consideration of price caps reduction meeting of the board of governors of the california iso by...

TRANSCRIPT

Consideration of Price Caps Reduction

Meeting of the

Board of Governors of the

California ISO

By

David ParquetVice President

Enron North America Corp.June 28, 2000

California Is Facing an Energy Supply Crisis that a Precipitous Reduction in Price Caps

Will only Heighten.

• The supply shortage is real; California desperately needs new generation.

• California has not added any significant new generation since the 1980’s.

• The existing thermal generation fleet is aging: 61% 30 years

• Demand has exploded with the economic boom, especially in San Francisco Bay Area.

• California competes vigorously with the rest of the growing West for increasingly scarce supplies.

2

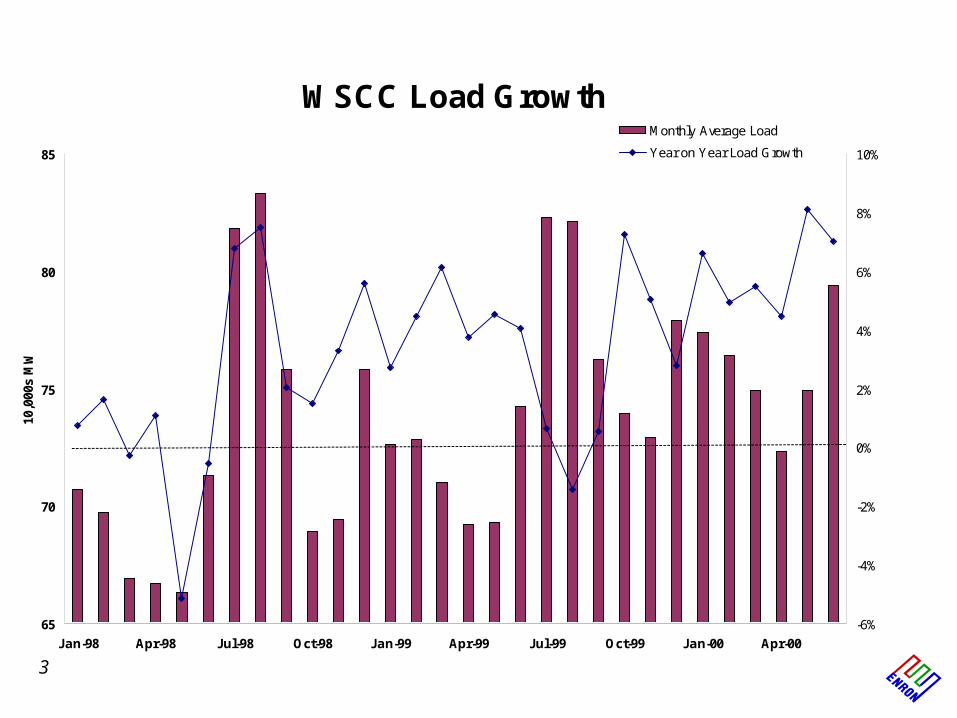

WSCC Load Growth

65

70

75

80

85

Jan-98 Apr-98 Jul-98 Oct-98 Jan-99 Apr-99 Jul-99 Oct-99 Jan-00 Apr-00

10,0

00s

MW

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Monthly Average Load

Year on Year Load Growth

3

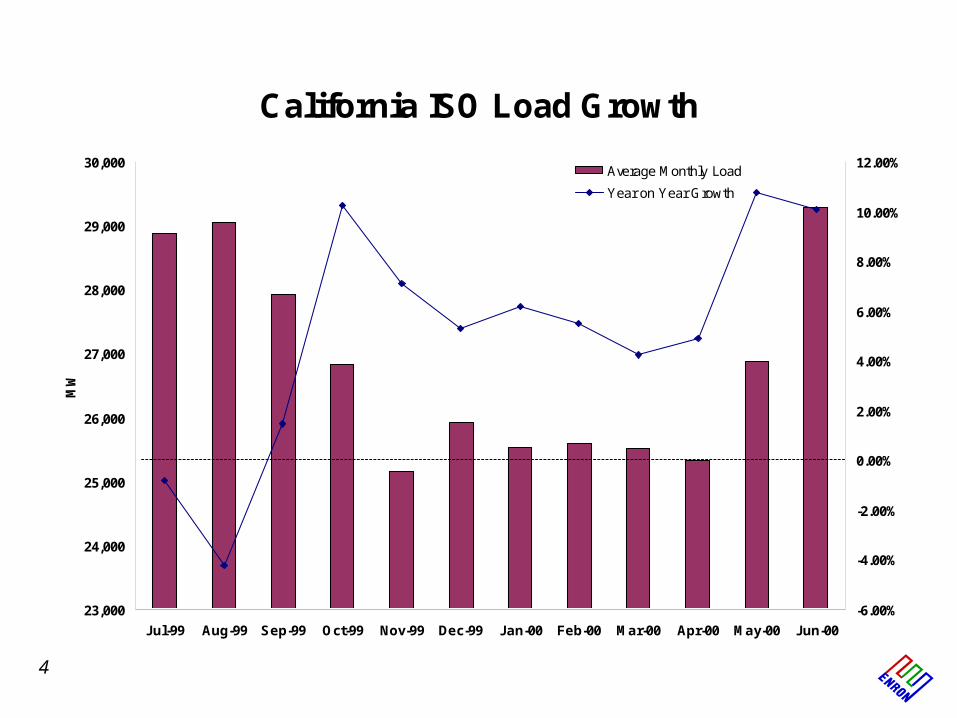

California ISO Load Growth

23,000

24,000

25,000

26,000

27,000

28,000

29,000

30,000

Jul-99 Aug-99 Sep-99 Oct-99 Nov-99 Dec-99 Jan-00 Feb-00 Mar-00 Apr-00 May-00 Jun-00

MW

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%Average Monthly Load

Year on Year Growth

4

0

20

40

60

80

100

120

140

160

Northwest Rockies Southwest California WSCC

WSCC Loads (GW)

California is not an island and cannot develop a self-contained solution.

5

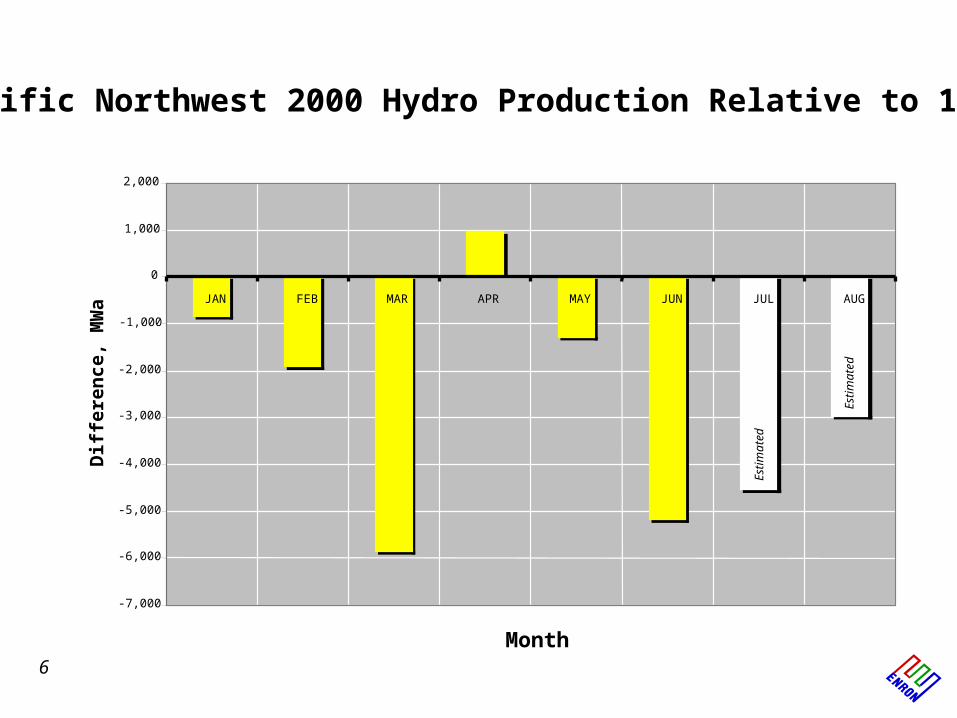

Pacific Northwest 2000 Hydro Production Relative to 1999

-7,000

-6,000

-5,000

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

JAN FEB MAR APR MAY JUN JUL AUG

Month

Dif

fere

nce

, M

Wa

Estim

ated

Estim

ated

6

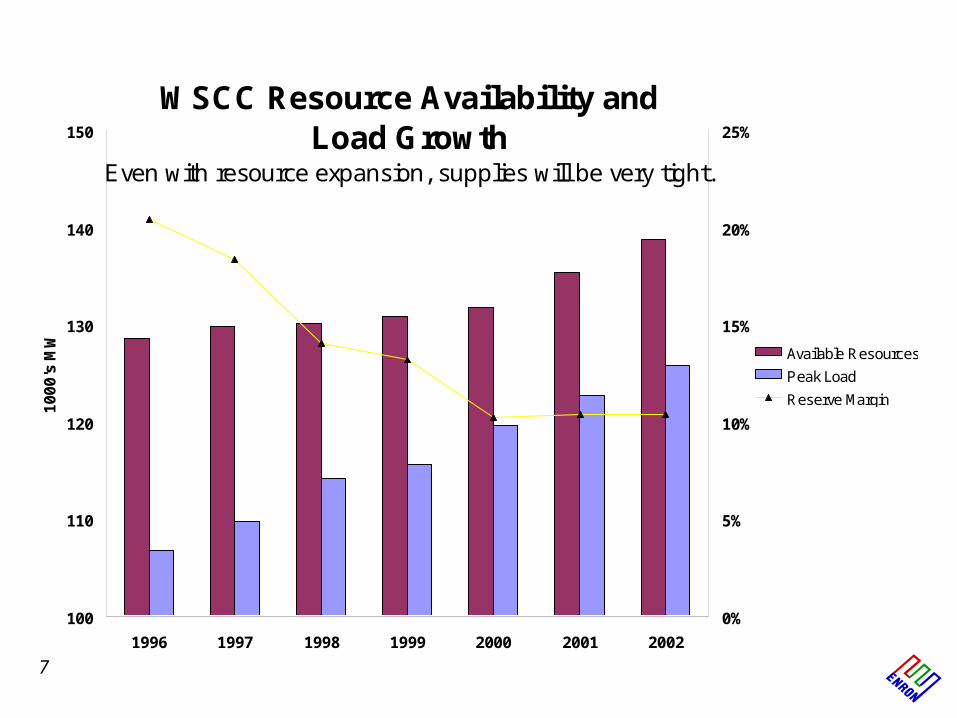

WSCC Resource Availability and Load Growth

Even with resource expansion, supplies will be very tight.

100

110

120

130

140

150

1996 1997 1998 1999 2000 2001 2002

10

00

's M

W

0%

5%

10%

15%

20%

25%

Available Resources

Peak Load

Reserve Margin

7

A Price Cap Reduction Will only Increase the Pressure on Reliability of California Electric System

• Investment in power plants will go elsewhere, taking jobs, economic and reliability benefits.

• Suppliers will sell outside California where markets are more predictable and prices are higher.

• Keeping the lights on will get tougher.

• Because of the interdependent linkages in California’s electric market, cannot change one aspect of structure without impacting all others.

• Uncertainty in the marketplace is the surest way to dry up the growing forward markets.

8

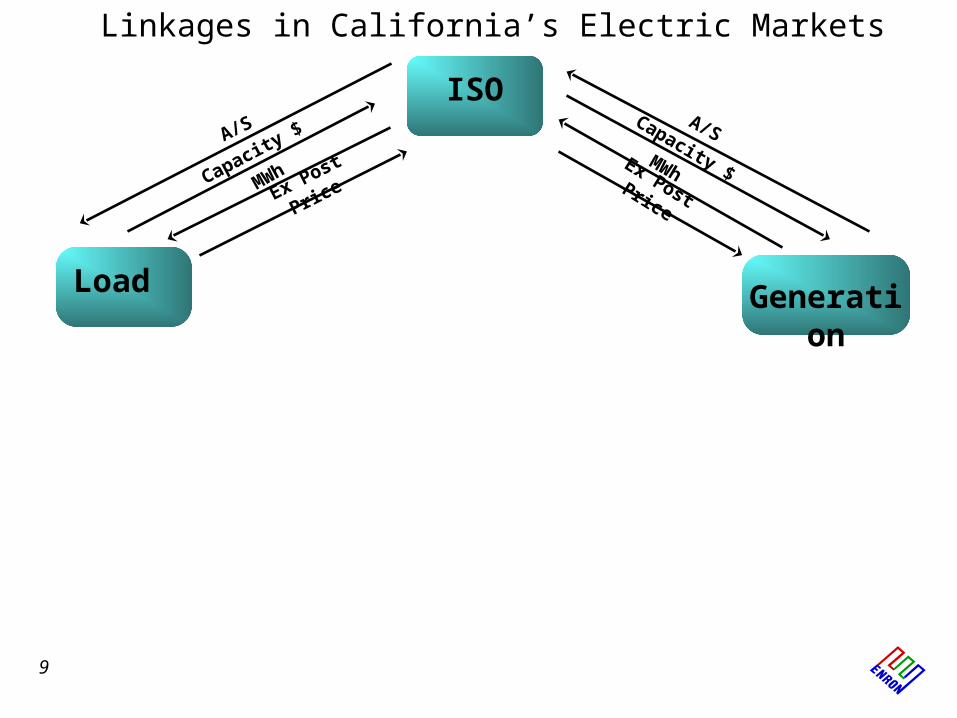

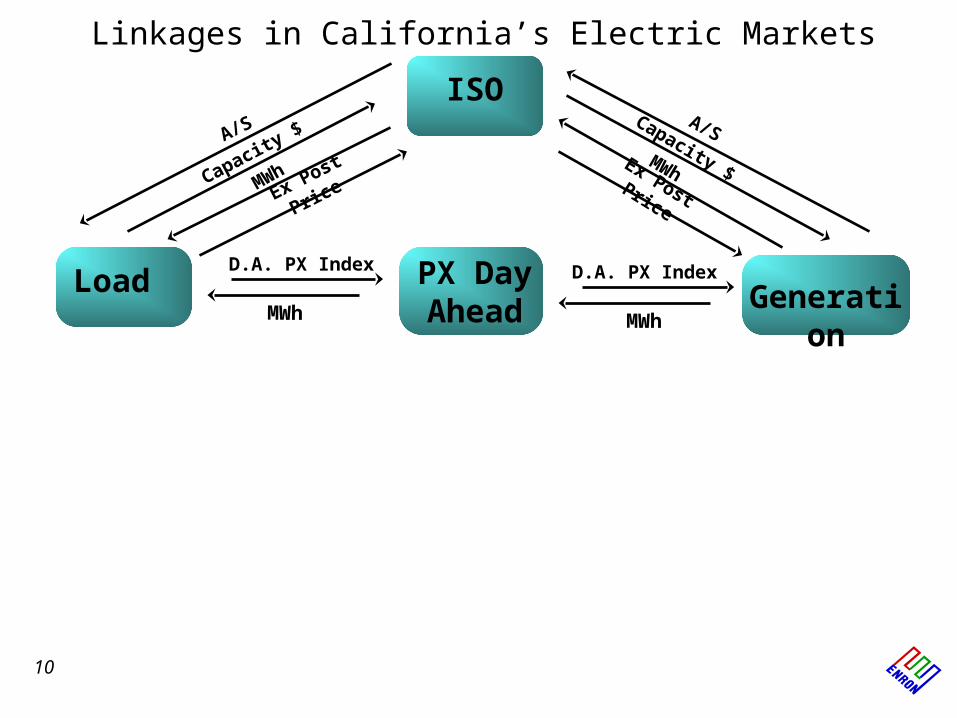

Load Generation

ISO

Linkages in California’s Electric Markets

A/S

Ex Post Price

MWhCapacity $Ex Post Price

MWh

Capacity $

A/S

9

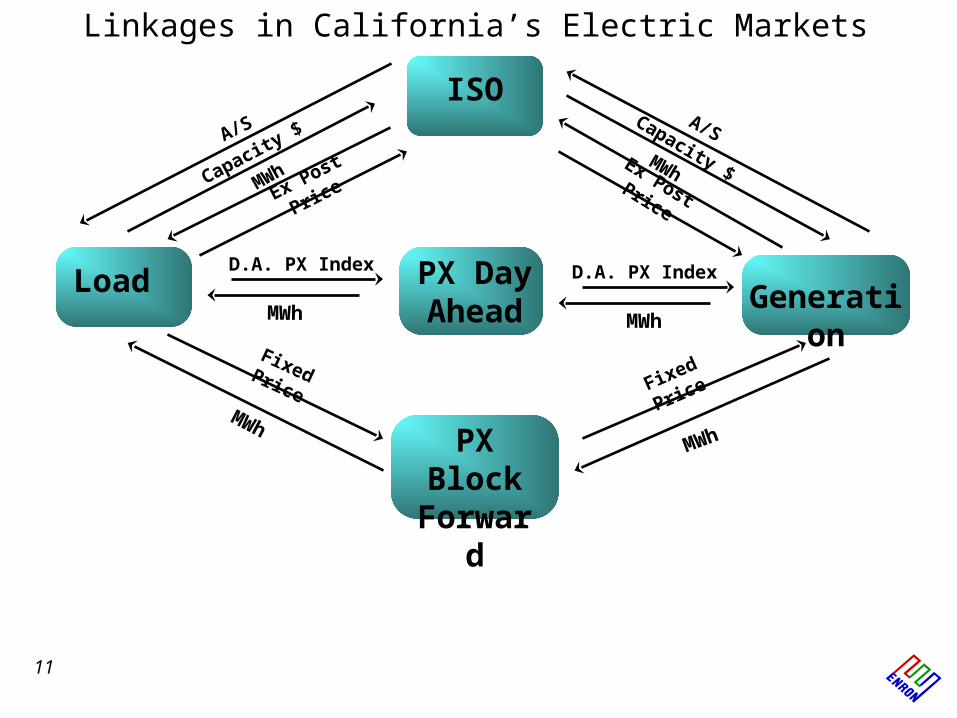

Load Generation

ISO

PX Day AheadMWh

D.A. PX Index D.A. PX Index

MWh

A/S

Capacity $

MWh

Ex Post Price

Capacity $MWhEx Post Price

A/S

Linkages in California’s Electric Markets

10

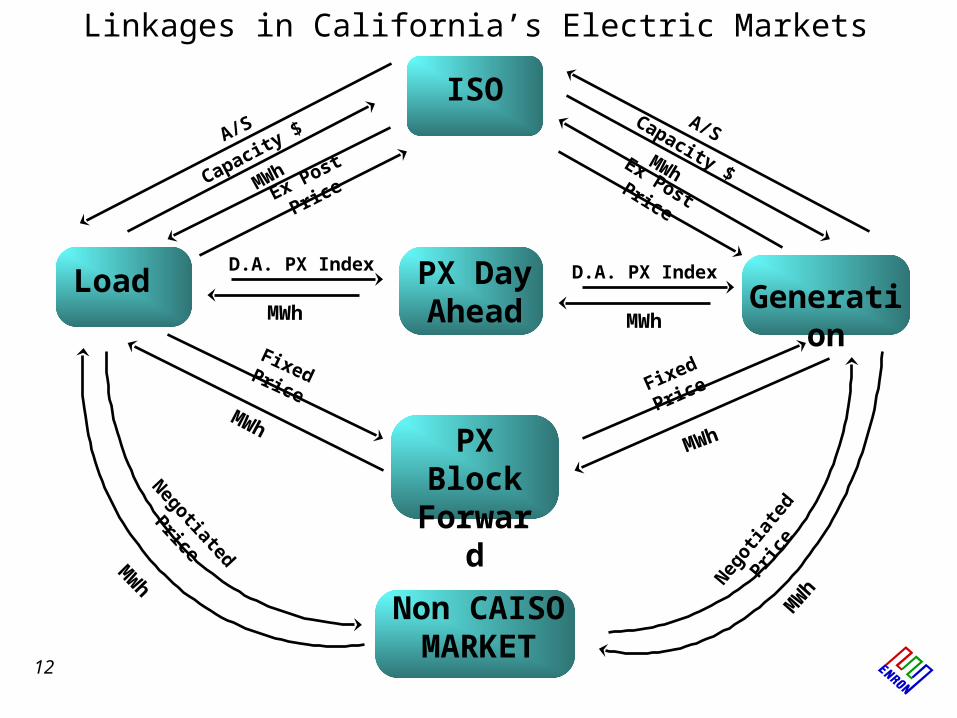

PX Block Forward

Load Generation

ISO

PX Day Ahead

Fixed Price

MWh

Fixed PriceMWh

MWh

D.A. PX Index D.A. PX Index

MWh

MWhEx Post Price

A/S

Capacity $

MWh

Ex Post Price

A/SCapacity $

Linkages in California’s Electric Markets

11

PX Block Forward

Load Generation

ISO

PX Day Ahead

Non CAISO MARKET

Fixed Price

MWh

Fixed PriceMWh

MW

h Negotiated

Price

MWh

D.A. PX Index D.A. PX Index

MWh

MW

h

Neg

otia

ted

Price

MWhEx Post Price

A/S

Capacity $

MWh

A/S

Ex Post Price

Capacity $

Linkages in California’s Electric Markets

12

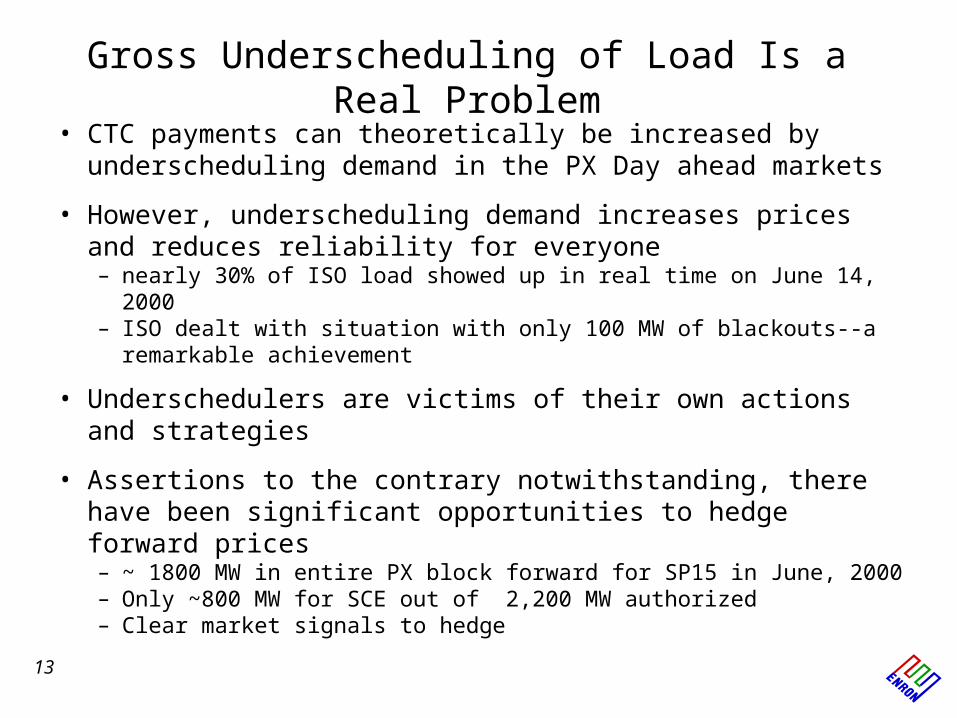

Gross Underscheduling of Load Is a Real Problem

• CTC payments can theoretically be increased by underscheduling demand in the PX Day ahead markets

• However, underscheduling demand increases prices and reduces reliability for everyone– nearly 30% of ISO load showed up in real time on June 14, 2000– ISO dealt with situation with only 100 MW of blackouts--a

remarkable achievement

• Underschedulers are victims of their own actions and strategies

• Assertions to the contrary notwithstanding, there have been significant opportunities to hedge forward prices– ~ 1800 MW in entire PX block forward for SP15 in June, 2000– Only ~800 MW for SCE out of 2,200 MW authorized – Clear market signals to hedge13

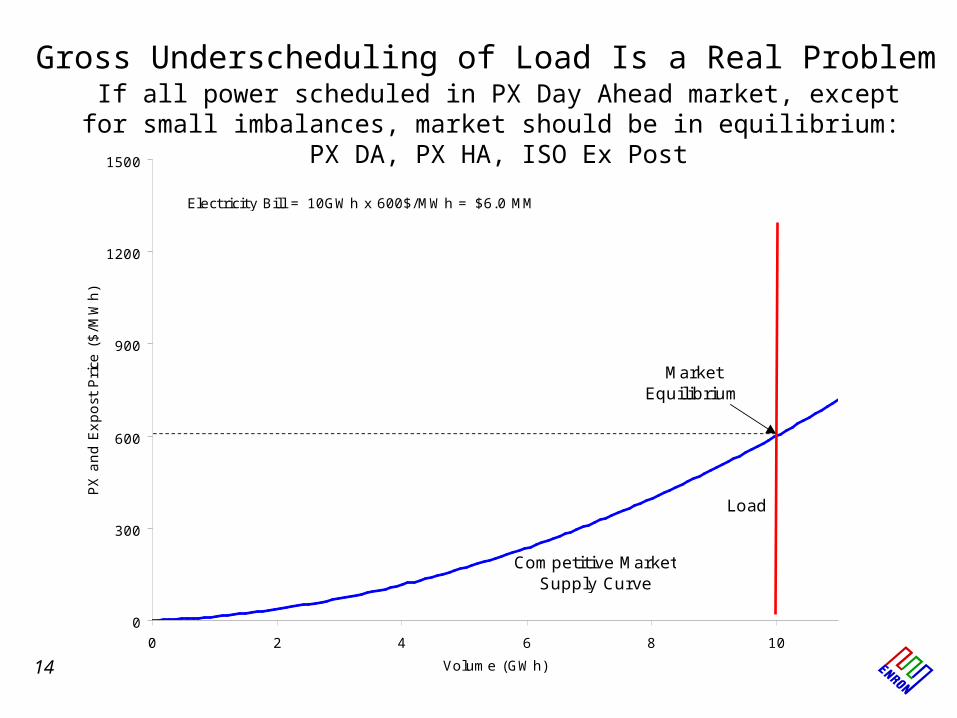

Gross Underscheduling of Load Is a Real Problem

If all power scheduled in PX Day Ahead market, except for small imbalances, market should be in equilibrium: PX DA, PX HA, ISO Ex Post

0

300

600

900

1200

1500

0 2 4 6 8 10

Volume (GWh)

PX

and E

xpost

Pri

ce (

$/M

Wh)

Competitive Market Supply Curve

Load

Electricity Bill = 10GWh x 600$/MWh = $6.0 MM

Market Equilibrium

14

Gross Underscheduling of Load Is a Real Problem

In actual fact, there is an incentive to underschedule, but consequence is pressure on real time reliability as Ex Post load grows.

0

300

600

900

1200

1500

0 2 4 6 8 10

Volume (GW)

PX

and E

xpost

Pri

ce (

$/M

Wh)

Load to Ex Post

Savings from Underscheduling Load

Load to PX Day Ahead

Electricity Bill = 8GWh x 400$/MWh + 2GWh x 600$/MWh = $4.4 MM

400

Underscheduling Value = $6.0 MM - $4.4 MM = $1.6 MM

Arbitrary Limit Bid

15

Gross Underscheduling of Load Is a Real Problem

But when there is massive underscheduling in a tight supply market, the ISO may have to take drastic action.

0

300

600

900

1200

1500

0 2 4 6 8 10

Volume (GW)

PX

and E

xpost

Pri

ce (

$/M

Wh)

Cost

Savings

Electricity Bill = 7GWh x 400$/MWh + 3GWh x 1500$/MWh = $7.3 MM

Underscheduling Value = $6 MM - $7.3 MM = -$1.3 MM

Arbitrary Limit Bid

(including replacement reserves to sustain

reliability)

Increasing load to Ex Post

16

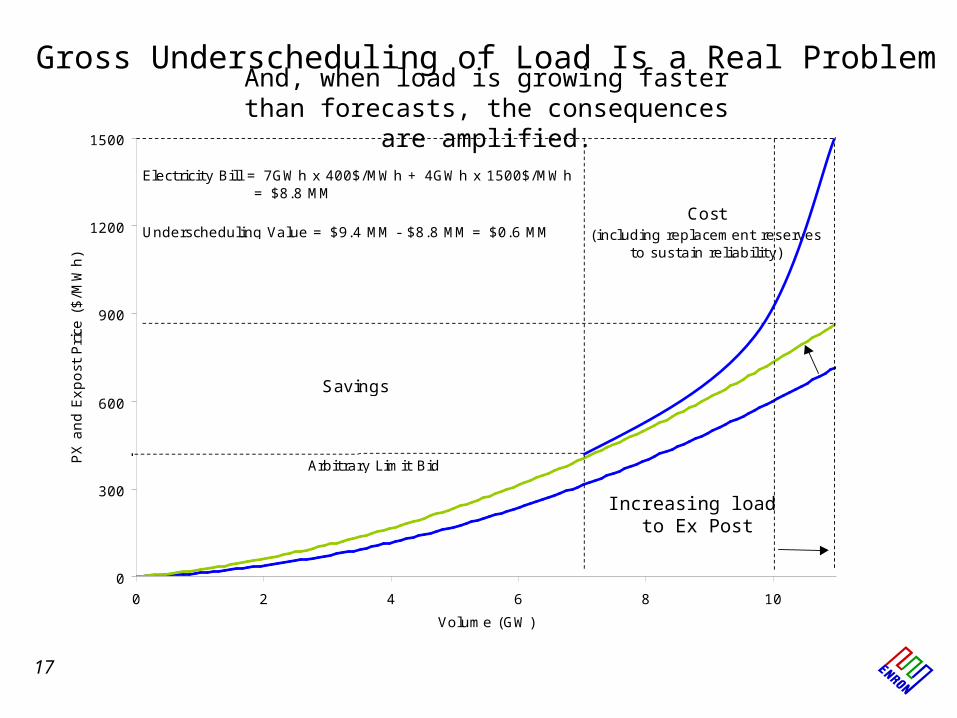

Gross Underscheduling of Load Is a Real ProblemAnd, when load is growing faster than

forecasts, the consequences are amplified.

0

300

600

900

1200

1500

0 2 4 6 8 10

Volume (GW)

PX

and E

xpost

Pri

ce (

$/M

Wh)

Cost

Savings

Electricity Bill = 7GWh x 400$/MWh + 4GWh x 1500$/MWh = $8.8 MM

Underscheduling Value = $9.4 MM - $8.8 MM = $0.6 MM

Arbitrary Limit Bid

(including replacement reserves to sustain reliability)

Increasing load to Ex Post

17

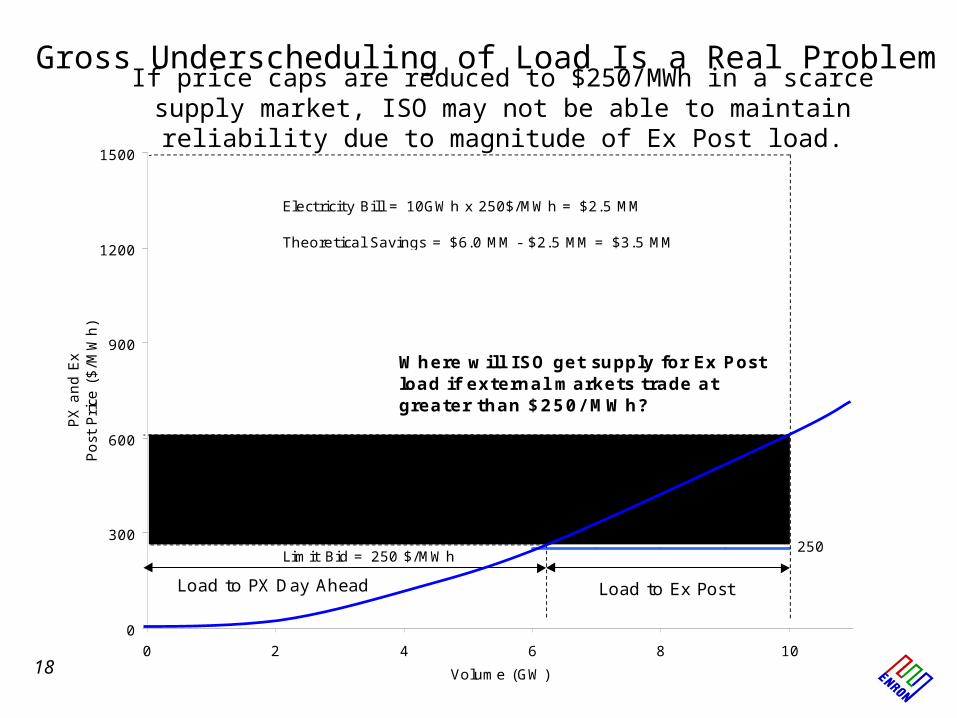

Gross Underscheduling of Load Is a Real ProblemIf price caps are reduced to $250/MWh in a scarce supply market, ISO

may not be able to maintain reliability due to magnitude of Ex Post load.

0

300

600

900

1200

1500

0 2 4 6 8 10

Volume (GW)

PX

and E

x

Post

Pri

ce (

$/M

Wh)

Theoretical Savings

Electricity Bill = 10GWh x 250$/MWh = $2.5 MM

Theoretical Savings = $6.0 MM - $2.5 MM = $3.5 MM

250

Load to Ex PostLoad to PX Day Ahead

Limit Bid = 250 $/MWh

Where will ISO get supply for Ex Post load if external markets trade at greater than $250/ MWh?

18

Recommendations

• Do not reduce price caps from $750/MWh to $250/MWh.

• Determine the root causes of the problem.- Market power abuse: supply and/or demand?- Market structure?- Load growth?- Resource scarcity?- Remove price caps? Parity with PX caps?

• Develop alternative solutions: market and other.- Structural market changes- Facilitate new resources/ease congestion:

generation, transmission- Demand side: bidding, real time prices

19

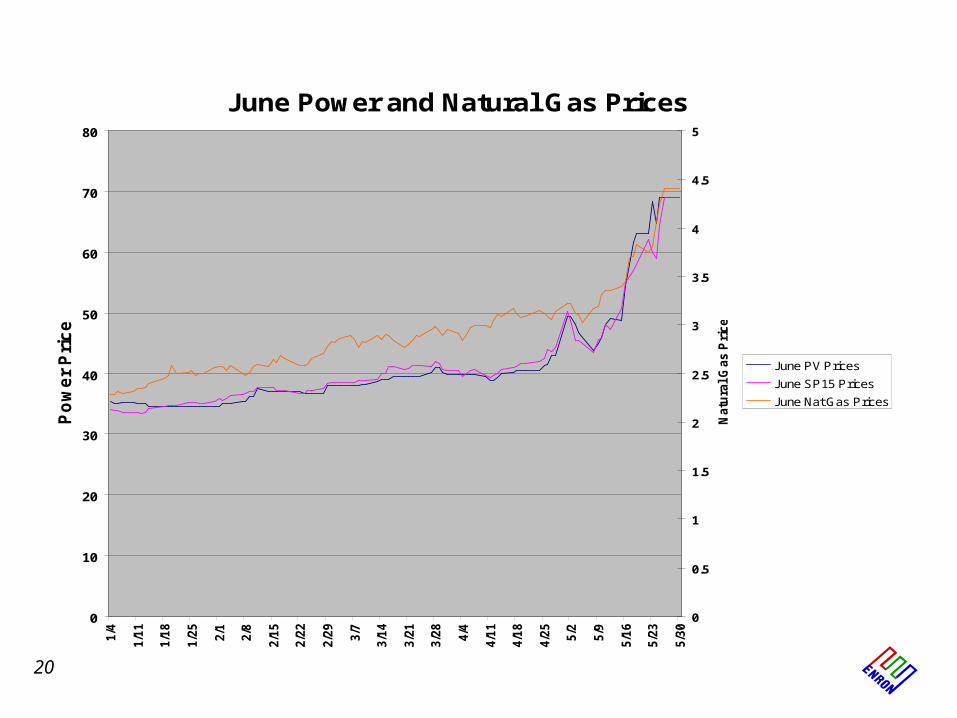

June Power and Natural Gas Prices

0

10

20

30

40

50

60

70

80

1/4

1/1

1

1/1

8

1/2

5

2/1

2/8

2/1

5

2/2

2

2/2

9

3/7

3/1

4

3/2

1

3/2

8

4/4

4/1

1

4/1

8

4/2

5

5/2

5/9

5/1

6

5/2

3

5/3

0

Po

we

r P

ric

es

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Natu

ral G

as P

rices

June PV Prices

June SP15 Prices

June Nat Gas Prices

20

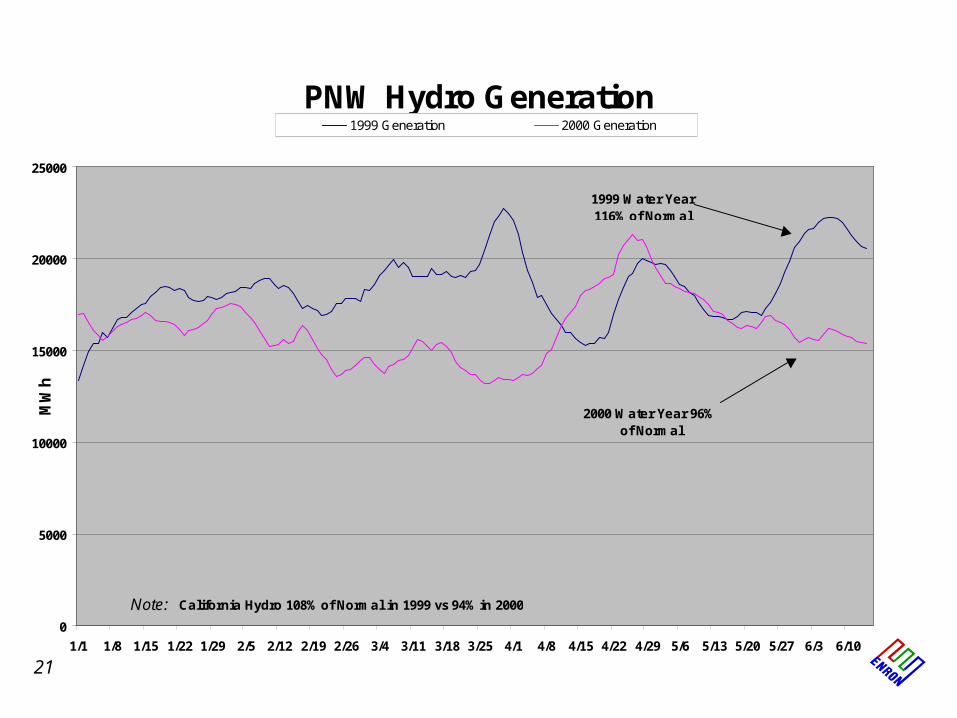

PNW Hydro Generation

0

5000

10000

15000

20000

25000

1/1 1/8 1/15 1/22 1/29 2/5 2/12 2/19 2/26 3/4 3/11 3/18 3/25 4/1 4/8 4/15 4/22 4/29 5/6 5/13 5/20 5/27 6/3 6/10

MW

h

1999 Generation 2000 Generation

1999 Water Year 116% of Normal

2000 Water Year 96% of Normal

Note: California Hydro 108% of Normal in 1999 vs 94% in 2000

21

June SP15 Block Forward Purchases vs. Power Prices

0

10

20

30

40

50

60

70

80

1/4/00 1/18/00 2/1/00 2/15/00 2/29/00 3/14/00 3/28/00 4/11/00 4/25/00 5/9/00 5/23/00

Po

wer

Pri

ces

0.00

1000.00

2000.00

3000.00

4000.00

5000.00

6000.00

7000.00

8000.00

MW

h

June PV Price

June SP-15 Price

BF Purchases

22