compiled by nut khorn page 1 · pdf filecompiled by nut khorn page 2 ... in microsoft excel...

TRANSCRIPT

Compiled by Nut khorn Page 1

Compiled by Nut khorn Page 2

Table of Contents

SYLLABUS FOR ......................................................................................................................... 4

1. Course Description: ................................................................................................................. 4 2. Course objectives ..................................................................................................................... 4 3. Course content ...................................................................................................................... 4 4. Learning Resources: ............................................................................................................... 5 Additional Reading ...................................................................................................................... 5

6. Evaluation of the student performance .................................................................................. 5 Knowing Our Finance Program ................................................................................................. 5 Internet Web for this Courses: .................................................................................................... 6 7-HOME WORK AND ASSIGNMENT ..................................................................................... 6

Homework and Assignment .................................................................................................. 7 Course Outline for Corporate Finance ................................................................................. 7

Lesson Plan .......................................................................................................................... 8 The road forward to Success in this course ......................................................................... 9

Management and Accountant ........................................................................................ 9

Notes: Financial statements ...................................................................................................... 10

Balance Sheet ............................................................................................................................ 10 Income Statement ...................................................................................................................... 10 Statement of Cash Flows ........................................................................................................... 10

Statement of Owner’s Equity .................................................................................................... 10 Conceptual Framework ...................................................................................................... 11 Review ................................................................................................................................ 12

The Key Attributes of Successful Companies ........................................................................... 13 Chapter 1. Introduction to Corporate Finance ................................................ 14

What is Corporate Finance? ..................................................................................................... 15

Hypothetical Organization Chart ............................................................................................. 16

The Financial Manager ............................................................................................................ 17 The Firm and the Financial Markets ....................................................................................... 17

Debt and Equity as Contingent Claims .................................................................................... 18 The Corporate Firm .................................................................................................................. 19 Goals of the Corporate Firm ..................................................................................................... 19 The Set-of-Contracts Perspective .............................................................................................. 19

Primary Market ............................................................................................................... 20

Secondary Markets .......................................................................................................... 20

Exchange Trading of Listed Stocks .......................................................................................... 20

Chapter Quiz .......................................................................................................................... 21 Chapter 2. Introduction to Valuation: The Time Value of Money ....................................... 23

The One-Period Case: Future Value ........................................................................................ 24 Present Value (PV) and Discounting ....................................................................................... 25 Compounding Periods ............................................................................................................... 26 Simplifications ........................................................................................................................... 26

Annuity ................................................................................................................................... 26 Perpetuity ............................................................................................................................... 27

EARs and APRs ......................................................................................................................... 27 Summary and Conclusions ................................................................................................. 29 Use Ms. Excel 2003, 2007, and 2010 ................................................................................. 29

Chapter Quiz ..................................................................................................................... 35

Chapter 3: Interest Rates and Bond Valuation .......................................................... 39 Valuation of Bonds and Stock ................................................................................................ 40

Compiled by Nut khorn Page 3

Bonds and Bond Valuation .................................................................................................... 40 Bond Features and Prices .................................................................................................. 40

Bond Values and Yields ......................................................................................................... 40 3.1 Definition and Example of a Bond .............................................................................. 41

Definition and Example of a Bond ........................................................................................... 41 3.2 How to Value Bonds.................................................................................................... 41 Pure Discount Bonds .............................................................................................................. 42 Level-Coupon Bonds .............................................................................................................. 42 Bond Concepts ....................................................................................................................... 43 Bond Markets ......................................................................................................................... 43

Bond Price Reporting ............................................................................................................. 44 Formulas of the Bonds ....................................................................................................... 44

In Microsoft Excel .................................................................................................................. 45 Problem on Chapter 3: ....................................................................................................... 46

Chapter Quiz ..................................................................................................................... 48

Chapter 04: Stock Valuation ............................................................................................. 50 Common Stock Valuation ......................................................................................................... 51 Cash Flows ................................................................................................................................ 51 The Present Value of Common Stocks ..................................................................................... 52

Case 1: Zero Growth .............................................................................................................. 52

Case 2: Constant Growth ........................................................................................................ 53

Case 3: Differential Growth or Supernormal Growth ............................................................ 54

Components of the Required Return ............................................................................. 54

Stock Market Reporting ............................................................................................................ 55 Solved Problems ................................................................................................................. 56

Chapter Quiz ...................................................................................................................... 58

Capital Budgeting ...................................................................................................................... 61

Chapter 5. Net Present Value and Other Investment Criteria ............................................... 61

What is Capital Budgeting? ...................................................................................................... 62 1. Net present value ................................................................................................................ 62

The Net Present Value (NPV) Rule .................................................................................... 62 Good Attributes of the NPV Rule .......................................................................................... 62

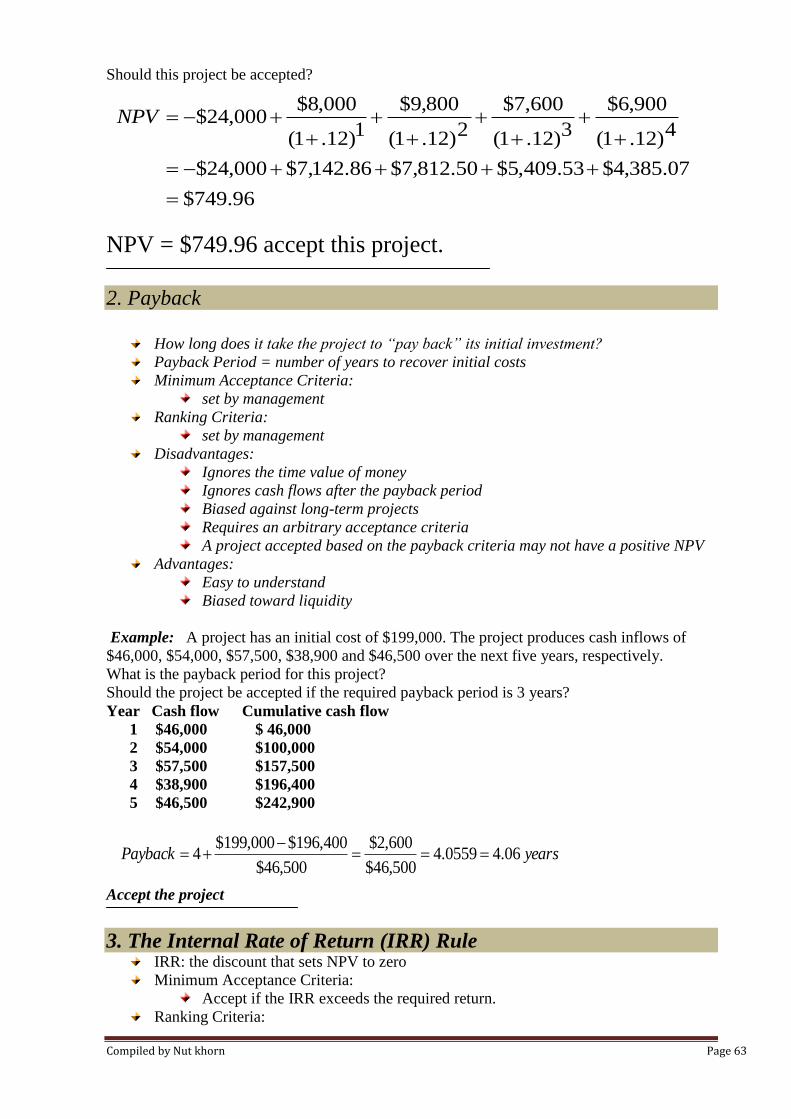

2. Payback .................................................................................................................................. 63 The Profitability Index (PI) Rule ........................................................................................... 65 The Practice of Capital Budgeting ......................................................................................... 65

Net Present Value Profile.......................................................................................................... 65 Accept/Reject Decision ....................................................................................................... 67 Problems on Chapter 5 ...................................................................................................... 69

Glossary ..................................................................................................................................... 75

Compiled by Nut khorn Page 4

SYLLABUS FOR

Corporate Finance

By Nut Khorn

(Course Facilitator)

For BBA students

1. Course Description:

This course aims to introduce to the students the modern fundamental theory of finance.

Specifically it refers to the issues faced by the modern day company in the management of its

financial function. This course is designed for both finance and non-finance major student.

At the end of the course, student will be familiar the central concepts of finance which include

net present value, agency theory, risk and return, financial analysis theory and international

financial theory.

2. Course objectives

The objectives of the course are to enable the student to:

1. Apply the financial technique in valuation and capital budgeting

2. Analyze financial statements and planning

3. Understand issues in working capital management

4. Analyze the issues in capital structure and dividend policy decision

5. Understand various sources of long term and short term finance

6. Analyze and evaluate contemporary corporate finance issue

3. Course content

Unit 1. THE WORLD OF FINANCE

Introduction to the corporate finance

Financial market and institution

Unit 2. ESSENTIAL CONCEPT IFN FINANCE

Financial statements, taxes and Cash flow

Analysis of financial statement

The time value of money

Unit 3. CAPITAL BUDGETING

Introduction to risk and return

Capital budgeting method

Unit 4. DIVIDEND POLICY AND CAPITAL STRUCTURE

Cost of Capital

Capital structure

The dividend controversy

Unit 5 WORKING CAPITAL MANAGEMEMT

Working capital policy

Managing Cash

Compiled by Nut khorn Page 5

Unit 6. CONTEMPORARY ISSUE IN FINANCE

International finance

Merger and acquisition

4. Learning Resources:

Required textbook

Ross Stephen A., Westerfield Randolph W., Jordon Bradford D. (2006) fundamentals of

coporate finance, McGraw- Hill international edition, Seventh edition.

Stephen A. Ross, Randolph W. Westerfield, and Jeffrey F. Jaffe, (2005), Corporate

Finance, McGraw- Hill international, 6th

Edition

Additional Reading

JOEL LERNER and JAMES A. CASHIN, (1998), ―financial Management” The Second

Edition, McGraw- Hill, (SCHAUM‘S OUTLINES).

Paul G. KEAT and PHILIP K.Y. YOUNG, (2000), ―Managerial Economics” The Third

Edition, Prentice Hall ( USA).

5. Course requirement

Student should have basic knowledge of Business mathematics, statistics, economics,

financial accounting, financial issues, Microsoft Office such MS. Word and Ms. Excel and

Casio.

6. Evaluation of the student performance

Course assessment:

Attendance and participation……………. 10%

Homework……………. 30%

Assignment………………................... 20 %

Mid-term Exam…………… 20%

Final Examination ………….. 20%

Total: ………….. 100%

Knowing Our Finance Program

Four major areas:

1. Corporate Finance (Financial Management): How the corporation raises and uses its

resources, short-term and long-term, capital structure, dividend policy and other

related topics on the financial management of the corporation.

2. Money and Capital Markets (Financial Markets and Institutions): Environment needed

for the development of our financial systems, money and capital markets, banking

system (central and commercial banks), other non-bank financial institutions.

3. Investment Analysis and Portfolio Management: Fundamental analysis for fixed

income securities (bonds) and equity securities (stocks), portfolio theory and

management, derivative securities and other related portfolio topics.

4. International Finance: Financial management in the context of the global financial

markets, foreign exchange principles and applications, international money and capital

markets, international diversification, and related topics.

Compiled by Nut khorn Page 6

Work Requirement for a Corporate Finance Major under Mr. Nut Khorn

• I will apply the international standard when I teach all finance courses I will require

that you do all the assigned work before class:

Read your textbook (slide presentation is not complete)

Read the power point materials

Do the assignments

Prepare for all examinations.

Internet research work.

• To perform well in my courses, you need to spend about a minimum of 15 hours per

week for this class. If you do not want to make this commitment, then do not take my

courses.

• You should be present in all my classes. If you do not show up for my lectures, I will

consider you as absent (no need to give excuses).

• If you fail any of my courses (I hope you won‘t), you must retake a new written

examination plus an oral examination to prove that you know the subjects.

Internet Web for this Courses:

www.mhhe.com/rwj (fundamentals of corporate finance) or www.mhhe.com/bmm

When you search the web you will get power point presentation (Slide), quizzes, multiple

choices, excel template, and so on.

Other webs to supporting of your course.

www.mhhe.com (General subjects)

www.mhhe.com/bh (Foundation of Financial Management)

www.mhhe.com/williams_basis14e (Financial & Managerial Accounting)

www.mhhe.com/garrison12e (Managerial Accounting)

www.wiley.com (General Subjects)

www.wiley.com/college/weygandt (Accounting Principles, Financial Accounting,

Hospital Accounting, and Managerial Accounting)

General Research: www.en.wikipedia.org

My Blog: www.nutkhorn.wordpress.com and Videos www.youtube.com/nutkhorn

Note: When you research the entire web above you should

enter the STUDENT CENTER OR STUDENT COMPONION.

7-HOME WORK AND ASSIGNMENT

Students MUST COMPLY STRICTLY with the following instructions in writing their

Home Work, Individual Assignments, Group Case-study and Group Case-Study Presentation.

1. The student(s) is expected to do his/her own research in order to write up individual

assignments and homework.

2. All Individual Assignments/Homework and Group Case-Study MUST be type written on

A-4 sized paper with adequate margins. You should include a TITLE PAGE and a LIST

OF CONTENTS.

3. Use headings and sub-headings to organize your report, including supporting material(s) as

attachments.

Compiled by Nut khorn Page 7

4. All reference books/published materials you refer to should be properly referenced (arrange

in this order: name of author(s), year, and title of the book, publisher, and the country the

book was published) and this must be included in a bibliography at the end of the assignment.

5. Use text referencing when you cite somebody else’s work from your references. Citation

may mean direct quoting, or paraphrasing, or summarizing, or simply to make a statement

of that author's view of finding. An example of text referencing: Beamer and Varner (2001),

Suggested that culture is not something we are born with, but rather it is learned.

6. Number all pages sequentially and securely staple and/or bind all sheets together.

Homework and Assignment

Course Outline for Corporate Finance

Teaching

Weeks Chapters Topics Date Time Allowed

Week 1

Week 2

Week 3

Week 4

Week 5

Week6

Week 7

Week8

Week 9

Week 10

Week 11

Week 12

Week 13

Week 14

Week 15

Week 16

Date Chapter Topic Homework & Assignment

dMeNIrkarTIpSarmUlbRt enAkñúgRbeTskm<úCa Assignment

Group = 4 Students

Ch01

Ch02 P2-7,9,30,36,38,50 Home work

Ch03 P3-8,13,18 Home work

Ch04 P4-16,19,27 Home work

Ch05 P5-11,12 Home work

Compiled by Nut khorn Page 8

Lesson Plan

Week 01

Date Chapter Main Contents Taught

Hours Others

Compiled by Nut khorn Page 9

The road forward to Success in this course

Management and Accountant

1. Actual Objective and Really Practices

2. Terminology

3. Conceptual Frame works

4. Theories

5. Formulas

6. Practices all time

Compiled by Nut khorn Page 10

Notes: Financial statements

The same financial statement sometime receives different titles.

Balance Sheet =Statement of Financial Position

=Statement of Financial Condition

Income Statement =Statement of Income

=Operating Statement

=Statement of Operations

=Statement of Operating Activities

=Earnings Statement

=Statement of Earnings

=Profit and Loss (P&L) Statement

Statement of Cash Flows =Statement of Cash Flow

=Cash Flows Statement

=Statement of Changes in Cash Position

=Statement of Changes in Financial Position

Statement of Owner‘s Equity =Statement of Changes in Owner‘s Equity

= Statement of Changes in Owner‘s Capital

=Statement of Shareholders' Equity*

=Statement of Changes in Shareholders' Equity*

= Statement of Changes in Capital Accounts*

* Corporation only.

Compiled by Nut khorn Page 11

Conceptual Framework

Objectives

To provide information:

Useful for investor and creditor decisions.

That helps predict cash flows.

About economic resources, claims to resources and changes in resources and

claims.

Qualitative

Characteristics

Elements

Recognition and

Measurement

Concepts

Financial

Statements

Constraints

Figure 1: Conceptual Framework

Compiled by Nut khorn Page 12

Review

Finance

Finance is a science. Like other sciences, it has fundamental concepts, principles, and theories.

Nobel Prize Winners Whose Work Has Contributed Significantly to Finance

Jame Tobin, 1981– Liquidity and Behavior under risk.

Franco Modigliani, 1985– Capital Structure and Dividend Policy.

Harry M. Markowitz, 1990– Portfolio theory.

Merton H. Miller, 1990– Capital Structure and Dividend Policy.

William F. Sharp, 1990– Capital Asset Pricing.

John Nash, 1994– Game theory.

James A. Mirrlees, 1996– Asymmetric Information.

William S. Vickrey, 1996- Asymmetric Information.

Robert C. Merton, 1997– Option Pricing

Myron S. Scholes, 1997– Option Pricing.

George A. Ackerloff, 2001– Adverse Selection.

A Michael Spence, 2001– Asymmetric Information.

Joseph E Stiglitz, 2001-- Asymmetric Information.

Danniel Kahmeman, 2002– Behavior al Finance.

Lornon L. Smith, 2002-- Behavior al Finance.

Functions of Financial Systems

Figure 2: Functions of Financial Systems

Compiled by Nut khorn Page 13

The Key Attributes of Successful Companies

First, successful companies have skilled people at all levels inside the company, including

leaders, managers, and a capable workforce.

Second, successful companies have strong relationships with groups outside the company.

For example, successful companies develop win–win relationships with suppliers and excel in

customer relationship management.

Third, successful companies have enough funding to execute their plans and support their

operations. Most companies need cash to purchase land, buildings, equipment, and materials.

Companies can reinvest a portion of their earnings, but most growing companies must also

raise additional funds externally by some combination of selling stock and/or borrowing in the

financial markets.

Just as a stool needs all three legs to stand, a successful company must have all three attributes:

skilled people, strong external relationships, and sufficient capital.

Compiled by Nut khorn Page 14

Chapter 1. Introduction to Corporate Finance

Chapter Outline

1.1 What is Corporate Finance?

1.2 Corporate Securities as Contingent Claims on Total Firm Value

1.3 The Corporate Firm

1.4 Goals of the Corporate Firm

1.5 Financial Markets

After studying this chapter, you should understand:

LO1 The basic types of financial management decisions and the role of the

financial manager.

LO2 The goal of financial management.

LO3 The financial implications of the different forms of business

organization.

LO4 The conflicts of interest that can arise between managers and owners.

Compiled by Nut khorn Page 15

Finance

Noun

1.[U] finance (for sth) money used to run a business, an activity or a project:

2.[U]the activity of managing money, especially by a government or commercial

organization:

3.finances [pl.] the money available to a person, an organization or a country; the way this

money is managed:

Corporate:

adjective

1.connected with a corporation:

2. (technical) forming a corporation:

3. involving or shared by all the members of a group:

Finance is the science of funds management.[1] The general areas of finance are business

finance, personal finance, and public finance.[2] Finance includes saving money and often

includes lending money. The field of finance deals with the concepts of time, money and risk

and how they are interrelated. It also deals with how money is spent and budgeted.

Corporate finance is an area of finance dealing with the financial decisions corporations make

and the tools and analysis used to make these decisions. The primary goal of corporate finance

is to maximize corporate value [1] while managing the firm's financial risks. Although it is in

principle different from managerial finance which studies the financial decisions of all firms,

rather than corporations alone, the main concepts in the study of corporate finance are

applicable to the financial problems of all kinds of firms.

What is Corporate Finance?

Corporate Finance addresses the following three questions:

1. What long-term investments should the firm engage in?

2. How can the firm raise the money for the required investments?

3. How much short-term cash flow does a company need to pay its bills?

The Balance-Sheet Model of the Firm

Total Value of Assets Total Firm Value to Investors:

Current Assets

Fixed Assets

1. Tangible Assets

2. Intangible Assets

Current Liabilities

Long-term Debt

Shareholders’ Equity

=

Compiled by Nut khorn Page 16

The Capital Budgeting Decision

The Capital Structure Decision

The Net Working Capital Investment Decision

--------------------------

---------------------

Capital Structure:

The value of the firm can be thought of as a pie.

The goal of the manager is to increase the size of the pie.

The Capital Structure decision can be viewed as how best to slice up the pie.

If how you slice the pie affects the size of the pie, then the capital structure decision

matters.

Hypothetical Organization Chart

Fixed Assets

1. Tangible Assets

2. Intangible Assets

What long-term investments should

the firm engage in?

Current Liabilities

Long-term Debt

Shareholders’ Equity

How can the firm raise the money

for the required investments?

Current Assets

Current Liabilities

How much short-term cash flow does a

company need to pay its bills?

70% Debt 30%

Equity

Compiled by Nut khorn Page 17

The Financial Manager

To create value, the financial manager should:

1. Try to make smart investment decisions.

2. Try to make smart financing decisions.

The Firm and the Financial Markets

Compiled by Nut khorn Page 18

Corporate Securities as Contingent Claims on Total Firm Value

The basic feature of a debt is that it is a promise by the borrowing firm to repay a fixed

dollar amount of by a certain date.

The shareholder’s claim on firm value is the residual amount that remains after the

debtholders are paid.

If the value of the firm is less than the amount promised to the debtholders, the

Shareholders get nothing

Debt and Equity as Contingent Claims

Combined Payoffs to Debt and Equity

Compiled by Nut khorn Page 19

The Corporate Firm

The corporate form of business is the standard method for solving the problems

encountered in raising large amounts of cash.

However, businesses can take other forms.

Forms of Business Organization

The Sole Proprietorship

The Partnership

General Partnership

Limited Partnership

The Corporation

Advantages and Disadvantages

Liquidity and Marketability of Ownership

Control

Liability

Continuity of Existence

Tax Considerations

A Comparison of Partnership and Corporations

Goals of the Corporate Firm

The traditional answer is that the managers of the corporation are obliged to make

efforts to maximize shareholder wealth.

The Set-of-Contracts Perspective

The firm can be viewed as a set of contracts.

One of these contracts is between shareholders and managers.

Compiled by Nut khorn Page 20

The managers will usually act in the shareholders‘ interests.

The shareholders can devise contracts that align the incentives of the managers

with the goals of the shareholders.

The shareholders can monitor the managers‘ behavior.

This contracting and monitoring is costly.

Managerial Goals

Managerial goals may be different from shareholder goals

Expensive perquisites

Survival

Independence

Increased growth and size is not necessarily the same thing as increased shareholder

wealth.

Do Shareholders Control Managerial Behavior?

Shareholders vote for the board of directors, who in turn hire the management team.

Contracts can be carefully constructed to be incentive compatible.

There is a market for managerial talent—this may provide market discipline to the

managers—they can be replaced.

If the managers fail to maximize share price, they may be replaced in a hostile

takeover.

Financial Markets

Primary Market

When a corporation issues securities, cash flows from investors to the firm.

Usually an underwriter is involved

Secondary Markets

Involve the sale of ―used‖ securities from one investor to another.

Securities may be exchange traded or trade over-the-counter in a dealer market.

Exchange Trading of Listed Stocks

Auction markets are different from dealer markets in two ways:

Compiled by Nut khorn Page 21

Trading in a given auction exchange takes place at a single site on the floor of

the exchange.

Transaction prices of shares are communicated almost immediately to the

public.

Chapter Quiz

1

Determining the mix of debt and equity to be used to finance a firm is which type of a decision?

A) capital budgeting

B) working capital

C) capital structure

2

Which one of the following statements concerning partnerships is correct?

A)

All partners enjoy limited liability if they create a general partnership of equal

shares.

B) A limited partner actively participates in running the partnership on a daily basis.

C) A general partnership terminates whenever one general partner decides to sell her share of the business.

D) A general partnership has an unlimited life while a limited partnership has a limited life.

3

Which one of the following statements concerning corporations is correct?

A) The rules describing how a corporation regulates its own existence are set forth in the bylaws.

B)

The procedures to be followed for electing corporate directors are included in the

articles of incorporation.

C) Corporate income is taxed only when the corporate earnings are distributed to shareholders.

D) A corporation is the easiest form of business entity to create.

4

The goal of financial management is to maximize the current:

A) net income per share.

B) dividends per share.

C) total assets.

D) market value per share.

5

Which one of the following statements concerning the financial markets is correct?

A) Shareholders exchange shares with each other in the primary market.

B) The New York Stock Exchange is an auction market.

C) Dealer markets have a physical trading floor.

D) Stocks traded in auction markets are said to trade over-the-counter.

6

Which one of the following provides limited liability for all of its owners?

A) sole proprietorship

B) partnership with only general partners

Compiled by Nut khorn Page 22

C) partnership with both general and limited partners

D) corporation

7

Which one of the following represents a potential agency problem?

A) adherence to the Sarbanes-Oxley Act in 2002

B) hiring a manager and compensating her with shares of company stock

C) paying a management bonus based on the number of employees managed

D) paying all company earnings out to shareholders in the form of dividends

8

Firms that "went dark" following the enactment of the Sarbanes-Oxley Act in 2002:

A) must still comply with all the terms of that act.

B) did not meet the requirements of the act and were involuntarily delisted by the SEC.

C) generally did so to avoid the high cost of compliance.

D) now trade on NASDAQ where previously the firm's shares were traded on the NYSE.

9

Which one of the following is found in the corporate bylaws?

A) intended life of the corporation

B) the state of residence

C) the number of shares that can be issued

D) the procedures for electing the directors

10

Which one of the following statements concerning financial markets is correct?

A) The NYSE is an auction market.

B) All dealer markets require a physical trading floor.

C)

Corporations initially sell shares of stock in the secondary market, which is an auction market.

D) All private sales of stock must first be registered with the SEC.

Compiled by Nut khorn Page 23

Chapter 2. Introduction to Valuation: The Time Value of Money

ONE OF THE BASIC problems faced by the financial manager is how to determine the value

today of cash flows expected in the future. For example, the jackpot in a PowerBall™ lottery

drawing was $110 million. Does this mean the winning ticket was worth $110 million? The

answer is no because the jackpot was actually going to pay out over a 20-year period at a rate

of $5.5 million per year. How much was the ticket worth then? The answer depends on the

time value of money, the subject of this chapter.

In the most general sense, the phrase time value of money refers to the fact that a dollar in hand

today is worth more than a dollar promised at some time in the future.

On a practical level, one reason for this is that you could earn interest while you waited; so a

dollar today would grow to more than a dollar later. The trade-off between money now and

money later thus depends on, among other things, the rate you can earn by investing. Our goal

in this chapter is to explicitly evaluate this trade-off between dollars today and dollars at some

future time.

A thorough understanding of the material in this chapter is critical to understanding material in

subsequent chapters, so you should study it with particular care.

We will present a number of examples in this chapter. In many problems, your answer may

differ from ours slightly. This can happen because of rounding and is not a cause for concern.

After studying this chapter, you should understand:

LO1 How to determine the future value of an investment made today.

LO2 How to determine the present value of cash to be received at a future

date.

LO3 How to find the return on an investment.

LO4 How long it takes for an investment to reach a desired value.

Compiled by Nut khorn Page 24

The One-Period Case: Future Value

The first thing we will study is future value. Future value (FV) refers to the amount of money

an investment will grow to over some period of time at some given interest rate. Put another

way, future value is the cash value of an investment at some time in the future. We start out by

considering the simplest case, a single period investment.

Future value (FV) The amount an investment is worth after one or more periods.

If you were to invest $10,000 at 5-percent interest for one year, your investment would

grow to $10,500.

$500 would be interest ($10,000 × .05)

$10,000 is the principal repayment ($10,000 × 1)

$10,500 is the total due. It can be calculated as:

$10,500 = $10,000× (1.05).

The total amount due at the end of the investment is calling the Future Value (FV).

In the one-period case, the formula for FV can be written as:

)1( rt

PVFV

Compounding

The process of accumulating interest on an investment over time to earn more interest.

Interest on interest

Interest earned on the reinvestment of previous interest payments.

Compound interest: Interest earned on both the initial principal and the interest reinvested

from prior periods.

Simple interest: Interest earned only on the original principal amount invested.

Compiled by Nut khorn Page 25

Present Value (PV) and Discounting

When we discuss future value, we are thinking of questions like, what my $2,000 investment

will grow to if it earns a 6.5 percent return every year for the next six years? The answer to this

question is what we call the future value of $2,000 invested at 6.5 percent for six years (verify

that the answer is about $2,918).

There is another type of question that comes up even more often in financial management that

is obviously related to future value. Suppose you need to have $10,000 in 10 years, and you

can earn 6.5 percent on your money. How much do you have to invest today to reach your

goal? You can verify that the answer is $5,327.26.

How do we know this? Read on.

Present value (PV) The current value of future cash flows discounted at the appropriate

discount rate.

Discount Calculate the present value of some future amount.

)1( rt

FVPV

Suppose you need $400 to buy textbooks next year. You can earn 7 percent on your money.

How much do you have to put up today?

The quantity in brackets,

)1(

1

rt

, goes by several different names. Because it‘s used to

discount a future cash flow, it is often called a discount factor. With this name, it is not

surprising that the rate used in the calculation is often called the discount rate. We will tend to

call it this in talking about present values. The quantity in brackets is also called the present

value interest factor (or just present value factor) for $1 at r percent for t periods and is

sometimes abbreviated as PVIF(r, t). Finally, calculating the present value of a future cash

flow to determine its worth today is commonly called discounted cash flow (DCF) valuation.

Compiled by Nut khorn Page 26

Compounding Periods

Compounding an investment m times a year for t years provides for future value of wealth:

For example, if you invest $50 for 3 years at 12% compounded semi-annually, your investment

will grow to

Simplifications

Annuity

A stream of constant cash flows that lasts for a fixed number of periods.

Perpetuity

A constant stream of cash flows that lasts forever

Annuity

A constant stream of cash flows with a fixed maturity.

The formula for the future value of an annuity is:

]1

[)1(

rCFV

rt

An annuity is set up in which there are yearly payments of $200 for 5 years with interest being

paid at the annual rate of 6% compounded annually. Find the amount of the annuity.

The formula for the present value of an annuity is:

Example: If you can afford a $400 monthly car payment, how much car can you afford if

interest rates are 7% on 36-month loans?

tm

m

rPVFV

1

93.70$)06.1(50$2

12.150$ 6

32

FV

tr

C

r

C

r

C

r

CPV

)1()1()1()1( 32

trr

CPV

)1(

11

Compiled by Nut khorn Page 27

Perpetuity A constant stream of cash flows that lasts forever.

The formula for the present value of perpetuity is:

Example : What is the value of a British consol that promises to pay £15 each year, every year

until the sun turns into a red giant and burns the planet to a crisp?

The interest rate is 10-percent.

EARs and APRs Stated interest rate:

The interest rate expressed in terms of the interest payment made each period. Also, quoted

interest rate.

Effective annual rate (EAR):

The interest rate expressed as if it were compounded once per year.

Annual percentage rate (APR)

The interest rate charged per period multiplied by the number of periods per year.

To see why it is important to work only with effective rates, suppose you‘ve shopped around

and come up with the following three rates:

59.954,12$)1207.1(

11

12/07.

400$36

PV

32 )1()1()1( r

C

r

C

r

CPV

r

CPV

Compiled by Nut khorn Page 28

Bank A: 15 percent compounded daily

Bank B: 15.5 percent compounded quarterly

Bank C: 16 percent compounded annually

Which of these is the best if you are thinking of opening a savings account? Which of these is

best if they represent loan rates?

1)1(

m

APRm

EAR

mrAPR

For example, suppose you are offered 12 percent compounded monthly. In this case, the

interest is compounded 12 times a year; so m is 12. You can calculate the effective rate as:

Sometimes it‘s not altogether clear whether or not a rate is an effective annual rate.

A case in point concerns what is called the annual percentage rate (APR) on a loan.

Truth-in-lending laws in the United States require that lenders disclose an APR on virtually all

consumer loans. This rate must be displayed on a loan document in a prominent and

unambiguous way.

Given that an APR must be calculated and displayed, an obvious question arises:

Is an APR an effective annual rate? Put another way, if a bank quotes a car loan at 12 percent

APR, is the consumer actually paying 12 percent interest? Surprisingly, the answer is no. There

is some confusion over this point, which we discuss next.

The confusion over APRs arises because lenders are required by law to compute the APR in a

particular way. By law, the APR is simply equal to the interest rate per period multiplied by the

number of periods in a year. For example, if a bank is charging

1.2 percent per month on car loans, then the APR that must be reported is 1.2% x 12 =14.4%.

So, an APR is in fact a quoted, or stated, rate in the sense we‘ve been discussing.

For example, an APR of 12 percent on a loan calling for monthly payments is really 1 percent

per month. The EAR on such a loan is thus:

The difference between an APR and an EAR probably won‘t be all that great, but it is

somewhat ironic that truth-in-lending laws sometimes require lenders to be untruthful about

the actual rate on a loan.

There are also truth-in-saving laws that require banks and other borrowers to quote an ―annual

percentage yield,‖ or APY, on things like savings accounts. To make things a little confusing,

an APY is an EAR. As a result, by law, the rates quoted to borrowers (APRs) and those quoted

to savers (APYs) are not computed the same way.

Compiled by Nut khorn Page 29

Summary and Conclusions

Two basic concepts, future value and present value are introduced in this chapter.

Interest rates are commonly expressed on an annual basis, but semi-annual, quarterly,

monthly and even continuously compounded interest rate arrangements exist.

The formula for the net present value of an investment that pays $C for t periods is:

Use Ms. Excel 2003, 2007, and 2010

Using a Spreadsheet for Time Value of Money Calculations

=fv(r,t,,-pv)

=pv(r, t,,-fv)

=rate(t,,-pv,fv)

=nper(r,,-pv,fv) a) Ordinary of FVA

=fv(rate,nper, -pv,0,0)

=fv(r,t,-C,,0)

b) FVA of Annuity Due:

=fv(rate, nper,-pv,0,1)

=fv(r,t,-C,,1)

a) Ordinary of PVA

=pv(rate,nper,-pv,0,0)

=pv(r,t,-C,,0)

b)PVA of Annuity Due:

=pv(rate, nper,-pv,0,1)

=pv(r,t,-C,,1)

APR= nominal(effect_rate, npery)

EAR=effect(nominal_rate,npery) End of Chapter 2

r

CPV :Perpetuity

trr

CPV

)1(

11:Annuity

Compiled by Nut khorn Page 30

a) Future Value (FV) FV r tPV 1

P2-1)

If you invest $12,000 today, how much you will have:

a. In 6 years at 7 percent?

b. In 15 years at 12 percent?

c. In 25 years at 10 percent?

P2-2) Assume you deposit $10,000 today in an account that pays 6 percent interest. How much

will you have in five years?

P2-3)

For each of the following, compute the future value:

Present Value Years Interest Rate

$2,250 30 18%

9,310 16 6%

76,355 3 12%

183,796 7 8%

P2-4) . Bottom Line, Inc. has identified an investment project with the following cash flows. If

the discount rate is 8 percent, what is the future value of these cash flows in Year 4? What is

the future value at a discount rate of 11 percent? At 24 percent?

Year Cash Flow

1 $500

2 600

3 700

4 800

P2-5) Kingen Credit Bank is offering 4.5 percent compounded annually on its saving accounts

.If you deposit $5,000 today, how much you will have in the account in 5 years? in 10 years? in

20 years?

P2-6) You have an investment that will pay you 1.5 percent per month. How much will you

have per dollar invested in 1 year? In 2 years?

P2-7) If today is Year 0, what is the future value of these cash flows five years from now? What

is the future value 10 years from now? Assume a discount rate of 14 percent per year.

Year Cash Flow

2 $25,000

3 50,000

5 75,000

P2-8) A investor deposits $1,000 into a bank account that pays interest at the rate of 10% per

year (payable at the end of each year). She leaves the money and all accrued interest the

account for 5 years.

a) How much money does she have after 1 year?

b) How much money does she have at the end of 5 years?

P2-9) You plan to make a series of deposits in an individual retirement accounts. You will

deposit $1,000 today, $2,000 in two years, and $2,000 in five years. If you withdraw $1,500 in

three years and $1,000 in seven years, assuming no withdrawal penalties, how much will you

have after eight years if the interest rate is 7 percent? What is the present value of these cash

flows?

Compiled by Nut khorn Page 31

b) Present Value (PV)

)1( rt

FVPV

P2-10) What is the present value of: a. $8,000 in 10 years at 6 percent? b. $16,000 in 5 years at 12 percent? c. $25,000 in 15 years at 8 percent? d. $1,000 in 20 periods at 20 percent?

P2-11) How much would you have to invest today to receive: a. $12,000 in 6 years at 12 percent? b. $15,000 in 15 years at 8 percent? P2-12) John Longwaite will receive $100,000 in 50 years. His friends are very jealous of him. If the funds are discounted back at a rate of 14 percent, what is the present value of his future “pot of gold”? P2-13) Suppose you have just celebrated your 19th birthday. A rich uncle has set up a trust fund for you that will pay you $150,000 when you turn 30. If the relevant discount rate is 9 percent, how much is this fund worth today? P2-14)

For each of the following, compute the present value:

Years Interest Rate Future Value

3 4% $15,451 5 12% 51,557

12 22% 886,073

6 20% 550,164

P2-15) Stellato Shaved Ice Company has identified an investment with the following cash flows. If the discount rate is 10 percent, what is the present value of these cash flows? What is the present value at 18 percent? At 24%?

Year Cash Flow

1 $1,000

2 200

3 800

4 1,500 P2-16) You will receive $1,000 after four years at a discount rate of 10 percent. How much is this worth today? P2-17) Smolinski Company is considering an investment that will return a lump sum (= total) of $500,000 5 years from now.

What amount should Smolinski Company pay for this investment in order to earn a 15% return?

P2-18) Imprudential,Inc., has an unfunded pension liabilities of $425 million that must be paid in 20 years. To assess the value of the firm’s stock, financial analysts want of discount this liabilities back to present. If the relevant discount rate is 8 percent, what is the present value of this liability?

Compiled by Nut khorn Page 32

P2-19) Suppose you are still committed to owning a $120,000 Ferrari. If you believe your mutual fund can achieve a 9 percent annual interest rate of return and you want to buy the car in 10 years on the day you turn 30, how much must you to invest today? P2-20) Calculate the present value of the following cash flows discounted at 10 percent. a. $1,000 received seven years from today. b. $2,000 received one year from today. c. $500 received eight years from today.

c) Find r P2-21) You are considering a two-year investment. If you put up $1,250, you will get back $1,350. What rate is this investment paying? P2-22)

Solve for the unknown interest rate in each of the following:

Present Value Years Future Value

$207.22 3 $307 $450.44 9 $761

$37,548.84 15 $136,771 $78,871.00 30 $255,810

P2-23) Assume the total cost of a college education will be $200,000 when your child enters college in 18 years. You presently have $15,000 to invest. What annual rate of interest must you earn on your investment to cover the cost of your child’s college education?

d) Find t P2-24) You’ve been offered an investment that will pay you 9 percent per

year. If you invest $ 15,000, how long until you have $30,000? How long until

you have $45,000?

P2-25)

Solve for the unknown number of years in each of the following:

Present Value Interest Rate Future Value

$542 4% $1,284

$1,834 9% $4,341

$22,196 23% $402,662

$96,591 34% $173,439

P2-26) You’re trying to save to buy a new $120,000 Ferrari. You have $40,000

today that can be invested at your bank. The bank pays 4 percent annual

interest on its accounts. How long will it be before you have enough to buy the

car?

P2-27) You expect to receive $80,000 at graduation in two years. You plant to

investing it at 6 percent until you have $120,000. How long will you wait from

now?

Compiled by Nut khorn Page 33

e) Find FV and PV (Interest is often compounded quarterly, semi-annually,

monthly, daily, and continuously in the real world.)

em

r rtmt

PVFVPVFV

,1

P2-28) Determine the amount of money in a saving account at the end of 5 years, given an initial deposit of $3,000 and an 8 percent annual interest rate when interest rate is compounded (a) annually, (b) semi-annually , (c) quarterly, (d) monthly, (e) daily, and (f) continuously. P2-29) Suppose $1,000 is invested at an annual interest rate of 6%. Compute the balance after 10 years if the interest is compounded (a) Quarterly (b) Monthly (c) Daily (d) Continuously P2-30) Suppose $1,000 is invested at an annual interest rate of 7%. Compute the balance after 10 years if the interest is compounded:

(a) Annually (c) Monthly (b)Quarterly (d) Continuously

f) Find PV =

)1(

11

rtr

C

P2-31) How much would you have to invest today to receive:

q. $5,000 each year for 10 years at 8 percent?

b. $40,000 each year for 40 years at 5 percent?

P2-32) Kilary Company is considering investing in an annuity contract that will

return $20,000 annually at the end of each year for 15 years. What amount

should Kilary Company pay for this investment if it ears a 6% return?

P2-33) You will receive $ 1,000 at the end of each period for four years. At

discount rate of 10% percent, what is cash flow currently worth?

P2-34) Zarita Enterprises earns 11% on an investment that pays back $110,000

at the end of each of the next 4 years. What is the amount Zarita Enterprises

invested to earn the 11% rate of return?

P2-35) An investment offers $2,250 per year for five years, with the first payment

occurring one year from now. If the required return is 10 percent, what is the

value of the investment? What would the value be if the payments occurred

for 40 years? For 75 years?

P2-36) Peter Lynchpin wants to sell you an investment contract that pays

equal $10,000 amount at the end of each of the next 20 years. If you require

an effective annual return of 14 percent on this investment, how much will you

pay for the contract to day?

g) Making- decisions P2-37) Plly Graham will receive $ 12,000 a year for the next 15 years as the result of her patent. If a 9 percent rate is applied, should she be willing to sell

out her future rights now for $100,000?

Compiled by Nut khorn Page 34

P2-38) Your rich uncle has offered you a choice of one of the three following alternatives: $10,000 now; $2,000 a year for eight years; or $24,000 at the

end of eight years. Assuming you could earn 11 percent annually, which alternative should you choose? If you could earn 12% percent annually, would you still choose the

same alternative?

h) Perpetuity PVr

C

P2-39) Consider a perpetuity paying $100 a year. If the relevant interest rate is 8 percent,

what is the value of consol?

P2-40) The market interest rate is 15 percent. What is the price of a consol bond that pays $120

annually?

P2-41) If the rate of interest is 10 percent and if the aim is to provided $100,000 a year in

perpetuity, What is the amount that must be set aside today?

Future Value of an Annuity (FVA) : ]1

[)1(

rCFV

rt

P2-42) If you deposit $1,000 at the end of each of the next 20 years into an account paying 8.5

percent interest, how much money will you have in the account in 20 years? How much will

you have if you make deposits for 40 years?

P2-43) . Assume an ordinary annuity of $500 at the end of each of the next three years:

What is the future value at 10%?

P2-44). What is the future value at the end of year 6 of a six-year annuity of $1,000 per year if

the expected return is 10%?

P2-45) You want to have $50,000 in your savings account five years from now, and you‘re

prepared to make equal annual deposits into the account at the end of each year. If the account

pays 9.5 percent interest, what amount must you deposit each year?

P2-46) Find the effective annual interest rate for each case:

APR Compounding Period

12% Monthly

8% Quarterly

10% Semiannually P2-47) Find the APR (the stated interest rate) for each case:

EAR Compounding Period

10% Monthly

5% Quarterly

24% Semiannually

P2-48)

The going rate on student loans is quoted as 8 percent APR. The terms of the loans call for

monthly payments. What is the effective annual rate (EAR) on such a student loan?

P2-49) Find the EAR in each of the following cases:

Compiled by Nut khorn Page 35

P2-50)

Find the APR, or stated rate, in each of the following cases:

P2-51)

First National Bank charges 7.5 percent compounded quarterly on its business loans. First

United Bank charges 7.5 percent compounded semiannually. As a potential borrower, which

bank would you go to for a new loan?

Chapter Quiz

1

Gloria wants to have $20,000 in her investment account ten years from now. Currently, she has nothing saved. How much would she have to deposit today to reach her goal if

this is the only amount she invests? She expects to earn 8.5 percent, compounded annually. How much must she deposit today?

A) $11,520.74

B) $9,684.28

C) $8,845.71

D) $14,705.88

2

Four years ago, your baseball card collection was worth $1,200. You have not added any cards to the collection over the past four years, but the collection has still increased in value. Today, it is worth $1,500. What rate of return are you earning on this collection?

A) 5.74 percent

B) 6.23 percent

C) 4.98 percent

D) 5.25 percent

3

Amy invested $1,500 in a stock that has returned 12 percent, compounded annually. Today, that investment is worth $3,600. How long has Amy owned this stock?

A) 5.92 years

B) 6.54 years

C) 7.18 years

D) 7.73 years

4

When your parents got married 38 years ago, they purchased a house for $31,900. They have taken good care of the house but have not invested any more money into it. Today, their house is valued at $149,900. What rate of return have your parents earned on their home?

A) 3.92 percent

B) 4.16 percent

Compiled by Nut khorn Page 36

C) 4.58 percent

D) 5.39 percent

5

Which one of the following statements is correct, assuming all else is constant?

A) The discount rate increases as the present value increases.

B) The future value decreases as the present value increases.

C) The time period increases as the interest rate increases.

D) The present value increases as the discount rate decreases.

6

You invested $5,000 at 6 percent simple interest for five years. How much total interest will you earn over these five years?

A) $300.00

B) $742.97

C) $1,500.00

D) $1,691.13

7

Scott and Todd are twins. Scott invests $50 a month for ten years starting on his 20th birthday. Todd invests $50 a month for ten years starting on his 25th birthday. Both Scott and Todd earn 7 percent. Which one of the following statements is correct based on this information? Assume they never withdraw any money from their accounts.

A)

Both Scott and Todd will have the same amount saved when they turn 60 if the

7 percent is simple interest.

B) Scott and Todd will earn the same amount of interest during the year of their 40th birthday if the 7 percent is simple interest.

C) Todd will have more money saved than Scott when they are 70 years old if the 7 percent is compounded annually.

D)

Scott and Todd will earn the same amount of interest during the year of their 50th birthday if the 7 percent is compounded annually.

8

Flo deposited $5,000 into her retirement account today. How much money will she have 40 years from now if this is the only deposit she makes and she earns an average of 13

percent, compounded annually?

A) $597,264

B) $648,306

C) $663,908

D) $671,909

9

You have been offered a business opportunity that will pay you $57,000 in six years if you

invest $25,000 today. What is the expected rate of return on this investment?

A) 14.72 percent

B) 15.36 percent

C) 15.78 percent

D) 16.22 percent

10

According to the Rule of 72, how long will it take you to double your money is you can

earn a 6 percent rate of return?

A) 6 years

B) 7.2 years

Compiled by Nut khorn Page 37

C) 9 years

D) 12 years

11

What is the interest rate per period multiplied by the number of periods per year called?

A) effective annual yield

B) compounded effective yield

C) periodic rate

D) annual percentage rate

12

Your employer has offered to contribute $50 a week to your retirement savings account.

Assume you work for this employer for another 15 years and earn an average return of 8.5 percent, compounded weekly, on your savings. What is this offer worth to you today?

A) $39,000

B) $42,315

C) $78,764

D) $81,309

13

This morning, you purchased some stereo equipment costing $2,659. You charged this purchase on your credit card. This card charges 16.9 percent interest, compounded monthly. How long will it take you to pay off this purchase if this is the only charge on your credit card and you make monthly payments of $40?

A) 15.13 years

B) 12.95 years

C) 14.82 years

D) 16.40 years

14

Every month for the past eight years you have invested $50 in a mutual fund. Today, your account is valued at $6,419. What rate of return have you been earning on this

investment?

A) 7.03 percent

B) 5.86 percent

C) 6.29 percent

D) 6.54 percent

15

You just purchased a home and agreed to a mortgage payment of $1,264 a month for 30

years at 7.5 percent interest, compounded monthly. How much interest will you pay over the life of this mortgage assuming that you make all payments as agreed?

A) $181,267

B) $274,266

C) $387,280

D) $455,040

16

You are going to receive $6,000 at the end of each quarter for the next five years. What is the net present value of these payments at a discount rate of 7 percent, compounded

Compiled by Nut khorn Page 38

quarterly?

A) $63,564

B) $100,517

C) $102,276

D) $103,012

17

What is the effective annual rate of 10.75 percent compounded continuously?

A) 11.04 percent

B) 11.19 percent

C) 11.30 percent

D) 11.35 percent

18

A preferred stock pays annual dividends of $1.80 per share. What is this stock worth to you today if you desire a 14.5 percent return on this investment?

A) $11.87

B) $12.41

C) $25.98

D) $26.10

19

A project will produce cash flows of $2,400, $2,800, and $4,100 a year for the next three years, respectively. What is the net value of these cash flows today if the applicable

discount rate is 12 percent?

A) $7,778.80

B) $8,056.16

C) $7,293.30

D) $8,303.57

20

Sue plans to save $100 at the beginning of each month for the next five years. Scott plans

to save $100 at the end of each month for the next five years. Assume that both Sue and Scott earn 4.5 percent on their savings. Which one of the following statements is correct given this information?

A) Sue will have $6,721.68 at the end of the five years.

B) Sue will have $25.17 more in her account than Scott will have in his account at the end of the five years.

C)

Scott will have $8.67 more in his account than Sue will have in her account after the first three years.

D)

Both Sue and Scott will have the same amount of money in their accounts after

five years.

End of the problem of Chapter 2

Compiled by Nut khorn Page 39

Chapter 3: Interest Rates and Bond Valuation After studying this chapter, you should understand:

LO1 Important bond features and types of bonds.

LO2 Bond values and yields and why they fluctuate.

LO3 Bond ratings and what they mean.

LO4 The impact of inflation on interest rates.

LO5 The term structure of interest rates and the determinants of bond

yields.

Compiled by Nut khorn Page 40

Valuation of Bonds and Stock

First Principles:

Value of financial securities = PV of expected future cash flows

To value bonds and stocks we need to:

Estimate future cash flows:

Size (how much) and

Timing (when)

Discount future cash flows at an appropriate rate:

The rate should be appropriate to the risk presented by the security.

Bonds and Bond Valuation When a corporation (or government) wishes to borrow money from the public on a long-term

basis, it usually does so by issuing or selling debt securities that are generically called bonds.

In this section, we describe the various features of corporate bonds and some of the

terminology associated with bonds. We then discuss the cash flows associated with a bond and

how bonds can be valued using our discounted cash flow procedure.

Bond Features and Prices

As we mentioned in our previous chapter, a bond is normally an interest-only loan, meaning

that the borrower will pay the interest every period, but none of the principal will be repaid

until the end of the loan. For example, suppose the Beck

Corporation wants to borrow $1,000 for 30 years. The interest rate on similar debt issued by

similar corporations is 12 percent. Beck will thus pay .12 x $1,000 = $120 in interest every

year for 30 years. At the end of 30 years, Beck will repay the $1,000.

As this example suggests, a bond is a fairly simple financing arrangement. There is, however, a

rich jargon associated with bonds, so we will use this example to define some of the more

important terms.

In our example, the $120 regular interest payments that Beck promises to make are called the

bond‘s coupons. Because the coupon is constant and paid every year, the type of bond we are

describing is sometimes called a level coupon bond. The amount that will be repaid at the end

of the loan is called the bond‘s face value, or par value. As in our example, this par value is

usually $1,000 for corporate bonds, and a bond that sells for its par value is called a par value

bond. Government bonds frequently have much larger face, or par, values. Finally, the annual

coupon divided by the face value is called the coupon rate on the bond; in this case, because

$120/1,000 = 12%, the bond has a 12 percent coupon rate.

The number of years until the face value is paid is called the bond‘s time to maturity. A

corporate bond will frequently have a maturity of 30 years when it is originally issued, but this

varies. Once the bond has been issued, the number of years to maturity declines as time goes

by.

Bond Values and Yields As time passes, interest rates change in the marketplace. The cash flows from a bond, however,

stay the same. As a result, the value of the bond will fluctuate. When interest rates rise, the

present value of the bond‘s remaining cash flows declines, and the bond is worth less. When

interest rates fall, the bond is worth more.

To determine the value of a bond at a particular point in time, we need to know the number of

periods remaining until maturity, the face value, the coupon, and the market interest rate for

bonds with similar features. This interest rate required in the market on a bond is called the

bond‘s yield to maturity (YTM). This rate is sometimes called the bond‘s yield for short.

Given all this information, we can calculate the present value of the cash flows as an estimate

of the bond‘s current market value.

For example, suppose the Xanth (pronounced ―zanth‖) Co. were to issue a bond with 10 years

to maturity. The Xanth bond has an annual coupon of $80. Similar bonds have a yield to

Compiled by Nut khorn Page 41

maturity of 8 percent. Based on our preceding discussion, the Xanth bond will pay $80 per

year for the next 10 years in coupon interest. In 10 years, Xanth will pay $1,000 to the owner

of the bond. The cash flows from the bond are shown in Figure 3. What would this bond sell

for?

As illustrated in Figure 3 , the Xanth bond‘s cash flows have an annuity component (the

coupons) and a lump sum (the face value paid at maturity). We thus estimate the market value

of the bond by calculating the present value of these two components separately and adding the

results together. First, at the going rate of 8 percent, the present value of the $1,000 paid in 10

years is:

3.1 Definition and Example of a Bond A bond is a legally binding agreement between a borrower and a lender:

Specifies the principal amount of the loan.

Specifies the size and timing of the cash flows:

In dollar terms (fixed-rate borrowing)

As a formula (adjustable-rate borrowing)

Coupon: The stated interest payment made on a bond.

Face value: The principal amount of a bond that is repaid at the end of the term. Also, par

value.

Coupon rate: the annual coupon divided by the face value of a bond.

Maturity: Specified date on which the principal amount of a bond is paid.

Yield to maturity (YTM): the rate required in the market on a bond.

Definition and Example of a Bond

Consider a U.S. government bond listed as 6 3/8 of December 2009.

The Par Value of the bond is $1,000.

Coupon payments are made semi-annually (June 30 and December 31 for this

particular bond).

Since the coupon rate is 6 3/8 the payment is $31.875.

On January 1, 2005 the size and timing of cash flows are:

3.2 How to Value Bonds Identify the size and timing of cash flows.

$31.875 $31.875

$31.875

$31.875

$1,031.875

1/1/05 6/30/05 12/30/05 6/30/09 12/06/09

Figure 3 : Cash flows of Bond

Compiled by Nut khorn Page 42

0

0 $

1

0 $

2

0 $

1 -

T

F $

t

Discount at the correct discount rate.

If you know the price of a bond and the size and timing of cash flows, the yield

to maturity is the discount rate.

Pure Discount Bonds Information needed for valuing pure discount bonds:

Time to maturity (T) = Maturity date - today‘s date

Face value (FV)

Yield to Maturity (YTM)

Present value of a pure discount bond at time 0:

Example: Find the value of a 30-year zero-coupon bond with a $1,000 par value and a YTM

of 6%.

11.174$000,1$

)06.01()1(30

YTMt

FVPV

Level-Coupon Bonds Information needed to value level-coupon bonds:

Coupon payment dates and time to maturity (t)

Coupon payment (C) per period and Face value (FV)

Yield to maturity (FV)

Notes: rFVC where r = discount rate

Value of a Level-coupon bond = PV of coupon payment annuity + PV of face value

)1()1(

11

YTMYTMtt

FV

YTM

cPV

Example: Find the present value (as of January 1, 2004), of a 6-3/8 coupon T-bond with semi-

annual payments, and a maturity date of December 2009 if the YTM is 5-percent.

On January 1, 2004 the size and timing of cash flows are:

tYTM

FVPV

)1(

0

0

0$

1

0$

2

0$

29

000,1$

30

0

0$

1

0$

2

0$

29

000,1$

30

0

0

C$

1

C$

2

C$

1T

FC $$

T

Compiled by Nut khorn Page 43

52.070,1$000,1$1

12/05.0

875.31$

)025.01()025.01( 1212

PV

Bond Concepts 1. Bond prices and market interest rates move in opposite directions.

2. Putting together our observations about yield measures, we have the following:

a) Premium bonds: Coupon rate > Current yield > Yield to maturity

b) Discount bonds: Coupon rate < Current yield < Yield to maturity

c) Par value bonds: Coupon rate = Current yield = Yield to maturity

3. A bond with longer maturity has higher relative (%) price change than one with shorter

maturity when interest rate (YTM) changes. All other features are identical.

4. A lower coupon bond has a higher relative price change than a higher coupon bond

when YTM changes. All other features are identical.

Bond Markets Bonds are bought and sold in enormous quantities every day. You may be surprised to learn

that the trading volume in bonds on a typical day is many, many times larger than the trading

volume in stocks (by trading volume, we simply mean the amount of money that changes

hands). Here is a finance trivia question: What is the largest securities market in the world?

Most people would guess the New York Stock Exchange. As if! In fact, the largest securities

market in the world in terms of trading volume is the U.S. Treasury market.

How Bonds Are Bought and Sold

As we mentioned all the way back in Chapter 1, most trading in bonds takes place over the

counter, or OTC. Recall that this means that there is no particular places where buying and

selling occur. Instead, dealers around the country (and around the world) stand ready to buy

and sell. The various dealers are connected electronically.

One reason the bond markets are so big is that the number of bond issues far exceeds the

number of stock issues. There are two reasons for this. First, a corporation would typically

have only one common stock issue outstanding (there are exceptions to this that we discuss in

our next chapter). However, a single large corporation could easily have a dozen or more note

and bond issues outstanding. Beyond this, federal, state, and local borrowing is simply

enormous. For example, even a small city would usually have a wide variety of notes and

bonds outstanding, representing money borrowed to pay for things like roads, sewers, and

schools. When you think about how many small cities there are in the United States, you begin

to get the picture!

Because the bond market is almost entirely OTC, it has little or no transparency.

A financial market is transparent if it is possible to easily observe its prices and trading

volume. On the New York Stock Exchange, for example, it is possible to see the price and

……………

1/1/04 6/30/04 12/31/04 6/30/09 12/31/09

$31.875 $31.875

$31.875

$1,031.875

Compiled by Nut khorn Page 44

quantity for every single transaction. In contrast, in the bond market, it is usually not possible

to observe either. Transactions are privately negotiated between parties, and there is little or no

centralized reporting of transactions.

Although the total volume of trading in bonds far exceeds that in stocks, only a very small

fraction of the total bond issues that exist actually trade on a given day.

This fact, combined with the lack of transparency in the bond market, means that getting up-to-

date prices on individual bonds is often difficult or impossible, particularly for smaller

corporate or municipal issues. Instead, varieties of sources of estimated prices exist and are

very commonly used.

Bond Price Reporting

Although most bond trading is OTC, there is a corporate bond market associated with the New

York Stock Exchange. If you were to look in The Wall Street Journal (or similar financial

newspaper), you would find price and volume information from this market on a relatively

small number of bonds issued by larger corporations.

This particular market represents only a sliver of the total market, however.

Mostly, it is a ―retail‖ market, meaning that smaller orders from individual investors are

transacted here. Bond quotes are shown in Figure 4

Formulas of the Bonds

1) Zero-coupon Bond:

)1( YTM t

FVPV

2) Level-Coupon Bond

a) Annually:

)1()1(

11

YTMYTM tt

FV

YTM

CPV

rFVC

b) Semi-annually:

)2

1()2

1(22

11

YTMYTM tt

FV

YTM

CPV

3) Find YTM

Figure 4: Bond Quotes

Compiled by Nut khorn Page 45

FVPVt

PVFVC

YTM4.06.0

PV

CCouponCYYieldCurrent

AmountBaseAmountCurrentChangeNet

PriceClosing)(

In Microsoft Excel

1) Annually: =pv(YTM,t,r*1,000,1,000)*-1

2) Semi-annually: =pv(YTM/2,t*2,r/2*1,000,1000)*-1

Compiled by Nut khorn Page 46

Problem on Chapter 3:

P3-1: What is the present value of a 10-year, pure discount bond that pays $1,000 at maturity

and is price to yield the following rate:

a) 5 percent

b) 10 percent

c) 15 percent

P3-2. The Lone Star Company has $1,000 par value of bonds outstanding at

9 percent interest. The bonds will mature in 20 years. Compute the current price of the bonds if the present yield to maturity is:

a) 6 percent. b) 8 percent.

c) 12 percent. P3-3. Applied Software has $1,000 par value bonds outstanding at 12

percent interest. The bonds will mature in 25 years. Compute the current price of the bonds if the present yield to maturity is:

a) 11 percent. b) 13 percent.

c) 16 percent. P3-4. The Hartford Telephone Company has a $1,000 par value bond

outstanding that pays 11 percent annual interest. The current yield to

maturity on such bonds in the market is 14 percent. Compute the price of bonds for these maturity dates:

a. 30 years. b. 15 years.

C. 1 year. P3-5. Ron Rhodes calls his broker to require about purchasing a bond of

Golden Year Recreation Corporation. His broker quotes a price of $1,170. Ron is concerned that the bond might be overpriced based on the fact

involved. The $1,000 par value of bond pays 13 percent interest, and it has 18 years remaining until maturity. The current yield to maturity on similar

bonds is 11 percent. Do you think the bond is overpriced? Do the necessary calculations.

P3-6. What is the present value of a 20-year pure discount bond paying

$1,000 at maturity if the approximate interest rate is:

a. 3 percent. b. 7 percent.

c. 25 percent. P3-7. Heather Smith is considering a bond investment in Locklear Airlines.