chutes and ladders in dairy - datcp home homepage and ladders in dairy ... the global dairy market...

TRANSCRIPT

1

Chutes and Ladders in Dairy

A few more ladders than chutes

October 2016

2

Food & Agribusiness Research and Advisory

Rabobank’s unique global team of 94 analysts – supporting knowledge based banking

3

Upfront summaryThe global dairy market faces more upside in months to come, but there are some chutes.

Six out of seven major dairy exporting regions currently have milk supply contracting.

Global exportable surplus is now tighter than any time since 2009.

Intl dairy prices have responded accordingly with 35% increases in prices.

Production will be slow to respond to higher prices.

Intl prices will have upward pressure for months to come.

But, US butter and cheese prices have some headwinds due to inventories.

Global inventories are also very weighty on prices, but less of a concern.

The strong USD will affect affordability in already struggling oil dependent markets.

4

Current market status

Downward pressure on prices – ‘chutes’

Section 1

Section 2

Section 4 Upward pressure on prices – ‘ladders’

Section 5 Price forecasts and alternative scenarios

5

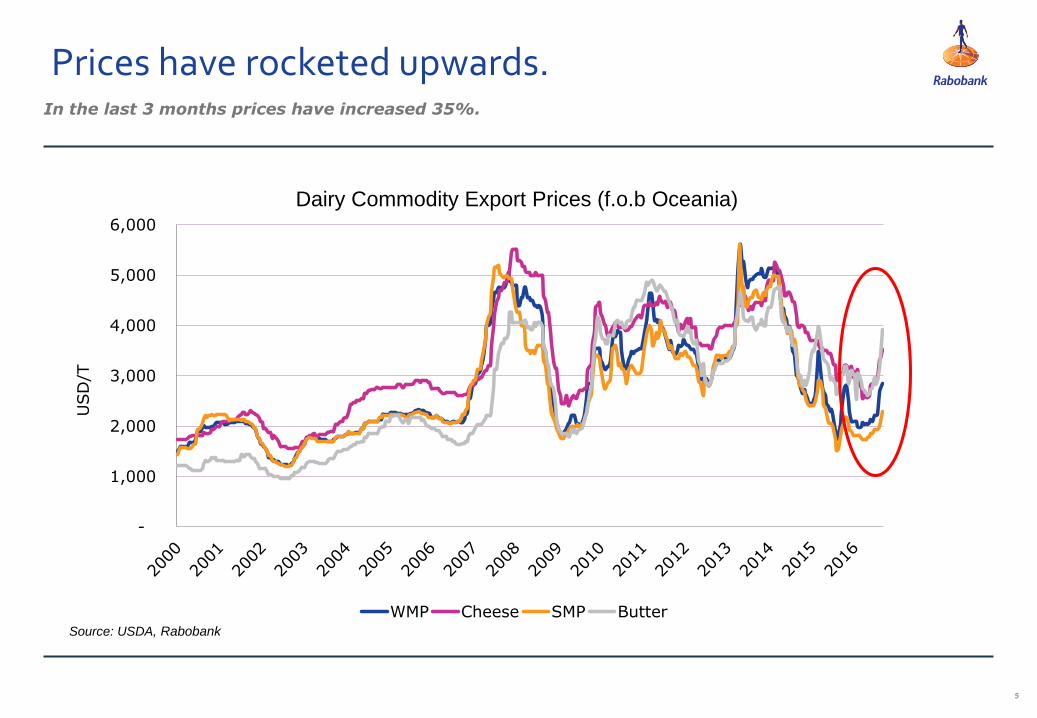

In the last 3 months prices have increased 35%.

Prices have rocketed upwards.

-

1,000

2,000

3,000

4,000

5,000

6,000

USD

/T

WMP Cheese SMP Butter

Commodity Export Prices Dairy Commodity Export Prices (f.o.b Oceania)

Source: USDA, Rabobank

6

Tough margins, bad weather, and fewer cows are biting into NZ supply.

New Zealand milk supply is now falling.

Source: DCANZ, Rabobank

New Zealand annual milk production

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

2011 2012 2013 2014 2015 2016

7

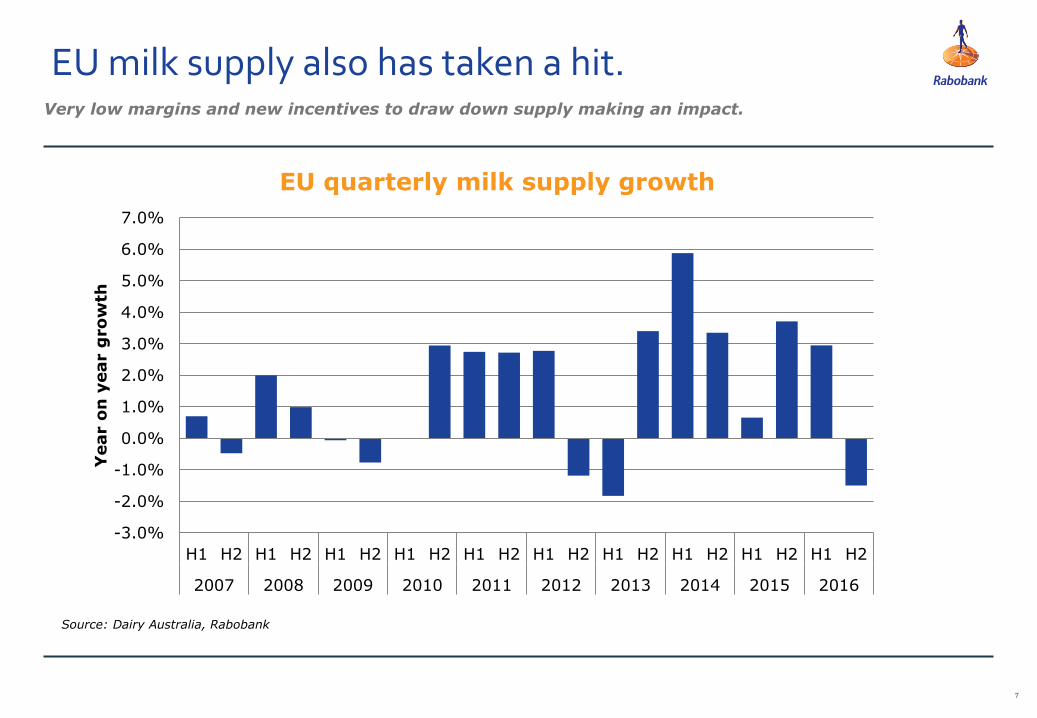

Very low margins and new incentives to draw down supply making an impact.

EU milk supply also has taken a hit.

Source: Dairy Australia, Rabobank

EU quarterly milk supply growth

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Year o

n y

ear g

ro

wth

8

High prices for butter and cheese and low feed costs have driven growth.

US milk supply is still growing.

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Jun

Aug

Oct

Dec

Feb

Apr

Jun

Aug

Oct

Dec

Feb

Apr

Jun

Aug

Oct

Dec

Feb

Apr

Jun

Aug

Oct

Dec

Feb

Apr

Jun

Aug

Oct

Dec

Feb

Apr

Jun

Aug

Oct

Dec

Feb

Apr

2011 2012 2013 2014 2015 2016

Year o

n y

ear g

ro

wth

Source: Rabobank, USDA Note: Mar to Jun 2013 breakdown is an est (due to govt shutdown)

US monthly milk supply growth

9

At current trajectory, Wisconsin will become the US’ largest producer by Oct 2019.

Growth is slowly moving back east.

2000

2200

2400

2600

2800

3000

3200

3400

3600

3800

Sep-1

6

Dec-1

6

Mar-

17

Jun-1

7

Sep-1

7

Dec-1

7

Mar-

18

Jun-1

8

Sep-1

8

Dec-1

8

Mar-

19

Jun-1

9

Sep-1

9

Dec-1

9

Mar-

20

Jun-2

0

Million lbs.

Cali vs. Wisconsin

Wisconsin California

Source: Rabobank, USDA

US milk supply growth 3 months to Aug 2016.

Source: Rabobank, USDA

10

The bottom line, global supply is shrinking.

Milk supply from the big exporters is falling.

Milk Production Growth of the ‘Big 7’

Source: RabobankNote: includes EU 27, USA, NZ, Australia, Brazil, Argentina, and Uruguay

-4%

-2%

0%

2%

4%

6%

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

Nov

Jan

Mar

May

Jul

2011 2012 2013 2014 2015 2016

Yoy

gro

wth

Big 6 milk supply growth

11

Most farmgate prices have moved up.Farmer margins are starting to look a little better.

Source: Rabobank

0

5

10

15

20

25

30

35

USD

/CW

T

Farmgate milk prices (USD equivalent) - select regions

China Netherlands (FCampina)NZ (Fonterra) US (All Milk Price)Ireland

12

We have passed the import hump.Global import demand is looking healthy again.

52

53

54

55

56

57

58

59

Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May

2014 2015 2016

Rollin

g 1

2 m

onth

(M

il M

T L

ME)

Exports from the Big 6

Source: Rabobank, GTIS

13

Global import growth is diverse.A diverse list of markets have shown solid import growth.

Global import growth – 3 months to July

Source: Rabobank, GTIS

14

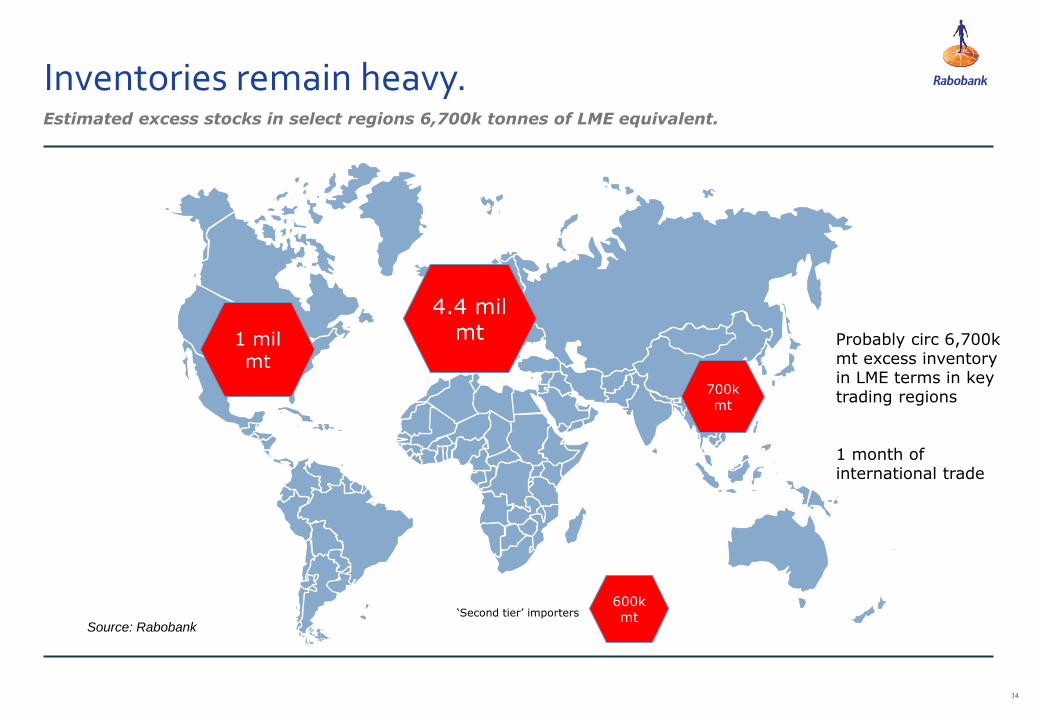

Inventories remain heavy.

700kmt

4.4 milmt1 mil

mt

600k mt

Estimated excess stocks in select regions 6,700k tonnes of LME equivalent.

‘Second tier’ importers

Probably circ 6,700k mt excess inventory in LME terms in key trading regions

1 month of international trade

Source: Rabobank

15

Stocks for cheese and butter are weighing on domestic prices.

US has realigned with international prices.

2,000

3,000

4,000

5,000

6,000

7,000

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

Jan-1

5

Apr-

15

Jul-

15

Oct-

15

Jan-1

6

Apr-

16

Jul-

16

US

D/

MT

Butter Markets

Oceania EU US CME

2000

3000

4000

5000

6000

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

Jan-1

5

Apr-

15

Jul-

15

Oct-

15

Jan-1

6

Apr-

16

Jul-

16

US

D/

MT

Cheese Markets

Oceania US CME

Source: Rabobank, USDA

16

Commercial disappearance was up 2.6% through 1H 2016.

US retail demand continues to grow.

-5%

0%

5%

10%

Apr

Jul

Sep

Dec

Mar

Jun

Aug

Nov

Feb

May

Aug

Oct

Jan

Apr

Jul

2013 2014 2015 2016

Natural Cheese Sales

-20%

-10%

0%

10%

20%

30%

Apr

Jul

Sep

Dec

Mar

Jun

Aug

Nov

Feb

May

Aug

Oct

Jan

Apr

Jul

2013 2014 2015 2016

Butter sales

-10%

-5%

0%

5%

10%

Apr

Jul

Sep

Dec

Mar

Jun

Aug

Nov

Feb

May

Aug

Oct

Jan

Apr

Jul

2013 2014 2015 2016

Yogurt Sales

-6%

-4%

-2%

0%

Apr

Jul

Sep

Dec

Mar

Jun

Aug

Nov

Feb

May

Aug

Oct

Jan

Apr

Jul

2013 2014 2015 2016

Milk Sales

Source: IRI

Yoy

change in v

ol

17

US exports are picking back up, despite USD.

70

75

80

85

90

95

100

105

600

700

800

900

1,000

1,100Ja

n-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

Jan-1

5

Apr-

15

Jul-

15

Oct-

15

Jan-1

6

Apr-

16

Jul-

16

USD

Index

K M

T L

ME

US exports vs. USD

US exports USD

Source: Rabobank, GTIS, OANDA

18

Summary of current market status.

6/7 export markets’ supply contracting.

Developed market demand growing.

China back in the market.

Buyers are shrugging the strong USD.

Significant inventory overhang remains.

US prices have realigned with the world.

1

2

3

4

5

6

19

Section 1

Section 2

Section 4 Upward pressure on prices – ‘ladders’

Section 5 Price forecasts and alternative scenarios

Downward price pressure – ‘chutes’

Current market status

20

Prices to remain low, keeping US dairy margins manageable.

Low feed prices helping boost milk supply.

Corn

250

300

350

400

450

500

550

600

650

700

750

USc /

bushel

CBOT Corn Previous forecast Rabobank forecast

Source: Rabobank

21

Low feed prices and an uptick in milk prices should boost US milk supply.

US production will continue to grow.

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

Dec

Mar

Jun

Sep

2011 2012 2013 2014 2015 2016 2017

US Milk Production Growth

Source: Rabobank, USDA Note: Mar to Jun 2013 breakdown is an est (due to govt shutdown)

Forecast

22

Affordability will be a major factor for many developing markets moving forward.

Strong USD to keep pressure on prices.

60

65

70

75

80

85

90

95

100

105

-

1,000

2,000

3,000

4,000

5,000

6,000

Nov-0

7

Jul-

08

Mar-

09

Nov-0

9

Jul-

10

Mar-

11

Nov-1

1

Jul-

12

Mar-

13

Nov-1

3

Jul-

14

Mar-

15

Nov-1

5

Jul-

16

USD

index

USD

/MT

USD vs. WMP

WMP USD

Source: Rabobank & OANDA

23

Continual GPD growth downgrades and rising debt a big concern for economists.

The global economy is still a little ‘wobbly’.

200

225

250

275

'95 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15

Debt/GDP

BRICS and "developed world" private non-financialand public sector debt as a % of "world" GDP*

*Data collated from 13 economies accounting for 68% of world nominal GDP

Global Economic Growth Forecasts (WEO)

Worrying Debt Levels

3

3

3

4

4

4

2014 2015 2016 2017 2018 2019

Yoy

gro

wth

%

April 2015 WEO April 2016 WEO

Source: Rabobank & WEO

24

Buyers know the market is still long milk.Estimated excess stocks in select regions 6,700k tonnes of LME equivalent.

High stock levels. Makes higher prices a tough argument.

Source: Rabobank

25

High inventories in the US will mean discounting and promotions to clear product.

US cheese and butter stocks a little too high.

0%

2%

4%

6%

8%

10%

12%

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Sto

cks t

o u

se r

atio

Cheese

0%

2%

4%

6%

8%

10%

12%

14%

16%

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Butter

2016 est.

2016 est.

Source: Rabobank & USDA

26

Current market status

Downward pressure on prices – ‘chutes’

Section 1

Section 2

Section 4 Upward pressure on prices – ‘ladders’

Section 5 Price forecasts and alternative scenarios

Upward pressure on prices – ‘ladders’

27

The biggest part of the recovery is the rapid decline in EU supply.

EU milk production will continue to contract.

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EU Milk Production Growth

Yo

ych

an

ge

Forecast

Source: EU commission, Rabobank

28

Production growth to continue slowing.

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

YO

Y p

ro

du

cti

on

gro

wth

Milk production growth of Big 7 exporters combined

Actual Recorded Growth

Rabo Forecast (by half)

Source: RabobankNote: includes EU 27, USA, NZ, Australia, Brazil, Argentina, and Uruguay

We have another 6 months of supply contraction ahead of us.

29

But US supply not keeping up with demand.

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

Apr-

13

Jul-

13

Oct-

13

Jan-1

4

Apr-

14

Jul-

14

Oct-

14

Jan-1

5

Apr-

15

Jul-

15

Oct-

15

Jan-1

6

Apr-

16

Jul-

16

Year

on y

ear

change

US Milk Supply vs. Demand

Supply Demand

High Prices hurt demand

Demand now outpacing supply for 18 months

Source: Rabobank & USDA

30

Market will remain under pressure.

(3)

(2)

(2)

(1)

(1)

-

1

1

2

2

3

3

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2012 2013 2014 2015 2016 2017

Million M

T L

ME

Exportable surplus vs. Import requirements

Others Asia MEA China Surplus

Forecast

Source: Rabobank

31

Effective dates, Oct 2016 – Mar 2017.

150 m EUR to be spent paying premiums to farms who reduce

supply.

Could theoretically remove 1 billion liters from the market.

Some markets will match the buy back prices.

It is unclear how effective the proposed measures will be.

Government Intervention.

EU Supply Reduction US Cheese Buy Backs

California FMMO Litigation

Will California be brought under the FMMO?

Proposal to be announced late 2016/ early 2017.

Then farmers provide feedback.

The objective is to raise farmgate milk prices in Cali.

US allocated $20 million to purchase cheese.

The purpose is to support the milk prices for farmers.

The $20 can only buy 5k MT of product – less than 1%

of US production.

Unlikely to be effective – but signals a renewed

willingness of the US government to intervene in price

support.

32

Current market status

Downward pressure on prices – ‘chutes’

Section 1

Section 2

Section 4 Upward pressure on prices – ‘ladders’

Section 5 Price forecasts and alternative scenariosPrice forecasts and conclusion

33

Rabobank dairy price forecasts: FOB Oceania

WMP prices fob Oceania: Historic and Rabo forecasts

-

1,000

2,000

3,000

4,000

5,000

6,000

Jan 2

006

Jul 2006

Jan 2

007

Jul 2007

Jan 2

008

Jul 2008

Jan 2

009

Jul 2009

Jan 2

010

Jul 2010

Jan 2

011

Jul 2011

Jan 2

012

Jul 2012

Jan 2

013

Jul 2013

Jan 2

014

Jul 2014

Jan 2

015

Jul 2015

Jan 2

016

Jul 2016

Jan 2

017

Jul 2017

USD

/MT

Source: Rabobank & USDA

34

Rabobank dairy price forecasts: US Wholesale

Class III: Rabo Forecast V CME Curve Class IV: Rabo Forecast V CME Curve

15

16

17

18

Q3e Q4f Q1f Q2f Q3f

2017

Class III Class III - Fut

12

13

14

15

16

17

Q2 Q3e Q4f Q1f Q2f

2016 2017

Class IV Class IV - Fut

USD

/CW

T

USD

/CW

T

Source: Rabobank, USDA, CME

35

An improvement in margins, but still uninspiring.

Producer margins.

IOFC BenchmarkCorn and Soy future prices as at Sep 30 2016

USD

/CW

T

-

2

4

6

8

10

12

14

16

18Ja

n-0

7

Jun-0

7

Nov-0

7

Apr-

08

Sep-0

8

Feb-0

9

Jul-

09

Dec-0

9

May-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Jun-1

2

Nov-1

2

Apr-

13

Sep-1

3

Feb-1

4

Jul-

14

Dec-1

4

May-1

5

Oct-

15

Mar-

16

Aug-1

6

Jan-1

7

Jun-1

7

Historic IOFC indicative breakeven Series1

Source: Rabobank & USDA

36

While generally improving, the dairy market still has some ups and downs in it.

Summary.

LaddersChutes

Massive supply adjustment underway.

Global demand expected to continue to chug along.

US still isn’t producing enough milk to meet needs.

Significant inventory overhang remains.

Global economy is still wobbly.

USD remains strong.

Government intervention good or bad, wont move the dial too much.

37

So what does it mean for dairy in the US

While profitable, milk prices will remain uninspiring for producers for the next 6-12 months.

The move back east. Producers and processors.

More pressure on government to help farmers.

More consolidation of US dairy farmers looking for margins.

Constant volatility in the market. More hedging.

1

2

3

4

5

38

Contact details

Tom Bailey

Senior Dairy Analyst

Food & Agribusiness Research and Advisory

“The financial link in the global

food chain”™