comparative healthcare financing trends in … · comparative healthcare financing trends in europe...

TRANSCRIPT

An IHS Life Sciences report

May 2016

COMPARATIVE HEALTHCARE FINANCING TRENDS IN EUROPE

A RETROSPECTIVE AND FORWARD-LOOKING VIEW

I. Executive summary ..................................................................................................... 3

II. Introduction ............................................................................................................... 5

III. Comparative retrospective analysis .............................................................................. 7

3.1 Public healthcare spending ................................................................................................................................ 7

3.2 Private healthcare spending ............................................................................................................................ 12

3.3 Pharmaceutical spending ................................................................................................................................ 17

3.4 Categories of care spending ............................................................................................................................. 26

3.5 Distribution of direct cancer care costs ............................................................................................................ 28

IV. Future trends analysis ............................................................................................... 31

7.1 Forecast public healthcare spending ................................................................................................................ 31

7.2 Forecast private healthcare spending ............................................................................................................... 36

7.3 Forecast pharmaceutical spending ................................................................................................................... 40

7.4 Forecast oncology pharmaceutical spending .................................................................................................... 45

7.5 Projected budget impact of emerging therapy classes ...................................................................................... 50

V. Conclusions .............................................................................................................. 55

VI. Appendix .................................................................................................................. 57

7.1 Additional country details ............................................................................................................................... 57

7.1.1 France ............................................................................................................................................................ 57

7.1.2 Germany ........................................................................................................................................................ 58

7.1.3 The Netherlands ............................................................................................................................................. 61

7.1.4 Poland ............................................................................................................................................................ 62

7.1.5 Spain .............................................................................................................................................................. 64

7.1.6 The UK ........................................................................................................................................................... 67

7.2 Macroeconomic data ...................................................................................................................................... 69

7.3 Data sources ................................................................................................................................................... 80

7.3.1 Total and private healthcare expenditures ....................................................................................................... 81

7.3.2 Categories of care spending ............................................................................................................................. 82

7.3.3 Public pharmaceutical reimbursement spending .............................................................................................. 83

7.4 Budget impact methodology ........................................................................................................................... 88

I. EXECUTIVE SUMMARY

Even before the onset of the 2008 financial crisis, European countries faced an imperative to contain costs.

Ageing populations and the growing challenge of meeting the associated healthcare demands saw countries

turn to emergency measures or embark upon substantive reforms to consolidate cost savings. In the

recessionary period that followed, cost-containment measures intensified, leading to negative or subdued

real-terms growth in public healthcare expenditures from the -3.6% compound annual growth rate over

2010-2014 observed in France to the 1.7% observed in Poland.

Despite representing a considerably smaller share of total public healthcare expenditure relative to

inpatient and ambulatory care costs, pharmaceuticals were a key target for cost containment over the

2010-14 period. Overall public-sector outlays for reimbursement spending on medicines saw significant

year-on-year (y/y) contractions in most countries, reaching 15% y/y in Poland.

Most European countries also saw higher rates of growth in private healthcare expenditure over this

period, on average three-to-seven percentage points above growth in public outlays in real terms. Rising

private contributions were associated with increases in the out-of-pocket (OOP) burden facing patients,

concentrated on pharmaceuticals in particular. Spain, one of the countries worst impacted by the financial

crisis, is estimated to have seen OOP spending increase from 78% of total

private healthcare expenditure in 2010 to 86% a year later.

This rising burden has led to serious debates surrounding the impact on access

and health outcomes. With growth in public healthcare expenditure expected

to remain negative or subdued in real terms through 2020, this raises important

questions over the potential impact on outcomes if pharmaceuticals remain a

key target for cost containment.

A reflection of gradual economic recovery, growth in overall public

pharmaceutical spending through 2020 is forecast to pick up pace relative to

the 2010-14 period in most countries. Reimbursement expenditure on oncology is expected to outpace the

pharmaceutical market as a whole, given the significant number of innovative treatments in this therapy

area anticipated to enter the market.

However, high growth scenarios envision compound annual growth of 6% to

8.4% in this expenditure, with oncology forecast to account for a broadly

comparable share of overall drug reimbursement spending relative to recent

trends. Under the high growth scenario, oncology’s share is forecast to

represent between 9% and 11% on average, with the exception of Poland at

31.2%. Budget impact analyses of some of the most significant breakthrough

treatments in breast cancer and non-small cell lung cancer suggest these

agents will absorb no more than 2.5% of projected oncology drug

The rising out-of-pocket

burden concentrated on

pharmaceuticals has led

to serious concerns

surrounding the impact

on access and ultimately

health outcomes.

Current anxieties

surrounding

sustainability of funding

for the next generation of

breakthroughs in

oncology may be

exaggerated.

reimbursement spending.

These findings, based on the potential budget impact of new treatments in some of the most common

cancers, suggest that current anxieties surrounding sustainability of funding may be exaggerated in certain

countries. Taking stock of current policy tools and the opportunities countries possess to achieve cost

savings in those areas of care which dominate spending – in particular, inpatient hospital care – forecast

expenditure appears broadly manageable.

Certain countries such as Poland and Spain are forecast to experience more acute financing challenges

given pre-existing inequities in access, other funding priorities and/or ongoing struggles to reign in deficit

spending. In these countries, a combination of already anticipated policy reforms and new policy

innovations involving broad-based stakeholder dialogue may be necessary to support comprehensive

access to emerging treatments.

This report was commissioned by AstraZeneca. All research and analysis were undertaken

independently by IHS Life Sciences.

II. INTRODUCTION

The past five years have been accompanied by a major shift in thinking in the world of healthcare. With

the genericization of atorvastatin in 2011, the era of on-patent, primary-care blockbuster drugs seemed to

have reached its high watermark. Healthcare systems around the world were prepared to benefit from the

so-called patent cliff, seeing new levels of cost containment achievable on the back of generic uptake. The

pharmaceutical industry faced serious question marks over declining R&D productivity and a dearth of

pipeline candidates.

Since that time, a new reality has emerged. The primary-care blockbuster model typified by atorvastatin

has given way to a new era of biologic and innovative small-molecule drugs broadly targeting specialist

care. A focus on targeted therapies in diseases like non-small cell lung cancer and melanoma, coupled with

progress in orphan and ultra-orphan diseases, has seen niche indications associated with premium pricing

come to play an unprecedented role in the treatment landscape.

High-cost therapies do not only reflect a move toward smaller patient

populations. The arrival of next-generation hepatitis C drugs such as sofosbuvir

has seen entry onto the market of agents associated with remarkable cure rates

that hold the potential to revolutionize treatment for relatively large numbers of

patients. Against this backdrop, question marks over the sustainability of industry

pipelines have been replaced by question marks over the sustainability of

healthcare systems.

Over the next five years, a wealth of new treatments are expected to reach the

market. Many of these innovations will be in the cancer field, where advances in immuno-oncology have

shown the potential of breakthrough treatments to significantly extend survival. Oncology will also see an

unprecedented move toward combination therapies, as emerging and existing products are found to

significantly enhance outcomes in concert in both existing and new indications.

What is without question an immense wave of progress for patients is also

posing increasingly challenging questions for policymakers, payers and

healthcare stakeholders more broadly. Accentuated by the global financial

crisis, and driven by long-term dynamics such as ageing populations and a

slowing pace of economic growth, many countries are in the midst of, or

embarking upon, major cost-saving drives. The need to address systemic

shortfalls in government financing of healthcare is pronounced in a number of

European countries. This reality means that the next wave of treatment

breakthroughs coincides with a period when cost containment is firmly on the

healthcare system agenda.

Question marks over

the sustainability of

industry pipelines have

been replaced by

question marks over

the sustainability of

healthcare systems.

The next wave of

treatment

breakthroughs

coincides with a period

when cost

containment is firmly

on the healthcare

system agenda.

Although much has been said regarding the sustainability of pharmaceutical spending, and debate has

centred in particular on list prices of emerging therapies, what has been absent so far is a critical analysis

which helps to frame the discussion in terms of broader healthcare financing trends, both recent and

forecast. The present report aims to evolve the current debate by providing such an analysis, looking at

healthcare financing trends over the retrospective period of 2010 to 2014, as well as looking forward

through 2020.

This analysis focuses on France, Germany, the Netherlands, Poland, Spain and the United Kingdom

(sometimes focused specifically on England for reasons of data availability). These countries were chosen to

represent a cross-section of Europe, reflecting a diverse set of healthcare systems, pharmaceutical pricing

and reimbursement policies, economic conditions and political circumstances. The analysis is intended to

be broadly applicable to other countries inasmuch as similarities across these factors permit extrapolation

of findings.

This report considers the structure of the healthcare market in each country with regards to public and

private contributions, how expenditure is distributed across different categories of care, and the evolution

of pharmaceutical spending both in general and with a particular focus on oncology. Exploration of these

broad trends in financing is joined by a consideration of policies pursued by these countries which have

enabled them to support access to innovations in treatment while managing costs. This retrospective

analysis lays the groundwork for a forecast of future trends through to 2020, looking to identify how market

structures and government policies are likely to position countries going forward.

In order to forecast future trends in expenditure, the analysis relies on a number of data sources and

methodologies. Top-line projections for overall healthcare and pharmaceutical spending and the

components of private market expenditure come from the IHS World Markets Healthcare Forecasts service,

which derives its forecasts based on projected economic growth and historical relationships between that

growth and various healthcare expenditure indicators. Economic growth forecasts derive from the

comprehensive macroeconomic data comprising the IHS World Economic Service.

Literature review and analysis of recent expenditure patterns and policy and cost-containment measures

were relied upon to derive a number of scenarios for future public reimbursement spending on oncology

pharmaceuticals specifically. A budget impact modelling approach was developed for a number of therapy

classes in order to interrogate these forecasts and validate their ability to absorb the financing

requirements of significant new treatments.

This report is accompanied by a detailed appendix in section VII, which outlines the data sources utilised,

offers a glossary of terms, provides various macroeconomic indicators for all countries, and explains the

above methodologies relied upon to generate the relevant forecasts and budget impact scenarios. It also

provides additional commentary on the market and policy landscapes for readers wishing to acquire further

details on a specific country.

III. COMPARATIVE RETROSPECTIVE ANALYSIS

3.1 PUBLIC HEALTHCARE SPENDING

European countries entered the crisis with both shared and unique healthcare challenges

Trends in healthcare spending between 2010 and 2014 must be placed in the context of the extraordinary

economic circumstances impacting European countries over that period. This window of time spans the

latter part of the recession sparked by the 2008 financial crisis, as well as the roots of economic recovery

since 2012.

Leading up to 2008, European countries were united in facing the secular trend of ageing populations and

the growing challenge of meeting the associated healthcare demands, creating a broad-based focus on

cost containment. Against this backdrop, however, countries exhibited different priorities and spending

commitments, some associated with reforms designed to consolidate cost savings in the long run:

France: The country faced a longstanding agenda to address the deficits plaguing its social security

system, with the national target for public healthcare spending overrun on average by EUR1.5 billion

each year since 1997.i

Germany: Despite its statutory healthcare system benefiting from relatively strong reserves, like France

the country was focused on cost containment due to its ageing population, including preparation of

major reforms to its system of free pricing for innovative pharmaceuticals.

The Netherlands: The country saw erratic growth in healthcare expenditure in the run up to the crisis,

with temporary surges in spending associated with implementation of a new statutory health insurance

system in 2006.

Poland: The country witnessed marked economic growth from the mid-1990s, helping drive an

approximately five-fold increase in total healthcare expenditure by 2009 as the government sought to

improve the relatively poor level of access and address the high out-of-pocket burden.

Spain: Like the Netherlands, the country experienced erratic growth in healthcare expenditure, seeing

periodic upticks in spending after its 17 autonomous communities took control of their healthcare

budgets in 2002.

England: Starting with the Labour government which came to power in 1997, England sought to

increase public healthcare spending as a share of GDP to bring it in line with the European average.

All countries experienced a slowdown in real-terms healthcare spending growth relative to pre-crisis

levels

As illustrated in Figure 1, in nominal terms, countries can be divided into those which saw declines in public

healthcare spending at the start of the 2010-14 period, and those which witnessed rising expenditures

throughout that time window.

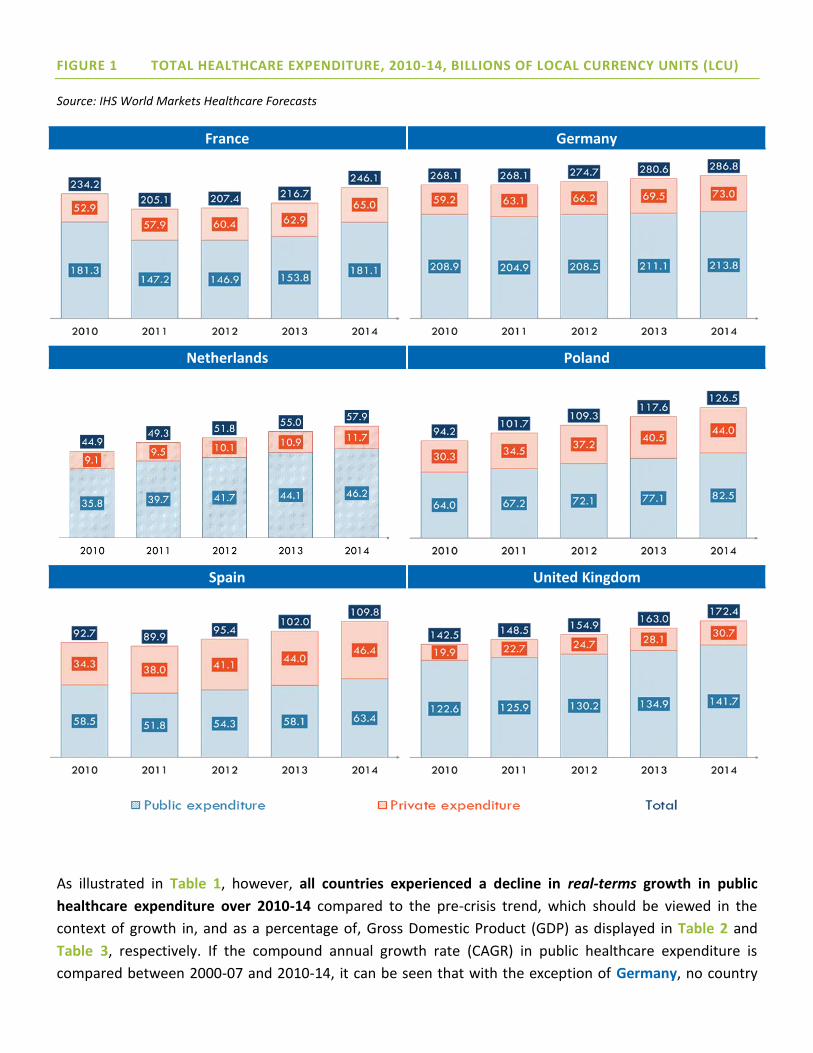

FIGURE 1 TOTAL HEALTHCARE EXPENDITURE, 2010-14, BILLIONS OF LOCAL CURRENCY UNITS (LCU)

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain United Kingdom

As illustrated in Table 1, however, all countries experienced a decline in real-terms growth in public

healthcare expenditure over 2010-14 compared to the pre-crisis trend, which should be viewed in the

context of growth in, and as a percentage of, Gross Domestic Product (GDP) as displayed in Table 2 and

Table 3, respectively. If the compound annual growth rate (CAGR) in public healthcare expenditure is

compared between 2000-07 and 2010-14, it can be seen that with the exception of Germany, no country

saw less than a four percentage-point drop in the real-terms CAGR in public healthcare spending between

the two periods.

TABLE 1 REAL-TERM COMPOUND ANNUAL GROWTH RATES IN PUBLIC HEALTHCARE EXPENDITURE,

2000-07 & 2010-14

2000-07 2010-14

France 3.1% -3.6%

Germany -1.2% -3.0%

The Netherlands 5.7% 1.6%

Poland 6.2% 1.7%

Spain 8.6% -0.9%

The UK 4.2% -1.2%

Source: IHS World Markets Healthcare Forecasts

TABLE 2 REAL AND NOMINAL YEAR-ON-YEAR GROWTH IN GROSS DOMESTIC PRODUCT, 2010-2014

2010 2011 2012 2013 2014

France Real 1.88% 2.09% 0.21% 0.75% 0.17%

Nominal 2.98% 3.05% 1.37% 1.51% 0.74%

Germany Real 3.94% 3.72% 0.62% 0.41% 1.58%

Nominal 4.87% 4.77% 1.91% 2.55% 3.35%

Netherlands Real 1.32% 1.66% -1.06% -0.41% 1.01%

Nominal 2.21% 1.81% 0.35% 0.93% 1.83%

Poland Real 3.71% 5.01% 1.55% 1.29% 3.35%

Nominal 6.11% 8.41% 3.99% 1.68% 3.79%

Spain Real 0.03% -1.00% -2.62% -1.67% 1.36%

Nominal 0.17% -0.97% -2.57% -1.11% 0.96%

The UK Real 1.54% 1.97% 1.18% 2.16% 2.85%

Nominal 4.70% 4.11% 2.82% 4.19% 4.74%

Source: IHS Global Economic Data

TABLE 3 GENERAL GOVERNMENT HEALTH EXPENDITURE AS A PERCENTAGE OF GROSS DOMESTIC

PRODUCT, 2010-2014

2010 2011 2012 2013 2014

France 8.68% 8.73% 8.83% 8.91% 9.02%

Germany 8.58% 8.31% 8.36% 8.57% 8.70%

The Netherlands 9.08% 9.09% 9.53% 9.62% 9.48%

Poland 4.90% 4.71% 4.58% 4.53% 4.51%

Spain 7.17% 7.00% 6.73% 6.50% 6.40%

The UK 7.94% 7.77% 7.80% 7.78% 7.58%

Source: World Health Organization Global Health Expenditure database

The downturn in the rate of healthcare spending growth does not necessarily reflect how severely each

country was impacted by the financial crisis. Poland, for example, avoided recession thanks to ongoing

public investments, but witnessed a decline in the CAGR in public healthcare spending of similar magnitude

to the Netherlands, where bursting of the country’s housing bubble led Dutch citizens to become some of

the most indebted in the Eurozone following the outbreak of the crisis.

Rather, these downturns reflect the extent to which different countries targeted healthcare – and in

many cases, pharmaceuticals in particular – in order to achieve cost savings in the public sector. That the

decline was relatively marginal in Germany indicates the extent to which some countries were already

undertaking significant cost-containment drives even before the onset of the crisis.

Growth in healthcare expenditure has remained subdued or faced significant cost-containment targets

since the roots of economic recovery

The roots of economic recovery saw public healthcare expenditure recover its losses by 2012 or 2013 in

France, Germany and Spain, leading to significant year-on-year (y/y) increases in some cases. However, by

period close, most countries were engaged in significant cost-savings drives or undertaking careful budget

management:

France: From 2010, the country’s annual target for health spending (l’Objectif National des Dépenses

d'Assurance Maladie: ONDAM) was limited to a maximum annual increase of 3%, subsequently revised

downwards in light of diminished economic growth prospects.

Germany: The country remained committed to cost containment, as evident even before the crisis,

with many of the associated policies focused on pharmaceutical expenditure (see discussion on trends

in pharmaceutical expenditure below).

The Netherlands: In the aftermath of the financial crisis, there was an increasing emphasis placed on

cost containment. Although the healthcare budget was allowed to grow despite a series of broader

austerity packages, growth was inevitably very subdued.

Poland: The public investments which helped Poland weather the financial crisis better than other

European countries subsequently led to concerns over the scale of public debt, weighing down on

growth in public spending relative to the pre-crisis period.

Spain: The worst impacted by the recession and Eurozone debt crisis amongst the countries considered

in this report, Spain’s economic recovery was delayed and still fragile, with persistently high levels of

unemployment and the consequent need to carefully manage outlays on healthcare as autonomous

communities struggled to balance their deficits.

The UK: The National Health Service (NHS) in England faced a target of GBP20 billion in efficiency

savings by 2015, with the scale of the deficits faced by provider organisations recognised to require

further cost savings in future.

KEY TAKE AWAY

The recent economic downturn led to significant declines in the rate of growth of public outlays on

healthcare in most European countries. However, even before the outbreak of the crisis, the secular trends

of ageing populations and reduced economic growth prospects in the developed world saw European

countries increasingly focused on cost containment. This reality meant that even countries such as Poland

and the UK, committed to aligning healthcare spending and outcomes with the European average, have had

to carefully manage new investments with cost savings.

The broad-based focus on cost containment, which has persisted beyond the recession, raises important

question marks over whether access to care and health outcomes have been negatively impacted. As the

discussion below on trends in private healthcare spending and pharmaceutical expenditure indicates, there

is reason to believe that the subdued rate of growth in healthcare spending has indeed restricted the

ability of European countries to maintain their commitment to universal access to comprehensive care.

3.2 PRIVATE HEALTHCARE SPENDING

Most European countries saw comparatively higher rates of growth in private healthcare expenditure

over 2010-14

Compared to the subdued rates of growth in public outlays on healthcare over the 2010-14 period, which in

real terms did not surpass approximately 2% y/y, European countries saw significantly higher growth in

real-terms private healthcare expenditure.

As shown in Table 4, with the exception of the Netherlands, which experienced a negative real-terms CAGR

in private healthcare spending over this time period, European countries saw private contributions toward

healthcare increase by approximately three-to-seven percentage points more y/y than public outlays in real

terms. This suggests that private sources of funding have plugged a gap left by the cost-containment

efforts characterising public-sector healthcare financing.

TABLE 4 REAL-TERM COMPOUND ANNUAL GROWTH RATES IN PRIVATE HEALTHCARE EXPENDITURE,

2010-14

2010-14 Difference relative to public outlays

France 1.5% 5.1%

Germany 1.6% 4.6%

The Netherlands -3.2% -4.8%

Poland 4.7% 3.1%

Spain 4.8% 5.7%

The UK 6.1% 7.4%

Source: IHS World Markets Healthcare Forecasts

Most European countries saw significant changes in the composition of private healthcare expenditure

over 2010-14 indicating increased financial burden on patients

Figure 2 illustrates the trajectory of private healthcare spending over 2010-14 in nominal terms, including

its composition by different funding sources.

FIGURE 2 PRIVATE HEALTHCARE EXPENDITURE, 2010-14, BILLIONS OF LCU

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain United Kingdom

N.B. The contribution of “private insurance” was removed from the graph for the Netherlands on the basis that the majority of spending in the voluntary health

insurance sector can be attributed to services such as plastic surgery or sports medicine, services which do not strictly qualify as healthcare-related for the

purposes of this report. Spending on such services may be captured in the “private insurance” contribution in other countries, thus challenging a completely like-

for-like comparison. However, due to the contribution of private insurance toward genuine healthcare-related items in these other countries, combined with

absence of data on the precise composition of this contribution, the private insurance indicator was otherwise retained, with the exception of the Netherlands.

Changes in the composition of private healthcare expenditure have been driven by trends unique to each

country:

France: The bulk of private spending is attributable to complementary insurance subscribed to by the

overwhelming majority of the population in order to offset the OOP costs otherwise required under the

public healthcare system. Due to austerity measures brought in to contain the spiraling healthcare

deficit (see the discussion on pharmaceutical expenditure below), the recessionary period saw a

dramatic increase in OOP payments, rising from 28% of overall private healthcare spending in 2010 to

34% in 2011. By period end, OOP payments accounted for 30% of the total, likely attributable to

government negotiations with the complementary insurance sector which subsequently saw the latter

expand patient coverage and contribute to the ongoing cost-savings drive.ii

Germany: In 2011, Germany’s Federal Cabinet agreed to raise the premiums paid for statutory health

insurance to the pre-crisis level of 15.5% of monthly salary – shouldered between employees and

employers – following a deficit reported by the country’s sick funds in 2010 for the first time in many

years.iii This saw OOP costs increase by a CAGR of 6.6% in nominal terms over 2010-14, rising to

account for 60% of overall private spending by period end, up from 56% in 2010.

The Netherlands: The country saw a significant increase in OOP spending, rising from 76.9% of total

private spending on healthcare to 83.8% in 2014; this trend can be explained by the steady increase in

the annual deductible required under the statutory health insurance package, more than doubling over

the period from 2009 to 2014.iv

Poland: The country made some progress with regards to its historically high levels of OOP spending

over the 2010-14 period, seeing this funding source decrease from 80% of total private expenditure on

health to 76% by period end. Over the same timeframe, growth in the country’s burgeoning market

for private insurance – dominated by employer-sponsored medical subscription packages – was

dramatic, rising to account for 9% of private healthcare expenditure in 2014, up from 4% in 2010.

Spain: Like France, the country saw a dramatic increase in OOP spending associated with

implementation of austerity measures, leading this contribution source to increase from 78% of total

private healthcare expenditure in 2010 to 86% a year later, before declining to 80% by 2014.

The UK: The country saw growth in the proportion of private healthcare spending attributable to the

private insurance market, dominated by employer-sponsored benefits.

What is noteworthy is that with the exception of France and Poland, no country exhibited a pattern of

increasing outlays from private insurance combined with reduced OOP spending, a pattern that would have

been indicative of insurers relieving the financial burden on patients imposed by the decline in public

expenditure. Even in Poland, the reduction in OOP spending had more to do with government reforms (see

discussion below) than growth in the voluntary insurance market. As such, the private insurance sector, as

it is currently structured in most European countries, would seem to have limited capacity to plug gaps in

public outlays on healthcare.

It is worth commenting on the composition of OOP spending in those countries where this funding source

accounts for an above-average share of overall private healthcare expenditure. For instance, while

prescription co-payments and spending on non-reimbursed over-the-counter medicines have historically

accounted for much of the OOP spend in Poland, Table 5 indicates that in Spain, pharmaceuticals have

actually accounted for a declining share of total OOP expenditure.

TABLE 5 PRIVATE SPENDING ON PHARMACEUTICALS IN ABSOLUTE VALUE AND AS A PERCENTAGE OF

TOTAL OUT-OF-POCKET EXPENDITURE IN SPAIN, 2010-2013

2010 2011 2012 2013

Private spending on

pharmaceutical products

(EUR mil)

3,475.40 3,520.11 3,594.27 3,738.84

Percentage of total OOP

spending 13.0% 10.7% 10.3% 10.2%

Source: EAE Business School report v

Changes in the composition of private healthcare expenditure have led to serious debates surrounding

the impact on access and health outcomes

Those countries which saw significant increases in OOP spending over the 2010-14 timeframe also

witnessed the emergence of political resistance or stakeholder concern surrounding the impact on patient

access. Whether due to introduction of new copayments as part of emergency austerity measures, or

increases in contributions to the statutory healthcare system, the rising burden on patients prompted

fears that patients would avoid seeking necessary care or face access restrictions:

In Spain, although in 2012 the Ministry of Health shifted 21 medicines, including many oral oncology

drugs, from the retail to the hospitals sector (accompanied by copayment elimination), there has been

increasing pressure to reduce reliance on this type of austerity measure. In fact, subsequent increases

to copayments for medicines, combined with proposals by the Ministry of Finance to increase user fees

in other parts of the healthcare system, led the Spanish Medical College Association to petition against

further reliance on these austerity measures in mid-2014, on the grounds it would defer patients from

seeking necessary treatment. In December of that year, the Socialist Party of Madrid proposed an

extraordinary budget item to eliminate copayments for vulnerable segments of the population,

including low-income pensioners and the disabled and unemployed without benefits, again over

concerns of the impact on access to care.vi,vii

In the Netherlands, in light of lower-than-anticipated healthcare spending, it has been suggested that

increases in cost-sharing dissuading patients from seeking care may have contributed to this

phenomenon.viii

In Germany, additional patient contributions under the statutory health insurance system have

provoked political debate, with the junior party in the governing coalition, the Social Democratic Party,

pushing for more of this additional payment to be covered by employers.

Even in those countries such as Poland where OOP spending has declined over the 2010-14 period, cost-

containment efforts targeting pharmaceuticals (see discussion below) have led manufacturers in some

cases to withdraw products from the market, with a significant potential impact on patient treatment and

outcomes. Thus, the absence of an increase in OOP burden as depicted in Figure 2 should not be equated

with lack of impact on patient access over this timeframe.

KEY TAKE AWAY

Subdued growth in public healthcare spending, driven by ongoing cost-containment efforts and worsened

by the recession, contributed to an uptick in private healthcare expenditure over the 2010-14 period. While

the composition of such spending differs across European countries, reflecting structural differences in

healthcare systems, many saw a significant increase in the OOP financial burden facing patients,

concentrated on pharmaceuticals in particular. This burden has prompted political debate and broader

stakeholder concern surrounding patient access.

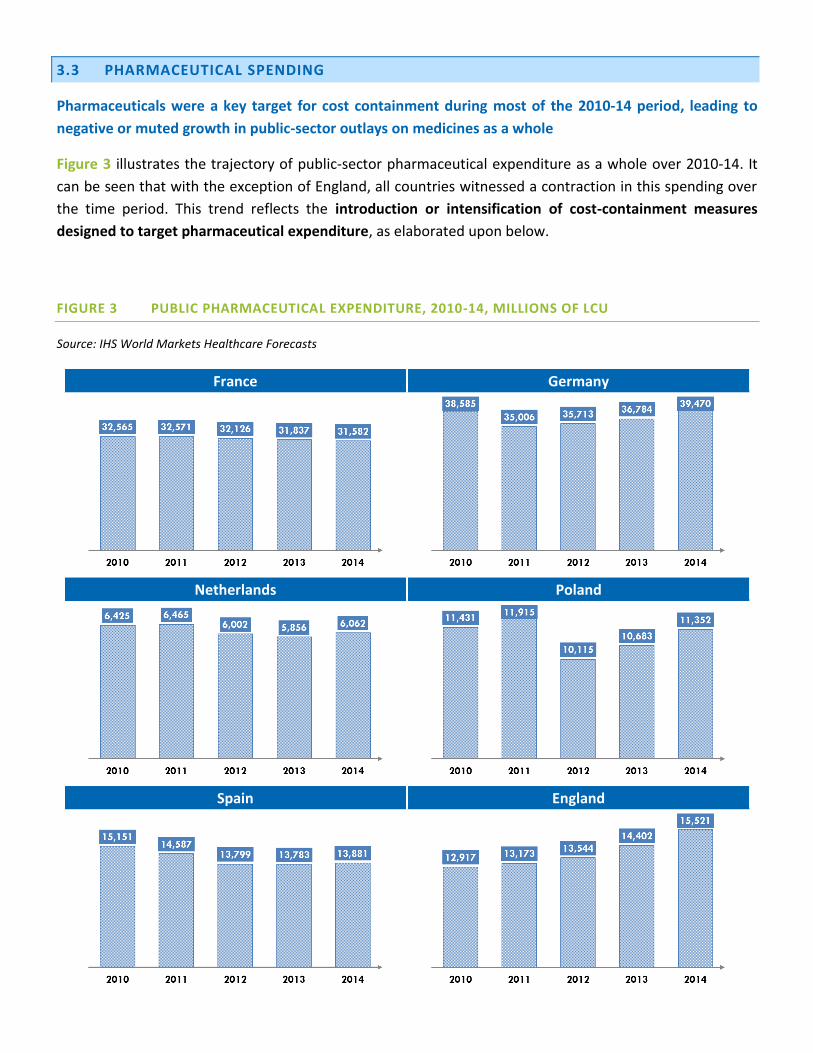

3.3 PHARMACEUTICAL SPENDING

Pharmaceuticals were a key target for cost containment during most of the 2010-14 period, leading to

negative or muted growth in public-sector outlays on medicines as a whole

Figure 3 illustrates the trajectory of public-sector pharmaceutical expenditure as a whole over 2010-14. It

can be seen that with the exception of England, all countries witnessed a contraction in this spending over

the time period. This trend reflects the introduction or intensification of cost-containment measures

designed to target pharmaceutical expenditure, as elaborated upon below.

FIGURE 3 PUBLIC PHARMACEUTICAL EXPENDITURE, 2010-14, MILLIONS OF LCU

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain England

France: Cost-containment policies targeting pharmaceuticals during the recession continued the trend

of bringing in emergency measures to rein in healthcare spending in line with the ONDAM, which

generally saw the government look to achieve savings on the scale of EUR2 billion annually. This

explains the 1-2% y/y contractions seen in the market in nominal terms as displayed in Figure 3. During

the height of the recessionary period between 2010 and 2012, the government delisted and decreased

the reimbursement rates of medicines with lower Service Medical Rendu (SMR) ratings, negotiated

increasingly higher price cuts with pharmaceutical manufacturers, and increased substitution targets

and prescription controls to drive generics penetration.ix

Germany: Cost-containment measures focused heavily on pharmaceuticals, with the 2010 passage into

law of the Pharmaceutical Market Restructuring Act (Arzneimittelmarkt-Neuordnungsgesetz: AMNOG),

which ended the country’s free-pricing regime and introduced central negotiation over

reimbursement rates for innovative drugs. Throughout the recessionary period, and following deficits

reported by the statutory insurance funds for the first time in many years, the mandatory rebate for

medicines not subject to the country’s internal reference pricing system was increased from 6% to 16%,

and a price freeze (initially intended to last for three years but since extended) was introduced for all

reimbursed medicines. Large savings were also made over the period through the use of generic

discount contracts.x These policies help to explain the significant contraction in the market observed

over 2010-11 in Figure 3. The market then went on to recover its losses, driven in part by a reduction in

the mandatory rebate and entry onto the market in 2014 of a record number of innovative new

medicines, including next-generation hepatitis C therapies.xi

The Netherlands: Subdued growth in pharmaceutical expenditure stemmed from a mixture of policy

levers and market dynamics. The slowdown in spending in the community pharmacy sector was

dramatic, a 16% decline in outlays over the period from 2008 to 2013.xii One policy initiative helping to

explain this trend involved the shifting of expensive therapies from the outpatient sector to hospital

budgets, thereby reliving the basic health insurance providers of this expenditure. On top of routine

use of international reference pricing, it has been suggested that a focus on generics – aided by

preferential prescribing policies implemented by insurers – also contributed to this phenomenon.xiii

Meanwhile, the health minister entered into a coalition agreement limiting public hospital spending to

2.5% y/y over 2012-15, putting pressure on hospital drug budgets. Between 2013 and 2014, the market

showed positive growth of 4% in nominal terms, most likely attributable, as in Germany, to market

entry of expensive new medicines.

Poland: Trends in pharmaceutical expenditure must be viewed through the lens of the country’s

Reimbursement Act of 2012, a watershed year for reform of the pricing and reimbursement system.

This far-reaching piece of legislation aimed to expand access to innovative medicines while also seeking

cost savings allowing the government to meet this objective, with pharmaceutical reimbursement

spending not to exceed 17% of total public healthcare expenditure. Savings over the period relied on a

reduction in and broadening of reference pricing groups, and ongoing rounds of price negotiations with

manufacturers, with the government reportedly calling for high double-digit cuts.xiv This explains the

22% y/y contraction in the community pharmacy market in 2012, which led to a 15% contraction in

the public pharmaceutical market overall.

Spain: As in France, austerity measures targeting pharmaceuticals were brought in to curb costs during

the recessionary period, leading to y/y contractions of 3-5% at the level of the overall public

pharmaceutical market. As part of the Heath Pact entered into between the central government and

the autonomous communities, starting in 2010, reforms to the internal reference-pricing system,

generic price cuts and reimbursement limits on on-patent medicines with no generic competitors were

implemented, designed to save EUR1.5 billion.xv Mandatory discounts were introduced for innovative

medicines, price cuts were negotiated, and prescribing by active ingredient encouraged. In 2012, the

government significantly increased pharmaceutical copayments and withdrew over 400 drugs from the

reimbursement list.xvi Subsequent emergency measures, involving copayments on hospital drugs for

outpatients and a EUR1 charge on all prescriptions, saw the government backtrack following legal

challenges and resistance from the autonomous communities.xvii

England: Set against the backdrop of subdued or negative growth in public pharmaceutical expenditure

in the other countries under analysis, England is noteworthy for the upward trajectory it has shown in

such spending over the 2010-14 period, growing initially at 2-3% y/y before rising to 6-8% y/y. In

theory the country possesses a free-pricing regime, which helps to explain this trend, although in

practice most manufacturers participate in the Pharmaceutical Price Regulation Scheme (PPRS) which

imposes pricing restrictions, and price concessions offered as part of patient access schemes are a

common occurrence. The stronger growth is also a reflection of the relative lack of cost-containment

policies targeting pharmaceuticals under the NHS’ GBP20 billion cost savings drive.

The subdued growth in public-sector reimbursement spending on pharmaceuticals over the retrospective

period gave rise to concerns over patient access to treatments and the potential impact on health

outcomes

France: Debate over the impact of austerity measures targeting pharmaceuticals centered on the

ability of the complementary insurance sector to absorb additional copayments without passing

costs onto patients. Non-profit mutual insurers announced a 5% jump in their contributions directly

linked to 2010 reforms involving reimbursement cuts and daily hospital fee increases.xviii Mutualité

Française, the umbrella organisation for France's complementary insurance sector, stated that many

insurers would refuse to cover the cost of drugs subject to the new lowest reimbursement rate.

Subsequent reimbursement cuts on drugs with intermediate SMR ratings prompted insurers to

consider re-evaluating “blind” reimbursement of medicines, with calls for more selective coverage.xix

The data in Figure 2 indicate that the private insurance sector has since absorbed a significant share of

costs, but OOP payments borne by patients remain higher than at the start of the 2010 period.

Germany: The amount that patients covered by statutory health insurance made in additional

payments to make up the difference between reference prices and the actual prices of medicines

reportedly increased by 22% y/y in 2014, amounting to EUR115 million.xx The increase in the

proportion of medicines requiring additional payments rose from 4.1% of reimbursed medicines in

2013 to 6.1% during 2014. It was reported that a significant number of manufacturers opted not to

lower their prices to the level of the government’s reference prices given the ongoing cost-containment

drive. The discount contracting system, responsible for significant savings, meanwhile gave rise to

increasing reports of supply shortages impacting patient access to generic medicines.xxi

The Netherlands: As highlighted above, in light of the lower-than-anticipated outlays on community

pharmacy, it has been suggested that increases in cost-sharing may have potentially dissuaded

patients from seeking care. Over the period from 2008 to 2013, pharmacy expenditure for the

population aged 65 and over decreased by 9%, significantly above other segments of the population,

despite the expectation that expenditure on medicines might be higher in this group.xxii

Poland: Although the Reimbursement Act lowered patient copayments for medicines, continued

rounds of price negotiations have reportedly led producers to withdraw medicines from the

reimbursement system, compelling patients to pay their full cost.xxiii Where manufacturers have

agreed to the price cuts, this has reportedly contributed to large-scale parallel export, leading to

problems with medicine supply shortages.xxiv As a result, there are serious concerns regarding the

impact of the reforms on patient access to medicines as well as the consequent risk posed to health

outcomes.

Spain: As described above, continued expansion of copayments for medicines ultimately led the

government to backtrack or propose supplementary aid for the most vulnerable segments of the

population due to concerns over the impact on access and outcomes. It was reported that almost one

quarter of the drugs removed from the reimbursement list during 2012 either experienced price

increases or were withdrawn entirely from the country.xxv The cumulative impact led innovative

medicines to account for a steadily smaller share of public spending on pharmaceuticals in the retail

sector.xxvi

England: Despite continued growth in public pharmaceutical expenditure, the country continues to lag

behind some of its peers with regards to access. A report issued by Cancer Research UK in August 2015

highlighted the shortfall in molecular diagnostic testing associated with targeted therapies for solid

tumours.xxvii Based on cancer incidence data and extrapolation of testing rates from a survey of labs,

the charity estimates that in 2014, 15,929 patients missed out on molecular diagnostic testing, due

either to lack of funding or awareness. Based on mutation rates, this translates into an estimated 3,552

patients who may have otherwise been eligible for targeted therapies. These access challenges can be

compared to the system in France, for example, where a national network has led to comprehensive

biomarker testing.

The composition of public pharmaceutical expenditure in the retail sector has remained broadly

consistent over the 2010-14 period

Figure 4 illustrates the share of the public retail pharmaceutical market attributed to select therapeutic

classes over time for the years for which data are available in each country. It can be seen that

cardiovascular, alimentary tract and metabolism, and nervous system drugs (Anatomical Therapeutic

Chemical (ATC) classes C, A and N, respectively) accounted for the largest shares of such spending across

most countries.

FIGURE 4 PUBLIC RETAIL PHARMACEUTICAL EXPENDITURE BY THERAPEUTIC AREA, 2010-14

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain United Kingdom

The genericiation of a significant number of primary-care blockbuster medicines coincided with the

period under analysis – a phenomenon referred to as the “patent cliff” – helping governments to hold

down costs and contributing to the subdued growth seen in the public market for pharmaceuticals as a

whole.

ATC classes accounting for the largest shares of retail spending – namely, ATC classes A and C – benefited

more than most from the associated genericization and hence cost savings in the community pharmacy

budget.

A number of countries have reported increases in spending in the outpatient setting on categories of

medicines such as oncology which have traditionally functioned as key drivers of inpatient hospital costs.xxviii

However, it can be seen in Figure 4 that oncology accounted for only a small minority of the total public

retail market over 2010-14, staying stable over this period across countries.

Growth in public spending on hospital medicines has varied across countries, with the portion

attributable to oncology broadly comparable

Figure 5 illustrates the trajectory of public spending on hospital medicines over 2010-14. In contrast to the

negative or muted growth in public-sector outlays on medicines as a whole, it can be seen that spending in

this segment of the market varied markedly by country.

While Germany witnessed y/y contractions on the scale of 1-2%, the remaining countries saw positive

growth. That growth ranged from the 1-3% y/y observed in France and Spain to the 11-13% seen in the

Netherlands and the consistent 15% seen in England. These dramatically different trajectories in spending

can be attributed to very different policy landscapes and frameworks for cost containment as elaborated

upon above.

FIGURE 5 PUBLIC HOSPITAL PHARMACEUTICAL EXPENDITURE, 2010-14, MILLIONS OF LCU

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain United Kingdom

Of the countries which saw public outlays on hospital pharmaceuticals increase significantly, there are

varied reasons for this phenomenon, which in general diverges from the trend of the overall market

identified in Figure 3:

In Poland, nominal growth in spending ranging from 6-9% y/y can be attributed to the Reimbursement

Act which, at the same time that it sought substantial cost savings, also sought to channel some of the

liberated funds into enhanced access to innovative medicines, in particular in secondary care

In England, nominal growth of 15% y/y can be attributed to the introduction of new medicines and

increased use of specialist therapies despite the commercial concessions made as part of patient

access schemes. Notably, oncology’s share of total hospital drug expenditure appears to have declined

even over a period where the Cancer Drugs Fund (CDF) overran its budget, suggesting there have been

cost offsets in baseline commissioning of cancer therapies

In the Netherlands, the nominal growth of 10-13% y/y has been corrected for the shifting of expensive

therapies from the outpatient sector to hospital budgets over this period, indicating this phenomenon

represents genuine spikes in expenditure in sharp contrast to the trend in community pharmacy

Figure 5 also illustrates the share of public spending on hospital medicines attributable to oncology in

particular where these data are available. It can be seen that this share is broadly comparable across

countries, ranging from 20-27%. The higher and steadily increasing share in the Netherlands reflects the

addition of outpatient oncology medicines to the hospital budget as described above.

In those countries where routine estimates of public hospital drug spending by therapeutic area are

available, oncology accounts for the largest single category of spending by a fair margin. Figure 6 illustrates

the distribution of public reimbursement spending on hospital medicines across therapeutic areas in France

and Germany.

FIGURE 6 PUBLIC HOSPITAL PHARMACEUTICAL EXPENDITURE BY THERAPY AREA, FRANCE &

GERMANY

Source: l’Agence nationale de securite du medicament et des produits de santé; Bundesverband der Pharmazeutischen Industriexxix

France (2013)

Germany (2014)

KEY TAKE AWAY

Public reimbursement spending on pharmaceuticals saw negative or muted growth over most of the 2010-

14 period, reflecting the targeting of this sector for cost-containment efforts as well as the impact of the

“patent cliff” which helped governments hold down costs in community pharmacy. Trends in

reimbursement spending on pharmaceuticals in the hospital sector varied more markedly, but the share

attributable to oncology was broadly comparable.

The targeting of pharmaceuticals for cost containment gave rise to concerns over patient access to

treatments and the potential impact on health outcomes, key learnings applicable to ongoing and future

cost-containment efforts.

3.4 CATEGORIES OF CARE SPENDING

Over 2010-14, the composition of public healthcare expenditure across categories of care has remained

broadly consistent

Figure 7 illustrates the distribution of total public healthcare expenditure across discrete categories of care

for the years for which data were available.

FIGURE 7 PUBLIC HEALTHCARE EXPENDITURE BY CATEORIES OF CARE, 2010-14

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain England

The data should be interpreted with caution, as governments classify categories of care differently.

However, within each country, it can be seen that the composition of public healthcare spending has

remained essentially constant over the retrospective period. This consistency might be expected given the

short timeframe relative to the timescales necessary to see significant shifts in care delivery and

organisation.

Inpatient services continue to account for the largest portion of expenditure

The share of spending accounted for by inpatient services has remained largely stable, despite countries

pursuing reforms seeking operational efficiency savings in this sector. Rationalization of hospital costs

formed a key part of France’s austerity measures during the recession for example, with 50% of the EUR2.4

billion in savings in 2011 expected to come from this sector.

In England, hospital efficiencies played a key role in the GBP20 billion in savings required of the NHS by

2015. In an independent review by Lord Carter of Coles for the Department of Health (the “Carter review”),

unwarranted variation in resource utilization by NHS hospitals is estimated to cost the system an

additional GBP5 billion out of the GBP55.6 billion spent annually.xxx

The fact that inpatient hospital costs as a share of total public healthcare expenditure have remained flat,

or decreased only very marginally as in the Netherlands and Spain, suggests that the inpatient segment of

care – which continues to account for the bulk of healthcare spending by some margin – should be a key

target for cost containment.

Medicines account for a comparatively smaller share of overall public healthcare expenditure

In contrast, pharmaceuticals (either alone or in combination with other nondurable medical goods,

depending on how data are reported) account for a comparatively smaller share of overall public healthcare

spending. It can be seen in Figure 7 that this share has decreased over 2010-14 in nearly all of the

countries under analysis, generally falling by two-to-four percentage points.

KEY TAKE AWAY

Although most European countries have sought to shift care out of hospital and into the home or

community setting, the inpatient segment continues to dominate the bulk of care expenditure.

Pharmaceuticals were a key target for cost-containment efforts over the 2010-14 period, but represent a

comparatively smaller share of healthcare spending. Going forward, inpatient care presents a significant

opportunity to realise cost savings.

3.5 DISTRIBUTION OF DIRECT CANCER CARE COSTS

Inpatient services represent the bulk of direct cancer care costs across European countries

Data on overall cancer care costs and its distribution across discrete categories of care are not consistently

gathered across European countries, and the figures which do exist do not adhere to a standardised

framework. As such, it is difficult to make precise like-for-like comparisons among the national-level data

sets that do exist. With these caveats in mind, the data illustrated in Figure 8 and Figure 9 provide general

insights into the scale and structure of cancer care spending and whether, at a broad level, there are

similarities across countries.

FIGURE 8 DISTRIBUTION OF DIRECT CANCER CARE COSTS I

France Germany (2009)

Source: Institut National du Cancer

xxxi

Source: Luengo-Fernandez R et al. (2013)xxxii

Netherlands Poland (2011)

Source: Cost of illness tool, Volksgezondheidenzorg

xxxiii

Source: NFZ, 2014xxxiv

FIGURE 9 DISTRIBUTION OF DIRECT CANCER CARE COSTS II

Spain (2011) England (2009)

Source: Sociedad Española de Oncología Médica, 2013

xxxv

Source: London Cancer New Drugs Group, 2014xxxvi

Allowing for the inevitable differences in how items are assigned to care categories, it can be seen that

patterns of direct cancer care expenditure are broadly similar across countries. Inpatient hospital costs

have accounted for the largest share of direct cancer care costs.

In Germany, the Netherlands and Spain, figures for inpatient care, hospital and specialist care, and

hospital admissions are reported respectively. In Germany and Spain, this care accounted for 66% and

62% of direct cancer care costs in 2009 and 2011, respectively, while in the Netherlands, it increased

from 65.3% in 2003 to 72.6% in 2011. The higher share in the Netherlands may be attributable to the

inclusion of certain specialist care costs which are not captured in this category in the other countries.

A like-for-like comparison with the remaining countries is difficult as they split out costs on other items

such as surgery and radiotherapy, some of which will be attributable to the inpatient setting and some

of which pertain to procedures conducted on an outpatient basis. In terms of radiotherapy, France and

Poland reported a larger share of total costs attributable to this category, at 12% and 18.9%,

respectively, in comparison to Spain and England, both at 5%.

In comparison to the proportion of spending allocated to inpatient care, direct cancer care costs in the

ambulatory sector are limited. Primary care costs are split out in Germany and the Netherlands, where

they accounted for a similar 2% and 5% of expenditure respectively. Outpatient spending, presumed to

capture all ambulatory care distinct from that in the primary care sector, accounted for a similar 11% in

Germany and 8% in England. Spending on palliative care, reported in France and England, accounted for

approximately 5% of costs in both cases.

Pharmaceuticals make up a smaller share of direct cancer care costs

For those countries which split out chemotherapy costs from other spending categories, it can be seen that

this item accounted for a broadly similar share, ranging from 26% in Spain to 32% in France and 35.6% in

Poland. Drug costs as a whole were reported in Germany and England, both at 18%. Caution should be

taken when comparing chemotherapy and drug costs in particular, as it is not always apparent how

acquisition costs versus preparation and administration costs are allocated. Another caveat is that the

Spanish data do not include onco-haematological drugs.

KEY TAKE AWAY

Inpatient services account for the lion’s share of direct cancer care costs and largely overshadow the

expenditure incurred by oncology drugs. There is an argument for the continued cost-containment drive

to focus on improving efficiency savings in non-drug spending categories, particularly to accommodate the

future generation of pipeline medicines that are anticipated to require administration in the hospital

setting, even if on an outpatient basis.

IV. FUTURE TRENDS ANALYSIS

7.1 FORECAST PUBLIC HEALTHCARE SPENDING

Over 2015-20, growth in public healthcare expenditure is expected to remain negative or subdued in real

terms

Figure 10 illustrates the forecast for topline healthcare expenditures from 2015 to 2020.

FIGURE 10 FORECAST TOTAL HEALTHCARE EXPENDITURE, 2015-20, BILLIONS OF LCU

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain United Kingdom

Table 6 indicates the projected CAGRs of public healthcare expenditure in real terms, which should be

viewed in combination with the forecast for y/y growth in GDP as displayed in Table 7. In most countries,

the projected growth rates in public healthcare expenditure translate into an improvement relative to the

2010-14 period.

The improvement is forecast to be greatest in France, the UK and Germany, a reflection of stronger

forecast economic growth predicted to lift public outlays on healthcare, although as elaborated upon

below, specific cost-containment targets place limits on spending.

In comparison, the Netherlands and Poland are expected to see marginal improvements, a reflection of

the above-average CAGRs in public healthcare expenditure seen over 2010-14, when most countries

saw negative real-term CAGRs.

In Spain, real-terms growth in public healthcare expenditure is forecast to be negative, reflecting

comparatively weaker economic growth prospects and the need to contain costs in line with deficit

targets. In nominal terms, public healthcare spending is expected to grow 2-3% y/y, with cost-

containment likely to be derived from pharmaceutical policy, which may be more accentuated if a left-

wing coalition forms the next Spanish government.

TABLE 6 FORECAST COMPOUND ANNUAL GROWTH RATES IN PUBLIC HEALTHCARE EXPENDITURE,

2015-20

Real-terms CAGR Difference relative to 2010-14

France 2.1% 5.7%

Germany -0.9% 2.1%

The Netherlands 1.9% 0.3%

Poland 2.8% 1.1%

Spain -1.3% -0.4%

The UK 2.1% 3.3%

Source: IHS World Markets Healthcare Forecasts

TABLE 7 REAL AND NOMINAL FORECAST YEAR-ON-YEAR GROWTH IN GROSS DOMESTIC PRODUCT,

2015-2020

2015 2016 2017 2018 2019 2020 2014

France Real 1.16% 1.25% 1.39% 1.34% 1.30% 1.44%

Nominal 2.29% 2.39% 2.82% 3.24% 2.97% 3.22%

Germany Real 1.45% 1.85% 2.02% 1.72% 1.51% 1.67%

Nominal 3.53% 3.73% 3.78% 3.33% 3.04% 3.14%

Netherlands Real 1.99% 1.36% 1.97% 1.77% 1.79% 1.81%

Nominal 2.38% 3.27% 4.12% 3.58% 4.17% 3.91%

Poland Real 3.61% 3.75% 3.26% 3.24% 2.97% 2.96%

Nominal 4.13% 4.65% 5.40% 5.40% 5.22% 5.21%

Spain Real 3.21% 2.73% 2.37% 2.27% 2.12% 2.03%

Nominal 3.84% 3.60% 3.70% 3.89% 3.77% 3.68%

The UK Real 2.33% 1.92% 2.48% 2.37% 2.29% 2.30%

Nominal 2.61% 2.57% 4.22% 4.66% 4.48% 4.38%

Source: IHS Global Economic Data

Cost-containment targets and the need to carefully manage expenditure versus other priorities are

forecast to continue to weigh on healthcare outlays

In absolute terms, forecast growth rates remain subdued, and even in Germany, despite the improvement

relative to the 2010-14 period, growth is forecast to be negative in real terms. On a country by country

basis, the reasons for the continued plateau in public healthcare spending are varied:

France: Given the persisting challenge of tackling social security deficits, the country’s ONDAM has

been revised downwards, set to 1.75% for 2016. xxxvii This reduces spending growth to an historic low.

The country’s stability programme envisions an ambitious target of EUR50 billion in savings by 2017.

Marisol Touraine, the French health minister, announced a series of cost-containment measures in the

social security financing act for 2016, including promotion of generics, reductions in medicines prices

and efficiencies in hospital spending.

Germany: With a significant share of public hospitals in Germany recording deficits, in 2015 the country

passed a law intended to reduce overcapacity as well as unnecessary operations in secondary

care.xxxviii It has been predicted that the law will result in additional spending of up to EUR5.4 billion by

2020, although this includes setting up systems and collaborative networks that will enable a

streamlining of operations, so its ultimate goal will be one of cost containment. Combined with the

major focus on cost containment in pharmaceutical expenditure, this drive means Germany is one of

two countries alongside Spain predicted to see a negative CAGR in total public healthcare spending

over 2015-20.

The Netherlands: Government finances are improving given past fiscal consolidation efforts, and the

Rutte government has agreed an austerity package spanning 2014-17 in a bid to reach a structurally

balanced budget by 2017. Although there are specific cost-containment efforts centered on the

country’s expensive system for long-term care, the main approach for the broader healthcare system

relies on promoting market forces and efficiency improvements.xxxix A controversial proposal from the

government to allow insurers to restrict choice of providers to only the most efficient (free choice

would have been associated with a higher premium) has since been altered to offer patients who select

preferred providers discounts on their premiums after originally being rejected by the Senate.xl The

latest proposal is envisaged to generate savings of about EUR1 billion, in the absence of which it will be

difficult to make further progress controlling health spending prior to the government’s term ending in

2017.

Poland: While the dynamism of the economy in the early 2000s enabled the government to support

the country through the recession impacting the rest of Europe, concerns about the scale of debt have

since weighed on public spending. At the same time, with the recent election of the Law and Justice

(Prawo i Sprawiedliwość) party, the new government intends to increase the share of GDP spent on

public healthcare from just over 4% to 6%. However, set against a number of other expensive

campaign pledges, including bringing the retirement age back to its previous level and providing a

statutory monthly sum for families with two or more children, this ambition will only be realised with

significant cost savings achieved in other areas.

Spain: The future direction of healthcare will hinge on resolution of the continued political uncertainty

stemming from the indecisive December 2015 national election, as well as whether any of the tax cuts

(with the potential to increase the deficit) unveiled during the election year are reversed. The Socialists

pledged during the election campaign to petition the European Commission to relax deficit targets set

for Spain, which has been in the corrective arm of the Stability and Growth Pact since April 2009.

However, the next government is expected to make significant healthcare budget adjustments,

particularly pertaining to greater management of drug spending as recommended by the European

Commission, in order to meet deficit objectives.

England: The political agenda to improve the country’s standing relative to average European spending

on healthcare places limits on the degree of cost containment going forward. Nonetheless, the English

NHS faces serious budgetary challenges, with the anticipation that the funding gap will reach GBP30

billion in 2020, assuming funding rises in line with inflation and no efficacy savings are made.xli The

government therefore expects the NHS to make efficiency savings of some GBP22 billion by this time.

These savings are expected to be realised through measures such as better staff roster management,

procurement efficiencies, reduced unnecessary hospital admissions, and improved stock management

of medicines.xlii

KEY TAKE AWAY

The forecast trend for continued subdued or negative real-terms growth in public outlays on healthcare is a

reflection of diminished economic growth prospects across the developed world, combined with the

persistence of structural economic issues which were not resolved by austerity measures during the crisis.

A full decade of subdued growth – a phenomenon already apparent in some countries even before the

financial crisis – raises important questions over the potential impact on outcomes if pharmaceuticals

remain a key target for cost containment at a time when healthcare demands are increasing due to

ageing populations, and patients have already seen significant increases in OOP spending.

7.2 FORECAST PRIVATE HEALTHCARE SPENDING

Over 2015-20, rates of growth of private healthcare expenditures are once again predicted to exceed

those of public outlays

Figure 11 illustrates the forecast for private healthcare expenditures from 2015 to 2020.

FIGURE 11 FORECAST PRIVATE HEALTHCARE EXPENDITURE, 2015-20, BILLIONS OF LCU

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain United Kingdom

The marginal improvements in the forecast rates of growth in public outlays on healthcare mean that as in

the retrospective period, private spending will be required to offset likely shortfalls in public-sector ability

to cater to rising healthcare demand.

However, as captured in Table 8, the difference between the projected rates of growth of the private

market and public outlays are forecast to be weaker compared to the retrospective period (reflecting in

part the marginal improvements in public spending itself), raising questions over the extent to which the

private market will be able to absorb healthcare demand if public resources prove inadequate.

TABLE 8 FORECAST COMPOUND ANNUAL GROWTH RATES IN PRIVATE HEALTHCARE EXPENDITURE,

2015-20

Real Difference relative to public outlays

France 2.4% 0.3%

Germany 1.6% 2.5%

The Netherlands 1.9% 0%

Poland 5.5% 2.7%

Spain 3.2% 4.5%

The UK 3.9% 1.8%

Source: IHS World Markets Healthcare Forecasts

The period over 2015-20 is predicted to see changes in the composition of the private market in a number

of European countries, in particular leading to greater OOP burdens for patients

France: France’s system for national health expenditure targets is intended to achieve savings without

compromising quality of care or shifting significant additional cost burden onto patients. While reports

have been put forward considering reforms to the country’s system for reimbursement of chronic

diseases (known as Affection de Longue Dureé: ALD) as well as the general three-tier system of

reimbursement rates for medicines, in reality the political system is not perceived to be favourable to

such sweeping changes. xliii Furthermore, the complementary insurance sector has already absorbed

costs (as highlighted in Figure 2 above) and it is unclear what additional costs this sector can absorb

before they are passed on to patients in the form of increased cost-sharing. As such, unlike some of the

other countries under analysis, the composition of the private market is expected to remain broadly

stable in France.

Germany: Since the beginning of 2015, the “additional” contribution (Zusatzbeitrag) to the statutory

insurance system for which employees are liable (traditionally 0.9% of pre-tax salary) can be freely set

by funds within defined limits. Although the average additional contribution rate was expected to rise

to 1.1% by 2016, it was reported early that year that 25 funds were charging more than this rate.xliv This

increase in cost sharing, coupled with the trend for rising payments on pharmaceuticals priced above

the reference reimbursement rate (see discussion on trends in pharmaceutical expenditure above), is

forecast to see OOP spending account for a growing share of private market expenditure, and growth

of the latter at a higher rate relative to public outlays.

The Netherlands: OOP payments are projected to account for a rising share of the private

marketplace, increasing from 85.7% in 2015 to 92.1% in 2020. This trajectory reflects trends in cost

sharing under the Dutch statutory health insurance system which, as discussed above, saw the annual

deductible more than double over the period from 2008 to 2014 to reach EUR375 in 2015. In 2016, this

deductible increased by EUR10, and premiums were expected to increase by EUR7 to an average of

EUR103 per month owing to higher healthcare costs. Going forward, the government is anticipated to

be more wary of enabling insurers to continue to pass rising costs on to patients.

Poland: Private insurance is set to rise from representing 9% of total private healthcare spending in

2014 to accounting for 29.3% in 2020, representing a nominal-term CAGR of 30.1%. In tandem, OOP

payments are forecast to fall from representing 75.4% of the private market in 2014 to 69.7% in 2020,

indicating that the rising contribution from the private insurance sector is not associated with a

significant offset of the comparatively high OOP spending patterns. Rather, the category of total

“other” private spending (including spending, for example, by charities and other institutions not

otherwise captured) is set to see a dramatic decline at a CAGR of 38.1% through 2020. These trends

reflect a maturation of the market as more employers are projected to offer medical subscription

packages in the country’s bourgeoning voluntary insurance sector.

Spain: OOP payments are forecast to account for an increasing share of private healthcare spending,

rising from 38.2% in 2015 to 52.4% in 2020, and helping drive growth of the overall private market. This

trend reflects increasing cost shifting to patients under measures to combat the budget deficit, but

also the relatively stronger contribution of private sources toward overall healthcare spending in Spain.

With specialists' fees generally more affordable than in other European countries, a significant

proportion of citizens seek private healthcare. This is true not only of affluent classes in urban areas,

but is also relatively common in rural areas where private specialists are often seen as a priority for

children and the elderly.xlv There are signs of renewed uptake of private health insurance as

dissatisfaction with constrained public services increases amongst citizens who can afford to pay

premiums, and autonomous communities that reduced public healthcare spending in 2012 and 2013

saw a rise of market share in private health insurance, a trend that is likely to continue.xlvi However, this

will be set against fewer workers being covered by employer-sponsored policies and a still limited

culture of opting for individual private coverage.

The UK: The private market is expected to remain relatively stable in terms of composition. The

broad-based political consensus around universal access to care limits scope for greater user fees, and

individual purchases of private medical insurance have been shown to be unresponsive to tax relief

(leading the Labour government in England to abolish the subsidy in 1997), meaning that the market

for private healthcare remains largely reliant on trends in employer-sponsored insurance.xlvii

KEY TAKE AWAY

Subdued growth in public healthcare spending over 2010-14 contributed to an uptick in private healthcare

expenditure, a trend which is forecast to continue over the 2015-20 timeframe. However, a number of

European countries saw patients or private insurers absorb significant new costs over 2010-14, posing

potential challenges to their ability to accommodate additional future funding gaps in public healthcare

provision. In other countries, political resistance to increased user fees or private-sector involvement

represents a significant obstacle to the private market absorbing shortfalls in public outlays.

7.3 FORECAST PHARMACEUTICAL SPENDING

Over 2015-20, growth in overall public pharmaceutical spending is forecast to pick up pace relative to the

2010-14 period in most countries

Even before the close of the 2010-14 period, a number of European countries saw an uptick in

pharmaceutical expenditure, driven in part by entry onto the market of an above-average number of high-

cost innovative therapies, notably next-generation hepatitis C treatments. In 2014, 45 new active

substances became available in Germany for instance, the largest number of new innovative medicines for

any one year in history..xlviii

Looking forward to 2020, a large number of new therapies, many offering breakthroughs in treatment in

oncology in particular, are set to enter the market.xlix As in 2013-14, with many treatments with significant

potential budget impact entering the market over the same time period, there will almost certainly be an

uptick in drug reimbursement spending.

Figure 12 illustrates the 2015-20 forecast for public pharmaceutical reimbursement spending based on

projected economic growth and historical relationships between that growth and healthcare expenditure.

These forecasts assume continued economic recovery, leading to upticks in reimbursement spending which

will need to be stretched to accommodate emerging new treatments.

FIGURE 12 FORECAST PUBLIC PHARMACEUTICAL EXPENDITURE, 2015-20, BILLIONS OF LCU

Source: IHS World Markets Healthcare Forecasts

France Germany

Netherlands Poland

Spain England

The change in the forecast rate of growth of public pharmaceutical spending and how it relates to the 2010-

14 trend varies by country:

France: After contracting y/y over most of the 2010-14 period, growth in public pharmaceutical