company presentation › ~ › media › files › o › opap-ir › copy of...company overview 4...

TRANSCRIPT

Company Presentation

February 2018

Agenda

History – Company Overview

Financial Overview

Strategy

Social Responsibility

Summary

© OPAP

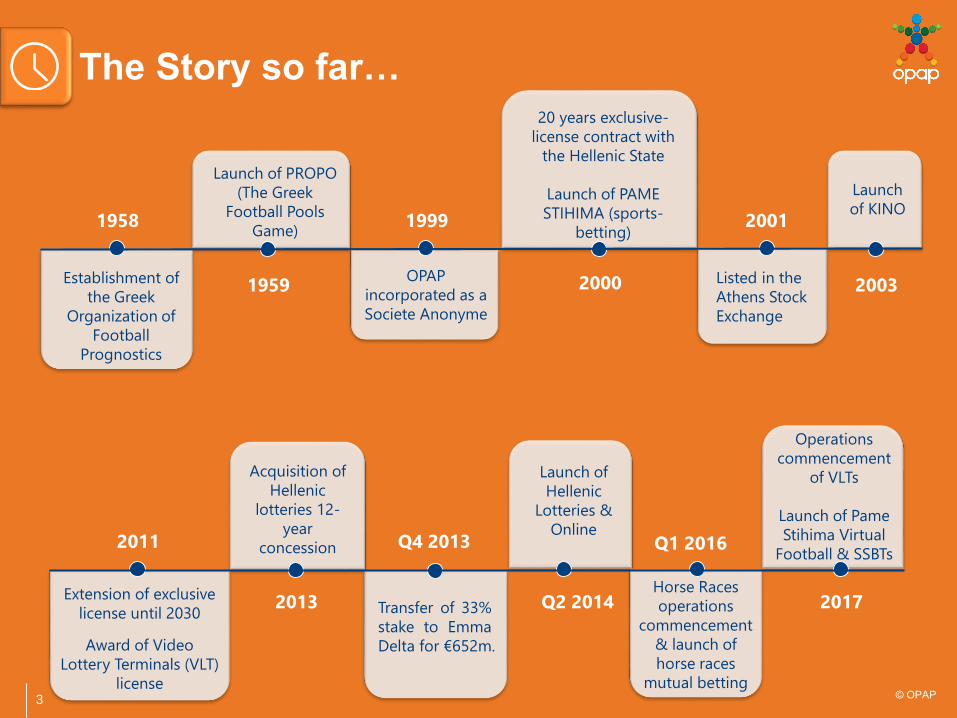

Launch of PROPO

(The Greek

Football Pools

Game)

3

The Story so far…

1958

Establishment of

the Greek

Organization of

Football

Prognostics

1959

1999

OPAP

incorporated as a

Societe Anonyme

20 years exclusive-

license contract with

the Hellenic State

Launch of PAME

STIHIMA (sports-

betting)

2000

2001

Listed in the

Athens Stock

Exchange

2011

Extension of exclusive

license until 2030

Award of Video

Lottery Terminals (VLT)

license

Acquisition of

Hellenic

lotteries 12-

year

concession

2013

Q4 2013

Transfer of 33%

stake to Emma

Delta for €652m.

Launch of

Hellenic

Lotteries &

Online

Q2 2014

© OPAP

Horse Races

operations

commencement

& launch of

horse races

mutual betting

Q1 2016

Operations

commencement

of VLTs

Launch of Pame

Stihima Virtual

Football & SSBTs

2017

Launch

of KINO

2003

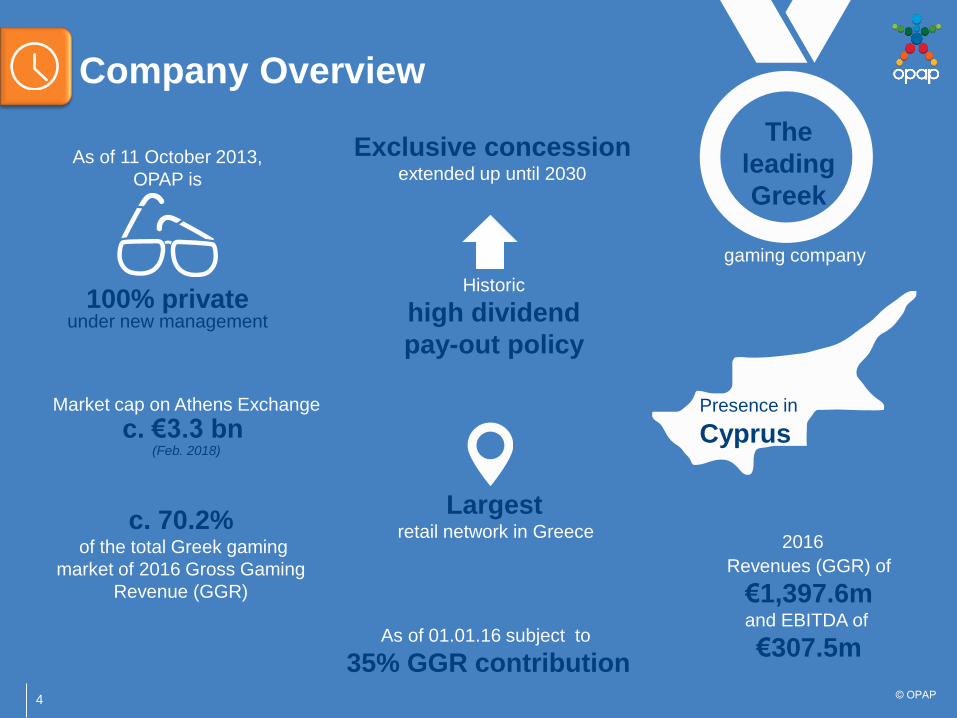

Company Overview

4

The

leading

Greek

gaming company

100% privateunder new management

As of 11 October 2013,

OPAP is

Presence in

Cyprus

Market cap on Athens Exchange

c. €3.3 bn(Feb. 2018)

Exclusive concessionextended up until 2030

c. 70.2%of the total Greek gaming

market of 2016 Gross Gaming

Revenue (GGR)

2016

Revenues (GGR) of

€1,397.6mand EBITDA of

€307.5m

Historic

high dividend

pay-out policy

As of 01.01.16 subject to

35% GGR contribution

Largest retail network in Greece

© OPAP

Date (%) Offering price (€)

25 April 2001 5,36% Initial Public Offering (IPO) 5,5

18 July 2002 18,90% Secondary offering 8,44

14 July 2003 24,45% Secondary offering 9,44

21 July 2005 16,44% Secondary offering 24,14

11 October 2013 33,00% Public tender 6,2

Public offerings -Shareholder Structure

5 © OPAP

Emma Delta Hellenic

Holdings Ltd33,00%

Free Float67,00%

• Although it has been declining due to macro related factors, Greek Gross Gaming Yield as % of the

GDP continues to compare favorably with many European peers

• The Greek gaming market is a fundamentally attractive market :

1. 10th largest gambling market in the European Union (2016 gross gaming yield of €1.89bn) in absolute value after Italy, United Kingdom, Germany, France, Spain, Netherlands, Sweden, Ireland and Finland which all benefit from higher GDP

2. 2016 gross gaming yield per adult of €199 (10th highest in Europe)3. 2015 gross gaming yield representing 1.08% of GDP (2nd highest amongst the graph’s sample – used to be the highest in 2010)

2016

gross gaming

yield

(€bn and % of

GDP(1))

2016 gross

gaming yield

per adult(2)(3)(€)

19,5

17,1

11,19,9

8,5

2,6 2,3 2,1 2,0 1,9 1,5 1,4 1,3 1,3 1,2

1,18%

0,76%

0,36%0,45%

0,76%

0,38%0,49%

0,75%

0,95%1,08%

0,35%

0,78%

0,38%0,47%

0,69%

Italy UK Germany France Spain NetherlandsSweden Ireland Finland Greece Belgium Portugal Austria DenmarkChech Rep

491

437

377

314279 275

238 228 225199 187 186 180 165 164

Ireland Finland Italy UK Sweden Denmark Slovenia Luxembourg Spain Greece Netherlands France Austria Portugal Belg ium

In €bn

In % of 2016

GDP

Source: H2GC

Note: Charts include top-15 EU-28 countries for GGR and GGR/per adult respectively. Gross gaming revenue including offline and online (onshore and offshore) gaming.

(1) Current price GDP

(2) Inhabitants over 18 years old

(3) Excluding Malta and Cyprus

Average: 0.66%

The Greek Gaming Market: A Comparative Review

6 © OPAP

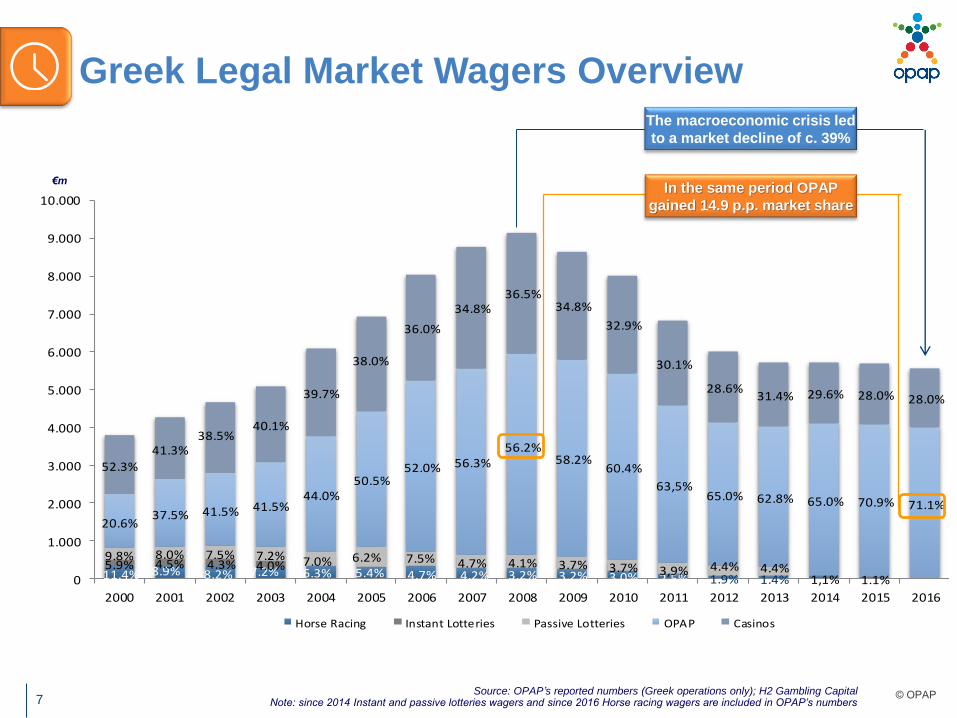

Source: OPAP’s reported numbers (Greek operations only); H2 Gambling CapitalNote: since 2014 Instant and passive lotteries wagers and since 2016 Horse racing wagers are included in OPAP’s numbers

11.4% 8.9% 8.2% 7.2% 6.3% 5.4% 4.7% 4.2% 3.2% 3.2% 3.0% 2.5% 1.9% 1.4% 1,1% 1.1%5.9% 4.5% 4.3% 4.0%9.8% 8.0% 7.5% 7.2% 7.0% 6.2% 7.5% 4.7% 4.1% 3.7% 3.7% 3,9% 4.4% 4.4%

20.6%37.5% 41.5% 41.5%

44.0%50.5%

52.0% 56.3%56.2%

58.2%60.4%

63,5%65.0% 62.8% 65.0% 70.9% 71.1%

52.3%

41.3%38.5%

40.1%

39.7%

38.0%

36.0%

34.8%36.5%

34.8%

32.9%

30.1%

28.6%31.4% 29.6% 28.0% 28.0%

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Horse Racing Instant Lotteries Passive Lotteries OPAP Casinos

€m

Greek Legal Market Wagers Overview

7 © OPAP

The macroeconomic crisis led

to a market decline of c. 39%

In the same period OPAP

gained 14.9 p.p. market share

Market size: €1.89bn

Source: OPAP’s reported numbers ; H2 Gambling Capital

OPAP is the Undisputed Leader of the Greek

Gaming Market

8

2016 GREEK GAMING MARKET (GGR)

41%

20%

9%

0,5%

14%

16%

Horse racing

International e-gaming operators

Casinos

Instant & Passives

OPAP Sports Betting

OPAP Numerical Games

© OPAP

OVERVIEW OF THE GREEK GAMING MARKET

• The Greek regulated gaming market comprises of:

• OPAP

• Betting products including also Horse Racing (since Jan. 2016)

• Lottery products

• Instant & Passives

• Video Lottery Terminals

• Casinos: includes all games played within casinos

• Like most other European lottery markets, the Greek gaming

market is regulated and controlled by the Hellenic Gaming

Commission

• Instant & Passives:

• Instants: Scratch games were successfully re-introduced in

May 2014 by an OPAP led consortium.

• Passives: Ethniko, Laiko and Kratiko, the passive lottery-

style games, represent c. 3.5% of the market

• The Greek casino market consists of 9 licensed casinos,

generating 14% of the total market’s gross gaming revenue,

dominated by Parnitha, Thessaloniki and Loutraki

• Pari-mutuel horserace betting since January 2016 is being

operated by OPAP S.A. following the acquisition of a relevant 20-

year license for a total consideration of €40.5m

• Fixed odds sports betting in Greece is solely organized by

OPAP, yielding €382m of gross gaming revenue in 2016.

OPAP

market share

70,2%

Significant exclusive concessions secured

through heavy investments in the past yearsMore than 50 years of exclusive concessions backlog already paid for

Oct2000

May2014

Jan2016

Jan2017

Oct2020

May2026

Jan2027

Oct2030

Concession Agreement (20 years)

Concession Extension Agreement (10 years)

Right of first refusal for any other game to be licensed by the Hellenic Gaming Commission

2011 VLT License (18 years)

Jan 2036

+ Right to

renew

2013 State Lotteries Concession Agreement (12 years)

Exclusive Right for online offering of OPAP’s exclusive lottery games

Exclusive offering of onshore online sports betting

Jun2014

Total upfront cost of license(100% already paid by

OPAP)

€323mn

€375mn

License fee to be negotiated on a case by case basis

Lega

cy G

ames

€560mn

VLT

s

€127mn(1)

Inst

ant

&

Pas

sive

s

€40.5mn

Ho

rse

Rac

ing

Included in upfront payments for legacy

licensesOn

line

(1): Total consideration of €190mn paid by consortium including OPAP, Scientific Games and Intralot, of which €127mn was paid by OPAP for its 67% stake © OPAP

Jan2035

2016 Horse Racing Concession Agreement (20 years)

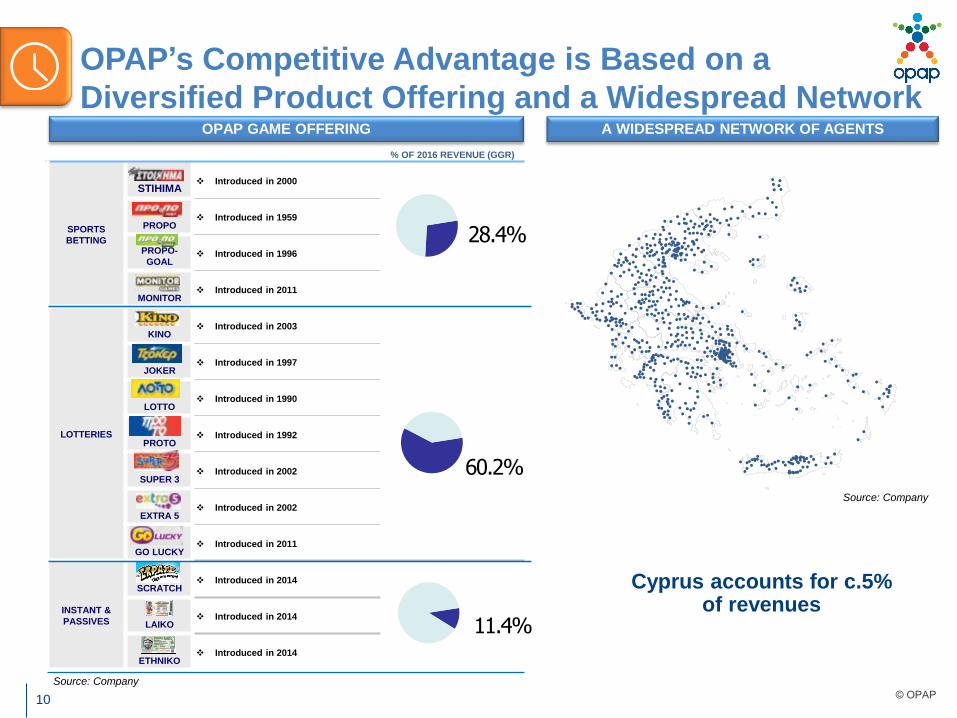

% OF 2016 REVENUE (GGR)

SPORTS

BETTING

STIHIMA Introduced in 2000

PROPO Introduced in 1959

PROPO-

GOAL Introduced in 1996

MONITOR Introduced in 2011

LOTTERIES

KINO Introduced in 2003

JOKER Introduced in 1997

LOTTO Introduced in 1990

PROTO Introduced in 1992

SUPER 3 Introduced in 2002

EXTRA 5 Introduced in 2002

GO LUCKY Introduced in 2011

INSTANT &

PASSIVES

SCRATCH Introduced in 2014

LAIKO Introduced in 2014

ETHNIKO Introduced in 2014

Source: Company

Cyprus accounts for c.5% of revenues

OPAP’s Competitive Advantage is Based on a

Diversified Product Offering and a Widespread Network

10

OPAP GAME OFFERING A WIDESPREAD NETWORK OF AGENTS

Source: Company

© OPAP

28.4%

60.2%

11.4%

The largest commercial network in Greece

From the past to the cohesive corporate branding image of today

Network

11

4,727 POS*

* Greece & Cyprus network as of 31.12.2016

Hellenic Lotteries products are distributed through

additional 7,191 POS & Street Vendors © OPAP

Petrol

stations

PostBank

BankBank BankGas stations Telecoms

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Lotteries Sports betting Instant & Passives

€m

OPAP’s Greek Revenue (GGR) Breakdown

12 © OPAP

Lotteries

Sports betting

Instant &

Passives

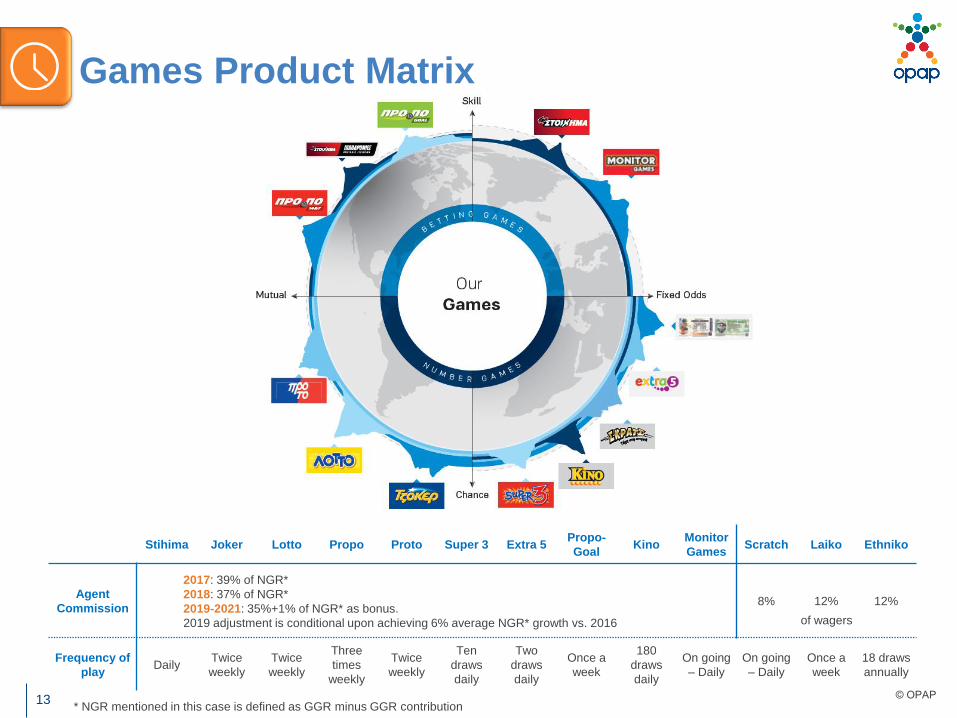

Games Product Matrix

13 © OPAP

Stihima Joker Lotto Propo Proto Super 3 Extra 5Propo-

GoalKino

Monitor

GamesScratch Laiko Ethniko

Agent

Commission8% 12% 12%

Frequency of

playDaily

Twice

weekly

Twice

weekly

Three

times

weekly

Twice

weekly

Ten

draws

daily

Two

draws

daily

Once a

week

180

draws

daily

On going

– Daily

On going

– Daily

Once a

week

18 draws

annually

2017: 39% of NGR*

2018: 37% of NGR*

2019-2021: 35%+1% of NGR* as bonus.

2019 adjustment is conditional upon achieving 6% average NGR* growth vs. 2016

* NGR mentioned in this case is defined as GGR minus GGR contribution

of wagers

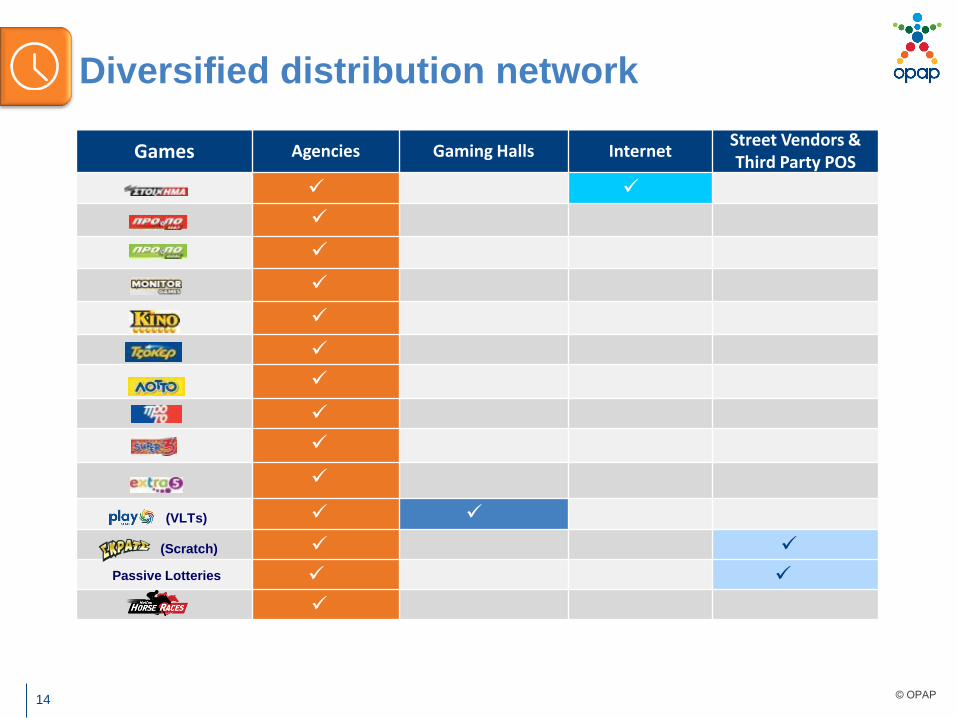

Diversified distribution network

14

Games Agencies Gaming Halls InternetStreet Vendors & Third Party POS

© OPAP

(VLTs)

(Scratch)

Passive Lotteries

It’s all about numbers

15

Financials

© OPAP

WAGERS AND MARGIN EVOLUTION SINCE 2004

Source: Company reports

3,177 3,6954,633 5,066 5,520 5,441 5,140

4,359 3,972 3,7114,259 4,257 4,230

53% 53% 47% 54% 57% 54% 55% 52% 52%

18% 25% 26,9%22%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Wagers (in €m) EBITDA Margin (as % of GGR)

COMMENTS

OPAP has recorded strong top line growth since 2003,

mainly driven by:

2003: Introduction of Kino

2007: Stihima risk management operation was taken in-house

2005-2008: Development of betting portfolio events through

introduction of new features in Stihima and increase of Kino

daily playing hours

2014: Introduction of Scratch and passive lotteries

Recent performance has been impacted by the adverse

economic environment:

Overall performance affected by satisfactory Kino

performance, launch of Instant & Passives in 2014, while

Stihima is affected by cyclicality of major football events every

2 years

January 2013: a 30% GGR contribution is introduced

January 2016: GGR contribution increased at 35%

2

3

1

OPAP FINANCIAL OVERVIEW

In €m 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Wagers 3,177 3,695 4,633 5,066 5,520 5,441 5,140 4,359 3,972 3,711 4,259 4,257 4,230

Growth% 39.2% 16.3%25.4% 9.3% 9.0% (1.4%) (5.5%) (15.2) (8.9) (6.6) 14.8 (0.0) (0.6)

Revenue

(GGR)*1,242 1,338 1,562 1,597 1,852 1,781 1,654 1,413 1,302 1,220 1,378 1,400 1,398

Growth % 28.2 7.7 16.7 2.2 16.0 (3.8) (7.1) (14.5) (7.9) (6.3) 12.9 1.6 (0.2)

EBITDA 659 714 738 860 1,057 967 911 734 674 222 347 377 308

Margin

(% of

GGR)53.0 53.3 47.2 53.9 57.1 54.3 55.1 51.9 51.7 18.2 25.2 27.0 22.0

Net Debt /

(Cash)(377) (412) (384) (493) (706) (700) (657) 97 (117) (77) (297) (155) (108)

Source: Company reports

* Gross Gaming Revenue

Financial Performance

16 © OPAP

4

12 4

3

0

500

1.000

1.500

2.000

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 12 13 14 15 16

0

200

400

600

800

1.000

'01 '02 '03 '04 '05 '06 07 '08 '09 '10 '11 12 13* 14 15 16

0

200

400

600

800

1.000

'01 '02 '03 '04 '05 '06 07 '08 '09 '10 '11 12 13* 14 15 160

200

400

600

800

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 12 13* 14 15 16

Revenue (GGR) (€m) 2001 - 16 EBITDA (€m) 2001 - 16

EBIT (€m) 2001 - 16 Net Profit (€m) 2001 - 16

Financial Overview

17

2013*: First year of 30% GGR contribution implementation

Since 2016 GGR contribution at 35%© OPAP

Financial Results 9M 2017 (1/2)

18 © OPAP

+5.6%Wagers(€m) Gross Gaming Revenue (€m)

+4.8%EBITDA* (€m) Net Profit* (€m)

Greek GDP 9M 2017

+1.19%

Retail Sales

(excl. fuels)

9M 2017

+2,0%

Department Stores

+0,6%

Pharmaceuticals

+1,6%

Furniture & Household Equipment

+4,5%

Food/Tobacco

-2,9%

New investments delivering strong Q3 performance

* Recurring figures excluding one-off items

3,044 3,214

0

500

1,000

1,500

2,000

2,500

3,000

3,500

9M 2016 9M 2017

998 1046

0

200

400

600

800

1.000

1.200

9M 2016 9M 2017

230 221

0

50

100

150

200

250

9M 2016 9M 2017

120107

0

20

40

60

80

100

120

140

9M 2016 9M 2017

-4.1% -10.5%

Financial Results 9M 2017 (2/2)

19 © OPAP

3,2%*

EBITDA

(€m)

Net Profit

(€m)

Net Profit margin on GGR

* Recurring figures excluding one-off items

EBITDA margin on GGR

Recurring figures*Reported figures

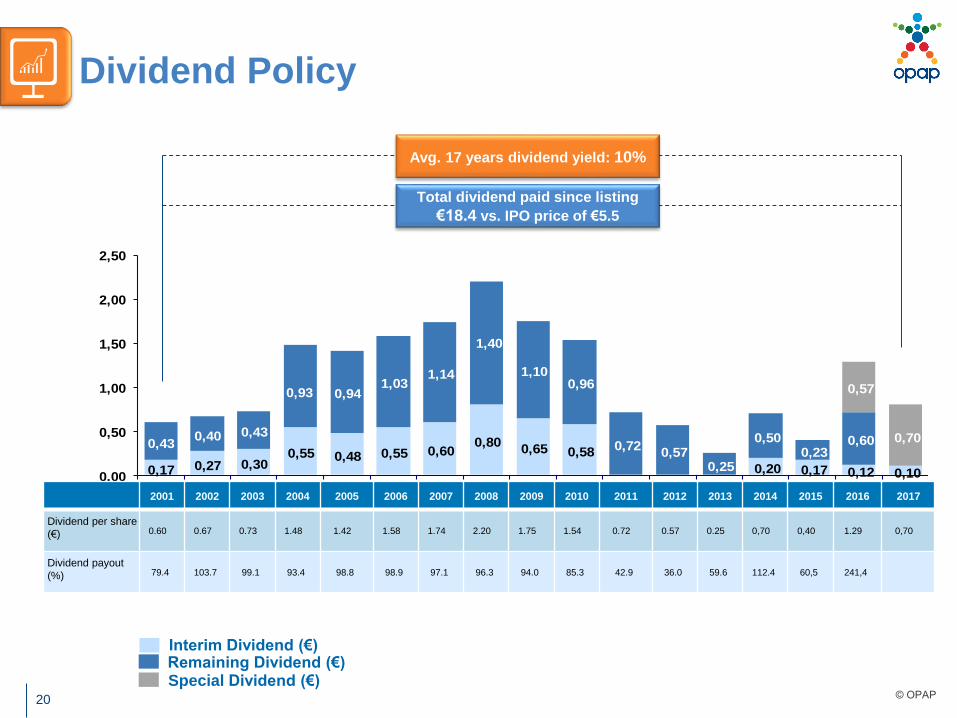

0,17 0,27 0,300,55 0,48 0,55 0,60

0,800,65 0,58

0,20 0,17 0,12 0,10

0,430,40 0,43

0,93 0,941,03

1,14

1,40

1,100,96

0,720,57

0,25

0,500,23

0,60

0,57

0,70

0,00

0,50

1,00

1,50

2,00

2,50

Interim Dividend (€)Remaining Dividend (€)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Dividend per share

(€) 0.60 0.67 0.73 1.48 1.42 1.58 1.74 2.20 1.75 1.54 0.72 0.57 0.25 0,70 0,40 1.29 0,70

Dividend payout

(%) 79.4 103.7 99.1 93.4 98.8 98.9 97.1 96.3 94.0 85.3 42.9 36.0 59.6 112.4 60,5 241,4

Dividend Policy

20 © OPAP

Avg. 17 years dividend yield: 10%

Total dividend paid since listing

€18.4 vs. IPO price of €5.5

Special Dividend (€)

• Embedding Customer Obsession

• Investing In Our Network

• Developing Our People

• Building a World-class Portfolio of Products & Services

• Leveraging the latest Digital & Technology Capabilities

• Committing to Our Communities

• Expanding the Power of Our Brand

• Rebuilding healthy relationships with the State, Regulator and other bodies

21

Commenting on the Q3 2017 financial

results, OPAP’s CEO, Mr. Damian

Cope, noted that:

After a solid first half of the year, Q3 marked a return to meaningful growth in both revenues and profitability for OPAP. This growth was primarily driven by a strong performance from our portfolio of Betting products, including SSBTs and Virtuals, and an increased contribution from VLTs.Notwithstanding the increasing pressures on our customers’ disposable income, OPAP is demonstrating that it can offer a broad range of attractive, gaming entertainment experiences. We continue to invest heavily in our products, our technology and our people in the delivery of our 2020 Vision and further progress has been made in each of our 8 strategic objectives. These results are already demonstrating the early benefits of these investments and are also testament to the hard work and contributions from everyone in the OPAP team, both our employees and our agents.We have also been intensifying our efforts in the important areas of corporate and social responsibility, including further investment in responsible gaming policies and programmes, while also working closely with the authorities in the battle against illegal gaming.Looking forward, we have a particularly busy few months ahead with a number of important milestones for both our technology migrations and product rollouts, but remain confident that we will deliver on our objectives for FY17 and beyond.

“

”

OPAP Strategy

© OPAP

To establish OPAP as a world class gaming entertainment company

22 © OPAP

Video Lottery Terminals (VLTs) License Agreement

Fully paid 18 years exclusive license of €560m for the

operation of 25,000 VLTs

VLTs will add a “growth engine” to OPAP’s performance

potential and is expected to be amongst the most

significant contributors to OPAP’s EBITDA in the long-

term

HR to receive 30%-35% of gross win in the form of

royalties

Max. allowed number of VLTs per venue: 50 in Gaming

Halls and 15 in existing OPAP agencies

Deployment deadline: December 31, 2019

23 © OPAP

Video Lottery Terminals (VLTs)

New Products - VLTs roll-out and performance ramp up in line with our expectations

Installed machines almost doubled in Q3 vs Q2

Increased roll-out pace expected until end 2017

Over 7,000 VLTs operational in Nov. 2017

Rollout - progressing well Performance - ramp-up underway

GGR / VLT / day*VLTs roll-out

Post

holiday

period1Q3

47

1,355 machines2

1,548 machines3

3,261 machines3

(1) Last week of August and full month of September(2) Machines operated in Q1. Calculation based on weighted avg.(3) Fully operational from the first week of the quarter

New technology providers shifting from a

heritage sole vendor dependence

24 *IGT provides the Horse racing pool engine

Channel

Platform/Application

Content

Retail Gaming Halls Digital

Horse Racing*

LotteryVLTs

VLTs

Sportsbetting(OTC, SSBTs)Pre game & Live betting,

Virtuals, Horse Racing

Kino, Tzoker & numeric games

Horse Racing*

Sportsbook

Lottery

Kino, Tzoker & numeric games

Sportsbook

Player Account Management

Sports Pre game & Live

betting, Horse Racing

Virtuals

© OPAP

“OPAP S.A. is a member of the World Lotteries Association (WLA) and the European Lotteries (EL) as well as the Global Lottery

Monitoring Systems (GLMS), independent unions composed of state or state-licensed lottery companies.

Both concession extension and VLTs license have been granted on the ground of OPAP’s social sustainability

• The largest social contributor in Greece measured in overall expenditure and variety of actions.

• Responsible Game: OPAP is offeringentertainment and recreation whileprotecting underage and othervulnerable groups.

• POS exclusive to gaming activities.

• European Responsible Gaming Standards and Sports betting Code of Conduct have been adopted by OPAP.

• OPAP received a level 3 accreditation by the World Lottery Association (WLA) for its Responsible Gamingstrategy

• OPAP supports the Therapy Centre for Dependent Individuals (KETHEA-ALFA) for the operation of the help-line 1114.

• OPAP transforms its business excellence into social contribution, through an integrated Corporate Social responsibility (CSR) Strategy.

• OPAP achieved significant recognition and awards by a number of independent agencies & bodies.

25

Social Responsibility

© OPAP

OPAP in Summary

26

Sole Concession until 2030

• Permits OPAP to enjoy the

growth of the Greek Gaming

Market

Sales Network

• Largest retail network in

Greece

Significant Cash Flows

• Secure & stable Dividends and

effective Investment Policy

Strong Fundamentals

• Favourable Market Dynamics,

Credibility and Growth

Solid Management Team

• Possesses significant

expertise, local know-how and

knowledge of the gaming

industry

© OPAP

Contacts

27

Nikos Polymenakos

Investor Relations [email protected]

Tel : +30 (210) 5798929

George Vitorakis

Head of Strategic Research [email protected]

Tel : +30 (210) 5798976

© OPAP

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

…………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………

28

Notes