conflicts of interest related parties … · charity • can lead to conflicts of interest or...

TRANSCRIPT

CONFLICTS OF INTEREST

RELATED PARTIES

RELATED PARTY TRANSACTIONS

The problem…

• Charity Trustees naturally bring with them to their

position connections which can be of benefit to the

charity

• Can lead to conflicts of interest or loyalty

Why is this an issue?

• Trustees have a legal duty to act only in the best

interest of the charity

• Decisions not being made in the Charity’s best

interest

• Reputational damage

• Can be invalid or open to challenge

• Conflicts of interest are not a problem providing they

are correctly and transparently addressed

Why is this an issue?

• Charity Commission see many cases of charities

getting into difficulty because conflicts of interest

were not addressed or were handled incorrectly

• Important to have in place robust systems

Who does this apply to?

• Trustees

• Senior management

• Someone able to engage charity in significant

financial transactions

Three step process………

IDENTIFY

PREVENT

RECORD

IDENTIFY

• A conflict of interest is any situation in which a

trustee’s personal interests or loyalties could, or

could be seen to, prevent the trustee from making a

decision only in the best interests of the charity.

• There is a conflict of interest where there is a

proposed transaction between the charity and a

connected person of a trustee or senior person in the

organisation. Similarly, there is a conflict of interest

where there is a benefit or a potential benefit to a

connected person

PREVENT

• Remove conflict of interest by not pursuing that

action, undertaking it differently, not appointing

trustee/trustee resignation

• Conflict of loyalty – e.g. potential new trustee who is

a trustee or is connected with another organisation

operating in the same field / competing for funds etc.

PREVENT

• Follow law/governing document in respect of

managing conflict

• In absence of governing document/legal provisions:

– require conflicted trustees to declare their interest at an

early stage and, in most cases, withdraw from relevant

meetings, discussions, decision making and votes

– consider updating their governing document to include

provisions for dealing with conflicts of interest

PREVENT

• Exceptionally, need to seek the authority of the

Commission where the conflict of interest is so acute

or extensive that following these options will not

allow the trustees to demonstrate that they have

acted in the best interests of the charity

PREVENT

• Conflicts of interest often arise because a decision

involves a potential trustee benefit.

• Trustee benefit must be properly authorised and the

trustees must follow any conditions attached to the

authority which say how the conflict of interest

should be handled (legal requirements)

RECORD

• Trustees should formally record any conflicts of

interest and how they were handled and must, if

they prepare accruals accounts, disclose any trustee

benefits in the charity’s accounts

Examples of benefits to trustees

• Sell, loan or lease charity assets to a charity trustee

• acquire, borrow or lease assets from a trustee for the charity

• Pay a trustee for carrying out their trustee role

• Pay a trustee for carrying out a separate paid post within the charity, even if that trustee has recently resigned as a trustee

• Pay a trustee for carrying out a separate paid post as a director or employee of the charity’s subsidiary trading company

• Pay a trustee, or a person or company closely connected to a trustee, for providing a service to the charity. This covers anything that would be regarded as a service and includes legal, accountancy or consultancy services through to painting or decorating the charity’s premises, or any other maintenance work

• employ a trustee’s spouse or other close relative at the charity (or at the charity’s subsidiary trading company)

• Make a grant to a service user trustee, or a service user who is a close relative of a trustee

• Allow a service user trustee to influence service provision to their exclusive advantage

Good practice

• Include provisions in governing document to deal

with conflicts of interest

• Conflicts of interest policy and register of interests

• Ensuring that meetings include an item to declare

potential conflicts at the start and have it minuted

• Transparency – public availability of register

• Pre-appointment issue for new trustees

RELATED PARTY TRANSACTION

• A related party transaction is a financial transaction

between the related party and the charity. A related

party transaction involves the transfer of assets or

liabilities or the performance of services by, to or for

a related party

• As auditors we have a duty to undertake work to

identify such transactions

Donations from trustees

• Trustees may also give to the charity. Donations

which are unrestricted do not have to be separately

disclosed. However, if the trustee specified how the

funds had to be used, then this may be exerting

significant influence and so restricted donations by

trustees do have to be disclosed.

Charity Commission Guidance

• https://www.gov.uk/government/publications

/conflicts-of-interest-a-guide-for-charity-

trustees-cc29/conflicts-of-interest-a-guide-for-

charity-trustees

The Charity Commission's new regulatory approach - are you informed?

Steve LawHead of Investigations TeamCharity Commission for England and Wales

Charity seminar

HW Fisher & Company

11 November 2014

The Charity Commission

The independent regulator of charities in England and Wales

Five statutory objectives (s14 CA 2011)

• The compliance objective – promoting compliance by charity trustees with their legal obligations

Commission’s functions (s15 (1)(3) CA 2011)

• Identifying and investigating apparent misconduct or mismanagement in the administration of charities

• taking remedial or protective action

Facts about charity

164,000 – registered charities

4,968 – new registrations in 2013-14

3.4 million – regular volunteers

1m – charity trustees

940,000 – charity workers

> £64bn – annual income of registered charities

£106bn – long term investments held by charities

Scale of charitable sector

Upholding public trust in charity

Commission’s work to uphold public trust • our strategic approach

• how we are improving already

• plans for the months ahead

Charities’ role in promoting public trust • what the public expects of you

• what we expect of you

Context for charity regulation

Changing public expectations of charity• Demands for greater accountability

• Evidence of public giving charities less ‘benefit of doubt’

• Media focus on charities (e.g. pay, investments)

Increased external scrutiny of Commission• National Audit Office review of Commission’s work

• Public Accounts Committee hearings

• Debates in Parliament

Significant cuts to Commission funding• CC budget 2013-14 - £21.4m

• CC budget 2007-8 - £31.7m

• = c. 50% real terms cut since 2007

New £8m funding• To invest in technology and frontline operations

Our new strategic approach

One of our most important statutory objectives is to increase public trust and confidence in charities.

“by concentrating on promoting compliance by charity trustees with their legal obligations,

by enhancing the rigour with which we hold

charities accountable, and by ensuring that we

uphold the definition of charity under charity

law” (Statement of regulatory approach, Commission’s Annual report and

accounts 2013/2014)

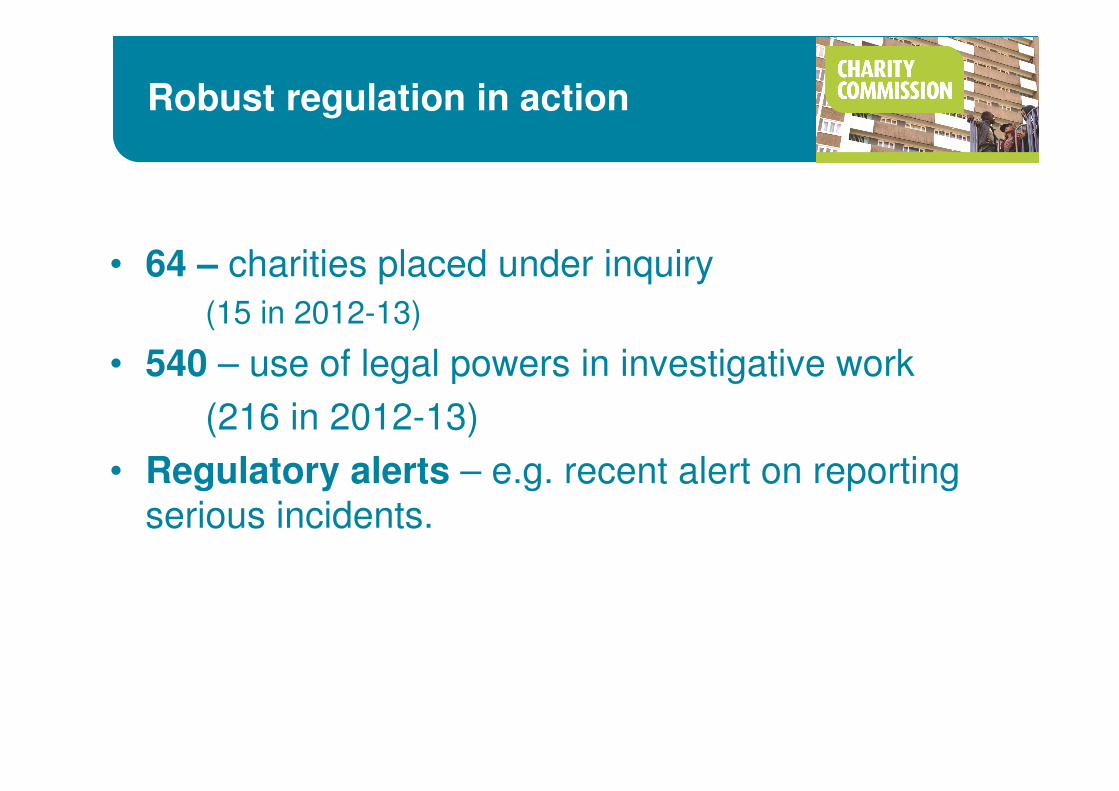

Robust regulation in action

• 64 – charities placed under inquiry

(15 in 2012-13)

• 540 – use of legal powers in investigative work

(216 in 2012-13)

• Regulatory alerts – e.g. recent alert on reporting

serious incidents.

More proactive approach

Operations / registrations

• New operations monitoring team

• 318 referrals, including 89 from registrations (between October 2013 & April 2014)

Accounts monitoring

• Casework related and themed accounts reviews

• 1,664 sets of accounts reviewed

Smarter, more focused guidance

• Clearer focus on expectations of trustees

• E.g. new Conflicts of Interest guidance

Greater transparency

Greater openness about statutory inquiries

• announcing inquiries when its in the public interest

• marking open inquiries against charities’ online entry

Reports of operational cases

New online charity search tool

• more information about charities

• easier to access from mobile devices

What we need to do now…

Risk • Better use of data

• Targeting work where it makes greatest impact

• Supporting increasingly proactive approach to case work

Digitisation • Digitising front-end services

• Streamlining low risk customer-facing services = recognising

charities are our customers

Structure • Recruiting 5-strong senior management team

• Skills and talent management agenda

Over to you…

What can you do to promote

public trust in charity?

Show integrity

Have trustees:

• acted within their powers?

• acted in good faith and only in interests of charity?

• adequately informed themselves?

• taken into account all relevant factors, disregarded

irrelevant factors?

• managed conflicts of interest?

• made decisions within range of decisions that

reasonable trustee body would make?

Be accountable

It is important that charities provide the public with information about how they spend their money

How accountable are charities?

86% charities filed annual returns on time

86% charities filed annual accounts on time

99% of sector income accounted for

= over all compliance is high… but:

58 charities have been subject to double

defaulters class inquiry

£47m of charitable funds now accounted for

Report serious incidents

1,280 serious incidents reported in 2013-14

> 580 reports so far this year

= huge underreporting by charities

Serious incidents include:

• fraud, theft, significant loss

• abuse of beneficiaries

• financial links to banned group

• Investigation by another regulator

= actual or suspected

Final thought…

Charities play an essential and

important role in society

Mismanagement in the Administration of a Charity

Practical Examples of when an Interim

Manager had been appointed and the actions

that might be taken

BRIAN JOHNSON

� Busy people with good intentions and good causes

� Rapid growth and the need for time and skills resource

� Resource deficiency leading to shortcuts

� Leading to:

– governance failings;

– risk management short-comings;

– Late filing of statutory documents; and

– Value for money reduction.

Mismanagement in the Administration of a Charity

36

Mismanagement in the Administration of a Charity

� Practical examples of governance failings

– charity acting outside of its constitution;

– proper meetings not being held;

– conflicts of interests;

• Trading subsidiaries

– acting reasonably;

– trustee remuneration; and

– Statutory documents not being

filed on time.

37

Mismanagement in the Administration of a Charity

� Practical examples of risk management failings

– Entering into agreements without professional advice;

– Failing to keep a risk register;

– Controls, cash and fraud;

– Brand management;

– Trading and losses;

– Ensuring proper security is in place;

– Restricted funds;

– Insuring activities properly; and

– Ensuring the charity is meeting its

objects.

38

Mismanagement in the Administration of a Charity

� Examples of when value for monetary considerations have

been neglected:

– Not tendering properly;

– Not reviewing on-going contracts;

– Tax and corporate structures;

– Effective advertising and brand maintenance;

– All costs incurred are in pursuance of the

charity’s objects; and

– Capital expenditure and infrastructure

programs are kept under control.

39

Mismanagement in the Administration of a Charity

� Professional advice;

– Auditors;

– Corporate structures and SPVs;

– Tax;

– Legal support;

• Employment;

• Health & Safety;

• Environment;

• Contractual and fundraising; and

– Charity Commission guidance

40

Mismanagement in the Administration of a Charity

41