christopher s. sears ice miller llp one american square indianapolis, indiana 46282 (317) 236-5891...

TRANSCRIPT

Christopher S. SearsIce Miller LLP

One American SquareIndianapolis, Indiana 46282

(317) 236-5891

Alphabet Soupin Employee Health Expense AccountsAlphabet Soupin Employee Health Expense Accounts The Evolution of Employee Health Expense

Accounts:o Flexible Spending Arrangement (“FSA”), 1979

o Health Reimbursement Account (“HRA”), 2002

o Health Savings Account (“HSA”), 2003

Alphabet Soup – FSA OverviewAlphabet Soup – FSA Overview FSA: Flexible Spending Arrangement

o Usually employee contributions through 125 plan (can be unfunded)

o Subject to use-it-or-lose-rule

o Limited to qualified medical expenses

o Employer must substantiate expenses before reimbursement

Alphabet Soup – HRA OverviewAlphabet Soup – HRA Overview HRA – Health Reimbursement Account

o Must only be employer contributions (can be unfunded)

o Accounts may roll over into next taxable year

o Limited to qualified medical expenses (but can include insurance premiums)

o Employer must substantiate expenses before reimbursement

Alphabet Soup – HSA OverviewAlphabet Soup – HSA Overview The “Medicare Prescription Drug Act” was

signed into law on December 8, 2003 This law added new Section 223 to the Internal

Revenue Code to create and govern Health Savings Accounts (“HSAs”)

Amended Internal Revenue Code Section 106 to allow for exclusion of amounts contributed to HSAs by an employer from employee income

What is an HSA?What is an HSA? An IRA-like account used to pay for qualified

medical expenses Has unique tax features—contributions are tax-

deductible going in, and tax free upon withdrawal if used for qualified medical expenses.

Must be coupled with a high deductible health plan (“HDHP”)

Must be established with a qualified HSA trustee (such as an insurance company, bank, or other person or entity approved by the IRS to be a trustee or custodian)

Why did Congressand the President Adopt HSAs?Why did Congressand the President Adopt HSAs? The government hopes that HSAs will:

o Increase personal control over health care dollars

o Increase private ownership of health insurance policies. (This will shift the currently dominant employer-offered insurance model so it will resemble how we purchase car insurance.)

o Decrease the number of uninsured Americans

It’s part of the “Ownership Society” concept, which states that people will be more careful about their health care dollars if they “own” the money and could profit from prudent decisions.

How Can HSAs Foster an “Ownership Society?”How Can HSAs Foster an “Ownership Society?” PERSONAL RESPONSIBILITY: HSA holders

will take time to become more savvy consumers. FREEDOM TO CHOOSE: Structure will allow

consumers to choose one’s own doctor and health insurance policy.

COMPETITION BETWEEN PROVIDERS: Individual ownership will make markets more competitive. Doctors and insurance companies must work harder to earn business.

Are HSAs a “Silver Bullet” that will Cure the Broken Health Care System? Are HSAs a “Silver Bullet” that will Cure the Broken Health Care System? No, the government sees HSAs as an alternative option, not a

replacement to other health care options such as conventional employer-sponsored insurance programs or Medicare/Medicaid.

Potential negative impacts during a transition to HSAs: o Employers could reap the cost savings from offering only

HDHPs, and not pass any of the savings on to employees. o This interim period could leave sick, lower-paid employees

vulnerable if they do not have the means to pay the high deductible

o The oldest and sickest consumers (those who are responsible for most health care costs) can not effectively shop for health care.

o Availability of consumer data to compare providers and services is currently very poor

Who is Eligible to Establish an HSA?Who is Eligible to Establish an HSA? Eligibility status is determined on a month-by-

month basis Any individual who as of the first day of the

month:o Is covered under a high-deductible health plan (HDHP)o Is not covered under any other health plan (whether as an

individual, spouse, or dependent) that is not an HDHP and that provides for any benefit covered by the HDHP

o Is not entitled (eligible and enrolled) to benefits under Medicare

o May not be claimed as a dependent Do not need to be an employee – can set up as an

individual

What is a High-deductible Health Plan?What is a High-deductible Health Plan? Deductible limits (indexed to increase with inflation)

o At least $1,050 for single coverage (for 2006)o At least $2,100 for family coverage (for 2006)

Deductible limits do not apply for preventative care (see IRS Notice 2004-23)o Periodic health evaluationso Routine prenatal and well-child careo Child & adult immunizationso Tobacco cessation programso Obesity weight-loss programso Screening services o Treatment that is ancillary to preventative careo Preventative care drugs (for someone with risk factors, but

asymptomatic)

What is a High-deductible Health Plan?What is a High-deductible Health Plan? Out-of-pocket expense limits (includes

deductibles & co-pays, but not premiums)o No more than $5,250 for single coverage (for 2006)

o No more than $10,500 for family coverage (for 2006)

Both can be higher for out-of-network services Can be a self-insured employer plan

What Non-HDHP Coverages are Allowed?What Non-HDHP Coverages are Allowed? Coverage for accidents, disability, dental care,

vision care, or long term careo HRA or FSA coverage would be impermissible non-HDHP

coverage if it can be used on a first-dollar basis to cover medical expenses generally

o Guidance indicates that separate drug plans that are not subject to the high deductible are not allowed without losing HDHP status.

Permitted insuranceo Workers’ compensation, tort liabilities, liabilities relating to

ownership or use of property, insurance for specified diseases, per diem hospitalization insurance

How are HSAs Funded?How are HSAs Funded? Contributions by an

eligible individual Contributions by an

employer of an eligible individual

Rollover contributions from an Archer MSA or another HSA (one per year; must roll w/in 60 days; not subject to annual contribution limits)

Contributions must be in cash

Contributions can only be made for those months that a person is an eligible individual

Contributions are fully vested and portable

Can be through a cafeteria plan

What are Contribution Limits for HSAs?What are Contribution Limits for HSAs? Maximum monthly amount is 1/12 of the annual

contribution limit for HSAs Annual limits (no limits for rollovers)

o For single coverage, lesser of the HDHP’s deductible (min. of $1,050) or $2,700 (for 2006)

o For family coverage, lesser of HDHP’s deductible (min. of $2,100) or $5,450 (for 2006)

o Additional catch-up contributions (up to $500 annually) for eligible individual age 55 to 65 ($700 in 2006)

What are Contribution Limits for HSAs?What are Contribution Limits for HSAs? Special rules for married people

o If either spouse has family coverage, both are treated as having it

o If each has family coverage, then contribution limit is based on lower deductible of the two and limit is split between the spouses, unless they agree otherwise

o Both spouses can make the catch-up contributions

Excess contributions are taxable plus 6% penalty tax if not distributed by tax deadlineo If returned, then only earnings on excess are taxed

(with no penalty tax)

What are the Tax Effects for Contributions?What are the Tax Effects for Contributions? Contributions for a taxable year may be made during the

year up to tax filing deadline and appreciate tax-free while in the HSAo Pre-funding issues

o Wait-and-see approach Contributions are deductible by the eligible individual in

determining gross income (above-the-line deduction) Employer contributions are deductible by employer;

excludable from employee’s income; not subject to withholding for FICA, FUTA, and RRA; and subject to a 35% excise tax if not made in comparable amounts to comparable employees

What Rules Apply to Distributions?What Rules Apply to Distributions? Distributions may be taken any time (even if not

currently an “eligible individual”) Distributions for qualified medical expenses of

eligible individual, spouse, and dependents are excludible from income

Distributions for any other purpose are subject to regular tax plus a 10% penalty tax

Distributions made after death, disability, or attaining age 65 are not subject to 10% penalty tax

How Can Accounts be Transferred?How Can Accounts be Transferred? Upon divorce

o Spouse can become account holder

o Transfer is not a taxable event

After deatho If spouse is HSA death beneficiary, then spouse

becomes account beneficiary, and death is not a taxable event

o If death beneficiary is non-spouse, HSA no longer exists and beneficiary gets taxed on HSA’s fair market value

What are Qualified Medical Expenses?What are Qualified Medical Expenses? Medical expenses defined

in IRC Section 213(d) Many out-of-pocket

medical care costs Prescription drug costs

and OTC drugs (as permitted by Rev. Rul. 2003-102)

Certain insurance premiumso Long-term care insurance

o COBRA premiums

o Health insurance while on unemployment

o Over age 65 – also any health insurance other than a Medicare supplemental policy

Health Savings Account ProductsHealth Savings Account Products Over 125 different HSA products are currently

being offered by HSA vendors nationwide o See http://greatlakeshsa.com/hsaproviders.html

Examples of vendors and products offered include:o FORTIS Financial Services

o Insurance companies

o Anthem By Design HSA, which offers an Anthem High Deductible Health Plan coupled with a Chase custodial account

Health Savings Account Products (cont'd)Health Savings Account Products (cont'd)

United Healthcare offers I Plan HSA which combines several HDHP options with a bank account or debit card issued by its own affiliate bank Exante (full HSA administration is included in the base fees)

Principal Bank, a division of the Principal Financial Group offers three different HSA products:o Principal Bank Choice Checking offers the convenience

of a checking account and debit cardo Principal HSA Mutual Funds offers 35 mutual funds

optionso Principal HSA Certificates of Deposit (CD) offers HSA

CDs in 1-year, 3-year and 5-year terms

Possible Build-Up of Savings for Families with an HSA - Various Time and Medical Expense ScenariosPossible Build-Up of Savings for Families with an HSA - Various Time and Medical Expense Scenarios

Health Savings Account Balances(Assumes a $4,000 deductible and deposit each year)

Account Balance After X Years

Age of Head of Household

Starting at 30

After Family Medical Expenses

of $1,000 Each Year

After Family Medical Expenses of $500 Each Year

Zero Family Medical

Expenses

5 Years 35 $ 17,406 $ 20,307 $ 23,208

10 Years 40 39,620 46,224 52,827

15 Years 45 67,972 79,301 90,630

20 Years 50 104,158 121,517 138,877

25 Years 55 150,340 175,397 200,454

30 Years 60 209,282 244,163 279,043

35 Years 65 284,509 331,927 379,345

Assumes 5% interest per year earned on your HSA deposits, and $4,000 is deposited each year. One Health Savings Account insurer (Medical Savings Insurance) pays 5% interest on balances in their Health Savings Accounts, and has paid that same interest rate since January 1, 1997, during the MSA pilot. Source: The HSA Coalition

Possible Build-Up of Savings for Families with an HSA - Various Time and Medical Expense ScenariosPossible Build-Up of Savings for Families with an HSA - Various Time and Medical Expense Scenarios

Health Savings Account Balances(Assumes a $2,000 deductible and deposit each year)

Account Balance After X Years

Age of Head of Household Starting

at 25

After Individual Medical Expenses

of $1,000 Each Year

After Individual Medical Expenses of $500 Each Year

Zero Individual Medical Expenses

5 Years 30 $ 5,802 $ 8,703 $ 11,604

10 Years 35 13,207 19,810 26,414

15 Years 40 22,657 33,986 45,315

20 Years 45 34,719 52,079 69,439

25 Years 50 50,113 75,170 100,227

30 Years 55 69,761 104,641 139,522

35 Years 60 94,836 142,254 189,673

40 Years 65 126,840 190,260 253,680

Assumes 5% interest per year earned on your HSA deposits, and $2,000 is deposited each year. One Health Savings Account insurer (Medical Savings Insurance) pays 5% interest on balances in their Health Savings Accounts, and has paid that same interest rate since January 1, 1997, during the MSA pilot. Source: The HSA Coalition

Average Use for Health Savings AccountsAverage Use for Health Savings Accounts On average Health Savings Account holders use

their account 4 times a year and end their first year with a balance of $840

The FactsThe Facts Fees charged by health savings account providers vary widely

(Source: HSAFinder.com survey, July 2005)

Fees range from $235 for the first year (Equity Trust Co.), to $0 (American Chartered Bank, Capitol Bank, Blackhawk Bank and First American Bank)

HDHPs that qualify to be partnered with an HSA are available through over 100 insurance companies currently

Most HDHPs have deductibles between $1,050 - $5,100 for singles and $2,100 - $10,200 for families

The Facts (cont'd)The Facts (cont'd)

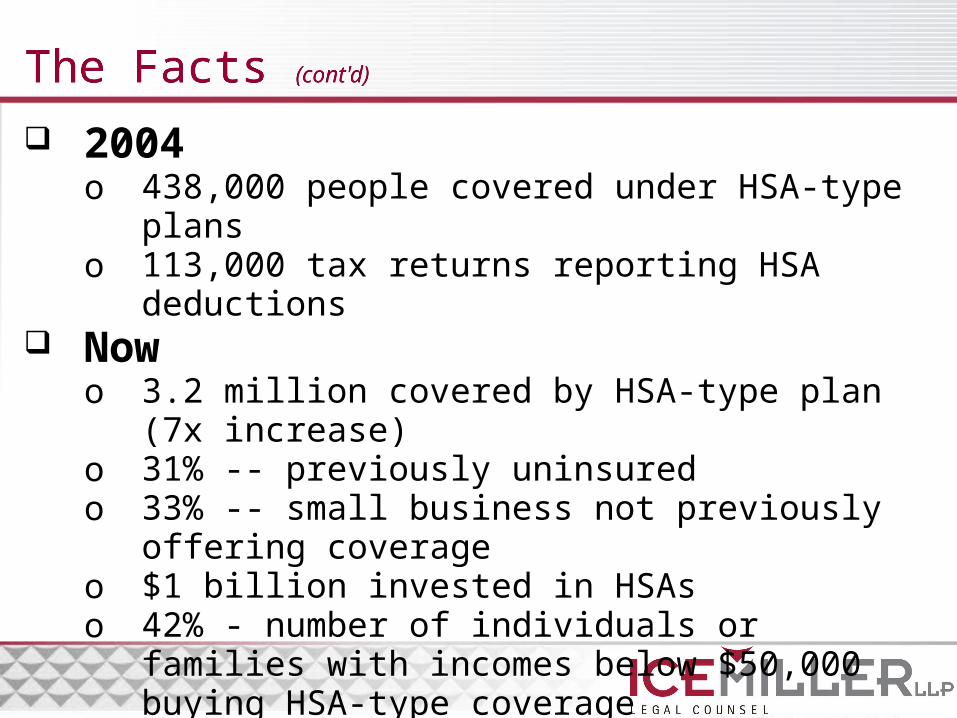

2004o 438,000 people covered under HSA-type planso 113,000 tax returns reporting HSA deductions

Nowo 3.2 million covered by HSA-type plan (7x increase)o 31% -- previously uninsuredo 33% -- small business not previously offering coverageo $1 billion invested in HSAso 42% - number of individuals or families with incomes

below $50,000 buying HSA-type coverage

Source: US Treasury Department Fact Sheet: “Dramatic Growth of Health Savings Accounts (HSAs)” (March 2006)

The Facts (cont'd)The Facts (cont'd)

Most commonly, monthly premium prices range from $51 to $100

61% of the employers are likely to offer HSAs in the near future (Source: Hewitt and Associates’ survey of 270 employers regarding HSAs)

One-third of the employers currently had the required benefit design structure in place to do so (Source: Hewitt and Associates’ survey of 270 employers regarding HSAs)

Several states have passed laws making individual contributions to HSAs tax-free and another 10 states have introduced legislation to do the same

Market response to HSAs with HDHP products has been modest

FSA HRA HSAEmployer-established

No restrictions for Medicare-eligibles

Employer-established

No restrictions for Medicare-eligibles

Must be covered by high deductible health plan (HDHP) which can be self-insured and no other plan that is not an HDHP

May not be Medicare-eligible

“Permitted insurance” allowed

EligibilityEligibility

FSA HRA HSAGenerally employee contributions through a 125 plan

No trust required – usually employer’s general assets

Must be employer contributions

No trust required – usually employer’s general assets

May be employee or employer contributions (can be through a 125 plan)

Funded trust required that must be maintained by a qualified HSA custodian

FundingFunding

FSA HRA HSAOnly qualified medical expenses

NO insurance premiums

Qualified medical expenses

Insurance premiums

Qualified medical expenses

Pre-age 65: (1) COBRA, long term care, while receiving unemployment compensation (all with no tax); (2) anything (with normal income tax plus a 10% penalty tax)

Post-age 64: (1) any health insurance except Medicare supplemental policies (with no tax); (2) anything (with only normal income tax)

Expense FlexibilityExpense Flexibility

FSA HRA HSANo, but employers generally allow accounts to be used post-employment for expenses incurred while employed

Subject to COBRA

No, but reimbursement for medical expenses of the former employee is permitted (e.g., to fund retiree health benefits)

Subject to COBRA

HSA belongs to the individual account beneficiary and is fully portable from employer to employer

Not subject to COBRA

PortabilityPortability

FSA HRA HSAUnused account balances are forfeited at end of taxable year

Unused account balances may accumulate and roll over to next year (at employer’s discretion)

Unused account balances accumulate and roll over to next year

May accept rollover contributions from Archer MSAs and other HSAs

Annual RolloversAnnual Rollovers

FSA HRA HSANone – limits are defined by employer and limited by nondiscrimination rules

None – limits are defined by employer and limited by nondiscrimination rules

Individual HDHP: lesser of 100% of deductible or $2,700

Family HDHP: lesser of 100% of deductible or $5,450

Contributions contingent on having a HDHP and none allowed post-65

Employer contributions subject to a comparability requirement (35% tax penalty if violated)

Contribution LimitsContribution Limits

FSA HRA HSAEmployee and employer contributions not taxable

Reimbursements not taxable if for qualified medical expenses (no other reimbursements allowed)

Employer contributions are not taxable

Reimbursements not taxable if for qualified medical expenses (no other reimbursements allowed)

Employer and employee contributions are not taxable

Reimbursements are not taxable if for qualified medical expenses

Other distributions subject to normal income taxes and 10% penalty (penalty does not apply after age 65, death, or disability)

Tax EffectsTax Effects

FSA HRA HSADivorced/surviving spouse and dependents eligible for COBRA

Divorced/surviving spouse and dependents eligible for COBRA

Death: spouse becomes HSA holder and HSA continues; other beneficiary receives distribution and HSA ceases

Divorce: HSA interest transferred to divorced spouse without tax

Death and DivorceDeath and Divorce