confidential – all rights reserved – ernst & young llp 2005 brian boyle – ernst &...

TRANSCRIPT

Confidential – All rights reserved – Ernst & Young LLP 2005

TE

Brian Boyle – Ernst & YoungBrian Boyle – Ernst & Young PRMIA Panel Discussion: Basel II Update PRMIA Panel Discussion: Basel II Update

September 26, 2005September 26, 2005

2 TConfidential – All rights reserved – Ernst & Young LLP 2005

AgendaAgenda

Basel Refresher

Basel II Regulatory Landscape

Basel II Timeline

Remaining Open Issues

Current State of Industry

Basel II: Other Challenges

3 TConfidential – All rights reserved – Ernst & Young LLP 2005

Brief HistoryBrief History

1988 Basel Accord: G-10 central banks agree to apply common minimum capital standards to banking industries

Basel I not applied directly but through national or transnational rules (U.S.: Capital Adequacy Guidelines, EU directive: CAD or Capital Adequacy Directive)

Basel I now applied to virtually all countries with internationally active banks (approx. 100 countries)

1996: Market Risk Amendment

2001: First Consultative Paper

June 2004: “International Convergence of Capital Measurement and Capital Standards: a Revised Framework”

4 TConfidential – All rights reserved – Ernst & Young LLP 2005

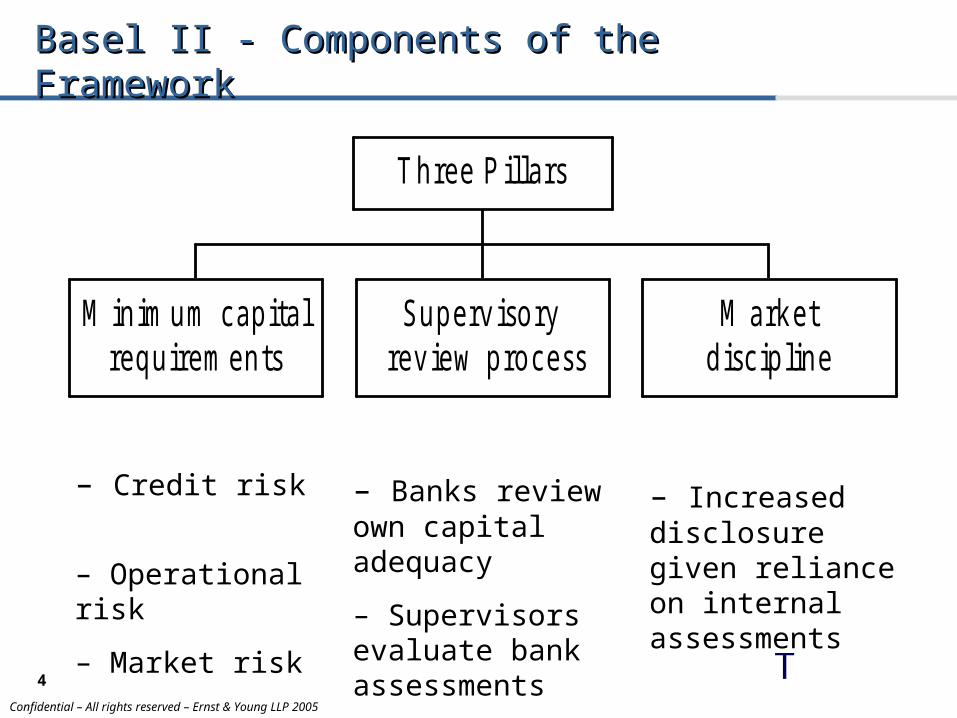

Basel II - Components of the FrameworkBasel II - Components of the Framework

M inimum capita lrequirements

Supervisory review process

M arketdisc ipline

Three P illa rs

– Credit risk

– Operational risk

– Market risk

– Banks review own capital adequacy

– Supervisors evaluate bank assessments

– Increased disclosure given reliance on internal assessments

5 TConfidential – All rights reserved – Ernst & Young LLP 2005

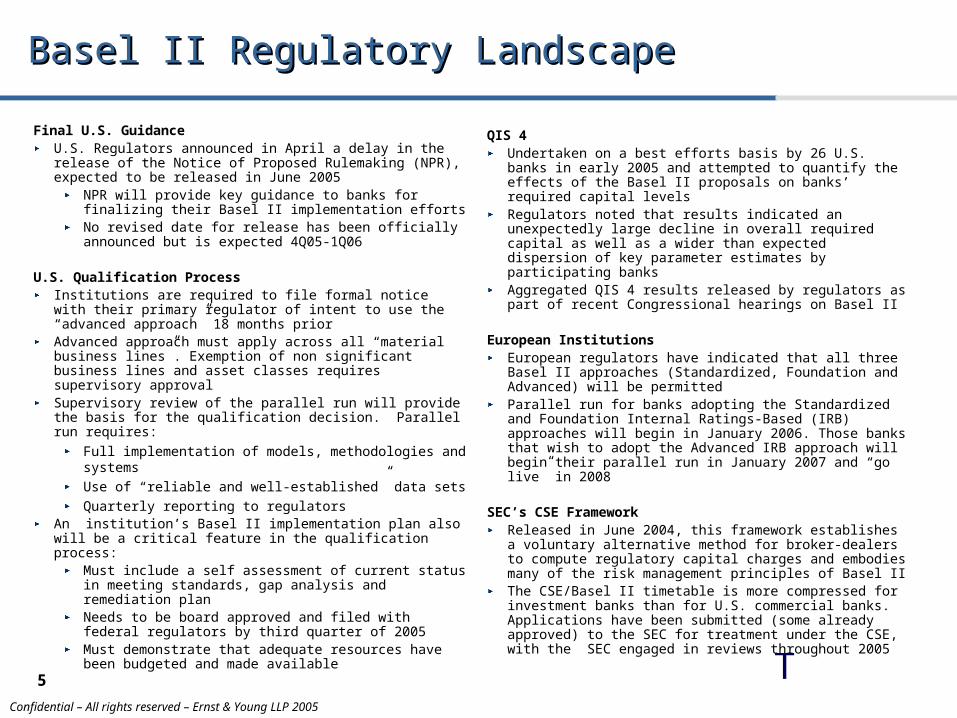

Basel II Regulatory LandscapeBasel II Regulatory Landscape

QIS 4Undertaken on a best efforts basis by 26 U.S. banks in early 2005 and attempted to quantify the effects of the Basel II proposals on banks’ required capital levelsRegulators noted that results indicated an unexpectedly large decline in overall required capital as well as a wider than expected dispersion of key parameter estimates by participating banksAggregated QIS 4 results released by regulators as part of recent Congressional hearings on Basel II

European Institutions European regulators have indicated that all three Basel II approaches (Standardized, Foundation and Advanced) will be permittedParallel run for banks adopting the Standardized and Foundation Internal Ratings-Based (IRB) approaches will begin in January 2006. Those banks that wish to adopt the Advanced IRB approach will begin their parallel run in January 2007 and “go live” in 2008

SEC’s CSE FrameworkReleased in June 2004, this framework establishes a voluntary alternative method for broker-dealers to compute regulatory capital charges and embodies many of the risk management principles of Basel IIThe CSE/Basel II timetable is more compressed for investment banks than for U.S. commercial banks. Applications have been submitted (some already approved) to the SEC for treatment under the CSE, with the SEC engaged in reviews throughout 2005

Final U.S. GuidanceU.S. Regulators announced in April a delay in the release of the Notice of Proposed Rulemaking (NPR), expected to be released in June 2005

NPR will provide key guidance to banks for finalizing their Basel II implementation effortsNo revised date for release has been officially announced but is expected 4Q05-1Q06

U.S. Qualification ProcessInstitutions are required to file formal notice with their primary regulator of intent to use the “advanced approach” 18 months priorAdvanced approach must apply across all “material business lines”. Exemption of non significant business lines and asset classes requires supervisory approvalSupervisory review of the parallel run will provide the basis for the qualification decision. Parallel run requires:

Full implementation of models, methodologies and systemsUse of “reliable and well-established” data setsQuarterly reporting to regulators

An institution’s Basel II implementation plan also will be a critical feature in the qualification process:

Must include a self assessment of current status in meeting standards, gap analysis and remediation planNeeds to be board approved and filed with federal regulators by third quarter of 2005Must demonstrate that adequate resources have been budgeted and made available

6 TConfidential – All rights reserved – Ernst & Young LLP 2005

Implementation TimelineImplementation Timeline

A-IRB transition period EU & UK Timeline for

Financial Institutions

2004 2005 2006 2007 2008 2009

Go live A-IRB EC first reading

of RBCD

Parallel run

FSA’s CP 05/03 published

Go live F-IRB & Standardized

F-IRB transition period

Implementation of ‘Equivalent’ oversight

Basel/IOSCO Working Group Report on Trading Book issues

Go live – banks

US Timeline for CSE and

Basel II 2005 2006 2007 2008 2009

Bank transition period Bank parallel run

Notice of proposed rulemaking?

Final bank rules?

Final CSE guidance

2004

Go live – I banks

I-bank parallel run

QIS 5

QIS 4

7 TConfidential – All rights reserved – Ernst & Young LLP 2005

Remaining Open IssuesRemaining Open Issues

Implementation Timing in U.S.

Basel II implementation timetable called into question with the announced delay in the release of the NPR U.S. regulators are expected to impose a 6- to 12-month “parallel processing” requirement for the advanced credit, market and operational regulatory capital methodologies that will drive consolidated U.S. reporting under Basel IICurrent indications are that the required parallel processing period will begin between January 1, 2007 and July 1, 2007 and end with live processing on January 1, 2008

Home/Host Responsibilities

Basel II will not lead to a flawlessly consistent banking framework due to legal and market differences across jurisdictions. Firms may be subject to redundant and uncoordinated reviews by multiple regulatory jurisdictionsThe Basel Accord Implementation Group group has developed a dozen case studies for supervisors using live examples

8 TConfidential – All rights reserved – Ernst & Young LLP 2005

Current State of IndustryCurrent State of Industry

General

Regulators initially indicated that there would be 10 mandatory Basel II banks in the U.S. - due to merger activity, this number has dropped to 7 mandatory banks. However, many opt-in banks are beginning to make firmer commitments to Basel IIMandatory and opt-in firms have developed baseline implementation plans and established a Basel II program management structure. These firms are now focused on meeting US qualification requirements

Current state assessmentGap analysisRemediation plans

U.S. regulators are beginning on-site visits, focusing on overall Basel II preparednessU.S. firms are responding to requests for information from host supervisorsFirms are examining ways to link regulatory initiatives -- SOX, ORM, Compliance -- to drive cost efficiencies

Credit RiskImplementation of dual ratings assignment and quantification methodologies for wholesale exposuresRefinement of segmentation framework and parameter estimates quantification methodology for retail exposuresEnhancement of internal controls related to model/process validation and Board and senior management oversightBuild/augmentation of data warehouse capabilities to collect historical default and loss data for credit portfolios, and input data for rating assignment modelsBuilding risk weighted asset calculatorEnhancement of systems for internal reporting and public disclosureFocus on the integration of risk and finance data

Operational RiskReview of operational risk management framework and organizational structuresInstitutionalization of loss data collection processes, normalizing external dataRefocus on self assessment process, key indicators and risk reportingAssessment of first iteration of operational risk quantification modelsReview of economic capital calculation and allocation process

9 TConfidential – All rights reserved – Ernst & Young LLP 2005

Basel II: Other ChallengesBasel II: Other Challenges

Level and Diverse Playing Field

Consistency between Accounting Standards

and Basel II

Bifurcated approach to Basel II in the US may result in added complexity and cost for foreign banks that elect to use the foundation approach in their home country

One year head start, in terms of reduced regulatory capital, for firms using the standardized and foundation approach (2007 start) compared to firms using the advanced approaches (2008 start)

The Fed is studying Basel II effects on competitiveness of processing banks, mortgages, small business lending, consolidation and credit card lending

Inconsistency in definitions between US GAAP and IAS accounting standards and Basel II. Conflicting definitions could lead to multiple sets of data and reporting requirements

Key areas of overlap are definitions of default and impairment, trading book and valuation of exposures, disclosures, and capital management

Loss Given Default Stress Testing

Banks that adopt the advanced IRB approach will need to consider stress scenarios (economic downturns) in estimates of Loss Given Default

10 TConfidential – All rights reserved – Ernst & Young LLP 2005

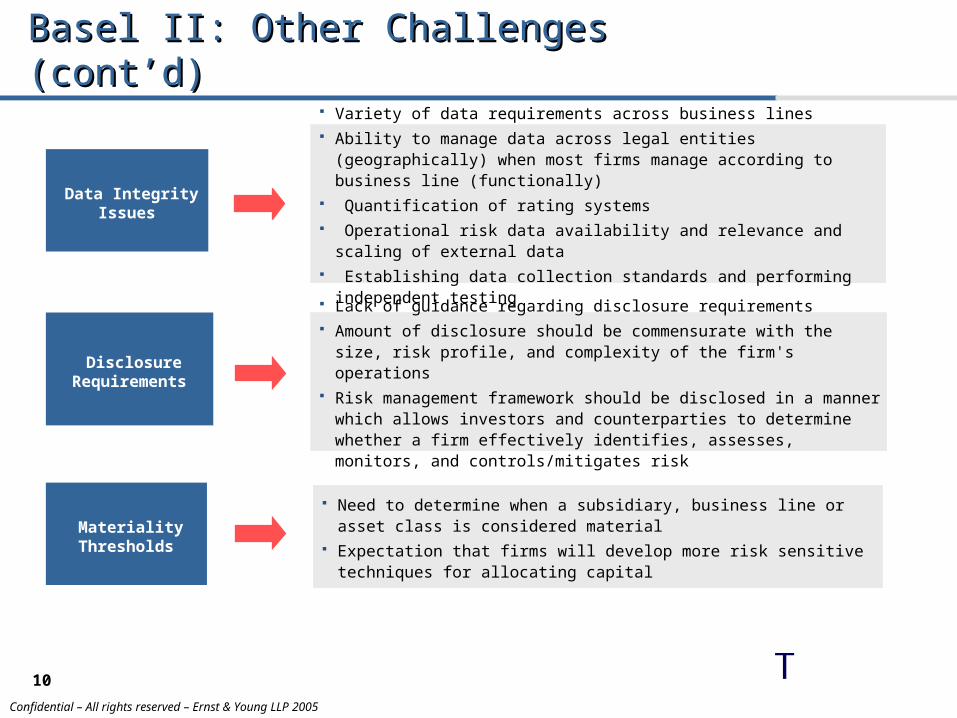

Disclosure Requirements

Lack of guidance regarding disclosure requirements Amount of disclosure should be commensurate with the size, risk profile, and complexity of

the firm's operations Risk management framework should be disclosed in a manner which allows investors and

counterparties to determine whether a firm effectively identifies, assesses, monitors, and controls/mitigates risk

Data Integrity Issues

Variety of data requirements across business lines Ability to manage data across legal entities (geographically) when most firms manage

according to business line (functionally) Quantification of rating systems Operational risk data availability and relevance and scaling of external data Establishing data collection standards and performing independent testing

Materiality Thresholds Need to determine when a subsidiary, business line or asset class is considered material Expectation that firms will develop more risk sensitive techniques for allocating capital

Basel II: Other Challenges (cont’d)Basel II: Other Challenges (cont’d)

11 TConfidential – All rights reserved – Ernst & Young LLP 2005

Contact InformationContact Information

Brian J. BoyleManagerErnst & Young LLP

[email protected](212) 773-7282

Confidential – All rights reserved – Ernst & Young LLP 2005

TETEwww.ey.com

© 2005 Ernst & Young LLP.

All Rights Reserved.

Ernst & Young is a registered trademark.