city of jacksonville city council agenda … of jacksonville city council agenda . ... sherbourne...

TRANSCRIPT

Please let the City offices know if you will need any special accommodations to attend or participate in the meeting by calling (541) 899-1231.

CITY OF JACKSONVILLE CITY COUNCIL AGENDA

OLD CITY HALL, 205 W Main St

CITY COUNCIL June 19, 2012

REGULAR SESSION 6:00 pm

1) CALL TO ORDER 2) a. MINUTES (June 5, 2012)

b. BILLS LIST

3) PUBLIC COMMENT (items not on the agenda) 4) ACTION / DISCUSSION ITEMS

(The public will be allowed to speak, one time, to any item during the action/discussion items. In order to speak you must sign in with the Recorder under the item for which you wish to speak)

a. IGA Jackson County IT services for Police Dept - Chief Towe b. GSI contract for water management c. Water Bond Post Issuance Policy d. Tentative year-end council meeting date and time to pay bills. (June 27, 4 pm) 5) COUNCIL DISCUSSION a. Mayor and council committee reports b. Staff reports Jeff Alvis - Devin Hull - Amy Stevenson - Stacey McNichols 6) ADJOURN

Jacksonville City Council, City of Jacksonville, Oregon City Council Meeting Minutes June 5, 2012

1

Transcribed by: Jan Garcia

REGULAR CITY COUNCIL MEETING June 5, 2012 at Old City Hall, 205 W Main St, Jacksonville

1. CALL TO ORDER (includes call to order, pledge of allegiance) 6:00 pm Present are Councilors Schatz, Jesser, Winterburn, Duane and Lewis and Mayor Becker; absent is Councilor Hayes. Staff members present are City Administrator Jeff Alvis, Treasurer Stacey McNichols, and Recorder, Jan Garcia, Planner Amy Stevenson and Fire Chief Devin Hull. 2. MINUTES / BILLS a. Minutes – May 15, 2012 Move to: Approve the minutes as presented Motion by: Councilor Duane was seconded Ayes – Unanimous b. Bills Move to: Approve the bills as submitted Motion by: Councilor Winterburn was seconded Roll call vote – Unanimous 3. PUBLIC COMMENT (items not on the agenda) No one spoke 4. ACTION / DISCUSSION ITEMS a. Evelyn Kinsella, RVCOG report on Food and Friends Ms. Kinsella gave an update on the numbers of seniors served in the Jacksonville community. It was noted that there were quite a few seniors in their home that were 80+ and 90+ years old. She thanked the Council for their financial support and stated that there was a large volunteer base for home deliveries especially. b. Scott Sherbourne CityCounty Insurance Representative - give risk assessment overview for the City. Sherbourne showed the trends the city has for loss in property and worker’s compensation areas over the past few years for the city. He states that the City is doing an excellent job managing the loss areas. Sherbourne explains to the Council that the event packet usage is being driven by the insurance market and the risk factors. Council Jesser asks if it is really necessary to have ‘multiple layers’ of documentation. Sherbourne states that it is from his insurance perspective. He confirmed that defraying liability by gathering increased information such as lists of vendors, OLCC licenses, certificates of insurance and business licenses will help to protect the risk to the city. Sherbourne will work with the staff to create appropriate event packets. c. Follow up on business license study session - City Council to give final direction to create policy.

This Final Action Agenda/Minutes is supplemented by electronic recordings of the meeting, which may be reviewed upon request to the City Recorder. A written copy of the City Council Meeting Action Minutes can be reviewed on-line at http://www. jacksonvilleor.us

Jacksonville City Council, City of Jacksonville, Oregon City Council Meeting Minutes June 5, 2012

2

Transcribed by: Jan Garcia

Administrator, Jeff Alvis states that the study session went well regarding business licenses and event packets. He requests that staff would be allowed to move forward with the creation of a policy to put in place until the code is codified in 2012-2013.

Move to: authorize staff to move ahead to create a policy for business licenses and events.

Motion by: Councilor Schatz was seconded Ayes – Unanimous

d. PUBLIC HEARING For the purpose of adopting the budget for the fiscal year 2012-13

Public Hearing was opened at 6:50 pm. Treasurer, Stacey McNichols explains the changes to the budget since approval by the Budget Committee in May. They are as follows: Gen 2-10, line 54 Utilities (planning department) to allow for a phone line to use for voice mail. Gen 2-11, line 96

Archiving and Codification was increased by $3,000 to allow for the substantial code changes that will be taking place this coming fiscal year. Parks 2-25, line 48 Marketing fund roll-over amount for the Transient Lodging Tax was firmed up now that there will be no other withdrawals from the fund this fiscal year. His 29, line 21 An additional $20,000 was set aside for code revision.

There was no public comment regarding the budget. PUBLIC HEARING was closed 6:55 pm. Move to: approve the budget as amended Motion by: Councilor Jesser was seconded. Roll Call vote: Ayes - unanimous

(Urban Renewal meeting was opened at 6:55 pm and closed at 6:59 pm at which time the Council meeting resumed.) Urban Renewal meeting minutes are recorded separately. e. Chief Hull report on the May 5 city-wide disaster drill. Fire Chief Devin Hull gave a detailed description of the city-wide disaster drill that took place on May 5, 2012. He detailed the wild land fire scenario, the updating of the EOP, evacuation of a neighborhood, community involvement by citizens along with two local churches, Map Your Neighborhood programs along with Ready Books. Calvary Church was staged for medical evacuation and Jacksonville Presbyterian Church was staged for general evacuation and food and shelter. It was noted that the current EOC within the police office was not of an adequate size to run a disaster out of. There was also mention of the debriefing that took place earlier that week with the key players in the event talking about what was learned and how to improve the event for the future. Hull’s information was well received and appreciated by the Council and those in the audience.

Jacksonville City Council, City of Jacksonville, Oregon City Council Meeting Minutes June 5, 2012

3

Transcribed by: Jan Garcia

f. Report on the 4th of July picnic Mayor Becker states that the planning for the picnic is moving forward. He states the picnic will be open to the surrounding communities also. He states a banner will be placed over California St reminding people of the picnic.

5. ORDINANCES AND RESOLUTIONS

a. RES 1090: A resolution adopting the budget for the City of Jacksonville for the fiscal year commencing July 1, 2012, making appropriations, imposing tax and categorizing the tax. .

Move to: approve Motion by: Councilor Duane was seconded Ayes – Unanimous b. RES 1091: A resolution extending City of Jacksonville Worker’s Compensation coverage to volunteers Move to: approve Motion by: Councilor Lewis was seconded Ayes – Unanimous c. RES 1092: A resolution certifying that the City of Jacksonville provides four or more municipal services to be eligible to receive state shared revenue. Move to: approve Motion by: Councilor Jesser was seconded Ayes – Unanimous d. RES 1093: A resolution declaring the city’s election to receive state revenues Move to: approve Motion by: Councilor Lewis was seconded Ayes – Unanimous e. RES 1094: A resolution setting new fees for administration and/or public works amending RES 1076. Move to: approve Motion by: Councilor Duane was seconded Ayes – Unanimous An emergency item was requested to be placed on the agenda for Urban Renewal. Councilor Jesser reopened the Urban Renewal meeting at 7:25 pm. Motion to add the emergency item to the agenda was approved unanimously. RES 12-001: A resolution adopting the Urban Renewal budget for the Jacksonville Urban Renewal district for the fiscal year commencing July 1, 2012, making appropriations and declaring tax increment. Move to: approve Motion by: Mayor Becker was seconded

Jacksonville City Council, City of Jacksonville, Oregon City Council Meeting Minutes June 5, 2012

4

Transcribed by: Jan Garcia

Ayes – Unanimous Urban Renewal meeting was adjourned at 7:26 pm. 6. Council Discussion a. Mayor and Council Committee reports Councilor Schatz states the next Parks Committee meeting is June 20 at 3 pm. Councilor Jesser states that the most recent Parking Commission meeting did not have a quorum and that a new meeting time will be set soon. The Planning Commission has set their rules for operation and had a study session regarding Roberts Rules. Jesser attended the debriefing after the disaster training and states that he sees an urgent need for policy and procedure books to be created so that in case of a disaster that keeps staff from making it into work there would be directions for volunteers who might have to step in. Councilor Hayes was absent. Councilor Duane asked Alvis if there was any word regarding BLM land that might be used by the city in association with the MRA land swap. She states that HARC is discussing the use of fonts on signs. Duane also stated that an HPF grant was awarded on a project that had been in question as a recipient due to the timing of the completion of the project. Councilor Winterburn states that none of his committees met. He states that he went to the Bandon Community Center and stated that their petting zoo was a huge draw. Councilor Lewis stated that the Timber Mountain people had another meeting from 11- approximately 5 pm. He states he believes one more meeting will be held. Jeff Alvis states MRA project continues to move forward. He states that the lot line adjustment has been finished and is being recorded this week and the appraisal is ready to start and the bio survey is on track. Mayor Becker was in Florida for 2 weeks and noted that that the cemetery in that area was a tourist draw. 7. ADJOURN 7:33 pm

Mayor, Paul Becker Jan Garcia, City Recorder Date approved:

Vendor Name Description Amount

ALSCO JANITORIAL SUPPLIES 8.50 BAXTER OFFICE PRODUCTS DIVIDER SHELF FOR PLANNING 89.98 CNA SURETY BOND POLICY FOR EMPLOYEES 139.40 DATA CENTER WEST OFF SITE BACK UP & OCH DSL 181.22 DONNA MCNURLEN CLEANING SERVICES JUNE 2012 660.00 JACKSONVILLE LUMBER COMPANY SUPPLIES FOR PLANNING DEPT 4.90 JUDY'S CENTRAL POINT FLORIST FLOWERS FOR CLARA WENDT 75.00 MAIL TRIBUNE NOTICE OF BUDGET HEARING 2,143.98 OREGON DEPARTMENT OF REVENUE TRAFFIC FINE ASSMTS MAY 2012 780.00 STAPLES BUSINESS ADVANTAGE FIRE PROOF FILE CAB - ARCHIVE RM 2,248.95

6,331.93

Vendor Name Description Amount

ALSCO JANITORIAL SUPPLIES 109.85 ALSCO JANITORIAL SUPPLIES 109.85 ALSCO JANITORIAL SUPPLIES 219.71 BEAVER TREE SERVICE, INC. TREE REMOVAL 655 E CALIFORNIA 1,700.00 BLACKBIRD SUPPLIES FOR CEMETERY 33.44 BLACKBIRD SUPPLIES FOR STREETS DEPT 26.99 DAY WIRELESS SYSTEMS PA SYSTEM FOR TROLLEY 1,687.83 FERGUSON WATERWORKS SUPPLIES FOR WATER DEPT 565.16 GLIDDEN PROFESSIONAL PAINT CENTERS SUPPLIES FOR STREETS DEPT 92.70 GRANGE CO-OP BACKPACK SPRAYER 199.98 GROUNDED ELECTRICAL CONTRACTING REPLACE LIGHT POST 210.50 GROUNDED ELECTRICAL CONTRACTING REPAIR LIGHTS BRITT / RTP GRANT 463.00 GROVER ELECTRIC AND PLUMBING SUPPLIES FOR CEMETERY 4.35 GROVER ELECTRIC AND PLUMBING SUPPLIES FOR PARKS 9.29 HILTON FUEL & SUPPLY CO. GRANITE/TOP SOIL -BRITT - RTP 308.00 JACKSONIVLLE LUMBER COMPANY SUPPLIES FOR STREETS DEPT 26.25 JACKSONVILLE LUMBER COMPANY SUPPLIES FOR CEMETERY 5.85 JACKSONVILLE LUMBER COMPANY SUPPLIES FOR PARKS 44.00 JACKSONVILLE LUMBER COMPANY SUPPIES FOR PARKS 50.00 JACKSONVILLE LUMBER COMPANY SUPPLIES -FOREST PARK GRANT 261.80 KAS & ASSOCIATES, INC SOUTH OREGON ST / SCA 2,459.50 LEAGUE OF OREGON CITIES DIFF CONVERSATION CONF.-JAN 150.00 LEAVE YOUR MARK, LLC STONE FOR BRITT/RTP GRANT 338.27 LES SCHWAB SUPPLIES FOR STREET EQUIP 1.32 MEDFORD TOOLS & SUPPLY INC. SUPPLIES FOR CEMETERY 14.90 N.W. FOREST RESOURCES MANAGEMENT LOCATING PROP LINE OF TREES 125.00 NEILSON RESEARCH CORPORATION ROUTINE WATER TESTING 73.50 ONE CALL CONCEPTS, INC. WATER LOCATE TICKETS 43.56 PXX PUBLIC WORKS MANAGEMENT, INC. CITIES WATER COALITION 529.50 RODDA PAINT SUPPLIES FOR STREETS DEPT 50.04 UNITED RENTALS SUPPLIES FOR STREETS DEPT 307.05 VALLEY WEB PRINTING MONTHLY WATER BILLING 127.50

10,348.69

Vendor Name Description Amount

KAS & ASSOCIATES, INC LEGAL DESCR. /MRA LAND SWAP 557.50

557.50

Vendor Name Description Amount

BLACKBIRD SUPPLIES FOR POLICE DEPT 7.98 CENTRAL POINT CLEANERS UNIFORM CLEANING 19.80 CITY OF MEDFORD FINANCE DEPT FUEL FOR PD MAY 2012 1,451.72 DICKS WRECKER SERVICE TOWING FOR POLICE DEPT 90.00 LEAGUE OF OREGON CITIES GOVT ETHICS TRAINING 115.00

1,684.50

CITY OF JACKSONVILLE

Bills Against the City - City Council

June 19, 2012

GENERAL FUND - ADMINISTRATION DEPARTMENT

GENERAL FUND - POLICE

PARKS & FACILITIES MANAGEMENT DEPARTMENT FUNDS

SDC FUND

V:\Bills, Utilities, Payroll Payments\FY 2011-2012 PAYMENTS\Council Bills\June 2012\Per 12- June 19, 2012 Bills List.xls 1 of 2

Vendor Name Description Amount

Vendor Name Description Amount

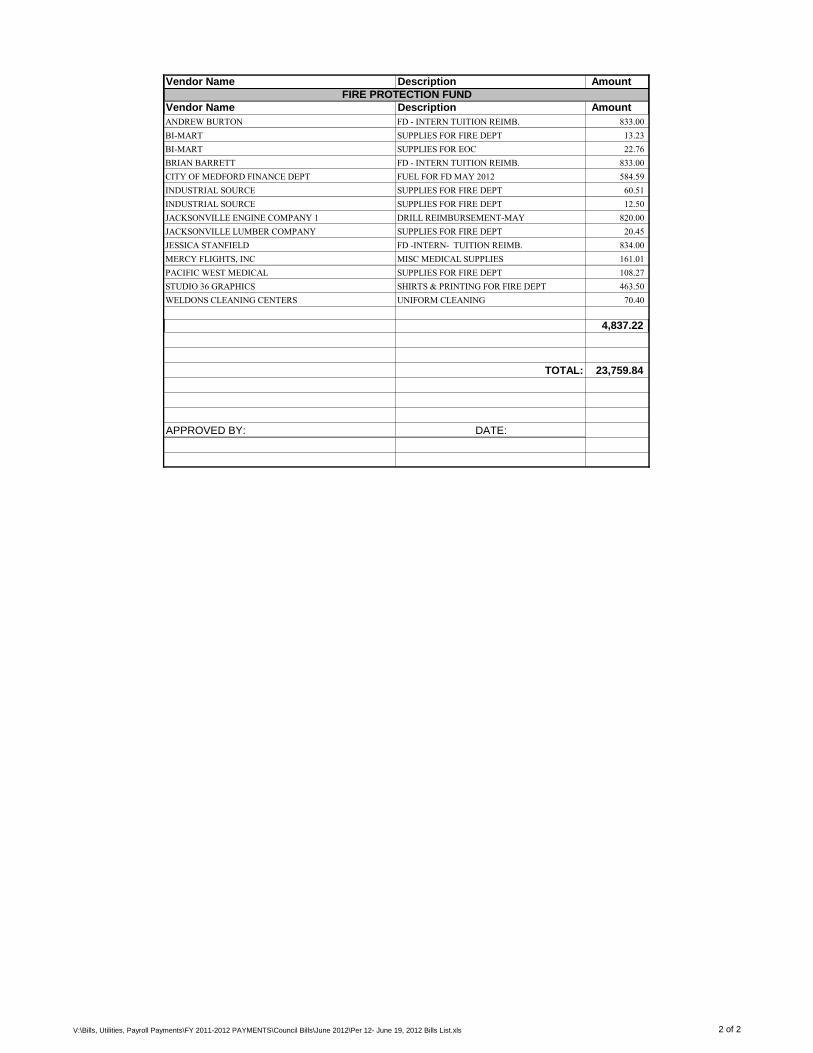

ANDREW BURTON FD - INTERN TUITION REIMB. 833.00 BI-MART SUPPLIES FOR FIRE DEPT 13.23 BI-MART SUPPLIES FOR EOC 22.76 BRIAN BARRETT FD - INTERN TUITION REIMB. 833.00 CITY OF MEDFORD FINANCE DEPT FUEL FOR FD MAY 2012 584.59 INDUSTRIAL SOURCE SUPPLIES FOR FIRE DEPT 60.51 INDUSTRIAL SOURCE SUPPLIES FOR FIRE DEPT 12.50 JACKSONVILLE ENGINE COMPANY 1 DRILL REIMBURSEMENT-MAY 820.00 JACKSONVILLE LUMBER COMPANY SUPPLIES FOR FIRE DEPT 20.45 JESSICA STANFIELD FD -INTERN- TUITION REIMB. 834.00 MERCY FLIGHTS, INC MISC MEDICAL SUPPLIES 161.01 PACIFIC WEST MEDICAL SUPPLIES FOR FIRE DEPT 108.27 STUDIO 36 GRAPHICS SHIRTS & PRINTING FOR FIRE DEPT 463.50 WELDONS CLEANING CENTERS UNIFORM CLEANING 70.40

4,837.22

TOTAL: 23,759.84

APPROVED BY: DATE:

FIRE PROTECTION FUND

V:\Bills, Utilities, Payroll Payments\FY 2011-2012 PAYMENTS\Council Bills\June 2012\Per 12- June 19, 2012 Bills List.xls 2 of 2

CITY OF JACKSONVILLE JACKSON COUNTY, OREGON

BOND POST-ISSUANCE COMPLIANCE PROCEDURES

PROCEDURE This Procedure establishes the requirements and procedures for ensuring compliance with federal laws relating to the issuance and post-issuance monitoring of tax-exempt bonds and taxable Direct Pay Bonds. RESPONSIBILITIES This Procedure statement represents the objectives of City of Jacksonville, Jackson County, Oregon (the “City”) and will be adhered to by all employees, officials, and financial representatives affiliated with the City. The City shall comply with all federal tax laws related to tax-exempt bonds, Direct Pay bonds, and bond financed facilities prior to and after issuance. The City shall monitor the requirements of section 148. The City Administrator is assigned the primary responsibility to monitor compliance with federal tax requirements for the City’s bond programs. The City Administrator may assign staff responsibility for certain components of this Procedure. GUIDELINES 1. Bond Issuances

With respect to all bond issues, the City Treasurer shall monitor and control the receipt, investment, expenditure and use of all bond proceeds and will take or omit to take any actions to cause interest on tax-exempt bonds to remain excludable from the gross income of bondholders. (United States Internal Revenue Code (the “Code”), §103 and 141 through 150). 2. Direct Pay Bond Issuances

As part of the American Recovery and Reinvestment Act of 2009 (the “Recovery Act”), Congress added §54AA and 6431 to the Code, which permits the City to obtain certain tax advantages when issuing taxable obligations for capital projects that meet certain requirements of the Code and Treasury regulations. Such bonds are referred to as “Direct Pay Bonds (DPB’s).”

A. DPB’s election - upon issuance, the City of Jacksonville will make the irrevocable election to have the special rule for qualified bonds apply. Interest on qualified DPB’s is included in bond holder’s gross income for federal income tax purposes and owners of the bonds will not receive any tax credits as a result of ownership.

B. Investor information – representatives of the City, including its financial advisors,

if any, will not make statements to investors or other interested parties that imply any tax credits or income exclusions will apply.

C. Available Project Proceeds – 100% of available project proceeds must be used

only for capital expenditures. Available project proceeds are the proceeds the City receives from the bonds minus proceeds it is allowed to spend on costs of issuance, minus proceeds allowed to fund a reasonably required reserve (up to 10%), if allowed under the Code and Treasury regulations, plus earnings from investments.

D. 2% Cost of Issuance limitation – the City, through our financial advisors, will

ensure the financed portion of costs to issue the bonds do not exceed 2% of the proceeds of the sale.

E. De minimis premium - the City, with the guidance of financial advisors and

underwriters, will ensure that no maturities are issued with more than the de minimis amount of premium as required by §54AA(d)(2)(C).

F. Secondary market trading - the City, through our financial advisors, will review

secondary market trading activity for Direct Pay bonds for the period between the sale date and the delivery date (date of issue) to determine if any of the bonds traded at a price greater than the issue price.

G. Timely expenditure – expenditure of bond proceeds shall be reviewed by the City

no less than annually, to ensure (a) proceeds are spent for the purpose stated in the authorizing resolution and as described in the tax documents and (b) proceeds, together with investment earnings on such proceeds, are spent within the timeframes described in the Tax Documents.

3. Private Activity Limitation Section 141 of the Code sets forth private activity tests for the purpose of limiting the volume of tax-exempt bonds that finance activities of persons other than state and local governmental entities. These tests serve to identify arrangements that actually or reasonably expect to transfer the benefits of tax-exempt financing to non-governmental persons, including the federal government. Following the issuance of bonds for the financing of property, the City of Jacksonville shall provide to the users of the property a copy of this Compliance Procedure and other appropriate written guidance advising that:

A. “Private business use” means use by any person other than the City, including

business corporations, partnerships, limited liability companies, associations, non-profit corporations, natural persons engaged in trade or business activity, and the United States of America and any federal agency, as a result of ownership of the property or use of the property under a lease, management or service contract (except for certain “qualified” management or service contracts), “naming rights” contract, “public-private partnership” arrangement, or any similar use arrangement that provides special legal entitlements for the use of the bond finance property;

B. No more that 10% of the proceeds of any tax-exempt bond issue (including the

property financed with the bonds) may be used for private business use, of which no more than 5% of the proceeds of the tax-exempt bond issue (including the property financed with the bonds) may be used for any “unrelated” private business use – that is, generally, a private business use that is not functionally related to the government’s purposes of the bonds; and no more that the lesser of $5,000,000 or 5% of the proceeds of a tax-exempt bond issue may be used to make or finance a loan to any person other than a state or local government unit;

C. Before entering into any special use arrangement with a non-governmental person

that involves the use of bond financed property, the user must consult with the City of Jacksonville, provide the City of Jacksonville with a description of the proposed non-governmental use arrangement, and determine whether that use arrangement, if put into effect, will be consistent with the restrictions on private business use of the bond financed property;

D. In connection with the evaluation of any proposed non-governmental use

arrangement, the City of Jacksonville will consult with bond counsel to obtain federal tax advice in whether that use arrangement, if put into effect, will be consistent with the restrictions on private business use of the bond financed property, and, if not, whether any “remedial action” permitted under §141 of the Code and applicable regulations may be taken as means of enabling that use arrangement to be put into effect without adversely affecting the tax-exempt status of the bonds.

4. Information Filing and Monitoring

At the time of issuance and throughout the bond life, issuers of governmental bonds must comply with certain information filing requirements under §149(e) of the Code:

A. Tax-exempt bonds: IRS Form 8038-G (Information Return for Tax-Exempt Governmental Obligations) must be filed by the 15th day of the second calendar month following the quarter in which the bonds were issued. For example, the due date of Form 8038-G for bonds issued on February 15th is May 15th.

B. Direct Pay (DPB’s) bonds: IRS Form 8038-B (Information Return for Build America

Bonds) or Form 8038-TC (Information Return for Tax Credit Bonds), as applicable, must be filed by the 15th day of the second calendar month following the quarter in which the bonds were issued.

C. The City Treasurer works with the City’s bond counsel to complete and file each

applicable Form 8038-G, 8038-B 8038-TC or other required form by the required due date after each bond issue.

D. Refundable Credit on Direct Pay (DPB’s) bonds: IRS Form 8038-CP (Return for

Credit Payment for Qualified Bonds) must be filed no later than 45 days before the related interest payment date, but no earlier than 90 days before the payment date. The City Treasurer will verify bond interest payable semi-annually 90 days before debt service payments are due and determine the refundable credit allowed for the interest portion of the payment. Federal rebates are payable only to the City and will be credited to the related debt service fund.

E. IRS Form 8038-T (Arbitrage Rebate, Yield Reduction and Penalty in Lieu of

Arbitrage Rebate) must be filed within 60 days after each five year period reporting deadline or within 60 days after the debt is retired, if arbitrage rebate applies (See Section 5).

5. Arbitrage Rebate

Tax-exempt obligations and DPBs provide a less expensive means of financing than other conventional approaches, resulting in a significant interest savings benefit. The federal government has imposed a variety of rules to restrict the use of tax-exempt financing and DPBs to prevent potential abuse. It is the City's Procedure to minimize the cost of arbitrage rebate and yield restriction while strictly complying with the law.

A. Definition of “arbitrage” – the ability to obtain tax-exempt and DPB proceeds and invest those funds in higher yielding securities, resulting in a profit to the issuer. Arbitrage is the difference (profit) earned.

B. Timeline – an arbitrage rebate installment payment is required to be paid no later than 60 days after the end of every 5th bond year throughout the term of a bond issue and within 60 days of retirement of the bonds.

C. Exceptions – there are exceptions to the general rebate requirements applicable to

government bond proceeds: the most common being the small issuer exception and spending exceptions. The City of Jacksonville shall consult with the City’s bond counsel to determine if any exceptions to rebate apply.

D. Monitoring – the City Treasurer will monitor ongoing compliance with regards to

arbitrage liabilities and will monitor expenditures prior to semi-annual target dates for six-month, 18-month, or 24 month spending exceptions.

E. “Bona fide” debt service funds – when possible, debt service funds will be accounted

for and funded to achieve a proper matching of revenues with principal and interest payments within each bond year so the earnings are exempt from arbitrage.

F. Schedule – the City Treasurer will maintain a schedule of each bond issue and the 5th

bond year. The City Treasurer reviews the schedule no less than annually to determine when a 5th bond year is approaching. Arbitrage rebate calculations on outstanding bond issues may be performed as often as annually or in alternating years, but never longer than the 5th year.

G. Calculations – the City has the option to perform arbitrage calculations internally or

to contract with a 3rd party provider for arbitrage rebate calculations and preparation of IRS Form 8038-T (Arbitrage Rebate, Yield Reduction and Penalty in Lieu of Arbitrage Rebate). 3rd party providers shall be requested to maintain a list of our bond issues and scheduled 5th anniversary bond years.

H. Procedures – the City will either complete the calculations internally or provide a 3rd

party provider with copies of all applicable records 30 to 60 days before the reporting deadline for the 3rd party provider to prepare the arbitrage calculations and submit a report and IRS Form 8038-T, if applicable, to the City.

I. Yield Restriction – The City Treasurer will monitor ongoing compliance with regards

to yield restriction. Interim arbitrage calculations will be used to evaluate investment strategies or optional elections that may reduce future rebate liabilities.

J. Payment – if positive arbitrage exists at the end of a 5th year bond period, the City

will prepare payment to submit with IRS Form 8038-T. Payment must equal at least 90% of the amount due as of the end of that 5th bond year.

K. Redemption – upon redemption of a bond issue, a payment of 100% of the amount

due must be paid no later than 60 days after the discharge date. L. Advance Refunding Escrows – State and Local Government Securities (SLGs) are

commonly used for refunding escrows to yield restrict the investments. The City works with its financial advisor to ensure SLGS for a refunding escrow account meet the yield restriction requirement.

6. Records Retention

A. This Procedure supersedes any other general document retention Procedure with

respect to the retention of documents related to bonds and bond financed facilities.

B. The City shall maintain all material records and information necessary to support a municipal bond issue’s compliance with §103 of the Code.

C. All records should be kept in a manner that ensures their complete access for so long

as they are material. Electronic media is the preferred method for storage of all documents required under this Procedure directive.

D. Except as stated in E. below, material records should generally be kept for as long as

the bonds are outstanding, plus 3 years after the final redemption date of the bonds. E. For certain federal tax purposes, a refunding bond issue is treated as replacing the

original new money issue. To this end, the tax-exempt status of a refunding issue is dependent upon the tax-exempt status of the refunded bonds. Thus, certain material

records relating to the original new money issue and all material records relating to the refunding issue should be maintained until 3 years after the final redemption of both bond issues.

F. State record retention policies should also be considered, but in the event of a

discrepancy, the guidelines established by the IRS shall prevail. G. Although the required records to be retained depend on the transaction and the

requirements imposed by the Code and the regulations, records common to most transactions include:

Basic records relating to the bond transaction (including the Official Statement, Board minutes and resolutions authorizing issuance, trustee statements, and bond counsel opinion); Documentation directing, authorizing and showing expenditure of bond proceeds, including purchase contracts, construction contracts, progress payments, invoices, cancelled checks, and payment of bond issuance costs;

Documentation evidencing use of bond-financed property by public and private sources (i.e., copies of management contracts);

Documentation evidencing all sources of payment or security for the bonds;

Documentation pertaining to any investment of bond proceeds (including the purchase and sale of securities, SLGs subscriptions, yield calculations for each class of investments, actual investment income received, the investment of proceeds, guaranteed investment contracts, and rebate calculations).

Information, records and calculations showing that, with respect to each bond issue, the Issuer was eligible for the “small issuer” exception or one of the spending exceptions to the arbitrage rebate requirements.

All tax returns and other communication related to the bonds such as IRS Forms 8038-G, 8038-T 8038-TC and 8038-R.

Any other documentation that is material to the bonds or the bond financed facilities based on particular facts.

The list above is general and only highlights the basic records that are typically material to many types of tax-exempt bond financings. Each transaction is unique and may, accordingly, have other records that are material to the requirements applicable to that financing. The decision as to whether any particular record is material must be made on a case-by-case basis and could take into account a number of factors, including, for instance, the various expenditure exceptions.

6. Reimbursement Resolutions

The City Treasurer is responsible for ensuring that Reimbursement Resolutions are prepared in accordance with §1.150-2 of the U.S. Treasury regulations for projects the City intends to finance with bonds. 7. Bond Proceed Expenditures Expenditures from bond proceeds will be in accordance with the City’s prevailing expenditure and delegation of City policies. 8. Bond Proceed Investments Bond proceeds will be invested in accordance with the City’s prevailing Investment Procedure. 9. Education and Training The City Administrator and his or her designated staff are responsible for staying current with any changes in the rules for tax-exempt and Direct Pay bonds. The City recognizes that such education and training is vital as a means of helping to ensure compliance with federal tax requirements in respect of its bonds. The City Administrator may rely upon outside advisors for assistance and guidance with these matters. 10. Material Event Disclosure (SEC, MSRB) The City will comply with all continuing disclosure requirements under SEC Rule 15c2-12. The Rule prohibits any broker, dealer, or municipal securities dealer from acting as an underwriter in a primary offering of municipal securities unless the issuer promises in writing to provide certain ongoing information. The annual financial information is to be sent to the MSRB as designated by the SEC. The City Treasurer will make notification in a timely manner, of any events described in the Continuing Disclosure Certificate entered into in connection with a series of bonds. 11. Due Diligence & Remedial Actions

In all activities related to bonds issued by or on behalf of the City, staff will exercise due diligence to comply with IRS Code governing tax-exempt and Direct Pay Bonds. The Issuer is aware of (a) the Voluntary Closing Agreement Program (known as “VCAP”) operated by the Internal Revenue Service which allows issuers to voluntarily enter into a closing agreement in the event of certain non-compliance with Federal tax requirements and (b) the remedial actions available under Section 1.141-12 of the Income Tax Regulations for private use of bond financed property which was not expected at the time the bonds were issued.

12. Periodic Review The City Treasurer will monitor compliance with the guidelines contained in this Procedure as well as any other covenants not specifically included herein.