common colds in the mortgage servicing environment

TRANSCRIPT

Common Colds in the Mortgage Servicing Environment . . .. . . and how to cure them

May 2017

Gene Collett, CRCM

Managing Director, Southwest Region

Loan Servicing Overview

2

STATEMENTS, PAYMENTS

AND TERMS1

ESCROW AND INSURANCE2

CUSTOMER-INITIATED

CORRESPONDENCE3

DELINQUENCY4

LOSS MITIGATION5

FORECLOSURE, BANKRUPTCY

AND EVICTION6

SERVICING TRANSFERS7

OTHER8

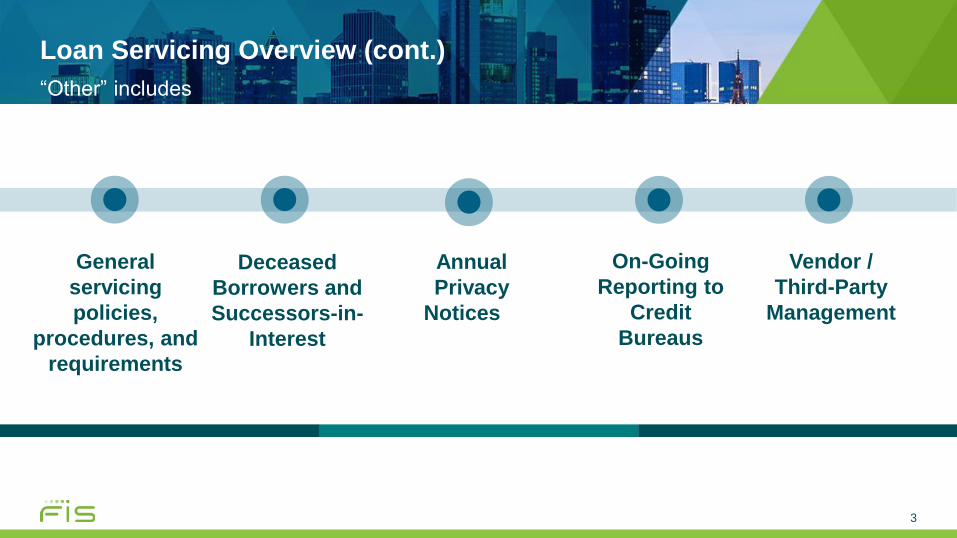

Loan Servicing Overview (cont.)

3

“Other” includes

On-Going

Reporting to

Credit

Bureaus

Deceased

Borrowers and

Successors-in-

Interest

Annual

Privacy

Notices

General

servicing

policies,

procedures, and

requirements

Vendor /

Third-Party

Management

Loan Servicing Overview (cont.)

4

• General servicing policies, procedures, and requirements 12 CFR § 1024.38

• Deceased Borrowers and Successors-in-Interest

– CFPB 2016 Amendments

– CFPB Interpretive Rule 2014-16, Application of Regulation Z’s Ability-to-Repay Rule to Certain Situations Involving Successors-in-Interest

– CFPB Bulletin 2013-12, Implementation Guidance for Certain Mortgage Servicing Rules

– 12 CFR § 1024.38

• Annual Privacy Notices 12 CFR § 1016.5

● On-Going Reporting to Credit Bureaus Fair Credit Reporting Act (FCRA)

• Vendor / Third-Party Management

– CFPB Compliance Bulletin and Policy Guidance 2016-02, Service Providers

– Federal Reserve Supervision and Regulation Letter 2013-21, Guidance on Managing Outsourcing Risk

– OCC Bulletin 2013-29, Third-Party Relationships: Risk Management Guidance

– CFPB Bulletin 2012-03, Service Providers

– FDIC Financial Institution Letter 2008-44, Guidance for Managing Third-Party Risk

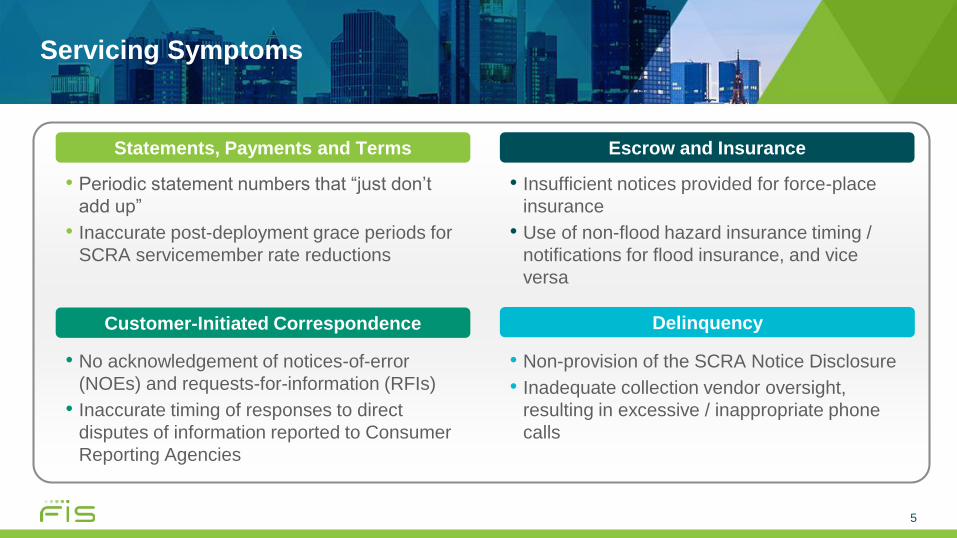

Servicing Symptoms

5

• Periodic statement numbers that “just don’t

add up”

• Inaccurate post-deployment grace periods for

SCRA servicemember rate reductions

• No acknowledgement of notices-of-error

(NOEs) and requests-for-information (RFIs)

• Inaccurate timing of responses to direct

disputes of information reported to Consumer

Reporting Agencies

• Insufficient notices provided for force-place

insurance

• Use of non-flood hazard insurance timing /

notifications for flood insurance, and vice

versa

• Non-provision of the SCRA Notice Disclosure

• Inadequate collection vendor oversight,

resulting in excessive / inappropriate phone

calls

Escrow and InsuranceStatements, Payments and Terms

Customer-Initiated Correspondence Delinquency

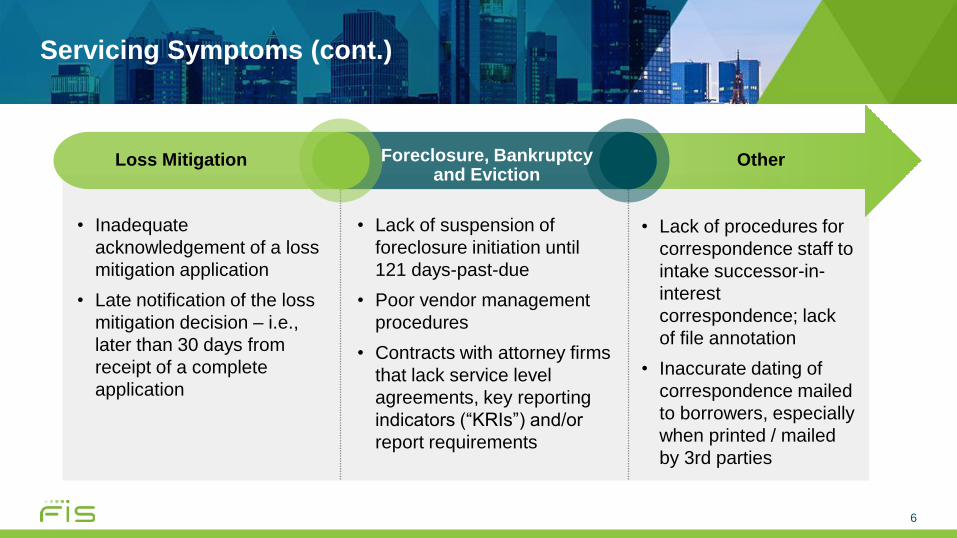

Servicing Symptoms (cont.)

6

• Lack of suspension of

foreclosure initiation until

121 days-past-due

• Poor vendor management

procedures

• Contracts with attorney firms

that lack service level

agreements, key reporting

indicators (“KRIs”) and/or

report requirements

• Lack of procedures for

correspondence staff to

intake successor-in-

interest

correspondence; lack

of file annotation

• Inaccurate dating of

correspondence mailed

to borrowers, especially

when printed / mailed

by 3rd parties

• Inadequate

acknowledgement of a loss

mitigation application

• Late notification of the loss

mitigation decision – i.e.,

later than 30 days from

receipt of a complete

application

Foreclosure, Bankruptcy and Eviction

OtherLoss Mitigation

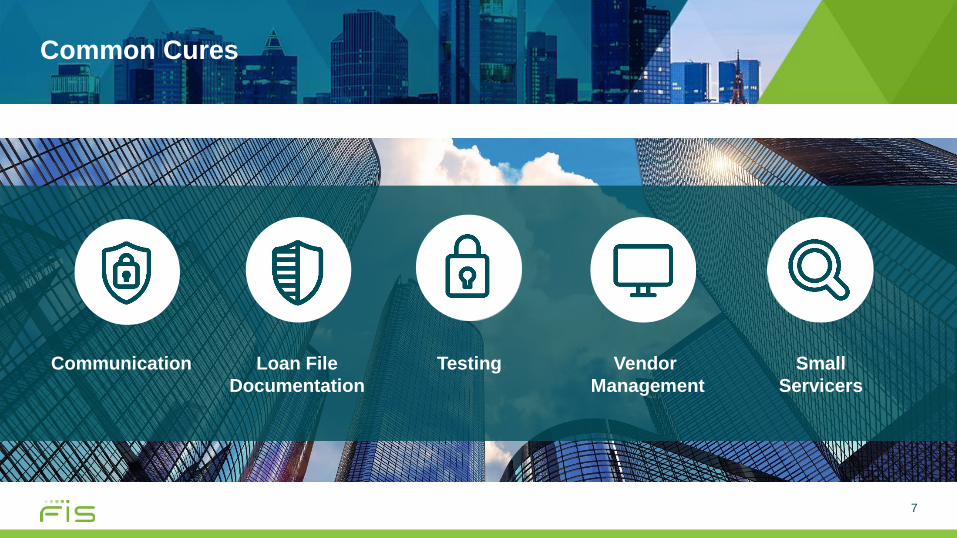

Common Cures

7

Small

Servicers

Loan File

Documentation

Testing Vendor

Management

Communication

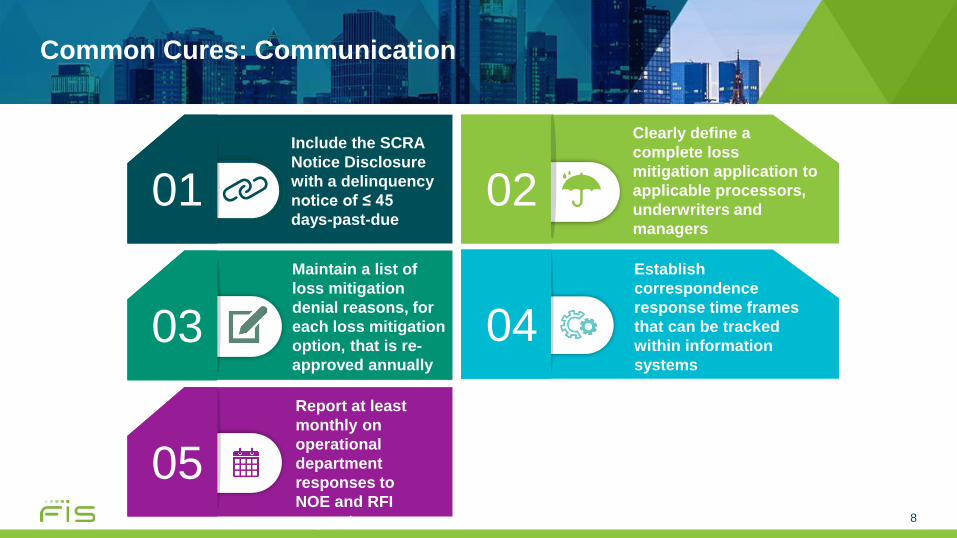

Common Cures: Communication

8

Include the SCRA

Notice Disclosure

with a delinquency

notice of ≤ 45

days-past-due

01

03

02

04

Clearly define a

complete loss

mitigation application to

applicable processors,

underwriters and

managers

Maintain a list of

loss mitigation

denial reasons, for

each loss mitigation

option, that is re-

approved annually

Establish

correspondence

response time frames

that can be tracked

within information

systems

05

Report at least

monthly on

operational

department

responses to

NOE and RFI

requests

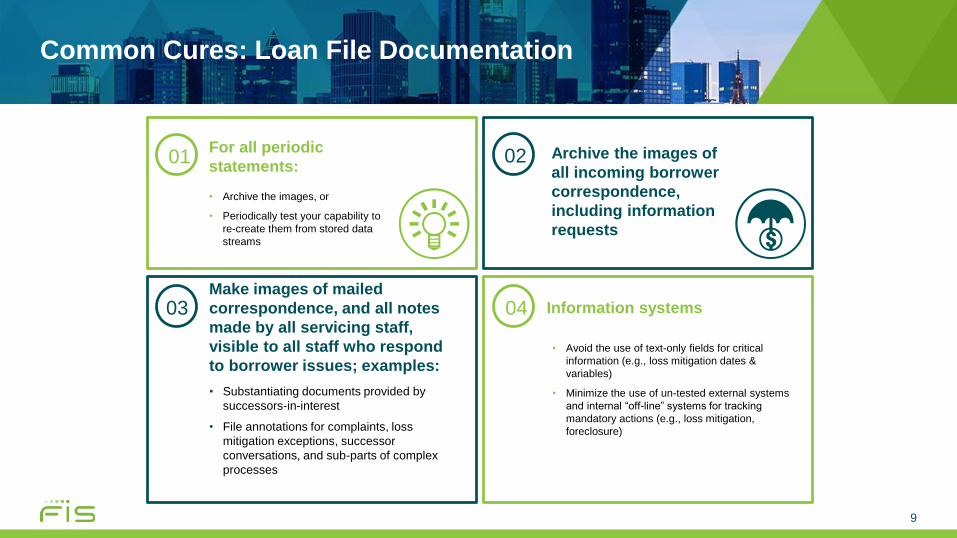

Common Cures: Loan File Documentation

9

01For all periodic

statements:

• Archive the images, or

• Periodically test your capability to

re-create them from stored data

streams

03Make images of mailed

correspondence, and all notes

made by all servicing staff,

visible to all staff who respond

to borrower issues; examples:

• Substantiating documents provided by

successors-in-interest

• File annotations for complaints, loss

mitigation exceptions, successor

conversations, and sub-parts of complex

processes

02 Archive the images of

all incoming borrower

correspondence,

including information

requests

04

• Avoid the use of text-only fields for critical

information (e.g., loss mitigation dates &

variables)

• Minimize the use of un-tested external systems

and internal “off-line” systems for tracking

mandatory actions (e.g., loss mitigation,

foreclosure)

Information systems

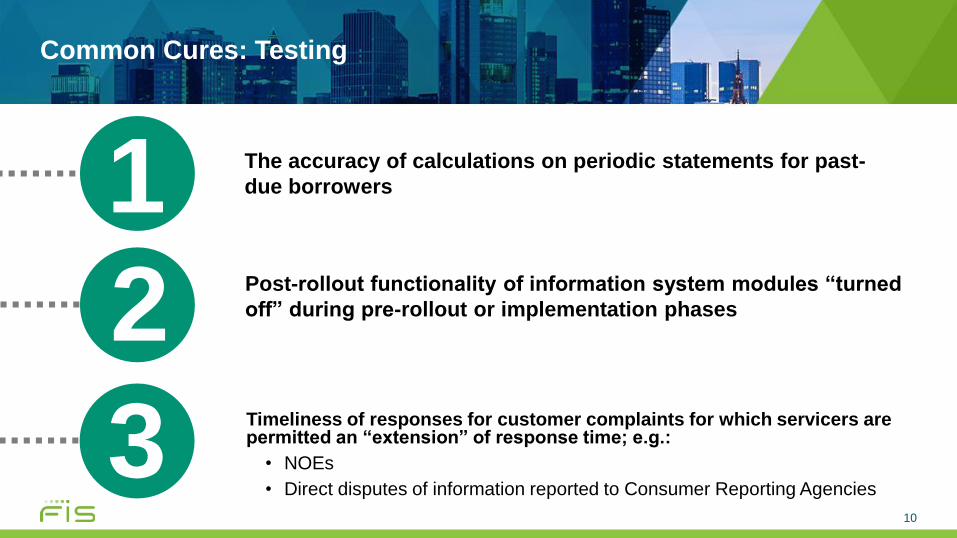

Common Cures: Testing

10

1 The accuracy of calculations on periodic statements for past-

due borrowers

Post-rollout functionality of information system modules “turned

off” during pre-rollout or implementation phases2

3Timeliness of responses for customer complaints for which servicers are permitted an “extension” of response time; e.g.:

• NOEs

• Direct disputes of information reported to Consumer Reporting Agencies

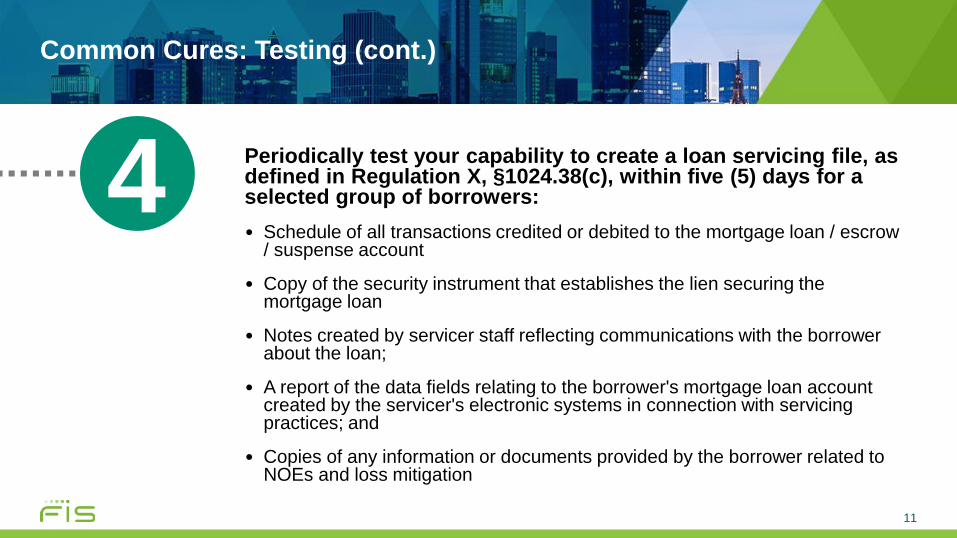

Common Cures: Testing (cont.)

11

4 Periodically test your capability to create a loan servicing file, as defined in Regulation X, §1024.38(c), within five (5) days for a selected group of borrowers:

• Schedule of all transactions credited or debited to the mortgage loan / escrow / suspense account

• Copy of the security instrument that establishes the lien securing the mortgage loan

• Notes created by servicer staff reflecting communications with the borrower about the loan;

• A report of the data fields relating to the borrower's mortgage loan account created by the servicer's electronic systems in connection with servicing practices; and

• Copies of any information or documents provided by the borrower related to NOEs and loss mitigation

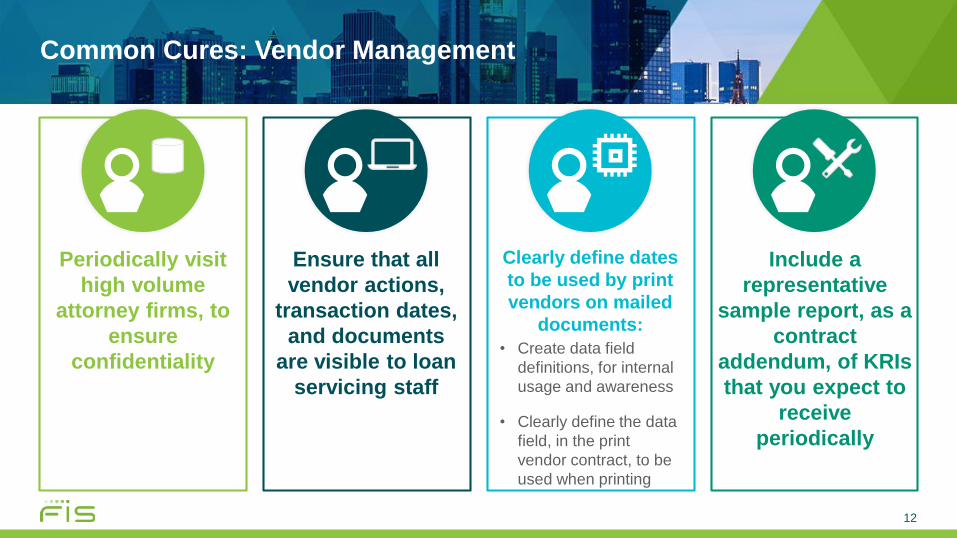

Common Cures: Vendor Management

12

Periodically visit

high volume

attorney firms, to

ensure

confidentiality

Ensure that all

vendor actions,

transaction dates,

and documents

are visible to loan

servicing staff

Clearly define dates

to be used by print

vendors on mailed

documents:

• Create data field

definitions, for internal

usage and awareness

• Clearly define the data

field, in the print

vendor contract, to be

used when printing

Include a

representative

sample report, as a

contract

addendum, of KRIs

that you expect to

receive

periodically

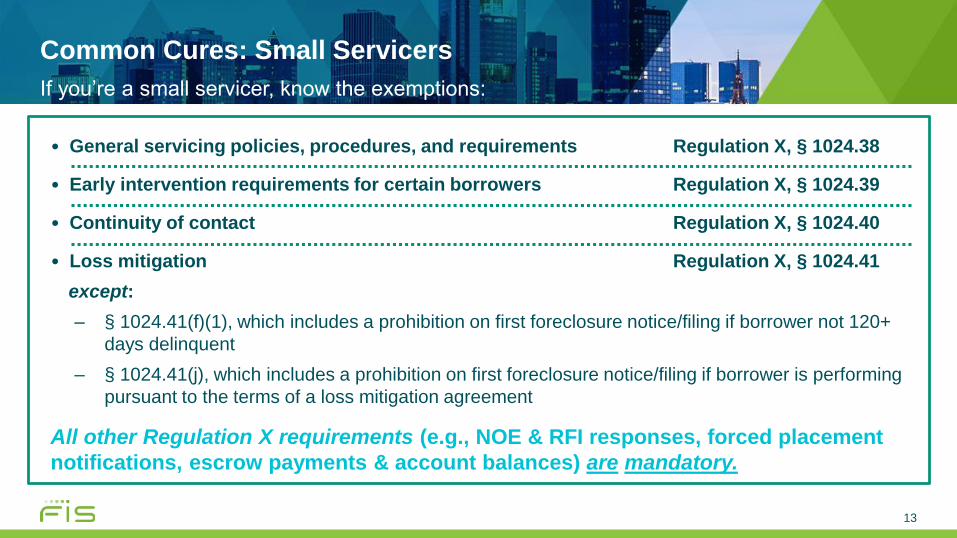

Common Cures: Small Servicers

13

If you’re a small servicer, know the exemptions:

• General servicing policies, procedures, and requirements Regulation X, § 1024.38

• Early intervention requirements for certain borrowers Regulation X, § 1024.39

• Continuity of contact Regulation X, § 1024.40

• Loss mitigation Regulation X, § 1024.41

except:

– § 1024.41(f)(1), which includes a prohibition on first foreclosure notice/filing if borrower not 120+

days delinquent

– § 1024.41(j), which includes a prohibition on first foreclosure notice/filing if borrower is performing

pursuant to the terms of a loss mitigation agreement

All other Regulation X requirements (e.g., NOE & RFI responses, forced placement

notifications, escrow payments & account balances) are mandatory.

14

Appendix A

Detailed Loan Servicing Overview,

with Citations

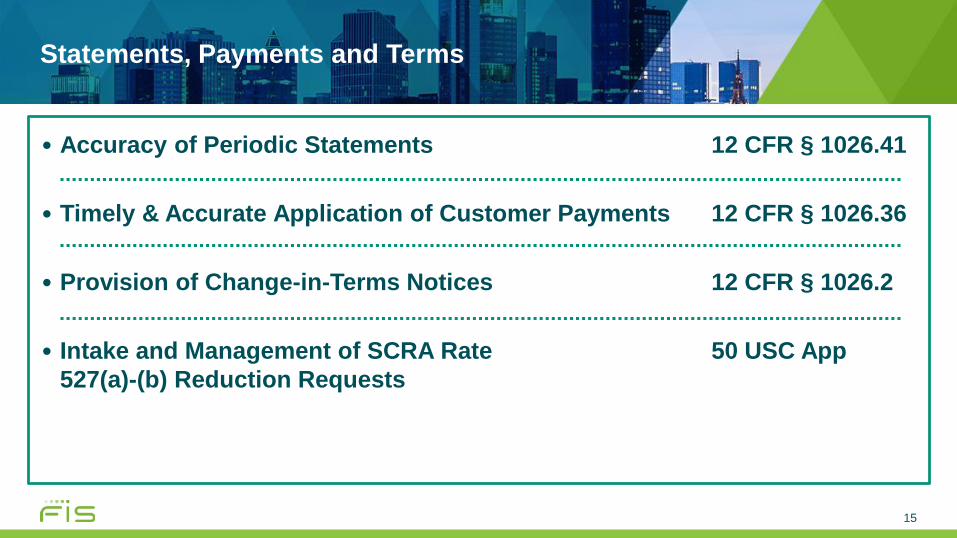

Statements, Payments and Terms

15

• Accuracy of Periodic Statements 12 CFR § 1026.41

• Timely & Accurate Application of Customer Payments 12 CFR § 1026.36

• Provision of Change-in-Terms Notices 12 CFR § 1026.2

• Intake and Management of SCRA Rate 50 USC App

527(a)-(b) Reduction Requests

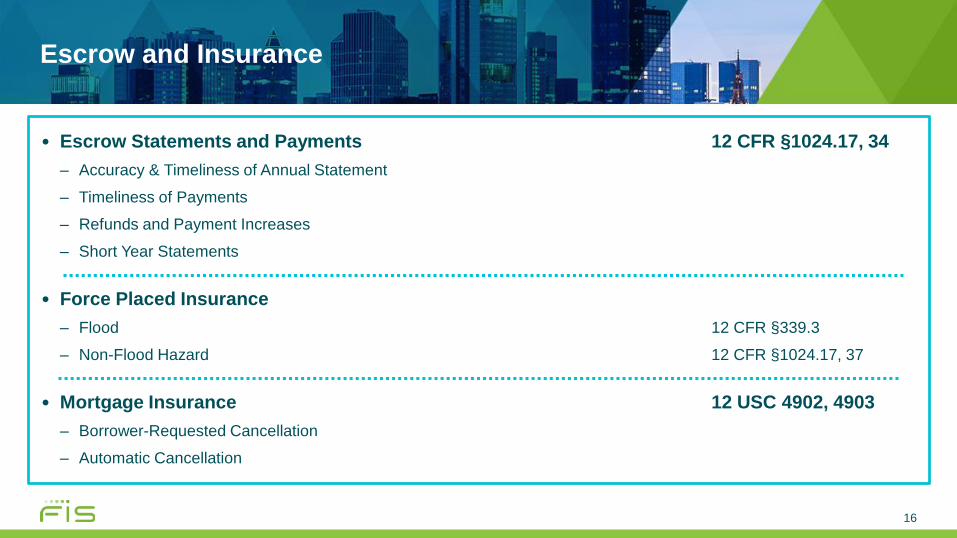

Escrow and Insurance

16

• Escrow Statements and Payments 12 CFR §1024.17, 34

– Accuracy & Timeliness of Annual Statement

– Timeliness of Payments

– Refunds and Payment Increases

– Short Year Statements

• Force Placed Insurance

– Flood 12 CFR §339.3

– Non-Flood Hazard 12 CFR §1024.17, 37

• Mortgage Insurance 12 USC 4902, 4903

– Borrower-Requested Cancellation

– Automatic Cancellation

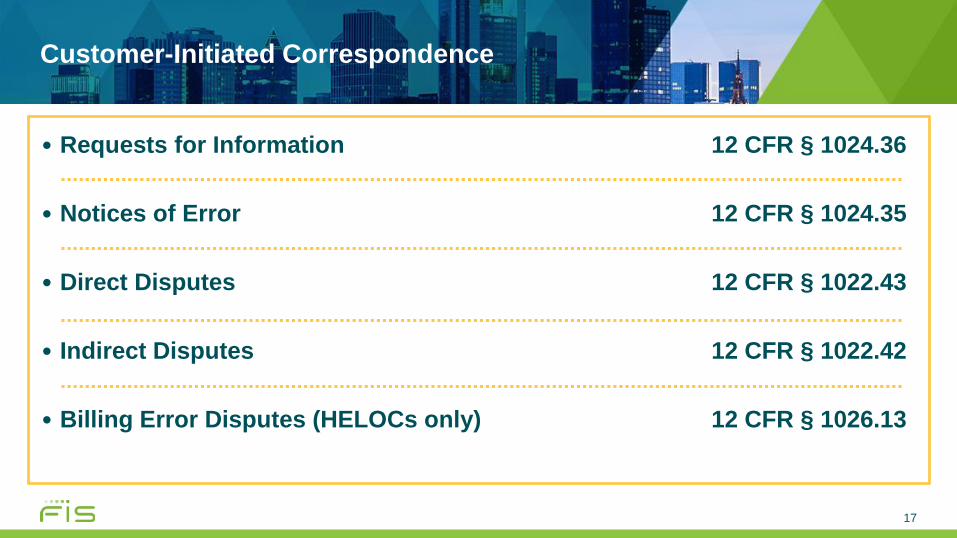

Customer-Initiated Correspondence

17

• Requests for Information 12 CFR § 1024.36

• Notices of Error 12 CFR § 1024.35

• Direct Disputes 12 CFR § 1022.43

• Indirect Disputes 12 CFR § 1022.42

• Billing Error Disputes (HELOCs only) 12 CFR § 1026.13

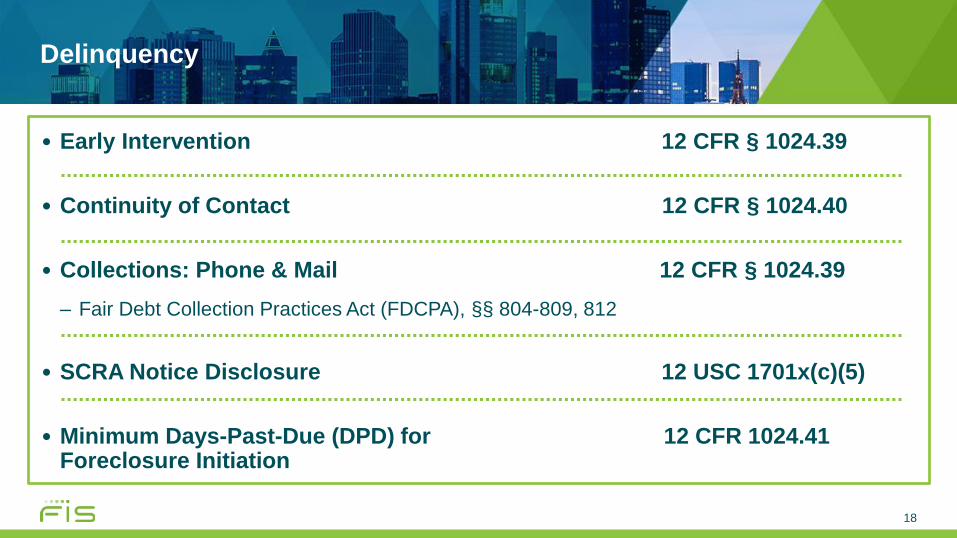

Delinquency

18

• Early Intervention 12 CFR § 1024.39

• Continuity of Contact 12 CFR § 1024.40

• Collections: Phone & Mail 12 CFR § 1024.39

– Fair Debt Collection Practices Act (FDCPA), §§ 804-809, 812

• SCRA Notice Disclosure 12 USC 1701x(c)(5)

• Minimum Days-Past-Due (DPD) for 12 CFR 1024.41Foreclosure Initiation

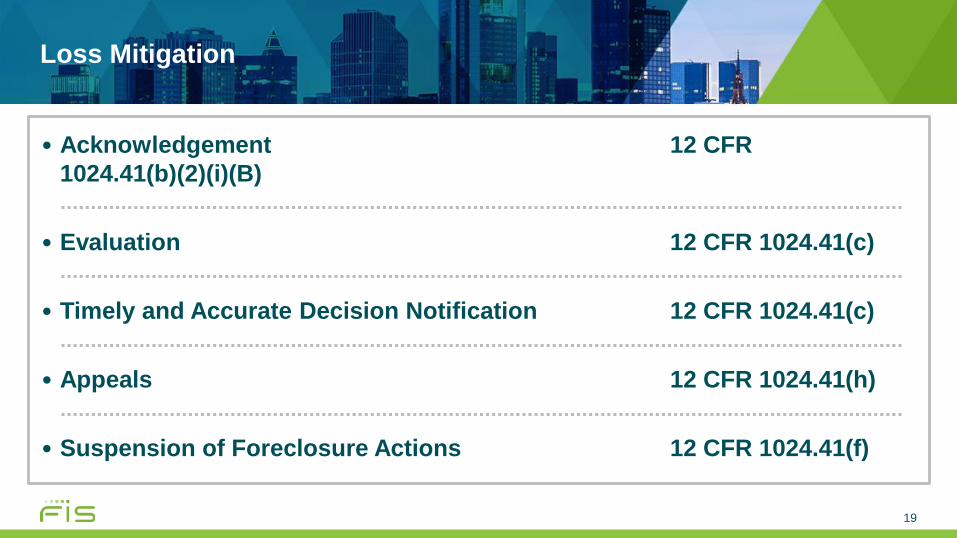

Loss Mitigation

19

• Acknowledgement 12 CFR

1024.41(b)(2)(i)(B)

• Evaluation 12 CFR 1024.41(c)

• Timely and Accurate Decision Notification 12 CFR 1024.41(c)

• Appeals 12 CFR 1024.41(h)

• Suspension of Foreclosure Actions 12 CFR 1024.41(f)

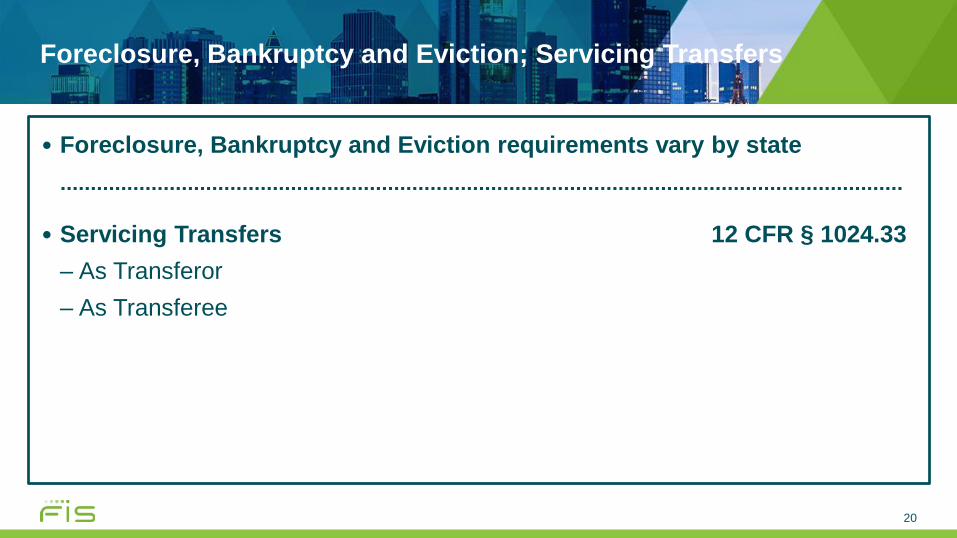

Foreclosure, Bankruptcy and Eviction; Servicing Transfers

20

• Foreclosure, Bankruptcy and Eviction requirements vary by state

• Servicing Transfers 12 CFR § 1024.33

– As Transferor

– As Transferee

Other Requirements

21

• General servicing policies, procedures, and requirements 12 CFR § 1024.38

• Deceased Borrowers and Successors-in-Interest

– CFPB 2016 Amendments

– CFPB Interpretive Rule 2014-16, Application of Regulation Z’s Ability-to-Repay Rule to Certain Situations Involving Successors-in-Interest

– CFPB Bulletin 2013-12, Implementation Guidance for Certain Mortgage Servicing Rules

– 12 CFR § 1024.38

• Annual Privacy Notices 12 CFR § 1016.5

● On-Going Reporting to Credit Bureaus Fair Credit Reporting Act (FCRA)

• Vendor / Third-Party Management

– CFPB Compliance Bulletin and Policy Guidance 2016-02, Service Providers

– Federal Reserve Supervision and Regulation Letter 2013-21, Guidance on Managing Outsourcing Risk

– OCC Bulletin 2013-29, Third-Party Relationships: Risk Management Guidance

– CFPB Bulletin 2012-03, Service Providers

– FDIC Financial Institution Letter 2008-44, Guidance for Managing Third-Party Risk

Thank You

Gene Collett, CRCM

Managing Director, Southwest Region