comments on “three glass tragedy beginning to rethink (us) financial policy” david a westbrook...

TRANSCRIPT

Comments on “Three Glass Tragedy

Beginning to Rethink (US) Financial Policy”

David A Westbrook

Andy Haldane

Bank of England

The Westbrook Thesis

• It has been a tragedy – but not a uniquely US one

• “Portfolio” approach to financial management:– May reduce risk– But increases uncertainty

• Risk is idiosyncratic; uncertainty is systematic • Systematic risk has gone up• Uncertainty manifests as:

– “Indeterminate” asset prices– “Downward biases” in asset prices

Different regulatory structures, same outcomes

Australia

Netherlands

France

Italy

China

Mexico

UK

Germany

Japan

Poland

Sweden

Norway

Spain

Portugal

Turkey

USA

Hong Kong

New Zealand

Singapore

-70

-60

-50

-40

-30

-20

-10

0

Integrated regulator

Objective -based

Institutional Functional

Chart 2: The percentage decrease in equity prices from 01/01/2007-10/12/2008

Per cent

Source: Datastream and Bank calculations

Systematic risk rises…

0

10

20

30

40

50

60

70

80

Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct. Jan.

Per cent(b)

2007

Average since 1998

08 09

…and implied losses exaggerated

Roots of Uncertainty

• Among the primary causes of uncertainty are:– Contract design (eg CDOn)– Industrial organisation of finance (eg

securitisation)– Myopia (eg VAR)– Network topology (eg CDS market)

ABCP

Equity

SIV

HY bonds

Mezzanine

Leveraged loans

Mezzanine tranche

Senior AAA

Senior ABS/CDOtranches

(andbank debt/

capital)

CDOmezzaninetranches

Senior

Mezzanine

Equity

Capital Notes

CDO

HY bonds

Mezz/second lien debt

Corporate assets

Leveraged loans

Equity

LBO’d company

CDO2

Mezzanine (often BBB-)

Sub-prime mortgages/Commercial mortgages

Senior

Equity

HEL ABS/CMBS

Mezzanine

BBB- ratedHEL ABS/

CMBSor

synthetic

Senior

Equity

CDO of ABS

CDOequity

tranches

Principal protected

notes

CPPI on CDO equity

FIN

AN

CIA

L E

CO

NO

MY

RE

AL

EC

ON

OM

Y

Financial contract design – ‘Russian Dolls’

MTNs

• Current episode borne of leveraging developments over the previous few years.

Sub-prime securitisation chain

Pre-crisis VaR

0

5

10

15

20

25

1 2 3 4 5 6 7 8 9

VaR Pre Crisis

Percent

Institution

Post-crisis VaR

0

5

10

15

20

25

1 2 3 4 5 6 7 8 9

VaR Post Crisis

VaR Pre Crisis

Percent

Institution

Post crisis CoVAR

0

5

10

15

20

25

1 2 3 4 5 6 7 8 9

Median CoVaR Post Crisis

VaR Post Crisis

VaR Pre Crisis

Percent

Institution

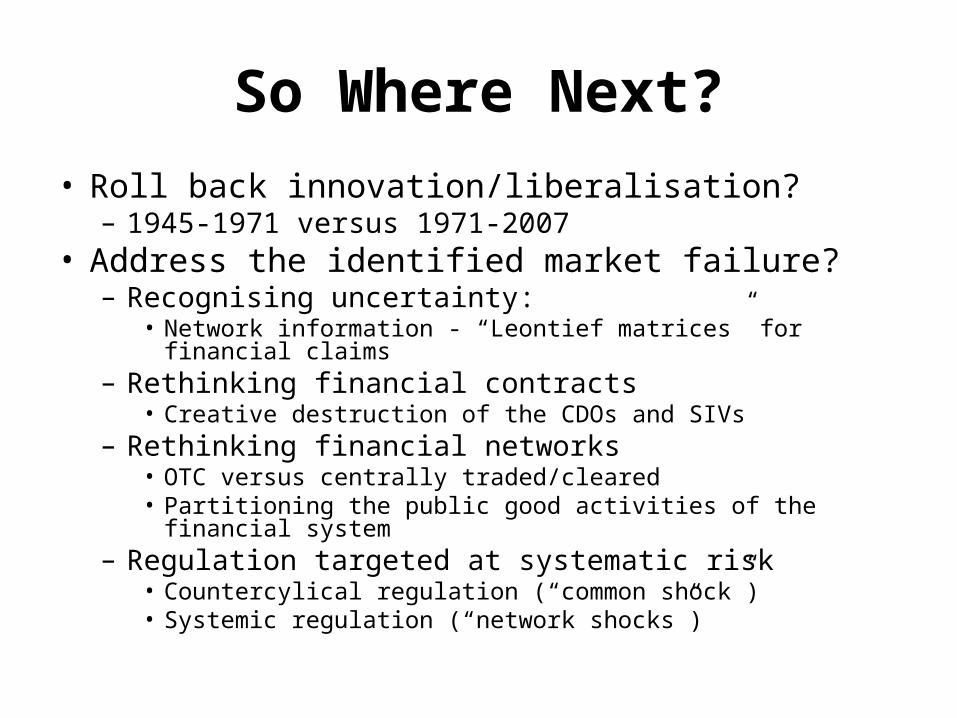

So Where Next?

• Roll back innovation/liberalisation?– 1945-1971 versus 1971-2007

• Address the identified market failure?– Recognising uncertainty:

• Network information - “Leontief matrices” for financial claims– Rethinking financial contracts

• Creative destruction of the CDOs and SIVs– Rethinking financial networks

• OTC versus centrally traded/cleared• Partitioning the public good activities of the financial system

– Regulation targeted at systematic risk• Countercylical regulation (“common shock”)• Systemic regulation (“network shocks”)

Financial Crises – Past and Present

Year 1881-1913 1919-1939 1945-1971 1973-1997

Probability of Crisis (%)

5 13 7 12

Depth of crisis (cumulative % GDP loss)

9.8 13.4 5.2 8.3

Average GDP growth (%)

1.93 0.98 2.13 2.43