companies act, 2013 practical aspects accounts and auditor & new provisions related to financial...

TRANSCRIPT

Companies Act, 2013Practical Aspects Accounts and Auditor & New Provisions Related to Financial Statements – Bhubaneshwar

26th February,2015 by CA Yagnesh DesaiB.Com. FCA.

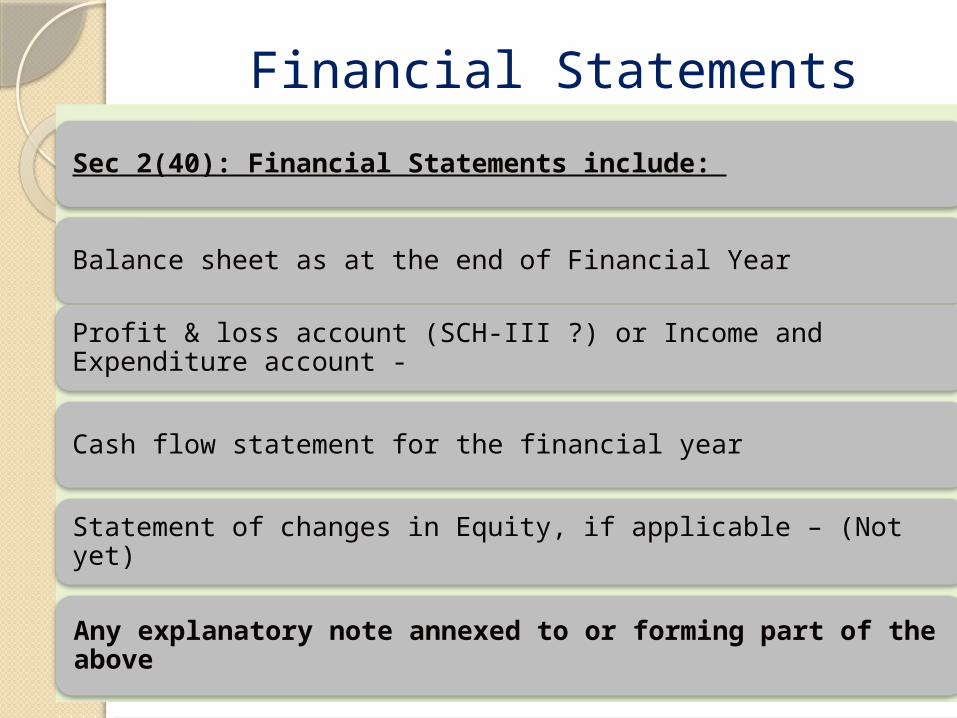

Financial StatementsSec 2(40): Financial Statements include:

Balance sheet as at the end of Financial Year

Profit & loss account (SCH-III ?) or Income and Expenditure account -

Cash flow statement for the financial year

Statement of changes in Equity, if applicable – (Not yet)

Any explanatory note annexed to or forming part of the above

Financial Statements

Give a True & Fair view

Compliance with Accounting Standards (Sec.133)

In the form Specified in Schedule III

• Insurance company• Banking company• Company engaged in generation or supply of electricity• Company governed by any other law for the time being in force

Not Applicable to

Cash Flow Statement – V IMP

Mandatory for all companies except: ◦ One Person Company, ◦ Small Companies ◦ Dormant Companies

◦ The Act 1956 did not mandate the preparation and presentation of cash Flow Statement

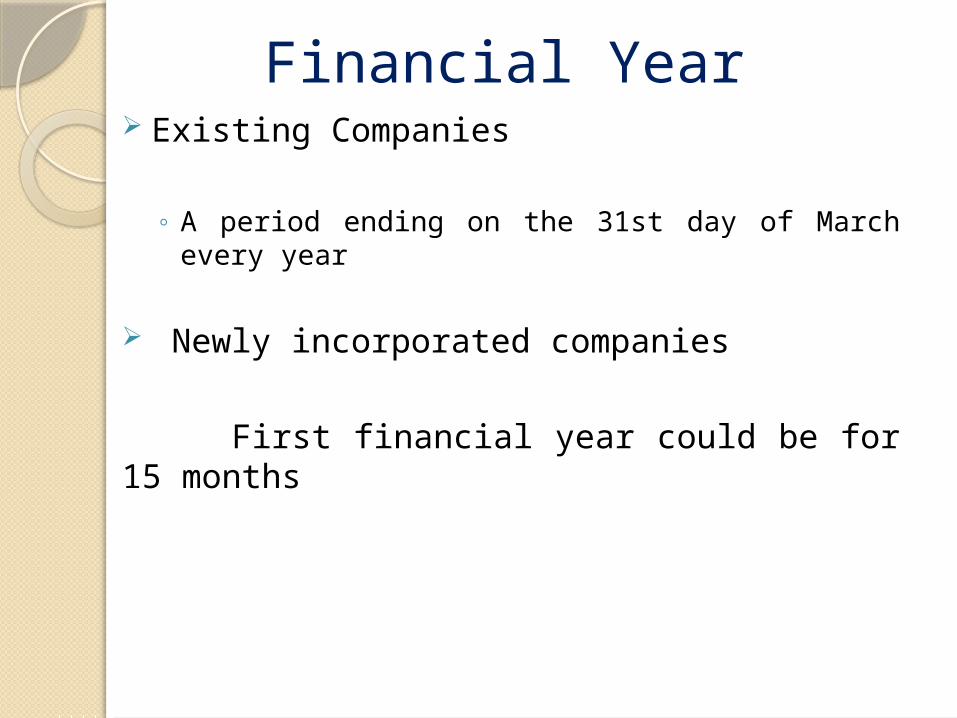

Financial Year Existing Companies

◦ A period ending on the 31st day of March every year

Newly incorporated companies First financial year could be for 15 months

Some more details to ROC The company shall intimate to the

Registrar on an annual basis at the time of filing of financial statement-

(a) the name of the service provider; (b) the internet protocol address of

service provider; (c) the location of the service provider

(wherever applicable); (d) where the books of account and

other books and papers are maintained on cloud, such address as provided by the service provider.

Consolidated Financial Statements – CFS

Standalone Financial Statement - SFS

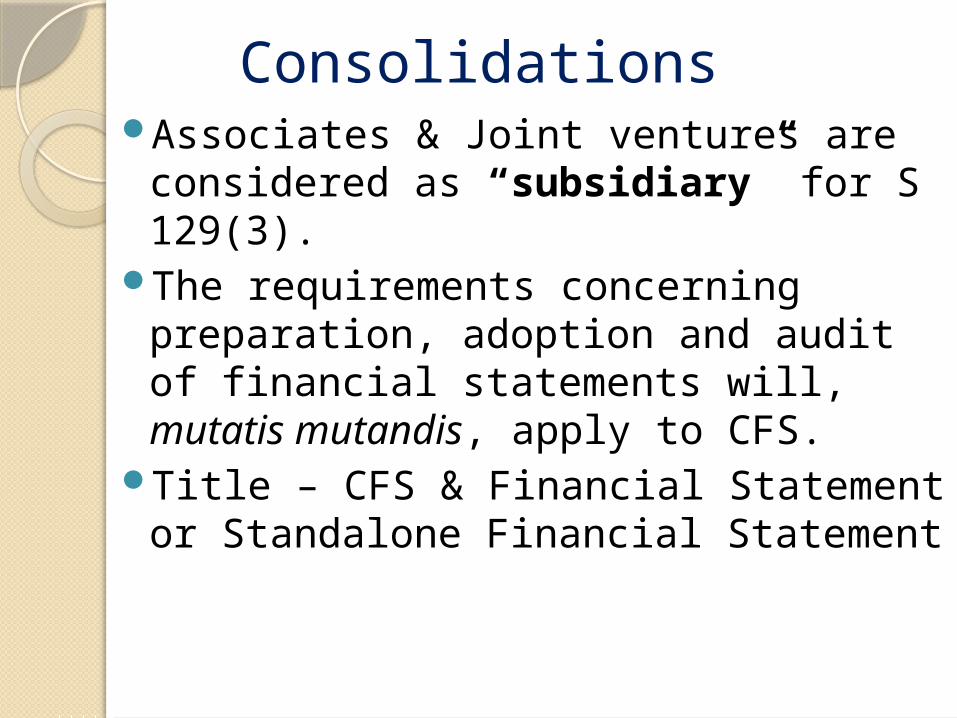

Consolidations Associates & Joint ventures are

considered as “subsidiary” for S 129(3).

The requirements concerning preparation, adoption and audit of financial statements will, mutatis mutandis, apply to CFS.

Title – CFS & Financial Statement or Standalone Financial Statement

No Subsidiary but associates and Joint Ventures – Is consolidation required ?Vide Notification dated 14th

October,2014 – not to consolidate till 31st March, 2015. Companies (Accounts) Amendment Rules , 2014

Intermediary wholly owned subsidiary exempt

Schedule III V/s Schedule VI

New Section added Viz “GENERAL INSTRUCTIONS FOR THE PREPARATION OF CONSOLIDATED FINANCIAL STATEMENTS Page 279”

General Circular 39/2014 about additional Information as envisaged for CFS.

Where a company is required to prepare CFS, it will mutatis mutandis follow the requirements of this Schedule as applicable to a company in the preparation of balance sheet and statement of profit and loss.

In CFS, the following will be disclosed by way of additional information:o In respect of each subsidiary, associate and joint

venture, % of net assets as % of consolidated net assets.

o In respect of each subsidiary, associate and joint venture, % share in profit or loss as % of consolidated profit or loss.

o Disclosures at (i) and (ii) are further sub-categorized into Indian and foreign subsidiaries, associates and joint ventures.

o For minority interest in all subsidiaries, % of net assets and % share as in profit or loss as % of consolidated net assets and consolidated profit or loss, separately.

All subsidiaries, associates and joint ventures (both Indian or foreign) will be covered under CFS.

A company will disclose list of subsidiaries, associates or joint ventures which have not been consolidated along with the reasons of non-consolidation.

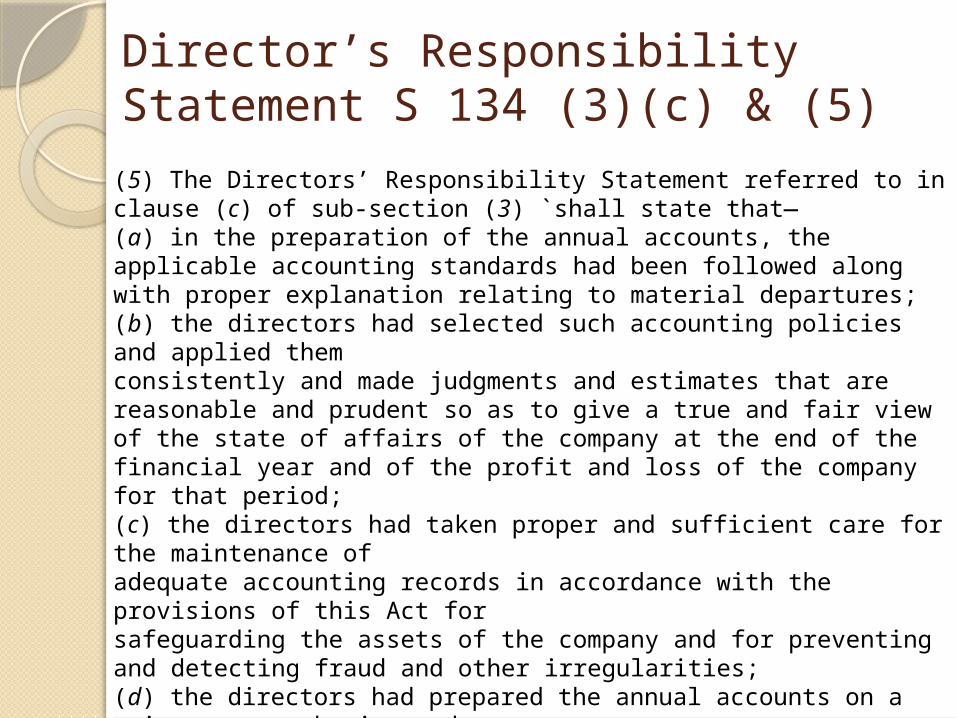

Director’s Responsibility Statement S 134 (3)(c) & (5)

(5) The Directors’ Responsibility Statement referred to in clause (c) of sub-section (3) `shall state that—(a) in the preparation of the annual accounts, the applicable accounting standards had been followed along with proper explanation relating to material departures;(b) the directors had selected such accounting policies and applied themconsistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the company at the end of thefinancial year and of the profit and loss of the company for that period;(c) the directors had taken proper and sufficient care for the maintenance ofadequate accounting records in accordance with the provisions of this Act forsafeguarding the assets of the company and for preventing and detecting fraud and other irregularities;(d) the directors had prepared the annual accounts on a going concern basis; and

Director’s Responsibility Statement

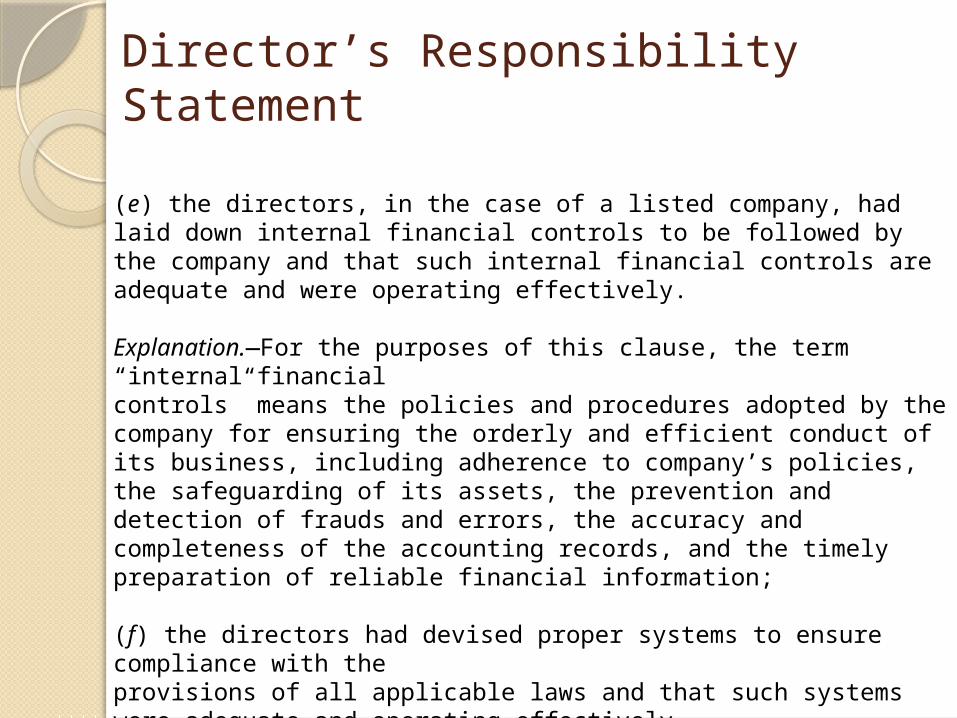

(e) the directors, in the case of a listed company, had laid down internal financial controls to be followed by the company and that such internal financial controls are adequate and were operating effectively.

Explanation.—For the purposes of this clause, the term “internal financialcontrols” means the policies and procedures adopted by the company for ensuring the orderly and efficient conduct of its business, including adherence to company’s policies, the safeguarding of its assets, the prevention and detection of frauds and errors, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information;

(f) the directors had devised proper systems to ensure compliance with theprovisions of all applicable laws and that such systems were adequate and operating effectively.

S 134 : Board’s Report Should be based on which statement – SFS or CFS ?

The Board report should be based on the stand alone financial statements. Rule 8 – The Companies (Accounts) Rules 2014. Chapter IX

It should also contain a separate section wherein a report on the Performance and financial position of each of the :

Subsidiaries ,Associates , and Joint venture companies included in the Consolidated Financial Statements

Approval of Financial Statements – Both or only SFC ?

Both stand alone and consolidated financial statements :

must be approved by the Board

They must be signed on behalf of the Board by :- When the Chairperson is Authorised by the

Board The Chairperson of the Company. When the Chairperson is not Authorised by

the Board and By any two directors of the company , out of which

one shall be Managing Director and CEO , if he is director

and

The company secretary wherever they are appointed

In case of One person Company ; only by one director.

Auditor’s Report must be attached with every financial statements.

Auditors

Particulars Section Rule Form No.

Manner and procedure of selection of auditor 139(1) 3

Conditions for Appointment

139(1), Second to proviso

4

139(2) 5

Manner in which the companies to rotate their auditor on the expiry of term

139(4) 6

Removal of auditor before expiry of his term 140(1) 7 ADT-2

Resignation of auditor 140(2) 8 ADT-3

Disqualification of auditor

141(3)(d)(i)

10.1

141(3)(d)(ii)

10.2

141(3)(d)(iii)

10.3

141(3)(e) 10.4

Other matters to be included in Audit Report 143(2) 11

Duties and powers of the company’s auditor with reference to the audit of the branch and the branch auditor

143(8) 12

Reporting of frauds by auditor 143(12) 13 ADT-4

Remuneration of cost auditor 148(3) 14

Appointment in next AGM

Auditor to issue: A Prior written consent to the appointment;

and A certificate stating that he/she satisfies the

criteria specified in Sec.141 and is qualified to be appointed as an Auditor *

Company to intimate- ( as against the auditor) to

Registrar; and Auditor in less than 15 days of such appointment , earlier onus was on the Auditor.

Certificate by Auditor Under Rule 4

“(1) The auditor appointed under rule 3 shall submit a certificate that -

(a) the individual or the firm, as the case may be, is eligible for appointment and is not disqualified for appointment under the Act, the Chartered Accountants Act, 1949 and the rules or regulations made there under;

(b) the proposed appointment is as per the term provided under the Act;

(c) the proposed appointment is within the limits laid down by or under the authority of the Act;

(d) the list of proceedings against the auditor or audit firm or any partner of the audit firm pending with respect to professional matters of conduct, as disclosed in the certificate, is true and correct.”

Rotation of the Auditor - Assess the applicability

Listed companies

Unlisted public companies having paid up share capital of Rs. 10cr or more;

Private companies having paid up share capital of Rs. 20cr or more;

Any company having public borrowings from financial institutions, banks or public deposit of Rs. 50cr or more

Rotation of the Auditor - Not Applicable to

Specifically a. One person company

b. b. Small companies

c. And also not applicable to ?????????

Rotation of the Auditor Individual – One Term of 5 consecutive years;

Firm - Two terms of 5 consecutive years each; The period for which the auditor has held office prior to

commencement of this act shall be considered; Transition period is for 3 years . Rotation of audit partners internally is possible as may be

resolved by the members of the Company. In case of Joint auditor, company to ensure that all auditors

DO NOT complete their terms in the same year. Explanation II(a) to sub rule 3 of Rule 6 (a) a break in

the term for a continuous period of five years shall be considered as fulfilling the requirement of rotation;

Refer : International Ethics Board of Accountants.

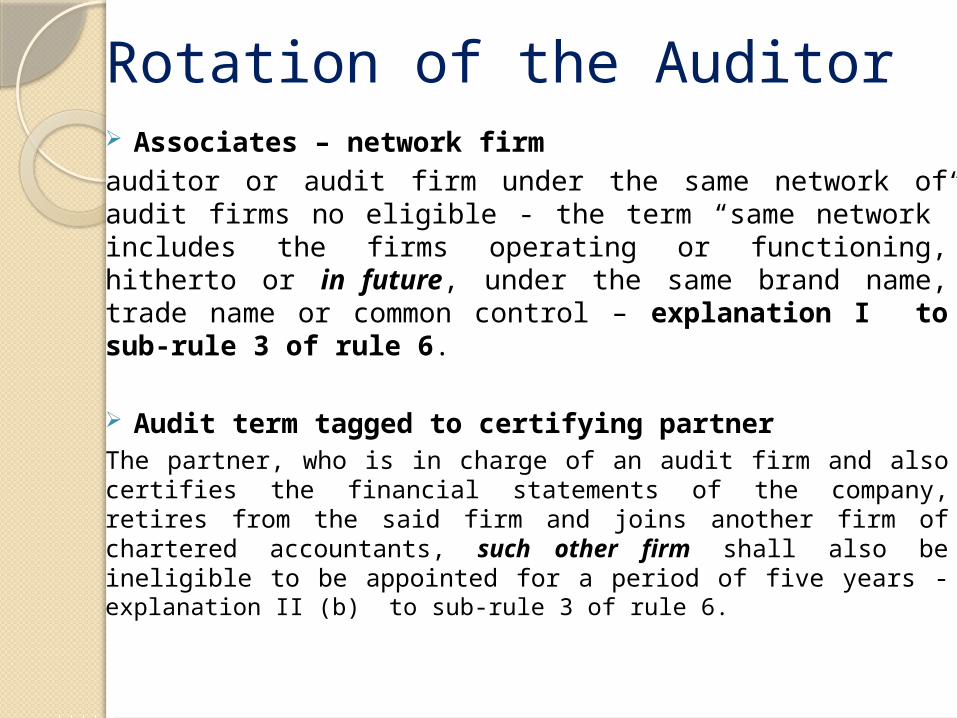

Rotation of the Auditor Associates – network firm auditor or audit firm under the same network of audit firms no eligible - the term “same network” includes the firms operating or functioning, hitherto or in future, under the same brand name, trade name or common control – explanation I to sub-rule 3 of rule 6.

Audit term tagged to certifying partner The partner, who is in charge of an audit firm and also certifies the financial statements of the company, retires from the said firm and joins another firm of chartered accountants, such other firm shall also be ineligible to be appointed for a period of five years - explanation II (b) to sub-rule 3 of rule 6.

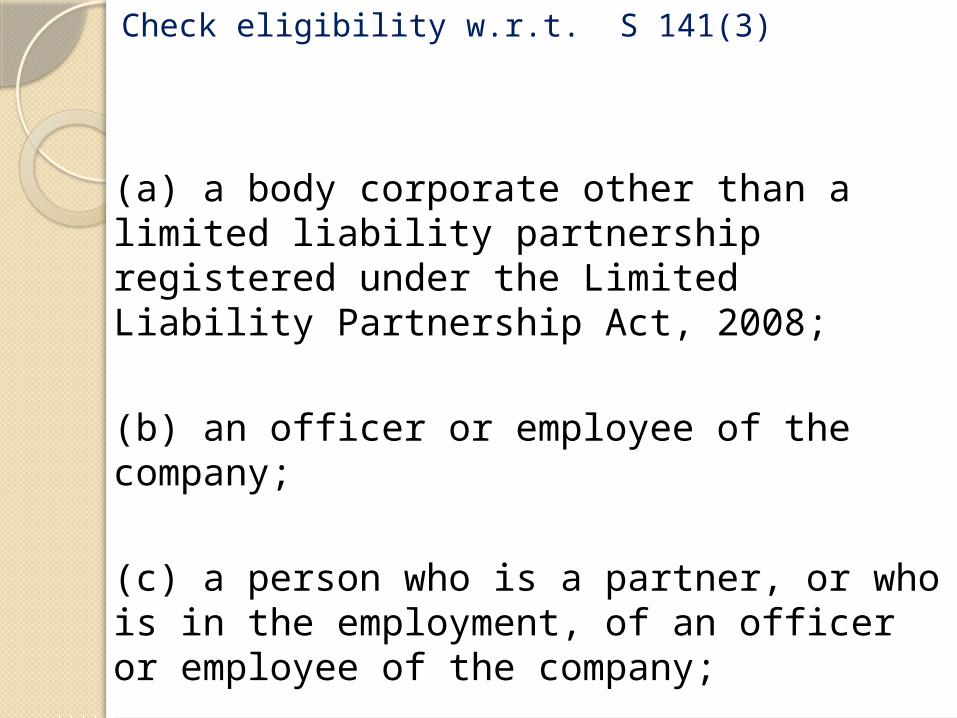

Check eligibility w.r.t. S 141(3)

(a) a body corporate other than a limited liability partnership registered under the Limited Liability Partnership Act, 2008;

(b) an officer or employee of the company;

(c) a person who is a partner, or who is in the employment, of an officer or employee of the company;

Check eligibility w r t 141(3)

(d) a person who, or his relative or partner—

(i) is holding any security of or interest in the company or its subsidiary, or of its holding or associate company or a subsidiary of such holding company:

Provided that the relative may hold security or interest in the company of face value not exceeding one thousand rupees or such sum as may be prescribed; - Rules 10 (1) Prescribed Rs. One lac – sixty days to rectify.

(ii) is indebted to the company, or its subsidiary, or its holding or associate company or a subsidiary of such holding company, in excess of such amount as may be prescribed; or Rules 10 (2) Prescribed Rs. Five lac

(iii) has given a guarantee or provided any security in connection with the indebtedness of any third person to the company, or its subsidiary, or its holding or associate company or a subsidiary of such holding company, for such amount as may be prescribed; Rules 10 (3) Prescribed Rs. One lac

Check eligibility w r t 141(3)

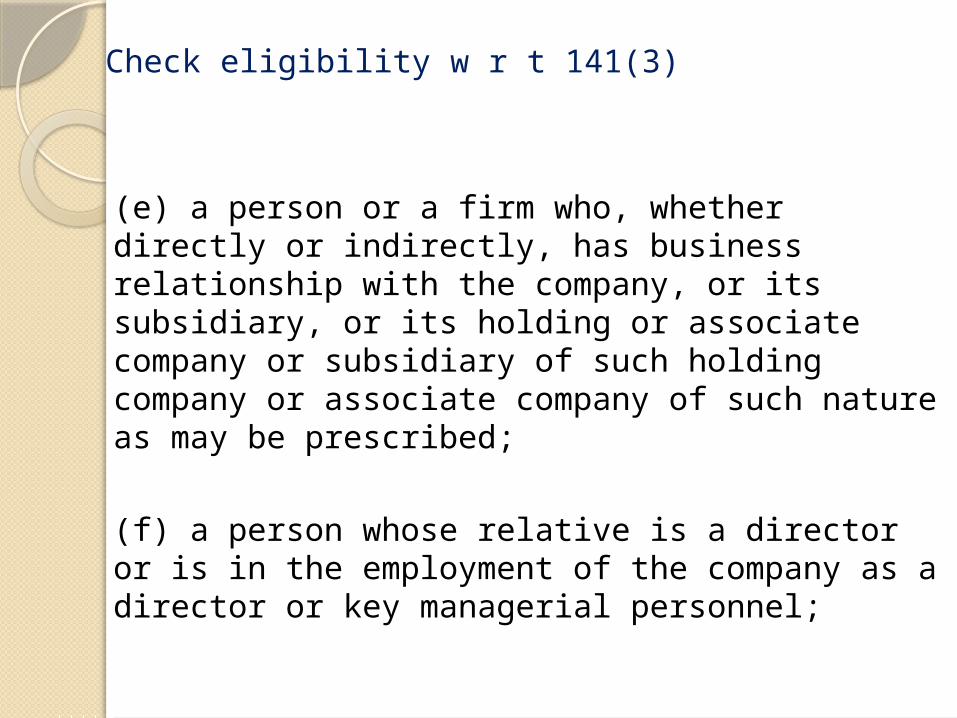

(e) a person or a firm who, whether directly or indirectly, has business relationship with the company, or its subsidiary, or its holding or associate company or subsidiary of such holding company or associate company of such nature as may be prescribed;

(f) a person whose relative is a director or is in the employment of the company as a director or key managerial personnel;

Check the Cap on No. of Audits S 141(3) (g) “a person who is in full time employment

elsewhere or a person or a partner of a firm holding appointment as its auditor, if such persons or partner is at the date of such appointment or reappointment holding appointment as auditor of more than twenty companies”

Includes OPC, private and small companies Companies (Amendment )Act 2000 private limited

companies were not considered Representation made by ICAI vide letter dated April

15,2014 to Hon’ble Minister. Also proposed to exclude private companies in draft

notification dated 24.6.2014 – no action till date. Why not transition provision for auditors ? For directors

one year transition provision.

Who is not Eligible for an appointment as an Auditor

S 141(3) (h) a person who has been convicted by a court of an offence involving fraud and a period of ten years has not elapsed from the date of such conviction;

(i) any person ( ?) whose subsidiary or associate company or any other form of entity, is engaged as on the date of appointment in consulting and specialised services as provided in section 144.

S 141(4) Where a person appointed as an auditor of a company incurs any of the disqualifications mentioned in sub-section (3) after his appointment, he shall vacate his office as such auditor and such vacation shall be deemed to be a casual vacancy in the office of the auditor.

Quiz

S 139 (10) Where at any annual general meeting, no auditor is appointed or re-appointed, the existing auditor shall continue to be the auditor of the company.

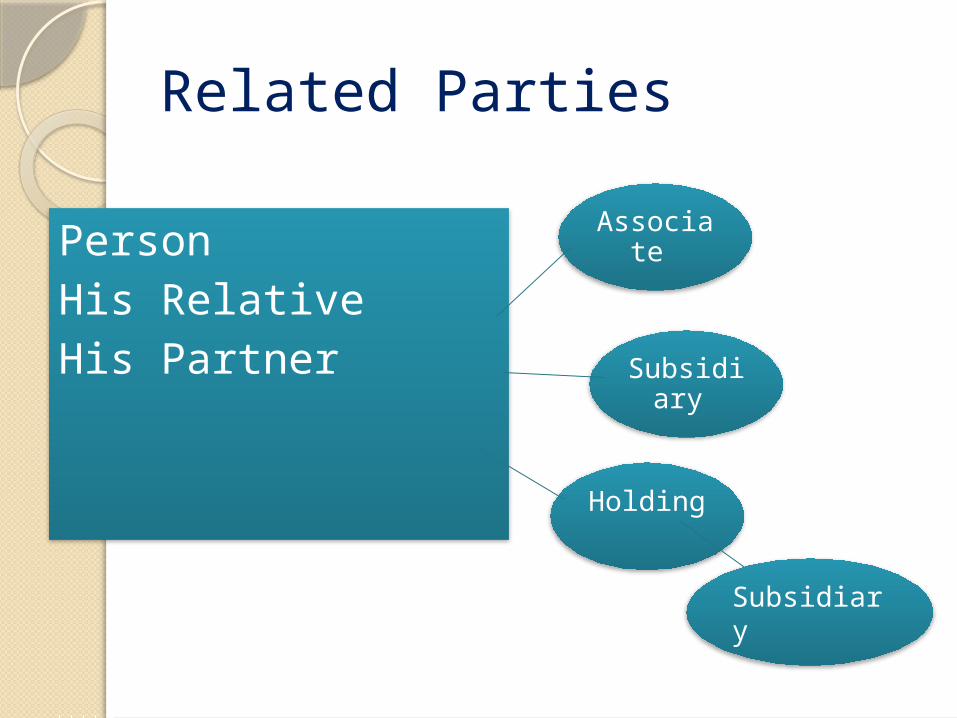

Related Parties

PersonHis RelativeHis Partner Subsidiar

y

Associate

Holding

Subsidiary

Relax !! Audit Report made easy to some extend

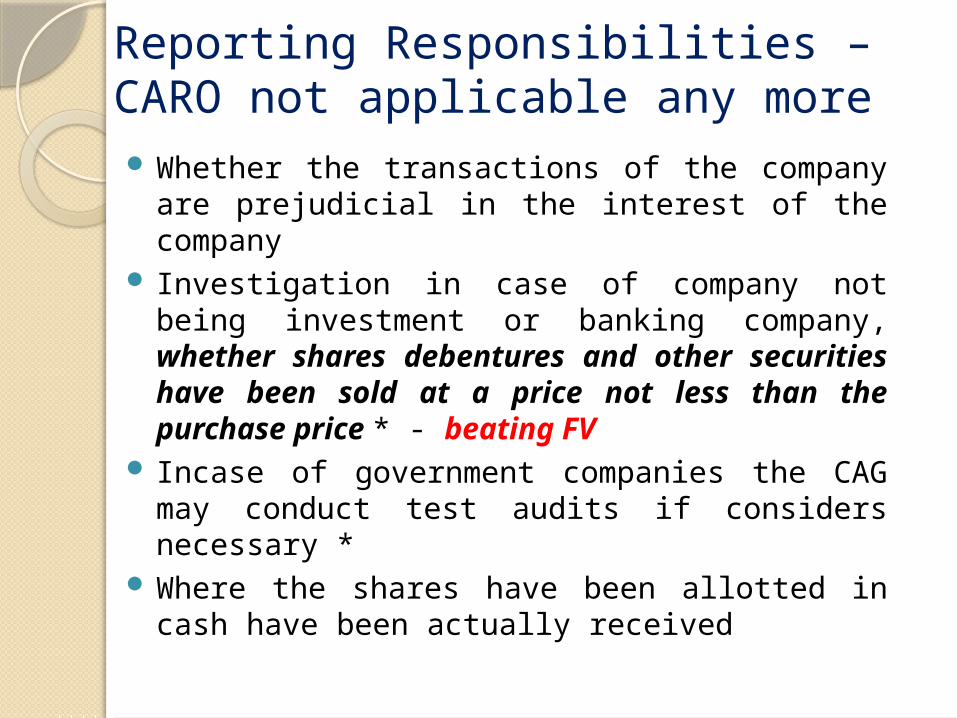

Reporting Responsibilities – CARO not applicable any more Whether the transactions of the company are

prejudicial in the interest of the company Investigation in case of company not being

investment or banking company, whether shares debentures and other securities have been sold at a price not less than the purchase price * - beating FV

Incase of government companies the CAG may conduct test audits if considers necessary *

Where the shares have been allotted in cash have been actually received

Reporting Responsibilities

Whether personal expenses have been charges to revenue expenses

Whether loans and advances made by the company has been shown as deposits – classification & presentation.

Whether loans and advances made by the company on the basis of security has been properly secured

Whether the terms on which they have been made are prejudicial to the interests of the company or it’s members

Auditor’s Report – Major Concerns

Matters which have adverse effect on functioning of the company *

The branch auditor shall submit his report to the company’s auditor * SA 600

Whether the company has adequate internal financial controls in place and the operating effectiveness of such control *

* This requirement is not applicable till 31st march,2015

Audit Report – Views and Comments – S 143(3)(j) r. w Rule 11Whether the company has :-disclosed the impact of pending

litigations on its financial position in FS

made provision for material foreseeable losses if any on long term contracts including derivative contracts *

whether there is any delay in transferring amounts required to be transferred to the Investor Education and Protection Fund (IEPF deferred)

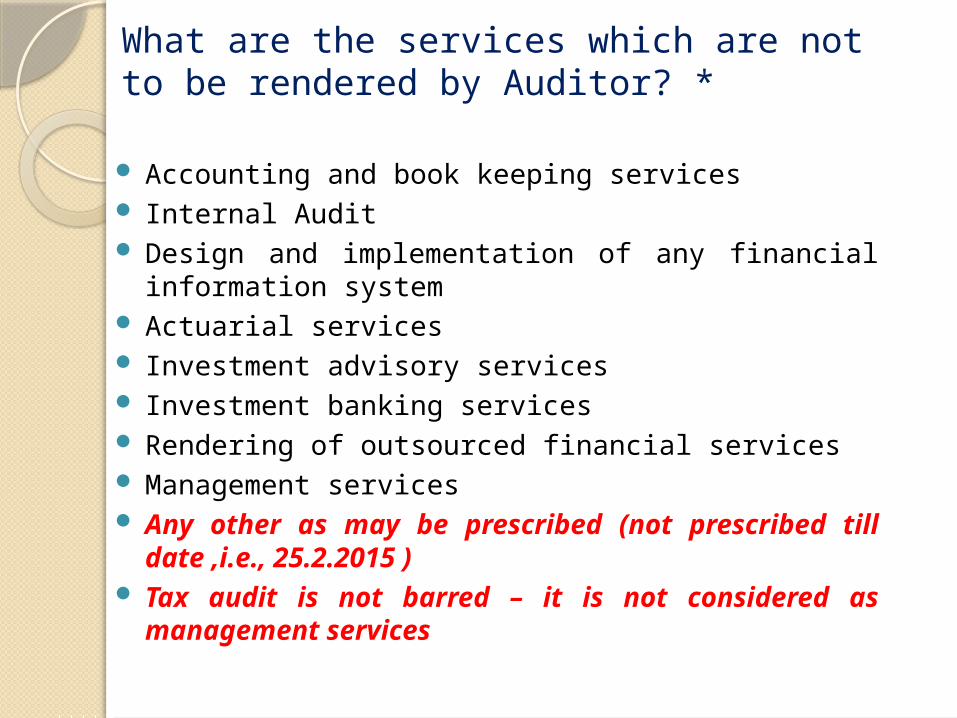

What are the services which are not to be rendered by Auditor? *

Accounting and book keeping services Internal Audit Design and implementation of any financial

information system Actuarial services Investment advisory services Investment banking services Rendering of outsourced financial services Management services Any other as may be prescribed (not

prescribed till date ,i.e., 25.2.2015 ) Tax audit is not barred – it is not considered

as management services

Watch Dog to Blood Hound

S 143(12)

If an auditor of a company has reason to believe that an offence involving fraud is being or has been committed against the company by officers or employees of the company, he shall immediately report the matter to the Central Government.

This requirement is not applicable till 31st March ,2015

Internal Audit S. 138 read with rule 13 , The companies ( Accounts) Rules 2014 The following class of companies shall be required to

appoint an internal auditor or a firm of internal auditors, namely:-

I Public Company

(a) every listed company;

(b) every unlisted public company having- (i) paid up share capital of Rs. 50 crore or more during

the preceding financial year; or (ii) turnover of Rs 200 crore or more during the

preceding financial year; or (iii) outstanding loans or borrowings from banks or public

financial institutions exceeding Rs 100 Crore or more at any point of time during the preceding financial year; or

(iv) outstanding deposits of Rs 25 crore or more at any point of time during the preceding financial year; and

Internal Audit (c) every private company having- (i) turnover of Rs. 200 crore or more during the preceding

financial year; or (ii) outstanding loans or borrowings from banks or public

financial institutions exceeding Rs. 100 crore or more at any point of time during the preceding financial year:

Compliance within Six months from the effective date.

S 138 (1) Such class or classes of companies as may be prescribed shall be required to appoint an internal auditor, who shall either be a chartered accountant or a cost accountant, or such other professional as may be decided by the Board to conduct internal audit of the functions and activities of the company. ----Now look at the rules

Internal Audit Section 138 refers – Chartered Accountant – Cost Accountant or

such other professional as may be decided by the Board to conduct internal audit of the functions and activities of the company.

Interestingly , Rule 13 – (Page 9) of Chapter IX does not make s mention of

Cost Auditor or

Any other professionals.

May or may not be the employee of the Company.

Thank You .. Now overTo Disclosures – Accounting Standards V Companies Act 2013.pptx