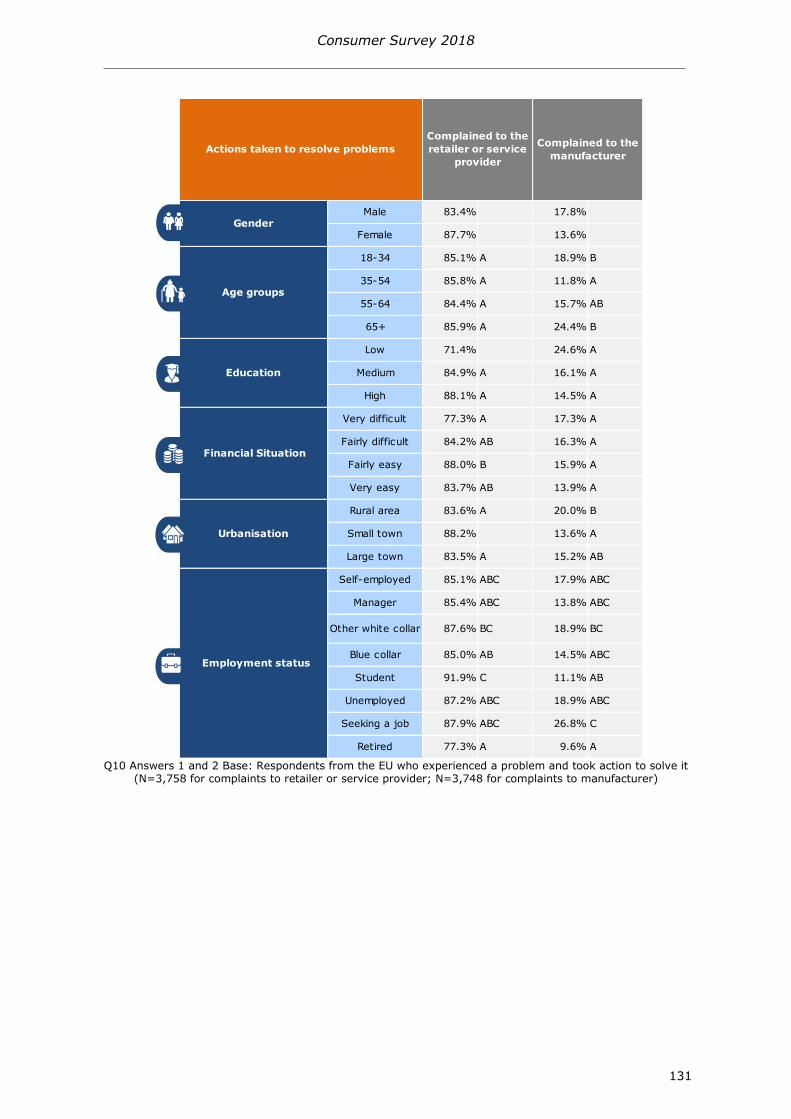

Actions taken to resolve problems (breakdown by kind of action plus no action taken) 129

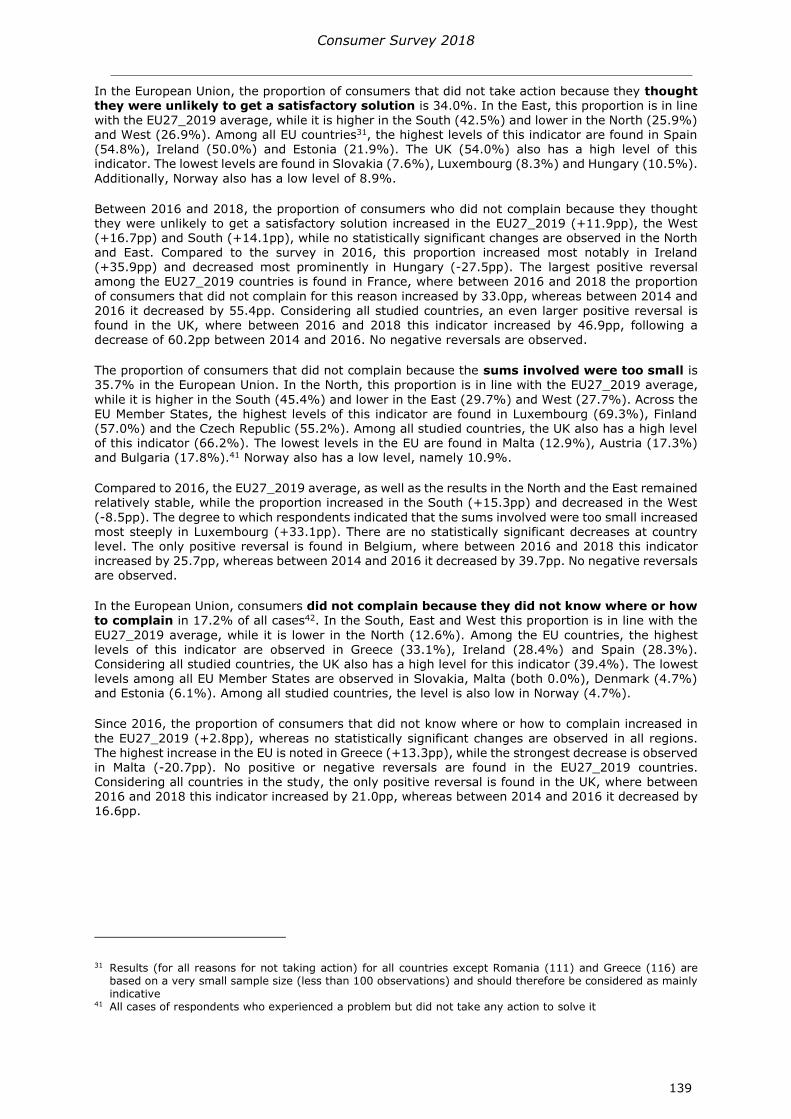

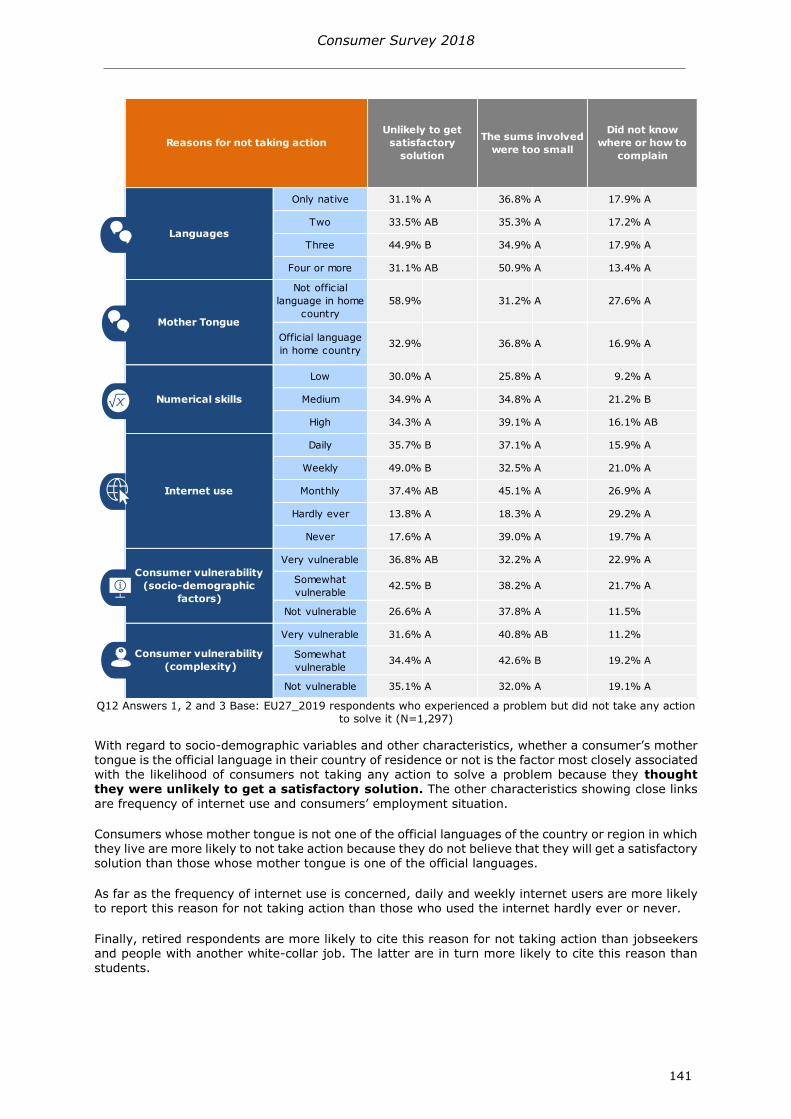

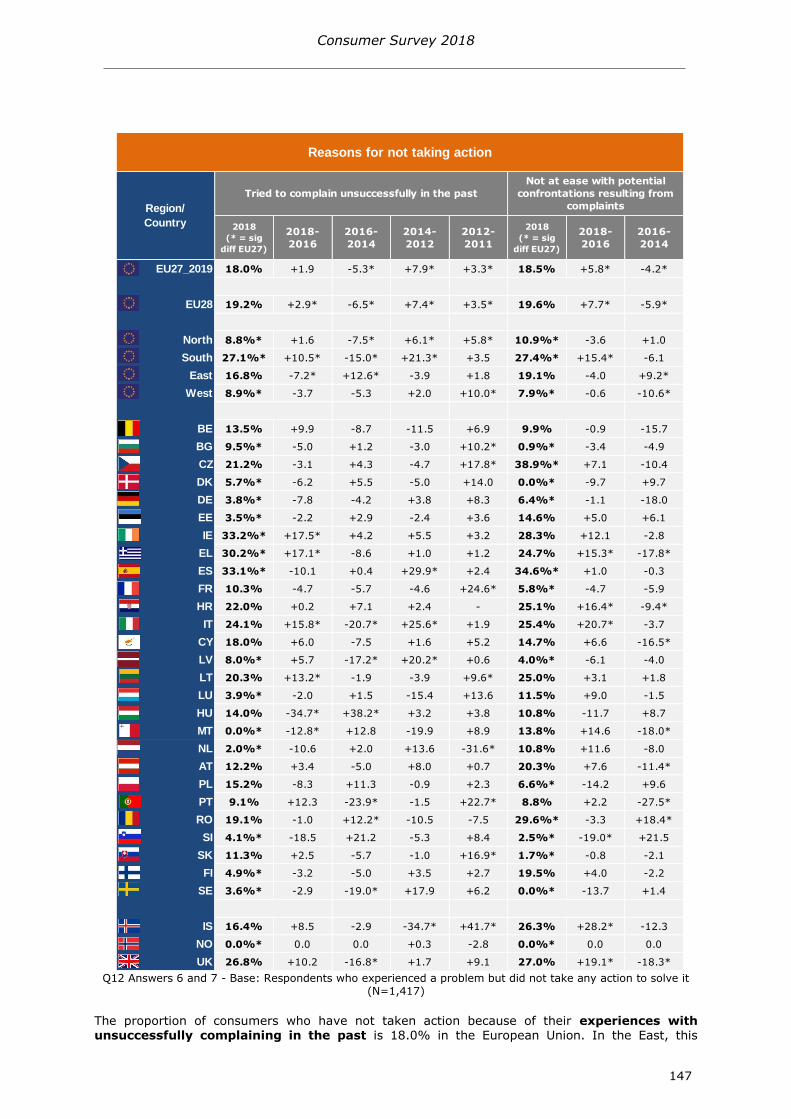

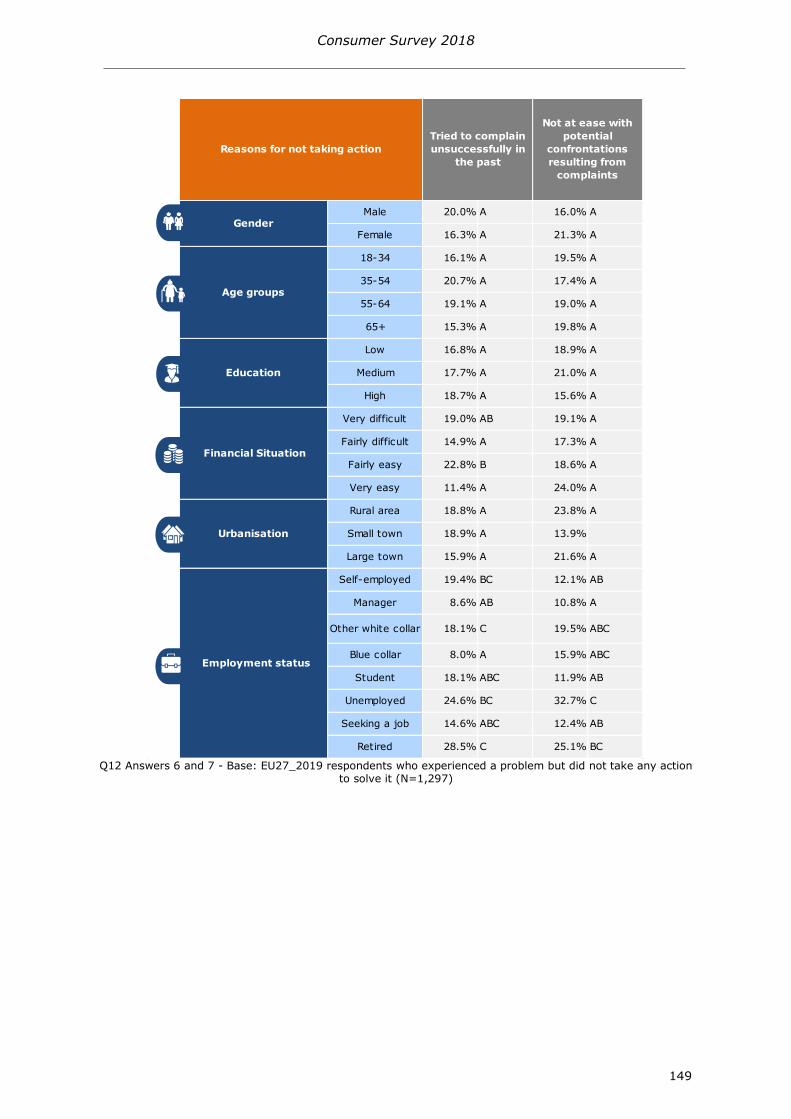

Reasons for not taking action 137

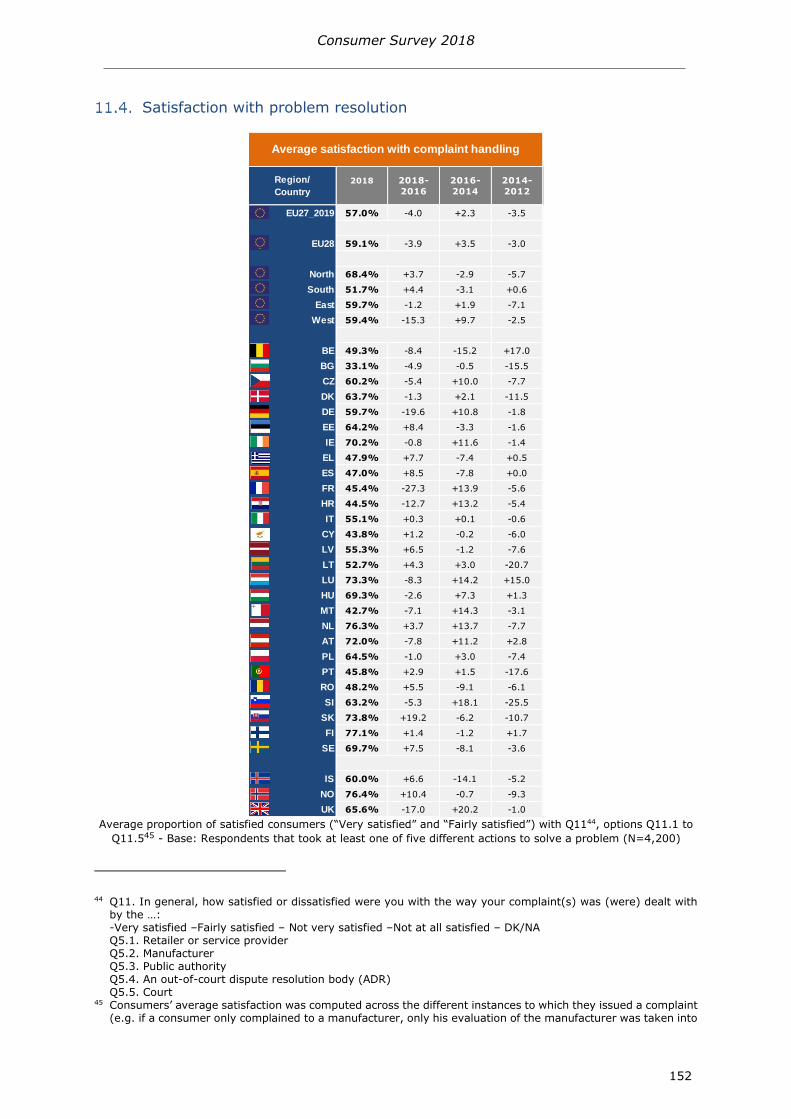

Satisfaction with problem resolution 152

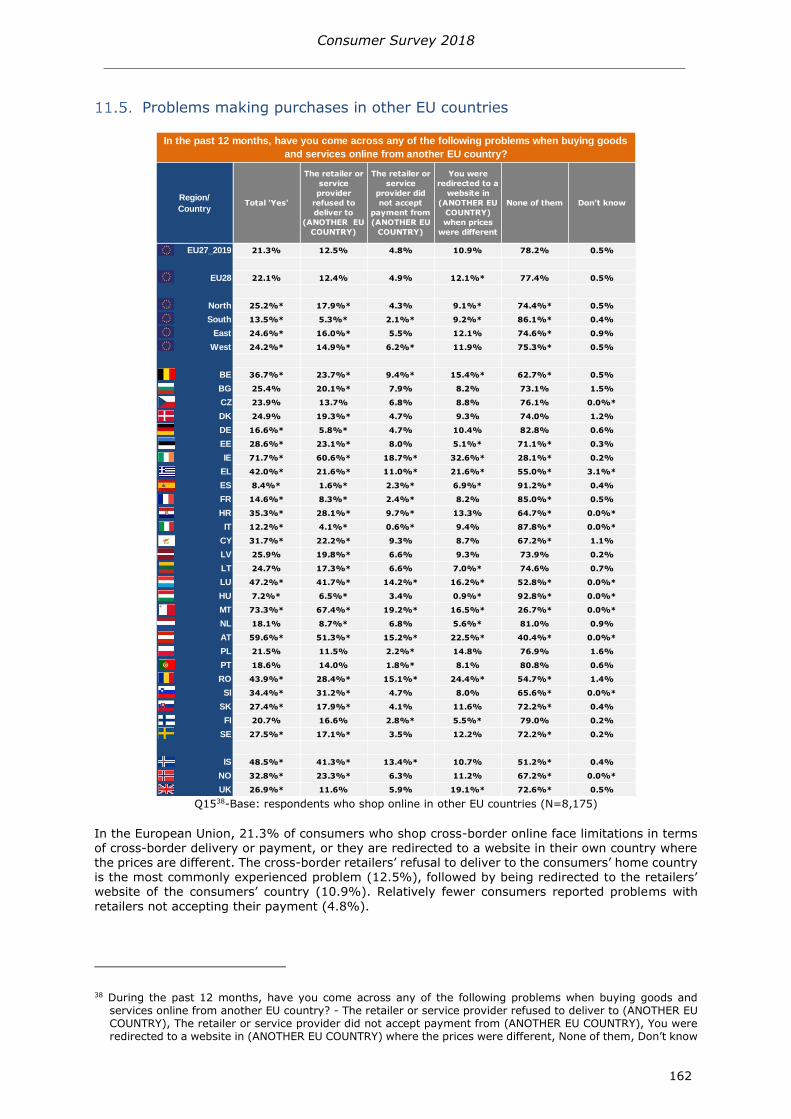

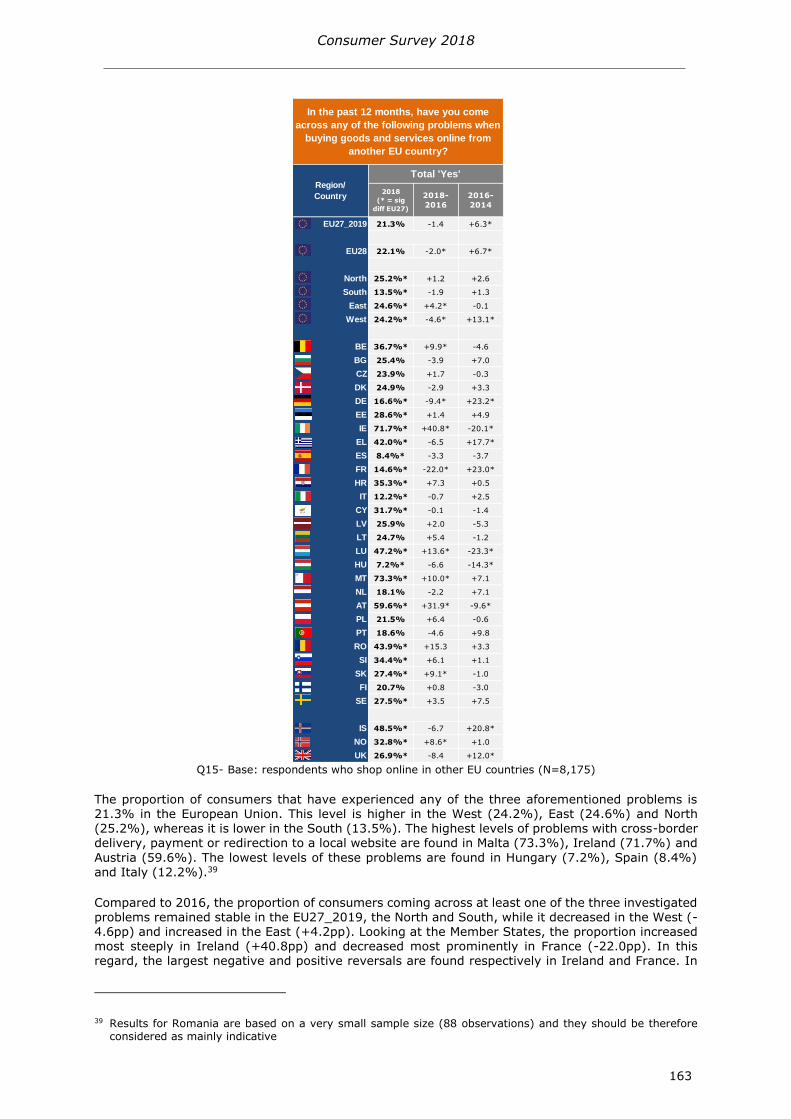

Problems making purchases in other EU countries 162

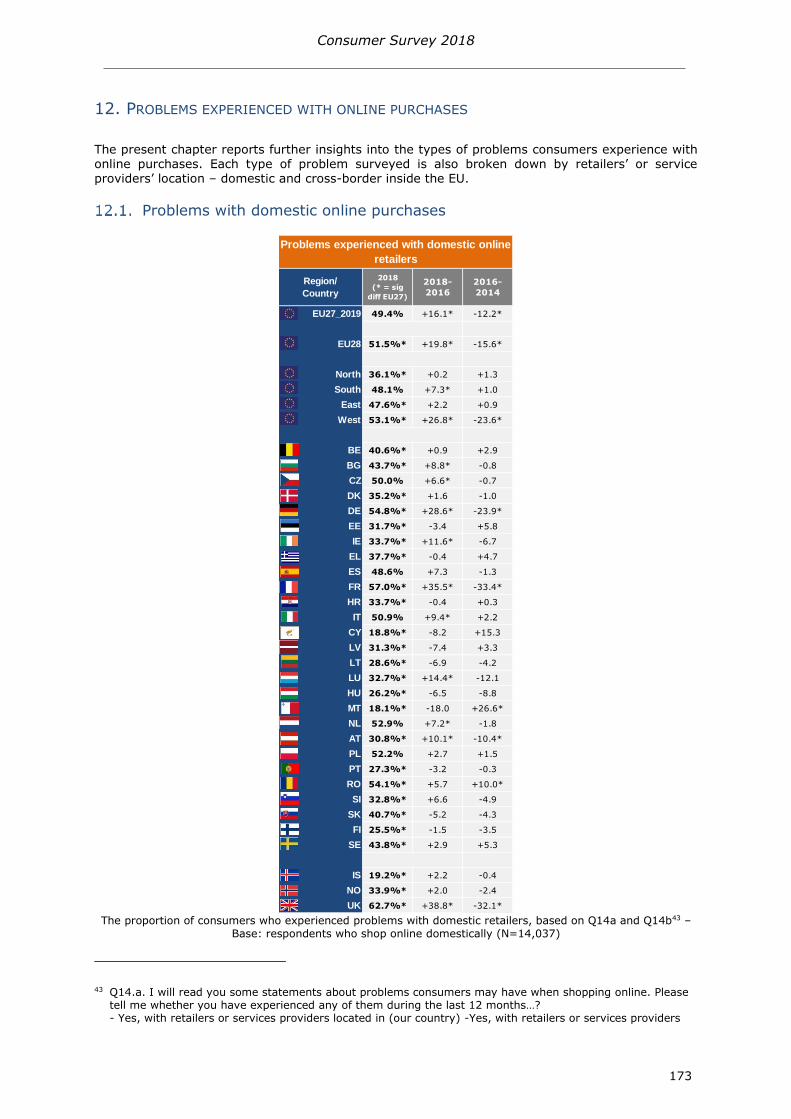

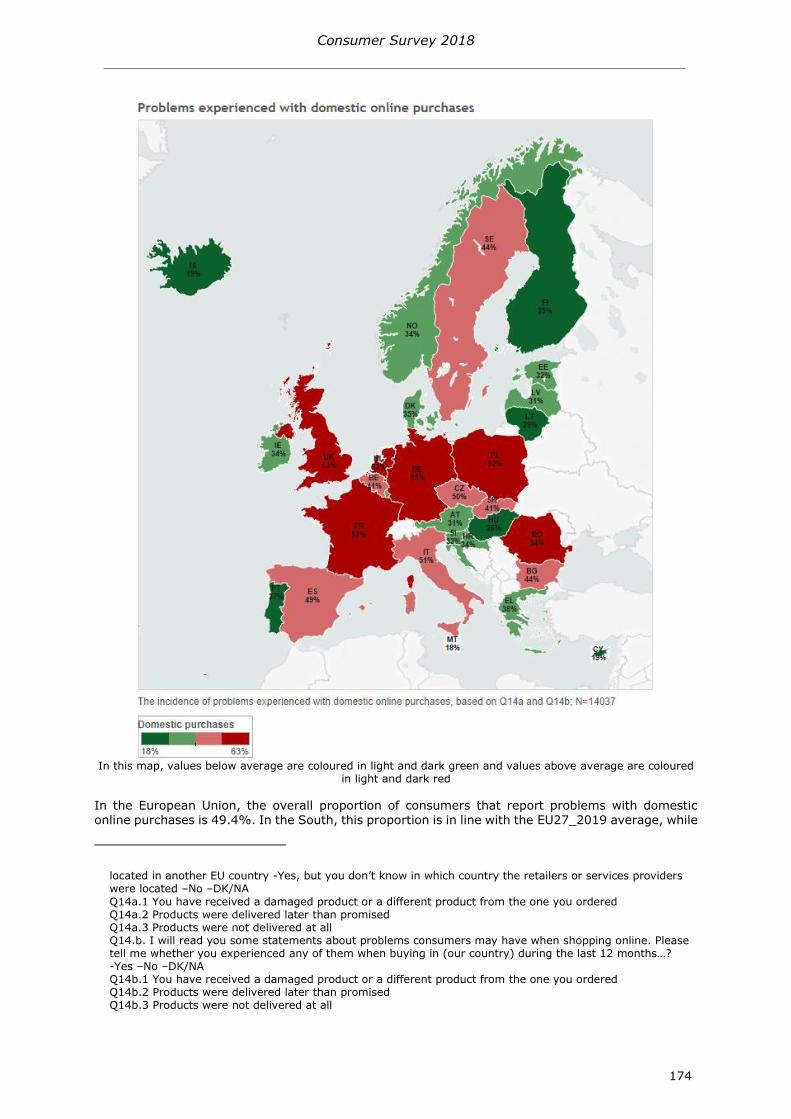

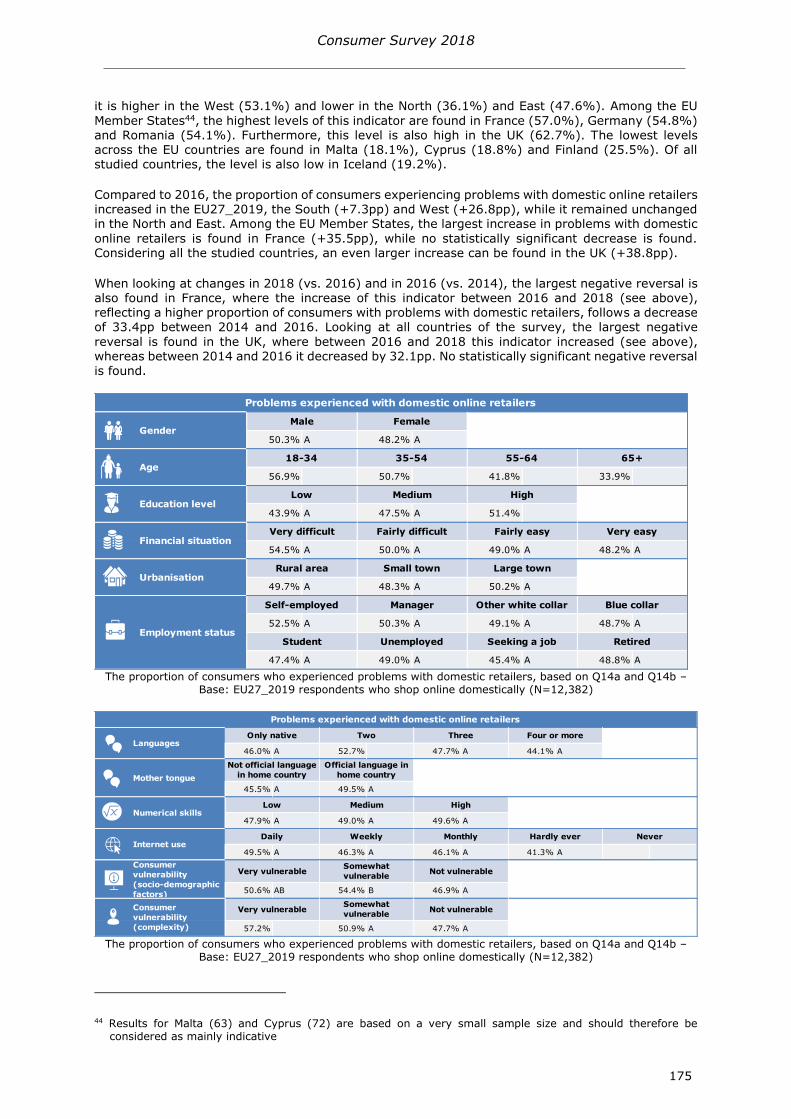

12 PROBLEMS EXPERIENCED WITH ONLINE PURCHASES 173

Problems with domestic online purchases 173

1211 Types of problems with domestic online retailers 177

Problems with cross-border purchases 182

1221 Types of problems with cross-border online retailers 186

Overall problems experienced 191

1231 Overall types of problems 193

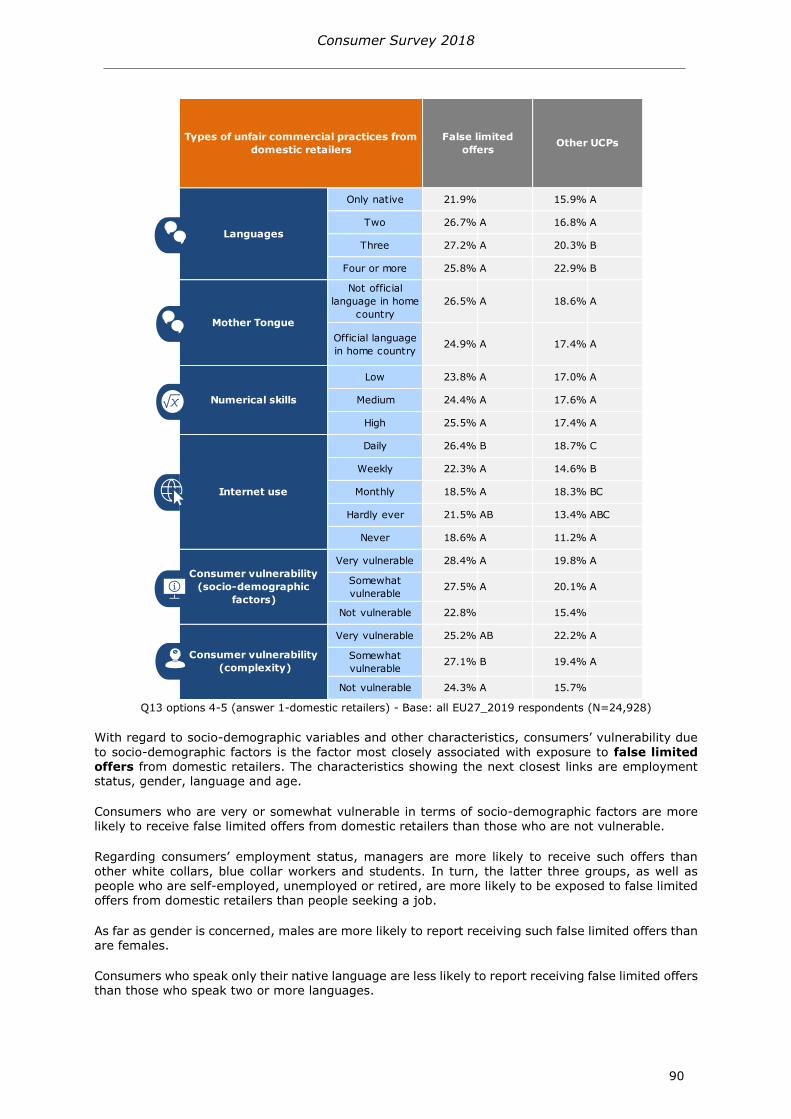

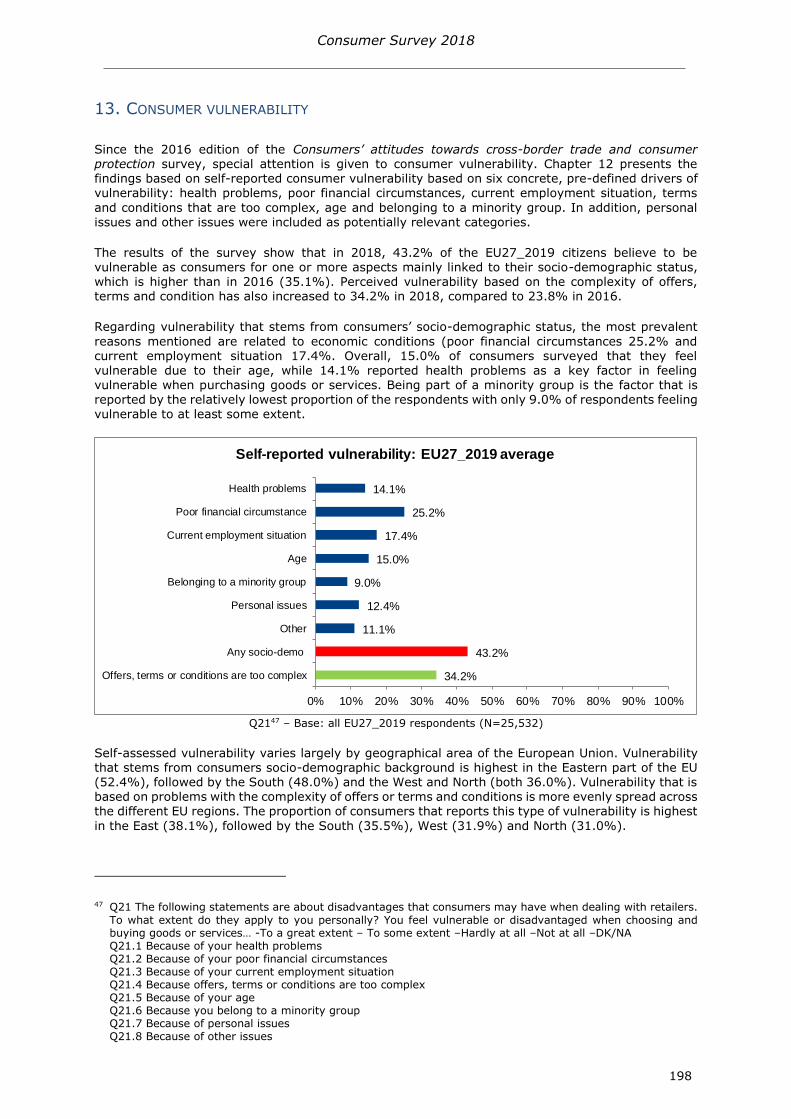

13 CONSUMER VULNERABILITY 198

14 DETERMINANTS OF CONSUMER CONDITIONS 202

15 ANNEX I SAMPLING METHODOLOGY 205

Consumer Survey 2018

7

1 INTRODUCTION

Introduction to the 2018 wave of the Consumer Survey

This report discusses the results of the 2018 edition of the survey on consumersrsquo attitudes towards

cross-border trade and consumer-related issues which is part of a series of reports within the EU Consumer Programme The study is a follow-up of a series of related studies that have been conducted since 20061 It was commissioned by the Consumers Health Agriculture and Food Executive Agency (Chafea) The European Commission gathers systematic evidence to monitor consumer markets and national consumer conditions within the EU summarised in the flagship Consumer Conditions Scoreboards (CCS) Results from this survey will feed the 15th edition of the CCS2

The present survey aims to deliver reliable results that are comparable with previous studies in the series on issues related to the attitudes perceptions and experiences of European consumers in the following areas

Domestic and cross-border commerce both online and offline

Knowledge of consumer rights

Trust in consumer protection

Perceptions of the product safety environment

Perceptions of environmental claims and their influence purchase decisions

Confidence in online shopping

Problems experienced actions taken and satisfaction with problem resolution

Exposure to unfair commercial practices

Consumer vulnerability

In total 28037 respondents took part in the survey which was carried out by GfK Social and

Strategic Research (GfK SSR) in the 27 Member States of the European Union and in the United Kingdom Iceland and Norway between 26 March and 11 May 2018 The report presents the overall results of the study as well as comparisons between the Member States socio-demographic variables and comparisons with the results from previous surveys

Sampling methodology

The target population includes all people aged 18 and above resident in the country surveyed and having sufficient command of (one of) the respective national language(s) to answer the questionnaire

In every country a random sample representative of the national population aged 18 or older was drawn by means of fixed line or mobile telephone number registers or Random Digit Dialling software The sampling procedure was set up to achieve a mix of respondents recruited through

mobile phone and fixed line Furthermore the sample intake was monitored to follow up on the

overall composition of the sample in terms of gender age and the ownership of a mobile andor a fixed phone For more information on the sampling methodology please consult Annex I

1 Special Eurobarometer 252 (2006) Special Eurobarometer 298 (2008) Flash Eurobarometer 282 (2009) Flash Eurobarometer 299 (2010) Flash Eurobarometer 332 (2011) Flash Eurobarometer 358 (2012) Flash Eurobarometer 397 (2014) and the Consumersrsquo attitudes towards cross-border trade and consumer related issues 2016 report (2016)

2 httpeceuropaeuconsumersconsumer_evidenceconsumer_scoreboardsindex_enhtm

Consumer Survey 2018

8

The respondents participated in a Computer Assisted Telephone Interview (CATI) conducted by

native speaking interviewers making use of a central programme They were interviewed on the core aspects of their experiences as consumers (see the aforementioned topics) as well as key socio-demographic variables such as age gender and education Based on these data averages and proportions are calculated for the countries and socio-demographic groups

121 Countries covered

The survey took place in the 27 EU Member States as well as in the United Kingdom Iceland and Norway The table below presents an overview of the country abbreviations and region comparisons used throughout the report

It should be noted that following the UKrsquos decision to leave the EU a new country grouping the EU27_2019 was introduced being equal to the EU28 without the UK The EU27_2019 is used as the main EU-aggregate and therefore as the comparison base for the results from the regions and countries While the EU28 aggregate (including the UK) is kept in the tables (for comparison

purposes) no comments are provided on this aggregate The terms lsquoEuropean Unionrsquo and lsquoEUrsquo used throughout the report always refer to the EU27_2019

The grouping of EU27_2019 countries into North East South and West regions was also adjusted to the new composition of the EU excluding the UK from the West In addition consistent with the analysis for the Market Monitoring Survey 2017 the Baltics (ie Lithuania Latvia and Estonia) were moved from the Eastern to the Northern region (the analysis has been adjusted for all years in the

report)

Finally Croatia has been included in the calculations of the EU27_2019 EU28 and regions results starting from 2012 This means that both for the 2014-2012 comparisons and the 2012-2011 comparisons Croatia is including in the EU averages For the latter comparison (ie 2012-2011) however Croatia is only included in the 2012 results resulting in a slight incoherence

Country EU27_2019 EU28 Region North

Region East

Region South

Region West

AT Austria X X X

BE Belgium X X X

BG Bulgaria X X X

CY Cyprus X X X

CZ Czech Republic X X X

DE Germany X X X

DK Denmark X X X

EE Estonia X X X

EL Greece X X X

ES Spain X X X

FI Finland X X X

FR France X X X

HU Hungary X X X

HR Croatia X X X

IE Ireland X X X

IT Italy X X X

LT Lithuania X X X

LU Luxembourg X X X

LV Latvia X X X

MT Malta X X X

NL Netherlands X X X

PL Poland X X X

PT Portugal X X X

RO Romania X X X

Consumer Survey 2018

9

122 Core questionnaire

The core questionnaire covered the following topics

Online and offline purchase of goods or services (trend questions)

Trust and perception of consumer protection (trend questions)

Perceptions of the product safety environment (trend questions)

Influence of environmental concerns on purchasing (trend questions)

Understanding of consumer rights (trend questions)

Problems experienced with domestic purchases in general actions taken (if no action taken reason why) satisfaction with complaint handling and time needed to resolve problem (trend questions)

Exposure to unfair commercial practices (trend questions)

Problems experienced when shopping online (domestic and cross-border purchases) (trend questions)

Consumer confidence in online shopping (trend questions)

Languages comfortably used for personal interests (trend question)

Numerical skills (trend questions)

Consumersrsquo self-reported vulnerability

123 Socio-demographic and background questions

Based on the final version of the questionnaire approved by the Contracting Authority the following questions were asked before the core questionnaire

Birthday rule (for fixed line sample)

Age

Gender

Phone ownership having a mobile (for fixed line sample)having a landline (for mobile line sample)

Regularity of using the internet

After the core questionnaire was completed the following socio-demographic questions were asked

Vulnerability (related to socio-demographic statusrelated to the perceived complexity of

offersterms and conditions)

SE Sweden X X X

SI Slovenia X X X

SK Slovakia X X X

UK United Kingdom X

NO Norway

IS Iceland

Consumer Survey 2018

10

Level of education

Employment situation (occupation)

Mother tongue of a respondent

Region of residence3

Subjective degree of urbanisation

Subjective financial situation

124 Analysis and reporting of statistically significant differences

All differences mentioned in the text are statistically significant unless otherwise mentioned Statistical significance is calculated at the 95 confidence level meaning that the null hypothesis of no difference has been rejected at 5 probability level Differences that are not statistically

significant are considered equal to 0 Consequently the report may describe two values as being equal even if the difference between both values is not equal to 0 It should also be mentioned that especially for measures referring to the entire EU27_2019EU28 given the large sample size for the

survey some differences could be statistically significant even if their absolute magnitude is very small

The findings for the EU27_2019 EU28 the four EU27_2019 regions (North South East and West) and the individual country results are analysed using cross-tabulations Please note that in the region and country tables results that are statistically different from the EU27_2019 average are indicated by asterisks

Differences between the levels of socio-demographic categories are analysed with a regression analysis which explores the relationship between a specific independent variable (eg age) and a dependent variable (eg online purchase behaviour) while considering the effects of other independent variables (eg gender education etc) This type of analysis is considered more appropriate when exploring the impact of socio-demographic variables due to the potential overlap (correlations) between different socio-demographic factors which need to be considered when

measuring the extent to which one of these factors affects the dependent variables The following

regression models are used for the analysis of the different dependent variables

Logit models when the dependent variable is binary (ie it takes only two possible values 0 and 1 eg trust in product safety trust in environmental claims)

Poisson models for dependent variables that can be thought of as a count variable (eg knowledge of consumer rights trust in organisations)

Linear models when the dependent variable is assumed to be numerical and linear (eg problems and complaints)

In all models a control variable on the region of residence of the person interviewed (North South East and West) has been included

3 Regions was recorded on NUTS level 3 (Estonia Croatia Latvia Lithuania Malta Slovenia amp Iceland) and NUTS level 2 (all other countries)

Consumer Survey 2018

11

The values shown in the tables of the socio-demographic analyses are based on model estimates4

Statistically significant differences between levels of a socio-demographic variable are indicated with letters The categories of a socio-demographic variable are statistically significant different from each other except when the categories share the same letter When a category is associated to a blank it means that it is statistically significant different from all the other categories Differences and equalities for socio-demographic results are only considered within each socio-demographic variable (eg 18-34 yearsrsquo old vs 35-54 yearsrsquo old) and not between socio-demographic variables (eg 18-34 yearsrsquo old vs women)

Up to five socio-demographic characteristics with the closest link with the respective dependent variable are reported on in detail Characteristics with the closest link are selected considering the average magnitude of the difference across the factor attributes ndash in absolute terms (eg the differences in the knowledge of consumer rights ndash in absolute terms ndash across the different levels of internet use) ndash and by looking at the overall coherence of these differences

The report describes changes between the current (2018) and previous (2016) waves In addition

changes in the latest waves (2018-2016) are compared to changes in the previous waves (2016-

2014) This is reported on only when both changes are significant and when the direction of the change has reversed ie from an increase to a decrease or from a decrease to an increase For positive indicators (ie knowledge of consumer rights domestic online shopping etc) these cases are labelled ldquonegative reversalrdquo and ldquopositive reversalrdquo respectively For negative indicators (eg problems and complaints exposure to unfair commercial practices etc) the labels are reversed to account for the negative valence of the indicator where an increase would reflect a change towards

the negative The current report focuses on the strongest positive and negative reversals which are determined by the highest absolute sum of both changes

125 Weighting and wave to wave comparisons

Data from the current wave was weighted based on the latest Eurostat data5 available on age (three groups 18-34 35-54 and 55+ year old) and gender distributions In addition the weighting was

also based on telephone ownership data from the Special Eurobarometer 4386 (three groups fixed only mobile only mixed) Finally population weights were also applied both on the EU27_2019 sample (for the EU27_2019 average) and the EU28 sample (for the EU28 average and regions) to account for differences in population size at country level

In contrast with the current Consumer Survey the Consumer Survey 2016 was only weighted on age and gender (in addition to the population weight) To facilitate comparisons between 2018 and 2016 a second weight was calculated for the 2018 survey based solely on age and gender

Both the Consumer Survey 2016 and 2018 have been conducted with a target population of 18+ years while the Consumer Surveys 2014 and earlier are based on a sample of 15+ years For comparisons between the years 2016 and 2014 the latter has been reweighted based on age and gender distributions Data from all waves before 2014 will be used for the wave to wave comparisons based on existing samples (population 15+) and using the existing weights provided by the Contracting Authority (also based on the 15+ population distribution) When comparing 2014 data

4 Model estimates are calculated using the margins function in Stata A margin is a statistic based on a fitted model calculated over a dataset in which some of or all the covariates are fixed at values different from what they really are In the models estimated for this report the margins function calculates the predicted means for the different values of a socio-demographic variable (eg age) while all the other covariates (including the

other socio-demographic variables) are hold fixed In practice the estimated value of a dependant variable Y (ex the of persons who have bought online in the last 12 months) for the male category is obtained under the hypothesis that all the persons interviewed are males while their remaining sociodemographic characteristics (used in the model as regressors) corresponds to the categories observed in the sample

In addition a pwcompare (group effects) option was added to the function to perform pairwise comparisons between all levels of a socio-demographic variable based on the estimated models These comparisons provided information to determine the variables with the closest link with the respective dependent variable

5 Eurostat Population on 1 January 2018 by age sex and NUTS 2 region updated on 27 February 2018

6 Special Eurobarometer 438 E-Communications and the Digital Single Market (2016) available via httpdataeuropaeueuodpendatadatasetS2062_84_2_438_ENG

Consumer Survey 2018

12

to previous waves the original weight will be used based on the 15+ population distribution The

difference in sampling will be clearly communicated when wave-to-wave changes are reported

To summarise the following weighting procedures were used to calculate the results presented in the final report additional analyses and country profiles

2018 Population gender amp age weighting (18+) phone ownership weighting

2016 Population gender amp age weighting (18+)

2014 Population gender amp age weighting (18+)

2014 Population gender amp age weighting (15+)

2012 Population gender amp age weighting (15+)

2011 Population gender amp age weighting (15+)

2010 Population gender amp age weighting (15+)

2009 Population gender amp age weighting (15+)

2008 Population gender amp age weighting (15+)

2006 Population gender amp age weighting (15+)

In conclusion it should be considered that in the light of the methodological approach indicated above

Changes with respect to the previous year ndash which are shown in graphs and tables throughout the report - are always computed on comparable data

However given the change in methodology applied for the 2018 results (age gender amp phone ownership) and the 2018-2016 comparison (age amp gender no phone ownership) it is not possible to compute the exact results for 20167 by subtracting the 2018-2016 change from

the 2018 results The same is true for the changes in previous waves

The applied methodology ensures comparability between the current (2018) and previous (2016) wave As such it is in principle possible to estimate values in level for 2016 by applying back the observed changes between 2016 and 2018 as reported in graphs and tables throughout the report However due to different weightings applied to the 2018 data for presenting the 2018 results and for comparisons with the 2016 results small differences may occur

Differences between 2014 and previous waves are reported based on the original methodology while data in levels is not reported as it is not consistent with the last two waves Because of the lack of comparability with data reported for the last two waves (2016 and 2018) it is not possible to estimate data in levels for the years 2012 and before

7 As presented in the 2017 Consumer Conditions Scoreboard (available via httpseceuropaeuinfositesinfofilesconsumer-conditions-scoreboard-2017-edition_enpdf)

Consumer Survey 2018

13

2 EXECUTIVE SUMMARYKEY FINDINGS

This report presents the findings of the 2018 edition of the survey on consumersrsquo attitudes towards cross-border trade and consumer-related issues which was carried out by GfK SSR8 for the Consumers Health Agriculture and Food Executive Agency (Chafea) and the Directorate General Justice and Consumers of the European Commission The present survey is part of a series of reports

within the EU Consumer Programme which has been performed since 2006 with the aim to monitor national consumer conditions across the EU For this purpose the study assessed several indicators of European consumersrsquo attitudes for 28037 respondents across the EU27_2019 Member States and in the United Kingdom Iceland and Norway For the studied indicators the present report discusses the overall results comparisons between Member States and differences with previous waves of this survey as well as across selected socio-demographic characteristics

In summary the present study reports on the current state of European consumersrsquo attitudes and

experiences regarding cross-border trade and consumer-related issues It provides insights in the magnitude and features of domestic as well as cross-border shopping and identifies areas for improving the consumer experiences The findings of the 2018 edition of this survey have worsened9 slightly for a wide variety of indicators compared to the 2016 edition Most of these developments

are driven for a large part by changes in the Western region After noticeable improvements in this region in the 2016 wave the indicators have gone back to resemble their previous levels

The first key indicator explored in the survey is online purchase behaviour In total almost three out of four EU27_2019 consumers recently bought goods or services online (720) The 2018 survey shows a small decrease of 14 percentage points in online shopping compared to 2016 which is slight reversal of the positive evaluation observed since 2006 Online shopping is most common in the Northern (785) Western (751) and Eastern (719) regions10 of the EU whereas in the Southern (660) region the indicator is lower

Most European consumers11 shop online within their own country (630) A more limited number

of Europeans purchase goods or services cross-borders inside the EU (283) or outside the EU (184) The results also show that the proportion of consumers making online purchases within their own country has slightly decreased compared to 2016 This decrease is mostly driven by a lower value in the Western region (-116pp12) while the degree of domestic online purchases has increased in all other regions The proportion of consumers making online purchases cross-border inside the EU has increased compared to 2016 (+91pp) these purchases have increased in the

Eastern (+57pp) Southern (+45pp) and Northern (+40pp) region while they have decreased in

the Western region (+144pp) Nevertheless cross-border online purchases in the Western region are still the second highest (322) after the Northern region (343)

The observed decrease in domestic online shopping is not reflected by a change in confidence in making online purchases which has remained stable since 2016 On average 694 of European consumers report that they are confident in domestic online shopping However it is noticeable that there is a decrease in confidence in the Western region (-73pp) which goes together with a decrease

in domestic online shopping in the same region Furthermore despite the increase in cross-border online shopping confidence in this type of shopping online decreases compared to 2016 (-79pp)

For effectively protecting online consumers it is important that individuals know their rights when shopping online This survey assessed the level of knowledge about three types of consumer rights the cooling-off period the legal guarantees and the regulation with regard to unsolicited products The average level of knowledge about these rights is at 455 a 27pp decrease compared

8 GfK SSR refers to the GFK Social amp Strategic Research unit which focuses on Public Affairs research GfK SSR has been taken over by the market research company Ipsos in October 2018 and is now part of the Ipsos

Public Affairs unit 9 ie lower values for positive indicators such as knowledge of consumer rights or higher values for negative

indicators such as exposure to unfair commercial practices 10 The grouping of EU27_2019 countries into North East South and West regions was adjusted to the new

composition of the EU excluding the UK from the West In addition consistent with the analysis for the Market Monitoring Survey 2017 the Baltics (ie Lithuania Latvia and Estonia) were moved from the Eastern to the Northern region (the analysis has been adjusted for all years in the report)

11 Throughout the remainder of the Executive Summary ldquoEuropean consumersrdquo and ldquoEuropeansrdquo will be used to refer to EU27_2019 consumers

12 Percentage points

Consumer Survey 2018

14

to the previous wave of the survey Whereas this decrease is evident in Western and Northern

Europe the knowledge of consumer rights has increased in the South (+42pp) Europeans in general are best informed about the cooling off period (610) and slightly less informed about faulty product guarantees (409) and unsolicited products (345)

The present report also assesses the trust of European consumers in the protection of their rights in the single market To study this the levels of different aspects of trust are measured First in terms of trust in organisations and redress mechanisms the respondents indicated the highest levels of trust in retailers and service providers (713) public authorities (618) and NGOs

(607) Lower levels of trust are observed for the ADR (Alternative Dispute Resolution 422) and courts (316) The average levels of trust have decreased in the present study compared to 2016 (-53 pp) The most notable decreases are observed for trust in NGOs (-88pp) courts (-75pp) and the ADR (-69pp)

In addition the survey also investigated trust in product safety which is considered a key driver of consumer confidence In the EU27_2019 almost 7 out of 10 consumers have expressed trust in

product safety However this trust has decreased compared to 2016 (-73pp) and this happened particularly in the West (-216pp)

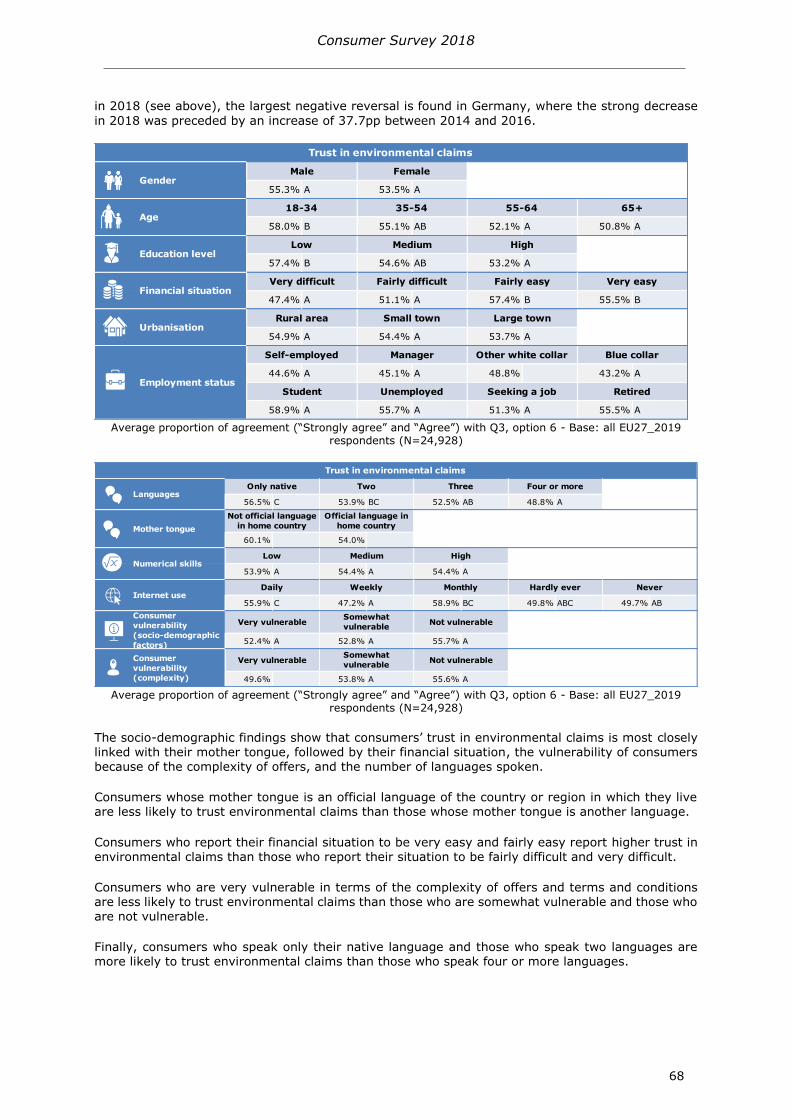

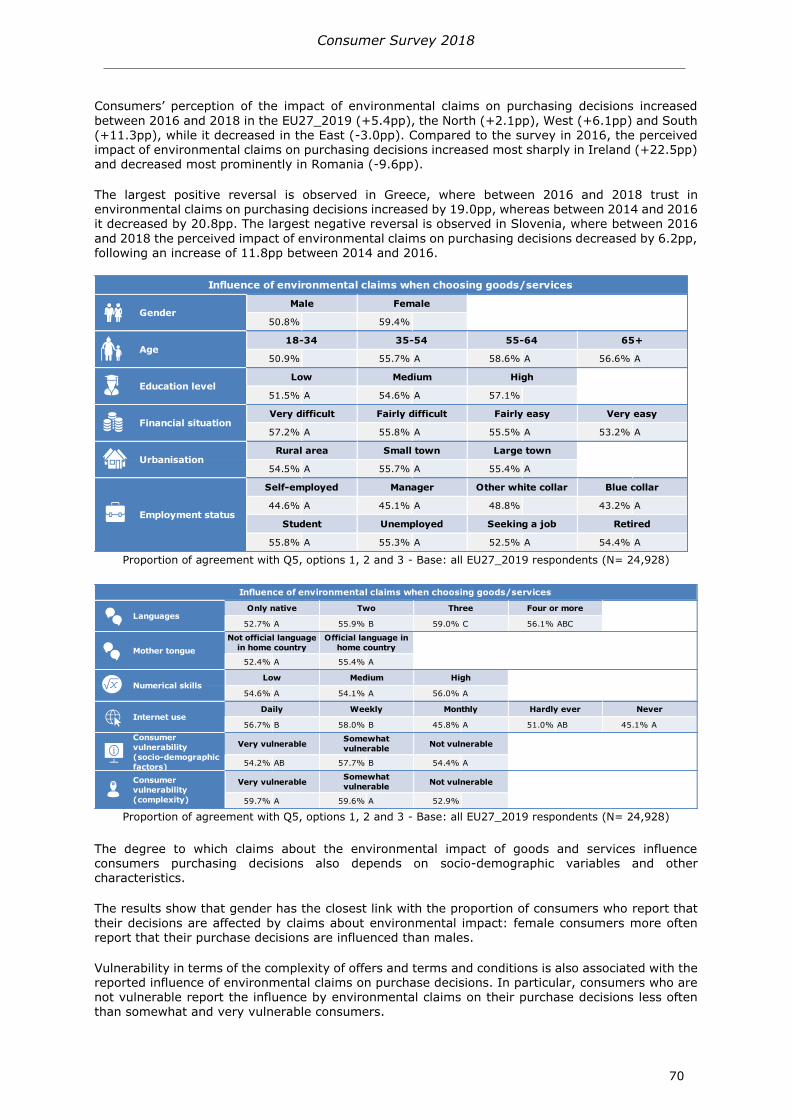

Trust in the reliability of environmental claims which is at 542 in the EU27_2019 also decreased between 2016 and 2018 (by 91 pp)

When shopping online some European consumers encounter unfair commercial practices (UCPs) The survey investigated the exposure to several types of practices that fall within the scope of the Unfair Commercial Practices Directive The overall findings show that the exposure to such practices

originating from domestic (227) and cross-border (48) retailers has increased compared to 2016 (with +47pp and +24pp respectively) In addition to unfair commercial practices consumers in Europe also face other illicit commercial practices when shopping online from domestic retailers (106) and cross-border retailers (36)

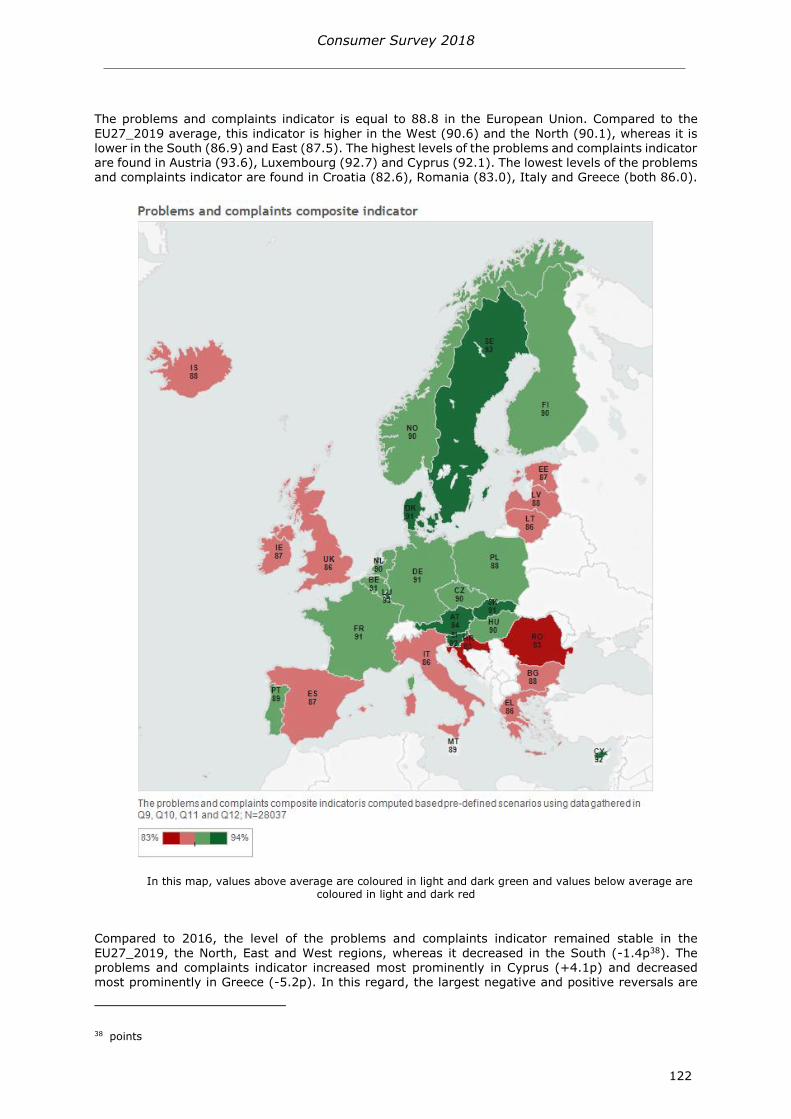

A composite problems and complaints indicator13 was developed in 2014 to measure the problems encountered by European consumers the actions they took their satisfaction with complaint handling and (if applicable) their reasons for not taking action A higher score on this

indicator represents fewer problems and a higher satisfaction with complaint handling The overall level of this indicator is at a high level in the EU27_2019 (a score of 888) and it is the highest in the

West (906) and North (901) regions

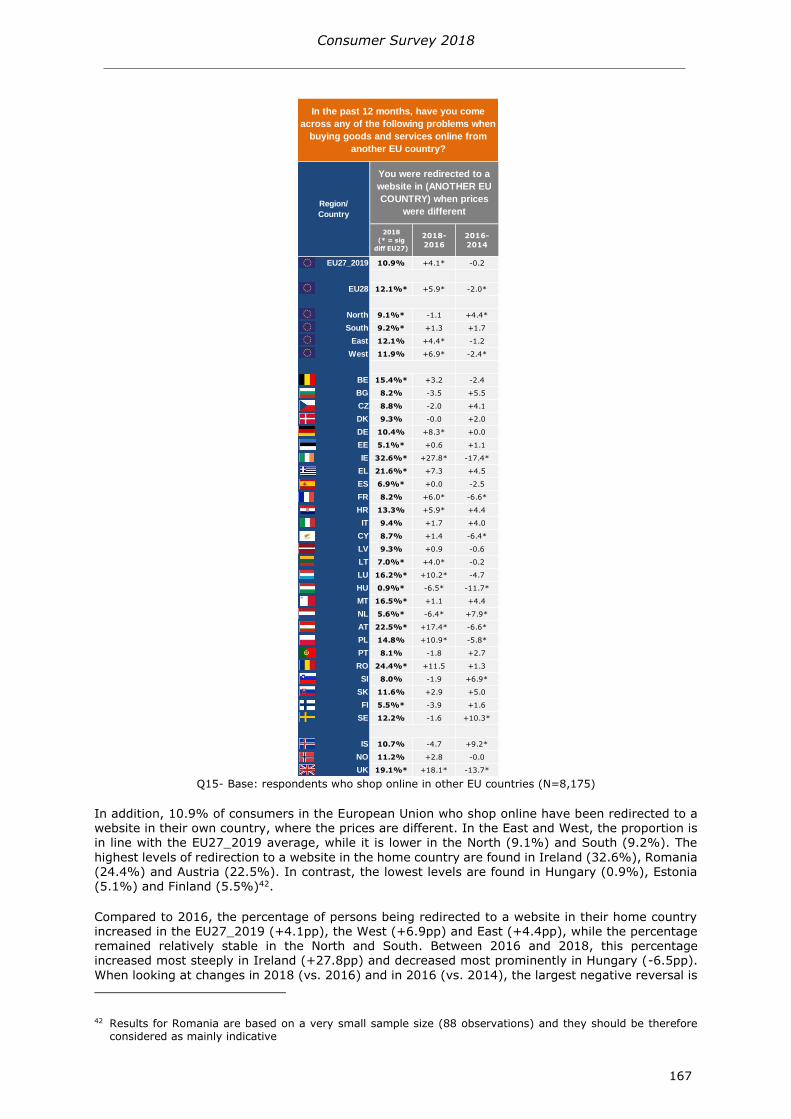

A fair share of European consumers (213) also experiences problems that are specific to online cross-border purchases from other EU countries The most common problems of this type are the refusal of retailers to deliver to the consumersrsquo country (125) and the redirection of consumers

to a website in their home country where prices are different (109) The exposure to both problems has increased since 2016 (respectively +26pp and +41pp)

European consumers are also exposed to problems specific to the delivery of online purchases Late delivery of goods is most common both for purchases from domestic online retailers (393) and cross-border retailers (278) In addition a noticeable proportion of respondents also experiences damaged or wrong deliveries of goods (respectively 198 for domestic and 115 for cross-border online purchases)

In case problems do occur the most likely actions taken by consumers are complaining to the retailer (852) or complaining to the manufacturer (157) In contrast bringing businesses to court (24) or addressing problems via an ADR platform (55) are the least likely actions In

some cases consumers refrain from taking any actions when faced with a problem The main reasons for not taking actions are that consumers believe it would take long to resolve the problem (412) or that the sums involved are too small (357)

13 See footnote 22 and 23 (page 117) in the main report for more information on this indicator and its computation

Consumer Survey 2018

15

Continuing the approach started with the 2016 wave of the survey the 2018 survey also assessed

consumer vulnerability The results show that about a quarter of the European consumers (265) self-identify as vulnerable for one or more aspects linked to their socio-demographic background This is lower than in 2016 (317) In contrast perceived vulnerability based on the experienced complexity of offer terms and conditions (342) has increased considerably since 2016 (213)

Finally multiple multivariate analyses were conducted to provide insights into the role of socio-demographic factors Consumersrsquo financial situation is the factor most closely linked to key consumer conditions indicators Specifically consumers in a difficult financial situation tend to show

lower trust in organisations lower confidence in online shopping lower trust in product safety lower trust in environmental claims and a higher probability to experience UCPs In addition severe financial problems are also negatively linked with trust in organisations trust in redress mechanisms and confidence in online shopping and positively linked with exposure to UCPs

Consumer Survey 2018

16

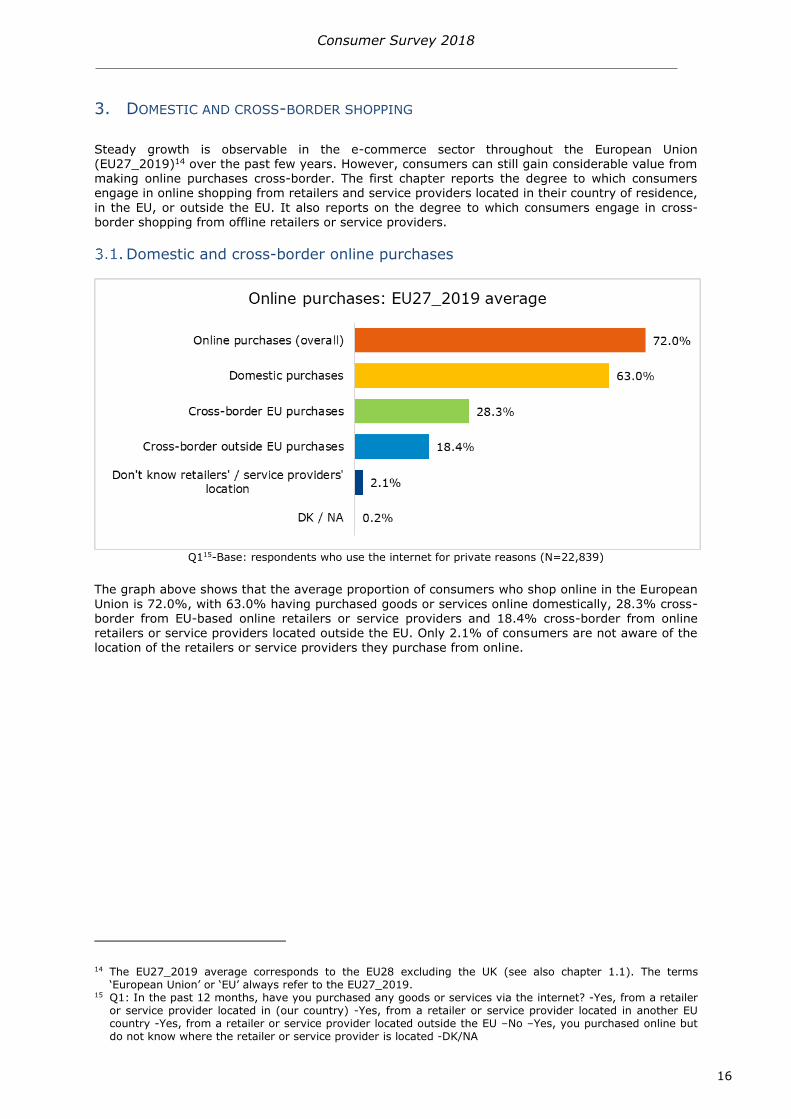

3 DOMESTIC AND CROSS-BORDER SHOPPING

Steady growth is observable in the e-commerce sector throughout the European Union (EU27_2019)14 over the past few years However consumers can still gain considerable value from making online purchases cross-border The first chapter reports the degree to which consumers engage in online shopping from retailers and service providers located in their country of residence

in the EU or outside the EU It also reports on the degree to which consumers engage in cross-border shopping from offline retailers or service providers

Domestic and cross-border online purchases

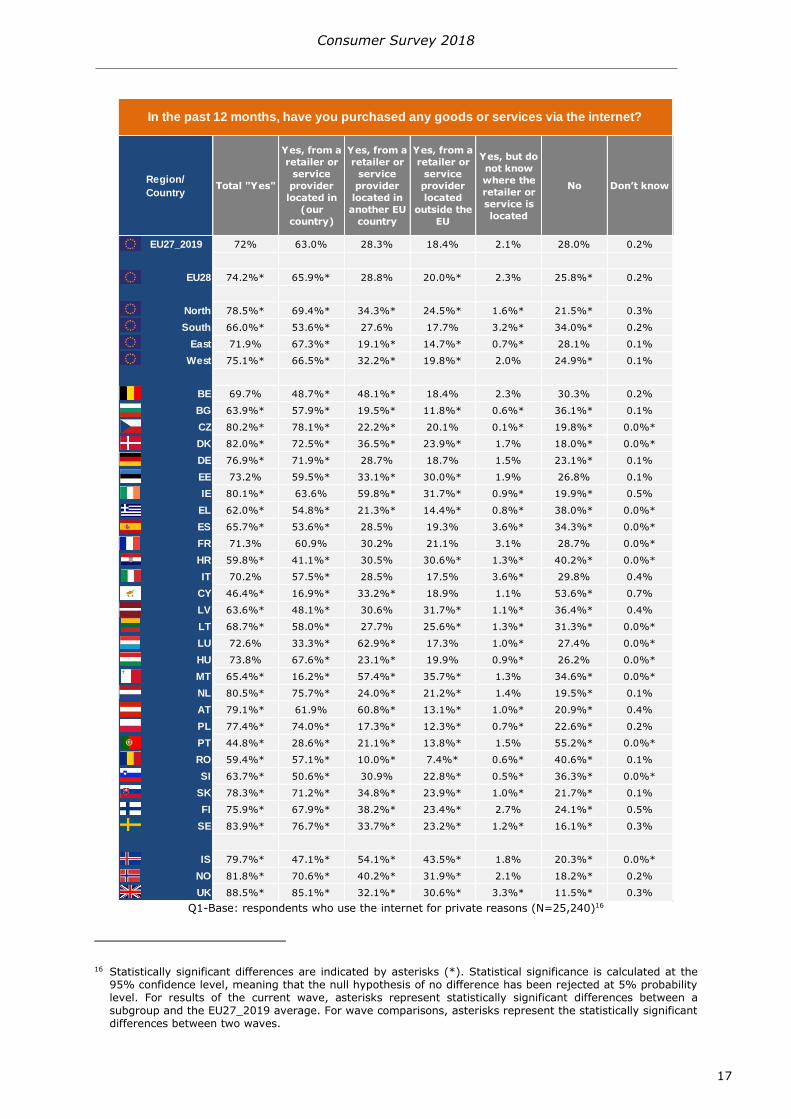

Q115-Base respondents who use the internet for private reasons (N=22839)

The graph above shows that the average proportion of consumers who shop online in the European

Union is 720 with 630 having purchased goods or services online domestically 283 cross-border from EU-based online retailers or service providers and 184 cross-border from online

retailers or service providers located outside the EU Only 21 of consumers are not aware of the location of the retailers or service providers they purchase from online

14 The EU27_2019 average corresponds to the EU28 excluding the UK (see also chapter 11) The terms lsquoEuropean Unionrsquo or lsquoEUrsquo always refer to the EU27_2019

15 Q1 In the past 12 months have you purchased any goods or services via the internet -Yes from a retailer or service provider located in (our country) -Yes from a retailer or service provider located in another EU country -Yes from a retailer or service provider located outside the EU ndashNo ndashYes you purchased online but do not know where the retailer or service provider is located -DKNA

Consumer Survey 2018

17

Q1-Base respondents who use the internet for private reasons (N=25240)16

16 Statistically significant differences are indicated by asterisks () Statistical significance is calculated at the 95 confidence level meaning that the null hypothesis of no difference has been rejected at 5 probability level For results of the current wave asterisks represent statistically significant differences between a subgroup and the EU27_2019 average For wave comparisons asterisks represent the statistically significant differences between two waves

Region

CountryTotal Yes

Yes from a

retailer or

service

provider

located in

(our

country)

Yes from a

retailer or

service

provider

located in

another EU

country

Yes from a

retailer or

service

provider

located

outside the

EU

Yes but do

not know

where the

retailer or

service is

located

No Donrsquot know

EU27_2019 72 630 283 184 21 280 02

EU28 742 659 288 200 23 258 02

North 785 694 343 245 16 215 03

South 660 536 276 177 32 340 02

East 719 673 191 147 07 281 01

West 751 665 322 198 20 249 01

BE 697 487 481 184 23 303 02

BG 639 579 195 118 06 361 01

CZ 802 781 222 201 01 198 00

DK 820 725 365 239 17 180 00

DE 769 719 287 187 15 231 01

EE 732 595 331 300 19 268 01

IE 801 636 598 317 09 199 05

EL 620 548 213 144 08 380 00

ES 657 536 285 193 36 343 00

FR 713 609 302 211 31 287 00

HR 598 411 305 306 13 402 00

IT 702 575 285 175 36 298 04

CY 464 169 332 189 11 536 07

LV 636 481 306 317 11 364 04

LT 687 580 277 256 13 313 00

LU 726 333 629 173 10 274 00

HU 738 676 231 199 09 262 00

MT 654 162 574 357 13 346 00

NL 805 757 240 212 14 195 01

AT 791 619 608 131 10 209 04

PL 774 740 173 123 07 226 02

PT 448 286 211 138 15 552 00

RO 594 571 100 74 06 406 01

SI 637 506 309 228 05 363 00

SK 783 712 348 239 10 217 01

FI 759 679 382 234 27 241 05

SE 839 767 337 232 12 161 03

IS 797 471 541 435 18 203 00

NO 818 706 402 319 21 182 02

UK 885 851 321 306 33 115 03

In the past 12 months have you purchased any goods or services via the internet

Consumer Survey 2018

18

Overall 630 of EU27_2019 respondents who use the internet for private reasons report shopping

online domestically Consumers residing in the North (694) East (673) and West regions (665) are more likely to engage in online shopping domestically compared to the EU27_2019 average while those in the South are less likely (536) Among the countries of the European Union the highest levels of domestic shopping online are found in the Czech Republic (781) Sweden (767) and the Netherlands (757) Among all the studied countries the highest level is found in the UK (851) The lowest levels are found in Malta (162) Cyprus (169) and Portugal (286)

The proportion of respondents who shop online cross-border from retailers or service providers in another EU country is 283 in the EU27_2019 The incidence of shopping online from retailers in another EU country in the South is in line with the EU27_2019 average17 while it is higher in the North (343) and the West (322) and lower in the East (191) The highest levels of online cross-border shopping from retailers or service providers in another EU country are found in Luxembourg (629) Austria (608) and Ireland (598) The lowest levels are found in

Romania (100) Poland (173) and Bulgaria (195)

In the European Union 184 of consumers shop online cross-border from retailers or service

providers in countries outside the EU For consumers in the South this incidence is in line with the EU27_2019 average while it is higher in the North (245) and West (198) and lower in the East (147) Among the EU countries the highest levels of this indicator are found in Malta (357) Latvia Ireland (both 317) and Croatia (306) Furthermore this level is also high in Iceland (435) and Norway (319) The lowest levels are found in Romania (74) Bulgaria

(118) and Poland (123)

Only 21 of EU27_2019 consumers do not know where the retailer or service provider they shopped from online is located For consumers in the West the proportion not being aware of the retailersrsquo location is in line with the EU27_2019 average while it is higher in the South (32) and lower in the North (16) and East (07) Among the EU countries the highest levels of this indicator are found in Italy Spain (both 36) Lithuania and Croatia (both 13) Additionally this level is also high in the UK (33) The lowest levels are found in the Czech Republic (01) Slovenia

(05) Bulgaria and Romania (both 06)

17 As mentioned in chapter 124 differences that are not statistically significant are considered equal to 0 regardless of their numerical level

Consumer Survey 2018

19

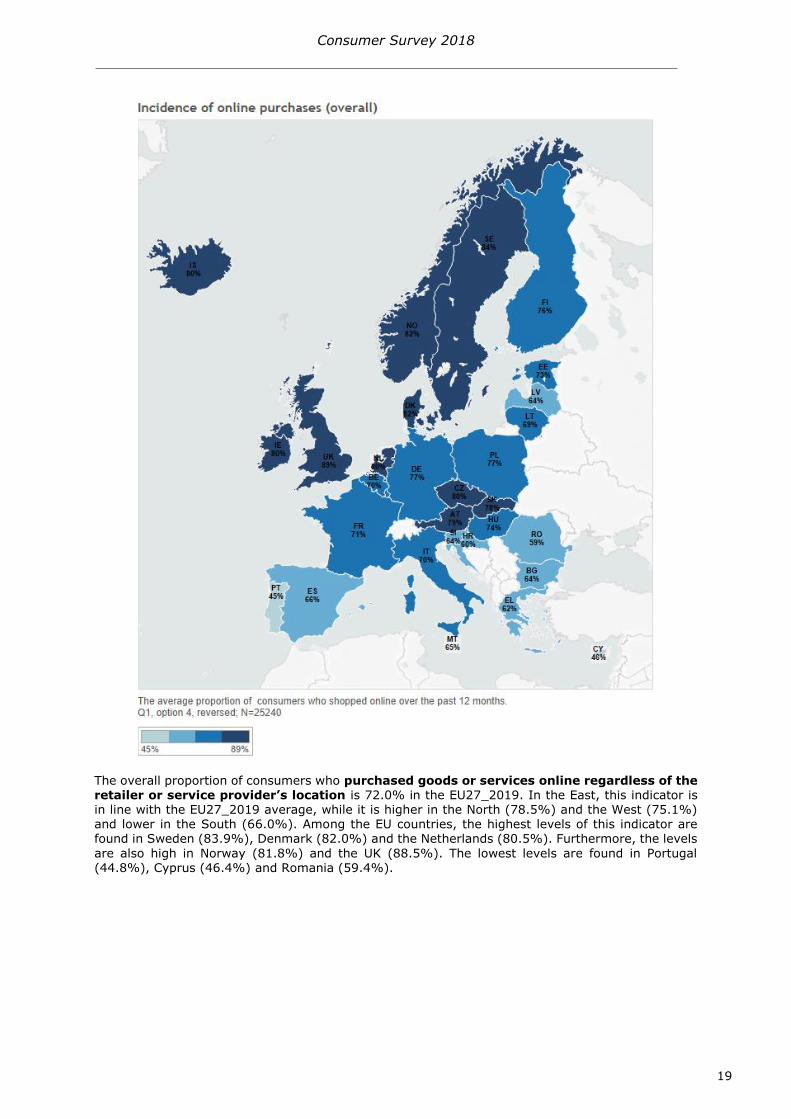

The overall proportion of consumers who purchased goods or services online regardless of the retailer or service providerrsquos location is 720 in the EU27_2019 In the East this indicator is in line with the EU27_2019 average while it is higher in the North (785) and the West (751) and lower in the South (660) Among the EU countries the highest levels of this indicator are found in Sweden (839) Denmark (820) and the Netherlands (805) Furthermore the levels

are also high in Norway (818) and the UK (885) The lowest levels are found in Portugal (448) Cyprus (464) and Romania (594)

Consumer Survey 2018

20

Q1-Base EU27_2019 respondents from the EU who use the internet for private reasons (N=2248718)

18 The EU27_2019 sample size for this table and all following socio-demographic tables is affected by missing values for some of the socio-demographic factors (internet use languages education amp urbanisation) Respondents with missing values for any of these socio-demographic factors are not included in the regression analysis used to estimate the results

Male 711 A 642 A 314 216 19 A 271 A 03 A

Female 698 A 625 A 254 152 23 A 282 A 01 A

18-34 787 688 A 355 264 20 AB 195 02 A

35-54 740 668 A 302 181 17 A 245 00 A

55-64 653 591 228 133 30 B 318 03 A

65+ 543 499 158 80 21 AB 438 02 A

Low 580 510 170 110 12 A 404 07 A

Medium 684 618 266 179 21 AB 299 01 A

High 757 674 317 200 23 B 221 02 A

Very difficult 652 A 574 A 209 187 A 14 A 340 A 02 A

Fairly difficult 688 A 609 A 284 A 175 A 16 A 299 A 00 A

Fairly easy 714 644 287 A 187 A 22 A 266 02 A

Very easy 745 682 306 A 192 A 31 A 222 02 A

Rural area 701 A 636 A 283 A 160 18 A 284 A 01 A

Small town 711 A 636 A 279 A 198 A 22 A 268 A 02 A

Large town 699 A 626 A 292 A 189 A 22 A 282 A 01 A

Self-employed 737 C 668 C 327 C 208 B 16 A 251 AB 02 ABC

Manager 758 C 669 BC 327 BC 212 B 25 AB 222 A 00 AB

Other white collar 729 BC 661 BC 287 B 173 A 20 AB 250 A 04 C

Blue collar 667 A 595 A 258 A 189 AB 27 AB 309 C 00 AB

Student 704 ABC 595 A 277 ABC 178 AB 17 AB 280 ABC 02 ABC

Unemployed 650 A 589 A 230 A 181 AB 23 AB 328 C 00 A

Seeking a job 656 A 587 A 220 A 191 AB 49 B 305 BC

Retired 692 AB 620 AB 275 AB 170 AB 15 A 295 C 01 B

Financial Situation

In the past 12 months have you

purchased any goods or services via the

Internet

Total Yes

Yes from a

retailer or service

provider located in

(our country)

Yes from a

retailer or service

provider located

in another EU

country

No Donrsquot know

Gender

Age groups

Education

Yes from a

retailer or service

provider located

outside the EU

Yes but do not

know where the

retailer or service

is located

Urbanisation

Employment status

Consumer Survey 2018

21

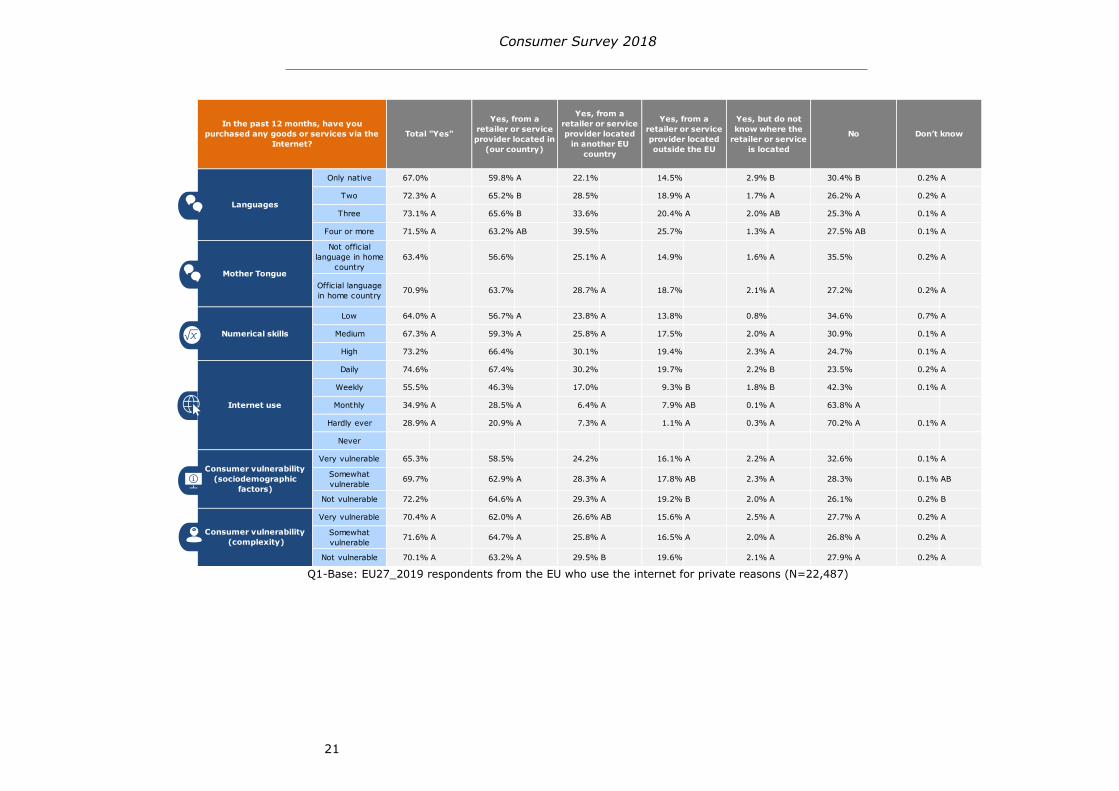

Q1-Base EU27_2019 respondents from the EU who use the internet for private reasons (N=22487)

Only native 670 598 A 221 145 29 B 304 B 02 A

Two 723 A 652 B 285 189 A 17 A 262 A 02 A

Three 731 A 656 B 336 204 A 20 AB 253 A 01 A

Four or more 715 A 632 AB 395 257 13 A 275 AB 01 A

Not official

language in home

country

634 566 251 A 149 16 A 355 02 A

Official language

in home country709 637 287 A 187 21 A 272 02 A

Low 640 A 567 A 238 A 138 08 346 07 A

Medium 673 A 593 A 258 A 175 20 A 309 01 A

High 732 664 301 194 23 A 247 01 A

Daily 746 674 302 197 22 B 235 02 A

Weekly 555 463 170 93 B 18 B 423 01 A

Monthly 349 A 285 A 64 A 79 AB 01 A 638 A

Hardly ever 289 A 209 A 73 A 11 A 03 A 702 A 01 A

Never

Very vulnerable 653 585 242 161 A 22 A 326 01 A

Somewhat

vulnerable697 629 A 283 A 178 AB 23 A 283 01 AB

Not vulnerable 722 646 A 293 A 192 B 20 A 261 02 B

Very vulnerable 704 A 620 A 266 AB 156 A 25 A 277 A 02 A

Somewhat

vulnerable716 A 647 A 258 A 165 A 20 A 268 A 02 A

Not vulnerable 701 A 632 A 295 B 196 21 A 279 A 02 A

In the past 12 months have you

purchased any goods or services via the

Internet

Total Yes

Yes from a

retailer or service

provider located in

(our country)

Yes but do not

know where the

retailer or service

is located

No Donrsquot know

Languages

Mother Tongue

Yes from a

retailer or service

provider located

in another EU

country

Numerical skills

Internet use

Consumer vulnerability

(sociodemographic

factors)

Consumer vulnerability

(complexity)

Yes from a

retailer or service

provider located

outside the EU

Consumer Survey 2018

22

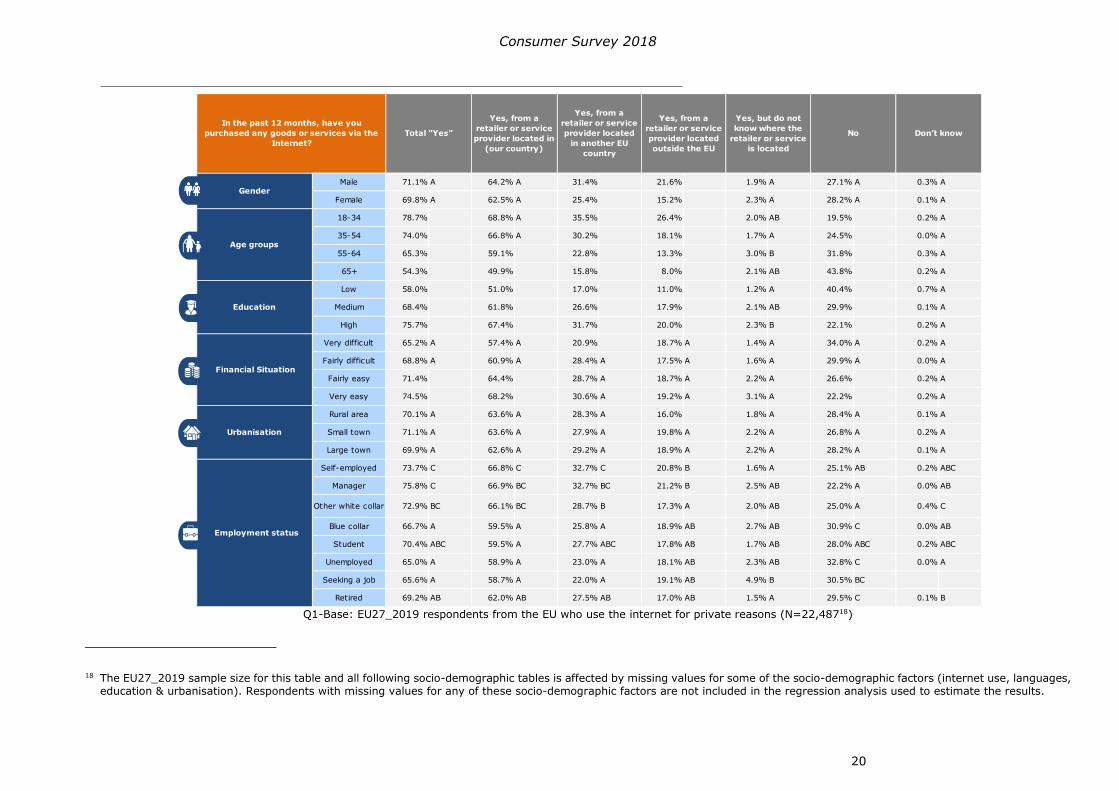

With regard to socio-demographic variables and other characteristics the results of the multivariate

analysis19 show that consumersrsquo internet use is the factor most closely associated20 with internet purchases in their own country followed by education age mother tongue and numerical skills

Regarding consumersrsquo frequency of internet use21 daily internet users are more likely to make domestic online purchases compared to those who use the internet weekly In addition weekly users also conduct more such purchases than monthly internet users and those who hardly ever use the internet

Highly educated consumers are more likely to purchase products and services online domestically than consumers with a medium level of education who in turn show higher values than consumers with a lower level of education

Regarding age domestic purchases are more common amongst consumers aged 18-54 years than amongst older consumers aged 55+

Consumers whose mother tongue is one of the official languages of the country or region they live in are also more likely to make such purchases than those whose mother tongue is not an official

language

Finally those with a high numerical skill level are more likely to make such purchases than those with a medium or low numerical skill level

Purchases of goods and services in another EU country via the internet is associated most closely with consumersrsquo age The characteristics showing the next closest links are education the number of languages spoken internet use and gender

Younger consumers (18-34 years) are more likely to engage in online cross-border shopping than all

other age groups In addition consumers aged 35-54 years are also more likely to make such purchases than those who are aged 55-64 years who in turn are also more likely to make such purchases than those aged 65+ years

Regarding consumersrsquo level of education highly educated consumers are most likely to make such purchases Furthermore those with a medium level of education are in turn more likely to make such purchases than those with a low level of education

Consumers that speak at least four languages are more likely to make such purchases than those

who speak fewer languages Those who speak three languages are also more likely to conduct cross-border online purchases than those who speak two languages who in turn are more likely to make such purchases than those who only speak their native language

Daily internet users are by far the most likely to purchase products or services online from retailers in another EU country In addition weekly internet users also show higher values than consumers who use the internet monthly and those who hardly ever use the internet

Finally males are more likely to make such purchases than females

When it comes to online purchases of goods and services from a retailer or service provider outside the EU consumersrsquo age is associated most closely with this indicator followed by gender education the number of languages spoken and frequency of internet use

As with cross-border purchases younger consumers (18-34 years) are most likely engage in online shopping in a country outside the EU In addition those who are aged 35-54 years are more likely

19 The values shown in the tables of the socio-demographic analyses are based on model estimates (see also chapter 124)

20 The sociodemographic characteristics having the closest link with the dependent variable are selected considering the average magnitude of the difference across the different levels of all the sociodemographic characters (eg the differences in the likelihood to purchase online- in absolute terms- across the different levels of internet use) and by looking at the overall coherence of this variability

21 Since Question 1 measured consumersrsquo online purchases the internet usage level lsquoNeverrsquo is excluded from the regression models

Consumer Survey 2018

23

to make such purchases than those who are aged 55-64 years who in turn are also more likely to

make such purchases than those aged 65+ years

As far as gender is concerned males are more likely to purchase goods or services online from traders outside of the EU than females

Highly educated consumers are more likely to make such purchases than the remainder of the population In addition those with a medium level of education are also more likely to make such purchases than those with a low level of education

Consumers that speak four languages or more are the most likely to make such purchases

Furthermore those who speak two or three languages also make more online purchases from retailers outside of the EU than consumers who only speak their native language

Finally daily internet users are noticeably more likely to conduct online purchases from countries outside the EU than less frequent internet users Weekly internet users also differ from those who use the internet hardly ever

When it comes to consumers making online purchases of goods and services from a retailer

or service provider whom they do not know the location of consumersrsquo numerical skills are most closely associated with this indicator followed by the frequency of internet use education employment status and age

Consumers with high or medium numerical skills22 are more likely to make online purchases from a retailer or service provider whom they do not know the location of than those with low numerical skills

Moreover daily or weekly internet users are also more likely to make online purchases from such

retailers than those who use the internet monthly or hardly ever

Regarding consumersrsquo level of education those who are highly educated are more likely to make such purchases than those with a low level of education

Job-seekers are the most likely to purchase products and services online without knowing the location of the retailers and more so than those who are retired or self-employed The latter two are the least

likely to conduct such purchases

Finally consumers that are 55-64 years old are more likely to purchase goods and services from

retailers whom they do not know the location of than consumers aged 35-54 years old

Offline cross-border purchases

When it comes to shopping cross-border from offline retailers or service providers the majority of respondents (852) has not performed such purchases in the past 12 months in the European Union Yet 145 of consumers in the EU27_2019 has purchased products or services offline in

another EU country during this timeframe

22 Respondentsrsquo numerical skills were measured with two short mathematical scenariosrsquo Suppose that the exact same product is on sale in shop A and shop B I will read you two statements about offers from shop A and shop B In each case please tell me which shop is cheaper 1 Shop A offers a TV set for 440 euro Shop B offers the exact same type of TV set at 500 euro but with a discount of 10 2 Shop A offers a TV set for 890 euro Shop B offers the exact same type of TV set at 940 euro but with a reduction of 60 euro 2 correct answers correspond to a high level of numerical skills 1 correct answer to a medium level and 0 correct answers to a low level

Consumer Survey 2018

24

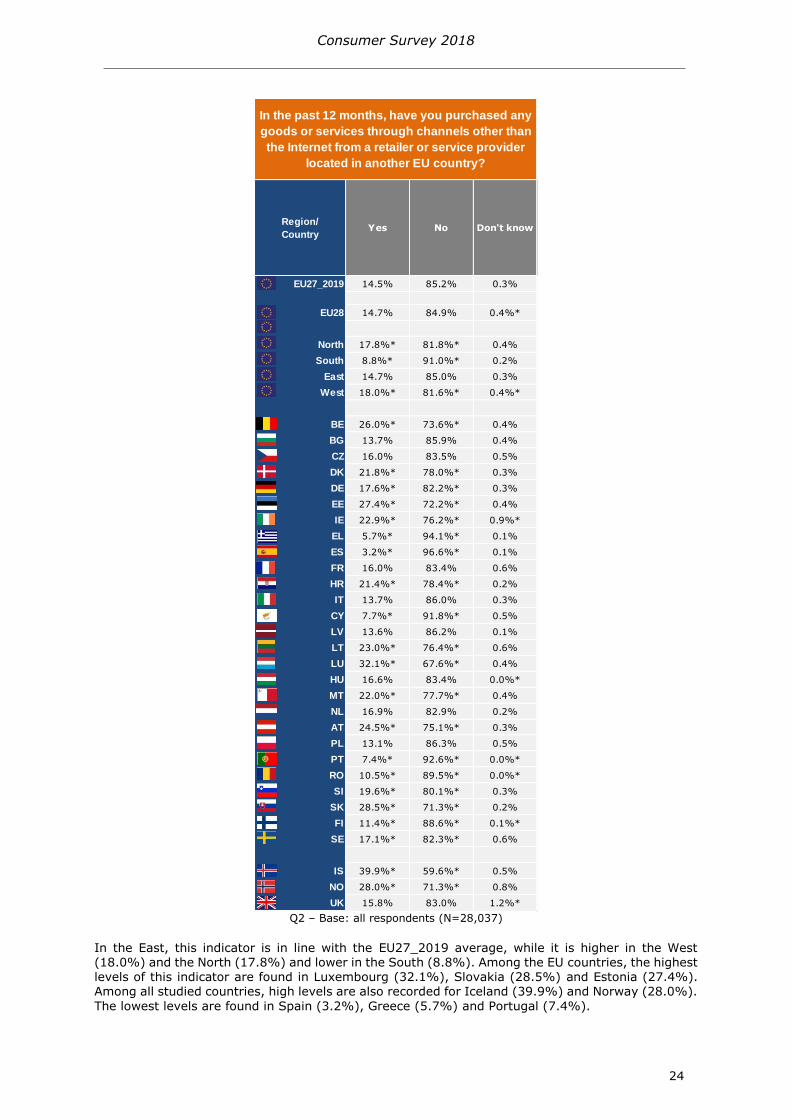

Q2 ndash Base all respondents (N=28037)

In the East this indicator is in line with the EU27_2019 average while it is higher in the West (180) and the North (178) and lower in the South (88) Among the EU countries the highest levels of this indicator are found in Luxembourg (321) Slovakia (285) and Estonia (274) Among all studied countries high levels are also recorded for Iceland (399) and Norway (280)

The lowest levels are found in Spain (32) Greece (57) and Portugal (74)

Region

CountryYes No Dont know

EU27_2019 145 852 03

EU28 147 849 04

North 178 818 04

South 88 910 02

East 147 850 03

West 180 816 04

BE 260 736 04

BG 137 859 04

CZ 160 835 05

DK 218 780 03

DE 176 822 03

EE 274 722 04

IE 229 762 09

EL 57 941 01

ES 32 966 01

FR 160 834 06

HR 214 784 02

IT 137 860 03

CY 77 918 05

LV 136 862 01

LT 230 764 06

LU 321 676 04

HU 166 834 00

MT 220 777 04

NL 169 829 02

AT 245 751 03

PL 131 863 05

PT 74 926 00

RO 105 895 00

SI 196 801 03

SK 285 713 02

FI 114 886 01

SE 171 823 06

IS 399 596 05

NO 280 713 08

UK 158 830 12

In the past 12 months have you purchased any

goods or services through channels other than

the Internet from a retailer or service provider

located in another EU country

Consumer Survey 2018

25

Q2 ndash Base all EU27_2019 respondents (N=2492823)

23 See footnote 18

Male 149 A 847 A 04

Female 143 A 855 A 02

18-34 168 B 826 A 06 B

35-54 155 B 842 A 03 B

55-64 114 A 884 B 02 AB

65+ 118 A 882 B 01 A

Low 100 898 01 A

Medium 139 858 03 A

High 159 838 04 A

Very difficult 160 AB 839 AB 01

Fairly difficult 136 A 860 B 04 A

Fairly easy 141 A 857 B 03 A

Very easy 168 B 828 A 04 B

Rural area 142 A 855 A 02 A

Small town 143 A 853 A 04 A

Large town 153 A 845 A 03 A

Self-employed 160 DE 836 AB 05 A

Manager 182 E 814 A 04 A

Other white collar 149 CD 848 BC 03 A

Blue collar 132 BC 867 CD 02 A

Student 162 CDE 838 ABC 02 A

Unemployed 99 A 894 D 10 A

Seeking a job 108 AB 887 D 05 A

Retired 134 ABCD 862 BCD 06 A

Age groups

In the past 12 months have you

purchased any goods or services through

channels other than the Internet from a

retailer or service provider located in

another EU country

Yes No Dont know

Gender

Education

Financial Situation

Urbanisation

Employment status

Consumer Survey 2018

26

Q2 ndash Base all EU27_2019 respondents (N=24928)

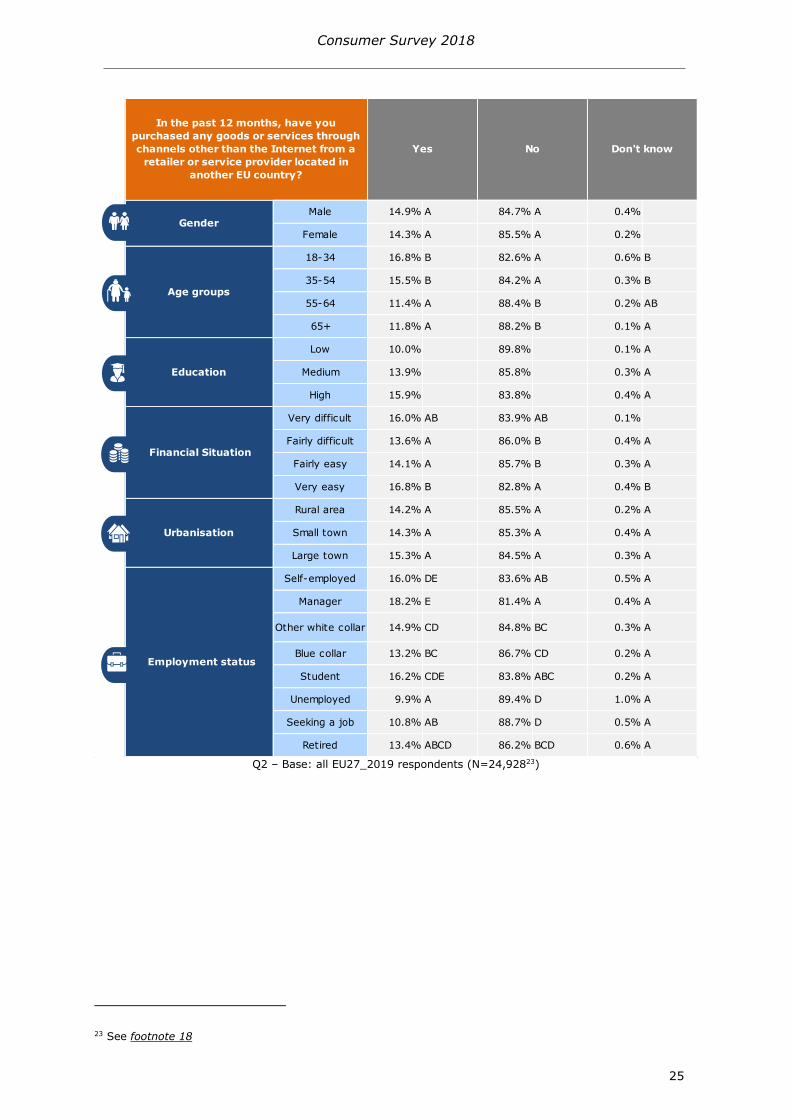

Regarding socio-demographic variables and other characteristics consumersrsquo language skills is the factor most closely associated with cross-border shopping in another EU country through channels other than the internet The characteristics showing the next closest links are education frequency of internet use age and employment status

Consumers speak at least four languages are more likely to make such purchases than those who speak three languages who in turn are more likely to make such purchases than those who speak two languages The latter group is also more likely to make such purchases than those who speak only their native language

Regarding consumersrsquo level of education highly educated consumers are more likely to purchase products and services offline in another EU country than those with a medium or low level of education Those with a medium level of education are also more likely to purchase products or

services offline in another EU country than consumers with a low level of education

Daily internet users are most likely to purchase products and services offline in another EU country compared to those who use the internet less frequently In contrast people that never use the internet show lower values for such purchases than daily or weekly internet users

As far as age is concerned consumers aged 18-54 years are more likely to engage cross-border shopping through channels other than the internet than older consumers aged 55 years or older

Only native 101 897 02 AB

Two 138 858 04 B

Three 201 796 04 AB

Four or more 240 759 01 A

Not official

language in home

country

138 A 851 A 12 A

Official language

in home country147 A 851 A 03 A

Low 119 A 878 A 03 A

Medium 134 A 863 A 03 A

High 154 842 04 A

Daily 156 840 04

Weekly 124 B 876 A 00 A

Monthly 92 AB 907 AB

Hardly ever 84 AB 916 AB

Never 54 A 945 B 01 A

Very vulnerable 141 A 857 A 03 A

Somewhat

vulnerable142 A 855 A 04 A

Not vulnerable 149 A 848 A 03 A

Very vulnerable 152 A 844 A 05 A

Somewhat

vulnerable150 A 847 A 03 A

Not vulnerable 144 A 853 A 03 A

In the past 12 months have you

purchased any goods or services through

channels other than the Internet from a

retailer or service provider located in

another EU country

Consumer vulnerability

(socio-demographic

factors)

Consumer vulnerability

(complexity)

No Dont know

Languages

Mother Tongue

Numerical skills

Internet use

Yes

Consumer Survey 2018

27

Finally regarding employment status managers are most likely to make offline cross-border

purchases and more so than any other consumer group except for self-employed consumers and students In contrast those who are unemployed are the least likely to engage in such purchases and are less likely to do so than managers students people who are self-employed other white collars and blue-collar workers

Consumer Survey 2018

28

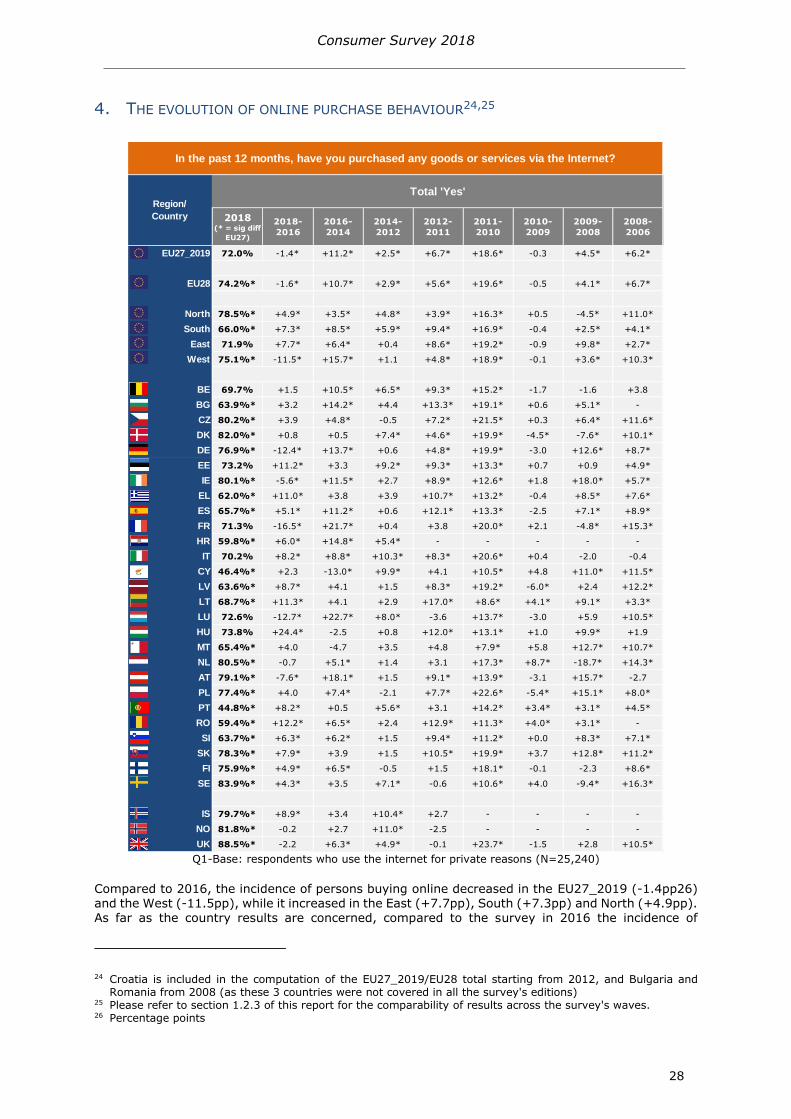

4 THE EVOLUTION OF ONLINE PURCHASE BEHAVIOUR2425

Q1-Base respondents who use the internet for private reasons (N=25240)

Compared to 2016 the incidence of persons buying online decreased in the EU27_2019 (-14pp26) and the West (-115pp) while it increased in the East (+77pp) South (+73pp) and North (+49pp) As far as the country results are concerned compared to the survey in 2016 the incidence of

24 Croatia is included in the computation of the EU27_2019EU28 total starting from 2012 and Bulgaria and Romania from 2008 (as these 3 countries were not covered in all the surveys editions)

25 Please refer to section 123 of this report for the comparability of results across the surveys waves 26 Percentage points

2018 ( = sig diff

EU27)

2018-

2016

2016-

2014

2014-

2012

2012-

2011

2011-

2010

2010-

2009

2009-

2008

2008-

2006

EU27_2019 720 -14 +112 +25 +67 +186 -03 +45 +62

EU28 742 -16 +107 +29 +56 +196 -05 +41 +67

North 785 +49 +35 +48 +39 +163 +05 -45 +110

South 660 +73 +85 +59 +94 +169 -04 +25 +41

East 719 +77 +64 +04 +86 +192 -09 +98 +27

West 751 -115 +157 +11 +48 +189 -01 +36 +103

BE 697 +15 +105 +65 +93 +152 -17 -16 +38

BG 639 +32 +142 +44 +133 +191 +06 +51 -

CZ 802 +39 +48 -05 +72 +215 +03 +64 +116

DK 820 +08 +05 +74 +46 +199 -45 -76 +101

DE 769 -124 +137 +06 +48 +199 -30 +126 +87

EE 732 +112 +33 +92 +93 +133 +07 +09 +49

IE 801 -56 +115 +27 +89 +126 +18 +180 +57

EL 620 +110 +38 +39 +107 +132 -04 +85 +76

ES 657 +51 +112 +06 +121 +133 -25 +71 +89

FR 713 -165 +217 +04 +38 +200 +21 -48 +153

HR 598 +60 +148 +54 - - - - -

IT 702 +82 +88 +103 +83 +206 +04 -20 -04

CY 464 +23 -130 +99 +41 +105 +48 +110 +115

LV 636 +87 +41 +15 +83 +192 -60 +24 +122

LT 687 +113 +41 +29 +170 +86 +41 +91 +33

LU 726 -127 +227 +80 -36 +137 -30 +59 +105

HU 738 +244 -25 +08 +120 +131 +10 +99 +19

MT 654 +40 -47 +35 +48 +79 +58 +127 +107

NL 805 -07 +51 +14 +31 +173 +87 -187 +143

AT 791 -76 +181 +15 +91 +139 -31 +157 -27

PL 774 +40 +74 -21 +77 +226 -54 +151 +80

PT 448 +82 +05 +56 +31 +142 +34 +31 +45

RO 594 +122 +65 +24 +129 +113 +40 +31 -

SI 637 +63 +62 +15 +94 +112 +00 +83 +71

SK 783 +79 +39 +15 +105 +199 +37 +128 +112

FI 759 +49 +65 -05 +15 +181 -01 -23 +86

SE 839 +43 +35 +71 -06 +106 +40 -94 +163

IS 797 +89 +34 +104 +27 - - - -

NO 818 -02 +27 +110 -25 - - - -

UK 885 -22 +63 +49 -01 +237 -15 +28 +105

In the past 12 months have you purchased any goods or services via the Internet

Region

Country

Total Yes

Consumer Survey 2018

29

consumers shopping online increased most steeply in Hungary (+244pp) and decreased most

sharply in France (-165pp) When looking at statistically significant changes in 2018 (vs 2016) and in 2016 (vs 2014) no positive reversal is found The largest negative reversal27 is found in France where between 2016 and 2018 this indicator decreased by 165pp whereas between 2014 and 2016 it increased by 217pp

Q1-Base respondents who use the internet for private reasons (N=25240)

27 Reversals are reported when both changes are statistically significant and when the direction of the change has reversed ie from an increase to a decrease or from a decrease to an increase Only the strongest positive and the strongest negative reversal are reported which are determined by the highest absolute sum of both changes

2018 ( = sig diff

EU27)

2018-

2016

2016-

2014

2014-

2012

2012-

2011

2011-

2010

2010-

2009

2009-

2008

2008-

2006

EU27_2019 630 -18 +103 +26 +46 +170 -02 +37 +66

EU28 659 -12 +92 +31 +36 +183 -02 +34 +71

North 694 +35 +47 +57 +03 +186 +07 -86 +107

South 536 +70 +62 +51 +74 +130 -06 +42 +32

East 673 +71 +69 +09 +68 +183 -06 +94 +30

West 665 -116 +148 +14 +27 +180 +01 +15 +114

BE 487 -29 +89 +67 +48 +116 +11 -50 +56

BG 579 +43 +154 +83 +92 +146 +07 +48 -

CZ 781 +42 +62 -26 +69 +242 +11 +32 +125

DK 725 -11 +25 +80 +24 +295 -27 -213 +105

DE 719 -96 +116 -01 +42 +185 -28 +109 +97

EE 595 +117 +35 +86 +47 +105 -12 -04 +53

IE 636 -93 +230 +65 +116 +62 +46 +18 +07

EL 548 +117 +53 +112 +29 +117 -05 +63 +41

ES 536 +76 +56 +14 +95 +100 -25 +98 +52

FR 609 -179 +186 +32 -16 +215 +13 -57 +157

HR 411 +75 +63 +62 - - - - -

IT 575 +64 +81 +65 +77 +164 +01 +02 +14

CY 169 -52 +52 +114 -22 -29 +52 +14 +41

LV 481 +63 +33 +37 +09 +173 -66 -07 +124

LT 580 +85 +53 +40 +125 +78 +52 +54 +25

LU 333 -339 +467 +47 +15 +18 -06 +17 +48

HU 676 +210 -07 +24 +99 +111 +29 +85 +30

MT 162 -32 +56 -08 +71 -04 +07 +34 -11

NL 757 -15 +53 -02 +40 +190 +90 -192 +165

AT 619 -164 +357 -34 +96 +52 +14 +60 +36

PL 740 +30 +87 -23 +69 +216 -57 +152 +90

PT 286 +35 -15 +74 +16 +79 +33 +14 +38

RO 571 +115 +66 +39 +109 +111 +40 +43 -

SI 506 +66 +57 +02 +63 +91 +11 +45 +77

SK 712 +96 +24 +18 +88 +181 +46 +107 +95

FI 679 +69 +66 +15 -29 +183 +01 -40 +73

SE 767 +17 +51 +75 -35 +127 +34 -103 +161

IS 471 +54 -13 +140 -28 - - - -

NO 706 -19 +44 +177 -109 - - - -

UK 851 +28 +06 +54 -10 +241 -05 +24 +109

In the past 12 months have you purchased any goods or services via the Internet

Region

Country

Yes from a retailer or service provider located in (our country)

Consumer Survey 2018

30

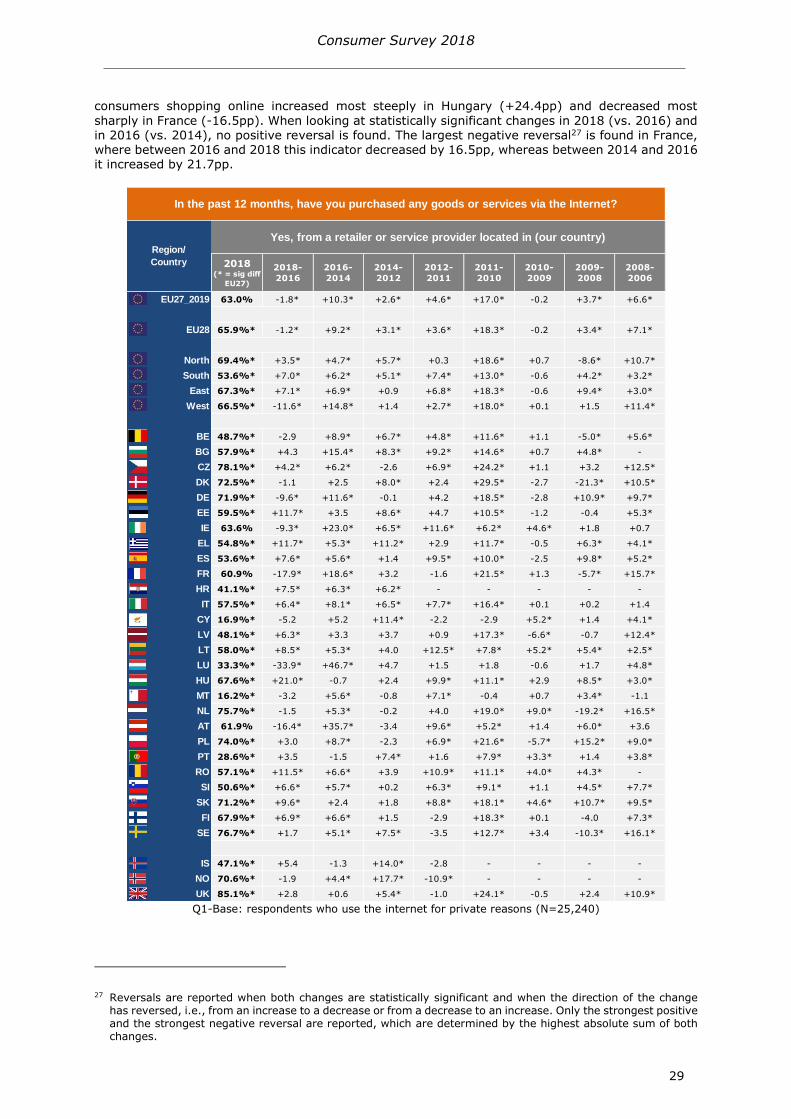

In terms of online shopping domestically the proportion of consumers having done so in the past 12

months decreased in the EU27_2019 (-18pp) and the Western region (-116pp) while the opposite pattern can be observed for the Eastern (+71pp) Southern (+70pp) and Northern regions (+35pp) Compared to the survey in 2016 the proportion of consumers who shop online domestically increased most steeply in Hungary (+210pp) The greatest decrease compared to 2016 is observed in Luxembourg (-339pp) In Luxembourg also the largest negative reversal is observed where the decrease between 2016 and 2018 was preceded by an increase of 467pp between 2014 and 2016 There are no statistically significant positive reversals

Q1-Base respondents who use the internet for private reasons (N=25240)

2018 ( = sig diff

EU27)

2018-

2016

2016-

2014

2014-

2012

2012-

2011

2011-

2010

2010-

2009

2009-

2008

2008-

2006

EU27_2019 283 +91 +03 +23 +47 +47 -05 +10 +13

EU28 288 +101 -07 +18 +50 +52 -03 +03 +17

North 343 +40 +32 +40 +49 +47 +04 -06 +26

South 276 +45 +53 +43 +43 +51 -03 +02 +19

East 191 +57 +29 +15 +21 +33 -08 +20 +02

West 322 +144 -46 +11 +65 +49 -06 +10 +18

BE 481 +37 +118 +23 +115 +79 -12 -04 +06

BG 195 +10 +29 +04 +58 +53 +05 +15 -

CZ 222 +68 +33 +39 +09 +33 -01 +13 +04

DK 365 +09 +26 -10 +75 +41 -28 +41 +42

DE 287 +143 -54 +37 +33 +57 -15 +16 +19

EE 331 +33 +31 +57 +80 +43 +24 -10 +27

IE 598 +357 -250 -25 +111 +62 +45 +139 +35

EL 213 +43 +13 -50 +97 +22 -12 +39 +38

ES 285 +69 +66 +06 +43 +44 -15 -07 +41

FR 302 +152 -44 -26 +112 +16 -06 +05 +20

HR 305 +36 +129 +73 - - - - -

IT 285 +27 +59 +87 +40 +56 +05 -03 -01

CY 332 -15 -95 +87 +53 +94 +07 +81 +91

LV 306 +53 +29 +65 +49 +58 -09 +27 +25

LT 277 +60 +60 +21 +54 +14 +20 +23 +17

LU 629 +278 -209 +111 -57 +139 -42 +41 +98

HU 231 +104 +25 +15 +51 +05 +03 +25 -04

MT 574 +67 -82 +48 +69 +44 +78 +90 +114

NL 240 +05 +61 -27 +29 +55 +44 -81 +11

AT 608 +369 -289 +104 +22 +99 -26 +139 +09

PL 173 +53 +10 +38 -03 +38 -16 +17 +09

PT 211 +58 +00 +33 +05 +73 +01 +27 +04

RO 100 +46 +13 -22 +29 +24 -06 +14 -

SI 309 +32 +98 +16 +57 +29 -11 +32 +17

SK 348 +105 +110 -85 +85 +43 -17 +77 +13

FI 382 +44 +39 -01 +48 +69 +11 +24 +14

SE 337 +50 +27 +94 +27 +32 +13 -59 +27

IS 541 +223 +35 +59 +54 - - - -

NO 402 +15 +26 +98 -11 - - - -

UK 321 +162 -73 -13 +78 +82 +09 -44 +50

In the past 12 months have you purchased any goods or services via the Internet

Region

Country

Yes from a retailer or service provider located in another EU country

Consumer Survey 2018

31

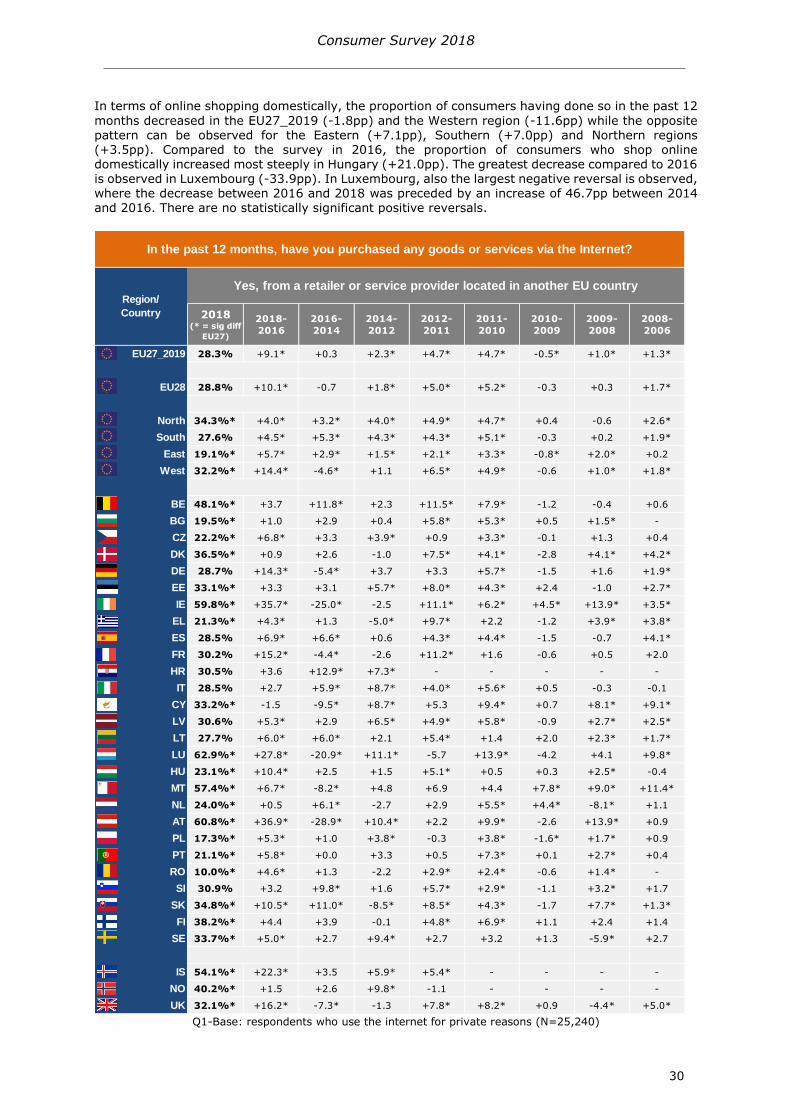

With regard to the share of consumers participating in cross-border online shopping in another EU

country it increased in the EU27_2019 (+91pp) and all the four regions (West +144pp East +57pp South +45pp and North +40pp) Compared to the survey in 2016 the share of consumers participating in cross-border online shopping in another EU country increased most steeply in Austria (+369pp) In Austria also the largest positive reversal is observed where the strong increase between 2016 and 2018 was preceded by a decrease by 289pp between 2014 and 2016 There are no statistically significant decreases or negative reversals

Q1-Base respondents who use the internet for private reasons (N=25240)

2018 ( = sig diff

EU27)

2018-

2016

2016-

2014

2014-

2012

2012-

2011

2011-

2010

2010-

2009

2009-

2008

2008-

2006

EU27_2019 184 +92 +04 +10 +22 +29 -03 +03 +07

EU28 200 +116 -25 +13 +24 +36 -03 +01 +08

North 245 +48 +60 +21 +33 +20 +12 -20 +27

South 177 +47 +36 +12 +31 +37 -05 +03 +09

East 147 +62 +28 +14 +09 +16 +00 +09 +01

West 198 +139 -36 +04 +23 +30 -06 +02 +09

BE 184 +67 +34 -02 +24 +36 +00 -13 +04

BG 118 +13 +37 +21 +02 +43 -05 +11 -

CZ 201 +65 +36 +40 +13 +26 +04 +07 +08

DK 239 +35 +63 +06 +45 -11 +06 -11 +31

DE 187 +138 -32 +16 +07 +29 -11 +21 +05

EE 300 +46 +115 +54 +35 +36 +18 -15 +13

IE 317 +278 -156 -18 +48 +09 +20 +47 +31

EL 144 +60 -39 +06 +39 +32 -18 +31 +20

ES 193 +23 +64 +07 +35 +46 -03 -01 +19

FR 211 +182 -72 -09 +46 +31 -04 -15 +17

HR 306 +26 +143 +27 - - - - -

IT 175 +65 +29 +18 +27 +30 -04 -01 +00

CY 189 +44 -30 -09 +10 +51 +06 +74 +10

LV 317 +106 +53 +49 +41 +48 +12 -04 +21

LT 256 +88 +73 +16 +19 +18 +12 +13 +07

LU 173 +127 -60 +22 +14 +19 +02 -06 +23

HU 199 +117 +15 +00 +13 +14 +05 +10 -09

MT 357 +15 -40 +76 +46 +81 +05 +57 +64

NL 212 +21 +80 +11 +10 +38 -00 -40 +23

AT 131 +93 -46 +10 +14 +17 -00 +04 -40

PL 123 +67 +05 +29 -05 +09 -03 +08 +03

PT 138 +42 +28 +07 +24 +38 -06 +07 +09

RO 74 +28 +29 -09 +06 +14 +04 +06 -

SI 228 +50 +84 +02 +48 +10 +03 +00 +16

SK 239 +119 +74 -42 +44 +24 -10 +19 +06

FI 234 +49 +32 -01 +49 +18 +45 -08 +15

SE 232 +33 +63 +36 +20 +26 -05 -45 +43

IS 435 +53 +32 +108 +07 - - - -

NO 319 +46 +45 +28 +50 - - - -

UK 306 +281 -220 +28 +44 +73 +04 -06 +19

In the past 12 months have you purchased any goods or services via the Internet

Region

Country

Yes from a retailer or service provider located outside the EU

Consumer Survey 2018

32

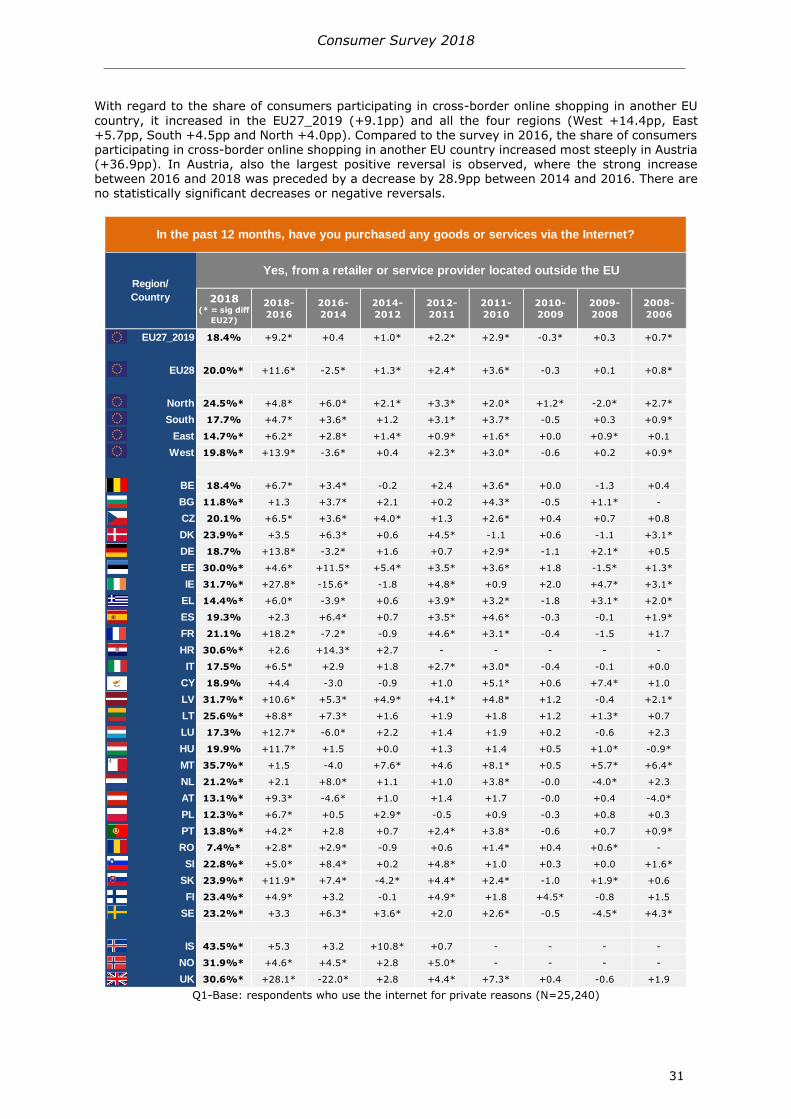

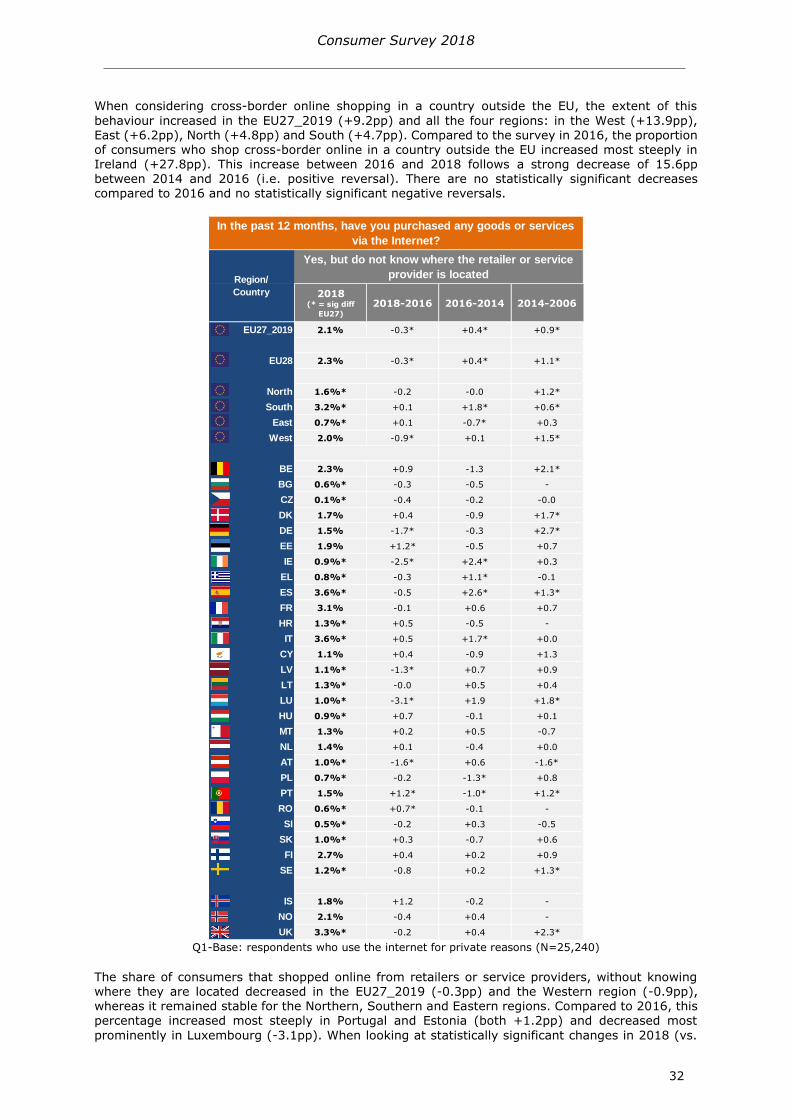

When considering cross-border online shopping in a country outside the EU the extent of this

behaviour increased in the EU27_2019 (+92pp) and all the four regions in the West (+139pp) East (+62pp) North (+48pp) and South (+47pp) Compared to the survey in 2016 the proportion of consumers who shop cross-border online in a country outside the EU increased most steeply in Ireland (+278pp) This increase between 2016 and 2018 follows a strong decrease of 156pp between 2014 and 2016 (ie positive reversal) There are no statistically significant decreases compared to 2016 and no statistically significant negative reversals

Q1-Base respondents who use the internet for private reasons (N=25240)

The share of consumers that shopped online from retailers or service providers without knowing where they are located decreased in the EU27_2019 (-03pp) and the Western region (-09pp) whereas it remained stable for the Northern Southern and Eastern regions Compared to 2016 this percentage increased most steeply in Portugal and Estonia (both +12pp) and decreased most

prominently in Luxembourg (-31pp) When looking at statistically significant changes in 2018 (vs

2018( = sig diff

EU27)

2018-2016 2016-2014 2014-2006

EU27_2019 21 -03 +04 +09

EU28 23 -03 +04 +11

North 16 -02 -00 +12

South 32 +01 +18 +06

East 07 +01 -07 +03

West 20 -09 +01 +15

BE 23 +09 -13 +21

BG 06 -03 -05 -

CZ 01 -04 -02 -00

DK 17 +04 -09 +17

DE 15 -17 -03 +27

EE 19 +12 -05 +07

IE 09 -25 +24 +03

EL 08 -03 +11 -01

ES 36 -05 +26 +13

FR 31 -01 +06 +07

HR 13 +05 -05 -

IT 36 +05 +17 +00

CY 11 +04 -09 +13

LV 11 -13 +07 +09

LT 13 -00 +05 +04

LU 10 -31 +19 +18

HU 09 +07 -01 +01

MT 13 +02 +05 -07

NL 14 +01 -04 +00

AT 10 -16 +06 -16

PL 07 -02 -13 +08

PT 15 +12 -10 +12

RO 06 +07 -01 -

SI 05 -02 +03 -05

SK 10 +03 -07 +06

FI 27 +04 +02 +09

SE 12 -08 +02 +13

IS 18 +12 -02 -

NO 21 -04 +04 -

UK 33 -02 +04 +23

In the past 12 months have you purchased any goods or services

via the Internet

Region

Country

Yes but do not know where the retailer or service

provider is located

Consumer Survey 2018

33

2016) and in 2016 (vs 2014) the largest positive reversal is found in Portugal where between 2016

and 2018 this indicator increased by 12pp whereas between 2014 and 2016 it decreased by 10pp The largest negative reversal is found in Ireland where between 2016 and 2018 this indicator decreased by 25pp whereas between 2014 and 2016 it increased by 24pp

Q2 ndash Base all respondents (N=28037)

2018

( = sig

diff EU27)

2018-

2016

2016-

2014

2018

( = sig

diff EU27)

2018-

2016

2016-

2014

2018

( = sig

diff EU27)

2018-

2016

2016-

2014

EU27_2019 145 -02 +34 852 +03 -34 03 -01 -00

EU28 147 -10 +45 849 +10 -45 04 +00 -00

North 178 +23 +21 818 -23 -20 04 -00 -01

South 88 +11 -11 910 -11 +11 02 -01 -01

East 147 +35 -01 850 -34 +04 03 -01 -03

West 180 -35 +87 816 +36 -88 04 -01 +01

BE 260 -03 +104 736 +04 -107 04 -01 +03

BG 137 -06 +36 859 +04 -35 04 +02 -00

CZ 160 +06 +02 835 -09 +01 05 +03 -03

DK 218 +43 +35 780 -42 -28 03 -01 -07

DE 176 -32 +104 822 +35 -104 03 -03 -00

EE 274 -44 +119 722 +41 -116 04 +03 -03

IE 229 -20 +76 762 +18 -78 09 +01 +03

EL 57 -29 +36 941 +32 -40 01 -03 +04

ES 32 +10 -20 966 -07 +16 01 -03 +04

FR 160 -54 +94 834 +52 -97 06 +02 +03

HR 214 +06 +69 784 -04 -70 02 -02 +02

IT 137 +21 -14 860 -22 +18 03 +01 -04

CY 77 -13 -78 918 +11 +93 05 +02 -15

LV 136 +00 +30 862 +01 -32 01 -01 +01

LT 230 +62 +23 764 -69 -19 06 +07 -04

LU 321 +11 -67 676 -09 +64 04 -02 +02

HU 166 +94 +14 834 -91 -14 00 -03 +00

MT 220 +03 +79 777 +00 -86 04 -03 +07

NL 169 -29 -49 829 +29 +47 02 -00 +01

AT 245 +11 +115 751 -06 -119 03 -05 +04

PL 131 +25 -10 863 -24 +16 05 -01 -07

PT 74 +07 +05 926 -06 -00 00 -01 -05

RO 105 +50 -23 895 -49 +23 00 -01 -00

SI 196 +03 +57 801 -05 -57 03 +03 00

SK 285 +91 -22 713 -86 +23 02 -05 -00

FI 114 +09 -37 886 -08 +39 01 -01 -02

SE 171 +21 +30 823 -19 -33 06 -02 +04

IS 399 +64 +97 596 -67 -101 05 +03 +03

NO 280 +02 +26 713 +09 -36 08 -11 +10

UK 158 -64 +118 830 +58 -117 12 +06 -01

In the past 12 months have you purchased any goods or services through channels other than the

Internet from a retailer or service provider located in another EU country

Region

Country

Yes No Dont know

Consumer Survey 2018

34

The incidence of consumers shopping cross-border online in another EU country through channels

other than the internet is 145 in the EU27_2019 In the East this indicator is in line with the EU27_2019 average while it is higher in the West (180) and North (178) and lower in the South (88) Among the EU countries the highest levels of this indicator are found in Luxembourg (321) Slovakia (285) and Estonia (274) In addition high levels are also recorded for Norway (280) and Iceland (399) The lowest levels are found in Spain (32) Greece (57) and Portugal (74)

The share of consumers engaging in cross-border shopping in another EU country through channels

other than the internet remained stable in the EU27_2019 while it decreased in the Western region (-35pp) and increased in the other regions (South +11pp North +23pp and East +35pp) compared to 2016 This percentage increased most steeply in Hungary (+94pp) and decreased most prominently in France (-54pp) The strongest positive reversal is found in Romania where between 2016 and 2018 this indicator increased by 50pp whereas between 2014 and 2016 it decreased by 23pp In contrast the highest negative reversal in the EU is found in Estonia where between 2016

and 2018 this proportion of consumers decreased by 44pp whereas between 2014 and 2016 it increased by 119pp Considering all countries of the survey an even stronger negative reversal is observed in the UK (-64pp between 2016 and 2018 +118pp between 2014 and 2016)

Consumer Survey 2018

35

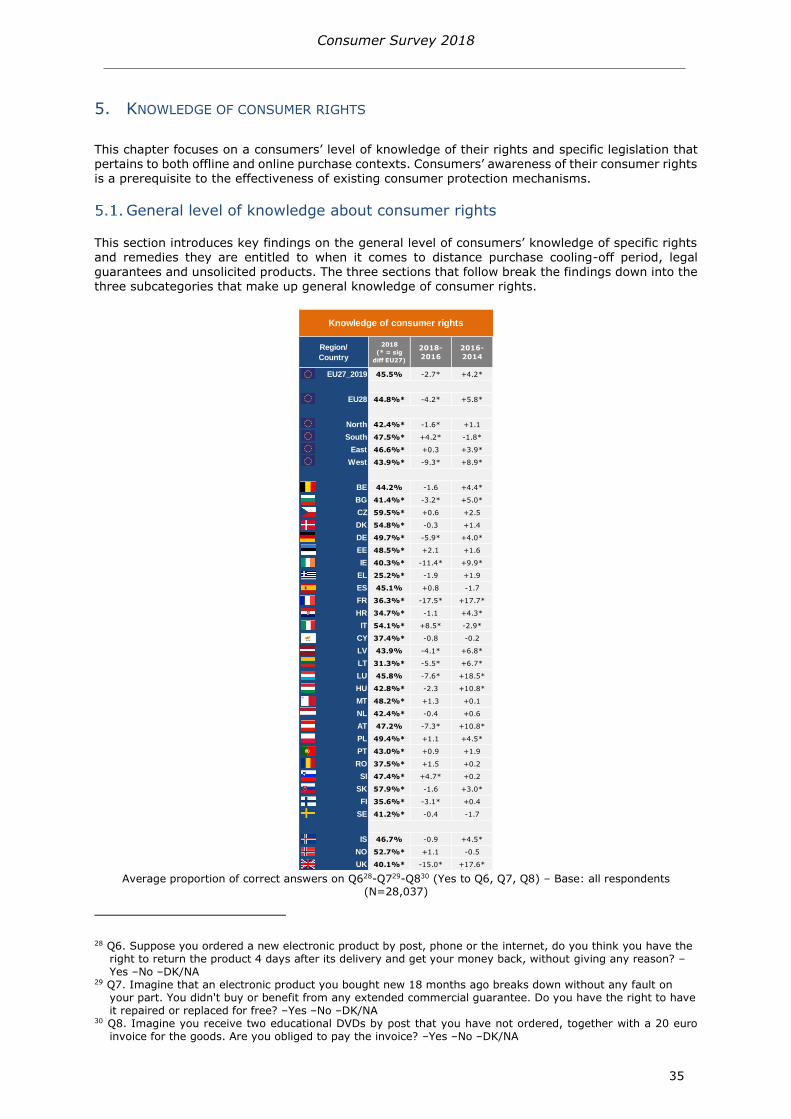

5 KNOWLEDGE OF CONSUMER RIGHTS

This chapter focuses on a consumersrsquo level of knowledge of their rights and specific legislation that pertains to both offline and online purchase contexts Consumersrsquo awareness of their consumer rights is a prerequisite to the effectiveness of existing consumer protection mechanisms

General level of knowledge about consumer rights

This section introduces key findings on the general level of consumersrsquo knowledge of specific rights and remedies they are entitled to when it comes to distance purchase cooling-off period legal guarantees and unsolicited products The three sections that follow break the findings down into the three subcategories that make up general knowledge of consumer rights

Average proportion of correct answers on Q628-Q729-Q830 (Yes to Q6 Q7 Q8) ndash Base all respondents

(N=28037)

28 Q6 Suppose you ordered a new electronic product by post phone or the internet do you think you have the right to return the product 4 days after its delivery and get your money back without giving any reason ndashYes ndashNo ndashDKNA

29 Q7 Imagine that an electronic product you bought new 18 months ago breaks down without any fault on your part You didnt buy or benefit from any extended commercial guarantee Do you have the right to have it repaired or replaced for free ndashYes ndashNo ndashDKNA

30 Q8 Imagine you receive two educational DVDs by post that you have not ordered together with a 20 euro invoice for the goods Are you obliged to pay the invoice ndashYes ndashNo ndashDKNA

Region

Country

2018

( = sig

diff EU27)

2018-

2016

2016-

2014

EU27_2019 455 -27 +42

EU28 448 -42 +58

North 424 -16 +11

South 475 +42 -18

East 466 +03 +39

West 439 -93 +89

BE 442 -16 +44

BG 414 -32 +50

CZ 595 +06 +25

DK 548 -03 +14

DE 497 -59 +40

EE 485 +21 +16

IE 403 -114 +99

EL 252 -19 +19

ES 451 +08 -17

FR 363 -175 +177

HR 347 -11 +43

IT 541 +85 -29

CY 374 -08 -02

LV 439 -41 +68

LT 313 -55 +67

LU 458 -76 +185

HU 428 -23 +108

MT 482 +13 +01

NL 424 -04 +06

AT 472 -73 +108

PL 494 +11 +45

PT 430 +09 +19

RO 375 +15 +02

SI 474 +47 +02

SK 579 -16 +30

FI 356 -31 +04

SE 412 -04 -17