consolidated financial statements report

TRANSCRIPT

CONSOLIDATEDFINANCIAL

STATEMENTSREPORT

Years endedDecember 31, 2007 and 2006

Dear Shareholders:

As Chairman of the Board and ChiefExecutive Officer of Lassonde IndustriesInc., I am pleased to announce that ourCompany has maintained, throughout thelast fiscal year, a sustained growth ratewhile abiding by the key principles guidingLassonde Industries Inc.’s development:sound management inspired by a vision oflong-term value creation.

If I were to sum up fiscal 2007 in a fewwords, I would say that we were able toachieve the business objectives that wehad established for ourselves for the year.

We made gains in most of our geographicmarkets and special efforts devoted tomarkets outside of Quebec were truly successful. In addition, we completed twoacquisitions toward the end of the year,allowing us to expand our product linesand for one of them, create new businessopportunities in western Canada andstrengthen our national position in the fruitjuices and drinks industry.

Net sales during the fourth quarterincreased 22.8% compared to last year’s

fourth quarter and reached $112.7 million.That drove net sales for 2007 to $401.0million, an increase of 13.5% compared tonet sales recorded during 2006.

Fourth quarter net earnings reached $9.3million and totalled $23.3 million for the2007 fiscal year. These results represent anincrease of $5.4 million over the samequarter of the previous fiscal year and of$9.6 million over the 2006 fiscal year.

The growth in profitability during the fourthquarter can be explained, in part, by theincrease in our net sales. The announcedreductions of the federal corporate incometax rates added $1.2 million to the fourthquarter results of 2007.

The increase in net earnings for fiscal year2007 can also be attributed, in part, to theimpact of higher net sales, on the operatingincome. The Company also benefited fromeconomies of scale linked to higher levelsof activities, thereby improving its operatingincome. In addition, It should be pointedout that significant unusual income taxcharges in 2006 and the recording of fiscal

02

Message to Shareholders

LASSONDE INDUSTRIES INC.

These two acquisitions open up a largearray of interesting business opportunitiesin addition to securing the commitment andknow-how of roughly a hundred newemployees to whom I wish a heartfelt welcome to the growing Lassonde family.

During fiscal 2007, we renewed our share redemption program and therebyproceeded to repurchase for cancellation54,160 Class A subordinate voting sharesfor a cash consideration of $2.0 million.These redemptions were done in accordancewith the rules and policies on normalcourse issuer bids of the Toronto StockExchange. The Company has renewed itsshare redemption program in 2008.

The Board of Directors declared a quarterlydividend of $0.125 per share, payable onMarch 17, 2008, to all registered holders of Class A and Class B shares as atFebruary 29, 2008. This is an eligible dividend.

The employees and management team of Lassonde Industries Inc. will continue tobuild on the quality of our products, thereputation of our brands such as Oasis,Fairlee and Canton, and our ability to innovate in order to reach our growth, profitability and value creation objectives for the shareholders.

benefits in 2007 and 2006 relating todecreases in statutory income tax ratesplayed a role when comparing the resultsof both fiscal years. These taxation factors,explained in detail in our ManagementReport, had the effect of creating a$4.1 million favourable variance when 2007net earnings are compared to the previousfiscal year.

As I mentioned earlier, I am also very proud to highlight the fact that LassondeIndustries Inc. continued to pursue its targeted expansion program by proceedingwith two acquisitions during 2007. Indeed,our A. Lassonde Inc. subsidiary purchasedthe ready-to-drink fruit juices and drinksdivision of McCain Foods (Canada) inNovember 2007. This transactionconsolidates the Company’s position inwestern Canada and confirms the status ofA. Lassonde Inc. as a truly nationalprovider of fruit juices and drinks. Also inNovember of 2007, Lassonde SpecialtiesInc. acquired substantially all of the assetsof Mondiv Food Products Inc. This acquisition enables the subsidiary to diversify its current product line and packaging offering, enhance its productdevelopment capability and extend its market to North America as a whole.

Message to Shareholders (continued)

LASSONDE INDUSTRIES INC.

03

Message to Shareholders (continued)

LASSONDE INDUSTRIES INC.

04

Despite signs of an economic slowdownand the pervasive volatility in the cost ofraw materials, the Company’s sound cost-control practices and ability to adapt to arapidly changing competitive landscapesupport its optimistic outlook, with respectto its ability to grow its net sales in themajority of its geographic markets in 2008.The integration of the recent acquisitionswill represent one of the Company’s priorities for the new fiscal year.

Finally, it is important to note that theseresults would not have been possible without the constant support and contribution of every member of our team.For each of them, excellence is a dailyobjective.

The other members of management joinme in thanking all of our associates andreaffirming our pride in working together.

Pierre-Paul LassondeChairman of the Board and Chief Executive Officer

755 Principale Street, Rougemont, Quebec J0L 1M0

Rougemont, Canada Pierre-Paul Lassonde Guy BlanchetteMarch 10, 2008 Chairman of the Board Vice-President, Finance

and Chief Executive Officer

Management’s responsibilityfor financial reporting

LASSONDE INDUSTRIES INC.

05

The preparation and presentation of the consolidated financial statements of Lassonde Industries Inc. and theother financial information contained in the MD&A for years ended December 31, 2007 and 2006 are theresponsibility of management.

This responsibility is based on a judicious choice of appropriate accounting principles and methods, the applicationof which requires making estimates and informed and careful judgments. It also includes ensuring that the financialinformation in the MD&A is consistent with the consolidated financial statements. The consolidated financialstatements were prepared in accordance with Canadian generally accepted accounting principles and wereexamined and approved by the Board of Directors.

The Company maintains disclosure controls and procedures which, in the opinion of management, providereasonable assurance regarding the disclosure of important information relating to the Company, as well as to itssubsidiaries, and the safeguarding of assets, and the well-ordered, efficient management of the Company’saffairs. Management recognizes its responsibility for conducting the Company’s affairs to comply with therequirements of applicable laws and established financial standards and principles.

The Board of Directors fulfills its duty, to oversee management in the performance of its financial reportingresponsibilities and to review the consolidated financial statements and MD&A, principally through itsAudit Committee. The Committee is comprised solely of directors who are independent of the Company and isalso responsible for making recommendations for the nomination of external auditors. Also, it holds periodicmeetings with members of management as well as external auditors, to discuss internal controls, auditingmatters and financial reporting issues. The external auditors have access to the Committee without management.The Audit Committee has reviewed the consolidated financial statements of Lassonde Industries Inc. and theannual management’s discussion and analysis and recommended their approval to the Board of Directors.

The enclosed consolidated financial statements were audited by Samson Bélair/Deloitte & Touche s.e.n.c.r.l.,Chartered Accountants, and their report indicates the extent of their audit and their opinion on the consolidatedfinancial statements.

Auditors’ report

LASSONDE INDUSTRIES INC.

Montreal, Canada Samson Bélair /Deloitte & Touche s.e.n.c.r.l.

March 10, 2008 Chartered Accountants

06Member of Deloitte Touche Tohmatsu

To the Shareholders ofLassonde Industries Inc.

We have audited the consolidated balance sheets of Lassonde Industries Inc. as at December 31, 2007and 2006 and the consolidated statements of earnings, comprehensive income, retained earnings andcash flows for the years then ended. These financial statements are the responsibility of the Company’smanagement. Our responsibility is to express an opinion on these financial statements based onour audits.

We conducted our audits in accordance with Canadian generally accepted auditing standards. Thosestandards require that we plan and perform an audit to obtain reasonable assurance whether thefinancial statements are free of material misstatement. An audit includes examining, on a test basis,evidence supporting the amounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimates made by management, as well asevaluating the overall financial statement presentation.

In our opinion, these consolidated financial statements present fairly, in all material respects, the financialposition of the Company as at December 31, 2007 and 2006 and the results of its operations and its cashflows for the years then ended in accordance with Canadian generally accepted accounting principles.

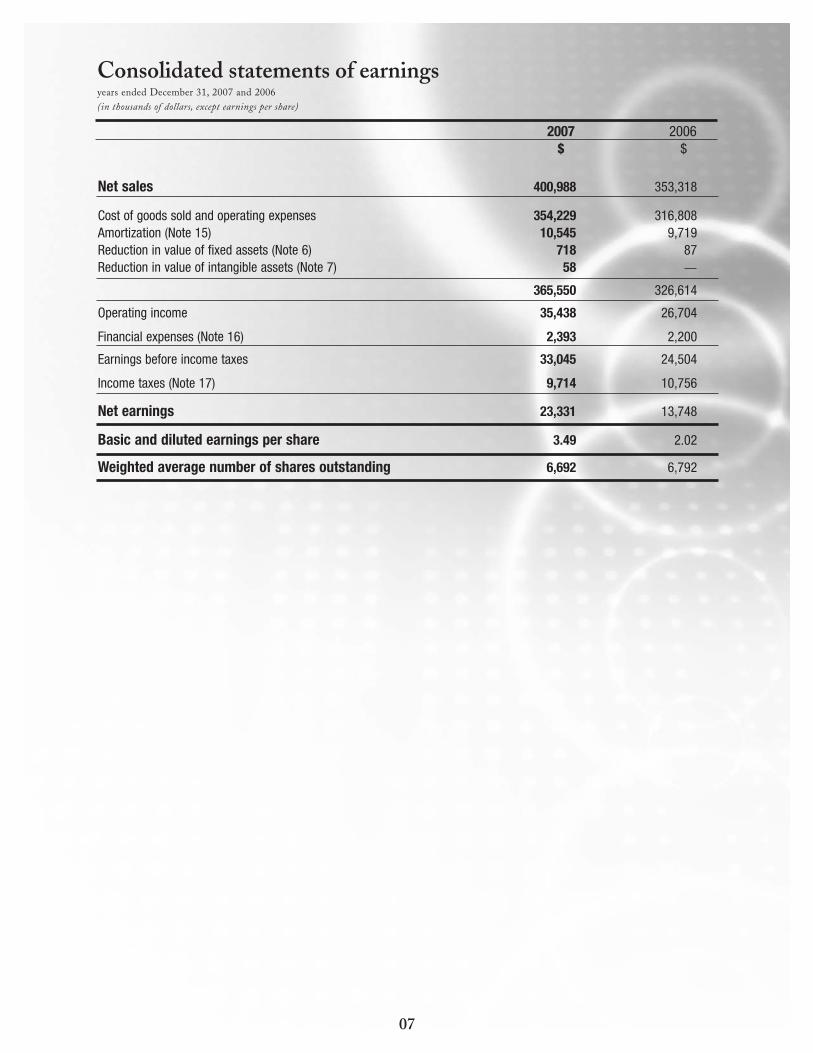

Consolidated statements of earnings

07

Net sales 400,988 353,318

Cost of goods sold and operating expenses 354,229 316,808Amortization (Note 15) 10,545 9,719Reduction in value of fixed assets (Note 6) 718 87Reduction in value of intangible assets (Note 7) 58

365,550 326,614

Operating income 35,438 26,704

Financial expenses (Note 16) 2,393 2,200

Earnings before income taxes 33,045 24,504

Income taxes (Note 17) 9,714 10,756

Net earnings 23,331 13,748

Basic and diluted earnings per share 3.49 2.02

Weighted average number of shares outstanding 6,692 6,792

2007 2006$ $

years ended December 31, 2007 and 2006(in thousands of dollars, except earnings per share)

Net earnings 23,331

Other comprehensive loss:Gains and losses on derivatives designated

as cash flow hedges,net of income taxes of $1,378,000 (2,800)

Gains and losses on derivatives designated as cash flow hedges transferred to net income,net of income taxes of $1,141,000 2,320

(480)

Comprehensive income 22,851

year ended December 31, 2007(in thousands of dollars)

Consolidated statement of comprehensive income

Balance, beginning of yearAs previously reported 103,807 97,099Adjustment related to the adoption of

new accounting policies (Note 3) 52

Restated 103,859 97,099

Net earnings 23,331 13,748

127,190 110,847

Excess of redemption cost of Class Ashares over stated capital (Note 10) (1,790) (3,033)

Dividends (3,545) (4,007)

Balance, end of year 121,855 103,807

years ended December 31, 2007 and 2006(in thousands of dollars)

Consolidated statements of retained earnings

08

2007$

2007 2006$ $

as at December 31, 2007 and 2006(in thousands of dollars)

Consolidated balance sheets

AssetsCurrent assets

Short-term investments 1,979Accounts receivable 42,932 36,587Inventories (Note 5) 90,122 77,107Prepaid expenses 1,387 1,108Fixed assets for resale 1,000Future income taxes (Note 17) 244 172Derivative instruments 830

136,515 116,953

Fixed assets (Note 6) 122,658 91,972Goodwill 5,157 2,531Intangible assets and other assets (Note 7) 17,042 8,190Net accrued benefit asset (Note 13) 4,112 5,118

285,484 224,764

LiabilitiesCurrent liabilities

Bank overdraft 2,078 1,524Bank indebtedness (Note 8) 13,340 5,740Accounts payable and accrued liabilities 53,982 39,091Income taxes 6,818 6,735Future income taxes (Note 17) 79Derivative instruments 1,624Current portion of long-term debt (Note 9) 925 5,061

78,767 58,230

Long-term debt (Note 9) 52,388 28,878Future income taxes (Note 17) 12,401 13,082

143,556 100,190

Shareholders’ equityCapital stock (Note 10) 19,118 19,362Contributed surplus 1,397 1,405

Accumulated other comprehensive loss (Note 11) (442)Retained earnings 121,855 103,807

121,413 103,807

141,928 124,574285,484 224,764

Commitments and contingencies (Note 20)

Approved by the Board

Director Director

09

2007 2006$ $

10

Operating activities

Net earnings 23,331 13,748Adjustments

Amortization 10,545 9,719Amortization of deferred charges 4,576 2,862Future income taxes (995) (257)Change in net accrued benefit asset 1,006 (668)Loss (gain) on disposal of fixed assets 2 (3)Change in derivative instruments 629 (463)Reduction in value of an investment 23Reduction in value of fixed assets 718 87Reduction in value of intangible assets 58Non-cash interest expense 307

40,177 25,048Changes in non-cash operating working

capital items (Note 18) (1,737) (804)

38,440 24,244

Financing activities

Change in bank indebtedness 4,705 5,740Increase in long-term debt 22,956Repayment of long-term debt (2,585) (3,967)Dividends paid (3,545) (4,007)Redemption of Class A shares (Note 10) (2,042) (3,463)

19,489 (5,697)

Investing activities

Business acquisitions (Note 4) (35,140)Acquisition of fixed assets (19,941) (13,187)Acquisition of intangible assets and other assets (5,419) (3,979)Disposal of fixed assets 38 69

(60,462) (17,097)

(Decrease) increase in cash and cash equivalents (2,533) 1,450Cash and cash equivalents, beginning of year 455 (995)

Cash and cash equivalents, end of year (2,078) 455

Cash and cash equivalents are comprised of cash, short-term investments and bank overdraft.

Additional cash flow information (Note 18)

years ended December 31, 2007 and 2006(in thousands of dollars)

Consolidated statements of cash flows

2007 2006$ $

11

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

1. Description of businessThe Company is active in the processing, conditioning, packaging and marketing of food products such as pure fruit juices,fruit drinks and wine, and of specialty food products such as canning of corn-on-the-cob, fondue broths, bruschetta topping and tapenades.

2. Accounting policiesThe consolidated financial statements have been prepared in accordance with Canadian generally accepted accounting principles and include the following significant accounting policies:

FINANCIAL STATEMENTS

The consolidated financial statements include the accounts of the subsidiaries.

REVENUE RECOGNITION

Sales are recorded when products are delivered, which is when ownership title is passed to the buyer and the recovery of theconsideration is reasonably assured.

The Company presents the trade marketing costs under the form of rebates or allowances related to the promotion of its products as a reduction of sales.

CASH AND CASH EQUIVALENTS

Cash and cash equivalents comprise cash, bank overdraft and short-term investments with maturities of three months or less at the date of acquisition.

SHORT-TERM INVESTMENTS

Short-term investments are recorded at fair market value and bear interest at rates varying from 4.29% to 4.31% in 2006.

INVENTORIES

Raw materials and supplies are valued at the lower of cost and replacement cost. Finished goods are valued at the lower of cost and net realizable value. Cost is determined using the first in, first out method.

FIXED ASSETS

Fixed assets are recorded at acquisition cost, net of government grants. Amortization is calculated over the useful lives of theassets using the following methods and annual rates:

Parking declining balance 10%Buildings declining balance 3%Machinery and equipment declining balance 10%

and straight-line from 2 1/2% to 33 1/3%Furniture and fixtures declining balance 20%

and straight-line from 10% to 33 1/3%Laboratory equipment declining balance 10%

and straight-line 20%Automotive equipment declining balance 15% and 20%

and straight-line 14 1/4%Computer system declining balance 30%

and straight-line 33 1/3%

GOODWILL

Goodwill represents the excess of the acquisition price over the fair value of the net assets of entities acquired at the date of acquisition. Goodwill is not amortized but is subject to an annual impairment test or more frequently if impairment indicators arise. Any excess of the carrying amount over the fair value of goodwill is charged to earnings for the year.

12

2. Accounting policies (continued)

INTANGIBLE ASSETS AND OTHER ASSETS

Intangible assets and other assets that are amortizable consist of the following items:

a) Technologies and software

Technologies and software are comprised of, among other things, software licenses for inhouse use and leading edge technologies and are recorded at acquisition cost. They are amortized using the straight-line method over their estimated useful lives varying from three to seven years.

b) TrademarksTrademarks are comprised of, among other things, trademarks and right of use. They are recorded at acquisition cost and amortized using the straight-line method over a period varying from two to twenty years.

c) Client relationshipsClient relationships are recorded at acquisition cost and are amortized using the straight-line method over a period varying from five to seven years.

d) CertificationsCertifications are comprised of, among other things, HACCP and FDA accreditations. They are recorded at acquisition cost and are amortized using the straight-line method over ten years.

e) Deferred charges

Deferred charges are comprised of incentives granted to customers related to the development and marketing of new products. These charges are recorded at cost and are amortized over a period of twelve to twenty-four months starting with the marketing of new products. Amortization of deferred charges is presented as a reduction of sales.

EMPLOYEE FUTURE BENEFITS

The cost of pension and other retirement benefits earned by employees is determined from actuarial calculations according tothe projected benefit method prorated on service, based on management’s best estimate assumptions of expected returns onthe plans’ assets, salary projections and the retirement ages of employees. Pension costs are charged to earnings and include:

. the cost of pension benefits provided in exchange for employees’ services rendered during the year;

. the amortization of the initial transitional obligation, past service costs and amendments on a straight-line basis over the expected average remaining service life of the employee group covered by the plans over five to eighteen years; and

. the interest cost of pension obligations, the return on pension funds assets and the amortization of cumulative unrecognizednet actuarial gains and losses in excess of 10% of the greater of the projected benefit obligation or market value of plan assets over the expected average remaining service life of the employee group covered by the plans.

INCOME TAXES

The asset and liability method is used in accounting for income taxes. Under this method, future income tax assets and liabilitiesare determined based on differences between the financial reporting and tax bases of assets and liabilities, and measured usingthe substantively enacted tax rates and laws that will be in effect when the differences are expected to reverse.

RESEARCH AND DEVELOPMENT

The research and development expense that does not satisfy the capitalization criteria is included in cost of goods sold andoperating expenses, net of the income tax credit.

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

13

2. Accounting policies (continued)

CURRENCY TRANSLATION

Monetary assets and liabilities are translated into Canadian dollars using the exchange rate in effect on the balance sheet date, whereas non-monetary assets and liabilities are translated using the historical exchange rates. Revenues and expenses are translated at the exchange rates in effect at the date of the transaction except for amortization, which is translated at historical rates.

DERIVATIVE INSTRUMENTS

The Company uses certain derivative instruments in order to eliminate or reduce its risks related to currency fluctuations having an influence on its purchases in foreign currencies. Management is responsible for establishing standards of acceptablerisks and does not use derivative instruments for speculative purposes. The Company uses these financial instruments solely for purposes of hedging probable future transactions and existing commitments or obligations.

The Company formally documents all relationships between hedging instruments and hedged items, as well as its riskmanagement objectives and strategy for undertaking various hedging transactions. This process includes linking all derivativesto specific assets and liabilities in the balance sheet, or specific future transactions. The Company also systematically determines, at inception of the hedge and over the term of the hedging relationship, whether changes in the cash flows of thehedged items can be effectively offset by the derivatives used in the hedging transactions.

The effective portion of exchange gains and losses on derivative financial instruments denominated in foreign currencies,qualifying for hedge accounting, used as a cash flow hedge of anticipated purchases denominated in foreign currencies, is recognized in other comprehensive income and reported as an adjustment to inventories when the purchase is recognized.

When a hedging relationship ceases to be effective, the corresponding gains or losses presented in accumulated other comprehensive income are reclassified to the statement of earnings of the period during which the underlying hedged transaction was recognized. If a hedged item is sold, extinguished or matures before the end of the related derivative instrument, the corresponding gains or losses presented in accumulated other comprehensive income are reclassified to the statement of earnings of the current period.

Derivative instruments that are economic hedges, but that do not qualify for hedge accounting, are recorded at their fair value and changes are charged to earnings.

IMPAIRMENT OF LONG-LIVED ASSETS

Long-lived assets are reviewed for impairment upon the occurrence of events or changes in circumstances indicating that thecarrying value of the assets may not be recoverable. Impairment is recognized when the carrying amount of a long-lived assetexceeds the undiscounted cash flows expected to result from its use and eventual disposal. The recognized impairment is measured as the excess of the carrying amount of the asset over its fair value.

USE OF ESTIMATES

The preparation of consolidated financial statements in accordance with Canadian generally accepted accounting principlesrequires management to make estimates, notably with respect to the allowance for doubtful accounts, inventories, the useful lives and amortization of fixed assets and intangible assets and other assets that can be amortized, the valuation of goodwill,the purchase price allocation of business acquisitions, accounts payable and accrued liabilities, notably the provision for trademarketing costs, future income tax assets and liabilities, actuarial assumptions and the assets retirement. These estimatesaffect the recorded amounts of assets and liabilities, the disclosure of contingent assets and liabilities as at the date of the consolidated financial statements and the reported amounts of sales and expenses during the reporting period. Since theprocess for presenting financial information presupposes the use of estimates, actual results could differ from those estimates.

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

14

3. New accounting policies and future accounting changes

NEW ACCOUNTING POLICIES

a) Financial instruments – Recognition and measurement

On January 1, 2007, the Company adopted CICA Handbook Section 3855, of the Canadian Institute of Chartered Accountants (“CICA”) “Financial Instruments – Recognition and Measurement.” This Section establishes when a financial instrument mustbe recorded on the balance sheet, the amount at which it must be recorded, and the standards for presenting gains and losses in the consolidated financial statements. Financial assets available for sale, assets and liabilities held for trading, and derivative financial instruments, whether or not they are part of a hedging relationship, are now measured at fair value.

The Company has made the following classifications:

. Cash and short-term investments are classified as assets held for trading and are measured at fair value. Gains and losses arising from periodic revaluation are recorded in net earnings.

. Accounts receivable are classified as loans and receivables and are measured at amortized cost.

. Bank overdraft, bank indebtedness, accounts payable and accrued liabilities and long-term debt are classified as other financial liabilities and are measured at amortized cost.

This new standard has been applied retroactively without restatement of the consolidated financial statements of prior periods.

Non-interest-bearing debt

As at January 1, 2007, the measuring of financial liabilities at amortized cost using the effective interest rate method had the following impact on the consolidated balance sheet: an increase in long-term future income tax assets of $384,000 andlong-term future income tax liabilities of $228,000, a decrease in fixed assets of $1,233,000, long-term debt of $708,000and opening retained earnings of $369,000.

Cash flow hedges

The effective portion of the changes in fair value of the hedging item is recorded in accumulated other comprehensive income,whereas the inefficient portion is recorded in financial expenses. The amounts recorded in accumulated other comprehensiveincome as part of cash flow hedges are reclassified in the statement of earnings in the period or periods in which the hedgeditem has an impact on net earnings.

As at January 1, 2007, the measuring of derivatives designated as cash flow hedges at fair value had the following impact onthe consolidated balance sheet: an increase in the derivative instruments captions under current assets and current liabilities of$322,000 and $266,000, respectively, and an increase in short-term future income tax liabilities of $18,000 and accumulatedother comprehensive income of $38,000. These amounts were reclassified to earnings in 2007.

Non-financial derivative instruments and embedded derivatives

The Company selected January 1, 2003 as its transition date for embedded derivatives. An embedded derivative is a component of a financial instrument or another contract with characteristics similar to a derivative financial instrument.As at January 1, 2007, the recording of non-financial derivative instruments had the following impact: an increase in derivativeinstruments under current assets of $629,000, in future income taxes within current liabilities of $208,000 and opening retained earnings of $421,000.

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

3. New accounting policies and future accounting changes (continued)

NEW ACCOUNTING POLICIES (CONTINUED)

a) Financial instruments – recognition and measurement (continued)

The following table summarizes the adjustments made following the adoption of the new accounting policies regarding financial instruments as at January 1, 2007.

Adjustmentson adoption

of new December accounting January 1,31, 2006 policies 2007

$ $ $

AssetsDerivative instruments 951 951Fixed assets 91,972 (1,233) 90,739Long-term future income taxes 384 384

Liabilities and shareholders’ equityShort-term future income taxes 79 226 305Derivative instruments 266 266Long-term debt 28,878 (708) 28,170Long-term future income taxes 13,082 228 13,310Retained earnings 103,807 52 103,859Accumulated other comprehensive income 38 38

b) Comprehensive income

On January 1, 2007, the Company adopted CICA Handbook Section 1530, “Comprehensive Income”. This Section describes the standards for reporting and disclosure recommendations with respect to comprehensive income and its components. Comprehensive income is the change in shareholders’ equity, that results from transactions and events from sources other than the Company’s shareholders. These transactions and events include gains and losses resultingfrom changes in the fair value of certain financial instruments.

The adoption of this Section implies that the Company now presents a consolidated statement of comprehensive income as a part of the consolidated financial statements.

c) Equity

On January 1, 2007, the Company adopted CICA Handbook Section 3251, “Equity,” replacing Section 3250, “Surplus.”It describes standards for the presentation of equity and changes in equity as a result of the application of Section 1530, “Comprehensive Income.”

d) Hedges

On January 1, 2007, the Company adopted CICA Handbook Section 3865, “Hedges”. The recommendations of this Section expand the guidelines required by Accounting Guideline 13 (AcG-13), Hedging Relationships. This Section describes when and how hedge accounting can be applied as well as the disclosure requirements. Hedge accounting enables the recording of gains, losses, revenues and expenses from the derivative financial instruments in the same period as for those related to the hedged item.

e) Financial Instruments – Disclosure and presentation

On January 1, 2007, the Company adopted CICA Handbook Section 3861, “Financial Instruments – Disclosure and Presentation.” This Section establishes standards for the presentation of financial instruments and non-financial derivatives and defines the information that should be disclosed about them.

15

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

3. New accounting policies and future accounting changes (continued)

FUTURE ACCOUNTING CHANGES

a) Financial instruments – Disclosures

The CICA issued the CICA Handbook Section 3862, “Financial Instruments – Disclosures “. This Section applies to fiscal years beginning on or after October 1, 2007. It describes the required disclosures related to the significance of financial instruments on the entity’s financial position and performance as well as the nature and extent of risks arising fromfinancial instruments to which the entity is exposed and how the entity manages those risks. This Section complements the principles of recognition, measurement and presentation of financial instruments of Sections 3855, “Financial Instruments – Recognition and Measurement”, 3863, “Financial Instruments – Presentation” and 3865, “Hedges”.

b) Financial instruments – Presentation

The CICA issued the CICA Handbook Section 3863, “Financial Instruments – Presentation”. This Section applies to fiscal yearsbeginning on or after October 1, 2007. It establishes standards for presentation for financial Instruments and non-financialderivatives. It complements standards of Section 3862, “Financial Instruments – Disclosures”.

c) Capital disclosures

The CICA issued the CICA Handbook Section 1535, “Capital Disclosures”. This Section applies to fiscal years beginning on or after October 1, 2007. It establishes standards for disclosing information about an entity’s capital and how it is managed to enable users of financial statements to evaluate the entity’s objectives, policies and procedures for managing capital.

The adoption of these three new standards described above as of January 1, 2008 will require additional disclosures in the consolidated financial statements.

d) Inventories

The CICA issued the CICA Handbook Section 3031, “Inventories,” which establishes inventory valuation standards and inventory costing methods. These recommendations apply to fiscal years beginning on or after January 1, 2008. The impact of the change will be a decrease of $372,000 in inventories, an increase of $117,000 in short-term future income tax assets,and a decrease of $255,000 in retained earnings.

e) Goodwill and intangible assets

The CICA issued the CICA Handbook Section 3064, “Goodwill and Intangible Assets.” This Section applies to fiscal years beginning on or after October 1, 2008. It establishes standards for the recognition, measurement, presentation and disclosureof goodwill and intangible assets. The Company is currently evaluating the impact of this new Section on January 1, 2009.

f) International financial reporting standards

The Accounting Standards Board of Canada has announced that the accounting standards used by public companies will converge with International Financial Reporting Standards (“IFRS”) during a transition period that should end by 2011. On February 13, 2008, the CICA confirmed that 2011 would be the changeover year from Canadian GAAP to IFRS. The Company will adopt these new standards according to the established timeline for these new rules. The Company is currently assessinghow these new standards will impact its consolidated financial statements.

16

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

4. Business acquisitionsi) On November 2, 2007, the Company acquired the assets related to the manufacture and marketing of ready-to-drink fruit

juices and fruit drinks of McCain Foods (Canada), a division of McCain Foods Limited, for $18,590,000, including acquisition fees of $296,000. The Company paid a cash consideration of $18,696,000. Earnings have been accounted for since the acquisition date.

ii) On November 26, 2007, the Company acquired substantially all of the assets and the working capital of Mondiv Food Products Inc., a Canadian manufacturer of specialty food products, for $18,863,000, including acquisition fees of $314,000.The Company paid a cash consideration of $16,444,000. The Company has an amount of $2,769,000 payable in the year following the transaction. Earnings have been accounted for since the acquisition date.

The purchase price allocation is preliminary and could be subject to change during next year. The assets acquired and liabilities assumed are presented at fair value and break down as follows:

Mondiv McCain Foods Food

(Canada) Products Inc. Total$ $ $

Assets purchasedCurrent assets 4,485 6,034 10,519Fixed assets for resale 1,000 1,000Land and buildings 4,500 5,051 9,551Machinery and equipment 4,650 5,746 10,396Other tangible assets 110 110Technologies and software 1,950 1,950Client relationships 2,027 1,100 3,127Trademarks 1,056 1,056Certifications 2,900 2,900Goodwill ($2,224,000 is tax deductible) 941 1,685 2,626

18,659 24,576 43,235

Liabilities assumedBank indebtedness 2,895 2,895Accounts payable and accrued liabilities 69 2,489 2,558Future income taxes 329 329

69 5,713 5,782Net assets purchased 18,590 18,863 37,453

Consideration givenDisbursement 18,696 16,444 35,140 Balance of purchase price (receivable) payable (106) 2,419 2,313

18,590 18,863 37,453

Fixed assets for resale consist of the machinery and equipment that was acquired but that cannot be used effectively by the Company.

17

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

5. Inventories2007 2006

$ $

Raw materials and supplies 48,712 37,289Finished goods 41,410 39,818

90,122 77,107

6. Fixed assets

2007 2006

Accumulated AccumulatedCost amortization Cost amortization

$ $ $ $

Land and parking 6,387 394 4,555 322Buildings 41,392 8,873 32,664 8,060Machinery and equipment 151,730 88,185 140,142 80,602Furniture and fixtures 3,973 2,788 3,617 2,406Laboratory equipment 622 482 570 464Automotive equipment 2,893 1,924 3,032 1,739Computer system 8,776 7,637 8,530 7,545Fixed assets in progress 17,168

232,941 110,283 193,110 101,138

Net book value 122,658 91,972

The Company reduced the value of certain equipment (machinery and equipment) by an amount of $718,000 in 2007. Thereduction was caused by the replacement of this equipment in 2008. A reduction in value of $87,000 has been recorded in 2006.

In 2007 and 2006, the Company recorded government assistance in an amount of $186,000 and of $281,000, respectively, as areduction of its fixed assets.

7. Intangible assets and other assets

2007 2006

Accumulated AccumulatedCost amortization Cost amortization

$ $ $ $

Technologies and software 4,027 1,804 1,934 1,592Trademarks 6,478 1,048 5,422 684Client relationships 5,544 1,173 2,417 739Certifications 2,900 14Deferred charges 10,994 8,862 5,718 4,286

29,943 12,901 15,491 7,301

Net book value 17,042 8,190

In 2007, the Company acquired technologies and software for an amount of $143,000 ($251,000 in 2006).

In 2007, The Company reduced the value of a trademark by $58,000. Due to declining sales associated with this trademark,management ran a test for recoverability and found that the carrying value exceeded future cash flows.

18

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

8. Bank indebtednessThe Company has various authorized credit facilities at its disposal, the amount of which may at no time exceed $80,150,000 in 2007 and $48,000,000 in 2006. The Company may, among other things, use revolving credit facilities up to a maximum ofUS$10,000,000. The Company may also use forward financial instruments for a maximum risk-equivalent amount ofCA$10,000,000. Furthermore, the Company may convert a portion of its credit facilities into a non-revolving term credit facilitynot exceeding CA$5,000,000. An amount of $13,340,000 was drawn as at December 31, 2007 and an amount of $5,740,000was drawn as at December 31, 2006. The credit facilities used bear interest at prime rate and/or at the bankers’ acceptancerates prevailing on the markets plus stamping fees. The authorized credit facilities are renewable every November. As atDecember 31, 2007, the prime rate was 6.0%. Bank indebtedness is secured by accounts receivable and inventories. The creditfacilities contain restrictive covenants that require the Company to maintain a financial ratio. As at December 31, 2007 and2006, this financial ratio was respected.

9. Long-term debt2007 2006

$ $

Loan, 6.50%, secured by a movable and immovable hypothec on certain equipment and buildings, payable through 2024 by thefollowing monthly principal instalments starting in August 2009:48 instalments of $79,750, 48 instalments of $135,000,48 instalments of $203,000, 35 instalments of $40,000 and one final instalment of $48,000. The rate is renewable on August 23,2021. The Company has the option to reimburse up to amaximum of 15% of the balance of the loan oneach anniversary date. i) 21,500

Loan, 5.90%, secured by a movable and immovable hypothec on certain equipment and buildings, payable through 2017 by thefollowing monthly principal instalments starting in May 2009:31 instalments of $112,000, 30 instalments of $194,000 and 40 instalments of $222,200. The rate is renewable on September 23,2014. The Company has the option to reimburse up to a maximum of 15% of the balance of the loan on each anniversary date. i) ii) 18,180 18,900

Loan, 5.50%, secured by a movable and immovable hypothec on certain equipment and buildings, payable through 2015 by thefollowing monthly principal instalments starting in May 2009:25 instalments of $50,760, 24 instalments of $93,000 and 29 instalments of $120,000. The rate is renewable on May 23,2008. The Company has the option to reimburse up to a maximum of 15% of the balance of the loan on each anniversary date. i) ii) 6,981 7,339

Loan, 6.50%, secured by a movable and immovable hypothec on certain equipment and buildings, payable through 2016 by thefollowing monthly principal instalments starting in May 2009:25 instalments of $25,920, 24 instalments of $40,000 and 32 instalments of $51,000. The rate is renewable on January 23,2014. The Company has the option to reimburse up to a maximum of 15% of the balance of the loan on each anniversary date. i) ii) 3,240 3,400

Loan, non-interest bearing, payable starting in 2006 in five equal and consecutive annual instalments through 2010. The discount ratesrange from 7.6% to 9.0% 1,399 2,734

19

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

9. Long-term debt (continued)

2007 2006

$ $Loan, non-interest bearing, payable starting in 2012 in five equal

and consecutive annual instalments through 2016. The discount rate is 7.9% i) 918

Obligation related to the acquisition of equipment, non-interest bearing,payable starting in December 2005 in eight equal annual instalments of $182,025 through 2012. The discount rate is 7.8% 731 1,092

Loan, non-interest bearing, payable in monthly instalments of $5,952 through 2011. The discount rate is 8.2% 239 349

Loan, non-interest bearing, payable upon certain conditions and maturing in 2008. The discount rate is 8.9% 125 125

53,313 33,939

Current portion 925 5,061

52,388 28,878

During the second quarter of 2007, the Company obtained a non-interest-bearing loan of $1,456,000 from a lending institution.The Company measured this debt using the effective interest rate method, the result being a $596,000 decrease in debt andfixed assets and a $185,000 increase in long-term future income tax assets and long-term future income tax liabilities.

i) These loans are subject to a restrictive covenant requiring the Company to maintain a financial ratio.

ii) These loans include a payment holiday of 24 principal instalments, starting in May 2007.

The book value of the assets provided as security for debt as at December 31, 2007 was $75,306,000 ($54,733,000 in 2006).

The first instalment of the loan payable starting in 2006 was withdrawn on January 3, 2007 by the lending institution.

Principal payments due within each of the next five years on long-term debt are as follows:

$

2008 9252009 2,7082010 4,0212011 3,9422012 5,354

10. Capital stockAuthorized

An unlimited number of first and second rank preferred shares, non-voting, issuable in one or several series, the attributes of which will be determined by the directors before their issuance. First preferred shares rank prior to second preferred shares with respect to the payment of dividends and reimbursement of capital, without par value

An unlimited number of Class A subordinate voting shares, without par value

An unlimited number of Class B multiple voting shares, without par value

2007 2006

$ $Issued

2,915,200 Class A shares (2,969,360 in 2006) 13,132 13,3763,752,620 Class B shares 5,986 5,986

19,118 19,362

20

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

10. Capital stock (continued)

During the year, the Company redeemed for cancellation in the normal course of business 54,160 Class A subordinate votingshares on the market for a cash consideration of $2,042,000, including $244,000 as a reduction of capital stock, $1,790,000 asa reduction of retained earnings and $8,000 as a reduction of contributed surplus. During the year ended December 31, 2006,the Company redeemed for cancellation in the normal course of business 92,500 Class A subordinate voting shares on the market for a cash consideration of $3,463,000, including $416,000 as a reduction of capital stock, $3,033,000 as a reduction ofretained earnings and $14,000 as a reduction of contributed surplus.

Stock option plan

The Company established a stock option plan pursuant to which it may grant stock options for Class A shares to its employeesand those of its subsidiaries. The exercise price of each stock option is equal to the closing price of the Company’s shares onthe day preceding the grant date.

These stock options generally vest at the annual rate of 20% and expire five to six years following the grant date. As atDecember 31, 2007 and 2006, 150,000 stock options for Class A shares were available under the stock option plan, but nonewere granted.

EARNINGS PER SHARE

Basic and diluted earnings per share are calculated using the weighted average number of shares outstanding during the year. The Company uses the treasury stock method for determining the dilutive effect of stock options. For the years endedDecember 31, 2007 and 2006, there were no dilutive items.

11. Accumulated other comprehensive loss

The accumulated other comprehensive loss of $442,000 is comprised of after tax unrealized gains and losses, on cash flowhedges. This amount will be charged to earnings during the next twelve months.

12. Risk management and fair value of financial instruments

FINANCIAL RISKS

Financial risk is the risk to the Company’s earnings that arises from fluctuations in interest rates and foreign exchange rates and the degree of volatility of these rates. The Company’s short-term credit facilities bear interest at variable rates.

The Company concluded approximately 5% of its sales and 41% of its purchases in foreign currencies. Consequently, certainassets, liabilities, revenues and expenses are exposed to exchange risk. As at December 31, 2007, the amounts in Canadian dollars of receivables and payables denominated in U.S. dollars totalled $2,459,000 ($2,366,000 in 2006) and $3,677,000($3,753,000 in 2006), respectively. The Company uses foreign exchange forward contracts when considered advantageous toreduce its exposure to foreign currency risk. The foreign exchange forward contracts available as at December 31, 2007 aredescribed in Note 20.

CREDIT RISK

The Company provides credit to its customers in the normal course of business. Credit evaluations are performed on an ongoing basis and the consolidated financial statements take into account allowances for losses. Most of the accounts receivable balance consists of amounts receivable from customers related to the food industry. As at December 31, 2007,three clients represent 48.2% (51.0% in 2006) of the accounts receivable balance. The Company carries out 53.8% of its saleswith three of its major clients (55.5% in 2006).

FAIR VALUE

The fair value of short-term investments, accounts receivable, bank overdraft, bank indebtedness and accounts payable andaccrued liabilities approximates their book values because of their short-term maturities.

The difference between the book value and the fair value of long-term debt represents a negative value of approximately$85,000 (a positive value of approximately $577,000 in 2006).

21

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

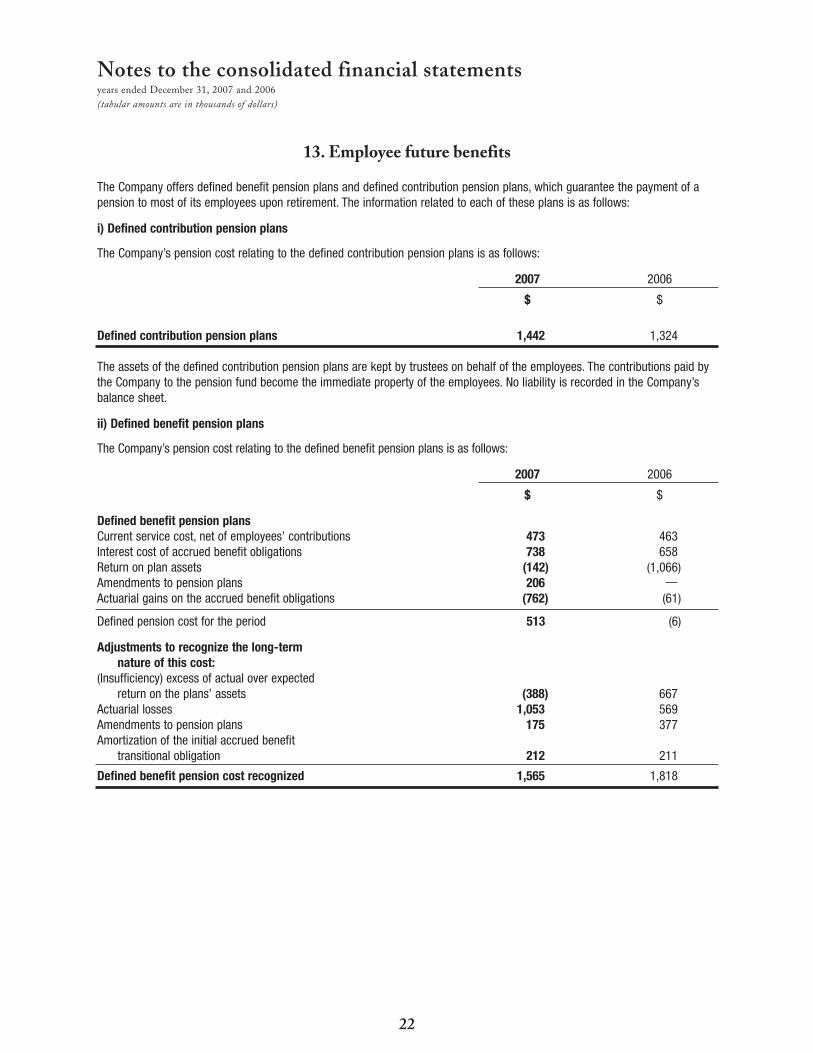

13. Employee future benefits

The Company offers defined benefit pension plans and defined contribution pension plans, which guarantee the payment of apension to most of its employees upon retirement. The information related to each of these plans is as follows:

i) Defined contribution pension plans

The Company’s pension cost relating to the defined contribution pension plans is as follows:

2007 2006

$ $

Defined contribution pension plans 1,442 1,324

The assets of the defined contribution pension plans are kept by trustees on behalf of the employees. The contributions paid bythe Company to the pension fund become the immediate property of the employees. No liability is recorded in the Company’sbalance sheet.

ii) Defined benefit pension plans

The Company’s pension cost relating to the defined benefit pension plans is as follows:

2007 2006

$ $

Defined benefit pension plansCurrent service cost, net of employees’ contributions 473 463Interest cost of accrued benefit obligations 738 658Return on plan assets (142) (1,066)Amendments to pension plans 206Actuarial gains on the accrued benefit obligations (762) (61)

Defined pension cost for the period 513 (6)

Adjustments to recognize the long-termnature of this cost:

(Insufficiency) excess of actual over expectedreturn on the plans’ assets (388) 667

Actuarial losses 1,053 569Amendments to pension plans 175 377Amortization of the initial accrued benefit

transitional obligation 212 211

Defined benefit pension cost recognized 1,565 1,818

22

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

13. Employee future benefits (continued)

ii) Defined benefit pension plans (continued)

The obligations of these plans are presented as follows:

2007 2006

$ $

Accrued benefit obligationsBalance, beginning of year 13,726 12,824Obligations transferred following a business acquisition 316Current service cost 485 476Interest cost of accrued benefit obligations 738 658Amendments to pension plans 206Benefits paid (286) (171)Actuarial gains (762) (61)

Balance, end of year 14,423 13,726

Assets of the pension plansBalance, beginning of year 14,127 10,733Assets transferred following a business acquisition 288Actual return on plan assets 142 1,066Employer contributions 53 53Employee contributions 12 13Benefits paid (286) (171)Employer funding to the plans 534 2,433

Balance, end of year 14,870 14,127

Surplus in fair value of assets over accruedbenefit obligations 447 401

Unamortized initial transitional obligation 578 790Unamortized actuarial losses 1,754 2,419Unamortized amendments to pension plans 1,333 1,508

Net accrued benefit asset 4,112 5,118

The composition of the pension plans’ assets is as follows:% %

Bonds 21.9 16.7Shares 25.5 29.7Mutual funds 8.4 10.4Treasury bonds 2.4Others* 41.8 43.2

100.0 100.0

* Deposits in trust prescribed by the Canada Revenue Agency for funded supplemental employee retirement plans, are non-interest bearing. The deposits in trust account for 38.8% of the pension plans’ assets in 2007 (42.9% in 2006).

23

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

13. Employee future benefits (continued)

ii) Defined benefit pension plans (continued)

During the year, the Company provided funding to the plan for management employees in the amount of $534,000. Furthermore,the Company made a plan contribution after the closing date for an amount of $194,000. In 2006, the Company provided fundingto the plan for management employees in the amount of $2,433,000.

The initial accrued benefit obligation of $2,029,000, at the inception of the plans, is amortized over the average remaining servicelife of active employees.

The significant actuarial assumptions used by the Company to measure its accrued benefit obligations are as follows:

2007 2006

Accrued benefit obligations as at December 31:Discount rate 5.0% to 5.5% 4.8% to 5.3%Rate of compensation increase 3.5% to 5.0% 3.3% to 5.0%

Benefit costs for the years ended December 31:Discount rate 4.8% to 5.3% 5.0% to 5.3%Expected rate of return on plan assets 3.0% to 7.5% 3.3% to 7.5%Rate of compensation increase 3.3% to 5.0% 3.5% to 5.0%

The accrued benefit obligations, the fair value of plan assets and the composition of pension plans’ assets are measured at the date of the annual financial statements. The most recent actuarial valuations, for funding purposes, of the plans were performed on September 30, 2007 and December 31, 2006 and the next actuarial valuations should be performed no later thanSeptember 30, 2008 and December 31, 2008.

14. Additional information on earnings

As at December 31, 2007, the research and development expense amounted to $736,000 ($992,000 in 2006) and the researchand development income tax credit amounted to $276,000 ($372,000 in 2006).

15. Amortization2007 2006

$ $

Fixed assets 9,579 8,800Technologies and software 212 265 Trademarks 306 271Client relationships 434 383Certifications 14

10,545 9,719

24

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

16. Financial expenses

2007 2006

$ $

Interest on long-term debt 2,216 1,827Interest – other 600 795Interest – income (644) (458)Exchange loss 221 36

2,393 2,200

17. Income taxesThe components of the provision for income taxes for the years ended December 31 are as follows:

2007 2006

$ $

Current 10,709 11,013Future (995) (257)

9,714 10,756

The components of the balance sheet for future income taxes are as follows:

Short-term future income tax assets:Accounts payable and accrued liabilities 120 119Research and development (70)Derivative instruments 233Loss carry-foward and provision 6Capital tax (45)Tax loss 53

244 172

Short-term future income tax liabilities:Research and development 79

Long-term future income tax liabilities:Fixed assets 10,545 10,815Net accrued benefit asset 1,327 1,731Goodwill, intangible assets and other assets 261 536Long-term debt 268

12,401 13,082

25

(70)

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

17. Income taxes (continued)

Reconciliation of the statutory income tax rate and the effective income tax rate on earnings is as follows:

2007 2006

% %

Combined basic federal and provincial income tax rate 32.8 32.7

Adjustment of future income taxes related to rate changes (4.3) (4.9)

Retroactive adjustment – provincial income taxes 15.2

Other items 0.9 0.9

Effective income tax rate on earnings 29.4 43.9

On June 9, 2006, the Government of Quebec enacted Bill 15 to amend the Taxation Act and other legislative provisions. As aresult of this amendment, the Company recorded an unusual income tax expense of $3,730,000.

18. Additional cash flow information

2007 2006

$ $

Changes in non-cash operating working capital itemsAccounts receivable (3,379) (4,202)Inventories (5,026) (4,725)Prepaid expenses (184) 243Accounts payable and accrued liabilities 6,769 2,650Income taxes 83 5,230

(1,737) (804)

Interest paid 1,999 1,866Income taxes paid 10,626 5,783

In 2007, the Company acquired fixed assets of which an amount of $3,739,000 was unpaid as at December 31, 2007($885,000 as at December 31, 2006). Furthermore, the Company recorded a capital tax credit receivable of $186,000 in 2007($281,000 in 2006) related to its fixed assets investments.

26

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

19. Segmented information

The Company operates only one reportable segment: the processing, conditioning, packaging and marketing of food products.The Company’s assets are located in Canada and substantially all of the net sales are conducted there.

20. Commitments and contingencies

i) At year-end, outstanding foreign exchange forward contracts to hedge fluctuations in currencies with respect to future purchases amount to $75,404,000.

In order to reduce the potential negative impact of a decrease in the value of the Canadian dollar compared to the U.S. dollar and Euros, the Company entered into several transactions in order to hedge future purchases in U.S. dollars and Euros:

Forward contracts Type Rate Contractual Net negative(CA dollars) amounts fair value

From 1 to 12 months Purchase 0.9437 to 1.1131 US$73,775,000 $775,0001 month Purchase 1.4387 to 1.4871 1,040,000 $19,000

Forward contracts are contracts whereby the Company is committed to purchase currencies at a predetermined rate.

ii) The Company is committed under operating leases for equipment and office space. In addition, the Company entered into service agreements for its operations and marketing activities. The payments over the forthcoming years are as follows:

Operating Othersleases

$ $

2008 2,311 3,8982009 1,872 6452010 1,647 2772011 1,542 722012 1,394 252013 and thereafter 2,404

iii) The Company is committed under various contracts to purchase raw materials. The payments over the forthcoming years are as follows:

$

2008 63,362 2009 19,8262010 19,826

27

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements

20. Commitments and contingencies (continued)

iv) As at December 31, 2007, the Company had letters of credit totalling $135,000 ($148,000 in 2006).

v) During the normal course of business, various proceedings and claims are instituted against the Company. The Company contests the validity of these claims and proceedings, and management believes that any settlement will not have a materialeffect on the financial position or on the consolidated earnings of the Company.

21. Related party transaction

During the second quarter of 2006, the Company acquired a land from a company controlled by a director of the Company who is also a majority shareholder. The transaction was measured at the exchange amount. The Company paid the total cashconsideration of $110,000 at the transaction date.

22. Comparative figures

Certain comparative figures have been reclassified to conform to the current year’s presentation.

28

years ended December 31, 2007 and 2006(tabular amounts are in thousands of dollars)

Notes to the consolidated financial statements