cima strategic enterprise management (sem) - improving decision-making in your organisation

DESCRIPTION

CIMA strategic enterprise management aims to help organisations create the proactive finance function that is needed to lead the creation and long-term sustainment of stakeholder value in private and public sector organisations. This report considers the development of management accounting tools and techniques and new enterprise technologies that can support better decision-making.TRANSCRIPT

Improving decision making in your organisationThe CIMA Strategic Enterprise Management (SEM) initiative

Improving decision making in your organisation Contents

1 Executive summary 5

2 The SEM vision 6

3 Why the emphasis on new technologies? 8

4 What is preventing progress in many companies? 10

5 The real world issues for SEM technology 11

6 The problematic relationship between managementaccounting and IT 12

7 The evolution of management accounting 16

8 Broadening the view on SEM 17

9 The key management accounting techniquesand competencies 18

10 A summary of the key components of SEM 20

11 Tracking how companies are developing SEM and 25evolving their finance functions – a new benchmarking service

3

CIM

A S

EMSt

rate

gic

Ente

rpris

e M

anag

emen

t

Improving decision making in your organisation

4

© CIMA, Chartered Institute of Management Accountants, 2003

“SAP” and mySAP.com are trademarks of SAPAktiengesellschaft, Systems, Applications and

Products in Data Processing, Neurottstrasse 16, 69190 Walldorf, Germany. The terms are

referenced in this guide. SAP AG is not the publisher of this book and not responsible for it

under any aspect of press law.

Writer: Stathis Gould, Head of Technical Issues, CIMA

Contact details: [email protected]

Telephone: +44 (0)20 8849 2379

Design: Oak Design

Print: Spin Offset

Improving decision making in your organisation

5

1 Executive summary

If any of these statements ring true foryour company, a better approach todecision making based on newtechnologies and well implementedmanagement accounting techniquesmay assist you in your efforts toimprove the quality and effectiveness ofyour strategic management processesand the running of your company. Onmany occasions, the common basis ofpoor performance and failedcompanies is bad management and inmost cases this rests squarely on thedecisions that have been made byexecutives.

The literature from SAP and othermajor enterprise software providers,and from leading commentators in thisfield, has been advocating SEM systemsas a basis for improving both the role ofthe finance function and decisionmaking in organisations. The latestbook by Cedric Read and the mySAPFinancials Team, The CFO as businessintegrator, is designed to help CFOstake advantage of informationtechnology and to leverage currentinvestments in ERP and SEM systems.There is much marketing material onthe benefits of emerging technologytools such as analytical software toimprove decisions in the areas ofhuman resource management, supplychain management and product lifecycle management and SEM moduleswhich can leverage the data that youhave residing in your businesswarehouse.

As software vendors also recognise,improving the performance of yourcompany is more than about investingin technology. And what the marketingdoes not always mention is that thereare many cases where new technologyand systems have not improved theintegration of management accountinginto the business to improve decisionmaking.

This report considers the progress ofSEM in organisations and why there isoften a difference between rhetoric andreality. For many companies the ERPand SEM technology has not necessarilyled to improved decision making andgreater transparency. The SEM debate ismuch wider than leveraging thebenefits of an ERP system with newsystems.

This report also shares some of thelearning experiences gained from theCIMA SEM Round Table with thefinance directors and chief financialcontrollers of large and medium sizedcompanies. The Round Table had eightlarge corporate participants, employingover 600,000 people, sharingexperiences and discussing case studiesto assist their desire to improve decisionmaking to improve their businessperformance in terms of increasedstakeholder value. It has emerged fromour discussions that the over emphasisof companies on technology ratherthan decision making in itself, and theextreme complexity of many largemultinational organisations, causesdifficulties with moving an organisationforward.

It is our aim to support companies’development in this area by establishinga benchmarking service. This willenable companies to keep in touchwith how other organisations areprogressing in terms of implementinginformation technology, developingtheir finance functions and improvingdecision making. It is with thisinformation that we hope executivescan identify improvement opportunitiesfor their businsses and financeprofessionals. �

• Not enough time for effective strategy development• Not receiving the right information to improve strategic

decision making• Your organisation’s employees have not got the information

they need, when they need it and as a result are notempowered to make the decisions required to manage thebusiness on a daily basis

• You are battling to manage your business operations in theway that you want

• Your finance function needs to evolve its role so it can addvalue to executive decision making

Improving decision making in your organisation

6

2 The SEM vision

The CIMA Round Table has definedthe measurement of success inadopting a SEM approach broadly intwo ways.

The first is by how well seniorexecutives feel they are able toempower their employees and devolveauthority to run an organisation asefficiently as it can be run in the presentday.

The second is by creating thenecessary space and acquiring theappropriate information to develop andexecute a superior strategicmanagement process that can take thecompany forward in the medium tolong term.

SEM should support the notions ofempowerment, better corporategovernance and business performance.Good governance applies equally to theperformance aspects of the businessand better corporate performance isunderpinned by achieving a balancebetween accountability and assuranceagainst value creation and resourceutilisation.

Empowered operations should bebased on one single truth with one setof robust, real time (or near real time),integrated information supplementedwith analytics that are both rigorousand consistent in approach. Anempowered board on the other hand,should have the space and clarity toarrive at an objective consensus of thebusiness model, which are the keylevers and when and how they shouldbe pulled. Executives need tocontinuously question the businessmodel through the use of feedbackloops and in the context of the market.This in turn should release time at Boardlevel to focus on the decisions thatmatter in value terms.

This is not an easy vision to achieve.While technology can help enable theSEM vision, better decision making inthe long term requires a broader set ofcompetencies and capabilities.

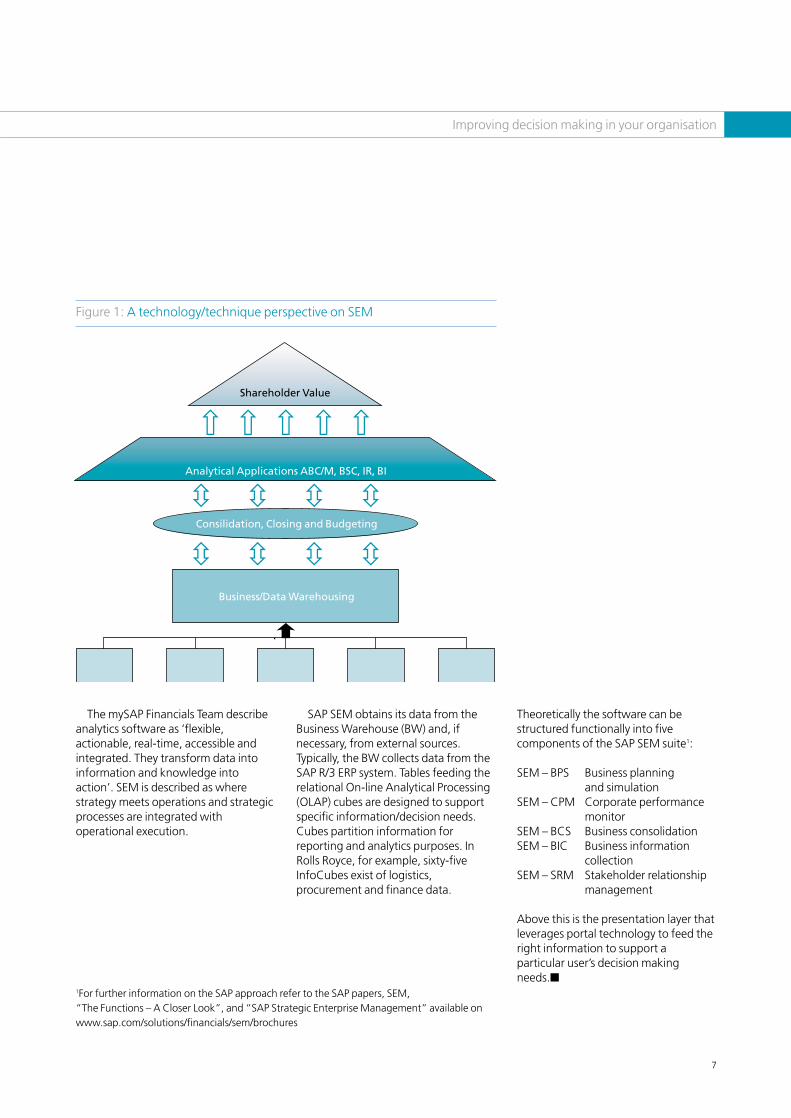

We know from the software vendorsthat from a technology perspective,SEM is an attempt to improve themanagement of an organisation bygiving finance professionals better toolsand approaches to improve analysis andinformation for senior executives andother managers. In this respect, thetheory was that SEM could fulfilexpectations for ERP and provide usefulinformation for senior managers. Thistheory, however, is difficult toimplement. As figure 1, illustrates SEMtechnologies exploit emerging datawarehousing and modellingtechnologies to deliver information andanalysis across a range of applicationareas. This is the sort of genericarchitecture that SEM might look liketechnologically.

At the bottom sit the organisation’sunderlying systems, which feed into adata warehouse in which informationcan be manipulated. This in turn willfeed structural applications such asconsolidation, the monthly andquarterly closing and the annualbudget.

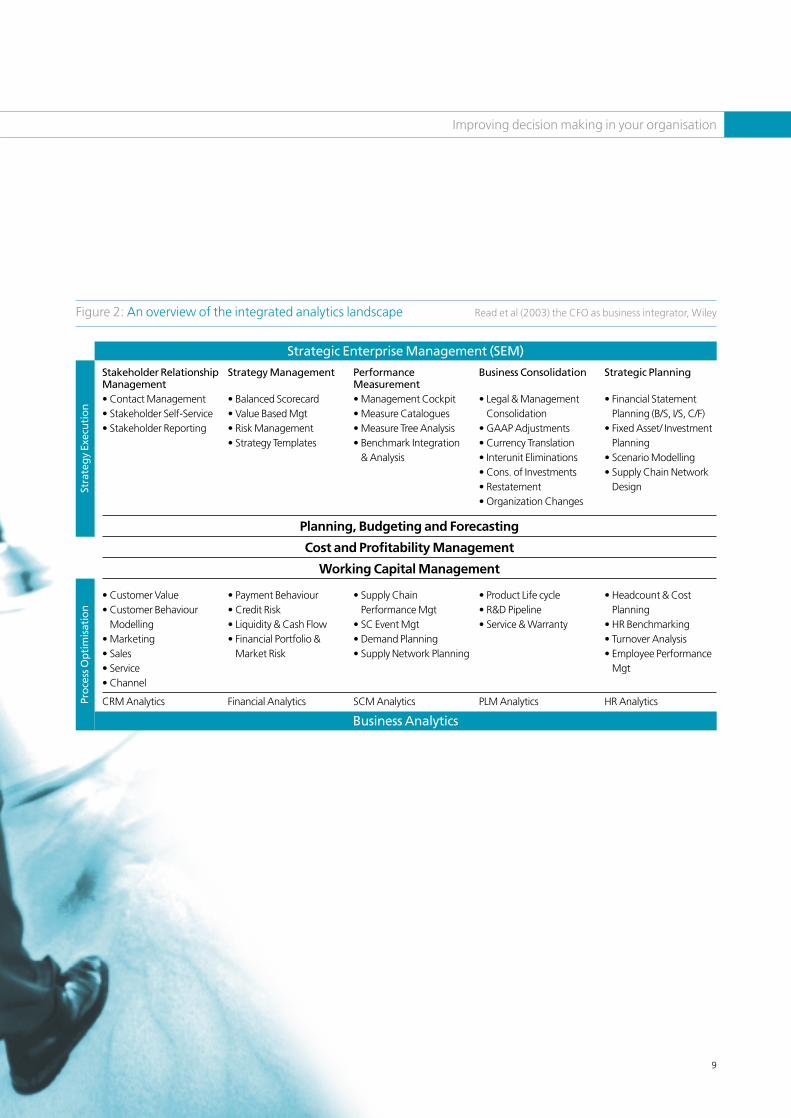

Above that are the more analyticalapplications such as activity basedcosting (ABC), the balanced scorecard(BSC) and investor relations andbusiness analytics for processoptimisation (figure 2 provides anoverview of the integrated analyticslandscape in the SEM environmentsenvisioned by Cedric Read and themySAP Financials Team).

While precise definitions cannot communicate thefull nature of SEM, a working definition could be:

An approach to strategic management which focuses oncreating and sustaining shareholder value through theintegrated use of best practice modelling and analysistechniques, technologies, and processes in support ofbetter decision making.

Improving decision making in your organisation

7

Figure 1: A technology/technique perspective on SEM

1For further information on the SAP approach refer to the SAP papers, SEM,“The Functions – A Closer Look”, and “SAP Strategic Enterprise Management” available onwww.sap.com/solutions/financials/sem/brochures

Shareholder Value

Analytical Applications ABC/M, BSC, IR, BI

Business/Data Warehousing

Consilidation, Closing and Budgeting

The mySAP Financials Team describeanalytics software as ‘flexible,actionable, real-time, accessible andintegrated. They transform data intoinformation and knowledge intoaction’. SEM is described as wherestrategy meets operations and strategicprocesses are integrated withoperational execution.

SAP SEM obtains its data from theBusiness Warehouse (BW) and, ifnecessary, from external sources.Typically, the BW collects data from theSAP R/3 ERP system. Tables feeding therelational On-line Analytical Processing(OLAP) cubes are designed to supportspecific information/decision needs.Cubes partition information forreporting and analytics purposes. InRolls Royce, for example, sixty-fiveInfoCubes exist of logistics,procurement and finance data.

Theoretically the software can bestructured functionally into fivecomponents of the SAP SEM suite1:

SEM – BPS Business planningand simulation

SEM – CPM Corporate performancemonitor

SEM – BCS Business consolidationSEM – BIC Business information

collectionSEM – SRM Stakeholder relationship

management

Above this is the presentation layer thatleverages portal technology to feed theright information to support aparticular user’s decision makingneeds.�

Improving decision making in your organisation

8

3 Why the emphasis on new technologies?

Having time for strategy formulationis or should be a key focus of mostexecutives’ attention. The challenge tobusiness leaders is to design, configureand adapt business models that delivervalue to customers. Consequently,executives are continually seeking todevelop strategies that producesuperior financial results. In addition totheir part in strategy development,senior executives also play an importantrole in business execution and effectivecontrol frameworks that are required toensure operational effectiveness. Formany industries, competitive advantageis transient. Companies develop newstrategies more quickly and have tomobilise their operations to executethese. Adopting new strategic positionssuccessfully depends on devolvingauthority to operations.

In order to support these roles, and toensure decision making processessupport shareholder value generation,executives need decision support andinformation systems that allowthem to:• Quickly identify changes in the

market environment and react tothem with new, adapted strategies;

• Evaluate and compute thesestrategies using scenario and activitybased planning;

• Integrate planning, budgeting andforecasting processes;

• Operationalise new strategies usingconcrete goals and correspondingmeasurements and initiatives;

• Acquire actual data from differentsources and consolidate financialdata flexibly;

• Monitor goal achievement andbenchmark the performanceinternally and externally; and

• Communicate efficiently withexternal stakeholders.

The adoption of these SEM systemsand analytical applications is claimed toresult in the movement away fromspreadsheet software for budgetingand performance measurement andbetter strategic decision makingbecause information for strategicinitiatives is included in the system.

It is only when this capability is inplace that an organisation can begin todevelop and sustain competitiveadvantage by enhancing strategicdecision making. To effectively supportthe value creation process executivesneed knowledge and information thatallows them to answer strategicquestions such as:• Which customers are delivering the

bulk of our economic profit?• Which parts of the business are

creating/destroying shareholdervalue?

• How is our business model working?• What are the real drivers of our

business performance?• What do these figures mean? How

important are they?• How do we know if we are doing

well relative to the competition?

Improving decision making in your organisation

9

Planning, Budgeting and Forecasting

Cost and Profitability Management

Working Capital Management

Strategic Enterprise Management (SEM)

Business Analytics

Figure 2: An overview of the integrated analytics landscape Read et al (2003) the CFO as business integrator, Wiley

Stakeholder RelationshipManagement• Contact Management• Stakeholder Self-Service• Stakeholder Reporting

Strategy Management

• Balanced Scorecard• Value Based Mgt• Risk Management• Strategy Templates

PerformanceMeasurement• Management Cockpit• Measure Catalogues• Measure Tree Analysis• Benchmark Integration

& Analysis

Business Consolidation

• Legal & ManagementConsolidation

• GAAP Adjustments• Currency Translation• Interunit Eliminations• Cons. of Investments• Restatement• Organization Changes

Strategic Planning

• Financial StatementPlanning (B/S, I/S, C/F)

• Fixed Asset/ InvestmentPlanning

• Scenario Modelling• Supply Chain Network

Design

• Customer Value• Customer Behaviour

Modelling• Marketing• Sales• Service• Channel

CRM Analytics

• Payment Behaviour• Credit Risk• Liquidity & Cash Flow• Financial Portfolio &

Market Risk

Financial Analytics

• Supply ChainPerformance Mgt

• SC Event Mgt• Demand Planning• Supply Network Planning

SCM Analytics

• Product Life cycle• R&D Pipeline• Service & Warranty

PLM Analytics

• Headcount & CostPlanning

• HR Benchmarking• Turnover Analysis• Employee Performance

Mgt

HR Analytics

Stra

teg

y Ex

ecu

tio

nPr

oce

ss O

pti

mis

atio

n

Improving decision making in your organisation

10

4 What is preventing progress in many companies?

Many companies have madesignificant investments in enterpriseresource planning (ERP) systems andtop-up analytical decision supportapplications to help improve theirmanagement information and decisionmaking. The technology exists or israpidly emerging but the managementaccounting techniques are not new.Advanced techniques includeshareholder value management (SVM),the balanced scorecard (BSC) andactivity-based costing/management(ABC/M). However, they are not aswidely used on an effective basis asmight be thought and the integrationof these techniques into a newinformation systems framework isextremely difficult to achieve in largecomplex organisations.

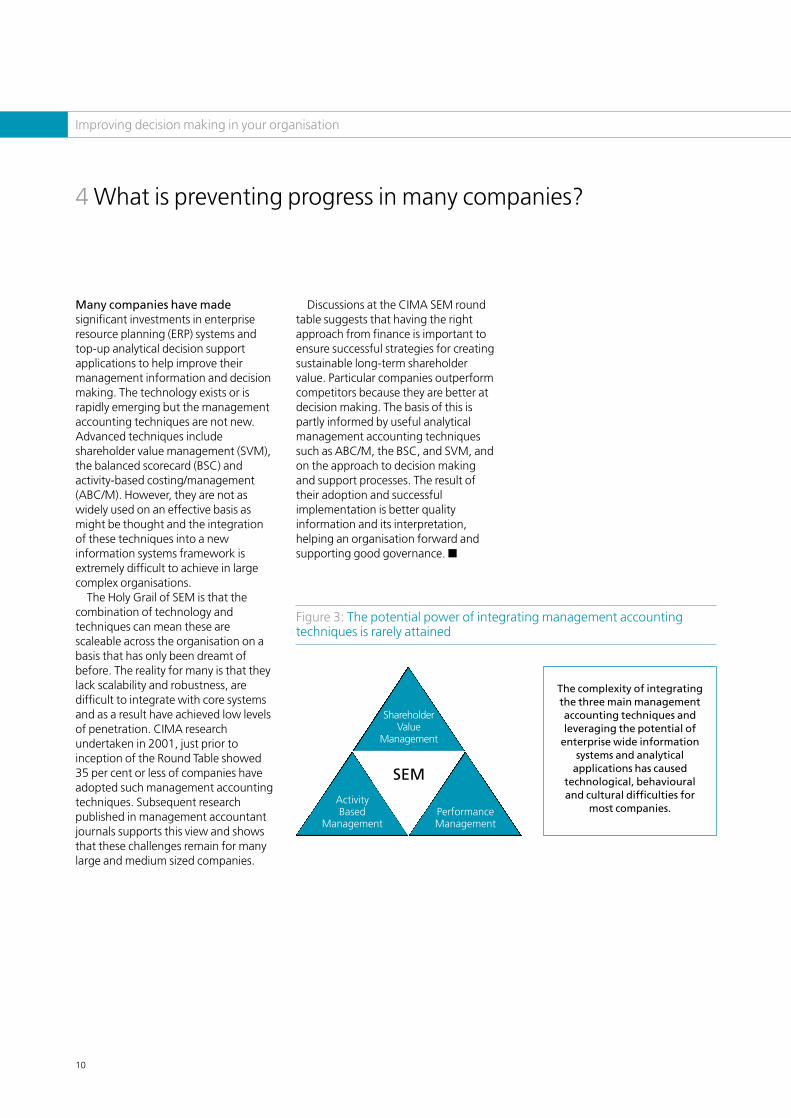

The Holy Grail of SEM is that thecombination of technology andtechniques can mean these arescaleable across the organisation on abasis that has only been dreamt ofbefore. The reality for many is that theylack scalability and robustness, aredifficult to integrate with core systemsand as a result have achieved low levelsof penetration. CIMA researchundertaken in 2001, just prior toinception of the Round Table showed35 per cent or less of companies haveadopted such management accountingtechniques. Subsequent researchpublished in management accountantjournals supports this view and showsthat these challenges remain for manylarge and medium sized companies.

Discussions at the CIMA SEM roundtable suggests that having the rightapproach from finance is important toensure successful strategies for creatingsustainable long-term shareholdervalue. Particular companies outperformcompetitors because they are better atdecision making. The basis of this ispartly informed by useful analyticalmanagement accounting techniquessuch as ABC/M, the BSC, and SVM, andon the approach to decision makingand support processes. The result oftheir adoption and successfulimplementation is better qualityinformation and its interpretation,helping an organisation forward andsupporting good governance. �

The complexity of integratingthe three main managementaccounting techniques andleveraging the potential of

enterprise wide informationsystems and analytical

applications has causedtechnological, behaviouraland cultural difficulties for

most companies.

Figure 3: The potential power of integrating management accountingtechniques is rarely attained

SEMActivityBased

Management

ShareholderValue

Management

PerformanceManagement

Improving decision making in your organisation

11

5 The real world issues for SEM technology

Systems like spaghettiThe problem is that, in reality, manyorganisations’ systems resemblespaghetti. There are differentoperational systems running ondifferent platforms, perhaps resultingfrom acquisitions and other sources ofdiversity. Those organisations that havepursued organic growth may be usingolder systems that until now have mettheir needs in terms of transactionalprocessing. Traditionally, manualintervention is required to convert thetangle into useful information andinsight for people elsewhere in theorganisation.

The historical view of many financefunctions is not the way in which manyCFOs want to work. Many willrecognise the following scenario.Operations people extract all theinformation they have and email it in tofinance. Intra-group differences areeliminated, totals are checked, theentries for last month’s figures arescrutinised and checks are made formovement in inventory. The data isentered into a spreadsheet andpresented to the executive committee.This is not how organisations should beworking but SEM technology does notseem to have solved all the problems,and indeed has introduced others.

The reality is that the systemsscenario is varied. Some organisationshave no ERP in place, relying purely onMicrosoft Excel or, in some cases, alsousing an integrating tool like Frango orHyperion. Others have an ERP system,maybe a few SAP SEM modules, orhave a planning and budgeting solutionbut still rely on Excel.

Many companies rely on a ‘best ofbreed’ solution. For example, takingERP and integrating into Hyperion anda data warehousing solution, thenfeeding it into Hyperion’s consolidationsystem, and then into Excel and PowerPoint.

It is not unusual for companies to behesitant to engage new technology.System complexity and a lack ofresources are as good a reason as any todelay investment in expensive software,particularly in times when overheadcontrol is a priority. For many,management’s attention was distractedfrom cost management because of the‘good times’ characterised by year onyear revenue growth. Currently, manyfinance professionals are focused moreon cost management and reductionsthan on better managerial support. �

Improving decision making in your organisation

12

6 The problematic relationship betweenmanagement accounting and IT

The complexity of utilising andintegrating the advanced managementtoolset, cannot be underestimated.Many management accountants arehindered by the problems of integratingsophisticated applications such as ABCinto the enterprise-wide system. TheRoyal Mail, which has made significantprogress in implementing newcorporate information systems toimprove decision making, took arounda year to bridge its ABC system with themain ERP system, and even now it is notfully integrated. An important lessonlearned in this case relates to thedifficulty of integrating different vendorsoftware and the high degree ofcustomisation required to makesystems work.

Field study research published in2002 by Granlund and Malmi into theimpact of ERP systems on managementaccounting in ten large companies,including Nokia and ABB, showed howin only half of the companies, productand customer level cost and profitabilityaccounting was handled in the ERPenvironment. Those that operated costaccounting outside the ERPenvironment used stand-alonesoftware or spreadsheets and eitherhad no time for configuring costinginto the ERP system or had recentlyinvested in separate software and hadcurrently no intention of integrating it.Those firms that operated costaccounting in the ERP system hadsimply transferred the previousprinciples into the new system whichmeant that costing had not become‘smarter’ but ‘faster’. Overall, theresearch found that ERP systems are notdriving the adoption of new accountingand control techniques.

The logical reason for the lack ofintegration of management accountingtechniques is mainly down tocomplexity. The cases both in thisresearch and within CIMA’s own RoundTable discussions have shown howmuch time and resource big enterprisesystem projects consume. The featuresvital for basic operations are configuredwell before ABC or balanced scorecardcapability, for example, are considered.It also important to ensure that criticalapplications such as the BusinessWarehouse are suitable. One companyhas created additional data warehousesindependent of the ERP system tofacilitate area based profitabilityanalysis. This is simply a return to poorfunctionality and complexity that hasnegative effects on decision makingcapability and can occur where ERPsystems are structured aroundresponsibility centres.

In terms of the functionality of thebalanced scorecard, all the companiesinvolved in the Granuland and Malmiresearch and most on our Round Tablewhich use the balanced scorecard,maintain it in spreadsheet or the LotusNotes environment. And althoughsome of the information contained inthe balanced scorecard report comesfrom the ERP system, some of it(particularly the externally sourcedinformation) comes from outside theERP system.

IT complexity can take different formssuch as integration of separatesoftware and enterprise systems andthe building of specific interfacesbetween these. The complexity of ITissues can make the quality of the ABCapproach fragile and IT constraints onthe use of management accountingsolutions can lead to weakmanagement information. Research byWillis in 2001 into the codes for cost

management in field operatingorganisations demonstrated that insome ERP systems there is no viablefunctionality or coding structure tobuild ABC conveniently into the system.

Therefore, an initial investment in ERPsystems or SEM component softwareshould take into account theintegration of management accountingtechniques to improve decision making.There needs to be recognition thatmajor shifts in managerial control anddecision making may not be seen for aperiod of time but ABM systems thatare not integrated and linked to existingfinancial and operations systems will bemore difficult and more expensive toupdate and maintain.

Markus Granlund and Jan Mouritsen,in introducing a selection of research onmanagement control and newinformation systems in the EuropeanAccounting Review (2003), also raisethe possibility that the ERP systems aremore concerned with certain aspects ofmanufacturing and distribution thanwith management control in practice.This is contrary to what the ERP vendorsstate about the role of these systems insupporting strategic management.They also usefully make the point thatthese are not permanent problems andthe intense product development andthe constant release of new softwarewill inevitably introduce solutions tomany of the emerged problems.

This is not to say integration ofmanagement accounting techniqueswith enterprise solutions does notpresent its own set of issues. In aHarvard Business Review article in1998, Cooper and Kaplan warned thatoperational control and activity basedcost systems have fundamentallydifferent purposes and as such the two

Improving decision making in your organisation

13

systems can only be partially integrated,and the integration must be handledthoughtfully. The two systems cannotuse the same inputs because theydefine cost differently and ABC haslower requirements for accuracy. ABCin giving a more strategic view of theorganisation, relies on strategic costingfor products, services, customers ororganisational units and this allowsmanagers to understand profitability atvarious levels. Costs are aggregatedacross multiple cost and responsibilitycentres. On the other hand, theoperational control system measuresactual expenses incurred in aresponsibility centre and features coststhat can be controlled. These costs areactual (rather than standard) and areupdated continually as opposed toperiodically.

The contextual nature ofmanaging performanceMany of the SEM Round Tablecompanies are showing how an SEMapproach, of which ERP and SEMsystems are only one driver, can allow

large corporates to balance the trade-offs between size and agility allowingthem to enhance shareholder value.The key driver of their efforts is fasterand better decision making at variouslevels of the organisation and not thetechnology. The way it is beingachieved, however, varies betweenorganisations and each has a differentand contingent emphasis.

There exists a tension in manyorganisations between accepting adegree of standardisation in terms ofprocesses and decision supportsystems, and customisation. Howsimilar can information flows andprocesses be to those of competitorsbefore sources of differentiation beginto be undermined? Some vendors havebeen accused of not wanting to dealwith companies which wish for a largeamount of customization to thevendor’s systems and approach. Oneresponse is to only deploy those SEMmodules that are required to supportspecifically identified processes andkeep existing systems where adequate.

In reality however, there are anumber of critical variables that need tobe considered that affect crucial issuesof balance and integration whendesigning, implementing and usingperformance management and henceSEM systems. Stan Brignall, based atAston University, has identified anumber of institutional factors thatneed to be considered in the design ofintegrated costing and performancemeasurement systems. The first set offactors relates to the business andproduct lifecycle, which includes thestrategy being pursued, mission andthe competitive environment. Thesecond are those related to anorganisation’s production or servicedelivery process type. These factors varyacross organisations and within any oneorganisation over time. Differentproduction and service process typesraise different issues for managementand require different managementaccounting systems, and some likeABM for example, may not beuniversally applicable. He argues thatthe customisation of SEM systems isnecessary to enable each organisationto align its systems to the context inwhich it operates (using the factorsidentified as a guide).

Improving decision making in your organisation The problematic relationship between management accounting and IT

14

Management accounting change is not rooted in newtechnologies but is about improving managerial work anddecision making

Other management writers raiseother factors such as recognising theimportance of differing stakeholderinterests, and therefore potential powerbases, and cultural factors, particularlybetween Western and Asianenvironments. The message for all CFOsis that the interactions between toolsand techniques is not unproblematicand it is not advisable to consider theseissues simplistically or, for example,along functional lines. The challenge ofmanagement accounting change isrooted as much in the behavioural andcultural aspects of changemanagement. In implementing achange programme and new systems itis necessary to recognise differentrationalities and understanding of thebusiness. Recent CIMA research on thechallenge of management accountingchange identified the following keyquestions that raise importantbehavioural and cultural issues:• Do staff understand the nature and

significance of the new systems?• Do the new systems fit the

established ways of working in theorganisation?

• How will the new systems impact onthe various factions within theorganisation?

Acceptance and ownership of newsystems is therefore unlikely with atechnically focused change programmethat gives little consideration to theinstitutional aspects of the changeprocess and ultimately what is trying tobe achieved with the new approaches.

As Fahy identified in his book on SEMsystems in 2001, an SEM approach canrelease finance professionals from thedrudgery of monthly corporatemonitoring allowing them toconcentrate on more valuable analysisso that their role takes on a morebusiness and support orientedperspective. In subsequent research byScapens and Jazayeri (2003) based inthe European division of a large USmultinational, although there were nofundamental changes in the nature ofthe management accountinginformation used following theimplementation of SAP, there werechanges in the role of managementaccountants. In particular, they identify:• The elimination of routine jobs;• More forward looking information;

and• A wider role for management

accountants.

The company does not, however,claim that SAP was the driver of thesechanges but rather that thecharacteristics of SAP (such asintegration, standardisation,routinization and centralisation),opened up certain opportunities andfacilitated changes that were alreadytaking place in the company (Scapenset al). The information from the SAPsystem was improving managementinformation (including the speed ofdelivery of reports) in the ‘bottom-half’of the company, but beyond operationsmanagers tended not to use SAP astheir source of information.

New technology is therefore enablingchange of the management accountingfunction but on a different basis thansome companies have perhapsexpected. In the past, financeprofessionals have either been criticisedfor not meeting the decision makingneeds of business executives orperceived to be undertaking only apolicing role. Businesses want financeprofessionals who can help them createshareholder value. To do this,organisations need to design andconfigure a sustainable business modeland this in turn requires a financefunction which can provide decisionsupport and analysis capability acrossthe range of strategic management andoperational activities. This involvesfinance professionals interactingregularly with other parts of thebusiness. As a supply chain managercommented in recent CIMA research(entitled The future direction ofmanagement accounting practice2003) – ‘the finance controller says thathe is happiest if he can stand up in theaccounting department and cannot seeanybody – because they are all outwhere they should be – havingmeetings with non-finance managers’.

One Round Table member, the Headof Pharmaceutical Finance andControlling for a large multinationalpharmaceutical company, describedhow all his reports spent around eightyper cent of their time in multi-disciplinary teams. The financeprofessional is viewed as central tonavigating the work of a particularfunction and providing the appropriateinformation to support decision makingand the advice where required toimprove decision making processes.In such an environment, the credibility

Improving decision making in your organisation

15

of individual finance professionals iscrucial and relates to theirunderstanding of the business modeland its value drivers. The progress ofthe finance function has been based ontheir mix of highly skilled people withdiverse backgrounds.

In thinking about the development ofthe finance function in yourorganisation, it is worth taking a stepback to consider the development ofmanagement accounting over time.This is useful in understanding whatmanagement accounting tools andtechniques should be used to helpbusiness and the vital skills thatbusiness accountants require to supportthe business. This will allow you toreview the type of role your businessaccountants undertake in yourorganisation.

It is also important to appreciate thatSEM is not simply some new magictechnology. SEM as a managementactivity has been around for decades,ever since companies began torecognise the need for better strategyformulation and execution. Financeprofessionals such as managementaccountants and others have beenproviding SEM type support usingspreadsheets, extract programmes anda lot of hard work. Over time, there hasbeen a continuous stream ofdecision/executive support typesoftware such as EIS, data mining anddashboards. Many of thesetechnologies were sold as a panacea forall firms’ reporting and analysisshortcomings. SEM technologies drawvaluable lessons from the less thansuccessful experiences with theseearlier technologies by recognising theprimacy of the executive and relegatingthe technology to a supporting role. �

Improving decision making in your organisation

16

7 The evolution of management accounting

Historically, management accountingwas grounded in factory and costaccounting. During the 1980s and1990s, new challenges emerged andthe traditional roles and methods werechallenged. In many organisationstoday, the changing role ofmanagement accounting manifestsitself with management accountantsbeing concerned with the future andmeeting organisational goals byworking with the management teamand other parts of the organisation toinfluence management behaviour anddecision making.

In the late 1980s and early 1990s, thefirst major development to evolve wasmulti-dimensional managerialaccounting and reporting through newhigh level approaches such as the multi-dimensional performancemeasurement (sometimes via thebalanced scorecard) and Activity BasedManagement. This was a directresponse to the narrow value addedperspective adopted by earlier costaccounting.

A second development has involvedbroadening the role of themanagement accountant from merelyan internal focus to the provision ofinformation and analysis aboutcompetitors and the external businessenvironment. This can be a key area ofdecision support, particularly becausethe standardisation of manyorganisations’ information flows andprocesses by software providers canundermine sources of differencebetween businesses. How suchbusiness intelligence is collected, storedand controlled is one question.Recognising its importance in askingthe right questions and in makingdecisions in the first instance,specifically in terms of the assessmentof strategic position, is another.

The managing director of the divisionof an international energy companydescribed to the Round Table how thekey decisions the board needed tomake were largely based on thefollowing reports prepared by thefinance function in conjunction withothers:• Weekly and monthly finance reports;• A balanced scorecard performance

measurement report;• Commodity market prices;• A monthly risk management

committee report;• Project implementations report.

In the SEM environment that is beingfostered, a range of information needsis supported with finance, risk basedand externally sourced information tocomplement internally derived data.The emphasis at this strategic level is ontimely and accurate information,flexible reporting and the minimisationof duplication of information.

Such developments have allowedmanagement accounting to play anactive role in supporting strategicdecision making and monitoring theimplementation and success ofstrategic plans. But the development ofthe finance function and financeprofessionals as strategic businessmanagers is a trend restricted to onlysome organisations. �

Improving decision making in your organisation

17

8 Broadening the view on SEM

CIMA SEM is very much aboutenhancing the role of managementaccountants to add value constantly aspart of a management team by taking avalue creation perspective and properlyintegrating advanced managementaccounting techniques and enablingtechnologies into the business.

Leading organisations can excel intheir decision making where they getthe right information and analysis, tothe right people at the right time.Operational managers, workers, andsuppliers where appropriate havebroader access to operatinginformation. But information provisionis only part of the story. Executives andsenior managers should receive theinformation that they need to steer thebusiness forward. Some organisationscontinue, however, to struggle informulating and delivering strategicobjectives because they have failed toeffectively decentralise theirmanagement accounting function andimprove their data interpretation. This ispartly down to people and approaches,in particular the interface betweenmanagement accountants and otherdisciplines, and partly down totechnology. What organisations knowis that they need finance professionalswho can help create shareholder value.This can only be achieved by financefunctions providing decision supportand internal consultancy across a rangeof strategic management activities andto different management levels. Therole being performed by manymanagement accountants should bebased on being a change agent andselling the idea of what can be donewith information.

Insight box: The shortcomings of management accounting and controlsystems in some organisations can be identified as:

• A lack of strategic focus on competitors, customers and products and the failureto address the information needs of wider stakeholder groups.

• The absence of the balanced scorecard approach and the focus on mainlyfinancial historical measures of performance. The financial bias in reportingsystems leads to a lack of focus on the drivers of performance. This also makes itdifficult to provide adequate support for cost reduction programmes.

• Reporting under traditional legacy systems is cyclical in nature and oftenrestricted to batch and month end reporting.

• In many cases IT is a constraint on an organisation’s ability to implement newreporting processes and measures, and to develop unique processes.

• Important business knowledge and understanding of the underlying processes isoften embedded in poorly documented spreadsheets.

• With business models and corporate strategies continually changing manyorganisations find that their reporting systems do not reflect the changingcorporate strategy.

• An excessive control focus has led to neglect of decision support for importantareas such as business problem solving and direction setting.

Source: Fahy M (2001) Strategic Enterprise Management Systems, CIMA

Improving decision making in your organisation

18

9 The key management accounting techniques and competencies

CIMA research published in 2003 onthe future directions of UKmanagement accounting practice putsstrategic management accounting asthe second vitally importanttool/technique for development in theperiod up to 2005. Advancedtechniques such as value addedaccounting, ABC and the balancedscorecard all make the top ten. It is alsointeresting to note the changing skill setof management accountants requiredin their role working alongside andsupporting their managerial colleagues,and integrating strategic, financial andoperating dimensions of a business.

The research found that the newapproaches to control are effectivelybased on the notion of empowerment,which relies on trust, teamwork andco-ordination. The managementaccounting function is becomingdecentralised (i.e. more integrated intothe business) while the financialaccounting function is experiencing anincreasing centralisation where routinetasks are outsourced. Where the focusis now on business processes,responsibility will cut across traditionalfunctional boundaries leading to theincreasing use of team basedperformance measures. Managementaccountants within a process should beworking with other managers moreclosely than their accountingcolleagues. To undertake this role, theyneed to understand the industry andbusiness that they are in and theproducts produced and customersserved. It is also interesting to note thatScapens, in his field research, identifiedthat the integrated nature of SAP led toa lack of confidence in the system, andincreased cross-functional co-operationand teamwork ultimately overcamethis. The key change was for the

finance function to look at the businessas a set of processes rather than asfunctions, resulting in a more processorientated organisation.

Skills diversity in theworkforceMany organisations across most sectorshave one issue in common which iscompeting in the market for talent andensuring a diverse workforce wherejobs are filled with the best and mostappropriate people. It is the technologyand systems space that is probably oneof the most competitive because of theshortage of skills. And many financeprofessionals lack skills in this areawhich can slow down implementationand increase risk of failure.

One big issue for finance teamsrelates to the skills updating that isrequired to work with new technologysuch as SAP SEM. Some financeprofessionals need to understand thestructures that underlie the SAPsoftware, the database and on-lineanalytical processing (OLAP) technologyand how data can best be manipulatedto suit management need. Financeprofessionals involved in enterprisesystems projects need to develop newskills in:• The creation, manipulation and

provision of the information set anddeployment of processes; and

• The use of information and analyticalcapability to make better decisions.

And above all they must understandthe business.

Before a SAP SEM implementation, itis important that the finance functionhas a clear idea of the information setupon which different parts of thebusiness will rely to manage thebusiness going forward. If this is notidentified, it is likely that the SEMimplementation will fail to live up tomanagers’ expectations.

Deloitte and Touche Consultingrecommends that the strategicdevelopment process within thecompany is at an advanced stagebefore the technology is implemented.Working within a value basedapproach, companies need to start byunderstanding the governing objectiveand the strategies which could drivemaximum profitable growth. Thetendency in many companies was forthe chief information officer to workfrom the wrong starting point.

Finance people with the right skillsets who can work with newtechnology are required. Although withOLAP tools it is possible to process thevast amount of data found incompanies in many ways, manymanagers do not have the skills or timefor this. It is also apparent from ourRound Table discussions that SAP andthe large consultancies seem also shortof the right people to develop thesetools. The Royal Mail in the UK hassecured specialists in OLAP technologythrough the contract market butretention is a key issue. Skillsdevelopment of in-house employeeshas become a focus and there are in-house ERP (R/3) technicians who havedeveloped new skills to work with thebusiness warehouse. The renewedfocus on process and skills developmentis certainly helping many businesses.

Improving decision making in your organisation

19

Information systems that reflect astrategic view of the organisation aresold on the basis that they typicallyinclude:• Analysis of costs and business drivers;• Indicators of progress towards

achievement of a ‘total quality’environment in the organisation; and

• Information relevant to strategicplanning and forecasting.

In addition, senior management’sinformation requirements may includeboth external and internal, as well asboth financial and non-financialinformation. As a result, seniormanagers require: • substantial flexibility in the type and

format of information which they canobtain from their informationsystems, i.e., the types of informationwhich managers require for strategicplanning purposes is likely to varyover time;

• flexible modelling capabilities toenable them to analyse data andinformation in whatever manner theyconsider appropriate in givencircumstances.

The focus for CIMA members andstudents is that they have access to: • Excellent analytical skills using not

just financial analysis, butcustomer/market analysis, statisticaland in some cases more sophisticatedmodelling techniques includingsimulation;

• A realisation of the need for multi-disciplinary team approach to informkey decision making (for exampleinvestment, marketing), including theability to integrate inputs fromdiverse experts;

• Strong commercial acumencharacterised by strong product,process and market knowledge,typically gained from an early stageby their practical experience whenstudying;

• Effective interpersonal skills whichallow them to adopt a moreconsultative approach;

• A strong coaching ability that helpsmanagers to be more focused onadding value;

• Forward looking perspective wherethey appreciate value rather thancost;

• An openness to sharing of bestpractice and a willingness to partnerwith the business managers. �

Improving decision making in your organisation

20

10 A summary of the key components of SEM

Creating and sustainingshareholder valueWithout doubt, one of the mostinfluential drivers of change in recentyears has been the growing demands ofindividual and institutional shareholdersfor greater value creation. However,there is increasing dissatisfactionamong senior managers with thequality of the strategic managementprocesses in their organisations. Itappears that growing stakeholderdemands and increasing organisationalcomplexity have revealed ashortcoming in many organisations’ability to respond to the increasedvelocity of change and enterprisemanagement. A properly managedvalue based approach provides topmanagement with a framework forsupporting decisions around strategyand structure.

Under the existing approach tostrategic management processes, manycompanies have failed to redesign thereporting and performancemanagement systems to take intoaccount the governing objective ofshareholder value. Consequently, manyof the systems currently in place reflecta bottom line profitability perspectiverather than a value perspective. Therhetoric of value management is notmatched by the reality of performancemanagement and business execution.

Until the transition to a value basedmanagement approach is adopted byan organisation, and the managementaccounting process supports this, thegoverning objective in yourorganisation could still be based on theinterests of the institution rather thanthe shareholders. The promotion ofgrowth, the need for prestige and theretention of the existing boundaries ofthe firm can all destroy value over time.Central to a SEM approach is managingfor value and maximising shareholdervalue by generating, choosing, andimplementing the best alternatives forbusiness strategy. The successful pursuitof a value based approach cannot bereserved for parts of the organisationand needs to be accompanied bydisciplined decision making with asingle governing objective and the rightperformance management approach.

It involves finance professionalsmoving their horizon from the monthlyprofit and loss statement to providingrelevant information that reflects thecompetitive environment and advisingon real value creating elements of theorganisation. The value based view ofthe organisation should cover fourimportant areas:1 A value assessment where a review of

economic profit across investedcapital by product leads to prioritiesbeing based on growth and return

2 Value driver analysis, which looks atoperational initiatives to create value.Some companies select the key valuedrivers behind each major P&L itemand also take into account strategicdrivers

3 Management processes redesign sothat management processes withinthe activities of planning, budgetingand performance managementsupport value objectives

4 Value reporting where performanceis communicated in an improved wayinternally and externally.

When Lloyds Bank in 1980s andBoots plc in the 1990s explicitly voicedtheir overall governing objective ofmanaging for value, the CEOs anddirectors spent much time in face toface meetings with the main fundmanagers to explain what this meantfor the management of the companyinternally, and how it would affect theirreporting to the markets. The success ofVBM and business performance inthese companies was down tounderstanding what factors drive value,what decisions are creating ordestroying value and establishing valueas the criterion for decision making atall levels.

Improving the process ofdecision makingThe CIMA Round Table has alsoconsidered the psychology and processof decision making within a SVMapproach. Evaluating the quality ofdecision making is very much abouthaving the right process. Goodoutcomes do not inform managerswhether a good decision makingprocess has been pursued. Improvingdecisions involves understanding whata good process is – deciding how todecide – before undertaking anyactions or diving into a SEM approach.

Executives and managers need tospend time on answering the question,What is it that we need to decide? Onlywhen the crux of the decision has beenunderstood can the actual decisionmaking process kick in. Understandingwhen a decision has to be made is alsojust as important. Technology does notimprove the dynamics of decisionmaking. Peoples’ attitudes andbehaviour does. People can drawfeedback from related decisions andexperiences and judge the context ofeach situation. Without analysing thedecision making process it is difficult tounderstand what decision support isrequired.

Improving decision making in your organisation

21

For finance professionals, decisionmaking is a key issue. Taking an initialstep back to view their context andenvironment is an essential part ofimproving decision making. In a worldwhere there is so much information,care has to be taken to challengeperceived reality and not be lulled intobelieving that our decision makingperspective is complete.

In terms of improving strategicdecision making, there are six keychoices and challenges for managers.These are:• Which decisions?• Which decision making process?• Who is involved?• When a decision has to be made?• What kind of decision support?• How to get consensus on quality?

Companies rarely treat decisionmaking as a distinguishing competenceof the business. Within a structuredframework for decision making, thetwo main issues that managers need tofocus on are identifying the opportunitiesfor profitable growth andunderstanding the strategic threats(whether internal or external) and thepossible management responses tothese.

Broadly, the intervention by thefinance function can occur at differentlevels from undertaking the rigorousanalysis upon which decisioninformation needs to be based to beingthe ‘high priests’ of SVM. The latterrequires setting financial goals todeliver the governing objective, settingkey financial metrics such as cost ofcapital and lease capitalisation andsetting reward measures.

Many boards and managers needstrategic insights and guidance onestablishing a structured and highquality decision making procedure.Senior managements’ informationrequirements will include both externaland internal, as well as both financialand non-financial information.

As providers of decision information,the finance function needs todetermine what decision support isappropriate so that decisions are basedon fact. For example, managers need tounderstand which products are makingan economic profit (loss) and, thestructural forces behind the economicprofit (loss). Forecasting of eachstructural factor allows the profilingover time of profitability and growth.Such analysis should be accompaniedwith quantitative and qualitativeinformation on competitors such asrelative pricing by product market andrelative economic costs, customerneeds and competitor offerings. Acomplete assessment includes an

analysis of the financial performancebased on the current strategy. Thisrequires creating income statementsand balance sheets at business unitlevel so information is generated on theeconomic profitability of individualproducts and customers. This type ofcomprehensive assessment allowsinsight into current strategicperformance and a managementconsensus on alternative strategies.

The rigour of analysis required toenable management to understand abusiness’ value drivers and potential forvalue creation can and should arguablybe, at least in large part, delivered bythe finance function. This is a significantmove away from basing decisions onintuition and experience and can honemanagement’s attention on thebusiness issues that may enable anorganisation to achieve and sustain acompetitive advantage over time.

Improving decision making in your organisation A summary of the key components of SEM

22

Empowering operationsAs discussed earlier, rather thanfocusing solely on control andtransaction processing, the financefunction can move towards a businessadvisor role based on supportingbusiness decisions. Various tools andtechniques can be deployed to facilitatethe transformation over a period oftime. These include effectivecommunication, Investors in Peopleaccreditation, the creation of abenchmarking culture and thedeployment of a SEM approach. Thesuccess of SEM in many companies onthe Round Table has so far been basedon improving decision making in the‘bottom-half’ of the organisation.

Better informed decisions are based on:• A common reporting model across

operations;• An optimised reporting process;• Single version of the truth;• Quicker decision making (although

not always in real time).

The implementation of an integrateddata warehouse for Rolls Royce, whichincluded both company and supplierinformation, rationalised operationalprocesses to deliver a common base foreffective Global ManagementReporting. This enabled faster productdevelopment, assembly, manufacture,and supply, and getting the rightinformation to the right people quicklyand easily.

The business benefits included:• Improved business and management

reporting;• Complete and up-to-date picture in

one single point of access;• Multi-business views and analysis;• Facilitation of the transformation of

data into knowledge;• Empower employees to make better

informed decisions. This includedsupporting people not only inmanufacturing but also in R&D andmarketing functions. Productplanners and senior corporateexecutives alike can monitor andimprove performance.

Financial and non-financialinformation is sourced from all parts ofthe business to feed the planningprocess and to support decision makingon sales volume planning throughmaterials requirements, cost, capacityand headcount planning, to profit andloss planning, financial budgeting andbalance sheet planning.

The utilisation of portaltechnology to facilitate theprocess of enpowermentThe development and utilisation of anEnterprise Portal allows users one-stopaccess to all types of information. Itcovers the range of information needsof different users to include:• Unstructured and structured content• Transaction processing• Collaborative data• Internal and external sources

Improving decision making in your organisation

23

The capability of portals varies.Cedric Read and the mySAP Financialsteam report in their new book thattasks which traditionally requirenavigating through multiple systemsare now accomplished with a few clicksof the mouse from the desktop. Readargues that CFOs need to drive portaldevelopment which includes selling thebenefits of portal usage and involvingend users in portal planning anddesign. Non-financial users willgenerally require different applicationsand reports. Tools for non-financialusers may be less powerful but moreintuitive and easier to use than for themanagement accountant.

The enterprise portal is marketed onthe basis that it has potential for cuttingacross functions and business units,allowing employees to manage theirown data and transactions, andproviding a ready made vehicle forsharing information and knowledge.Depending on the design of the portal,it also could allow for thestandardisation of business practicesamong employees, suppliers andbusiness partners. The Royal Mail iscurrently considering the decisionmaking and information needs ofdifferent types of user and may feel theneed for different types of portal fordifferent users.

Business-to-employee (B2E)connectivity, as some people havetermed it, involves using Internettechnology to develop a relationshipwith the employee by acting as acorporate home page. It can provide anentry point for finding and connectingother sites on the corporate Intranet.The B2E portal is a personalised, ever-changing mix of news, resources,applications and e-commerce options;it becomes a desktop destination for

everyone in an organisation and theprimary vehicle by which people dotheir work. Its content can be dividedinto four application categories:• Connecting employees: comprising

corporate financial information,competitive intelligence andcorporate communications,connected to online learning,employee self-service applicationsand pay-related information;

• Operational systems: including cross-functional management reporting,workforce planning, performancemeasurement and other operationalapplications;

• Workgroup collaboration: rangingfrom discussion forums andnewsgroups to documentmanagement, web conferencing andinstant messaging;

• External connectivity: linkingcustomer extranets, partner portalsand external intelligence feeds to theIntranet.

The value proposition of the portalencompasses qualitative benefits suchas enhanced productivity, improvedmanagement information, improvedconnectivity and employee satisfaction,and quantitative benefits focused onreduced transaction processing costs,elimination of redundant infrastructureand associated maintenance costs.

The advent of web services has nowalso meant that portals are increasinglycustomisable. The key factor formanagement accountants is helping toensure that the content is meaningfulotherwise portals will not be exploitedby users.

Strategic orientation offinance professionalsIn his book, SEM Systems, Fahysuggested that to be genuinelyeffective at dealing with strategicbusiness decisions which seniorexecutives face, finance professionalsneed to move away from simply dealingwith their traditional focus on internalcontrols/transaction process. This inturn requires the following renewedemphasis on:• Pro-actively suggesting options in

business decision making rather thanonly evaluating strategic investmentdecisions, understanding thebehaviour of costs with respect tochanging volumes and marketconditions, including which activities,products and customers are addingvalue;

• Evaluate the organisation andbusiness unit performance andreview its strategies on a continuousbasis helping communicate strategicobjectives to employees in a mannerwhich allows them to operationalisestrategy, using their analytical skills tounlock the value in customer andcost information in evaluatingproposals;

• Monitor the progress towardsstrategic goals through performancetracking measures;

• Fine tune and re-configure thebusiness model in the face ofcompetition and help build a cultureof value creation in the organisation;

• Evaluate new initiatives aimed atachieving profitable growth;

• Move to a system of allocation ofresources on the basis of valuecreation. This is not the same asasking how much more capitalinvestment is required to make thebusiness more profitable at themargin.

Improving decision making in your organisation A summary of the key components of SEM

24

Understanding the businessmodel and effectiveperformance measurementThe characteristics of a goodperformance measurement frameworkcan be framed regardless of theenterprise systems architecture beingdeployed or contemplated. Thesoftware providers supply products thatare aimed at supporting the keyfeatures of a good performancemeasurement system i.e. measures aredefined using several perspectives:financial and non-financial, predictiveand historical, external and internal.The key criteria for performancemeasurement is to inform managementthat there is a link right through fromthe corporate level to the managementand then operational level so thatdecision making and resulting actionsand control are in line with strategy. Thecommon difficulties that companiesface, identified in discussion withPricewaterHouseCoopers at one RoundTable, are firstly around an ambiguouscorporate or business strategy.Ambiguity at this level will mean thatthe senior executive management teamwill struggle to translate the businessstrategy into specific tangible strategicobjectives and clear measures thatreflect strategy and core processes thatunderlie it, and will help employeesachieve it.

Secondly, performance measures arenot aligned to strategy. It is notuncommon for managers to flood theirorganisations with many differentperformance measures withoutassessing whether they are actuallymeasuring performance againststrategic objectives. This is often causedby a lack of understanding of whichfactors (particularly intangibles) drivecorporate performance and value.Without this knowledge there cannoteasily be an understanding of howinformation, control and rewardsystems can facilitate change inpeoples’ behaviours so that they addvalue.

Two organisations deliveredpresentations to the Round Tabledemonstrating how a balancedscorecard type approach and strategymapping had been used to understandthe main intangible drivers ofperformance and interrelationships andto measure performance.

Shell’s implementation of a balancedscorecard approach began in 1996 andhas evolved into a robust frameworkthat now also forms the basis ofemployees’ appraisals. This has led to aproject being undertaken by CranfieldSchool of Management, which ishelping to bring the organisation’sperformance data together so thatrelationships between identified valuedrivers can be empirically tested andfuture analysis of the business modeland performance continues to have arobust foundation. The Scorecard hasbeen developed to fit Shell’s uniquecircumstances and culture and theperspectives found on the genericScorecard, initially developed by Kaplanand Norton, have been adapted.

The aim of Shell’s work is to:1 Supply a powerful analysis of the

levers of management;2 Build on Shell’s current strengths and

ensure increased knowledge anddata collection;

3 Understand where all the data is, theformat needed etc, so that it is quickand easy to collect and analyse infuture;

4 Validate the structure of theScorecard; and

5 Facilitate double loop learning whereexisting assumptions can bechallenged.

The Inland Revenue identified thebalanced scorecard as the best meansto create and communicate strategicalignment throughout theorganisation, and for being a goodframework for a decision support toolat board level. A process of strategymapping with executives and seniormanagement was used to understandthe business model and create aniterative process for change, which wasseen as the best way forward fordeveloping the organisation’s direction.The Inland Revenue pursued thisapproach to:• Ensure shared goals and objectives;• A strategy and its drivers brought to

life;• Focusing the organisation on

delivering value for customers andother stakeholders; and

• Less and more relevant informationto the board to enable strategicdecision making.

The result of this project has been abetter shared understanding by theboard and senior managers of how thebusiness works. Value trees have beencreated that systematically link theoperating elements of the business tovalue creation. This enables a betterdialogue with stakeholders such as theHM Treasury on where money is bestspent. �

Improving decision making in your organisation

25

11 Tracking how companies are developing SEM and evolvingtheir finance functions – a new benchmarking service

Different companies are at differentstages of implementing an SEMapproach. Indeed, some are takingdifferent paths depending on theirexisting strengths and weaknesses. Anumber of presentations have beengiven to the CIMA SEM Round Tablefrom companies including Shell, SouthAfrican Breweries, Roche, PowerGen,Rolls Royce, Lloyds TSB, Boots and theRoyal Mail.

For many organisations, SEM hasbeen a part of the process ofreconfiguring the finance function tofocus on supporting and improvingdecision making rather than onlyfocusing on historical and actualreporting. It has been part of anintegrated long term plan to improveprocesses and information flows,thereby ensuring that the right peoplehave the right information and quickly.It is also about the finance functionassisting in creating strategies andimproving management control. Betterinformed decisions at both operationaland strategic level is the nirvana. Therate of change in most companies is atan evolutionary rather thanrevolutionary pace.

To support companies’ developmentin this field, CIMA is consideringestablishing a benchmarking service forcompanies which will enable them tokeep up to speed with how otherorganisations are progressing in termsof implementing informationtechnology, developing their financefunctions and improving decisionmaking. Potential outputs wouldinclude:• Six monthly anonymous summaries

to be released publicly; and• More detailed feedback to each

company as to where they areagainst leading companies.

If you are interested in this serviceand wish to discuss your participation,please contact Stathis Gould at CIMAon 0208 849 2379 or [email protected]

This service is at an early stage ofdevelopment and we wish to engage anumber of companies so to make theservice of greater value to participantsand to understand all the areas andactivities that we need to benchmarkbefore we launch. �

Improving decision making in your organisation

26

Participants

The following organisations andindividuals have participated in theRound Table:UnileverPowergenBBCElan Corporation plcAllied Irish BankThe Royal MailRocheAllied DomecqShell and Cranfield School ofManagementLloyds TSBRolls RoyceBNFLInland RevenueDeloitte and Touche ConsultingPricewaterhouseCoopersBellis-Jones, Hill and Prodacapo

Partners for Change

John BarbourCorporate Value Improvement Ltd

Martin Bryant(former Director of CorporateDevelopment at Boots and ManagingDirector of Boots Retail International)

Steve Marshall,former chief executive of Railtrack andThorn EMI

Martin Fahy(Round Table Convenor)Senior lecturer inAccounting and Information Systems atNational University of Ireland.

For more information about SEM andthe Round Table look atwww.cimasem.com or contact [email protected]

Improving decision making in your organisation

References and further reading

Brignall, T. J. (1997), ‘A ContingentRationale for Cost System Design inServices’. Management AccountingResearch, Vol.8, No. 3, 325-46.

Burns, J., Ezzamel M. andScapens R. (2003),The Challenge of ManagementAccounting Change, CIMA

CIMA, data warehousing technicalbriefing, 2003

CIMA and Cranfield University,Understanding corporate value:Managing and reporting intellectualcapital, 2003

Cooper, R. (1999) ‘Reasons forinnovation’, Australian CPA, Oct 1999,Vol. 69, Iss.9, p.75.

Davenport, T. (1998), ‘Putting theenterprise into the enterprise system’,Harvard Business Review, Vol. 76, No. 4,Jul/Aug., pp.121-31.

Economist (Feb 2002), How AboutNow? A survey of the real-timeeconomy

Low, J. and Siesfeld, T., Ernst & Young(1998), ‘Measures that matter’,Strategy and Leadership,Mar./Apr., p. 24.

Evans, H., Ashworth, G., Gooch, J. andDavies, R. (1996), ‘Who needsperformance management?’,Management Accounting (UK), Dec.1996, p.20-25.

Fahy, M. (2001), Strategic EnterpriseManagement Systems, CIMA

Granlund, M. and Malmi, T. (2002),Moderate impact of ERPS onmanagement accounting: a lag orpermanent outcome? ManagementAccounting Research, 13, 299-321.

Granlund, M. and Mouritsen, J. (2003),Introduction: Problematizing therelationship between managementcontrol and IT, European AccountingReview, 12:1, 77-83

Kaplan, R. S. and Cooper, R. (1998),Cost and Effect: Using Integrated CostSystems to Drive Profitability andPerformance,Harvard Business SchoolPress.

Kaplan, R. S. and Norton, D. P. (1996),The Balanced Scorecard: TranslatingStrategy into Action,Harvard Business School Press.

Kaplan, R. S. and Norton, D. P. (2001),The Strategy-focused organization :how balanced scorecard companiesthrive in the new business environment,Harvard Business School Press

Myrtveit, M. and Bean, M. (2000),‘Business modelling and simulation’,Wirtschafts Informatik, special print,Vol. 2, No. 42, Apr.

Rappaport, A. (1997), CreatingShareholder Value: A Guide forManagers and Investors, New York:Free Press.

Read, C., Scheuermann H. D. and themySAP Financials Team (2003), The CFOas business integrator, Wiley

Scapens, R., Ezzamel, M.,Baldvinsdottir, G. (2003),The Future Direction of UKManagement Accounting Practice,CIMA

Scapens, R. W. and Jazayeri, M. (2003),ERP systems and managementaccounting change: opportunities orimpacts? European Accounting Review12:1, 201-233

Schneider, P. (1999), ‘Wanted: Erpeopleskills’, CIO Magazine, 1 Mar.

The Bramald Consultancy (November1996), Report on ManagementAccountants’ use of IT.

Wefers, M. (2000), ‘Strategic enterprisemanagement with the balancedscorecard’, Wirtschafts Informatik,special print, Vol. 2, No. 42, Apr.

SAP Strategic Enterprise ManagementBrochures and White Paperswww.sap.com/solutions/financials/sem/brochures

Improving decision making in your organisation: The CIMA Strategic Enterprise Management (SEM) initiative

The Chartered Institute of Management Accountants (CIMA) represents financial managers and accountants working in industry, commerce, not-for-profitand public-sector organisations. Its key activities relate to business strategy, information strategy and financial strategy. CIMA is the voice of more than 77,000students and 59,000 members in 154 countries. its focus is to qualify students, to support both members and employers and to protect the public interest.

The Chartered Institute of Management Accountants, 26 Chapter Street, London SW1P 4NP +44 (0) 20 7663 5441 www.cimaglobal.com