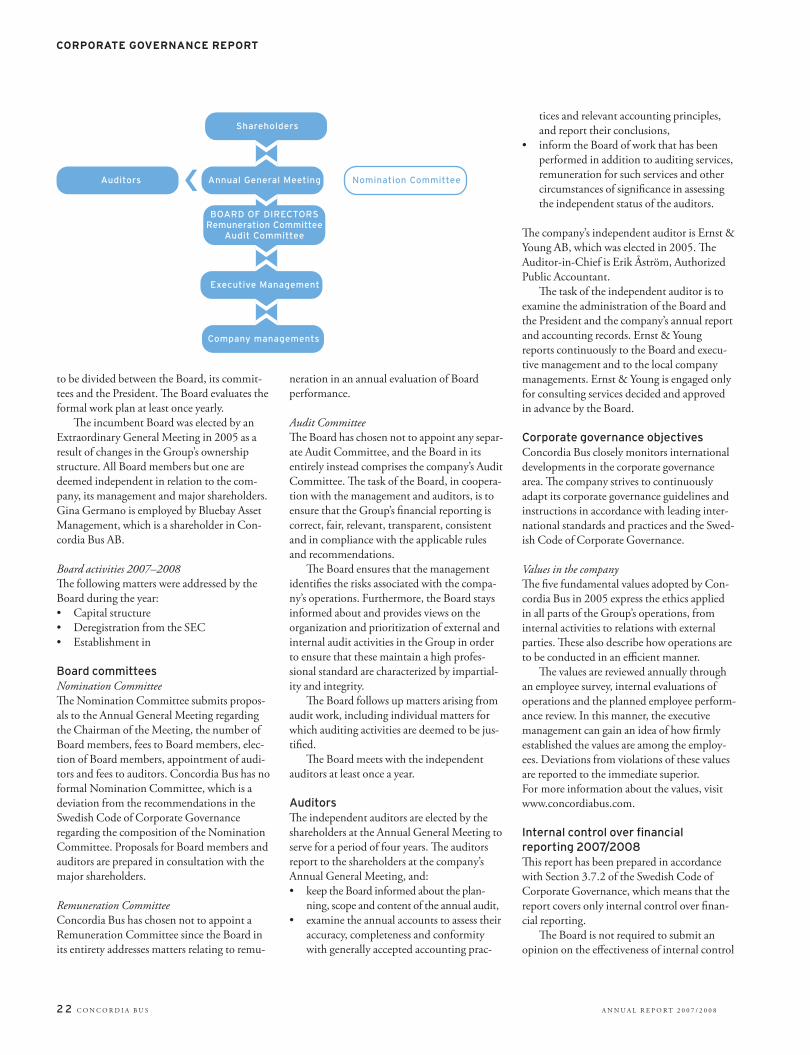

concordia bus annual report 2007/2008 -...

TRANSCRIPT

CONCORDIA BUS ANNUAL REPORT 2007/2008^

KAPITEL02 Presenting Concordia Bus 04 Statement from the CEO 06 Vision, mission, goals and strategies 08 Market 12 Swebus 14 Concordia

Bus Finland 15 Concordia Bus Norway 16 Swebus Express 17 Concordia Bus Fleet 18 Sustainability 20 Management systems and share

data 21 Corporate governance 24 Board of Directors 25 Executive Management 26 Administration report 29 Consolidated income state-

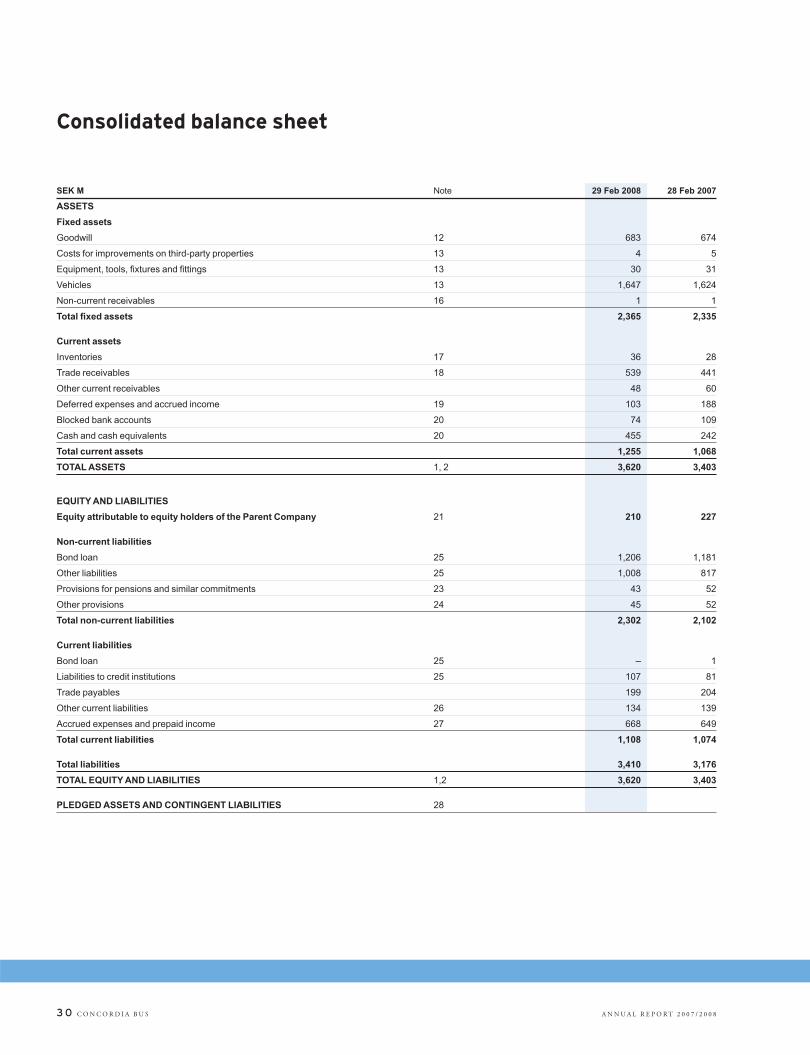

ment 30 Consolidated balance sheet 31 Consolidated statement of changes in equity 32 Consolidated cash flow statement 33 Parent

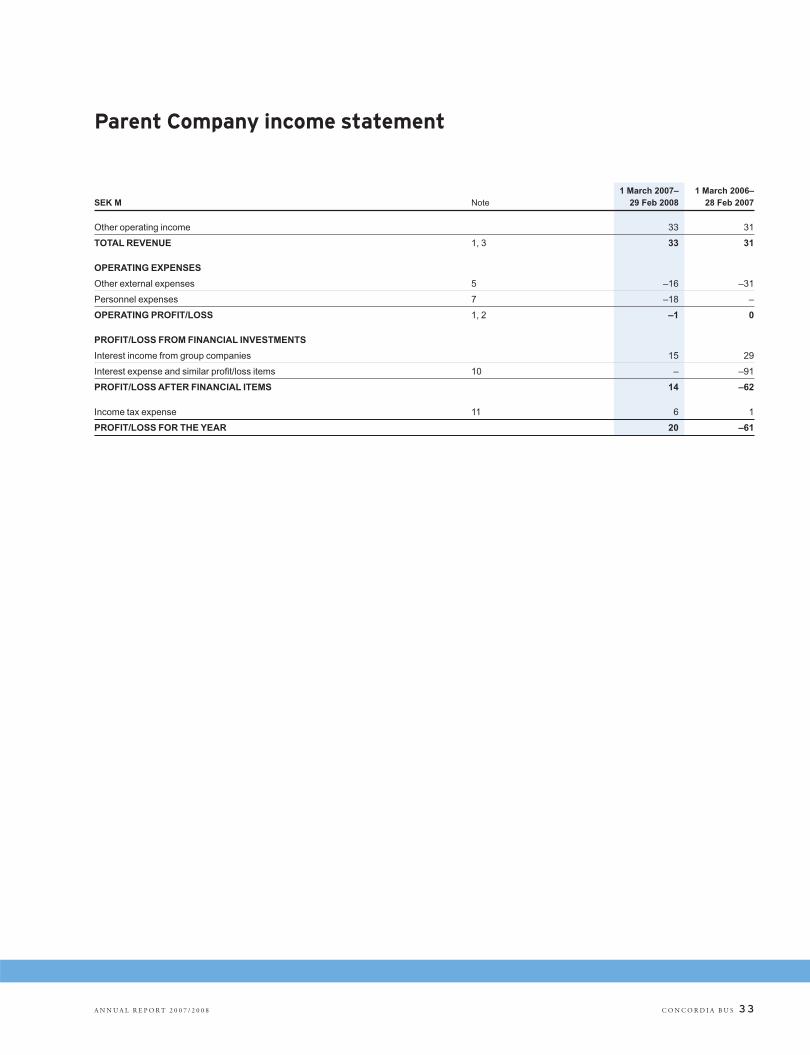

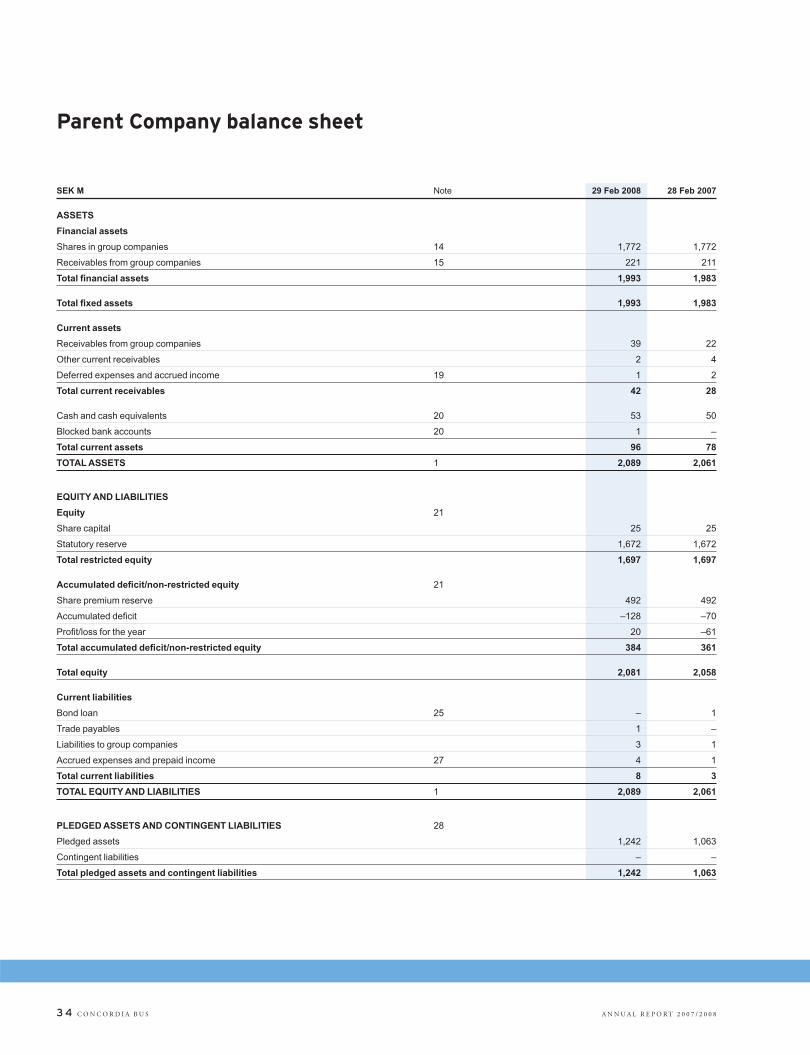

Company income statement 34 Parent Company balance sheet 35 Parent Company statement of changes in equity 36 Parent Company

cash flow statement 37 Notes 58 Audit report 59 Addresses, Glossary and Definitions 60 Historical overview

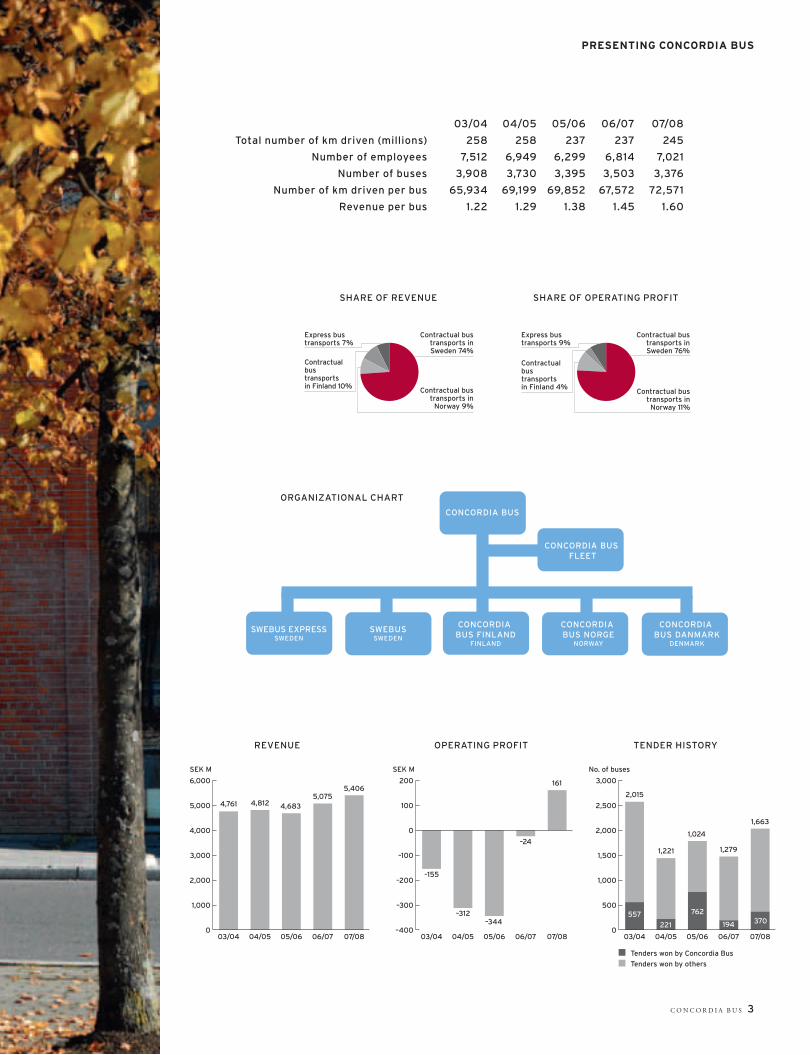

KEY FINANCIAL RATIOS SEK M, unless otherwise stated 03/04* 04/05* 05/06** 06/07** 07/08**

Revenue 4,761 4,812 4,683 5,075 5,406Operating profit –155 –312 –344 –24 161

Profit after net financial items –463 –562 –794 –246 –16Profit after tax –409 –560 –795 –245 –15

Cash flow for the year 149 –169 2 117 211Cash and cash equivalents*** 346 175 231 351 529

Equity/assets ratio, % –9.7 –31.1 –0.6 6.7 5.7Equity –330 –873 –17 227 210

Equity per ordinary share –66 –174.6 –0.85 11.35 10.50* According to Annual Accounting Act

** According to IFRS*** Cash and cash equivalents include

blocked bank accounts.

KAPITEL

CONCORDIA BUS’S VALUES We keep our promises to customers We respect our employees – and earn their respect in return

We value good leadership We have integrity We are committed to quality

^^ ^^

CONCORDIA BUS WON ITS FIRST TRANSPORT CONTRACT

IN DENMARK, EFFECTIVE FROM AUTUMN 2008.

REVENUE FROM LONG-DISTANCE BUS TRANSPORT SERVICES AMOUNTED TO SEK 351 MILLION (365).

OPERATING PROFIT WAS SEK 19 MILLION (10).

REVENUE FROM CONTRACTUAL BUS TRANSPORT SERVICES IN NORWAY TOTALLED SEK 463

MILLION (443). OPERATING PROFITWAS SEK 23 MILLION (19).

REVENUE FROM CONTRACTUALBUS TRANSPORT SERVICES IN

FINLAND REACHED SEK 517 MILLION (409). OPERATING PROFIT

WAS SEK 9 MILLION (–9).

REVENUE FROM CONTRACTUAL BUS

TRANSPORT SERVICES INSWEDEN AMOUNTED TO

SEK 3,990 MILLION (3,668).OPERATING PROFIT WAS

SEK 153 MILLION (7).

REVENUE IN THE CONCORDIA BUS GROUP ROSE TO

SEK 5,406 MILLION (5,075).

FOR 2007 THE CONCORDIA BUSGROUP REPORTED AN

OPERATING PROFIT OF SEK 161 MILLION (–24).

THE CONCORDIA BUS GROUP WON CONTRACTS FOR 370 BUSES (194)

IN THE YEAR’S TENDERS

^

IN 2007 THE GROUP PURCHASED 133 BUSES (377)FOR A TOTAL OF SEK 306 MILLION (931)

UNDER FINANCE LEASES.

2 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

Presenting Concordia Bus

. ..

.Sweden

Market leader. Swebus has 103 bus

transport contracts and 200 million

passengers in a market worth SEK 12

billion, of which 90% is deregulated.

Challenging car transports.

Norway

Top three. Concordia Bus Norway

has 8 bus transport contracts and 11

million passengers in a rapidly dereg-

ulating market worth SEK 11 bil-

lion. Around 30% of bus services are

competitively tendered. Challenging

car transports.

Finland

Top three. Concordia Bus Finland

has 45 bus transport contracts and

31 million passengers in a market

worth SEK 5 billion that is under-

going gradual deregulation. Approx-

imately 47% of bus services are com-

petitively tendered. Challenging car

transports.

Denmark

New operator. As of 2008, start of

the fi rst bus transport contract in a

fully competitive market worth SEK

6 billion. Challenging car transports.

LONG-DISTANCE TRAFFIC

Market leader. Swebus Express has

2.2 million passengers on 30 long-

distance bus lines. Challenging car,

air and rail transports.

BUS FLEET MANAGEMENT

Th e only Nordic specialist company.

Concordia Bus Fleet Group optim-

izes purchasing, management and

sales of the approximately 3,400

buses in the Group’s fl eet.

CONTRACTUAL BUS TRANSPORT SERVICES

C O N C O R D I A B U S 3

CONCORDIA BUS

CONCORDIA BUS FLEET

SWEBUS EXPRESSSWEDEN

SWEBUSSWEDEN

CONCORDIA BUS FINLAND

FINLAND

CONCORDIA BUS NORGE

NORWAY

CONCORDIA BUS DANMARK

DENMARK

ORGANIZATIONAL CHART

0

1,000

2,000

3,000

4,000

5,000

6,000

07/0806/0705/0604/0503/04

4,761

SEK M

4,812 4,6835,075

5,406

REVENUE OPERATING PROFIT TENDER HISTORY

PRESENTING CONCORDIA BUS

03/04 04/05 05/06 06/07 07/08

Total number of km driven (millions) 258 258 237 237 245

Number of employees 7,512 6,949 6,299 6,814 7,021

Number of buses 3,908 3,730 3,395 3,503 3,376

Number of km driven per bus 65,934 69,199 69,852 67,572 72,571

Revenue per bus 1.22 1.29 1.38 1.45 1.60

SHARE OF REVENUE SHARE OF OPERATING PROFIT

Contractual bustransports inSweden 74%

Contractual bustransports in

Norway 9%

Express bus transports 7%

Contractual bus transports in Finland 10%

Contractual bustransports inSweden 76%

Contractual bustransports in

Norway 11%

Express bus transports 9%

Contractual bus transports in Finland 4%

–400

–300

–200

–100

0

100

200

07/0806/0705/0604/0503/04

–155

SEK M

–312–344

–24

161

0

500

1,000

1,500

2,000

2,500

3,000

07/0806/0705/0604/0503/04

557

2,015

No. of buses

1,221

221

1,024

762

1,279

194

1,663

370

Tenders won by Concordia BusTenders won by others

4 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

Earnings aided by resource-effi ciency and quality

Th e outlook for public bus transports is

bright. Already the most common mode of

public transport, it is growing steadily and

appears to be approaching a major modern

breakthrough. As municipalities and county

councils invest in their infrastructure, quality

aspects are slowly but surely gaining more

attention.

Th e future also looks promising for Con-

cordia Bus. Th e customers rely on our ser-

vices and we are gradually enhancing both

our products and our ability to do more with

less. Improved resource-effi ciency is one of

the main drivers behind our rapid earnings

growth, which is unparalleled in the industry.

Earnings up by more than SEK 200 million Concordia Bus delivered a fi nancial result

that is fully on par with the promised growth.

In the span of two years, we have improved

our operating result by a half million Swedish

kronor. Th e year’s increase was approximately

SEK 200 million, enabling the company to

post its fi rst-ever operating profi t.

An internal dialogue about the factors

that create success in our industry lies behind

the transformation of Concordia Bus. Every

day, I meet inspired employees that can serve

as role models for all of us in the company.

At each and every depot there are traffi c

supervisors, bus drivers, traffi c planners and

other staff who together give our customers

and clients the highest measured quality in

the industry. Th ey love their jobs and are

dedicated to doing them well. I am proud of

everything they have achieved and share their

sense of commitment.

The right transport services at the right cost I am very satisfi ed with the fi nancial develop-

ment and am convinced that there is still a

great deal more this company can accom-

plish. We have already taken several steps

along the way to creating even better bus

transports throughout the Nordic region and

a still more resource-effi cient and credible

Concordia Bus.

A provider of road transport services

stands or falls with its ability to develop and

deliver the services customers want at a price

that covers the related costs and provides a

STATEMENT FROM THE CEO

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 5

reasonable surplus. However, the existence of

a predefi ned transport network limits our

freedom to defi ne the product we deliver,

and means that good planning and resource-

effi ciency are decisive in meeting the set targets.

Th e perspective is almost ecological – we

should never use more resources than we

need. Th e point is not to expend more eff ort,

but to do everything more effi ciently than we

did yesterday and more effi ciently than our

competitors today.

I believe that the realignment of Concordia

Bus into a process-driven company was a

turning point. By measuring ourselves against

a set of carefully defi ned performance indic-

ators and making use of benchmarking, we

have been able to enhance our quality while

at the same time signifi cantly strengthening

our earnings.

Stealing market share from carsWe are not challenging the railways and have

no dispute with other providers of road trans-

port services, whether they operate in the

open market or enjoy the protection of a

granted concession. It is cars we all want to

steal market shares from, the thoughtless rec-

reational motorists and private automobiles

that day after day drive to and from work car-

rying only a driver. We are committed to

increasing the use of public transport for the

benefi t of the taxpayers and the environment,

as much as for our own sake.

A modern bus requires fewer than four

passengers to be an environmentally superior

alterative to the automobile. And even greater

environmental gains are possible by increas-

ing the number of passengers on the buses.

We and other major transport providers

are working strenuously to minimize environ-

mentally hazardous emissions and reduce

the use of fossil fuels. Th ese eff orts have been

successful and our long-term ambition at

Concordia Bus is to reach a point where our

operations are climate- and eco-neutral. In

the meantime, increased ridership on our

buses nonetheless has a faster and greater

eff ect without any cost to the county trans-

port authorities or the taxpayers.

Here, there is a natural affi nity of interests

between all players in the public transport

sector, whether clients or contractors. If we

and other operators are given better scope to

off er transport services that are truly customer-

driven, we can fi nally create the product

needed by society today and in the future.

Incentive agreements are the key Overly detailed tender documents that specify

not only the needs to be satisfi ed but also how

this is to take place are an everyday burden

for public transport operators. And when the

amount of compensation is also fi xed and

regulated on the basis of production, the

situation is further aggravated. Despite this,

so-called gross cost contracts have become

even more common than before. An already

shackled transport operator is left without

any incentive whatsoever to increase the

number of passengers or improve their satis-

faction.

Concordia Bus advocates wider use of

incentive agreements in the public transport

sector. It must be profi table for all parties

when the operator does everything right.

Higher quality transports that lead to more

passengers on the buses and lower environ-

mental impact should provide scope to sup-

plement the operator’s fi xed compensation

with a variable component based on ticket

revenues.

Our own profi tability is now stable and

expected to strengthen further. We have

proven our ability to calculate, win and

deliver on contracts better than most. Th e

internal risks are low, but there are external

risks that are beyond Concordia Bus’s con-

trol, particularly the price of fuel, environ-

mental requirements and access to qualifi ed

manpower.

I have already spoken of the company’s

many dedicated managers and employees,

but I am well aware that our employee pro-

grams have not yet reached all the way out to

the front lines where supervisor meets driver

and driver meets customer. Th e transport

contracts of the future require employees who

know what is expected of us all and can easily

follow up their performance. Th is is where we

are headed.

Ragnar Norbäck

President & CEO

STATEMENT FROM THE CEO

6 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

Customer experience in focus

VISION, MISSION, GOALS AND STRATEGIES

The customer experience is at the core of Concordia Bus’s business. By realizing its objectives for perceived quality, the company can also meet its operating and fi nancial goals.

In the Nordic region there is a rising need,

and demand, for public transport. Competi-

tion for previously protected transport ser-

vices is contributing to growth in the dereg-

ulated segment of the market.

Concordia Bus is active exclusively in

road transport services, above all through

transport contracts awarded by public sector

agencies. Since the compensation payable

under these transport contracts is largely

fi xed, Concordia Bus is working to boost the

share of controllable revenue. A change of

this type raises the operator’s risk and respons-

ibility for encouraging customers to increase

their use of transport services.

Long-term goalsConcordia Bus sets goals in three diff erent

categories: Market goals, operating goals and

fi nancial goals. To reach each and every one

of these goals, the company has formulated a

number of diff erent strategies.

Market goals

• More than 80% satisfi ed customers.

• Market leader in selected segments of the

Nordic region and among the top three in

all four countries.

• More than one third of all scheduled road

transport services in the Nordic region.

• Highest quality rating among leading

public transport operators from the Insti-

tute for Quality Development, SIQ.

• Highest credibility among the clients.

Operating goals

• Motivated Employee Index of more than

80.

• Climate-neutral.

• Fewer than 1 personal injury per a

distance equal to 100 times the earth’s

circumference.

Financial goals

• Profi t margin of 3–5%.

• Return on capital employed of at least 10%.

• Return on equity of at least 15%.

• Equity/assets ratio of 25%.

• Cash fl ow that covers investment needs

and shareholder dividends.

StrategiesTh e strategies are divided into fi ve diff erent

areas: growth, market effi ciency, structure,

resource management and employee develop-

ment.

An increased undertaking in the local

transport service contracts is a key compon-

ent not only of Concordia Bus’s growth

ambitions but also for development in other

prioritized strategic areas. Th e company seeks

greater responsibility for the service off ering,

timetable and sales, as well as compensation

for both the provision of transport services

and the number of passengers. Concordia

Bus aims to grow both organically and

through increased penetration of existing

markets, but also via product diversifi cation

and by playing an active role in the anticip-

ated consolidation of the market.

Market effi ciency will be improved

through new transport solutions, ongoing

productifi cation, improved tender prepara-

tion, careful contract management and active

communication. A new communication plat-

form was launched in the past year and a new

graphic identity will be introduced in the

year ahead.

In every geographical market, Concordia

Bus strives to promote the existence of strong

industry organizations. Strategic partnerships

accelerate the company’s own pace of develop-

ment and assessment of the company’s fi nan-

cial and corporate structure satisfi es other

primarily fi nancial goals.

Because resource management is of cen-

tral importance to Concordia Bus and is a

critical competitive strength, the related strat-

egies cover a number of diff erent initiatives.

Resource optimization through fl eet manage-

ment, continuous development of the com-

pany’s already market-leading expertise in

traffi c planning and evaluation of the group-

wide services are a few strategic priorities in

the resource management area. Safety issues

also belong to this category, as do the increas-

ingly urgent and prioritized environmental

activities. However, process control and

benchmarking of effi ciency and performance

have the greatest impact of all.

Motivated employees are needed in every

part of the company’s operations, where the

shared values serve as a foundation for the

creation of a professional culture. Th e com-

pany encourages employee commitment and

strives to systematically utilize this commit-

ment and provide individual feedback on

work performance. Powers and responsibili-

ties must be absolutely clear and the decision-

making processes eff ective. Managers are

developed in accordance with established

leadership criteria and each employee is given

opportunities for personal development

through at least one yearly evaluation to-

gether with his or her manager and matching

of skills to work duties. Th e bus drivers are

trained in a way that refl ects the company’s

obligations to its customers and Concordia

Bus strives to be perceived as the industry’s

most attractive employer.

Increase in uniform working methodsTo realize the vision “Everyone wants to

travel with us” and achieve its goals, the com-

pany focuses on continuous improvement of

its working methods through benchmarking.

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 7

VISION, MISSION, GOALS AND STRATEGIES

In this context, customer-perceived quality is

the single most important factor and motivated

employees are vital for long-term success.

Concordia Bus has fi ve basic shared val-

ues that steer development of the company’s

working methods: Credibility, mutual

respect, good leadership, integrity and qual-

ity. Th ese values provide a platform not only

for the company’s day-to-day operations, but

also its strategies, goals and even its vision.

Better solutions through process controlTh e shared values also create a framework for

process control and a growing number of

group-wide working methods in production,

accounting, fi nance and administration.

Group-wide working methods are of major

importance, above all for quality manage-

ment and resource-effi ciency.

25 carefully selected performance indic-

ators make it possible to identify the areas

where the company is performing most suc-

cessfully. 17 interdisciplinary process teams

that involve 120 employees in nine main pro-

cesses evaluate alternative methods for

enhancing quality in everything the company

does. Each team is headed by a president or

member of the Executive Management.

When a routine is created or changed, the

results are documented and added to the

continuously revised and updated collection

of group-wide rules and routines known as

Policies & Instructions.

Successful benchmarking has enabled

recent years’ improvements in contract starts

and wind-ups, implementation of in-house

customer surveys and development of the

Green Journey pilot project.

In the past two years the share of group-

wide working methods has grown dramatic-

ally and now makes up around 25% of all

identifi ed processes, a share that is expected

to grow further.

VALUESFive shared values define the ethics applied in all parts of the Group’s operations, from internal activities to relations with external parties. They also describe how the company strives to conduct its activities in an efficient manner. Through sys-tematic monitoring, the management can deter-mine how firmly established the values are throughout the company.

WE KEEP OUR PROMISES TO THE CUSTOMERSOur customers see us as credible. The informa-tion we provide is perceived as timely and suffi-cient in scope. Our commitments are long term.

WE RESPECT OUR EMPLOYEES – AND EARN THEIR RESPECT IN RETURNOur company stands for equal treatment of all employees. Together we create a secure and con-genial working environment that stimulates initia-tive and ideas for improvement. We encourage health and development, and recognize achieve-ment. We react to a lack of respect towards to company and its employees.

WE VALUE GOOD LEADERSHIPWe have well defined leadership criteria. Our managers place the interests of our customers and the company first. We promote cooperation across borders and provide feedback on work performance. We can be trusted with confidences.

WE HAVE INTEGRITYAt Concordia Bus we comply with the applicable laws, rules and industry standards. We take our responsibility for the environment and society. Our relationships with business partners are characterized by mutual respect.

WE ARE COMMITTED TO QUALITYWe deliver results. Our services maintain the promised level of quality as a minimum require-ment. We use systematic follow-up and develop-ment of operations to ensure lasting correction of errors and deviations.

APPRECIATED The customers enjoy accessibi-lity, reliability and courteous service. The public transport authorities recognize the value of Concordia Bus’s advice. The drivers represent Concordia Bus’s approach to good custo-mer relations.

CREDIBLE Concordia Bus keeps its promi-ses, maintains a high level of safety and provides transport solutions that support society’s objectives for development of road transports.

RESOURCE-EFFICIENCY

Concordia Bus has a low pro-duction cost in relation to its delivered quality and offers effective solutions that also contribute to sustainable long-term development.

ROAD TRANSPORT

Concordia Bus provides scheduled transport services under contracts, in partnership or independently.

MISSION:AN APPRECIATED, CREDIBLE AND

RESOURCE-EFFICIENT PROVIDER OF ROAD TRANSPORT SERVICES

VISION: EVERYONE WANTS TO TRAVEL WITH US

^

8 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

By winning the Danish contract in 2008, Concordia Bus has made a breakthrough into a market worth approximately SEK 6 billion. This is equal to more than 20% of the entire deregulated market in the Nordic region, which is the company’s home market.

Th e public transport market in Sweden, Nor-

way, Denmark and Finland generates annual

revenue in the range of SEK 70 billion.

Scheduled bus transports account for more

than half of this total, or around SEK 40 bil-

lion, of which approximately SEK 28 billion

is tendered in open competition. Th is is Con-

cordia Bus’ market – scheduled competitively

tendered bus transport services for passengers

in the Nordic region.

With annual revenue of SEK 5.4 billion,

Concordia Bus is the largest bus transport

operator in the Nordic region and one of the

ten largest public transport companies in

Europe.

Young people the most frequent usersTh e majority of Concordia Bus’s customers

are passengers in urban traffi c. Surveys in

Sweden show that 70% of the population

uses public transport occasionally, with

women outnumbering men and young

people the most frequent users of all. Around

15% use public transport daily and an equal

share never use it. Industry surveys on cus-

tomer satisfaction among users of public bus

transports show that two of three are satisfi ed

or highly satisfi ed.

Convenience of cars still attractive 50 years have passed since the automobile

MARKET

A complex and evolving market

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 9

MARKET

POLITICIANS CUSTOMERIMAGE›

CLIENT OPERATORCONTRACT: 5–10 YEARS›

CO

ND

ITIO

NS

›

DE

LIV

ER

Y

››

IMAGE

Fee per km, hour and bus

Model for public procurement of

public transport services.

Th e rules for procurement of public bus transport services are

relatively similar in all four Nordic countries and are based on the

guidelines in the EU’s public procurements directive.

took over as favoured mode of transport in

the Nordic region. Despite eff orts by politi-

cians and transport companies, the public

transport sector’s market share has been stag-

nant at around 20% for decades. With few

exceptions, the situation is similar through-

out the EU. In other words, the foremost

competitor to bus transports by far is the car,

a costly alternative that leads to congestion

and increased environmental impact but

off ers a high level of convenience. Rail trans-

ports, with annual revenue of around SEK 7

billion in Sweden during 2006, are the domi-

nant competitor for long-distance travel.

Th e automobile is retaining or even

strengthening its grip on travellers every-

where, except for in the metropolitan areas.

For longer distances, signifi cantly more trav-

ellers choose the train than bus. Concordia

Bus’s long-distance bus transports have

focused on transports within or to and from

Sweden, and currently account for around

7% of the company’s total revenue. Revenue

in this category comes exclusively from the

individual customers, i.e. the passengers.

School bus transports are sometimes ten-

dered in connection with urban transports

and currently make up around 1.0% of oper-

ations in Concordia Bus, while transports to

and from airports account for 0.3%.

Th e Nordic public transport market gen-

erates annual revenue of around SEK 70 bil-

lion. A total of around 14,000 buses operate

in scheduled traffi c in the region. Concordia

Bus has a fl eet of 3,376 buses, down by 3.6%

compared to the end of fi scal 2006-2007.

Competition increasingPrior to 1989, public bus transport services in

the individual markets were not exposed to

competition and services were provided

under concessions that gave the operators

exclusive rights to all traffi c in a specifi c area

and to the revenue from this traffi c.

Although EU public procurement regula-

tions permit the award of concessions for an

unlimited period, today the transport author-

ities are putting nearly all contracts in both

Sweden and Denmark up for tender, while

the share is 47% in Finland and 31% in

Norway. Between 2008 and 2010 the open

market will grow substantially in Norway,

whereas development in Finland is progress-

ing more slowly.

Th e rising number of passengers is also

contributing to growth in the market. Th e

growth rate is currently highest in Sweden,

where it exceeds 5% annually. Without

exception, bus transport services in the capi-

tal city regions make up the largest single

market in each country and employ around

half of the total number of buses. In many

more sparsely populated regions, the use of

public transport is declining.

The Nordic modelTh e system for procurement and production

of public transport services is essentially the

same in the four Nordic countries.

Th e client, which is a politically

appointed public transport authority, has

overall responsibility for the provision of

public transport services in a particular

region. Today there are some 60 such author-

ities in the Nordic countries. Th e client also

decides whether to provide public transport

services under an existing concession or to

invite tenders through a public procurement.

Th is responsibility includes decision on time-

tables, ticket pricing and contract periods.

Th e diff erence between production costs and

operating revenue is covered by taxes.

Th e operator is the bus company that

provides transport services according to the

terms of the contract. Th is company can be

an international group, a small or mid-sized

privately owned company or an enterprise

owned by a municipality or county council.

Th e contract between the client and oper-

ator regulates the way in which transport ser-

vices are provided based on the terms and

conditions in the tender documents. It gener-

ally runs for a period of 5-8 years and the

operator typically receives payment on a gross

cost basis. Th e amount paid to the operator

under a gross cost contract is based solely on

the number of kilometers or hours driven,

while all ticket revenues go to the public

transport authority. A net cost contract

instead assigns the bulk of ticket revenues to

the operator. An incentive contract is a cross

between a gross cost and net cost contract,

and is based on the gross cost model but

allows the operator to increase its revenue if

the number of passengers rises. One thing all

three contract types have in common is that

the compensation is indexed over time to

refl ect changes such as rising fuel or payroll

costs.

London’s public transport system is organ-

ized according to principles similar to those

found in the Nordic countries. Areas of Eng-

land outside London are exposed to unlim-

ited competition, along the same lines as bus

freight transports in the Nordic countries.

Th e continental model for public bus trans-

port services is based on close cooperation

between the public and private sectors, which

is expressed through the guidelines for public

procurements described in EU legislation.

1 0 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

MARKET

›

Germany

CO

NT

RA

CT

PR

ICIN

G

TIME FROM START OF DEREGULATION

›

Norway

Finland

Sweden

Denmark

England

Level of compensation changes over timeContract pricing typically follows the curve

shown in the “Deregulation and pricing

cycle” diagram. Before deregulation begins in

a certain area, the level of compensation is

high. Because there is only one public trans-

port authority in each area, but often a large

number of bidders, an imbalance arises when

traffi c is tendered. In many cases, the span

between the highest and lowest bids is con-

siderable, sometimes so large that the lowest

is not even suffi cient to cover the bidder’s

costs. Regardless of the motives behind such

tactics, a gradual market correction takes

place so that the price increases over time. As

a result, the prices will fall relatively slowly

after the fi rst tender, and will then rise some-

what faster after bottoming out.

Concordia Bus believes that the market

will eventually consolidate into a small num-

ber of effi cient and quality-driven players. In

Denmark this has already taken place.

At the current price levels, ticket revenues

are not adequate to cover traffi c costs. Th e so-

called self-fi nancing ratio varies both between

countries and over time, but currently averages

at around 50–60% throughout the Nordic

region. Th e remainder is covered by tax rev-

enues. Th e degree of consolidation among

transport authorities is increasing, mainly as a

means for achieving scale economies.

Costs are rising faster than revenue, partly

as a result of surging fuel prices and a ten-

dency for transport solutions to become more

resource-intensive in the form of increased

driver time and empty transports. Due to

insuffi cient indexation in many contracts,

this cost growth is a problem for operators as

well.

SwedenNearly all scheduled public bus transports are

competitively tendered. Th e market is worth

approximately SEK 12 billion, which is

around 40% more than the second largest

Nordic market. Gothenburg, Luleå and

Västerås are the largest cities that do not con-

tract out all bus transports.

With a market share of 20% and 2,551

buses, Concordia Bus and Swebus are the

leading providers of public bus transports

tendered by county transport authorities. A

market share of over 50% makes Concordia

Bus and Swebus’s sister company Swebus

Express the leader in that small portion of

long-distance transports carried out by

express bus rather than rail. Th ese transports

and conducted on behalf of, and fully

fi nanced by, the individual customers.

Swedes are travelling more by car and by

public transport, both within and outside

Stockholm, which accounts for close to 45%

of all public transport in the country. Over

the past fi ve years, the number of trips by

public bus transport increased by around 5%.

Volumes in the underground system were

largely unchanged, while other rail-bound

traffi c rose by between 13% and 18%. Th e

underground, light rail and local trains all

had around 15% fewer passengers than the

buses.

Contracts for some 2,300 buses will be

opened for new tenders over the next three

years.

NorwayNorwegian public bus transports employ

some 7,000 buses and generate annual reve-

nue in the range of SEK 11.5 billion. Th e

share of competitively tendered transports is

growing and currently amounts to 31%,

equal to around 2,200 buses.

Concordia Bus Norway has a market

share of 17% of competitive public bus trans-

ports.

Th e market is relatively fragmented and

immature, with a large number of local oper-

ators. All international operators in the Nor-

dic region are also active in Norway. In the

coming three years, contracts for 1,835 buses

will be put to tender for the fi rst time. Th e

remaining non-competitive transports are

based on concession agreements.

FinlandTh e Finnish market for public bus transports

is worth the equivalent of SEK 5 billion. 47%

of this total, equal to approximately SEK 2.3

billion, is procured, above all through com-

petitive tendering of transports in the largest

cities of Helsinki and Turku. Th e country’s

third largest city, Tampere, has also started to

procure bus transports in open competition.

Concordia Bus Finland operates only in

the Helsinki region, where all transports are

procured in open competition. Helsinki mar-

ket is worth the equivalent of SEK 1.7 billion

and employs 1,205 buses.

Concordia Bus Finland is the market-

leader alongside the municipally-owned

Helb, while Veolia is number three. Th e com-

pany has enlarged its market share for the

third consecutive year and currently com-

mands 30% of the market, with 380 buses.

Without access to a well situated depot, the

company lacks opportunity to compete for

contracts in the Turku area where 80% of bus

transports are tendered competitively. Th e

situation is the same in the Tampere region.

Th ere are 964 buses in service outside the

three major cities, but none of these trans-

ports are tendered and no change is antici-

pated in the near future. A large share of this

traffi c consists of express buses operating

under exclusive concessions.

DenmarkIn the spring of 2008 Concordia Bus won its

fi rst tender in Denmark, a contract for 54

buses in the Copenhagen area eff ective from

the autumn of 2008.

Public bus transports in Denmark were

deregulated in the early 1990s and generate

an estimated SEK 6 billion in annual reve-

nue. All transports are competitively ten-

dered and close to half of the volume will

come up for bids within the next three years.

Th e latest measurements indicate a

decrease in use of public transport. Th e

underlying reasons are unknown, and it is

also uncertain whether this is a lasting trend.

UK-based Arriva acquired Veolia’s opera-

tions in 2007 and now operates around 1,600

buses with a market share of 52%. Keolis has

acquired 30% of Busslink (formerly SL-Bus)

in Sweden and also operates in Denmark

through City-Trafi k, which has a market

share of 9%.

DEREGULATION AND PRICING CYCLE

In Europe, only the UK has carried out more extensive

deregulation than the Nordic countries. In other parts of

Europe, most public transports are still conducted under

concessions with privately or publicly owned operators.

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 1 1

MARKNAD

ArrivaArriva is a listed British company that is

expanding outside the UK. In the Nordic

region, the company has traffi c in Sweden

and Denmark. Th e Nordic fl eet consists of

1,726 buses.

VeoliaVeolia is a listed French company that also

provides transport services on trains and

ferries. Th e company is the only operator

that has, or has had, scheduled traffi c in all

of the Nordic countries, but has now left

the Danish market. Th e fl eet consists of

1,579 buses.

Busslink/City-Trafi k/KeolisFrench Keolis is the principal owner of

Busslink, which formerly called SL-Buss

and was at that time wholly owned by

SLL. Today SLL has a holding of 30%. In

Denmark, Keolis owns the company City-

Trafi k. Th e fl eet consists of 1,613 buses.

Helb/City of HelsinkiTh e City of Helsinki’s bus company Helb

is the largest operator in the Helsinki

region and the second largest bus company

in Finland, after Koiviston Auto. Th e com-

pany has no operations outside Finland.

Th e fl eet consists of around 600 buses.

Nettbuss/NSBTh e Norwegian state railway operator

NSB own’s Norway’s largest bus company

Nettbuss. Th e company also has opera-

tions in Sweden (Orusttrafi ken, KR-trafi k

and Säffl ebussen) and Denmark. Th e fl eet

consists of 1,900 buses.

TideTide is a listed company with operations

in bus and boat transports in Norway.

Today the company is active mainly in

Bergen and Hordaland County. Th e fl eet

consists of around 1,000 buses.

Norgesbuss/Fosen/TorghattengruppenTorghattengrupen is a majority share-

holder in the listed company Fosen, which

also includes Norgesbuss. Th e corporate

group has no operations outside Norway.

Th e fl eet consists of 800 buses.

THE LARGEST OPERATORS

^

1 2 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

Customer-driven in every dimension

Managing Director Jan Bosaeus

Annual revenue SEK 4,080 million (3,778)

Market share 30% (31%)

Number of passengers 200 million (190)

Number of employees 5,514 (5,425)

Number of buses 2,551 (2,758)

Number of km driven 185 million (178)

Competitors Busslink, Veolia, Arriva,

Orusttrafiken, etc.

Website www.swebus.se

The ability to offer secure and effi cient bus transports characterized by consideration and respect for the customer at all times is decisive for Swebus’s success. As the market leader, the company welcomes the chance to take greater responsibility for developing public transport in a more customer-oriented direction.

SWEBUS

Swebus 74%

SHARE OF CONCORDIA BUS’S REVENUE

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 1 3

Swebus’s vision is to be a word-class service

company. Th e Swedish unit of the group’s

contractual transport operations develops,

sells and produces public transport services

on contract on to some 20 clients in more

than 100 locations throughout Sweden. Th e

company is the market leader in Sweden,

with responsibility for nearly one in every

three bus journeys in the country.

Increased profi tabilityTh ree years ago Swebus adopted a plan for

gradual and sustainable earnings growth, a

plan the company has succeeded in realizing.

During these three years, operating profi t has

increased by more than SEK 350 million.

Profi tability is now stable and operating

profi t for the past fi nancial year reached SEK

73 million.

Th e current profi tability is proof that

Swebus has chosen the right path. When pro-

fessionalism, effi ciency and customer satisfac-

tion all improve, this is also visible in the

fi nancial results.

Swebus was formed through a merger

between three state-owned enterprises – SJ

Buss, GDG and Postens diligenstrafi k. At the

end of fi scal 2007–2008 the company had

around 100 transport contracts and approxi-

mately 8,000 employees working full time,

part time or on a contract basis. Th e majority

of these were drivers of the approximately

2,300 buses in scheduled traffi c. Th e 25%

largest contracts generated around 75% of

transport revenues. Service, maintenance and

local management/administration are carried

out in leased facilities.

A full 98% of transport revenues come

from the clients and only 2% from passenger

ticket purchases in a few individual contracts.

It is vital to increase the share of contracts

providing the operator with both fi xed com-

pensation and variable revenue based changes

in passenger volumes. Contracts with a large

incentive component result in lower tax

fi nancing.

Consolidated market sharesBecause the largest contracts in Sweden were

not subject to new tenders in the past year,

the dominant operators’ market shares

changed only marginally. Swebus, with 30%

of the market, is larger than its two closest

competitors combined. Busslink commands

18% of the market and Veolia 12%.

In the year’s tenders, Swebus extended its

contract with Kalmar County and was

awarded a new contract for urban traffi c in

Umeå. Th e contract on Gotland, where Swe-

bus is responsible for regional transports, will

be opened to new tenders 2008. In Stock-

holm the tenders for Märsta and Ekerö were

lost. Th e company lost its contract in Jön-

köping to a competitor that submitted a very

low bid.

In 2008 contracts will be tendered for

around 700 buses and in 2009 for an addi-

tional 840. Today Swebus operates around

25% of these transports.

Working for changePrice remains the decisive factor in most

transport contract tenders. In dialogue with

the clients, Swebus is working to reduce the

focus on fi xed price contracts and improve

the scope to off er the customer- oriented

transport services that are the company’s

business mission.

Th e client typically determines the time-

table. It would benefi t the customers, and in

a longer perspective also the client and tax-

payers, if the operator were instead given

responsibility for creating a timetable that

delivers maximum benefi t for the customers

and client based on certain pre-defi ned crite-

ria. Th e results of the 2007 Public Transport

Barometer survey support this argument.

Th e yearly survey, which is conducted by

the Swedish Public Transport Association

(SLTF) shows that customers value simplicity

in public transport services over reliability,

speed and security, which have always been

among the top customer priorities. Departure

times, on the other hand, are not listed among

the fi ve most important factors for customers.

Swebus is working to increase the share of

incentive contracts in the public transport

sector, among other things through the bus

operators’ industry organization.

Higher effi ciencyWhether the timetable is created by the client

or Swebus, good traffi c planning is critical for

the company to operate successfully. Th e per-

formance management system developed by

Concordia Bus is the most eff ective in the

industry, and the only one that makes up part

of a larger customer-oriented model for pro-

cess control.

In the past year Swebus further improved

its planning effi ciency. For the customers this

means better traffi c solutions, without ever

compromising on safety or security and

always with room for a comfort and con-

venience that contributes to a positive experi-

ence of the journey.

For the client, a high level of planning

effi ciency is synonymous with improved

transport services and a cost reduction that

can decrease the long-term need for tax sub-

sidies. It also provides scope to allocate

resources to an expanded service off ering that

attracts more customers.

One consequence of ineffi ciency is that

drivers are available to customers only for

around two thirds of their so-called driving

time. Th e remaining time is spent at the

depot, at the starting/end stops and during

empty transports. 13% of the total kilome-

ters driven by Swebus consist of empty trans-

ports, which means that every day Swebus is

forced to drive two times the Earth’s circum-

ference without any passengers onboard.

Proactive environmental effortsFrom a societal and the environmental per-

spective, bus transports are an excellent alter-

native. Buses off er environmental advantages

even when carrying only a few passengers,

and a reduced number of cars on the road

alleviates traffi c congestion and provides

greater scope for commercial transports,

bicyclists and pedestrians. Th e challenge for

Swebus lies in encouraging more people to

choose the bus as their mode of transport.

When it comes to the ability to pro-

actively seek new ways of maximizing re-

source-effi ciency in the environmental area

and meeting continuously escalating environ-

mental challenges, Swebus is a forerunner.

Th e company continuously measures and

takes action to reduce its environmental

impact, which will be presented for the fi rst

time in a comprehensive environmental report

during 2008. Swebus’s goal is to achieve a 20%

reduction in greenhouse gas emissions per pas-

senger by the year 2012 and to increase the use

of renewable energy in the company’s buses

and premises. In addition, the company has

joined forces with clients in an environmental

project to increase the number of passengers

and minimize empty transports.

Dedicated employeesDedicated employees that share Swebus’s

values and have the knowledge necessary to

develop the company’s operations in the right

direction are essential for success. Swebus

therefore works actively to foster both dedica-

tion and expertise. Several of the 25 perform-

ance indicators used by Swebus and the other

companies in the Concordia Bus Group are

aimed at providing both managers and other

employees with opportunities for personal

SWEBUS

1 4 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

CONCORDIA BUS FINLAND

Concordia Bus Finland has dramatic-ally increased its share of bus trans-ports in the Helsinki region, which accounts for half of the country’s total public transport volume. The company is also driving the develop-ment of the new generation of trans-port contracts that demand respons-iveness the needs of both clients and customers.

Finland’s local bus transports are subject to

extensive tendering only in and around the cit-

ies of Helsinki and Turku. Th e Helsinki market

is around eight times larger than that in Turku,

and in the past year Concordia Bus expanded

its share of this market from 25% to 30%. Th e

company operates around 380 buses.

Growing confi denceTh e Finnish market is fragmented and

marked by the very fi rst tender, which took

place in Helsinki during 1995 on conditions

that came to inhibit a mutually benefi cial

development for all parties. Transports are

often micromanaged based on considerations

other than customer needs and the bus com-

panies generally have no profi tability, which

is hampering adaptation of their operations

to modern demands on customer orien tation

and resource-effi ciency.

Concordia Bus Finland originally started

operations in the Helsinki region and still

works exclusively in this market. For the third

consecutive year, the company has been

A partner for tomorrow’s public transport authorities

Managing Director Tom Ward

Annual revenue EUR 56 million, equal to

SEK 530 million (414)

Market share 30% (25%)

Number of passengers 31 million (26)

Number of employees 805 (623)

Number of buses 380 (298)

Number of km driven 25.7 million (22.4)

Competitors Veolia Transport, Helsingin

Bussiliikenne, Westendin Linjat, Pohjolan

Liikenne

Website www.concordiabus.fi

entrusted with new transport contracts in the

region and is today number two after the

City of Helsinki’s own bus operator Helb.

Th e market in Turku is equally divided

between the municipal bus company and a

number of smaller operators.

In 2007 the City of Tampere carried out

its fi rst public tender of bus transport ser-

vices. Veolia made the winning bid, which is

limited to 5% of the city’s local buses. Over

the next three years transports corresponding

to around 1,000 buses will be tendered in the

Finnish market, of which more than 200 rep-

resent a net increase.

Long-term dialogueConcordia Bus Finland is gradually improv-

ing its resource-effi ciency and is continuously

increasing the share of buses of the highest

environmental standard, Euro 5 and EEV, in

its fl eet. Th e most important measure over

time is focused on maintaining a continuous

and constructive dialogue with the public

transport authorities in order to establish a

reputation as the best local transport com-

pany from both their own and a customer

perspective.

Like the three Scandinavian countries,

Finland is having diffi culty attracting its own

young people to choose a career as bus driver.

Foreign nationals are therefore a welcome

addition to the bus companies’ staff .

Concordia Bus Finland has a progressive

human resource policy. Scheduling with con-

sideration to the individual employee has

contributed to a working environment char-

acterized by good relations, a positive atmo-

sphere, well functioning cooperation with the

unions and falling sickness absence rates.

Concordia Bus Finland 10%

SHARE OF CONCORDIA BUS’S REVENUE

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 1 5

A platform for strong growth

Managing Director Geir Ledsten

Annual revenue NOK 416.2 million,

equal to SEK 491 million

Market share 17% (19%)

Number of passengers 11.5 million (9.8)

Number of employees. 700 (489)

Number of buses 330 (337)

Number of km driven 17.5 million (17.3)

Competitors Veolia, Norgesbuss, Tide

Website www.concordiabus.no

CONCORDIA BUS NORWAY

Competitive tenders in the Norwegian market are expected to increase by 85% over the next three years, and Concordia Bus is well positioned for rapid growth.

Th e deregulated segment of the Norwegian

market for scheduled public bus transports

expanded by 26% to 31% in 2007. Th e rate

of growth is expected to reach twice that level

during 2008-2009, mainly due to competi-

tive tendering for bus transports in the

Bergen region for the fi rst time.

In the initial phase of the Bergen tender,

the client Skyss in Hordaland County has

contracted Concordia Bus to operate 44 of

200 buses. Th is is well in line with the com-

pany’s ambition for development in Norway.

In the deregulated segment of the market,

Concordia Bus currently holds the number

three position with a market share of 17%.

Low consolidationNorgesbuss & Torghatten-gruppen, Veolia

and Concordia Bus together command more

than half of the deregulated market. At the

start of 2008, however, around 70% of the

Norwegian market was still regulated. Public

transport authorities in several counties have

started to collaborate in provision of bus

transport services and an ongoing process of

consolidation is also taking place among

independent local operators.

Although investments in public transport

are rising, buses are nonetheless losing market

shares to automobiles outside the major cit-

ies, making the environment one of several

losers. Customers, public transport authori-

ties, taxpayers, operators and others all have

an interest in a continued rapid transition to

competitive tendering, which results in more

needs-driven and resource-effi cient bus trans-

ports. So far, however, lowest price has been

the dominant selection criterion in most cases.

A qualifi ed partnerConcordia Bus Norway originates from the

former privately-owned Schöyens Bilcen-

traler, whose operations were concentrated in

Oslo and Akershus. Th e company now serves

the entire Østland area and will also be active

in Vestlandet starting in summer 2008.

As part of a group with the entire Nordic

region as its base, the company can serve as a

forerunner in the transformation of the Nor-

wegian bus market. In Concordia Bus Nor-

way, the public transport authorities have

access to a qualifi ed partner with a strong cus-

tomer focus and the resources to prepare ten-

ders, quality systems, etc., that meet high

quality standards. Quality in connection with

the launch of new transport contracts is high

and the statistics also indicate reliability in an

insignifi cant share of cancelled departures.

Employee turnover in the company is low

in view of the country’s powerful economic

growth and very low unemployment rate. At

the same time, sickness absence is decreasing.

Eff orts to improve the working environment

together with the union organizations have

high priority.

Concordia Bus Norway 9%

SHARE OF CONCORDIA BUS’S REVENUE

1 6 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

Th e fundamental conditions for express bus

operations are completely diff erent from

those for local bus transports, mainly in that

revenue comes exclusively from the individ-

ual passengers.

At Swebus Express, express bus transports

consist of scheduled transports that cover a

distance of at least 100 km and cross a least

one county line. Unlike rail-bound transports,

there is no opportunity to benefi t from public

sector subsidies in this segment.

Swebus Express is the dominant player

above all on bus lines with a large customer

base, such as the Swedish triangle Stockholm-

Gothenburg-Malmö, and also operates to the

Norwegian and Danish capital cities.

Major challengesRail transports are the foremost competitor

for eco-conscious customers in the public

transport sector and, unlike express buses,

increased their volumes in 2007. Th e market

share for rail transports is estimated at

approximately 75%, while Swebuss Express

has around 5%. Including express bus trans-

ports, the company has a market share of over

50%.

Automobiles are a fi nancially and environ-

mentally inferior alternative to express bus

transports, but nonetheless gained ground in

the past year. Th rough an objectionary right,

the aff ected public transport authorities can

still prevent boarding and deboarding of indi-

vidual passengers within the same county.

Young people, students and seniors are the

key customer groups for Swebus Express, and

price is often the decision factor for their

choice. Sales take place to a growing extent

over the Internet, which provides convenience

for the customers and scope to keep prices low.

By purchasing a ticket 24 hours before depar-

ture, the customer is guaranteed a seat on the

bus.

Alongside the express product, Swebus

Express operates commuter transports

between Stockholm and Uppsala.

Increased effi ciencyIn the past year the company increased its

resource-effi ciency by revising the seat guar-

antee, reducing the number of owned buses

in service, winding up commuter lines and

other lines with weak demand, boosting the

share of online sales, reducing the number of

administrative staff and raising the share of

environmentally-friendly buses in the com-

pany’s own fl eet. Swebus Express has also

increased the number of campaigns and

special off ers.

Attractive offersTh e company strives to continuously optim-

ize the relative price advantages of its prod-

ucts, which is necessary in achieving a sus-

tainable improvement in customer satisfac-

tion and loyalty.

Swebus Express will continue enhancing

its resource-effi ciency through improved sup-

port systems, increased capacity utilization

and the purchasing of even more vehicles of a

high environmental standard. Th e company

also aims to strengthen its position through

attractive off ers to the customers.

Lowest price for long distance travel

Managing Director Joakim Palmkvist

Annual revenue SEK 355 million (367)

Market share > 50%

Number of passengers 2.2 million (2.5)

Number of employees 210 (239)

Number of buses 100 (110)

Number of km driven 17 million (19.2)

Competitors SJ, Säfflebuss

Website www.swebusexpress.se

SWEBUS EXPRESS

Swebus Express has continued to strengthen its position as the market leader in scheduled express bus transports. From a fi nancial perspect-ive, product development and effi -ciency improvements are making this product increasingly superior to car transports. Compared to rail travel, however, express buses are still a minor presence.

Swebus Express7%

SHARE OF CONCORDIA BUS’S REVENUE

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 1 7

Concordia Bus Fleet gives the Group a detailed overview of the Nordic region’s largest bus fl eet and greater leverage in bidding for transport contracts.

Concordia Bus Fleet bases all purchasing of

buses on dynamic calculations of the total cost

of ownership over the entire lifecycle of each

bus. Th e calculations take into account not

only the purchase price and fi nancing cost of

the buses, but also their resale value and costs

for fuel, service, spare parts, etc. Th is method

for purchasing vehicles provides far better con-

trol over an area that normally makes up

around 40% of a bus company’s total costs.

By acquiring all buses via a single company

Concordia Bus is able to exploit its scale econ-

omies while at the same time standardizing its

purchasing routines, which further improves

the scope to optimize operations.

At the time it was established in 2006,

Concordia Bus Fleet was the fi rst company of

its kind in the Nordic market. With a small

and highly specialized staff , Concordia Bus

Fleet purchases and fi nances buses in a fl eet

that is spread across four countries. Th e

Group’s central purchasing department then

handles the fi nal acquisition. Concordia Bus

Fleet optimizes utilization of the Group’s bus

fl eet to reduce both tied-up capital and the

need for new investments. Th is contributes to

satisfying the client’s requirements in the most

resource-effi cient manner possible. Handling

the buses in a separate company also ensures

greater transparency and security for the fi nan-

ciers.

Competitive total solution Concordia Bus’s operations are focused on

meeting the requirements in a large number of

multi-year transport contracts containing

individual and far-reaching demands on the

local traffi c and buses.

Th e detailed tender specifi cations put for-

ward by the transport authorities require extens-

ive system support in the operating companies.

Concordia Bus Fleet has developed a sophisti-

cated, comprehensive and robust model that is

used by the Group and its operating units.

Before making a bid, the operating com-

pany is assisted by Concordia Bus Fleet to cal-

culate exactly how the bus concept in the tender

in question should be structured to achieve a

cost advantage. Th rough effi cient resource allo-

cation, the need for new investments can be

reduced and the bid be made more competitive,

at the same time that the transport services

become more profi table. If the tender is won,

Concordia Bus Fleet provides the operating

company with a complete package consisting of

buses, fi nancing, administration and other bus-

related services. Th e concept is based on pre-

agreed market-based terms between the parties,

with both fi xed and variable compensation.

Flexibility through right of return Th e operating companies in the Concordia

Bus Group lease buses from Concordia Bus

Fleet with a right of return. If the operating

company wishes to adjust its bus fl eet during

the term of the contract, this can be done after

a short notice period. In the event that a com-

pany loses one of its transport contracts, it has

the right to cancel the lease according to a pre-

determined notice period and to return all of

the aff ected buses.

When a transport contract expires, the

buses are either sold or relocated. Th is right of

return during ongoing transport contracts

accelerates the elimination of excess capacity

in the operating companies, which thereby

achieve greater fl exibility and cost-awareness

and are able to maximize utilization of the bus

fl eet.

At the end of the fi scal year, close to 98%

of the buses were on lease to operating compa-

nies in the Concordia Bus Group. Th e remain-

ing buses were either for sale or, when deemed

more advantageous for internal optimization,

leased outside the Group. In the past fi scal year

Concordia Bus Fleet sold 260 buses.

Lower cost of acquisition Two years after its formation, Concordia Bus

Fleet has acquired and fi nanced buses for a

total of SEK 1.7 billion. Th is means that the

company has been responsible for the pur-

chase of nearly every fi fth bus in Sweden, Nor-

way and Finland. Th e acquisitions are fi nanced

through fi nance leases in which the contract

period is shorter than the useful life of the

buses, thereby reducing fi nancing risk. In the

past fi scal year the company acquired 392

buses from fi ve diff erent Swedish and foreign

manufacturers, and continuously evaluates

alternative suppliers.

Concordia Bus Fleet expects to acquire up

to 300 buses annually over the next three

years. In 2008 the company is conducting an

in-depth analysis of the fl eet that includes

every individual bus. Th e results will serve as

a basis for the proactive measures needed by

Concordia Bus to optimally meet the needs

of customers and clients in each part of the

Nordic market.

Total control reduces costs

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

20082007200620052004

Operating leasesFinance leasesOwned buses

Number

2,568

1,317

1,470

1,569

1,731

23

23

31 328

2,237

1,7951,562

1,216

512

1,648

BREAKDOWN OF BUSES BY TYPE OF FINANCING

CONCORDIA BUS FLEET

1 8 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

Long-term sustainable travel

Concordia Bus works toward sustainable transport development with a focus on customer benefi t and innovation. The Group’s new environmental policy has provided the fi rst necessary platform for this process.

In 2007 Concordia Bus formulated and adopted

a group-wide environmental policy that refl ects

a commitment to developing public transport’s

benefi ts to society through continuous measures

to promote sustainable development.

As a next step, the management will choose

how to implement focus and integrate it with

both operating activities and process develop-

ment. Th e long-term target is for the company

to become climate-neutral.

Higher capacity utilization increases benefi tsBuses are environmentally superior to automo-

biles even when carrying only a few passengers.

Th e more people who choose the bus instead of

a car, the greater the environmental gains. In

order for bus transports to become climate-

neutral – on the road and in the workshops and

depots – energy consumption and emissions

must be further reduced.

Measures such as new fuels, new bus tech-

nology and fuel-effi cient driving can contribute

to increased sustainability, and transport effi -

ciency also has a direct infl uence on environ-

mental impact. Optimized timetables with a

minimum of unproductive time help to reduce

negative environmental eff ects, and pressure on

the environment is further alleviated by main-

taining the smallest possible distance between

the bus storage yards and the fi rst stop. Th e use

of energy, water, cleaning agents and chemicals

in connection with vehicle service is also signi-

fi cant from an environmental standpoint.

230 million passengersToday’s needs must be satisfi ed in a way that

makes it possible to also meet future needs. In

other words, all development must be sustain-

able in the long term.

Concordia Bus drives more people and more

buses than any other operator in the Nordic

countries. Every fi fth bus operated in the Nordic

region belongs to the company and around 5%

of all diesel fuel sold in the Nordic market is used

to transport its 230 million passengers. Th is rep-

resents a major environmental responsibility.

All three of the company’s defi ning charac-

teristics – appreciated, credible and resource-

effi cient – have a direct bearing on environ-

mental performance. In a longer perspective,

public transports without environmental

responsibility can never be perceived as reliable

or appreciated. Transport solutions that do not

support society’s ambitions for road traffi c lack

credibility. Th e resource-effi ciency requirement

means that low production costs must be com-

bined with high quality and eff ective solutions

that contribute to sustainable development.

In 2005 Swebus adopted an environmental

plan and began working according to an environ-

mental management system based on ISO

14001:2004, while the companies in Norway

and Finland were both already certifi ed to this

environmental standard.

Th e Group has an environmental council

consisting of the environmental directors of each

subsidiary. Th e environmental council draws up

guidelines for the Group’s joint environmental

eff orts. Every year, the aff ected employees in

each organization attend an environmental

course. Recurring audits are used to monitor

environmental activities and their results.

Integrated environmental aspects Th e new group-wide environmental policy

emphasizes the long-term nature of these meas-

ures. Environmental aspects must be coordi-

nated and integrated with the development of

processes, services, quality issues, etc., in order

to create lasting value for all stakeholders. Th e

commitment applies to all areas of activity, not

only bus transports.

Concordia Bus aims to be one of the most

eco-adapted alternatives for public transport and

long-distance bus travel. With a focus on cus-

tomers and innovation, the company strives to

be an industry leader in the development of sus-

tainable public transport.

Successful environmental work demands

clearly defi ned goals and continuous evaluation.

SUSTAINABILITY

A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8 C O N C O R D I A B U S 1 9

SUSTAINABILITY

BREAKDOWN OF BUS FLEET BY ENGINE CLASS/EURO CLASS

BREAKDOWN OF BUSFLEET BY FUEL TYPE

EMISSIONS TONNES

Carbon dioxides 211,712

Nitrogen oxides 3,054

Particulates 39

Hydrocarbons 40

Diesel 96.17%Ethanol 2.37%

CNG/Biogas 1.44%

Electricity 0.02%

EEV 1.53%

Euro 0 0.51%

Euro 1 10.18%

Euro 2 42.82%Euro 3 32.68%

Euro 4 9.56%

Euro 5 2.74%

Environmental aspects are therefore integrated with

general business development, which means that tar-

gets are set at least yearly in connection with adop-

tion of the annual business plan and are followed up

systematically. For several years, the company has

worked actively to develop performance indicators

for the Group’s total environmental impact.

Th e environmental policy underlines a few areas

that are of particular importance for successful envir-

onmental management, such as responsible use of

energy, a reduced share of fossil fuels, conservation

of resources, an increase in the employees’ environ-

mental knowledge and encouragement of their

environmental initiatives.

Decreased fuel consumption Fuel consumption in the buses and their emissions

of greenhouse gases (GHGs) and particulates,

together with energy for heating, are the key focus

areas for environmental eff orts.

With the Nordic region’s largest bus fl eet and a

positive operating result, there is good potential to

act as a driving force for technological advances that

can reduce the environmental footprint of transport

services. Th e ongoing transition to increasingly eco-

effi cient buses and upgrading of existing buses is

also enabling these to meet modern environmental

standards.

Th e number of kilometers driven with passen-

gers rose by 3.4% in the past fi scal year despite a

decrease of 3.6% or 127 buses in the fl eet, mainly

thanks to improved transport effi ciency. Th e com-

pany’s total diesel consumption reached 94.3 mil-

lion liters, corresponding to 96% of the total num-

ber of kilometers driven. Total carbon dioxide emis-

sions amounted to 211,000 tonnes.

Concordia Bus collaborates with bus manufac-

turers and other suppliers to develop new genera-

tions of more resource-effi cient and innovative

vehicles and engines. In the current fi scal year, the

company will reduce its fuel consumption in exist-

ing transports by 2%. Emissions of carbon dioxide

are expected to decrease by 4,000 tonnes through

measures such as modernization of the bus fl eet,

improved maintenance, eco-adapted driving and

optimized use of the buses with the best environ-

mental performance.

Th e buses use Environmental Class 1 (EC1) diesel

with various additives to reduce fuel-generated emis-

sions. Of total fuel consumption, ethanol and CNG

accounted for an unchanged share of nearly 5%.

In several cities where Concordia Bus is respons-

ible for public transport, promising trials are under-

way to test new, natural fuel additives that reduce

emissions of both GHGs and particulates. By 2012,

GHG emissions will be reduced by 20% per passen-

ger kilometer.

Modernization of treatment plantsEnergy consumption at the depots is falling and will

be further reduced over the next three-year period.

Th e conversion from chemical to biological or

fresh water processes in the depots’ treatment plants

has resulted in a 50% decrease in hazardous emis-

sions. Modernization of the treatment plants is con-

tinuing in pace with the availability of new treat-

ment and recycling technology.

Each depot has an individual waste plan. When

a bus is scrapped, close to 90% of the components

are recovered.

Safety comes fi rstA high level of safety is vital in all of the company’s

transports, and in all other operating activities. Th e

traffi c safety policy expresses the company’s ambi-

tion to serve as a role model in traffi c. Safety-related

work is conducted systematically and as an integral

part of other operations.

Safety and security are the top priorities in day-

to-day bus transports, are take precedence over

comfort, convenience and punctuality. In 2007

Concordia Bus won an award in Sweden for its traf-

fi c safety eff orts including several thousand self-

administered speed checks that resulted in lower

driving speeds.

Th e buses undergo technical tune-ups and ser-

vice every 10,000 kilometers and have earned the

industry’s top scores in annual vehicle inspections

for the past two years. In addition, each bus is sub-

ject to a daily 29-point safety check that is per-

formed before entering service for the day.

Th e company’s active approach to safety

includes follow-up of threats and violence against

customers or staff and risks related to traffi c incid-

ents. An in-house developed computer system

handles data and contributes to a safe and secure

environment where traffi c fl ows smoothly without

disruptions.

2 0 C O N C O R D I A B U S A N N U A L R E P O R T 2 0 0 7 / 2 0 0 8

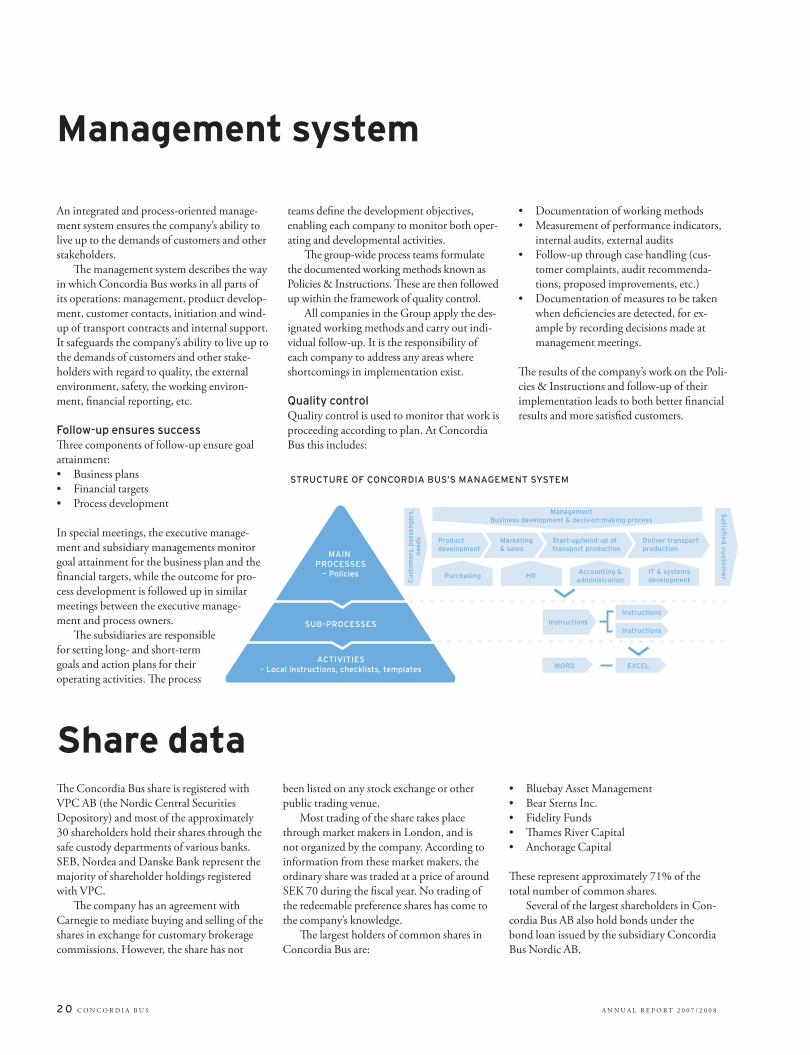

Management system

Share dataTh e Concordia Bus share is registered with

VPC AB (the Nordic Central Securities

Depository) and most of the approximately

30 shareholders hold their shares through the

safe custody departments of various banks.

SEB, Nordea and Danske Bank represent the

majority of shareholder holdings registered

with VPC.

Th e company has an agreement with

Carnegie to mediate buying and selling of the

shares in exchange for customary brokerage

commissions. However, the share has not

been listed on any stock exchange or other

public trading venue.

Most trading of the share takes place

through market makers in London, and is

not organized by the company. According to

information from these market makers, the

ordinary share was traded at a price of around

SEK 70 during the fi scal year. No trading of

the redeemable preference shares has come to

the company’s knowledge.

Th e largest holders of common shares in

Concordia Bus are:

• Bluebay Asset Management

• Bear Sterns Inc.

• Fidelity Funds

• Th ames River Capital

• Anchorage Capital

Th ese represent approximately 71% of the

total number of common shares.