company report - xueqiudoc.xueqiu.com/150f9735335115a3fe835399.pdf · we believe hyper-growth stage...

TRANSCRIPT

Tuesday, November 10, 2015

Company Report China Merchants Securities (HK) Co., Ltd.

Hong Kong Equity Research

Please see penultimate page for additional important disclosures. China Merchants Securities (CMS) is a foreign broker-dealer unregistered in the USA. CMS research is prepared by research analysts who are not registered in the USA. CMS research is distributed in the USA pursuant to Rule 15a-6 of the Securities Exchange Act of 1934 solely by Rosenblatt Securities, an SEC registered and FINRA-member broker-dealer. 1

Sky Light (3882 HK) Dual imaging growth engines after GoPro. Initiate at BUY ■ Strong imaging design expertise to win orders from tech innovators

(Netgear/Canary/iON), after being GoPro’s major supplier for 10+ years

■ GoPro’s continued mainstream demand in APAC/ EMEA, and new orders

from IP camera/car camcorder to drive 24% FY15E-17E EPS CAGR

■ Initiate BUY with TP of HK$3.36 (46% upside), based on undemanding

valuation of 8.0x FY16E P/E given 30% ROE and 9% dividend yield

GoPro expectation reset to stable growth We believe hyper-growth stage of action camera market has passed (50% FY12-

14 shipment CAGR) and the market is resetting expectation on GoPro (CMS est.

17% FY15E-17E shipment CAGR). As the sole manufacturer of GoPro consumer

grade cameras since 2005, we expect Sky Light to benefit from GoPro’s

accelerating mass market penetration (> 50% of 9M15 shipments are consumer

grade models). We estimate Sky Light’s action camera shipment/revenue to grow

at 16%/12% CAGR during FY15E-17E and our sensitivity test suggested 6%

downside to our conservative FY16E EPS estimate if GoPro makes a mere

7%YoY shipment growth (vs. our base case of +19%YoY).

Dual growth engines in FY16E: Smart home, specialty camera With continued R&D investment and leading-edge imaging technology, Sky

Light’s recent order wins in IP cameras (Netgear/Canary/iON), car camcorders

(Chinese internet), police cameras (US) emerge as new growth engines, in our

view. We expect home imaging and digital imaging revenue to grow at 35%/37%

CAGR during FY15E-17E, and we believe the newly set-up Xian R&D center

focusing on 4K/LTE/cloud/image analysis as well as the US subsidiary will

strengthen product development and accelerate overseas expansion.

Trading at deep discount but with high ROE and div. yield Trading at 5.5x FY16E P/E, 35% discount to its peers, Sky Light is undervalued

considering its 30% ROE and 9% dividend yield. We initiate coverage on Sky

Light with BUY rating and TP of HK$3.36 (46% upside), based on 8.0x FY16E

P/E, 6% discount to HK-listed camera component makers. We believe market

concerns on GoPro slowdown is overdone, given Sky Light unjustified valuation

after 39% share price correction from peak in Aug. Near-term catalysts include 3

new products (Netgear new IP cam/car camcorder/police cam) launch in Dec.

Financials

HK$mn 2013 2014 2015E 2016E 2017E

Revenue 1,623 2,092 2,869 3,433 4,034

Growth (%) -2.2% 29.0% 37.1% 19.7% 17.5%

Net profit 147 202 258 336 398

Growth (%) 20.2% 36.9% 27.9% 30.0% 18.4%

EPS (HK$) N/A N/A 0.37 0.42 0.50

DPS (HK$) N/A N/A 0.18 0.21 0.25

P/E (x) N/A N/A 6.27 5.48 4.63

P/B (x) N/A N/A 1.68 1.63 1.38

ROE (%) 61.0% 92.2% 26.8% 29.7% 29.9%

Source: Company data, CMS (HK) estimates

Marley Ngan Alex Ng

852-31896635

852-3189 6125

Initiation

BUY

Previous

N/A

Price HK$2.30

12-month Target Price (Potential upside)

HK$3.36 (+46%)

Previous N/A

Price Performance

Source: Bigdata

% 1m 6m 12m

3882 HK (22.6) (5.0) (5.0) HSI 1.2 (17.6) (3.5)

China Technology

Hang Seng Index 22727

HSCEI 10506

Key Data

52-week range (HK$) 1.6-3.74

Market cap (HK$ mn) 1,841

Avg. daily volume (mn) 5.38

BVPS (HK$) 1.37

Shareholding Structure Tang Wing Fong Terry 52.8%

Sky Light Employees’ Trust 8.1%

Wu Yongmou 7.9%

No. of shares outstanding (mn) 800 Free float 25.0%

Related Research

1. Sky Light (3882 HK, NR) – More than a GoPro proxy; IP camera taking shape (2 Sep 2015)

-40

-20

0

20

40

60

Jul/15 Oct/15

(%) 3882 HSI Index

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 2

Investment thesis Sky Light and GoPro: resetting expectation to stable growth We believe GoPro’s action camera market hyper-growth stage (50% FY12-14 shipment CAGR) has passed and it is time to reset a more realistic expectation with shipment growth of 17% CAGR during FY15E-17E. We believe GoPro will maintain its leadership in global action camera market with demand shifting from professional grade to consumer grade models solely manufactured by Sky Light, backed by GoPro’s product mix change in 9M15 (consumer grade shipment >50%).

We expect Sky Light to maintain share allocation of 52% given its long-established relationship with GoPro since 2005, imaging expertise and increasing demand for consumer grade products. We estimate Sky Light action camera shipment/revenue to grow at 16%/12% CAGR in FY15E-17E. We believe our estimates are conservative and our sensitivity test suggested 6% downside to our FY16E EPS estimate if GoPro only made a mere 7%YoY shipment growth (vs. CMS base est. +19%YoY).

Smart Home as new growth engine in FY16E (20% of sales) Home surveillance demand is always there, and we believe self-installed, self-monitored IP camera market is booming as network infrastructure (wifi/3G/4G), hardware (IP camera/smartphone) and software (apps for live streaming) are now in place. With strong interests in creating Smart Home ecosystem, global tech companies/ start-up including Google (GOOG US), Xiaomi, Qihoo 360 (QIHU US), Netgear (NTGR US), Canary all released first smart IP camera in 2H14 or this year as an entry point to bolster their foothold in the fast-growing market.

We expect Sky Light’s home imaging revenue/shipment to grow at 35%/33% CAGR during FY15E-17E, contributing 22% of FY17E sales. IP camera shipment first commenced in 3Q14 to Netgear (Arlo) with revenue tripled HoH in 1H15. We are positive on Sky Light’s home imaging outlook given Netgear strong growth, Canary ramp-up and more client wins in overseas market.

From imaging hardware to software: 4K/LTE/image analysis Sky Light is extending its product offering from hardware (camera) to software (apps and online imaging platform) with newly set up Xian R&D center focusing on 4K/LTE/image analysis. We believe imaging will continue to be an important part in IoT market with new technology being applied on specialty cameras. We estimate digital imaging revenue to grow at 37% CAGR during FY15-17E, with China internet company led car camcorder project on the way (Shipment: 4Q15E). Other high-margin specialty cameras including police camera/shooting camera are also taking shape.

High ROE, High dividend, attractive valuation We initiate coverage on Sky Light with BUY rating and TP of HK$3.36 (46% upside), based on 8.0x FY16E P/E, 6% discount to camera component maker 1-yr fwd P/E mean. Our TP also implies 27% discount to Chicony (2385 TT), GoPro OEM supplier focusing on professional grade models. Trading at 5.5x FY16E P/E, 35% discount to its HK-peers 8.5x FY16E P/E, Sky Light’s valuation is attractive considering its higher ROE at 30% (vs. peers 18%) and high dividend yield at 9% (management targets to maintain dividend payout at 50% like 1H15).

Our FY15-17E EPS estimates are lower than consensus by -5-9% as we are more conservative on GoPro shipment outlook. Downside risks include share loss from GoPro, lower than expected demand for IP camera and specialty camera (car camcorder and police camera).

Dual growth engines in FY16E: Smart Home IP cameras (Netgear, Canary) and specialty cameras (car

camcorder / police camera)

GoPro expectation reset, a stable growth is likely. Change in product mix with increasing demand for consumer grade models set to benefit Sky Light

LT outlook: Expanding from hardware cameras to imaging software solutions in 4K/LTE/

image analysis

High ROE, high dividend yield at attractive valuation. Initiate at BUY with TP of

HK$3.36 (46% upside)

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 3

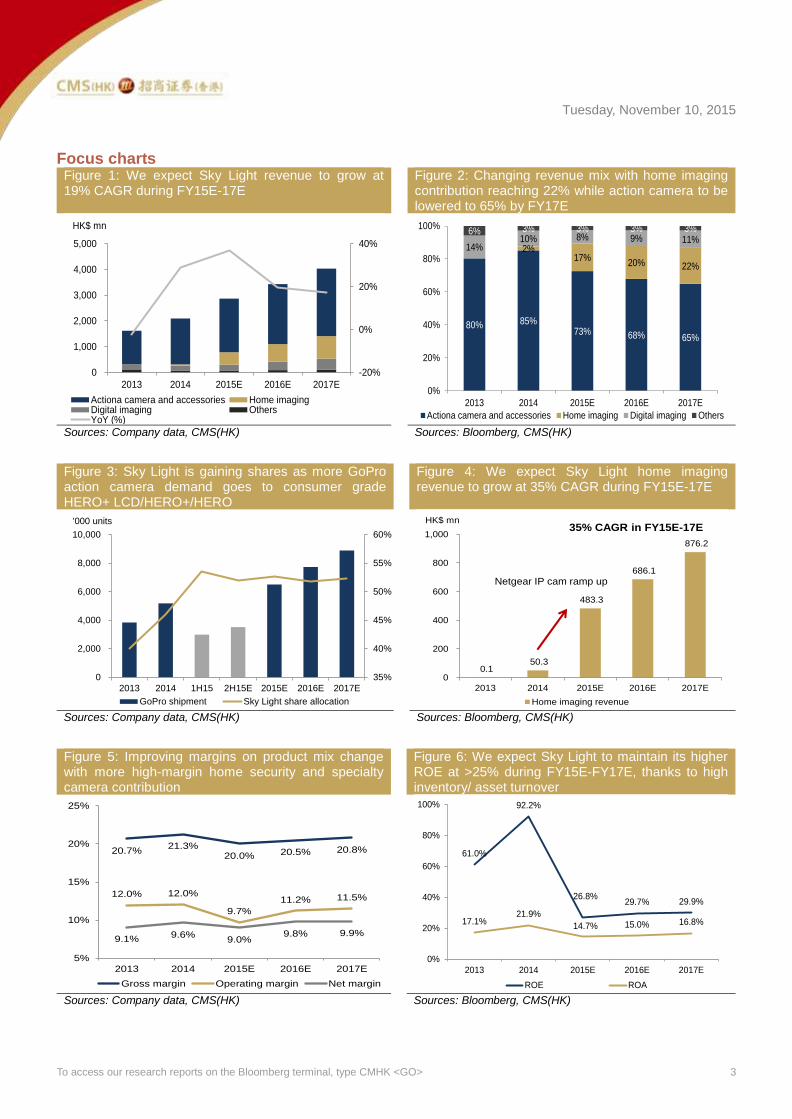

Focus charts Figure 1: We expect Sky Light revenue to grow at 19% CAGR during FY15E-17E

Figure 2: Changing revenue mix with home imaging contribution reaching 22% while action camera to be lowered to 65% by FY17E

Sources: Company data, CMS(HK) Sources: Bloomberg, CMS(HK)

Figure 3: Sky Light is gaining shares as more GoPro action camera demand goes to consumer grade HERO+ LCD/HERO+/HERO

Figure 4: We expect Sky Light home imaging revenue to grow at 35% CAGR during FY15E-17E

Sources: Company data, CMS(HK) Sources: Bloomberg, CMS(HK)

Figure 5: Improving margins on product mix change with more high-margin home security and specialty camera contribution

Figure 6: We expect Sky Light to maintain its higher ROE at >25% during FY15E-FY17E, thanks to high inventory/ asset turnover

Sources: Company data, CMS(HK) Sources: Bloomberg, CMS(HK)

-20%

0%

20%

40%

0

1,000

2,000

3,000

4,000

5,000

2013 2014 2015E 2016E 2017E

Actiona camera and accessories Home imagingDigital imaging OthersYoY (%)

HK$ mn

80% 85%73% 68% 65%

2%17%

20% 22%

14%10% 8% 9% 11%

6% 3% 3% 3% 3%

0%

20%

40%

60%

80%

100%

2013 2014 2015E 2016E 2017E

Actiona camera and accessories Home imaging Digital imaging Others

35%

40%

45%

50%

55%

60%

0

2,000

4,000

6,000

8,000

10,000

2013 2014 1H15 2H15E 2015E 2016E 2017E

GoPro shipment Sky Light share allocation

'000 units

0.1 50.3

483.3

686.1

876.2

0

200

400

600

800

1,000

2013 2014 2015E 2016E 2017E

Home imaging revenue

HK$ mn35% CAGR in FY15E-17E

Netgear IP cam ramp up

20.7%21.3%

20.0% 20.5% 20.8%

12.0% 12.0%

9.7%

11.2% 11.5%

9.1%9.6%

9.0%9.8% 9.9%

5%

10%

15%

20%

25%

2013 2014 2015E 2016E 2017E

Gross margin Operating margin Net margin

61.0%

92.2%

26.8%29.7% 29.9%

17.1%21.9%

14.7% 15.0% 16.8%

0%

20%

40%

60%

80%

100%

2013 2014 2015E 2016E 2017E

ROE ROA

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 4

Contents

Investment thesis ........................................................................................................................................................... 2 1. Sky Light and GoPro: resetting expectation to stable growth on mass market adoption ...................................... 5

Why we think GoPro can maintain its leadership position and where does the demand come from? 5 Why we expect Sky Light to maintain its share allocation? 6

2. Smart home: redefining wireless IP camera as next growth engine in FY16E ...................................................... 7 Why IP camera, supposed to be an “old” product, booming all of a sudden? 7 Why we are positive on Sky Light’s home imaging segment? 8

3. From camera to imaging software solution: 4K/LTE/image analysis ..................................................................... 9 Connected car: car camcorder project with leading China internet company is on the way 9 New Xian R&D center focusing on 4K/LTE/image analysis 9

Financial Analysis ........................................................................................................................................................ 10 Valuation ...................................................................................................................................................................... 12 Appendix 1: Sky Light company profile ....................................................................................................................... 14 Appendix 2: GoPro company profile ............................................................................................................................ 17 Appendix 3: Action camera and IP camera ................................................................................................................. 18 Financial summary ....................................................................................................................................................... 19

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 5

1. Sky Light and GoPro: resetting expectation to stable growth on mass market adoption

We believe GoPro will maintain its leadership in action camera market, but it is time to set a more realistic expectation on demand. Action camera market’s hyper-growth stage has passed, in our view, and we are conservative on GoPro shipment growth estimate at 17% CAGR during FY15E-17E (vs. 50% FY12-14 CAGR), with Sky Light maintaining its share allocation at 52%. We expect Sky Light action camera revenue to grow at 12% CAGR in FY15E-17E.

Why we think GoPro can maintain its leadership position and where does the demand come from?

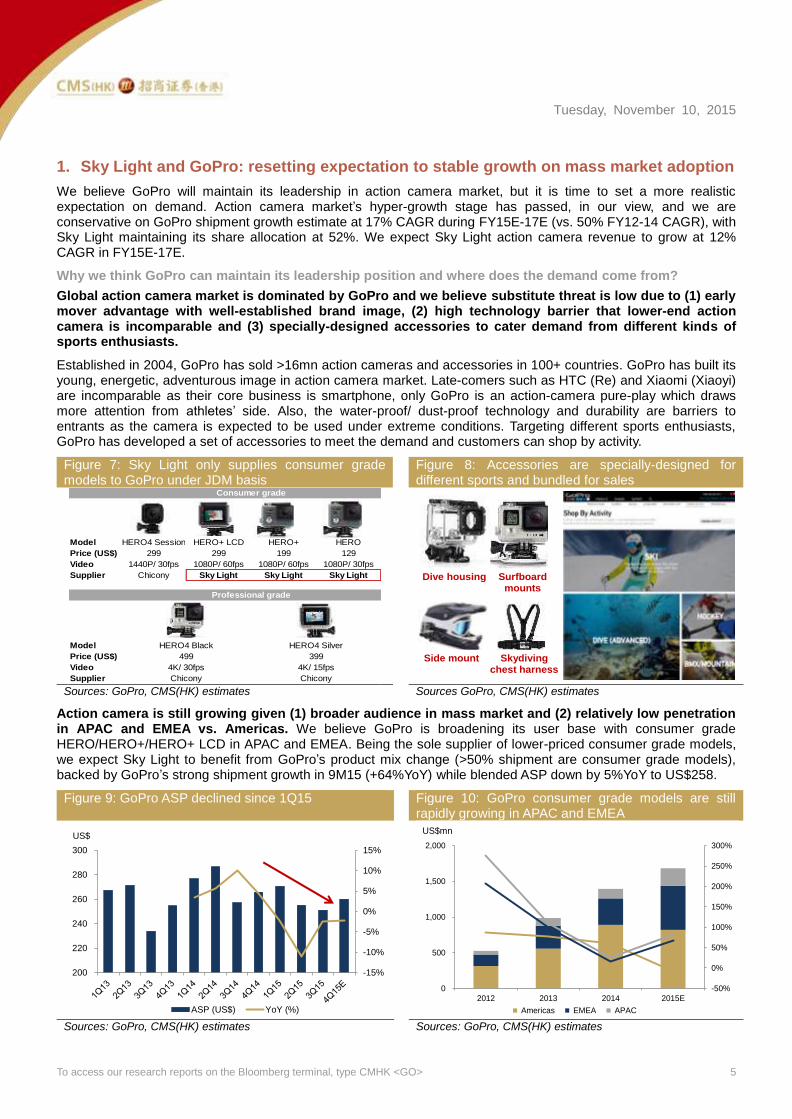

Global action camera market is dominated by GoPro and we believe substitute threat is low due to (1) early mover advantage with well-established brand image, (2) high technology barrier that lower-end action camera is incomparable and (3) specially-designed accessories to cater demand from different kinds of sports enthusiasts.

Established in 2004, GoPro has sold >16mn action cameras and accessories in 100+ countries. GoPro has built its young, energetic, adventurous image in action camera market. Late-comers such as HTC (Re) and Xiaomi (Xiaoyi) are incomparable as their core business is smartphone, only GoPro is an action-camera pure-play which draws more attention from athletes’ side. Also, the water-proof/ dust-proof technology and durability are barriers to entrants as the camera is expected to be used under extreme conditions. Targeting different sports enthusiasts, GoPro has developed a set of accessories to meet the demand and customers can shop by activity.

Figure 7: Sky Light only supplies consumer grade models to GoPro under JDM basis

Figure 8: Accessories are specially-designed for different sports and bundled for sales

Sources: GoPro, CMS(HK) estimates Sources GoPro, CMS(HK) estimates

Action camera is still growing given (1) broader audience in mass market and (2) relatively low penetration in APAC and EMEA vs. Americas. We believe GoPro is broadening its user base with consumer grade HERO/HERO+/HERO+ LCD in APAC and EMEA. Being the sole supplier of lower-priced consumer grade models, we expect Sky Light to benefit from GoPro’s product mix change (>50% shipment are consumer grade models), backed by GoPro’s strong shipment growth in 9M15 (+64%YoY) while blended ASP down by 5%YoY to US$258.

Figure 9: GoPro ASP declined since 1Q15 Figure 10: GoPro consumer grade models are still rapidly growing in APAC and EMEA

Sources: GoPro, CMS(HK) estimates Sources: GoPro, CMS(HK) estimates

Model HERO4 Session HERO+ LCD HERO+ HERO

Price (US$) 299 299 199 129

Video 1440P/ 30fps 1080P/ 60fps 1080P/ 60fps 1080P/ 30fps

Supplier Chicony Sky Light Sky Light Sky Light

Model

Price (US$)

Video

Supplier

Consumer grade

HERO4 Black

499

4K/ 30fps

Chicony

Professional grade

HERO4 Silver

399

4K/ 15fps

Chicony

Dive housing Surfboard mounts

Side mount Skydiving chest harness

-15%

-10%

-5%

0%

5%

10%

15%

200

220

240

260

280

300

ASP (US$) YoY (%)

US$

-50%

0%

50%

100%

150%

200%

250%

300%

0

500

1,000

1,500

2,000

2012 2013 2014 2015E

Americas EMEA APAC

US$mn

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 6

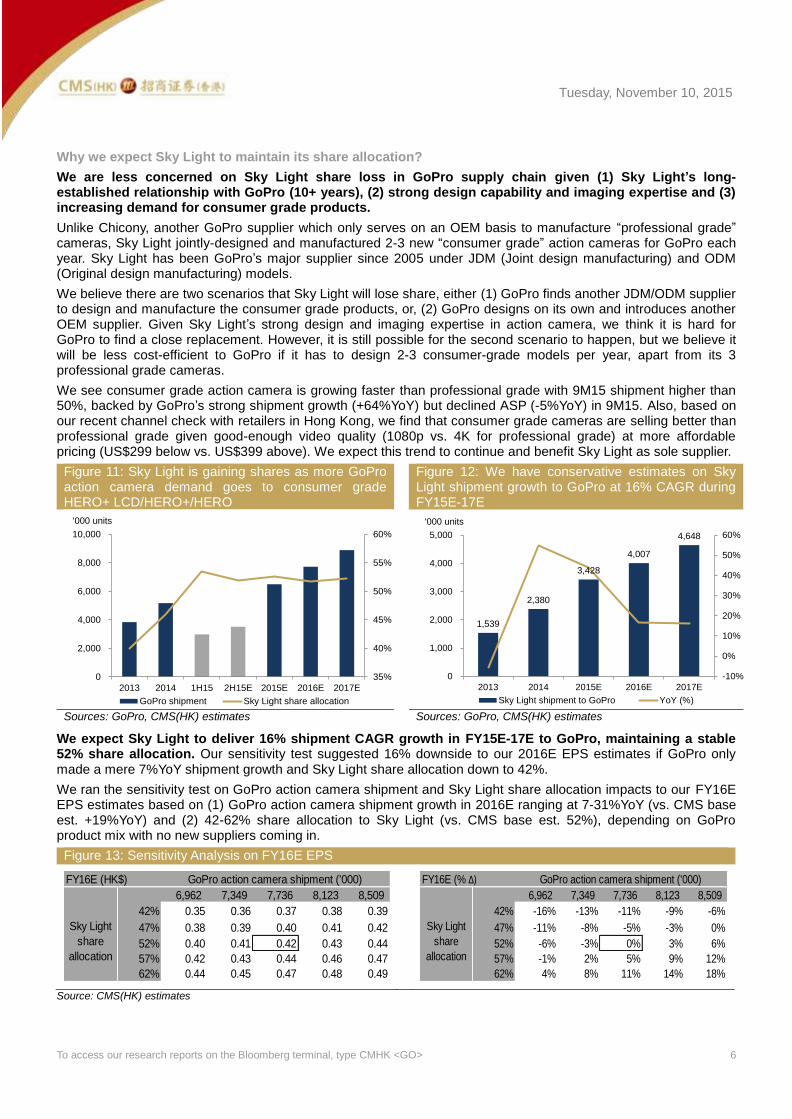

Why we expect Sky Light to maintain its share allocation?

We are less concerned on Sky Light share loss in GoPro supply chain given (1) Sky Light’s long-established relationship with GoPro (10+ years), (2) strong design capability and imaging expertise and (3) increasing demand for consumer grade products.

Unlike Chicony, another GoPro supplier which only serves on an OEM basis to manufacture “professional grade” cameras, Sky Light jointly-designed and manufactured 2-3 new “consumer grade” action cameras for GoPro each year. Sky Light has been GoPro’s major supplier since 2005 under JDM (Joint design manufacturing) and ODM (Original design manufacturing) models.

We believe there are two scenarios that Sky Light will lose share, either (1) GoPro finds another JDM/ODM supplier to design and manufacture the consumer grade products, or, (2) GoPro designs on its own and introduces another OEM supplier. Given Sky Light’s strong design and imaging expertise in action camera, we think it is hard for GoPro to find a close replacement. However, it is still possible for the second scenario to happen, but we believe it will be less cost-efficient to GoPro if it has to design 2-3 consumer-grade models per year, apart from its 3 professional grade cameras.

We see consumer grade action camera is growing faster than professional grade with 9M15 shipment higher than 50%, backed by GoPro’s strong shipment growth (+64%YoY) but declined ASP (-5%YoY) in 9M15. Also, based on our recent channel check with retailers in Hong Kong, we find that consumer grade cameras are selling better than professional grade given good-enough video quality (1080p vs. 4K for professional grade) at more affordable pricing (US$299 below vs. US$399 above). We expect this trend to continue and benefit Sky Light as sole supplier.

Figure 11: Sky Light is gaining shares as more GoPro action camera demand goes to consumer grade HERO+ LCD/HERO+/HERO

Figure 12: We have conservative estimates on Sky Light shipment growth to GoPro at 16% CAGR during FY15E-17E

Sources: GoPro, CMS(HK) estimates Sources: GoPro, CMS(HK) estimates

We expect Sky Light to deliver 16% shipment CAGR growth in FY15E-17E to GoPro, maintaining a stable 52% share allocation. Our sensitivity test suggested 16% downside to our 2016E EPS estimates if GoPro only made a mere 7%YoY shipment growth and Sky Light share allocation down to 42%.

We ran the sensitivity test on GoPro action camera shipment and Sky Light share allocation impacts to our FY16E EPS estimates based on (1) GoPro action camera shipment growth in 2016E ranging at 7-31%YoY (vs. CMS base est. +19%YoY) and (2) 42-62% share allocation to Sky Light (vs. CMS base est. 52%), depending on GoPro product mix with no new suppliers coming in.

Figure 13: Sensitivity Analysis on FY16E EPS

Source: CMS(HK) estimates

35%

40%

45%

50%

55%

60%

0

2,000

4,000

6,000

8,000

10,000

2013 2014 1H15 2H15E 2015E 2016E 2017E

GoPro shipment Sky Light share allocation

'000 units

1,539

2,380

3,428

4,007

4,648

-10%

0%

10%

20%

30%

40%

50%

60%

0

1,000

2,000

3,000

4,000

5,000

2013 2014 2015E 2016E 2017E

Sky Light shipment to GoPro YoY (%)

'000 units

FY16E (HK$)

0.42 6,962 7,349 7,736 8,123 8,509

42% 0.35 0.36 0.37 0.38 0.39

47% 0.38 0.39 0.40 0.41 0.42

52% 0.40 0.41 0.42 0.43 0.44

57% 0.42 0.43 0.44 0.46 0.47

62% 0.44 0.45 0.47 0.48 0.49

GoPro action camera shipment ('000)

Sky Light

share

allocation

FY16E (% ∆)

6,962 7,349 7,736 8,123 8,509

42% -16% -13% -11% -9% -6%

47% -11% -8% -5% -3% 0%

52% -6% -3% 0% 3% 6%

57% -1% 2% 5% 9% 12%

62% 4% 8% 11% 14% 18%

GoPro action camera shipment ('000)

Sky Light

share

allocation

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 7

2. Smart home: redefining wireless IP camera as next growth engine in FY16E

It comes to a tipping point for consumer use (self-installed, self-monitored) IP camera in home surveillance, fueled by tech giants’ interest in creating “Smart Home” ecosystem. We expect Sky Light’s home imaging revenue/shipment to grow at 35%/33% CAGR during FY15E-17E.

Why IP camera, supposed to be an “old” product, booming all of a sudden?

Home surveillance demand is always there, just the “new” IP camera changes how we keep an eye on our home. We are positive on home security IP camera growth outlook and we believe now is the time for it to take off as network infrastructure (Wifi/3G/4G), hardware (IP camera/smartphone) and software (app for live streaming) are now ready.

Compared to traditional home security system which required high set up and monthly monitoring fees, what consumers want is a self-installed, self-monitored system with lower cost but more functions. We believe the market potential and demand are strong that attracts startups as well as tech giants to develop IP cameras for home security. For instance, Canary, a start-up founded in 2012, launched its smart home monitoring system on a fundraising website and reached its US$100,000 goal within couple of hours. The company has now raised more than US$41.2mn in 3 rounds of fund raisings. Another start-up Dropcam, offering similar solution, was acquired by Nest Labs (Google’s subsidiary focusing on home automation) for US$555mn backed in 2014. In 2015, Nest Labs

launched Nest Cam to replace Dropcam. For China market, Xiaomi (Xiaoyi 小蚁智能摄像机) and Qihoo 360 (360

WiFi camera 360智能摄像机) both released IP camera in 2014.

Figure 14: Nest Cam can detect and analyze sound and motion to identify whether there is an intruder or just your kitten moving around.

Figure 15: With Canary IP camera, you can watch what is happening in your home anytime, choose to sound the siren or make an emergency call if suspicious activity is detected.

Sources: Nest, CMS(HK) Sources: Canary, CMS(HK)

Figure 16: Top selling IP camera for home security Brand Product Special features

Nest Cam

Can detect and analyze whether an object is human or tree or animal Activity zones allow users to highlight the most important areas and get personalized alerts if

something happens there 8x digital zoom, 2-way talk

Canary

Can detect abnormal actions and send users notification with recorded video Monitor air quality, temperature, humidity Free cloud recording, 2-way talk

Netgear

Small, 100% wire-free and waterproof, can be mount of trees and place outdoor Bundled with Netgear smart home base station Cheaper than Nest Cam and Canary (ASP: US$159)

Source: CMS(HK)

Makeemergency call

Live streaming

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 8

We expect Sky Light home imaging revenue to grow at 35% CAGR during FY15E-17E, contributing 22% of total revenue by 2017E. We estimate home imaging revenue to reach HK$483mn/686mn/876mn in FY15E/16E/17E.

Why we are positive on Sky Light’s home imaging segment?

Sky Light has started IP camera shipment to Netgear (Arlo) since 3Q14. Attributable to the strong demand for Arlo, commented by Netgear CEO, Netgear reported strong beat 3Q15 results (stock price up 40% in Oct 2015) with robust retail business growth at +25%YoY while Sky Light 1H15 home imaging revenue tripled to HK$183mn.

Following initial success of Arlo, we believe Netgear will accelerate new models roll out. New product, designed and manufactured by Sky Light, is expected to launch in Dec 2015. We expect >80% of Sky Light’s FY15E home imaging revenue to come from Netgear with shipment upside from new products.

Sky Light also supplies IP camera to start-up companies including Canary and iON, though volume is in a relatively small amount compared to Netgear. In sum, we estimate IP camera FY15E/16E shipment at 1.2mn/1.6mn, which we think is conservative given FY15E planned capacity expansion of 2.1mn. In terms of ASP, we have not factored in the potential ASP upside from increasing Canary/iON shipment (ASP: US$70-80) vs. Netgear ASP at US$40-50.

Figure 17: We expect Sky Light home imaging revenue to grow at 35% CAGR during FY15E-17E

Figure 18: Home imaging shipment to grow at 33% CAGR during FY15E-17E with slight improvement in ASP

Sources: Company, CMS(HK) estimates Sources: Company, CMS(HK) estimates

Figure 19: Netgear’s retail business turned around with IP camera Arlo, manufactured by Sky Light, in 4Q14

Figure 20: Changing revenue mix with home imaging contribution reaching 22% by 2017E

Source: CMS(HK) Sources: Company, CMS(HK) estimates

0.1 50.3

483.3

686.1

876.2

0

200

400

600

800

1,000

2013 2014 2015E 2016E 2017E

Home imaging revenue

HK$ mn35% CAGR in FY15E-17E

Netgear IP cam ramp up

380

400

420

440

460

480

0

500

1,000

1,500

2,000

2,500

2014 1H15 2H15E 2015E 2016E 2017E

Home imaging shipment ASP

'000 units HK$

-6% -6%

1%

9%

2%

19%

25%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

Netgear retail revenue YoY (%)

Arlo launched

US$mn

80% 85%73% 68% 65%

2%17%

20% 22%

14%10% 8% 9% 11%

6% 3% 3% 3% 3%

0%

20%

40%

60%

80%

100%

2013 2014 2015E 2016E 2017E

Actiona camera and accessories Home imaging Digital imaging Others

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 9

3. From camera to imaging software solution: 4K/LTE/image analysis

Sky Light is extending its product offering from hardware to software, from camera to online imaging platform. We believe imaging will continue to be an important part in IoT, with more advanced imaging technology such as 4K video/ LTE/ image analysis being applied on specialty cameras. We estimate digital imaging revenue (including specialty cameras such as car camcorder, police camera, shooting camera etc.) to grow at 37% CAGR during FY15E-17E.

Connected car: car camcorder project with leading China internet company is on the way

Sky Light is engaged in a car camcorder project with a leading internet company in China, shipment is expected to commence in Dec 2015. We believe the car camcorder will include higher specs and more functionalities than the average products on street, leveraging on the map and user base established by the internet company. We expect the product to include 4G connectivity to transfer real time traffic information. Sky Light first offered car camcorder solution in 2013 with self-developed app to keep track of car’s position, direction and speed. We expect car camcorder demand to increase given its increasing usage on car security, parking and recording car accident to determine liability. We believe car camcorder usage is still in an infant stage with more potential on connectivity (LTE), video and image quality (4K/wide-angle) upgrade. New Xian R&D center focusing on 4K/LTE/image analysis

We are positive on Sky Light R&D capability with stable R&D to sales ratio at 3.5-4%. In 1H15, Sky Light has set up a new R&D center (apart from the one in Shenzhen with 350 team size) focusing on mobile apps, cloud platform, LTE connectivity and video analytic technology. There are 400 R&D persons (11% of total staff) and will increase the number to 450-500 by FY16E. With strong imaging expertise, we believe Sky Light can win more new orders in specialty camera such as police camera and shooting camera. Police camera shipment will commence in 4Q15 to a leading US police device provider. Specialty cameras are high-margin business (GPM above company average of 20-21%) given their stringent requirements in better resolution, connectivity and image analytic technology. We are positive on Sky Light to win more overseas orders on specialty cameras with the newly set up subsidiary in US. Figure 21: Sky Light car camcorder and self-developed app to keep track of car’s position, direction and speed

Figure 22: Sky Light maintain a stable R&D expense to sales ratio at 3.5-4%

Sources: Company, CMS(HK) Sources: Company, CMS(HK) estimates

57.77

83.38

114.75

137.32

161.35

3.0%

3.5%

4.0%

4.5%

0

50

100

150

200

2013 2014 2015E 2016E 2017E

R&D expense R&D to sales ratio

HK$ mn

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 10

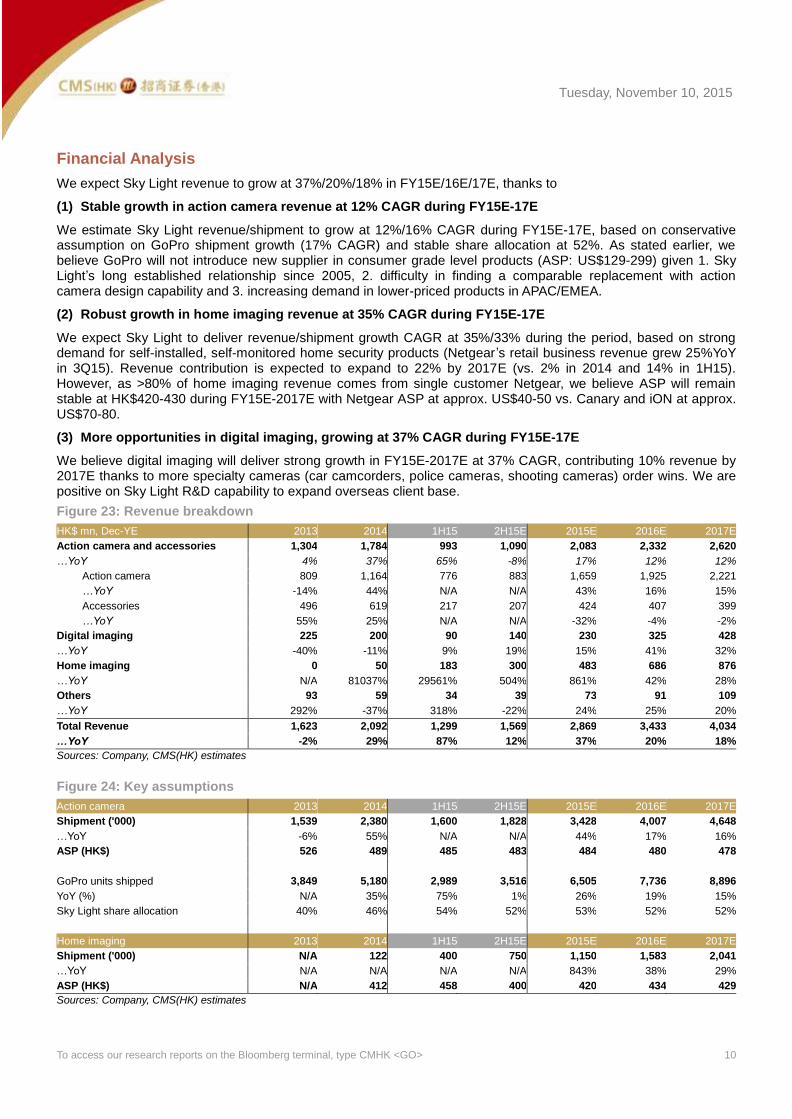

Financial Analysis

We expect Sky Light revenue to grow at 37%/20%/18% in FY15E/16E/17E, thanks to

(1) Stable growth in action camera revenue at 12% CAGR during FY15E-17E

We estimate Sky Light revenue/shipment to grow at 12%/16% CAGR during FY15E-17E, based on conservative assumption on GoPro shipment growth (17% CAGR) and stable share allocation at 52%. As stated earlier, we believe GoPro will not introduce new supplier in consumer grade level products (ASP: US$129-299) given 1. Sky Light’s long established relationship since 2005, 2. difficulty in finding a comparable replacement with action camera design capability and 3. increasing demand in lower-priced products in APAC/EMEA.

(2) Robust growth in home imaging revenue at 35% CAGR during FY15E-17E

We expect Sky Light to deliver revenue/shipment growth CAGR at 35%/33% during the period, based on strong demand for self-installed, self-monitored home security products (Netgear ’s retail business revenue grew 25%YoY in 3Q15). Revenue contribution is expected to expand to 22% by 2017E (vs. 2% in 2014 and 14% in 1H15). However, as >80% of home imaging revenue comes from single customer Netgear, we believe ASP will remain stable at HK$420-430 during FY15E-2017E with Netgear ASP at approx. US$40-50 vs. Canary and iON at approx. US$70-80.

(3) More opportunities in digital imaging, growing at 37% CAGR during FY15E-17E

We believe digital imaging will deliver strong growth in FY15E-2017E at 37% CAGR, contributing 10% revenue by 2017E thanks to more specialty cameras (car camcorders, police cameras, shooting cameras) order wins. We are positive on Sky Light R&D capability to expand overseas client base.

Figure 23: Revenue breakdown

HK$ mn, Dec-YE 2013 2014 1H15 2H15E 2015E 2016E 2017E

Action camera and accessories 1,304 1,784 993 1,090 2,083 2,332 2,620

…YoY 4% 37% 65% -8% 17% 12% 12%

Action camera 809 1,164 776 883 1,659 1,925 2,221

…YoY -14% 44% N/A N/A 43% 16% 15%

Accessories 496 619 217 207 424 407 399

…YoY 55% 25% N/A N/A -32% -4% -2%

Digital imaging 225 200 90 140 230 325 428

…YoY -40% -11% 9% 19% 15% 41% 32%

Home imaging 0 50 183 300 483 686 876

…YoY N/A 81037% 29561% 504% 861% 42% 28%

Others 93 59 34 39 73 91 109

…YoY 292% -37% 318% -22% 24% 25% 20%

Total Revenue 1,623 2,092 1,299 1,569 2,869 3,433 4,034

…YoY -2% 29% 87% 12% 37% 20% 18%

Sources: Company, CMS(HK) estimates

Figure 24: Key assumptions

Action camera 2013 2014 1H15 2H15E 2015E 2016E 2017E

Shipment ('000) 1,539 2,380 1,600 1,828 3,428 4,007 4,648

…YoY -6% 55% N/A N/A 44% 17% 16%

ASP (HK$) 526 489 485 483 484 480 478

GoPro units shipped 3,849 5,180 2,989 3,516 6,505 7,736 8,896

YoY (%) N/A 35% 75% 1% 26% 19% 15%

Sky Light share allocation 40% 46% 54% 52% 53% 52% 52%

Home imaging 2013 2014 1H15 2H15E 2015E 2016E 2017E

Shipment ('000) N/A 122 400 750 1,150 1,583 2,041

…YoY N/A N/A N/A N/A 843% 38% 29%

ASP (HK$) N/A 412 458 400 420 434 429

Sources: Company, CMS(HK) estimates

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 11

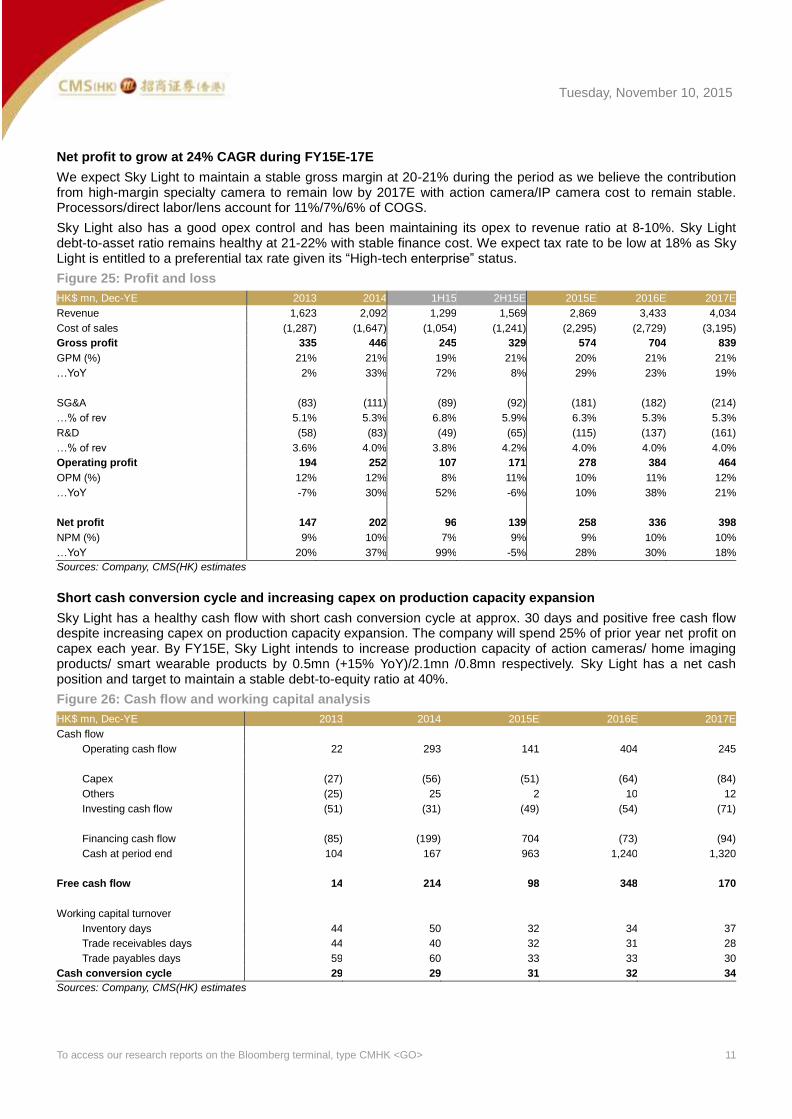

Net profit to grow at 24% CAGR during FY15E-17E

We expect Sky Light to maintain a stable gross margin at 20-21% during the period as we believe the contribution from high-margin specialty camera to remain low by 2017E with action camera/IP camera cost to remain stable. Processors/direct labor/lens account for 11%/7%/6% of COGS.

Sky Light also has a good opex control and has been maintaining its opex to revenue ratio at 8-10%. Sky Light debt-to-asset ratio remains healthy at 21-22% with stable finance cost. We expect tax rate to be low at 18% as Sky Light is entitled to a preferential tax rate given its “High-tech enterprise” status.

Figure 25: Profit and loss

HK$ mn, Dec-YE 2013 2014 1H15 2H15E 2015E 2016E 2017E

Revenue 1,623 2,092 1,299 1,569 2,869 3,433 4,034

Cost of sales (1,287) (1,647) (1,054) (1,241) (2,295) (2,729) (3,195)

Gross profit 335 446 245 329 574 704 839

GPM (%) 21% 21% 19% 21% 20% 21% 21%

…YoY 2% 33% 72% 8% 29% 23% 19%

SG&A (83) (111) (89) (92) (181) (182) (214)

…% of rev 5.1% 5.3% 6.8% 5.9% 6.3% 5.3% 5.3%

R&D (58) (83) (49) (65) (115) (137) (161)

…% of rev 3.6% 4.0% 3.8% 4.2% 4.0% 4.0% 4.0%

Operating profit 194 252 107 171 278 384 464

OPM (%) 12% 12% 8% 11% 10% 11% 12%

…YoY -7% 30% 52% -6% 10% 38% 21%

Net profit 147 202 96 139 258 336 398

NPM (%) 9% 10% 7% 9% 9% 10% 10%

…YoY 20% 37% 99% -5% 28% 30% 18%

Sources: Company, CMS(HK) estimates

Short cash conversion cycle and increasing capex on production capacity expansion

Sky Light has a healthy cash flow with short cash conversion cycle at approx. 30 days and positive free cash flow despite increasing capex on production capacity expansion. The company will spend 25% of prior year net profit on capex each year. By FY15E, Sky Light intends to increase production capacity of action cameras/ home imaging products/ smart wearable products by 0.5mn (+15% YoY)/2.1mn /0.8mn respectively. Sky Light has a net cash position and target to maintain a stable debt-to-equity ratio at 40%.

Figure 26: Cash flow and working capital analysis

HK$ mn, Dec-YE 2013 2014 2015E 2016E 2017E

Cash flow

Operating cash flow 22 293 141 404 245

Capex (27) (56) (51) (64) (84)

Others (25) 25 2 10 12

Investing cash flow (51) (31) (49) (54) (71)

Financing cash flow (85) (199) 704 (73) (94)

Cash at period end 104 167 963 1,240 1,320

Free cash flow 14 214 98 348 170

Working capital turnover

Inventory days 44 50 32 34 37

Trade receivables days 44 40 32 31 28

Trade payables days 59 60 33 33 30

Cash conversion cycle 29 29 31 32 34

Sources: Company, CMS(HK) estimates

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 12

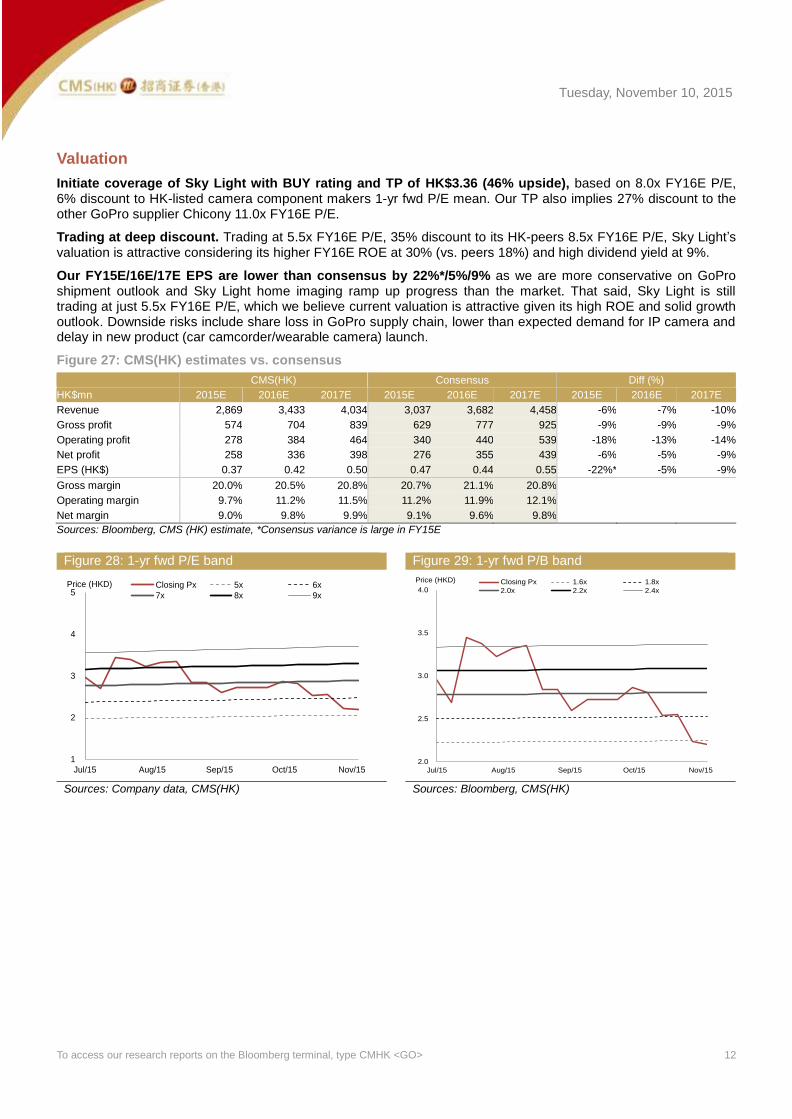

Valuation

Initiate coverage of Sky Light with BUY rating and TP of HK$3.36 (46% upside), based on 8.0x FY16E P/E, 6% discount to HK-listed camera component makers 1-yr fwd P/E mean. Our TP also implies 27% discount to the other GoPro supplier Chicony 11.0x FY16E P/E.

Trading at deep discount. Trading at 5.5x FY16E P/E, 35% discount to its HK-peers 8.5x FY16E P/E, Sky Light’s valuation is attractive considering its higher FY16E ROE at 30% (vs. peers 18%) and high dividend yield at 9%.

Our FY15E/16E/17E EPS are lower than consensus by 22%*/5%/9% as we are more conservative on GoPro shipment outlook and Sky Light home imaging ramp up progress than the market. That said, Sky Light is still trading at just 5.5x FY16E P/E, which we believe current valuation is attractive given its high ROE and solid growth outlook. Downside risks include share loss in GoPro supply chain, lower than expected demand for IP camera and delay in new product (car camcorder/wearable camera) launch.

Figure 27: CMS(HK) estimates vs. consensus

CMS(HK) Consensus Diff (%)

HK$mn 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E

Revenue 2,869 3,433 4,034 3,037 3,682 4,458 -6% -7% -10%

Gross profit 574 704 839 629 777 925 -9% -9% -9%

Operating profit 278 384 464 340 440 539 -18% -13% -14%

Net profit 258 336 398 276 355 439 -6% -5% -9%

EPS (HK$) 0.37 0.42 0.50 0.47 0.44 0.55 -22%* -5% -9%

Gross margin 20.0% 20.5% 20.8% 20.7% 21.1% 20.8%

Operating margin 9.7% 11.2% 11.5% 11.2% 11.9% 12.1%

Net margin 9.0% 9.8% 9.9% 9.1% 9.6% 9.8%

Sources: Bloomberg, CMS (HK) estimate, *Consensus variance is large in FY15E

Figure 28: 1-yr fwd P/E band Figure 29: 1-yr fwd P/B band

Sources: Company data, CMS(HK) Sources: Bloomberg, CMS(HK)

1

2

3

4

5

Jul/15 Aug/15 Sep/15 Oct/15 Nov/15

Price (HKD) Closing Px 5x 6x

7x 8x 9x

2.0

2.5

3.0

3.5

4.0

Jul/15 Aug/15 Sep/15 Oct/15 Nov/15

Price (HKD) Closing Px 1.6x 1.8x

2.0x 2.2x 2.4x

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 13

Figure 30: Peers valuation

Company Ticker Rating Market Cap (US$ mn)

Current Price (LC$)

52-Wk Price Range (LC$)

Avg Turnover (US$ mn)

P/E (x) P/B (x) ROE (%)

FY15E FY16E FY15E FY16E FY15E FY16E

Sky Light 3882 HK BUY 237.5 2.3 1.6 / 3.74 1.3 6.27 5.48 1.68 1.63 27% 30%

Camera Supply Chain

Sunny Optical 2382 HK BUY

2,530.5 17.9 10.38 / 19.94 10.9 21.4 16.6 4.0 3.4 21% 23%

Cowell 1415 HK BUY

407.6 3.8 3.02 / 8.85 1.5 5.6 4.6 1.2 1.0 28% 25%

Truly 732 HK NEUTRAL

686.3 1.8 1.82 / 4.3 1.4 6.4 6.0 0.7 0.6 11% 11%

Q-tech 1478 HK N/A

225.4 1.7 1.21 / 3.89 0.1 8.2 6.6 1.1 1.0 14% 16%

Avg

10.4 8.5 1.8 1.5 19% 18%

GoPro Supply Chain

Chicony 2385 TT N/A

1,635.0 76.0 73.3 / 90.35 4.0 12.7 11.0 2.4 2.3 17% 20%

Hon Hai 2317 TT N/A

41,082.1 84.5 74.19 / 94.95 94.0 9.3 9.2 1.3 1.2 14% 14%

Ambarella AMBA US N/A

1,801.9 56.9 44.45 / 129.19 223.9 31.7 18.6 8.1 5.0 30% 32%

Lianchuang 600363 CH N/A

1,272.1 18.3 9.34 / 29.86 59.8 N/A N/A N/A N/A N/A N/A

Sony 6758 JP N/A

35,444.8 3,463.0 2247 / 3970 224.6 N/A 22.9 1.8 1.5 -6% 8%

TK Group 2283 HK BUY

228.2 2.1 1.52 / 3 0.2 8.8 7.1 2.7 2.2 32% 32%

Avg 15.6 13.7 3.3 2.5 18% 21%

Sources: Bloomberg, CMS (HK) estimate

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 14

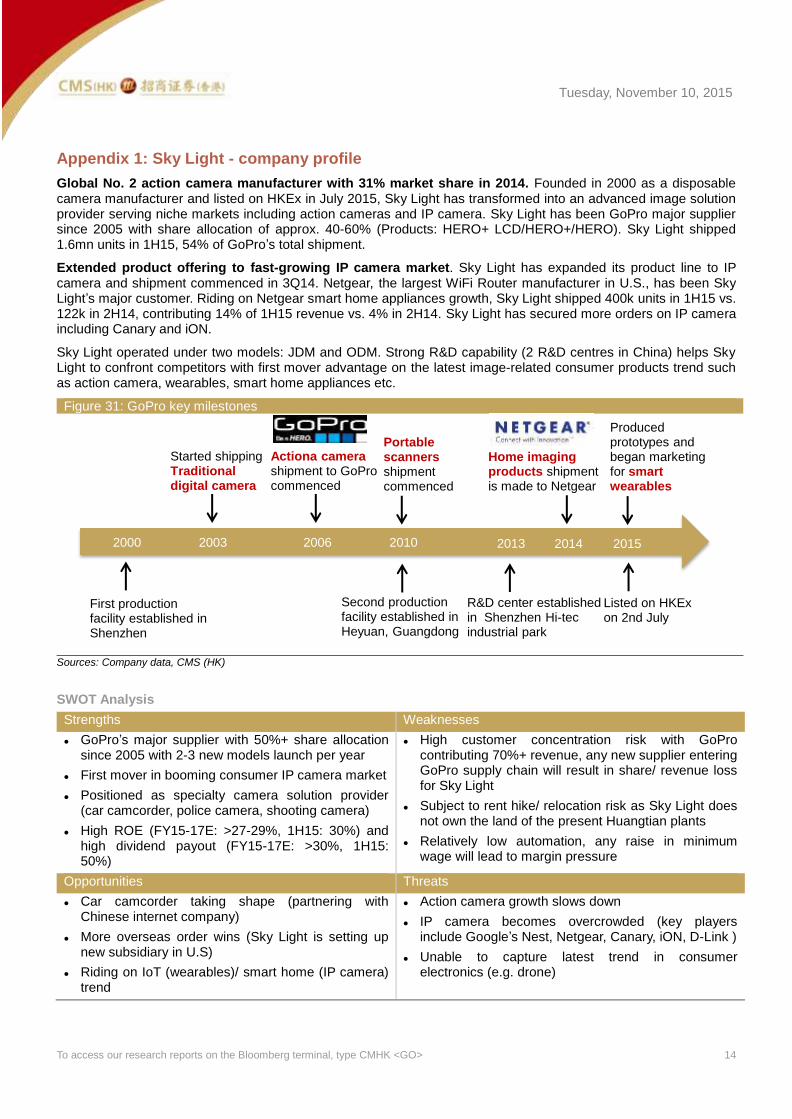

Appendix 1: Sky Light - company profile

Global No. 2 action camera manufacturer with 31% market share in 2014. Founded in 2000 as a disposable camera manufacturer and listed on HKEx in July 2015, Sky Light has transformed into an advanced image solution provider serving niche markets including action cameras and IP camera. Sky Light has been GoPro major supplier since 2005 with share allocation of approx. 40-60% (Products: HERO+ LCD/HERO+/HERO). Sky Light shipped 1.6mn units in 1H15, 54% of GoPro’s total shipment.

Extended product offering to fast-growing IP camera market. Sky Light has expanded its product line to IP camera and shipment commenced in 3Q14. Netgear, the largest WiFi Router manufacturer in U.S., has been Sky Light’s major customer. Riding on Netgear smart home appliances growth, Sky Light shipped 400k units in 1H15 vs. 122k in 2H14, contributing 14% of 1H15 revenue vs. 4% in 2H14. Sky Light has secured more orders on IP camera including Canary and iON.

Sky Light operated under two models: JDM and ODM. Strong R&D capability (2 R&D centres in China) helps Sky Light to confront competitors with first mover advantage on the latest image-related consumer products trend such as action camera, wearables, smart home appliances etc.

Figure 31: GoPro key milestones

Sources: Company data, CMS (HK)

SWOT Analysis

Strengths Weaknesses

GoPro’s major supplier with 50%+ share allocation since 2005 with 2-3 new models launch per year

First mover in booming consumer IP camera market

Positioned as specialty camera solution provider (car camcorder, police camera, shooting camera)

High ROE (FY15-17E: >27-29%, 1H15: 30%) and high dividend payout (FY15-17E: >30%, 1H15: 50%)

High customer concentration risk with GoPro contributing 70%+ revenue, any new supplier entering GoPro supply chain will result in share/ revenue loss for Sky Light

Subject to rent hike/ relocation risk as Sky Light does not own the land of the present Huangtian plants

Relatively low automation, any raise in minimum wage will lead to margin pressure

Opportunities Threats

Car camcorder taking shape (partnering with Chinese internet company)

More overseas order wins (Sky Light is setting up new subsidiary in U.S)

Riding on IoT (wearables)/ smart home (IP camera) trend

Action camera growth slows down

IP camera becomes overcrowded (key players include Google’s Nest, Netgear, Canary, iON, D-Link )

Unable to capture latest trend in consumer electronics (e.g. drone)

2000

First production facility established in Shenzhen

2003

Started shipping Traditionaldigital camera

2006

Actiona camerashipment to GoPro commenced

2010

Portablescanners shipment commenced

2013

R&D center established in Shenzhen Hi-tec industrial park

2014

Home imaging products shipment is made to Netgear

2015

Listed on HKExon 2nd July

Second production facility established in Heyuan, Guangdong

Produced prototypes and began marketing for smart wearables

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 15

Figure 32: Product description

Action camera and accessories (73% of FY15E revenue)

Model HERO HERO+ HERO+ LCD Brand GoPro GoPro GoPro Release date Oct-14 Sep-15 Jun-15 Selling Price (US$) 129 199 299 Description

Video 1080p30 1080p60 1080p60 Photo 5MP/ 5fps 8MP/ 5 fps 8MP/ 5 fps Waterproof 40m 40m 40m Built-in wireless No Wi-Fi + Bluetooth Wi-Fi + Bluetooth Touch display No No Yes Memory up to 32GB up to 64GB up to 64GB

Home Imaging (17% of FY15E revenue)

Model Arlo Canary iON the home Brand Netgear Canary Connect iON Release date Nov-14 Mar-15 Mar-15 Selling Price (US$) 159 199 129 Description

Camera 1280p HD 1080p 720p 110° 147° 102° Night vision Night vision Night vision Sensors Motion detection Motion detection N/A

Temperature

Humidity Air quality

Audio N/A Built-in speaker and microphone

Built-in speaker and microphone

Connectivity Wi-Fi Wi-Fi Wi-Fi Special feature Waterproof

Two-way talk

Completely wireless

Digital Imaging (8% of FY15E revenue)

Product Waterproof digital camera Portable scanner Others: digital camcorders, police cameras, car camcorders, wearable cameras, shooting cameras

Release date 2003 2010 2007 Source: Company, CMS(HK)

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 16

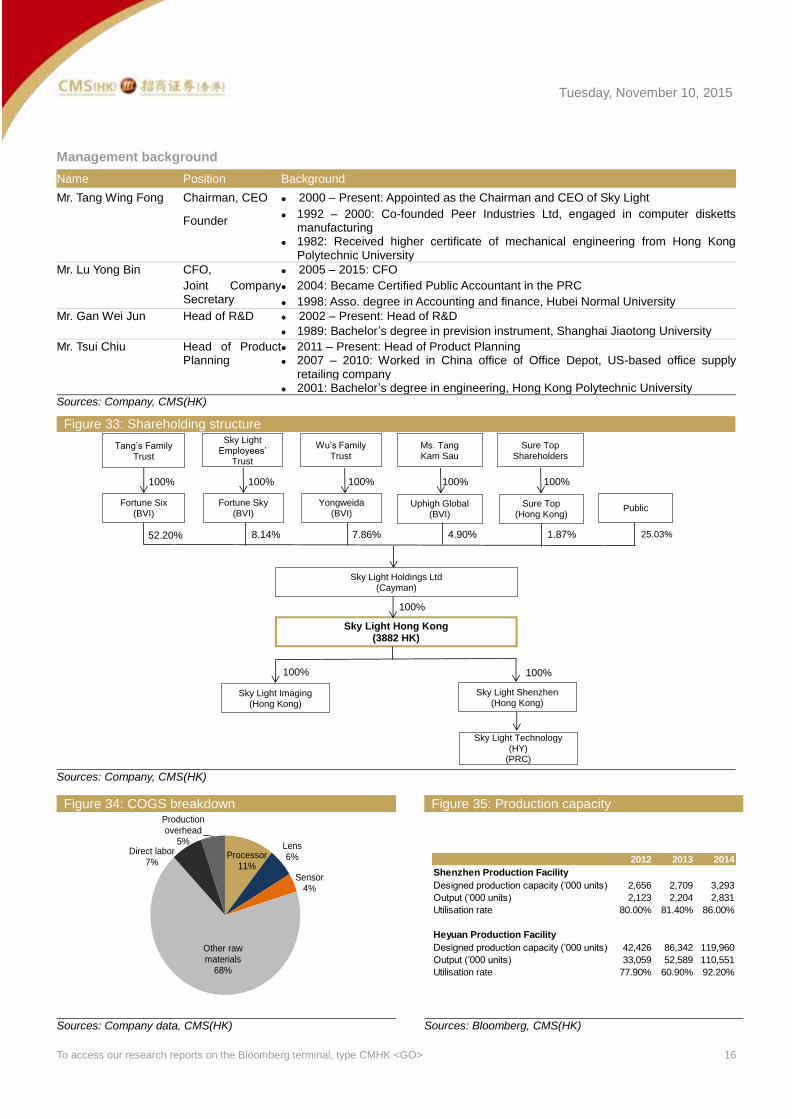

Management background

Name Position Background

Mr. Tang Wing Fong Chairman, CEO 2000 – Present: Appointed as the Chairman and CEO of Sky Light

Founder 1992 – 2000: Co-founded Peer Industries Ltd, engaged in computer disketts

manufacturing

1982: Received higher certificate of mechanical engineering from Hong Kong

Polytechnic University

Mr. Lu Yong Bin CFO, 2005 – 2015: CFO

Joint Company Secretary

2004: Became Certified Public Accountant in the PRC

1998: Asso. degree in Accounting and finance, Hubei Normal University

Mr. Gan Wei Jun Head of R&D 2002 – Present: Head of R&D

1989: Bachelor’s degree in prevision instrument, Shanghai Jiaotong University

Mr. Tsui Chiu Head of Product Planning

2011 – Present: Head of Product Planning

2007 – 2010: Worked in China office of Office Depot, US-based office supply

retailing company 2001: Bachelor’s degree in engineering, Hong Kong Polytechnic University Sources: Company, CMS(HK)

Figure 33: Shareholding structure

Sources: Company, CMS(HK)

Figure 34: COGS breakdown Figure 35: Production capacity

Sources: Company data, CMS(HK) Sources: Bloomberg, CMS(HK)

Sky Light Employees’

Trust

Wu’s Family Trust

Fortune Six(BVI)

Sure Top Shareholders

Ms. Tang Kam Sau

Tang’s Family Trust

Fortune Sky(BVI)

100%100%

Yongweida(BVI)

100%

Uphigh Global(BVI)

100%

Sure Top(Hong Kong)

100%

Public

Sky Light Holdings Ltd(Cayman)

52.20% 8.14% 7.86% 4.90% 1.87% 25.03%

100%

Sky Light Hong Kong(3882 HK)

Sky Light Imaging(Hong Kong)

Sky Light Shenzhen(Hong Kong)

Sky Light Technology(HY)

(PRC)

100% 100%

Processor11%

Lens6%

Sensor4%

Other raw materials

68%

Direct labor7%

Production overhead

5%

2012 2013 2014

Shenzhen Production Facility

Designed production capacity (’000 units) 2,656 2,709 3,293

Output (’000 units) 2,123 2,204 2,831

Utilisation rate 80.00% 81.40% 86.00%

Heyuan Production Facility

Designed production capacity (’000 units) 42,426 86,342 119,960

Output (’000 units) 33,059 52,589 110,551

Utilisation rate 77.90% 60.90% 92.20%

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 17

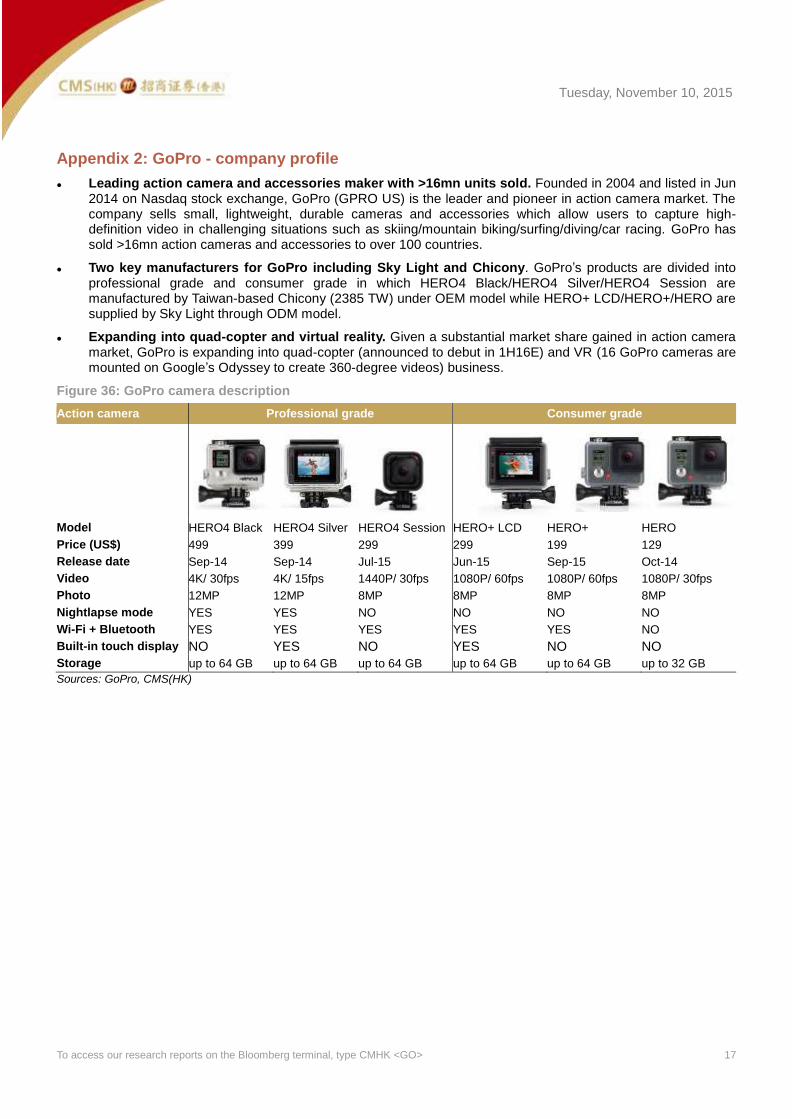

Appendix 2: GoPro - company profile

Leading action camera and accessories maker with >16mn units sold. Founded in 2004 and listed in Jun 2014 on Nasdaq stock exchange, GoPro (GPRO US) is the leader and pioneer in action camera market. The company sells small, lightweight, durable cameras and accessories which allow users to capture high-definition video in challenging situations such as skiing/mountain biking/surfing/diving/car racing. GoPro has sold >16mn action cameras and accessories to over 100 countries.

Two key manufacturers for GoPro including Sky Light and Chicony. GoPro’s products are divided into professional grade and consumer grade in which HERO4 Black/HERO4 Silver/HERO4 Session are manufactured by Taiwan-based Chicony (2385 TW) under OEM model while HERO+ LCD/HERO+/HERO are supplied by Sky Light through ODM model.

Expanding into quad-copter and virtual reality. Given a substantial market share gained in action camera market, GoPro is expanding into quad-copter (announced to debut in 1H16E) and VR (16 GoPro cameras are mounted on Google’s Odyssey to create 360-degree videos) business.

Figure 36: GoPro camera description

Action camera Professional grade Consumer grade

Model HERO4 Black HERO4 Silver HERO4 Session HERO+ LCD HERO+ HERO

Price (US$) 499 399 299 299 199 129

Release date Sep-14 Sep-14 Jul-15 Jun-15 Sep-15 Oct-14

Video 4K/ 30fps 4K/ 15fps 1440P/ 30fps 1080P/ 60fps 1080P/ 60fps 1080P/ 30fps

Photo 12MP 12MP 8MP 8MP 8MP 8MP

Nightlapse mode YES YES NO NO NO NO

Wi-Fi + Bluetooth YES YES YES YES YES NO

Built-in touch display NO YES NO YES NO NO

Storage up to 64 GB up to 64 GB up to 64 GB up to 64 GB up to 64 GB up to 32 GB

Sources: GoPro, CMS(HK)

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 18

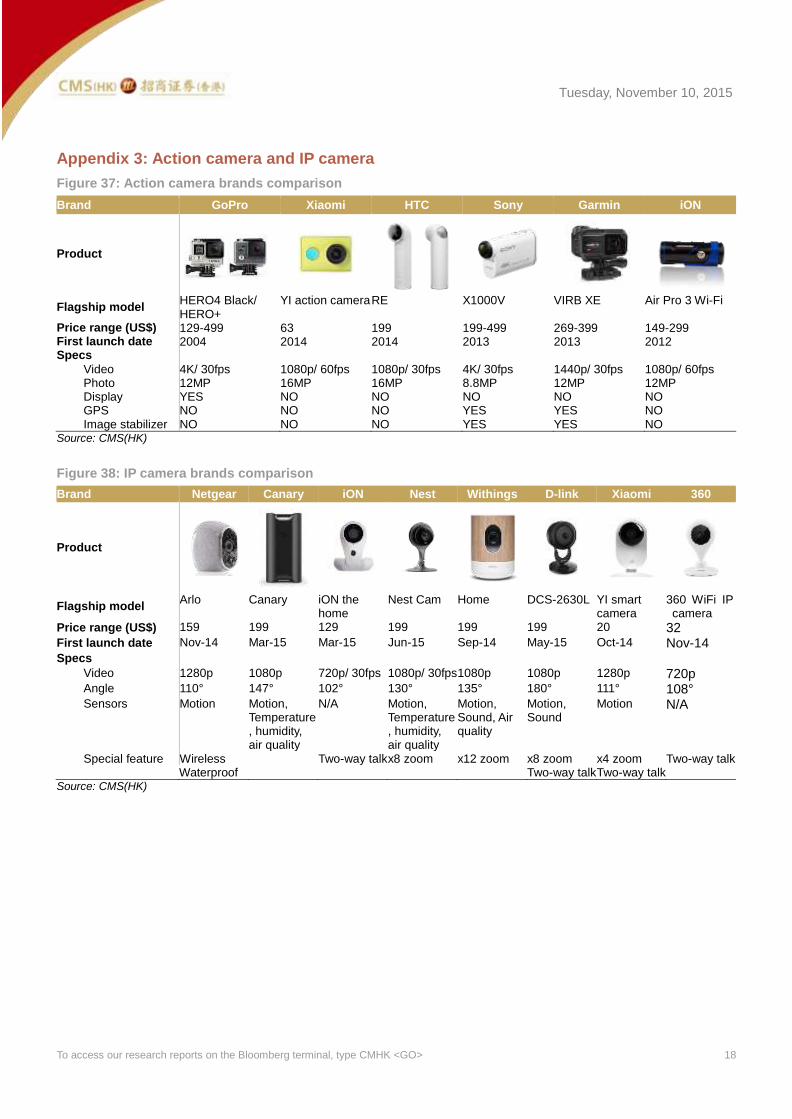

Appendix 3: Action camera and IP camera

Figure 37: Action camera brands comparison

Brand GoPro Xiaomi HTC Sony Garmin iON

Product

Flagship model HERO4 Black/ HERO+

YI action camera RE X1000V VIRB XE Air Pro 3 Wi-Fi

Price range (US$) 129-499 63 199 199-499 269-399 149-299 First launch date 2004 2014 2014 2013 2013 2012 Specs

Video 4K/ 30fps 1080p/ 60fps 1080p/ 30fps 4K/ 30fps 1440p/ 30fps 1080p/ 60fps Photo 12MP 16MP 16MP 8.8MP 12MP 12MP Display YES NO NO NO NO NO GPS NO NO NO YES YES NO Image stabilizer NO NO NO YES YES NO

Source: CMS(HK)

Figure 38: IP camera brands comparison

Brand Netgear Canary iON Nest Withings D-link Xiaomi 360

Product

Flagship model Arlo Canary iON the

home Nest Cam Home DCS-2630L YI smart

camera 360 WiFi IP camera

Price range (US$) 159 199 129 199 199 199 20 32 First launch date Nov-14 Mar-15 Mar-15 Jun-15 Sep-14 May-15 Oct-14 Nov-14 Specs

Video 1280p 1080p 720p/ 30fps 1080p/ 30fps 1080p 1080p 1280p 720p Angle 110° 147° 102° 130° 135° 180° 111° 108° Sensors Motion Motion,

Temperature, humidity, air quality

N/A Motion, Temperature, humidity, air quality

Motion, Sound, Air quality

Motion, Sound

Motion N/A

Special feature Wireless Two-way talk x8 zoom x12 zoom x8 zoom x4 zoom Two-way talk Waterproof Two-way talk Two-way talk

Source: CMS(HK)

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 19

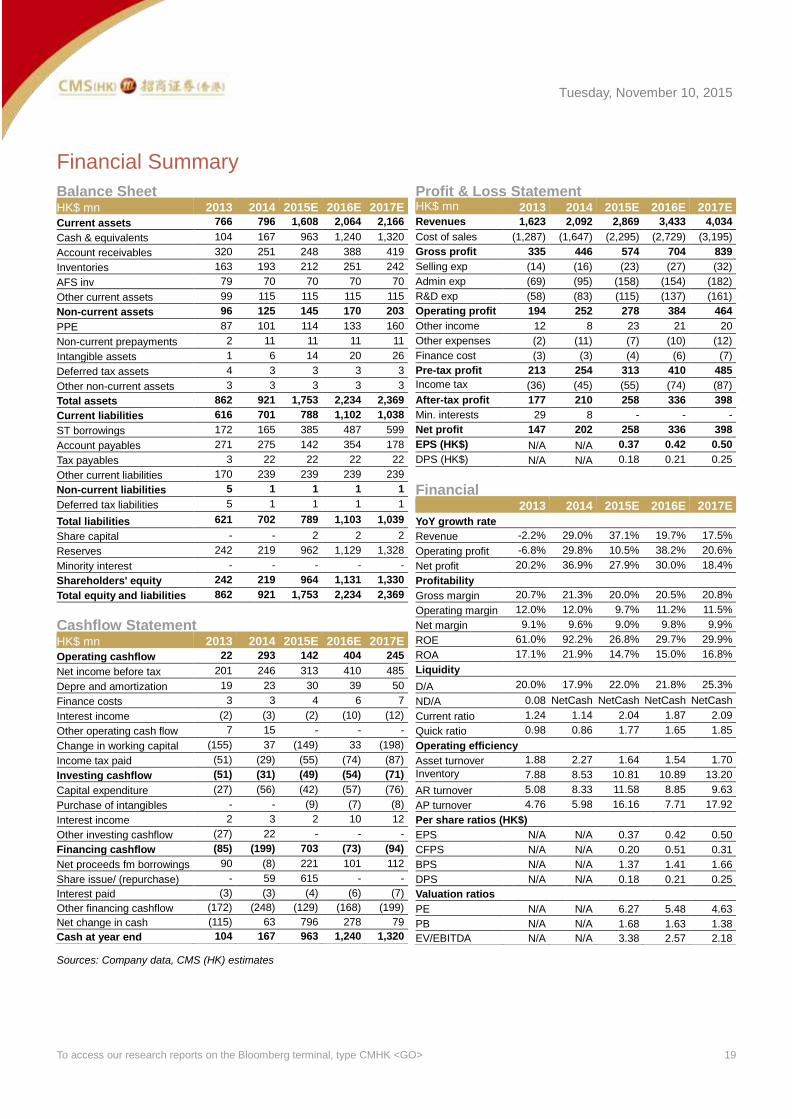

Financial Summary

Balance Sheet

HK$ mn 2013 2014 2015E 2016E 2017E

Current assets 766 796 1,608 2,064 2,166

Cash & equivalents 104 167 963 1,240 1,320

Account receivables 320 251 248 388 419

Inventories 163 193 212 251 242

AFS inv 79 70 70 70 70

Other current assets 99 115 115 115 115

Non-current assets 96 125 145 170 203

PPE 87 101 114 133 160

Non-current prepayments 2 11 11 11 11

Intangible assets 1 6 14 20 26

Deferred tax assets 4 3 3 3 3

Other non-current assets 3 3 3 3 3

Total assets 862 921 1,753 2,234 2,369

Current liabilities 616 701 788 1,102 1,038

ST borrowings 172 165 385 487 599

Account payables 271 275 142 354 178

Tax payables 3 22 22 22 22

Other current liabilities 170 239 239 239 239

Non-current liabilities 5 1 1 1 1

Deferred tax liabilities 5 1 1 1 1

Total liabilities 621 702 789 1,103 1,039

Share capital - - 2 2 2

Reserves 242 219 962 1,129 1,328

Minority interest - - - - -

Shareholders' equity 242 219 964 1,131 1,330

Total equity and liabilities 862 921 1,753 2,234 2,369

Cashflow Statement

HK$ mn 2013 2014 2015E 2016E 2017E

Operating cashflow 22 293 142 404 245

Net income before tax 201 246 313 410 485

Depre and amortization 19 23 30 39 50

Finance costs 3 3 4 6 7

Interest income (2) (3) (2) (10) (12)

Other operating cash flow 7 15 - - -

Change in working capital (155) 37 (149) 33 (198)

Income tax paid (51) (29) (55) (74) (87)

Investing cashflow (51) (31) (49) (54) (71)

Capital expenditure (27) (56) (42) (57) (76)

Purchase of intangibles - - (9) (7) (8)

Interest income 2 3 2 10 12

Other investing cashflow (27) 22 - - -

Financing cashflow (85) (199) 703 (73) (94)

Net proceeds fm borrowings 90 (8) 221 101 112

Share issue/ (repurchase) - 59 615 - -

Interest paid (3) (3) (4) (6) (7)

Other financing cashflow (172) (248) (129) (168) (199)

Net change in cash (115) 63 796 278 79

Cash at year end 104 167 963 1,240 1,320

Profit & Loss Statement HK$ mn 2013 2014 2015E 2016E 2017E Revenues 1,623 2,092 2,869 3,433 4,034

Cost of sales (1,287) (1,647) (2,295) (2,729) (3,195)

Gross profit 335 446 574 704 839

Selling exp (14) (16) (23) (27) (32)

Admin exp (69) (95) (158) (154) (182)

R&D exp (58) (83) (115) (137) (161)

Operating profit 194 252 278 384 464

Other income 12 8 23 21 20

Other expenses (2) (11) (7) (10) (12)

Finance cost (3) (3) (4) (6) (7)

Pre-tax profit 213 254 313 410 485

Income tax expense

(36) (45) (55) (74) (87)

After-tax profit 177 210 258 336 398

Min. interests 29 8 - - -

Net profit 147 202 258 336 398

EPS (HK$) N/A N/A 0.37 0.42 0.50

DPS (HK$) N/A N/A 0.18 0.21 0.25

Financial Ratios

2013 2014 2015E 2016E 2017E

YoY growth rate

Revenue -2.2% 29.0% 37.1% 19.7% 17.5%

Operating profit -6.8% 29.8% 10.5% 38.2% 20.6%

Net profit 20.2% 36.9% 27.9% 30.0% 18.4%

Profitability

Gross margin 20.7% 21.3% 20.0% 20.5% 20.8%

Operating margin 12.0% 12.0% 9.7% 11.2% 11.5%

Net margin 9.1% 9.6% 9.0% 9.8% 9.9%

ROE 61.0% 92.2% 26.8% 29.7% 29.9%

ROA 17.1% 21.9% 14.7% 15.0% 16.8%

Liquidity

D/A 20.0% 17.9% 22.0% 21.8% 25.3%

ND/A 0.08 NetCash NetCash NetCash NetCash

Current ratio 1.24 1.14 2.04 1.87 2.09

Quick ratio 0.98 0.86 1.77 1.65 1.85

Operating efficiency

Asset turnover 1.88 2.27 1.64 1.54 1.70

Inventory turnover

7.88 8.53 10.81 10.89 13.20

AR turnover 5.08 8.33 11.58 8.85 9.63

AP turnover 4.76 5.98 16.16 7.71 17.92

Per share ratios (HK$)

EPS N/A N/A 0.37 0.42 0.50

CFPS N/A N/A 0.20 0.51 0.31

BPS N/A N/A 1.37 1.41 1.66

DPS N/A N/A 0.18 0.21 0.25

Valuation ratios

PE N/A N/A 6.27 5.48 4.63

PB N/A N/A 1.68 1.63 1.38

EV/EBITDA N/A N/A 3.38 2.57 2.18

Sources: Company data, CMS (HK) estimates

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 20

Investment Ratings

Industry Rating Definition

OVERWEIGHT Expect sector to outperform the market over the next 12 months

NEUTRAL Expect sector to perform in-line with the market over the next 12 months

UNDERWEIGHT Expect sector to underperform the market over the next 12 months

Company Rating Definition

BUY Expect stock to generate 10%+ return over the next 12 months

NEUTRAL Expect stock to generate +10% to -10% over the next 12 months

SELL Expect stock to generate loss of 10%+ over the next 12 months

Analyst Disclosure

The analysts primarily responsible for the preparation of all or part of the research report contained herein hereby certify that: (i) the views expressed in this research report accurately reflect the

personal views of each such analyst about the subject securities and issuers; and (ii) no part of the analyst’s compensation was, is, or will be directly or indirectly, related to the specific

recommendations or views expressed in this research report.

Regulatory Disclosure

Please refer to the important disclosures on our website http://www.newone.com.hk/cmshk/en/disclosure.html.

Disclaimer

This document is prepared by China Merchants Securities (HK) Co., Limited (“CMS HK”). CMS HK is a licensed corporation to carry on Type 1 (dealing in securities), Type 2 (dealing in futures),

Type 4 (advising on securities), Type 6 (advising on corporate finance) and Type 9 (asset management) regulated activities under the Securities and Futures Ordinance (Chapter 571). This

document is for information purpose only. Neither the information nor opinion expressed shall be construed, expressly or impliedly, as an advice, offer or solicitation of an offer, invitation,

advertisement, inducement, recommendation or representation of any kind or form whatsoever to buy or sell any security, financial instrument or any investment or other specific product. The

securities, instruments or strategies discussed in this document may not be suitable for all investors, and certain investors may not be eligible to participate in some or all of them. Certain

services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. CMS HK is not registered as a

broker-dealer in the United States and its products and services are not available to U.S. persons except as permitted under SEC Rule 15a-6.

The information and opinions, and associated estimates and forecasts, contained herein have been obtained from or are based on sources believed to be reliable. CMS HK, its holding or

affiliated companies, or any of its or their directors, officers or employees (“CMS Group”) do not represent or warrant, expressly or impliedly, that it is accurate, correct or complete and it should

not be relied upon. CMS Group will not accept any responsibility or liability whatsoever for any use of or reliance upon this document or any of the content thereof. The contents and information

in this document are only current as of the date of their publication and will be subject to change without prior notice. Past performance is not indicative of future performance. Estimates of

future performance are based on assumptions that may not be realized. The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially

different results. Opinions expressed herein may differ or be contrary to those expressed by other business divisions or other members of CMS Group as a result of using different assumptions

and/or criteria.

This document has been prepared without regard to the individual financial circumstances and investment objectives of the persons who receive it. Use of any information herein shall be at the

sole discretion and risk of the user. Investors are advised to independently evaluate particular investments and strategies, take financial and/or tax advice as to the implications (including tax) of

investing in any of the securities or products mentioned in this document, and make their own investment decisions without relying on this publication.

CMS Group may have a long or short position, make markets, act as principal or agent, or engage in transactions in securities of companies referred to in this document and may also perform

or seek to perform investment banking services or provide advisory or other services for those companies. This document is for the use of intended recipients only and this document may not

be reproduced, distributed or published in whole or in part for any purpose without the prior consent of CMS Group. CMS Group will not be liable for any claims or lawsuits from any third parties

arising from the use or distribution of this document. This document is for distribution only under such circumstances as may be permitted by applicable law. This document is not directed at you

if CMS Group is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. In particular, this document is only made available to certain US

persons to whom CMS Group is permitted to make available according to US securities laws, but cannot otherwise be made available, distributed or transmitted, whether directly or indirectly,

into the US or to any US person. This document also cannot be distributed or transmitted, whether directly or indirectly, into Japan and Canada and not to the general public in the People’s

Republic of China (for the purpose of this document, excluding Hong Kong, Macau and Taiwan).

Tuesday, November 10, 2015

To access our research reports on the Bloomberg terminal, type CMHK <GO> 21

Important Disclosures for U.S. Persons

This research report was prepared by CMS HK, a company authorized to engage in securities activities in Hong Kong. CMS HK is not a registered broker-dealer in the United States and,

therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This research report is provided for distribution solely to “major

U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Any U.S. recipient of this research report wishing to effect any transaction to buy or sell securities or related financial instruments based on the information provided in this research report

should do so only through Rosenblatt Securities Inc, 20 Broad Street 26th Floor, New York NY 10005, a registered broker dealer in the United States. Under no circumstances should any

recipient of this research report effect any transaction to buy or sell securities or related financial instruments through CMS HK. Rosenblatt Securities Inc. accepts responsibility for the contents

of this research report, subject to the terms set out below.

The analyst whose name appears in this research report is not registered or qualified as a research analyst with the Financial Industry Regulatory Authority (“FINRA”) and may not be an

associated person of Rosenblatt Securities Inc. and, therefore, may not be subject to applicable restrictions under FINRA Rules on communications with a subject company, public appearances

and trading securities held by a research analyst account.

Ownership and Material Conflicts of Interest

Rosenblatt Securities Inc. or its affiliates does not ‘beneficially own,’ as determined in accordance with Section 13(d) of the Exchange Act, 1% or more of any of the equity securities mentioned

in the report. Rosenblatt Securities Inc, its affiliates and/or their respective officers, directors or employees may have interests, or long or short positions, and may at any time make purchases

or sales as a principal or agent of the securities referred to herein. Rosenblatt Securities Inc. is not aware of any material conflict of interest as of the date of this publication.

Compensation and Investment Banking Activities

Rosenblatt Securities Inc. or any affiliate has not managed or co-managed a public offering of securities for the subject company in the past 12 months, nor received compensation for

investment banking services from the subject company in the past 12 months, neither does it or any affiliate expect to receive, or intends to seek compensation for investment banking services

from the subject company in the next 3 months.

Additional Disclosures

This research report is for distribution only under such circumstances as may be permitted by applicable law. This research report has no regard to the specific investment objectives, financial

situation or particular needs of any specific recipient, even if sent only to a single recipient. This research report is not guaranteed to be a complete statement or summary of any securities,

markets, reports or developments referred to in this research report. Neither CMS HK nor any of its directors, officers, employees or agents shall have any liability, however arising, for any

error, inaccuracy or incompleteness of fact or opinion in this research report or lack of care in this research report’s preparat ion or publication, or any losses or damages which may arise from

the use of this research report.

CMS HK may rely on information barriers, such as “Chinese Walls” to control the flow of information within the areas, units, divisions, groups, or affiliates of CMS HK.

Investing in any non-U.S. securities or related financial instruments (including ADRs) discussed in this research report may present certain risks. The securities of non-U.S. issuers may not be

registered with, or be subject to the regulations of, the U.S. Securities and Exchange Commission. Information on such non-U.S. securities or related financial instruments may be limited.

Foreign companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in effect within the United States.

The value of any investment or income from any securities or related financial instruments discussed in this research report denominated in a currency other than U.S. dollars is subject to

exchange rate fluctuations that may have a positive or adverse effect on the value of or income from such securities or related financial instruments.

Past performance is not necessarily a guide to future performance and no representation or warranty, express or implied, is made by CMS HK with respect to future performance. Income from

investments may fluctuate. The price or value of the investments to which this research report relates, either directly or indirectly, may fall or rise against the interest of investors. Any

recommendation or opinion contained in this research report may become outdated as a consequence of changes in the environment in which the issuer of the securities under analysis

operates, in addition to changes in the estimates and forecasts, assumptions and valuation methodology used herein.

No part of the content of this research report may be copied, forwarded or duplicated in any form or by any means without the prior consent of CMS HK and CMS HK accepts no liability

whatsoever for the actions of third parties in this respect.

Hong Kong

China Merchants Securities (HK) Co., Ltd.

Address: 48/F, One Exchange Square, Central, Hong Kong

Tel: +852 3189 6888 Fax: +852 3101 0828