committee agenda topics - charlotte, north carolinacharlottenc.gov/citycouncil/focus-areas... ·...

TRANSCRIPT

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 1

COMMITTEE AGENDA TOPICS

I. Subject: Eastland Redevelopment Update Action: On October 1, 2013, the City entered into a Memorandum of Understanding (MOU) with Studio Charlotte Development, LLC (SCD) for a period of six months to develop a possible development framework for the site of the former Eastland Mall. The MOU will expire on March 31, 2014. At today’s meeting, staff will provide a recommendation for the Committee on potential next steps for the site. If ready, the Committee may make a recommendation to the full Council for consideration at a future business meeting.

II. Subject: Charlotte Community Capital Fund Modifications Action: The Charlotte Community Capital Fund was established by the City and several community partners in 2003 to help small businesses in the Charlotte region gain access to capital that is otherwise unavailable through conventional lending. The majority of the funds that were provided to the Fund to be used as loan guarantees mature on March 31, 2014, subject to renewal by the partners. On January 28, 2014, the Fund’s Operating Committee approved modifications to the Fund intended to increase its utilization, and has requested the City to renew as a Fund sponsor for an additional ten-year term. Tom Davis, Chairman of the Fund’s Operating Committee will share the recommended changes with the Committee. No action required.

III. Next Meeting Date: Thursday, April 3, 2014 at 2:00 p.m. Room CH-14

COMMITTEE INFORMATION Present: Michael Barnes, Vi Lyles, Al Austin, Claire Fallon and LaWana Mayfield Others: Ed Driggs, Kenny Smith and Greg Phipps Time: 12:00 Noon – 1:28 p.m.

ATTACHMENTS

1. Eastland Redevelopment Update Presentation 2. Charlotte Community Capital Fund Presentation 3. Charlotte Community Capital Fund Operating Committee Meeting – January 28th

Minutes 4. The Support Center Proposal for Fund Administrator of the Charlotte Community

Capital Fund

DISCUSSION HIGHLIGHTS Chairman Barnes called the meeting to order and asked everyone to introduce themselves. This is probably the only Committee that essentially is the City Council. Last time we had the Mayor and this time we’ve got most of the Council with us which is great. The first item on our agenda today is the

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 2 Eastland redevelopment update and the second item is the Charlotte Community Capital Fund modification proposal. Mr. Richardson, I will turn it over to you regarding the first item. Richardson: The last time we met, just two weeks ago, what we promised to bring back to you was if you recall the developer, Studio Charlotte, has requested a five month extension of the exclusive negotiating period on the 80-acre site. We previewed to you last time our recommendation was not to extend but not to preclude the opportunities to work with Studio Charlotte in the future. What we promised to bring back to you today was what might be an approach or recommended next steps for you to consider and if we can get there today we’d likely see this action in a Council meeting in the next couple days. That is what I would like to do today so some key observations that are familiar to you; and we’ve talked about it certain times over the last six months. The 80-acre site we have determined at this time is too difficult, too complex for one entity to develop as we would like. We also point out that the site in whatever state it ends up in the future, a great redevelopment, we purpose to do that, will require some infrastructure; it will require storm water control and we’ll talk a little bit about that today. It will also require street network. Those are the things that we want to begin thinking about. Our approach is this; these are the things the City can do, we have expertise on staff to do, so we propose this approach; develop that storm water analysis and design of that water future that the 80-acre site would need; creating that in a regional manner, not regional in the sense of multi-county but regional with regards to the parcels that will develop on the site; putting in the storm water controls now would make an enhanced future as well as an easier to develop an 80-acre site for future development. We propose to begin to work on that. Develop those preliminary “master street/block” plans that anticipates and begin to think where the logical development pads and framework for the site. The last thing I think is just as important, begin to identify and explore different partnerships, public sector, private sector for a phase redevelopment. That I think is intuitive and that is what we plan to do. I will point out to you that the site as shown, the bottom lower right, that is where I mentioned the storm water control facility. This is where the site drains; this is a map provided by our Stormwater folks and this is probably where the storm water retention facility would be and we think it could be developed around the site handle all the storm water controls for the balance of the site. Obviously, there is development happening here; the zoning is in place now for a convenience store, gas station in this general area. We are working through that rezoning to try to preserve and approve the Right-of-Way off of Sharon Amity and begin that full street network right through here into the property. This development is going to naturally need to be coordinated with this development as well; they’ve got to be linked in some way. Back of the site, and I will talk about this in a few moments, but one of our recommendations is to preserve the back of the site for future exploration and some related development. As I said before, we are not precluding from working with Studio Charlotte in the future; we just think perhaps the appropriate acreage in the back for a film studio is where we would like to be today. The area in front, Central Avenue that is going to be the area we would want to develop and ask the master developer what should go there; what market will be driving us into those places. If you are ready this is what our action would be for you; decline the developer’s request to extend the MOU period and direct us into those things I just talked about, design and placement of storm water infrastructure that creates that site amenity and satisfied new development ordinance for the site. Design this “master street/block framework” and begin work to identify the selection of

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 3 appropriate partners, both private and public. I will point out here, as I said before, we want to reserve the appropriate amount of acreage at the rear of the site that is appropriate for a film studio element if we decide that is the way we want to go. Barnes: Let’s talk about that for just a second. You recall at the last meeting, I asked you to talk to us about what we had requested from Studio Charlotte and what we had received over the course of the last six months. The exclusivity period ran for six months. Richardson: At the end of this month will be six months. Barnes: Right, and so you indicated what you had received as of November 2013, you indicated what you had received as of March 6th of this year. I would like for you, if you could Mr. Richardson, talk about what have received from Studio Charlotte since November 2013 also talk about what you have not received just so we are aware of where things are. Richardson: As a reminder certainly, as we look at public/private partnerships that request City funding certainly we have a general framework that applies to every single one of those and it is three components. What’s the cost of the project, not just a high level estimate, which is what we’ve received, but what is the detailed analysis of where the line items construction costs so I can see and test verify and feel comfortable with as we present to you. The second thing we look for is what is the sources of financing, private financing that can be applied toward that total project costs. We’ve received some information from the developer about that. We talked last time about partners, sponsorships crossing the table, but there has been some movement, but not enough to give assurance of what level of private financing can be applied. And it is simple math; you take the costs you apply the private financing to it and is there a gap that the public is asked to fill and then we further analyze that gap to say well what we can provide statutorily, given our limits of public financing. Those are the things we require and we received high level construction costs, certainly we’ve received some information on how Studio Charlotte would finance; it was from debt and equity but it is just not to the level that we feel comfortable with tying up the 80-acre site, as large as it, for an exclusive negotiation period any further than we’ve done. That is what we are not recommending today. Barnes: So you talked about what you have received, could you talk about the quality of what you have received? Richardson: Mr. Hesse has aligned himself with SAIC, a very reputable design construction firm and they have given us the high level numbers. What we are missing is the detailed analysis, what are the things that are in that line item budget that we can test. The contractor is here with us and these are ballpark numbers, high level numbers and we need more than that. Barnes: Would it be fair to say that there is no proof of concept at this point? Richardson: I’m not sure what those terms mean. I want to be careful with my words because they’ve given us some information, but it is just not to the level that we normally require for public participation.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 4 Barnes: Fair enough. Since November 2013 what have you received? Richardson: We received that information, high level costs on various phases or districts of the plan and then as we drill down into the financing and the gap it was the analysis done on Phase 1 which was the rear acreage film studio. We think that is where they made the most progress so it is intuitive for us to begin to think about working to see if the smaller site plan can work for a future film development. That is my recommendation today. Barnes: Have you received any update since March 6th? Richardson: We talked a couple of times but no additional information on those things I outlined earlier. If you are ready, that is the action and then we would propose to take that forward to the next Council Business Meeting, but as reminded that is the action. Barnes: Any questions from the Committee? Is there a motion from the Committee? Mayfield: With this recommendation Brad, where does that leave the current conversation that we are having with Studio Charlotte just for disclosure and clarification? Richardson: What we are proposing to do today is to recommend that we not extend an exclusive negotiating period with the current development team for the entire 80-acre site, nor do we think it is probably appropriate to do an exclusive negotiation of any kind right now. However, I think we’ve said before we have communicated to the development team that we would be interested in further conversations about a future film related studio site that naturally would sit on the back of the property anyway, the lowest part. We are willing and interested in continuing those conversations. Mayfield: So are we saying we are opening this process back up? Richardson: If by process you mean RFP, proposals, no mame. Our process would as I’ve outlined before, begin the infrastructure planning and design, which we can do in house. We don’t anticipate spending money at this point. We’ve still got the building being demolished; the contractor has about 45 more days on site so not opening up a process again. Mayfield: It is really the third part of the seventh bullet, the selection of appropriate partners, both public and private that I’m trying to get a clearer understanding of. What does that mean if we are not going to open up an RFP process? Richardson: One of the things that we would like to explore and have your authorization to do is determine is there a master development entity, not a person but a firm, that is well experienced in distressed areas of communities, as we designated Eastland to be, and beginning to put together a market-driven integrated approach for the development and that is what we would be doing. Fallon: Let me understand something. Have you gotten update on financial partners, letters of intent, and seed money? Richardson: No mame not since March 6th when our last update was.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 5 Fallon: So nothing has changed? Richardson: Correct. Lyles: I’m going to follow-up to Ms. Mayfield’s comments. I think I understand the first bullet that would be a situation where you would have the storm water plan done for the 80-acre site and that is infrastructure that would need to be done at some point and then the “master street/block framework”. Is that consistent with the former planning study for the area? Tell me what the design of a master street block framework does and how it happens. Is it consistent with where we are? Mumford: Let me reference the plan from 2007 or 2008. The world has changed dramatically; we are not trying to resurrect that plan because I don’t think that would work. The idea and Brad mentioned this, to have a master developer doesn’t mean somebody that is actually a physically developer, this is somebody that thinks essentially the breakup of 80 acres into manageable parcels and understanding the market demand that is out there and the feasibility to develop differently around a water feature that is there for retention purposes. As Brad mentioned, there is a parcel along Central Avenue that has that exposure to market. We have a piece that we call on the back side of the property that has different dynamics, so what we would entertain is engaging somebody with market and development experience to help guide this effort. We are not talking about a long-wended develop a master plan and put more plans on the table; we are really talking about a quick assessment of the market and what can be feasibly done and then look at that infrastructure on the site to determine what sort of road network might need to be there to access those parcels. Lyles: That is very helpful because I don’t know that is what I thought when I read those words. When I read selection of appropriate partners, I was thinking again of a process that we would have to go through that the Council – so let me see if I can say this back to you Mr. Mumford; that the staff would actually work to improve the site for the storm drainage that has to occur so that would be coming back to the Council as a cost or somehow we will see that. Then the next two steps are actually to engage expertise to determine the market for the area for development that could then be sued for the next step? Mumford: Correct. Lyles: It is a geographic kind of like instead of 80-acres you look at it and say it is 80 should it be ten of 80 or whatever, but you would be looking to gain that expertise in the real estate development community? Mumford: Correct; test that to make sure that it makes sense, that it is financeable, developable. Lyles: So when you think through that I think I had a better sense of what that meant versus that third bullet. Then on the last thing about the reserve and appropriate amount of acreage at the rear, I’m wondering if the test is really for the film studio to be tested against the information that you are gaining versus automatically doing a reserve. Does that make sense? Mumford: It does but what we want to do is recognize the film industry in this community is growing and it is important and I think everybody agrees with that. We all also agree that there is some action

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 6 to be taken in Raleigh to give some direction on the film credits. That is important to understand so we want to be appropriately acknowledging that the reality of the film industry in this community. We don’t feel that that parcel we call the back is the highest and best use for retail because you can’t see it, but you don’t need that kind of visibility for a film studio. We are appreciating that we feel that potentially there is something there with film studio; we want to break this down to a smaller component on that site and get extremely focused on the feasibility analysis on how the film studio would work, what are the directly related ancillary and development opportunities; how does that fit into the site plan. It is not the full 80-acres but there are certainly arguably some things that can be developed that do work because a film studio might be there. It is a lot of questions still out there but we are not suggesting that has to be a film studio back there; we are suggesting that we do think there is enough to continue to analyze that to make a determination. Lyles: I feel much more comfortable with the concept of if we are going to have a plan that is going to look at this as a master development, saying to a developer that we really want to support the film industry in Charlotte and this is an opportunity versus reserve an appropriate amount of acreage. Does that make sense? Mumford: Certainly, that is fair. Lyles: I would be more supportive of that and if this is a motion of bullets, I would be more supportive of that bullet not saying reserve an appropriate amount but maybe a slash that says in recognition of the opportunities with the film industry in Charlotte for the development plan to consider that in the market based assessment. Barnes: I understand and here is what I’m hearing from Vice Chair and from our staff. This is for the community too. What we are saying is that we would like to analyze the site fully to determine whether there are infrastructure needs, road infrastructure and other infrastructure needs at the 80-acre site that might be put into place in the near future to help redevelop the entire site in sections perhaps and that we are looking to receive private sector and public sector feedback on how that might occur across the entire site and that we are also aware of the importance of the film industry in the City in light of the various projects that are going on now and have gone one to the potential need for or a potential opportunity for a studio with any particular partner, not necessarily Studio Charlotte and that in recognition of that there will be an awareness of that site of the potential use of part of the site for a film studio purpose of film purpose. Is that consistent? Kimble: I think that is what I heard you all say. Barnes: We all heard the same thing, okay. Lyles: And is that consistent with the staff recommendation? Barnes: Is that consistent with the recommendation? Richardson: Yes. Barnes: And was that a motion you made?

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 7 Lyles: That was a motion. Barnes: Is there a second? A second from Ms. Fallon. Austin: Just a point of clarification, is that a continuation or a modification of that? Will Studio Charlotte still have an opportunity to engage with us around the possibility as well as opening up other studios as well? Richardson: Yes. Barnes: Any discussion on the motion? Lyles: One more thing. In terms of as we saw this kind of work before, I think about the site that is on Stonewall I think coming up around the Kenilworth area and we’ve had instances where we’ve done things to make properties more marketable and this is consistent with our past practices. I just want to make sure that we let the community know that we are being consistent with our practices in economic development and master development for major acreages and we are doing this within the context of the best use of that property in the new environment that we are living in today versus 2007. Fallon: And a benefit to Charlotte. Barnes: And by things to make it more marketable you mean the $14 million we spent buying the property and raising the mall? Lyles: Right. Austin: And that we are still very committed to the east side and this particular site as well. Mayfield: So here is the question for clarification for me. What we are recommending now, what I’m trying to understand is if that we’ve been having this conversation for six months. Why didn’t we do this originally? Just for clarification so that everybody understands how we get to understanding that this will be best step, the next step for us opposed to when we had already through the community identified the money to raise the area, everything that we’ve already invested into it and then when we put the RFP out to get a full for whatever proposal they brought to the table knowing that okay, it is as is. So this is your used car, you are buying as is; these are the things you are going to need to do. What we’re saying today is okay, maybe we need to go back and look at the car, go under the hood a little bit more because there might be some other things that are happening. I’m just trying to get a clearer understanding of how we got here and to make sure that everyone, not only in this room, but the community understands that if we are looking at our best practices how did we get to this conversation today? Mumford: Originally the idea was is there a way that we could dispose of the full acreage, the full 82 acres in one entity and develop it all. What we’ve learned over the course of the last several months is that is probably too big an endeavor for entity to undertake. So what we are suggesting is instead

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 8 of 82 acres take smaller more manageable parcels of land, understand those uses and test that against the market, make sure that all the parcels are related and can have the development occur, but break this down into smaller pieces. That is why it is different than before. Before it was the whole acreage going forward it will be smaller pieces. Does that make sense? Mayfield: It does but for me it just looks like we are getting ready to start this process over. What we are doing is starting – we are this far into the conversation and we are going back to here, and what I want to make sure is if we had the RFP process, if we are going to look at identifying public and private partners that we are not doing a disservice on who those partners may be and having as much opportunity as possible and as much transparency in who is going to be at the table that is going to help create this market based program that is going to make a suggestion of how we move forward, which I have no concerns about our staff doing just that. Just wanted to make sure for clarification sake; I was understanding exactly what we are saying and that you are hearing what my concerns are. Barnes: Ms. Mayfield, I understand what you are saying and the reason I think you feel that way and I share the feeling is because we were led to believe that there was a substantive project there that was going to be moving forward quickly and that was not the case. Luckily, we are in a position, because of the work we did several years ago to refine that master planning work and take it to another level, but I understand what you are saying. Smith: I don’t think it is uncommon during the course of any commercial development, both the marketing and/or the due diligence period to arrive at a possibility to change directions. I don’t think it is uncomment to say you know what we had this 80-acre parcel and now we think it is five parcels. Staff’s perspective I think to have come to it from the point of reference they did to subsequently say maybe this is just too much for an individual entity to bite off. I don’t think it is uncommon at all. VOTE: Councilmember Lyles made the motion and it was seconded by Councilmember Fallon to:

A. Decline the request from Studio Charlotte Development, LLC for an extension of the Memorandum of Understanding beyond its March 31, 2014 termination date; and

B. Direct staff to explore a redevelopment strategy for the Eastland site that includes the following activities: − Consider the design and placement of storm water infrastructure that creates

a site amenity and satisfies applicable development ordinances. − Develop a preliminary master street/block plan that defines the logical

connectivity for the site. − Explore partnerships (both public and private) that lead to an integrated and

market-based program for site redevelopment. − Continue to consider film-related uses as development components

given the benefits of the emerging film industry to Charlotte. The vote was recorded as unanimous (Barnes, Lyles, Austin, Fallon and Mayfield).

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 9 Barnes: Thank you so much to the Committee and our staff for your hard work. We appreciate everything you all have been doing. We also appreciate the work of the community in trying to arrive at a good outcome for east Charlotte so thank everybody for their efforts. Kimble: This recommendation will go to the City Council meeting Monday night, March 24th. II. Charlotte Community Capital Fund Modification Richardson: This was referred just recently by Manager Carlee to the Committee. The timing of the referral came after the Operating Committee of the Charlotte Community Capital Fund made a recommendation for you to consider. Just a hair of background for you. The Charlotte Community Capital Fund was called two years ago the SBE Loan Fund. It started about ten years ago and it had an expiration date of ten years, but we needed to come back and check in with you and that is what we are doing today. We changed the name by the way about three years ago because we had some confusion in the community about only certified SBEs apply for loans. We were trying to clear up that confusion and we recommended the name change. Today you are going to hear from Eric Nelson, part of our staff in Neighborhood & Business Services. He is one of our representatives to the Operating Committee. He does a lot of small business lending. The actual request today will be made by Mr. Tom Davis, many of you know Tom. I’ve got a little bit of information on Tom, but he is a career banker at First Citizens Bank, spent a lot of time over on Freedom Drive, Chairman of the Freedom Drive Development Association years ago so he is the right person to give you a perspective globally on small business thinking in town. Dale Harrold, to my left is the current manager of the program at Self Help and has been a long time good partner for us as well. Today it is a request and we’ve got time to come back for questions. If you happen to be comfortable today we can send it on to Council for consideration, but there is no real rush today. We want you to get familiar with the program. Nelson: What we want to do basically is provide a brief overview of the fund, when it was originated, some of the successes and then I will turn it over to Tom to discuss the specifics and what the Committee recommendations are. The purpose of the fund, it was originated back in 2003 was to assist businesses with gaining access to capital who might not otherwise be able to obtain a long agreement. Vi was in fact the Chair in 2003. Lyles: If I’m going to take complete credit for all of the successes then all the failures happened on someone else’s watch. Nelson: One of the things that occurred back then was that the City went out and sought support from private as well as other foundations to help start this particular effort and it wound up in 13 community partners that included local banks as well. The oversight for the Committee is provided by the Operating Committee which the City has a couple of representatives. Loans are typically made to businesses for the purpose of buying equipment. Equipment and inventory needs are one of the biggest things we see in the small business community and often times pay their employees until they are paid by people that they are doing work for. The fund as it currently sits right now services six counties and it was originally set up for a ten-year period. At this point, we are at the expiration period and we’ve got the fund approvers. Here is a list of the original investors and

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 10 you can see there has been some consolidation obviously because of their bank and the banking industry. The fund is $1,979,480. You’ll see a list of the current members of the Operating Committee. Tom Davis is Chair and Nigel Long and “Bo” Powell and I are the other two City representatives.

Harrold: There is one addition; there is an ex officio member from PNC who is responsible for serving on the committee on behalf of PNC located in their Greensboro Office, someone who has been very helpful.

Nelson: Here to provide an overview of the funds’ performance since its inception is Tom Davis, Committee Chair … Davis: The results over the ten-year period, we made 111 loans for a total of $5,193,000 since inception in 2003. Barnes: Sir could you state your name for the record please? Davis: I’m Tom Davis and I am chair of the Operating Committee for Charlotte Community Capital Fund. It is obvious that the fund activity has declined a little bit recently but some of the obvious reasons are the economy. Also I think that the fund generates loans from referrals from bankers and in a great many situations from inquiries received directly by to Self Help and just changing in the banking industry, the business banking, small business lending sectors have changed a lot over the years and that model has changed. They are a lot more accountable for other things other than making small loans. So, we’ve been challenged by that fact, trying to get referral from sources through-out our community. We want to be able to gather data on where we are getting referral from within the programs demographics and how companies are performing. We’ve had good success with minority and female lending, numerous start-ups. Eight-two of our 100 loans have been made in Mecklenburg County so the large majority of the loans are originated here. Phipps: Do you have any kind of idea of the average term of the loans? Davis: I would say the typical term is probably five years. Harrold: I’m Dale Harrold; I’ve been the Fund Manager since 2003. A typical loan term is going to run from five to seven years. We have used it in situations where an owner of a business wanted to acquire the property in which they were located, but lacked sufficient equity so we used it to close the lateral gap in which case we agreed to release it from the fund once the balance was paid down to appropriate level of the loan value and that is what typically would occur in a normal amortization within that time period of five to seven years. Davis: We’ve had 47 loans paid off. Our loan losses, we’ve had 16 defaults over the ten-year period and that represents 14% of the total reserve. Considering the level of risk, we feel this is very good. The reserve fund status, the original fund balance was $1,979,480 and we’ve had $207,344 in loses charged to the reserve leaving us a current reserve of $1,772,136.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 11 The recommendations from the Operating Committee- representative of investors in the fund- is that we recognize there is a need to increase our marketing efforts and we have attempted to do that. The City is technically an allocation of services agreement is responsible for marketing the fund and we utilize Virginia Banks when she was here and helping us to begin developing a marketing strategy and we felt like we needed to reach out to the Support Center who is a community development DCFI like Self Help; they have a branch office here in Charlotte to help us with our marketing effort. We felt like we had more feet on the ground here they have legal representative for business development representative here. We felt like it would be a good opportunity to utilize their services and in fact their manager and lenders are former Self Help employees and they are a tenant of ours so we know them very well. We felt like we’ve increased our utilization by allowing third party lenders to utilize the fund and we’ve had conversations with Mechanics & Farmers Bank and New Dominion Bank and both of them are very receptive to this. Finally we had a talk with the Support Center and certainly they are ready to be a third party lender as well. Self Help is the exclusive lender at this point. We felt like if we could extend our outreach in the community a little more it might have some better success by engaging third party lenders so that is why we have chosen that course to pursue. Another issue is we are a little concerned about the sustainability of the fund so we are recommending to incorporate a 1% administrative fee into the loan agreement to help recapitalize the loan officer service. Unlike our loan portfolio, you can sustain your portfolio with interest and repayment of loans; this was a big reserve and we really had no way to sustain the fund. Fallon: You didn’t have a reserve before the 1% or any reserve? Davis: We do have 1%; since 2008 we’ve had a 1% and this would be an additional 1%. Fallon: So it would be 2%? Davis: Right. Barnes: And how is that paid for? Does it come out of the loan? Davis: This would come out of the loan proceeds. Audience: But it can be added to the loan. Davis: This is very typical of a loan that is a marginal loan whether it is an SBA guaranteed loan or North Carolina Capital Access Program. We typically try to charge a fee that is kind of a risk premium. Barnes: I see the third bullet point will add 2% to the deal. How much does those first two bullet points add to the cost of administering the program? Davis: We are in negotiations right now; the only additional cost would be a fee that we are negotiating with the Support Center to help us with our marketing effort and also to provide us with more marketing data and more loan data and we could be talking about $500 to $700 per month for that service as funds administrator. That would be the only additional cost of the fund.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 12 Barnes: Let me play devil’s advocate for a second on a couple of issues. You’ve made 82 loans inside of Mecklenburg County; I don’t know how many inside Charlotte and I’d like to know that. But also 29 were made outside of Mecklenburg County and the City of Charlotte has put in the lions share in terms of individual, contributed the lion’s share of the money the $500,000 and I also note that even after the downturn in 2008 that you had your fourth best year in terms of loans granted in 2009 and the things have trailed off ever since. Could it be that the need for this has evaporated? Davis: No, I honestly think the need has probably increased. I still think, even though the recession was technically over long ago, small businesses are still feeling the impact of that. I think the need is there and I think we need to be more effective in how we market it and get the accessibility and exposure to it. We are concerned about those numbers too, I agree with you but we did question the need for it, but we feel like it is a matter of more outreach and we feel like we want to give that effort before we give up on it. Barnes: I understand. Let me ask you this. I don’t know how Grameen Bank markets itself and the micro loans that it does, but apparently it has been fairly successful. Davis: I’ve heard they have very good success. Barnes: I would be curious to know Mr. Kimble or Richardson, how they’ve gone about marketing their program and whether there is some relationship that could be established either with Mechanics & Farmers, New Dominion, BofA, Wells Fargo or any other bank in the community to add this opportunity either on their website or to their marketing materials for small businesses because here is what concerns me and this happens in government. When things like this become underutilized or unutilized, we find ways to either drive up the costs by adding more fees or paying some third party to do more work in order to spend the money. I don’t like doing that. If I’m spending public money, I want to do it because there is a justifiable need to do it, not because of something we’ve done for ten, 15 or 20 years and we just feel like we need to keep doing it. So what I’m honestly asking you to do is justify the existence of the program in light of the changes we seen, the diminished loan utilization rate, the proposed increase in costs for the program and the fact that I’m still concerned about the number of loans granted inside this City since we have put $500,000 into it as opposed to outside of Charlotte. I recognize that the other contributing partners have relationships outside the City, but we’ve put in the bulk of the money. Richardson: We talk about that often and you’ve asked a couple of questions and I will address them if you don’t mind. We’ve got 25% of the contribution, yet we receive 80% of the loan volume. That is something we look at and that is a good return of our investment. Grameen Bank is an interesting but very unique model; $1,500 average loans, no marketing at all, none, only word of mouth. Only word of mouth to women in our community who are trying to earn an income and often times are struggling. So as a point of comparison, I don’t think that is the right one but your point is very well taken about how we can collectively market this program. Barnes: I wasn’t comparing them; I was asking how Grameen Bank has gone about marketing itself as opposed to how the fund is marketing itself.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 13 Lyles: Is it word of mouth or is it referrals among that group? A lot of non-profits encourage those loans so there is another party involved in it so I just wondered about that. Harrold: If you don’t mind I’d like to say that users say here is the support network to find and model correctly and the average loan size in this program is the largest and you’ve got the numbers. It is larger by factor probably 15 to 20 times. Fallon: I would be happier if the 2% came out of the loan proceeds before because I worry about someone defaulting on it and you go with that 2% on top of it. Phipps: In relation to the question you asked, I notice that we also make loans in other municipalities when other municipalities haven’t really contributed as an investor. Have we approached them to consider a fair contribution? Davis: The investor’s footprint is within those municipalities. Most all of our investors are buying Time Warner Cable. Our investor’s footprint does cover the MSA so to speak, we just have not extended to reach as much as we could have to those neighboring counties. That gets back to your question Mr. Barnes about are we throwing good money after bad money with the work that we do next, but I just feel like we need more expertise as far as marketing and to your point about the social media and have more presence on the Internet. I think we can have more success and more bang for the buck and whether that is through the Support Center or technically the City of Charlotte is charged to allocate the services program for marketing the funds whether we find allocation of funds from there. It is going to take some money to market the fund. Harrold: In reference back to the 2% as a point of comparison, when the Small Business Administration issues a guarantee their up-front fee is 3.25% so the 2% fee is not out of line at all in terms of the only alternative in the market place and in most cases the folks that are making loans are not eligible to participate in the fund. Mayfield: Just for clarification the Support Center is a Raleigh-based community development financial institution and were there no local organization that you had conversations with as far as partnering to continue? What I was thinking about was Councilmember Barnes mentioned the amount of money that the City is contributing to this and it would be great to have that breakdown of how the loans are issued within the City and outside of the City limits. Were there no local organizations that seemed like a good partner? Harrold: I know that is really Eric’s question because he was responsible for that, but let me say that I am actually the original fund manager and have managed it for its entire life. I also work for Self Help which is headquartered in Durham as is Support Center and I am not aware of another CDFI that really mirrors the model of service support that the Support Center does and the fact that they have chosen; they do have a staff member who is permanently based in Charlotte and they are in a sense as Charlotte based as Self-Helper is. Brad’s point is well taken in that over 80% of the loans have been made in Mecklenburg County and virtually all of those have been within the Charlotte city limits. Eric can give you the account and run it by the footprint if you want, but the point is and Tom alluded to that as well, the majority of the funds were supplied by outside sources who are all regional in nature. I was not involved in securing initial funds; I came as the fund was getting ready to open.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 14 The regional provider such as the banks, Time Warner Cable, Foundation for the Carolinas, John S. and James L. Knight Foundation, etc., all had a regional group and frankly were not interested in, as I understand it, a Charlotte based fund. I think Brad’s point is well taken. The City of Charlotte has gotten a really good bang for its buck by getting the majority of the loans and providing a minority share of the funds. Barnes: I would submit to you that the people of Charlotte have hundreds of millions of dollars in these banks and spend millions of dollars with Time Warner. I hear you but I think we all have a little bit of cash in one of these entities, or a mortgage or a car loan or something. But I understand. Harrold: Our data indicates that 80% of the businesses who use the fund in the Charlotte region are located in Mecklenburg County and I don’t doubt that. If you look at how we’ve lined up, we’re exactly like the CSA. Austin: Committee, since we had a very detailed presentation from Small Business INClusion Program and they are looking at new strategies and new approaches, I’m wondering if there are any synergies between these two programs as a way of marketing a little bit better. Barnes: And we’ve got our expert right there to help us do that. Richardson: It is no coincidence that the former SBE Program and this SBE Loan Fund were conceived at the same time. I told you the name was changed a few years back because the perception in the community was that it had to be a certified SBE to be eligible for this loan fund. That is not the same and that is why we changed the name, but the next recommendation is to adjust the geography just like you did with the CBI Program so they are overlapping. Our intent as a tool in our toolbox for certified SBEs and now MWBEs working in the City is to use that as a marketing outlet as well in the new rebranded CBI, Charlotte Business INClusion Program. Mayfield: Thinking about the fact that the Support Center has their SBA area lending pilot program with a maximum loan amount of $200,000; if we were to move forward with this would it be a combination. Would this program stay separate or would we look at utilizing some of the programs that they have? If this has a max of $200,000 for that particular loan and we see that in 2013, we did only a total of $198,000 between five different organizations and looking at how the numbers have gone down, do we have a max on how much the loan can be currently and second trying to understand our 13 county combined statistical area. It would be helpful for me to know if we expand the area what their buy-in is into this so we can possibly look at reducing that amount that is from the City by having stronger partners come in or are we still looking at doing this expansion to match our Business INClusion Program by keeping the current partners and not expanding? Richardson: I can take the second question and that is I don’t think the Operating Committee has envisioned, at least in its current form, of asking other municipalities and governments in those districts to participate. That is certainly reasonable and the second part I think is we are not asking for additional City funding, it is just to keep the funds designated for this program. Barnes: Let’s clarify that. We’ve only put in $500,000 and as it has been paid back over the years. Do we put in $500,000 a year? It is just one time right? It is a revolving loan fund.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 15 Richardson: It is not lent directly; it is to leave there in the event of a borrower’s default. Barnes: So we secure ties with that money? Richardson: It helps make the loans more attractive. Our money is still there and we’re not asking for more money; it is a small amount of money and we’ve based some losses against the investment. Barnes: But we haven’t put in $500,000 per year for the last 11 years? Richardson: The action that the Operating Committee is asking you to take is just like every other partner, leave it in for additional ten-year term and make some changes. One thing we will recommend you receive annual and quarterly reports to the Operating Committee. You don’t see those very often and we want to see those. We think that should be an addition to the recommendation to Council. Barnes: I don’t like the idea of leaving North Carolina and I’m not so sure we really need to expand it. We just need to market it; five loans bother me a lot. Lyles: I guess I have a little bit of skin in this game. Barnes: I’m sorry Ms. Mayfield had another question, I’m sorry. He answered the second one. Harrold: You notice that the fund was actually restructured in 2008 beginning in 2009. The reason for that is the SBA changed their treatment of how these funds were actually used in the event of liquidation. Previously, the local office of the SBA had allowed us to treat that as a funding source instead of collateral which meant that it did not have to be liquidated first. The SBA centralized that process in Little Rock in 2008 and they said that is collateral and they immediately stopped making loans because we were giving 85% of it to the SBA and it was an effective use of funds so we immediately stopped using the fund. While I have the floor, I guess I would remind the group. Not that you need reminding when we keep talking about what happened in 2009. The years of 2009, 2010 and 2011 in particular, I would use the term in the small business community, just gut wrenching. You know the old saying if I had nickel; if I had $5.00 for every phone call I took that said I need working capital, I need money how can I get some and the first question we ask was, tell me how you have restructured your business so that you can survive in what is now a new reality. If the answer came back and said I’m just holding on waiting for things to turn around, our next response was, sorry we can’t help you. The management had to show that they were reacting to some of the greatest turmoil that I’ve seen in our economy in my lifetime and I have been in the lending business since 1973. Lyles: When this program was created it was based upon an analysis by the small and minority business firms and addressing what were their highest priorities to be successful to make a difference in it and I don’t know that those have changed because I think in the last presentation we had it was still access to capital, access to management capacity building and those things so I think when we ask the question is the program needed the question would be, my perspective on the answer would be if it is aligned with our Business INClusion Program, aligned with what we are doing with minorities

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 16 and small businesses then the need is still there. It is still the same market of people that we are trying to serve. The next thing that I think about the program is I always say that what was innovative ten years ago has become routine, so when we created this program for the Foundation for the Carolinas for some of the other partners that came out of the not for profit world to also contribute as much as the City put in. That was a huge change because we were trying to send the message that we were going to support smaller minority businesses in this community. When you look at the banking footprint it is not as much as when you look at the Knight Foundation, the Foundation for the Carolinas and the City. Then the final thing that I would say about this is that when something does become routine you do need to question it so for the me the question is how do we align it with what we are doing now and it meets those requirements and if it is doing what we need to do for both the SBE and the new MWBE emphasis that is an important aspect of this fund. The last thing I’m going to say is this fund was created because someone came to me and they wanted to actually have a tree planting contract with the City. They were a small business, but they didn’t have those trucks that the City often requires to go around to water the trees. This loan fund provides capital for those types of projects where you have the skill and the ability, but you can’t size up or meet the City’s requirement for some of the equipment that is required and we had a place to say in all of those sessions that we are working with these small and minority owned businesses and MWBEs to say you can quality for a City contract if you need this kind of equipment, here is the fund to go to. How it is structured to accomplish that I think is important, but at the same time those opportunities are still out there where a piece of equipment or software makes a huge difference that makes those folks eligible and gives them access to governmental contracts. I think the idea of going out and asking other governments would just stand in the way because it took us a year to get this built. If we go and just say well we’ve got this great program, come join us, you know how it works; if people come and ask us to join them, I’d be like really. But what I’m saying is I think the questions are needed and I’m discouraged by the amount of loans, so if it is marketing then let’s put it with the INClusion Program and the work that we are doing and come back and within a year. We haven’t seen the performance then we are done. It is kind of like, well maybe this isn’t the right way to do it, but until we answer; I know that there is a need by the businesses. If the fund isn’t meeting that need that is another thing, but I also know it is a part of our strategy for access that works with our other strategies and I believe that makes a big difference. Phipps: I know when it was originally adopted that it was a ten-year term so why are we sticking to ten-years? Have we evaluated to look at something that could be slightly less than ten years or why the ten-year timeframe? Lyles: I’d be comfortable that we have a one-year timeframe if these strategies work to come back and have a report to assess whether it ought to be another set of years. I’m more in the line have we tested it, can we make the market work for it versus a ten-year term. I don’t know if that is consistent with some of the documents that a lot of these organizations would require, I don’t know that, but I think that is an excellent point. Harrold: With all due respect, there is going to be a certain amount of adding the Support Center when people move in the role and there is going to be a certain amount of start-up time. There is also substantial amount of administrative overhead involved with all the other lenders and I guess I would like to publicly state for the record that Self Help has not charged a single cent in overhead and administration fees for 10 ½ years nor do we plan to continue doing so, but I would respectfully

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 17 suggest that a year is way too short of a time period and would suggest a minimum terms of three years. Lyles: The three years would make sense. Mayfield: Would three years be enough? Realistically, we are thinking about everything that you just shared and the fact that we need to build in that transition time. If that realistically enough time for us to really see if this is successful? You all as a committee came together and what you agreed upon as a committee was ten years so we would be basically telling you to go back to the committee and say all of that changed. I’m not a fan of when we appoint and identify a committee to work on an issue to just cut whatever the committee decided on if you all came to the agreement because I’m assuming there was a lot of discussion about how many years would be appropriate before you decided unanimously to approve ten. Harrold: There is a lot of work involved because every time the fund is restructured and/or modified we have to contact the investors and not all of them really know where to internally house their investments in the fund and with changes in staffing, it is time consuming to determine which area of the bank has the investment on their books. Wells, for example, we finally ended up out in their community development bank. There is some of what I would call friction time whenever it is renewed. I will defer to Eric and Tom but I would just remind you I did use the word minimum. Davis: You are right the committee did request ten years and one think I think we still believe in the fund but to Dale’s point, you’ve got to contact each one of those investors and it is time consuming. I think five years would be more reasonable personally. I think that would give us enough time; you need to have a sense of urgency with it as well so I can understand we need report to you on the funds’ performance, but I personally would like to see us do five years. Nelson: One of the things that I don’t want to miss in this; all of these actions that we were requesting today were initiated by Committee members recognizing that the fund had not been performing at a level we would have liked to see it perform. We formed a Transition Committee that met for over 12 months assessing what can we do to help this fund become more productive by providing better access to potential borrowers, increase marketing efforts and increase reporting by gathering data rather than just having Self-Help as the only assess point for obtaining a loan. We are currently aligned with Small Business INClusion of Charlotte and from a banking perspective, I spent 25+ years in the bank, but one thing is that we hope you guys done miss in this whole thing, is that is probably the toughest … business community so if the market is more challenged then their financial statements are going to be challenged, which means that their ability to pay becomes even more challenging. One of the things that we can pride in the fund is the fund has done a very good job of being good stewards of all of the investor’s funds. We would readily compare our funds’ performance in the last ten years against any funding company. I would like to think that most financial institutions would die to have a performance like that. So Self Help is truly to be commended for what they have done. We just think there are other things that we can do differently. I agree that we can do that in a shorter time but by putting more performance measures in place, so we can provide you guys information on a regular basis like who applied, why they were denied and what we can do to help businesses, we think this kind of information will be more useful to you.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 18 Harrold: I just want to comment or add to Eric’s comments, there is one other significant obstacle to small business lending in this climate and that is the size of loans that we are talking about. Given that interest margins and operating costs where they are I will go ahead and say in public, banks are simply not interested in a loan too small. Even for good credit risks it is very difficult to find financing. There really is a need for this fund and I don’t see anybody else really doing it. Barnes: What I’m hearing is there is, and by the way I like pushing on this like this because it makes people think and it makes me think and I think it is good to have us push back and you guys push back and you arrive at good outcomes I hope. But what I’m hearing is that you all feel like five-years is a reasonable period of time as opposed to the ten years which I think is fair as well. What I’m also hearing is that you believe there is a need in the community for the service. I don’t disagree with you. What I’m hearing is that you need some assistance marketing the program so that you get more applicants and I think Ms. Rosado, the Chamber and the major banks can help market this opportunity either directly or indirectly because there a lot of people in this City, and I’m sure in the surrounding region, but speaking for Charlotte, there are a lot of people in this community who I think would like to have access to capital of this nature to start a business to help their business succeed. We want you to do well, it is just that when we see the numbers dwindling like this it causes some concern for me and I believe for the rest of the Committee. I quite candidly like your current footprint and I don’t think you need to expand it beyond that if you market it right. I certainly don’t believe we have any business loaning money to people in South Carolina. Just to be candied with you and I think the further you get away from Mecklenburg County the more difficult that analysis becomes for me. I understand the footprint issue with the Business INClusion Program but that is for people wanting to do business here, not us sending money out of Charlotte. That is a problem so I wouldn’t be a fan of that, but I do like the track and respect the current footprint. Again from my perspective, I can respect the current footprint and I just think that if we talk about that marketing piece and the banks and the Chamber and our Business INClusion Program that we might move it in a better direction. Harrold: And with the addition of the Support Center. Barnes: Well, let’s talk about that. Harrold: Let me make one statement. Barnes: Make one statement. Harrold: One of the things that we found during the course of the gut wrenching recession was the impact that it had on Self Help as an organization. Because of our own issues brought about by the recession we actually shifted our priorities away from small business lending for a period of time as a major priority. We found that it was costing us about 120% of what we were lending in terms of administrative overhead. It was not something that we felt was sustainable to continue at that level of resource allocation. We have now begun to reallocate resources back towards small business lending and we’ve actually recently entered into a new partnership with Bank of America and the Foundation that propels us even more squarely into that, but the point that I’m headed toward is the Support Center is narrowly focused in on that small entrepreneurial start up that is so difficult to serve. That is where the focus is and that is why we fully support bringing them in as a partner

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 19 because they really have the resources and the allocation of resources to develop that sector I think more effectively than we can. Barnes: What did you say their fee is? Harrold: The fee is a discussion we have not been involved in. Davis: Negotiable of between $500 and $700 per month. Barnes: And that comes out of the 1.7? Davis: Yes. Lyles: I guess I’m going along with the Chair in terms of trying to summarize and get to a place where we are comfortable. I think that $500 to $700 for administration just because I like the idea of the walk-in traffic being the same place and getting more and actually asking you to do more to get some place that houses it because I don’t know of another place to do that. I think it would be great if they came to see Eric but I know that is not his job and I think to try to find someone else to do it is going to be difficult. So to me reasonable cost of doing business and especially linked to the ability to have that client market, I also don’t want to forget the point that you made on the 2%. I think that is an excellent point to incorporate in this. I’m not sure where we are landing on the alignment area; I hear the Chair saying pretty consistently and adamantly not to South Carolina. If that is okay we’re making the loans in Mecklenburg County so why do it when the loans are being made here; let’s try to continue there. I don’t know if a motion is in order yet Mr. Chair. Barnes: I was going to ask the Committee; there is still some reading I would like to do. I like what I’ve heard so for but can we bring it back at a subsequent meeting? Richardson: We anticipated that you might have questions and we’d come back in two weeks. Lyles: Oh, I’m sorry you had another slide. Richardson: We knew there would be a lot of discussion because small business banking is a hot question so we’ve logged in these questions. What other ones can we bring back? Barnes: I’ve got some because I wanted you to talk through that previous slide, the second bullet point. Davis: Monitor additional data points to better measure performance; this is really part of how we understand where our referral sources are, understanding what our activity is to Dale’s point of the number of calls they get about requests that we are not able to meet because of decimated balance sheet or income statements so it is really getting a better understanding of the nature of requests, getting a better understanding of the impact we are having on job creation. It really was not the purpose of the fund but still a good benchmark. Just being able to retrieve better data that Self Help just honestly doesn’t have the capacity to do right now and the volunteers on the Committee really

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 20 don’t have the capacity to do that so it is really using the Support Center and their capacity to help us pull together the statistical information. Barnes: We appreciate that. Would it be feasible for you all to come back in March of 2015 with an update on how things have gone over the last 12 months? We do want to know how things are going so I’m not suggesting that you change the ten years, but that you give us an update on the performance in March 2015. Would that work for you all so we will know before this Council changes? Davis: Sure, we’d be glad to do that. Harrold: Before we go, I have a story I want to tell; I want to put a face on the program. I’m not going to name the borrower’s name but one of our first loans in the fall of 2003 was for $15,000 to a woman who was starting up a snack distributorship aimed at a particular ethnic minority in the community. Over the course of the next years, we made her two additional loans and roughly similar amounts and about two years ago one Friday afternoon at a quarter to 5:00 the doorbell downstairs rang and I wasn’t expecting anybody, but it was her. She came up and said I want to pay my loan off and I want to hug your neck. She said we are now in five states and we’ve got 55 people working and I bless the day you made us these loans. Barnes: About like Shark Tank? Lyles: I think you should tell that story more often and that is the kind of thing that gets the word out about works in this community and segments of the community so thank you for sharing and the idea of using that tool. Phipps: The loans that are made, are they on the books of Self Help? Harrold: That is correct. Phipps: Can you classify that type of thing? Harrold: They would be categorized or they would be graded as all of our loans are in a particular grade. Loans under $50,000 we do not perform any on-site visits, so many of these loans do not get that rate of attention just because it is expensive, unless they go past due, in which they get lots of attention. Davis: The Operating Committee reviews the fund’s loan portfolio and all of its components including the follow-up past dues and we have certain parameters that we have to stay within. The fund could just end if we don’t meet our standards. Richardson: What I’m sensing is that next time we will come back; the only question I heard is how many loans are in Charlotte out of that Mecklenburg County subset. There was an earlier question about justifying the program and I don’t think we ended up with a remaining question there. Barnes: Let me say it this way. The preparing would be to address, not expanding beyond the current footprint.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 21 Richardson: I’ve got that as a question for the Operating Committee and how do they react to that. Barnes: Yes, the next piece is and the reason why I don’t think you have to expand beyond that footprint is because if you use the Chamber, if you use Ms. Rosado’s office, if you use Wells, BofA and the other big banks to help market a program through their website or either through social media, it may not be necessary to expand it to 13 counties and South Carolina. That is my thinking and my position. With regards to the other issues, you’ve got the cost issues that we talked about, you also and in fact the simplest thing may be to get the minutes because I don’t remember all my questions today because I did a lot of talking earlier. Richardson: We talked through a lot of them. Barnes: If you have any questions about what I said call me. Harrold: With all due respect you mentioned the large banks, the Chamber and I can very accurately and personally say to you that at least one of those banks while they are both good supporters of the fund and continue to be, but when it comes to direct involvement of the people in the bank’s network we are not even allowed to put a piece of marketing material inside for the City website directing them to us. With all due respect, I think your expectations of the support we will get from the banking community are very optimistic. Barnes: Is that one of the banks that is either currently headquartered or formerly headquartered here? Harrold: Yes. Barnes: I’ll talk to the Mayor and we will figure that out because what I’m suggesting is not necessarily that they allow us to put literature on their property but they recognize that there are a lot of people who cannot qualify for loans through the main stream, and I’m not putting this on you Mr. Harrold, but what I’m talking about is them at least putting some link on their website, on the small business website that will direct them to you guys. Harrold: Then with all due respect we are just a flea. Barnes: You are but you are a flea that at least 112 loans have been made out of. Harrold: Out of the context of a major organization, we are not even around here. Barnes: All I’m saying is let’s talk to Wells and BofA, PNC or whoever we need to talk to about a link on their website; whatever support they can provide because it behooves them to help create businesses in this City and the region. Is that fair? Mayfield: This ties in with that and I guess this would fall more in your category Ms. Rosado, when we are having this City partnering and sponsoring the different events. Every year, we have opportunities for people to come here with small business ideas; we need to make sure that we have

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 22 representation for this at those events immediately so a prime example, the whole conversation that started around mobile grocery stores was because someone presented in his presentation one, well during the year and a half that we’ve been working on the language he has also been trying to identify the funding to purchase the bus or whatever that transportation is going to be for his grocery store and there is a disconnect. This information for this organization is doing just that can give the opportunity for that $5,000 to $10,000 loan needed to purchase the vehicle for him to move forward with his award winning idea. That conversation hasn’t happened so there is a basic; we’re looking up here as far as how to make the connections on that executive level and again I’ve said this before, that grass tops and grass roots. We’re having this grass tops conversation; the grass roots conversation is every couple of months we are having some type of event where we are encouraging entrepreneurs and small business people to come to the table with their ideas. This needs to be set up there so people know okay now for you top five, top three, that one and for you others here is now some possible funding sources outside of the big. So it goes along with what you were saying as not necessarily looking at the big banks, but how do we utilize what we are already doing because we are working in silos, so we need to have some more transparency. Harrold: In response to your question, we have generally participated in most of those organized events over the past 10 ½ years. Over the past couple of years, we have been less diligent as I have primarily been assigned to a different team personally, and we just didn’t have the resources to do that, which is why again we need the Support Center for getting out and doing that; working on that level that you are talking about, the grassroots funding. Fallon: Why wouldn’t the bank? They are not going to lend to these small people and you are not a rival and it’s an accommodation to the community. Barnes: We will find out. I’ll talk to the Mayor and we’ll find out. Harrold: The short answer is these are larger organizations and you in the smaller banks are still a relevantly large organization there is no profit for the bank in looking at this market sector; it is a net loss in terms of the expenses and I hear what you are saying about the bank. We have frankly marketed and asked the banks so we have banks that are represented on our Operating Committee and we have beat our heads against that wall for ten years Mr. Chairman. Barnes: I will join you in that very shortly because we are not asking for money. Fallon: Have you gone to the credit unions? Harrold: Actually we do; we belong to the credit union association … but again marketing of the fund is not Self Help’s responsibility. We’ve done a lot of that through the years. Barnes: We got you; we’re going to help you. Harrold: Yes, we have worked and I personally have had contact with several of the local credit unions but again it is not our primary charge to market. Barnes: We are losing the Committee so Mr. Manager unless there is something else that you’ve got.

Economic Development & Global Competitiveness Committee Meeting Summary for March 20, 2014 Page 23 Kimble: Next meeting, I want to call your attention to a 2:00pm start time on April 3rd as opposed to noon. Ms. Lyles will not be here as she is out of town. The meeting was adjourned at 1:28 p. m.

Economic Development & Global Competitiveness

Council Committee Thursday, March 20, 2014 at 12:00 noon

Room CH-14 Committee Members: Michael Barnes, Chair Vi Lyles, Vice Chair Al Austin Claire Fallon LaWana Mayfield

Staff Resource: Ron Kimble, Deputy City Manager

AGENDA

Distribution: Mayor/City Council Ron Carlee, City Manager Leadership Team Executive Team

I. EASTLAND REDEVELOPMENT UPDATE – 30 minutes Staff: Brad Richardson, Neighborhood & Business Services Action: On October 1, 2013, the City entered into a Memorandum of Understanding (MOU) with Studio Charlotte Development, LLC (SCD) for a period of six months to develop a possible development framework for the site of the former Eastland Mall. The MOU will expire on March 31, 2014. At today’s meeting, staff will provide a recommendation for the Committee on potential next steps for the site. If ready, the Committee may make a recommendation to the full Council for consideration at a future business meeting.

II. CHARLOTTE COMMUNITY CAPITAL FUND MODIFICATIONS – 30 minutes

Guest: Tom Davis, Chairman, CCCF Operating Committee Staff: Eric Nelson, Neighborhood & Business Services Action: The Charlotte Community Capital Fund was established by the City and several community partners in 2003 to help small businesses in the Charlotte region gain access to capital that is otherwise unavailable through conventional lending. The majority of the funds that were provided to the Fund to be used as loan guarantees mature on March 31, 2014, subject to renewal by the partners. On January 28, 2014, the Fund’s Operating Committee approved modifications to the Fund intended to increase its utilization, and has requested the City to renew as a Fund sponsor for an additional ten-year term. Tom Davis, Chairman of the Fund’s Operating Committee will share the recommended changes with the Committee. No action required. Attachment: Summary of the Modifications approved on January 28, 2014.

III. NEXT MEETING DATE: Thursday, April 3, 2014 at 2:00pm, Room CH-14 Tentative Schedule:

• Amateur Sports Development at Bojangles Coliseum/Ovens Auditorium

5/9/2014

1

Eastland Redevelopment Update

March 20, 2014

Economic Development & Global Competitiveness Committee

Eastland Redevelopment Key Observations

• An 80-acre site is difficult for a single entity to develop due to speculative market conditions that will shape future development of the entire site.

• The site will require key infrastructure, primarily storm water controls and a street network.

5/9/2014

2

Eastland Redevelopment Recommended Approach

• Develop preliminary storm water analysis and design.

• Develop preliminary “master street/block” plan that defines the logical connectivity for the site.

• Identify and explore partnerships (both public and private) for a phased redevelopment of the site.

Eastland Redevelopment Conceptual Development Framework

Conceptual Framework

5/9/2014

3

Eastland Redevelopment Recommended Committee Action

• Decline the Developer’s request to extend the Memorandum of Understanding beyond March 31, 2014.

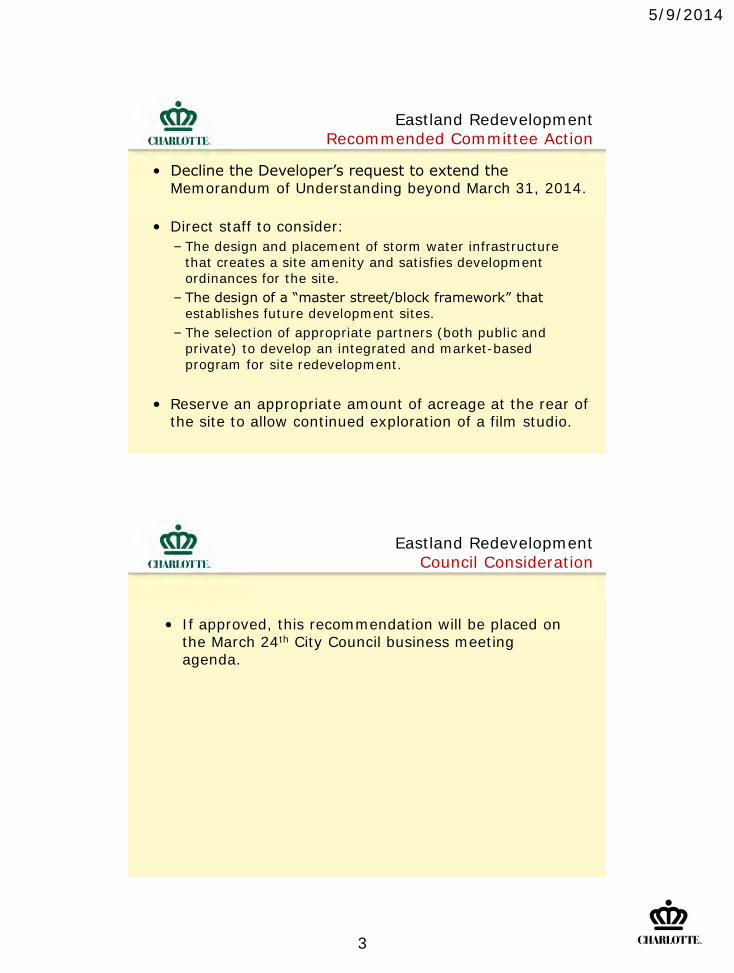

• Direct staff to consider: – The design and placement of storm water infrastructure

that creates a site amenity and satisfies development ordinances for the site.

– The design of a “master street/block framework” that establishes future development sites.

– The selection of appropriate partners (both public and private) to develop an integrated and market-based program for site redevelopment.

• Reserve an appropriate amount of acreage at the rear of

the site to allow continued exploration of a film studio.

Eastland Redevelopment Council Consideration

• If approved, this recommendation will be placed on the March 24th City Council business meeting agenda.

5/9/2014

1

Economic Development & Global Competitiveness Committee

March 20,2014

Charlotte Community Capital Fund Purpose

• A public/private fund established in 2003 to assist small businesses with gaining access to capital otherwise unavailable through conventional lending.

• Established as a partnership between 13 community partners, including the City, local banks and foundations.

• Oversight is provided by an Operating Committee of original Fund investors, including two appointments by the Mayor and City Council.

• Funds are not used as direct business loans. Funds are used as an 85% guarantee for business loans made by Self-Help, a non-profit community development lender in Charlotte.

5/9/2014

2

Charlotte Community Capital Fund Purpose

• Loans are typically used for equipment and inventory purchases

and to support working capital needs.

• The fund serves small businesses in Mecklenburg, Cabarrus, Rowan, Union, Anson, Gaston and Lincoln counties.

• Original agreements established a 10-year term for the Fund, subject to extensions approved by the investors.

Investor Amount

City of Charlotte $500,000

Wells Fargo Bank $375,000

Bank of America $250,000

John S. and James L. Knight Foundation $250,000

Foundation for the Carolinas $150,000

Branch Bank & Trust $100,000

PNC Bank $100,000

Fifth Third Bank $99,480

Piedmont Natural Gas $ 50,000

Time Warner Cable $ 40,000

Park Sterling Bank $ 40,000

First Citizens Bank $ 25,000

TOTAL $1,979,480

Charlotte Community Capital Fund Original Investors

5/9/2014

3

• Tom Davis – First Citizens Bank, Chairman • Betty Brain – BB&T • Ben Freeman – Wells Fargo • Dale Harrold – Self-Help Credit Union • Nigel Long – City of Charlotte (City Council Appointment) • Kevin McNeil – Bank of America • Eric Nelson – City of Charlotte • Nikki Patel – Park Sterling Bank • Robert Powell – City of Charlotte (Mayoral Appointment) • Michael Tanck – Time Warner Cable • Bonnie Zelweck – Fifth Third Bank • Vacant – PNC Bank

Charlotte Community Capital Fund Operating Committee

Year # of Loans Total Avg. Loan Amt.

2003-04 27 $1,532,400 $56,756

2005 15 $ 534,560 $35,637

2006 19 $1,079,679 $56,825

2007 7 $ 570,000 $81,429

2008 4 $ 198,000 $49,500

2009 14 $ 344,400 $24,600

2010 8 $ 329,000 $41,125

2011 4 $ 96,000 $24,000

2012 8 $ 311,000 $38,875

2013 5 $ 198,000 $39,600

111 $5,193,039 $46,784

Charlotte Community Capital Fund Annual Performance

5/9/2014

4

Borrower Profile # of loans Total % of Total

Minority 60 $ 2,878,960 54.1%

Females 56 $ 2,625,775 50.5%

Start-Ups 61 $ 2,862,275 55.0%

Mecklenburg County 82 $ 3,898,039 73.9%

Charlotte Community Capital Fund Performance Measures

Reserve Fund Status:

Original Reserve Fund Balance $1,979,480

Loan Losses ($207,344)