cmi.comesa.int · web viewas a result, the trade deficit reduced from usd 1276.6 million recorded...

TRANSCRIPT

Exchange rate volatility and its effect on macroeconomic management in Rwanda

Prepared by Wilberforce NUWAGIRA

July 2014

The views expressed in this Working Paper are those of the author and do not necessarily represent those of COMESA. Working Papers describe research in progress by the author and are published to elicit comments and to further debate.

Abstract

In this study, we investigate exchange rate volatility and its impact on macroeconomic

management in Rwanda. To establish the empirical relationship between exchange rate

volatility and its impact on macroeconomic management, we build our analysis on quarterly

data spanning the period 2000Q1-2013Q4 and different quantitative techniques are

employed; we utilize structural vector autoregressive model (SVAR), Vector error correction

model (VECM), Granger causality, generalized conditional autoregressive model (GARCH) and

threshold autoregressive model (TAR). The econometric analysis starts with testing the

stochastic properties of data and we find most variables integrated of order I (1) save for

lnexp and lnexchrate_vol. Accordingly the paper proceeds by measuring the exchange rate

volatility using GARCH model and on the basis of exchange rate volatility and other variables

specified in the model we Estimate SVAR model and vector error correction models and the

main empirical result indicate that exchange rate volatility has a negative impact on

Rwanda’s exports .Other variables like gross domestic product, investment, current account

balance and CPI inflation are insignificant to exchange rate shocks but emerge correctly

signed. The study further confirms that there is a threshold level (4.33) beyond which

exchange rate becomes disruptive. In the view of these findings a number of policy

implications emerge which are also discussed in the present analysis.

Key words: Exchange rate volatility, GARCH, SVAR, VECM, Granger causality and TAR

1

I. Introduction

The real exchange rate is one of the key economic indicators of the economy’s international

competitiveness, and therefore has a strong influence on a country’s macroeconomic

management particularly foreign trade developments. Many developing economies have

experienced high real exchange rate volatility and this translates into high degree of

uncertainty for the two main monetary policy objectives that policymakers often seek to

achieve: price stability and economic growth.

Exchange rate volatility1 is a central theme in the debate on the performance of exchange

rate regimes. The consequences of this volatility for economic activities have always been a

major concern for policy makers. After World War II, the Bretton Woods agreements

created the International Monetary Fund and set up a world-wide system of fixed exchange

rates. One objective of this system was to foster international exchanges of goods and

services.

In 1973, the Bretton Woods system was abandoned and many countries allowed their

exchange rates to float. The consequence was an increase in exchange rate volatility thus,

the debate on the optimal management of exchange rates attracted renewed attention and

indeed experience shows that the relationship between exchange rate volatility and

macroeconomic developments have been extensively studied in both theoretical and

empirical studies.

Researchers for instance, clarida (1999) argue that the demise of the Bretton Woods

exchange rate system has led to significant fluctuations in both real and nominal exchange

rates. The liberalization of capital flows and the associated intensification of cross border

financial transactions appears to have exacerbated the volatility of exchange rates. Indeed a

study by Flood and Rose (1999) indicate that exchange rate volatility can have negative

effect on international trade particularly exports. The impact of global economy on

developing countries like Rwanda is significantly driven by swings among the currencies of

1 Exchange rate volatility is a statistical measure of the tendency of the exchange rate to rise or fall sharply within a short period and is important in understanding foreign exchange market behavior.

2

major economic powers-the overvaluation of the exchange rate undermines non-resource

exports and has adverse implications for growth.

Exchange rate assessment is a crucial element in evaluating Rwanda’s international

competitiveness and thus its macroeconomic performance and sustainability of its policies

and therefore has assumed a prominent place in economic development strategies as a

measure of export competitiveness.

Despite Rwanda’s impressive growth rates and its ability to maintain the stability of her

currency, her economy is still characterized by both internal and external macroeconomic

disequilibria, alongside low savings and investment rates. In addition, her exports are

mainly composed of traditional commodities like coffee, tea and minerals whose prices are

subject to fluctuations on the international market. This has prompted the government of

Rwanda to undertake reforms aimed at revamping the economy.

Since 1995, Rwanda has undergone a process of far-reaching economic and financial

reforms featuring particularly in trade and exchange rates. However, empirical evidence

reveals that there is a widespread presumption that volatility on the exchange rates of

developing countries is one of the main sources of economic instability around the world.

For Rwanda like any other developing country adhering to floating exchange rate, exchange

rate volatility is inescapable fact of life. It is not in itself a bad thing since exchange rate

movements are part of the adjustment mechanism through which economies react and

readjust to new sets of information and economic shocks nonetheless some argue that

exchange rates are too volatile given the underlying economic fundamentals and create

significant management problems for the financial institutions, businesses and economic

policy makers. In the light of recent macroeconomic developments in Rwanda, it becomes

quite important to examine the effects of exchange rate volatility on the economy.

Despite vast literature on the effects of exchange rate volatility on macroeconomic

management, little has been done to assess the impact of exchange rate volatility on

macroeconomic management citing Rwanda’s case. This study attempts to fill this gap by

3

exploring the impact of exchange rate volatility on macroeconomic management in

Rwanda.

Secondly, the studies that dealt with the exchange rate volatility and its effect on

macroeconomic management have yielded mixed results. This prompts the need to attempt

to shed light on this issue by providing empirical estimates on exchange rate volatility on

macroeconomic management whose results would give an idea for policy makers about the

level of real exchange rate volatility and serve as a basis for policy oriented

recommendations related to the modeling and the choice of exchange rate regime.

The objective of this study is to investigate the exchange rate volatility and its effect on

macroeconomic management in Rwanda, establish the extent beyond which exchange rate

becomes disruptive and give the appropriate macroeconomic policy to minimize the

volatility of exchange rates and their impact on Rwanda’s macroeconomic management.

The rest of this paper is structured as follows. Section 1 entails introduction, motivation of

the study, objectives and scope of the study. Section 2 includes overview of Rwandan

economy as relates to exchange rate volatility and macroeconomic management, section 3

includes both theoretical and empirical literature as relates to the study section 4

describes the methodology to be followed, and section 5 reports empirical results and

section 6 presents discussion of results, conclusion and recommendations.

II.Overview of exchange rate and macroeconomic management in Rwanda

As an open low income country, Rwanda considers exchange rate as a key macroeconomic

policy instrument that ensures export promotion and economic growth. The main goal of

Rwanda’s exchange rate policy is to provide a conducive environment that promotes

exchange rate stability and support the government’s objective of accomplishing export-led

growth.

4

In view of the above, the exchange rate policy in Rwanda is analyzed in two distinct

periods; the first period reflects a system of fixed exchange rate and the second period, a

more flexible exchange rate system.

During the fixed exchange rate system, foreign currencies of the banking system were held

by the central bank, it was the sole institution authorized to carry out exchange

transactions. The exchange rate was initially pegged to the Belgian franc, then to the

American dollar and finally to the special drawing rights (SDR). Its value did not reflect

economic reality due to lack of exchange rate flexibility (Himili, 2000). During this period,

the exchange rate seemed to be overestimated; causing the rising of effective prices of

Rwandan exports and loss of competitiveness on the international market. However, many

reforms of exchange rate system were undertaken since 1990 to correct the overvaluation

of FRW and improve external competitiveness.

The statutory order n° SP 1 of 3rd March 1995 organizing the foreign exchange market

instituted a flexible system of exchange of RFW. To avoid the risks related to the flexible

exchange system, the central bank has chosen a more flexible exchange rate policy of FRW

with nominal anchor, which links the level of exchange rate to the fundamentals of the

economy. The reform of the exchange rate system began with the launch of the structural

adjustment programs (SAP) in 1990. Residents were authorized to hold accounts in foreign

currencies in commercial banks since 1990, while in 1995, the flexible exchange rate

system was introduced and new exchange control regulations were put in place. The main

features of these new regulations are: full liberalization of current and capital account

operations, determination of the exchange rate by the market, introduction of foreign

exchange bureaus, authorization of foreign direct investment in Rwanda and the transfer of

returns on investment abroad.

Other measures were taken later to supplement these exchange control regulations for

instance the right granted to exporters to own and use their foreign currency export

proceeds and authorization given to residents to withdraw money from their foreign

currency accounts without providing any justification. For some operations, however, prior

approval from the BNR was maintained; this concerned invisible operations (medical care,

5

tourist trips, etc.) for which the purchase of foreign currency was subject to ceilings and

capital transfers abroad that were not related to current operations

The objective of this flexible system is approaching as much as possible the exchange rate

equilibrium level; to stabilize prices and support growth. Under this system, BNR

intervenes on foreign market to smoothen the volatility of exchange rate using its reference

rate as the average of interbank exchange rate and the BNR intervention rate.

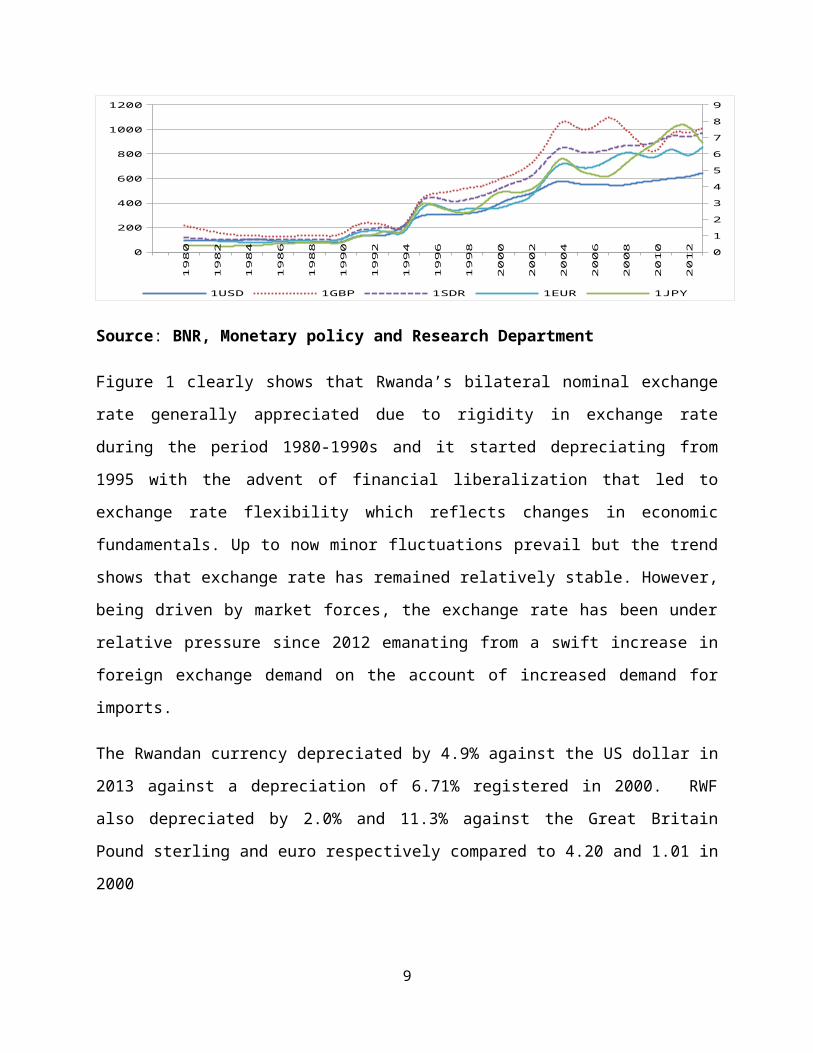

Fig 1: Bilateral nominal exchange rate of RWF (1980-2013)

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

130

200

400

600

800

1000

1200

0

1

2

3

4

5

6

7

8

9

1USD 1GBP 1SDR 1EUR 1JPY

Source: BNR, Monetary policy and Research Department

Figure 1 clearly shows that Rwanda’s bilateral nominal exchange rate generally

appreciated due to rigidity in exchange rate during the period 1980-1990s and it started

depreciating from 1995 with the advent of financial liberalization that led to exchange rate

flexibility which reflects changes in economic fundamentals. Up to now minor fluctuations

prevail but the trend shows that exchange rate has remained relatively stable. However,

being driven by market forces, the exchange rate has been under relative pressure since

2012 emanating from a swift increase in foreign exchange demand on the account of

increased demand for imports.

The Rwandan currency depreciated by 4.9% against the US dollar in 2013 against a

depreciation of 6.71% registered in 2000. RWF also depreciated by 2.0% and 11.3%

against the Great Britain Pound sterling and euro respectively compared to 4.20 and 1.01

in 2000

6

Similarly, in the context of EAC, the RWF depreciated against Kenyan shillings and

Tanzanian shillings by 2.6% and 3.0%, while appreciated against Ugandan shillings and

Burundian franc by 0.1% and 3.5% respectively. From the above trends, it is clear that

since 2012, RWF has faced persistent swings however, BNR through its policies and

measures including effective communication and market displine has managed to ensure

stability of Rwandan currency.

Figure 2: Development of REER in Rwanda

Jan-0

5

May

-05

Sep-0

5

Jan-0

6

May

-06

Sep-0

6

Jan-0

7

May

-07

Sep-0

7

Jan-0

8

May

-08

Sep-0

8

Jan-0

9

May

-09

Sep-0

9

Jan-1

0

May

-10

Sep-1

0

Jan-1

1

May

-11

Sep-1

1

Jan-1

2

May

-120.00

20.00

40.00

60.00

80.00

100.00

120.00

REERmREERxREERt

Source: BNR, Monetary Policy and Research Department

The figure below depict the trends of the three time series of REER obtained by using

different weights from imports ( REERm), exports ( REERx) and total trade ( REERt).

A closer look at the figure above shows that since 2005 the real effective exchange rate has

been appreciating but a sharp real appreciation is observed in 2008 mainly due to the

appreciation of the nominal value of the RWF against the currencies of major trading

partners. The RWF appreciated by 1.9% against the Kenyan shillings, 5.6% versus the

Burundi franc, 0.01% against US dollar,7.4% compared to the British Pound and by 13.6%

against the South African Rand. On the other hand, the appreciation of the real effective

exchange rate in 2008 was due to high inflation in Rwanda during this period compared to

prices in the major trading partners. Indeed inflation rate was 22.4% in Rwanda, 16.3% in

Kenya, 14.2% in Uganda, 13.5% in Tanzania, 1.6% in Euro Area, 3.1% in United Kingdom

and 0.1% in the US. However, we observe moderate REER depreciation since 2012 up to

7

present but RWF remains quite stable as moderate bilateral depreciation against USD, GBP

and EURO during this period is insulated by an increase in relative prices given that

domestic inflation has increased in relation to foreign inflation and the slowing pace of

nominal exchange rate depreciation.

Table 1: EAC currencies depreciation against USD (2008 – 2013)

Year USD/RWF USD/KES USD/UGX USD/TZS USD/BIF

2008 2.64% 21.98% 16.50% 15.37% -0.04%2009 2.26% -2.46% -3.47% 0.53% 8.92%2010 4.06% 6.51% 21.41% 10.47% -0.58%2011 1.63% 3.66% 5.75% 7.88% 3.94%2012 4.51% 1.06% 7.25% -0.20% 18.09%2013 6.12% 0.76% -4.98% -0.04% 1.13%

6 Years Average 3.54% 5.25% 7.08% 5.67% 5.24%Source: BNR, Financial Markets Department

The stability of RWF has been mainly attributed to good performance of external trade

coupled with the increased inflows from Budget support. Regarding external trade, the

Rwandan export sector continues to register good performance on the account of

impressive performance of formal exports whose value stood at USD 573 million in 2013,

representing an annual increase of 18.7%, while the volume increased by 6.8%. In the same

period, formal imports free on board(FOB) slightly increased by 2.2% in value amounting

to USD 2247.4 million and by 4.3% in volume. As a result, the trade deficit reduced from

USD 1276.6 million recorded in 2012 to USD 1224.9 million in 2013 and Import cost

insurance freight (CIF) cover by exports increased to 25.4% against 22.9% recorded in

2012. Including informal cross border trade, exports covered 30% of imports from 27.7%

in 2012.

As a consequence, in 2013 the overall balance of payments recovered from a deficit of USD

205.5 million recorded in 2012 to a surplus of USD 223.4 million and the BNR’s

intervention on domestic foreign exchange market declined from USD 455 million sold in

2012 to USD 322 sold in 2013. However, during the last two years the Rwandan franc

recorded upward trend depreciation due to an increase in imports of goods, especially the

8

capital and intermediate goods to finance the 8.6% and 8.0% GDP growth rate that the

country has recorded in 2011 and 2012 respectively.

Looking forward, BNR is committed to keep the RWF exchange rate fundamentally market-

driven. Therefore, BNR continues to progressively monitor domestic and international

economic environment to take appropriate decision in the due course.

Figure 3: exchange rate volatility and Rwanda’s export performance

2000QI

2000Q3

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

2011Q3

2012Q1

2012Q3

2013Q1

2013Q3

0

1

2

3

4

5

6

7

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

LNEXP LNEXCHRATE_VOL(right axis)

Source: BNR, Monetary Policy and Research Department

From figure 3 above, we observe that for the entire sample period Rwanda’s exports have

relatively been constant with only occasional increases and decreases registered in some

periods. We however observe that periods of low real exchange rate volatility were

associated with increase in the growth of exports but those periods of high real exchange

rate volatility such as 2002, 2003 and 2009 were associated with a sharp decline in

exports. This implies that real exchange rate volatility negatively impacts on Rwanda’s

exports to her major trading partners and Since we can witness the importance of exports

to the growth of Rwanda’s GDP, the effects of the volatility of the Rwandan franc should

not be taken for granted but should be carefully considered by policy makers. Hence, this

suggests a need for empirical research that provides further insight into the extent to

9

which this variability of the real exchange rate impacts on exports and to provide possible

suggestions of ways to control or alleviate it.

Figure 4: Real Exchange rate volatility real Gross Domestic Product

2000QI

2000Q3

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

2011Q3

2012Q1

2012Q3

2013Q

1

2013Q

34.8

5

5.2

5.4

5.6

5.8

6

6.2

6.4

6.6

6.8

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

LNRGDP LNEXCHRATE_VOL(right axis)

Source: BNR, Monetary Policy and Research Department

The figure above demonstrates that in Rwanda real gross domestic product decrease as

real exchange rate volatility increase however, we observe minor downward fluctuations in

growth and this is attributed to the fact that exchange rate variability has been moderate

and therefore has had a minimal effect to Rwanda’s exports competitiveness and real GDP

growth.

Figure 5: Real Exchange rate volatility and CPI Inflation

2000QI

2000Q3

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

2011Q3

2012Q1

2012Q3

2013Q

1

2013Q

30

1

2

3

4

5

6

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

LNCPI LNEXCHRATE_VOL(right scale)

Source: BNR, Monetary Policy and Research Department

10

Figure 5 above, depicts that over the sample period, upward movements in consumer

price index has always moved in tandem with exchange rate depreciation suggesting that

in periods when inflation was high the value of the Rwandan currency was eroded.

Similarly, sharp real exchange rate depreciation has always caused inflationary pressures.

Figure 6: real exchange rate volatility and investment

2000QI

2000Q3

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

2011Q3

2012Q1

2012Q3

2013Q

1

2013Q

30

1

2

3

4

5

6

7

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

LNINV LNEXCHRATE_VOL(right axis)

Source:BNR, Monetary and Research Department

A closer look at figure 6 above indicates that investment slightly slows down when

exchange rate volatility becomes high because volatility impacts on investment by

decreasing the credit available from the banking sector due to high inflationary pressures

and interest rates that alter market signals leading to inefficient allocation of investment

resources, loss of confidence in government policies thus damaging the expected return on

investment. However, it is observed that for Rwanda exchange rate variability has been low

and thus have had minimal effect on investment.

III. LITERATURE

III.1. Theoretical Literature

The impact of exchange rate volatility on macroeconomic management has gained

considerable importance in literature since 1970’s, following the adoption of floating

exchange rate from fixed exchange rate regime by most developing countries. Besides

being an important macroeconomic variable, it is also a very key variable in international

trade. Exchange rate has been defined as the price of one currency in terms of another

11

(Mordi, 2006). The increase or decrease of real exchange rate indicates strength and

weakness of currency in relation to foreign currency and it is a yardstick for evaluating the

competitiveness of domestic industries in the world market (Razazadehkarsalari, Haghiri

and Behrooznia, 2011). When there is deviation of this rate over a period of time from the

benchmark or equilibrium, exchange rate is called exchange rate volatility.

There are many factors contributing to real exchange rate volatility and the main ones

being the level of output, inflation, the openness of an economy, interest rates, domestic

and foreign money supply, the exchange rate regime and central bank independence

(Stancik, 2007). The degree of the impact of each of these factors varies and depends on a

particular country’s economic condition.

Olimor and Sirajiddinov (2008) in their study identify an inverse relationship between

exchange rate volatility on both the trade outflows and inflows in Uzbekistan. They contend

that there was a high presence of volatility in the exchange rate system after exchange rate

reforms of 2001 and 2003.

Bleaney (2008), in his work, examines the adjustment of domestic prices to exchange rate

movement as the reason for the existence of correlation between real exchange rate

volatility and trade openness.

Devereux and Engel (2003) emphasized that a flexible exchange rate gives room for the

adjustment of relative price, when prices are sluggish, while Engel and Rogers (2001) on

their part, analyze the border effects on relative prices for a sample of 55 European

countries from 1981 to 1997 and concluded that exchange rate volatility accounts for parts

of deviations in those prices.

Dornbusch (1989) examine the differences in RER volatility between developing and

industrialized countries. He identified the fact that volatility is higher in developing

countries, when comparing to industrialized countries. The author further identified three

12

times higher volatility in developing countries than in industrialized countries, but failed to

explain explicitly why such differences in volatility between the industrialized countries

and developing countries exit.

Based on a sample of 79 countries over the 1974–2003 periods Calderon (2004)

constructed the volatility of real effective exchange rate fluctuations as the standard

deviation of changes in the real effective exchange rate over a 5-year window. His results

also confirm that real exchange rate fluctuations in developing countries are four times as

volatile as in industrial economies.

Chen (2004) in his study, explains that an increase in price rigidity in the event of the

uncertainty caused by exchange rate volatility (i.e. firms becomes unwilling to change their

prices due to the possibility of later reversion to exchange rate). Apart from this, volatility

would account for much of inability of Purchasing Power parity (PPP) in cross-country

analyses and decrease the speed of mean adjustment towards PPP. By testing for speed of

convergence, the author discovered a positive significant coefficient for exchange rate

volatility that is the higher exchange rate volatility, the stickier the prices are.

III.2. Empirical literature

Empirical studies on the impact of exchange rate volatility on the macroeconomic

management are based on different theoretical frameworks, empirical models and samples

which often produce divergent results. In this regard, the following subsection reviews

relevant empirical studies on the impact of exchange rate volatility on macroeconomic

management. Indeed a sizeable chunk of the literature focusing on the impact of exchange

rate volatility on macroeconomic management is mixed at best.

Aydin (2010) employed panel data to examine the impact of exchange rate volatility in 182

countries spanning the period 1973-2008 and discovered different dynamics in the impact

of macroeconomics fundamentals on the equilibrium real exchange rate of Sub-Saharan

economies in the less advance economies.

13

Arize et al (2000) in their study, examine the RER volatility on the exports of 13 less

developed countries with quarterly data series for the period 1973-1996. They employed

Johansen’s Multivariate procedure and Error Correction Model to investigate the both the

long-run relationship and short-run dynamics explicitly, their result shows a significant

negative effect of volatility on export flows.

Broda (2004) using panel data of 75 countries for the period of 1973-1996 investigates the

impact of exchange rate volatility on economic fundamental by employing VAR model. The

findings show the presence of substantial shocks to terms of trade and real GDP in the

short-term. The result further confirms the negative shocks, resulting in larger exchange

rate movements in countries that adopted flexible exchange rate.

Accam (1997), while examining the exchange rate volatility and FDI flows in some selected

20 least developed countries, using OLS estimation, and employing standard deviation as a

proxy for instability in exchange rate volatility, the result shows a significant negative

relationship between exchange rate uncertainty and FDI flows for the period.

Aidin (2010) employs panel data for 182 countries from 1973 to 2008 and finds different

dynamics in the impact of macroeconomic fundamentals on the equilibrium real exchange

rate of sub-Saharan African economies compared with less advanced economies.

Wang and Barrett (2002) employ sectoral level monthly data and a multivariate GARCH-M

estimator and find that real exchange rate risk has insignificant effects in most sectors,

although agricultural trade volumes appear highly responsive to real exchange rate

volatility. Feenstra and Kendall (1991), Caporale and Doroodian (1994) and Lee (1999)

also employed a GARCH-type mechanism to estimate the volatility and found negative

relationship.

Meanwhile, Kroner and Lastrapes (1993) using the similar methodology obtained mixed

results with varied signs and magnitudes. Summarizing, most of the studies present strong

evidence that greater uncertainty in exchange rates (high volatility) reduces the foreign

trade flows (imports and exports) of a country.

14

Haussmann, Panizza, and Rigobon (2004) document those large cross-country differences

(74 industrial and developing countries; 1980–2000) in the long run volatility of the real

exchange rate. They employed the standard deviation of the growth rate of the real

exchange rate as a measure of volatility. The results imply that the real exchange rate of

developing countries is approximately three times more volatile than the real exchange

rate in industrial countries.

Schnabl (2007) identified robust evidence through panel estimation that exchange rate

stability is associated with more growth in the European Monetary Unit (EMU) periphery.

The evidence, according to him, is strong for Emerging Europe which has moved to more

stable environment.

In the synthesis, a big chunk of literature reviewed on the subject, the impact of exchange

rate volatility on the macroeconomic management remain ambiguous and several studies

has mostly been done on the exchange rate volatility on trade flows.

From the empirical literature, we also observe that the impact of exchange rate volatility on

macroeconomic management particularly on trade has been studied more in industrialized

economies than in emerging and developing economies.

In the context of Rwanda such a relationship is still unknown to the best of our knowledge

save for the study that was conducted on exchange misalignment in Rwanda.

From the methodological perspective, more recent studies have employed

cointegration/error correction frame work in estimating the relationship between

exchange rate volatility and macroeconomic management. Though literature is not

unanimous as to which measure is appropriate for measuring exchange rate volatility,

recent literature seems to be increasingly adopting the use of Bollerslev’s generalized

autoregressive conditional heteroscedasticity (GARCH) models.

15

IV Methodology

Drawing on Bernanke (1986) and Sims (1986), we ulitilize structural autoregressive model

(SVAR) given that it imposes contemponeous structural restrictions consistent with

economic theory. The form of the structural vector autoregression (SVAR) used in this

paper reflects the fact that Rwanda is a small, relatively open economy for which exchange

rate shocks can be an important driver

In a vector autoregressive framework all variables are endogenous and as a reduced form

of representation of a large class of structural models (Hamilton, 1994), SVAR model offers

both empirical trackability and a link between data and theory using the assumptions

underlying the structure of the economy. This approach identifies impulse responses by

imposing a priori restrictions on the variance-covariance matrix of the structural

innovations.

To capture the impact of exchange rate volatility on macroeconomic management, we

estimate a six variable SVAR model with exchange rate volatility (exchrate_vol), gross

domestic product (rgdp), private investment (inv), CPI inflation (lncpi), exports (exp) and

current account balance (c_bal) all in natural logarithm with the exception of current

account balance and on the basis of the estimated SVAR model we identify the dynamic

impulse response function. The model is thus specified as-

Zt= (lnexchrate_vol, lnrgdp, lninv, cpi, lnexp, c_bal)……….. (1)

The choice of structural ordering of variables should not be interpreted as an attempt to

provide strict identification of structural shocks but to assess the long run impact of

exchange rate volatility on macroeconomic management. In a matrix form a kin to

Hamilton (1994), the SVAR model is written as –

α 0x t=nt+α 1xt−1+α 2xt−2+……..α pt−px +μt……………. (2) Where X t is a vector of

endogenous variables, μt is the error term and pis the number of lags. The white noise

error imply that the structural disturbances are serially uncorrelated such that E=∆ where

E|μt μt '|= ∆ is the diagonal matrix. If we multiply equation 2 byα 0−1, we obtain a reduced

form VAR of the dynamic structural model

16

X t=α 0−1(nt+α 1xt−1+α 2xt−1+……………α pxt-p+μt…………………(3)

X t=c t+φ1xt−1+φ2xt−2+……………..φ pxt−p+ε t

Where φ s=α 0−1α s(s=1…..p), ∁=α 0

−1n and ε t=α 0−1μ t

The variance- covariance matrix of the structural innovations is thus given by E|ε t εt|'=α 0−1

E|μt μt '|(α 0−1)'=α 0

−1∆(α 0−1)'=ω

To generate the structural shocks, we use structural factorization of the variance-

covariance matrix of the reduced form VAR residualsω. Since the estimation of the SVAR

model has n2 more parameters than the VAR, in order to find a unique solution we require

both the order condition and the rank condition to be satisfied.

The order condition requires that the number of parameters in the matrices α 0and D

should be less than the number of free parameters in the matrixω . Sinceω is a symmetric

matrix, then the number of free parameters of the matrix ω is defined by n (n+1)/2.

Where n is the number of endogenous variables included in the system.

Assuming that D is a diagonal matrix thenα 0 can have no more free parameters than n (n-

1)/2. We can impose two different restrictions on matrixα 0. The first is the normalization

restriction that aims to assign the value of 1 to variablesX t ,i in each of the ith equation.

And the second is the exclusion restriction that aims to assign zero to some variables in the

equation (especially contemporaneous relations). These restrictions are defined by the

theoretical model. After obtaining the sufficient condition for the local identification, we

impose the restrictions suggested by the theoretical model2 and construct the matrix α 0 to

ascertain the relationship between the error terms of the reduced form model and the

structural disturbances ε t=α 0−1μ t

2 See Hamilton(1994)

17

[εtlnrgdpεtcpiεtlnexpεtlninvεtcbal

εtlnexchratevol]=[

1 0 0 0 0 0b21 1 0 0 0 0b31 a32 1 0 0 0b41 b42 b43 1 0 0b51 b52 b53 b54 1 0b61 b62 b63 b64 b65 1

] [μ t lnrgdpμ t cpiμt lnexpμ t lninvμ t cbal

μt lnexchratevol]…….. (4)

The μt denotes the shocks to the variables already specified in this model and this recursive

identification scheme is a kin to Ito and Sato (2007), Hahn (2003) and McCarthy (2000),

and implies that the identified shocks contemporaneously affect their corresponding

variables and those variables that are ordered at a later stage, but have no impact on those

that are ordered before.

Under this structure, the model is estimated as a SVAR using structural factorization and

structural decomposition to obtain the dynamic impulse responses. The impulse responses

of all other variables to the orthogonalised shock of exchange rate volatility provide the

impact of exchange rate volatility on macroeconomic management.

Though our main approach is to estimate the effect of exchange rate volatility on

macroeconomic management in Rwanda is SVAR model, we first need to measure exchange

rate volatility.

In the context of this study, generalized autoregressive conditional heteroskedasticity

(GARCH) model is used to measure and account for empirical features in exchange rate

volatility. GARCH model similar to bollersev (1986) is a simple model which models

current conditional variance with geometrically declining weights in lagged squared

residuals. The key insight of GARCH lies in the distinction between conditional and

unconditional variances of the innovations process {ε t}. The term conditional implies

explicit dependence on a past sequence of observations. The term unconditional is more

concerned with long-term behavior of a time series and assumes no explicit knowledge of

the past. GARCH models characterize the conditional distribution of ε t by imposing serial

dependence on the conditional variance of the innovations. The precondition of using the

GARCH method of estimation is to test for the presence of the ARCH effects in the real

18

effective exchange rate process. To do this the Lagrange Multiplier (LM) ARCH test was

employed.

The real effective exchange rate was assumed to follow a first-order autoregressive AR process, denoted AR

(1), and the following equation is estimated:

∆ (lnreer )t=β+β1∆(lnreer)t−1+ε t………………. (5)

Wherelnreer is natural logarithm of the real exchange rate andε t is disturbance term. If this

Lm ARCH test emerges as significant with chi-square distribution test statistic greater than

critical value less than 5% threshold, REER follows an ARCH(1,1) process and allows us to

generate the GARCH(1,1) a series measure of exchange rate volatility therefore the GARCH

process takes the relationship in equation 3 below

ht2=∅ 0+∅ 1 εt−1

2 +∅ 2h t−12 …………….. (6)

Where ht2 is the time variant conditional variance of the real exchange rate, ε t−1

2 is the

squared residuals obtained from equation 2 and∅ 0 ,∅ 1,∅ 2 are model parameters.

We also employ threshold autoregressive model (TAR) to examine the exchange rate

volatility threshold for Rwanda based on the sequential least squares estimation and we

consider a two regime threshold autoregression. TAR model is specified as –

y t=¿(α 0+α 1 y t−1+αρy t−ρ) 1(q t−1≤ γ) + (θ0+θ1 y t−1+..........+θρyt−ρ) 1(q t−1>γ) +ε t……………

(7) Where 1(.) denotes the indicator function, q t−1=q (y t−1……..y t−ρ) is a known function of

the data, ρ is the autoregressive order, γ is a threshold variable, αandθ are the

autoregressive slopes when q t−1≤ γ andq t−1>γ respectively and ε t is the error term assumed

to be a martingale difference sequence with respect to past history of y t. It is allowed to be

conditionally heteroskedastic

Most of the relevant data was collected from the world development indicators data set,

MINECOFIN and others from BNR statistics department. A longer time serie or monthly

19

data would be better but due to unavailability of high frequency data particularly monthly

data, we were prompted to use quarterly series.

V.Empirical Findings

V.1: Unit Root test

The analysis begins with ascertaining the order of integration of the variables. The

procedure adopted in this study involves the use of the Augmented Dickey Fuller class of

unit root tests. It is essential to investigate whether data series are stationary at level or in

differences. The importance of tests for stationarity of variables is rooted in the fact that

regression involving non-stationary variables leads to spurious regressions since the

estimated coefficients would be biased and inconsistent. When all or some of the variables

are not stationary, it is important therefore to carry out appropriate transformation

(differencing) to make them stationary.

Table2: Unit Root test

Variables ADF statistic(Absolute values)

Critical values1% 5% 10%

Order of integration

Lnrgdp 7.34 4.14 3.49 3.17 I(1)Lnexchrate_vol

4.29 4.14 3.49 3.17 I(0)

Lncpi 4.96 4.14 3.49 3.17 I(1)Lnexp 4.31 4.14 3.49 3.17 I(0)Lninv 8.78 4.14 3.49 3.17 I(1)C_bal 2.74 2.61 1.95 1.61 I(1)

Since unit root tests are sensitive to the presence of deterministic regressors, three models

are estimated. The most general model with a drift and time trend is estimated first and

restrictive models i.e. with a constant and without either constant and trend, respectively,

are estimated. Unit root tests for each variable, is performed on both levels and first

differences. The ADF test results reported in the table above indicate that all the variables

are stationary at first difference except exports and the indicator for exchange volatility

that become stationary at level; we therefore, reject the hypothesis of non stationarity at

5% level of significance.

20

V.2. Cointegration Test

Cointegration implies that despite being individually non-stationary, a linear combination

of variables can be stationary. Cointegration among variables reflect the presence of long-

run relationship in the system, the basic idea is that individual economic time series

variables wander considerably, but certain combinations do not move far apart from each

other. Generally, if variables are integrated of order “d” and produce a linear combination

which is integrated of order less than “d” say b, then the variables are said to be

cointegrated and thus long-run relationship exist.

To conduct the test for cointegration, the study applies the Johansen’s (1988) maximum

likelihood procedure since it allows for testing the presence of more than one cointegrating

vector.

Table. 3. Unrestricted cointegration Rank test (Trace statistic)

21

From the tables 3 and 4 the results obtained reveal the existence of one cointegrating

equation. The maximum eigenvalue and the trace statistics are both greater than their

critical values and their associated p-valves are significant thus, the null hypothesis of no

22

Series: LNRGDP LNINV LNEXP LNEXCHRATE_VOL LNCPI C_BAL Lags interval (in first differences): 1 to 1

Hypothesized Trace 0.05No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.907492 240.1804 150.5585 0.0000At most 1 0.516566 114.0163 117.7082 0.0837At most 2 0.343582 75.49380 88.80380 0.3078At most 3 0.253694 36.67746 42.91525 0.1826At most 4 0.227853 21.16863 25.87211 0.1724At most 5 0.131361 7.463850 12.51798 0.2986

Trace test indicates 1 cointegrating eqn(s) at the 0.05 level * denotes rejection of the hypothesis at the 0.05 level **MacKinnon-Haug-Michelis (1999) p-values

Table. 4. Unrestricted cointegration Rank test (maximum

Eigenvalue statistic)

VHypothesized Max-Eigen 0.05No. of CE(s) Eigenvalue Statistic Critical Value Prob.**

None * 0.907492 126.1641 50.59985 0.0000At most 1 0.516566 38.52250 44.49720 0.1931At most 2 0.343582 22.31073 38.33101 0.8432At most 3 0.253694 15.50884 25.82321 0.5887At most 4 0.227853 13.70477 19.38704 0.2745At most 5 0.131361 7.463850 12.51798 0.2986

Max-eigenvalue test indicates 1 cointegrating eqn(s) at the 0.05 level * denotes rejection of the hypothesis at the 0.05 level **MacKinnon-Haug-Michelis (1999) p-values

cointegration is rejected and the alternative for the one rank is accepted at 5% level of

significance. The presence of cointegration in the relationship among variables mimics the

existence of long-run relationship between real GDP as a proxy for macroeconomic

management and regressors implying that real GDP has a mean reversion property in the

long run, where the mean is viewed as the equilibrium rate. Hence, the cointegrating

equation captures the steady state relationship between the real GDP and its regressors.

V.3. Results of Granger causality

The concept of granger causality propounded by Sir Clive Granger in 1969 to describe the

causal relationships between variables specified in an econometric model. Causal relations

are studied because economists and policy makers alike need to know the consequence of

the various policy actions they would like to take. This concept is predicated on the idea

that variable X Granger causes Y if variable Y can be better predicted on the basis of

histories of both Y and X than can be predicted using the history of Y alone.

In the context of this study, Causality test is performed to identify the presence and

direction of causality among the variables specified in the model. This helps in identifying

variables that are endogenously determined and conditional on the other explanatory

variables in the model.

Table 5. Results of Granger causality

Pair wise Granger Causality TestsDate: 05/28/14 Time: 10:09Sample: 1 56Lags: 3

Null Hypothesis: Obs F-Statistic Prob.

LNEXP does not Granger Cause LNEXCHRATE_VOL 52 1.91475 0.1407 LNEXCHRATE_VOL does not Granger Cause LNEXP 3.01940 0.0394

DLNRGDP does not Granger Cause LNEXCHRATE_VOL 52 0.90146 0.4479 LNEXCHRATE_VOL does not Granger Cause DLNRGDP 0.24475 0.8646

DLNINV does not Granger Cause LNEXCHRATE_VOL 52 0.97655 0.4122 LNEXCHRATE_VOL does not Granger Cause DLNINV 1.63870 0.1938

23

DLNCPI does not Granger Cause LNEXCHRATE_VOL 52 2.24151 0.0964 LNEXCHRATE_VOL does not Granger Cause DLNCPI 0.24375 0.8653

DC_BAL does not Granger Cause LNEXCHRATE_VOL 52 0.89225 0.4525 LNEXCHRATE_VOL does not Granger Cause DC_BAL 0.88197 0.4576

The Granger causality result between exchange rate volatility and exports indicate a

unidirectional causality that moves from exchange rate volatility to exports confirming that

exchange rate volatility influences exports. In the same vein, unidirectional causality

running from exchange rate volatility to real gross domestic product is also observed in the

relationship between the two variables.

Further still, we find unidirectional causality in the relationship between exchange rate

volatility and the consumer price index that moves from lncpi to lnexchrate_vol

V.4. Vector Error Correction Model

After establishing cointegration among variables, it is appropriate to model the short-run

dynamics of real GDP as a proxy for macroeconomic management and explanatory

variables particularly exchange rate volatility for Rwanda. Vector error correction model

enables us to capture the short run dynamics of the model and this is formulated based on

the identified long run relationships. The VECM has cointegration relation built into the

specification so that it restricts the long run behavior of the endogenous variable to

converge to their cointegrating relationships while allowing for short run adjustment

dynamics. The cointegrating term is known as the error correction term since the deviation

from long run equilibrium is corrected gradually through a series of partial short run

adjustments. Thus cointegration implies the presence of error correcting representation

and any deviation from equilibrium will revert back to its long run path. Existence of

cointegration allows for the analysis of the short run dynamic model that identifies

adjustment to the long run equilibrium relationship through the error correction model

(ECM) representation.

The equation is represented as:

24

∆ x t=∅ ∆t+αβ ' x t−1+γ1∆ xt−1+γ p−1∆ x t− p+1+ECT t−1…………………. (7)

Where ECTt-1 is the error correcting term, DXt-1 is a vector of first differences of

explanatory variables and Xαβ t-1 is a matrix of cointegrating vectors

The general VECM model for lnrgdp as a proxy of macroeconomic management and

lnexchrate_vol is represented below using the respective variables used in the estimation

of the long run equilibrium equation.

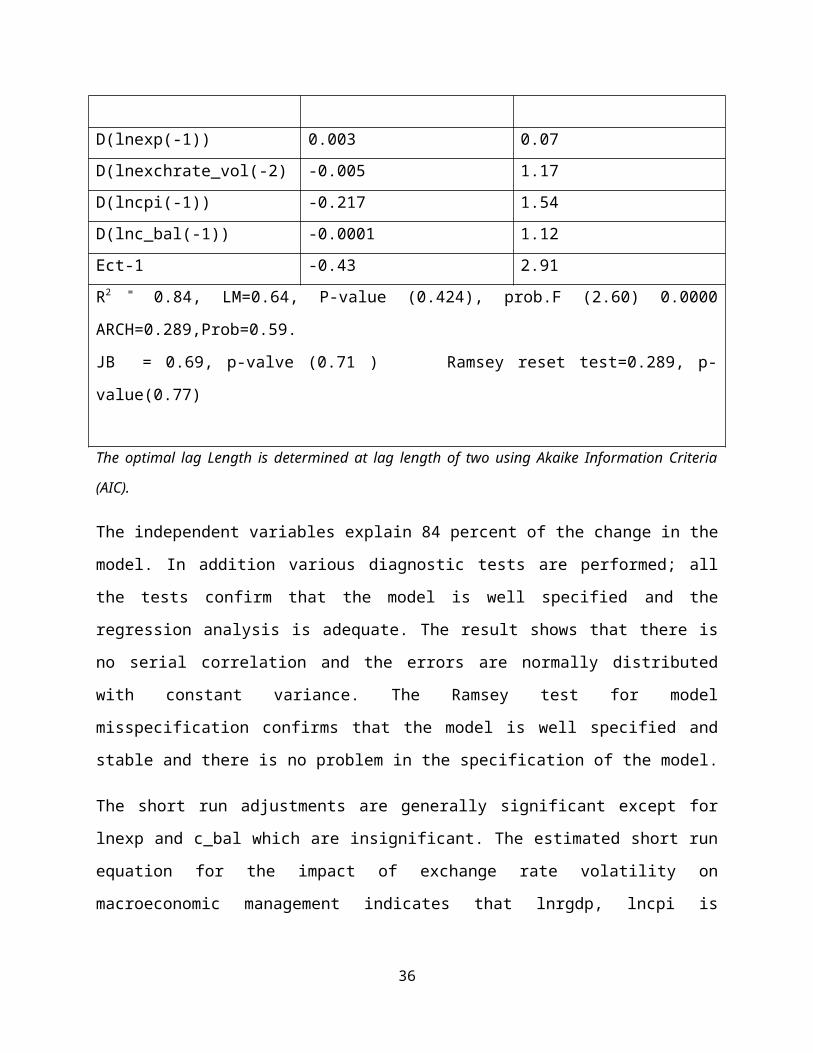

Table 6. VECM Model

Variables coefficients T-values

D(lnrgdp(-1)) 0.161 2.91

D(lninv(-1)) 0.116 1.42

D(lnexp(-1)) 0.003 0.07

D(lnexchrate_vol(-2) -0.005 1.17

D(lncpi(-1)) -0.217 1.54

D(lnc_bal(-1)) -0.0001 1.12

Ect-1 -0.43 2.91

R2 = 0.84, LM=0.64, P-value (0.424), prob.F (2.60) 0.0000 ARCH=0.289,Prob=0.59.

JB = 0.69, p-valve (0.71 ) Ramsey reset test=0.289, p-value(0.77)

The optimal lag Length is determined at lag length of two using Akaike Information Criteria (AIC).

25

The independent variables explain 84 percent of the change in the model. In addition

various diagnostic tests are performed; all the tests confirm that the model is well specified

and the regression analysis is adequate. The result shows that there is no serial correlation

and the errors are normally distributed with constant variance. The Ramsey test for model

misspecification confirms that the model is well specified and stable and there is no

problem in the specification of the model.

The short run adjustments are generally significant except for lnexp and c_bal which are

insignificant. The estimated short run equation for the impact of exchange rate volatility on

macroeconomic management indicates that lnrgdp, lncpi is correctly signed and significant

and Other variables though correctly signed emerged insignificant.

The vector error correction term (-0.43) is negative and significant which indicates that 43

percent of the disequilibrium in the previous period is corrected for in one quarter. Thus it

takes slightly above two quarters for the deviation to adjust to the long run steady state

position.

V.5. Impulse responses

To obtain the impact of exchange rate volatility on macroeconomic management, we

utilized SVAR model using structural factorization to recover the structural errors

identified in our recursive matrix. On the basis of the estimated model, we obtain the

dynamic impulse response functions (IRFs) using structural decomposition as the impulse

definition.

The results of the exchange rate shock under the identification framework described in the

SVAR model depict the impact of a one structural standard deviation shock defined as

exogenous, unexpected or temporary exchange rate volatility shock on other

macroeconomic variables specified in the model. The solid line in each panel is the

estimated dynamic impulse response while the dashed lines denote a two standard error

confidence band around the estimate.

26

Panel 1: impulse response functions (exchange rate shock)

-.02

-.01

.00

.01

5 10 15 20 25 30

Response of LNRGDP to Shock6

-.06

-.04

-.02

.00

.02

.04

5 10 15 20 25 30

Response of LNINV to Shock6

-.12

-.08

-.04

.00

.04

.08

5 10 15 20 25 30

Response of LNEXP to Shock6

-2

-1

0

1

2

5 10 15 20 25 30

Response of lncpi to Shock6

-60

-40

-20

0

20

40

60

5 10 15 20 25 30

Response of C_BAL to Shock6

-.4

-.2

.0

.2

.4

.6

.8

5 10 15 20 25 30

Response of LNEXCHRATE_VOL to Shock6

Response to Structural One S.D. Innovations ± 2 S.E.

Generally, the dynamic impulse responses obtained from the SVAR model shown in the

panel 1 above depict that most variables emerge correctly signed albeit most of them

turning out to be insignificant with the exception of exports and exchange rate own

structural innovations. The insignificance in most of variables could be due to the fact that

Rwanda’s exchange rate has generally been stable over the sample period. The result for

output and inflation is not surprising and a plausible explanation is that Rwanda’s financial

system is still plagued with structural weakness which has hampered the transmission

mechanism.

A one standard deviation structural shock on exchange rate volatility emerged positive and

significant as apriori expected implying that exchange rate volatility is positively impacted

by its own structural innovations with a contemporaneous impact which dies out after 3

quarters.

The finding on exports reveals that a one standard deviation structural shock on exchange

rate volatility negatively impacts exports and takes 2 quarters to reach full impact and dies

gradually after 10 quarters. Indeed exchange rate risk creates unconducive environment

27

for exports particularly real appreciation of exchange rate renders exports expensive and

less competitive on the international market.

V.6: Exchange rate threshold for Rwanda

The threshold for exchange rate volatility is obtained by estimating a two regime

autoregresion. Threshold autoregressive model based on sequential least squares

estimation method allows for the time varying thresholds and focus on the adjustment

dynamics when real exchange rate deviations exceed upper and lower forecast threshold.

The analysis begins with the idea that real exchange rates follow a non linear adjustment

process that is represented as a regime switching process.

Using a general TAR model akin to Bruce Hansen and Caner (2001), we examine the

presence of non linearities and establish the threshold beyond which movements in

Rwandan currency against other currencies becomes disruptive.

Table 8: Threshold Estimation______________________________________________________________________

Threshold Estimate: 4.33585167.95 Confidence Interval: [4.31147003, 4.36348057]Sum of Squared Errors .07295039Residual Variance: .001585878Joint R-Squared: .765330579Heteroskedasticity Test (p-value):.008966413______________________________________________________________________

Regime1 q<=4.33585167Parameter Estimates______________________________________________________________________Independent Variables Estimate St Error______________________________________________________________________Intercept 4.4532275 .147745142rgdp .0002787 .000518951inv .001047878 .000497347cpi -.008468768 .003077717exp .00018555 .000212639

28

Table 9: threshold estimates for regime2

Regime2 q>4.33585167Parameter Estimates______________________________________________________________________Independent Variables Estimate St Error______________________________________________________________________Intercept 4.67141385 .064915602Rgdp -.001405351 .000356509Inv .000238536 .000241331Cpi .002423562 .002238266Exp .000469146 .000092513

Tables 8 and 9 above show the threshold estimates for both regimes and provides evidence

for rejecting the null hypothesis of linearity given some threshold model and taking into

account the residual heteroskedasticity as suggested by white (1980), the model emerges

as non linear given that it yields a p-value (0.0089) less than 1% suggesting that the TAR

model with threshold value q is significant.

Figure 6. Confidence interval construction

020

4060

8010

0Li

kelih

ood

Rat

io S

eque

nce

in G

amm

a

4.2 4.3 4.4 4.5 4.6Threshold Variable

LR(Gamma) 95% Critical

Confidence Interval Construction for Threshold

29

The figure below depicts the sequential least squares estimate of the threshold as 4.33 with

95% asymptotic confidence interval (4.33, 4.36). The value of gamma where the likelihood

ratio lies below the red line yields the confidence region. The estimates 4.33 points to a

reasonable evidence for two regime specification and that the thresholds exists within the

interval ipso facto TAR splits the regression function into two regimes depending on

whether nominal exchange rate has been rising more than 4.33 and this threshold is

interpreted as the level beyond which volatility destabilizes Rwanda’s nominal exchange

rate implying that it is a threshold beyond which the negative effect of exchange rate

volatility becomes significant. From these point estimates we can look back at the historical

sample and examine how the TAR model splits the model into regimes and the first regime

is unusual regime consisting of 20% of the observation and regime two is usual regime as it

includes 80% of observations. This is consistent with estimated two-regime threshold for

South Africa which shows a threshold of 4.12, and the first regime is the usual regime as

79% of observations are included. The second and unusual regime is when the exchange

rate includes 21% of the observations. Though econometric techniques cannot replace

economic reasoning and intuition, the results are consistent with the intuitive expectations

and theory.

Figure: 7: exchange rate volatility

30

05

1015

exra

tevo

l

2006m1 2008m1 2010m1 2012m1 2014m1t

2006:2014Exchange Rate Volatility in Rwanda

We identify the episodes of volatility as depicted in the figure above. Exchange rate

volatility is measured on the basis of GARCH model where GARCH model based on

conditional variance is taken as the exchange rate volatility and the antecedents

characterizing the episodes are equally traced within the sample period.

In the 2006-2007 period, the exchange rate was low and stable insinuating that there was

real appreciation(overvaluation) of Rwandan currency mainly due to upsurge in aid flows

during this period which helped to beef up international reserves.

During the period 2008-2010, Rwandan currency was volatile owing to global financial

crisis that led to the drawdown of Rwanda’s international reserves and this led to

instability of exchange rate.

2012-2013 exchange rate variability was high with depreciation of the currency reaching

5.9% by end 2013 and this was mainly driven by aid freezing by donors exacerbated by

high demand of foreign exchange to import thereby reducing our international reserves

nonetheless, the depreciation has eased to 1.5% in 2014.

VI. Conclusion and policy Recommendations

31

Exchange rate remains an important element of international competitiveness and

continues to play a role in macroeconomic management. Though we find massive literature

on this particular subject, researchers and policy makers alike have not reached a

consensus regarding the impact of exchange rate volatility on macroeconomic

management.

The main objective of this study is to examine the relationship between exchange rate

volatility on macroeconomic management using quarterly dataset spanning the period

2000Q1-2013Q4. We employed a triangulation of GARCH, VECM, SVAR, TAR and Granger

causality. SVAR was employed to estimate the exchange rate volatility and its effect on

macroeconomic management and the linkage with the long run equilibrium path whereas

vector error correction model (VECM) was used to assess the short run impacts, Granger

Causality test was also to ascertain causal relationship between variables and the direction

of causality and threshold autoregressive (TAR) model was used to estimate the threshold

beyond which exchange rate becomes disruptive.

Since cointegration necessitates variables to be stationary, the stochastic properties of data

were assessed on the basis of ADF and the results indicate that all variables are stationary

at first difference except lnexp and lnexchrate_vol.

The main result from the long run model indicates that exchange rate volatility has a

negative impact on exports owing to the fact that exchange rate volatility can create a

volatile unconducive environment for exporters particularly real exchange appreciation

which discourages exports by making them expensive and less competitive. This has a dire

consequence for economies like Rwanda who heavily rely on primary products whose

price is not stable at the international market.

In the short run, the vector error correction term emerged as -043 which indicate that 43%

of the disequilibrium in the previous period is corrected for in a quarter. It therefore takes

slightly above 2 quarters for the deviation to adjust to the long run steady state position.

32

Causality test in reveal the presence and direction of causality between exchange rate

volatility and the explanatory variables particularly exports and GDP. The direction of

causality was found to be unidirectional in both cases.

Using TAR model, the null hypothesis of linearity is rejected and we deduce that the

exchange volatility in Rwanda is non linear

We further find the threshold band of 4.33 to 4.36 which are point estimates beyond which

exchange rate variability disrupts Rwanda’s real exchange rate.

Finally, the relevance of any empirical study lies in plausibility of its findings, accuracy of

its predictions and its simplication of measures to be taken to achieve the desired

outcomes. In the light of this, the paper recommends a number of but not limited to the

following recommendations-

Creating enabling environment geared towards improving the export base of the country

while reducing the over-reliance on the foreign imports should be at the core of

macroeconomic policies aimed at stabilizing exchange rate and boosting growth.

Though insignificant to exchange rate shock, inflation positively responds to the exchange

rate shock and this calls for the need to improve local production of commodities to

maintain and dampen pressures that would be occasioned by the exchange rate volatility

that accrue from high demand for imports which requires more foreign exchange.

The government should consider establishing well developed hedging facilities and

institutions that can protect its exporters against the exchange rate risk and also create a

conducive environment to influence the risk adjusted return on investment in order to

reduce the volatility of capital flows and in turn reduce currency volatility.

33

References

Schnabl, Gunther. 2007. “Exchange Rate Volatility and Growth in Emerging Europe and East Asia”. Open Economic Review, 10, 1007/s11079-008-9084-6.

Arize, A.C., Osang, T. & Stottje, D. J. 2000. “Exchange Rate Volatility and Foreign Trade: Evidence from thirteen LDCs. Journal of Business & Economic Statistics, 18 (1), pp. 10-17.

Arize, A.C., Malindretos, J. & Kasibhatla, K.M. 2003. “Does Exchange Rate Volatility Depress Export Flow: The case of LDCs. International Advances in Economic Research, 9 (1), pp. 7-19.

DeGrauwe, P. (1988), “Exchange Rate Variability and the Slowdown in Growth of International Trade”, IMF Staff Papers, 35, 63-84.

Kroner, K. F. and W. D. Lastrapes, (1991) “Impact of Exchange Rate Volatility onInternational Trade: Reduced Form Estimates Using the GARCH-in-Mean Model”,Manuscript, University of Arizona

Flood, R.P. and A.K. Rose (1999), ‘Understanding Exchange Rate Volatility withoutthe Contrivance of Macroeconomics’, Economic Journal, 109, 459, F660-72.

Engle, R. F. (2003). “Risk and Volatility: Econometric Models and Financial Practice”, Nobel Lecture, December 8, 2003.

Engle, F.R., and Rangel, J.G., (2004). The Spline–GARCH Model for Low Frequency Volatility and its Global Macroeconomic Causes, Review of Financial Studies, 21, 1187–1722.

Clarida, Richard H. (1999) “G-3 Exchange Rate Relationships: A Recap of theRecord and a Review of Proposals for Change”, NBER Working Paper 7434.December.

Kroner, K., and W. Lastrapes. 1993. “The Impact of Exchange Rate Volatility onInternational Trade: Reduced From Estimates Using the GARCH-in-Mean Model.”International Money and Finance 12:298–318.

Hausmann, R., U. Panizza, and R. Rigobon. 2004. “The Long-Run Volatility Puzzle ofthe Real Exchange Rate.” NBER Working Paper, vol. WP 10751.

Broda, C. “Term of trade and Exchange Rate Regimes in developing countries, Journal of International Economics, 63:1, 31-58, 2004.

Aydin, B. “Exchange Rate Assessment for Sub-Saharan Economies IMF Working Paper 10:162, 2010.

34

Accam, B. Survey of Measurement of Exchange Rate Instability, Mimeo, 1997.

Sarno, Lucio, Ibrahim Chowdhury and Mark P. Taylor. 2004. .Non-Linear Dynamics in the Law of One Price: A Broad-Based Empirical Study..Journal of International Money and Finance, 23, pp. 1-25.

Hansen, B., 1999, “Threshold effects in non-dynamic panels: estimation, testing, and inference”, Journal of Econometrics 93 (2), 345–368.

White, H. (1980). “A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity.”Econometrica, 48: 817–838.

Sanusi, A.R. (2010), ‘’Exchange Rate Pass-Through to Consumer Prices in Ghana: Evidence from Structural Vector Auto-Regression’’, Journal of Monetary and Economic Integration 10(1): 25-54.

McCarthy, J. (2000), ‘’Pass-Through of Exchange Rates and Import Prices to Domestic Inflation in Some Industrialized Economies’’, BIS Working Papers 79.

Ito, T., and K. Sato (2007), ‘’Exchange Rate Pass-Through and Domestic Inflation: A Comparison between East Asia and Latin American Countries’’’ RIETI Discussion Paper Series 07-E-040

Hamilton, J.D. (1994), Time Series Analysis, Princeton University Press, Princeton.

35

APPENDICES

Appendix1: trends of variables

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.8

5 10 15 20 25 30 35 40 45 50 55

LNRGDP

4.5

5.0

5.5

6.0

6.5

5 10 15 20 25 30 35 40 45 50 55

LNINV

-1

0

1

2

3

4

5 10 15 20 25 30 35 40 45 50 55

LNFDI

3.5

4.0

4.5

5.0

5.5

6.0

6.5

5 10 15 20 25 30 35 40 45 50 55

LNEXP

-8

-7

-6

-5

-4

5 10 15 20 25 30 35 40 45 50 55

LNEXCHRATE_VOL

3.8

4.0

4.2

4.4

4.6

4.8

5.0

5 10 15 20 25 30 35 40 45 50 55

LNCPI

-800

-600

-400

-200

0

5 10 15 20 25 30 35 40 45 50 55

current a/c bal

Appendix 2: GARCH (1,1) Estimation output

Dependent Variable: LNREERMethod: ML - ARCH (Marquardt) - Normal distributionDate: 05/28/14 Time: 09:56Sample (adjusted): 2 56Included observations: 55 after adjustmentsConvergence achieved after 55 iterationsPresample variance: backcast (parameter = 0.7)GARCH = C(3) + C(4)*RESID(-1)^2 + C(5)*GARCH(-1)

Variable Coefficient Std. Error z-Statistic Prob.

C 0.729854 0.331007 2.204955 0.0275LNREER(-1) 0.833815 0.076074 10.96061 0.0000

Variance Equation

C 0.000407 0.000236 1.722981 0.0849RESID(-1)^2 0.819186 0.445496 1.838819 0.0659GARCH(-1) 0.106112 0.143687 0.738494 0.4602

R-squared 0.740392 Mean dependent var 4.356089Adjusted R-squared 0.735494 S.D. dependent var 0.069038S.E. of regression 0.035507 Akaike info criterion -3.824928Sum squared resid 0.066818 Schwarz criterion -3.642443Log likelihood 110.1855 Hannan-Quinn criter. -3.754360Durbin-Watson stat 1.638253

36

Appendix 4: exchange rate volatility regimes

2000q1

2000q3

2001q1

2001q3

2002q1

2002q3

2005q2

2005q4

2006q2

2006q4

2007q2

2007q4

2008q2

2009q2

2009q4

2010q3

2011q1

2011q3

2012q1

2012q3

2013q1

2013q34

4.1

4.2

4.3

4.4

4.5

4.6

4.7

Regime 2>4.3 Regime 1<=4.3

37