company performance and its determinants: … performance and its... · company performance and its...

TRANSCRIPT

COMPANY PERFORMANCE AND ITS DETERMINANTS AN ANALYSIS OF MALAYSIA PROPERTY LISTED COMPANIES

Leong Siaw Hua

HF SS49S P3S

Corporate Master in Business Administration 2010

LS83 2010

fusat Kbidmat Makiumat Akademik ~lJyenE~m MAlAYSIA SARAWAK

PKHIOMAT MAKLUMAT AKAOEMIK

1IIIIIIIIIIi~illllllllll 1000246477

COMPANY PERFORMANCE AND ITS DETERMINANTS AN ANALYSIS OF MALAYSIA

PROPERTY LISTED COMPANIES

LEONG SlAW HUA

A dissertation submitted in partial fulfillment of the requirements for the degree of Corporate Master in Business Administration

Faculty of Economics and Business UNIVERSITI MALAYSIA SARAWAK

2010

DECLARATION AND COPYRIGHT

Name Leong Siaw Hua

Matric Number 08031525

I hereby declare that this research is the result of my own investigation except where otherwise stated Other sources are acknowledged by footnotes giving explicit references and bibliography is appended

Signature

Date

copy Copyright by Leong Siaw Hua and Universiti Malaysia Sarawak

ii

-V~~~-----------Y---------------------------------------------------------~

ACKNOWLEDGEMENTS

- r J

My pnmary acknowledgement and appreciations to those who aided me in

accomplishing my final year project First of all I would like to express my special thanks to

my supervisor for his guidance and valuable advises in completing my project

I am pleased to acknowledge to the lecturers in Faculty Economic and Business upon

their willingness and patient in guiding me and helping me in finishing this project

Apart from that I would Like to take this opportunity to thank both my parents for their

concern understanding and encouragement along the way Not to forget to thank my friends

for their guidance suggestion opinion and sharing of information in accomplishing this

project

III

-

ABSTRACT

COMPANY PERFORMANCE AND ITS DETERMINANTS AN ANAYSIS OF

MALA YSIA PROPERTY LISTED COMPANIES

By

Leong Siaw Hua

( The purpose of this study is to identify the key success factors that affect Malaysia property

companies performance The hypothesis of property company performance and its

determinants are tested using annual time series data from 1999-2008 The analysis reveals

that the coefficient for shareholder fund capital expenditure and plants and equipments are

negative where an increase in shareholder fund capital expenditure and plants and

equipments will cause return on assets to decreas~ This happened when firms internal

characteristics (cash flows insider ownership and firm size) are include in the regression

analysis indicating that the efficiency of investment in plant and property and equipment and

capital expenditure are very much depended on firms internal characteristics There is the

rejection of null hypothesis at 1 per cent significant level for all the variables except for

capital expenditure and cash flow However positive relationship is found between capital

expenditure plants and equipments and return on assets when they are tested in a separate

regression The results further showed that the return on assets shows negative in figure and is

fluctuated throughout the years where the percentage of profit became smaller in year 2008 as

compared to year 2007

iv

ABSTRAK

PRESTASI SYARIKA T DAN PENENTU FAKTORNY A ANALISIS TERHADAP SYARIKAT BARTA BENDA MALAYSIA TERSENARAI

Oleh

Leong Siaw Bua

Tujuan kajian ini adalah untuk mengenal pasti faktor pengunci kejayaan yang mempengaruhi

kerjayaan syarikat harta benda Malaysia tersenarai Hipotesis kajian diuji dengan

menggunakan data siri masa dari tahun 1999 sehingga tahun 2000 Hipotesis mendedahkan

bahawa angkari bagi pemegang dana modal perbelanjaan dan loji dan peralatan adalah

negatif di mana peningkatan dalam pemegang dana modal perbelanjaan dal loji dan

peralatan akan menyebabkan pemulangan asset berkurangan Ini berlaku apabila cirri-ciri

syarikat dalaman (aliran tunai pemilikan dalaman and saiz syarikat) dimasukan dalam

kemunduran anal isis menunjukkan kecekapan pelaburan dalam kilang and harta benda dan

peralatan dan modal perbelanjaan adalah bergantung pada cirri-ciri syarikat dalaman Dengan

ini penolakan daripada null hipotesis pada satu peratus kemantapan paras bagi semua

pemboleh ubahnya kecuali modal perbelanjaan dan aliran tunai Walau bagaimanapun

hubungan positif didapati di antara modal perbelanjaan dan loji dan peralatan dengan

pemulangan dalam asset ketika diuji dalam regression yang berasingan Pemulangan dalam

asset menunjukkan angka negatif dan tidak tetap melintasi tahun di mana peratus dari

keuntungan menjadi semakin kurang pada tahun 2008 dibandingkan dengan tahun 2007

v

-- VOLi

Pusat Khidmat Maklumat Akademik ~IVERSm MALAYSIA SARAWAK

T ABLE OF CONTENTS

DECLARATION AND COPyRIGHT II

ACKNOWLEDGEMENT III

LIST OF TABLES viii

LIST OF FIGURES IX

ABSTRACT IV

ABSTRAK V

CHAPTER ONE INTRODUCTION

10 Introduction

11 An Overview of Malaysia Property Market 8

12 Problem Statements 13

13 Objective 14

14 Significant and scope ofthe Study 14

15 Summary 15

CHAPTER TWO LITERATURE REVIEW

20 Introduction 16

21 Relationship between Return on Assets Plant and Equipment and Company 16

Performance

22 Relationship between Capital Expenditure Debts and Cash Flows toward 18

Company Performance

23 Relationship between Size and Company Performance 21

24 Relationship between Shareholder Funds and Company Performance 22

25 Relationship between Insider Ownership and Company Performance 23

VI

~107i7 1

26 Summary 25

CHAPTERTHREEMETHOLOGY

30 Introduction 26

31 Hypotheses 26

32 Research Design 29

321 Data Sample and Data Collection 29

322 Empirical Model 30

33 Summary 31

CHAPTER FOUR EMPIRICAL RESULTS

40 Introduction 32

41 Descriptive Statistics 33

42 Regression Analysis 34

43 Summary 39

CHAPTER FIVE CONCLUSION AND RECOMMENDATIONS

50 Introduction 41

51 Summary and Findings of the Study 41

52 Limitation of Study 44

53 The Underlying Factors of the Market and Implications 45

54 Conclusion 47

REFERENCES 48

VII

-~-------------- - ---shy

LIST OF TABLES

Title Page

Table 1 Supply of Residential Units in Malaysia 10

Table 2 Total Transaction Values (RMm) 12

Table 3 Total Number of Transaction 12

Table 4 Summary Statistics of the Variables 33

Table 5 Result of Insider Ownership Cash Flow and Size 34

Table 6 Result of Plants and Equipments Capital Expenditures and Shareholder 35 Fund

Table 7 Result of Panel Least Square Regression 36

VIII

LIST OF FIGURES

Title Page

Figure 1 Key Success Factor for Property Sector 5

Figure 2 Factors affect Company Performance in Property Sector 26

Figure 3 Return on Assets 38

IX

IOZ17J I

CHAPTER ONE

INTRODUCTION

10 Introduction

Malaysia experienced a strong beating from global financial crisis in the first half of 2009

as the Gross Domestic Product (GDP) contracted significantly Since then there were some

positive movements in some economic indicators in 3rd quarter due to the government national

recovery packages that restore market confidence and maintain the stability of financial market

and expectation of positive growth in the 4th quarter and these growth show evidence that

Malaysia is out of recession and there is still an upside potential in the investment of property in

Malaysia There are signs of improvement on the worldwide economy where stocks that

decreased in value previously are strong enough to get back to the market For example Dow

Jones gained 40 after their March low

The slowdown in Malaysias economy has caused Malaysians become more cautious with

their investment in properties However property prices in Malaysia remain one of the most

competitive in the region They offer stronger investment returns as compared to its neighboring

countries

In encouraging foreign investments economy liberalization measure introduced by the

government has made 2009 a significant new era in Malaysias development history The

comprehensive package with new policies are said to have a significant impact towards real

--- --------- - -------- - -

estate sector as the restrictions for foreign investors to purchase the properties in Malaysia had

been removed These measures aimed to increase the number of transactions and attract overseas

investment

Plants and equipments one of the firms strategic action is the main factor to determine the

success of property sector Bhat (2000) noted that the age of property company size plant and

equipment building and return on assets can help to increase profits and improve the

competitive edge of a company Porter (1989) states that the key success factor for property

sector depend on internal factors and external factors Internal factors especially plants and

equipments is the key success factor of property sector because they are valuable and imitability

as a strategic location determined the success of a property company The author stated that

looking for locations that are economically attractive is one of the critical dimensions of success

Kamarulzaman Hassan the analyst of T A Securities Holdings Berhad support this point by stated

that location of property is an issue besides demand and supply Bhat (2000) support that plants

and equipments determined the cost and revenue as they have direct impact on maintenance

expenditures However Porter (1989) stated that imitating is profitable if the industry is great but

it will become a way of insuring disaster if the industry is less attractive

Population in an area is the important factor which determined the demand and supply of

property Supply and demand is the backbone of a market economy The demand is high when

there is a larger population The standard of living and the development land affect the choice of

consumers in their decision making on the types of property and the location to invest This is

supported by Porter (1989) where tremendous demand for new building and demographic shift in

2

rates

the populatjon is the important factor for property sector In the concept of economics price is a

reflection of supply and demand Property contained large per cent of buyers cost Oversupply

will force the price to go down as the demand is less than the supply in the market However this

is no longer happened as developers know how to control the situation after experienced the crisis

hits on 1987 and 1997

In Porter 5 forces suppliers are the determinant factors that affect the profits gained and the

costs to customers The materials used in the construction of property tend affect the price and

this will be the burden of customers Barney (1991) noted that resources owned must enabled a

finn outperfonn its competitors The resources are carefully managed in order to achieve the

objective of sustainable development Malaysia has no problem on materials such as sand and

cement as Malaysia is the sole proprietor However material such as steel is said to affect the

costs of construction as the price of steel is depend on world market which subject to exchange

The threat of new entrants into the market is said to affect the profit gained as the entry

barriers are low Porter (1989) noted that the situation of rivalry in property sector has always

been active where a lot of new competitors have come in The competitors have enough capital to

finance a lot of new projects The increasing number of competitors combined with slowing

demand has led to overcapacity which caused the profit to drop

3

Poter (1989) stated that there are two ways property firms can gain competitive advantage I

One is lowest cost and another one is differentiation Property firms managed to gain higher

margin at prevailing price levels if they are able to develop and finance their projects and deliver

at a lower cost The author further stated that property firms can better utilizE the land or gain

higher profits per square foot if they are skilled in employing new concepts into projects or

skilled in property design

Other financial factors are debt equity cash flows capital expenditure plants and

equipments SIze insider ownership and return on assets (Bhat 2000 Vol garis Asteriou and

Agiomirgianakis 2002) From the above variables cash flows insider ownership and firm size

could be categorized as internal firms characteristics and capital expenditure plants and

equipments and shareholder fund as firm strategic action Those variables are important as they

significantly affect firm performance Presented below is a comprehensive framework of key

success factor for property sector

I Competitive advantage is the taking of offensive or defensive actions in order to create a defendable position in an

industry

4

q Figure 1 Key Success Factor for Property Sector

~CI

Firm Performance

ROA

Drivers

~i ~~ 3a ~i ~~ 11)=gt3111 rIJshyn ~~

Internal Firms Characteristics Firms Strategic Action

Plant amp Equipment

Cash Flow

Insider Ownership

Size Capital Expenditure

Shareholder Fund

5

------------------~-------------~-

The performance of a firm is always measured by return on asset or return on equity and

one of the ways to achieve high perfonnance is improving the return on assets of company

Return on assets has significant impact towards company performance as it enabled a firm to

have an effective maintenance system which tends to increase profits and improve competitive

edge Return on assets represents the efficiency of assets utilization in a company ~Iigh return on

assets tends to affect the efficient management of a company (Bhat 2000)

A greater cash flow is said to increase the risk of being take over by other finns (Davis and

Stout 1992) This is because firm holding free cash flow may find it hard to perform due to the

increase government pressures This happened in the long run when the financial markets and

legal systems become more strengthened (Brush Bromiley and Hendrickx 2000) Firms with

large cash flow tend to have higher rates of return up to one year start from the day they are

identified by value line However they only out perform firms that are of similar size (Stephen

and Joseph 2000) The author noted that free cash flow hypothesis predicts that firms that are

overinvesting will face pressure form investors Thus the cash flow will distribute to

shareholders instead of reinvest in the finn The study further found that by using Tobins Q in

the analysis finns with low Q and high free cash flow should have a superior performance postshy

listing as they are forced to use their cash flow in a more efficient way

Other than this size of a firm has the ability to affect firm performance Firm with larger

size is considered to be more efficient compared to firm with smaller size Small firms are less

competitive as they have less power However firms might suffer from inefficiency when they

become larger Thus cause inferior financial performance (Majumdar 1997) Other than this

6

--- - -- ===============~==~======~~====~~~ -

firms with larger size tend to have an easy access to loans especially longer-term loans and this is

considered to affect sales and profit of a firm (Topalova 2004)

Other than that a higher equity ownership will enhance the interest of the controlling

shareholders in non-stationary distribution of dividends (Filatotchev et aI 2001 La Porta et aI

2000a) Merton (1974) noted that there is a positive relationship between equity volatility and

shareholder wealth Equity holders have the incentive to increase cash flow volatility of a firm

(Jensen and Meckling 1976) However there are literatures showing that equity volatility caused

both positive and negative impact towards shareholder wealth Shareholder wealth is proved to

decrease more when there is an increase in equity volatility for firms with low interest coverage

low investment low cash flow and high leverage (Shin and Stulz 2000)

Plants and equipments is the physical assets owns by a company that cannot quickly

convert to cash It is one of the investments of a company The return on investment generates

from plants and equipments able to help a company in sustaining growth The decrease in plants

and equipments investment tends to affect performance of a firm Revaluation of plants and

equipments is proved to improve forecasts of future earnings in the case that dividends may be

paid

One of the important factors that have to be concerned is the capital expenditure of a firm

The capital expenditure of a company is significantly related to profitability Generally

profitability is related inversely to the liability Thus the more debt a company incurs the worse

its earnings An appropriate capital expenditure allows firms to minimize capital structure Thus

7

- - oVloj ~l

reduce the total costs of firms Capital expenditures have a negative relationship with future

returns of firms (Baker Stein and Wurgler 2003)

The value of a company is made up of debt and equity Debt can boost as weH as hurts

company performance A moderate debt allowed company to gain market shares while an

excessive debt will bring about market share losses Debt is considered to create a better

monitoring opportunities The presence of debt enabled cash flow claims contractually set at the

time of borrowing However the failure to meet the claims will lead to bankruptcy or loss of

control over an asset even the entire firm (Damodaran 2009) Firms that are more likely to issue

debt are those with financial needs Thus financial deficits have become the determinant of the

decision to issue debt (Diamond 1991)

Debt has been analyzed as disciplinary in the shareholders-manager conflict Debt tends to

help in managing the conflict as it is easier to control the shareholders in modifying the leverage

ratio than to adjust the share of capital (Bruslerie and Latrous 2007) Debt improves company

performance in which it allows shareholders to select the first-best investment policy It reduces

the distortion in shareholders investment incentives (Lyandres and Zhdanov 2007)

11 An Overview of Malaysia Property Market

Malaysia real estate is expected to warm up in the second half of 20 1 0 before ushering

in the Spring in 2011 (Borneo Post Business 30122009) Malaysia property market is on an

upward trend as the prices of middle class suburban property is rising due to the steady stock

8

---~7T7r---------~~-------------------------- --------------r~------------------ J

market movement Generally high rise residential units in Kuala Lumpur increase about 12 to 18

per cent per annum for the last 15 to 20 years The demand is expected to continue as a result of

the limited land space stated by the Director of Ho Chin Soon Research

Sarawak one of the states of Malaysia recorded the highest increased in 2008 which was

about 47 The performance of the Sarawak property market moderated in HI 2009 There were

11867 transactions recorded in HI 2009 with a total value of RMl 66 billion Compared to the

HI and H2 2008 the volume of transactions increased by 1l1 but decreased by l2

respectively Value of transactions showed the same movement that is increased by 48 against

HI 2008 but decreased by 78 against H2 2008

Residential property sub-sector continued to lead in market share accounting for 468

followed by agricultural (360) commercial (101) development land (44) and industrial

(28) sub-sectors Volume of transactions in residential commercial and industrial sub sectors

was higher against HI 2008 but lower compared to H2 2008 Conversely agricultural sub-sector

noted the opposite movement whereas development land sub-sector rose against both halves of

2008 In terms of value residential and development land sub-sectors increased against HI 2008

but decreased against H2 2008 Conversely commercial and agricultural sub-sectors declined

against both halves of 2008 whilst industrial sub-sector noted higher value Sarawak lead to the

highest increased in year 2008 followed by Labuan (253) and Kuala Lumpur (25)

The yield on property investments is considered much higher than the yield on a similar

sum generates in other types of investments In order to strengthen Malaysia property market

9

Malaysia government had come out with various programs to encourage foreign investor to

purchase residential properties in order to increase the inflow of foreign currency as well as to

encourage property development and other sector such as construction

In Malaysia large greenfield developments are considered costly to build when housing

market for residential properties has reached the equilibrium Malaysian developers who involved

in Greenfield projects will have to spend large amount of time and money as they have to provide

infrastructure such as roads communication cables substations electricity waste water treatment

plant and street lighting where all these cost are always borne by the local councilor the state

government in other countries

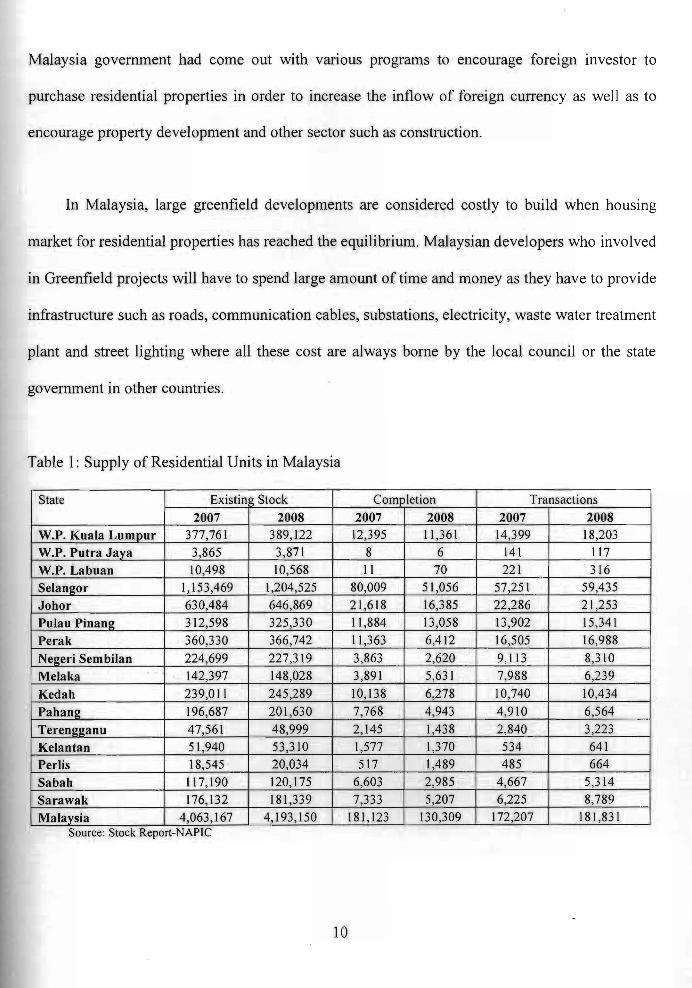

Table I Supply of Residential Units in Malaysia

State Existin o Stock Completion Transactions

2007 2008 2007 2008 2007 2008 WP Kuala Lumpur 377761 389122 12395 11361 14399 18203

WP Putra Jaya 3865 3871 I 8 6 141 117

WP Labuan 10498 10568 11 70 221 316

Selangor 1153469 1204525 80009 51056 57251 59435

Johor 630484 646869 21 618 16385 22286 21253

Pulau Pinang 312598 32~330 11884 13058 13902 15341

Perak 360330 366742 11363 6412 16505 16988

Negeri Sembilan 224699 227319 3863 2620 I 9113 8310

Melaka 142397 148028 3891 5631 7988 6239

Kedah 239011 245289 10138 6278 10740 10434

Pahang 196687

47561

201630 7768 4943 4910 6564

Terengganu 48999 2145 1438 2840 3223

Kelantan 51940 53310 1577I I 1370 534 641 I

Perlis 18545 20034 517 1489 485 664

Sabah 117190 120175 6603 I 2985 4667 5314

Sarawak 176132 181339 7333 5207 6225 8789

Malaysia II 4063167 4193 150 181123 130309 172207 181831 Source Stock Report-NAPIC

10

The numbers of housing are considered overbuilding There were 4193150 units of houses

in Malaysia in 2008 and 130309 were completed

In terms of transactions Selangor accounted for the largest number (59435) followed by

lohor (21253) and Kuala Lumpur (18203) Kuala Lumpur had 389122 homes and the largest

number of homes is in Selangor with 1204525 homes Perak comes forth with 366742

There were large numbers of unsold property Due to this developers will have to face

problem of unsold stock and on the same time they will have to bear the maintenance cost for

providing free infrastructure and the costs of obtaining approvals for development

There is a need to realign the number of units coming into the marketplace in terms of

consumers affordability as economic slowdown Other than this subsidies should also give to

fist-time home buyers so that they are afford to have their first home

Banks do provide various types of financing for property development It includes a wide

range of debt and equity instruments depend on the needs of the projects The purpose of

financing is to encourage developers and construction firms to reinvest in new projects Return

on assets allowed investors to know how well a company has been using its capital assets and

equity The higher the returns the more likely the company is going to generate profit

11

Table 2 Total Transaction Values (RMm)

Sector 1H08 1H09 2H08 2H09 FY08 FY09 YoY

Residential 2078265 1764710 2052132 2053509 4130397 3818219 -756

Commercial 843955 684591 817636 848961 1661591 1533552 -771 I

Industrial 407991 324113 I 381752 321443 789743 645556 -1826 I

Agricultural 439135 361146 412076 427401 851211 788547 -736

Development 876319 445376 524626 360437 1400945 I 805813 -4248

Others 046 031 251 1116 297 1147 28620

Total 4645665 3579967 4188473 4012867 8834184 7592834 -1405 Source JPPH and MIDFR

Table 3 Total Number of Transaction

Sector I 1H08 1H09 2H08 2H09 FY08 I FY09 YoY Residential II 108040 96859 I 108662 114821 216702 211680 -232

~~~

Commercial 15259 14571 16490 18782 31749 33353 505

Industrial 3972 3596 4154 4465 8126 8061 -080 Agricultural 36659 32793 32295 36433 68954 69226 039 Development 7611 7367 7091 I 8274 14702 15641 639 Others I 10 6 19 7 29 31429 Total 171542 155196 168698 182794 340240 337990 -066

Source JPPH and MIDFR

The KL Property index performed in line with FBM KLCI which gam +486ytd as

compared to the broader market of +451 The Malaysian Home Price Index (MHPI) indicated

that the performance of MHPI was stable in 4Q08 until 2Q09 during the time when the economy

was at its most vulnerable

Refer to a report prepared by MIDF AMANAH INVESTMENT BANK BERHAD on

equity beat it stated that the recovery in 2H09 was because of i) lower cost of funds ii)

innovative promotional package iii) liberalization of policies and iv) the RM670 billion

economic stimulus

12

swings that that

people decided

The property market surprised many as it performed stronger than the broader market in

2009 Property sector showed a marginal -066yoy declined in total number of transaction in

comparison with -1405yoy declined in the value of property Residential propel ties continued

to lead the market which accounted for 60 of total property transactions and about 50 of total

value transacted in 2009 The high demand was due to mid-end property type that is vast liquidity

Its yield and easy disposal made it popular among investor especially during a challenging

economy

12 Problem Statements

The recent uncertainty in the stock market seems to affect property market The wide

cause uncertainty in the property market tend to affect the confidence of

investors A fall in the stock market tends to increase the demand for property where many

to invest in property as a hedge against stock market fluctuations Overall

confidence of the purchasers seems to be the largest factor affects the demand of property

Ever since the strike of world financial crisis and a shrinking economy with the falling

demand of exports it is the time for us to re-evaluate the management of countrys real estate

There is still lack of the participation of foreign investors in this sector to drive its marketability

The slowdown of global economic policy flip flops as well as slow liberalization measures do

not seemed to build up confidence in property sector The slowdown in Malaysias economy has

caused the stocks and real estate turn sluggish It is therefore important for us to analyze the

13

performance of Malaysias property market to build up confidence in people who adopt the wait

and see attitude in view of the uncertainty in the world economy

13 Objective

The objective of this study is to identify the key success factors that affect Malaysia

property companies performance

14 Significant and Scope of the Study

This study is important as it identify the performance of Malaysias property market It

enables investors to make the decision on whether they should invest in property as the

slowdown in Malaysia economy has caused its traditional investment instruments such as real

estate become slowly moving It is hope that this study will help to improve the international

marketing in order to overcome the sluggishness in local demand of countrys real estate

This study is based on panel data from Thompsom Financial database The sample data

will emphasized on at least 10 years on shareholder funds cash flow capital expenditure plants

and equipments size and insider ownership from year 1999-2008 The sample data included

return on assets (ROA) where most of the previous studies using it to measure company

performance

14

1

fusat Kbidmat Makiumat Akademik ~lJyenE~m MAlAYSIA SARAWAK

PKHIOMAT MAKLUMAT AKAOEMIK

1IIIIIIIIIIi~illllllllll 1000246477

COMPANY PERFORMANCE AND ITS DETERMINANTS AN ANALYSIS OF MALAYSIA

PROPERTY LISTED COMPANIES

LEONG SlAW HUA

A dissertation submitted in partial fulfillment of the requirements for the degree of Corporate Master in Business Administration

Faculty of Economics and Business UNIVERSITI MALAYSIA SARAWAK

2010

DECLARATION AND COPYRIGHT

Name Leong Siaw Hua

Matric Number 08031525

I hereby declare that this research is the result of my own investigation except where otherwise stated Other sources are acknowledged by footnotes giving explicit references and bibliography is appended

Signature

Date

copy Copyright by Leong Siaw Hua and Universiti Malaysia Sarawak

ii

-V~~~-----------Y---------------------------------------------------------~

ACKNOWLEDGEMENTS

- r J

My pnmary acknowledgement and appreciations to those who aided me in

accomplishing my final year project First of all I would like to express my special thanks to

my supervisor for his guidance and valuable advises in completing my project

I am pleased to acknowledge to the lecturers in Faculty Economic and Business upon

their willingness and patient in guiding me and helping me in finishing this project

Apart from that I would Like to take this opportunity to thank both my parents for their

concern understanding and encouragement along the way Not to forget to thank my friends

for their guidance suggestion opinion and sharing of information in accomplishing this

project

III

-

ABSTRACT

COMPANY PERFORMANCE AND ITS DETERMINANTS AN ANAYSIS OF

MALA YSIA PROPERTY LISTED COMPANIES

By

Leong Siaw Hua

( The purpose of this study is to identify the key success factors that affect Malaysia property

companies performance The hypothesis of property company performance and its

determinants are tested using annual time series data from 1999-2008 The analysis reveals

that the coefficient for shareholder fund capital expenditure and plants and equipments are

negative where an increase in shareholder fund capital expenditure and plants and

equipments will cause return on assets to decreas~ This happened when firms internal

characteristics (cash flows insider ownership and firm size) are include in the regression

analysis indicating that the efficiency of investment in plant and property and equipment and

capital expenditure are very much depended on firms internal characteristics There is the

rejection of null hypothesis at 1 per cent significant level for all the variables except for

capital expenditure and cash flow However positive relationship is found between capital

expenditure plants and equipments and return on assets when they are tested in a separate

regression The results further showed that the return on assets shows negative in figure and is

fluctuated throughout the years where the percentage of profit became smaller in year 2008 as

compared to year 2007

iv

ABSTRAK

PRESTASI SYARIKA T DAN PENENTU FAKTORNY A ANALISIS TERHADAP SYARIKAT BARTA BENDA MALAYSIA TERSENARAI

Oleh

Leong Siaw Bua

Tujuan kajian ini adalah untuk mengenal pasti faktor pengunci kejayaan yang mempengaruhi

kerjayaan syarikat harta benda Malaysia tersenarai Hipotesis kajian diuji dengan

menggunakan data siri masa dari tahun 1999 sehingga tahun 2000 Hipotesis mendedahkan

bahawa angkari bagi pemegang dana modal perbelanjaan dan loji dan peralatan adalah

negatif di mana peningkatan dalam pemegang dana modal perbelanjaan dal loji dan

peralatan akan menyebabkan pemulangan asset berkurangan Ini berlaku apabila cirri-ciri

syarikat dalaman (aliran tunai pemilikan dalaman and saiz syarikat) dimasukan dalam

kemunduran anal isis menunjukkan kecekapan pelaburan dalam kilang and harta benda dan

peralatan dan modal perbelanjaan adalah bergantung pada cirri-ciri syarikat dalaman Dengan

ini penolakan daripada null hipotesis pada satu peratus kemantapan paras bagi semua

pemboleh ubahnya kecuali modal perbelanjaan dan aliran tunai Walau bagaimanapun

hubungan positif didapati di antara modal perbelanjaan dan loji dan peralatan dengan

pemulangan dalam asset ketika diuji dalam regression yang berasingan Pemulangan dalam

asset menunjukkan angka negatif dan tidak tetap melintasi tahun di mana peratus dari

keuntungan menjadi semakin kurang pada tahun 2008 dibandingkan dengan tahun 2007

v

-- VOLi

Pusat Khidmat Maklumat Akademik ~IVERSm MALAYSIA SARAWAK

T ABLE OF CONTENTS

DECLARATION AND COPyRIGHT II

ACKNOWLEDGEMENT III

LIST OF TABLES viii

LIST OF FIGURES IX

ABSTRACT IV

ABSTRAK V

CHAPTER ONE INTRODUCTION

10 Introduction

11 An Overview of Malaysia Property Market 8

12 Problem Statements 13

13 Objective 14

14 Significant and scope ofthe Study 14

15 Summary 15

CHAPTER TWO LITERATURE REVIEW

20 Introduction 16

21 Relationship between Return on Assets Plant and Equipment and Company 16

Performance

22 Relationship between Capital Expenditure Debts and Cash Flows toward 18

Company Performance

23 Relationship between Size and Company Performance 21

24 Relationship between Shareholder Funds and Company Performance 22

25 Relationship between Insider Ownership and Company Performance 23

VI

~107i7 1

26 Summary 25

CHAPTERTHREEMETHOLOGY

30 Introduction 26

31 Hypotheses 26

32 Research Design 29

321 Data Sample and Data Collection 29

322 Empirical Model 30

33 Summary 31

CHAPTER FOUR EMPIRICAL RESULTS

40 Introduction 32

41 Descriptive Statistics 33

42 Regression Analysis 34

43 Summary 39

CHAPTER FIVE CONCLUSION AND RECOMMENDATIONS

50 Introduction 41

51 Summary and Findings of the Study 41

52 Limitation of Study 44

53 The Underlying Factors of the Market and Implications 45

54 Conclusion 47

REFERENCES 48

VII

-~-------------- - ---shy

LIST OF TABLES

Title Page

Table 1 Supply of Residential Units in Malaysia 10

Table 2 Total Transaction Values (RMm) 12

Table 3 Total Number of Transaction 12

Table 4 Summary Statistics of the Variables 33

Table 5 Result of Insider Ownership Cash Flow and Size 34

Table 6 Result of Plants and Equipments Capital Expenditures and Shareholder 35 Fund

Table 7 Result of Panel Least Square Regression 36

VIII

LIST OF FIGURES

Title Page

Figure 1 Key Success Factor for Property Sector 5

Figure 2 Factors affect Company Performance in Property Sector 26

Figure 3 Return on Assets 38

IX

IOZ17J I

CHAPTER ONE

INTRODUCTION

10 Introduction

Malaysia experienced a strong beating from global financial crisis in the first half of 2009

as the Gross Domestic Product (GDP) contracted significantly Since then there were some

positive movements in some economic indicators in 3rd quarter due to the government national

recovery packages that restore market confidence and maintain the stability of financial market

and expectation of positive growth in the 4th quarter and these growth show evidence that

Malaysia is out of recession and there is still an upside potential in the investment of property in

Malaysia There are signs of improvement on the worldwide economy where stocks that

decreased in value previously are strong enough to get back to the market For example Dow

Jones gained 40 after their March low

The slowdown in Malaysias economy has caused Malaysians become more cautious with

their investment in properties However property prices in Malaysia remain one of the most

competitive in the region They offer stronger investment returns as compared to its neighboring

countries

In encouraging foreign investments economy liberalization measure introduced by the

government has made 2009 a significant new era in Malaysias development history The

comprehensive package with new policies are said to have a significant impact towards real

--- --------- - -------- - -

estate sector as the restrictions for foreign investors to purchase the properties in Malaysia had

been removed These measures aimed to increase the number of transactions and attract overseas

investment

Plants and equipments one of the firms strategic action is the main factor to determine the

success of property sector Bhat (2000) noted that the age of property company size plant and

equipment building and return on assets can help to increase profits and improve the

competitive edge of a company Porter (1989) states that the key success factor for property

sector depend on internal factors and external factors Internal factors especially plants and

equipments is the key success factor of property sector because they are valuable and imitability

as a strategic location determined the success of a property company The author stated that

looking for locations that are economically attractive is one of the critical dimensions of success

Kamarulzaman Hassan the analyst of T A Securities Holdings Berhad support this point by stated

that location of property is an issue besides demand and supply Bhat (2000) support that plants

and equipments determined the cost and revenue as they have direct impact on maintenance

expenditures However Porter (1989) stated that imitating is profitable if the industry is great but

it will become a way of insuring disaster if the industry is less attractive

Population in an area is the important factor which determined the demand and supply of

property Supply and demand is the backbone of a market economy The demand is high when

there is a larger population The standard of living and the development land affect the choice of

consumers in their decision making on the types of property and the location to invest This is

supported by Porter (1989) where tremendous demand for new building and demographic shift in

2

rates

the populatjon is the important factor for property sector In the concept of economics price is a

reflection of supply and demand Property contained large per cent of buyers cost Oversupply

will force the price to go down as the demand is less than the supply in the market However this

is no longer happened as developers know how to control the situation after experienced the crisis

hits on 1987 and 1997

In Porter 5 forces suppliers are the determinant factors that affect the profits gained and the

costs to customers The materials used in the construction of property tend affect the price and

this will be the burden of customers Barney (1991) noted that resources owned must enabled a

finn outperfonn its competitors The resources are carefully managed in order to achieve the

objective of sustainable development Malaysia has no problem on materials such as sand and

cement as Malaysia is the sole proprietor However material such as steel is said to affect the

costs of construction as the price of steel is depend on world market which subject to exchange

The threat of new entrants into the market is said to affect the profit gained as the entry

barriers are low Porter (1989) noted that the situation of rivalry in property sector has always

been active where a lot of new competitors have come in The competitors have enough capital to

finance a lot of new projects The increasing number of competitors combined with slowing

demand has led to overcapacity which caused the profit to drop

3

Poter (1989) stated that there are two ways property firms can gain competitive advantage I

One is lowest cost and another one is differentiation Property firms managed to gain higher

margin at prevailing price levels if they are able to develop and finance their projects and deliver

at a lower cost The author further stated that property firms can better utilizE the land or gain

higher profits per square foot if they are skilled in employing new concepts into projects or

skilled in property design

Other financial factors are debt equity cash flows capital expenditure plants and

equipments SIze insider ownership and return on assets (Bhat 2000 Vol garis Asteriou and

Agiomirgianakis 2002) From the above variables cash flows insider ownership and firm size

could be categorized as internal firms characteristics and capital expenditure plants and

equipments and shareholder fund as firm strategic action Those variables are important as they

significantly affect firm performance Presented below is a comprehensive framework of key

success factor for property sector

I Competitive advantage is the taking of offensive or defensive actions in order to create a defendable position in an

industry

4

q Figure 1 Key Success Factor for Property Sector

~CI

Firm Performance

ROA

Drivers

~i ~~ 3a ~i ~~ 11)=gt3111 rIJshyn ~~

Internal Firms Characteristics Firms Strategic Action

Plant amp Equipment

Cash Flow

Insider Ownership

Size Capital Expenditure

Shareholder Fund

5

------------------~-------------~-

The performance of a firm is always measured by return on asset or return on equity and

one of the ways to achieve high perfonnance is improving the return on assets of company

Return on assets has significant impact towards company performance as it enabled a firm to

have an effective maintenance system which tends to increase profits and improve competitive

edge Return on assets represents the efficiency of assets utilization in a company ~Iigh return on

assets tends to affect the efficient management of a company (Bhat 2000)

A greater cash flow is said to increase the risk of being take over by other finns (Davis and

Stout 1992) This is because firm holding free cash flow may find it hard to perform due to the

increase government pressures This happened in the long run when the financial markets and

legal systems become more strengthened (Brush Bromiley and Hendrickx 2000) Firms with

large cash flow tend to have higher rates of return up to one year start from the day they are

identified by value line However they only out perform firms that are of similar size (Stephen

and Joseph 2000) The author noted that free cash flow hypothesis predicts that firms that are

overinvesting will face pressure form investors Thus the cash flow will distribute to

shareholders instead of reinvest in the finn The study further found that by using Tobins Q in

the analysis finns with low Q and high free cash flow should have a superior performance postshy

listing as they are forced to use their cash flow in a more efficient way

Other than this size of a firm has the ability to affect firm performance Firm with larger

size is considered to be more efficient compared to firm with smaller size Small firms are less

competitive as they have less power However firms might suffer from inefficiency when they

become larger Thus cause inferior financial performance (Majumdar 1997) Other than this

6

--- - -- ===============~==~======~~====~~~ -

firms with larger size tend to have an easy access to loans especially longer-term loans and this is

considered to affect sales and profit of a firm (Topalova 2004)

Other than that a higher equity ownership will enhance the interest of the controlling

shareholders in non-stationary distribution of dividends (Filatotchev et aI 2001 La Porta et aI

2000a) Merton (1974) noted that there is a positive relationship between equity volatility and

shareholder wealth Equity holders have the incentive to increase cash flow volatility of a firm

(Jensen and Meckling 1976) However there are literatures showing that equity volatility caused

both positive and negative impact towards shareholder wealth Shareholder wealth is proved to

decrease more when there is an increase in equity volatility for firms with low interest coverage

low investment low cash flow and high leverage (Shin and Stulz 2000)

Plants and equipments is the physical assets owns by a company that cannot quickly

convert to cash It is one of the investments of a company The return on investment generates

from plants and equipments able to help a company in sustaining growth The decrease in plants

and equipments investment tends to affect performance of a firm Revaluation of plants and

equipments is proved to improve forecasts of future earnings in the case that dividends may be

paid

One of the important factors that have to be concerned is the capital expenditure of a firm

The capital expenditure of a company is significantly related to profitability Generally

profitability is related inversely to the liability Thus the more debt a company incurs the worse

its earnings An appropriate capital expenditure allows firms to minimize capital structure Thus

7

- - oVloj ~l

reduce the total costs of firms Capital expenditures have a negative relationship with future

returns of firms (Baker Stein and Wurgler 2003)

The value of a company is made up of debt and equity Debt can boost as weH as hurts

company performance A moderate debt allowed company to gain market shares while an

excessive debt will bring about market share losses Debt is considered to create a better

monitoring opportunities The presence of debt enabled cash flow claims contractually set at the

time of borrowing However the failure to meet the claims will lead to bankruptcy or loss of

control over an asset even the entire firm (Damodaran 2009) Firms that are more likely to issue

debt are those with financial needs Thus financial deficits have become the determinant of the

decision to issue debt (Diamond 1991)

Debt has been analyzed as disciplinary in the shareholders-manager conflict Debt tends to

help in managing the conflict as it is easier to control the shareholders in modifying the leverage

ratio than to adjust the share of capital (Bruslerie and Latrous 2007) Debt improves company

performance in which it allows shareholders to select the first-best investment policy It reduces

the distortion in shareholders investment incentives (Lyandres and Zhdanov 2007)

11 An Overview of Malaysia Property Market

Malaysia real estate is expected to warm up in the second half of 20 1 0 before ushering

in the Spring in 2011 (Borneo Post Business 30122009) Malaysia property market is on an

upward trend as the prices of middle class suburban property is rising due to the steady stock

8

---~7T7r---------~~-------------------------- --------------r~------------------ J

market movement Generally high rise residential units in Kuala Lumpur increase about 12 to 18

per cent per annum for the last 15 to 20 years The demand is expected to continue as a result of

the limited land space stated by the Director of Ho Chin Soon Research

Sarawak one of the states of Malaysia recorded the highest increased in 2008 which was

about 47 The performance of the Sarawak property market moderated in HI 2009 There were

11867 transactions recorded in HI 2009 with a total value of RMl 66 billion Compared to the

HI and H2 2008 the volume of transactions increased by 1l1 but decreased by l2

respectively Value of transactions showed the same movement that is increased by 48 against

HI 2008 but decreased by 78 against H2 2008

Residential property sub-sector continued to lead in market share accounting for 468

followed by agricultural (360) commercial (101) development land (44) and industrial

(28) sub-sectors Volume of transactions in residential commercial and industrial sub sectors

was higher against HI 2008 but lower compared to H2 2008 Conversely agricultural sub-sector

noted the opposite movement whereas development land sub-sector rose against both halves of

2008 In terms of value residential and development land sub-sectors increased against HI 2008

but decreased against H2 2008 Conversely commercial and agricultural sub-sectors declined

against both halves of 2008 whilst industrial sub-sector noted higher value Sarawak lead to the

highest increased in year 2008 followed by Labuan (253) and Kuala Lumpur (25)

The yield on property investments is considered much higher than the yield on a similar

sum generates in other types of investments In order to strengthen Malaysia property market

9

Malaysia government had come out with various programs to encourage foreign investor to

purchase residential properties in order to increase the inflow of foreign currency as well as to

encourage property development and other sector such as construction

In Malaysia large greenfield developments are considered costly to build when housing

market for residential properties has reached the equilibrium Malaysian developers who involved

in Greenfield projects will have to spend large amount of time and money as they have to provide

infrastructure such as roads communication cables substations electricity waste water treatment

plant and street lighting where all these cost are always borne by the local councilor the state

government in other countries

Table I Supply of Residential Units in Malaysia

State Existin o Stock Completion Transactions

2007 2008 2007 2008 2007 2008 WP Kuala Lumpur 377761 389122 12395 11361 14399 18203

WP Putra Jaya 3865 3871 I 8 6 141 117

WP Labuan 10498 10568 11 70 221 316

Selangor 1153469 1204525 80009 51056 57251 59435

Johor 630484 646869 21 618 16385 22286 21253

Pulau Pinang 312598 32~330 11884 13058 13902 15341

Perak 360330 366742 11363 6412 16505 16988

Negeri Sembilan 224699 227319 3863 2620 I 9113 8310

Melaka 142397 148028 3891 5631 7988 6239

Kedah 239011 245289 10138 6278 10740 10434

Pahang 196687

47561

201630 7768 4943 4910 6564

Terengganu 48999 2145 1438 2840 3223

Kelantan 51940 53310 1577I I 1370 534 641 I

Perlis 18545 20034 517 1489 485 664

Sabah 117190 120175 6603 I 2985 4667 5314

Sarawak 176132 181339 7333 5207 6225 8789

Malaysia II 4063167 4193 150 181123 130309 172207 181831 Source Stock Report-NAPIC

10

The numbers of housing are considered overbuilding There were 4193150 units of houses

in Malaysia in 2008 and 130309 were completed

In terms of transactions Selangor accounted for the largest number (59435) followed by

lohor (21253) and Kuala Lumpur (18203) Kuala Lumpur had 389122 homes and the largest

number of homes is in Selangor with 1204525 homes Perak comes forth with 366742

There were large numbers of unsold property Due to this developers will have to face

problem of unsold stock and on the same time they will have to bear the maintenance cost for

providing free infrastructure and the costs of obtaining approvals for development

There is a need to realign the number of units coming into the marketplace in terms of

consumers affordability as economic slowdown Other than this subsidies should also give to

fist-time home buyers so that they are afford to have their first home

Banks do provide various types of financing for property development It includes a wide

range of debt and equity instruments depend on the needs of the projects The purpose of

financing is to encourage developers and construction firms to reinvest in new projects Return

on assets allowed investors to know how well a company has been using its capital assets and

equity The higher the returns the more likely the company is going to generate profit

11

Table 2 Total Transaction Values (RMm)

Sector 1H08 1H09 2H08 2H09 FY08 FY09 YoY

Residential 2078265 1764710 2052132 2053509 4130397 3818219 -756

Commercial 843955 684591 817636 848961 1661591 1533552 -771 I

Industrial 407991 324113 I 381752 321443 789743 645556 -1826 I

Agricultural 439135 361146 412076 427401 851211 788547 -736

Development 876319 445376 524626 360437 1400945 I 805813 -4248

Others 046 031 251 1116 297 1147 28620

Total 4645665 3579967 4188473 4012867 8834184 7592834 -1405 Source JPPH and MIDFR

Table 3 Total Number of Transaction

Sector I 1H08 1H09 2H08 2H09 FY08 I FY09 YoY Residential II 108040 96859 I 108662 114821 216702 211680 -232

~~~

Commercial 15259 14571 16490 18782 31749 33353 505

Industrial 3972 3596 4154 4465 8126 8061 -080 Agricultural 36659 32793 32295 36433 68954 69226 039 Development 7611 7367 7091 I 8274 14702 15641 639 Others I 10 6 19 7 29 31429 Total 171542 155196 168698 182794 340240 337990 -066

Source JPPH and MIDFR

The KL Property index performed in line with FBM KLCI which gam +486ytd as

compared to the broader market of +451 The Malaysian Home Price Index (MHPI) indicated

that the performance of MHPI was stable in 4Q08 until 2Q09 during the time when the economy

was at its most vulnerable

Refer to a report prepared by MIDF AMANAH INVESTMENT BANK BERHAD on

equity beat it stated that the recovery in 2H09 was because of i) lower cost of funds ii)

innovative promotional package iii) liberalization of policies and iv) the RM670 billion

economic stimulus

12

swings that that

people decided

The property market surprised many as it performed stronger than the broader market in

2009 Property sector showed a marginal -066yoy declined in total number of transaction in

comparison with -1405yoy declined in the value of property Residential propel ties continued

to lead the market which accounted for 60 of total property transactions and about 50 of total

value transacted in 2009 The high demand was due to mid-end property type that is vast liquidity

Its yield and easy disposal made it popular among investor especially during a challenging

economy

12 Problem Statements

The recent uncertainty in the stock market seems to affect property market The wide

cause uncertainty in the property market tend to affect the confidence of

investors A fall in the stock market tends to increase the demand for property where many

to invest in property as a hedge against stock market fluctuations Overall

confidence of the purchasers seems to be the largest factor affects the demand of property

Ever since the strike of world financial crisis and a shrinking economy with the falling

demand of exports it is the time for us to re-evaluate the management of countrys real estate

There is still lack of the participation of foreign investors in this sector to drive its marketability

The slowdown of global economic policy flip flops as well as slow liberalization measures do

not seemed to build up confidence in property sector The slowdown in Malaysias economy has

caused the stocks and real estate turn sluggish It is therefore important for us to analyze the

13

performance of Malaysias property market to build up confidence in people who adopt the wait

and see attitude in view of the uncertainty in the world economy

13 Objective

The objective of this study is to identify the key success factors that affect Malaysia

property companies performance

14 Significant and Scope of the Study

This study is important as it identify the performance of Malaysias property market It

enables investors to make the decision on whether they should invest in property as the

slowdown in Malaysia economy has caused its traditional investment instruments such as real

estate become slowly moving It is hope that this study will help to improve the international

marketing in order to overcome the sluggishness in local demand of countrys real estate

This study is based on panel data from Thompsom Financial database The sample data

will emphasized on at least 10 years on shareholder funds cash flow capital expenditure plants

and equipments size and insider ownership from year 1999-2008 The sample data included

return on assets (ROA) where most of the previous studies using it to measure company

performance

14

1

DECLARATION AND COPYRIGHT

Name Leong Siaw Hua

Matric Number 08031525

I hereby declare that this research is the result of my own investigation except where otherwise stated Other sources are acknowledged by footnotes giving explicit references and bibliography is appended

Signature

Date

copy Copyright by Leong Siaw Hua and Universiti Malaysia Sarawak

ii

-V~~~-----------Y---------------------------------------------------------~

ACKNOWLEDGEMENTS

- r J

My pnmary acknowledgement and appreciations to those who aided me in

accomplishing my final year project First of all I would like to express my special thanks to

my supervisor for his guidance and valuable advises in completing my project

I am pleased to acknowledge to the lecturers in Faculty Economic and Business upon

their willingness and patient in guiding me and helping me in finishing this project

Apart from that I would Like to take this opportunity to thank both my parents for their

concern understanding and encouragement along the way Not to forget to thank my friends

for their guidance suggestion opinion and sharing of information in accomplishing this

project

III

-

ABSTRACT

COMPANY PERFORMANCE AND ITS DETERMINANTS AN ANAYSIS OF

MALA YSIA PROPERTY LISTED COMPANIES

By

Leong Siaw Hua

( The purpose of this study is to identify the key success factors that affect Malaysia property

companies performance The hypothesis of property company performance and its

determinants are tested using annual time series data from 1999-2008 The analysis reveals

that the coefficient for shareholder fund capital expenditure and plants and equipments are

negative where an increase in shareholder fund capital expenditure and plants and

equipments will cause return on assets to decreas~ This happened when firms internal

characteristics (cash flows insider ownership and firm size) are include in the regression

analysis indicating that the efficiency of investment in plant and property and equipment and

capital expenditure are very much depended on firms internal characteristics There is the

rejection of null hypothesis at 1 per cent significant level for all the variables except for

capital expenditure and cash flow However positive relationship is found between capital

expenditure plants and equipments and return on assets when they are tested in a separate

regression The results further showed that the return on assets shows negative in figure and is

fluctuated throughout the years where the percentage of profit became smaller in year 2008 as

compared to year 2007

iv

ABSTRAK

PRESTASI SYARIKA T DAN PENENTU FAKTORNY A ANALISIS TERHADAP SYARIKAT BARTA BENDA MALAYSIA TERSENARAI

Oleh

Leong Siaw Bua

Tujuan kajian ini adalah untuk mengenal pasti faktor pengunci kejayaan yang mempengaruhi

kerjayaan syarikat harta benda Malaysia tersenarai Hipotesis kajian diuji dengan

menggunakan data siri masa dari tahun 1999 sehingga tahun 2000 Hipotesis mendedahkan

bahawa angkari bagi pemegang dana modal perbelanjaan dan loji dan peralatan adalah

negatif di mana peningkatan dalam pemegang dana modal perbelanjaan dal loji dan

peralatan akan menyebabkan pemulangan asset berkurangan Ini berlaku apabila cirri-ciri

syarikat dalaman (aliran tunai pemilikan dalaman and saiz syarikat) dimasukan dalam

kemunduran anal isis menunjukkan kecekapan pelaburan dalam kilang and harta benda dan

peralatan dan modal perbelanjaan adalah bergantung pada cirri-ciri syarikat dalaman Dengan

ini penolakan daripada null hipotesis pada satu peratus kemantapan paras bagi semua

pemboleh ubahnya kecuali modal perbelanjaan dan aliran tunai Walau bagaimanapun

hubungan positif didapati di antara modal perbelanjaan dan loji dan peralatan dengan

pemulangan dalam asset ketika diuji dalam regression yang berasingan Pemulangan dalam

asset menunjukkan angka negatif dan tidak tetap melintasi tahun di mana peratus dari

keuntungan menjadi semakin kurang pada tahun 2008 dibandingkan dengan tahun 2007

v

-- VOLi

Pusat Khidmat Maklumat Akademik ~IVERSm MALAYSIA SARAWAK

T ABLE OF CONTENTS

DECLARATION AND COPyRIGHT II

ACKNOWLEDGEMENT III

LIST OF TABLES viii

LIST OF FIGURES IX

ABSTRACT IV

ABSTRAK V

CHAPTER ONE INTRODUCTION

10 Introduction

11 An Overview of Malaysia Property Market 8

12 Problem Statements 13

13 Objective 14

14 Significant and scope ofthe Study 14

15 Summary 15

CHAPTER TWO LITERATURE REVIEW

20 Introduction 16

21 Relationship between Return on Assets Plant and Equipment and Company 16

Performance

22 Relationship between Capital Expenditure Debts and Cash Flows toward 18

Company Performance

23 Relationship between Size and Company Performance 21

24 Relationship between Shareholder Funds and Company Performance 22

25 Relationship between Insider Ownership and Company Performance 23

VI

~107i7 1

26 Summary 25

CHAPTERTHREEMETHOLOGY

30 Introduction 26

31 Hypotheses 26

32 Research Design 29

321 Data Sample and Data Collection 29

322 Empirical Model 30

33 Summary 31

CHAPTER FOUR EMPIRICAL RESULTS

40 Introduction 32

41 Descriptive Statistics 33

42 Regression Analysis 34

43 Summary 39

CHAPTER FIVE CONCLUSION AND RECOMMENDATIONS

50 Introduction 41

51 Summary and Findings of the Study 41

52 Limitation of Study 44

53 The Underlying Factors of the Market and Implications 45

54 Conclusion 47

REFERENCES 48

VII

-~-------------- - ---shy

LIST OF TABLES

Title Page

Table 1 Supply of Residential Units in Malaysia 10

Table 2 Total Transaction Values (RMm) 12

Table 3 Total Number of Transaction 12

Table 4 Summary Statistics of the Variables 33

Table 5 Result of Insider Ownership Cash Flow and Size 34

Table 6 Result of Plants and Equipments Capital Expenditures and Shareholder 35 Fund

Table 7 Result of Panel Least Square Regression 36

VIII

LIST OF FIGURES

Title Page

Figure 1 Key Success Factor for Property Sector 5

Figure 2 Factors affect Company Performance in Property Sector 26

Figure 3 Return on Assets 38

IX

IOZ17J I

CHAPTER ONE

INTRODUCTION

10 Introduction

Malaysia experienced a strong beating from global financial crisis in the first half of 2009

as the Gross Domestic Product (GDP) contracted significantly Since then there were some

positive movements in some economic indicators in 3rd quarter due to the government national

recovery packages that restore market confidence and maintain the stability of financial market

and expectation of positive growth in the 4th quarter and these growth show evidence that

Malaysia is out of recession and there is still an upside potential in the investment of property in

Malaysia There are signs of improvement on the worldwide economy where stocks that

decreased in value previously are strong enough to get back to the market For example Dow

Jones gained 40 after their March low

The slowdown in Malaysias economy has caused Malaysians become more cautious with

their investment in properties However property prices in Malaysia remain one of the most

competitive in the region They offer stronger investment returns as compared to its neighboring

countries

In encouraging foreign investments economy liberalization measure introduced by the

government has made 2009 a significant new era in Malaysias development history The

comprehensive package with new policies are said to have a significant impact towards real

--- --------- - -------- - -

estate sector as the restrictions for foreign investors to purchase the properties in Malaysia had

been removed These measures aimed to increase the number of transactions and attract overseas

investment

Plants and equipments one of the firms strategic action is the main factor to determine the

success of property sector Bhat (2000) noted that the age of property company size plant and

equipment building and return on assets can help to increase profits and improve the

competitive edge of a company Porter (1989) states that the key success factor for property

sector depend on internal factors and external factors Internal factors especially plants and

equipments is the key success factor of property sector because they are valuable and imitability

as a strategic location determined the success of a property company The author stated that

looking for locations that are economically attractive is one of the critical dimensions of success

Kamarulzaman Hassan the analyst of T A Securities Holdings Berhad support this point by stated

that location of property is an issue besides demand and supply Bhat (2000) support that plants

and equipments determined the cost and revenue as they have direct impact on maintenance

expenditures However Porter (1989) stated that imitating is profitable if the industry is great but

it will become a way of insuring disaster if the industry is less attractive

Population in an area is the important factor which determined the demand and supply of

property Supply and demand is the backbone of a market economy The demand is high when

there is a larger population The standard of living and the development land affect the choice of

consumers in their decision making on the types of property and the location to invest This is

supported by Porter (1989) where tremendous demand for new building and demographic shift in

2

rates

the populatjon is the important factor for property sector In the concept of economics price is a

reflection of supply and demand Property contained large per cent of buyers cost Oversupply

will force the price to go down as the demand is less than the supply in the market However this

is no longer happened as developers know how to control the situation after experienced the crisis

hits on 1987 and 1997

In Porter 5 forces suppliers are the determinant factors that affect the profits gained and the

costs to customers The materials used in the construction of property tend affect the price and

this will be the burden of customers Barney (1991) noted that resources owned must enabled a

finn outperfonn its competitors The resources are carefully managed in order to achieve the

objective of sustainable development Malaysia has no problem on materials such as sand and

cement as Malaysia is the sole proprietor However material such as steel is said to affect the

costs of construction as the price of steel is depend on world market which subject to exchange

The threat of new entrants into the market is said to affect the profit gained as the entry

barriers are low Porter (1989) noted that the situation of rivalry in property sector has always

been active where a lot of new competitors have come in The competitors have enough capital to

finance a lot of new projects The increasing number of competitors combined with slowing

demand has led to overcapacity which caused the profit to drop

3

Poter (1989) stated that there are two ways property firms can gain competitive advantage I

One is lowest cost and another one is differentiation Property firms managed to gain higher

margin at prevailing price levels if they are able to develop and finance their projects and deliver

at a lower cost The author further stated that property firms can better utilizE the land or gain

higher profits per square foot if they are skilled in employing new concepts into projects or

skilled in property design

Other financial factors are debt equity cash flows capital expenditure plants and

equipments SIze insider ownership and return on assets (Bhat 2000 Vol garis Asteriou and

Agiomirgianakis 2002) From the above variables cash flows insider ownership and firm size

could be categorized as internal firms characteristics and capital expenditure plants and

equipments and shareholder fund as firm strategic action Those variables are important as they

significantly affect firm performance Presented below is a comprehensive framework of key

success factor for property sector

I Competitive advantage is the taking of offensive or defensive actions in order to create a defendable position in an

industry

4

q Figure 1 Key Success Factor for Property Sector

~CI

Firm Performance

ROA

Drivers

~i ~~ 3a ~i ~~ 11)=gt3111 rIJshyn ~~

Internal Firms Characteristics Firms Strategic Action

Plant amp Equipment

Cash Flow

Insider Ownership

Size Capital Expenditure

Shareholder Fund

5

------------------~-------------~-

The performance of a firm is always measured by return on asset or return on equity and

one of the ways to achieve high perfonnance is improving the return on assets of company

Return on assets has significant impact towards company performance as it enabled a firm to

have an effective maintenance system which tends to increase profits and improve competitive

edge Return on assets represents the efficiency of assets utilization in a company ~Iigh return on

assets tends to affect the efficient management of a company (Bhat 2000)

A greater cash flow is said to increase the risk of being take over by other finns (Davis and

Stout 1992) This is because firm holding free cash flow may find it hard to perform due to the

increase government pressures This happened in the long run when the financial markets and

legal systems become more strengthened (Brush Bromiley and Hendrickx 2000) Firms with

large cash flow tend to have higher rates of return up to one year start from the day they are

identified by value line However they only out perform firms that are of similar size (Stephen

and Joseph 2000) The author noted that free cash flow hypothesis predicts that firms that are

overinvesting will face pressure form investors Thus the cash flow will distribute to

shareholders instead of reinvest in the finn The study further found that by using Tobins Q in

the analysis finns with low Q and high free cash flow should have a superior performance postshy

listing as they are forced to use their cash flow in a more efficient way

Other than this size of a firm has the ability to affect firm performance Firm with larger

size is considered to be more efficient compared to firm with smaller size Small firms are less

competitive as they have less power However firms might suffer from inefficiency when they

become larger Thus cause inferior financial performance (Majumdar 1997) Other than this

6

--- - -- ===============~==~======~~====~~~ -

firms with larger size tend to have an easy access to loans especially longer-term loans and this is

considered to affect sales and profit of a firm (Topalova 2004)

Other than that a higher equity ownership will enhance the interest of the controlling

shareholders in non-stationary distribution of dividends (Filatotchev et aI 2001 La Porta et aI

2000a) Merton (1974) noted that there is a positive relationship between equity volatility and

shareholder wealth Equity holders have the incentive to increase cash flow volatility of a firm

(Jensen and Meckling 1976) However there are literatures showing that equity volatility caused

both positive and negative impact towards shareholder wealth Shareholder wealth is proved to

decrease more when there is an increase in equity volatility for firms with low interest coverage

low investment low cash flow and high leverage (Shin and Stulz 2000)

Plants and equipments is the physical assets owns by a company that cannot quickly

convert to cash It is one of the investments of a company The return on investment generates

from plants and equipments able to help a company in sustaining growth The decrease in plants

and equipments investment tends to affect performance of a firm Revaluation of plants and

equipments is proved to improve forecasts of future earnings in the case that dividends may be

paid

One of the important factors that have to be concerned is the capital expenditure of a firm

The capital expenditure of a company is significantly related to profitability Generally

profitability is related inversely to the liability Thus the more debt a company incurs the worse

its earnings An appropriate capital expenditure allows firms to minimize capital structure Thus

7

- - oVloj ~l

reduce the total costs of firms Capital expenditures have a negative relationship with future

returns of firms (Baker Stein and Wurgler 2003)

The value of a company is made up of debt and equity Debt can boost as weH as hurts

company performance A moderate debt allowed company to gain market shares while an

excessive debt will bring about market share losses Debt is considered to create a better

monitoring opportunities The presence of debt enabled cash flow claims contractually set at the

time of borrowing However the failure to meet the claims will lead to bankruptcy or loss of

control over an asset even the entire firm (Damodaran 2009) Firms that are more likely to issue

debt are those with financial needs Thus financial deficits have become the determinant of the

decision to issue debt (Diamond 1991)

Debt has been analyzed as disciplinary in the shareholders-manager conflict Debt tends to

help in managing the conflict as it is easier to control the shareholders in modifying the leverage

ratio than to adjust the share of capital (Bruslerie and Latrous 2007) Debt improves company

performance in which it allows shareholders to select the first-best investment policy It reduces

the distortion in shareholders investment incentives (Lyandres and Zhdanov 2007)

11 An Overview of Malaysia Property Market

Malaysia real estate is expected to warm up in the second half of 20 1 0 before ushering

in the Spring in 2011 (Borneo Post Business 30122009) Malaysia property market is on an

upward trend as the prices of middle class suburban property is rising due to the steady stock

8

---~7T7r---------~~-------------------------- --------------r~------------------ J

market movement Generally high rise residential units in Kuala Lumpur increase about 12 to 18

per cent per annum for the last 15 to 20 years The demand is expected to continue as a result of

the limited land space stated by the Director of Ho Chin Soon Research

Sarawak one of the states of Malaysia recorded the highest increased in 2008 which was

about 47 The performance of the Sarawak property market moderated in HI 2009 There were

11867 transactions recorded in HI 2009 with a total value of RMl 66 billion Compared to the

HI and H2 2008 the volume of transactions increased by 1l1 but decreased by l2

respectively Value of transactions showed the same movement that is increased by 48 against

HI 2008 but decreased by 78 against H2 2008

Residential property sub-sector continued to lead in market share accounting for 468

followed by agricultural (360) commercial (101) development land (44) and industrial

(28) sub-sectors Volume of transactions in residential commercial and industrial sub sectors

was higher against HI 2008 but lower compared to H2 2008 Conversely agricultural sub-sector

noted the opposite movement whereas development land sub-sector rose against both halves of