class 4 notes the economics of business harvard extension school instructor: bob wayland teaching...

TRANSCRIPT

CLASS 4 NOTES

The Economics of Business

Harvard Extension SchoolInstructor: Bob WaylandTeaching Associate: Natasha Wambebe

2

Recap of Previous Classes

Where does economic wealth originate? Why does trade and hence markets

emerge?According to Coase why do firms emerge

(coagulate) from the buttermilk? What factor does Alchian and Demsetz

stress in the formation and shape of firms?

Which factor does Alchian and Demsetz employ to distinguish among types of firms?

Outline is incomplete without oral accompaniment

Outline is incomplete without oral accompaniment

3

Recap of Previous Classes…

What factors influence the extent of vertical integration in Stigler’s industry life cycle model?

What decision-making value does simple profit maximization play in a world of uncertainty?

What are the characteristics of adaptive behaviors and adoptive forces?

What can you learn about trial-and-error from a nearsighted grasshopper?

What are the evolutionary economic factors that are analogous to the biological forces of heredity, mutation, and natural selection?

Outline is incomplete without oral accompaniment

4

Recap of Previous Classes…

What is the “dominant design” model of product sector evolution as outlined by Nelson and Winter?

What is the “competence puzzle”What roles do routines play in

organizations?

5

Steven Klepper, “Entry, Exit, Growth and Innovation over the Product Life Cycle”

Outline is incomplete without oral accompaniment

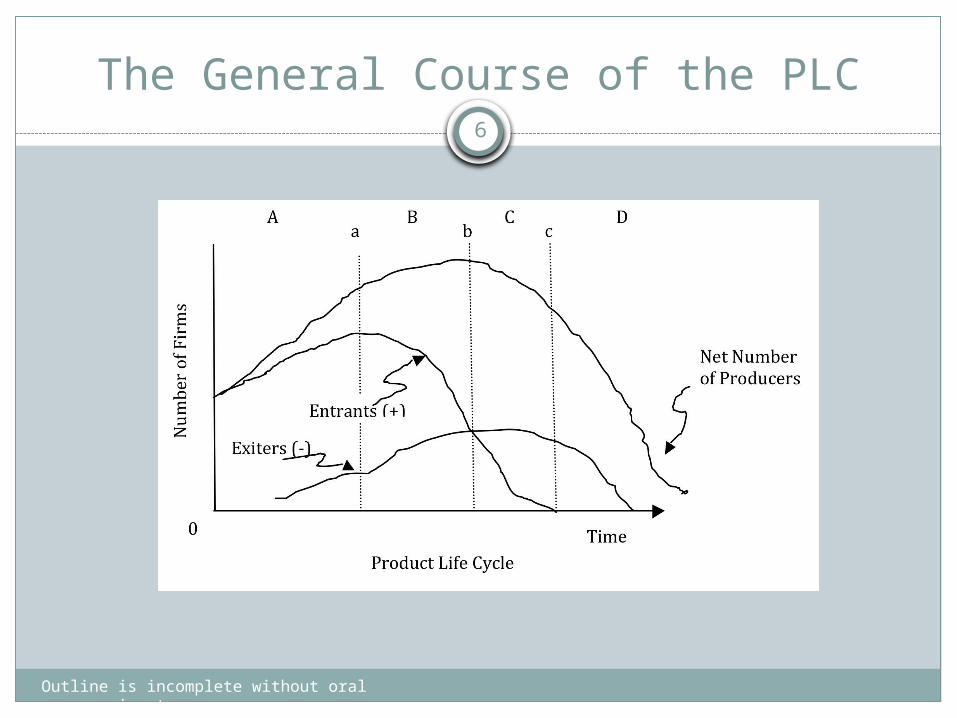

Empirical Literature – Six “Regularities”

Number of entrants often rises at the beginning of an industry but declines over time until number of entrants becomes small or zero

Number of producers increases initially, reaches a peak, then declines despite continued industry growth

Rate of change of the market shares of the largest firms declines eventually and the industry structure stabilizes

The diversity of competing product variations and the number of significant product innovations tend to reach a peak during the period of growth in number of producers, then decline

Over time, producers devote increasing effort to process relative to product innovation

While the number of producers is growing, the most recent entrants account for a disproportionate share of product innovations

Outline is incomplete without oral accompaniment

6

The General Course of the PLC

7

Steven Klepper’s PLC Model

Outline is incomplete without oral accompaniment

Two foundations:Product demand is the incentive for both

process and product innovation Process innovation is conditioned by total demand for the

firm’s product: the greater that demand, the greater the potential return to process

Product innovation is conditioned by the demand of new buyers

Firms are endowed with distinctive capabilities that determine the type and effectiveness of their innovation efforts

8

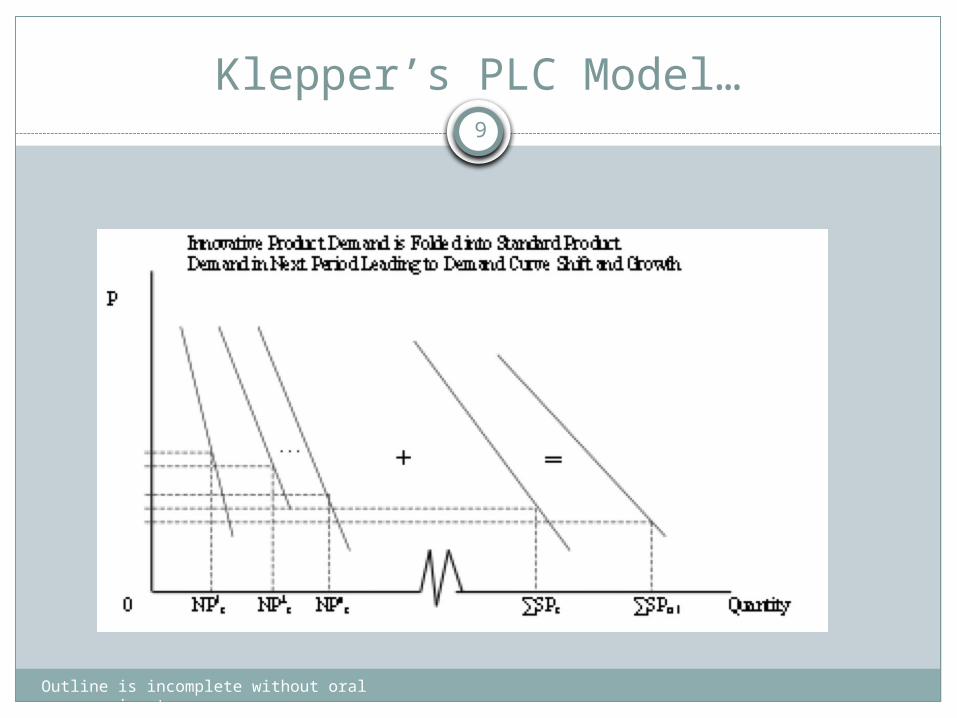

Klepper’s Model of PLC…

Outline is incomplete without oral accompaniment

At the beginning of each period all firms decide:Incumbents: stay or exitPotential entrants decide whether to jump inAll decisions are based on expected profitsAll firms produce a standard product, are price

takers, and the price clears the marketThe market grows through entry and the folding-in

of distinctive products to enhance the standard product and enlarge its market

This may seem to conflict with Alchian’s point about profit maximization as a guide to behavior under uncertainty but Klepper apparently assumes that period t prices are known and uncertainty applies only to subsequent periods. Thus his firms are very near-sighted.

9

Klepper’s PLC Model…

Outline is incomplete without oral accompaniment

10

Klepper Model Decisions

Outline is incomplete without oral accompaniment

Incumbent firms make a limited number of decisions. How much research and development to conduct on,

respectively, product and process innovation, How much in adjustment charges to incur, if any, to

increase sales and hence output

Potential entrants must decide if their product development skills are sufficient to jump in and earn a profit and to survive given the incumbents’ volume based advantages.

11

Klepper’s Product Innovation Formula

Outline is incomplete without oral accompaniment

A firm’s ability to create a significantly innovative product depends upon its innovative skill, the resources applied to product innovation, and the opportunity for innovation in the product or category described by a function g(rd). Product innovation skills, s, are distributed randomly and reach a maximum at

smax. The successful product innovator earns a monopoly profit, G, on sales of the

innovative product. All producers monitor their rivals’ innovations at a cost of F per period. This

enables them to incorporate the innovations into their own products in the following period. (recall imitation in Alchian) This process fosters a convergence among product variations.

The formula for revenues and costs associated with the product innovation function:

Eq (a): [si + g(rdit)]G – rdit – F To ensure that a firm can’t live on product innovation alone, F is assumed

greater than the net returns from product innovation: F > [si + g(rdit)]G – rdit

12

Klepper’s Product Demand Curve

Outline is incomplete without oral accompaniment

Total standard product quantity demanded in period t, Qt, is a function of price in the period, ft(pt), which is a standard continuous, downward sloping demand curve.

Incumbent firm outputs grow at the market growth rate for the past period. Quantity for firm i in period t = firm i’s output in previous period times the ratio of market output in time t to time t-1:

Eq (b): Qi t = Qi t-1 (Qt/Qt-1))

Outline is incomplete without oral accompaniment

13

Klepper’s Market Adjustment Function

If an incumbent firm desires to increase output even more, it can do so by incurring an adjustment cost given by the function m(∆ qit). Results in expanded market share.

This function is assumed to be concave and increasing without bound to reflect increasing marginal adjustment costs.

If a firm does employ m to reduce costs, its output becomes:

Eq (b1): Qi t = Qi t-1 (Qt/Qt-1)) + ∆qit

14

Klepper’s Production Cost and Process Innovation Functions

Outline is incomplete without oral accompaniment

The average cost of production is assumed independent of firm output but directly related to amount spent on process innovation, rcit, through the function l(rcit) which acts to reduce the average cost per standard product.

As rcit increases, l(rcit) asymptotically approaches an upper bound reflecting diminishing returns to investments in cost reduction.

Average unit cost for the standard product after process innovation gains is then:

Eq (c): c – l(rcit) Average contribution or margin per unit of standard product is:

Eq (d): p – [c- l(rcit) ] or p – c + l(rcit)

15

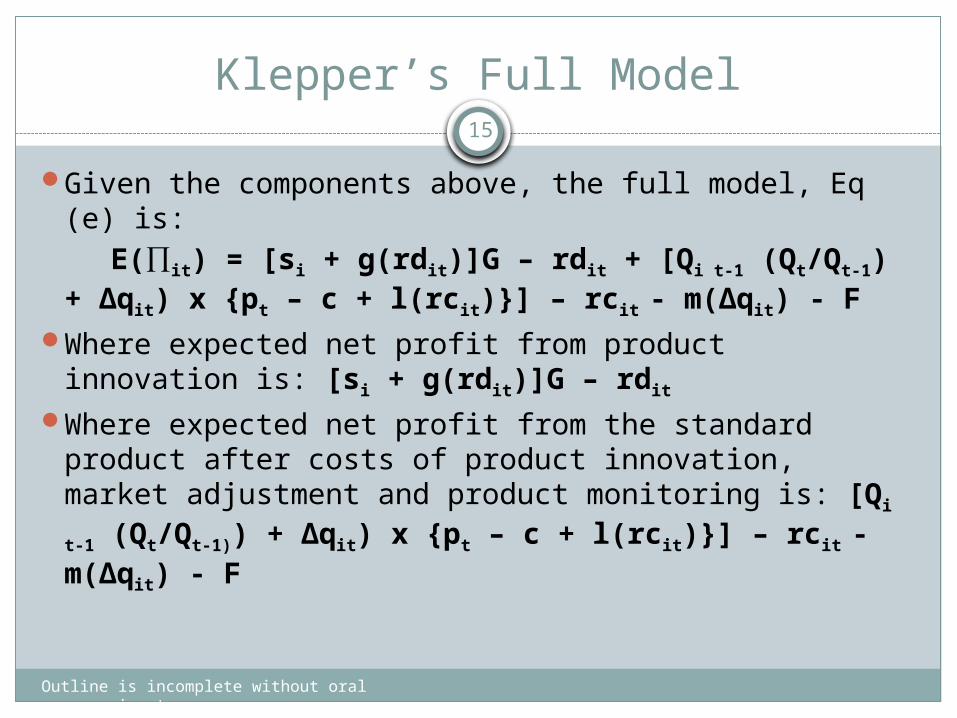

Klepper’s Full Model

Outline is incomplete without oral accompaniment

Given the components above, the full model, Eq (e) is:

E(∏it) = [si + g(rdit)]G – rdit + [Qi t-1 (Qt/Qt-1) + ∆qit) x {pt – c + l(rcit)}] – rcit - m(∆qit) - F

Where expected net profit from product innovation is: [si + g(rdit)]G – rdit

Where expected net profit from the standard product after costs of product innovation, market adjustment and product monitoring is: [Qi t-1 (Qt/Qt-

1)) + ∆qit) x {pt – c + l(rcit)}] – rcit - m(∆qit) - F

16

Klepper’s PLC Model…

Outline is incomplete without oral accompaniment

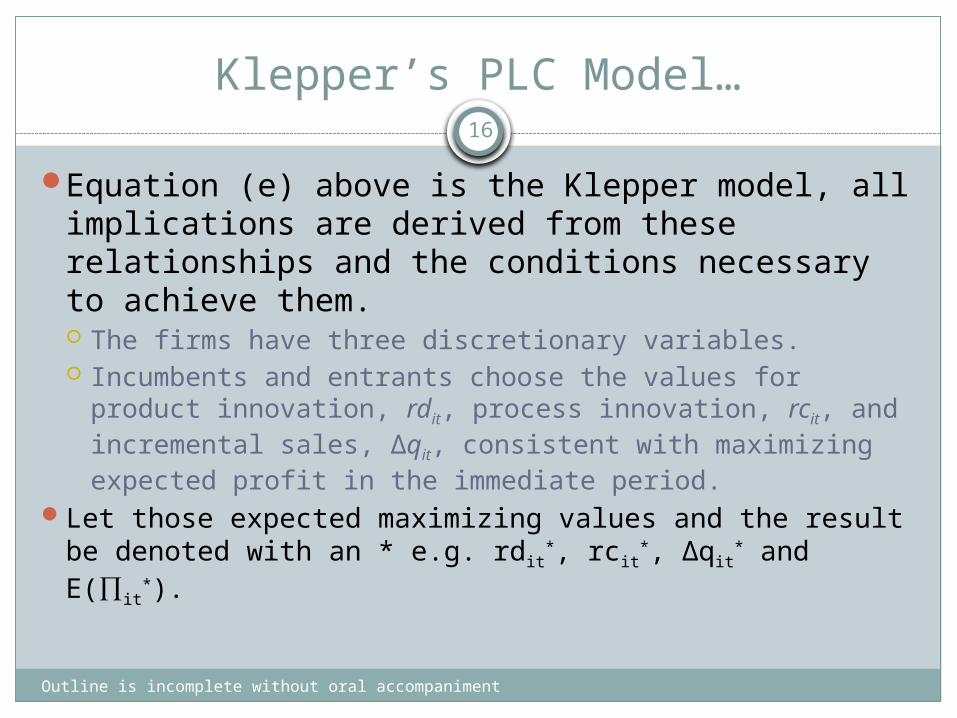

Equation (e) above is the Klepper model, all implications are derived from these relationships and the conditions necessary to achieve them. The firms have three discretionary variables. Incumbents and entrants choose the values for

product innovation, rdit, process innovation, rcit, and incremental sales, ∆qit, consistent with maximizing expected profit in the immediate period.

Let those expected maximizing values and the result be denoted with an * e.g. rdit

*, rcit*, ∆qit

* and E(∏it*).

Outline is incomplete without oral accompaniment

17

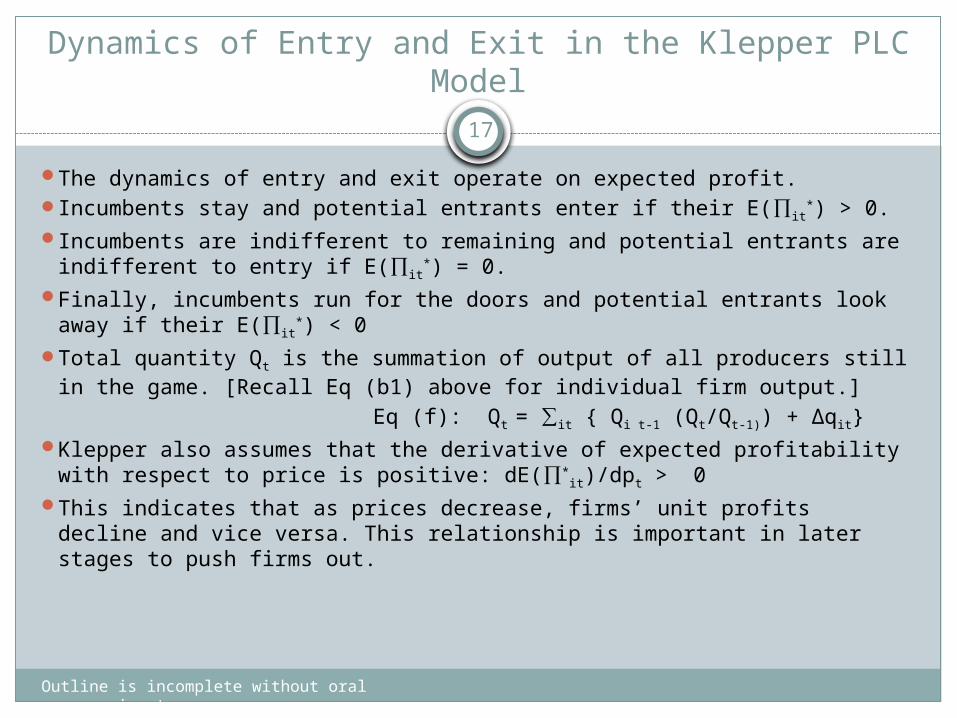

Dynamics of Entry and Exit in the Klepper PLC Model

The dynamics of entry and exit operate on expected profit. Incumbents stay and potential entrants enter if their E(∏it

*) > 0. Incumbents are indifferent to remaining and potential entrants are

indifferent to entry if E(∏it*) = 0.

Finally, incumbents run for the doors and potential entrants look away if their E(∏it

*) < 0 Total quantity Qt is the summation of output of all producers still in

the game. [Recall Eq (b1) above for individual firm output.] Eq (f): Qt = ∑it { Qi t-1 (Qt/Qt-1)) + ∆qit} Klepper also assumes that the derivative of expected profitability

with respect to price is positive: dE(∏*it)/dpt > 0

This indicates that as prices decrease, firms’ unit profits decline and vice versa. This relationship is important in later stages to push firms out.

18

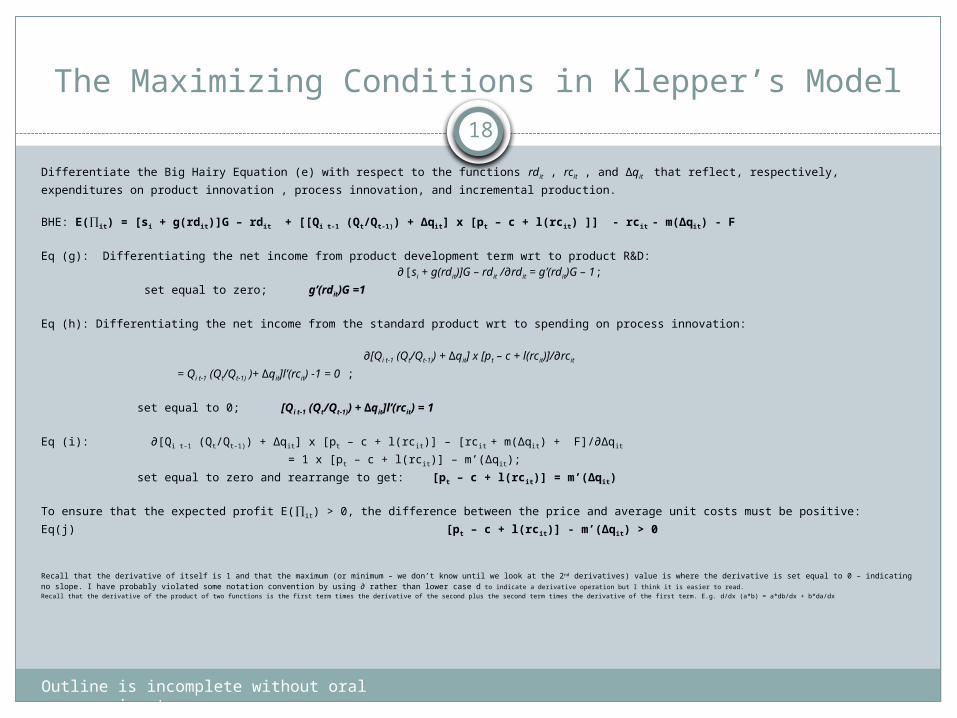

The Maximizing Conditions in Klepper’s Model

Outline is incomplete without oral accompaniment

Differentiate the Big Hairy Equation (e) with respect to the functions rdit , rcit , and ∆qit that reflect, respectively,

expenditures on product innovation , process innovation, and incremental production. BHE: E(∏it) = [si + g(rdit)]G – rdit + [[Qi t-1 (Qt/Qt-1)) + ∆qit] x [pt – c + l(rcit) ]] - rcit - m(∆qit) - F

Eq (g): Differentiating the net income from product development term wrt to product R&D: ∂[si + g(rdit)]G – rdit /∂rdit = g’(rdit)G – 1;

set equal to zero; g’(rdit)G =1

Eq (h): Differentiating the net income from the standard product wrt to spending on process innovation: ∂[Qi t-1 (Qt/Qt-1)) + ∆qit] x [pt – c + l(rcit)]/∂rcit

= Qi t-1 (Qt/Qt-1) )+ ∆qit]l’(rcit) -1 = 0 ;

set equal to 0; [Qi t-1 (Qt/Qt-1)) + ∆qit]l’(rcit) = 1

Eq (i): ∂[Qi t-1 (Qt/Qt-1)) + ∆qit] x [pt – c + l(rcit)] – [rcit + m(∆qit) + F]/∂∆qit

= 1 x [pt – c + l(rcit)] – m’(∆qit);

set equal to zero and rearrange to get: [pt – c + l(rcit)] = m’(∆qit)

To ensure that the expected profit E(∏it) > 0, the difference between the price and average unit costs must be positive:

Eq(j) [pt – c + l(rcit)] - m’(∆qit) > 0

Recall that the derivative of itself is 1 and that the maximum (or minimum – we don’t know until we look at the 2nd derivatives) value is where the derivative is set equal to 0 – indicatingno slope. I have probably violated some notation convention by using ∂ rather than lower case d to indicate a derivative operation but I think it is easier to read. Recall that the derivative of the product of two functions is the first term times the derivative of the second plus the second term times the derivative of the first term. E.g. d/dx (a*b) = a*db/dx + b*da/dx

19

Klepper’s Lemmas

Outline is incomplete without oral accompaniment

Lemma 1: for all i and t, if Eq (f) is satisfied, then rdit* = rd*

Therefore the incremental profits earned from product innovation {[si + g(rdit)]G – rdit} are constant and differ only by the value of s.

Lemma 2. For all surviving cohort members that entered in period k, rcit

* = rctk, ∆qit

*=∆qtk, Qit = Qt

k and Vit*= Vt

k. Each cohort group finds that their profit maximizing doses of ∆q, Q, and V are

identical for all members and constant over time Period t-1 Q of the standard product for all entrants in time t is 0, therefore if

the profit maximizing values of the choice variables affecting process innovation are identical in that period,

The requirement of Eq (g) that growth is proportional to industry growth and will continue to be so in subsequent periods coupled with Eq (h) which requires that the incremental investment in additional growth be equal to the net margin on additional units, means that the profit maximizing values will remain on a sort of steady state course

Vit* = [Qi t-1 (Qt/Qt-1) + ∆qit

*] x [pt – c + l(rcit*)] – [rcit

* + m(∆qit

*)] or the formula for

the profit maximizing standard product values, is introduced late as a sort of short hand

20

Klepper’s Lemmas continued

Outline is incomplete without oral accompaniment

Lemma 3. For each firm i in the market in time t, the larger its output in the previous period, Qi t-1 , then the larger rcit , ∆qit, and Vit . The intuitive explanation is that the larger the standard

product output quantity, the more units to spread the process innovation costs over and the larger the appropriable profit. Therefore the larger firm will seek to increase Q.

Lemma 4: For each firm i in the market in t and t-1; Qit > Qit-1 and rcit > rcit-1

Surviving firms experience increased output and, because process innovation is conditioned on output, increased investment in process innovation.

Outline is incomplete without oral accompaniment

21

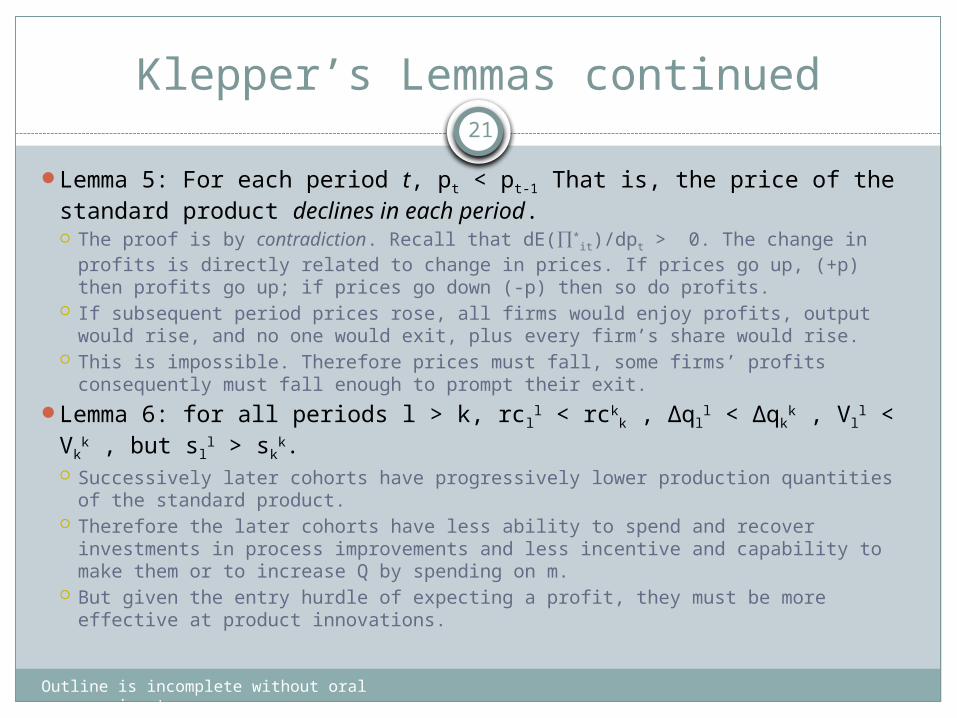

Klepper’s Lemmas continued

Lemma 5: For each period t, pt < pt-1 That is, the price of the standard product declines in each period. The proof is by contradiction. Recall that dE(∏*

it)/dpt > 0. The change in profits is directly related to change in prices. If prices go up, (+p) then profits go up; if prices go down (-p) then so do profits.

If subsequent period prices rose, all firms would enjoy profits, output would rise, and no one would exit, plus every firm’s share would rise.

This is impossible. Therefore prices must fall, some firms’ profits consequently must fall enough to prompt their exit.

Lemma 6: for all periods l > k, rcll < rck

k , ∆qll < ∆qk

k , Vll < Vk

k , but sll

> skk.

Successively later cohorts have progressively lower production quantities of the standard product.

Therefore the later cohorts have less ability to spend and recover investments in process improvements and less incentive and capability to make them or to increase Q by spending on m.

But given the entry hurdle of expecting a profit, they must be more effective at product innovations.

Outline is incomplete without oral accompaniment

22

Lemma 7: After some period, stt > smax and entry ceases.

At least some members of each entry cohort have si = smax and therefore always profit from product innovation and expand quantity and share as their distinctive product customers shift to buying the standard product from them and they grow.

This can’t go on forever, so at some point p must fall low enough to push some out and only those who are favored on the process as well as product innovation side will remain.

The threshold or entry-level s needed to be profitable then rises until it exceeds the maximum possible.

Lemma 8: In each period t, sll > sk

k for l > k . This is another consequence of the head start the earlier cohorts have in

enlarging their sales of the standard product. Since lemma 6 indicates that successive cohorts have lower levels of

spending on process innovation, market enlargement, and have a lower earning base of standard product sales, they must compensate by successively higher innovation capabilities

23

Klepper Relates Propositions to Regularities

Outline is incomplete without oral accompaniment

Proposition 1. Initially the number of entrants may rise or fall, but eventually it will fall to zero. This is essentially a restatement of lemmas 6 and 7. Firms are attracted to the growing, profitable market and see an opportunity to

exploit their product innovation skills. Eventually the threshold product innovation skill required to offset the volume

advantages of incumbents rises sufficiently to bar new entrants. Proposition 2. Initially the number of firms may rise over time but

eventually it will decline steadily. As price and hence expected unit profits decline, some less innovative firms will

exit to be replaced by more innovative but smaller entrants. Eventually the advantages enjoyed by growing incumbents become

insurmountable and entry ceases. Larger, more innovative incumbents continue to expand and gain share, pushing

out the less “fit.” This process of concentration continues until a stable balance is achieved among

a relatively few large firms.

Outline is incomplete without oral accompaniment

24

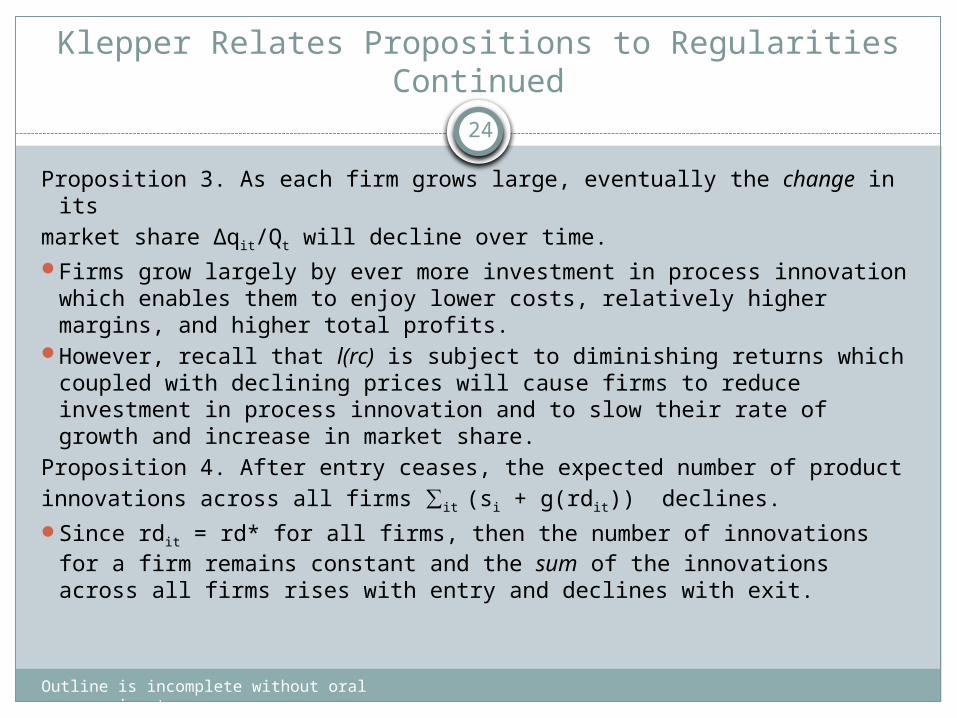

Klepper Relates Propositions to Regularities Continued

Proposition 3. As each firm grows large, eventually the change in itsmarket share ∆qit/Qt will decline over time. Firms grow largely by ever more investment in process innovation

which enables them to enjoy lower costs, relatively higher margins, and higher total profits.

However, recall that l(rc) is subject to diminishing returns which coupled with declining prices will cause firms to reduce investment in process innovation and to slow their rate of growth and increase in market share.

Proposition 4. After entry ceases, the expected number of productinnovations across all firms ∑it (si + g(rdit)) declines. Since rdit = rd* for all firms, then the number of innovations for a

firm remains constant and the sum of the innovations across all firms rises with entry and declines with exit.

Outline is incomplete without oral accompaniment

25

Klepper Relates Propositions to Regularities Continued

Proposition 4. After entry ceases, the expected number of product innovations across all firms ∑it (si + g(rdit)) declines. Since rdit = rd* for all firms, then the number of innovations for a firm remains constant

and the sum of the innovations across all firms rises with entry and declines with exit. Proposition 5. For each firm i that remains in the market in period t, the

ratio of expenditures on process innovation relative to product innovation increases steadily; rcit/rdit > rci t-1/rdi t-1. Since rd is constant over time and growth entails an increase in output of the standard

product, eventually the greater opportunity to appropriate returns on process innovation will overwhelm the returns from the fixed number of product innovations per firm.

Proposition 6. For all periods t, itk < it

l for k<l. The observation that members of younger cohorts are more skilled product innovators than older groups follows from the fact that they are smaller, receive relatively little profit from standard product sales and must compete to survive by being more product innovative.

26

Cross-sectional Implications of Keppler’s PLC Model

Outline is incomplete without oral accompaniment

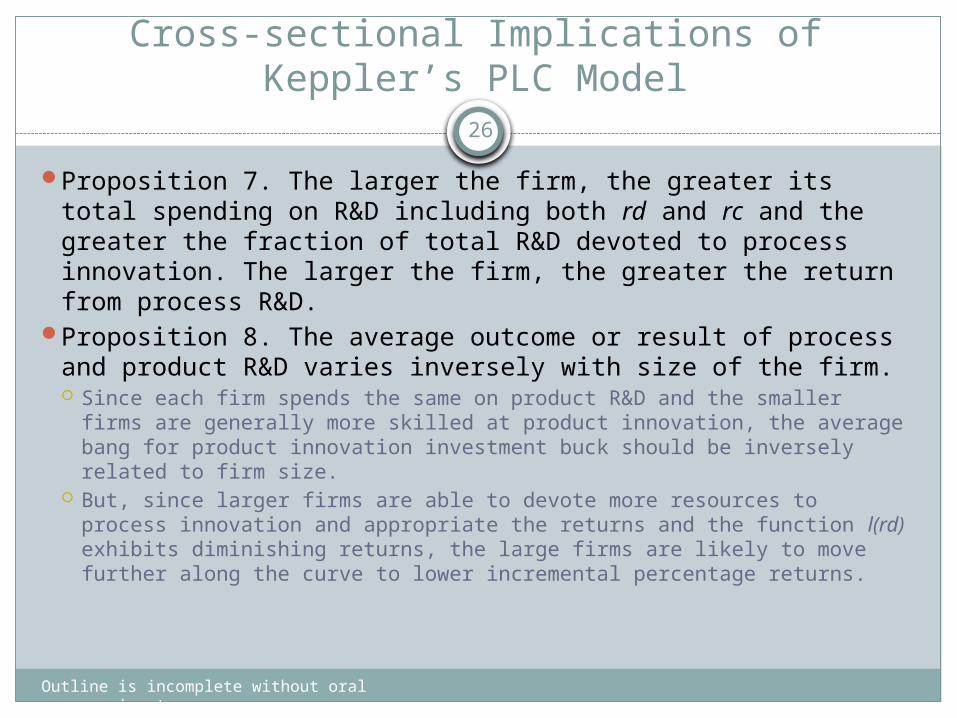

Proposition 7. The larger the firm, the greater its total spending on R&D including both rd and rc and the greater the fraction of total R&D devoted to process innovation. The larger the firm, the greater the return from process R&D.

Proposition 8. The average outcome or result of process and product R&D varies inversely with size of the firm. Since each firm spends the same on product R&D and the smaller

firms are generally more skilled at product innovation, the average bang for product innovation investment buck should be inversely related to firm size.

But, since larger firms are able to devote more resources to process innovation and appropriate the returns and the function l(rd) exhibits diminishing returns, the large firms are likely to move further along the curve to lower incremental percentage returns.

27

Cross-sectional Implications of Keppler’s PLC Model

Outline is incomplete without oral accompaniment

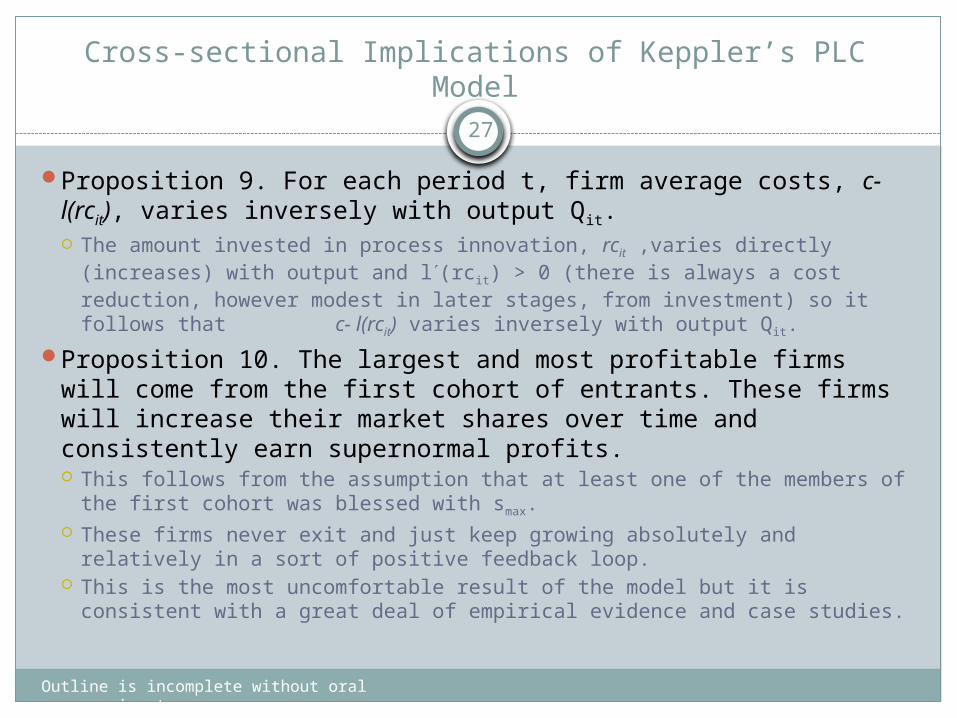

Proposition 9. For each period t, firm average costs, c-l(rcit), varies inversely with output Qit. The amount invested in process innovation, rcit ,varies directly (increases)

with output and l(rcit) > 0 (there is always a cost reduction, however modest in later stages, from investment) so it follows that c- l(rcit) varies inversely with output Qit.

Proposition 10. The largest and most profitable firms will come from the first cohort of entrants. These firms will increase their market shares over time and consistently earn supernormal profits. This follows from the assumption that at least one of the members of the first

cohort was blessed with smax. These firms never exit and just keep growing absolutely and relatively in a

sort of positive feedback loop. This is the most uncomfortable result of the model but it is consistent with a

great deal of empirical evidence and case studies.

28

Summary of Klepper’s PLC Model

Outline is incomplete without oral accompaniment

Klepper has developed a dynamic evolutionary model that produces results consistent with the empirical observations of the PLC.

Klepper’s model is elegant or simple in that it reflects two intuitively appealing notions. First, the returns and ability to appropriate returns from process innovation depends upon the

size of the firm. This is another way of saying that there are more units of output and sales over which to spread and recover the costs of process innovation.

Second, firms possess different innovation skills and levels and pursue different directions, especially in the early days of a product market.

This evolutionary approach is somewhat different than the historical explanation of how firm structures evolve. Provides insight into the birth and death of firms and the concentration of many industries. End state may also suggest why disruptive technologies are effective against settled firms.

Historically, industry characteristics were seen shaping the cost functions of the firm and establishing barriers to entry which in turn determined industry structure.

In many respects the dynamic evolutionary approach is more compatible with many “regularities” observed within and across different industries.

29

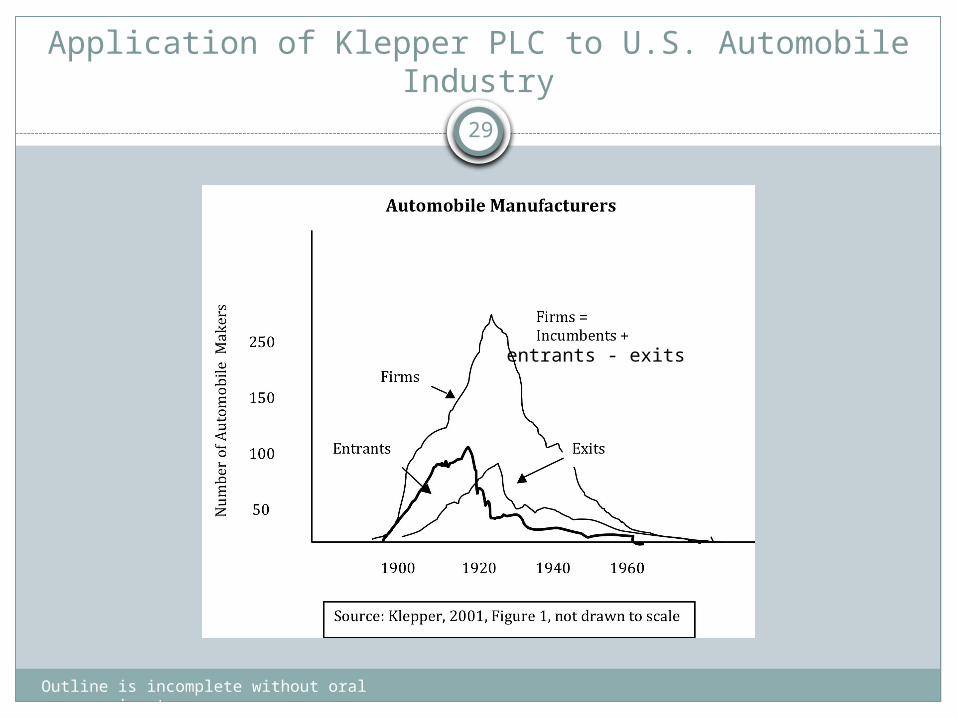

Application of Klepper PLC to U.S. Automobile Industry

Outline is incomplete without oral accompaniment

entrants - exits

30

Next Week

Outline is incomplete without oral accompaniment

Hirshleifer on relationship between internal transfer prices and market prices

Williamson (1981) describes boundaries of firm in light of contracting and governance costs