comprehensive annual financial report -...

TRANSCRIPT

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED AUGUST 31, 2013

STAFFORD MUNICIPAL SCHOOL DISTRICT

1625 STAFFORDSHIRE ROAD

STAFFORD, TEXAS 77477

WWW.STAFFORDMSD.ORG

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED AUGUST 31, 2013

PREPARED BY:

CARLA MERKA

CHIEF FINANCIAL OFFICER

STAFFORD MUNICIPAL SCHOOL DISTRICT

1625 STAFFORDSHIRE ROAD

STAFFORD, TEXAS 77477

WWW.STAFFORDMSD.ORG

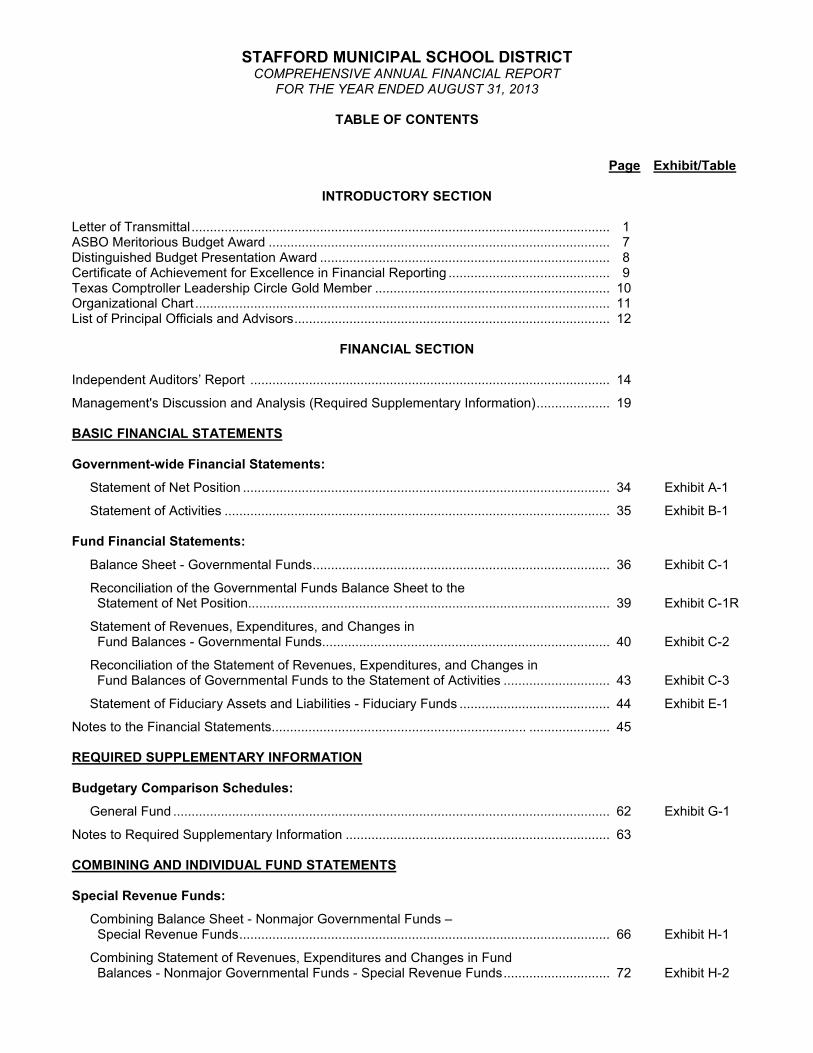

STAFFORD MUNICIPAL SCHOOL DISTRICTCOMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED AUGUST 31, 2013

TABLE OF CONTENTS

Page Exhibit/Table

INTRODUCTORY SECTION

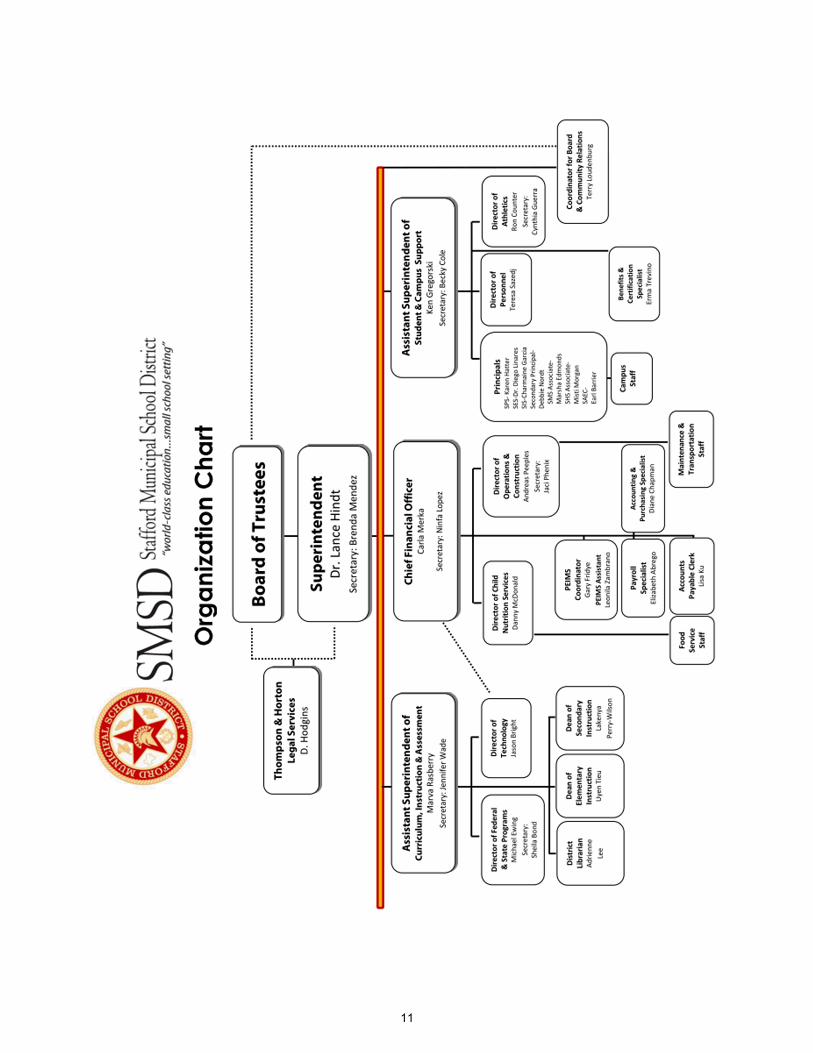

Letter of Transmittal .................................................................................................................. 1ASBO Meritorious Budget Award ............................................................................................. 7Distinguished Budget Presentation Award ............................................................................... 8Certificate of Achievement for Excellence in Financial Reporting ............................................ 9Texas Comptroller Leadership Circle Gold Member ................................................................ 10Organizational Chart ................................................................................................................. 11List of Principal Officials and Advisors...................................................................................... 12

FINANCIAL SECTION

Independent Auditors’ Report .................................................................................................. 14

Management's Discussion and Analysis (Required Supplementary Information).................... 19

BASIC FINANCIAL STATEMENTS

Government-wide Financial Statements:

Statement of Net Position .................................................................................................... 34 Exhibit A-1

Statement of Activities ......................................................................................................... 35 Exhibit B-1

Fund Financial Statements:

Balance Sheet - Governmental Funds................................................................................. 36 Exhibit C-1

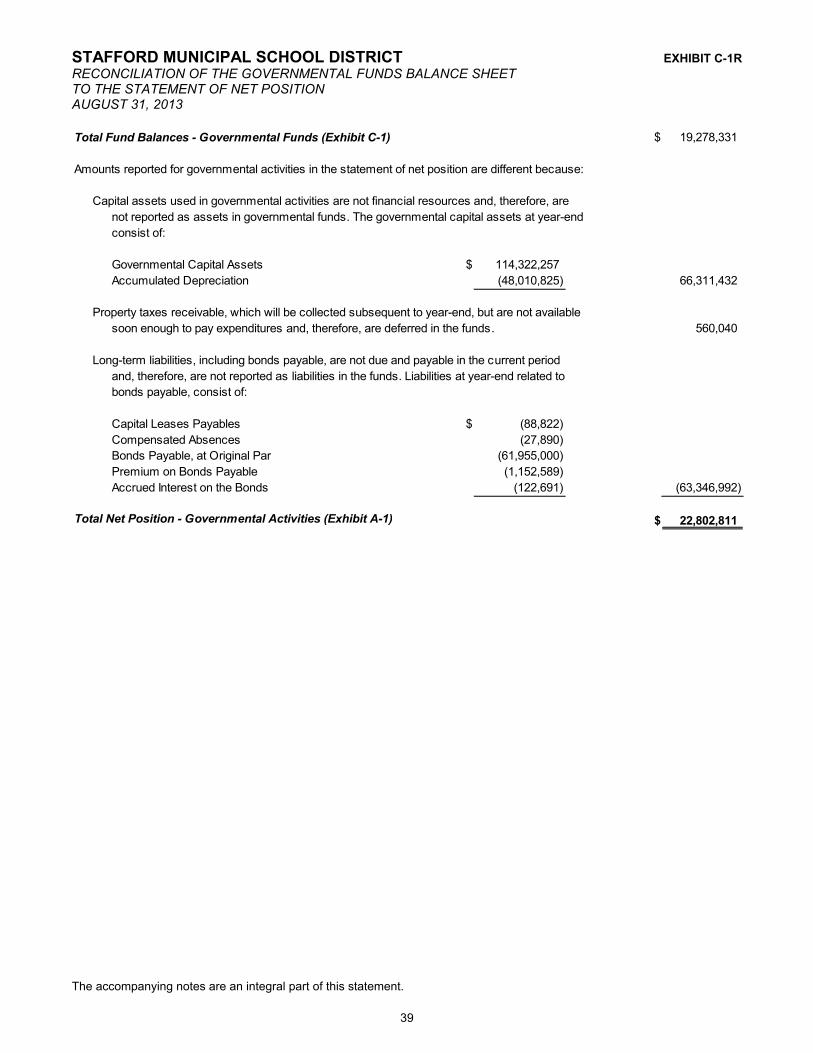

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Position.......................................... ........................................................ 39 Exhibit C-1R

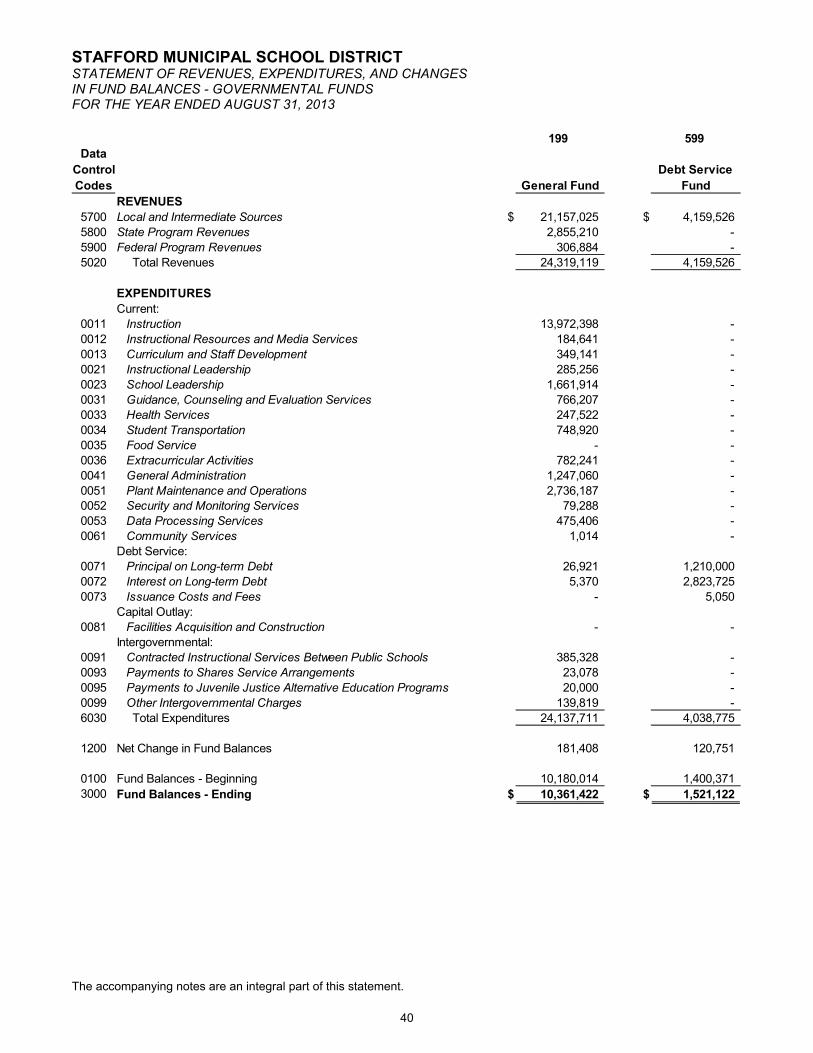

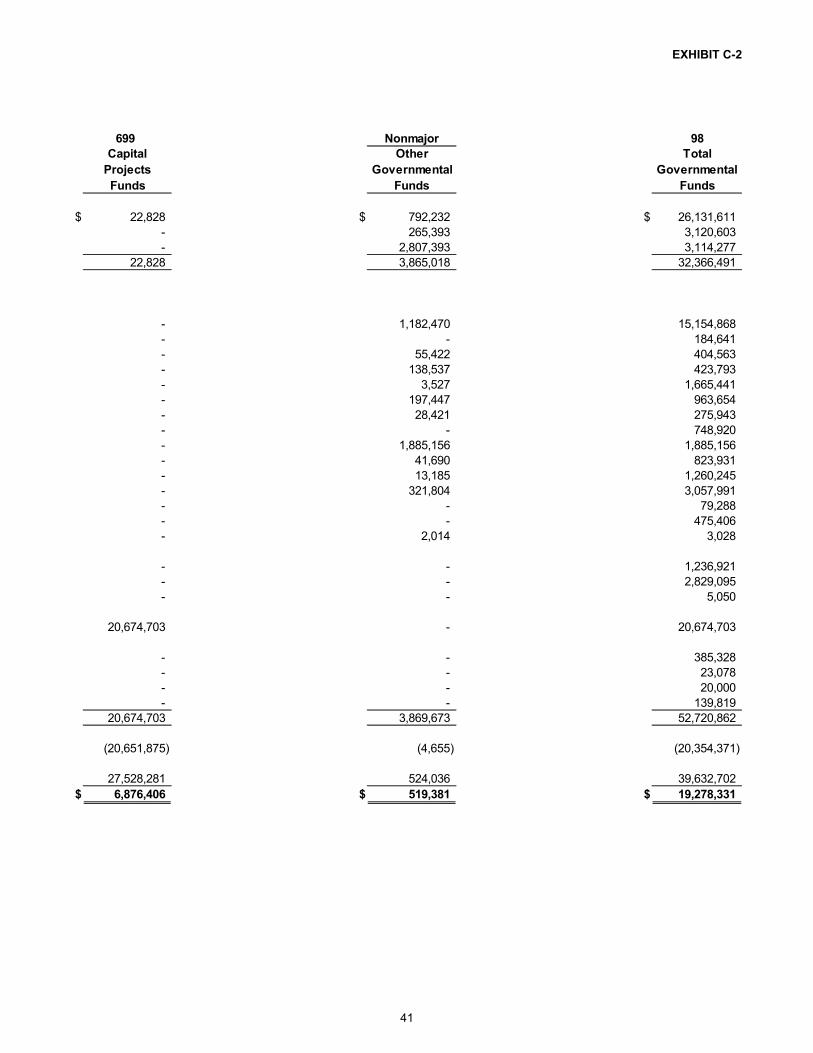

Statement of Revenues, Expenditures, and Changes in Fund Balances - Governmental Funds.............................................................................. 40 Exhibit C-2

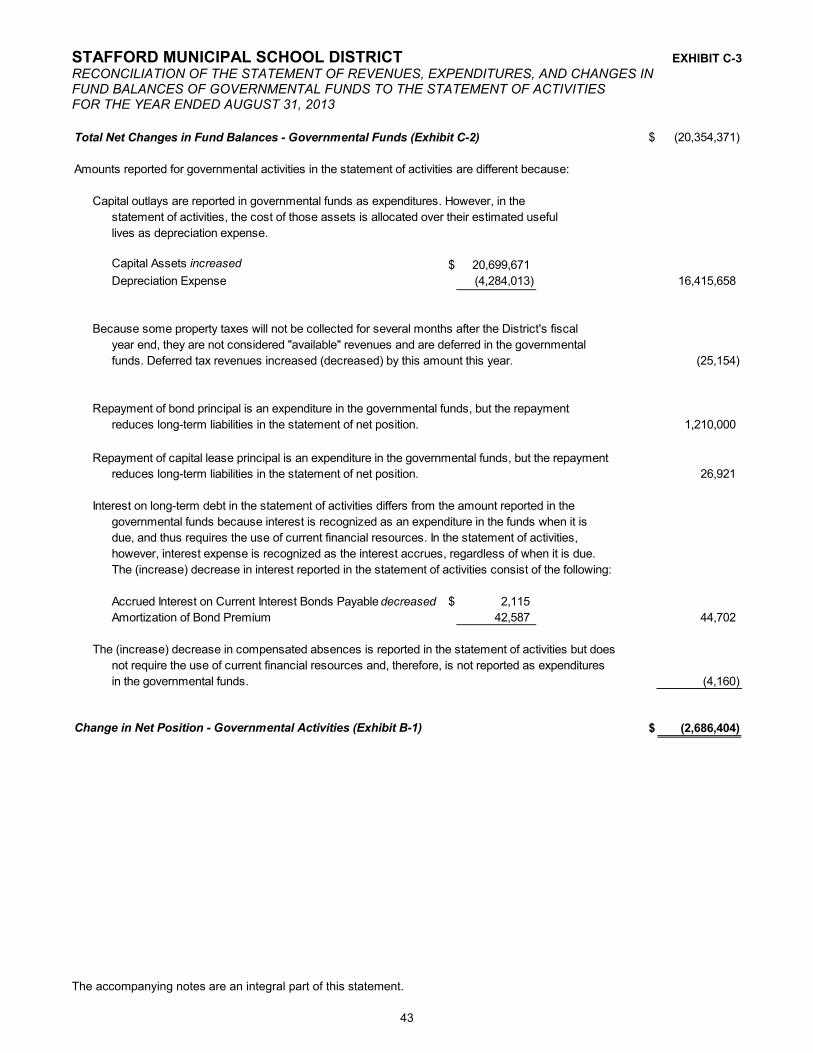

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities ............................. 43 Exhibit C-3

Statement of Fiduciary Assets and Liabilities - Fiduciary Funds ......................................... 44 Exhibit E-1

Notes to the Financial Statements..................................................................... ...................... 45

REQUIRED SUPPLEMENTARY INFORMATION

Budgetary Comparison Schedules:

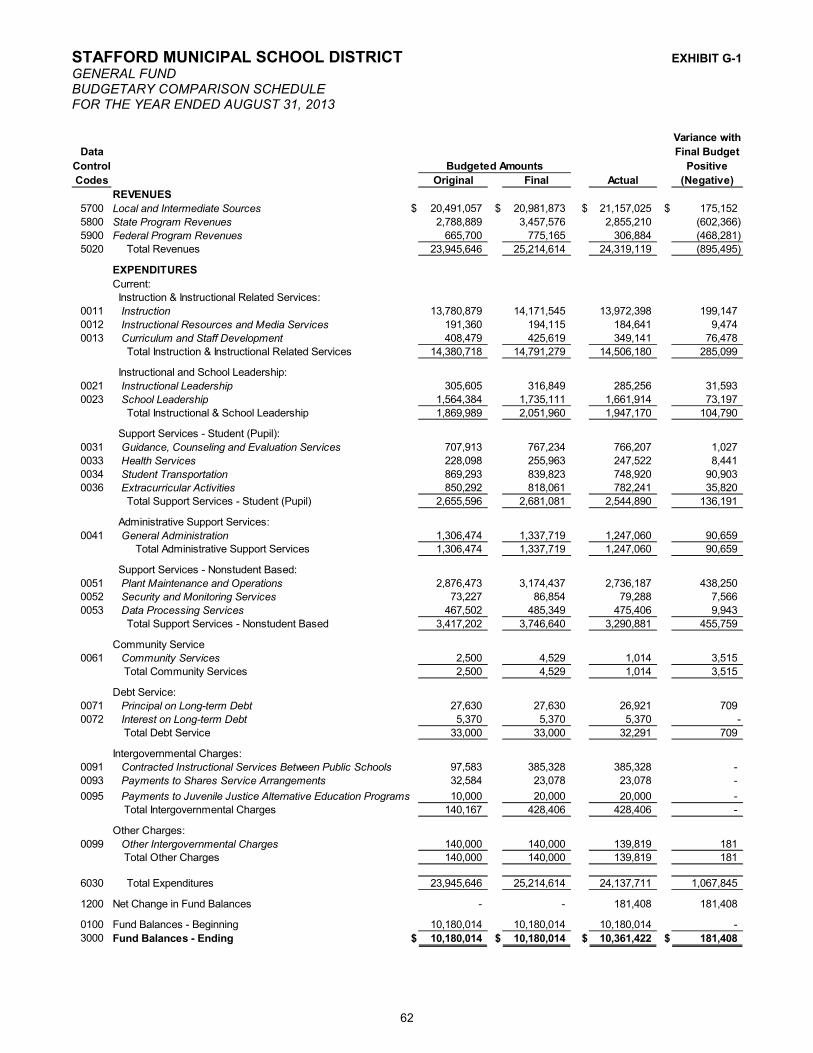

General Fund ....................................................................................................................... 62 Exhibit G-1

Notes to Required Supplementary Information ........................................................................ 63

COMBINING AND INDIVIDUAL FUND STATEMENTS

Special Revenue Funds:

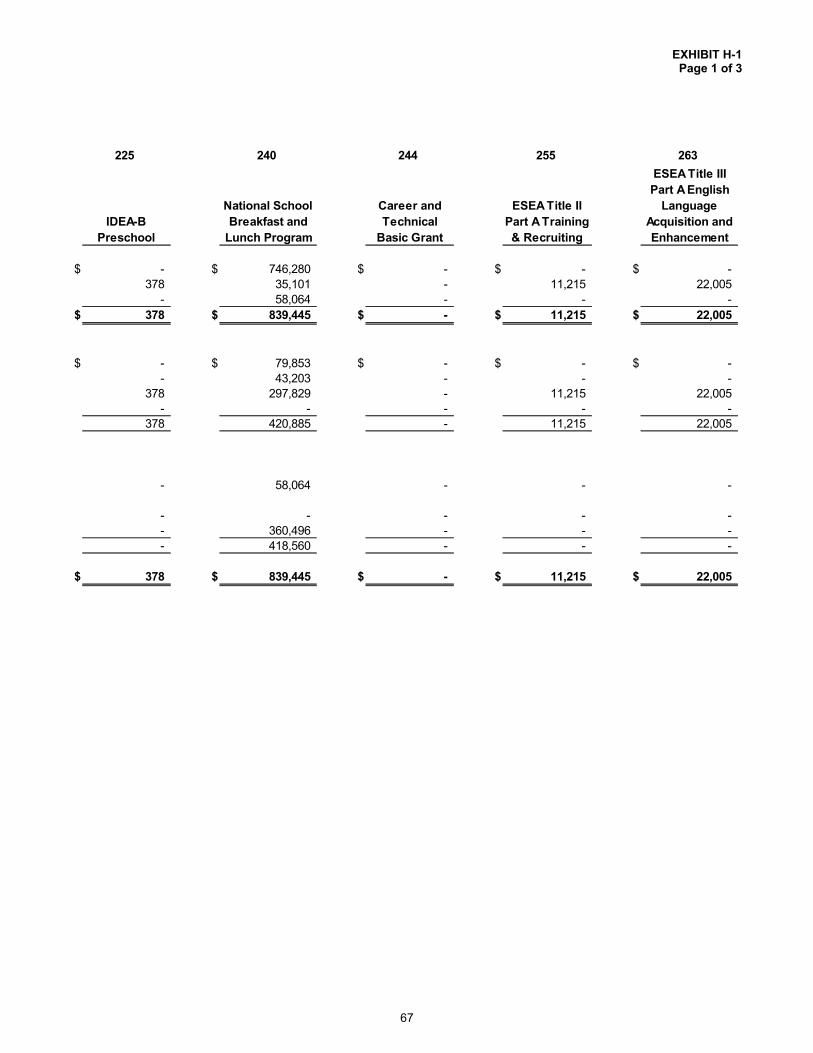

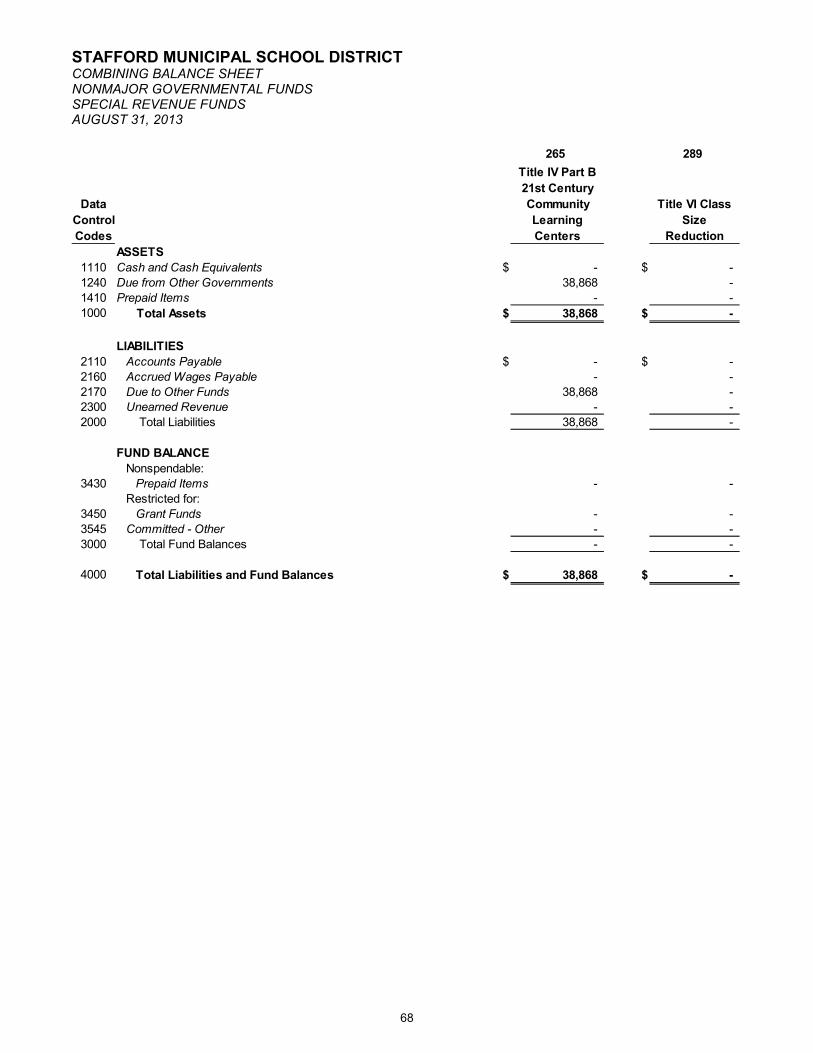

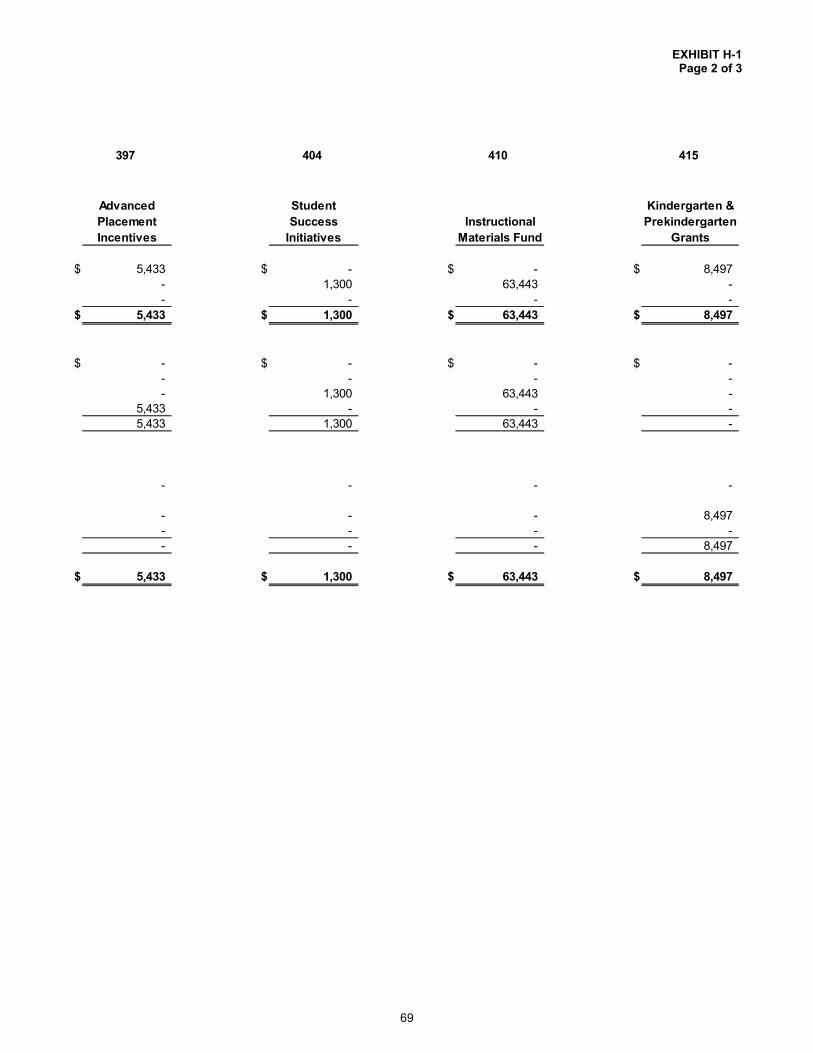

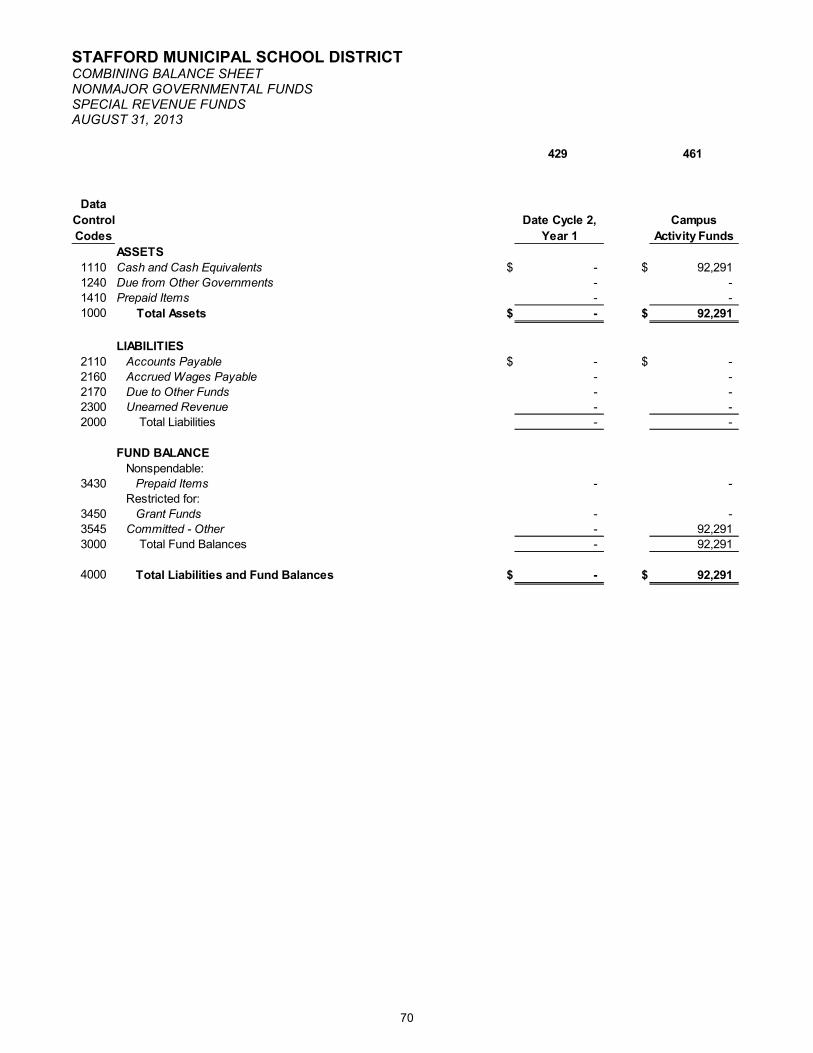

Combining Balance Sheet - Nonmajor Governmental Funds – Special Revenue Funds..................................................................................................... 66 Exhibit H-1

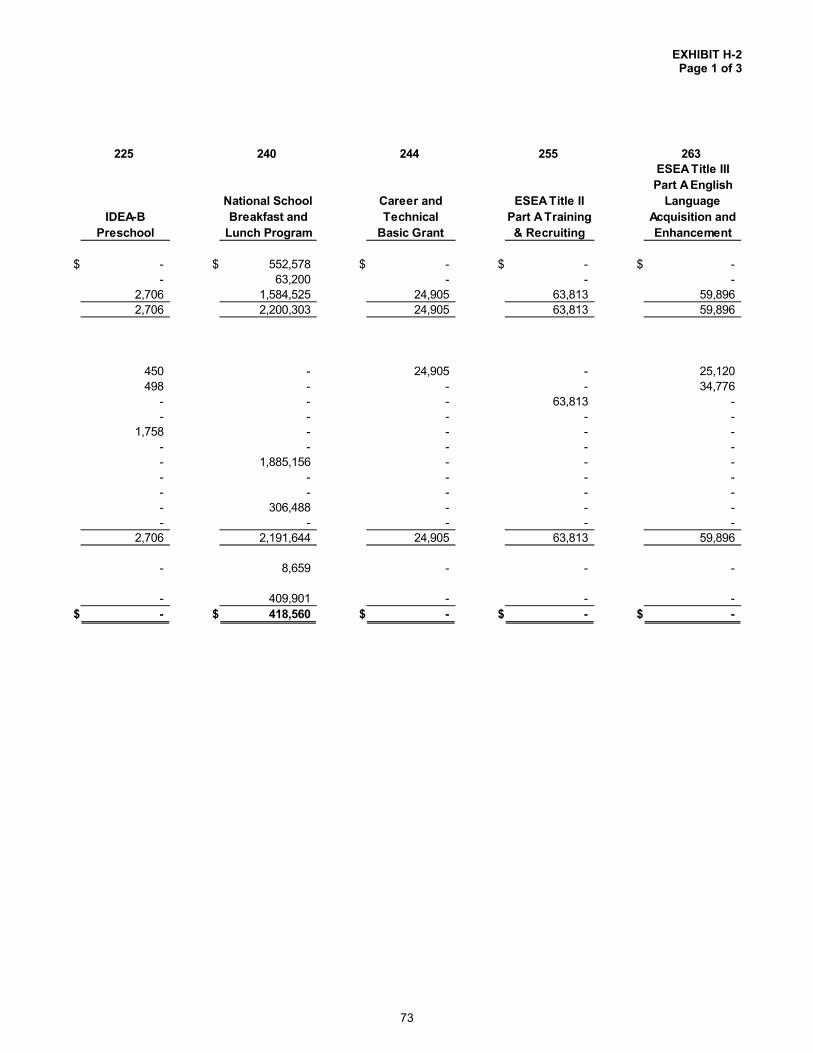

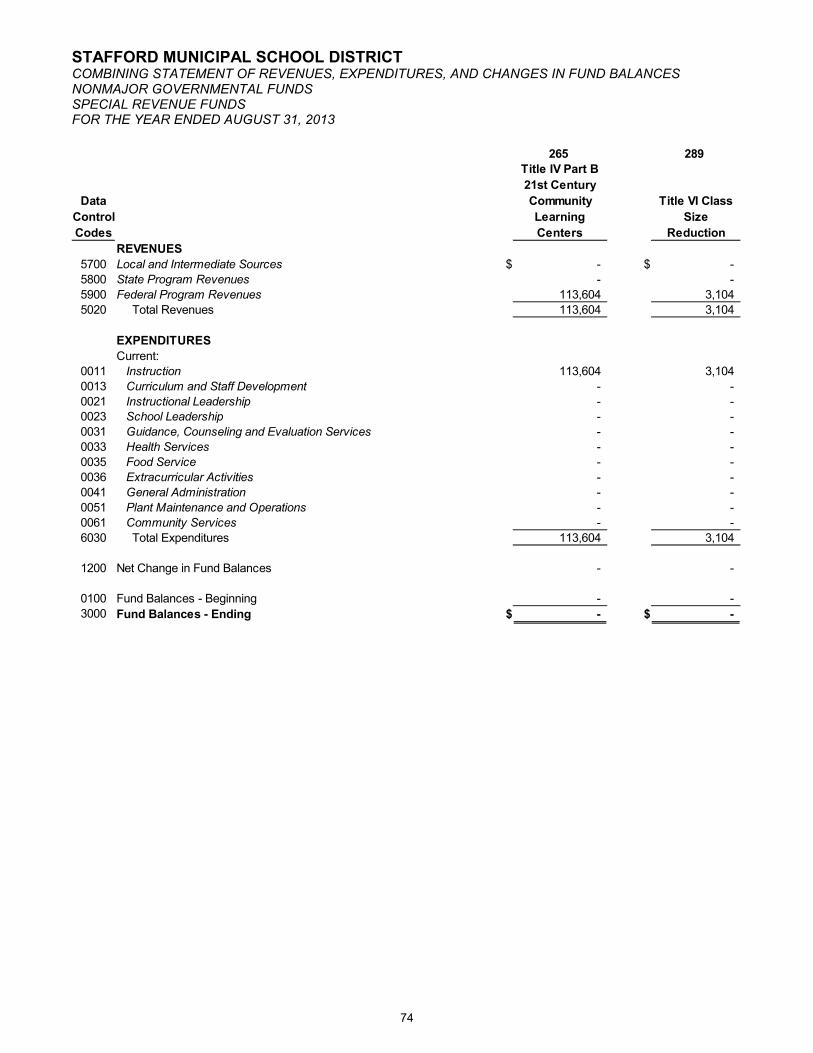

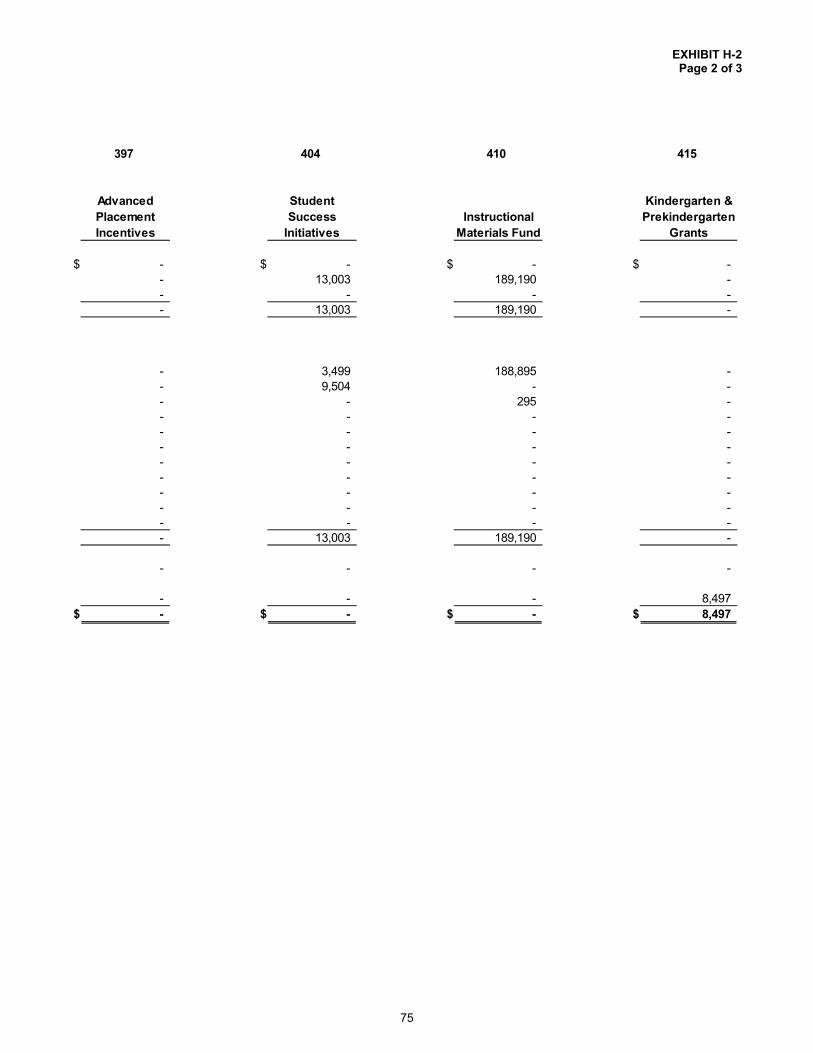

Combining Statement of Revenues, Expenditures and Changes in Fund Balances - Nonmajor Governmental Funds - Special Revenue Funds............................. 72 Exhibit H-2

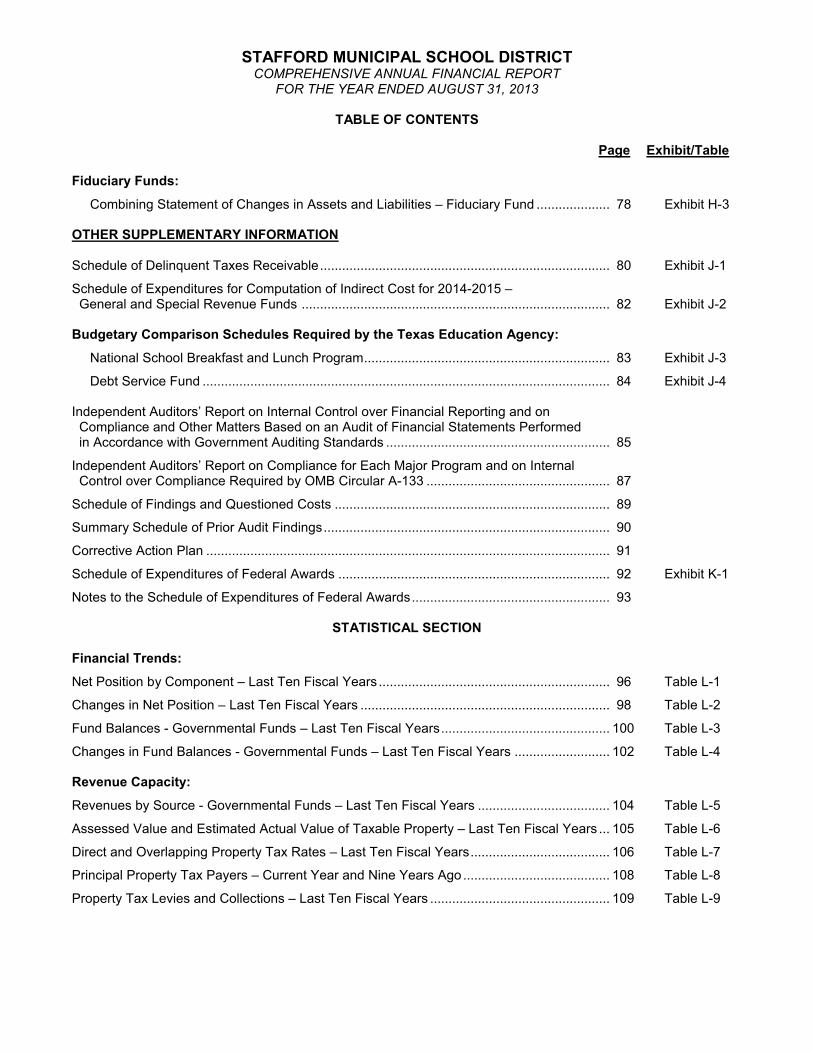

STAFFORD MUNICIPAL SCHOOL DISTRICTCOMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED AUGUST 31, 2013

TABLE OF CONTENTS

Page Exhibit/Table

Fiduciary Funds:

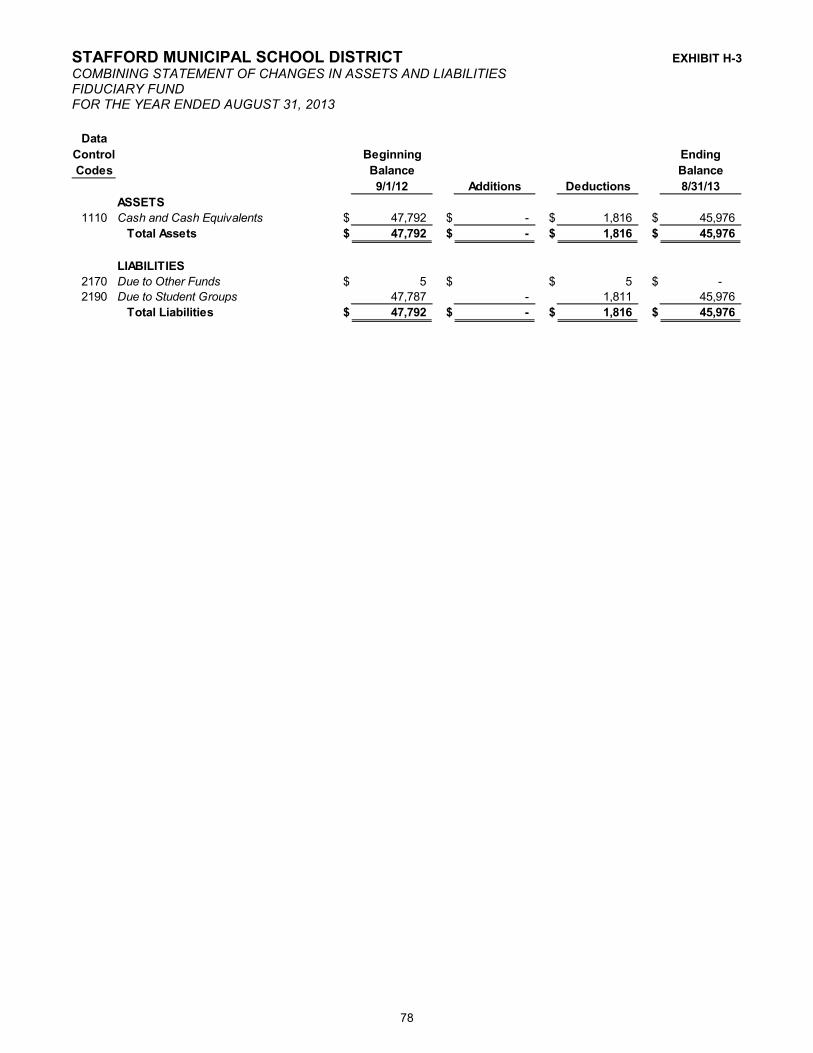

Combining Statement of Changes in Assets and Liabilities – Fiduciary Fund .................... 78 Exhibit H-3

OTHER SUPPLEMENTARY INFORMATION

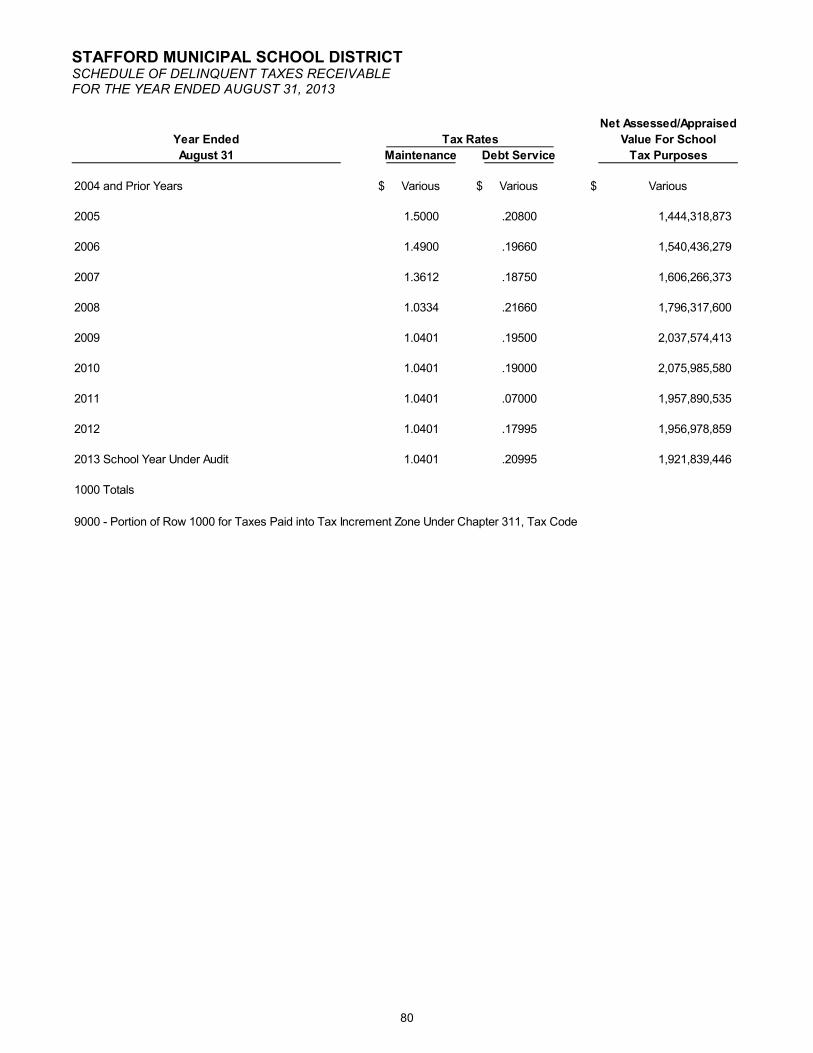

Schedule of Delinquent Taxes Receivable............................................................................... 80 Exhibit J-1

Schedule of Expenditures for Computation of Indirect Cost for 2014-2015 – General and Special Revenue Funds .................................................................................... 82 Exhibit J-2

Budgetary Comparison Schedules Required by the Texas Education Agency:

National School Breakfast and Lunch Program................................................................... 83 Exhibit J-3

Debt Service Fund ............................................................................................................... 84 Exhibit J-4

Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ............................................................. 85

Independent Auditors’ Report on Compliance for Each Major Program and on Internal Control over Compliance Required by OMB Circular A-133 .................................................. 87

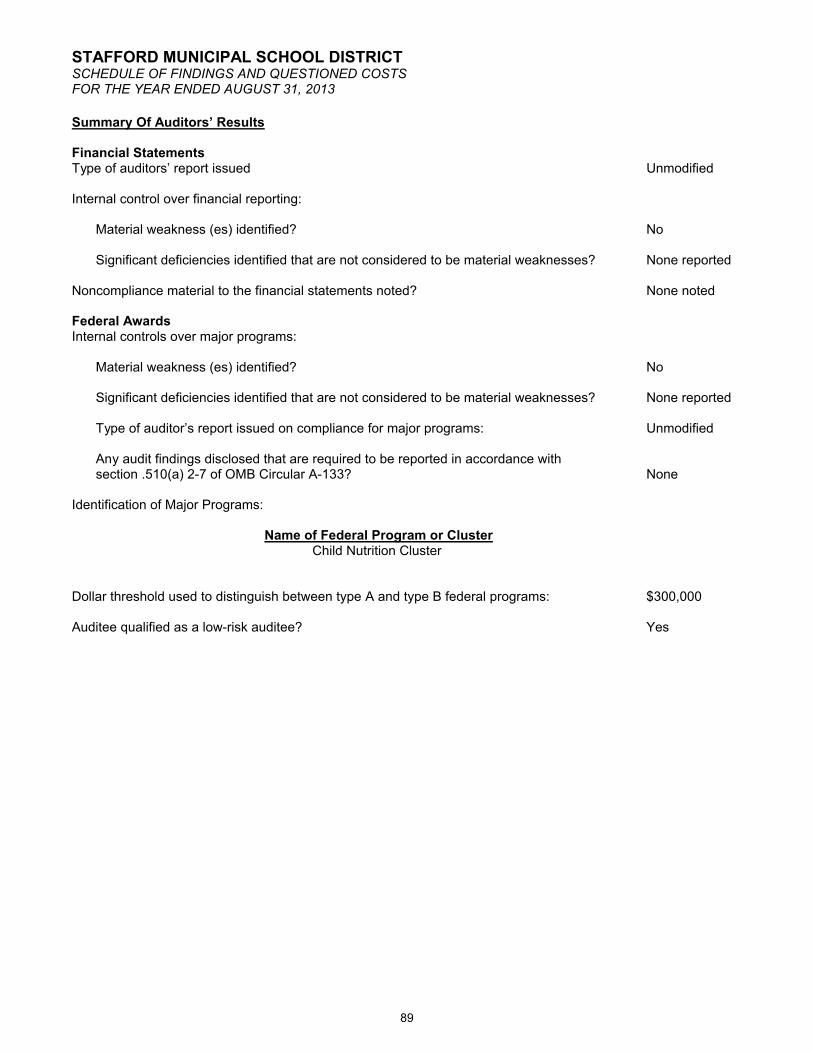

Schedule of Findings and Questioned Costs ........................................................................... 89

Summary Schedule of Prior Audit Findings.............................................................................. 90

Corrective Action Plan .............................................................................................................. 91

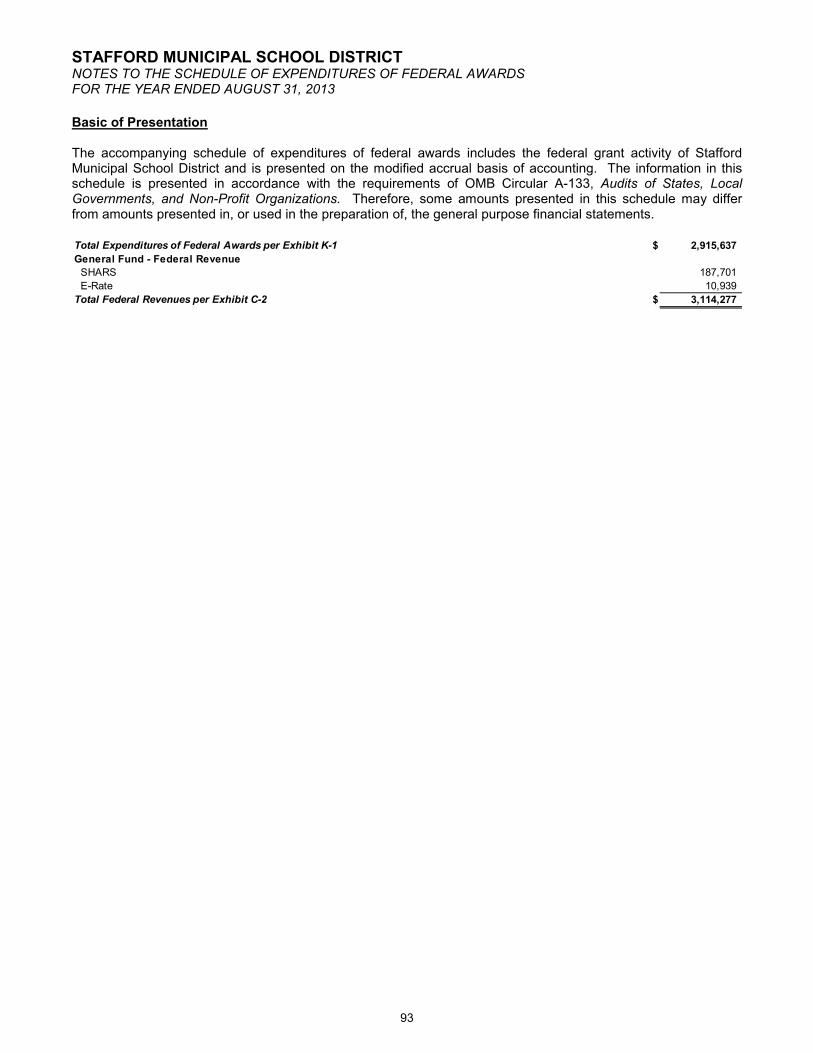

Schedule of Expenditures of Federal Awards .......................................................................... 92 Exhibit K-1

Notes to the Schedule of Expenditures of Federal Awards...................................................... 93

STATISTICAL SECTION

Financial Trends:

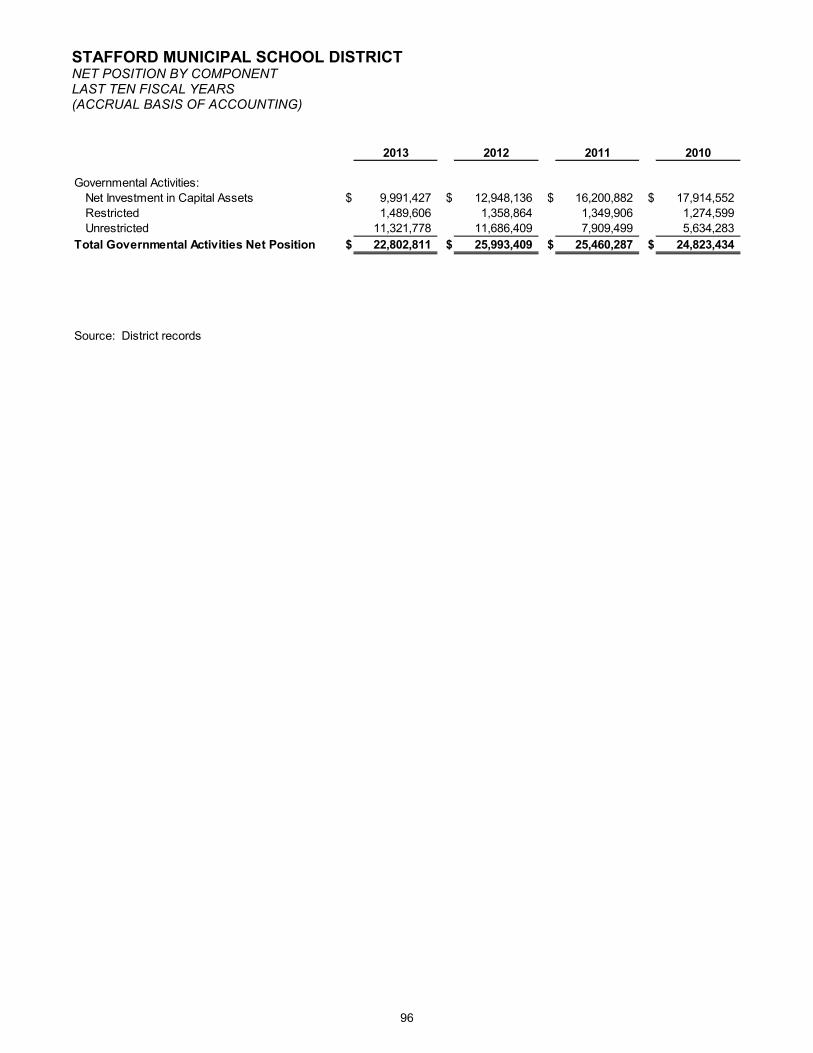

Net Position by Component – Last Ten Fiscal Years ............................................................... 96 Table L-1

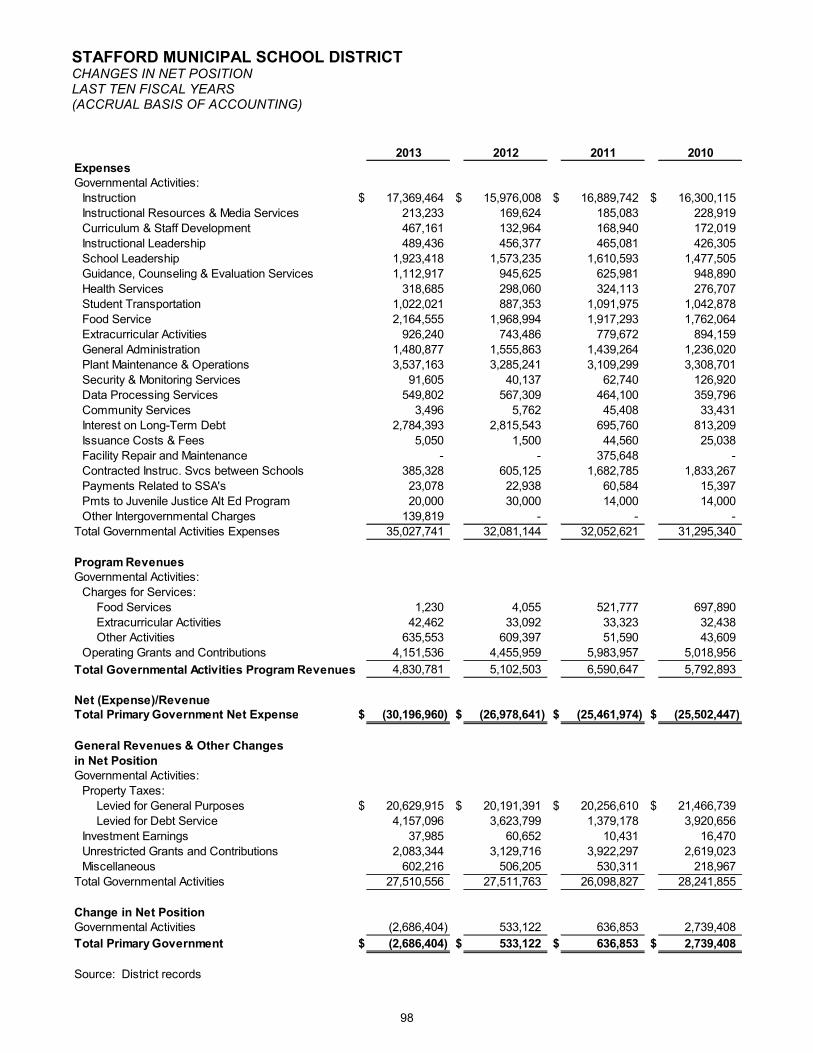

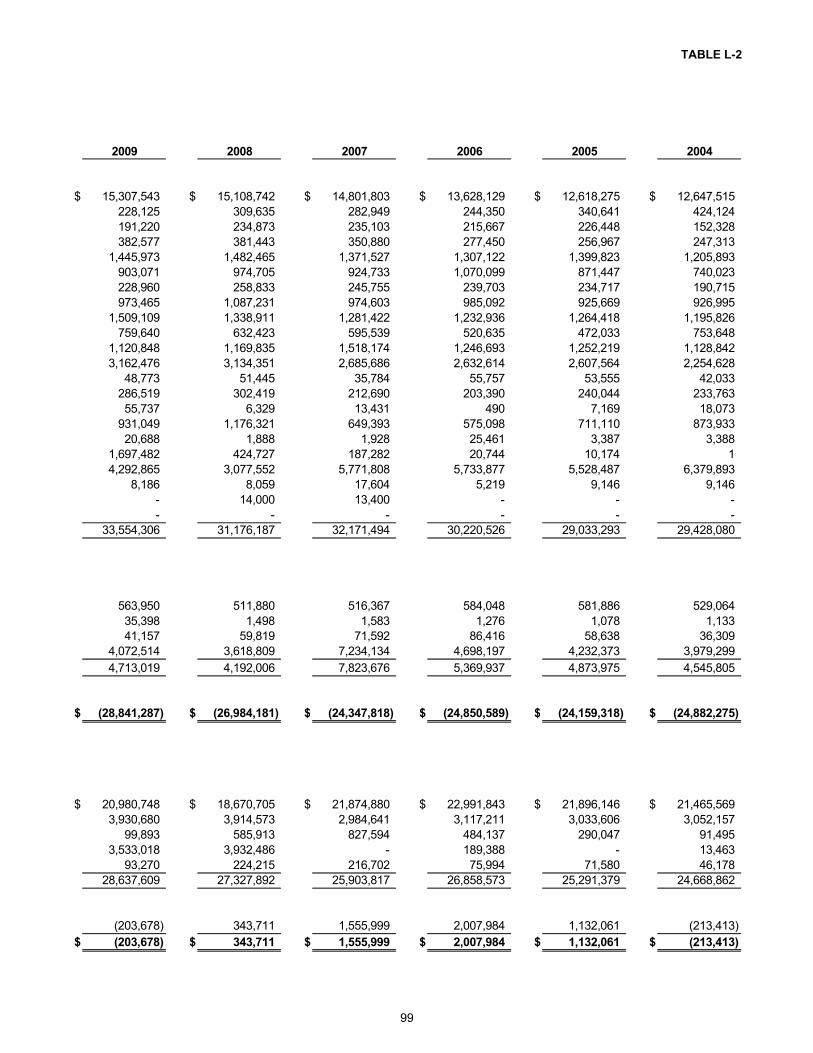

Changes in Net Position – Last Ten Fiscal Years .................................................................... 98 Table L-2

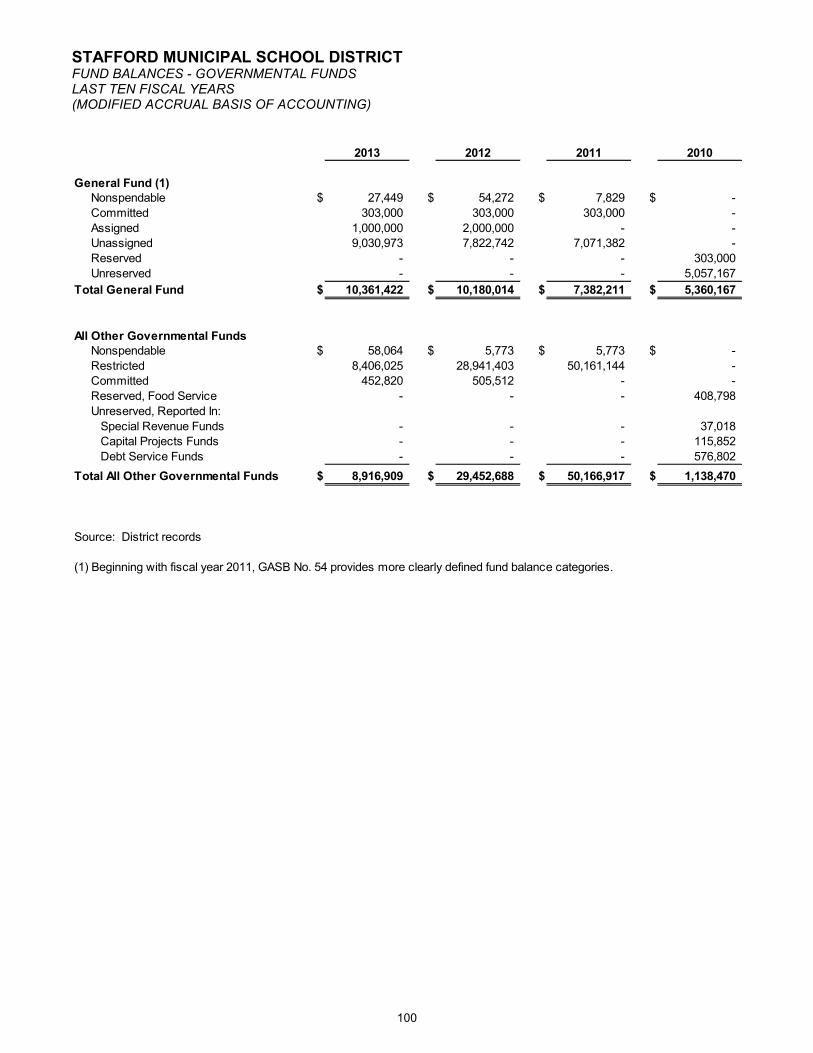

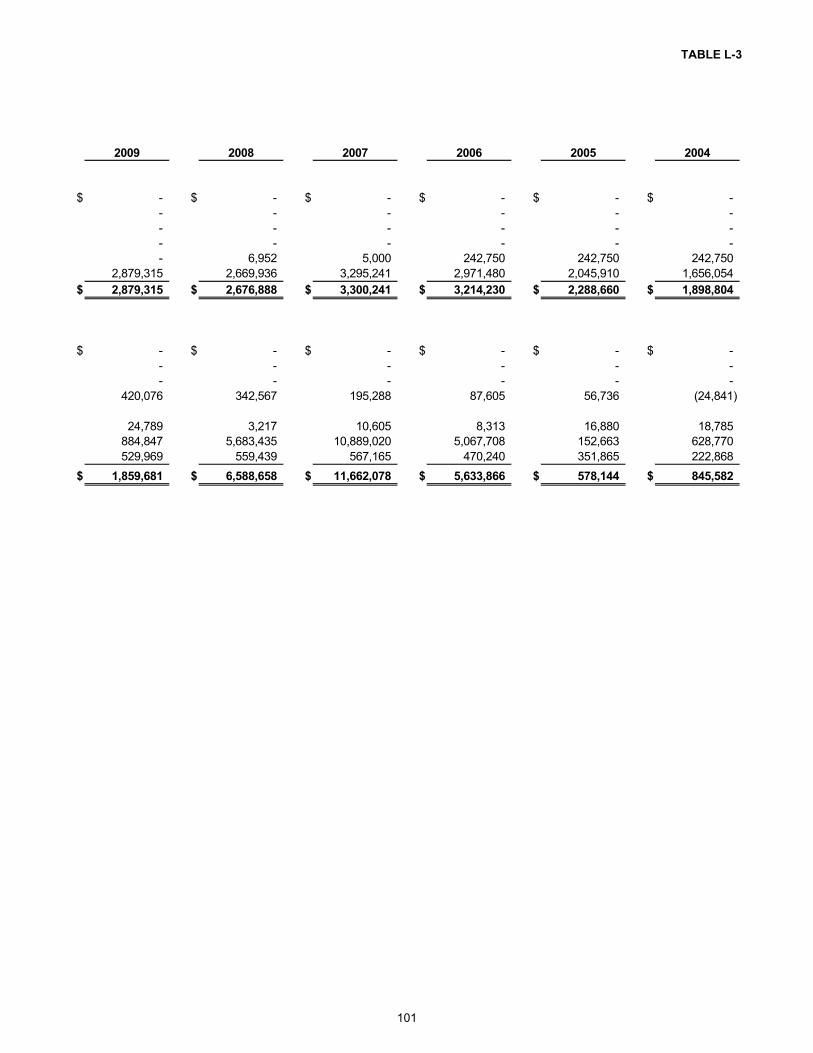

Fund Balances - Governmental Funds – Last Ten Fiscal Years.............................................. 100 Table L-3

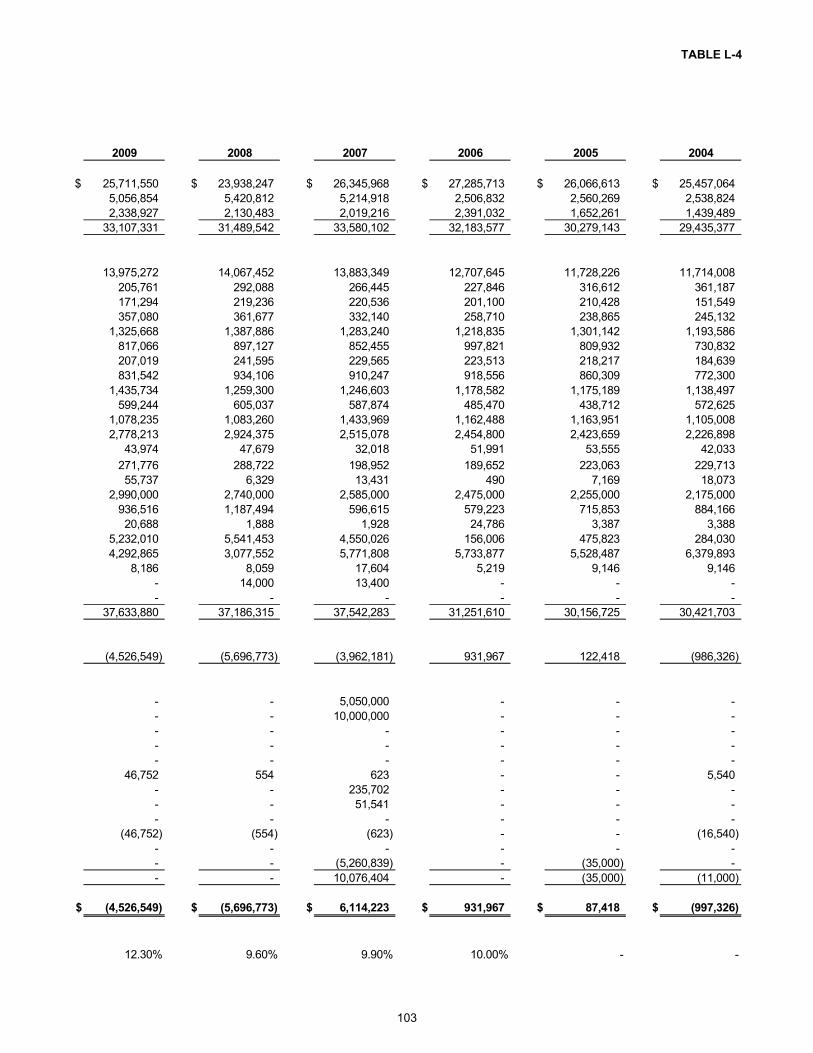

Changes in Fund Balances - Governmental Funds – Last Ten Fiscal Years .......................... 102 Table L-4

Revenue Capacity:

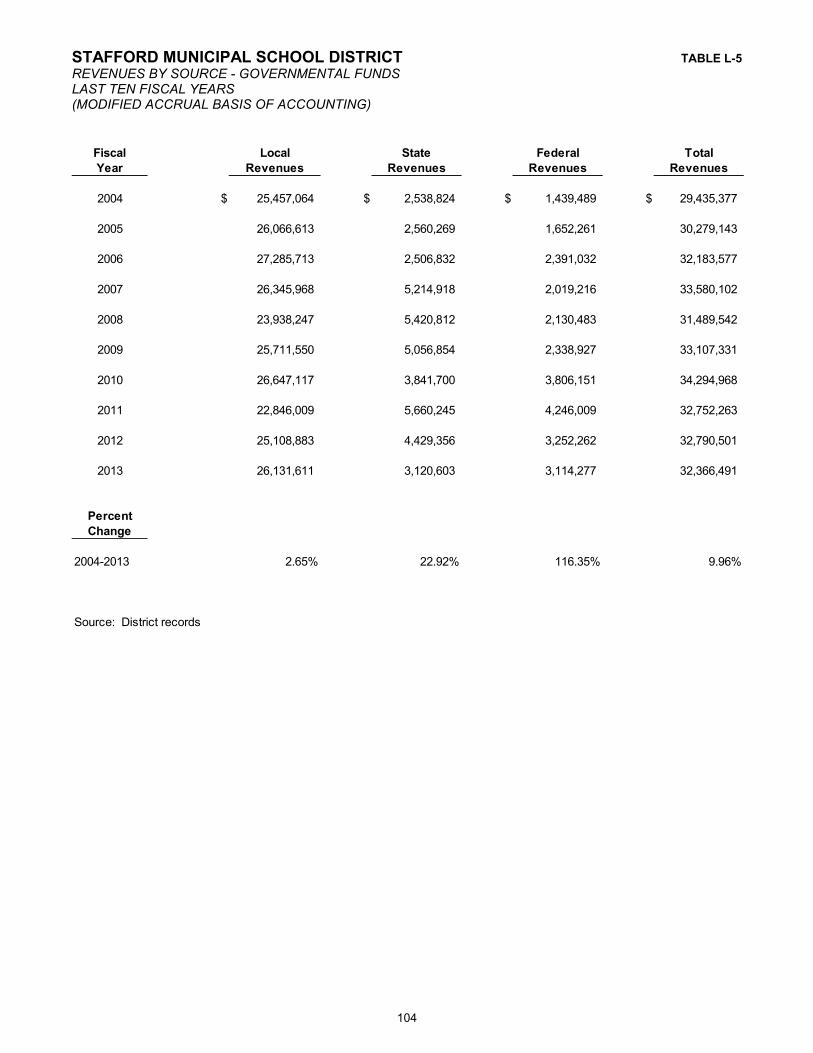

Revenues by Source - Governmental Funds – Last Ten Fiscal Years .................................... 104 Table L-5

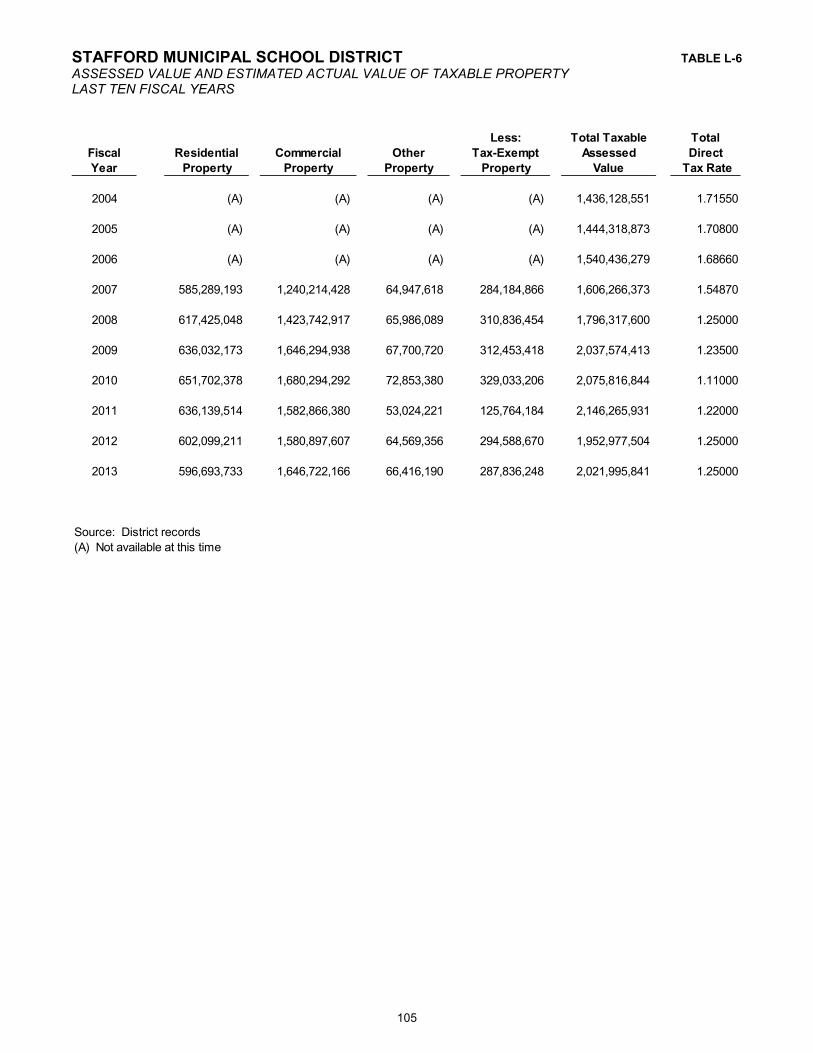

Assessed Value and Estimated Actual Value of Taxable Property – Last Ten Fiscal Years ... 105 Table L-6

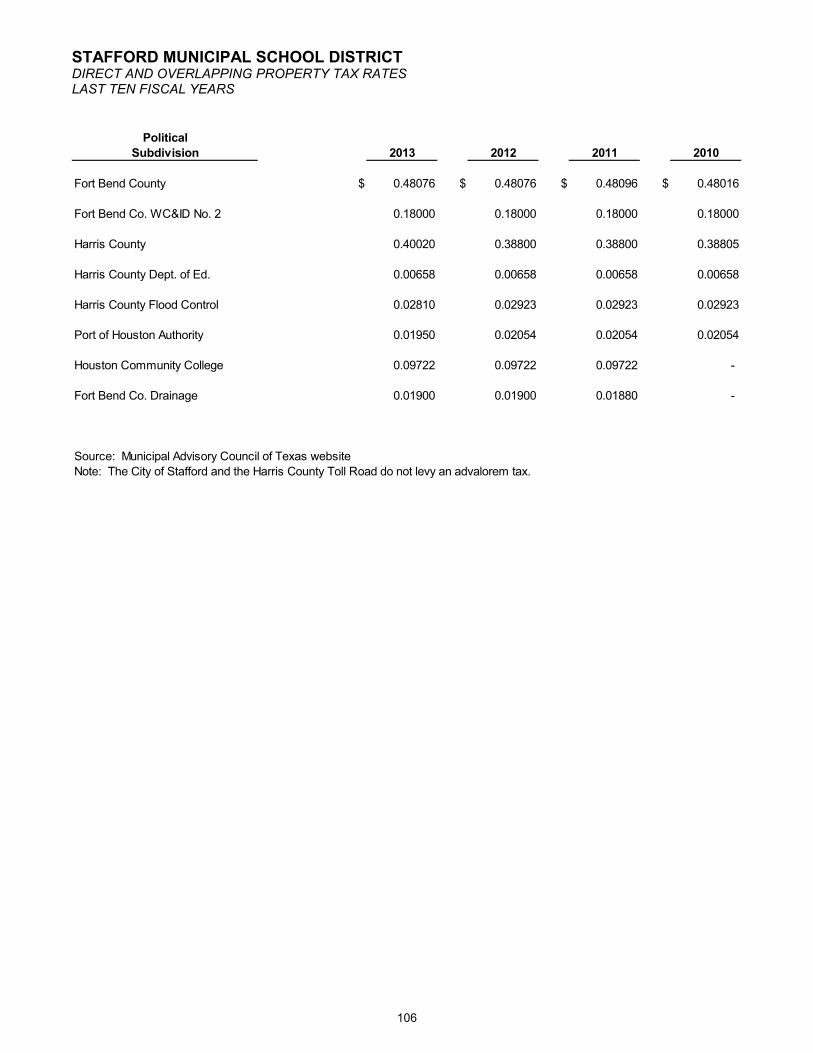

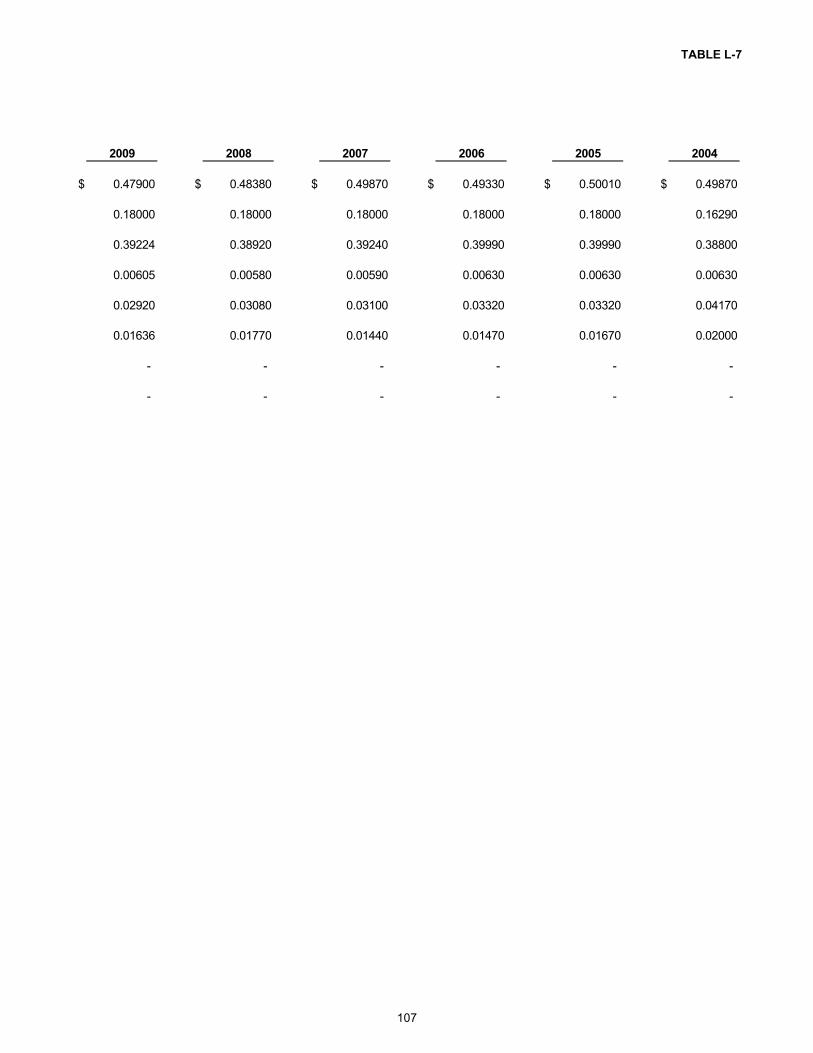

Direct and Overlapping Property Tax Rates – Last Ten Fiscal Years...................................... 106 Table L-7

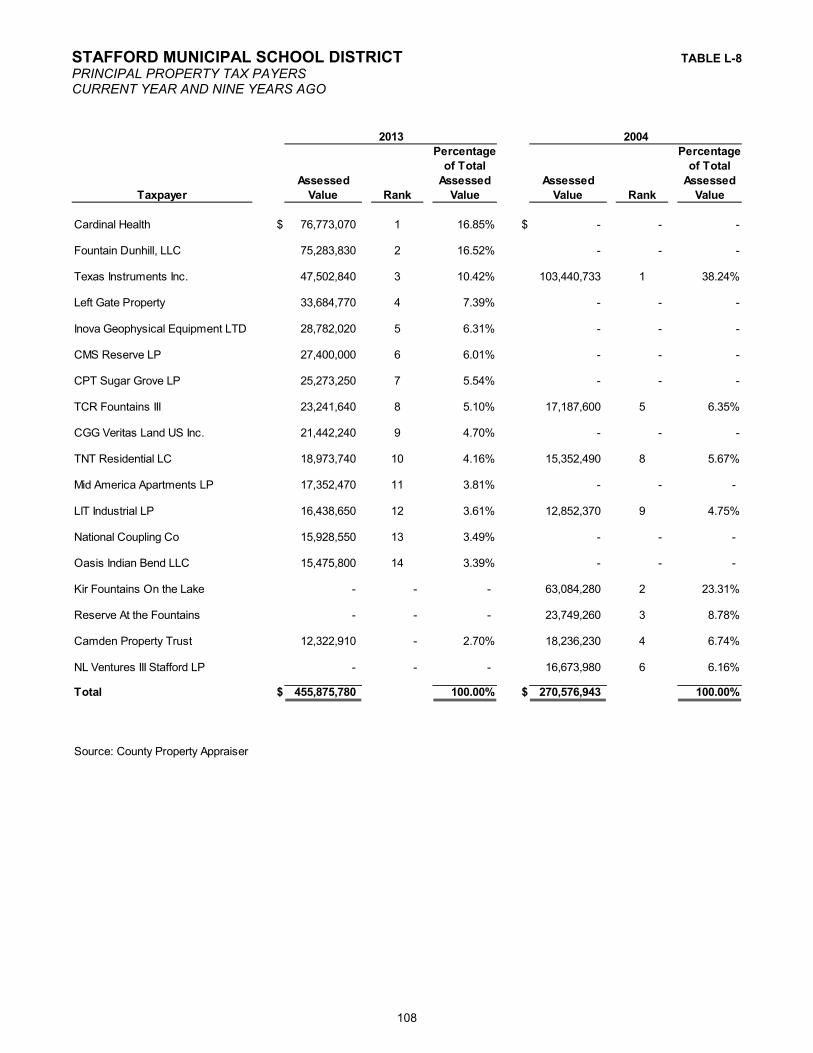

Principal Property Tax Payers – Current Year and Nine Years Ago........................................ 108 Table L-8

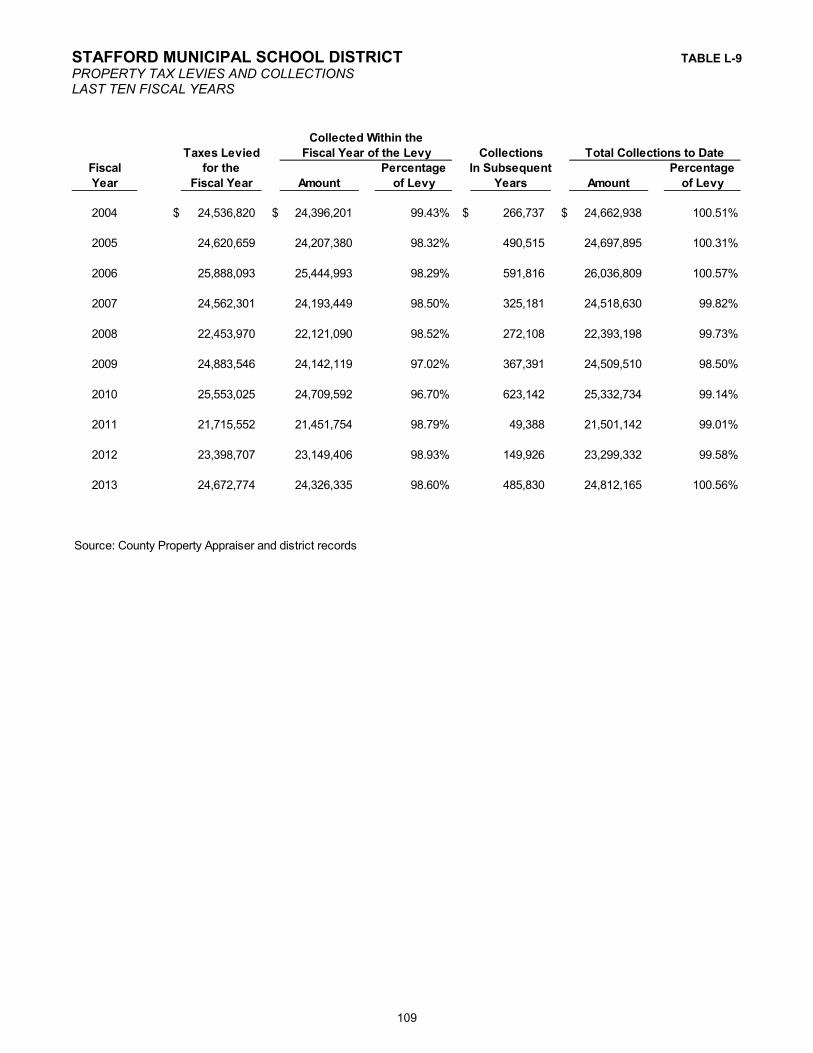

Property Tax Levies and Collections – Last Ten Fiscal Years ................................................. 109 Table L-9

STAFFORD MUNICIPAL SCHOOL DISTRICTCOMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE YEAR ENDED AUGUST 31, 2013

TABLE OF CONTENTS

Page Exhibit/Table

Debt Capacity:

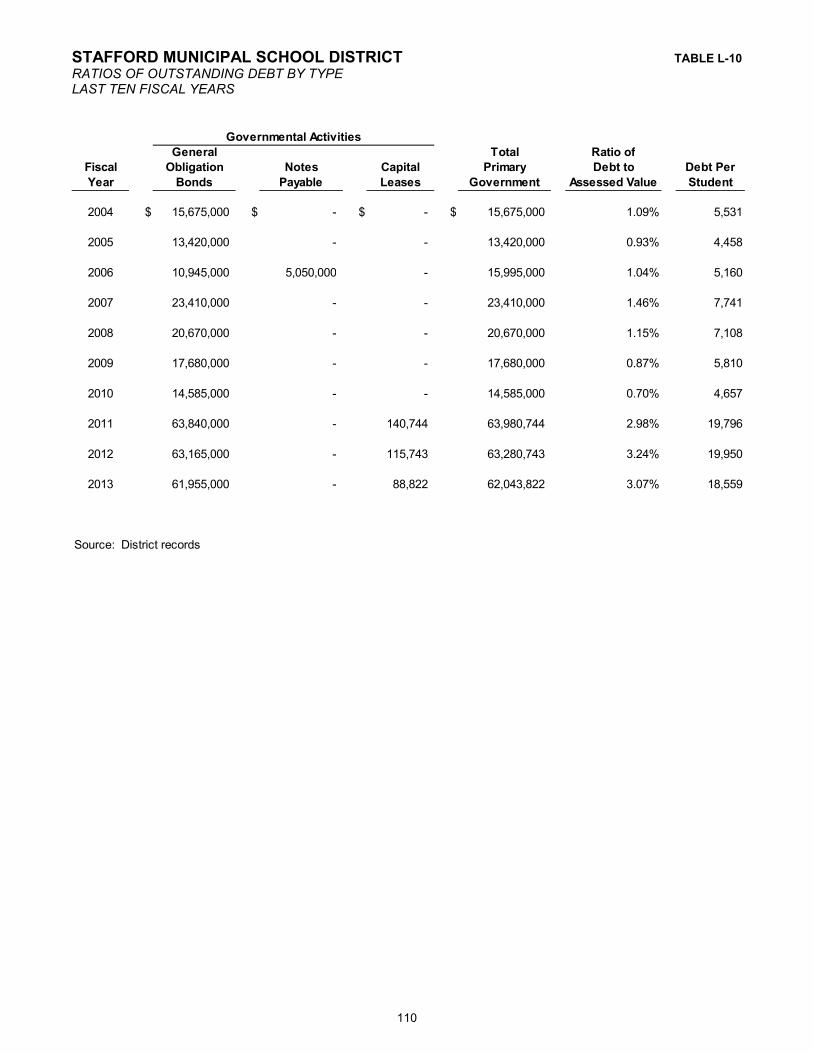

Ratios of Outstanding Debt by Type – Last Ten Fiscal Years.................................................. 110 Table L-10

Ratios of General Bonded Debt Outstanding – Last Ten Fiscal Years .................................... 111 Table L-11

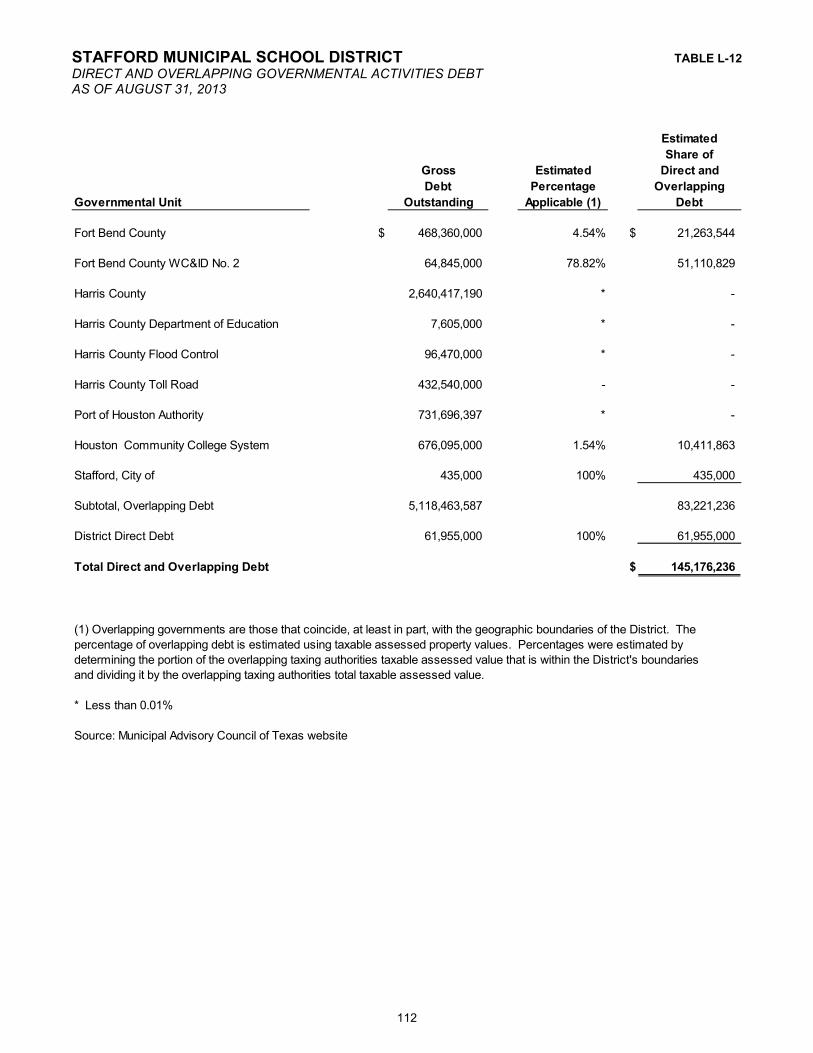

Direct and Overlapping Governmental Activities Debt ............................................................. 112 Table L-12

Demographic and Economic Information:

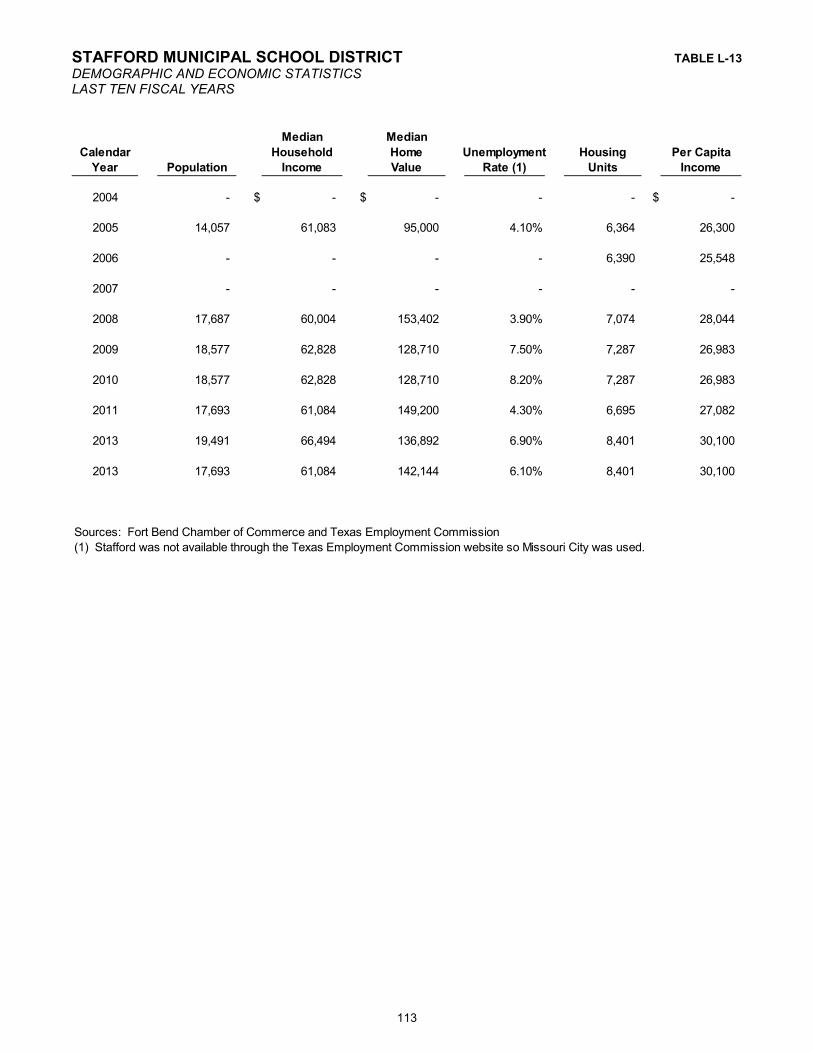

Demographic and Economic Statistics – Last Ten Fiscal Years .............................................. 113 Table L-13

Principal Employers – Current Year and Nine Years Ago........................................................ 115 Table L-14

Operating Information:

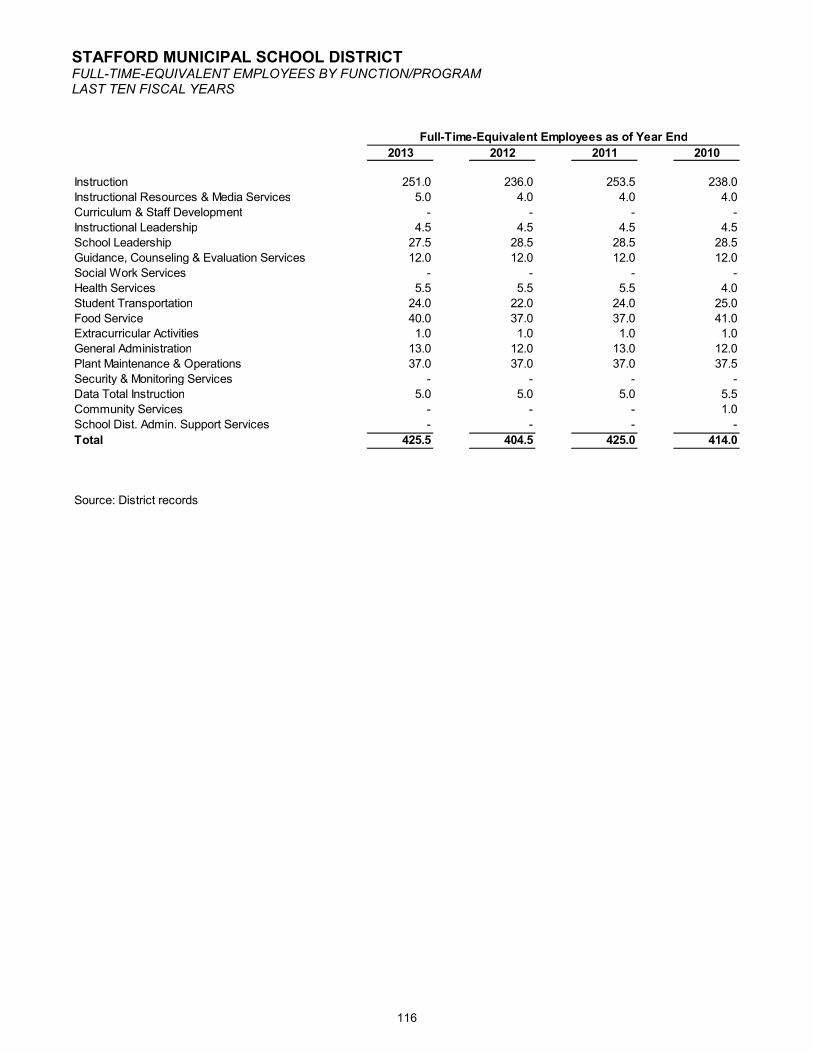

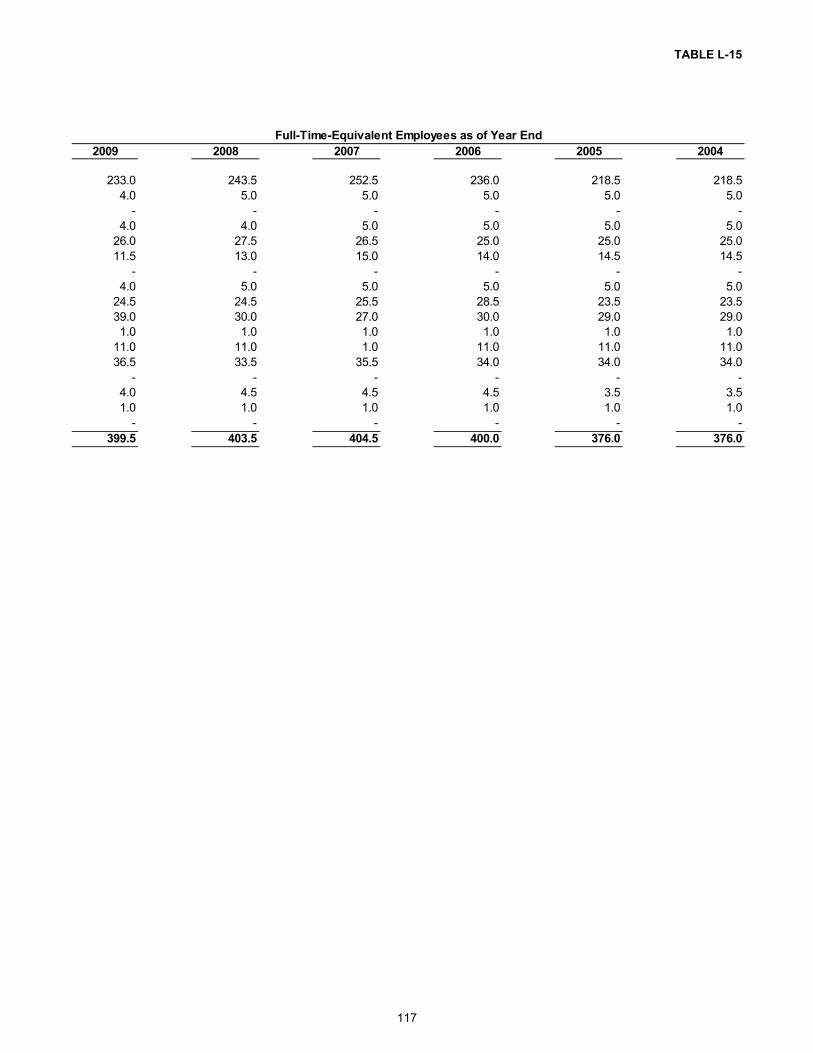

Full-Time-Equivalent Employees by Function/Program – Last Ten Fiscal Years .................... 116 Table L-15

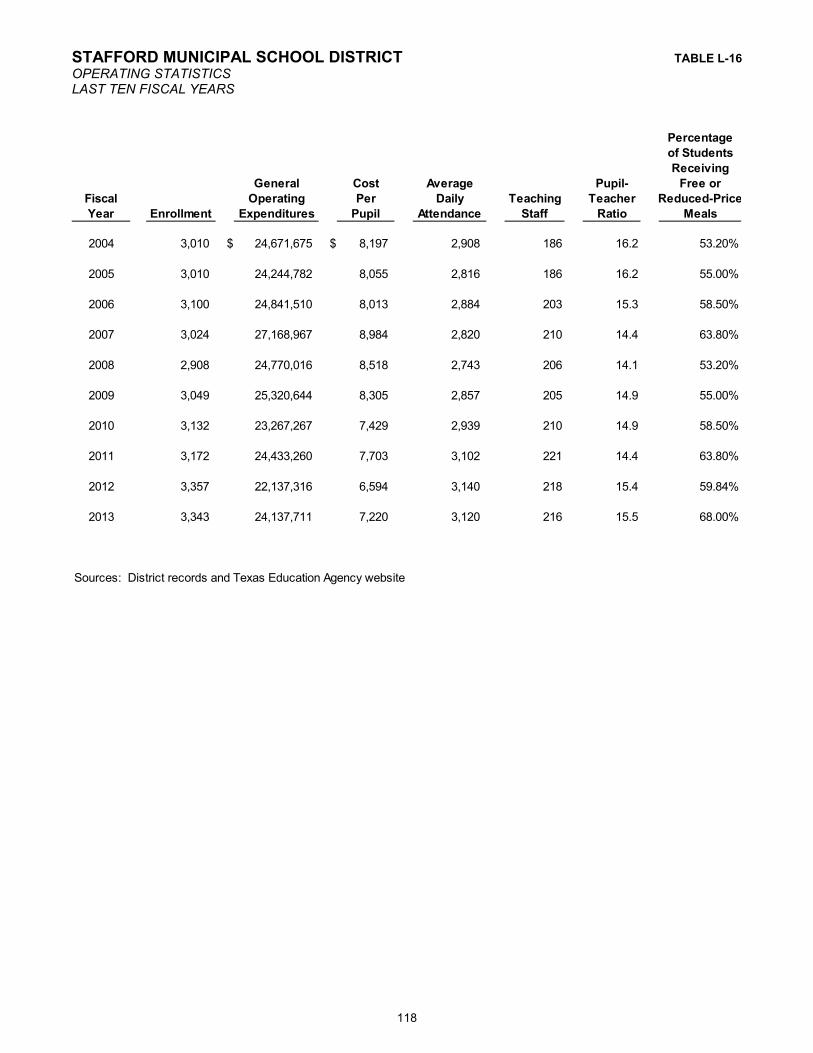

Operating Statistics – Last Ten Fiscal Years............................................................................ 118 Table L-16

Teacher Base Salaries – Last Ten Fiscal Years ...................................................................... 119 Table L-17

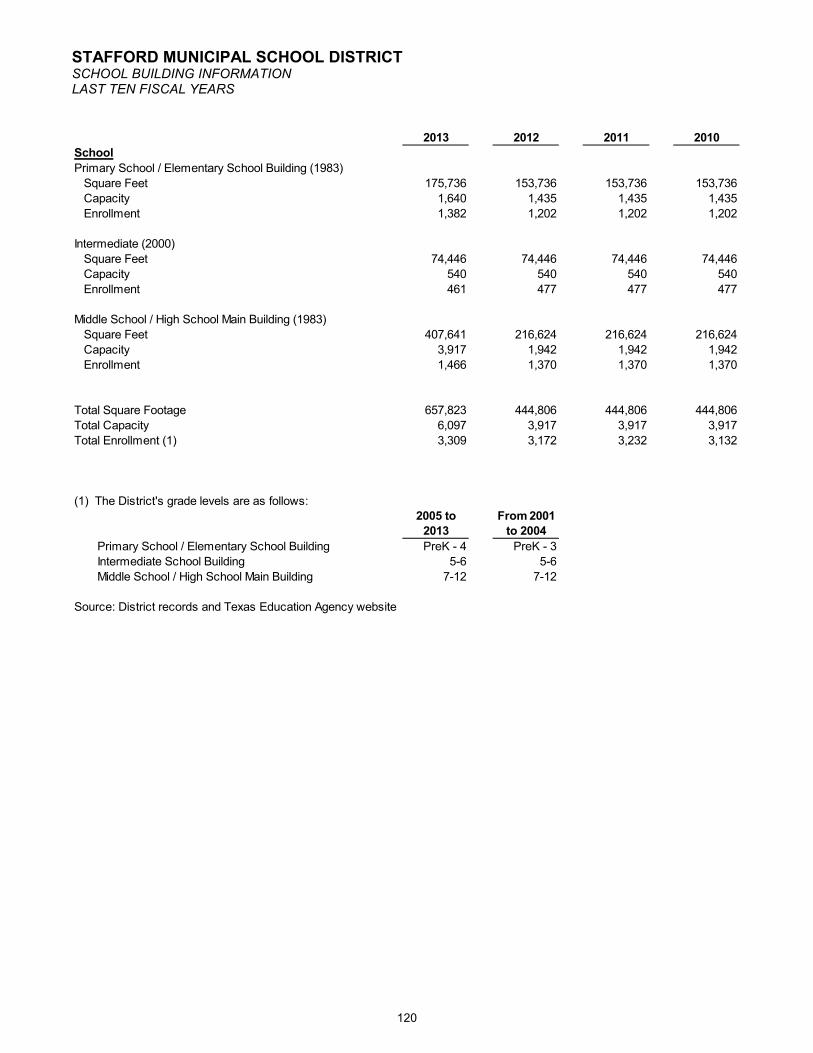

School Building Information – Last Ten Fiscal Years ............................................................... 120 Table L-18

This page is left blank intentionally.

Introductory Section

This page is left blank intentionally.

1

January 13, 2014

Board of TrusteesStafford Municipal School DistrictFort Bend and Harris Counties, Texas

Dear Board Members:

INTRODUCTION

State law requires that all general-purpose local governments publish within 150 days of the close of eachfiscal year a complete set of financial statements presented in conformity with generally accepted accountingprinciples (GAAP) and audited in accordance with generally accepted auditing standards by a firm of licensedcertified public accountants. Pursuant to that requirement, we hereby issue the Comprehensive Annual Financial Report (CAFR) of the Stafford Municipal School District (SMSD) for the fiscal year ended August 31, 2013.

The CAFR is presented in three sections: introductory, financial, and statistical. The Introductory Section includesthis transmittal letter, list of principal officials, list of consultants and advisors, and the District’s organizational chart. The Financial Section includes the basic financial statements and the combining and individual fund financial statements and schedules, as well as the auditor’s report on the basic financial statements and schedules. The Statistical Section includes selected financial and demographic information, generally presentedon a multiyear basis.

GAAP also requires that management provide a narrative introduction, overview, and analysis to accompany thebasic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittalis designed to complement MD&A and should be read in conjunction with it. The District’s MD&A can be foundimmediately following the report of the independent auditors.

This report consists of management’s representations concerning the finances of the District. Consequently, management assumes full responsibility for the completeness and reliability of all of the information presented inthis report. In order to provide a reasonable basis for making those representations, management of SMSDhas established a comprehensive internal control framework that is designed to protect the government’s assets from loss, theft, or misuse. Additionally, the internal control framework is designed to compile sufficient reliable information for the preparation of the District’s financial statements in conformity with GAAP. Since the costs of internal controls should not outweigh their benefits, the District’s comprehensive framework of internal controls has been designed to provide reasonable assurance rather than absolute assurance that the financial statementswill be free from material misstatement. To the best of our knowledge and belief, this financial report is complete and reliable in all material respects.

The financial statements of the Stafford Municipal School District have been audited by Hereford, Lynch, Sellars& Kirkham, P.C., a firm of licensed certified public accountants. The goal of the independent audit is to providereasonable assurance that the financial statements of the District for the fiscal year ended August 31, 2013 are free of material misstatement. The independent audit involves examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements; assessing the accounting principles used and significant estimates made by management; and evaluating the overall financial statement presentation. The independentauditors concluded, based upon the audit, that there was a reasonable basis for rendering an unmodified opinion that the District’s financial statements for the fiscal year ended August 31, 2013 are fairly presented in conformitywith GAAP. The independent auditor’s report is presented as the first component of the financial section of this report.

2

The independent audit of the financial statements is part of a broader, federally mandated “Single Audit” designedto meet the special needs of federal grantor agencies. The standards governing Single Audit engagementsrequire the independent auditor to report not only the fair presentation of the financial statements, but also on the audited government’s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal awards.

Copies of this report will be widely distributed throughout the Stafford Municipal School District. A copy will besent to the City of Stafford, the city’s Chamber of Commerce, Moody’s and Standard and Poor’s Financial Rating Services, the Municipal Advisory Council, the Single Audit Clearinghouse, and the Texas Education Agency.

PROFILE OF THE DISTRICT

In 1977, following a disannexation election, Stafford Municipal School District was created out of the 181-square-mile Fort Bend ISD and Houston ISD. The disannexation was the result of a grass roots movement toreturn to a small, city-based school system.

After passage of the election creating the district, the City of Stafford spent five years in federal and state courts in the pursuit of creating the school district. The Fifth Circuit Court of Appeals ruled in favor of the City of Staffordand the district became a reality. Becoming a municipal school district instead of an independent schooldistrict, the school partnered with the city in ways that increased the efficiency of the tax dollar for Stafford residents and businesses.

In the fall of 1982, the elementary school opened to the district’s first 547 students in a leased warehouse. Grades six through eleven were added the following year, bringing the total student enrollment to 1,057. Seniorswere added the next year. In 2000, the new Intermediate School was added to the district facilities onStaffordshire Drive, joining Primary, Elementary, Middle, and High Schools.

Enrollment in the District’s five campuses for the 2012/2013 school year was at 3343 while the Average Daily Attendance (ADA) was 3,120.

There are over 29 home languages spoken by our 3,343 students. Some of these include (but are not limited to):

Amharic, Arabic, Bengali, Cambodian, Cantonese, Farsi, French, Gujarati, Malayalam, Mandarin, Serbian, Sindhi, Telugu, Thai, Tigrinya, Tulu, Urdu, Vietnamese, Yoruba, Tagalog

The District occupies seven square miles within Fort Bend and Harris Counties with diverse geographic areas thatinclude the communities of Promenade, Kingsway, Dove Country, Stafford Run, and other neighborhoods.

The Stafford Municipal School District is an independent public educational governmental unit operating underapplicable laws, and regulations of the State of Texas which provides a full range of educational servicesappropriate to grade levels pre-kindergarten through twelfth grade. These include regular and enriched academic education, special education for handicapped students, occupational education, and educational services for those with limited English proficiency. These basic programs are supplemented by a wide variety of offerings infine arts, athletics, and other extracurricular programs.

A seven member Board of Trustees, with staggered three-year terms, governs the school district.

Effective September 1, 2003 Texas Education Code 11.303 was put into law and it provided for the City Council to participate jointly with the Board of Trustees for the following actions:

Hearings and work sessions on the budget and ad valorem tax rate Adopting of annual budget and ad valorem tax rates Authorization for bonded debt issuance

The District receives funding from local, state and federal funding sources. The District is included in one, the Cityof Stafford, governmental “reporting entity” as defined by the Governmental Accounting Standards Board (GASB) in its Statement Number 14, “The Financial Reporting Entity,” as revised by GASB Statement Number 39, andthere are no component units included within the reporting entity. Management of the District is independent of other state and local governments. The Fort Bend County Tax Assessor-Collector collects taxes for the District, but exercises no control over its expenditures.

3

The annual expenditure budget serves as the foundation for the District’s financial planning and control. Theobjective of these budgetary controls is to ensure compliance with legal provisions embodied in the annual expenditure budget. Stafford MSD has a diverse student population and the instructional methods that will bestsuit the needs of each student is given significant consideration by all parties involved in the budget process.

Budget-to-actual comparisons are provided in this report for the General Fund. This comparison is presented as required supplementary information.

BUDGETING

The annual budget serves as the foundation for the District’s financial planning and control. The budget process begins in January when the Long-Range Plan is presented to the Board of Trustees. The enrollment projectionscontained in this plan form the basis for significant budgetary decisions including per pupil allocations to eachcampus, instructional staffing allocations, and other required service levels. Once the Long-Range Plan isapproved, the SMSD Board of Trustees and City of Stafford City Council can begin discussions concerningbudget strategies and priorities, and establish the budget calendar. Personnel units are allocated to each campus based on projected student enrollment following state mandated ratios, as applicable. Each campus receives abasic allotment per student to be used for supplies, materials, equipment, staff development and other appropriate instructional costs. Decisions concerning utilization of this allocation are made by the site-baseddecision making teams. Budgets for non-campus units are developed by department heads and reviewed by the Superintendent and Chief Financial Officer. Following the budget development process, consolidated budgetary information is presented to the Board of Trustees and City Council in workshops and regular meetings. The proposed budget must be prepared by August 31st for a September 1st fiscal year start date. The BoardPresident must call a special joint meeting for the purpose of discussing and adopting the budget and the taxrate. A notice of this meeting is required to be published at least ten days, but not more than 30 days before the public meeting.

Budget-to-actual comparisons are provided in this report for each individual governmental fund or program for which an appropriated annual budget has been adopted.

The budget may be amended during the year to address unanticipated or changing needs of the District. Changes to functional expenditure categories require Board of Trustee approval. However, budget changes not requiringan increase in total appropriations and within functional categories may be approved by management without Board approval.

FACTORS AFFECTING FINANCIAL CONDITION

IntroductionThe information presented in the financial statements is perhaps best understood when it is considered from thebroader perspective of the specific environment within which the Stafford Municipal School District operates.

Local EconomyThe local economy is based predominantly on commercial and industrial activities. Cardinal Health 411, Inc., is our largest taxpayer for the District. The Fountains is also located in the District - a division of Dunhill PartnersInc.

Stafford has a population of approximately 18,500 and in 2008 the city was named by the Fortune SmallBusiness magazine as one of the 100 best places to live and launch. Stafford ranked 36th for its minimal taxes, cheap housing and ample available land.

The median market value of a residence in Stafford is $142,144 and those taxpayers enjoy a 20% local homestead exemption, a low school district tax rate, and no city property tax.

AccessMajor access to the District is provided by U.S. Highway 59, which extends from Houston to the Rio Grande Valley, and U.S. Highway 90-A, which travels westward through the District to San Antonio and to the Davis Mountains of West Texas.

4

EnrollmentApproximately 21.6% of SMSD students reside in apartments, while the remaining 78.4% reside in variousresidential areas in or around Stafford. Since apartment construction and occupancy rates heavily influence enrollment rates, SMSD personnel carefully monitor these factors during the year.

The District continued the Limited Open Enrollment (LOE) program in 2012/2013. The LOE program allows fornon-Stafford students to attend the Stafford Municipal School District tuition free as long as they have met ourstringent criteria. This program brought in well over 500 students each of the past five years.

The District provides employees (of SMSD and the City of Stafford) living outside of Stafford the option toenroll their children in SMSD. For 2012/2013, SMSD had 65 inter-district students enrolled.

The economic disadvantage rate of the District continues to increase annually and finished at 68.23% for the 2012/13 school year.

State FundingThe State of Texas provides funding for public education via a financing formula which weights student attendance levels, property value per student, the District’s tax effort, and regional variations in payroll and othercosts. The District is considered a “property-rich” school district because the assessed value of property perstudent is higher than the target amount established by the Texas Legislature. The target taxable value perstudent enforced for 2012/13 was $476,500, while the comparable value for the District was $508,136.

Statewide, many districts were taxing at $1.50 tax cap for maintenance and operations in 2005/2006. TheLegislature passed House Bill 1 (H.B.1) mandating districts to compress tax rates by 88.67% of the2005/2006 maintenance and operations tax rate ($1.321183 for SMSD) for 2006/2007 and by 66.67% of the2005/2006 maintenance and operations tax rates ($0.993383 for SMSD) for 2007/2008. Districts were then able to assess an additional four cents above the compressed rate for enrichment without a voter election. The Stateholds each district harmless by capping the target revenue as combined state and local revenue per weighted student the district had in 2005/2006, or would have had in 2006/2007 under old law. This adjustment to the target essentially holds the District’s combined state and local revenue at the amount received in 2005/2006 per weighted student level.

Since SMSD is “property-rich” school district, the District paid over $385,000 to the State for redistribution to “property-poor” school districts.

Cash ManagementCash available in excess of cash requirements was invested in the one of three investment pools used by the District and government agency securities. Stafford MSD participates in Texpool, TexStar, and Lone Starinvestment pool. The District’s investment policy is to minimize risk while maintaining a competitive yield on its portfolio. The District’s deposits were entirely covered by Federal Deposit Insurance Corporation (FDIC) insurance and pledged collateral for the year ended August 31, 2013.

To comply with the reporting requirements set forth in House Bill 2459, quarterly investment reports were prepared and submitted to the Board of Trustees. The reports detailed the District’s investment position as of theend of each quarter and reflected the compliance with the District’s investment strategy and the investment policies.

In addition to the quarterly report, the Board of Trustees of Stafford MSD requires that a comprehensive report onthe investment program and investment activity be presented annually. The annual report shall include a reviewof the activities and total yield for the preceding 12 months, suggest policies, strategies, and improvements that might enhance the investment program, and propose an investment plan for the next year. SMSD has complied with this requirement for 2013/2014.

Debt ManagementThe Texas Education Code Section 45.003(e) specifies that a school district is able to issue unlimited tax bonds,provided that the district demonstrates its projected ability to pay such bonds plus the District’s outstandingbonds (excluding bonds authorized by an election held on or before April 1, 1992 and issued before September 1, 1992) at a debt service rate of not more than $0.50 per $100 of assessed valuation. Stafford MSD’s debtservice tax rate in 2012/13 was $0.20995 which is well below the legal limit.

5

Risk ManagementThe District’s risk management program encompasses various means of protecting the District against loss.District instructional facilities range in age from twenty-six to one year. Property and casualty insurance onall facilities, fixtures, and equipment is provided by commercial carriers and liability insurance coverage isprovided by North American Solutions. The District strives to ensure the safety and health of the students andemployees through its accident prevention programs, safety education programs, and safety inspections.

In addition, the District strives to maintain employee benefit programs designed to retain and attract qualifiedpersonnel. To achieve this, the District participates in TRS Active-Care (health insurance program administered through the State) and offers various types of insurance coverage to employees through our Third Party Administrator, TCG. Portions of the coverage available (such as medical, dental and life insurance) are partially paid by the District. The District also participates in a worker’s compensation program through Creative Risk Funding.

MAJOR INITIATIVES AND ACCOMPLISHMENTS

Community SupportIn November 2006, the voters in the Stafford Municipal School District approved a $15.05 million bondreferendum.

In May 2011, the voters in the Stafford Municipal School District approved a $49.9 million bond referendum.

The mission statement of the District is to “Prepare each student to become a critical thinker and an ethical, productive citizen, in the pursuit of excellence through an unwavering commitment to provide multiple life and learning experiences led by dedicated professionals using innovative teaching techniques in an engaging learning environment.” Continuing to aggressively implement the Long-Range Technology Plan not only demonstrates theDistrict’s effort to accomplish this mission but also enables children to experience hands on learning by utilization of leading edge technologies. Computer labs were updated to improve academic success through computer-assisted learning. Secondary Math and Science classrooms were outfitted with ceiling-mounted projectors toutilize promethean board instructional technology. The success of these and many other programs is evident in the continued improvement in student performance on the Texas Assessment of Knowledge and Skills (TAKS) Test.

The 2012/13 financial structure of the Stafford Municipal School District provided support to work toward or accomplish the following goals:

1. Attract and retain a highly-qualified staff. The education of students is a labor-intensive process andpayroll expenditures comprise approximately 78.74% of the General Fund expenditures. The Board voted to approve a 3% salary increase for all personnel. The District is offers competitive salaries with neighboring school districts.

2. Maintain a fiscally responsible tax rate. In 2012/13, the tax rate was compressed to $1.04005 asrequired by H.B. 1 while keeping the general fund balance of approximately $10 million. This fund balance represents approximately 5 months of operating expenditures.

3. Provide educational programs and activities that ensure all students are ready for higher education and/or the workforce. The District has been able to continue financially supporting programs such as math and science pull-out programs, automotive technology, an engineering academy, etc.

A Eleventh Consecutive Schools FIRST Superior RatingThe Stafford Municipal School District received a rating of “Superior Achievement” under the School FinancialIntegrity Rating System of Texas (FIRST), which is the highest rating possible, for the 11

thconsecutive year.

The FIRST rating system is a financial accountability system for Texas school districts developed by the TexasEducation Agency (TEA) in response to Senate Bill 875 of the 76th Texas Legislature in 1999. The primarygoal of Schools FIRST is to achieve quality performance in the management of school districts' financialresources, a goal made more significant due to the complexity of accounting associated with Texas' schoolfinance system.

7

8

9

10

11

12

STAFFORD MUNICIPAL SCHOOL DISTRICTLIST OF PRINCIPAL OFFICIALS AND ADVISORSAUGUST 31, 2013

BOARD OF TRUSTEES

Name OfficeEd Casitllo PresidentVirginia Rosas Vice PresidentGreg Holsapple SecretaryEttienne Zak TrusteeCindy Hoelscher TrusteeRodney Butler TrusteeAuturo Jackson Trustee

CITY COUNCIL

Council Member PositionLeonard Scarcella MayorFred Woolridge Mayor Pro TemCecil Willis CouncilmanWen Guerra CouncilmanKen Mathew CouncilmanFelecia Evans-Smith CouncilmanRobert Sorbet Councilman

ADMINISTRATIVE OFFICIALS

Name of Official PositionDr. Lawrence Hindt SuperintendentKen Gregorski Assistant SuperintendentMarva Rasberry Assistant SuperintendentCarla Merka Chief Financial Officer

CONSULTANTS AND ADVISORS

Name Advisory RoleHereford, Lynch, Sellars & Kirkham, P.C. AuditorsAndrew Kurth LLP Bond CounselFrost National Bank Depository BankRBC Capital Markets Financial AdvisorThompson & Horton LLP General Counsel

13

FINANCIAL SECTION

14

HLSKHereford, Lynch, Sellars & Kirkham

Certified Public Accountants • A Professional Corporation

Conroe Members of the Cleveland1406 Wilson Rd., Suite 100 American Institute of Certified Public Accountants 111 East BootheConroe, Texas 77304 Texas Society of Certified Public Accounts Cleveland, Texas 77327Tel 936-756-8127 Private Companies Practice Section Tel 281-592-6443Metro 936-441-1338 of the AICPA Division for Firms Fax 281-592-7706Fax 936-756-8132

INDEPENDENT AUDITORS’ REPORT

The Board of Trustees of Stafford Municipal School District1625 StaffordshireStafford, Texas 77477

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of Stafford Municipal School District (District), as of and for the year ended August 31, 2013, and the related notes to the financial statements, which collectively comprise the District's basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessments of the risk of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

15

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund, and the aggregate remaining fund information of Stafford Municipal School District, as of August 31, 2013, and the respective changes in financial position, thereoffor the year then ended in accordance with accounting principles generally accepted in the United States of America.

Emphasis of Matter

As described in Note A. 3. Implementation of New Standard in the notes to the financial statements, for August 31, 2013, the District adopted new accounting guidance, GASB Statement No. 65, Items Previously Reported as Assets and Liabilities. Our opinion is not modified with respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and budgetary comparison information, as listed in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Government Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise Stafford Municipal School District’s basic financial statements. The introductory section, combining and individual fund financial statements, and statistical section, are presented for purposes of additional analysis and are not a required part of the basic financial statements. The schedule of expenditures of federal awards is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is also not a required part of the financial statements.

The combining and individual fund financial statements and other supplementary information, including the schedule of expenditures of federal awards, are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual fund financial statements and the schedule of expenditures of federal awards are fairly stated in all material respects in relation to the basic financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

16

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated January 13, 2014, on our consideration of the Stafford Municipal School District’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Stafford Municipal School District’s internal control over financial reporting and compliance.

Respectfully,

Hereford, Lynch, Sellars & Kirkham, P.C.

HEREFORD, LYNCH, SELLARS & KIRKHAM, P.C.Certified Public Accountants

Conroe, TexasJanuary 13, 2014

17

Management's Discussion and Analysis

18

This page is left blank intentionally.

19

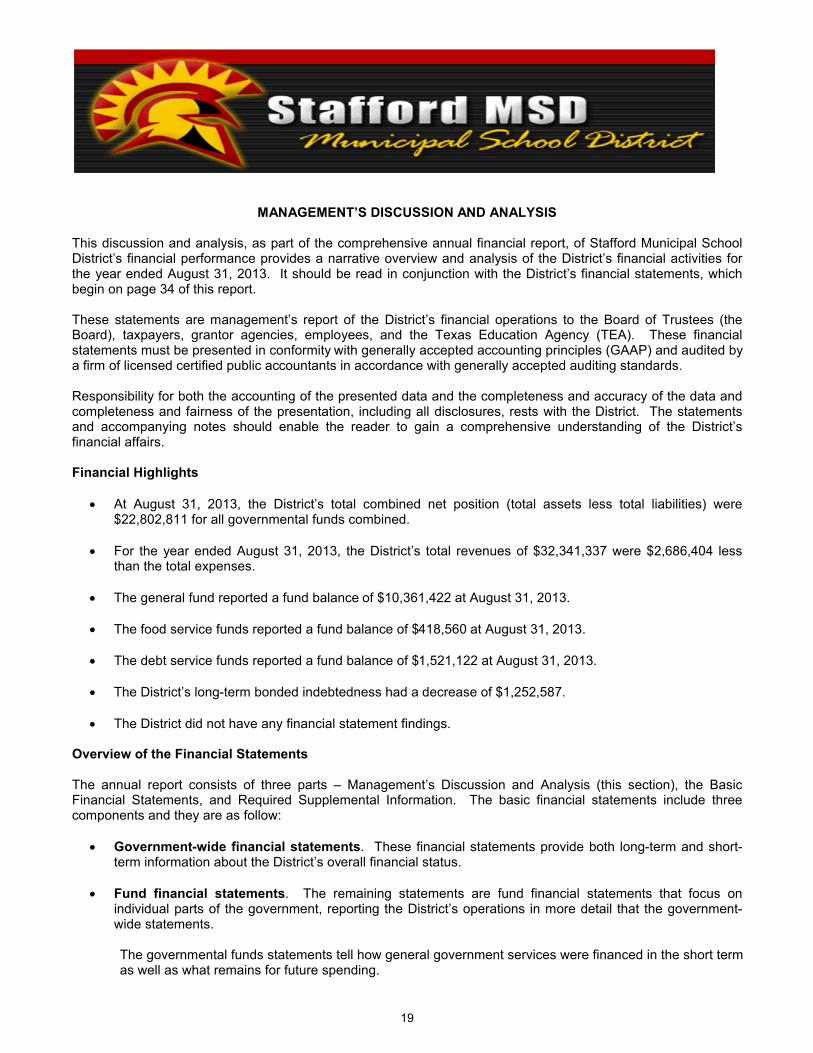

MANAGEMENT’S DISCUSSION AND ANALYSIS

This discussion and analysis, as part of the comprehensive annual financial report, of Stafford Municipal School District’s financial performance provides a narrative overview and analysis of the District’s financial activities for the year ended August 31, 2013. It should be read in conjunction with the District’s financial statements, which begin on page 34 of this report.

These statements are management’s report of the District’s financial operations to the Board of Trustees (the Board), taxpayers, grantor agencies, employees, and the Texas Education Agency (TEA). These financial statements must be presented in conformity with generally accepted accounting principles (GAAP) and audited by a firm of licensed certified public accountants in accordance with generally accepted auditing standards.

Responsibility for both the accounting of the presented data and the completeness and accuracy of the data and completeness and fairness of the presentation, including all disclosures, rests with the District. The statements and accompanying notes should enable the reader to gain a comprehensive understanding of the District’s financial affairs.

Financial Highlights

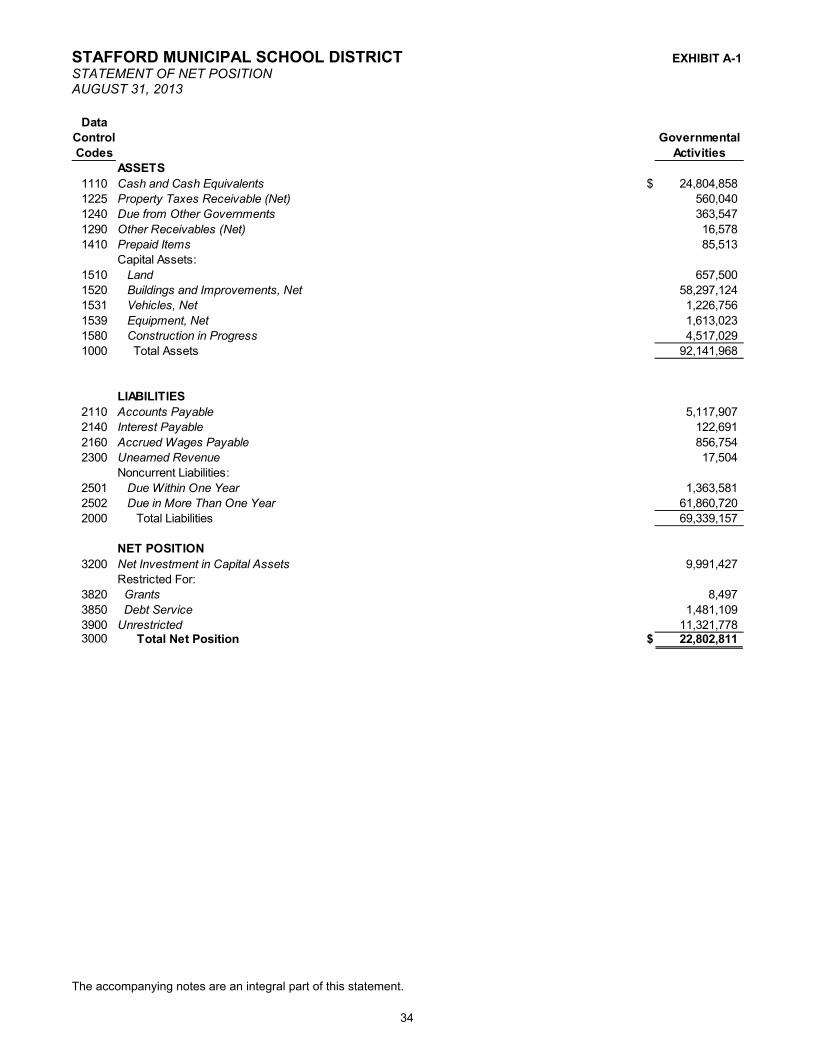

At August 31, 2013, the District’s total combined net position (total assets less total liabilities) were $22,802,811 for all governmental funds combined.

For the year ended August 31, 2013, the District’s total revenues of $32,341,337 were $2,686,404 lessthan the total expenses.

The general fund reported a fund balance of $10,361,422 at August 31, 2013.

The food service funds reported a fund balance of $418,560 at August 31, 2013.

The debt service funds reported a fund balance of $1,521,122 at August 31, 2013.

The District’s long-term bonded indebtedness had a decrease of $1,252,587.

The District did not have any financial statement findings.

Overview of the Financial Statements

The annual report consists of three parts – Management’s Discussion and Analysis (this section), the Basic Financial Statements, and Required Supplemental Information. The basic financial statements include three components and they are as follow:

Government-wide financial statements. These financial statements provide both long-term and short-term information about the District’s overall financial status.

Fund financial statements. The remaining statements are fund financial statements that focus on individual parts of the government, reporting the District’s operations in more detail that the government-wide statements.

The governmental funds statements tell how general government services were financed in the short term as well as what remains for future spending.

20

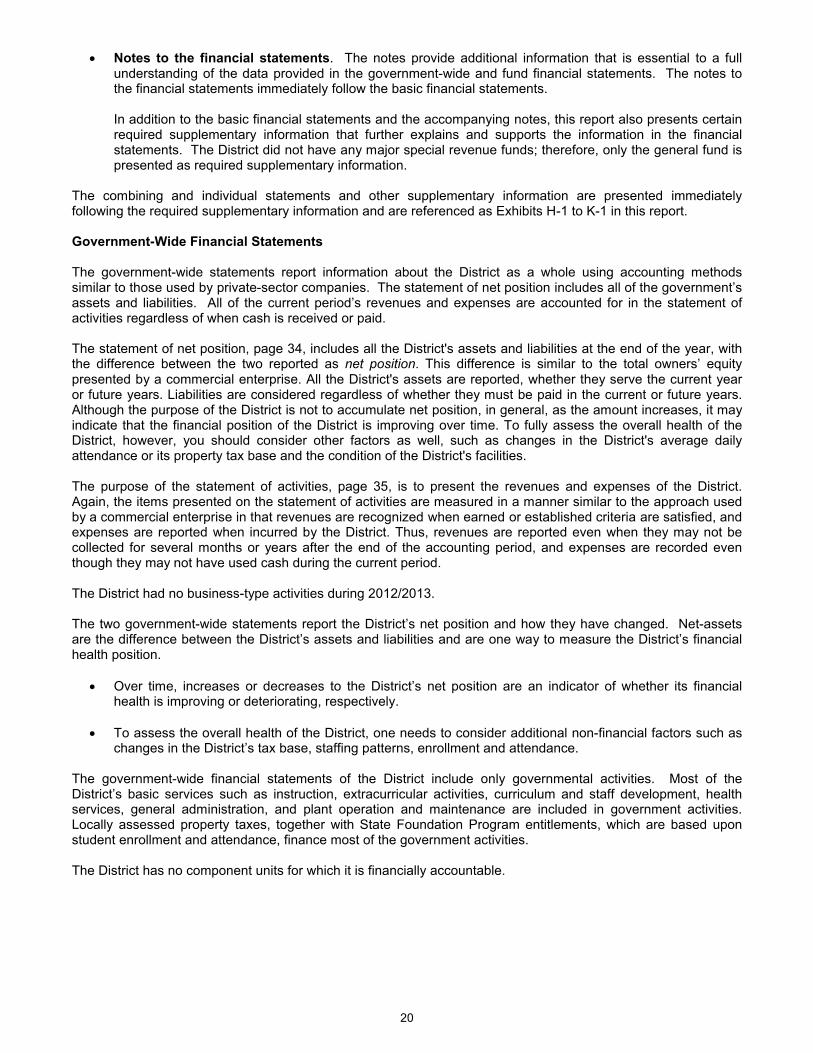

Notes to the financial statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements immediately follow the basic financial statements.

In addition to the basic financial statements and the accompanying notes, this report also presents certain required supplementary information that further explains and supports the information in the financial statements. The District did not have any major special revenue funds; therefore, only the general fund is presented as required supplementary information.

The combining and individual statements and other supplementary information are presented immediately following the required supplementary information and are referenced as Exhibits H-1 to K-1 in this report.

Government-Wide Financial Statements

The government-wide statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The statement of net position includes all of the government’s assets and liabilities. All of the current period’s revenues and expenses are accounted for in the statement of activities regardless of when cash is received or paid.

The statement of net position, page 34, includes all the District's assets and liabilities at the end of the year, with the difference between the two reported as net position. This difference is similar to the total owners’ equity presented by a commercial enterprise. All the District's assets are reported, whether they serve the current year or future years. Liabilities are considered regardless of whether they must be paid in the current or future years. Although the purpose of the District is not to accumulate net position, in general, as the amount increases, it may indicate that the financial position of the District is improving over time. To fully assess the overall health of the District, however, you should consider other factors as well, such as changes in the District's average daily attendance or its property tax base and the condition of the District's facilities.

The purpose of the statement of activities, page 35, is to present the revenues and expenses of the District. Again, the items presented on the statement of activities are measured in a manner similar to the approach used by a commercial enterprise in that revenues are recognized when earned or established criteria are satisfied, and expenses are reported when incurred by the District. Thus, revenues are reported even when they may not be collected for several months or years after the end of the accounting period, and expenses are recorded even though they may not have used cash during the current period.

The District had no business-type activities during 2012/2013.

The two government-wide statements report the District’s net position and how they have changed. Net-assets are the difference between the District’s assets and liabilities and are one way to measure the District’s financial health position.

Over time, increases or decreases to the District’s net position are an indicator of whether its financial health is improving or deteriorating, respectively.

To assess the overall health of the District, one needs to consider additional non-financial factors such as changes in the District’s tax base, staffing patterns, enrollment and attendance.

The government-wide financial statements of the District include only governmental activities. Most of the District’s basic services such as instruction, extracurricular activities, curriculum and staff development, health services, general administration, and plant operation and maintenance are included in government activities. Locally assessed property taxes, together with State Foundation Program entitlements, which are based upon student enrollment and attendance, finance most of the government activities.

The District has no component units for which it is financially accountable.

21

Fund Financial Statements

The fund financial statements (starting on page 36) provide more detailed information about the District’s most significant funds, not the District as a whole. Funds are simply accounting devices that are used to keep track of specific sources of funding and spending for particular purposes.

Some funds are required by State law and other funds are mandated by bond agreements or bond covenants.

The Board of Trustees establishes other funds to control and manage money set aside for particular purposes or to show that the District is properly using certain taxes and grants.

Other funds are used to account for assets held by the District in a custodial capacity; these assets do not belong to the District but the District is responsible to properly account for them.

All of the District’s funds can be divided into the following two categories:

Governmental Funds: Most of the District’s basic services are included in governmental funds, which focus on (1) how cash and other financial assets that can readily be converted to cash flow in and out and (2) the balances left at year-end that are available for spending. Consequently, the governmental fund statements provide a detailed short-term view that helps to determine whether there are more or fewer financial resources that can be spent in the near future to finance the District’s programs. Since this information does not encompass the additional long-term focus of the government-wide statements, we provide additional information at the bottom of the governmental funds statement, or on the subsequent page, that explain the relationship (or differences) between them.

The District maintains several individual governmental funds organized according to their type (special revenue, debt service and capital projects). Information is presented separately in fund financial statements for the general fund, special revenue fund, debt service fund, and capital projects fund, general and capital projects funds are considered major funds. The District adopts an annual appropriated budget for its general fund, food service program within the special revenue fund, and debt service fund. Budgetary comparison schedules have been provided to demonstrate compliance with these budgets.

Fiduciary Funds: The District serves as the trustee, or fiduciary, for certain funds such as scholarship and student activity funds. The District is responsible for ensuring that the assets reported in these funds are used for their intended purposes. All of the District’s fiduciary activities are reported in a separate statement of fiduciary net position and a statement of changes in fiduciary net position. These activities are excluded from the District’s government-wide financial statements because the District cannot use these assets to finance its governmental operations.

The notes to the financial statements (starting on page 45) provide narrative explanations or additional data needed for full disclosure in the government-wide statements or the fund financial statements.

In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information that further explains and supports the information in the financial statements. Required supplementary information can be found on pages 62-63 of this report.

Other supplementary information including combining statements and compliance schedules can be found on pages 66-93 of this report.

Financial Reporting Entity

In 1976, Stafford residents voted to create a breakaway school district, on what would offer a small school environment for their children. In 1982, the District was established and opened their doors for the first school year as Stafford Municipal School District. The District is the only municipal school district in the State of Texas. Being a municipal school district allows the District a unique opportunity to partner with the City.

22

During the 78th

Texas Legislative session, HB 2964, now TEC 11.303 was enacted which made changes to the District’s budget and property tax rate adoption process as stated below.

11.303[0]. MUNICIPAL SCHOOL DISTRICTS. (a) Except as otherwise provided by this section, a school district operating under former Chapter 24 may continue to operate under that chapter as it existed on May 1, 1995, and under state law generally applicable to school districts that does not conflict with that chapter.

(b) The governing body of the municipality may participate in annual hearings or work sessions held by the board of trustees of the municipal school district on the budget and ad valorem tax rate for the coming year.

(c) The board of trustees of a municipal school district and the governing body of the municipality shall jointly hold any hearing required by law as a condition for the adoption of an annual budget and imposition of an ad valorem tax.

(d) Neither an annual budget for a municipal school district nor an ad valorem tax to be imposed for the district may be adopted without the affirmative vote of:

(1) a majority of the members of the board of trustees of the municipal school district present and voting; and

(2) at least three-quarters of the total of the voting members of the board of trustees and the governing body of the municipality that are present and voting.

(e) If a quorum of the members of the governing body of the municipality is not present at a meeting required under Subsection (c), the board of trustees may adopt a budget or an ad valorem tax rate without regard to the requirements of Subsection (d).

(f) Notwithstanding former Section 24.06(c), as it existed on May 1, 1995, the governing body of the municipality shall adopt an ordinance providing for the levy and assessment of the tax approved pursuant to Subsection (d) or (e).

(g) After adopting an ordinance levying a tax for the municipal school district, the governing body of the municipality shall provide a certified copy of the ordinance to the district's board of trustees.

(h) This section may not be construed as authorizing the governing body of a municipality to levy a tax for the support of schools of a municipal school district without fully complying with all applicable provisions of the Tax Code.

Added by Acts 2003, 78th Leg., ch. 304, § 1, eff. Sept. 1, 2003.

As required by GAAP, the financial statements of the reporting entity include those of the District (as the primary government) as an independent reporting entity clearly within the criteria established by GASB.

The District encompasses approximately seven square miles and is located in Fort Bend and Harris Counties, Texas, approximately 25 miles southwest of downtown Houston.

The District currently includes a primary school, an elementary school, an intermediate school, a middle school, a high school, and an alternative campus. The District is also a member of the Fort Bend County Juvenile Justice Alternative Educational Placement. The District serves over 3,340 students and provides a full range of educational services appropriate to grade levels Pre-K through 12. These services include regular and enriched academic education, special education for children with special needs, career and technology education, and programs for students with limited English proficiency. These basic programs are supplemented by a wide variety of offerings in fine arts and athletics.

After experiencing several years of fast growth, the District’s student enrollment became relatively static in 1999-2000. The TEA Snapshot reported an enrollment of 2,868, peaking at 2,897 on the 2001-2002 snapshot date, with the District experiencing declining enrollment from 2001-2002 through the end of 2002-2003. The District ended the 2003-2004 school year with an enrollment of 2,838. In the summer of 2003 the District’s Board approved a Limited Open Enrollment (LOE) program that, as of the TEA snapshot date for 2003 added 99 non-resident students, 204 added 106 non-resident students, and 2005 added 235 non-resident students, which increased the District’s total enrollment to 2,810, 2,838, and 3,014 respectively. With the Hurricane Katrina and Hurricane Rita in the 2006 fiscal year, the enrollment jumped to an all-time high of 3,119 including 257 LOE students. During the 2006-2007 fiscal year, about 150 of the hurricane evacuee students left SMSD resulting in a final enrollment of 2,992. In 2007-2008, the strict criteria for the LOE program contributed to an overall decline in enrollment resulting in a final enrollment of 2,902. In 2011-2012 the total enrollment was 3,172 students which included 611 LOE. In 2012-2013 the total enrollment was 3,343 which included 777 LOE students.

23

The mission of SMSD, a diverse and visionary learning community, is to prepare each student to become a critical thinker and an ethical, productive citizen, an unwavering commitment to provide multiple life and learning experiences led by dedicated professionals using innovative teaching techniques in an engaging learning environment.

The formation of the Stafford Municipal School District, the partnership with the City of Stafford, and the involvement of the businesses reinforce the feeling in Stafford, Texas, Where Children Are Important!

The goals for the District improvement include the following:

To improve student achievement as measured by the Academic Excellence Indicators. Optimize student success. Maintain a quality, highly-motivated, and achievement-oriented staff. Address the opportunities and challenges of a changing community. Implement enhanced systems that will improve the school district operation.

Accounting System and Budgetary Controls

The diverse nature of the District’s operations and the necessity of legal compliance preclude recording the financial transactions of the District in a single fund. The District’s accounting system is organized and operated on a ‘fund basis’. Each fund is a distinct, self-balancing accounting entity. The various funds are fully described in Note A. 4. of the Notes to the Financial Statements starting on page 45 of the accompanying financial statements.

In developing, evaluating, and improving the District’s accounting system, consideration is given to the adequacy of the internal control structure. Internal controls are designed to prevent loss from unauthorized use or disposition and assure that transactions are executed in accordance with management’s authorization and recorded properly to permit the preparation of financial statements in accordance with GAAP. The concept of reasonable assurance recognizes that the cost of a control should not exceed the benefits likely to be derived, and the evaluation of costs and benefits requires estimates and judgments by management.

All internal control evaluations occur within the above-mentioned framework. We believe the District’s internal control structure adequately safeguards assets and provides reasonable assurance of the proper recording of financial transactions.

As a recipient of federal and state financial assistance, the District also is responsible for ensuring that an adequate internal control structure is in place to ensure compliance with applicable laws and regulations related to these programs. The internal control structure is subject to periodic evaluation by management of the District.

As a part of the District’s single audit, tests are made to determine the adequacy of the internal control structure, including that portion related to federal financial assistance programs, as well as to determine that the District has complied with applicable laws and regulations. The results of the District’s single audit for the fiscal year ended August 31, 2013, indicated no instances of material weaknesses in the internal control structure and no instances of material noncompliance with applicable laws and regulations.

The District maintains budgetary controls to ensure compliance with legal provisions embodied in the annual appropriated budget approved by the District’s Board. Budgetary control is maintained at the functional level. Principals and directors have primary responsibility for controlling their budgets as necessary and ensuring that no expenditure is made unless funds have been properly authorized. Funds are properly authorized when approved by the Board at the function level.

Activities of the General Fund, Special Revenue Funds, Debt Service Fund, and Capital Projects Fund are included in the annual appropriated budget. The level at which expenditures cannot legally exceed the appropriated amount is established by function within an individual fund. The District also maintains an encumbrance accounting system as one technique of accomplishing budgetary control.

Encumbrances lapse at year end.

24

Factors Affecting Financial Condition

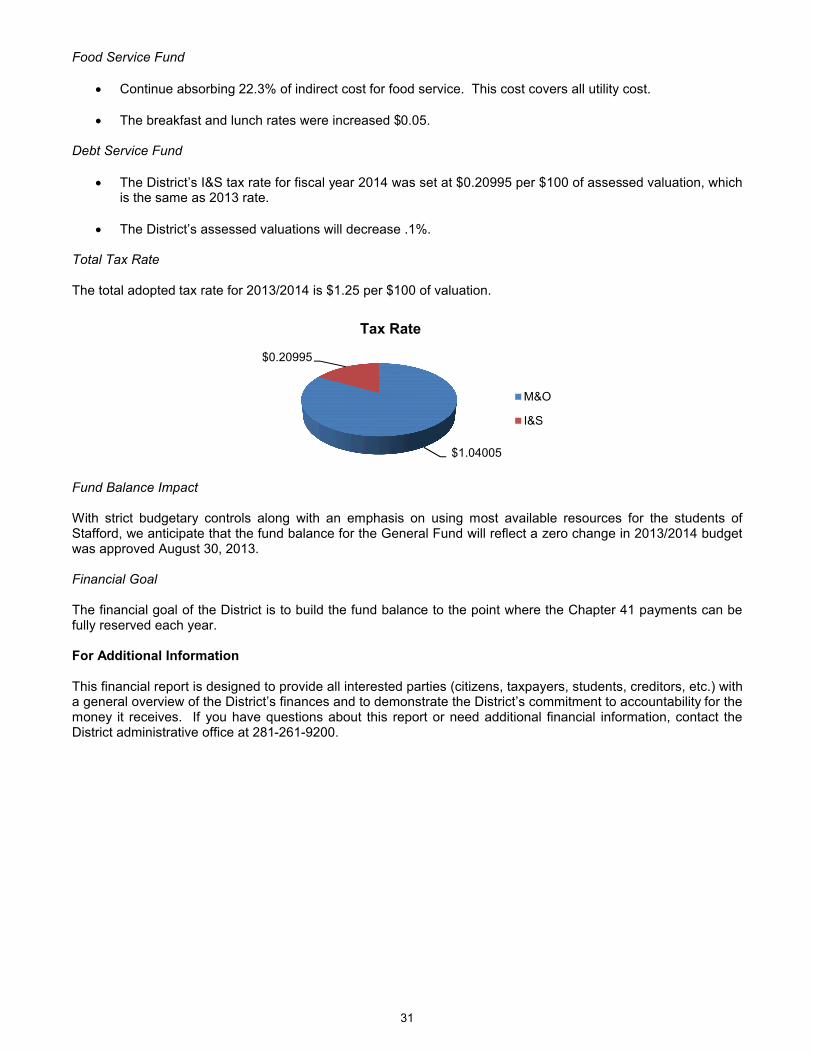

For fiscal year 2013, the District adopted the maximum compressed the maintenance and operating (M&O) ad valorem tax rate of $1.00005 per $100 valuation and the Board approved the four ‘enrichment’ pennies resulting in an adopted M&O tax rate of $1.04005.

During the 2004 fiscal year, the District established a budget process which includes thorough planning, review, and analysis of expenditures at all levels. The District did several initiatives to increase district efficiency andreduce the impact of Chapter 41 expenses. In fiscal years 2005, 2006, 2007, 2008, 2009, 2010, 2011 and 2012the district continued the initiatives started in 2004 to include:

Begin reviewing and discussing the budgets and tax rates in the month of January with the Stafford Municipal School District school board and the Stafford City Council.

There was a continuation of the LOE program whereby non-resident students could attend district schools which kept more resources in the district.

With the implementation of the Chapter 41 strategies, an organizational culture of openness and self-evaluation, the establishment of written procedures, the District is making great strides in building support and targeting resources to achieve the greatest positive impact for all of our students. The financial, cultural, educational, and recreational climate of the area is a testimony to the collective leadership and to the community’s progressive attitude toward responsible growth and their vision of the future.

In November 2006, SMSD taxpayers approved $15.05 million in bonds for district renovations, upgrades, central plant, science labs, technology equipment, and construction of a new cafeteria and playgrounds. In May 2011, SMSD taxpayer approved $49.9 million in bonds for district renovations, tennis courts, security upgrades, new roof, additional classrooms, and buses.

The District received a financial rating of Superior Achievement from the Financial Integrity Rating System of Texas (FIRST).

The Business Services Department earned the following awards for their transparent efforts in regards to the budget and financial statements:

ASBO Meritorious Budget Award for 2012/2013 2012-2013 Distinguished Budget Presentation Certificate of Achievement for Excellence in Financial Reporting Texas Comptroller Leadership Circle Gold Member

Academic Initiatives and Awards

The District has implemented several academic initiative programs to enhance student performance. These programs include district-wide administration of a nationally norm-referenced test, the Iowa Test of Basic Skills (ITBS) test. They also include the PSAT test for all freshmen and sophomores providing an opportunity for these students to participate without any financial hardships placed on the parents. The district has also enhanced academic programs by providing a fully aligned curriculum for teachers through the purchase of the C-SCOPE curriculum. This curriculum is Texas Essential Knowledge and Skills (TEKS) correlated and allows for both vertical and horizontal alignment, prepared model lessons, daily sponge activities, instructional consideration, and assessment lesson pre-requisites.

In addition, the District has an articulation agreement with Houston Community College Systems, which allows high school students an opportunity to earn college credit hours while in high school.

For the first time schools throughout America have a national performance rating as required by the ‘No Child Left Behind’ Act. Starting in the 2004-2005 school year this meant two accountability systems for Texas schools: the existing Academic Excellence Indicator System (AEIS) and the new Adequate Yearly Progress (AYP). For 2011/2012, Primary and Elementary campuses met AYP, while Intermediate, Middle and High School did not meet AYP. All campuses were rated as Academically Acceptable under AEIS. In 2012/2013 the State of Texas requested a waiver regarding ESEA flexibility and the waiver was recently approved in September 2013. Specifically, this waiver of the federal Accountability Performance Targets/Standards Setting Procedures allows TEA to replace the current AYP calculations and performance targets with the state’s robust accountability rating system. The Texas Accountability System meets the intent and purposes of the ESEA statute. Based upon the

25

Texas Accountability System, SMSD campuses were rated with the highest rating of “Met Standard”. As part of the accountability system, System Safeguards were identified for the following campuses: Stafford High School, Stafford Middle School, and Stafford Intermediate. SMSD has implemented target goals and strategies to ensure the students at each campus meet System Safeguards for 2014.

SMSD offered one session of summer school for students, who performed below acceptable levels on their STAAR Math and/or their end-of-course grade was below passing.

Student Athletic Accomplishments

The student-athletes made tremendous strides in the development of an elite program. The seniors provided the leadership that was needed and the entire program committed themselves with their hearts and souls to create a legacy for our future athletes to follow. The most important areas of improvement were within the commitment, pride, and work ethic of our student-athletes.

All sports had a number of accomplishments during the 2012/2013 school year including, but not limited to, football, boys' basketball team, girls' basketball, boys’ soccer and baseball won bi-district championship, and a high number of student-athletes that made Academic All-District teams.

Community Accomplishments

The SMSD is located in Fort Bend County one of the fastest growing counties in the nation. SMSD has greatly benefited from the generosity and support of local non-profits and businesses throughout the Fort Bend County and Houston areas. The George Foundation has funded district programs including instruction, student leadership and assistance. It also has awarded scholarships. The SMSD Education Foundation provided scholarships and teacher grants to supplement the resources needed by our faculty and students. ACHIEVE Fort Bend promotes the value of education and encourages business support of at-risk students. The Fort Bend Chamber and Houston Area Realtors Association create opportunities for SMSD to share information about our schools. The Fort Bend County Fair focuses on youth education annually awards scholarships to high school youth. The Houston Livestock Show and Rodeo Art Program has annually recognized art students and awarded scholarships. Big Brothers Big Sisters has provided our students with professionally supported mentors. Area businesses and church organizations have provided career day speakers, donated services, supplies, technology, and recognition gifts to students and staff.

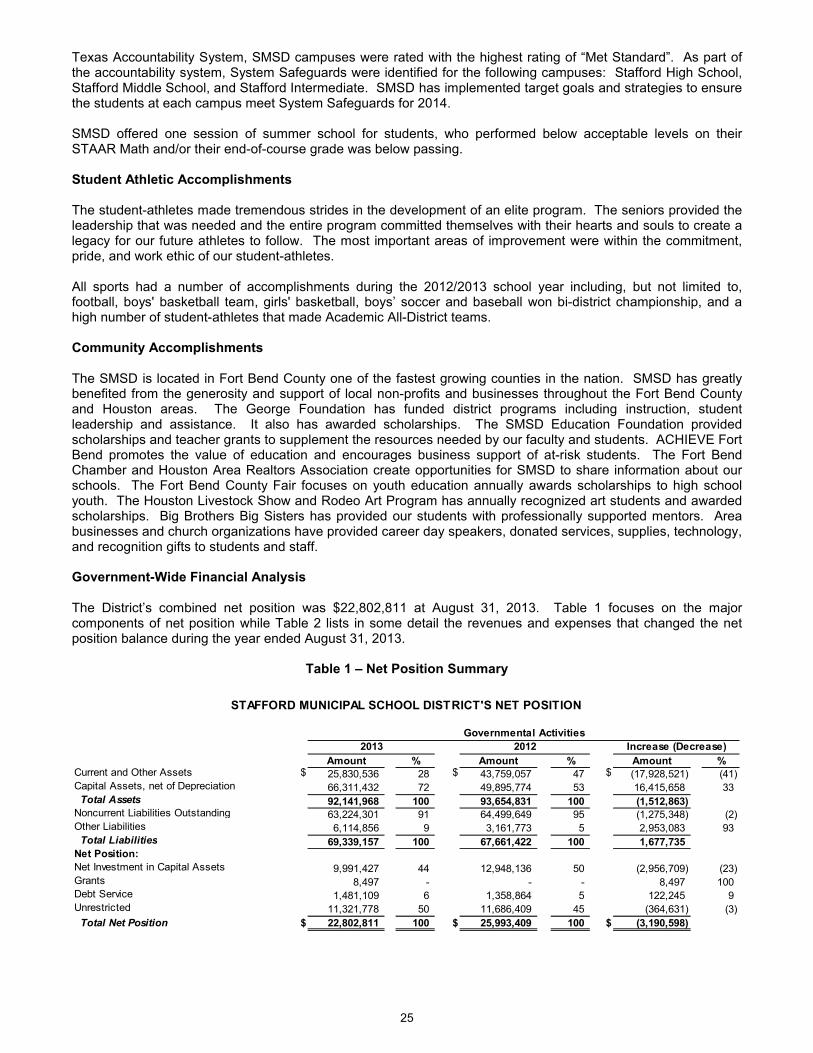

Government-Wide Financial Analysis

The District’s combined net position was $22,802,811 at August 31, 2013. Table 1 focuses on the major components of net position while Table 2 lists in some detail the revenues and expenses that changed the net position balance during the year ended August 31, 2013.

Table 1 – Net Position Summary

Amount % Amount % Amount %Current and Other Assets $ 25,830,536 28 $ 43,759,057 47 $ (17,928,521) (41) Capital Assets, net of Depreciation 66,311,432 72 49,895,774 53 16,415,658 33 Total Assets 92,141,968 100 93,654,831 100 (1,512,863) Noncurrent Liabilities Outstanding 63,224,301 91 64,499,649 95 (1,275,348) (2) Other Liabilities 6,114,856 9 3,161,773 5 2,953,083 93 Total Liabilities 69,339,157 100 67,661,422 100 1,677,735 Net Position:

Net Investment in Capital Assets 9,991,427 44 12,948,136 50 (2,956,709) (23) Grants 8,497 - - - 8,497 100 Debt Service 1,481,109 6 1,358,864 5 122,245 9 Unrestricted 11,321,778 50 11,686,409 45 (364,631) (3)

Total Net Position $ 22,802,811 100 $ 25,993,409 100 $ (3,190,598)

Governmental Activities

2013 2012 Increase (Decrease)

STAFFORD MUNICIPAL SCHOOL DISTRICT'S NET POSITION

26

Investment in capital assets (e.g., land, buildings, furniture and equipment), less any related debt used to acquire those assets that is still outstanding is $9,991,427. Although the District’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the District’s net position (approximately 6%) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net position may be used to finance day-to-day operations without constraints established by debt covenants, enabling legislation, or other legal requirements.

Table 2 – Changes in Net Position Summary

2013 2012

Amount % Amount % Amount %

Revenue:

Program Revenues:

Charges for Services $ 679,245 2 $ 646,544 2 $ 32,701 5

Operating Grants and Contributions 4,151,536 13 4,455,959 14 (304,423) (7)

General Revenues:

Property Taxes, Levied for General Purpose 20,629,915 64 20,191,391 62 438,524 2

Property Taxes, Levied for Debt Service 4,157,096 13 3,623,799 11 533,297 15

Grants and Contributions Not Restricted

to Specific Programs 2,083,344 6 3,129,716 9 (1,046,372) (33)

Investment Earnings 37,985 - 60,652 - (22,667) (37)

Miscellaneous 602,216 2 506,205 2 96,011 19

Total Revenues 32,341,337 100 32,614,266 100 (272,929)

Expenses:

Instruction 17,369,464 50 15,976,008 50 1,393,456 9

Instructional Resources and Media Services 213,233 1 169,624 1 43,609 26

Curriculum and Staff Development 467,161 1 132,964 - 334,197 251

Instructional Leadership 489,436 1 456,377 1 33,059 7

School Leadership 1,923,418 5 1,573,235 5 350,183 22

Guidance, Counseling and Evaluation Services 1,112,917 3 945,625 3 167,292 18

Social Work Services - - - - - 100

Health Services 318,685 1 298,060 1 20,625 7

Student Transportation 1,022,021 3 887,353 3 134,668 15

Food Service 2,164,555 6 1,968,994 6 195,561 10

Extracurricular Activities 926,240 3 743,486 2 182,754 25

General Administration 1,480,877 4 1,555,863 5 (74,986) (5)

Plant Maintenance and Operations 3,537,163 10 3,285,241 10 251,922 8

Security and Monitoring Services 91,605 - 40,137 - 51,468 128

Data Processing Services 549,802 2 567,309 2 (17,507) (3)

Community Services 3,496 - 5,762 - (2,266) (39)

Interest on Long-term Debt 2,784,393 9 2,815,543 9 (31,150) (1)

Current Debt Fees 5,050 - 1,500 - 3,550 237

Facilities Repair and Maintenance - - - - - 100

Contracted Instructional Services Between Schools 385,328 1 605,125 2 (219,797) (36)

Payments Related to Shared Services Arrangements 23,078 - 22,938 - 140 1

Payments to Juvenile Justice Alternative Ed. Programs 20,000 - 30,000 - (10,000) (33)

Other Charges 139,819 - - 139,819 100

Total Expenses 35,027,741 100 32,081,144 100 2,946,597

Change in Net Position (2,686,404) 533,122 (3,219,526)

Net Position - Beginning 25,993,409 25,460,287 533,122

Prior Period Adjustment - Implement GASB 65

for Bond Issuance Costs (504,194) - (504,194)

Net Position - Beginning, as restated 25,489,215 25,460,287 28,928

Net Position - Ending $ 22,802,811 $ 25,993,409 $ (3,190,598)

Increase (Decrease)

Governmental Activities

STAFFORD MUNICIPAL SCHOOL DISTRICT'S CHANGES IN NET POSITION

27

$-

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

2011-2012 2012-2013

Governmental Activity Revenue

Charges for Services

Operating Grants andContributions

General Revenues

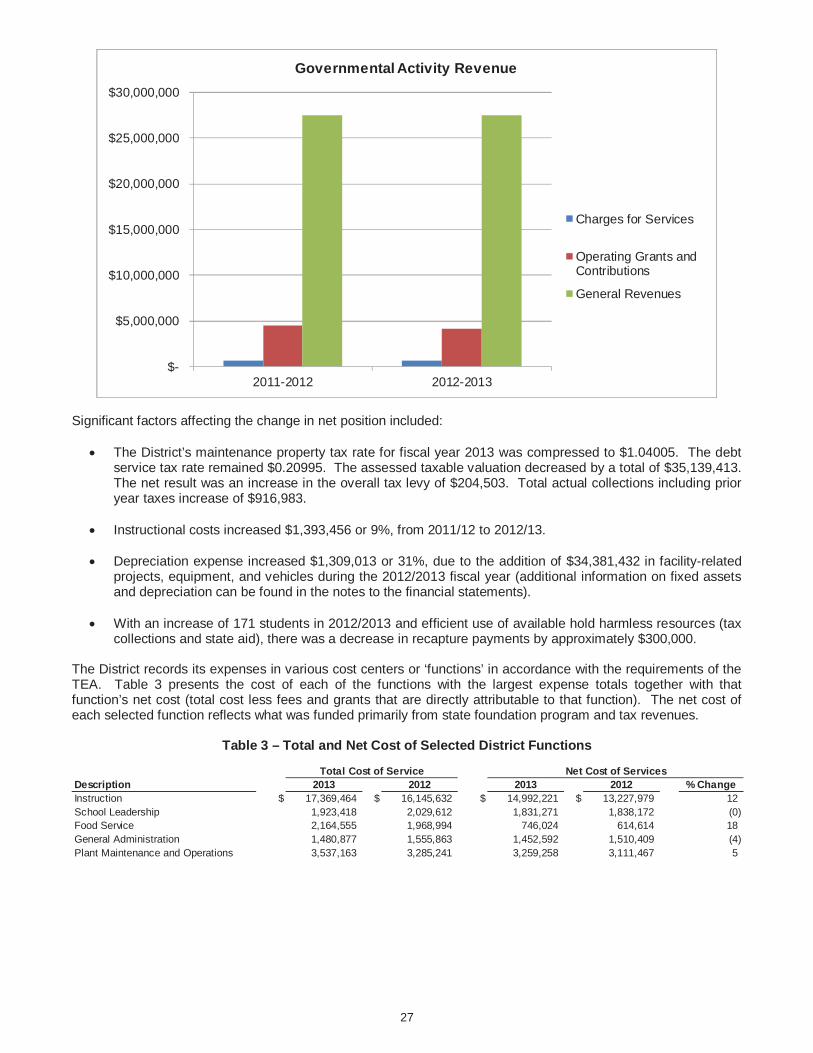

Significant factors affecting the change in net position included:

The District’s maintenance property tax rate for fiscal year 2013 was compressed to $1.04005. The debtservice tax rate remained $0.20995. The assessed taxable valuation decreased by a total of $35,139,413.The net result was an increase in the overall tax levy of $204,503. Total actual collections including prioryear taxes increase of $916,983.

Instructional costs increased $1,393,456 or 9%, from 2011/12 to 2012/13.

Depreciation expense increased $1,309,013 or 31%, due to the addition of $34,381,432 in facility-relatedprojects, equipment, and vehicles during the 2012/2013 fiscal year (additional information on fixed assetsand depreciation can be found in the notes to the financial statements).

With an increase of 171 students in 2012/2013 and efficient use of available hold harmless resources (taxcollections and state aid), there was a decrease in recapture payments by approximately $300,000.

The District records its expenses in various cost centers or ‘functions’ in accordance with the requirements of theTEA. Table 3 presents the cost of each of the functions with the largest expense totals together with thatfunction’s net cost (total cost less fees and grants that are directly attributable to that function). The net cost ofeach selected function reflects what was funded primarily from state foundation program and tax revenues.

Table 3 – Total and Net Cost of Selected District Functions

Description 2013 2012 2013 2012 % ChangeInstruction $ 17,369,464 $ 16,145,632 $ 14,992,221 $ 13,227,979 12School Leadership 1,923,418 2,029,612 1,831,271 1,838,172 (0)Food Service 2,164,555 1,968,994 746,024 614,614 18General Administration 1,480,877 1,555,863 1,452,592 1,510,409 (4)Plant Maintenance and Operations 3,537,163 3,285,241 3,259,258 3,111,467 5

Total Cost of Service Net Cost of Services

28

Financial Analysis of the Individual Funds

As noted earlier, the District uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements.

The District’s individual funds are accounted for on the modified accrual basis of accounting. Under this basis of accounting, revenues are recognized when they are earned and available, and expenditures are recognized when a legal liability occurs, except for earned, accrued interest on debt which is recognized when paid.

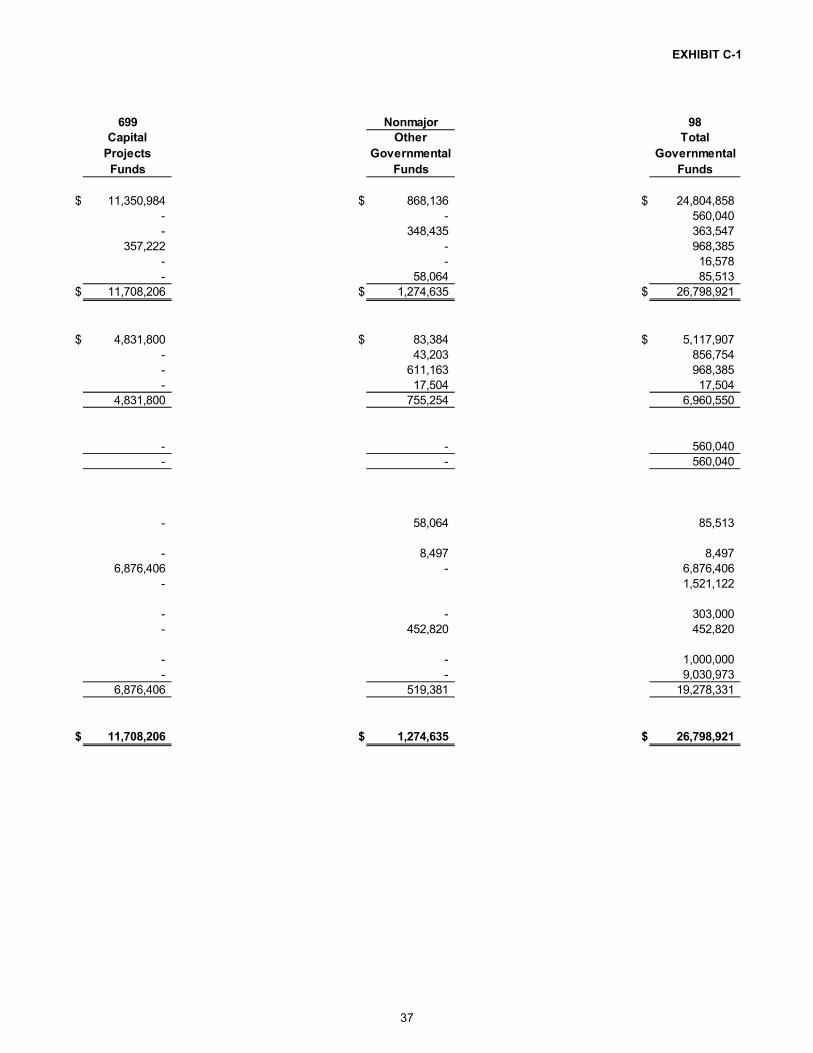

As of August 31, 2013, the District’s combined governmental funds (as presented in Exhibit C-1 on page 36 of this report) reported a combined fund balance of $19,278,331. This compared to a combined fund balance of $39,632,702 at August 31, 2012, or a decrease of $20,354,371. Total revenues from governmental fund types decrease of $424,010 and expenditures increased $2,109,878 over prior year (governmental revenues and expenditures are presented in Exhibit C-2 on page 40).

The following chart presents the amounts of undesignated and reserved fund balances for the 2012/2013 fiscal year:

Nonspendable, 0.44%

Unassigned, 46.85%

Committed, 3.92%

Restricted, 43.60%

Assigned, 5.19%

General Fund Budgetary Highlights

In accordance with State law and generally accepted accounting standards, the District prepares an annual budget for the General Fund, the Food Service Special Revenue Fund, and for the Debt Service Fund. TheDistrict budgets the Capital Projects Fund for each project, which routinely may cover several years. Special Revenue Funds have budgets approved by the funding agency and are amended throughout the year as required.

During the year ended August 31, 2013, the District amended its budget as required by State law and to reflect current levels of revenue and anticipated expenses. District officials have adopted a conservative approach to budgeting anticipated revenues and expenditures and utilize strict budgetary controls.

Overall, the expenditures for the general fund were less than the total budget by $1,076,903 or 4.27%.

29

Capital Assets and Debt Administration

Capital Assets

Capital assets are generally defined as those items that have useful lives of two years or more and have an initial cost or value (if donated) of an amount determined by the Board. The District follows the policy of capitalizing all purchases and gifts of capital type assets that have an initial purchase price or value of $5,000 or more. District capital assets (except land) are depreciated on a straight-line basis over the anticipated life of the asset with annual depreciation expense charged to the functional categories based upon the relative use of the asset. Additional information on the District’s capital assets can be found in the notes to the financial statements.At August 31, 2013, the District had a total of $66,311,432 invested in capital assets such as land, buildings, vehicles, and equipment net of depreciation (see Table 4). Of this a total of $20,699,671 was invested in the year ended August 31, 2013.

Table 4 – Capital Assets and Depreciation

2013 2012

Amount % Amount % Amount %

Land $ 657,500 1 $ 657,500 1 $ - -

Construction in Progress 4,517,029 7 18,231,882 37 (13,714,853) (75)

Buildings and Improvements 58,297,124 88 27,872,896 56 30,424,228 109

Vehicles 1,226,756 2 1,521,646 3 (294,890) (19)

Furniture and Equipment 1,613,023 2 1,611,850 3 1,173 -

Totals $ 66,311,432 100 $ 49,895,774 100 $ 16,415,658

STAFFORD MUNICIPAL SCHOOL DISTRICT'S CAPITAL ASSETS

Governmental Activities

Increase (Decrease)

(net of depreciation)

Major capital asset projects/purchases during the current fiscal year included the following:

Bond Projects $33,942,409

Debt Administration

The laws of the State of Texas give the voters of each public school district in the state the right to approve the sale of bonds for the construction, maintenance, and equipping of school buildings and facilities. Principal and interest relating to bonds issued as a result of the successful passage of a bond election are payable from the proceeds of a debt service tax which is assessed on all taxable property within the District. This tax is levied in addition to the maintenance and operation tax and the expenditure of money from this levy is restricted to the payment of expenses, including principal and interest, related to such bonded debt.

SMSD taxpayers approved $49.9 million in bonds for district renovations, upgrades, maintenance facilities, technology equipment, and construction of a new high school wing.

At August 31, 2013, the District had three bond issues outstanding of which the unpaid principal totaled $61,955,000.

Table 5 summarizes the District’s outstanding debt at August 31, 2013. More detailed information regarding the District’s debt obligations is presented in Notes F of the Notes to the Financial Statements.

Table 5 – Summary of Outstanding Debt

2013 2012

Amount % Amount % Amount %

General Obligation Bonds (Net) $ 63,107,589 100 $ 64,360,176 100 $ (1,252,587) (2)

Capital Leases 88,822 - 115,743 - (26,921) (23)

Compensated Absences 27,890 - 23,730 - 4,160 18

Totals $ 63,224,301 100 $ 64,499,649 100 $ (1,275,348)

STAFFORD MUNICIPAL SCHOOL DISTRICT'S OUTSTANDING NONCURRENT LIABILITIES

Governmental Activities

Increase (Decrease)

30

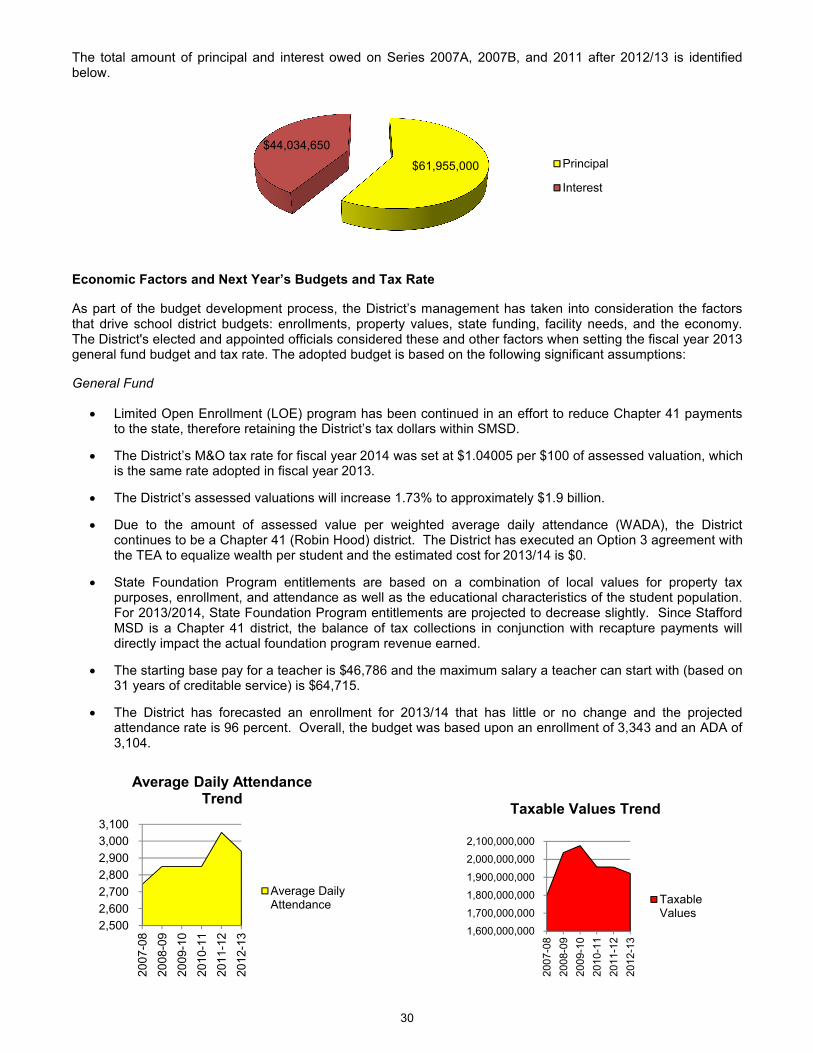

The total amount of principal and interest owed on Series 2007A, 2007B, and 2011 after 2012/13 is identified below.

Economic Factors and Next Year’s Budgets and Tax Rate

As part of the budget development process, the District’s management has taken into consideration the factors that drive school district budgets: enrollments, property values, state funding, facility needs, and the economy. The District's elected and appointed officials considered these and other factors when setting the fiscal year 2013general fund budget and tax rate. The adopted budget is based on the following significant assumptions:

General Fund

Limited Open Enrollment (LOE) program has been continued in an effort to reduce Chapter 41 payments to the state, therefore retaining the District’s tax dollars within SMSD.

The District’s M&O tax rate for fiscal year 2014 was set at $1.04005 per $100 of assessed valuation, which is the same rate adopted in fiscal year 2013.