circular to murray & roberts holdings limited...

TRANSCRIPT

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION

The definitions commencing on page 5 of the Circular apply to the whole of the Circular, including its annexures and the Notice of General Meeting and form of proxy attached to it, unless the contrary appears from a specific document.

If you are in any doubt as to the action you should take, please consult your CSDP, Broker, attorney, accountant, banker or other professional adviser immediately.

If you have disposed of all of your Murray & Roberts Shares then the Circular, together with the accompanying notice of General Meeting and form of proxy, should be forwarded to the purchaser of such shares or to the Broker, CSDP, banker or other agent through whom such disposal was effected.

Additional copies of the Circular, in its printed format, may be obtained during business hours from the Company and the lead JSE sponsor at their respective addresses listed on page 2, from Monday, 7 October 2013, until Wednesday, 6 November 2013. Copies of the Circular are available in the English language only. The Circular will also be available on the Murray & Roberts website (www.murrob.com) as from 7 October 2013.

The General Meeting convened in terms of the Notice of General Meeting will be held at Douglas Roberts Centre, 22 Skeen Boulevard, Bedfordview, Johannesburg on Wednesday, 6 November 2013, immediately following the conclusion of the Annual General Meeting scheduled at 11:00 on the same date.

Action required

• CertificatedShareholdersandDematerialisedShareholderswith“ownname”registration,whoareunabletoattendtheGeneralMeeting and wish to be represented thereat, must complete and return the attached form of proxy in accordance with the instructions contained therein and return it to the Transfer Secretaries to be received no later than 11:00 on Monday, 4 November 2013.

• DematerialisedShareholders,otherthanDematerialisedShareholderswith“ownname”registration,who: – are unable to attend the General Meeting and wish to be represented thereat, must provide their CSDPs or Brokers with their

voting instructions in terms of the custody agreement entered into between themselves and the CSDPs or Brokers concerned, in the manner and within the time stipulated therefore. If no instructions are provided to their CSDPs or Brokers, then voting will take place in terms of the custody agreement entered into between themselves and the CSDPs or Brokers concerned;

– wish to attend the General Meeting, must instruct their CSDPs or Brokers to issue them with the necessary authorities to attend the General Meeting, in the form of a Letter of Representation.

Murray & Roberts does not accept any responsibility and will not be held liable for any failure on the part of any CSDP or Broker of a Dematerialised Shareholder to notify such shareholder.

Murray & Roberts Holdings Limited(Incorporated in the Republic of South Africa)

(Registration number: 1948/029826/06)(JSE share code: MUR) (ISIN: ZAE000073441) (ADR Code: MURZY)

(the “Company”)

CIRCULAR TO MURRAY & ROBERTS HOLDINGS LIMITED SHAREHOLDERS

relating to:

• theacquisitionbyMurray&RobertsHoldingsLimitedofalltheordinarysharesinCloughLimitedthatitdoesnotalreadyown at A$1,46 cash per share, expected to consist of a cash payment of A$1,32 per share paid by Murray & Roberts and a proposed dividend of A$0,14 per share paid by Clough, as per the executed scheme implementation agreement. The total cash consideration is expected to be A$461,4 million (ZAR4 296 million);

and incorporating:

• aNoticeofGeneralMeeting;and• aformofproxy,applicabletoCertificatedShareholdersandDematerialisedShareholderswith“ownname”registration

only.

Date of issue: 7 October 2013

Financial adviser and lead JSE sponsor South African legal counsel Australian legal counsel

Independent reporting accountants JSE sponsor Transfer secretaries and auditors

TABLE OF CONTENTS

The definitions and interpretations set out on pages 5 to 9 of the Circular apply, mutatis mutandis, to the following table of contents:Forward-looking statements 1Corporate information 2Action required by shareholders 3Salient dates and times 4Definitions 51. Introduction and purposes of the Circular 102. Background to the parties 11

2.1 History and nature of the business of Murray & Roberts 112.2 History and nature of the business of Clough 13

3. Murray & Roberts rationale 164. Terms of the Acquisition 17

4.1 Details of the Acquisition 174.2 Conditions precedent 184.3 Additional information required for Clough 194.4 Details of material assets acquired during the past three years 194.5 Categorisation 19

5. Opinion and recommendation 196. Working capital statement 207. Pro forma financial effects relating to the Acquisition 208. Directors 21

8.1 Directors’ responsibility statement 218.2 Directors’ interests in Murray & Roberts securities 218.3 Directors’ interests in transactions 228.4 Directors’ remuneration 228.5 Directors’ service contracts 238.6 Movements in share options of executive directors during the year ended 30 June 2013 23

9. Major Murray & Roberts Shareholders 2310. Litigation statement and contingent liabilities 24

10.1 Murray & Roberts 2410.2 Clough 24

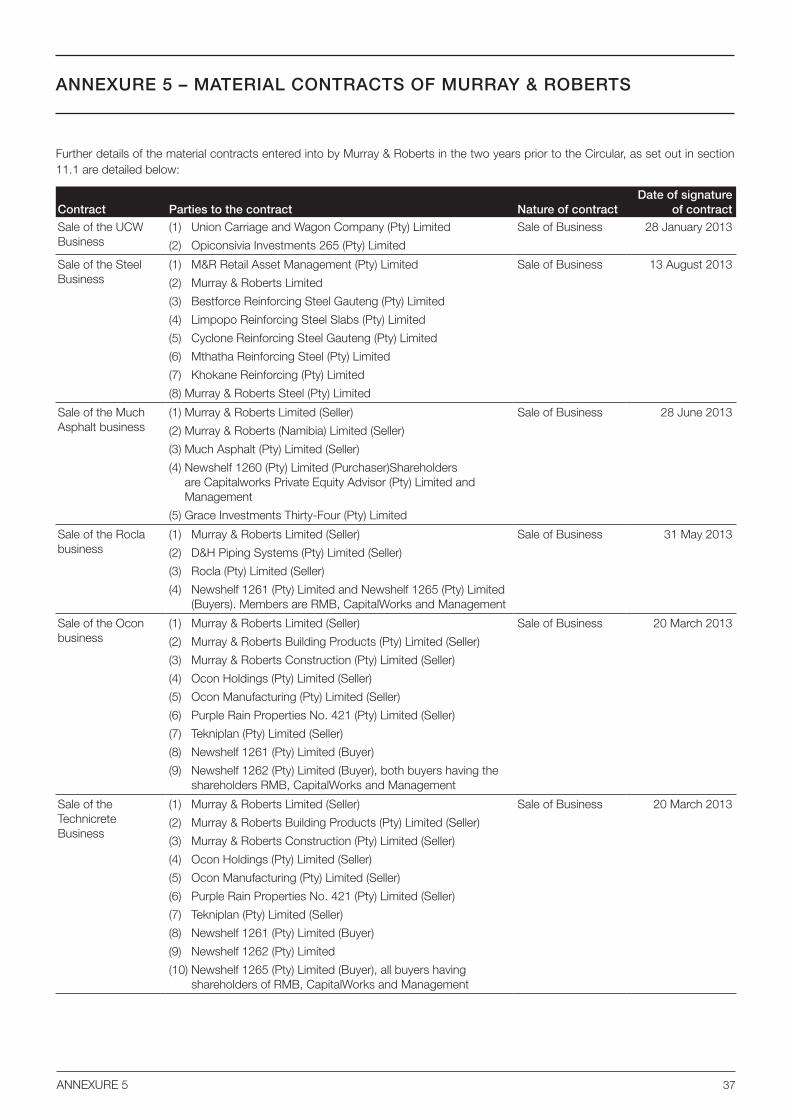

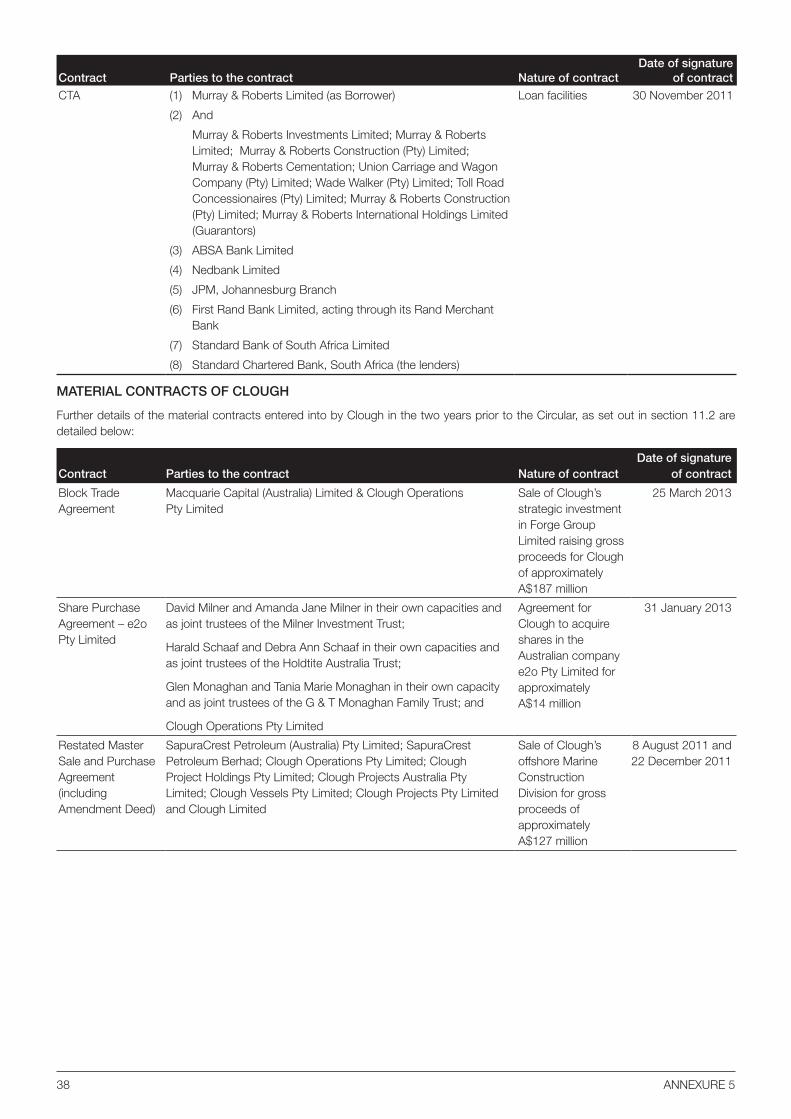

11. Material contracts 2411.1 Murray & Roberts 2411.2 Clough 25

12. Material borrowings 2613. Material change 2614. Expenses relating to the Acquisition 2615. General meeting 2716. Expert’s consents 2717. Documents available for inspection 27

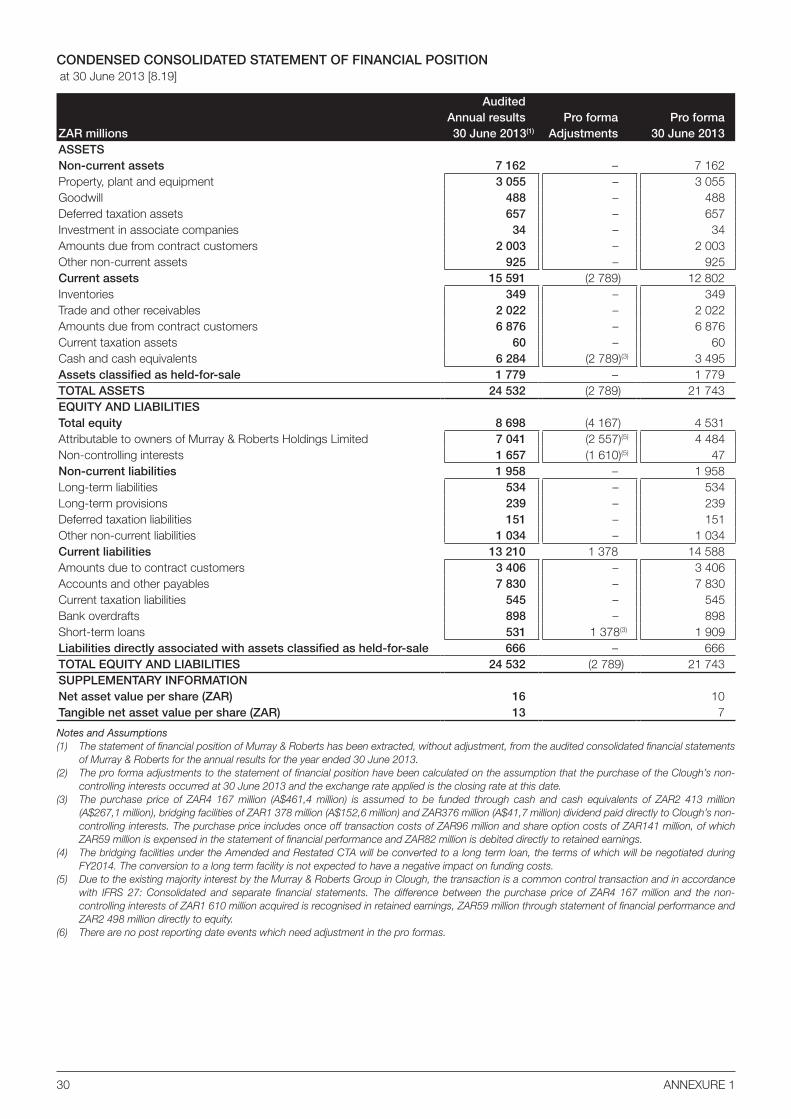

Annexure 1: Pro forma financial information of Murray & Roberts regarding the Acquisition 28Annexure 2: Independent reporting accountant’s assurance report on the compilation of pro forma financial information

included in a Circular31

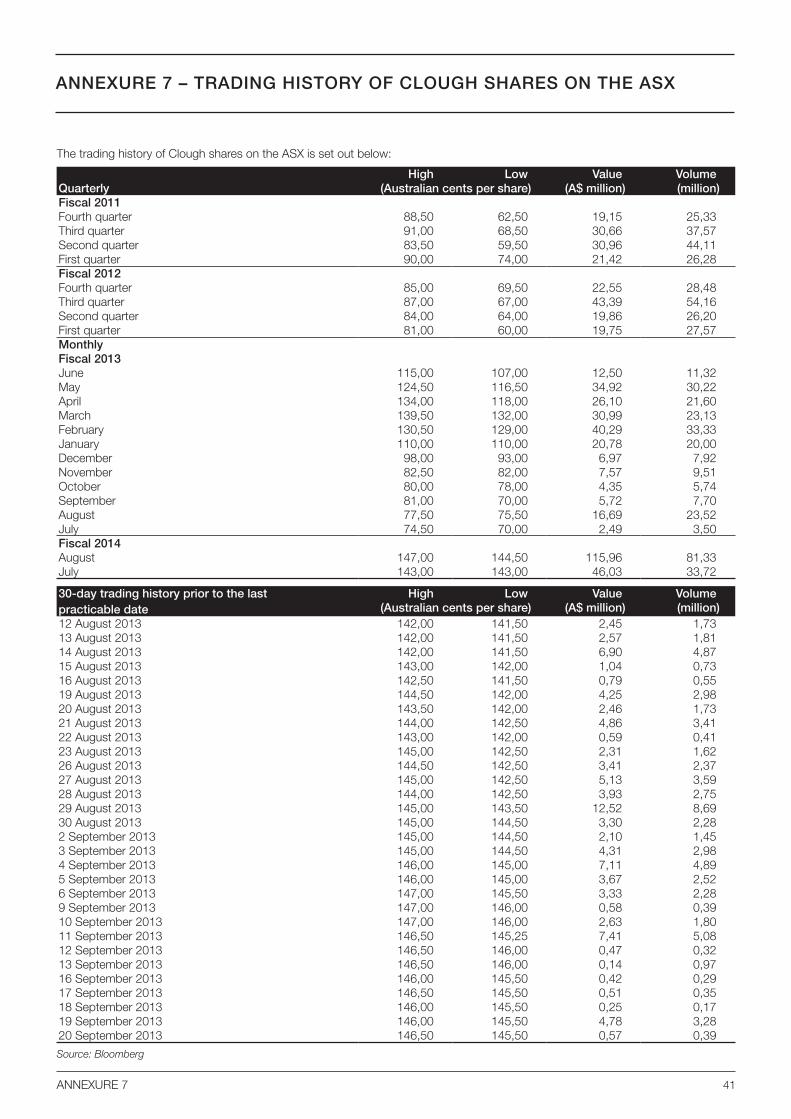

Annexure 3: Material borrowings of the Murray & Roberts Group 33Annexure 4: Material borrowings of the Clough Group 36Annexure 5: Material contracts of Murray & Roberts 37Annexure 6: Salient terms of the amended and restated CTA 39Annexure 7: Trading history of Clough Shares on the ASX 41Annexure 8: Historical financial information for Clough 42Annexure 9: Major operating subsidiaries of Murray & Roberts as at the date of the Circular 168

Notice of General Meeting 169Voting and Proxies 170Form of Proxy 171Notes to form of Proxy 172

1

FORWARD-LOOKING STATEMENTS

TheCircularincludesvarious“forward-lookingstatements”withinthemeaningofSection27AoftheUSSecuritiesAct101933andSection 21 E of the Securities Exchange Act of 1934 that reflect the current views or expectations of the Board with respect to future events and financial and operational performance. All statements other than statements of historical fact are, or may be deemed to be,forward-lookingstatements,including,withoutlimitation,thoseconcerning:theGroup’sstrategy;theeconomicoutlookfortheindustry;andtheGroup’s liquidityandcapital resourcesandexpenditure.Theseforward-lookingstatementsspeakonlyasof thedate of the Circular and are not based on historical facts, but rather reflect the Group’s current expectations concerning future results andeventsandgenerallymaybeidentifiedbytheuseofforward-lookingwordsorphrasessuchas“believe”,“expect”,“anticipate”,“intend”,“should”,“planned”,“may”,“potential”orsimilarwordsandphrases.TheGroupundertakesnoobligationtoupdatepubliclyor release any revisions to these forward looking statements to reflect events or circumstances after the date of the Circular or to reflect the occurrence of any unexpected events. Further, the Group shall not be liable in any manner whatsoever to any person in relation to such forward looking statements.

Certain of the information included in the Circular, relating to the economic outlook of the industry has been sourced from the following documents: LNG EPC/EPCM Market Attractiveness Outlook – January 2013 – Wood Mackenzie; The next Qatar – 27 June 2013 – The Economist; Global LNG Outlook – 10 September 2012 – Macquarie Equities Research and Regional Oil & Gas Developments – 05 September 2013 – Standard Bank.

Neither the content of the Group’s website, Clough’s website nor any website accessible by hyperlinks on the Group’s website is incorporated in, or forms part of, the Circular.

2

CORPORATE INFORMATION

DIRECTORS OF MURRAY & ROBERTS

ExecutiveHJ Laas (Group Chief Executive)AJ Bester (Group Financial Director)

Non-executiveM Sello* (Chairman)DD Barber*NBLanga-Royds*JM McMahon*#WA Nairn*RT Vice*

* Independent

# British Citizen

BusinessaddressandregisteredofficeMurray & Roberts Holdings LimitedDouglas Roberts Centre22 Skeen BoulevardBedfordview, 2007(PO Box 1000, Bedfordview, 2008, South Africa)

Company secretaryE Joubert, BCom (Acc) Hons CA (SA)Douglas Roberts Centre22 Skeen BoulevardBedfordview, 2007(PO Box 1000, Bedfordview, 2008, South Africa)

Financial adviser Macquarie First South Capital (Proprietary) Limited(Registration number 2003/014483/07) The Place 2nd Floor, South Wing, 1 Sandton Drive, Sandown, 2196(PO Box 783745, Sandton, 2146, South Africa)

Lead JSE sponsorMacquarie First South Capital (Proprietary) Limited(Registration number 2003/014483/07) The Place 2nd Floor, South Wing 1 Sandton Drive, Sandown, 2196 (PO Box 783745, Sandton, 2146, South Africa)

South African legal counsel Webber Wentzel 10 Fricker Road, Illovo BoulevardJohannesburg, 2196(PO Box 61771, Marshalltown, 2107,South Africa)

Australian legal counselCorrs Chambers Westgarth Level 15, Woodside Plaza240 St Georges TerracePerth, Western Australia, 6000(GPO Box 9925, Perth WA, 6001)

Independent reporting accountants and auditorsDeloitte & Touche(Practice Number 902276)Deloitte PlaceBuilding 1, The Woodlands, 20 Woodlands Drive, Woodmead, 2196(Private Bag X6, Gallo Manor, 2052, South Africa)

JSE sponsorDeutsche Securities (SA) Proprietary Limited(Anon-bankmemberoftheDeutscheBankGroup)(Registration number 1995/011798/07)3 Exchange Square, 87 Maude Street, Sandton, 2196(Private Bag X9933, Sandton, 2146, South Africa)

Transfer secretaries Link Market Services South Africa (Proprietary) Limited(Registration number 2000/007239/07)13th Floor, Rennie House, 19 Ameshoff StreetBraamfontein, 2001(PO Box 4844, Johannesburg, 2000, South Africa)

Transactional BankerThe Standard Bank of South Africa Limited(Registration Number 1962/000738/06)3 Simmonds StreetJohannesburg, 2000(PO Box 61344, Marshalltown, 2107, South Africa)

Date of incorporation 2 June 1948

Place of incorporationSouth Africa

3

ACTION REQUIRED BY SHAREHOLDERS

The definitions commencing on page 5 of the Circular apply to the whole of the Circular, including its annexures and the Notice of General Meeting and form of proxy attached to it, unless the contrary appears from a specific document.

The Acquisition and additional matters related thereto are subject to Murray & Roberts Shareholders passing the requisite ordinary resolutions at the General Meeting convened in terms of the Notice of Meeting to be held at Douglas Roberts Centre, 22 Skeen Boulevard, Bedfordview, Johannesburg on Wednesday, 6 November 2013 immediately following the conclusion of the Annual General Meeting scheduled at 11:00 on the same date.

GENERAL MEETING

A notice convening the General Meeting is attached to and forms part of the Circular.

CertificatedShareholdersandDematerialisedShareholderswhohaveelected“ownname”registrationinthesub-registermaintainedby a CSDP as at the Voting Record Date are entitled to attend or be represented by proxy at the General Meeting. Murray & Roberts Shareholders who are unable to attend the General Meeting but wish to be represented thereat, are requested to complete and return the attached form of proxy in accordance with the instructions contained therein. The duly completed forms of proxy must be received by the Transfer Secretaries by no later than 11:00 on Monday, 4 November 2013.

DematerialisedShareholdersasattheVotingRecordDatewhohavenotelected“ownname”registrationinthesub-registermaintainedby a CSDP, must provide their CSDPs or Brokers with their instruction for attendance and/or voting at the General Meeting in the manner stipulated in the custody agreement governing the relationship between such Murray & Roberts Shareholders and their CSDPsorBrokers.TheseinstructionsmustbeprovidedtotheCSDPsorBrokersbythecut-offtimeanddateadvisedbytheCSDPsor Brokers for instructions of this nature. Should they wish to attend the General Meeting, they must request a Letter of Representation from their CSDP or Broker. If no instructions are provided to their CSDPs or Brokers, then voting will take place in terms of the custody agreement entered into between themselves and the CSDPs or Brokers concerned.

If you hold your Murray & Roberts Shares in certificated form through a nominee, you should timeously make the necessary arrangements with your nominee.

Murray & Roberts does not accept responsibility and will not be held liable for any failure on the part of the CSDP of a Dematerialised Shareholder to notify such Shareholders of the General Meeting or any business to be conducted thereat.

EXCHANGE CONTROL REGULATIONS PERTAINING TO NON-RESIDENTS

In terms of the Exchange Control Regulations of South Africa:

• Anysharecertificates thatmightbe issuedon theJSEtoMurray&RobertsShareholdersnot resident inSouthAfricawillbeendorsed“Non-Resident”;

• Anynewsharecertificates,dividendandresidualcashpaymentsbasedonemigrants’sharescontrolledintermsoftheExchangeControl Regulations, will be forwarded to the Authorised Dealer in foreign exchange controlling their blocked assets. The election by emigrants for the above purpose must be made through the authorized dealer in foreign exchange controlling their blocked assets.Suchsharecertificateswillbeendorsed“Non-Resident”;and

• Dividendandresidualcashpaymentsduetonon-residentsarefreelytransferablefromtheRepublicofSouthAfrica.

4

SALIENT DATES AND TIMES

The definitions and interpretations commencing on set out on page 5 of the Circular apply, mutatis mutandis, to the following salient dates and times:

Key action 2013

Posting Record Date to be eligible to receive the Circular Friday 27 September

Posting of Circular to Murray & Roberts Shareholders Monday 7 October

First Court Date* Tuesday 8 October

Posting of Scheme Booklet on or about* Monday 14 October

Last Day to Trade to participate in and vote at the General Meeting Friday 25 October

Voting Record Date to participate in and vote at the General Meeting Friday 1 November

Last day to lodge forms of proxy in respect of the General Meeting by 11:00 Monday 4 November

General Meeting to be held immediately following the conclusion of the Annual General Meeting scheduled at 11:00 on the same date Wednesday 6 November

Result of General Meeting released on SENS Wednesday 6 November

Result of General Meeting published in the South African press Thursday 7 November

Clough General Meeting and Scheme Meeting* Friday 15 November

Second Court Date* Wednesday 20 November

Suspension of trading in Clough shares on ASX* Thursday 21 November

Clough Special Dividend payment date Thursday 3 December

Scheme Implementation Date and payment of Scheme Consideration* Wednesday 11 December

* Applicable to Clough shareholders only

Notes:1. The above dates and times are subject to amendment. Any material amendment will be released on SENS and published in the South African press.2. All times quoted in the Circular are local times in South Africa on a 24-hour basis, unless specified otherwise.3. No orders to dematerialise or rematerialise securities will be processed from the Business Day following the Last Day to Trade up to and including the

Voting Record Date, but such orders will again be processed from the first Business Day after the Voting Record Date.4. The certificated register will be closed between the Last Day to Trade and the Voting Record Date.5. If the General Meeting is adjourned or postponed, forms of proxy submitted for the General Meeting will remain valid in respect of any adjournment

or postponement of the General Meeting unless the contrary is stated on such form of proxy.

5

DEFINITIONS

In the Circular, the annexures and attachments hereto, unless a contrary intention is indicated, references to the singular include the plural and vice versa, words denoting one gender include the others, expressions denoting natural persons include juristic persons and associations of persons and vice versa, and the words in the first column hereunder have the meaning stated opposite them in the second column, as follows:

“Acquisition” the acquisition by Murray & Roberts, through its wholly owned subsidiary, Murray & Roberts (Aus) of the Clough Minority Shares together with the cancellation of the Clough Options and the Clough Performance Rights pursuant to the Option Offer and Performance Right Offer, for the Consideration;

“Amended and Restated CTA” the amendments to and restatement of the CTA dated 16 September 2013, entered into by MRL(asborrowerandguarantor),Murray&Roberts(Aus)(asco-borrowerandguarantorpostthe acquisition of the Clough Minority Shares), Murray & Roberts (as a guarantor), and certain of its subsidiaries (as guarantors), the terms of which is set out in Annexure 6 to the Circular;

“Annual General Meeting” the 65th Annual General Meeting of Murray & Roberts Shareholders to be held at 11:00 at Douglas Roberts Centre, 22 Skeen Boulevard, Bedfordview, Johannesburg on Wednesday, 6 November 2013;

“ASIC” Australian Securities and Investment Commission;“ASX” ASX Limited ACN 008 624 691 or, as the context requires, the financial market operated by it;“ASX Listing Rules” the official listing rules of ASX; “ATO” Australian Taxation Office and includes the Commissioner of Taxation;“Australian Dollar” or “A$” or “A$ cents”

the official currency of Australia;

“BAM Clough” the joint venture formed between Royal Netherlands Harbourworks and Clough in 1964, to provide marine facility engineering and construction services to the resources industry, currently trading as BAM Clough International;

“BBSW” Australian Bank Bill Reference Rate;“Board” or “Directors” the board of directors of Murray & Roberts as at the Last Practicable Date, whose names are

listed on page 10 of the Circular;“Broker” any person registered as a broking member in equities in terms of the rules of the JSE in

accordance with the provisions of the Financial Markets Act;“Business Day” any day other than a Saturday, Sunday or official public holiday in South Africa and Australia

and when used in the context of the Scheme means a Business Day within the meaning of the ASX Listing Rules;

“Capital Payment” expected cash payment of A$1,32 per share to be paid by Murray & Roberts to eligible Scheme Participants equating to approximately A$393,6 million (ZAR3 664 million) in cash. Such Capital Payment excludes the expected Clough Special Dividend of A$0,14 per share. In circumstances where it is believed that the ATO may make a determination which would have the effect of the Clough Special Dividend not being Fully Franked or imputation (attributable) credits being denied, the Clough Independent Directors reserve the right to reduce or not to determine the Clough Special Dividend. If the Clough Special Dividend is not determined or if it is reduced the Capital Payment will be adjusted accordingly so that Scheme Participants receive the Consideration of A$1,46 per Clough Share;

“CertificatedShareholders” shareholders who hold Certificated Shares;“CertificatedShares” Murray & Roberts Shares which are not dematerialised in terms of the requirements of Strate,

title to which is represented by a share certificate or other Documents of Title;“Circular” this document, dated 7 October 2013, including the annexures, Notice of General Meeting

and form of proxy contained herein;“Clough” Clough Limited, ABN 59 008 678 813, a company incorporated in Australia the shares

of which are traded on the ASX (ASX code: CLO), with its registered address at Alluvion, 58 Mounts Bay Road, Perth, Western Australia 6000;

“Clough AMEC” the joint venture formed in 2004 between Clough and AMEC with the purpose of providing asset support services for oil and gas operations in Australia and Southeast Asia;

“Clough Board” or “Clough Directors”

the board of directors of Clough (as constituted from time to time);

6

“Clough Coens” Clough Coens Commissioning and Completions, an incorporated joint venture between Clough and Coens Energy that provides highly specialised commissioning and completions services to onshore and offshore oil and gas facilities, including drilling rigs and fabricated process equipment manufactured in Korea and China;

“Clough General Meeting” a general meeting of Clough Shareholders duly convened by Clough to approve the giving of Financial Assistance and Financial Benefits;

“Clough Group” Clough and its subsidiaries;“Clough Independent Directors” Clough Directors not associated with Murray & Roberts;“Clough Loan” the loan from Clough to Murray & Roberts (Aus) of at least A$184,5 million, (ZAR1 718 million)

funded from Clough’s existing cash reserves in order to partially satisfy the Consideration. The Clough Loan amount will be equal to A$200,0 million:a) plus the amount by which the Capital Payment is adjusted in the event of the Special

Dividend being less than $0,14 per Clough Share; andb) less any amounts paid or payable by Clough pursuant to the Option Offer and the

Performance Right Offer (expected to be approximately A$15,5 million (ZAR144 million));“Clough Minority Shareholders” shareholders of Clough Minority Shares;“Clough Minority Shares” 298 153 192 ordinary shares in the issued share capital of Clough, held by Clough Minority

Shareholders (excluding the Clough Shares and vesting Clough Options and Clough Performance Rights);

“Clough Option” an option to subscribe for a Clough Share issued by Clough under the Clough employee option plan, both vested and unvested;

“Clough Performance Right” a right to be issued with or transferred into Clough Shares, or be paid the market price of those shares (at the election of Clough), as granted by Clough under the Clough executive incentive scheme, including (after the date of their grant) up to A$1,75 million, (ZAR16,3 million) in Performance Rights expected to be granted in October 2013 by Clough;

“Clough Share” A fully paid ordinary share in the capital of Clough;“Clough Shareholders” each person who is a registered holder of a Clough Share at the Scheme Record Date;“Clough Special Dividend” a Fully Franked dividend of up to A$0,14 per share which, if determined by the ATO, will

be paid by Clough following approval of the Scheme, and subject to the Scheme becoming Effective, to those persons registered as Clough Shareholders on the Special Dividend Record Date;

“Coens Energy” a Korean oil and gas manpower and logistics firm, and a party to the Clough Coens incorporated joint venture;

“Companies Act” the South African Companies Act, No. 71 of 2008, as amended from time to time;“Companies Regulations” the Companies Regulations, 2011, promulgated under the Companies Act, as amended from

time to time;“Competition Act” The South African, Competition Act, No. 89 of 1998, as amended from time to time;“Competition Commission” the Competition Commission as contemplated in the Competition Act;“Competition Tribunal” the Competition Tribunal as contemplated in the Competition Act;“Conditions Precedent” the conditions precedent to which the Acquisition is subject, a summary of which is set

out in section 4.2 of the Circular and which are fully set out in schedule 1 to the Scheme Implementation Agreement;

“Consideration” the total purchase consideration payable, expected to be approximately A$461,4 million (ZAR4 296 million) comprising the:– Capital Payment (approximately A$393,6 million (ZAR3 664 million));− Clough Special Dividend (approximately A$41,7 million (ZAR388 million)); − Option Offer Consideration and Performance Right Offer Consideration (approximately

A$15,5 million (ZAR144 million)) pursuant to the Option Offer and Performance Right Offer; and

− estimated Acquisition transaction costs of approximately A$10,6 million (ZAR99 million) (excluding VAT);

“Corporations Act” Australian Corporations Act 2001 (Cth);“Court” the Federal Court of Australia or any other court of competent jurisdiction under the

Corporations Act agreed in writing by Clough and Murray & Roberts;“CSDP” Central Securities Depository Participant, as defined in Section 1 of the Financial Markets Act,

appointed by individual shareholders for purposes of, and in regard to, the dematerialisation of Documents of Title for the purpose of incorporation into Strate;

“CTA” common terms agreement dated 30 November 2011, entered into by MRL (as borrower), Murray & Roberts (as a guarantor) and certain of its subsidiaries (as guarantors);

7

“Dematerialised Shareholders” Murray & Roberts Shareholders who hold Murray & Roberts Shares on the South African branch register which have been incorporated into the Strate system and which are no longer evidenced by physical Documents of Title, the evidence of ownership of which is determined electronicallyandrecordedinsub-registersmaintainedbyCSDPs;

“Dematerialised Shares” Murray & Roberts Shares that have been dematerialised or have been issued in dematerialised form, and are held on a sub-register of Murray & Roberts Shareholders administered by a CSDP;

“Documents of Title” share certificates, certified transfer deeds, balance receipts or any other physical Documents of Title to Murray & Roberts Shares;

“Effective” when used in relation to the Scheme, the coming into effect of the Scheme order anticipated on the Scheme Implementation Date and pursuant to Section 411(10) of the Corporations Act;

“Effective Date” the date on which the Scheme becomes Effective;“EPC” engineering, procurement and construction services;“EPCM” engineering, procurement, construction and management services;“Exchange Control Regulations” the Exchange Control Regulations, 1961, as amended, promulgated in terms of Section 9 of

the South African Currency and Exchanges Act No. 9 of 1933, as amended;“Executive Management” the executive management of Murray & Roberts or Clough as the context requires;“Existing Clough Shares” 478 957 478 Clough Shares, held by MRL;“FEED” front end engineering design;“Financial Markets Act” the South African Financial Markets Act, No. 19 of 2012, as amended from time to time;“Financial Assistance” the financial assistance to be given by Clough Group to Murray & Roberts (Aus) and its

related parties in connection with the Scheme by Clough providing the Clough Loan to Murray & Roberts (Aus);

“FinancialBenefits” the financial benefits to be given by Clough or any other related party of Clough to Murray & Roberts (Aus) in connection with the Scheme which requires the approval of Scheme Participants for the purposes of Chapter 2E of the Corporations Act, including the financial benefits under the Clough Loan;

“FIRB” Foreign Investment Review Board of Australia;“First Court Date” the first day on which the application made to the Court for the orders under the Corporations

Act that the Scheme Meeting be convened is heard;“FLNG” floating liquefied natural gas;“Forge” Forge Group Limited, ACN 065 464 226, a company incorporated in Australia and whose

shares are traded on the ASX (ASX code: FGE); “Forge Group” Forge and its subsidiaries;“Franking Credits” theunderlyingtaxpaidbyacompanyonpre-taxprofitsfromwhichanydividendswerepaid,

which may reduce the amount of tax an individual shareholder pays on such dividend income received in order to prevent double taxation;

“FSP” Murray & Roberts Holdings Limited Forfeitable Share Plan approved by Murray & Roberts Shareholders in October 2012;

“Fully Franked” a dividend on which Clough has already paid income tax to the ATO entitling eligible Clough Shareholders to a Franking Credit for the full amount of tax Clough has already paid;

“FY2012” financial year ended 30 June 2012;“FY2013” financial year ended 30 June 2013;“FY2014” financial year ending 30 June 2014;“FY2015” financial year ending 30 June 2015;“FY2016” financial year ending 30 June 2016;“Gautrain” Gautrain Rapid Rail Link;“General Meeting” the General Meeting of Murray & Roberts Shareholders to be held at Douglas Roberts

Centre, 22 Skeen Boulevard, Bedfordview, Johannesburg on Wednesday, 6 November 2013 immediately following the conclusion of the Annual General Meeting scheduled at 11:00 on the same date, which meeting is convened by way of the Notice of General Meeting;

“Government Agency” anygovernmentorrepresentativeofagovernmentoranygovernmental,semi-governmental,administrative, fiscal, regulatory or judicial body, department, commission, authority, tribunal, agency, competition authority or entity and includes any minister (including, for the avoidance of doubt, the Treasurer of the Commonwealth of Australia), ASIC, ATO, ASX, FIRB, JSE, the SARB and any regulatory organisation established under statute or any stock exchange;

“GPMOF” Gorgon Pioneer Materials Offloading Facility;“Grant Samuel” Grant Samuel & Associates Pty Limited, ACN 003 241 745, a company incorporated in

Australia;“GST” Goods and Services Tax levied by the ATO in Australia. GST has the same meaning given to

that expression in the A New Tax System (Goods and Services Tax) Act 1999;

8

“HeadlineProfitPerShare” profit per Murray & Roberts Share excluding profits or losses associated with the sale or termination of discontinued operations, fixed assets or related businesses, or from any permanent devaluation or write off of their values calculated by dividing the Company’s adjusted profit by the weighted average number of issued shares;

“IFRS” International Financial Reporting Standards and Interpretations adopted by the International AccountingStandardsBoard(“IASB”)andtheInternationalFinancialReportingInterpretationsCommittee of the IASB;

“Income Tax” income tax levied in terms of the Income Tax Act;“Income Tax Act” the South African Income Tax Act No. 58 of 1962, as amended from time to time;“Independent Expert” Grant Samuel, the Independent Expert appointed in respect of the Scheme by Clough, in

terms of the Scheme Implementation Agreement;‘Independent Expert Report” the report in connection with the Scheme to be prepared by the Independent Expert in

accordance with the Corporations Act, and ASIC policy and practice, for inclusion in the Scheme Booklet;

“JIBAR” Johannesburg Interbank Agreed Rate;“JSE” JSE Limited, registration number 2005/022939/06, a public company duly incorporated

in accordance with the laws of South Africa, licensed as an exchange under the Financial Markets Act;

“JSE Listings Requirements” or “Listings Requirements”

the Listings Requirements of the JSE, as amended from time to time by the JSE;

“Last Day to Trade” the last Business Day to trade in Murray & Roberts Shares in order to be included in the shareholder register on the Voting Record Date;

“Last Practicable Date” 20 September 2013, being the last practicable date prior to finalisation of the Circular;“Letter of Representation” a letter of representation issued by a CSDP or Broker to a Murray & Roberts Shareholder for

the purposes of authorising attendance by the Murray & Roberts Shareholder at the General Meeting;

“LNG” liquefied natural gas;“MOI” the memorandum of incorporation of Murray & Roberts; “MRL” Murray & Roberts Limited, registration number 1979/003224/06, a public company duly

incorporated in accordance with the laws of South Africa;“Murray & Roberts” or the “Company”

Murray & Roberts Holdings Limited, registration number 1948/029826/06, a public company incorporated in accordance with the laws of South Africa, the shares of which are listed on the JSE (JSE: MUR), with its registered address at Douglas Roberts Centre, 22 Skeen Boulevard, Bedfordview, 2007, South Africa;

“Murray & Roberts Shares” ordinary shares with no par value in the authorised and issued share capital of Murray & Roberts;

“Murray & Roberts Shareholders” shareholders of Murray & Roberts Shares;“Murray & Roberts (Aus)” Murray & Roberts Pty Ltd, ACN 105 617 865, a private company duly incorporated in Australia; “Murray & Roberts Group” or the “Group”

Murray & Roberts and its subsidiaries;

“Notice of General Meeting” the notice of General Meeting forming part of the Circular;“Option Offer” an offer made by Clough, in accordance with the terms of the Scheme Implementation

Agreement to each holder of Clough Options to cancel each of their Clough Options for the Option Offer Consideration;

“Option Offer Consideration” A$1,46 per Clough Share, which is equivalent to the sum of the Capital Payment plus the Clough Special Dividend, payable to Scheme Participants less the exercise price of the relevant Clough Options;

“Performance Right Offer” an offer made by Clough, in accordance with the terms of the Scheme Implementation Agreement, to each holder of Clough Performance Rights to cancel each of their Clough Performance Rights for the Performance Right Offer Consideration, conditional on the Scheme becoming Effective;

“Performance Right Offer Consideration”

A$1,46 per Clough Share, which is equivalent to the sum of the Capital Payment plus the Clough Special Dividend, payable to Scheme Participants;

“Posting Record Date” the date determined by the Board in accordance with Section 59 of the Companies Act for Murray & Roberts Shareholders to be eligible to receive the Circular;

“Reporting Accountant” or “Auditors” or “Independent Reporting Accountant” or “Deloitte & Touche”

Deloitte & Touche, Registered Auditors;

9

“SAICA” South African Institute of Chartered Accountants;“SARB” South African Reserve Bank;“Scheme” the proposed scheme of arrangement, pursuant to the Scheme Implementation Agreement

between Clough and the Scheme Participants under Part 5.1 of the Australian Corporations Act which if implemented will give effect to the Acquisition, subject to any alterations or conditions made or required by the Court under Section 411(6) of the Corporations Act and approved in writing by Clough and Murray & Roberts (Aus);

“Scheme Booklet” the information to be despatched by Clough to Clough Shareholders and approved by the Court, including the Scheme, explanatory statement in relation to the Scheme issued pursuant to Section 412 of the Corporations Act and registered with ASIC, the Independent Expert’s Report, the deed poll, a summary of the Scheme Implementation Agreement and a notice of meeting convening the Scheme Meeting and Clough General Meeting (together with proxy forms);

“Scheme Consideration” The total amount of approximately A$404,2 million (ZAR3 763 million) payable by Murray & Roberts comprising:– the Capital Payment (A$393,6 million (ZAR3 664 million)) in cash; and– estimated Acquisition transaction costs of approximately A$10,6 million (ZAR99 million);

“Scheme Implementation Agreement”

the written agreement in relation to the Acquisition, entered into between Murray & Roberts, Murray & Roberts (Aus) and Clough on 28 August 2013, a full copy of which can be obtained from Murray & Roberts’ website hosted at www.murrob.com, and which document will be available for inspection;

“Scheme Implementation Date” the fifth Business Day following the Scheme Record Date, or such other date as ordered by the Court or agreed between Clough and Murray & Roberts (Aus);

“Scheme Meeting” the meeting ordered by the Court to be convened pursuant to Section 411(1) of the Corporations Act in respect of the Scheme;

“Scheme Participant” each person who is a Clough Shareholder as at the Scheme Record Date, other than MRL;“Scheme Record Date” 17:00 WAST on the ninth Business Day following the Effective Date or such other date and

time as Clough and Murray & Roberts (Aus) agree;“Scheme Share” A Clough Share held by a Scheme Participant;“Second Court Date” the second day on which an application made to the Court for the Scheme order is heard

or, if the application is adjourned for any reason, the second day on which the adjourned application is heard;

“SENS” the Stock Exchange News Service of the JSE;“South Africa” the Republic of South Africa;“South African Group” the Company and those of its subsidiaries incorporated in South Africa;“Special Dividend Record Date” 17:00 WAST on the fifth Business Day following the Effective Date or such other date and time

as Clough and Murray & Roberts (Aus) agree;“Strate” Strate Limited, registration number 1998/022242/06, a public company duly incorporated

in accordance with the laws of South Africa and a registered central securities depository in terms of the Financial Markets Act;

“Strate system” an electronic custody, clearing and settlement environment, managed by Strate, for all share transactions concluded on the JSE and off-market, and in terms ofwhich transactions insecurities are settled and transfers of ownership in securities are recorded electronically;

“Sub-Register” the record of Dematerialised Shares administered and maintained by a CSDP and which forms part of the Company’s register of members as defined in the Companies Act, excluding any nominees;

“Transfer Secretaries” Link Market Services South Africa Proprietary Limited, registration number 2000/007239/07, a company duly incorporated in accordance with the laws of South Africa;

“UCW” Union Carriage & Wagon Company Pty Limited;“VAT” value-addedtaxleviedintermsoftheSouthAfricanValue-AddedTaxAct,No.89of1991,as

amended from time to time;“Voting Record Date” the date on which Murray & Roberts Shareholders must be included in the shareholder register

in order to be eligible to vote at the General Meeting;“WAST” Western Australia Standard Time; and“ZAR” or “Rand” or “R” or “cents” the lawful currency of South Africa. A$ amounts have been translated into ZAR at the ZAR/

A$ exchange rate as at the close of South African business on the Last Practicable Date, of ZAR9,31/A$. A$ amounts stated as at FY2013 and/or FY2012, have been translated at the 30 June 2013 (ZAR9,03) or 30 June 2012 (ZAR8,40), spot rate. A$ amounts during FY2013, have been translated at an average rate for that period (ZAR9,05). Any other A$ amount, included in the Circular relating to the Murray & Roberts Group has been extracted from the Annual Financial Statements for FY2013.

10

CIRCULAR TO SHAREHOLDERS

DIRECTORSM Sello* (Chairman)

HJ Laas (Group Chief Executive)

AJ Bester (Group Financial Director)

DD Barber*

NBLanga-Royds*

JM McMahon#*

WA Nairn*

RT Vice*

* Non-executive# British Citizen

Murray & Roberts Holdings Limited(Incorporated in the Republic of South Africa)

(Registration number: 1948/029826/06)(JSE share code: MUR) (ISIN: ZAE000073441) (ADR Code: MURZY)

(the “Company”)

1. INTRODUCTION AND PURPOSE OF THE CIRCULAR

Murray & Roberts announced on Tuesday, 30 July 2013, a proposed acquisition involving the purchase of all of the Clough Minority Shares, that is, the shares that Murray & Roberts does not already own, as well as payments to cancel the Clough Options and Clough Performance Rights held by Clough employees.

Subsequently, on 29 August 2013, Murray & Roberts announced, post the successful completion of a confirmatory due diligence, that it had entered into a binding Scheme Implementation Agreement with Clough, on 28 August 2013, whereby the Murray & Roberts Group, through its wholly owned subsidiary, Murray & Roberts (Aus), will acquire the Clough Minority Shares, at A$1,46 cash per share, expected to consist of a cash payment of A$1,32 per share to be paid by Murray & Roberts (the Capital Payment) and the Clough Special Dividend of A$0,14 per share paid by Clough. The price of the payments for the Clough Options and Clough Performance Rights pursuant to the Option Offer and Performance Right Offer respectively has been determined with reference to the relevant contractual arrangements.

The payment to the Scheme Participants as well as the payments under the Option Offer and Performance Right Offer, and estimated transaction costs, is expected to result in the Consideration of approximately A$461,4 million, (ZAR4 296 million). The Acquisition will be implemented by way of the Scheme.

Subject to the fulfilment or waiver, as the case may be, of the Conditions Precedent (a summary of which is set out in section 4.2 of the Circular) and following the implementation of the Acquisition, Clough will become a wholly owned subsidiary of Murray & Roberts, held through Murray & Roberts (Aus) and MRL respectively, each a wholly owned subsidiary of Murray & Roberts.

The purpose of the Circular is to:

• provideMurray&RobertsShareholderswithrelevantinformationregardingtheAcquisitionandtheimplicationsthereof,in order to enable Murray & Roberts Shareholders to make an informed decision whether to vote in favour of the ordinary resolutions required to implement the Acquisition; and

• convenetheGeneralMeetingatwhichmeetingtheordinaryresolutionsrequiredtoapproveandimplementtheAcquisitionwill be proposed.

11

The Board has evaluated the rationale for, and the terms and conditions of, the Acquisition, and believes that it iscompellingforstrategicandfinancialreasons.Forthisreason,theBoardisoftheopinionthattheAcquisitionisconsistentwithMurray&Roberts’strategyandwillsignificantlyenhanceMurray&RobertsShareholdervalue.Accordingly, after due consideration, the Board unanimously recommends Murray & Roberts Shareholders vote in favour of all the resolutions necessary to approve and implement the Acquisition, as set out in the Notice of General Meeting.

2. BACKGROUND TO THE PARTIES

2.1 History and nature of the business of Murray & Roberts

2.1.1 Incorporation and history

Murray & Stewart was founded in South Africa in 1902 by John Murray and James Stewart. In 1934, John Murray’s son, Douglas Murray, and Douglas Roberts entered into a partnership to form Roberts Construction. The Company was incorporated as Roberts Construction Holdings Limited and registered in South Africa on 2 June 1948 as a public company.

In 1951, Roberts Construction Holdings Limited became a public company listed on the JSE and, in 1967, Murray & Stewart and Roberts Construction merged to become Murray & Roberts Limited. During the 1970s through the 1990s, the Group diversified the industries in which it operated, growing and developing its operations in the fields of process engineering, project management and design.

During the 2000s, the Group underwent a strategic change through a series of key disposals and acquisitions. These included the disposal of Unitrans in 2004 and the acquisitions of Cementation in 2004 and Concor in 2006. In addition, the Group became a shareholder in Clough in 2003, of which it currently holds 61,6%.

In July 2011, Henry Laas and Cobus Bester were appointed as Group Chief Executive and Group Financial Director respectivelyandlaunchedathree-yearrecoveryandgrowthstrategy,recommittingtheGrouptotheobjectiveofdeliveringinfrastructure to enable economic and social development in a sustainable way.

The recovery phase of this strategy was focussed on improving liquidity and improving operational performance, and the growthphaseprimarilyondisposalsandacquisitions,asseveraloftheGroup’sbusinesseswereidentifiedasnon-coreandits operating platforms were not optimally aligned with key market sectors and geographies identified. At the conclusion of FY2012, the Group had disposed of the Steel Business, including Cisco and in the second half of FY2013 disposed of UCW. Finally, at year end 2013, the Group announced the disposal of its Construction Products Africa operating platform (excluding Hall Longmore), comprising the Group’s construction materials and manufacturing businesses. The businesses that were disposed of are Much Asphalt, Rocla, Technicrete and Ocon Brick.

The Group ended FY2013 having successfully negotiated its recovery phase in 2012 and accomplished all significant milestones targeted in the first of its two growth years. In the first of the growth years the Group returned to profitability, signalling more robust and sustainable levels of revenue and profit.

On 30 July 2013, Murray & Roberts announced the proposed Acquisition, executing a binding Scheme Implementation Agreement on 28 August 2013 to effect the Acquisition.

2.1.2 Nature of the business

Murray & Roberts has created employment, developed skills, installed infrastructure, delivered services, applied technology andbuiltcapacitythroughoutSouthandsub-SaharanAfricafor111years,makingwhattheBoardbelievestobeasignificantcontributiontosustainablesocio-economicdevelopmentintheregion.

The Company offers civil, mechanical, electrical, mining and process engineering; and general building, construction and infrastructure development services in the global underground mining market, and in the natural resources and infrastructure sectors of selected emerging markets.

Murray & Roberts operates in Southern Africa, the Middle East, Asia, Australasia and North and South America. The head office of the Company is based in Johannesburg, South Africa, and it has principal offices in Australia, Botswana, Canada, Chile, Ghana, Namibia, the United States of America, the United Arab Emirates and Zambia.

Murray&Robertsisagroupofworld-classcompaniesandbrandsalignedtothesamepurposeandvision,andguidedbythe same set of values:

• Purpose–Deliveryofinfrastructuretoenableeconomicandsocialdevelopmentinasustainableway.

• Vision – By 2020Murray & Roberts will be the leading diversified engineering and construction group in the globalunderground mining market and selected emerging markets in the natural resources and infrastructure sectors.

• Values–Care,Integrity,Respect,AccountabilityandCommitment.

2.1.3 Organisational Structure

The Murray & Roberts Group operates through a holding company structure. The Company conducts all of its business through its subsidiaries, joint ventures and associates.

12

Structurally, the Group began FY2013 with five operating platforms which, by the end of the financial year, had reduced to four platforms after the disposal of the Construction Products Africa platform. Two platforms represent the Group’s regional businesses (with primarily an African focus) and the remaining two, its international businesses (with a global focus).

The table below presents the primary operating companies organised by operating platform, as well as the geographic markets and market sectors in which each platform operates.

Operating platforms CompaniesMain geography markets Market sectors

Construction Africa and Middle East

Murray & Roberts Construction Murray & Roberts Marine Murray & Roberts Middle EastMurray & Roberts ConcessionsTolcon

Regional:Africa Southeast AsiaMiddle East

Metals and MineralsEnergy, IndustrialInfrastructureBuilding

Engineering Africa Murray & Roberts Projects GenrecWade WalkerConcor EngineeringMurray & Roberts Water

Regional:Africa

Metals and MineralsEnergy (Oil and Gas, Power)Industrial

Construction Global Underground Mining

Murray & Roberts CementationCementation CanadaRUC CementationCementation Sudamérica

International:AfricaSoutheast AsiaAustralasiaAmericas

Metals and Minerals

Construction Australasia Oil and Gas and Minerals

Clough International:AustralasiaSoutheast AsiaAfrica

IndustrialMetals and Minerals (Surface)Energy (Oil and Gas, Power)

2.1.4 Disposal of non-core assets

As discussed above and as disclosed in the Group Annual Financial Statements for FY2013, the Group made substantial progress with the implementation of its strategy through the following disposals:

• On 29 January 2013, the Group announced the disposal of the business, assets and liabilities of UCW. The disposal became effective on 13 June 2013 and the Group realised a fair value in the sale price, which was in excess of the carrying value.

• ThedisposaloftheCapeTownIronandSteelWorkswhichwasannouncedduringFY2012becameunconditionalfollowingapproval received from the Competition Commission, with proceeds of ZAR80 million.

• On28June2013,theGroupannouncedthedisposalofitsConstructionProductsAfricaoperatingplatform(excludingHall Longmore). The group of businesses included Much Asphalt, Rocla, Technicrete and Ocon Brick. The total cash consideration in respect of the disposal will be approximately ZAR1 325 million before transaction costs. Of the total cash consideration, ZAR1 150 million will be received on the effective date, ZAR75 million is receivable 12 months after the effective date and ZAR100 million is receivable 24 months after the effective date of such transaction. Negotiations with potential buyers for Hall Longmore are ongoing and Murray & Roberts Shareholders will be advised in due course of the outcome thereof.

The proceeds from the disposal of these businesses will be utilised to reduce short term debt in South Africa. Further informationregardinganymaterialcontractsresultingfromtheabovedisposalsofnon-coreassets,duringFY2013,aresetout in section 11 of the Circular.

2.1.5 Update on the Group’s major claims processes

Murray & Roberts’ uncertified revenue, representing outstanding claims, remained largely unchanged as at FY2013, at ZAR2,1 billion (June 2012: ZAR2,0 billion).

During FY2013 the Group continued to pursue its entitlements in terms of these claims including the completed GPMOF, Dubai International Airport and Gautrain project. It is expected that the legal and commercial processes on these claims will be closed out towards the end of FY2016.

The Board and management remain committed to the resolution of all contractual disputes and the collection of proceeds from claim settlements, while recognising that this will continue to be a challenging and protracted process.

The eventual collection of these expected significant cash proceeds from claim settlements is envisaged to be applied towards funding the Group’s growth aspirations.

13

2.1.6 Prospects for Murray & Roberts as enlarged by the Acquisition

Murray&Robertscurrentlyconsistsofworld-classcompaniesandbrandsalignedto thesamepurposeandvision,andguided by the same set of values. By 2020, Murray & Roberts aims to be the leading diversified engineering and construction group in the global underground mining market and selected markets in the natural resources and infrastructure sectors.

The recovery and growth strategy was a short term strategy to be implemented over the period from FY2012 to the end of FY2014. The new strategic future strategy will follow the recovery and growth strategy and is intended to be the plan for the next phase of the Group’s progress towards achieving its aim for 2020.

TosupporttheGroup’slong-termvision,theBoardhasredefinedthemarketsectorsonwhichtofocus.Broadlystated,theBoard has identified energy (oil and gas and power) and mining and minerals as the sectors presenting the most attractive medium-to-long-termgrowthopportunities.ThesesectorswillunderpintheGroup’splansforthenewstrategicfuturestrategy.

The Group’s improved balance sheet will allow it to engage the future with confidence. The Acquisition will contribute to the execution of the Company’s strategy by increasing the Group’s exposure to the oil and gas sector and thereby more strongly positioning the Group for its new strategic future strategy.

The Board is pleased with the significant improvement in FY2013 over the FY2012 financial results and expects earnings from the international operating platforms (which includes Clough) to grow faster than those from the regional operating platforms in FY2014.

The international businesses are expected by the Board to, over time, experience stronger growth relative to the regional businesses. Nevertheless, achieving increased profitability in the South African operations, remains a priority.

In addition to ongoing growth opportunities in Clough’s existing geographic markets, Murray & Roberts sees significant potential to leverage Clough’s expertise to pursue opportunities in and around Africa’s rapidly emerging oil and gas markets, for both existing and new clients.

2.2 History and nature of the business of Clough

2.2.1 Incorporation and history

Clough was founded in 1919 by John Oswald Clough. Harold Clough joined his father’s business in 1953 and oversaw Clough’s transformation from a local civil construction company, into a significant engineering force, beginning with the successful execution of the Narrows Bridge contract. Clough became an engineering construction company rather than a building company and retained its building division, but it was only a small part of the total operation.

In the 1950’s Clough diversified its services into civil and heavy engineering contracting, while the 1960’s set the tone for Clough’s future as the company entered the oil and gas sector.

Clough began moving into the resources arena and formed the Harbourworks Clough Joint Venture in 1964, and was subsequentlyawardedtheParkerPointironoreloadoutjettyforHamersleyIron.Thiswasthestartofa50-yearrelationshipbetween Clough and Royal Netherlands Harbourworks, known as BAM Clough.

The Barrow Island Oil Field development, the Group’s first oil and gas project was completed in 1966, and it continues to operate today. In the 1970’s and the 1980’s Clough continued to expand, opening an office in Queensland in 1973, and delivering its first project in Africa, the Nigerian Agricultural Project. In 1975 Clough was awarded its first major construction contract for the iconic Swan Brewery in Perth. The early 1980’s saw the award of the Group’s first major offshore project, Woodside’s North Rankin ‘A’, and entry into the LNG market with the construction of Australia’s first LNG Jetty for Woodside’s North West Shelf. Clough also established operations in Papua New Guinea, which remains an important region for its business today.

Clough’s reputation for technical innovation was further enhanced during the 1990’s when the Group was awarded challenging projects, including:

• thePagerunganGasField,builtonaremoteislandinIndonesia,withnoexistinginfrastructure;

• theEPCprojectfortheDhodakGasplant,inthemiddleofthePakistanidesert;and

• theonshore/offshoreEastSparProjectinWesternAustralia,whichwonAustralia’stopengineeringaward.

It was at this point that Clough became known as an oil and gas specialist.

During the first decade of the millennium, Clough designed and constructed three LNG load out jetties, built Papua New Guinea’sfirstoilrefineryandsecureditsfirstoperationsandmaintenancecontractfortheConocoPhillips,Bayu-Undanfacilityin the Timor Sea.

In 2004, Murray & Roberts acquired a significant stake in Clough increasing its shareholding in Clough from 4,9% to 29,3%.

14

In 2007, the Clough family sold its remaining shareholding to Murray & Roberts and Harold Clough stepped down as Chairman, signalling the end of a very important part of Clough’s history.

The award of substantial Australian construction projects such as Chevron’s Gorgon and ExxonMobil’s Papua New Guinea LNG projects, further enhanced Clough’s prospects. In 2005, Clough, as part of the Kellogg Joint Venture, was awarded the Gorgon LNG FEED Project, and in 2009 Chevron awarded the Kellogg Joint Venture the Gorgon EPCM contract.

In 2011, Clough made a strategic decision to exit the marine construction sector with the sale of its Marine Construction Division. In 2012, Clough was awarded three contracts for the Wheatstone LNG project:

• Hook-upandCommissioning;

• Operability,ReliabilityandMaintainability;and

• LNGJetty.

Early in 2013, Clough disposed of its shareholding in Forge, a multidisciplinary EPC service provider. Clough also acquired a specialist boutique Australian commissioning contractor e2o Pty Limited and established the Clough Coens joint venture to provide specialist commissioning and completion services to onshore and offshore oil and gas facilities.

2.2.2 Nature of the business

Clough is an engineering and project services company providing engineering, construction and asset support services to energy and resource projects in Australia and Papua New Guinea. It delivers full project lifecycle services. Through BAM Clough, Clough is a market leader in Jetties and Near Shore Marine design and construction in Australia and Papua New Guinea.

Clough focuses on the energy and chemicals sector particularly in oil, conventional gas, LNG and petrochemicals, and in the metals and minerals sector in the iron ore, precious and other metals markets.

2.2.3 Organisational Structure

Clough’s services are delivered through four business divisions.

1. Engineering – Clough’s engineering services are provided across the entire project lifecycle, which is a key competitive differentiator. Clough employs nearly 500 engineers and technical staff across Australia, Papua New Guinea and Asia. Engineering services are supplied to blue chip energy and resources clients. The Clough Group offers full lifecycle engineering services including:

• Conceptevaluation;

• Projectfeasibilitystudies;

• Basisofdesign;

• FEED;

• Detaileddesign;

• SpecialisedprocessLNGengineeringdesign;

• Engineering,procurement,constructionandprojectmanagement;and

• Processoptimisationanddebottlenecking.

2. Capital projects – Clough’s Capital Projects business delivers fully integrated EPC, or any part thereof, including Design andConstruct andConstruct-only solutions formajor energy and resources projects. Capital Projects employs over3 000 engineering, construction and project management staff from bases across Australia and Papua New Guinea. Infrastructure design and construct capabilities include:

• Processfacilities;

• Balanceofplantinfrastructure;

• Powergeneration;

• Compressionfacilitiesandinfieldpipelines;and

• Offshorefabricationcapability.

3. Jetties and near shore marine – Jetties and Near Shore Marine, along with Capital Projects represent Clough’s core foundation businesses, where its focus is on providing excellence in project execution and superior productivity for clients. Through BAM Clough, Clough is a market leader in Jetties and Near Shore Marine design and construction. BAM Clough designs and constructs a range of marine infrastructure for blue chip clients, including:

• Oil,gasandmineralsimportandexportjetties/terminals;

• Portsandportdevelopment;

• Berthingstructures,quaywallsandbreakwaters;

• Intakeandoutfallstructures/pipelines;and

• In-housedesignandconstructcapability.

15

4. Commissioning and asset support – Clough’s Commissioning and Asset Support services help major energy and resource clients’ transition from construction to operations. During 2013, commissioning services were strengthened, with the acquisition of e2o Pty Ltd in January 2013 and the establishment of Clough Coens in May 2013. Clough Coens, a joint venture between Clough and Korean manpower firm, Coens, was established to provide independent and integrated commissioning services to the world’s largest fabrication yards operating out of Korea and China. Asset support services are delivered through a 10-year joint venture with AMEC Engineering Pty Ltd, a Subsidiary of AMEC plc. Clough’scommissioning and asset support services include:

• Onshoreandoffshorepre-commissioningandcommissioning;

• Reliabilitymodelling;

• Operationalreadiness;

• Maintenancemanagementandexecution;

• Shutdownsandturnarounds;

• Supplychainmanagement;

• Operatorsmaintenancestaff,competencyassuranceandtraining(classroomande-training);

• Fullsuiteofparentoilandgas,LNG,andmining&mineralsengineeringandEPCservices;and

• Decommissioning.

2.2.4 Prospects: Favourable outlook for Clough

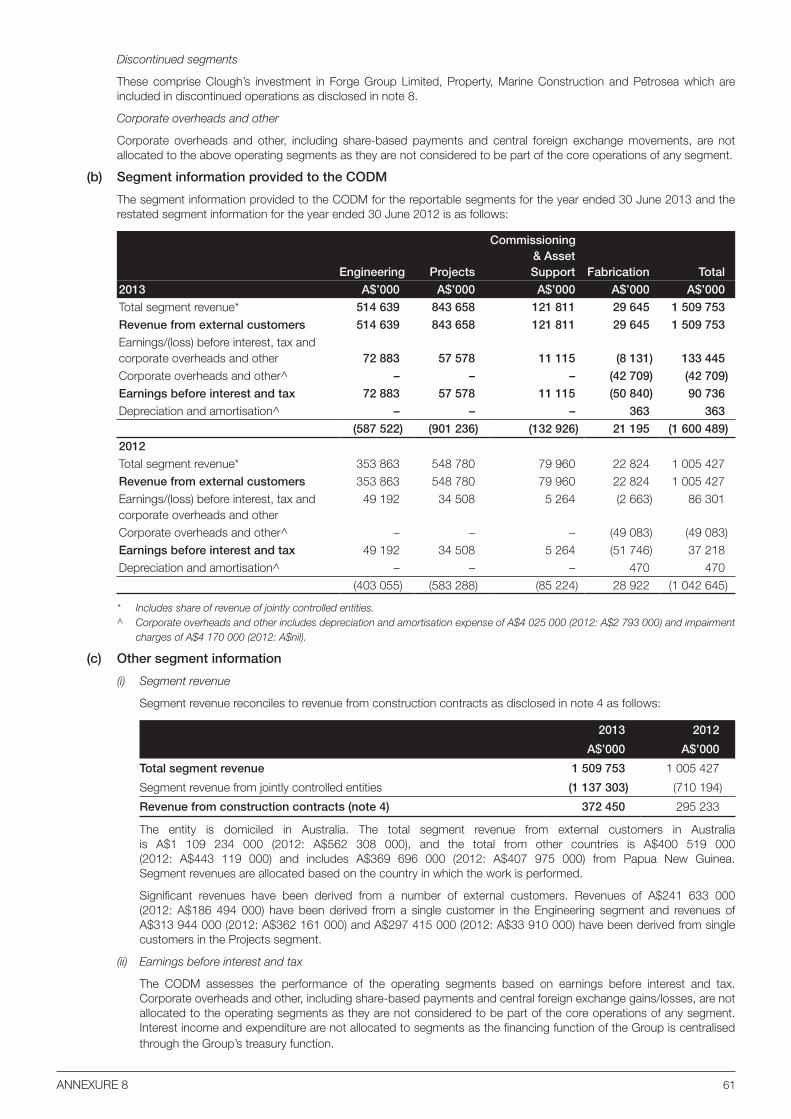

Clough reported record earnings for FY2013, reporting revenue from operations of A$1 635 million (ZAR14 800 million) (refer to reconciliation in Annexure 8, note 1) and earnings before interest and tax of A$90,7 million (ZAR821 million). Clough enters FY2014 with a strong order book of A$2,3 billion (ZAR20,6 billion), of which A$1,4 billion (ZAR12,6 billion) is secured for FY2014.

Expanding Clough’s asset support capability to provide increased operational support to clients will be a key focus as projects transition from the construction phase to the operations phase. Clough will furthermore seek to diversify earnings acrossitsbusinessdivisions,marketsandgeographicregions,andre-establishingitsbusinessintheminingandmineralsmarket remains a key part of its strategy.

Clough significantly strengthened its commissioning capability during FY2013 through the acquisition of a leading Australian commissioning contractor e2o Pty Ltd and the establishment of the Clough Coens joint venture, to provide commissioning services to the world’s largest fabrication yards in South Korea and China.

In addition to delivering on current LNG projects, Clough will target the following business opportunities:

– Mining and Minerals – Clough seek to diversify its earnings across its business divisions, markets and geographic regions.Re-establishingthebusinessintheminingandmineralsmarketremainsakeypartof itsstrategy.Despitea market correction of unprecedented proportions, the cyclical nature of the mining and minerals sector should see this market rebound, and Clough is expected to be well positioned to leverage opportunities when the time comes. Clough’s aim is to grow project revenue from the Australian mining and minerals sector to 10% – 20% of annual revenue.

– Commissioning and Asset Support – In FY 2013 the Commissioning and Asset Support division exceeded revenue, earnings before interest and tax and earnings before interest and tax margin expectations, while continuing to expand its order book. This division has strong growth outlook as the Australian LNG capital projects transition from the construction phase to operations phase.

– LNG Projects – Significant opportunity exists during the LNG operations phase, including brownfield capital expansions as well as minor and medium sustaining capital project works, which combined with a controlled international expansion, will supplement work on the major Australian capital projects.

– Clough Coens – Clough established the Clough Coens joint venture in South Korea in May 2013. Clough has a 55% share in this partnership, which was established to provide commissioning services to South Korea’s shipbuilding industry which include some of the world’s largest fabrication yards. South Korea undertakes about half of the world’s shipbuilding activities, and is the world’s largest fabricator of oil and gas facilities, such as super tankers, LNG carriers, FLNG units, drill ships, and complex integrated fixed and floating production facilities. The business model for the new venture supports shipyards and/or operators during one of the most important phases of any EPC project, thecompletionsphase,byofferingspecialisedhook-upandcommissioningservices.CloughandCoenshavebothworked in the South Korean fabrication industry, and have been cooperating together for some time.

The alignment on business values and vision between the two companies has resulted in the decision to enter into this jointventure.Thebusinesswillcommencewithworkin-handand60commissioningtechniciansdeployedonprojectsin South Korea and China. The decision to partner with Coens allows Clough to target the world’s largest fabrication yards in South Korea and China with innovative commissioning and completions services. More than 100 potential opportunitiesoverthenear-to-mediumtermhavebeenidentified.

16

• International:

– In the short-to-medium term, Clough has incorporated into its business plan a controlled and orderly expansionof engineering led activities beyond Australia and Papua New Guinea. The first step in this expansion will be the establishment of a United Kingdom engineering centre in Glasgow, Scotland, in FY2014, to provide engineering services to the North Sea and Africa. An engineering office will also be established in Jakarta to support the Tangguh project and to leverage further opportunities in Southeast Asia.

Murray & Roberts does not intend to make changes to the existing operations of Clough and is highly supportive of Clough’s strategy and current management. In FY2014, Murray & Roberts will support Clough to expand its asset support capabilities to provide increased operational support to clients as the Australasia LNG capital projects under construction transition from the construction phase to the operations phase. Further, Murray & Roberts will assist Clough in positioning the business to benefit from any cyclical recovery in the global mining and minerals sector.

3. MURRAY & ROBERTS RATIONALE

Murray & Roberts considers the Acquisition to be consistent with the Group’s long term growth strategy, and the next step towards achieving the Group’s strategic objectives. The Murray & Roberts Group has had an interest in Clough since 2003, and the potential strategic benefits of fully owning Clough have been recognised by management for some time. The Acquisition has a number of key benefits for the Group as it:

– Secures control of 100% of Clough’s operations, assets, cash flow and strategic direction, creating a wholly-ownedinternationaldiversifiedengineeringandconstructionbusiness.

In recent years, Clough has become an increasingly more relevant part of Murray & Roberts’ business. However, due its 61,6% shareholding, it has had limited access to the cashflows Clough has been generating.

For FY2013, Clough generated A$293 million (ZAR2 652 million) of cash, (including cash from the sale of its investment in Forge) while Murray & Roberts received A$12,4 million (ZAR112 million) in dividends in relation to the previous financial year’s earnings. However, Murray & Roberts will receive dividends of A$67,1 million (ZAR624 million) in relation to FY2013 earnings, subject to the implementation of the Scheme and declaration of the Clough Special Dividend. The Acquisition will allow Murray & Roberts to have full access to 100% of Clough’s future cashflows.

For FY2013, Clough had A$441 million (ZAR3 984 million) cash on hand. Some of Clough’s surplus cash is proposed to be used to fund the Acquisition.

– Increases Murray & Roberts’ exposure to one of its target market sectors, namely oil and gas, which is considered to offer attractive growth potential.

Murray&Robertsviewstheglobalenergysector,inparticularoilandgasandpower,tohaveastrongmedium-tolong-term growth outlook.

In addition to ongoing growth opportunities in Clough’s existing geographic markets, Murray & Roberts sees significant potential to leverage Clough’s expertise to pursue opportunities in and around Africa’s rapidly emerging oil and gas markets, for both existing and new clients.

Clough has an order book of A$2,3 billion, (ZAR20,6 billion), equivalent to 1.4 times FY2013 revenue of A$1 635 million, (ZAR14 800 million) (refer to reconciliation in Annexure 8, note 1), representing 45% of Murray & Roberts’ consolidated pro forma order book as at 30 June 2013.

Further growth is anticipated to result from Clough repositioning itself across the oil and gas sector lifecycle in part aided by its recent acquisition of e2o Pty Limited, and the launch of its international commissioning and asset support business, Clough Coens.

– Simplifiesthecorporateandoperatingstructureoftheconsolidatedgroup,consistentwithMurray&Roberts’recovery and growth strategy.

Following the implementation of the Scheme and the completion of the recently announced disposal of the Construction ProductsAfricamanufacturingbusinesses,Murray&Robertswillhavefouroperatingplatforms,allcomprisingwholly-owned subsidiaries:

• tworegionalplatforms(ConstructionAfricaandMiddleEast,andEngineeringAfrica);and

• twointernationalplatforms(ConstructionGlobalUndergroundMining,andConstructionAustralasiaOil&GasandMinerals).

The new structure is expected to facilitate Murray & Roberts being a more efficient and focussed business.

17

− Isexpectedtobeimmediatelyprofitpershareaccretive.

OnaFY2013pro-formabasistheAcquisitionis36%accretivetoMurray&Roberts’pro-formaprofitspersharefromcontinuing operations. The pro forma financial effects relating the Acquisition is set out in section 7 of the Circular.

– Will result in Murray & Roberts maintaining a net cash position.

Consolidated pro forma debt will remain largely unaffected by the Acquisition after utilising Clough cash to part finance the Acquisition and redeploying funds to be received from recent asset disposals in the second quarter of FY2014, as set out in section 4.1.2.

– Presents low execution risk given Murray & Roberts’ existing understanding of the business which has been established over more than a decade.

Murray & Roberts currently owns 61,6% of Clough after first acquiring a shareholding in 2003. Clough became a subsidiary of Murray & Roberts and was consolidated with effect from 1 July 2007, and Murray & Roberts currently has three representatives on the Clough Board.

4. TERMS OF THE ACQUISITION

4.1 Details of the Acquisition

Transaction structure

Murray & Roberts will acquire the Scheme Shares through Murray & Roberts (Aus) such that post the Acquisition, the Murray & Roberts Group will own 100% of the issued share capital of Clough.

Scheme Implementation Agreement

The Acquisition will be implemented through the Scheme. The Scheme is subject to the terms and Conditions Precedent as set out in the Scheme Implementation Agreement. A summary of the Conditions Precedent is set out in section 4.2 below.

Scheme Booklet

Clough expects to send a Scheme Booklet to Scheme Participants in mid October 2013 containing full details of the Scheme. The Scheme Booklet will include, amongst other things, the reasons for the Clough Independent Directors’ unanimous recommendation to support the Scheme, and a copy of the Independent Expert’s Report.

Independent Expert

Clough has appointed Grant Samuel, to provide an Independent Expert’s Report in respect of the Scheme, in accordance with the Corporations Act, and policies and practices of ASIC. The Clough Independent Directors will unanimously recommend that Scheme Participants vote in favour of the Scheme, in the absence of a superior proposal, and subject to Grant Samuel, the Independent Expert, expressing an opinion that the Scheme is in the best interests of Scheme Participants (and the Independent Expert not changing that opinion, or otherwise withdrawing its Independent Expert’s Report).

Timing

Subject to all requisite approvals being obtained and the Conditions Precedent summarised in section 4.2, the Scheme is anticipated to be implemented on or about 11 December 2013.

4.1.1 Consideration

The amount payable to each Scheme Participant upon the successful implementation of the Scheme is A$1,46 cash per Scheme Share. The aforementioned amount is expected to comprise the Capital Payment (A$1,32 per Scheme Share, payable by Murray & Roberts) and the Clough Special Dividend (A$0,14 per Clough share payable by Clough). The Clough Special Dividend will only be paid if the Scheme becomes Effective.

If Clough reasonably believes that the Clough Special Dividend will not be able to be Fully Franked, then Clough and Murray & Roberts will consult in good faith to determine the extent to which Clough can pay a Fully Franked dividend conditional on the Scheme becoming Effective.

If as a result, the Clough Special Dividend is reduced from A$0,14 per Clough Share, Murray & Roberts has agreed to increase the Capital Payment so that the total amount paid to Scheme Participants under the Scheme will remain A$1,46 cash per Scheme Share. In this event, the Clough Loan will increase equivalent to the reduction in the Clough Special Dividend.

The payment to cancel the Clough Options and Clough Performance Rights is expected to be paid concurrently with the payment to the Scheme Participants, while the Acquisition transaction costs are likely to be paid within 30 days of the Scheme Implementation Date.

18

4.1.2 Funding of the Scheme Consideration

Murray & Roberts intends to fund the Scheme Consideration of approximately A$404,2 million (ZAR3 763 million) through a combination of the utilisation of Clough Special Dividend proceeds receivable by MRL, the Clough Loan as well as new bank debt as follows:

• theCloughLoanofapproximatelyA$184,5million(ZAR1718million),providedtoMurray&Roberts (Aus)byClough,funded from Clough’s existing cash reserves. In the event that the Clough Special Dividend is reduced from A$0,14 per Clough Share, the Clough Loan will increase equivalent to the reduction in the Clough Special Dividend. The Clough Loan will require Clough Minority Shareholder approval by a special majority, (at least 75% of the votes cast by eligible CloughMinorityShareholderspresentandvoting)attheCloughGeneralMeeting).TheCloughLoanapprovalwillbeinter-conditional with the implementation of the Scheme;

• ApproximatelyA$152,6million(ZAR1421million)newbankdebtprovidedbyexistinglendersunderbilateralfacilityletters,which will be governed by the Amended and Restated CTA; and

• CloughSpecialDividendproceedsofapproximatelyA$67,1million(ZAR624million)receivablebyMRL.

Immediately following the Scheme Implementation Date, Murray & Roberts’ consolidated pro forma gross debt is expected to increase by approximately ZAR1 378 million. However, after utilising Clough cash to part finance the Acquisition and redeploying funds expected to be received in the second quarter of FY2014 from recent asset disposals (prior to implementation of the Acquisition), Murray & Roberts’ consolidated pro forma debt position will remain largely unaffected by the Acquisition.

The shareholders of MRL and Murray & Roberts have passed the resolutions required to provide the necessary financial assistance for the purposes of the Acquisition, as required in terms of Section 44 and Section 45 of the Companies Act.

The Directors are satisfied, pursuant to proving any financial assistance related to the Acquisition, that:

• therewerenocircumstancesknowntotheBoardthatmaydisqualifyMurray&Robertsfromrelyingontheexemptionfromthe prohibition of unlawful financial assistance in Section 44(3) of the Companies Act;

• immediatelyafterprovidingsuchfinancialassistance,Murray&Robertswouldsatisfythesolvencyandliquiditytest,ascontemplated in Section 4 of the Companies Act;

• thetermsunderwhichthefinancialassistanceisproposedtobegivenarefairandreasonabletoMurray&Roberts;and

• allapplicablerequirementsandrestrictionsinrespectoffinancialassistancesetoutintheMOIhavebeensatisfied.

4.2 Conditions precedent

The Acquisition is subject to the fulfilment of a number of Conditions Precedent a summary of which is set out below:

• Regulatoryapproval,includingFIRB,SARB,andanyrelevantGovernmentalAgency;

• GrantSamuelastheIndependentExpertconcludingthattheSchemeisinthebestinterestsofSchemeParticipants(andthe Independent Expert not changing that opinion or otherwise withdrawing its Independent Expert’s Report);

• Shareholderapproval:

– by Murray & Roberts Shareholders of the Acquisition (being an ordinary majority of 50% plus 1 vote of the total number of voting rights exercised at the General Meeting by Murray & Roberts Shareholders present and voting, either in person or by proxy); and

– by Scheme Participants of the Scheme by the requisite majorities (being a majority in number of more than 50% of the Scheme Participants present and voting and at least 75% of the total number of votes cast at the Scheme Meeting by Scheme Participants present and voting, either in person or by proxy); and

– by eligible Clough Minority Shareholders of the Financial Assistance and Financial Benefits by a special majority (at least 75% of the votes cast by eligible Clough Minority Shareholders present and voting at the Clough General Meeting).

• TheCourtapprovingtheScheme;

• NoClough IndependentDirectorwithdrawingormodifyinghis/her recommendationor voting intention subject to theconclusion of the Independent Expert and no superior proposal emerging;

• NoCloughPrescribedEvents and/orCloughMaterial AdverseChange (each asdefined in section1of theSchemeImplementation Agreement) occurring between the date of the Scheme Implementation Agreement and the day before the Second Court Date;

• TherepresentationsandwarrantiesofeachofCloughandMurray&Robertsbeingmateriallytrueandcorrectonthedaybefore the Second Court Date; and

• PriortotheSecondCourtDate,75%ormoreoftheOptionsonissueasat28August2013(bynumber):

– having vested and been exercised;

– being the subject of binding agreements under which they will either be transferred to Murray & Roberts (Aus) or cancelled; or

– having otherwise been dealt with as agreed between Clough and Murray & Roberts (Aus).

Full details of the Conditions Precedent are set out in Schedule 1 of the Scheme Implementation Agreement, a document available for inspection and available on the Murray & Roberts website hosted at www.murrob.com

19

4.3 Additional information required for Clough

It is envisaged that Clough will operate as a standalone, wholly owned unlisted subsidiary, and its underlying assets and liabilities will not be transferred to Murray & Roberts. Given the limited changes to Clough’s assets and liabilities, changes to Clough’s guarantees or warranties as a result of the Acquisition are expected to be minimal.

The Scheme Implementation Agreement does not preclude Clough from carrying on an associated business to that of Murray & Roberts. Furthermore, there is no promoter to the Acquisition and Clough will retain legal title to its assets.