consolidated financial results fiscal year 2003...

TRANSCRIPT

Consolidated Financial Results Fiscal Year 2003

EURO DISNEY S.C.A.

Consolidated Financial Results Fiscal Year 2003

EURO DISNEY S.C.A.

November 17, 2003

André Lacroix

Chairman and CEO

Euro Disney

André Lacroix

Chairman and CEO

Euro Disney

2003 Situation

Strategic analysis and new management methodology

New 2004 actions

Disneyland Resort Paris / Theme Park LeaderLeading European Theme Parks (2002*)

2 5002 9003 0303 0003 1003 2003 800

12 403

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

DLRP Park 1 Park 2 Park 3 Park 4 Park 5 Park 6 Park 7

Attendance('000 guests)

* FY’03 figures

Source: Revenue Development and Consumer Knowledge, FY’03 except for type of Park ticket (October FY’04)

High Guest Satisfaction

Intent to recommend / revisit has also reached high rates

Probably yes9 %

Definitely yes90 %

No1 % Probably

yes27 %

No6 %

Definitely yes67%

Intention to recommend

Intention to revisit

Source : Consumer Knowledge, FY’02 and FY’03 Guest Satisfaction Barometer

2003 Situation

Strategic analysis and new management methodology

New 2004 actions

Jeffrey R. SPEED

Senior Vice Presidentand

Chief Financial Officer

Euro Disney S.C.A.

Jeffrey R. SPEED

Senior Vice Presidentand

Chief Financial Officer

Euro Disney S.C.A.

Business Context

Fiscal Year 2003 Financial Results

Liquidity Outlook

Business Context: GeneralBusiness Context: General

Challenging macro-economic and geo-political environment

Difficult year for the entire travel and tourism industry

Visibility with respect to bookings remains somewhat clouded

Price discounting across the industry

Business Context: Euro Disney First SemesterBusiness Context: Euro Disney First Semester

Increase in top line revenues, primarily in first quarter

=> Revenues increase 8%

Increased costs and expenses linked to the new two-park Resort

=> Decreased EBITDA Margin*As % of revenues: 12% vs 19% in FY’02

*Before royalties and management fees

Business Context: Euro Disney Second SemesterBusiness Context: Euro Disney Second Semester

Decline in volume during second semester

=> Revenues down 9%

Prudent yield management to preserve pricing

Management implemented proactive cost control measures

=> Stable EBITDA Margin*As % of revenues: 29% vs 30% in FY’02

*Before royalties and management fees

Business Context

Fiscal Year 2003 Financial Results

Liquidity Outlook

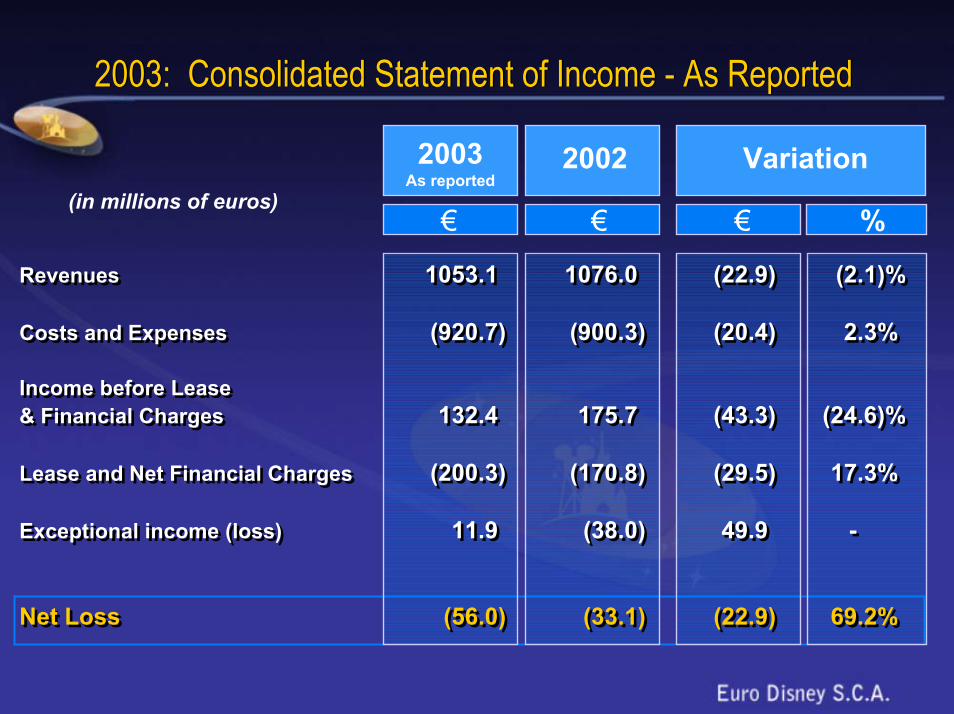

2003: Consolidated Statement of Income - As Reported2003: Consolidated Statement of Income - As Reported

2003As reported

2002 Variation(in millions of euros)

%

Revenues 1053.1 1076.0 (22.9) (2.1)%

Costs and Expenses (920.7) (900.3) (20.4) 2.3%

Income before Lease& Financial Charges 132.4 175.7 (43.3) (24.6)%

Lease and Net Financial Charges (200.3) (170.8) (29.5) 17.3%

Exceptional income (loss) 11.9 (38.0) 49.9 -

Net Loss (56.0) (33.1) (22.9) 69.2%

Revenues 1053.1 1076.0 (22.9) (2.1)%

Costs and Expenses (920.7) (900.3) (20.4) 2.3%

Income before Lease& Financial Charges 132.4 175.7 (43.3) (24.6)%

Lease and Net Financial Charges (200.3) (170.8) (29.5) 17.3%

Exceptional income (loss) 11.9 (38.0) 49.9 -

Net Loss (56.0) (33.1) (22.9) 69.2%

€€€

Fiscal Year 2003 Results: Basis of PresentationFiscal Year 2003 Results: Basis of Presentation

As-reported results reflect adoption of required change in accounting principle

Impact of accounting change is a decrease of €11 million in NetIncome (€20 million decrease in EBITDA offset by €9 million decrease in Depreciation and Amortisation)

In addition, due to the waiver on Royalties and Management Feesfor the last three quarters of FY’03 (a reduction of €27 million), we will focus our discussion on EBITDA before Royalties and Management Fees

To enhance comparability between fiscal periods, we will presentFY’03 before taking into account the accounting change

2003: Key Financial Results2003: Key Financial Results

2003*

€ €

2002 Variation

%€(in millions of euros)

Revenues 1053.1 1076.0 (22.9) (2.1)%

EBITDA before Royaltiesand Management Fees 226.1 275.3 (49.2) (17.9)%

As % of revenues 22% 26% (4) ppt

Revenues 1053.1 1076.0 (22.9) (2.1)%

EBITDA before Royaltiesand Management Fees 226.1 275.3 (49.2) (17.9)%

As % of revenues 22% 26% (4) ppt

*Before accounting change

The Resort SegmentThe Resort Segment

2002

%€ € €Revenues 1029.5 1048.7 (19.2) (1.8)%

EBITDA Before Royaltiesand Management Fees 215.5 262.9 (47.4) (18.0)%

As % of revenues 21% 25% (4) ppt

Revenues 1029.5 1048.7 (19.2) (1.8)%

EBITDA Before Royaltiesand Management Fees 215.5 262.9 (47.4) (18.0)%

As % of revenues 21% 25% (4) ppt

2003* Variation(in millions of euros)

*Before accounting change

The Resort Segment: Focus on Theme ParksThe Resort Segment: Focus on Theme Parks

2003 Variation2002

Revenues (in millions of euros) 508.5 526.0 (17.5) (3.3)%

Attendance (in millions) 12.4 13.1 (0.7) (5.3)%

Average guest spending 40.7 40.1 0.6 +1.5%(in euros, excluding V.A.T)

Revenues (in millions of euros) 508.5 526.0 (17.5) (3.3)%

Attendance (in millions) 12.4 13.1 (0.7) (5.3)%

Average guest spending 40.7 40.1 0.6 +1.5%(in euros, excluding V.A.T)

€ € €

Theme ParksTheme Parks

%

The Resort Segment: Focus on HotelsThe Resort Segment: Focus on Hotels

2003 Variation2002

€ € €

Revenues (in millions of euros) 416.7 411.7 +5.0 +1.2%

Occupancy 85.1% 88.2% (3.1)ppt

Average spending per room 183.5 175.1 +8.4 +4.8%(in euros, excluding V.A.T)

Revenues (in millions of euros) 416.7 411.7 +5.0 +1.2%

Occupancy 85.1% 88.2% (3.1)ppt

Average spending per room 183.5 175.1 +8.4 +4.8%(in euros, excluding V.A.T)

Hotels and Disney VillageHotels and Disney Village

%

Real Estate Development SegmentReal Estate Development Segment

2003 Variation

%

2002

Revenues 23.6 27.3 (3.7) (13.6)%

EBITDA before Royaltiesand Management Fees 10.6 12.4 (1.8) (14.5)%

As % of revenues 45% 45% -

Revenues 23.6 27.3 (3.7) (13.6)%

EBITDA before Royaltiesand Management Fees 10.6 12.4 (1.8) (14.5)%

As % of revenues 45% 45% -

€ € €(in millions of euros)

Operating Costs EvolutionOperating Costs Evolution

2003* 2002 Variation(in millions of euros)

Direct operating costs 625.8 613.3 +12.5 +2.0%

Marketing and Sales costs 105.2 95.4 +9.8 +10.3%

General and Administrative costs 96.0 92.0 +4.0 +4.3%

Sub Total Operating Costs 827.0 800.7 +26.3 +3.3%

Royalties and Management fees 8.1 35.5 (27.4) (77.2)%

Depreciation and amortisation 75.0 64.1 +10.9 +17.0%

Operating Costs 910.1 900.3 +9.8 +1.0%

Direct operating costs 625.8 613.3 +12.5 +2.0%

Marketing and Sales costs 105.2 95.4 +9.8 +10.3%

General and Administrative costs 96.0 92.0 +4.0 +4.3%

Sub Total Operating Costs 827.0 800.7 +26.3 +3.3%

Royalties and Management fees 8.1 35.5 (27.4) (77.2)%

Depreciation and amortisation 75.0 64.1 +10.9 +17.0%

Operating Costs 910.1 900.3 +9.8 +1.0%

€ € %€

*Before accounting change

Increase in Lease and Financial Charges in Line with ExpectationsIncrease in Lease and Financial Charges in Line with Expectations

20022003 Variation

Lease and Financial Charges 200.3 170.8 +29.5 17.3 %

Increase mainly due to:- Increase in principal reimbursement by the

financing companies (incl. in lease) +18.2

- Increased interest charges +9.5- Other +1.8

Lease and Financial Charges 200.3 170.8 +29.5 17.3 %

Increase mainly due to:- Increase in principal reimbursement by the

financing companies (incl. in lease) +18.2

- Increased interest charges +9.5- Other +1.8

%€€ €(in millions of euros)

Exceptional ItemsExceptional Items

2002

Income (Loss)before Exceptional Items (57.3) 4.9 (62.2) -

Exceptional income (loss) 11.9 (38.0) 49.9 131.3%

Net Loss (45.4) (33.1) (12.3) 37.2%

Income (Loss)before Exceptional Items (57.3) 4.9 (62.2) -

Exceptional income (loss) 11.9 (38.0) 49.9 131.3%

Net Loss (45.4) (33.1) (12.3) 37.2%

€ € €

2003* Variation(in millions of euros)

%

*Before accounting change

Cash BalancesCash Balances

2003 2002 Variation(in millions of euros)

€€ €Beginning Cash Equivalent Balance 21.3 548.4 (527.1)

Cash flow from Operating Activities 88.1 48.7 +39.4

Proceeds from Fixed Assets Sales 45.4 1.4 +44.0

Capital Expenditures and Other (74.2) (271.1) +196.9

Cash flow used in Investing Activities (28.8) (269.7) +240.9

Cash Flow used in Financing Activities (34.6) (306.1) +271.5

Ending Cash Equivalent Balance 46.0 21.3 +24.7

Beginning Cash Equivalent Balance 21.3 548.4 (527.1)

Cash flow from Operating Activities 88.1 48.7 +39.4

Proceeds from Fixed Assets Sales 45.4 1.4 +44.0

Capital Expenditures and Other (74.2) (271.1) +196.9

Cash flow used in Investing Activities (28.8) (269.7) +240.9

Cash Flow used in Financing Activities (34.6) (306.1) +271.5

Ending Cash Equivalent Balance 46.0 21.3 +24.7

Business Context

Fiscal Year 2003 Financial Results

Liquidity Outlook

Modification of Royalties and Management Fee Payments on March 28, 2003

Royalties and Management Fees for the last three quarters of fiscal year 2003 were waived

Modification of payment terms for fiscal year 2004 (fiscal year-end payment rather than quarterly)

The waived amounts relating to fiscal year 2003, may become due to the extent that EBITDA exceeds €450 million in any fiscal year from2004 to 2008

Additional Liquidity Efforts

Limited programme of asset sales with gross proceeds of €45 million

Debt Security Deposit reduction until March 31, 2004

€45 million subordinated credit line from The Walt Disney Company

Conclusion: First Semester FY’04 Outlook

Our current forecasts do not assume a recovery until second semester FY’04.

Barring any unforeseen events, sufficient liquidity until March 31, 2004.

Between now and March 31, 2004, we will work with our various stakeholders to find a long-term resolution to our financial challenges.

At the same time, we will remain focused on managing and relaunching the business.

2003 Situation

Strategic analysis and new management methodology

New 2004 actions

Opportunity for Growth Linked to Penetration Rates

Total European Population* DLRP European Core Target **

16 %

Total Population: 329 M

Visitors

Non visitors

(52M) 25 %

Total Core Target: 122 M

Non visitors

(30M)

Visitors

* Includes France, UK, Germany, Benelux, Italy and Spain** Core target: families with children (3 to 15) + young adults (20 to 35) - rejecters + kids core target + income qualifier-

Source: Advancy Consulting, LabLB May 2001

Growth Opportunity for Parks Attendance

0123456789

101112

FY'98FY'99FY'00FY'01FY'02FY'03FY'04FY'05FY'06FY'07

EMEA

U.S.

CAGR ‘03-‘07

U.S. 3.4%EMEA 4.1%

In Mil Guests

*Includes the Middle East nd Africa**based Population of 14 European Union countries (not including Greece and Switzerland) Source: PricewaterhouseCoopers

N.B.: data related to leisure and theme parks and taking into account the free-entrance Parks in which the rides are not free.

2003 Situation

Strategic analysis and new management methodology

New 2004 actions

2003 Situation

Strategic analysis and new management methodology

New 2004 actions

2003 Situation

Strategic analysis and new management methodology

New 2004 actions

New 2004 actions

A new marketing strategy

A new management team

A new capital structure

New 2004 actions

A new marketing strategy

A new management team

A new capital structure

New 2004 actions

A new marketing strategy

A new management team

A new capital structure

New 2004 actions

A new marketing strategy

A new management team

A new capital structure

Our Four Strategic Assets

The Disney brand

A complete tourist destination in the heart of Europe

Unique know-how to bring legends and fantasy to life and provide unforgettable memories

Cast Members who are devoted to their work

Consolidated Financial Results Fiscal Year 2003

EURO DISNEY S.C.A.

Consolidated Financial Results Fiscal Year 2003

EURO DISNEY S.C.A.

November 17, 2003