city gas distribution in india - a virtual conference

TRANSCRIPT

City Gas Distribution in India - A Virtual Conference

Session: Key Trends, Developments And Post-Covid-19 Outlook

India Infrastructure

January 21, 2021

Mr. Prashant VasishtVice President and Co-Head, Corporate RatingsICRA Limited

Speaker

Agenda

01 02

0504

03

06

Trends Impact of Covid-19

OutlookKey Issues and

Challenges

3

Performance of

Incumbents during

Covid-19

Opportunities for CGD

Companies

City Gas Distribution: Trends

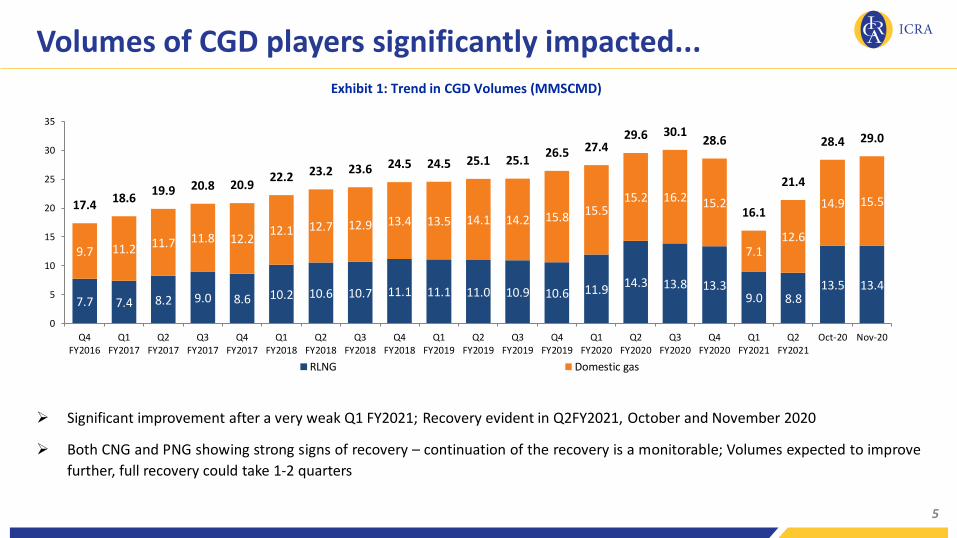

Volumes of CGD players significantly impacted...

➢ Significant improvement after a very weak Q1 FY2021; Recovery evident in Q2FY2021, October and November 2020

➢ Both CNG and PNG showing strong signs of recovery – continuation of the recovery is a monitorable; Volumes expected to improve

further, full recovery could take 1-2 quarters

5

Exhibit 1: Trend in CGD Volumes (MMSCMD)

7.7 7.4 8.2 9.0 8.6 10.2 10.6 10.7 11.1 11.1 11.0 10.9 10.6 11.914.3 13.8 13.3

9.0 8.813.5 13.4

9.7 11.2 11.7 11.8 12.212.1 12.7 12.9 13.4 13.5 14.1 14.2 15.8 15.5

15.2 16.2 15.2

7.112.6

14.9 15.517.418.6

19.9 20.8 20.922.2 23.2 23.6 24.5 24.5 25.1 25.1

26.5 27.429.6 30.1

28.6

16.1

21.4

28.4 29.0

0

5

10

15

20

25

30

35

Q4FY2016

Q1FY2017

Q2FY2017

Q3FY2017

Q4FY2017

Q1FY2018

Q2FY2018

Q3FY2018

Q4FY2018

Q1FY2019

Q2FY2019

Q3FY2019

Q4FY2019

Q1FY2020

Q2FY2020

Q3FY2020

Q4FY2020

Q1FY2021

Q2FY2021

Oct-20 Nov-20

RLNG Domestic gas

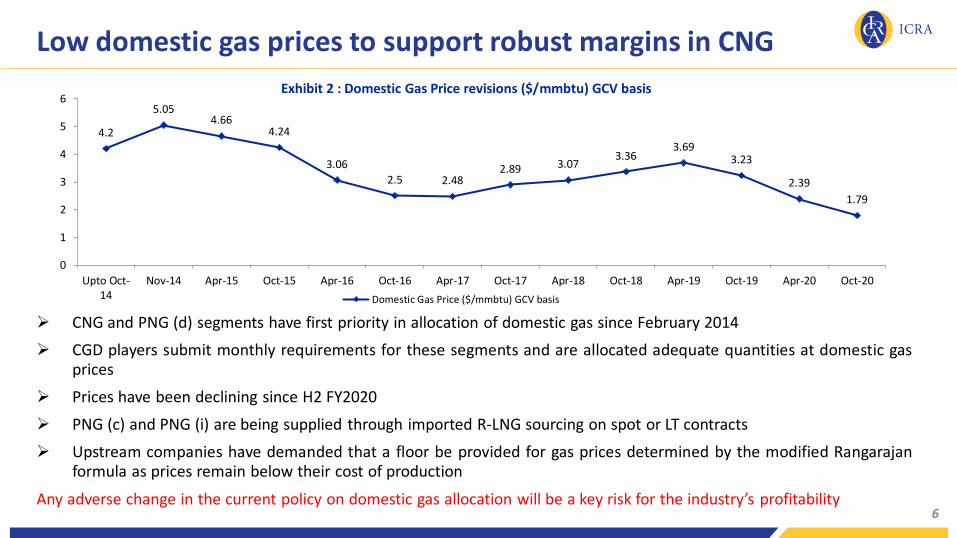

Low domestic gas prices to support robust margins in CNG

➢ CNG and PNG (d) segments have first priority in allocation of domestic gas since February 2014

➢ CGD players submit monthly requirements for these segments and are allocated adequate quantities at domestic gasprices

➢ Prices have been declining since H2 FY2020

➢ PNG (c) and PNG (i) are being supplied through imported R-LNG sourcing on spot or LT contracts

➢ Upstream companies have demanded that a floor be provided for gas prices determined by the modified Rangarajanformula as prices remain below their cost of production

Any adverse change in the current policy on domestic gas allocation will be a key risk for the industry’s profitability6

Exhibit 2 : Domestic Gas Price revisions ($/mmbtu) GCV basis

4.2

5.054.66

4.24

3.06

2.5 2.482.89 3.07

3.363.69

3.23

2.39

1.79

0

1

2

3

4

5

6

Upto Oct-14

Nov-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 Apr-18 Oct-18 Apr-19 Oct-19 Apr-20 Oct-20

Domestic Gas Price ($/mmbtu) GCV basis

CNG and PNG (d) cost competitive

7

Traditional Fuels City Gas

City Gas

cheaper on

energy terms

by

Fuel Selling Unit Selling

Price

Gross

Calorific

Value (GCV)

GCV Unit Energy Cost

(Rs/million

Kcal)

Fuel Selling

Price

Selling

Unit

Energy Cost

(Rs/million

Kcal)^

MS Rs./litre 85.0 8419 Kcal/litre 10091 CNG 42.70 Rs./kg 3389 66%HSD Rs./litre 75.1 9036 Kcal/litre 8315 CNG 42.70 Rs./Kg 3389 59%Auto LPG Rs./litre 46.6 10800 Kcal/kg 7987 CNG 42.70 Rs./Kg 3389 58%Sub. LPG Rs./Cylinder 694 10800 Kcal/Kg 4525 PNG (d) 27.50 Rs./m3 2957 35%

Un-sub. LPG Rs./Cylinder 694 10800 Kcal/Kg 4525 PNG (d) 27.50 Rs./m3 2957 35%

Bulk LPG Rs./Kg 71.0 10800 Kcal/Kg 6574 PNG © 42.01 Rs./m3 4517 31%LDO Rs./litre 36.6 8800 Kcal/litre 4156 PNG (I) 34.37 Rs./m3 3696 11%

Furnace Oil Rs./kg 32.1 10440 Kcal/kg 3072 PNG (I) 34.37 Rs./m3 3696 -20%

Source: Prices from websites of IOC and BPCL at Delhi, ICRA analysis; Prices as on January 19, 2021Note: (d): domestic, (I): industrial, ©: commercial. ̂ GCV of gas assumed at 9300 Kcal/m3.

Exhibit 3: Energy cost comparison with traditional fuels

CNG and PNG (d) segments highly competitive due to domestic allocation; especially CNG…

PNG (i) to continue to face pressure due to non-competitiveness against liquid fuels

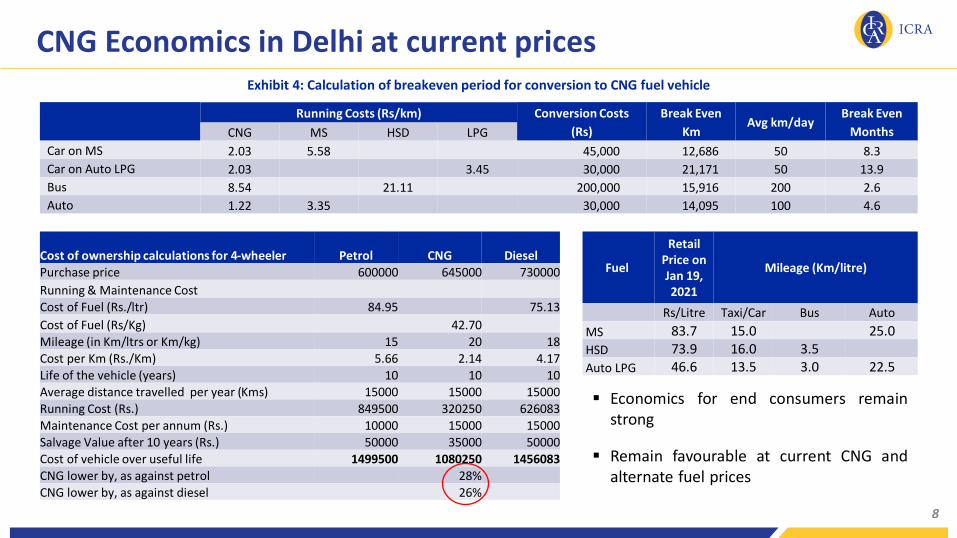

CNG Economics in Delhi at current prices

8

Cost of ownership calculations for 4-wheeler Petrol CNG DieselPurchase price 600000 645000 730000

Running & Maintenance Cost

Cost of Fuel (Rs./ltr) 84.95 75.13

Cost of Fuel (Rs/Kg) 42.70Mileage (in Km/ltrs or Km/kg) 15 20 18

Cost per Km (Rs./Km) 5.66 2.14 4.17

Life of the vehicle (years) 10 10 10Average distance travelled per year (Kms) 15000 15000 15000Running Cost (Rs.) 849500 320250 626083

Maintenance Cost per annum (Rs.) 10000 15000 15000Salvage Value after 10 years (Rs.) 50000 35000 50000Cost of vehicle over useful life 1499500 1080250 1456083

CNG lower by, as against petrol 28%CNG lower by, as against diesel 26%

▪ Economics for end consumers remainstrong

▪ Remain favourable at current CNG andalternate fuel prices

Fuel

Retail Price on Jan 19, 2021

Mileage (Km/litre)

Rs/Litre Taxi/Car Bus Auto

MS 83.7 15.0 25.0

HSD 73.9 16.0 3.5

Auto LPG 46.6 13.5 3.0 22.5

Running Costs (Rs/km) Conversion Costs

(Rs)

Break Even

KmAvg km/day

Break Even

MonthsCNG MS HSD LPG

Car on MS 2.03 5.58 45,000 12,686 50 8.3

Car on Auto LPG 2.03 3.45 30,000 21,171 50 13.9

Bus 8.54 21.11 200,000 15,916 200 2.6

Auto 1.22 3.35 30,000 14,095 100 4.6

Exhibit 4: Calculation of breakeven period for conversion to CNG fuel vehicle

Impact of Covid-19

Impact of covid-19 pandemic on gas sector

➢ Indian LNG demand saw surge due to collapse in spot prices

➢ Challenges for aggregators to market term LNG volumes given the price differential over spotLNG; moreover inventory losses on LNG were witnessed

➢ Demand from CGD and industrial sector had declined sharply since lockdown in March; now

recovering

➢ LNG re-gasifiers had declared force majeure and deferred supplies; while earlier capacity

utilisations had dipped to 55-60% levels, major terminals are now operating at 95-100% volumes

compared to pre-Covid levels

➢ Transmission lines capacity utilization had declined due to 30-40% lower volumes; however with

easing of lockdowns now operating at 95-100% volumes as compared to pre-Covid-19 levels

➢ Consumption of gas is now at almost pre-Covid levels

➢ Delays in project execution owing to restrictions on movement of men and material furtherdragged by 2nd and 3rd waves in some areas and social distancing rules

Segment wise impact on CGD companies

• Significant impact on sale to public/private transport due to lockdowns

• Recovery has been V-shaped; Volumes near about 90%+ of earlier levels

• Conversion/cost advantages continue to remain strongCNG

• Significant impact continues and volumes seeing recovery as industries resume

• Volumes could take few more months to reach earlier levels

• Significant fall in liquid fuels and coal prices are further dampenersPNG (I)

• Mostly sales concentrated in cities – largely Restaurants & Hotels

• Over 70% volumes lost due to curbs

• All volumes lost may not recover; customer behavioral changes – less dine out

• Relatively small in overall mix

PNG (C)

• Volumes increased due to more at home dining

• Volumes limited <10% of total for any playerPNG (D)

Other challenges; New projects could face delays...

• Delayed realization of receivables from industrial PNG players; Increased short term funding requirements

• Vendors and contractors facing liquidity issues and need capital to work on construction sites

• Existing companies with low regulatory pressure could curtail capex

• Projects in new GAs could face heightened challenges:-• Project cost increase; Achieving financial closure could be prolonged (esp for new entrants)

• Statutory Clearances have got delayed

• Equipment orders delayed; Renegotiations could be a reality

• Labor availability severely impacted – laying pipeline, last mile of domestic connections, new CNG stations, etc.

• Force majeure approvals from PNGRB may not be adequate

• Possible impact on long term demand/prospects is the larger concern – especially new projects

• Post covid challenges with management of labor/strict distancing rules

Force Majeure relief to CGD companies

• On Nov 5, PNGRB allowed extension to 41 CGD companies setting up projects in 185 GAs to complete MWP

• PNGRB has considered 69 days as the centrally imposed lockdown period and 60 days as the restoration period

• Most of the 185 entities have received the basic extension of 129 days only, 38 entities have received extensions ranging from 136-251 days largely at locations that had longer state enforced lockdowns

• Considering strict penalties that can be imposed for delay in executing the MWP, fairly limited and case by case extensions will ensure that players are not complacent

13

New Open Access Regulations – November 2020

• On November 27, 2020, the PNGRB has released a final regulation for determination of transportation ratefor City Gas distribution.

• The regulations have kept most aspects of the access code unchanged, except clarifying further on openaccess. The PNGRB has clarified that the existing CNG stations of franchise/dealers (including OMC’sCNG/LCNG stations) will not be considered as third-party shipper for the purpose of allowing access.

• While any additional capacity expansion at existing premise will also not be considered as third-party, settingup of CNG compressor at a new liquid fuel pumps will be considered as third-party. Major CGD players –Indraprastha Gas and Mahanagar Gas have a significant portion (>50%) of their CNG stations on OMCnetworks, thus, this regulation significantly lessens the risk of third-party competition and margincontraction for them.

• The risk of third-party marketing would continue to remain for large industrial PNG markets catered to byplayers like Gujarat Gas in Gujarat given the price sensitive and large market as well the access to multiplegas sources in the vicinity. However, the impact would be limited as only a maximum of ~20% of customercan shift to third-party.

• CGD companies filed litigations against the said regulations at draft stage itself as it would hurt the prospectsof the authorized players and allow third parties to select and takeaway profitable segments.

14

Unified Tariff Regime implemented with pooled tariff approach

• To reduce distance-based tariff dislocation in

natural gas pricing, PNGRB implemented UTR

• Tariff policy based on the pooling of the

approved tariffs for the pipelines forming the

national gas grid

• Pipeline network divided in two zones; Zone-1 as

first 300 KM from injection point and everything

thereafter falls in Zone-2

• Zone-1 tariff to be 40% of Zone-2

• Transmission tariff for majority of the players

utilizing single pipeline whether in Zone- 1 or

Zone-2 to witness increase in the transportation

costs

• Consumers located in Zone-2 and receiving gas

which flows through multiple pipelines to benefit

with tariff expected to moderate by around 40% 15

Pipeline Name Pipeline Operator Current Tariff, Rs. /mmbtu*

Unified Tariff, Rs.

/mmbtu*Zone-1 Zone-2

Integrated Hazira Vijaipur Jagdishpur

Pipeline

GAIL (India) Limited

19.83, 36.86, 45.38, 49.64 26.75 66.87

Dahej-Uran Dabhol Panvel NG Pipeline 29.55, 39.85 26.75 66.87

Dahej-Vijaipur (DVPL)-Vijaipur Dadri

(GREP) (Capacity augmentation)26.75 66.87

Jagdishpur-Bokaro-Haldia-Dhamra NG

Pipeline63.46 26.75 66.87

Dadri-Bawana-Nangal NG Pipeline 14.04, 14.06 26.75 66.87

Chainsa-Jhajjjar-Hissar NG Pipeline 7.85 26.75 66.87

Dabhol-Bangalore NG pipeline 45.37, 45.41, 45.44 26.75 66.87

Dadri Panipat NG PipelineIndian Oil Corporation

Limited16.46 26.75 66.87

East-West PipelinePipeline Infrastructure

Limited65.50, 75.33, 78.65, 79.77, 80.15 26.75 66.87

GSPL's High Pressure Gujarat Gas GridGujarat State Petronet

Limited33.15, 34.84, 34.86 26.75 66.87

Shahdol-PhulpurReliance Gas Pipelines

limited96.33 26.75 66.87

Mehsana-Bhatinda GSPL India Gasnet

Limited

0.90, 41.39 26.75 66.87

Bhatinda-Jammu-Srinagar NA 26.75 66.87

Mallavaram-Bhopal-Bhilwara-VijaipurGSPL India Transco

LimitedNA 26.75 66.87

Pollution map

16

Mandatory switch to PNG by industrial units in Delhi

Could spark a trend across several other states grappling with high levels of airpollution

• On December 22, 2020, the Ministry of Environment, Forest and Climate Change, identifiedabout 1,644 industrial units spread across 50 industrial areas in Delhi to switch over to PNGowing to the high levels of pollution. Additionally, Delhi Pollution Control Committee,Indraprastha Gas Limited and Delhi government were also asked to work in close coordinationto target the completion of switch over to PNG by January 31, 2021.

• The directive by the Ministry would provide a boost to the industrial volumes of incumbent IGL.

• Additionally, with several cities in Northern India featuring among the top 20 most pollutedcities globally, such as Jodhpur, Jind, Gurugram, Agra, Ghaziabad, Lucknow and Varanasi otherstate pollution control boards may follow suit which would benefit the incumbent CGD entitiesin these cities

• In October 2017, Supreme Court had banned use of pet coke and furnace oil in NCR to controlpollution levels. The court had also directed Governments of Rajasthan, Haryana and UttarPradesh. However, compliance by consumers was slow

17

Performance of incumbents during Covid-19

Industry Response to Pandemic

➢ The Ministry of Home Affairs notified natural gas supply as an essential service whichcontinued to operate within the lockdown

➢ CGD entities were able to receive gas supplies and maintained the supply of gas to alltypes of consumers

➢ CNG sales were down 70-80% in early days of the lockdown owing to which operatorsrationalized services by closing upto 2/3rd of company owned company operatedoutlets

➢ Project activities stopped owing to lockdown and migration of labour; startedgradually with the easing of lockdowns

➢ Companies individually and collectively approached PNGRB for extension of timelinesin meeting MWP

➢ Companies increased prices in some GAs

19

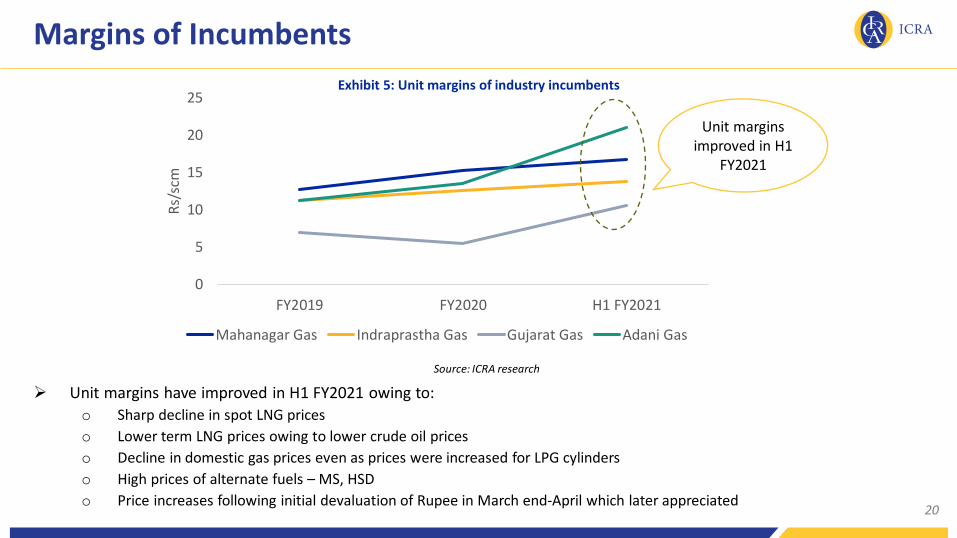

Margins of Incumbents

➢ Unit margins have improved in H1 FY2021 owing to:

o Sharp decline in spot LNG prices

o Lower term LNG prices owing to lower crude oil prices

o Decline in domestic gas prices even as prices were increased for LPG cylinders

o High prices of alternate fuels – MS, HSD

o Price increases following initial devaluation of Rupee in March end-April which later appreciated

Source: ICRA research

20

0

5

10

15

20

25

FY2019 FY2020 H1 FY2021

Rs/

scm

Mahanagar Gas Indraprastha Gas Gujarat Gas Adani Gas

Unit margins improved in H1

FY2021

Exhibit 5: Unit margins of industry incumbents

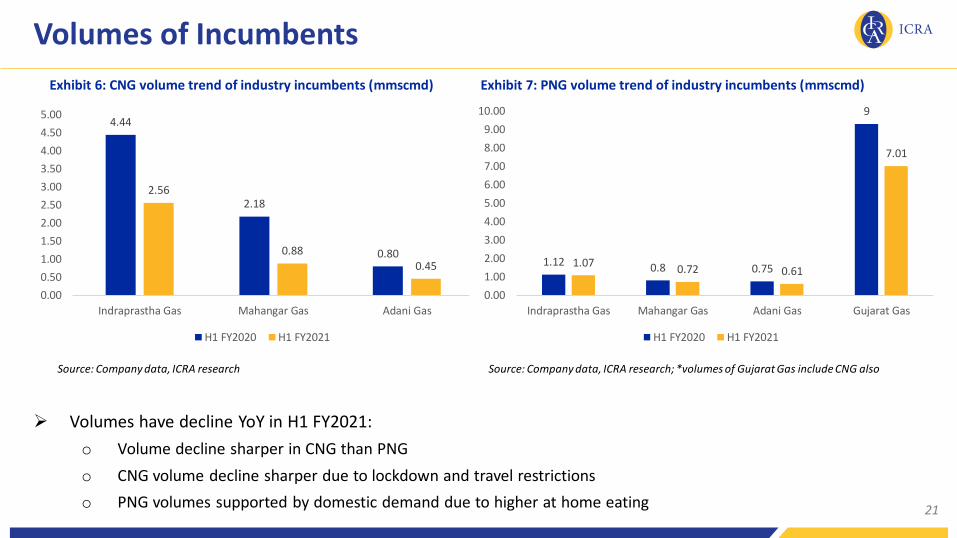

Volumes of Incumbents

Source: Company data, ICRA research Source: Company data, ICRA research; *volumes of Gujarat Gas include CNG also

21

Exhibit 6: CNG volume trend of industry incumbents (mmscmd) Exhibit 7: PNG volume trend of industry incumbents (mmscmd)

4.44

2.18

0.80

2.56

0.88

0.45

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Indraprastha Gas Mahangar Gas Adani Gas

H1 FY2020 H1 FY2021

1.12 0.8 0.75

9

1.070.72 0.61

7.01

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Indraprastha Gas Mahangar Gas Adani Gas Gujarat Gas

H1 FY2020 H1 FY2021

➢ Volumes have decline YoY in H1 FY2021:

o Volume decline sharper in CNG than PNG

o CNG volume decline sharper due to lockdown and travel restrictions

o PNG volumes supported by domestic demand due to higher at home eating

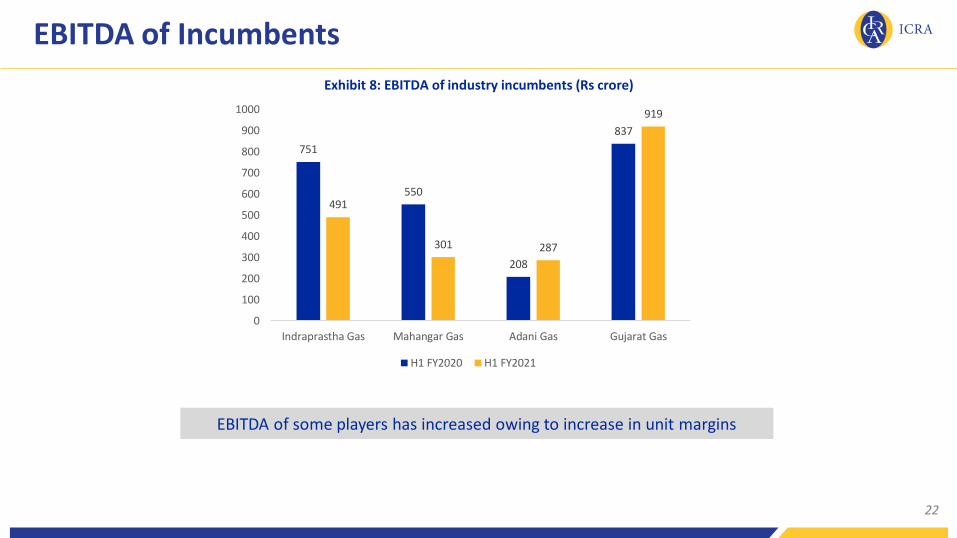

EBITDA of Incumbents

Source: ICRA research

22

Exhibit 8: EBITDA of industry incumbents (Rs crore)

751

550

208

837

491

301 287

919

0

100

200

300

400

500

600

700

800

900

1000

Indraprastha Gas Mahangar Gas Adani Gas Gujarat Gas

H1 FY2020 H1 FY2021

EBITDA of some players has increased owing to increase in unit margins

Key Issues and Challenges

Key Issues and Challenges

➢ Anemic pace of approvals

➢ Despite recommendations by PNGRB states yet to provide regulatory push such

as lower road tax on CNG/LNG vehicles, single window clearance for approvals

etc

➢ Delays and disruption caused due to Covid-19 in project execution

➢ Shortage of skilled manpower

➢ Overbooked contractors and suppliers

➢ Different VAT rates across states

➢ Competition from electric vehicles especially for state transport bus segment

24

Small scale LNG

25

➢ Laying pipelines remains a long-drawn processowing to multiple approvals

➢ More economical/less capex to deploy SSLNGfor locations that are distant from trunkpipelines

➢ Coverage of several charge areas in GAs withintimelines may not be possible owing tostretched contractors due to large number ofprojects being executed within the country

➢ Attractiveness of LNG and CNG as a fuel vis-à-vis HSD especially for commercial vehicles

➢ Current low spot prices of LNG make forattractive economics against alternate fuelsand SSLNG may enable rapid seeding ofmarket

Opportunities for CGD companies

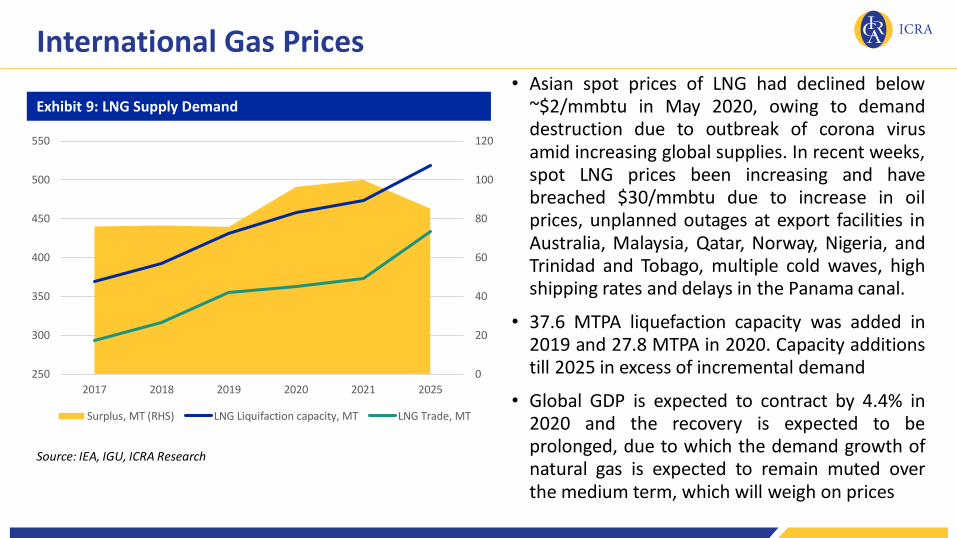

International Gas Prices

Exhibit 9: LNG Supply Demand

• Asian spot prices of LNG had declined below~$2/mmbtu in May 2020, owing to demanddestruction due to outbreak of corona virusamid increasing global supplies. In recent weeks,spot LNG prices been increasing and havebreached $30/mmbtu due to increase in oilprices, unplanned outages at export facilities inAustralia, Malaysia, Qatar, Norway, Nigeria, andTrinidad and Tobago, multiple cold waves, highshipping rates and delays in the Panama canal.

• 37.6 MTPA liquefaction capacity was added in2019 and 27.8 MTPA in 2020. Capacity additionstill 2025 in excess of incremental demand

• Global GDP is expected to contract by 4.4% in2020 and the recovery is expected to beprolonged, due to which the demand growth ofnatural gas is expected to remain muted overthe medium term, which will weigh on prices

Source: IEA, IGU, ICRA Research

0

20

40

60

80

100

120

250

300

350

400

450

500

550

2017 2018 2019 2020 2021 2025

Surplus, MT (RHS) LNG Liquifaction capacity, MT LNG Trade, MT

International Gas Prices

Exhibit 10: Crude and Gas Price Trend

Source: IEA, IGU, ICRA Research

0

10

20

30

40

50

60

70

80

90

0.00

4.00

8.00

12.00

16.00

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Oct

-20

No

v-2

0

Dec

-20

$/b

bl

$/m

mb

tu

Japan LNG Import Price Henry Hub Price UK NBP

Japan Spot prices Brent (on RHS)

• Consumers are switching to

alternate fuels wherever

possible

• PNG (I) will be most affected;

shift to FO, LSHS, LPG,

Propane, Coal will happen

• More importantly PNG (I)

margins could get compressed

significantly or turn negative

• Some minor impact in PNG (C)

as well

• CGD companies have increased

offtake of long-term volumes

• Prices are expected to

significantly decline by March

LNG driven CVs➢ Setting up of new LNG stations – 1000 planned over next 3

years at every 200-300 km along the golden quadrilateral

➢ Enabling regulatory amendments have been made for

manufacture of LNG vehicles and setting up of LNG stations

➢ PNGRB has allowed setting up of LNG stations by any entity

even one that is not authorized in a GA

➢ Commissioning of new LNG Terminals a key enabler of

growth

➢ Transporters yet to adopt LNG vehicles owing to lack of

refueling stations

➢ Network of stations still 2-4 years away post which

adoption will be possible

➢ Higher initial capital investment though ownership cost

over lifetime of the vehicle may be lower

Economics of LNG vs HSD Commercial Vehicle

30

Exhibit 11: Payback Period for LNG vs HSD Commercial Vehicle

HSD LNG

Initial Cost Rs 40 lakh Rs 53 lakh

Maintainance Cost Rs 50000 Rs 60000

Distance Travelled per year (km)

1,00,000 1,00,000

Mileage 3.3 km/liter 4 km/kg

Cost of Fuel Rs 75.1/liter* Rs 60/kg (Rs 42.7/kg CNG)*

Payback Period 1.8 years

Source: ICRA research, * HSD and CNG price in Delhi as on Jan 19, 2021

China’s Experience:

➢ At the end of 2018 about 3.5 lakh CV on LNG ofwhich 2/3rd were Heavy Duty Trucks andremaining were buses and coaches

➢ Sales of LNG trucks jumped 500% in 2017 owingto improved discount of LNG vs HSD as well asmove to Euro-VI emission norms

Preferred Fuel for Heavy Trucks:

➢ Higher energy density similar to HSD so higherdistance for refueling and lower fuel tankvolume

➢ Higher fuel injection pressure required in thecylinder which is more efficient for LNG thanCNG

Outlook

31

Ramp up in new GAs to drive CGD demand growth

32

PNG(I) volumes witnessing gradual recovery with pick-

up in industrial activity

CNG demand expected to increase driven by

favourable economics and preference for personal

mobility

PNG(D) consumption to increase with aggressive roll-out to meet targets

PNG(C) volumes to remain muted due to curbs

Ramp-up in new GAs as the initial infrastructure

building phase nears completion

1 2 3 4 5

Outlook

➢ Despite the current run-up, spot LNG prices expected to remain low over the

medium term which should spur demand.

➢ Several CGD projects at the cusp of increasing offtake substantially after 2-2.5 years

of setting up of network

➢ LCNG stations an increasingly viable option for servicing off grid locations especially

faced with Covid-19 delays and overbooked contractors

➢ Incumbents aggressively undertaking capex to make up for lost time

➢ A lower tax incidence on CNG, LNG vis-à-vis MS, HSD remains an advantage

➢ New tariff regulations would aid the economics of CGD entities for GAs distant from

the west coast due to lower pipeline tariff especially for PNG(I and C) segments

33

Thank You!

Contact Details

Prashant Vasisht

Vice President and Co-Head Corporate Ratings

+91-9818316222

© Copyright, 2021 ICRA Limited. All Rights Reserved.

All information contained herein has been obtained by ICRA from sources believed by it to be accurate and reliable. Although reasonable care has

been taken to ensure that the information herein is true, such information is provided 'as is' without any warranty of any kind, and ICRA in particular,

makes no representation or warranty, express or implied, as to the accuracy, timeliness or completeness of any such information. Also, ICRA or any of

its group companies, while publishing or otherwise disseminating other reports may have presented data, analyses and/or opinions that may be

inconsistent with the data, analyses and/or opinions in this publication. All information contained herein must be construed solely as statements of

opinion, and ICRA shall not be liable for any losses incurred by users from any use of this publication or its contents.