cia. hering - 4q16 results

TRANSCRIPT

4Q16 ResultsConference Call

February 24th, 2017 – 11:00 am (BrT)09:00 am (NY)/ 02:00 pm (London)

4Q16 Results

DISCLAIMER

This presentation contains forward-looking statements regarding the

prospects of the business, estimates for operating and financial

results, and those regarding Cia. Hering's growth prospects. These are

merely projections and, as such, are based exclusively on the

expectations of Cia. Hering management concerning the future of the

business and its continued access to capital to fund the Company’s

business Plan. Such forward-looking statements depend, substantially,

on changes in market conditions, government regulations,

competitive pressures, the performance of the Brazilian economy and

the industry, among other factors and risks disclosed in Cia. Hering’s

filed disclosure documents and are, therefore, subject to change

without prior notice.

• Financial Performance

• Outlook

• Q&A

2

FINANCIAL PERFORMANCE

GROSS REVENUES AND BREAKDOWN BY BRAND

R$ MILLION

GROSS REVENUES BREAKDOWN PER CHANNEL

DOMESTIC MARKET EX-OTHER REVENUES

2016, R$ MILLION – CHANGE 2016 X 2015

Gross Revenue of R$ 1.7 billion in 2016, mainly impacted by franchise and multibrand performance,

and negative effects of macroeconomic scenario.

3

4Q16 4Q15 Change 2016 2015 Change

504.9 595.4 -15.2% 1,706.3 1,857.3 -8.1%

384.9 475.4 -19.0% 1,270.7 1,415.0 -10.2%

64.4 58.4 10.3% 218.2 204.8 6.6%

31.7 35.9 -11.5% 118.7 130.2 -8.8%

15.6 17.4 -10.4% 64.6 82.4 -21.6%

10.2 12.5 -18.0% 42.1 42.8 -1.7%InternationalMarket

HERING STORE NETWORK

GROSS SALES

SELL-OUT, R$ MILLION

Gross revenues of R$ 1,436.8 million (-8.9%), impacted by SSS drop

due to macroeconomic scenario, consumer’s flow reduction and

lower traffic.

¹ Change in store count over the last 12 months.

STORE REFURBISHMENT PLAN

• 100 stores refurbished in 18 states of the country

• R$ 8.4 million as subsidies and financing part of the

amount invested

Hering Store Pq. Dom Pedro Sh. Campinas – SP State

4

FINANCIAL PERFORMANCE

EBITDA of R$ 207.6 million (-21.0%) due to operational deleveraging,

reversal of lawsuit gains related to the Compulsory Loan to

Eletrobrás¹ and expenses related to Protege Goiás Fund.

Stable margin in the year (39.5%) and +200 bp in 4Q16,

resulting from better inventory management, which enabled

lower leftovers of past collections, with a consequent volume

reduction of markdown.

GROSS PROFIT

R$ MILLION

EBITDA

R$ MILLION

5¹ Further details in the Explanatory Notes number 12.

FINANCIAL PERFORMANCE

NET INCOME

R$ MILLION

CAPEX

R$ MILLION

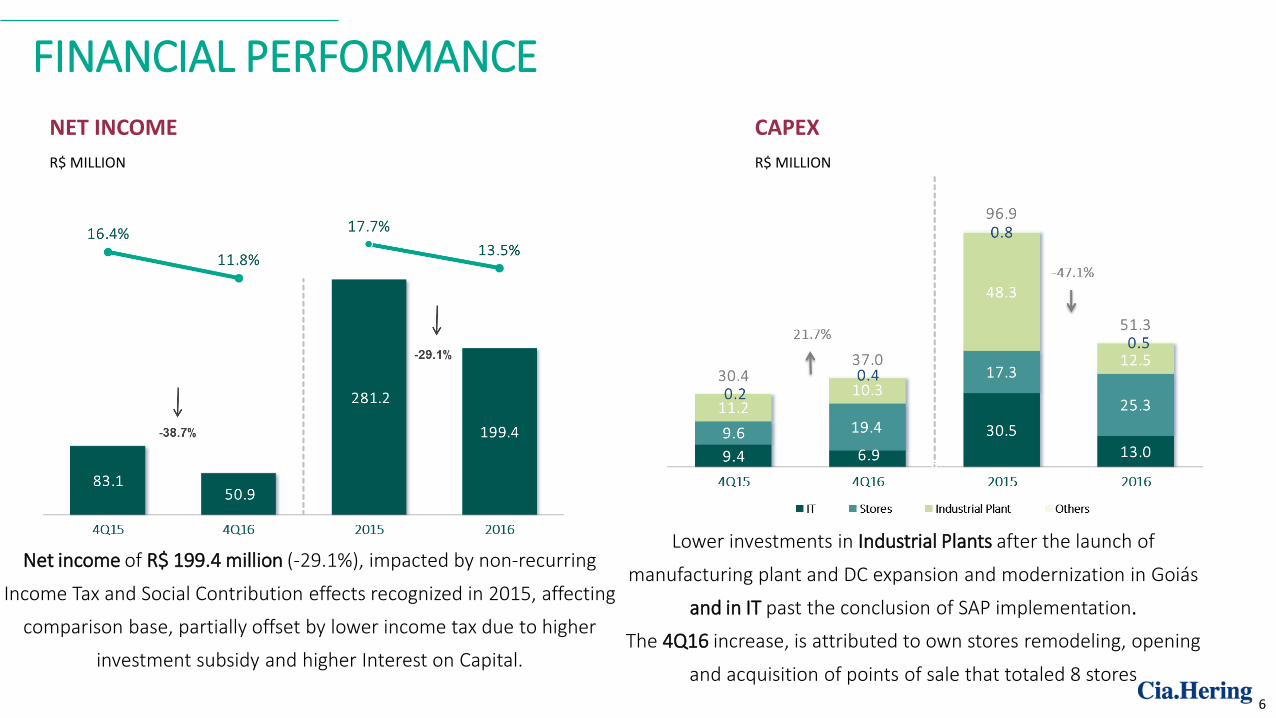

Net income of R$ 199.4 million (-29.1%), impacted by non-recurring

Income Tax and Social Contribution effects recognized in 2015, affecting

comparison base, partially offset by lower income tax due to higher

investment subsidy and higher Interest on Capital.

Lower investments in Industrial Plants after the launch of

manufacturing plant and DC expansion and modernization in Goiás

and in IT past the conclusion of SAP implementation.

The 4Q16 increase, is attributed to own stores remodeling, opening

and acquisition of points of sale that totaled 8 stores

6

FINANCIAL PERFORMANCE

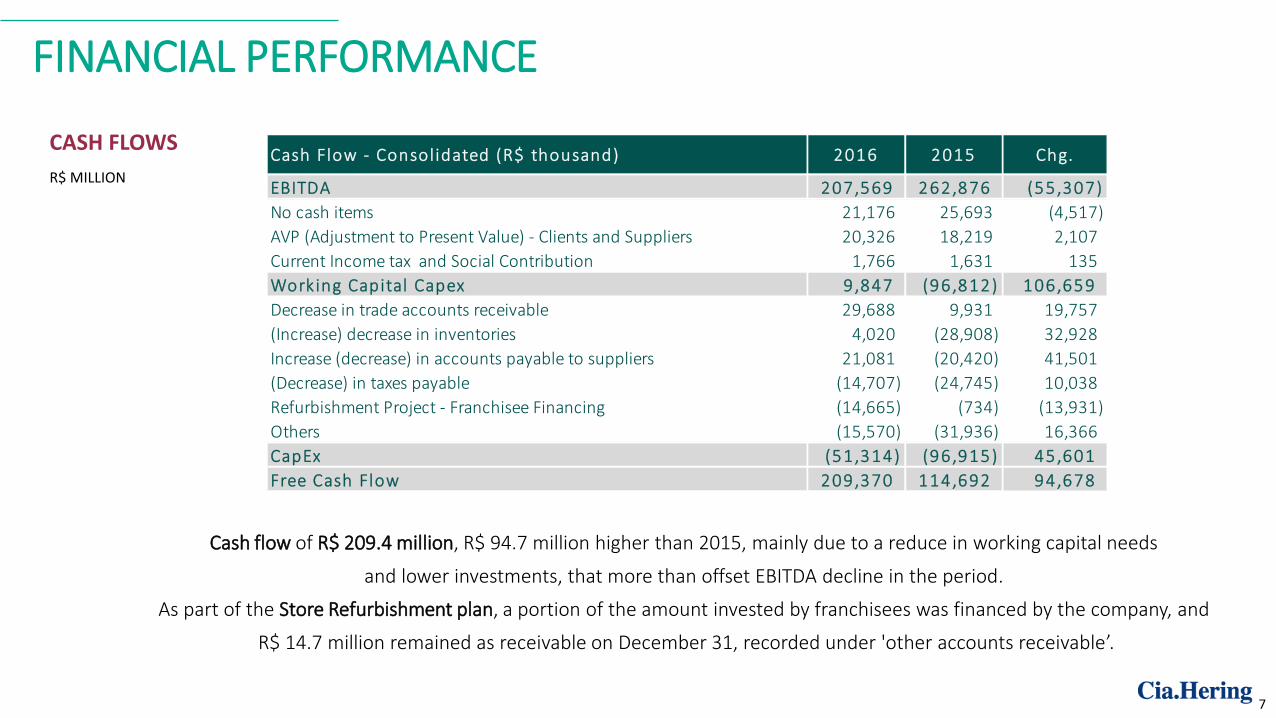

Cash flow of R$ 209.4 million, R$ 94.7 million higher than 2015, mainly due to a reduce in working capital needs

and lower investments, that more than offset EBITDA decline in the period.

As part of the Store Refurbishment plan, a portion of the amount invested by franchisees was financed by the company, and

R$ 14.7 million remained as receivable on December 31, recorded under 'other accounts receivable’.

CASH FLOWS

R$ MILLION

7

Cash Flow - Consolidated (R$ thousand) 2016 2015 Chg.

EBITDA 207,569 262,876 (55,307)

No cash items 21,176 25,693 (4,517)

AVP (Adjustment to Present Value) - Clients and Suppliers 20,326 18,219 2,107

Current Income tax and Social Contribution 1,766 1,631 135

Working Capital Capex 9,847 (96 ,812) 106,659

Decrease in trade accounts receivable 29,688 9,931 19,757

(Increase) decrease in inventories 4,020 (28,908) 32,928

Increase (decrease) in accounts payable to suppliers 21,081 (20,420) 41,501

(Decrease) in taxes payable (14,707) (24,745) 10,038

Refurbishment Project - Franchisee Financing (14,665) (734) (13,931)

Others (15,570) (31,936) 16,366

CapEx (51,314) (96,915) 45 ,601

Free Cash Flow 209,370 114,692 94,678

FINANCIAL PERFORMANCE

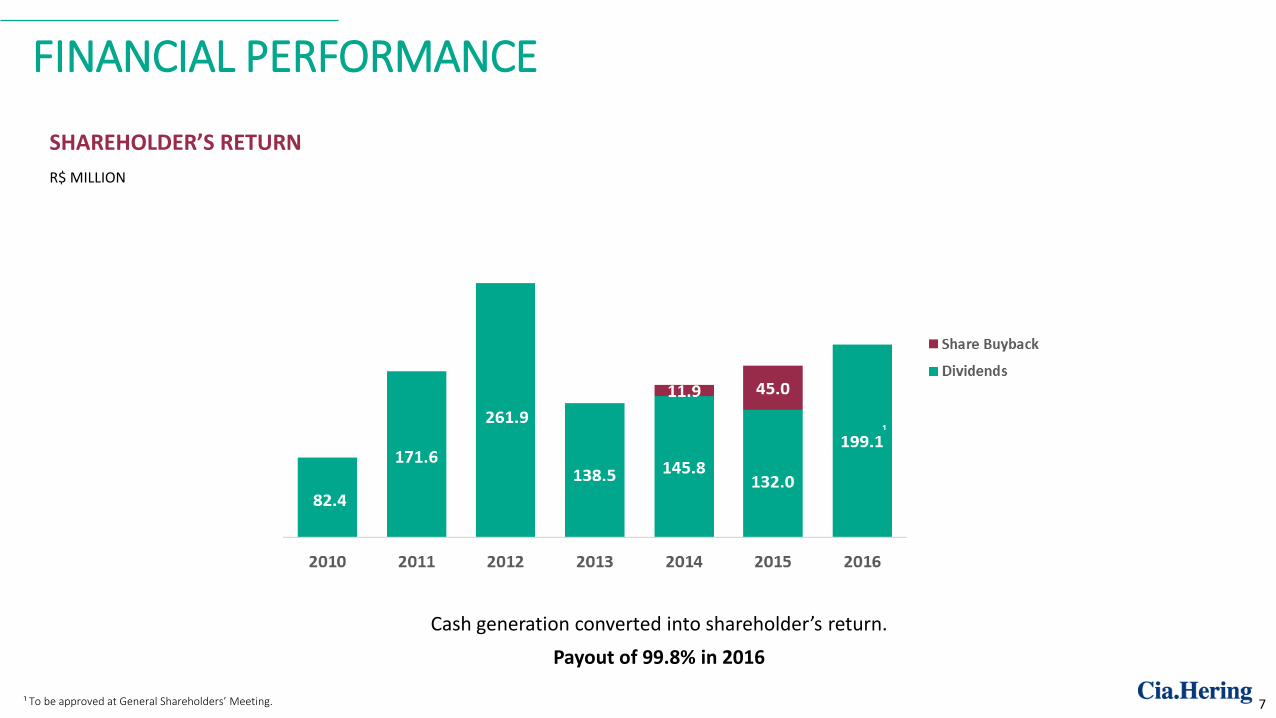

Cash generation converted into shareholder’s return.

Payout of 99.8% in 2016

SHAREHOLDER’S RETURN

R$ MILLION

7¹ To be approved at General Shareholders’ Meeting.

OUTLOOK

9

• Expectations on economy’s gradual recovery along the year, however not yet materialized in the

beginning of the year;

• Strategy based on Product and Store (P&S) continues:

• Improvements in Product rises and are translated into growth in orders received in the latest showrooms;

• Stores: refurbishments progresses, but at slower pace, and we will keep improving buying experience and VM;

• E-commerce: investments in traffic increase and conversion, in the channel that should present the

highest growth over the next years;

• Multibrand: implementation of client segmentation as priority.

INVESTOR RELATIONS TEAM

Fabio Hering – CEOFrederico Oldani – CFO and IROBruno Salem Brasil – IR ManagerCaroline Luccarini – IR Analyst

www.ciahering.com.br/ir+55 (11) 3371 – 4867/[email protected]