company profile - max m. fisher college of business · web viewits 2003 revenue of 21,504 million...

TRANSCRIPT

Summary

This report is to estimate intrinsic value of Alcoa. First of all, to understand what makes this business tick and to know how Alcoa gets in its present shape, I tried to analyze the industry using Porter's Model. Then, as an attempt to gauge the company's operational efficiency and ability to generate profits, company financial statements were analyzed. Based on industry and company analysis, forecast and valuation were made through ReOI model and Monte Carlo simulation.

Valuation result is 22 dollars for normal case and 36 dollars for alumina shortage case. My recommendation based on the company's intrinsic value is WAIT until the middle of April because uncertainty related to alumina is too big right now.

Table of Contents

Page

1 Company Profile 32 Basic Market Data 33 Industry Analysis 44 Company Analysis 115 Forecast 166 Valuation 207 Recommendation 218 Accounting Quality 21

Appendices 1 ~ 17

1. Company Profile

2

Alcoa, since founded in 1888, has long been the world's leading producer of aluminum, fabricated aluminum and alumina. It controls more than 70 % of US primary production and produces about 17% of world primary aluminum production. Its 2003 revenue of 21,504 million is 58.5% of total combined revenue of other aluminum companies in North American continent including Alcan and secondary production companies.

The company is fully integrated through the whole value chain in the industry. Operating 41 countries, it is active in bauxite mining, refining, smelting, fabrication and recycling with significant investment in Brazil, Australia and China.

In 2002 US market and Europe market accounted for 63% and 21% of its revenue respectively. By industry sector, major markets are packaging and consumer (24.7%), automotive (13.3%), building and construction (10.8%) and aerospace (7.4%). By product segment, revenue from engineered products and flat-rolled products accounted for about 47% of total revenue.

Figure 11

Sales Change by Product

0

5000

10000

15000

20000

25000

1998 1999 2000 2001 2002

Sale

s (in

milli

on)

Alumina

Other

Packaging

Engineered

Flat Rolled

Primary Metal

2. Basic Market Data

▪ Share Price 37.39 (Feb.27,2004) ▪ Trailing PE 30.93▪ Shares Outstanding 868.49 Million ▪ Forward PE 14.90▪ Market Capitalization 32.47 Billion

▪ PEG Ratio (5yr exp) 1.59

▪ 52 week high/low 39.44 / 18.45 ▪ Price to Sales 1.5▪ Beta 0.878 ▪ Price to Book 2.69▪ Average Volume (3 5.35 Million ▪ % Held by insiders 1%

1 source: company annual reports

3

M)

▪ Ticker AA (NYSE)▪ % Held by Institution 80.21%

3. Industry Analysis

3-1 Supplier Power

Supplier power in aluminum industry is potentially huge. A recent dramatic example of supplier power was witnessed when US aluminum industry's output dropped by 28.1% in 2001 because of a hike in electricity price.

Electricity: Since electricity cost is the largest element of aluminum manufacturing production (above 20%), securing sources of low cost electricity is critical to aluminum producers. For example, Alcan has been known as the lowest cost producer because of its high level of electricity self sufficiency (about 62%), which is far higher than the industry average of 28%.2

Bauxite: Even though bauxite could be found almost everywhere, large scale commercial production is highly concentrated in a handful of mines in a few countries. In 2001, Australia, Jamaica, Brazil and Guinea produced 70% of total world production.

Alumina: Alumina refineries are built close to bauxite mines because refineries have to be tailored to particular ore characteristics of the mine and bauxite transportation is very costly ($22/ton). For that reason, alumina production is geographically concentrated as well. In addition, alumina from each refinery is different in particle characteristics and smelters prefer to use alumina from a single refinery. Possible shortage of alumina in 2004 and 2005 causes a lot of confusion for future aluminum prices. It will turn out that this report's final recommendation is up to future alumina supply demand balance.

To address potentially high supplier power, Alcoa is highly vertically integrated. Alcoa is the world largest raw material producer as well as the largest aluminum manufacturer, operating 2 stand alone bauxite mines, 9 refineries and 28 smelters and various sources of electricity worldwide.

Alcoa's recent distress was caused by rising electricity cost in US. Alcoa had to shut down smelters in Oregon and Texas in 2002, reduced production in North Carolina in 2002 and decided to idle some part of its facilities in the Pacific Northwest and New York State in 2003. 2 Alcan 2002 Annual Report

4

Alcoa's long term strategy should be to move smelter capacity to countries with low cost sources of electricity. Alcoa already dismantled Tacoma and Troutdale and decided to invest in a new smelter in Iceland and other hydroelectricity projects in Brazil. This transition process, in my opinion, will take more than a dozen years and will result in transforming the world aluminum industry as well as Alcoa and US aluminum market. Higher labor cost and increasing environmental cost will add impetus to this trend.

3-2 Customer Power

Customer power is disproportionately strong in aluminum industry. Major customers for aluminum producers are transportation (30%), packaging and containers (17%) and construction industry, which consist of relatively fewer numbers of major players.

Figure 23

US Shipment by End Users 2003

16.2%

37.8%8.2%

6.7%

6.2%

24.9%ConstructionTransportationConsumer DurablesElectricalMachineryPackaging

On the other hand, aluminum is basically a commodity and production differentiation is difficult. more significant is that some customers might choose a substitute such as plastic and steel when aluminum prices are too high.

Since customers tend to be gigantic manufacturers, they usually want to secure long term large quantity contracts. No aluminum producer can afford to lose those big customers because refineries and smelters can not even temporarily shut down without incurring huge cost. This lack of manufacturing flexibility and extreme amount of fixed cost often forces companies to operate under their cost curve.

3 The Aluminum Association

5

Alcoa appears to have competitive advantage in dealing with customer power. Its size and financial stability has made itself one of favorites of big customers who need long term contracts. With increased practice of long term contracts Alcoa started using derivatives such as futures and options for hedging purpose.

Strategic motives behind Alcoa's recent acquisitions of Alumax, Reynolds, Cordant and many others can be seen from various angles. However, one possible interpretation is to see them as an attempt to balance customer power through consolidation in US aluminum industry. For example, after the company acquired Reynolds, which dominated aluminum packaging market, in 2000, it acquired Ivex Packaging Corp. in 2002, allowing it to enter plastic packaging market to, in my view, maximize its market power in packaging industry.

3-3 Substitute

Aluminum competes with other metals for various end users. Competition exists in packaging (glass, paper, plastics and steel), construction (composites, steel and wood), transportation (magnesium, titanium and steel) and electrical application (copper).

New application of aluminum or a competitor, relative price change among competing materials, technological breakthrough in usage of a material, and introduction of new material can make significant effect on competing dynamics among metals.

Alcoa has traditionally been addressing this issue by investing in R&D. Recently the company showed its unusual enthusiasm for entering substitutes market by acquiring Ivex Packaging Corp. in 2002, entering the thermoformed plastics and plastic extrusions markets. In the same year, Alcoa Fujikura Ltd became sole owner of Engineered Plastic Components, Inc., a supplier of automotive precision-molded components and assembles.

Due to various causes including weakening dollar and increasing Chinese demand, metal prices hiked in 2003 while aluminum was one of the weakest performers. Surprisingly, price difference between aluminum and competing metals are at highest level during the scope of this report, 1987~2003 as depicted in Figure 3. I expect that aluminum will substitute for other metals in some instances. Further discussion will be made in Forecast Section.

6

Aluminum, Copper & Nickel

0

500

1000

1500

2000

2500

3000

3500

Jan-01Jul-01 Jan-02Jul-02Jan-03 Jul-03Jan-04

Alumi

num/

Copp

er

020004000600080001000012000140001600018000

Nick

el AluminumCopperNickel

3-4 Entry / Exit / Expansion Barrier

It is very difficult for a new firm to enter aluminum industry. First, The industry is prohibitively capital intensive. Required capital to build a standard size smelter (250,000 tons) is estimated far above 1 billion dollars (Alcoa has 28 smelters). Second, existing producers preoccupy critical resources. A new producer, if it wants to be vertically integrated, needs to find, for example, commercially viable bauxite mines, almost all of which are already owned by existing producers. Third, mini-mills do not have competitive advantages in aluminum industry. In steel industry, better efficiency of mini-mills drove steel giants to a corner. Aluminum mini-mills lack the technology to make high quality can sheet, which is most lucrative market in the industry.

However, outside North America, many aluminum producers are government owned. Pechiney, recently acquired by Alcan, in France was wholly owned by its government and Norwegian government holds 51% of Norsk Hydro. In case, as it has been, a government wants to produce aluminum for as part of industrial development program or for national security purpose, entry barriers mentioned above can be abated significantly. Government intervention has contributed to a chronic problem in aluminum industry in that higher cost producers could stay with government subsidy.

Incumbent producers have not found an easy way to expand and grow in the aluminum industry. Besides tremendous required capital for expansion, possibility of overcapacity has hindered companies to expand fast. As a result, Alcoa has sought to expand through acquisition of existing companies and brown field projects. In fact, Alcoa has not invested in a new smelter for the past 20 years. It, in my

7

view, resulted in higher maintenance cost and decrease in asset efficiency. This issue will be revisited in Company Analysis section.

3-5 Competition

Competition in aluminum industry is potentially very high. It stems mainly from two factors. First, aluminum is a commodity, for which product differentiation is hard to come by. Second, aluminum producers are basically price takers as prices are set by supply-demand balance in London Metal Exchange. However, lack of flexibility in assets and output, long lead time to add new capacity and the huge required capital imply that a company can not encroach on others' market share without risking prohibitively costly punishment by prolonged overcapacity and plummeting prices.

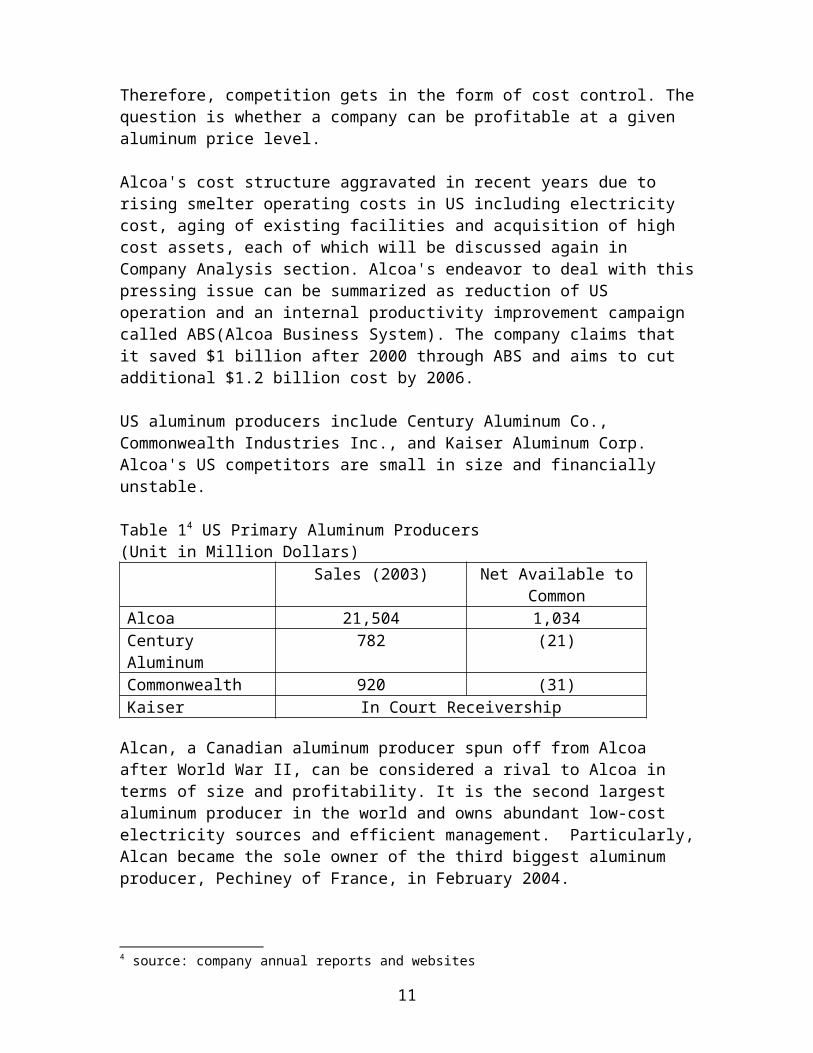

Therefore, competition gets in the form of cost control. The question is whether a company can be profitable at a given aluminum price level.

Alcoa's cost structure aggravated in recent years due to rising smelter operating costs in US including electricity cost, aging of existing facilities and acquisition of high cost assets, each of which will be discussed again in Company Analysis section. Alcoa's endeavor to deal with this pressing issue can be summarized as reduction of US operation and an internal productivity improvement campaign called ABS(Alcoa Business System). The company claims that it saved $1 billion after 2000 through ABS and aims to cut additional $1.2 billion cost by 2006.

US aluminum producers include Century Aluminum Co., Commonwealth Industries Inc., and Kaiser Aluminum Corp. Alcoa's US competitors are small in size and financially unstable.

Table 14 US Primary Aluminum Producers(Unit in Million Dollars)

Sales (2003) Net Available to Common

Alcoa 21,504 1,034Century Aluminum

782 (21)

Commonwealth 920 (31)Kaiser In Court Receivership

Alcan, a Canadian aluminum producer spun off from Alcoa after World War II, can be considered a rival to Alcoa in terms of size and profitability. It is the second largest aluminum producer in the world 4 source: company annual reports and websites

8

and owns abundant low-cost electricity sources and efficient management. Particularly, Alcan became the sole owner of the third biggest aluminum producer, Pechiney of France, in February 2004.

Table 25 World Leading Aluminum Producers(Unit in Million Dollars)

Sales (2003) Net Available to Common

Alcoa 21,504 1,034Alcan (Canada) 13,640 283Pechiney (France) 13,314 (546)

As already mentioned either company could not influence the other's market share without investing hugely in new capacity, which would be prohibitively risky and costly attempt. Rather the two companies will focus on cost cutting to be more profitable at foreseeable market prices. Another possibility is tacit collusion between the two dominants to affect market price since the combined primary production capacity of the two is estimated to be about 35% of world primary capacity.

3-6 Market Size and Growth

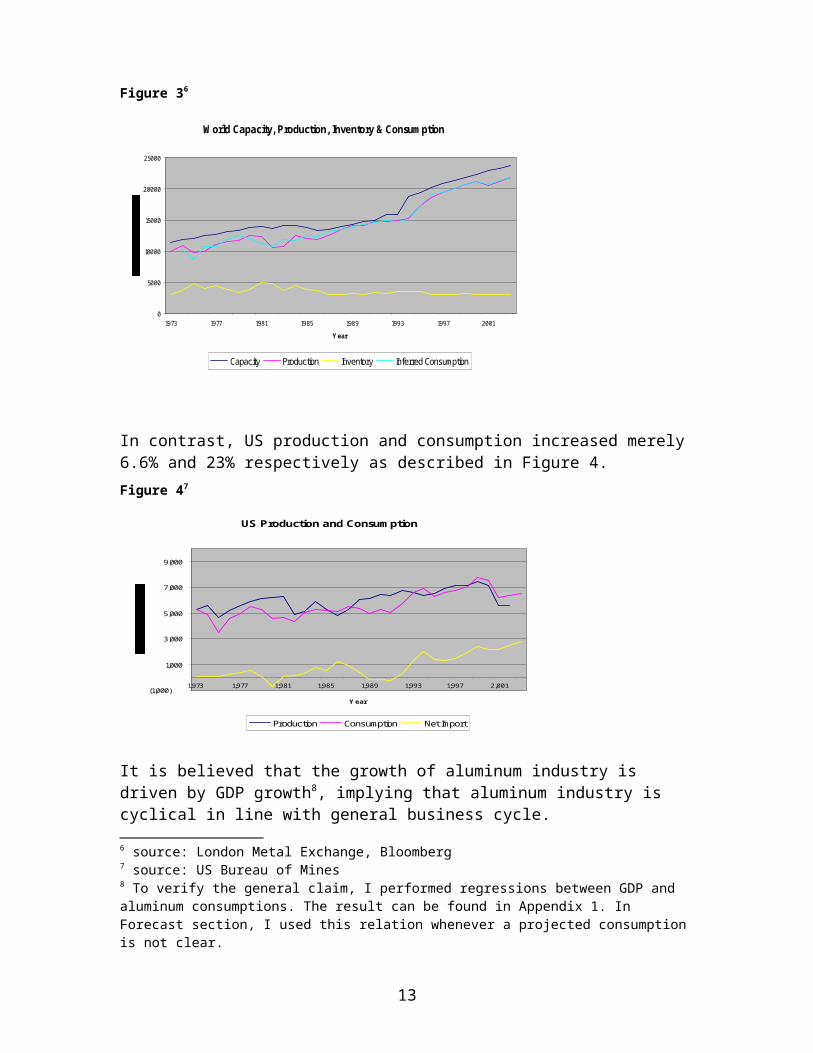

World capacity, production and consumption have grown more than 200% during 1973-2003 periods as shown Figure 1.

Figure 36

World Capacity, Production, Inventory & Consumption

0

5000

10000

15000

20000

25000

1973 1977 1981 1985 1989 1993 1997 2001Year

Capacity Production Inventory Inferred Consumption

In contrast, US production and consumption increased merely 6.6% and 23% respectively as described in Figure 4.

5 source: company annual reports and websites6 source: London Metal Exchange, Bloomberg

9

Figure 47

US Production and Consumption

(1,000)

1,000

3,000

5,000

7,000

9,000

1,973 1,977 1,981 1,985 1,989 1,993 1,997 2,001

Year

Production Consumption Net Import It is believed that the growth of aluminum industry is driven by GDP growth8, implying that aluminum industry is cyclical in line with general business cycle.

Aluminum prices have relatively been stable through the last 100 years. Using US physical spot price for the period of 1900 – 2003, I found standard deviation of yearly change is mere $0.088 per pound. If we exclude years affected by supply or demand shocks such as world wars and oil shocks, then standard deviation can be as low as $0.044 per pound.

7 source: US Bureau of Mines 8 To verify the general claim, I performed regressions between GDP and aluminum consumptions. The result can be found in Appendix 1. In Forecast section, I used this relation whenever a projected consumption is not clear.

10

Figure 5

Triang(-0.26636, 0.0027000, 0.40625)

0

1

2

3

4

5

6-0

.3

-0.2

-0.1 0.0

0.1

0.2

0.3

0.4

0.5

1.2% 7.9%90.9%-0.2200 0.2600

BestFit Student VersionFor Academic Use Only

Using BestFit, distribution of price changes during the last 36 years is found as a triangle distribution (-0.22, 0.0027, 0.26) with exclusion of outliers caused by oil shocks.

This distribution will be used to estimate future aluminum prices in Forecast section.

Figure 6 describes price movement from 1987 to 2003. After fluctuation of late 1980s and early 1990s that was caused by CIS producers, prices stabilized since mid 1990s

Figure 6

Aluminum Price (1987-2003)

1,000

1,500

2,000

2,500

1,987 1,991 1,995 1,999 2,003

LME

3 M

onth

s/M

etric

ton

4. Company Analysis

4-1 Overview

The overall performance of Alcoa and important market factors for the period of 1987 to 2003 are shown in Figure 79 for profitability and 8 for growth.9 In calculating ROCE for 1992, I did not include accounting charge related to the restructuring of retirement benefits. Appendix 2 is to show the effect of the accounting charge of $1,162 million to Figure 1 and regression result.

11

Figure 7

Aluminum Price vs Alcoa ROCE

0.200.300.400.500.600.700.800.901.001.101.20

1987 1991 1996 2000

LME

Pric

e

-20.0%

0.0%

20.0%

40.0%

ROCE

Aluminum Price ROCE

Figure 7 describes that Alcoa's profitability fluctuated as aluminum prices moved as commonly expected. Through the 17 year period, Alcoa recorded an average of 11.3% of ROCE.10 Figure 8

GDP, US Demand & Aloca Shipment

0

2000

4000

6000

8000

10000

1987 1991 1995 1999 2003

Met

ric to

ne

80100120140160180200220

US G

DP G

row

th

US Consumption Alcoa Shipment US GDP

The company grew solidly during that period in spite of setbacks in early 1990s and recent years. Its shipment increased 1.28 times from 2.2 million metric tones to 5.05 million metric tones with average annual growth rate of 5.75%.

4-2 Financial Statement Analysis

4-2-1 Common Size Analysis / Trend Analysis / Ratio Analysis

Discussion of implications from patterns to be revealed through these analyses will be incorporated in profitability analysis and growth analysis section.10 9.1% if the accounting charge in 1992 is included.

12

As you can find in Appendix 3, 4 and 5, common size analysis and trend analysis reveals apparently deteriorating patterns in almost all aspects. Most conspicuous are the following four patterns. First, long-term debt is increasing too fast even though the company reduced it by large amount in 2003. Second, growth rate of share holders' equity far exceeds that of retained earnings. Third, growth rate of PPE is deteriorating while goodwill gets to account for more portions of total assets. Fourth, the company pays less proportion of tax out of operating income with years. Even though a few patterns related to income items are shown but they are not apparent.

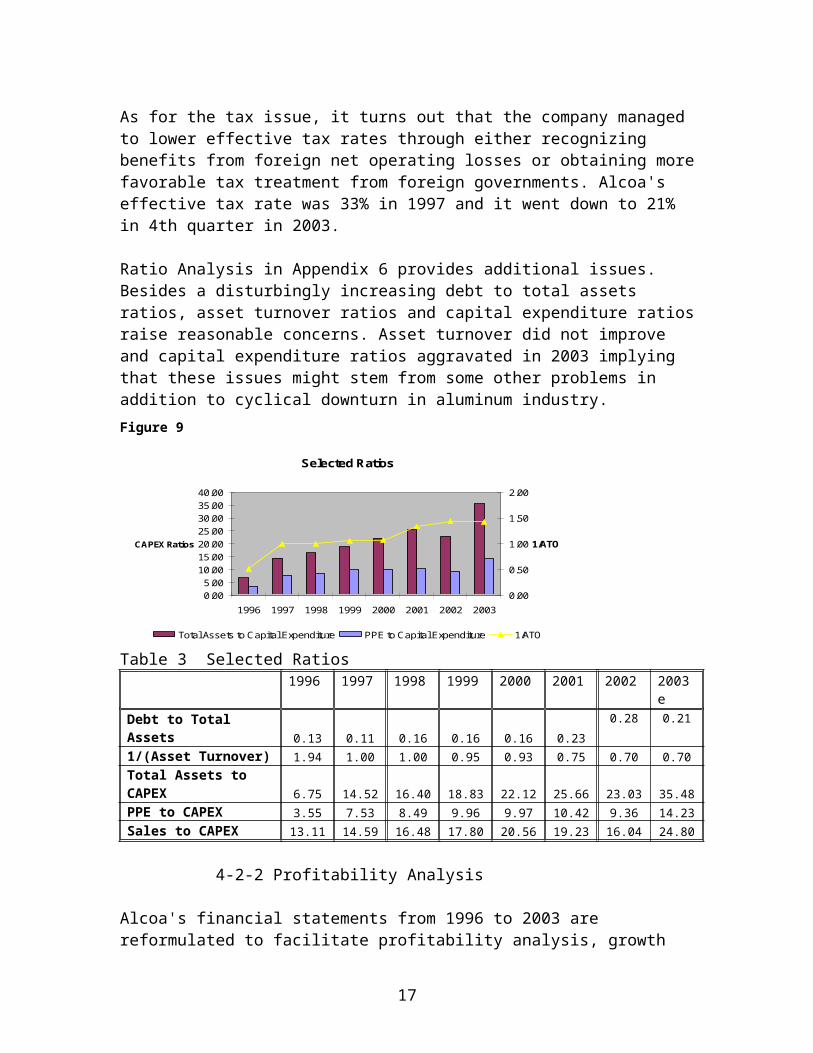

As for the tax issue, it turns out that the company managed to lower effective tax rates through either recognizing benefits from foreign net operating losses or obtaining more favorable tax treatment from foreign governments. Alcoa's effective tax rate was 33% in 1997 and it went down to 21% in 4th quarter in 2003.

Ratio Analysis in Appendix 6 provides additional issues. Besides a disturbingly increasing debt to total assets ratios, asset turnover ratios and capital expenditure ratios raise reasonable concerns. Asset turnover did not improve and capital expenditure ratios aggravated in 2003 implying that these issues might stem from some other problems in addition to cyclical downturn in aluminum industry.Figure 9

Selected Ratios

0.005.00

10.0015.0020.0025.0030.0035.0040.00

1996 1997 1998 1999 2000 2001 2002 2003

CAPEX Ratios

0.00

0.50

1.00

1.50

2.00

1/ATO

Total Assets to Capital Expenditure PPE to Capital Expenditure 1/ATO

Table 3 Selected Ratios1996 1997 1998 1999 2000 2001 2002 2003

eDebt to Total Assets 0.13 0.11 0.16 0.16 0.16 0.23

0.28 0.21

1/(Asset Turnover) 1.94 1.00 1.00 0.95 0.93 0.75 0.70 0.70Total Assets to CAPEX 6.75 14.52 16.40 18.83 22.12 25.66 23.03 35.48PPE to CAPEX 3.55 7.53 8.49 9.96 9.97 10.42 9.36 14.23Sales to CAPEX 13.11 14.59 16.48 17.80 20.56 19.23 16.04 24.80

13

4-2-2 Profitability Analysis

Alcoa's financial statements from 1996 to 2003 are reformulated to facilitate profitability analysis, growth analysis and forecast as you can see Appendix 7 and 8. Appendix 9 and 10 shows common size analysis and trend analysis from reformulated statements. Insights from those analyses are incorporated in the following profitability analysis and growth analysis. Table 6 summarizes profitability analysis.

Table 62003 2002 2001 2000 1999 1998 1997

Return on Common Equity (ROCE) 15.90% 0.79% 5.80% 15.49% 13.20% 16.49% 13.43%Return on Net Operating Asset(RNOA) 10.76% 1.54% 4.75% 11.74% 10.50% 13.73% 12.13%

Financial Leverage DriversNet Borrowing Cost (NBC) 2.32% 2.74% 2.89% 4.48% 3.63% 5.13% 6.27%SPREAD 8.45% -1.21% 1.86% 7.26% 6.87% 8.60% 5.87%Financial Leverage (FLEV) 0.608 0.621 0.565 0.516 0.393 0.321 0.221

Operating Liability Leverage DriversReturn on operating assets(ROOA) 8.17% 2.14% 3.61% 9.34% 7.70% 9.72% 8.46%Short term borrowing rate (after tax) 3.44% 3.39% 1.61% 4.26% 3.29% 3.57% 3.64%Operating Leverage SPREAD 4.72% -1.25% 2.00% 5.08% 4.41% 6.15% 4.82%Operating Liability Leverage (OLLEV) 0.505 0.504 0.487 0.494 0.561 0.631 0.690

Next LevelsProfit Margin 9.85% 1.42% 4.09% 8.09% 6.81% 7.85% 6.58%Core Sales PM 7.83% 7.42% 10.07% 13.54% 11.76% 10.78% 11.14%Sales PM 0.055 0.054 0.073 0.088 0.080 0.070 0.068Gross Margin Ratio 0.203 0.198 0.220 0.245 0.232 0.222 0.229Operating Expense Ratio 0.125 0.124 0.120 0.109 0.114 0.114 0.117Operating Tax Ratio 0.024 0.020 0.028 0.047 0.037 0.037 0.043Other Operating Income Ratio 0.044 -0.040 -0.032 -0.007 -0.012 0.008 -0.003

1/Asset Turnover 0.915 0.921 0.861 0.689 0.648 0.572 0.542Receivables Turnover 0.128 0.130 0.127 0.107 0.117 0.117 0.118Inventory Turnover 0.115 0.119 0.113 0.095 0.107 0.104 0.104PPE Turnover 0.574 0.583 0.542 0.485 0.560 0.515 0.516Goodwill Turnover 0.300 0.295 0.258 0.162 0.084 0.062 0.018Accounts Receivable Turnover 0.084 0.078 0.076 0.068 0.069 0.060 0.060R $ PR Cost Turnover 0.150 0.164 0.156 0.131 0.144 0.149 0.164Other noncurrent Liabilities 0.146 0.120 0.091 0.079 0.094 0.093 0.093Other Turnovers 0.178 0.155 0.144 0.119 0.087 0.077 0.103

The analysis provides clear insights on the company's profitability. While the company appears to have come back to impressively high level of ROCE, it was largely due to increased financial leverage and further reduced net borrowing cost, not due to improved operation.

The company's core ability to generate profits from sales as reflected in core sales profit margin numbers have kept deteriorating over time. ATO seems to have troubles in recent years. Individual profit margins

14

and turnovers generally have gotten worse except accounts receivable turnover.

Figure 10

ROCE, FLEV & NBC

-5.00%

10.00%

25.00%

40.00%

55.00%

70.00%

1997 1998 1999 2000 2001 2002 2003

Net Borrowing Cost (NBC)

Financial Leverage (FLEV)

Return on Common Equity (ROCE)

Figure 11

Core Sales PM & ATO

-2.00%

2.00%

6.00%

10.00%

14.00%

18.00%

1997 1998 1999 2000 2001 2002 2003

Cor

e Sa

les

PM

0.000

0.500

1.000

1.500

2.000

2.500

1/AT

O

Core Sales PM Asset Turnover

In other words, whereas ROCE has moved in line with aluminum price and other market factors as discussed in overview section of company analysis, its profit generating ability has decreased over time. It is worth noting that profit margin in 2003 is a historical high of 9.85% while core sales profit margin is just 7.83%. It was caused by abnormally high gains from unusual items such as currency translation and available for sale securities, not from its core operations.

It is not easy to detect what might have caused it because almost all indicators moved in one direction together. Fluctuation of aluminum prices can not fully explain the disturbing fact because prices in recent several years were very stable and prices in 2003 were higher than those in 1998 and 1999.

However, the pattern of deterioration gives a clue to understand this issue. Two turning points in the pattern appear to be 1998 and 2000, in which the company acquired Alumax and Reynolds respectively. I conjecture that troubles caused by the acquisitions should be one part of explanation.

4-2-3 Growth Analysis

To measure of return for shareholders and a company's ability to grow, I am going to look into the company's residual earnings during the years between 1996 and 200311.11 Residual earnings as (ROCE-Cost of Equity Capital)*CSEt-1

15

Cost of equity capital and beta for Alcoa for the period of 1996 to 2003 are shown in table 7.12

Table 4 Yearly Change of Risk-Free and Beta

Year Risk-Free Beta1996 0.064 0.4641997 0.064 0.9121998 0.053 0.6711999 0.056 0.3882000 0.060 0.4182001 0.050 1.3902002 0.046 1.2982003 0.040 1.282

In Appendix 11, I assumed three scenarios. In the first scenario I used changing risk free rates and betas from Table 7. Constant beta of 0.878 was used for the second scenario. For the third scenario constant cost of equity capital of 10.69% was assumed with constant risk free rate of 5.42% and beta of 0.878. Risk premium of 6% was used throughout all of the three scenarios.

Results show that the company made negative residual earnings in two scenarios and earned negligible positive residual earnings in a scenario. In sum, the company does not appear to have earned residual earnings over the past 7 year period. Given the low interest rates in the period, it is quite disappointing. Fluctuation of growth rates of residual earnings is surprisingly large and big negative growth occurred, in all three scenarios, in 2000 and 2001. This analysis provides evidence that whereas Alcoa achieved solid growth of CSE and other items through the acquisitions, the acquired assets might not be properly functioning.

4-2-4 Interpretation

My hypothesis is that the company's operating efficiency and ability to generate profit were damaged by a series of acquisitions, idling capacity and aging facilities. Patterns observed above indicate that the company had to borrow hugely to finance the acquisitions affecting debt ratio and FLEV. However, unfortunately, the acquired assets had higher cost structure resulting in lower core sales pm. On top of it, packaging market, which Reynolds serves, was struggling since 2001, aggravating the situation. Perhaps organizational turmoil in Reynolds and Alumax worsened their performance, losing core customers, suppliers, distributors or important employees.

Idling capacity, which still consumes a certain level of cost, definitely must have driven down efficiency ratios and core sales pm. A large scale of layoffs since 2000 might have discouraged employees, 12 Risk free rates are from 10 year US Treasury bond rates. Betas come from regressions with S&P as benchmark. For how the data was used, see Appendix 10.

16

lowering productivity. Rising electricity cost and employee benefit cost must have added some negative influence.

Alcoa wanted to start investing heavily in long term assets to maintain long term capacity and efficiency because its assets started showing aging effects13. However, the company had been in financial constraints due to a series of acquisitions and therefore capital expenditure was restrained, pushing CAPEX ratios high to the ceiling.

Fortunately, net borrowing costs had stayed low and FLEV was high and aluminum prices started to recover from 2002 low. Furthermore, the economy started picking up with weakening US dollar and soaring stock market. As a result, the company could show a good ROCE and PM numbers in 2003.

My next question is whether the damage to efficiency and margin is permanent or temporary. To answer to the question, I will need interviews with Alcoa officials and additional information. For now, I will assume that the company will gradually recover from the damage for the coming 5 years.

5. Forecast

As in many cases in valuation, it is inevitable to make a lot of assumptions. Particularly I face two serious obstacles. First, I will assume that Alcoa does not acquire other companies. This is problematic because companies in this industry grow through acquisitions. Increasing capacity with green field projects is extremely risky and costly in aluminum industry. However, it is more difficult to project when and which company Alcoa will acquire. Second problem stems from future aluminum price. Predicting a mid to long term aluminum price is as tricky as predicting a stock price. As a result I will use industry consensus projections for 2004 and 2005 and try random simulation for the period of 2006 to 2008 basing on historical data.

5-1. Sales Forecast

5-1-1 Price Forecast

The O'Carroll Aluminum Bulletin estimate will be used for 2004 and 2005 with a moderate modification to incorporate substitute effect. The source is said to be one of a few to estimate supply and demand through bottom up approach. Its projection of supply-demand balance and prices is summarized as below.13 Average age of Alcoa's smelters is over 25 years in my calculation including acquired assets.

17

Table 5 Price ForecastProjection for 2004 and 2005 Changes in Smelter Capacity (Western World)

2003 2004 2005 2004 2005US 0 0

Projected World Consumption 27,300 29,234 31,077 Canada 2 148% Change 7.1% 7.1% 6.3% Latin America 55

Western Europe 130 52Projected World Production 27,868 28,948 30,253 Africa 117 50

% Change 7.3% 3.9% 4.5% Asia 199 347Oceania 35 31

Projected World Capacity 31,135 32,073 33,666 Western World 538 628% Change 5.4% 3.0% 5.0%

Source: The O'Carroll Aluminum BulletinCapacity Utilization % 91.9% 91.6% 92.0%

Implied Inventory Change 568 (286) (824)

Price 0.65 0.73 0.77Price (Alumina Shortage) 0.65 0.76 0.88

Source: The O'Carroll Aluminum Bulletin

However, it appears that they did not incorporate possibility of substitute effect. As discussed in Industry Analysis section, prices of metals such as copper, steel and nickel have spiked while aluminum prices have relatively been stable. Current difference between aluminum and other metals is at historical highest within the scope of my study, 1987 ~ 2003. On top of it, prices of other metals are expected to go up further in, at least, coming a few years14. I expect other metals will be replaced with aluminum in a wide range of industries centering on small businesses, low value product users and, especially, easy switching sectors. Consequently I conjecture for 2004 and 2005 that approximately additional 4% demand increase for aluminum will be generated from electric equipment market (for wiring / replacing copper), packaging industry (for steel cans and closures / replacing ordinary steel), automotive (for ordinary steel components) and construction (for corrosion resistance / replacing nickel and galvanized steel), expecting 0.77 (0.82 in case of alumina shortage) for 2004 and 0.80 (0.90 in case of alumina shortage) for 2005.

It is very controversial if there will be an actual alumina shortage. Some market observers claim that alumina shortage has begun in reference to alumina prices at spot market. However, considering spot market buyers are mostly Chinese manufacturers, who in many cases buy large amount of raw materials to stock for future usage, others believe that the shortage, if any, will be temporal. I attached alumina supply demand forecast prepared by The O'Carroll Aluminum Bulletin as Appendix 14.

14 See Appendix 12 for Forecasted Supply Demand Balance for copper, nickel and zinc.

18

For prices after 2005 my projection is based on historical data. I used BestFit program to find distribution pattern of price movements during the past 36 years as shown in Industry Analysis section. The result is used as input data for Monte Carlo simulation.

5-1-2 Shipment and Unit Price Forecast

Market estimate per product line is attached as Appendix 1315.

Increasing shipment is largely due to Boeing's increased orders, recovery of autos and trucks, and electrical equipment. While it is generally estimated that electrical industry is likely to struggle due to lack of new investment, I believe some copper users, especially in wiring and appliance, will switch to aluminum in 2004 and 2005. Packaging market is forecast to be stagnant and modest growth is predicted for consumer durables. From the market forecast mentioned above, I prepared Alcoa's shipment and unit price forecast per product line as shown Table 6. I assume that, as prices spike in 2004 and 2005, Alcoa restarts some of its idling capacity of 595 thousand metric tones.

I considered the scheduled addition of a new smelter capacity of 322 kmt in 2007 and expansion of Quebec smelter. For unit price for packaging line, possibility of introduction of new consumer products with higher margin was incorporated.

5-2. Core Sales PM and Asset Turnover

My main idea was that, even though absolute numbers are likely to be very good in 2004 and 2005 thanks to high aluminum prices, in relative measure the company's core sales pm will be equivalent to 2003 level, improving a little in 2007 and 2008 as new low cost capacity comes on stream, high cost capacity in US is dismantled and other troubles are dissolved.

A problem was caused by the fact that I could not obtain information about Alcoa's variable cost structure. I used industry data from mid 1990s16. For simplicity purpose, I assumed only two point estimations of core sales pm in every year forecasted. However, in reality, it should be continuous, not discrete. Electricity price, which is rising almost everywhere over the world, was assumed constant mainly because of lack of data.

15 Source: The O'Carroll Aluminum Bulletin and various trade associations such as The Aluminum Association, Wards Automotive, United Brewers Association and others.16 Some professional organizations sell updated industry cost data.

19

The company's asset efficiency to generate sales is expected to be a little higher in 2004 and 2005 with return of some of idle capacity. It is likely to show moderate improvement in 2007 and 2008 with addition of new efficient capacity and dismantlement and divestiture of less efficient assets.

Table 6 Forecast of Shipment and Unit Price per Product Line2003 2004 2005 2006 2007 2008

Aluminum Price 0.7 0.82 0.8 0.8072 0.8130 0.8175

Capacity 3345 3645 3645 3645 3967 3967Idle Capacity 595 295 295 295 150 0

Add on New Capacity 322Shipment 5047 5194 5440 5546 5915 6005Unit Price 1.937 2.073 2.064 2.031 1.855 1.823

Unit Added Value 1.237 1.253 1.264 1.224 1.043 1.005Sales 21504 23691 24703 24782 24146 24084

Primary MetalShipment 1952 1850 1900 1900 2181 2181Unit Price 0.752 0.820 0.800 0.807 0.813 0.818

Unit Added Value 0.052 0.000 0.000 0.000 0.000 0.000Sales 3229 3337 3344 3374 3901 3923

Flat RolledShipment 1819 1946 2044 2095 2147 2201Unit Price 1.203 1.350 1.330 1.337 1.343 1.348

Unit Added Value 0.503 0.530 0.530 0.530 0.530 0.530Sales 4815 5781 5980 6162 6344 6524

Engineered ProductShipment 879 984 1063 1106 1133 1162Unit Price 2.890 3.320 3.300 3.307 2.813 2.618

Unit Added Value 2.190 2.500 2.500 2.500 2.000 1.800Sales 5589 5415 5848 6082 4987 4601

PackagingShipment 167 165 165 170 170 170Unit Price 8.751 8.870 8.850 8.857 10.813 10.818

Unit Added Value 8.051 8.050 8.050 8.050 10.000 10.000Sales 3215 2922 2922 3011 3740 3740

OthersShipment 230 248 268 276 284 292Unit Price 5.245 8.820 8.800 7.807 6.813 6.818

Unit Added Value 4.545 8.000 8.000 7.000 6.000 6.000Sales 2654 4820 5194 4737 4250 4372

AluminaShipment 7671 7700 7700 7700 7700 7700Unit Price 0.119 0.184 0.184 0.184 0.120 0.120

Unit Added ValueSales 2002 1416 1416 1416 924 924

World Real GDP Growth 2.63 2.69 2.81 2.78 2.76Developed Country Real GDP Growth 1.63 1.81 2.03 2.02 2.03US Real GDP Growth 1.50 1.90 2.50 2.50 2.50

5-3. Cost of Operating Capital and ReOI Growth Rate

20

The company's cost of operating capital in 2003 is estimated as 9.145% with risk free rate of 4.95% (10 year Treasury bond rate), beta of 0.878, market premium of 6%, and borrowing rate of 6.6%. Since it is very likely that risk free rates will rise in the near future, I set 10% as default for Alcoa's cost of operating capital. The effect from the company's repayment of debt will be offset by rising borrowing rates. Valuation incorporates sensitivity analysis for cases with different cost of operating capital from 9.15% to 14%.

Given the wild fluctuation of ReOI in the studied period, which might not be a typical cycle for aluminum industry, it is very hard to estimate long term ReOI for Alcoa. I assume Alcoa's long term ReOI to range from 2% to 3%.

6. Valuation (with Monte Carlo Simulation)

Input list is attached as Appendix 15. Below is Monte Carlo simulation model for valuation.

Table 7 Valuation Model (ReOI with Monte Carlo)

2003 A 2004E 2005E 2006E 2007E 2008E

Sales 21,504 23,691 24,703 24,782 24,146 24,084Growth in Sales 10.2% 4.3% 0.3% -2.6% -0.3%

Core Sales PM 0.125 0.115 0.115 0.13 0.131/ATO 0.75 0.78 0.75 0.7 0.65ReOI 468 1,185 914 991 1,449 1,565

Growth in ReOI 153.1% -22.8% 8.5% 46.1% 8.1%

Cost of Operating Capital 0.0915 0.1000 0.1000 0.1000 0.1000 0.1000Discount Rate 0.1000 0.8264 0.7513 0.6830 0.6209PV of ReOI 118.5 755.4 744.8 989.5 972.0Total PV 3,580Continuing Value 24,927PV of CV 15,478NOA 2003 20,050 Cost of Operaqting Capital after 2008Value of NOA 39,108 0.1000NFO 6750 ReOI Growth RateV 2003 32,358 0.035Value per share(at 868.49 million) 37.26

Valuation Result and Sensitivity Analysis

At 10% of cost of operating capital, valuation result is 22 dollars in normal case and 36 dollars in alumina shortage case. For summarized result of simulations, see Appendix 16 and 17.

21

Distribution of output and input sensitivity for the default case are depicted as follows;

15 25 35 45

5% 90% 5% 19.8981 41.1871

Mean=30.46991

Distribution for Value per share / 2003 A/J23(Sim#1)

0.0000.0100.0200.0300.0400.0500.0600.0700.0800.0900.100

Mean=30.46991

15 25 35 45

@RISK Student VersionFor Academic Use Only

Regression Sensitivity for Value per share /2003 A/J23 ...

Std b Coefficients

0

1

2

3

4

Unit Added Value / 2004/C33 .066

Aluminum Price / 2006/E6 .068

Aluminum Price / 2005/D6 .144

Aluminum Price / 2008/G6 .817

@RISK Student VersionFor Academic Use Only

-1 -0.75 -0.5 -0.25 0 0.25 0.5 0.75 1

Valuation result varies depending on cost of operating capital as follows;

Cost of Capital Mean Normal Case Alumina Shortage

10% (Default) 30.47 22 37.59.15%

(present)35 25 45

11% 26.37 19.5 3312% 23.22 17.8 28.413% 20.71 15.6 25.214% 18.68 14.2 22.4

7. Recommendation17

Current price of 37.39 is appropriate if we assume alumina shortage will come to existence in 2004 and 2005, which is quite uncertain at present. Accordingly I recommend that you wait until alumina issue is clarified in a couple of months. I expect that the issue will be cleared when Alcoa and Alcan issue their first quarter result in the middle of April.

17 I made a lot of assumptions in estimating Alcoa's intrinsic value. Therefore, attention should be paid to any deviation from my assumptions such as interest rate change, electricity price, major end users' trend, other metals' price movement and many others. If any deviation happens, the intrinsic value should be re-estimated.

22

8. Accounting Quality

Since the most of information I used for this report came from the company's financial statements, I checked accounting quality of Alcoa using Beneish 5 and 8 variables models. The result is as follows;The Full Beneish model for earnings manipulation detection (Based on Eight Variables)

Year 2002 2001 2000 1999 1998 1997 1996INPUT VARIABLES

Net Sales 20,263 22,497 22,659 16,323 15,340 13,319 13,061 CGS 16,247 17,539 17,111 12,536 11,933 10,275 9,966 Net Receivables 2,378 2,386 3,461 2,199 2,163 1,581 1,675 Current Assets (CA) 6,313 6,449 7,578 4,800 5,025 4,416 4,281 PPE (Net) 12,111 11,530 12,850 9,133 9,133 6,667 7,078 Depreciation 1,108 1,234 1,199 888 842 735 747 Total Assets 29,810 28,355 31,691 17,066 17,463 13,071 13,450 SGA Expense 1,147 1,256 1,088 851 783 682 709 Net Income (before Ext. Items) 420 908 1,484 1,054 853 805 515 CFO (Cash flow from op.) 1,839 2,411 2,851 2,236 2,197 1,888 1,887 Current Liabilities 4,461 4,885 7,954 3,003 3,268 2,453 2,373 Long-term Debt 8,365 6,384 4,987 2,657 2,877 1,457 1,690

DERIVED VARIABLESOther L/ T Assets [TA-(CA+PPE)] 11,386 10,376 11,263 3,133 3,305 1,988 2,091

DSRI 1.1065 0.6944 1.1338 0.9554 1.1879 0.9258 #REF!GMI 1.1120 1.1110 0.9475 0.9573 1.0290 1.0368 #REF!AQI 1.0438 1.0296 1.9359 0.9701 1.2441 0.9782 #REF!SGI 0.9007 0.9929 1.3882 1.0641 1.1517 1.0198 #REF!

DEPI 1.1534 0.8828 1.0383 0.9526 1.1764 0.9614 #REF!SGAI 0.9863 0.8600 1.0858 0.9791 1.0032 1.0601 #REF!

Total Accruals/ TA -0.0476 -0.0530 -0.0431 -0.0693 -0.0770 -0.0829 -0.1020LVGI 1.0826 0.9732 1.2313 0.9424 1.1766 0.9901 #REF!

M = -6.065+ .823 DSRI + .906 GMI + .593 AQI + .717 SGI + .107 DEPIM-score (5-variable model) -2.76 -3.07 -2.02 -2.97 -2.47 -2.95 #REF!

M = -4.84 + .920 DSRI + .528 GMI + .404 AQI + .892 SGI + .115 DEPI -.172 SGAI + 4.679 Accrual to TA - .327 LeverageM-score (8-variable model) -2.62 -2.93 -1.95 -2.81 -2.46 -2.92 #REF!Note: if M > -2.22, firm is likely to be a manipulator

The result indicates that the company might have manipulated earnings in 2000. Further investigation to identify the causes is need. However, M scores for other years are quite sound.

23

Ending Page

24