cio business update investment performance report

TRANSCRIPT

Restricted

ANZ.800.984.0080

CIO Business Update & Investment Performance Report

Oasis Fund Management Limited

Mark Rider Chief Investment Officer

For meeting on 16th March 2017

FOR DISCUSSION

Restricted

Chief Investment OfficePage 1 of 9

CIO Investment Performance Report for Oasis Fund Management Limited

Capacity

Trustee / IDPS Operator

Action Requested

For Discussion

Objective / Purpose

Fiduciary Research leverages ANZ CIO’s expertise and Sector Reviews in conjunction with research opinions and ratings from Mercer and other secondary research providers in making investment recommendations. Fiduciary Research reviews the managed funds on the Oasis investment menu on an ongoing basis and provides an overview on the investment quality of the managed funds in a quarterly performance monitoring report presented to WIGF and the Oasis Fund Management Limited Board. Objectives of this exercise include:

• Improving the composition of the wrap investment menu by offering quality products and at the same time promoting consistency and alignment across ANZ Wealth platforms;

• Reviewing fund performance and research house ratings and following-up on issues identified;

• Highlighting any investment issues and making appropriate recommendations;

• Providing updates on specific funds that appear on the Fund Watch List as a result of poor research house ratings.

Risk Assessment

This paper provides an investment performance summary and identifies any material investment risks and CIO action items. Investment risks are monitored by CIO who also engage with Mercer, the primary investment consultant for ANZ Wealth and other external research houses. A variation of this investment performance report (for OFM) is also presented to WIGF for consideration of investment risks and appropriate courses of action.

Risk Culture / Ethics / Impact to Customers

The CIO’s strong risk culture and governance processes in place and comprehensive due diligence of the investment menus and menu changes has a positive impact for customers through seeking to provide the best investment menus possible with a diverse range of options for meeting customer goals, while managing and minimising investment risks that may lead to goals not being achieved.

Related Party Transactions and Conflicts of Interest

Related party issues and conflicts of interest have been considered and are not relevant. This paper relates to a generic update on activities and an investment summary that applies to all investors in Oasis Products and does not involve any related party transactions.

Appendices

Appendix 1 – Oasis Top and Bottom Performing Funds – December 2016, 2 pages.

Appendix 2 – Oasis Direct Equity Share Additions, Removals and New Issuance – December 2016, 2 pages.

Appendix 3 – Oasis Direct Equity Recommended Limits Exception Reporting, 1 page.

ANZ.800.984.0081

ANZ.800.984.0082

Executive Summary - Oasis Investment Options

Menu Changes and Fund Performance Highlights • Fiduciary Research recommends a range of managed fund additions and closures from the wrap investment menu to WIGF for 'endorsement' and

subsequently for the Chief Investment Officer to ' approve' under Board sub-delegation . The investment menu changes over the quarter are on page 3 of this paper and include 10 fund additions. This is consistent with offering an open menu with high quality, regula rly monitored and a diverse range of investments .

• Mercer has rated 61% of funds on the Oasis platform. Of the funds rated by Mercer, 94% have been rated 'A' or 'B+' predominantly across Australian and international equities. The majority of remaining funds not rated by Mercer have ratings from one of the other external resea rch houses utilised by CIC (Lonsec, Morn ingstar and Chant West) .

• The top performing funds over 1-year are predominately Austra lian equity funds with value style Austra lian equity managers achieving the best results. The bottom performing funds over 1-year are also predominately Australian equity funds with growth style Australian equity managers.

---Oasis Wrap ~ ~ ~

I SSu oe:::o ""11:::0111~ auu r1a11a~oe111oe1n. """' '-'u11:::0

Key information for year

• 96% of funds recorded positive 1 - year absolute returns.

• 63% of funds recorded 1st or 2nd quartile performance over 1-year against peer group.

Additional commentary

• The best performing sectors were fixed interest and cash funds.

• The worst performing sectors were Australian equities and multi-sector funds. Fiduciary Research will engage with the CIC team in reviewing the funds in these sectors.

• The Yarra Income Plus Fund and Aberdeen Multi-Asset Income and Multi-Asset Real Return funds have a Lonsec ' Fund Watch' rating . Fiduciary Research will review post finalisation of CIO's sector review and will continue to monitor developments within Yarra I Aberdeen and outcome of Lonsec's rating .

• The suspended and terminating funds are being managed appropriately. The managers are progressively paying out cash to investors as assets are realised with most of the funds close to making final termination payouts. Fiduciary Research continues to monitor these funds ensuring investors' best interests are met.

• Fiduciary Research closely monitors those funds with performance or other issues and makes appropriate recommendations. The majority of funds that appear in the ' Fund Watch' section, that have either poor resea rch or performance related issues, have been closed to new investors. Fiduciary Research is closely monitoring the Hunter Hall situation and has been in contact with Hunter Hall to discuss the recent developments and steps taken by Hunter Hall to restore investor confidence. Fiduciary Research has also been observing redemption activity across the Hunter Hall funds on Oasis and Macquarie platforms. At this stage there is no material increase in redemption activity. Aligned advisers and Dea ler Groups with significant holdings in the funds have been contacted and notified of the potential risks.

• All sha re diversification exceptions have been followed-up and responses were received and recorded from the advisers and or members.

Restricted

Chief Investment Office Page 2 of 9

ANZ.800.984.0083

Wrap Managed Funds Investment Menu Changes

The following menu changes were " Endorsed" by WIGF and "Approved" by the CIO under Board sub-delegation at the 28th October and 25th November 2016 WIGF meetings.

Fund Additions

AB Managed Volatility Equities Fund

Grant Samuel Tribeca Alpha Plus Fund

Magellan Infrastructu re Fund (Unhedged)

CFML Cash Fund A

CFML Fixed Interest Fund

CFML Listed Property Fund A

CFML Schroder Equity Opportunities Fund

CFML MFS International Shares Fund A

CFML Colonial Infrastructure Fund

CFML RARE Emerging Markets Fund

A Funds approved only for IDPS investors

Restricted

Sector

Australian Shares

Australian Shares

Global Shares

Cash

Global Fixed Interest

Australian Listed Property

Australian Shares

Global Shares

Global Shares

Global Shares

Fund Closure

N/A

Sector

Chief Investment Office Page 3 of 9

Restricted

Chief Investment OfficePage 4 of 9

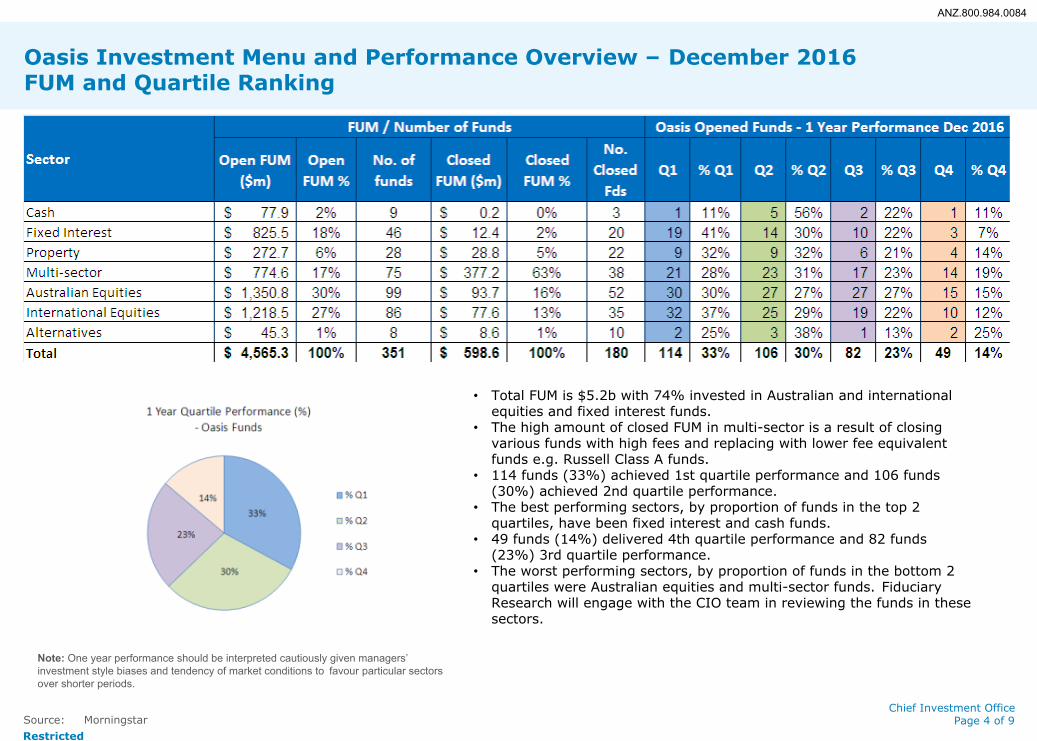

Oasis Investment Menu and Performance Overview – December 2016FUM and Quartile Ranking

Source: Morningstar

• Total FUM is $5.2b with 74% invested in Australian and international equities and fixed interest funds.

• The high amount of closed FUM in multi-sector is a result of closing various funds with high fees and replacing with lower fee equivalent funds e.g. Russell Class A funds.

• 114 funds (33%) achieved 1st quartile performance and 106 funds (30%) achieved 2nd quartile performance.

• The best performing sectors, by proportion of funds in the top 2 quartiles, have been fixed interest and cash funds.

• 49 funds (14%) delivered 4th quartile performance and 82 funds (23%) 3rd quartile performance.

• The worst performing sectors, by proportion of funds in the bottom 2 quartiles were Australian equities and multi-sector funds. Fiduciary Research will engage with the CIO team in reviewing the funds in these sectors.

Note: One year performance should be interpreted cautiously given managers’ investment style biases and tendency of market conditions to favour particular sectors over shorter periods.

ANZ.800.984.0084

Restricted

Chief Investment OfficePage 5 of 9

Oasis Investment Menu and Performance Overview – December 2016Distribution of Mercer Ratings

Source: Mercer and Lonsec

Note: Mercer has ceased rating all diversified funds. Ratings for the 64 diversified funds denoted ** reflect Lonsec ratings.

• From a total of 351 open funds, Mercer has rated 215 funds (61%) and Lonsec has rated 64 multi-sector funds. Mercer ceased rating multi-sector funds in March 2015. The majority of remaining funds have ratings from one of the other external research houses utilised by CIO (Morningstar and Chant West).

• Of the funds rated by Mercer, 94% have been rated ‘A’ or ‘B+’ predominantly across Australian and international equities.

• 12 funds (6%) out of the 215 funds have a sub-investment grade rating (‘B’) mainly across the international and Australian equities sectors. Fiduciary Research are assessing the outcomes of recent sector reviews with the view to close poorly rated funds to new investors.

• Of the 64 multi-sector funds rated by Lonsec, 61 are ‘H Rec’, ‘Rec’ and ‘IG’ ratings. The Yarra Income Plus Fund and Aberdeen Multi-Asset Income and Multi-Asset Real Return funds have a ‘Fund Watch’ rating. For an update on these funds, refer to the Fund Watch list on pages 8 and 9.

• 88% of total open fund FUM has favourable Mercer/Lonsec ratings with 10% not rated by Mercer or Lonsec. 2% of total open fund FUM has Mercer sub-investment grade ratings.

• 81 ratings (25%) are older than 12 months, 77 are Mercer ratings.

ANZ.800.984.0085

Oasis Fund Watch List Suspended / Terminating Funds

Fund

ANZ.800.984.0086

Commentary

Susoended I Terminating Funds - Only where an update is available

All Star I AM Australian Share Fund $2.22m I ssue/update: EQT, as RE of the Fund, advised the Fund has not attracted the

Australian Unity Wholesale Conservat ive Growth Portfolio

Goldman Sachs I nternational Wholesale Fund

GVI Aubrey Globa l Growt h & Income (Hedged) Fund

Restricted

$1.82

Ni l

desired level of FUM and does not expect any futu re growt h . As a result EQT believe that it is in the best interest s of investors to terminate the Fund effective 9t h December 2016.

Action: Fiduciary Research will monitor the Fund's wind-up process and ensure investors' best interests are being met. I ssue/update: AU advised the Fund is experiencing a decline in inflows and together with t he Funds' relatively small size, limits the Funds' ability to meet investment object ives. As a resu lt AU believe that it is in the best interests of investors to terminate the Fund effective 15th March 2017 .

Action: Fiduciary Research will monitor the Fund's wind-up process and ensure investors' best interests are being met. I ssue/update: Goldman Sachs has det ermined to wind-up the Fund effective 11th October 2016. Due to the Fund 's small size and lack of growth prospects, Goldman Sachs decided it was in investors' best int erests to terminate the Fund.

Action: Fiduciary Research can confi rm t he final payment was processed to investors' cash accounts on the 18th November 2016.

$2.36m I ssue/update: Treasury Group, as RE of t he Fund, advised that it is in the best interests of investors to terminate the Fund effective 15th November 2016.

Action: Fiduciary Research can confi rm the fina l payment was processed to investors' cash accounts on the 11th January 2017.

Chief Investment Office Page 6 of 9

ANZ.800.984.0087

Oasis Fund Watch List Suspended / Terminating Funds (cont.)

Fund Commentary

Suspe nded I Terminating Funds - Only where an update is available ( cont.)

Macquarie Diversified Private Equity 0.01m I ssue/update: MIMAL, as Trust ee of the Fund, has advised that the manager of Fund - Accumulat ion 2003 the last remaining investment , ROC Alt ernat ive investment Trust III has received

an offer to purchase the Funds holdings at a discount of 26% to the Fund's 30 September 2016 net asset va lue. Taking int o considerat ion the mat erially more favourable price t han was previously avai lable and the best interest s of investors in the Fund, MIMAL has decided to accept the offer. I n deciding t o accept t he offer, MIMAL took into account providing invest ors' liquidity and certainty, and avoiding the risk that over t ime t he va lue of the investment may fall materially.

Smallco Investment Fund

van Eyk Blueprint Balanced Fund (VBB)

van Eyk Blueprint Capital St able Fund (VBC)

van Eyk Blueprint High Growt h Fund (VBG)

Restricted

Action: Fiduciary Research can confirm the proceeds were paid to investors' cash accounts on the 12th January 2017.

$19.3m Issue/update: Smallco advised their intention to no longer accept applications into the Fund, effective 31st January 2017. The manager decided to take a proactive approach limiting funds under management and safeguarding future investment performance for the benefit of existing investors in t he Fund.

Action: Fiduciary Research can confi rm the Fund was closed to applications for new and existing investors and removed from the Oasis investment menu in February 2017. The Fund remains open to regular withdrawals .

$7.86m I ssue/update: Macquarie announced t heir decision to terminate t he funds effective 15t h August 2014. All of t he liquid assets of the funds have been

$2.92m realised and distributed t o investors. Macquarie advised it may t ake a significant amount of t ime before the illiquid assets are fully realised . Macquarie suspended

$5.97m unit pricing for t he 3 diversified funds in July 2015 as a result of uncertaint y over the valuation of t he largest remaining asset wit hin the funds . Further, when pricing resumes, t he unit price for the funds may change mat erially .

Action: Fiduciary Research will monitor t he suspension of unit pricing and terminat ion process t o ensure investors' best interest s are met. Since terminat ion the approximat e ret urn for each fund has been; 82% VBC, 83% VBB and 83% VBG.

Chief Investment Office Page 7 of 9

ANZ.800.984.0088

Oasis Fund Watch List Poor Research House Ratings / Staff Turnover I Other

Fund Commentary

Poor Research House Ratings I Staff Turnover I Other Aberdeen Australian Equities Fund $2.50m I ssue/update : The Fund is ' B' rated by Mercer as a result of changes within the investment team

Aberdeen Mult i-Asset Income Fund

Aberdeen Mult i-Asset Real Return Fund

AMP Capital Asian Equity Growth Fund

Colonial FS Concentrated Austral ia Share Fund

DOH Global Fixed Interest Alpha Fund

Hunter Hall Austral ian Value Trust (AVT)

Hunter Hall Global Equity Trust (GET)

Hunter Hall Value Growth Trust (VGT)

Restricted

including leadership changes, low FUM and lacklustre performance.

Action: The Fund was .ci.Q.s.ed to new investors in December 2013, following Board approval. No further action planned .

$2.76m I ssue/update : The funds have experienced persistent turnover of the co-portfolio managers over the years and more recently the departure of Archie Struthers in July 2016. Current ly there is a

$13.05m review of roles and responsibi lities within Aberdeen's Multi-Asset business. In response, Lonsec has placed the funds on ' Fund Watch'.

Action: Fiduciary Research will review post final isation of CIO's sector review and will continue to monitor developments within Aberdeen and outcome of Lonsec's rating.

$0.0lm I ssue/update : Mercer has rated the Fund 'B' on the view the manager is under- resourced and hence question the strategy's competitive edge with respect to the quality of research and its ability to outperform its peer group.

Action: The Fund was .ci.Q.s.ed to new investors in December 2012, following Board approval.

$1.03m I ssue/update : The Fund is 'B' rated by Mercer on the view the manager will struggle meeting performance objective targets and has a poor record of retain ing investment leaders.

Action: The Fund was .ci.Q.s.ed to new investors in July 2014, following Board approval.

$1. llm I ssue/update : Mercer has downgraded the Fund to 'B' as a result of low but persistent level of staff turnover and constant changes to the investment and risk management processes.

Action: The Fund was closed to new investors in July 2015, following Board approval.

$2.05m I ssue/update : Hunter Hall advised Peter Hall, CIO tendered his resignat ion on 27 December 2016 for personal and fami ly reasons and wi ll leave the fi rm in June 2017. James McDonald has been

$2.51m appointed interim CIO. James has 19 years' experience in global equity markets and has been portfol io manager at Hunter Hall since 2003. Ownership of the fi rm also remains uncertain. Peter Hall

$6.96m has sold 19.9% of his stake to Washington H Soul Pattinson & Co (Soul) and intends to dispose of his remaining 24% holding. Soul is seeking fu ll ownership of Hunter Hall but may remain a large minority shareholder as Pinnacle Investment lodged a 2nd and higher takeover bid for the fi rm. Following the announcement of Hall 's resignation, the funds were downgraded to ' redeem' and 'Negat ive' by research houses. Action: The VGT was closed to new investors in Jan 2015 and the AVT closed to new investors in October 2016, following Board approval. Fiduciary Research is closely monitoring the situation as there is a risk of investment team instability and hence the abil ity to implement the investment process, concerns over the Hunter Hall business model and its ongoing viabil ity. Fiduciary Research has been in contact with Hunter Hall to discuss the recent developments and the steps taken by Hunter Hall t o restore investor confidence. Fiduciary Research has also been observing redemption activity across the funds on the ANZ and Macquarie platforms. At this stage there is no material increase in redemption activity. Aligned advisers and Dealer Groups with significant holdings in the funds have been contacted and notified of the potential risks.

Chief Investment Office Page 8 of 9

ANZ.800.984.0089

Oasis Fund Watch List Poor Research House Ratings/ Staff Turnover I Other (cont.)

Fund - Commentary

Poor Research House Ratings I Staff Turnover I Other Ccont.l

Integrity Australian Share Fund

Macquarie Australian Small Companies Fund

MHOR Austral ian Small Caps Fund

(previously EQT SGH Wholesale Absolute Return)

UBS I nternational Shares Fund

Yarra Australia Infrastructure & Property Equity Fund

(previously Goldman Sachs Australian Infrastructure & Property Equity Fund) Yarra Income Plus Fund

(previously Goldman Sachs I ncome Plus Fund)

Yarra Global Small Companies Fund

(previously Goldman Sachs Global Small Companies Fund)

Restricted

$1.33m I ssue/updat e: The Fund has undergone heightened team instability with experienced investors Michael Murray, Glen Bertram and David Boyle all leaving the firm in rapid succession The Fund has suffered extended periods of poor performance relative to benchmark and decl ining AUM. Research houses have lost conviction in the manager and downgraded the Fund; Mercer 'B' and Morningstar 'Negative'. Action: The Fund was~ to new investors in March 2016, following Board approval.

$1.14m I ssue/updat e: The Fund's co-portfolio managers, James Dougherty and Liam Donohue have made the decision to leave Macquarie. Matthew Fist has been appointed Portfolio Manager of the Fund, supported by Patrick Hodgens, Head of Listed Equities. Following the resignations, Lonsec have placed the Fund on 'Fund Watch'. Lonsec is scheduled to discuss these developments with Macquarie before issuing further ratings guidance. Action: The Fund was~ to new investors in December 2013, following Board approval. Fiduciary Research will monitor developments within the Macquarie equity team and the research house ratings upon the completion of their review.

$0.16m I ssue/updat e: The Fund has one sub- investment grade rating, Mercer 'B'. In August 2016, the Fund was t ransitioned to a new specialist small cap manager, MHOR Asset Management and renamed the MHOR Australian Small Caps Fund . Action: The Fund was~ to new investors in September 2013, following Board approval. Fiduciary Research is monitoring the fund and ratings updates under the new manager.

$1.71m I ssue/updat e: The Fund has a Mercer 'C' rating following the key departure of Nick Irish and analyst Richard Green. The uncertainty surrounding the future of this strategy, the history of team instability and poor fund performance is of concern. Action: The Fund was~ to new investors in September 2016 following Board approval.

$0.02m I ssue/updat e: The Fund has Mercer 'B' rat ing due to a combination of new and relatively inexperienced co-portfol io managers and team under resourcing. The Fund also fai led to meet ANZ governance requirements in relation to SPSS30 investment and liquidity stress testing. Action : The Fund was closed to new investors in April 2016, following Board approval.

$7.19m I ssue/ updat e: The buy-out of Goldman Sachs Australian operation by senior management and TA Associates was completed in early January 2017 and a new brand Yarra Capital Management has taken effect. Most of the investment team has transit ioned across and the prospect of equity in Yarra should al ign their interests. Research houses have retained their ' Fund Watch' and 'Negative' ratings as they

$4.21m hold discussions with the manager and continue to monitor developments. Action: Post completion of CIO's sector review, Fiduciary Research is considering closing the Yarra Global Small Companies Fund to new investors, and will review the Yarra Income Plus Fund post final isation of CIO's sector review. Fiduciary Research will continue to monitor research house ratings and review once final ised.

Chief Investment Office Page 9 of 9 *The End*

Appendix

Restricted

Appendix 1: Oasis Investment MenuTop Performing Funds 1 Year to December 2016

Fund Oasis FUM ($m) Sector Net

ReturnRelative Return Action / Status

Baker Steel Gold Fund $0.07 Alternatives 91.9% 30.5%**

No action. FR closed the Fund to new investors in Oct 2014. Solid gold demand has significantly increased valuations across the Fund’s core holdings. Strong stock selection with a focus on gold producers has been key to the Fund’s outperformance. Manager retains a focus on quality assets with good operating margins.

Maple-Brown Abbott Australian Geared Equity Fund - Wholesale Units

$1.87 Australian Equities 30.1% 18.3%**

No action. Outperformance primarily related to overweight materials and energy sectors and underweight financials and healthcare, the result of the manager's value based investment philosophy. The impact of leverage also contributed to performance. Fund has 2 recommended ratings from research houses.

Dimensional Australian Value Trust $9.88 Australian

Equities 28.5% 16.7%**

No action. Outperformance for the period was achieved by underweight positions in healthcare, industrials, information technology and an overweight position in materials. From a style perspective positive size and value premiums also contributed to outperformance.

Lazard Select Australian Equity Fund – Wholesale $2.85 Australian

Equities 26.2% 14.4%**

No action. The portfolio is substantially overweight in high quality resource companies and simultaneously lowered the weighting to defensive, high yield sectors such as infrastructure. This positioning has contributed to positive performance as resources have rallied and many ‘bond proxy’ equities have sold off.

CFML Schroder Equity Opportunities Fund $0.00 Australian

Equities 24.0% 12.2%**No action. The Fund’s significant overweight to materials sector aided performance. The portfolio was tilted to big, low cost miners and underweight those sectors and stocks where valuations looked stretched such as the banks and REITs.

Realindex RAFI Australian Small Companies Fund - Class A $0.07 Australian

Equities 24.8% 11.6%**

No action. FR closed the Fund to new investors in Oct 2015. Small cap value stocks outperformed their growth counterparts, creating a boost for portfolio performance. The Fund’s ‘value’ tilt had the portfolio overweight materials/mining services companies which aided relative performance during the year.

Lazard Emerging Markets Fund $3.27 International Equities 22.3% 10.6%**

No action. Stock selection within the financials, industrials, and consumer discretionary sectors were key drivers of outperformance. Overweight positions in Russia and Brazil and underweight China added value from a country perspective.

Celeste Australian Small Companies Fund $0.51 Australian

Equities 23.2% 10.0%**No action. The Fund benefited from a bounced back in undervalued mining services stocks as well as a sell-off in high PE defensive stocks. Outperformance was achieved by an over allocation to materials as well as underweight IT and financials sectors.

Antipodes Global Fund $0.19 International Equities 17.2% 9.2%**

No action. FR closed the Fund to new investors in Sept 13. Relative performance benefited from strong stock picking long and short and currency management. The portfolio achieved gains in thematic clusters, such as, U.S. natural gas recovery, low cost oil producers with long duration assets and European restructuring stories.

Platinum Japan Fund $11.5 International Equities 11.5% 8.6%**

No action. Strong Japanese market over the last quarter saw most stocks in the portfolio rally. The Funds’ key holdings in energy producers, exporters, electronics manufacturers and currency positions were strong contributors to relative performance.

* Relative to Morningstar Peer Group. ** Relative to Asset Class Specific Benchmark

ANZ.800.984.0090

Appendix

Restricted

Appendix 1: Oasis Investment MenuBottom Performing Funds 1 Year to December 2016

Fund Oasis FUM ($m) Sector Net

ReturnRelative Return Action / Status

SGH ICE $0.58 Australian Equities -5.6% -18.8%**

The Fund is benchmark unaware. Over the last year key drivers of performance within the small cap index were resource and lower quality industrials, stocks the manager avoids. No action. Manager focuses on industrial franchise companies with sustainable earnings growth. The Fund has a ‘quality’ bias and is highly rated by research houses.

Colonial Future Leaders Fund $0.46 Australian Equities -5.3% -18.5%**

No action. FR closed the Fund to new investors in Oct 2013. The Fund’s significant underweight position to small materials/resource companies which rose strongly during the period had a substantial negative effect on relative performance.

Ironbark Copper Rock Emerging Markets Opportunities Fund $0.13 International

Equities -4.9% -16.6%**

Poor performance is attributed to the previous manager’s agribusiness strategy. Agricultural commodities was one of the worst performing sectors within the global universe. On 30 Sept 16 the Fund was transitioned to Copper Rock with a new, more diversified emerging markets strategy. Action: FR has assessed CIO's sector review (which downgraded this fund to Replace on the APL) and is comfortable leaving the Fund open as a result of 2 research house investment grade ratings and strategy’s niche offering.

CBG Australian Equities Leaders Fund $42.81 Australian

Equities -4.1% -15.9%**

Underperformance for the period was driven by an underweight position in materials and energy sectors and poor stock selection within the financials sector. Action: FR will review the Fund following the completion of CIO's sector review in Q2 2017. The Fund has strong long term performance and Lonsec rates the Fund as Investment Grade.

Bennelong Kardinia Absolute Return Fund $14.96 Australian

Equities -2.3% -14.1%**

The managers’ stock selection process has a bias towards quality, growth and earnings momentum. These factors all underperformed in 2016 as the market rotated aggressively into value strategies. The Fund was also underweight materials sector which dominated performance in Q4 2016. No action. The Fund has good long-term performance and is favourably rated.

Hyperion Small Growth Companies Fund $7.91 Australian

Equities -0.9% -14.0%**

No action. Manager closed the Fund to all investors in May 2016. Rapidly rising commodity prices and recent market rotation out of higher PE quality stocks into lower PE stocks such as banks and resources has hurt the Fund’s performance. The manager maintains its long-term focus on high quality businesses with competitive advantage.

Platypus Australian Equities Fund $0.86 Australian

Equities -1.9% -13.7%**No action. FR closed the Fund to new investors in Jul 2014. A sharp market rotation away from growth stocks into cyclical value stocks hurt performance. Largest detractor to the portfolio was an underweight allocation to financials and materials sectors.

Macquarie Asia New Stars No.1 Fund $5.64 International

Equities -15.5% -13.7%**

Underperformance driven by the surge in lower-quality, higher risk cyclical sectors and the Fund's underweight position to these sectors. No action. The Fund is highly rated and retains its quality bias favouring companies that are conservatively capitalised and can sustainably grow their earnings and competitiveness in the long term.

Colonial First State Wholesale Global Resources Fund $16.72 International

Equities 41.1% -13.6%**

No action. Underperformance for the period was driven by underweight positions in diversified metals and steel producers (such as Anglo American and Vale respectively) as commodity prices rebounded during the year. Strong peer relative performance over short and long term and positive ratings. Fund remains Approved on APL following recent sector review.

Hunter Hall Australian Value Trust $2.05 Australian

Equities -0.4% -13.6%**

FR closed the Fund to new investors in Oct 2015. Underperformance was largely driven by stock specific issues. A few stock holdings faced short-term challenges which detracted from performance. The manager is focused on quality companies and is confident and committed restoring positive portfolio performance. Action: Refer to ‘Watch List’ regarding Peter Hall’s departure.

* Relative to Morningstar Peer Group. ** Rela ive to Asset Class Specific Benchmark

ANZ.800.984.0091

Appendix

Restricted

Appendix 2: Oasis Direct EquityShare Additions & Removals – December 2016

• The tables above show the additions and removals of direct equities from the constituent list of the S&P/ASX 300 Index that are made available through Oasis. A total of 2 ordinary shares were added, while 3 ordinary shares were removed from the investment menu during the December 2016 quarter. In addition, one hybrid share was added to the direct equity investment menu during the December 2016 quarter.

• In addition, during the December 2016 quarter, 2 corporate bonds were removed from the investment menu as the securities matured.

Listed Security Additions

Constituent Name ASX Code Security Type Viva Energy REIT VVR Ord Share

Westgold Resources Limited WGX Ord Share

Insurance Australia Group Capital Notes IAGPD Hybrid

Listed Security Removals

Constituent Name ASX Code Security Type SAI Global Limited SAI Ord Share

UGL Limited UGL Ord ShareVitaco Holdings Limited VIT Ord Share Origin Energy Notes ORGHA Corporate BondWoolworths Notes II WOWHC Corporate Bond

ANZ.800.984.0092

Appendix 2: Oasis Direct Equity Direct Listed Securities - New Issuance Subscriptions

IAG Capital Notes Hybrid 30 December 2016 • Approved by ANZ CI O I I PO Sub Committee and API C. • Morningstar - 'Subscribe' and Lonsec - 'Approved' . • S&P company credit rating for IAG is 'A' (Long Term) . • IAG ordinary shares are in S&P/ ASX Top 100 I ndex. • IAGPD rank ahead of ordinary shares (IAG) and equally with other

IAG Capital Notes and any other equal ranking instruments.

The approval process for IPOs I new issuance is based on the I PO Framework under the responsibility of the WPC IPO Subcommittee, whose purpose is to review the appropriateness of all internally and externally produced listed and unlisted investment products offered as new issuance for the purposes of distribution by ANZ Wea lth (ANZW) channels in Austral ia, including the Wrap platforms. As a resu lt of th is process the hybrids listed in the table were offered as new ! PO/ issuance and also added onto the share investment menu.

Restricted

ANZ.800.984.0093

Appendix

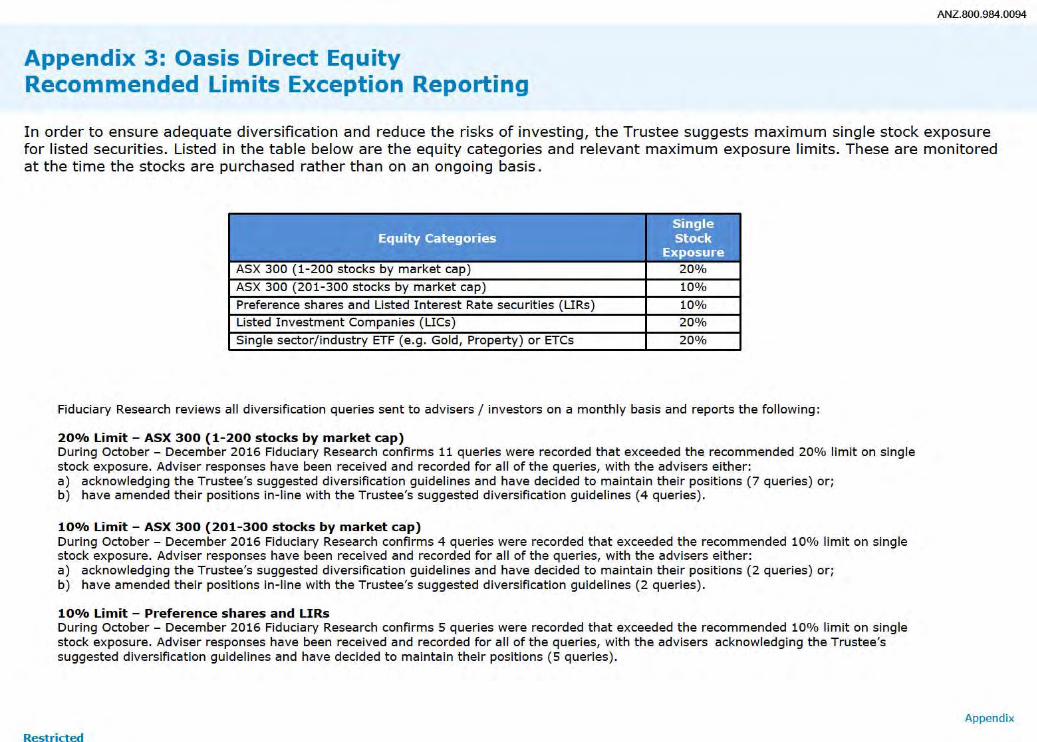

Appendix 3: Oasis Direct Equity Recommended Limits Exception Reporting

ANZ.800.984.0094

In order to ensure adequate diversification and reduce the risks of investing, the Trustee suggests maximum single stock exposure for listed securities. Listed in the table below are the equity categories and re levant maximum exposure limits. These are monitored at the time the stocks are purchased rather than on an ongoing basis.

..._..,11r.ira iii•Hllit.'J(;.,h:.io .,,;-,_ t.."'i1hTol~ - - - 1-.:41 ,..__.., I ....

ASX 300 (1-200 stocks by market cap) 20% ASX 300 (201-300 stocks by market cap) 10% Preference shares and Listed Interest Rate securities (LIRs) 10% Listed Investment Companies (LICs) 20%

Single sector/industry ETF (e.g. Gold, Property) or ETCs 20%

Fiduciary Resea rch reviews all diversification queries sent to advisers I investors on a monthly basis and reports the following :

200/o Limit - ASX 300 (1-200 stocks by market cap) During October - December 2016 Fiduciary Research confi rms 11 queries were recorded that exceeded the recommended 20% limit on sing le stock exposure. Adviser responses have been received and recorded for all of the queries, with the advisers either: a) acknowledging the Trustee's suggested diversification guidelines and have decided to maintain their posit ions (7 queries) or; b) have amended their positions in-line with the Trustee's suggested diversification guidelines (4 queries) .

100/o Limit - ASX 300 (201-300 stocks by market cap) During October - December 2016 Fiduciary Research confi rms 4 queries were recorded that exceeded the recommended 10% limit on single stock exposure. Adviser responses have been received and recorded for all of the queries, with the advisers either: a) acknowledging the Trustee's suggested diversification guidelines and have decided to maintain their posit ions (2 queries) or; b) have amended their positions in-line with the Trustee's suggested diversification guidelines (2 queries) .

10010 Limit - Preference shares and LIRs During October - December 2016 Fiduciary Research confi rms 5 queries were recorded that exceeded the recommended 10% limit on single stock exposure. Adviser responses have been received and recorded for all of the queries, with the advisers acknowledging the Trustee's suggested diversification guidelines and have decided to maintain their positions (5 queries).

Restricted

Appendix