community infrastructure levy economic viability...

TRANSCRIPT

Project Ref: 27169

October 2012

Stratford-on-Avon District Council

Stratford-on-Avon CIL

Community Infrastructure Levy Economic Viability Study

Stratford-on-Avon CIL

Community Infrastructure Levy Economic Viability Study

ii

We print on 100% recycled paper from sustainable suppliers accredited to ISO 14001.

Stratford-on-Avon CIL

Community Infrastructure Levy Economic Viability Study

iii

Document Control Sheet

Project Name: Stratford-on-Avon CIL

Project Ref: 27169

Report Title: Community Infrastructure Levy Economic Viability Study

Doc Ref: Final report/rev04

Date: October 2012

Name Position Signature Date

Prepared by: Mark Felgate Associate MF/NC

30/10/2012

Reviewed by: Nigel Clark

Development Director

NC/MF 30/10/2012

Approved by: J Baker Partner JB

30/10/2012

For and on behalf of Peter Brett Associates LLP

Revision Date Description Prepared Reviewed Approved

000 03/08/2012 Draft Report MF NC JB

02 09/08/2012 Final Draft MF NC JB

03 08/10/12 Final Report MF/NC MF/NC JB

04 30/10/12 Final Report (amended) MF JB

Peter Brett Associates LLP disclaims any responsibility to the Client and others in respect of any matters outside the scope of this report. This report has been prepared with reasonable skill, care and diligence within the terms of the Contract with the Client and generally in accordance with the appropriate ACE Agreement and taking account of the manpower, resources, investigations and testing devoted to it by agreement with the Client. This report is confidential to the Client and Peter Brett Associates LLP accepts no responsibility of whatsoever nature to third parties to whom this report or any part thereof is made known. Any such party relies upon the report at their own risk.

© Peter Brett Associates LLP 2012

Stratford-on-Avon CIL

Community Infrastructure Levy Economic Viability Study

iv

Stratford-on-Avon CIL

Community Infrastructure Levy Economic Viability Study

v

Contents

1 Introduction ............................................................................................................................... 7 1.1 Background .................................................................................................................... 7 1.2 Community Infrastructure Levy (CIL) ............................................................................. 8 1.3 Approach to Governance ............................................................................................. 10

2 Development Typologies ....................................................................................................... 12 2.2 Residential ................................................................................................................... 12 2.3 Non Residential ............................................................................................................ 12

3 Viability Assumptions ............................................................................................................ 17 3.1 Reviewing the Existing Viability Evidence (Value and Costs) ..................................... 17 3.2 Consultation with the Development Industry ............................................................... 18 3.3 Our Approach ............................................................................................................... 21

4 Residential Viability Assessments ....................................................................................... 24 4.1 Assumptions ................................................................................................................ 24 4.2 Dwelling Mix ................................................................................................................. 24 4.3 Coverage, or Saleable Floorspace .............................................................................. 25 4.4 Sales Value for Open Market Housing ........................................................................ 25 4.5 Sales Value for Affordable Housing ............................................................................. 27 4.6 Build Costs ................................................................................................................... 29 4.7 The Code for Sustainable Homes ................................................................................ 30 4.8 Developer’s Profit and Professional Fees and Financing ............................................ 31 4.9 Additional or ‘Abnormal’ Development Costs .............................................................. 31 4.10 CIL and Community Gain Package ............................................................................. 32 4.11 Generic Residential Viability Appraisals ...................................................................... 32 4.12 Sensitivity Testing ........................................................................................................ 33 4.13 Summary of Findings from Residential Analyses and Recommended CIL Approaches 36 4.14 Affordable Housing ...................................................................................................... 38 4.15 Design Costs ................................................................................................................ 38

5 Non-Residential Assessments .............................................................................................. 40 5.1 Non-Residential Assumptions ...................................................................................... 40 5.2 Approach ...................................................................................................................... 40 5.3 Establishing Gross Development Value (GDV) ........................................................... 40 5.4 Costs ............................................................................................................................ 41 5.5 Site Coverage .............................................................................................................. 41 5.6 Developer Profit ........................................................................................................... 41 5.7 Build Costs ................................................................................................................... 42 5.8 Professional Fees, Overheads .................................................................................... 42 5.9 Development Contributions Other than CIL ................................................................. 42 5.10 Finance ........................................................................................................................ 43 5.11 Marketing Fees ............................................................................................................ 43 5.12 Acquisition Fees and Land Tax ................................................................................... 43 5.13 Land for Non-residential Uses ..................................................................................... 43 5.14 Non Residential Development Analysis ....................................................................... 44 5.15 B-class Uses ................................................................................................................ 44 5.16 Retail Uses ................................................................................................................... 45 5.17 Leisure Development ................................................................................................... 46 5.18 Care Homes and Extra Care Living ............................................................................. 47 5.19 Other Non-residential Development ............................................................................ 47 5.20 Summary and Sensitivity Testing on Non-residential Development ............................ 48

6 Conclusion .............................................................................................................................. 51

Stratford-on-Avon CIL

Community Infrastructure Levy Economic Viability Study

vi

Tables

Table 2.1: Residential Notional Sites for Viability Testing ..................................................................... 12 Table 4.1: Typical Floorspace by Dwelling Type ................................................................................... 24 Table 4.2: Current Market Schemes ..................................................................................................... 26 Table 4.3: Market Summary .................................................................................................................. 27 Table 4.4: Residential Viability Findings ................................................................................................ 33 Table 4.5: Sensitivity Testing to Achieve Viability ................................................................................. 34 Table 4.6: Sensitivity Testing to maximise % of affordable housing with varying levels of CIL ............ 34 Table 4.7: Approach 1 ........................................................................................................................... 37 Table 4.8: Approach 2 ........................................................................................................................... 37 Table 5.1: Non Residential Uses – Rent and Yields ............................................................................. 40 Table 5.2: Non Residential Uses – Site Coverage Ratios ..................................................................... 41 Table 5.3: Non Residential Uses – Build Costs..................................................................................... 42 Table 5.4: B-class Development ........................................................................................................... 44 Table 5.5: Out of town centre retail uses ............................................................................................... 45 Table 5.6: Town Centre Residual Analysis ........................................................................................... 46 Table 5.7: Hotel Viability Levy ............................................................................................................... 46 Table 5.8: Mixed Leisure CIL Charge .................................................................................................... 47 Table 5.9: Care Homes Viability ............................................................................................................ 47

Figures

Figure 1.1: Evidence to Inform CIL Charging Schedule .......................................................................... 9 Figure 5.1 Scope for CIL ....................................................................................................................... 48 Figure 5.2 Sensitivity analysis – minus 10% on values ......................................................................... 49 Figure 5.3 Sensitivity analysis – plus 10% on values ............................................................................ 50

Appendices

Appendix 1: Residential Viability Appraisals Appendix 2: Non-Residential Viability Appraisals Appendix 3: Glossary

CIL Economic Stratford-on-Avon CIL

7

1 Introduction

1.1 Background

1.1.1 Peter Brett Associates were commissioned to undertake an Economic Viability Assessment

of the proposed Community Infrastructure Levy by Stratford-on-Avon District Council. This

report is a viability assessment which seeks to set out the implications of differing levels of

viability for a variety of types of residential and non-residential developments, and how this

might support a Community Infrastructure Levy.

1.1.2 It should be noted that this report is not an independent scheme valuation for sites in

Stratford-on-Avon. No responsibility whatsoever is accepted to any third party who may seek

to rely on the content of the report for such purposes.

1.1.3 Government planning policy on viability and the deliverability of development is set out in the

National Planning Policy Framework (NPPF). It addresses the importance of ensuring

deliverability in paragraph 173:

“To ensure viability, the costs of any requirements likely to be applied to development, such

as requirements for affordable housing, local standards, infrastructure contributions or other

requirements should, when taking account of the normal cost of development and on-site

mitigation, provide acceptable returns to a willing land owner and a willing developer to

enable the development to be deliverable.”

1.1.4 The importance of delivery cannot be underestimated. To ensure robust and sound

development plan documents, local authorities must ensure that Local Plans are deliverable.

This effectively means that the infrastructure plans must be an integral part of spatial

planning and therefore funding issues are becoming increasingly important. This section

considers the opportunities for funding from developer contributions arising from the viability

of developments, both residential and commercial.

1.1.5 The main driver of development viability is the change in residual land value. If the residual

land value created by the proposed development is not substantially in excess of the existing

use value, then the development will not be considered viable by the market.

1.1.6 The basis of viability testing in this Report is through a series of generic site appraisals,

using the residual value (RV) approach. This needs to take account of a wide variety of

inter-related factors which are explored below, which include various items of planning

obligations and community gain expected to be delivered through the operation of the

planning system.

1.1.7 The key question is whether a suggested level of CIL, combined with other planning

obligations, including affordable housing will inhibit development generally, and conversely,

what level of CIL, and continuing contributions through S.106 Agreements, can be delivered

whilst maintaining economic viability?

CIL Economic Stratford-on-Avon CIL

8

1.1.8 CIL is a new levy that local authorities in England and Wales can choose to charge on new

developments in their area. The introduction of CIL corresponds to changes in the way that

Section 106 obligations can work and it is likely that most Local Authorities in England will

choose to use CIL in order to continue using some of the value created by development to

fund the infrastructure required. In large schemes, typical infrastructure provision might

include new secondary schools, and green infrastructure.

1.1.9 It should be noted that not only should evidence of viability be presented, but as the Appeal

Court judgement in the case of Blyth Valley has made clear, viability assessments must be

founded on robust evidence and it is insufficient to rely on ‘custom and practice’ or ‘going

rates’.

1.1.10 One of the most significant items of community gain sought from residential development

sites is affordable housing, not currently sought through CIL, but secured through S.106

agreements. This reflects both the affordable housing need in the District, but also the

increasing role that planning contributions have taken in delivering new affordable housing

stock. As the importance of planning contributions in funding infrastructure increases, the

cumulative effect of the planning contributions can lead, in some circumstances, to the

economic viability of a site being called into question. Although the cost of contributions is

normally factored into site financial appraisals by developers when land purchase is

contemplated, the development industry needs to demonstrate a profit, since no business

exists without a profit motive.

1.1.11 It is increasingly important therefore that policy relating to planning obligations is realistic and

credible, taking into account the local housing market, the economics of development,

including price, supply, demand, need, and profit issues.

1.1.12 It is clear that the main issues relate to the viability of residential development. In our

experience, there are relatively few locations where ‘B’ class uses are able to support CIL,

although some forms of retail are clearly viable and able to bear a levy without compromising

viability (particularly large format convenience retail). It is necessary to understand the

viability of non-residential development, if only to underpin a decision to charge a £0 rate.

The council may want to review CIL when economic conditions are more favourable,

although it must be emphasised that there is currently a very significant viability gap.

1.2 Community Infrastructure Levy (CIL)

1.2.1 The Planning Act 2008 introduced the power to charge a Community Infrastructure Levy

(CIL) and the details of setting the charge are set out in the CIL Regulations and Guidance.

CIL is a new levy that local authorities in England and Wales can choose to charge on new

developments in their area.

1.2.2 Before a charging authority can apply a CIL, it has to produce a CIL charging schedule. This

charging schedule has to be informed by relevant infrastructure funding gap and viability

evidence. The process of developing a CIL charging schedule is illustrated in Figure 1.1

below.

CIL Economic Stratford-on-Avon CIL

9

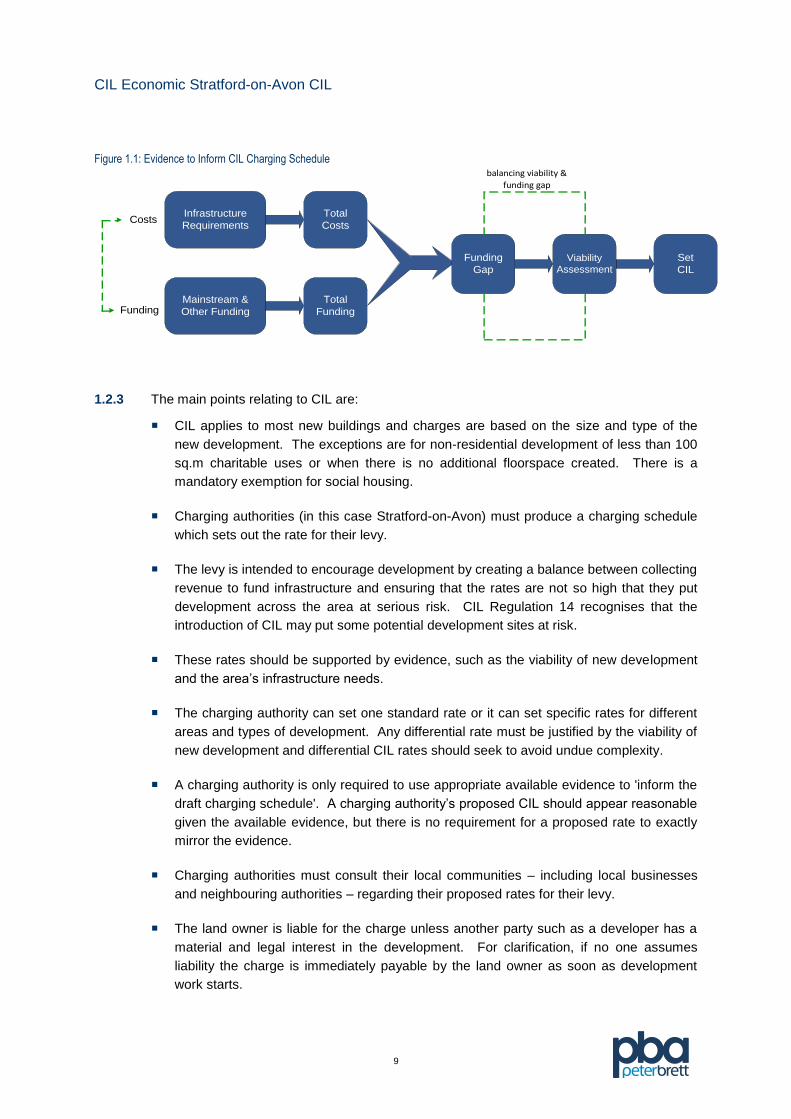

Figure 1.1: Evidence to Inform CIL Charging Schedule

1.2.3 The main points relating to CIL are:

CIL applies to most new buildings and charges are based on the size and type of the

new development. The exceptions are for non-residential development of less than 100

sq.m charitable uses or when there is no additional floorspace created. There is a

mandatory exemption for social housing.

Charging authorities (in this case Stratford-on-Avon) must produce a charging schedule

which sets out the rate for their levy.

The levy is intended to encourage development by creating a balance between collecting

revenue to fund infrastructure and ensuring that the rates are not so high that they put

development across the area at serious risk. CIL Regulation 14 recognises that the

introduction of CIL may put some potential development sites at risk.

These rates should be supported by evidence, such as the viability of new development

and the area’s infrastructure needs.

The charging authority can set one standard rate or it can set specific rates for different

areas and types of development. Any differential rate must be justified by the viability of

new development and differential CIL rates should seek to avoid undue complexity.

A charging authority is only required to use appropriate available evidence to 'inform the

draft charging schedule'. A charging authority’s proposed CIL should appear reasonable

given the available evidence, but there is no requirement for a proposed rate to exactly

mirror the evidence.

Charging authorities must consult their local communities – including local businesses

and neighbouring authorities – regarding their proposed rates for their levy.

The land owner is liable for the charge unless another party such as a developer has a

material and legal interest in the development. For clarification, if no one assumes

liability the charge is immediately payable by the land owner as soon as development

work starts.

Mainstream &

Other Funding

Infrastructure

Requirements

Total

Funding

Total

Costs

Funding

GapViability

Assessment

Set

CIL

Funding

Costs

balancing viability &

funding gap

CIL Economic Stratford-on-Avon CIL

10

If the charging authority chooses it can adopt an exceptional circumstances policy to

allow relief from the Levy. However, there are state aid considerations that may arise

from exemptions.

While the charge becomes due at commencement, the charging authority can choose to

adopt a payment phasing policy.

The charging authority can use up to 5% of CIL receipts to finance administrative

expenses in connection with the Levy. It should be noted that on-going CIL

consultations suggests there should be no cap to administrative expense fee financed

from CIL receipts.

1.2.4 Our approach has been guided by the Planning Act 2008, the CIL Regulations (2010 and

2011) and the March 2010 Charge Setting and Charging Procedures statutory guidance

document. The fundamental premise is that the CIL is intended to enable the delivery of

growth and it must be set at a level that does not put at risk the overall level of development

in the area.

1.3 Approach to Governance

1.3.1 Although not part of this commission the council should start to think about the governance

of CIL. It could be considered that setting the CIL is the easy part: the hard part will be

thinking about deciding which infrastructure providers and projects get CIL funding.

1.3.2 There are tensions pulling CIL funding three ways. Local neighbourhoods are expected by

the Government to get a “meaningful proportion” of CIL funding to spend at local level; and

for Stratford-on-Avon there will be competing priorities between the district and county (let

alone the competition between departments within the authority). Then there are a range of

other stakeholders – from PCTs, Highways Agency and emergency services, all of whom will

want their slice of funding.

1.3.3 CIL Regulation 123 requires LPAs to specify a list of infrastructure projects intended to be

funded from CIL. It restricts the use of planning obligations for infrastructure that will be

funded in whole or in part by the CIL, to ensure no duplication between the two types of

developer contributions.

1.3.4 Although Charging Authorities will not be examined on these issues, it would be a very good

idea for stakeholders to agree a common protocol about how these issues be dealt with

once the CIL money starts flowing in. Although strictly speaking not within the remit of the

examination, the examination at Newark and Sherwood saw a two-hour debate about how

CIL funding would be shared out. The examiner’s report devotes a number of pages to the

issue that are worth reviewing. By contrast, Shropshire has taken a “place plan” approach

which sticks closely to very local priorities. Spending profiles are reviewed annually, and

these choices provide a basis for an annual revision of the Regulation 123 list.

1.3.5 It is clear that there will be a number of different approaches to the governance of CIL

funding as rates emerge around the country. Early discussions on principles will be valuable

before the money arrives. That way, discussions can be usefully kept quite abstract, rather

CIL Economic Stratford-on-Avon CIL

11

than turning into a zero-sum argument about which agency gets the limited funding

available.

1.3.6 The NPPF stresses the need to ensure that the cumulative policies and standards set out in

a Local Plan do not render so much development unviable that the plan’s housing and other

development requirements cannot be delivered. Whilst the viability of a plan should not be

an overriding factor in the setting of plan policy, plans that do not take account of this are at

risk of failing to be found sound when examined.

1.3.7 The objectives of this report are to use the available evidence to assess the ability of

different types of development to support a CIL. The stages of the study are to:

Review the types of development likely to come forward during the plan period, use this

as a basis to generate some hypothetical development typologies;

Consider the evidence relating to the costs and values of different residential and non-

residential development in Stratford-on-Avon and establish assumptions to inform both

residential and non-residential viability appraisals; and

Undertake a series of viability tests on the hypothetical development typologies and

consider whether there is sufficient value to support a CIL.

CIL Economic Stratford-on-Avon CIL

12

2 Development Typologies

2.1.1 We have identified a set of development typologies for Stratford-on-Avon District. These are

standard generic models, which have been informed by real situations, but are not intended

to represent any actual future developments. The selected typologies are purely for

modelling viability, and for the avoidance of doubt, are not policy options being considered

by the council.

2.2 Residential

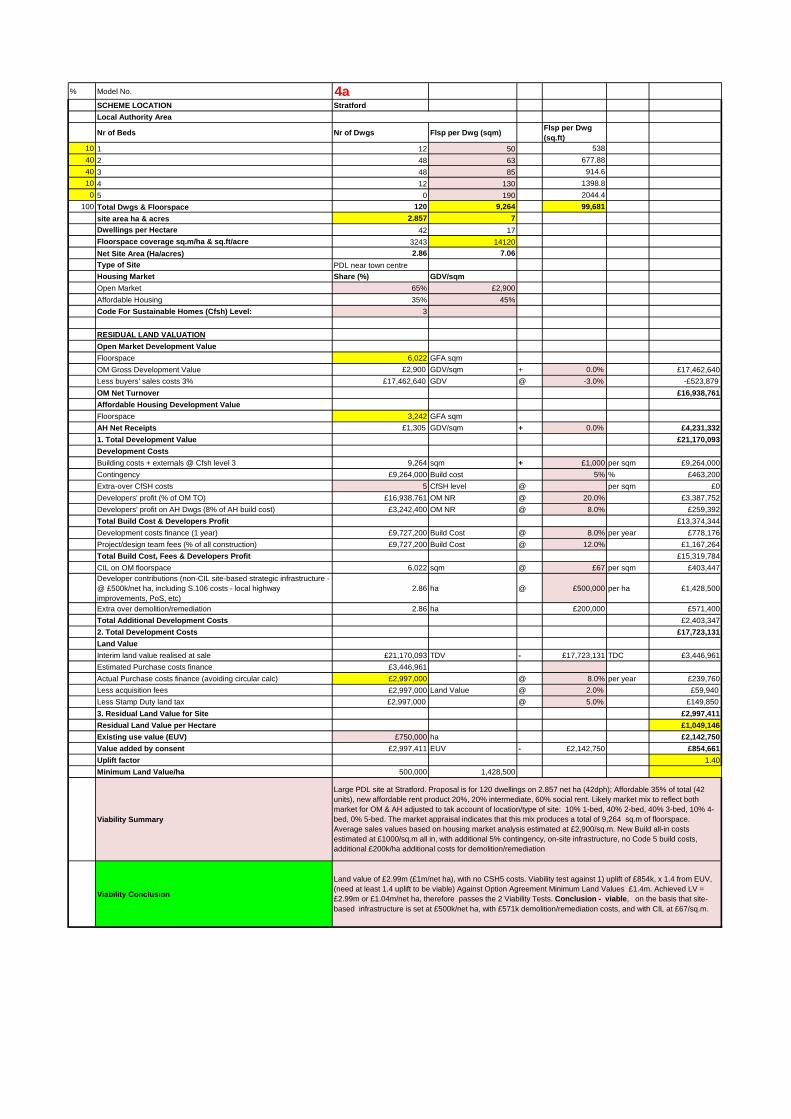

2.2.1 The notional residential sites tested are set out in Table 2.1.

Table 2.1: Residential Notional Sites for Viability Testing

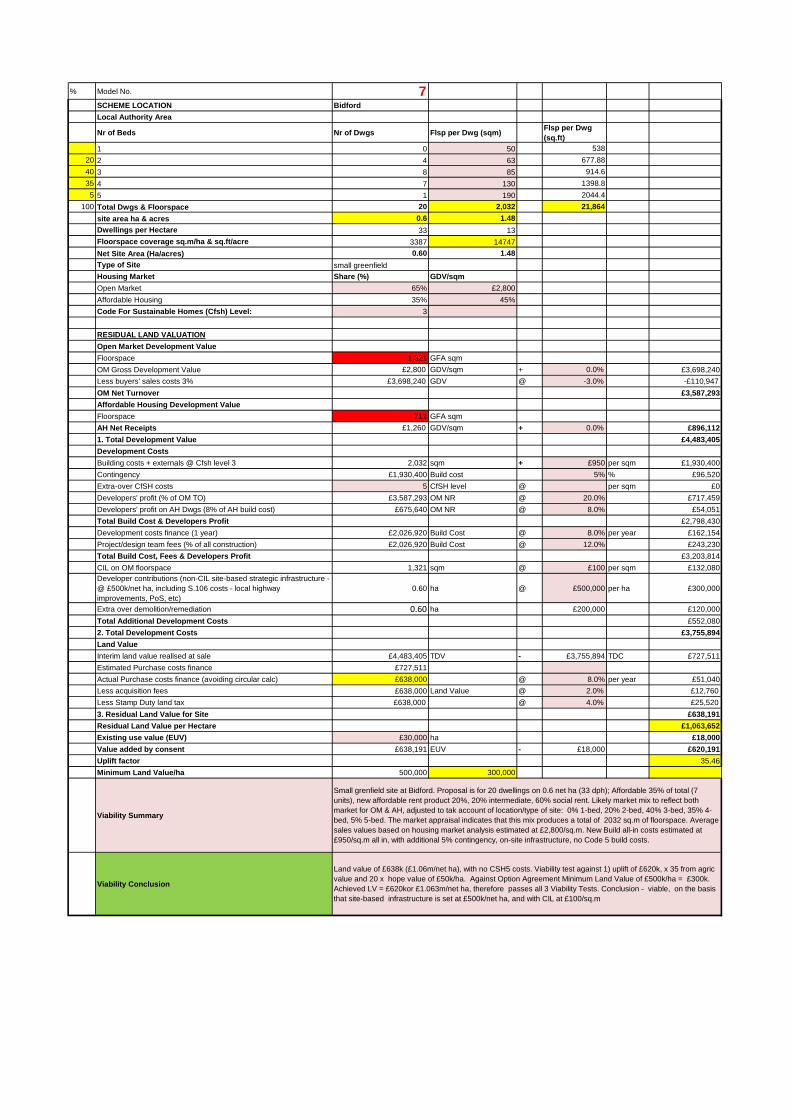

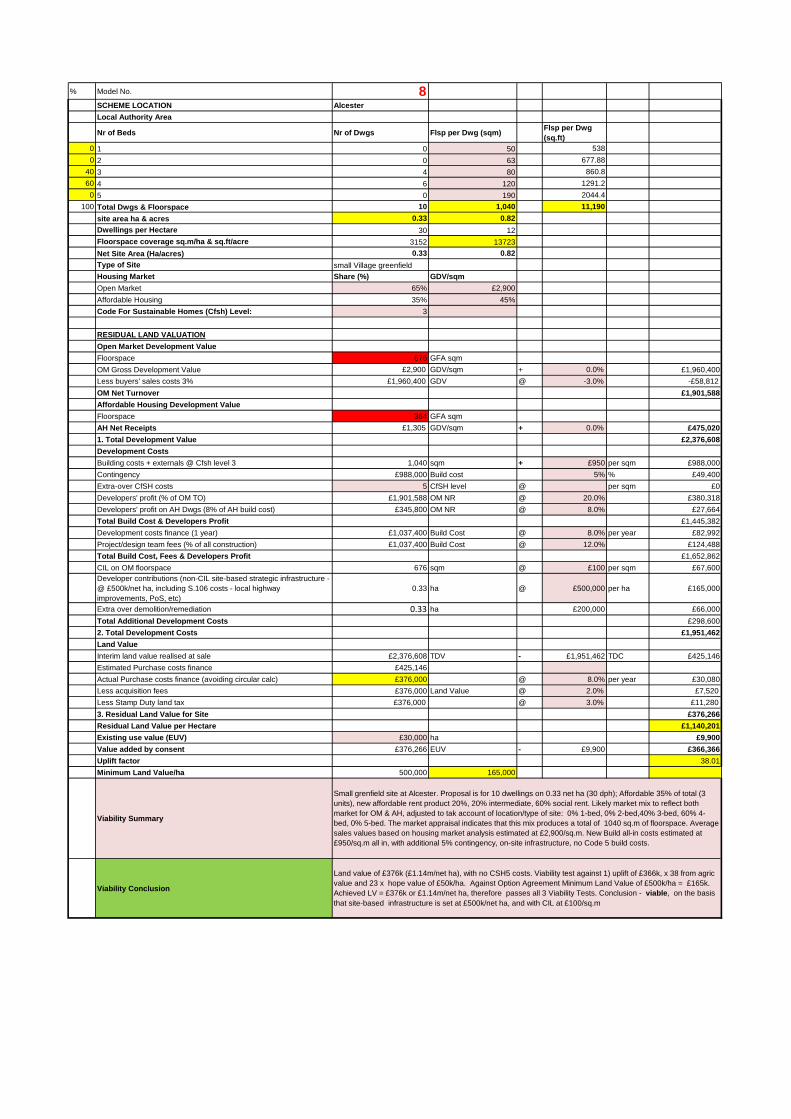

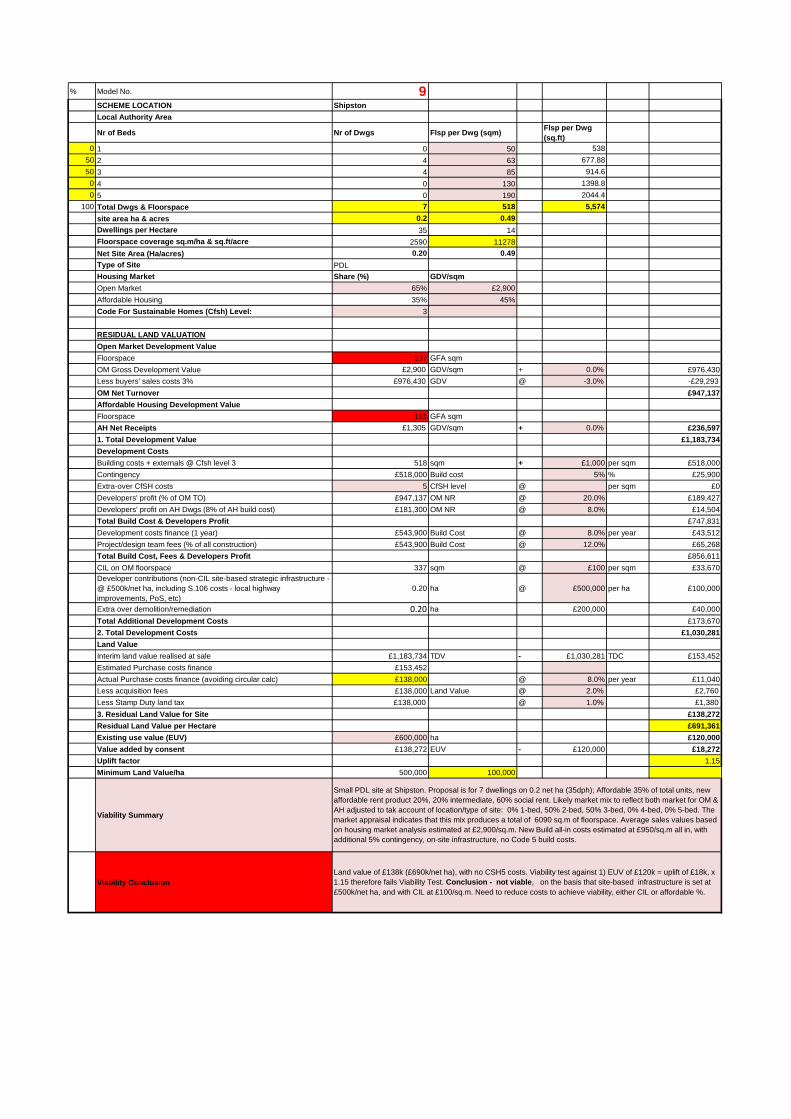

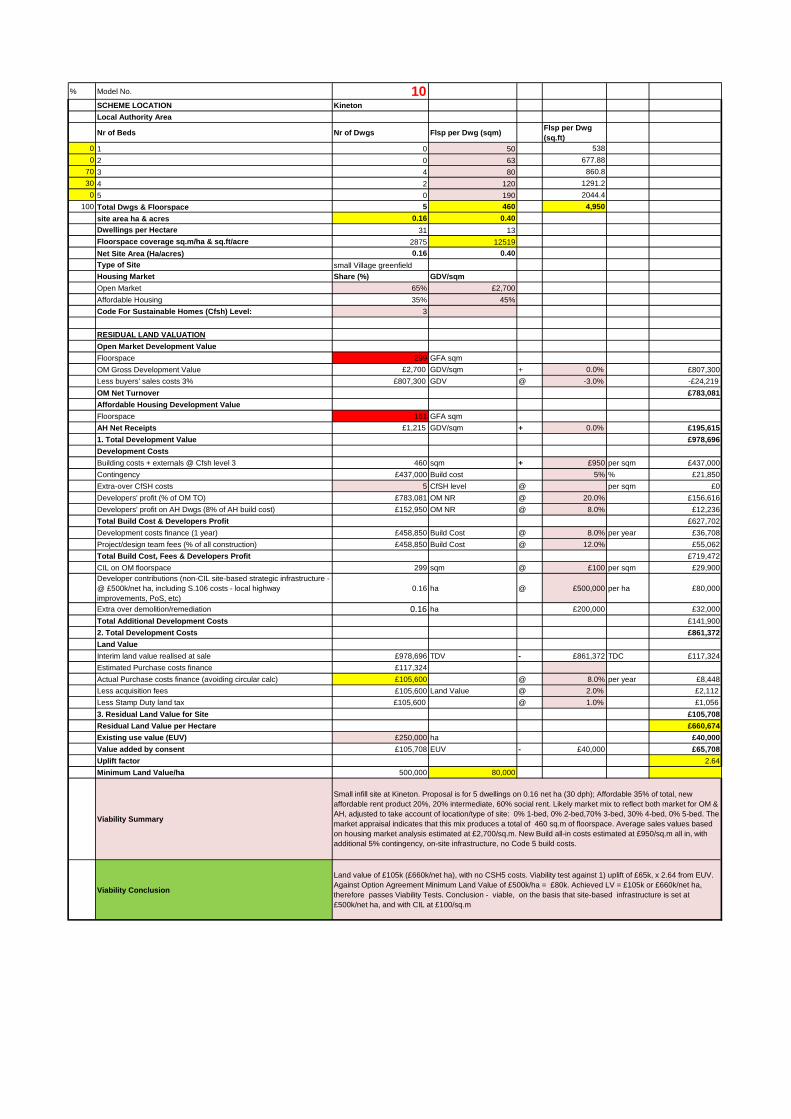

Generic Site Nominal Location

Dwelling Capacity

1 urban extension model Stratford-upon-Avon

2000

2 urban extension model Stratford-upon-Avon

500

3 urban extension model Southam 200

4 large PDL model Stratford-upon-Avon

120

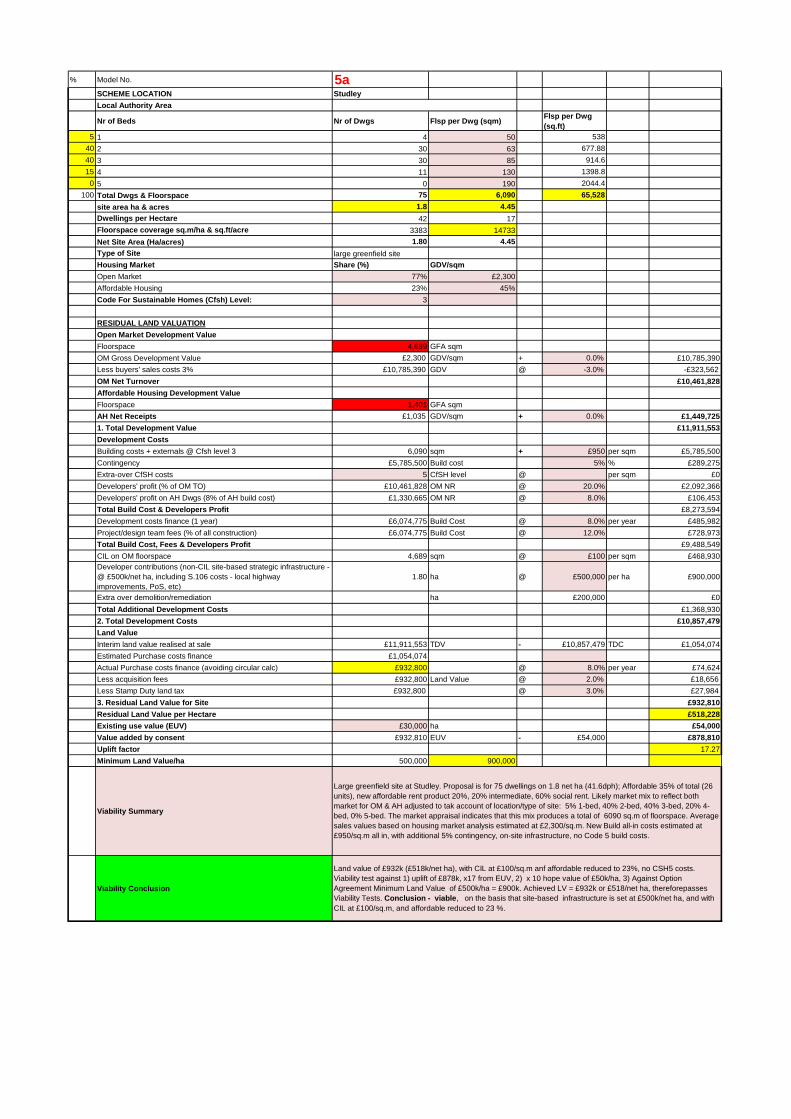

5 Greenfield model Studley 75

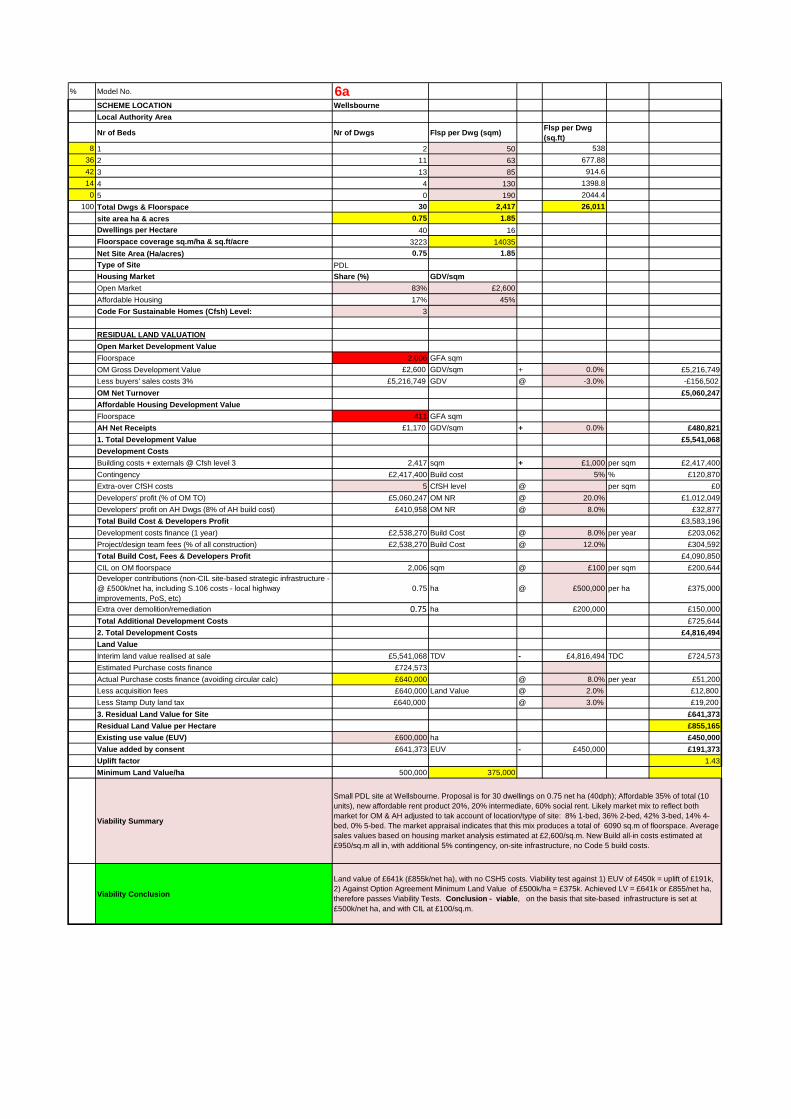

6 PDL model Wellesbourne 30

7 Greenfield model Bidford-on-Avon 20

8 Greenfield infill model1 Alcester 10

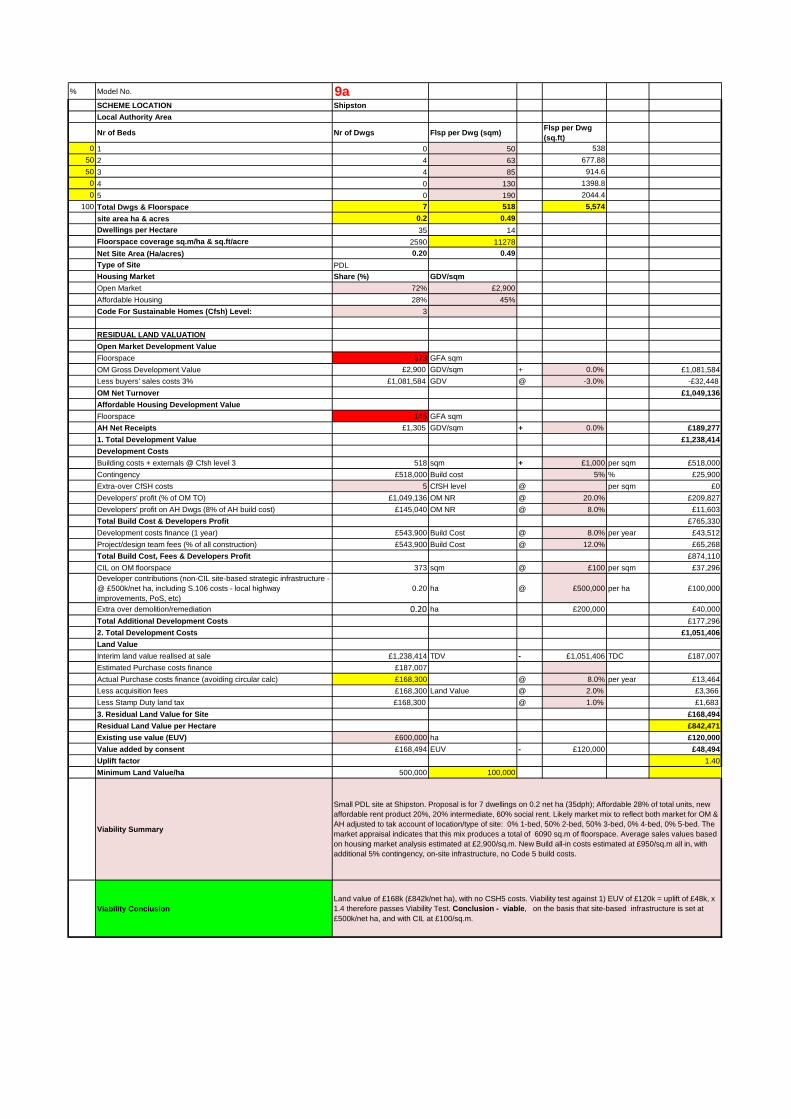

9 Small PDL model Shipston 7

10 Greenfield infill model1 Kineton 5

11 Greenfield infill model1 Tysoe 5

2.3 Non Residential

2.3.1 Based on our understanding of Stratford-on-Avon District, previous experience and the

authority’s future development plans we have identified some ‘typical’ development

typologies. These have been informed by real situations, but are not intended to represent

any actual developments.

2.3.2 Whilst many developments may share the same use class, they are not necessarily the

same use in terms of Section 13 of the CIL Regulations. Therefore we have tested a range

of non-residential typologies within the same use class, as per the CIL regulations.

Retail uses (A1)

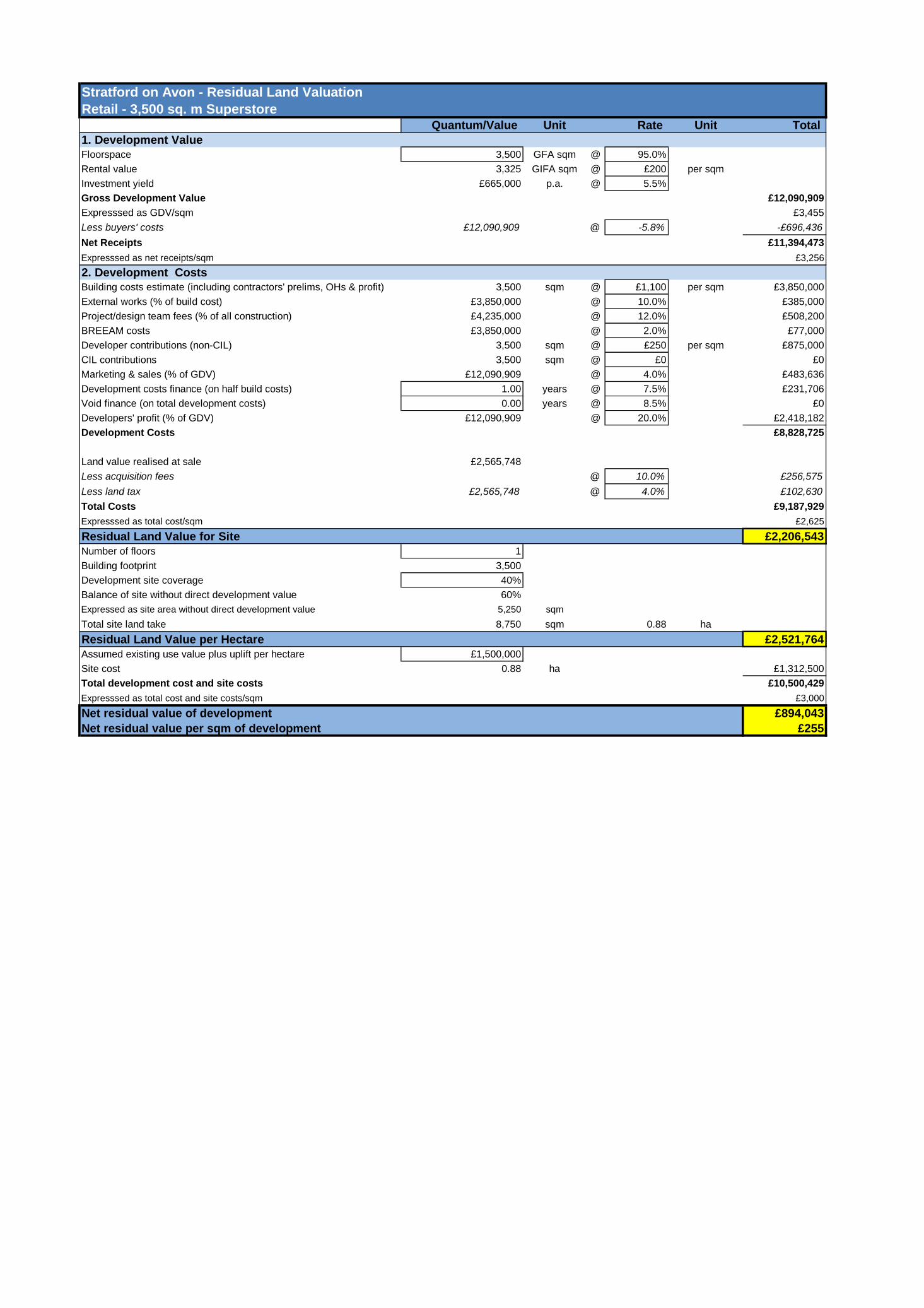

2.3.3 We have based our A1 assumptions on four retail typologies:

1 Please note that all infill sites are considered to be located within settlements

CIL Economic Stratford-on-Avon CIL

13

Superstore and supermarkets – out of town centre/urban extension development of

gross 3,500 sq.m with a site coverage of 40%;

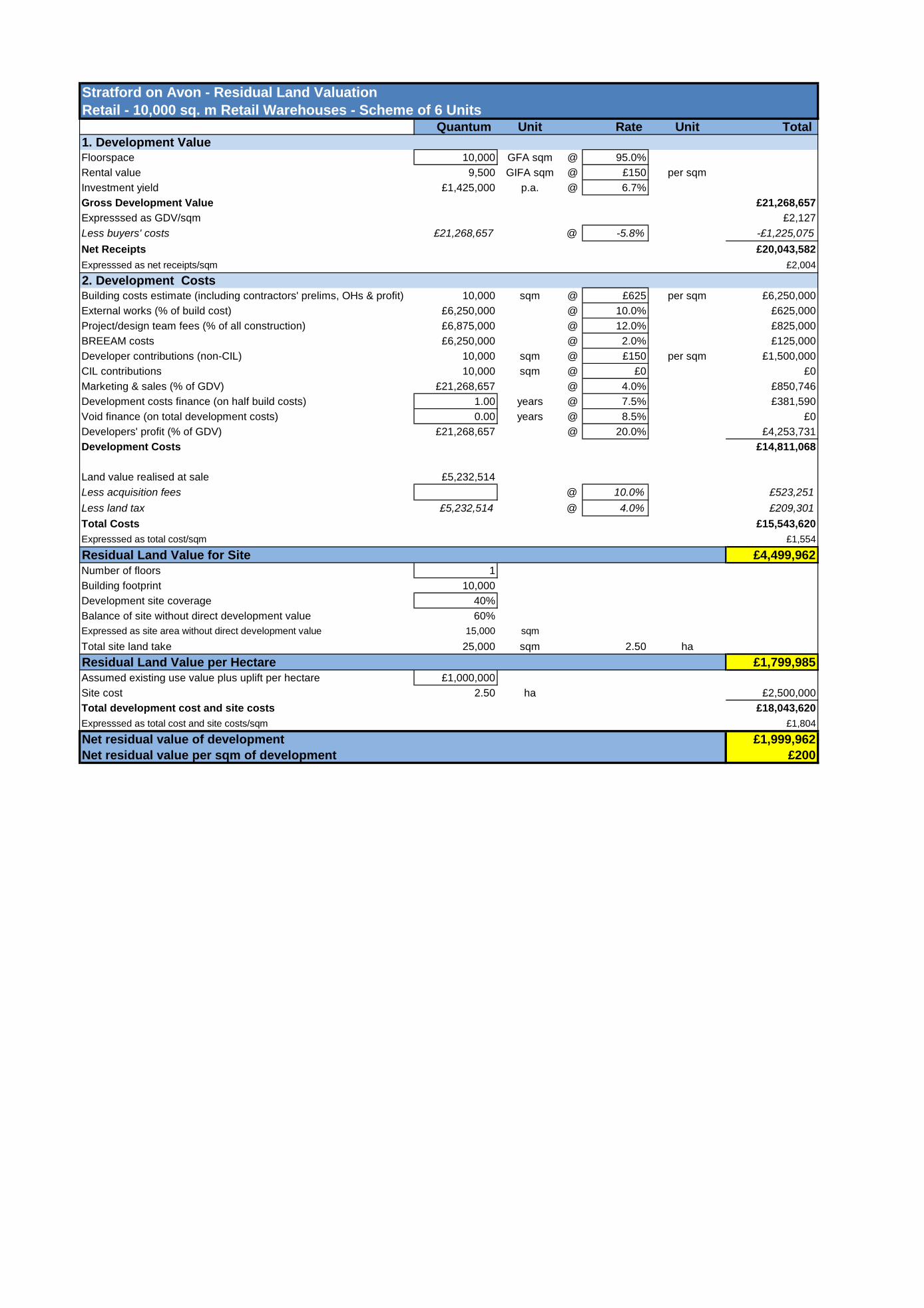

Retail warehouses – out of town centre development of six retail warehouses totalling

10,000 sq.m gross with a site coverage of 40%;

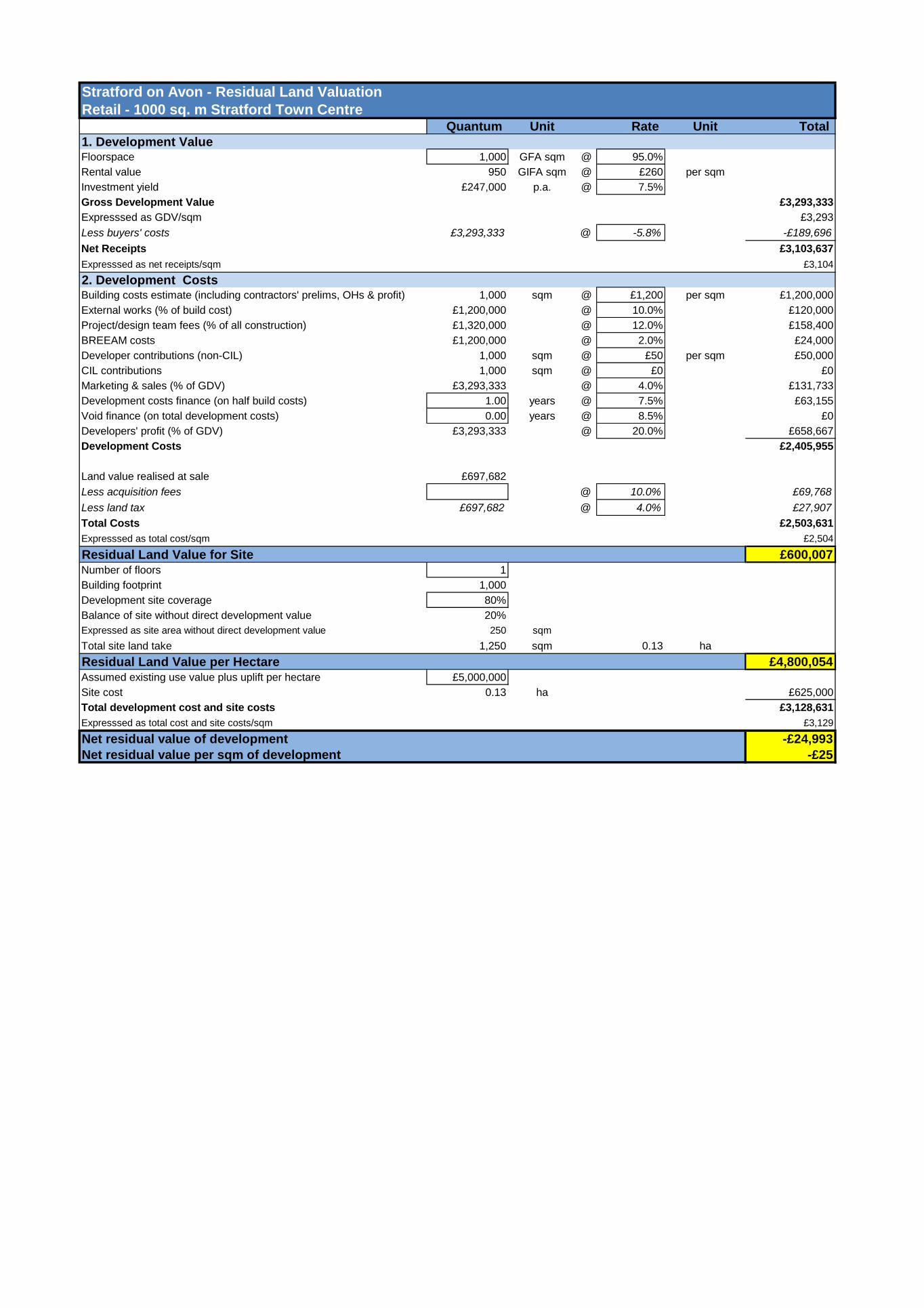

Town centre retail in Stratford-upon-Avon – Stratford-on-Avon’s Local Plan sets out the

town centre boundary which represents a reasonable delineation between in and out of

centre areas in functional terms. As the highest value area, it is considered that if town

centre development in this location is not viable then it won’t be viable in other centres;

and

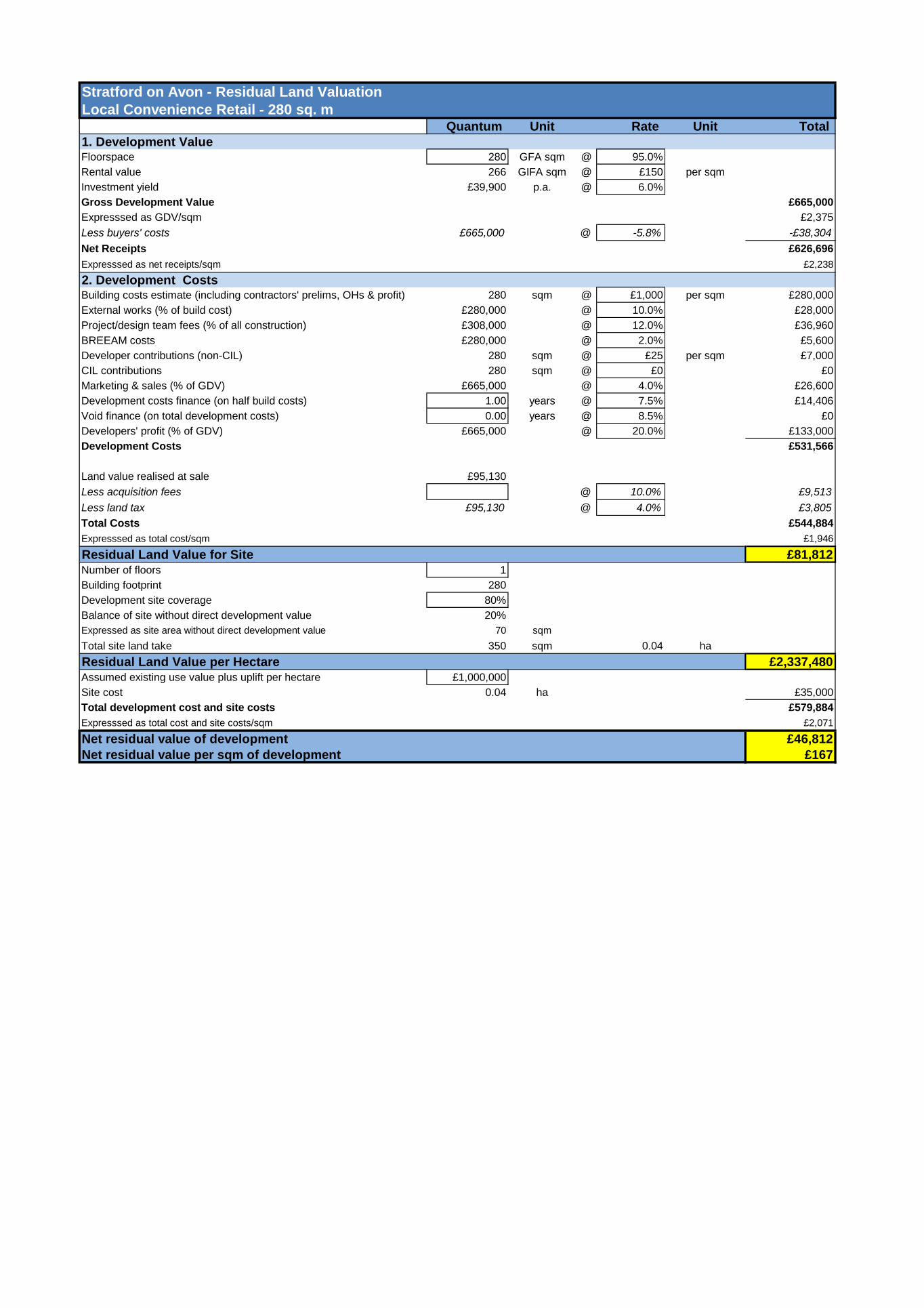

Local convenience retail – all locations, size of 280 sq.m with site coverage of 80%.

2.3.4 In determining these convenience orientated typologies it is understood that the council has

not planned for any in centre supermarkets or superstores and therefore we have not

specifically tested this use – however it is understood that there is ongoing interest in out of

town centre locations and therefore we have tested these locations. If an in centre

convenience development does occur then the charge will be on the basis of the in town

centre appraised scheme.

Other Retail ‘A’ uses (A2 – A5)

2.3.5 Whilst other ‘A’ uses are differentiated in terms of the use class order it is considered for the

purposes of this work that as town centre uses they will generally compete for similar space

as retail units and therefore occupy the same sorts of premises. On that basis it is not

necessary to consider these individually for testing purposes as a reasonable approach

needs to be taken. Therefore any recommendations relating to town centre retail will also

apply to all these types of uses as well.

2.3.6 It should also be noted that many of these uses are unlikely to exceed 100 sq.m flooorspace

and therefore would not be eligible for a CIL charge.

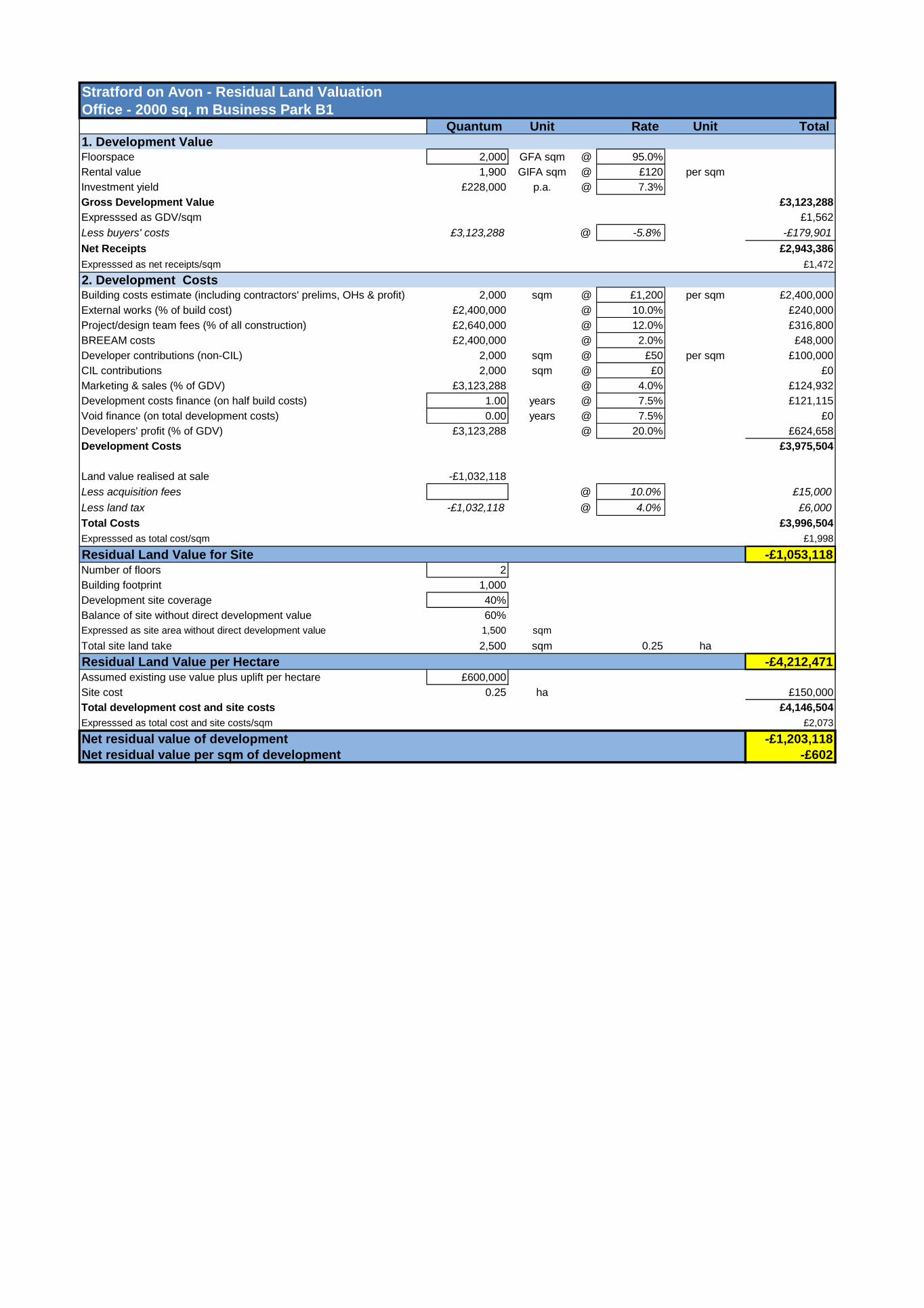

B1 Business Offices

2.3.7 We have used two B1 Office typologies:

In town – 800 sq.m with building foot print site coverage of 90% (development over 5

floors); and

Edge of town development of gross 2,000 sq.m building foot print site coverage of 40%

(development over two floors).

2.3.8 The non-office B1 uses are covered by the B2/B8 uses discussed below.

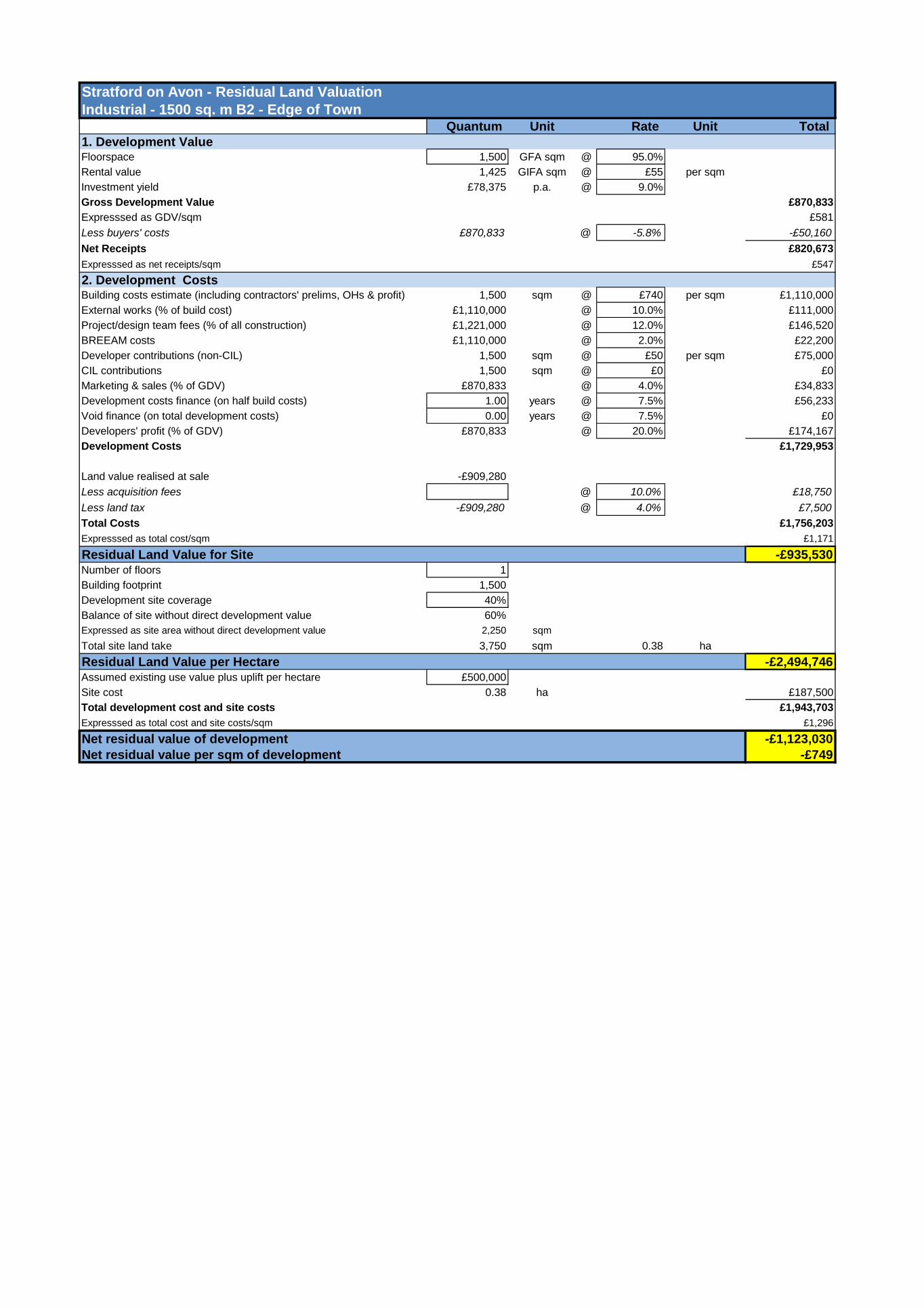

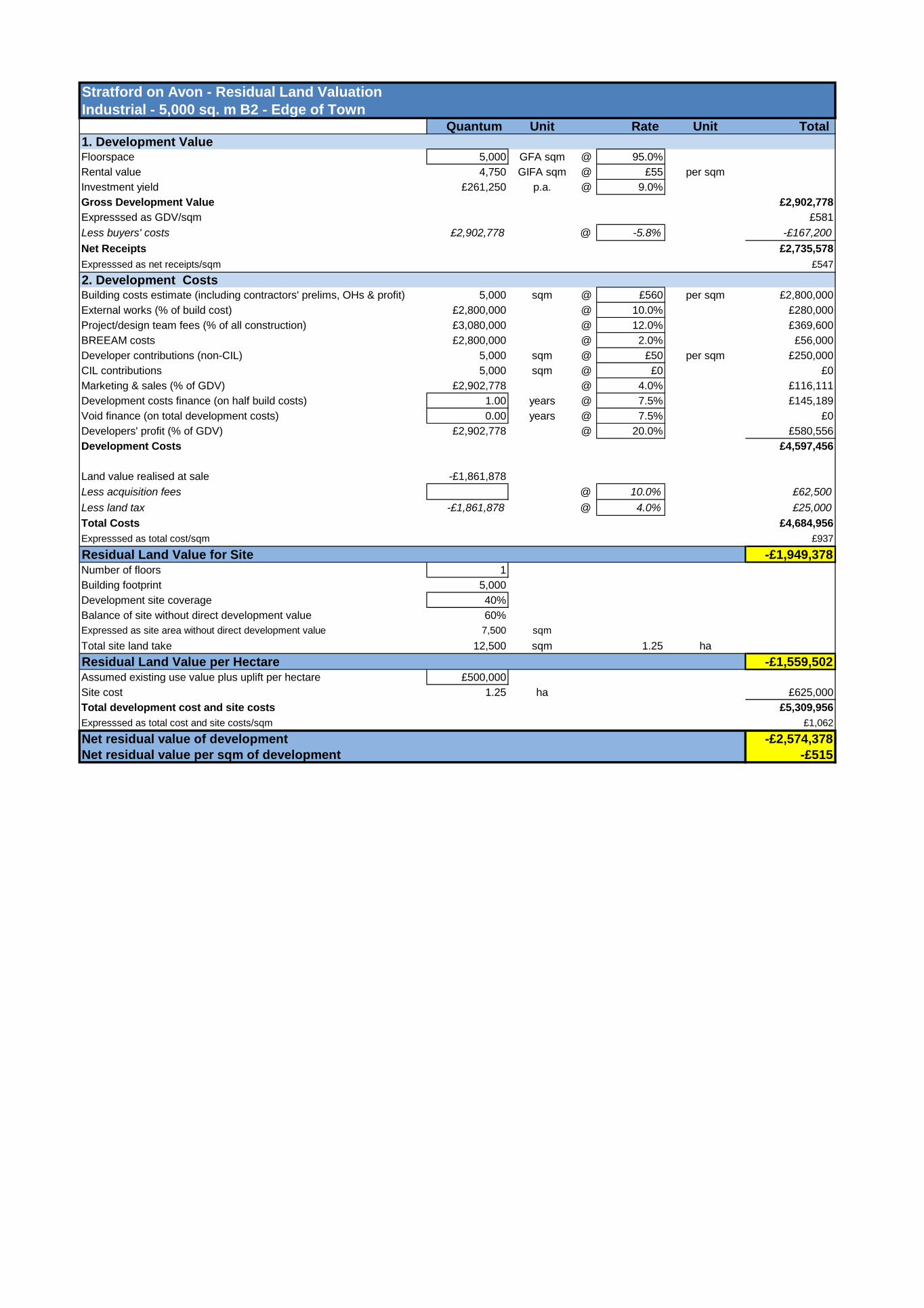

B2 General Industrial

2.3.9 We have used two B2 general industrial typologies:

CIL Economic Stratford-on-Avon CIL

14

Edge of town industrial units of gross 1,500 sq.m with site coverage of 40%. May

include subdivisions into smaller workshop units; and

Edge of town industrial unit of gross 5,000 sq.m with site coverage of 40%.

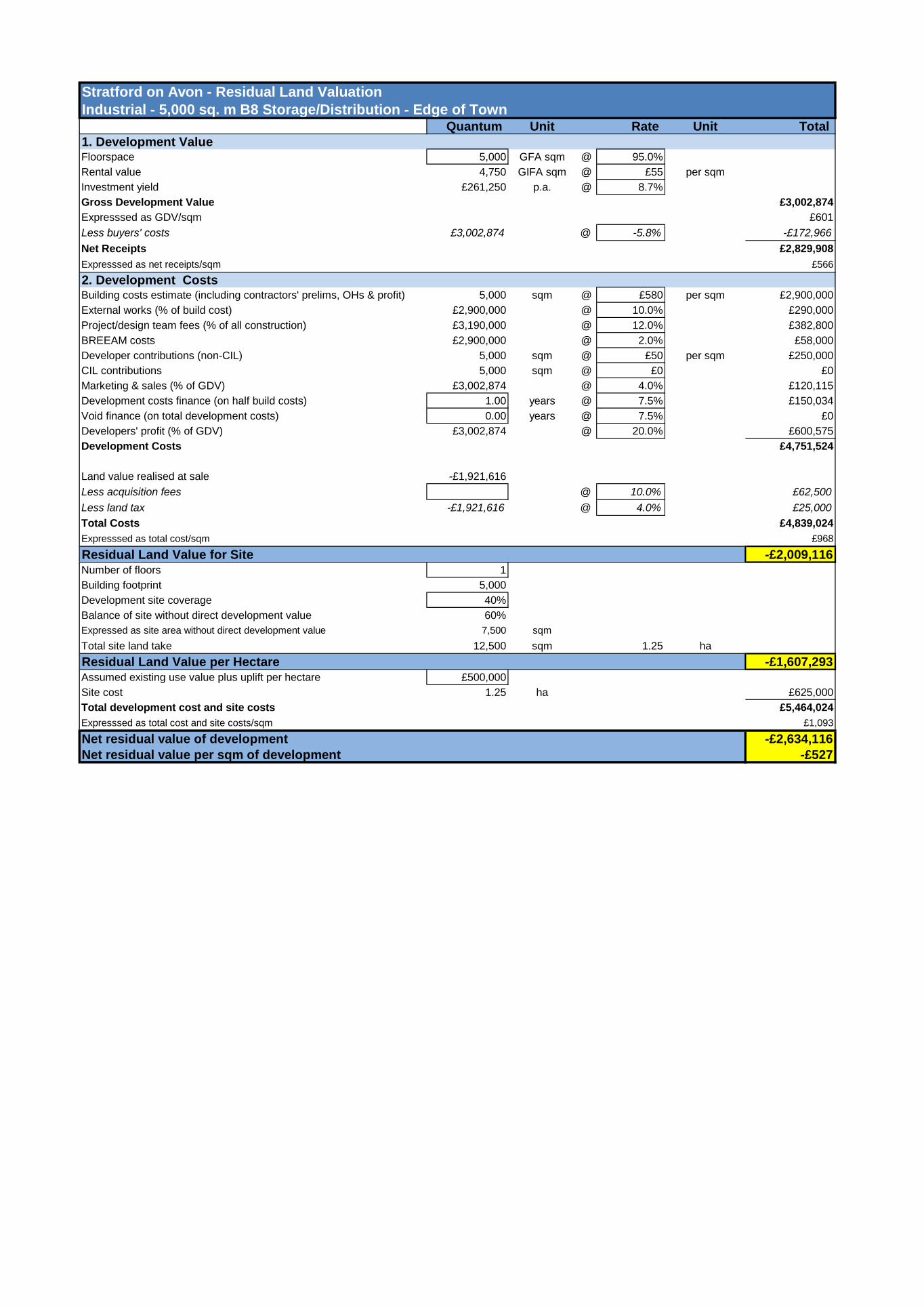

B8 Storage/Distribution

2.3.10 As per B2 General Industrial, in practice the activity will have the same types of premises

and similar values as the larger B2 typology; i.e. warehouse of gross 5,000 sq.m with site

coverage of 40%.

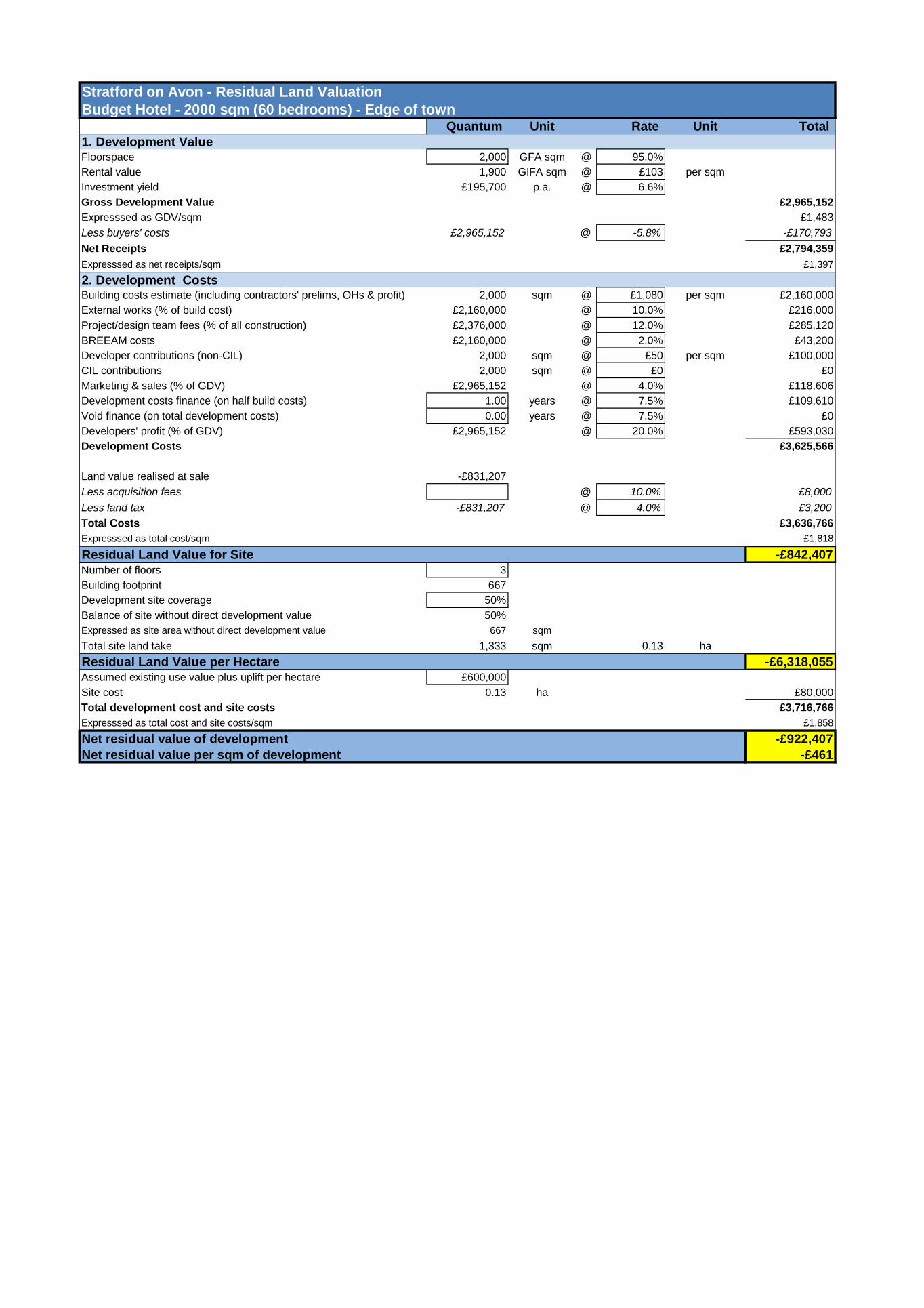

C1 Hotels

2.3.11 60 bedroom hotel of gross 2,000 sq.m on two floors on an edge of town site with 80% site

coverage.

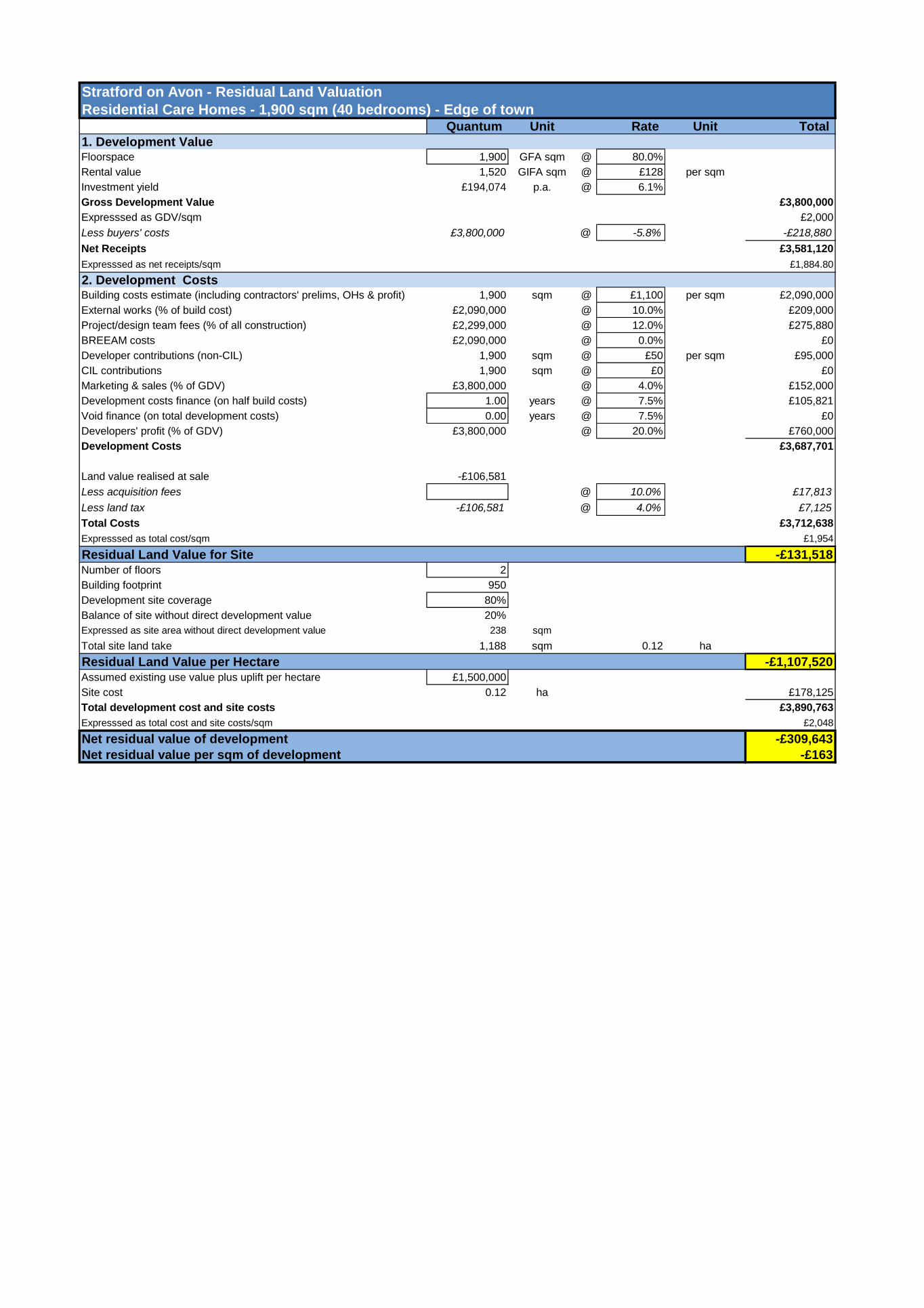

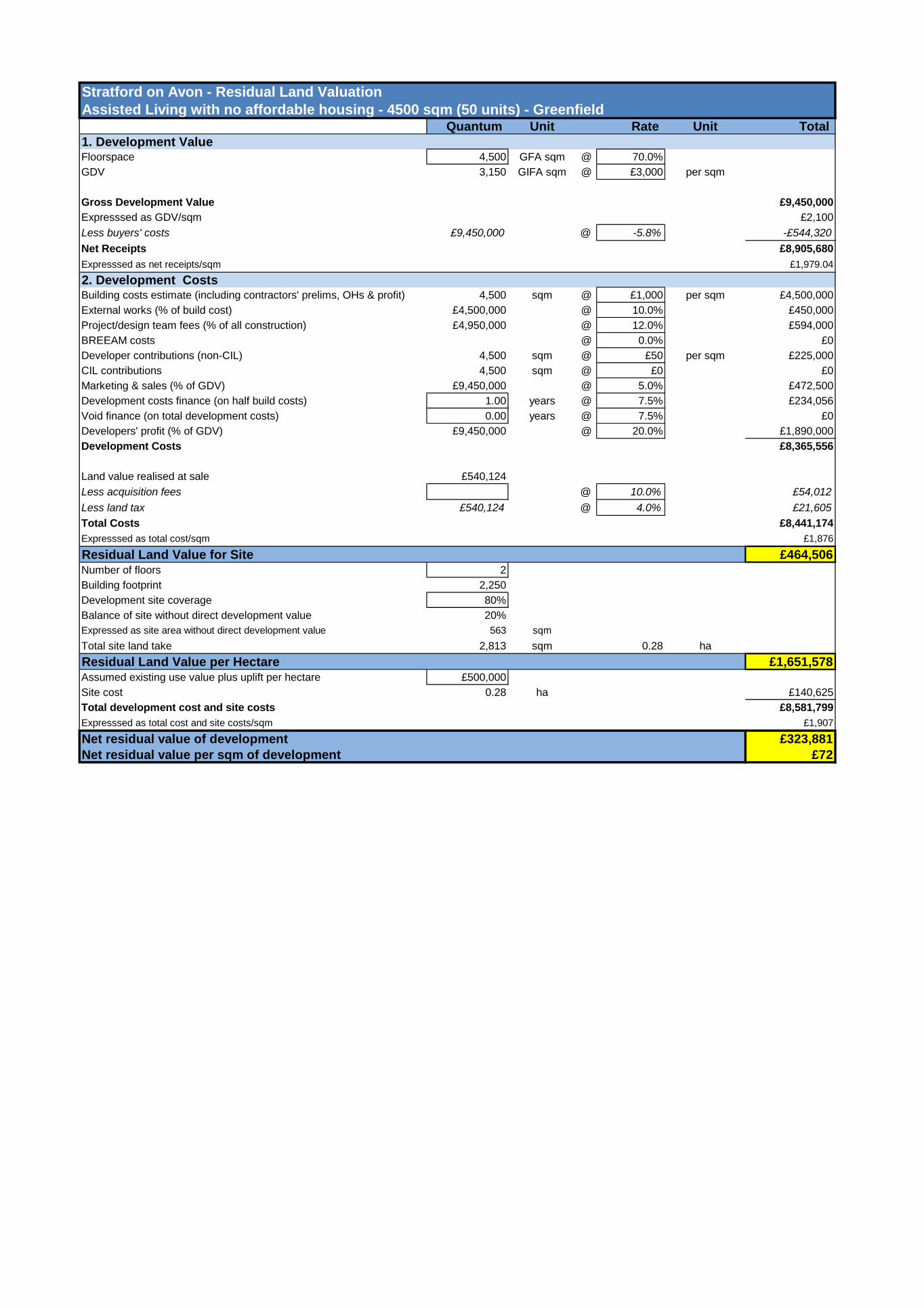

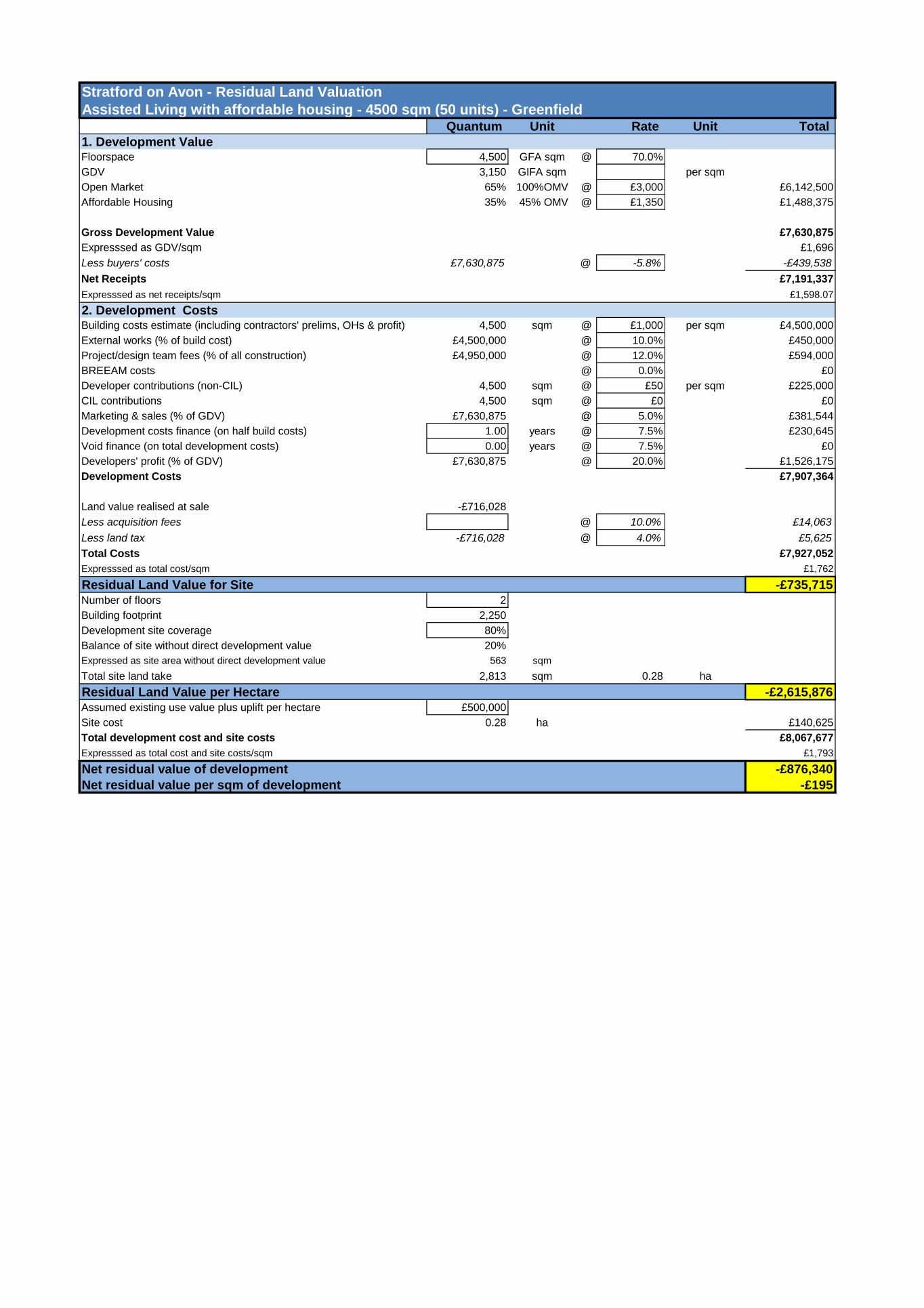

Care Homes and Extra Care Living

2.3.12 In addition to residential development it is appropriate in Stratford-on-Avon to also test

different types of specific accommodation for the older population. To this end two models

have been tested – Care Homes and extra care living accommodation.

2.3.13 The former provides a residential setting where a number of older people live, usually in

single rooms, and have access to on-site care services – they will offer different levels of

care from basic personal care assistance to fully qualified nursing medical care. We have

tested a 40 unit scheme.

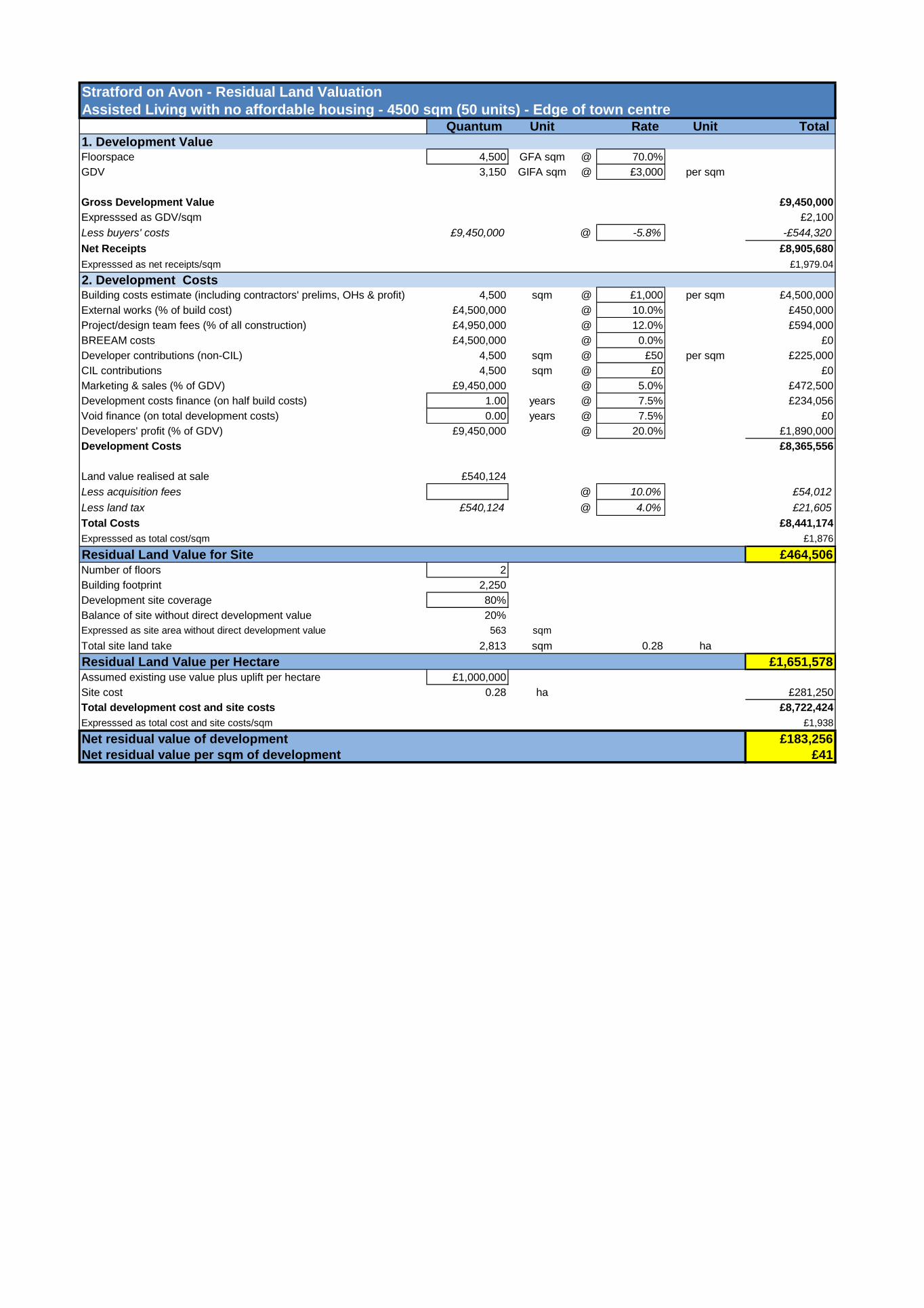

2.3.14 Our second model is extra care living, whereby you live independently in your own home, but

it is located within the grounds of a communal facility which again can provide a range of

services from personal care to medical care. We have tested a 50 unit scheme. It is

considered that for the purposes of testing at a strategic level the scheme to be tested will be

the basic facility which includes the individual units and basic communal facilities such as a

common room. It is noted that varying degrees of medical and restaurant facilities can also

form part of these schemes, however for the purposes of this study it is considered that

these are cost neutral and that if they are provided then they are effectively paid for by the

future residents on top of the basic purchase.

2.3.15 We have tested three different sites, edge of town centre, greenfield and greenfield with a

policy target of 35% affordable housing. Clearly if an affordable housing requirement is

added it will impact on the viability of the scheme to contribute to other S106 costs and CIL.

For the purpose of this study we have used the same blended proportion for affordable

housing as used in the residential appraisals.

D1 Non Residential Institutions

2.3.16 Non residential institutions will vary from public sector or charitable institutions such as

health centres, Children’s Centres, libraries and museums through to commercial uses such

as private sector child care facilities. Many of these will be charitable or public sector uses

CIL Economic Stratford-on-Avon CIL

15

which are not viable in any commercial sense and we have not sought to test these. We

propose that the majority of other development falling into this category will be similar to

town centre shops – in that they are ‘selling’ services such as childcare.

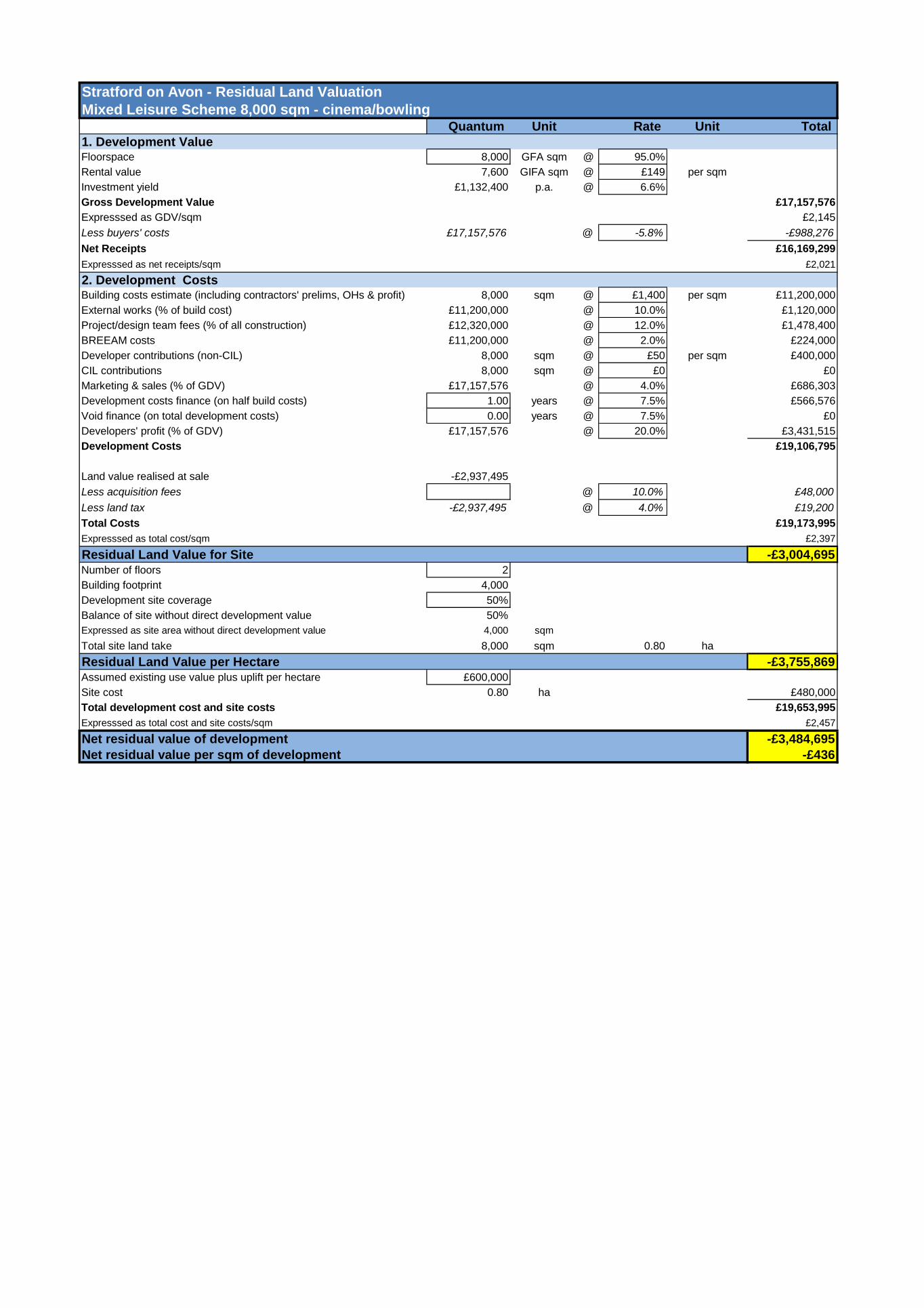

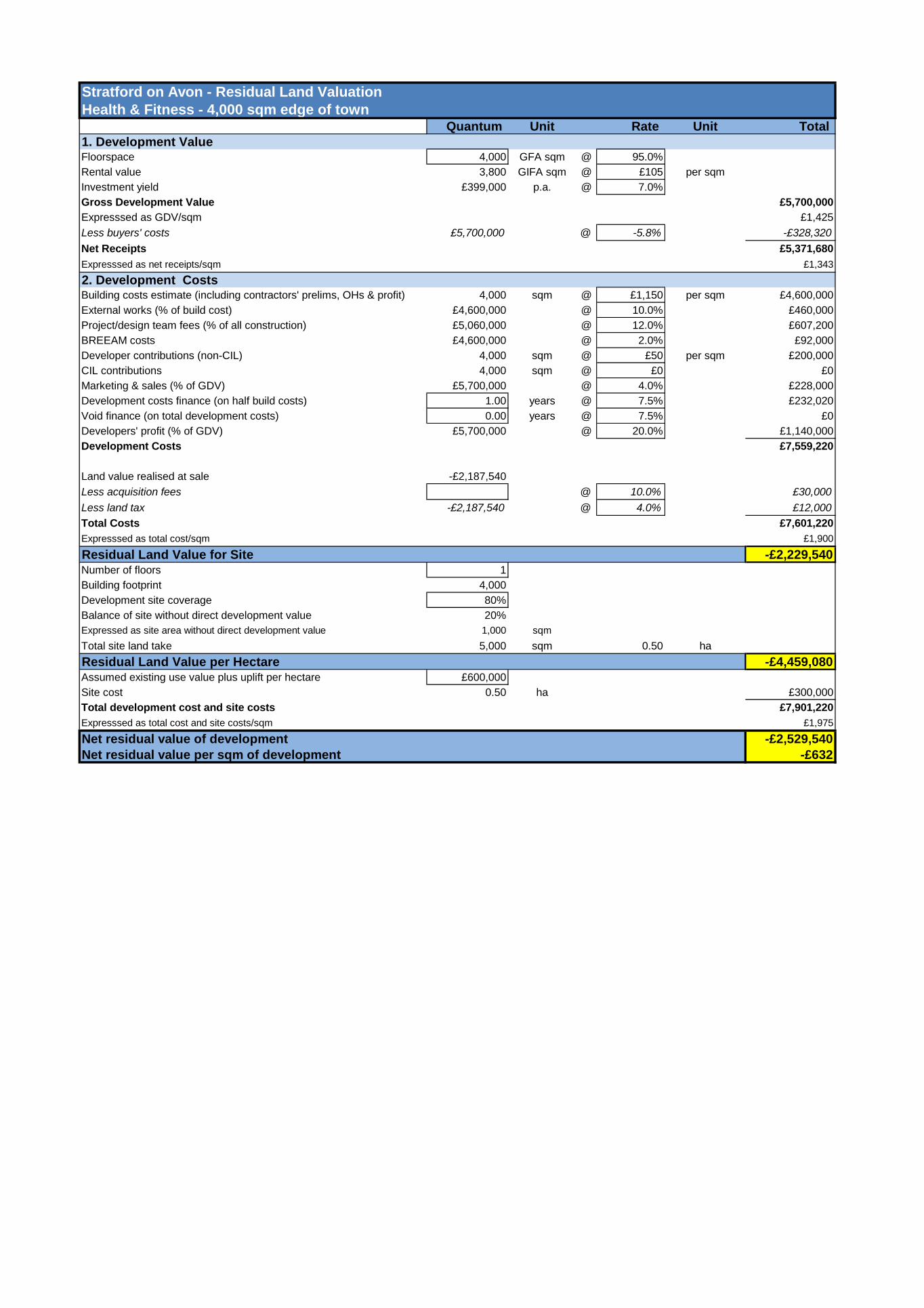

D2 Assembly and Leisure

2.3.17 Assembly and leisure also varies considerably but with common factors. We have tested

two types of development which may come forward:

A mixed leisure scheme to include facilities such as cinema, bowling, health and leisure

complex, gambling and associated eating and drinking establishments; and

A stand-alone commercial health and leisure facility.

Sui Generis

2.3.18 Sui Generis uses include theatres; hostels providing no significant element of care; scrap

yards; petrol filling stations; shops selling and/or displaying motor vehicles; retail warehouse

clubs; nightclubs; launderettes; taxi businesses; amusement centres; and casinos. The

types of premises, value of uses and development costs for premises accommodating these

types of activity will vary considerably; and this means that Sui Generis uses cannot be

treated in the same way as the other use classes.

2.3.19 Our approach to this issue has been to consider the types of premises and locations that

may be used for Sui Generis and assess whether the costs and value implications may have

similarities with other uses. We have also considered the likely developments within the plan

period as a guide to whether more detailed work might be useful.

Theatres – very few new theatres are being developed in the UK and the exceptions –

such as Chester – are in locations with large catchments, an existing foundation of

extensive artistic activity and a local authority with the means and inclination to pay.

Hostels providing no significant element of care – these are likely to be either charitable

or public sector uses such as probation hostels, half-way houses, refuges, etc., or low

cost visitor accommodation such as Youth Hostels. Our view is that the charitable uses

are dependent upon public subsidy for development and operation, and therefore not

viable in any commercial sense. Youth Hostels are operated on a social enterprise basis

with small financial returns. Neither of these scenarios offers significant commercial

viability.

Scrapyards – there may be new scrapyard/recycling uses in Stratford-on-Avon in the

future, particularly if the prices of metals and other materials rise. Subject to consent

these are likely to occupy the same sorts of premises as many B2 uses and therefore

the viability will be covered by the assessment of the viability of B2 uses.

Petrol filling stations – we are aware that the recent new filling stations have generally

been as part of larger supermarket developments, with independent filling stations

closing. It seems unlikely that there will be significant new stand-alone filling station

development.

CIL Economic Stratford-on-Avon CIL

16

Selling and/or displaying motor vehicles - sales of vehicles are likely to occupy the same

sorts of premises and locations as many B2 uses and therefore the viability will be

covered by the assessment of the viability of B2 uses.

Retail warehouse clubs – these retail uses are likely to be in the same type of premises

as the out of town A1 retail uses and covering the same purchase or rental costs.

Therefore they are covered by this viability assessment.

Nightclubs/Laundrettes/Taxi businesses/Amusement centres – these uses are likely to

be in the same type of premises as A1 town centre retail uses and covering the same

purchase or rental costs. Therefore they are covered by this viability assessment.

Casinos – The Casino Advisory Panel has advised the Government where the one

regional, eight large and eight small casinos should be located and the locations have

not included Stratford-on-Avon District. While an existing hotel may add a small casino

to its existing operation this will be part of the overall hotel viability.

CIL Economic Stratford-on-Avon CIL

17

3 Viability Assumptions

3.1 Reviewing the Existing Viability Evidence (Value and Costs)

3.1.1 Obtaining the data – we use a range of information sources in setting benchmark land values and

getting intelligent inputs to our residual value modelling. The regulations require Charging

Authorities to use “appropriate available evidence” in setting their CIL Charge. The sources we

used are as follows.

Internet sources. In order to keep costs down, we take advantage of free sources such as

Estates Gazette, or Davis Langdon cost levels – which have the great advantage of showing

the typical buildings used for the calculation. We also use management consultants’ studies,

quality press reports (FT.com is an excellent source) and industry sector specialist studies.

We use existing information available to the council, such as SHLAA evidence and the

Employment Land Review. There are good reasons to use this already existing information. It

has great advantages of ensuring that there is no contradiction between different studies that

could be used against the CIL charge at examination.

BCIS and Spons cost sources are available to us.

We source residential revenues and other viability variables from a range of sources, including

generic websites, such as the Right Move, and Zoopla, in addition to the Land Registry,

together with direct research with developers, (including Registered Providers of affordable

housing), and agents operating in the area. Revenues have been checked against market

research in the emerging SHMA 2012 Update, which corroborates our findings that revenues

have increased 5% between 2007 and 2010, and 7.5% over the past year to March 2012.

3.1.2 Information on land and property values has been taken from industry standard sources including

the EGi, CoStar (Focus) and Property Week databases.

3.1.3 To estimate construction costs, as well as standard sources such as BCIS, we use data from cost

consultants Davis Langdon. These figures allow for increasingly stringent Building Regulations,

which add to construction costs. For costs such as external works, fees, finance and developers’

margins, we used high-level approximations. We also make separate estimates for S106 and other

site-specific planning contributions. These represent the average over a range of scheme types.

Where relevant, we also distinguish between different parts of the District, to ensure that we have

the right evidence to inform any proposal for geographic differentials in the levy rate.

3.1.4 Our view on this issue is that a simple Charging Schedule with few variations is preferable for

examination and implementation. We need to distinguish circumstances where particular types of

site are prone to different economic circumstances that affect viability. This includes, for instance,

the additional costs associated with large greenfield urban extensions, where the site specific

infrastructure costs required to open up the site for development are significantly greater than for

smaller, brownfield sites. On the other hand, brownfield sites tend to have a much higher existing

use value, based on commercial values as opposed to agricultural value. This can mean that large

greenfield urban extensions, and in some circumstances, brownfield sites, may be unable to

support the same affordable housing and/or CIL rate as other locations.

CIL Economic Stratford-on-Avon CIL

18

3.2 Consultation with the Development Industry

3.2.1 In our experience, local agents and developers are always happy to explain where the

market is at, what is going on, and why.

3.2.2 The consultation with the development industry has helped to make our assumptions more

robust, and these discussions also help us see where potential objections to the CIL might

come from, so that the council can be better prepared to address objections at examination.

3.2.3 We have also carried out discussions with local registered affordable housing providers

based on their current experience of rent and sale revenues in order to provide a suitable set

of affordable housing values to include in the viability calculations.

3.2.4 The key data includes:

Estimated market values of completed development (per sq m);

Existing use and open market land values;

Basic build cost (per sq m);

External works (% of build cost);

Contingencies;

Professional fees (% of build cost);

Marketing & sales costs (% of development value);

Typical S106 costs;

Finance costs (typical prevailing rates);

Developer’s margin (% of revenue);

The net developable area (site area less land needed for open space or major site

infrastructure); large urban extensions normally have a gross to net ratio of between

50% and 70%, depending on size and physical circumstances, including drainage and

flood constraints; and

The density and mix of development.

3.2.5 To determine benchmark land values, we pull together the evidence gained in the stages

above, use market evidence of actual transactions, and filter these findings through our own

professional judgment and experience. All this information is used to inform the viability

modelling.

3.2.6 We worked with the council to set up a Stakeholder meeting for agents, developers and

affordable housing providers active in the District. All members of the Strategic Housing

CIL Economic Stratford-on-Avon CIL

19

Land Availability Assessment (SHLAA) Panel were invited. The meeting took place on 13th

July 2012, and in addition to the consultants and council officers, it was attended by the

following parties:

Andrew Murphy, Stansgate Planning;

Peter Clarke, Peter Clarke & Co;

Keith Greenall, Greenall Construction;

Mike Hill, Bromford Housing Association;

David Joseph, Bloors;

John Acres, Turleys;

Anne Smith, Taylor Wimpey; and

Simon Gibbs, Bigwoods.

3.2.7 There was a useful discussion on market factors that have fed into the viability assessments.

A number of interviews have taken place subsequently with developers and agents to inform

and corroborate the cost and value information.

3.2.8 At the meeting it was explained that we had agreed with the council that we would run over

20 viability assessment models to cover both residential and non-residential typologies.

These were tested to cover different locations across the district to reflect geographical

differences in revenues and costs. These notional sites are set out at the beginning of

Section 2.

3.2.9 These models have been completed using local values and costs to test what level of CIL

can be achieved without risking viability, as well as testing current affordable housing

requirements contained in the emerging Local Plan. These different applications have also

been used to assess different density and location factors.

3.2.10 We have allowed for a set of residential viability tests to cover notional developments of

different sizes, locations, densities and mixes, greenfield/brownfield as well affordable

housing and sustainable construction requirements. In order to provide a robust evidence

base it was important that we modelled this broad cross section of development types.

3.2.11 We have also allowed for a set of non-residential viability tests to cover different uses and

some different scenarios within some key uses. In particular we have developed a clear

process for considering retail, where large format out of centre convenience retail continues

to be one of the best-performing investment markets. The sector is characterised by strong

yields and high land values. Hence it should be able to support high levels of CIL. In

contrast, high street retail is generally much weaker with less potential to support CIL

charges. If all retail is merged into one category, total CIL receipts may be much less than

they could be. On the other hand, if retail is split into two categories for CIL purposes, we

need to ensure that the split is based on robust evidence; otherwise the split may be set

aside by the examiner, as happened recently in Newark and Sherwood.

CIL Economic Stratford-on-Avon CIL

20

3.2.12 The proportion and type of affordable housing is one of the key determinants of residential

viability. The dual effect of the imposition of both CIL and the affordable housing

requirement can render some models unviable, or if it is on the borderline of viability, we

refer to the concept of marginal viability. This happens when it is unclear as to whether an

owner would accept the uplift amount. In the event of marginal viability, we carry out

sensitivity testing, which tests what reduction in the level of different development

requirements and obligations is required to achieve viability. Typically, this is likely to involve

a reduction in the proportion of affordable housing sought and a consequential increase in

the proportion of private housing. This would have the effect of increasing the overall land

value until ‘viability’ has been reached. Alternatively, reducing the level of CIL may achieve

viability, and, in the event of marginal viability, it is a political decision as to whether to aim

for maximising either CIL or affordable housing.

What is Economic Viability?

3.2.13 Viability, or a lack of viability, is a concept frequently referred to by developers and

landowners in negotiating contributions towards the provision of community facilities. The

argument put forward is that the overall burden of community gain items can reduce the

actual value to the owner below that of its existing or alternative value, or to such a level as

to render it ‘unviable’, or simply not profitable enough to make a sale worthwhile to the

owner, taking account of taxation liability and relocation costs.

3.2.14 Viability has a central role in policy evolution and negotiations but there is little government

guidance as to how viability negotiations are to be conducted or how local authorities are to

make decisions based upon the outcome of a viability appraisal.

3.2.15 The NPPF provides clear guidance on viability, stressing in para. 173 that, in order to ensure

viability and deliverability:

The costs of any requirements likely to be applied to development, such as requirements for

affordable housing, standards, infrastructure contributions or other requirements should,

when taking account of the normal cost of development and mitigation, provide competitive

returns to a willing land owner and willing developer to enable the development to be

deliverable.

3.2.16 Further guidance is provided in ‘Viability Testing Local Plans’ (Local housing Delivery Group,

June 2012), which emphasises that:

An individual development can be said to be viable if, after taking account of all costs,

including central and local government policy and regulatory costs, and the cost and

availability of development finance, the scheme provides a competitive return to the

developer to ensure that development takes place, and generates a land value sufficient to

persuade the land owner to sell the land for the development proposed.

3.2.17 The Government’s established aim through planning is to ensure that enough land is

identified and brought forward for development, but it recognises that in order to do so,

residual land values must be high enough to encourage landowners to sell land. It therefore

CIL Economic Stratford-on-Avon CIL

21

requires local authorities not to impose a burden of planning gain and affordable housing that

is so great as to depress the land value below that which is sufficient to bring land forward.

3.3 Our Approach

3.3.1 The critical question is what is a ‘viable’ land value? What should be reasonably expected

by landowners as a residual value, once all costs have been deducted? The approach we

have taken to this concept is that it is rational to assume that if a residual value is arrived at

which is in reasonable excess of the current or alternative site value including its current or

potential income, taking account of all sale and related costs, the landowner be pursued by

developers, and the site be delivered through the operation of the market.

3.3.2 What is a ‘reasonable excess’ in practice? It must be a level sufficiently acceptable, given all

the planning circumstances, to persuade the landowner to dispose to a developer. This

must work both ways in a sale; for example, some landowners may be willing to sell at a

given price, but cannot attract a purchaser, in which case the price is too high.

3.3.3 The definition of ‘viability’ for the purposes of this assessment is the attainment of a site

value sufficiently in excess of the current site value that all stakeholders, including the

purchaser and landowner, all acting reasonably and rationally, would accept, thus securing

delivery of the proposed development.

3.3.4 Clearly, not all landowners adhere to the same concept of reasonableness and rationality in

defining viability. Studies of economic viability have taken two broad approaches. One

relates to the acceptability of development land prices to existing/alternative non-residential

use values (‘the economic approach’). The other relates acceptability to expectations based

on residential land prices currently being achieved (‘the psychological approach’).

3.3.5 Residential - We use three benchmarks to assess residential viability. The first is the simple

comparison of relative land values, comparing the value achieved on the assumption of a

planning consent with the existing use value (EUV), (the ‘economic’ approach). If a value

with consent is sufficiently in excess of the current site value, taking account of current and

potential incomes, then the site can be considered to be viable in principle. The difference in

values is measured by an uplift factor.

3.3.6 As an example, a typical small infill site of 0.2 ha suitable for about 8 dwellings, currently

comprising of unused incidental open space, with a nominal open market value (OMV) of

£10,000 without planning permission, might be worth say £250,000 with a residential

consent, having allowed for all development costs and contributions.

3.3.7 The significant increase in value of £240,000 represents an uplift factor of 24, and would

plainly demonstrate viability. The excess varies in different circumstances, reflecting current

use and taxation levels.

3.3.8 At the other end of the scale, the owner of a brownfield site with an existing use value of

£400,000 that could be worth £440,000 with a residential permission would consider that the

increase of £40,000 (or uplift factor of 1.1), insufficient to persuade the owner to sell,

particularly given taxation on capital gains, in addition to sale and possible relocation costs.

CIL Economic Stratford-on-Avon CIL

22

For most sites, an uplift factor of more than 1.4 will be required to enable viability, depending

on site characteristics and circumstances. An uplift of 1.4 would normally be considered to

be marginally viable.

3.3.9 In addition to achieving an acceptable uplift factor taking account of the existing use value,

all sites must exceed the opportunity cost of income that could be generated by an

alternative use. As an example a 1 ha brownfield site in an appropriate location (eg, close to

a town centre) could theoretically accommodate about 100 cars for parking at £5 per day for

say 40 weeks, or 200 days, which would generate an annual income of £100k.

3.3.10 At 50% capacity taking account of overall and fluctuating demand, as well as voids, 50 cars

would generate £50k per year. The uplift value should take account of potential for such

income, and the potential annual interest that would be generated by the sale which would

be forgone if the site remains a car park. The uplift should significantly exceed the potential

income of the alternative use.

3.3.11 A second benchmark test is against ‘hope value’. This applies to most land adjoining built-up

areas of settlements, and to sites within settlements in alternative lower value uses which

are perceived to have ‘hope’ of a change of use. The hope value of agricultural land is in the

region of £50k/ha, and for brownfield sites this needs to be considered on an individual

basis.

3.3.12 Greenfield urban extensions are often subject to option agreements, where the value is

calculated at the time planning permission is granted, and where there is frequently a

minimum value provision in the agreement. This is the third benchmark comparison, and

currently, the typical minimum land value is about £500k per net developable ha and

greenfield sites that achieve less than this are deemed not to be viable.

3.3.13 There may be occasions where minimum land values are not achieved but the landowner

and promoter are both keen to secure a deal, in which case a land value is negotiated. This

may be slightly above or below the minimum, but the standard used is the best against which

to benchmark achieved residual value (RLV).

3.3.14 Each of the residential generic site typologies is tested against all three benchmarks, where

appropriate, and the viability conclusion is based on these tests.

3.3.15 Non-residential – We take a similar approach to the residential testing in that we compare

the residual value with that of an existing use value plus uplift. As previously described, sites

in town centres will already have a high existing use value in comparison to say an

agricultural field. They are normally generating income and therefore a reasonable approach

needs to be taken in terms of both their existing value as often a going concern and the uplift

required incentivising redevelopment. For town centre sites we look at local market data

when property has exchanged and then apply an uplift factor of at least 1.4 to provide a

realistic incentive. Our view on uplift is also within the context of the type of use proposed,

high value uses such as supermarkets require a greater uplift as the landowner will know the

greater value of these uses and therefore expect a higher price. A similar approach is taken

CIL Economic Stratford-on-Avon CIL

23

to out of centre and edge or out of town sites, although clearly the existing use values will

change according to location.

CIL Economic Stratford-on-Avon CIL

24

4 Residential Viability Assessments

4.1 Assumptions

4.1.1 A number of assumptions need to be made as part of the viability appraisal process in order to

illustrate site value and its ability to meet community gain, and remain viable. A site can be

developed in a myriad of different ways, and the variables are so numerous that the permutations

are infinite. Each generic site Viability Appraisal considers the variables that affect the site value,

to enable a site’s market and physical characteristics, and costs, to be inputted into each appraisal

to reach viability conclusions.

4.1.2 Each Viability Appraisal in Appendix 1 summarises the development assumptions. This includes

the site area, the total number of dwellings, with details of mix and tenure, in order to arrive at

floorspace assumptions. Sales values and build costs are also summarised. A merged mix of

affordable and open market housing, based on 35% provision of affordable residential floorspace

has been used. Each generic site appraisal is summarised in Appendix 1, and clearly sets out the

development assumptions that underpin each viability appraisal. The principal variable factors are

explored below:

4.2 Dwelling Mix

4.2.1 The dwelling mix for each generic site is derived from information contained in the SHMA on

recommended dwelling mix for both affordable and open market housing.

4.2.2 This is modified to reflect the location and site characteristics of each generic site, and the housing

market in the nominal location. Town centre sites are more likely to accommodate town houses

with some flats, whilst greenfield urban extensions have a much higher proportion of family

dwellings, and reflect the entire range of market demand.

4.2.3 Each generic site appraisal makes reasoned assumptions about the type of dwellings and density

that would be appropriate for the location and size of the site, and sets out a summary, detailing the

assumptions made about the total number of dwellings, the mix of types, and the resultant floor

areas, informed by different dwelling sizes favoured by private developers, and Registered

Providers (RPs) of affordable housing. As a guide, a range of typical floorspaces, for different

dwelling types, applicable to both flats and houses, is set out in table 2.4.10.

Table 4.1: Typical Floorspace by Dwelling Type

Dwelling Type Typical Floorspace Range sq.m

1-bed 2 person 45 - 50

2-bed 3 person 60 - 65

2-bed 4 person 65 - 70

3-bed 5 person 75 - 80

3-bed 6 person 80 - 90

4-bed 6 person 100 - 120

4-bed 8 person 120 - 180

5-bed 8+ persons 185+

CIL Economic Stratford-on-Avon CIL

25

4.3 Coverage, or Saleable Floorspace

4.3.1 In order to establish housing land values, assumptions need to be made about the likely saleable

floorspace of the dwellings, in order to generate an overall sales turnover. Until the onset of the

recession, the vast majority of housing schemes ranged from around 4,000 sq.m/ha for

predominantly 2 - 2.5 storey development, and up to 4,600 - 5,500 sq.m/ha for 2.5 - 4 storey

scheme.

4.3.2 Since the recession, with market resistance to 3+ storey townhouses and flats, developers are

reducing coverage to an average ranging from 3,000-3,700 sq.m/ha. There is a diminishing return

on the third storey in townhouses, since lower sale prices per sq.m are achieved, and there comes

a point where a higher land value can be generated on traditional 2-storey dwellings.

4.3.3 Floorspace is also affected by the loss of land given over to other uses than residential. Housing

needs to be serviced by roads for instance, and, for larger developments, land is required for public

open space, strategic landscaping, community buildings, employment, and possibly schools.

4.3.4 The provision of such non-residential land uses have been taken into account in reaching net

residential areas, and have been considered in the generic site viability appraisals. Evidently, the

proportion of saleable floorspace per site has a major effect on sales turnover, and in turn, on land

value, which is a consequence of the relationship between sales turnover and development costs,

profit, and overhead. Total turnover is dramatically increased by greater coverage.

4.4 Sales Value for Open Market Housing

4.4.1 In order to arrive at a total sales turnover, assumptions need to be made about sales values.

These have been sourced from an assessment of the housing market based on discussions with

local developers and agents about their current experience, and generic websites such as the

Right Move and Zoopla. We use revenues for new properties because it is from these figures that

current and future land values are derived.

4.4.2 As a guide, open market sales prices per sq.m for new homes, allowing for a reduction between

asking price and achieved selling prices, vary from the lowest at around £2,300 in Studley, to

£2,600 - £2,800 in the eastern settlements of Southam, Kineton and Wellesbourne, to £3,000 in

Stratford-upon-Avon, with the highest prices being achieved in some of the Henley-in-Arden

(£3,300) and Welford (£3,800). This represents an increase of about 10% on selling prices in 2009

when the range was about £2,100 - £2,800, which is a commentary on the strength and resilience

of Stratford-on-Avon District’s housing market.

4.4.3 Sales values are also affected by the specification of the development. A high specification

scheme, usually in a high demand location, can lead to premium sale prices. Open market sales

values are also affected by the proportion of affordable housing on a site, as well as the

juxtaposition of open market housing with affordable housing, particularly social rented units.

4.4.4 Values are also affected by the size of the site, reflecting return on capital employed across a

period of time, the cost of financing a purchase compared with the time taken to receive all site

sales value.

CIL Economic Stratford-on-Avon CIL

26

4.4.5 The helpful discussions with the development industry at the meeting on 13th July provided

invaluable information about the various elements of the housing market, particularly about likely

sales revenues.

4.4.6 Sales rates also have a major effect on the overall financing, and most volume housebuilder

projects seek to achieve around 35-40 open market sales per year (down some 20% from 2007) in

order to justify the land economics upon which the land purchase is based. On larger sites (of, say,

4+ developers), and allowing for affordable housing, this would result in some 200+ dwellings per

annum being completed.

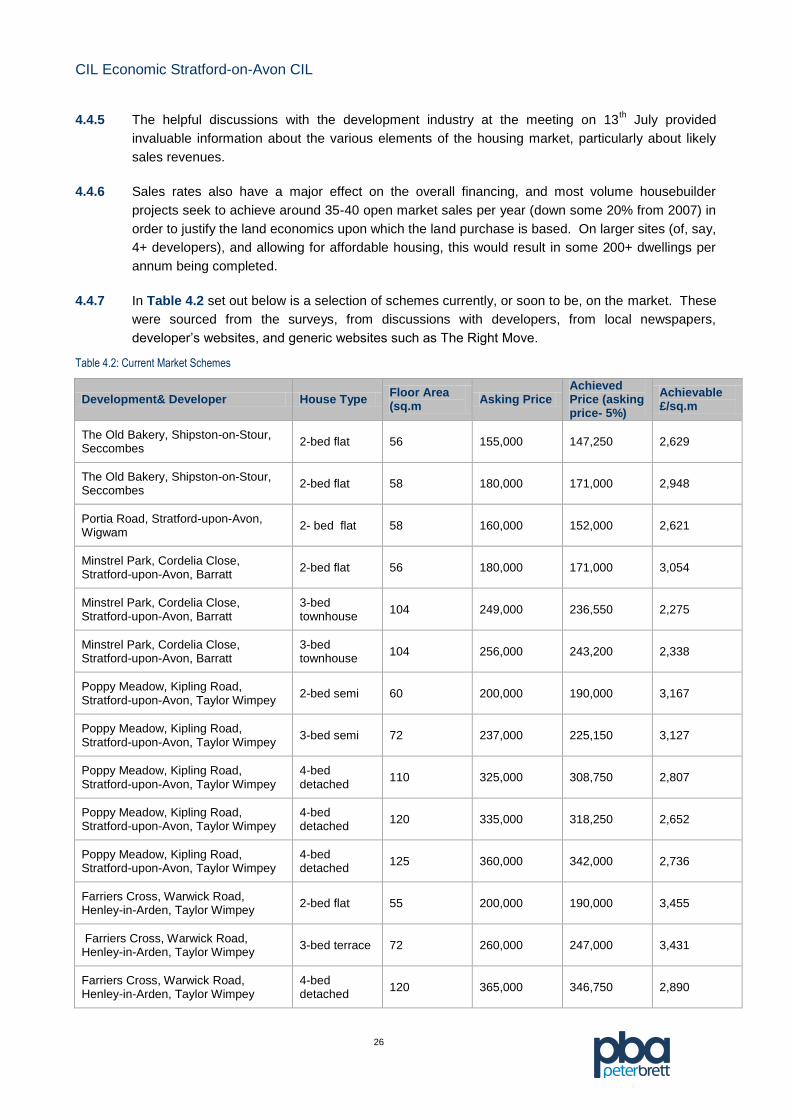

4.4.7 In Table 4.2 set out below is a selection of schemes currently, or soon to be, on the market. These

were sourced from the surveys, from discussions with developers, from local newspapers,

developer’s websites, and generic websites such as The Right Move.

Table 4.2: Current Market Schemes

Development& Developer House Type Floor Area (sq.m

Asking Price Achieved Price (asking price- 5%)

Achievable £/sq.m

The Old Bakery, Shipston-on-Stour, Seccombes

2-bed flat 56 155,000 147,250 2,629

The Old Bakery, Shipston-on-Stour, Seccombes

2-bed flat 58 180,000 171,000 2,948

Portia Road, Stratford-upon-Avon, Wigwam

2- bed flat 58 160,000 152,000 2,621

Minstrel Park, Cordelia Close, Stratford-upon-Avon, Barratt

2-bed flat 56 180,000 171,000 3,054

Minstrel Park, Cordelia Close, Stratford-upon-Avon, Barratt

3-bed townhouse

104 249,000 236,550 2,275

Minstrel Park, Cordelia Close, Stratford-upon-Avon, Barratt

3-bed townhouse

104 256,000 243,200 2,338

Poppy Meadow, Kipling Road, Stratford-upon-Avon, Taylor Wimpey

2-bed semi 60 200,000 190,000 3,167

Poppy Meadow, Kipling Road, Stratford-upon-Avon, Taylor Wimpey

3-bed semi 72 237,000 225,150 3,127

Poppy Meadow, Kipling Road, Stratford-upon-Avon, Taylor Wimpey

4-bed detached

110 325,000 308,750 2,807

Poppy Meadow, Kipling Road, Stratford-upon-Avon, Taylor Wimpey

4-bed detached

120 335,000 318,250 2,652

Poppy Meadow, Kipling Road, Stratford-upon-Avon, Taylor Wimpey

4-bed detached

125 360,000 342,000 2,736

Farriers Cross, Warwick Road, Henley-in-Arden, Taylor Wimpey

2-bed flat 55 200,000 190,000 3,455

Farriers Cross, Warwick Road, Henley-in-Arden, Taylor Wimpey

3-bed terrace 72 260,000 247,000 3,431

Farriers Cross, Warwick Road, Henley-in-Arden, Taylor Wimpey

4-bed detached

120 365,000 346,750 2,890

CIL Economic Stratford-on-Avon CIL

27

Development& Developer House Type Floor Area (sq.m

Asking Price Achieved Price (asking price- 5%)

Achievable £/sq.m

Farriers Cross, Warwick Road, Henley-in-Arden, Taylor Wimpey

5-bed detached

165 435,000 413,250 2,505

The Hathaways, Bishopton Lane, Bishopton, Stratford-upon-Avon, Taylor Wimpey

2-bed semi 60 218,000 207,100 3,452

The Hathaways, Bishopton Lane, Bishopton, Stratford-upon-Avon, Taylor Wimpey

3-bed terrace 75 250,000 237,500 3,167

The Hathaways, Bishopton Lane, Bishopton, Stratford-upon-Avon, Taylor Wimpey

4-bed detached

110 310,000 294,500 2,677

The Hathaways, Bishopton Lane, Bishopton, Stratford-upon-Avon, Taylor Wimpey

3-bed detached

105 320,000 304,000 2,895

Barton Road, Welford-on-Avon, Peter Clarke

4-bed detached

140 700,000 665,000 4,750

4.4.8 A summary of the market in terms of the theoretically achievable land values, sales price per sq. m,

coverage and house types is shown in Table 4.3 below:

Table 4.3: Market Summary

Land Value / net dev ha

Sale Price/sq.m Coverage sq.m / ha Target House Types by Market

£2.5m to £4.2m per ha

£2700 - £3500

3,000 – 3,600 for housing 4,000 - 5,000 for flats/town houses

Preference of developers is firmly for traditional 2-storey 2-4 bed family housing with gardens. Limited up-market flatted schemes can achieve high prices in the best town centre locations.

4.5 Sales Value for Affordable Housing

4.5.1 Registered Providers of Social Housing (RPs) - housing associations and other qualified providers -

have historically had access to funds from the Homes and Communities Agency in the form of

subsidy from public funds, such as Social Housing Grant (SHG) to purchase land, and develop or

purchase affordable housing, including units from developers through the operation of S.106

agreements. The most common delivery of affordable housing is that properties are built by the

developer and transferred to the RP at a price below the full market value through the operation of

S.106 agreements. The formal expectation since 2008 has been that grant will not be available on

developer-led sites that deliver affordable housing through S.106. The gap between the full cost

and the price paid to a developer represents the level of private subsidy (e.g. developer or

landowner subsidy).

4.5.2 In the current economic climate, it is increasingly important to ensure that the most effective use is

made of public funds. The HCA guideline has recently changed, and now RPs should only pay the

capitalised net rental stream on S.106 sites. In addition, the new affordable rent tenure may have

an impact upon revenues. Under this new system brought in by the HCA, RPs be able to charge up

to 80% of gross market rents (inclusive of service charges). In a recent study by DSP Housing and

Development Consultants for Elmbridge Council, it is concluded that the price likely to be received

by a developer for completed units would be no lower with affordable rent than with social rent, and

probably higher, although there is as yet insufficient evidence to quantify the likely increase.

CIL Economic Stratford-on-Avon CIL

28

4.5.3 The council is currently finalising a Strategic Housing Market Assessment Review (SHMA),

which considers housing market mix for both affordable and open market dwellings.

Consultant GL Hearne has carried out an assessment of typical housing mix of dwelling

types to reflect the needs of the population over the plan period. It considers the following

issues:

An overview of housing market conditions - before 2008 and after 2008;

A market appraisal - analysing house price & sale trends - housing stock and

understanding affordability;

Profiles of spatial variations and trends in house prices, market turnover and new build

sales in Stratford-upon-Avon, main rural centres and rural areas;

Housing market dynamics includes consulting estate agents and letting agents. including

buy to let/investment market, checking supply and demand trends; and

Assessing entry level housing costs between tenures and assessment of income, to

assess social rent, affordable rent, private rent and owner occupation.

4.5.4 Our discussions with developers and agents sought views on the state of the housing

market, land values in different parts of the district, sales vales, the types of development, or

dwelling mix, targeted by developers on different sites, and sales rates. These discussions

reveal the following open market housing mix that is generally sought by developers on new

sites:

1-bed 5%

2-bed 35%

3-bed 40%

4-bed 15%

5-bed 5%

4.5.5 These findings are broadly compatible with the housing mix recommendations of the GL

Hearne SHMA Update of June 2012. Whilst the draft SHMA update has been used to inform

preparation of this report, it has not been adopted as council policy, and its testing should not

be regarded as an endorsement. The SHMA update found the following future blended

dwelling mix requirements for both affordable and open market units in the period to 2028:

1-bed 8%

2-bed 34%

3-bed 40%

4+-bed 14%

4.5.6 In reaching conclusions for site assessment yields, we have used these proportions as a

guideline, but taken account of individual site characteristics, and rounded total proportions

up or down to suit these characteristics.

4.5.7 Following discussions with RPs, the generic viability appraisals use revenues that equate to

the level of capitalised rental and revenues for all affordable housing tenures, based on the

CIL Economic Stratford-on-Avon CIL

29

tenure split in the SHMA. Local RPs have estimated this to be about 48% to 52% of the

open market sales values, representing a rate that RPs can purchase from developers

without the use of grant subsidy. They also commented that our estimate of open market

sales was on the high side, and that there was no difference in blended affordable revenues

resulting from an alteration from the 75% - 25% social rent-shared ownership, to the 60%-

20%-20% proposed tenure split in the SHMA to include the new affordable rent product.

This is because the reduction in revenue from shared ownership and social rent is

compensated by an increased from affordable rent.

4.5.8 We have erred on the side of caution, and have assumed a 45% blended revenue from

affordable floorspace. It may be that the overall revenue from affordable housing will

consistently return above 45% of open market revenue, as a result of the new affordable rent

tenure, and this should be the subject of future monitoring by the council in discussion with

RPs.

4.5.9 Each site viability appraisal assumes that affordable housing will be provided on site at 35%

of the total residential floor area, and within this policy a tenure profile applies, with a

minimum requirement of 75% Social Rent and a maximum of 25% Shared Ownership. Any

alternative tenure profiles will require consultation and adoption as council policy, as

suggested in the SHMA Update.

4.5.10 There are an infinite number of possible ways to provide affordable accommodation, with or

without grant. We have assumed, in line with the latest HCA Guidance, that no social

housing grant be available to support the transfer and acquisition of affordable housing

through their delivery by S.106 agreements from the private housing developers to housing

associations.

4.6 Build Costs

4.6.1 The overall build costs, including on-site infrastructure, must be deducted from total turnover

to give an interim land value. After research of the BCIS sources and consultation with the

housebuilding industry operating locally, a range of all-in build costs including externals have

been used. The normal range used in the viability appraisals range from £950/sq.m up to

£1,000/sq.m, to include additional Code 3 build costs, discussed below.

4.6.2 Volume and regional housebuilders usually build at an average of about £800 - £950/sq.ft all

in, including normal infrastructure and externals, and the range reflects the ability of the

volume housebuilders to achieve significant economies of scale in the purchase of materials

and the use of labour. Many smaller developers are unable to attain these economies, so

their construction costs be higher; however, this can be compensated for by lower

overheads, and this often enables smaller developers to acquire sites in competition. We

have opted on the side of caution in our assumptions, with the addition of a 5% contingency.

4.6.3 Build costs for conversions are often as high as new build, particularly since they are in the

main carried out in small schemes by individual developers without economies of scale. In

addition, build costs for flats are generally higher than for traditional 2/3 storey

developments, due to higher costs associated with circulation space, multi-storey

CIL Economic Stratford-on-Avon CIL

30

construction, and extra facilities such as lifts. RPs also tend to specify higher build costs than

the volume housebuilders. This is because they frequently employ a contractor for the

construction of affordable dwellings, as opposed to developers who either employ

construction workers, or engage in direct sub-contracting. In this way, the volume builders

build at cost, whereas the Housing Associations will be paying a profit element on top of

build costs to the contractor.

4.6.4 Typically, a Housing Association might have build costs of about £1,000/sq.m. In order to

compensate for these higher build costs, an RP will not require the profit levels sought by the

private developers, typically 20% of gross turnover, and in addition, part of the building costs

fees may be absorbed in the contractor’s build cost. The generic site appraisals have

reflected the likely build costs of each individual site, depending on its scale and

characteristics. Much of the affordable housing delivered through S.106 agreements is

actually built by the volume developers at their lower rates, and a build profit on affordable

housing provision has been factored into the appraisals.

4.7 The Code for Sustainable Homes

4.7.1 The government has previously committed to ensuring that all new-build homes are zero

carbon from 2016. In the Budget ‘Plan for Growth’ of March 2011 the government has

updated the guidance on costs of implementing the code for sustainable homes in order to

ensure that it remains viable to build new homes in the context of the recession.

4.7.2 From 2016, the revised definition of Zero Carbon now only meets Code for Sustainable

Homes (CSH) Level 5, requiring that 100% of emissions from heating, lighting, and heating

hot water need to be reduced or generated on site. The consequence for construction costs

has yet to be fully assessed, but the new standards result in higher build costs, that could

affect viability. The possible increased costs for implementing the Code have been

estimated in a report by CLG “Code for Sustainable Homes, a Cost Review”, March 2010,

updated in August 2011.

4.7.3 The additional cost estimates for all the Code Levels vary depending on site type, location,

and size. The updated report suggests that Level 3 can be achieved for an average

additional cost of £1,000 per home, and the scenarios modelled for Level 5 show average

cost increases of £19,740. Strategic greenfield sites have higher costs at £1,400/unit for

level 3, and £20,000 for level 5.

4.7.4 It is important to reflect the circumstances applying both today for sites coming up for

development, and for sites that be developed post-2016, to reflect Code 5 requirements. We

have therefore allowed additional costs for the extra CSH costs - Code 3 at an average of

£1,000/unit (£1,400/unit for strategic greenfield sites), which are built into the base cost of

£950/sq.m, with an additional £20,000/unit for Code 5, where construction is anticipated to

be post 2016.

4.7.5 It should also be noted that whilst we have tested at a Level 5 equivalent and that there have

been indications in the past that the building regs would be changed to reflect this position, a

firm commitment has yet to be made regarding changing the building regs to reflect Level 5

CIL Economic Stratford-on-Avon CIL

31

by 2016. Therefore this is a cautionary approach and when revised building regs are

confirmed the council will need to consider the impact.

4.8 Developer’s Profit and Professional Fees and Financing

4.8.1 All developers have a slightly different approach to levels of profit and overhead. Profits are

derived from turnover across a number of sites, some of which may have been held long-

term in land banks, and others acquired as a result of option agreements where price is

established at a discount to Open Market Value (OMV). The most appropriate profit level is

that which most developers currently assume when appraising sites for purchase for

immediate development. This is an accurate reflection of the operation of the market for

land and new homes for a study that is reflecting conditions in 2011.

4.8.2 Our discussions with developers and agents reveal an acceptable profit margin of between