clash of the titans - nordea · clash of the titans • we recommend to keep an overweight in...

TRANSCRIPT

Global Asset Allocation Strategy

June 2019

Investments │ Wealth Management

Clash of the Titans

Clash of the

Titans• We recommend to keep an overweight in Europe. Valuation is

attractive, and investors are too pessimistic on the region.

• Japan appears cheap, but is uninspiring on all other accounts,

especially earnings, and we keep the underweight.

• Within equity sectors we underweight Industrials on the back of

weakness in the cycle, and overweight Health Care. Hence we

keep a defensive stance.

EQUITY STRATEGY: Keep overweight in Europe

FIXED INCOME STRATEGY: Keep OW in HY

• New tariffs from both US and China, a broadening of the conflict

towards export restrictions and tougher rhetoric from both

parties, in combination with too optimistic markets, led to a

pullback in May.

• On the one hand, the service sector remain strong, and the

situation for households are healthy. On the other hand, the

escalation in geopolitic friction fuels uncertainty, and leading

indicators for the industrial sector are not convincingly turning

around, pointing towards continued weakness.

• Risks have increased, and the development in the US-China

conflict is hard to predict. Keep neutral.

KEEP EQUITIES NEUTRAL

June 2019

• We recommend to keep overweight in high yield bonds. With still

low real rates supporting the economies, the carry over

government bonds is worth harvesting.

• Overall, we still expect modest returns from bonds in 2019, as

spread and yield levels are low in a historic context.

Market performance & recommendations

Markets hit by the escalation in the US-China conflict

Current allocation Previous allocation

ASSET ALLOCATION - N + Comments

Equities

Fixed Income

EQUITY REGIONS - N +

North America

Europe

Japan

Emerging Markets

Denmark

Finland

Norway

Sweden

EQUITY SECTORS - N +

Industrials

Cons Discretionary

Cons Staples

Health Care

Financials

IT

Comm. Services

Utilities

Energy

Materials

Real Estate

BOND SEGMENTS - N +

Government

Investment Grade

High Yield

Emerging MarketsSource: Thomson Reuters / Nordea

Broadly speaking, data has started to improve

Some signs of a near-term bottom in global growth

Source: Thomson Reuters / Nordea

Services doing ok, manufacturing still a worry

Source: Thomson Reuters / Nordea

• Global economic growth has started to show signs of a near-term bottom. However, there are still significant risks to the downside.

• Indeed, hard data has started to improve compared to downbeat expectations, but further market upside would need more than stabilisation short-term.

• Troublingly, trade growth continues to sag and the uncertainties there and around the euro area outlook linger.

…but the conflict raises uncertainty: German evidenceWeakness in global trade is not only about US-China conflict…

US-China conflict: Escalation creating uncertainty – watch out for 2nd round effects

Source: Thomson Reuters / Nordea Source: Thomson Reuters / Nordea

• Weak trade is not only about the US-China conflict: Other cyclical (less liquidity) and structural factors (technology, terms of trade) are at play as well.

• Rising uncertainty highlights a potential drag on growth via confidence (2nd round effects).

• We expect a “truce”, but markets are complacent regarding timing and substance. The conflict is about economic supremacy and therefore long-lasting.

Improvement in the earnings revision ratio

Stable earnings expectation, but risks to the outlook

Source: Thomson Reuters / Nordea

Stable 2019 growth expectations

Source: Thomson Reuters / Nordea

• 2019 earnings expectations are stabilizing, partly on the back of a lower base in 2018. Also, the massive downtrend in revisions have turned around.

• Many leading indicators point to weak economic growth and together with renewed trade tensions this could continue to weigh on earnings expectations.

• Tight labour markets and rising wage growth could also pressure margins going forward. In sum, increased risk to the earnings outlook.

Real yields bottoming for now, dampening risk appetite USD upside contributes to less risk friendly monetary conditions

• The market still expects one Fed cut this year and one in 2020, but the Fed signals a steady hand: potential for positive surprises (cuts) limited from here.

• Inflation expectations are falling, putting a floor under real yields. At the same time, the USD is at highs for the year and might appreciate further.

• Although medium term monetary factors are showing signs of improvement, short term this means less tailwinds from monetary factors than in Q1.

Fed’s dovish pivot priced – monetary factors provide less tailwind in the short term

Source: Thomson Reuters / Nordea Source: Thomson Reuters / Nordea

US yield curve (10Y vs 3M) has been flirting with inversion

• Slowing growth with no considerable inflation pressure made parts of the US yield curve (10Y vs 3M) to invert in H1 2019, and again during May.

• A partial inversion raises concerns, but it is important to look at other information in the economy before using this measure as a predictor of recession.

• Recession or not, a flat curve is a headwind for the economy, challenging banking business. NB: Yield curves are more than signals, they drive the cycle.

The yield curve: Signaling recession or not?

Source: Thomson Reuters / Nordea Source: Thomson Reuters / Nordea

8

Can Fed rate cuts extend the cycle? 2-10s says yes, 3M-10s no

This material was prepared by Investments |

Tensions in the Middle east pose a risk to the oil priceWeaker sterling as risk of a harder Brexit has increased

May’s departure amplifies Brexit uncertainty

Source: Thomson Reuters / Nordea Source: Thomson Reuters / Nordea

• Prime minister May will quit as Conservative party leader on June 7th, and the leading contenders to succeed her all want a tougher Brexit deal.

• May’s departure amplifies the uncertainty around Brexit, and the chance of a no deal seems to have risen, but the Parliament ultimately decides.

• Renewed tensions between US and Iran, and fear of supply disruption also in Libya and Venezuela, is making the outlook for oil cloudy.

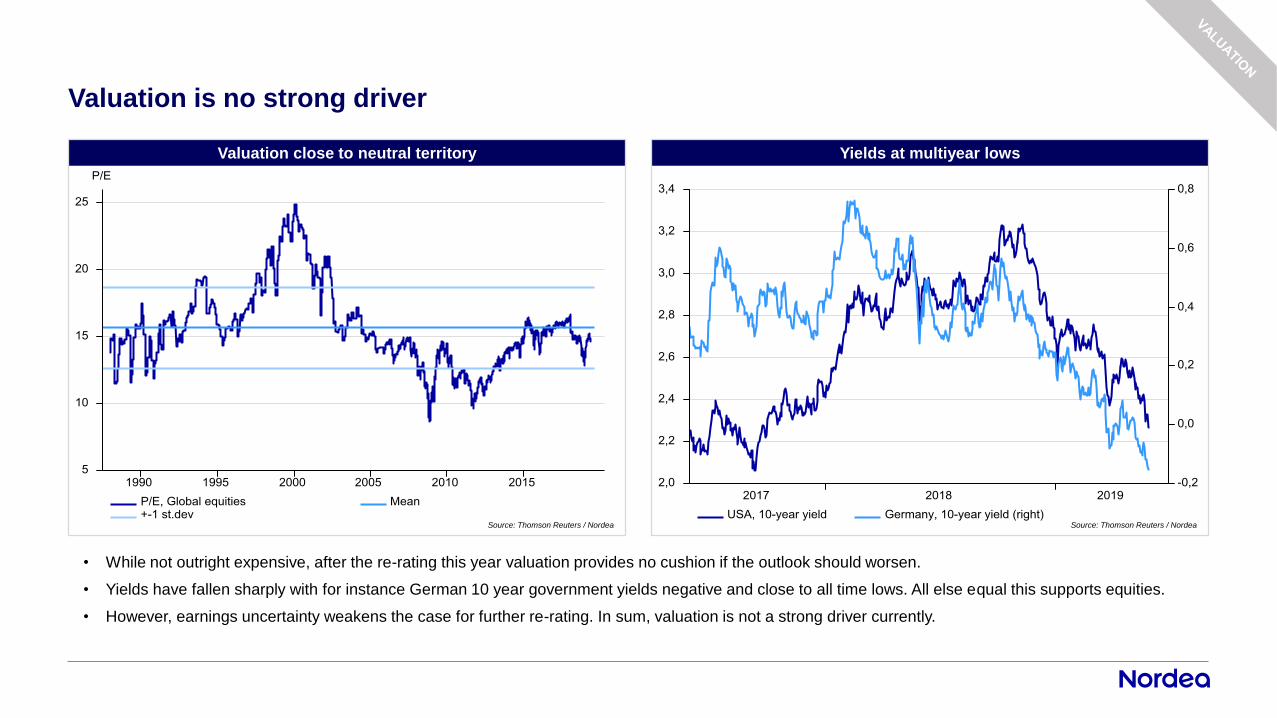

Valuation is no strong driver

Yields at multiyear lows

Source: Thomson Reuters / Nordea Source: Thomson Reuters / Nordea

Valuation close to neutral territory

• While not outright expensive, after the re-rating this year valuation provides no cushion if the outlook should worsen.

• Yields have fallen sharply with for instance German 10 year government yields negative and close to all time lows. All else equal this supports equities.

• However, earnings uncertainty weakens the case for further re-rating. In sum, valuation is not a strong driver currently.

Marked reaction from investors in a bearish directionSudden spikes in volatility seems to be a new trend

Trade worries hit an already fragile sentiment

Source: Thomson Reuters / Nordea Source: Thomson Reuters / Nordea

• Mid-May proved to be yet another wake-up call for markets. A tweet from Trump can obviously have an impact if sentiment levels are stretched.

• With the pullback, sentiment are now at more healthy levels, and technical indicators are not as stretched anymore.

• However, equity flows continue to disappoint and investors seems a bit reluctant. Overall, sentiment is more balanced, but politics linger as a negative.

Yield and spread on high-yield bonds have been decreasingMore attractive yields only found in risky bonds

• Central banks have put monetary tightening on hold. This has supported bonds, and creates a decent environment for credits going forward.

• The economic growth outlook is moderate, but that should be enough for corporates to service their debt obligations and keep default rates low for now.

• We favor high-yield bonds in our recommendations and keep government bonds underweight. The yield on German bonds is close to historic lows.

Seeking returns in high-yield

Source: Thomson Reuters Source: Thomson Reuters

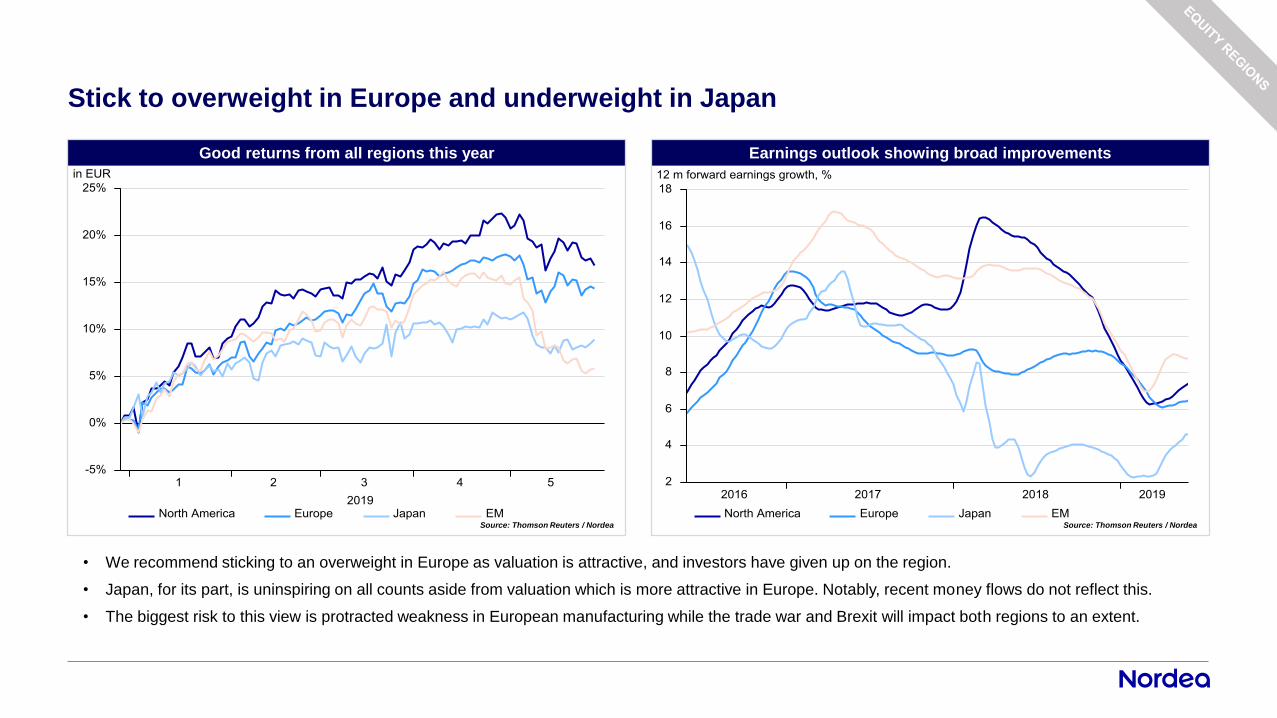

Earnings outlook showing broad improvements

Stick to overweight in Europe and underweight in Japan

Source: Thomson Reuters / Nordea

Good returns from all regions this year

Source: Thomson Reuters / Nordea

• We recommend sticking to an overweight in Europe as valuation is attractive, and investors have given up on the region.

• Japan, for its part, is uninspiring on all counts aside from valuation which is more attractive in Europe. Notably, recent money flows do not reflect this.

• The biggest risk to this view is protracted weakness in European manufacturing while the trade war and Brexit will impact both regions to an extent.

Nordea Global Asset Allocation Strategy Contributors

Strategists

Andreas Østerheden

Senior Strategist

Denmark

Sebastian Källman

Strategist

Sweden

Ville Korhonen

Fixed Income Strategist

Finland

Espen R. Werenskjold

Senior Strategist

Norway

Hertta Alava

Senior Strategist

Finland

Assistants

Victor Karlshoj Julegaard

Assistant/Student

Denmark

Mick Biehl

Assistant/Student

Denmark

Amelia Marie Asp

Assistant/Student

Denmark

Frederik Saul

Assistant/Student

Denmark

Global Investment Strategy

Committee (GISC)

Michael Livijn

Chief Investment Strategist

[email protected] Sweden

Antti Saari

Chief Investment Strategist

Finland

Witold Bahrke

Chief Investment Strategist

Denmark

Sigrid Wilter Slørstad

Chief Investment Strategist

Norway

Kjetil Høyland

Chief Investments Strategist

Norway

DISCLAIMER

Nordea Investment Center gives advice to private customers and small and medium-sized companies in Nordea regarding investment strategy and concrete

generic investment proposals. The advice includes allocation of the customers’ assets as well as concrete investments in national, Nordic and international

equities and bonds and in similar securities. To provide the best possible advice we have gathered all our competences within analysis and strategy in one

unit - Nordea Investment Center (hereafter “IC”).

This publication or report originates from: Nordea Bank Abp, Nordea Bank Abp, filial i Sverige, Nordea Bank Abp, filial i Norge and Nordea Danmark, Filial af

Nordea Bank Abp, Finland (together the “Group Companies”), acting through their unit Nordea IC. Nordea units are supervised by the Finnish Financial

Supervisory Authority (Finanssivalvonta) and each Nordea unit’s national financial supervisory authority.

The publication or report is intended only to provide general and preliminary information to investors and shall not be construed as the sole basis for an

investment decision. This publication or report has been prepared by IC as general information for private use of investors to whom the publication or report

has been distributed, but it is not intended as a personal recommendation of particular financial instruments or strategies and thus it does not provide

individually tailored investment advice, and does not take into account your particular financial situation, existing holdings or liabilities, investment knowledge

and experience, investment objective and horizon or risk profile and preferences. The investor must particularly ensure the suitability of his/her investment as

regards his/her financial and fiscal situation and investment objectives. The investor bears all the risks of losses in connection with an investment.

Before acting on any information in this publication or report, it is recommendable to consult one’s financial advisor. The information contained in this report

does not constitute advice on the tax consequences of making any particular investment decision. Each investor shall make his/her own appraisal of the tax

and other financial advantages and disadvantages of his/her investment.

Ansvarsreservation