company presentation august 2014 - jefferies · tion), nonwovens, and plastic films ... company...

TRANSCRIPT

Company presentation August 2014

The ANDRITZ GROUP

2

Contents

ANDRITZ GROUP overview

Business areas and long-term growth potential

Long-term goals and outlook for 2014

Company presentation August 2014

3

GLOBAL PRESENCE

250 production sites and service/sales companies worldwide

HEADQUARTERS

Graz, Austria

EMPLOYEES

24,126 (as of June 30, 2014)

* MEUR = million euro

Company presentation August 2014

The ANDRITZ-GROUP

Overview

KEY FINANCIAL FIGURES 2013

>> Order intake: 5,611 MEUR* >> Sales: 5,711 MEUR

>> Net income: 53 MEUR >> Equity ratio: approx. 17%

* Average share of ANDRITZ

GROUP’s total order intake

4

HYDRO

>> Electromechanical equipment for hydro-

power plants (especially turbines and

generators)

>> Pumps (e.g. for water transport and irrigation)

>> Turbogenerators for thermal power stations

PULP & PAPER

>> Equipment for production of all types of pulp,

paper, tissue, and board

>> Energy boilers

>> Production equipment for biofuel (2nd genera-

tion), nonwovens, and plastic films

30-35%*

A world market leader in most business areas

HYDRO and PULP & PAPER as well as …

Company presentation August 2014

30-35%*

* Average share of ANDRITZ

GROUP’s total order intake

5

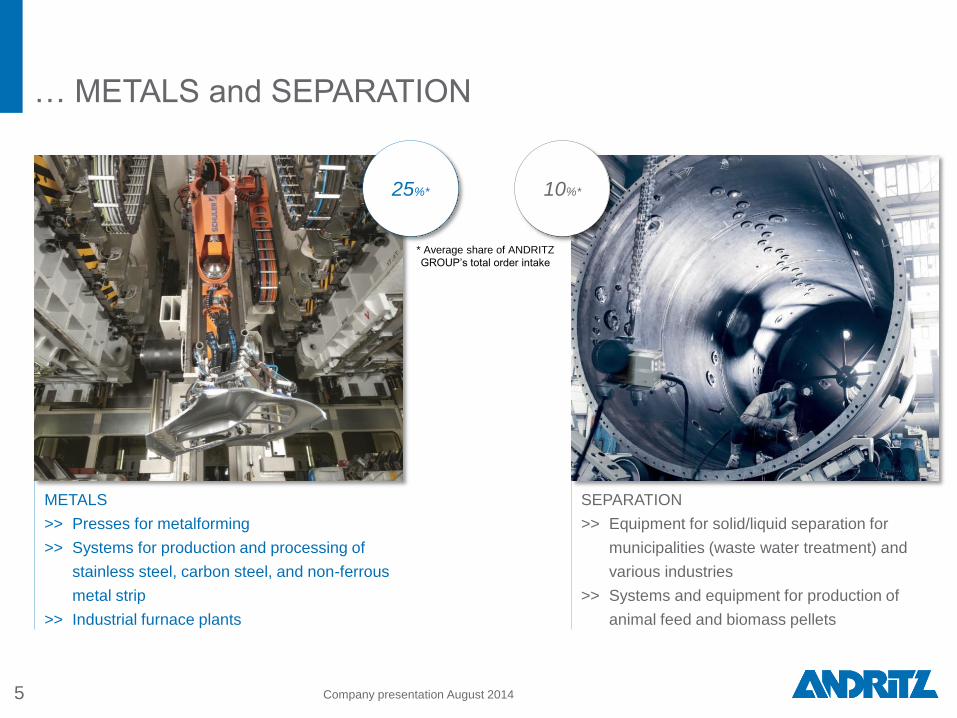

METALS

>> Presses for metalforming

>> Systems for production and processing of

stainless steel, carbon steel, and non-ferrous

metal strip

>> Industrial furnace plants

SEPARATION

>> Equipment for solid/liquid separation for

municipalities (waste water treatment) and

various industries

>> Systems and equipment for production of

animal feed and biomass pellets

Company presentation August 2014

… METALS and SEPARATION

25%* 10%*

6 Company presentation August 2014

1,481 1,744

2,710

3,283 3,610

3,198 3,554

4,596

5,177

5,711

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Sales of the ANDRITZ GROUP (MEUR)

Recent acquisitions by business area

2011 AE&E Austria 2011 Iggesund Tools 2011 Tristar Industries 2011 Asselin-Thibeau 2012 AES 2013 MeWa METALS 1997 Sundwig 1998 Thermtec 2000 Kohler 2002 SELAS SAS Furnace Div. 2004 Kaiser 2005 Lynson 2008 Maerz 2012 Bricmont 2012 Soutec 2013 Schuler (> 95%) 2013 FBB Engineering SEPARATION 1992 TCW Engineering 1995 Jesma-Matador 1996 Guinard 2000 UMT 2002 3SYS 2004 Bird Machine 2004 NETZSCH Filtration 2004 Fluid Bed Systems 2005 Lenser Filtration 2006 CONTEC Decanter 2009 Delkor Capital Equipment 2009 Frautech 2010 KMPT 2012 Gouda 2013 Shende Machinery

HYDRO 2006 VA TECH HYDRO 2007 Tigép 2008 GE Hydro business 2008 GEHI (JV) 2010 Precision Machine 2010 Hammerfest Strøm (59%) 2010 Ritz 2011 Hemicycle Controls PULP & PAPER 1990 Sprout-Bauer 1992 Durametal 1994 Kone Wood 1998 Kvaerner Hymac 1999 Winberg 2000 Ahlstrom Machinery 2000 Lamb Baling Line 2000 Voith Andritz Tissue LLC (JV) 2002 ABB Drying 2003 IDEAS Simulation 2003 Acutest Oy 2003 Fiedler 2004 EMS (JV) 2005 Cybermetrics 2005 Universal Dynamics Group 2006 Küsters 2006 Carbona 2006 Pilão 2007 Bachofen + Meier 2007 Sindus 2008 Kufferath 2009 Rollteck 2010 Rieter Perfojet 2010 DMT/Biax

Compound Annual Growth Rate (CAGR) of Group sales 2004-2013: +16% p. a. (thereof approx. half organic growth)

Strengthening of market position

Growth through organic expansion and acquisitions

77 103 55

220

384 366 247

409

678

1,177

1,401 1,286

893 869

126 208 174

337

494

710 599

822

1,082

1,595

1,815

2,048

1,517 1,498

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 H1 2014

3

12 12 13 18

26

39

51 56

52

87

114

124

52

Rollteck

Frautech

Delkor

Ahlström

rem. 50%

Guinard

rem. 50%

Fläkt

Selas

Fiedler

IDEAS

Acutest

Thermtec

rem.

24.5%

Kaiser

AFSR

Netzsch

Bird

Lenser

Universal

Lynson

VA TECH

HYDRO

Kuesters

BMB

Tigép

Sindus

GE Hydro

GEHI

Kufferath

Maerz

DMT/Biax

Rieter

Perfojet

Precision

Machine

KMPT

Ritz

Hammer-

fest (33%)

7

Continuing strong net cash position

■ Net liquidity as of end of period (MEUR)

■ Gross liquidity as of end of period (MEUR)

■ Dividend paid out after AGM for the previous year (MEUR)

AE&E

Austria

Iggesund

Tools

Tristar

Industries

Asselin-

Thibeau

Hemi-

cycle

Controls

Hammer-

fest (59%)

Bricmont

Soutec

Schuler

(~ 25%)

AES

Gouda

Schuler

(> 70%)

Shende

Machinery

(80%)

FBB

MeWa

Company presentation August 2014

8

Key figures Q2/H1 2014 at a glance: unchanged solid

cash position, low capex and favorable net working capital

Company presentation August 2014

The Schuler Group was consolidated into the consolidated financial statements of the ANDRITZ GROUP as of March 1, 2013

Unit H1 2014 H1 2013 +/- Q2 2014 Q2 2013 +/-

Order intake MEUR 2,980.2 2,526.0 +18.0% 1,238.0 1,237.7 +0.0%

Order backlog (as of end of period) MEUR 7,555.7 7,644.4 -1.2% 7,555.7 7,644.4 -1.2%

Sales MEUR 2,659.4 2,610.1 +1.9% 1,439.9 1,446.3 -0.4%

EBITDA MEUR 175.7 136.0 +29.2% 106.2 104.0 +2.1%

EBITA MEUR 133.4 96.9 +37.7% 84.8 82.7 +2.5%

EBIT MEUR 94.4 65.9 +43.2% 65.4 62.8 +4.1%

EBT MEUR 92.7 62.8 +47.6% 65.2 60.8 +7.2%

Financial result MEUR -1.7 -3.1 +45.2% -0.2 -2.0 +90.0%

Net income (including non-controlling interests) MEUR 64.9 44.8 +44.9% 45.6 43.0 +6.0%

Cash flow from operating activities MEUR 49.0 -86.5 +156.6% -12.0 -6.8 -76.5%

Capital expenditure MEUR 34.4 44.4 -22.5% 17.2 23.0 -25.2%

Equity ratio % 16.9 17.2 - 16.9 17.2 -

Liquidity MEUR 1,497.7 1,459.2 +2.6% 1,497.7 1,459.2 +2.6%

Net liquidity (after deduction of all financial liabilities) MEUR 868.8 817.7 +6.2% 868.8 817.7 +6.2%

Net working capital MEUR -511.9 -524.5 +2.4% -511.9 -524.5 +2.4%

EBITDA margin % 6.6 5.2 - 7.4 7.2 -

EBITA margin % 5.0 3.7 - 5.9 5.7 -

EBIT margin % 3.5 2.5 - 4.5 4.3 -

Employees (as of end of period; without apprentices) - 24,126 23,849 +1.2% 24,126 23,849 +1.2%

Business areas and long-term growth

potential

ANDRITZ GROUP overview

9

Long-term goals and outlook for 2014

Contents

Company presentation August 2014

10

HYDRO

Challenging, but market…

Large-scale projects Small-scale projects Pumps

Market update Solid demand for

modernizations

Pumped storage projects

on hold due to low

electricity prices

Greenfield hydropower

projects in emerging

markets (Africa,

South America)

Good activity to continue,

especially in emerging

markets (high energy

demand, low capex needs)

Demand for special pumps

to remain high (irrigation,

water transport, etc.)

Competition main competitors: Alstom (FR); Voith (DE)

Impact from GE/Alstom JV remains to be seen

Outlook

Company presentation August 2014

HYDRO

…with long-term growth potential

11 Company presentation August 2014

Old installed base in developed world requires continuous investment in

modernization and rehabilitation of installed turbines and generators

Source: Eurelectric

* Efficiency is a measure of performance of energy conversion and thus describes the ratio between the power input and the effective power output.

~55 % of worldwide installed

capacity older than 30 years

~33 % of the global hydropower

potential has been developed

so far

Population growth and economic growth in emerging markets drive demand for

new hydropower stations or major upgrades of existing installations

Small-scale hydropower stations to show good demand due to

low capex requirements and practically no interference with nature

The high efficiency of hydropower*

12

Pulp Paper and

packaging Nonwoven and

plastic film

Service

Market

update

Investments in greenfield pulp mills

to continue

Modernization projects to increase

capacity, efficiency, and profitability

of existing mills

Green energy investments

Regionally different development

for biomass pelleting projects

Stable demand for

tissue and

container board

machines

Reasonable

project activity for

nonwoven

Good potential

in certain niches

plastic film: drastic

market decline

due to overcapacity

Good potential

to grow

organically and

by acquisitions

Competition ANDRITZ is mainly active in pulp – main competitor: Valmet (FI)

unchanged stiff price competition

Outlook

Company presentation August 2014

PULP & PAPER

Stable project activity, but fierce competition

13

Metalforming Stainless steel Furnaces

Market update Good demand from automobile

manufacturers continuing,

especially in Asia and Latin America

Stable demand

from other industries

Investment activity

to remain at low level,

some investment projects

planned in H2/2014

Good demand

to continue

Competition world market leader

main competitors from Japan and China

stable competition at challenging level

among top 3 suppliers worldwide

main competitors: Danieli (IT), SMS (DE),

Mitsubishi / VAI

stable competition at challenging level

Outlook

Company presentation August 2014

METALS: good project activity in metalforming,

aluminum and furnaces, low in carbon and stainless steel

14

Status on Schuler restructuring

Company presentation August 2014

Q4 2013: expenses and provisions (~40 MEUR) for structural

improvement program

Current program to be finished until end of 2014

Goal of restructuring:

Organization and cost structure adjustments according to

market requirements in terms of earnings and growth

Expected annual cost savings between 15 and 20 MEUR

Schuler management recently increased guidance for 2014:

Sales: ~1.1 – 1.2 bn EUR (before: 1.1 bn. EUR)

EBITA margin: 7-8% (before: 6-7%)

METALS: Light vehicle production (in million units)

Growth per region 2013-2020

15 Company presentation August 2014

Source: PwC Autofacts 2014 Q1 Data Release

South America*

North America*

Middle East/Africa*

EU*

East Europe*

Developing

Asia Pacific*

Developed

Asia Pacific* 4.5m

16.3m

1.5m

15.9m

3.6m

27.1m

13.6m

Σ Growth light vehicle

production: +25.5m CAGR: +3.9%

+2.6m (CAGR: +2.1%)

+2.1m (CAGR: +5.6%)

+1.2m (CAGR: +8.8%) -0.8m (CAGR: -0.9%)

+15.5m (CAGR: +6.7%)

+1.7m (CAGR: +5.7%)

Total light vehicle

production 2013: 82.5m

* figures in black colour show total car production in 2013, figures in orange colour show expected production increase 2013-2020 with compound annual growth rate.

+3.2m (CAGR: +2.7%)

16

Municipalities Industries Animal feed Biomass pelleting

Market update Investment activity at

reasonable levels but

mainly in developed

markets

Reasonable demand

in food processing

Low project activity in

mining, minerals, and

chemical industries

Continuing

at solid level

Stable demand

to continue

Competition very fragmented market with some global and several regional competitors

ANDRITZ‘s

product issues

Step-by-step progress has been made, expected to be resolved by end of 2014

Restructuring Organizational adjustments and full implementation to be finished by year-end

Outlook

Company presentation August 2014

SEPARATION

Adjusting organization to increase product focus

ANDRITZ GROUP overview

Long-term goals and outlook for 2014

17

Business areas and long-term growth potential

Contents

Company presentation August 2014

Goal: 7%, improve to 8%

with top line sales growth

4.7

5.2 5.3 5.1

6.3 6.1 6.1

6.4 6.5

5.1

7.2 7.2 6.9

2.9**

5.0

937

1,319 1,110 1,225

1,481 1,744

2,710

3,283 3,610

3,198 3,554

4,596

5,177

5,711**

2,654

0

1.000

2.000

3.000

4.000

5.000

6.000

00

01

02

03

04

05

06

07

08

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 H1 2014

EBITA margin (%) Sales (MEUR)

*

* Including restructuring expenses

2005-2009: avg. 6.0%

2000-2004: avg. 5.3%

Target to continue long-term profitable growth

Goal: maintain 7% and improve to 8% with top line sales growth

18

** Including Schuler as of March 1, 2013; no pro forma figures are available for the reference periods of last years.

% MEUR

Company presentation August 2014

19 Company presentation August 2014

Outlook for remainder of 2014

Investment activity to remain at current levels

HYDRO

Lower but still satisfactory project

activity for modernizations and new

hydropower stations; increasing price

competition at selective projects;

market for pumps quite active

PULP & PAPER

Solid project activity for modernizations/

capacity increases and power/biomass

boilers; good pipeline for greenfield pulp

mill projects, although decisions probably

moving to end of 2014/beginning of 2015

METALS

Global metal forming market to

stay at good level; project activity

for stainless steel to remain at

subdued level; good market

activity in aluminum to continue

SEPARATION

Low project activity in mining to remain;

increasing project activity in chemicals;

good investment activity in environment,

food processing, and feed/biomass

pelleting plants

stable +

ANDRITZ GROUP

>> Slight increase in sales due to Schuler consolidation effect (contribution of additional two months in 2014)

>> Significant improvement of net income targeted

stable +

stable + stable +/-