christopher nichols, fia -...

TRANSCRIPT

October 2014

Christopher Nichols, FIA

Global Absolute Return Strategies

This presentation is intended for investment professionals and must not be relied on by anyone else

Standard Life Investments: introduction

Standard Life PLC

• A FTSE 100 Financial Services company, established in 1825

• €11.2bn market cap, rated A1 by Moody’s

Standard Life Investments

• A wholly owned independent company since 1998, offices in

Edinburgh, London, Dublin, Paris, Boston, Montreal, Hong Kong,

Beijing and Seoul

• One of the fastest growing asset managers in the world

• Over €243.7bn of AuM (over 50% from external clients)

Absolute Return

• A 49 strong Multi-Asset Investing Team with over €86.5bn AuM

• Macro Strategists, Global Economics, Macro Management and Risk

& Structuring

• Range of return-targeted risk-minimisation capabilities

2

An exchange rate of £1:€1.2488 as at 30 June 2014 has been used

Source: Standard Life Investments, 30 June 2014

Genesis of Absolute Return Capabilities The Standard Life DB Pension Fund

Liabilities plus approach avoided the volatility in funding position

* The average UK Institutional Pension Portfolio

Source: Standard Life Investments and Towers Watson Statistics, 31 March 2014

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Q4 0

5

Q1 0

6

Q2 0

6

Q3 0

6

Q4 0

6

Q1 0

7

Q2 0

7

Q3 0

7

Q4 0

7

Q1 0

8

Q2 0

8

Q3 0

8

Q4 0

8

Q1 0

9

Q2 0

9

Q3 0

9

Q4 0

9

Q1 1

0

Q2 1

0

Q3 1

0

Q4 1

0

Q1 1

1

Q2 1

1

Q3 1

1

Q4 1

1

Q1 1

2

Q2 1

2

Q3 1

2

Q4 1

2

Q1 1

3

Q2 1

3

Q3 1

3

Q4 1

3

Q1 1

4

CAPS median

Liability Benchmark

GARS + Overlay

Background

• 80% funded DB plan in 2005

• Deficit reduction plan

• Drive to reduce risk and burden on sponsor

Genesis of GARS

• Examination of risk drivers

• Elimination of unrewarded risk

Client requirements

• Deliver the return target with least risk

• Transparent positioning

• Liquid instruments

• Safety-first approach

Counterparty selection and diversification

Daily collateralisation

Cash / G7 gov’t securities only

• Daily priced and dealt without notice

3

4

The Global Absolute Return Strategies Fund

Fund objective:

• Cash +5% per year, gross performance target, (rolling 3 years basis)

• 1/3 to 1/2 the risk of equity markets (expect volatility of 4% to 8%)

Key components:

Breadth: Investment opportunities, irrespective of the environment

Balance: Risk-based portfolio construction; ensures genuine diversity

Time frame: 3 year investment outlook; exploits established inefficiencies

A proven track record in delivering the Fund objectives

GARS

Time

Asset

Value

Equity

approach

GARS € performance

5 Delivering positive lower risk performance in challenging markets

* Source: Standard Life Investments converted € performance of £, institutional pooled pension portfolio to the 26/01/2011. GARS SICAV portfolio performance from

the 27/01/2011 to the 31/08/2014. ** Source: Thomson Datastream, 6 month Euribor. A conversion rate of £1:€1.260817 as at 31/08/2014 has been used

Standard Life Investments claims compliance with the Global Investment Performance Standards (GIPS®). The fund specific data presented above is supplementary

information to the Euro GARS GIPS® composite report, which is enclosed in the Appendix for your reference

• €7.7bn SICAV portfolio size (as at 31/08/2014)

• 7.8% gross annualised return (from inception to 31/08/2014)

• 5.5% volatility (Annualised figure, using monthly returns, from 01/07/2006 to

31/08/2014)

90

100

110

120

130

140

150

160

170

180

190

Price (

indexed t

o 1

00 a

t in

ception)

Cash (Euribor)** Target Return € GARS (gross)*

• Volatility:

GARS 5.5%

Global Equities 13.1% (annualised, using monthly data from 01/07/2006 to 31/08/2014)

• Maximum Drawdown:

GARS -14.3%

Global Equities -52.9% (using daily data to 31/08/2014)

• VaR (95%, weekly):

GARS -1.3%

Global Equities -3.7% (using weekly data to 31/08/2014)

Risk comparison

6

* Source: Standard Life Investments converted net € performance of £ Fund to the 26/01/2011. GARS SICAV Fund performance from the 27/01/2011 to 31/08/2014

** Source: FactSet, MSCI World €. Source: Standard Life Investments, net performance from 12/06/2006 to 31/08/2014

Delivering returns with less risk

55

65

75

85

95

105

115

125

135

145

155

165

175

185

Price (

indexed t

o 1

00 a

t in

ception)

Global Equities** € GARS (net)*

GARS vs Global Equities

Up months 70/98 vs 64/98

Upside capture 38.8%

Downside capture 3.8%

Uncorrelated return in down markets

7

* Source: Thomson Datastream, 6 month Euribor. ** Source: FactSet, MSCI World (€). Source: Standard Life Investments, gross performance, from

01/07/2006 to 30/06/2014. Portfolio performance is based on € converted performance of the £, institutional pooled pension portfolio from 12/06/2006 to

26/01/2011. SICAV GARS portfolio performance from the 27/01/2011 to 30/06/2014

3.5 3.3 1.7

1.8 2.3 1.3

-4.0

0.6

-4.4

3.3

0.7

5.5

11.3

1.5

4.6

2.3

4.8

-0.6

0.2

-1.3

1.6

3.7

5.5

-1.9

3.3

1.3

3.8

-0.4

0.2

3.7

0.6 1.3 0.9 0.9 1.0 1.1 1.2 1.2 1.1 1.3 1.3 1.1 0.5 0.4 0.3 0.3 0.2 0.2 0.3 0.3

0.3 0.4 0.5 0.4 0.3 0.3 0.2 0.1 0.1 0.1 0.1 0.1 0.1 0.1

5.6

4.2

1.6

5.2

-2.7

-5.0

-16.0

-0.9

-4.8

-20.8

-7.6

14.6

12.8

6.1

9.6

-3.3

2.2

11.0

-0.8 -1.5

-9.8

11.3

8.9

-0.2

5.4

0.1

10.8

-0.4

4.0

6.2

1.4

5.8

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

%

GARS (gross) Cash (Euribor)* Global Equities**

GARS investment approach

8

A broad range of return opportunities

Enduring diversity – through a wider opportunity set

Market

• Dynamic Allocation

• Long term risk premia such

as Equities, Credit, Listed

Real Estate

• Used only when we expect

to be rewarded on a 3 year

view

Security Selection

• Active security selection

• Conventional benchmarks

• Bottom-up, Focus on Change

process

Relative Value

• Seek pairs of related markets or

segments

• Our view is performance will differ over

3 years

• Profit from the difference in performance

irrespective of market direction

Directional

• Specific directional investment

ideas

• In markets with little or no long term

risk premium

• With significant return potential on a

3 year view

T

R

A

D

I

T

I

O

N

A

L

A

D

V

A

N

C

E

D

Multi-Asset Investing Team

9

* Based in North America

GARS Portfolio Constructors

Real Returns and Rates teams provide macro research and views that influence, but do not directly drive, the GARS portfolio hence these teams are not counted

in the number of investment professionals for the product and are greyed out.

Source: Standard Life Investments, 22 September 2014

Critical combination of skills and experience

MAI Team Members: Staff Area Average years

in industry

Average years at

Standard Life Investments

Economic Framework 11 Global Strategy 17 7

Risk Investigation 7 Multi-Asset Risk & Structuring 12 8

Idea Development and Implementation 23 Multi-Asset Management & Implementation 16 9

Development / Communication 8 Multi-Asset Investment Specialists 21 8

Tenure Size Strength

Head of Multi-Asset and Macro Investing

Jason Hepner CFA

Dr Anne Friel PRM

Multi-Asset Risk and Structuring

Dr Brian Fleming CFA PRM

Dr Robert de Roeck

Dr Jens Kroeske PRM FRM

Guy Stern CFA

Multi-Asset / Macro Portfolio Management

Malin Nairn

James Esland CFA

Multi-Asset Business Management

Rates

Philip Laing

Real Returns

Jonathan Gibbs

Roger Sadewsky

Colette Conboy

Scott Smith CFA

Sebastian Mackay

Murray Forbes

Multi-Asset

Adam Rudd CFA

David Sol Owen McCrossan FIA

Richard Martin FIA

Global Strategy

Andrew Milligan

Frances Hudson

Craig Hoyda

Neil Matheson CFA*

Alex Grassino*

Govinda Finn

Harry Smith

Jeremy Lawson

Alex Wolf

James McCann Neil Richardson

Naglis Vysniauskas

Katy Forbes CFA

Adam Skerry

Tom Walker

Jack Kelly

Liam O’Donnell CFA

Ross Hutchison

Norest Zvavamwe CFA Sean Flanagan CFA

Christopher Nichols FIA

Mark Foster FFA

Malcolm Jones FFA

David Bint

Tam McVie*

Stuart Peskin CFA*

Andrew Spooner*

Rahul Khasgiwale CFA*

Multi-Asset Investment Specialists

David Kirkpatrick

Multi-Asset Implementation

Audrey Simpson Julia Mikhniak Alex Berry

Jennifer Catlow CFA Stephen Kerr Kevin Hogg

Harry Barnes Kenny MacMaster

Chris Faulkner - MacDonagh

10

Process

Integrated with full skill set across Standard Life Investments

Idea Generation

Selection

Implementation

Investment

Governance &

Oversight

• Independent Risk

Analysis

• Counterparty Risk

Management

• Investment

governance

Fundamental

economic

analysis

Asset class

team views

and strategies

Quantitative

modelling

Valuation

modelling

Multi Asset Risk and Structuring

Pre-trade risk Diversification measurement Scenario Analysis

Strategic Investment Group

• Review

• Debate

• Ratify / Reject

Conviction

Diversity

Liquidity

Multi Asset Management

Strategy implementation Final position sizing Execution

Cash & Derivatives,

37.85%

European Equity, 9.99% UK Equity,

7.86%

Global Equity, 7.22%

Mexican Government Bonds

vs Euro, 4.95%

Global REITs, 4.94%

European Investment Grade

Credit, 4.91%

UK Investment Grade Credit, 4.91%

High Yield Credit, 3.16%

US Equity, 3.15%

Brazilian Government Bonds,

3.04%

Global Miners vs Swiss Equity, 2.88%

Global Equity Oil Majors, 2.84%

Chinese Equity, 2.30%

Diverse pool of return-seeking positions

11 Source: Standard Life Investments GARS SICAV portfolio, 30 June 2014

A more

informative view

Share of physical

allocation Share of market

risk exposure

European Equity

Global Equity

Global REITs

Global Equity Oil Majors

US Equity

UK Equity

High Yield Credit

Chinese Equity European Investment

Grade Credit UK Investment Grade

Credit Liquid Instruments

Long US Dollar vs Canadian Dollar

Long US Dollar vs Euro

Long Mexican Peso vs Australian Dollar

Long Equity Variance

Australian Short-term Interest Rates

Mexican Government Bonds vs Euro

Long US Dollar vs Japanese Yen

Short UK Real Yields

Brazilian Government Bonds

Suppressed European Interest Rate Volatility

European Long-End Curve Steepener

FX Hedging

US Equity Technology Sector vs US Equity

Small Cap

Japanese vs Korean Equity

German vs French Equity

Global Miners vs Swiss Equity

European vs US and Japanese Duration

Asian Basket vs US Variance

China Equity vs UK Equity Volatility

Security Selection

Risk profile

• The portfolio is exposed to multiple & diverse market risks

• Total stand-alone investment risk that is deployed to seek returns is 14.9%

• Equivalent equity volatility is 13.7%

• Independent risk analysis shows the benefits of investment diversification

12 Source: Standard Life Investments GARS SICAV portfolio, 30 June 2014

To

tal

sta

nd

-alo

ne

ris

k

10.91%

3.94%

0%

2%

4%

6%

8%

10%

12%

14%

Diversification benefits

Expected

Directional

Market returns

Relative value

Security selection

Historical scenario analysis

13

* MSCI World Returns prior to 2000 denoted in European Currency Units, except for 1987 which is denoted in German Marks

Source: GARS SICAV, RiskMetrics, 30/06/2014

-28 -26 -24 -22 -20 -18 -16 -14 -12 -10 -8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18

Black Monday 1987

Gulf War 1990

Rate Rise 1994

Mexican Crisis 1995

Asian Crisis 1997

Russian/LTCM

Tech Wreck (April 07 - 14, 2000)

Sept 11th

Equity Sell-Off (August 23 - October 09, 2002)

Equity Rally (October 10 - November 27, 2002)

Gulf War 2 (March 01 - 23, 2003)

Bond Rally (May 01 - June 13, 2003)

Bond Sell-Off (June 14 - July 31, 2003)

Emerging Market Sell-Off 2006 (May 01 - June 08, 2006)

Subprime Debacle 2007 (July 15 - August 15, 2007)

Bank Meltdown 2008 (September 12 - October 15, 2008)

Euro Crisis (July 22 - August 23, 2011)

QE jitters (May 22 - June 24, 2013)

% Move

Portfolio outlook / themes

Multi-Speed Global Growth

European vs US and Japanese Duration

German vs French Equity

Short UK Real Yield

Central Bank Policy

Australian Short Term Duration

Japanese vs Korean Equity

US Dollar vs Japanese Yen

14

Source: Standard Life Investments UK GARS portfolio, 31 August 2014

Maximising our insight on global investment markets

Resources and Demand

Global Equity Oil Majors

Global Miners vs Swiss Equity

Mexican Peso vs Australian Dollar

Earnings Potential

US Equity Tech vs Small Cap

European Equity

Global REITS

15

Key benefits of GARS

Longer term outlook Exploits established inefficiencies

Low turnover / costs

Durably diverse Broad range of return-seeking strategies

Work well together in many scenarios

Transparent Full risk & return attribution

Regulated / onshore

Accessible / Liquid Daily access

No notice, lockup or gate

Fits existing portfolios Low correlation

Low flat fee structure – a core solution

Exceptional rewards for modest risk levels

Appendices

Strategic Investment Group: Regular attendees

• Key attributes:

Foremost strategic thinkers

Diversity of backgrounds

Regular meetings to discuss portfolio

Assess new ideas from across the asset class desks

Forum to examine, test and approve multi-asset strategies

17

Source: Standard Life Investments, 04 September 2014

An experienced and proven team

Name Position Relevant experience (years)

Guy Stern (Chair) Head of Multi-Asset and Macro Investing 32

Andrew Milligan Head of Global Strategy 36

Stan Pearson Head of European Equities 30

Richard House Head of Emerging Market Debt 21

Craig MacDonald Head of Credit 19

Neil Matheson Senior Vice-President, Investment Strategy 33

Dr Brian Fleming Head of Multi-Asset Risk and Structuring 12

Roger Sadewsky Investment Director, Multi-Asset Investing 30

Frances Hudson Global Thematic Strategist 29

Neil Richardson Investment Director, Multi-Asset Investing 30

Philip Laing Investment Director, Fixed Income 25

Ken Dickson Investment Director, Money Markets & Foreign

Exchange 28

Jason Hepner Investment Director, Multi-Asset Investing 17

Jeremy Lawson Chief Economist, Global Strategy 15

Adam Rudd Investment Director, Multi-Asset Investing 9

Sebastian MacKay Investment Director, Multi-Asset Investing 15

Jack Kelly Investment Director, Fixed Income 21

Scott Smith Investment Director, Multi-Asset Investing 9

David Sol Investment Director, Multi-Asset Investing 12

Strategy activity over the last 4 quarters

18 Source: Standard Life Investments GARS portfolio, 03 September 2014

Q2 2014

Closed European Duration

(Forward Start)

Added Brazilian Gov’t

Bonds (hedged)

Reduced Investment Grade

credit exposure in UK and EU

Reduced UK Equity exposure

Added US $ vs NZD

Added INR vs €

Added European Banks

Relative Value

Modified the implementation

of the European Long-End

Curve Steepener

Closed Relative Variance

Income

Closed Hang Seng vs S&P

Volatility

Added Long Equity

Variance

Reduced High Yield exposure

Added Australian Short-

term Interest Rates

Added European vs US and

Japanese Duration

Added Suppressed

European Interest Rate

Volatility

Q3 2014 – to date Q4 2013 Q1 2014

Added Short UK Real Yield

Closed US Equity Technology

vs Taiwan Equity

Increased US Equity

Technology vs Small Cap

exposure

Added Global Miners vs

Swiss Equity

Reduced Chinese equity beta

exposure

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14

Spre

ad (

%)

Date

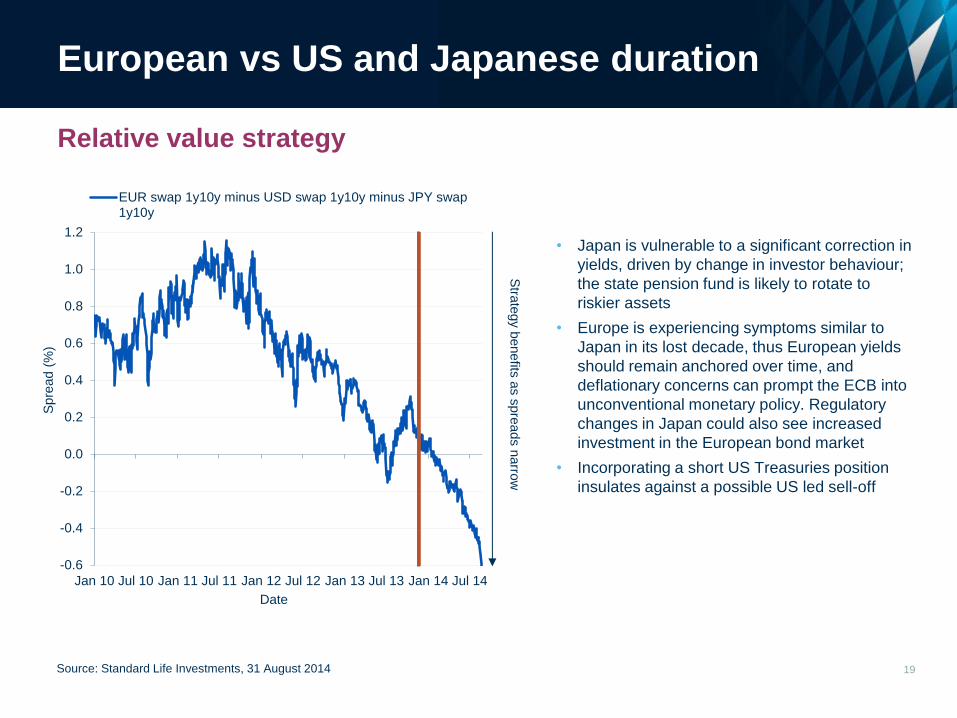

EUR swap 1y10y minus USD swap 1y10y minus JPY swap1y10y

European vs US and Japanese duration

• Japan is vulnerable to a significant correction in

yields, driven by change in investor behaviour;

the state pension fund is likely to rotate to

riskier assets

• Europe is experiencing symptoms similar to

Japan in its lost decade, thus European yields

should remain anchored over time, and

deflationary concerns can prompt the ECB into

unconventional monetary policy. Regulatory

changes in Japan could also see increased

investment in the European bond market

• Incorporating a short US Treasuries position

insulates against a possible US led sell-off

19

Relative value strategy

Source: Standard Life Investments, 31 August 2014

Stra

tegy b

enefits

as s

pre

ads n

arro

w

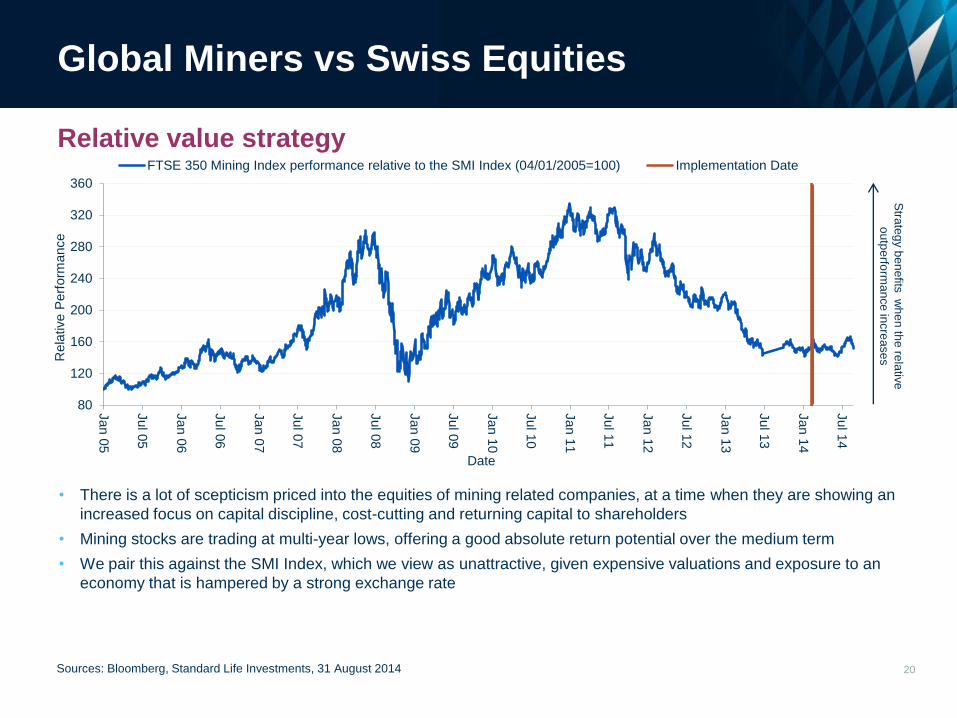

80

120

160

200

240

280

320

360

Jan 0

5

Jul 0

5

Jan 0

6

Jul 0

6

Jan 0

7

Jul 0

7

Jan 0

8

Jul 0

8

Jan 0

9

Jul 0

9

Jan 1

0

Jul 1

0

Jan 1

1

Jul 1

1

Jan 1

2

Jul 1

2

Jan 1

3

Jul 1

3

Jan 1

4

Jul 1

4

Rela

tive P

erf

orm

ance

Date

FTSE 350 Mining Index performance relative to the SMI Index (04/01/2005=100) Implementation Date

Global Miners vs Swiss Equities

• There is a lot of scepticism priced into the equities of mining related companies, at a time when they are showing an

increased focus on capital discipline, cost-cutting and returning capital to shareholders

• Mining stocks are trading at multi-year lows, offering a good absolute return potential over the medium term

• We pair this against the SMI Index, which we view as unattractive, given expensive valuations and exposure to an

economy that is hampered by a strong exchange rate

20 Sources: Bloomberg, Standard Life Investments, 31 August 2014

Relative value strategy

Stra

teg

y b

en

efits

wh

en

the

rela

tive

ou

tpe

rform

an

ce

incre

ase

s

7

8

9

10

11

12

13

14

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14

Yie

ld (

%)

Date

Bank of America Merrill Lynch Brazilian Government bond indexyield

Brazilian Government Bonds

• The Brazilian central bank has raised interest

rates sharply to combat inflation and defend

the Real; the result is that Brazil has one of

the highest levels of real interest rates in the

world

• The economic slowdown gives an opportunity

for the central bank to begin to cut rates: retail

sales, credit growth and industrial production

are all weak

21

Directional strategy

Source: Bloomberg, 31 August 2014

Stra

tegy b

enefits

when th

e y

ield

tighte

ns

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

Jan

00

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Jan

14

NZ

D/U

SD

Date

US Dollar-New Zealand Dollar Exchange Rate

US Dollar vs New Zealand Dollar

• The continued withdrawal of quantitative easing

in the US will cause money supply growth to

slow, and stronger economic growth can be a

driver of US dollar strength

• The NZD is one of the most overvalued

currencies in the world as measured by a range

of metrics; safe haven flows and high carry are

principle reasons for the overvaluation

• The overheating New Zealand housing market

is cooling down, which makes it unlikely that the

central bank will aggressively raise interest

rates

22

Directional strategy

Source: Bloomberg, 31 August 2014

Stra

tegy b

enefits

when th

e U

S D

olla

r appre

cia

tes

Indian Rupee vs Euro

23 Source: Bloomberg, 31 August 2014

• This pairing benefits from the Indian Rupee's

appeal as a carry currency and the need in

Europe for the Euro to depreciate. The Indian

central bank and government have gained

credibility by reducing the current account

deficit and by introducing an inflation target;

further reforms and an increase in FX reserves

make the currency less vulnerable to rate rises

in the US.

• ECB actions in the form of the TLTRO and

potential QE later this year should have the

effect of dampening the currency. Recent bank

deleveraging in time for the AQR looks to be

almost complete, hence a support of Euro

strength is in the process of being removed

Directional strategy

Stra

tegy b

enefits

when th

e E

UR

depre

cia

tes

30

40

50

60

70

80

90

100

Jan 0

0

Jan 0

1

Jan 0

2

Jan 0

3

Jan 0

4

Jan 0

5

Jan 0

6

Jan 0

7

Jan 0

8

Jan 0

9

Jan 1

0

Jan 1

1

Jan 1

2

Jan 1

3

Jan 1

4

INR

/EU

R

Date

EUR-INR Exchange Rate

European Equity Banks

24 Source: Bloomberg, 31 August 2014

Relative value strategy

• An improvement in European economic

conditions should entail lower loan provisions

and an increase in lending, which in turn

should improve profitability measure such as

Return on Equity and support valuations

• Movement towards a banking union within

Europe can support the sector over the

medium term which should boost sentiments

around earnings and valuations; the banks

index is still trading cheaply on a Price-to-Book

metric compared to its history

• Lower peripheral spreads and core

government bond yields have reduced the cost

of equity for banks

Stra

teg

y b

en

efits

wh

en

the

rela

tive

ou

tpe

rform

an

ce

of

Eu

rop

ea

n b

an

ks in

cre

ase

s

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12 Jan 13 Jul 13 Jan 14 Jul 14

Rela

tive

pe

rfo

rma

nce

Date

EuroStoxx Banks index performance relative to EuroStoxx index(Rebased at 100 as of January 2003)

Implementation date

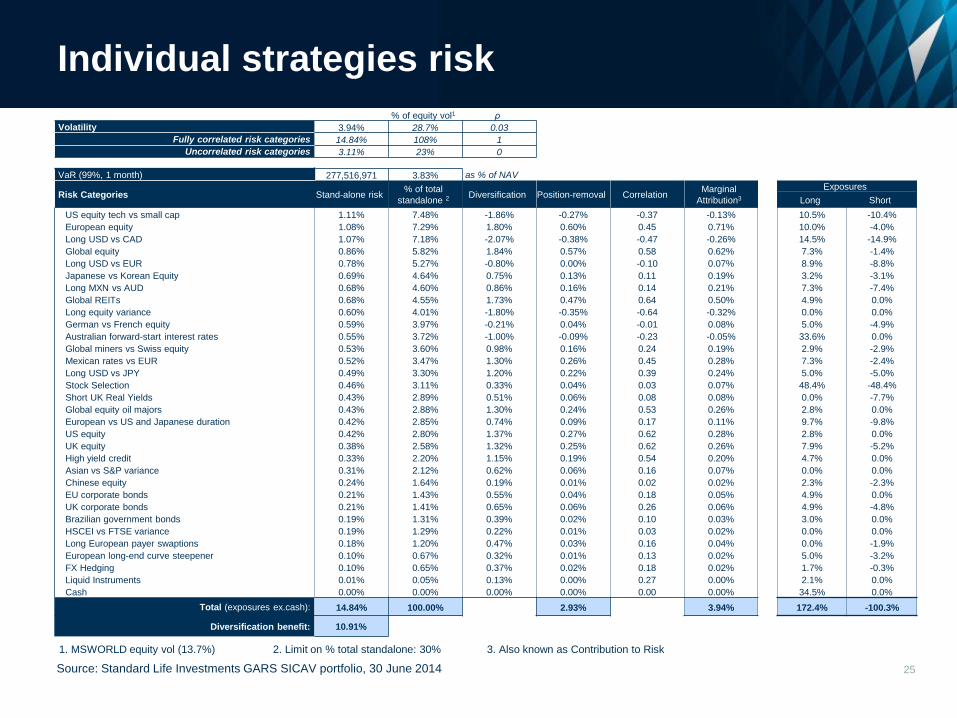

Individual strategies risk

25

1. MSWORLD equity vol (13.7%) 2. Limit on % total standalone: 30% 3. Also known as Contribution to Risk

% of equity vol1 ρ

Volatility 3.94% 28.7% 0.03

Fully correlated risk categories 14.84% 108% 1

Uncorrelated risk categories 3.11% 23% 0

VaR (99%, 1 month) 277,516,971 3.83% as % of NAV

Risk Categories Stand-alone risk % of total

standalone 2 Diversification Position-removal Correlation Marginal

Attribution3

Exposures

Long Short

US equity tech vs small cap 1.11% 7.48% -1.86% -0.27% -0.37 -0.13% 10.5% -10.4%

European equity 1.08% 7.29% 1.80% 0.60% 0.45 0.71% 10.0% -4.0%

Long USD vs CAD 1.07% 7.18% -2.07% -0.38% -0.47 -0.26% 14.5% -14.9%

Global equity 0.86% 5.82% 1.84% 0.57% 0.58 0.62% 7.3% -1.4%

Long USD vs EUR 0.78% 5.27% -0.80% 0.00% -0.10 0.07% 8.9% -8.8%

Japanese vs Korean Equity 0.69% 4.64% 0.75% 0.13% 0.11 0.19% 3.2% -3.1%

Long MXN vs AUD 0.68% 4.60% 0.86% 0.16% 0.14 0.21% 7.3% -7.4%

Global REITs 0.68% 4.55% 1.73% 0.47% 0.64 0.50% 4.9% 0.0%

Long equity variance 0.60% 4.01% -1.80% -0.35% -0.64 -0.32% 0.0% 0.0%

German vs French equity 0.59% 3.97% -0.21% 0.04% -0.01 0.08% 5.0% -4.9%

Australian forward-start interest rates 0.55% 3.72% -1.00% -0.09% -0.23 -0.05% 33.6% 0.0%

Global miners vs Swiss equity 0.53% 3.60% 0.98% 0.16% 0.24 0.19% 2.9% -2.9%

Mexican rates vs EUR 0.52% 3.47% 1.30% 0.26% 0.45 0.28% 7.3% -2.4%

Long USD vs JPY 0.49% 3.30% 1.20% 0.22% 0.39 0.24% 5.0% -5.0%

Stock Selection 0.46% 3.11% 0.33% 0.04% 0.03 0.07% 48.4% -48.4%

Short UK Real Yields 0.43% 2.89% 0.51% 0.06% 0.08 0.08% 0.0% -7.7%

Global equity oil majors 0.43% 2.88% 1.30% 0.24% 0.53 0.26% 2.8% 0.0%

European vs US and Japanese duration 0.42% 2.85% 0.74% 0.09% 0.17 0.11% 9.7% -9.8%

US equity 0.42% 2.80% 1.37% 0.27% 0.62 0.28% 2.8% 0.0%

UK equity 0.38% 2.58% 1.32% 0.25% 0.62 0.26% 7.9% -5.2%

High yield credit 0.33% 2.20% 1.15% 0.19% 0.54 0.20% 4.7% 0.0%

Asian vs S&P variance 0.31% 2.12% 0.62% 0.06% 0.16 0.07% 0.0% 0.0%

Chinese equity 0.24% 1.64% 0.19% 0.01% 0.02 0.02% 2.3% -2.3%

EU corporate bonds 0.21% 1.43% 0.55% 0.04% 0.18 0.05% 4.9% 0.0%

UK corporate bonds 0.21% 1.41% 0.65% 0.06% 0.26 0.06% 4.9% -4.8%

Brazilian government bonds 0.19% 1.31% 0.39% 0.02% 0.10 0.03% 3.0% 0.0%

HSCEI vs FTSE variance 0.19% 1.29% 0.22% 0.01% 0.03 0.02% 0.0% 0.0%

Long European payer swaptions 0.18% 1.20% 0.47% 0.03% 0.16 0.04% 0.0% -1.9%

European long-end curve steepener 0.10% 0.67% 0.32% 0.01% 0.13 0.02% 5.0% -3.2%

FX Hedging 0.10% 0.65% 0.37% 0.02% 0.18 0.02% 1.7% -0.3%

Liquid Instruments 0.01% 0.05% 0.13% 0.00% 0.27 0.00% 2.1% 0.0%

Cash 0.00% 0.00% 0.00% 0.00% 0.00 0.00% 34.5% 0.0%

Total (exposures ex.cash): 14.84% 100.00% 2.93% 3.94% 172.4% -100.3%

Diversification benefit: 10.91%

Source: Standard Life Investments GARS SICAV portfolio, 30 June 2014

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Eq

uitie

s

FX

Dura

tio

n

Pro

pert

y

Vo

latilit

y

Cre

dit

Sto

ck S

ele

ction

Cash

Div

ers

ific

atio

n

Fu

nd V

ola

tilit

y

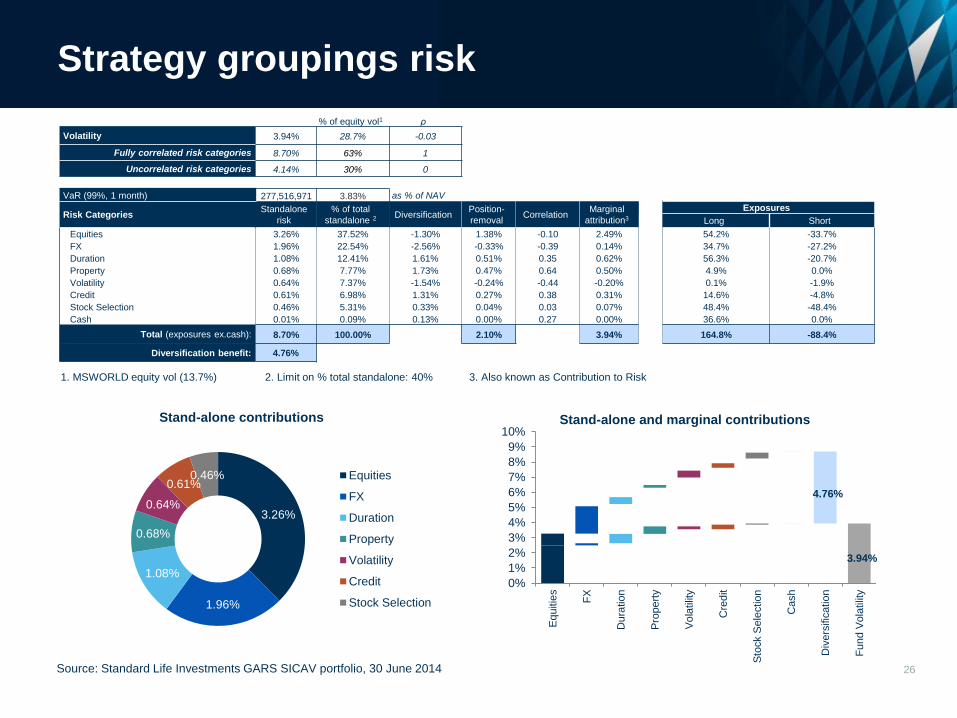

Strategy groupings risk

26

% of equity vol1 ρ

Volatility 3.94% 28.7% -0.03

Fully correlated risk categories 8.70% 63% 1

Uncorrelated risk categories 4.14% 30% 0

VaR (99%, 1 month) 277,516,971 3.83% as % of NAV

Risk Categories Standalone

risk

% of total

standalone 2 Diversification Position-

removal Correlation

Marginal

attribution3

Exposures

Long Short

Equities 3.26% 37.52% -1.30% 1.38% -0.10 2.49% 54.2% -33.7%

FX 1.96% 22.54% -2.56% -0.33% -0.39 0.14% 34.7% -27.2%

Duration 1.08% 12.41% 1.61% 0.51% 0.35 0.62% 56.3% -20.7%

Property 0.68% 7.77% 1.73% 0.47% 0.64 0.50% 4.9% 0.0%

Volatility 0.64% 7.37% -1.54% -0.24% -0.44 -0.20% 0.1% -1.9%

Credit 0.61% 6.98% 1.31% 0.27% 0.38 0.31% 14.6% -4.8%

Stock Selection 0.46% 5.31% 0.33% 0.04% 0.03 0.07% 48.4% -48.4%

Cash 0.01% 0.09% 0.13% 0.00% 0.27 0.00% 36.6% 0.0%

Total (exposures ex.cash): 8.70% 100.00% 2.10% 3.94% 164.8% -88.4%

Diversification benefit: 4.76%

1. MSWORLD equity vol (13.7%) 2. Limit on % total standalone: 40% 3. Also known as Contribution to Risk

Stand-alone contributions Stand-alone and marginal contributions

4.76%

3.94%

Source: Standard Life Investments GARS SICAV portfolio, 30 June 2014

3.26%

1.96%

1.08%

0.68%

0.64%

0.61% 0.46% Equities

FX

Duration

Property

Volatility

Credit

Stock Selection

Forward-looking scenarios

World Economic Forum 2013

• Economic / Political

• Environmental

• Societal / Technological

Current scenarios of interest

• QE: Continuation & Abrupt End

• EU moves apart

• Commodity shock

• China crisis

• Trade war

• Russia West Standoff

• Inflation Shock

• Liquidity Drought

27 Shaded regions represent the origin of one or more scenarios

28

Expert views inform portfolio outcomes

China Crisis

Description:

• Rebalancing causes growth to slow significantly

• Compounded by rising inflation / wages

• Demographics limits future development

• Debt-fuelled investment boom / misallocation of resources - debt quality / defaults rise

• Productivity growth remains low or falls further

Sources: Standard Life Investments & Bloomberg, June 2014

Combining quantitative expertise with subjective judgement

Key Factor Shock

CNY Volatility 4.8%

Australian

Dollar

-15%

MSCI EM -75%

Copper -60%

China Crisis

29

Expert views inform portfolio outcomes

Russia West Standoff

Description:

• Russia restores sphere of influence over former-soviets to distract from weak economy

• Energy supply disruption impacts European growth, especially in Germany / Eastern

Europe

• Sanctions strengthened in response to military intervention

• Banking exposures in France, Italy Sweden and Austria impacted

Sources: Standard Life Investments & Bloomberg, June 2014

Combining quantitative expertise with subjective judgement

Key Factor Shock

Oil Price +20%

S&P 500 -5%

DAX -14%

CAC -10%

10yr Bund

yield

-0.5%

Russia West Standoff

Regular liquidity monitoring

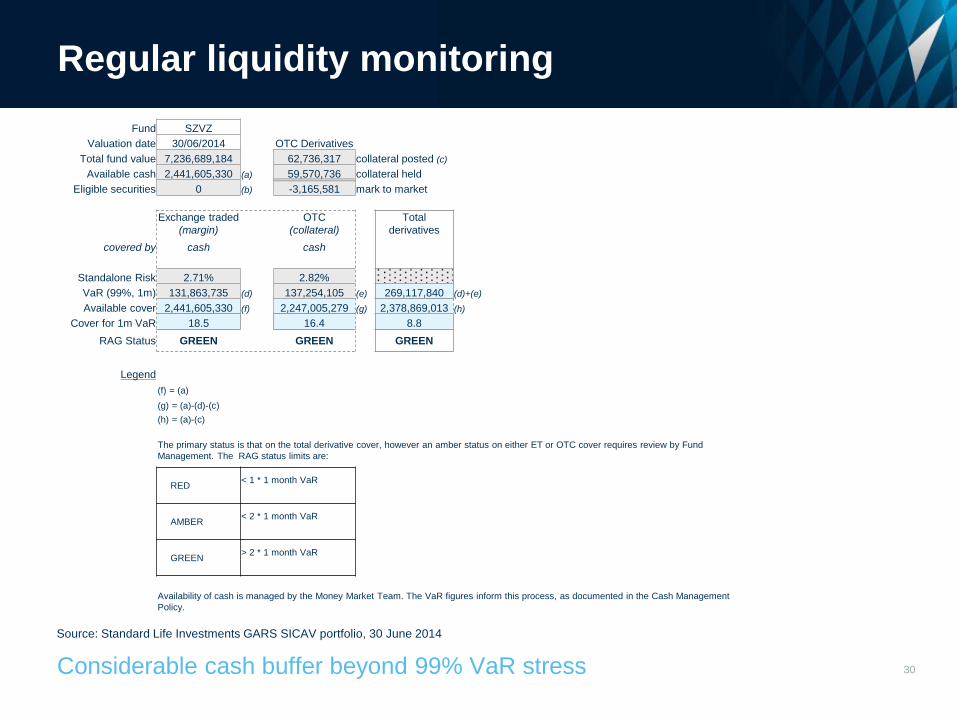

30

Source: Standard Life Investments GARS SICAV portfolio, 30 June 2014

Considerable cash buffer beyond 99% VaR stress

Fund SZVZ

Valuation date 30/06/2014 OTC Derivatives

Total fund value 7,236,689,184 62,736,317 collateral posted (c)

Available cash 2,441,605,330 (a) 59,570,736 collateral held

Eligible securities 0 (b) -3,165,581 mark to market

Exchange traded

(margin)

OTC

(collateral)

Total

derivatives

covered by cash cash

Standalone Risk 2.71% 2.82%

VaR (99%, 1m) 131,863,735 (d) 137,254,105 (e) 269,117,840 (d)+(e)

Available cover 2,441,605,330 (f) 2,247,005,279 (g) 2,378,869,013 (h)

Cover for 1m VaR 18.5 16.4 8.8

RAG Status GREEN GREEN GREEN

Legend

(f) = (a)

(g) = (a)-(d)-(c)

(h) = (a)-(c)

The primary status is that on the total derivative cover, however an amber status on either ET or OTC cover requires review by Fund

Management. The RAG status limits are:

RED < 1 * 1 month VaR

AMBER < 2 * 1 month VaR

GREEN > 2 * 1 month VaR

Availability of cash is managed by the Money Market Team. The VaR figures inform this process, as documented in the Cash Management

Policy.

Ex-post risk analysis

• Expect volatility range of 4 –

8%

• We track realised volatility

relative to expectation and to

risk model estimates

• Many different bases can be

used:

Monthly, weekly, daily data

Various window sizes and

weightings

• Measuring relative to equities

is a useful way to normalise

• We expect to be 1/3 to 1/2 of

equity volatility

31 Source: Standard Life Investments UK GARS portfolio; Datastream MSWRLD$(RI)~£. 30 June 2014

Financial turbulence – measuring the unusual

• An extension to the v-mask methodology

• Monitors unusual moves in

strategy returns (like V-masks)

correlation/covariance (not necessarily corresponding to big

moves)

• It evaluates the level of unusualness of today's moves and

records an ‘event’ if it is statistically significant (relative to a

95% historical confidence)

32 Source: Standard Life Investments UK GARS portfolio, 18 September 2014

+0.5%

+0.5%

-0.5%

-0.5%

S&P 500 FTSE 100

Usual

Unusual

S&P 500 FTSE 100

0

50

100

150

200

250

0

50

100

150

200

250

Sep 04 Feb 06 Jun 07 Oct 08 Mar 10 Jul 11 Dec 12 Apr 14

Glo

bal equity

index

Unusualn

ess index

GARS strategies unusualness

Global Equity (rhs) Unusualness index (lhs) limit

V-Masks for individual positions and overall

33

Short-term v-masks

(zero return, exponentially weighted, half-life = 3m, 99% confidence),

1 year of daily data

Source: Standard Life Investments, June 2014

34 34 Study rejects hypothesis of ‘random walk’ over 2-8 year view

Philosophical foundation: Hard evidence for asset allocation opportunity horizon

• Picking short-term market

peaks and troughs is

notoriously difficult

• Research indicates

opportunities for mean

reversion do exist on a 2-5

year investment horizon

• Investment decisions to

exploit these opportunities

are based on in-depth

qualitative analysis

Non-Outlier Max Non-Outlier Min

75%

25%

Median

Box Plot: 1-Year Equivalent Volatility of UK Equity Market

Total Real Return Data: 1900 - 2002, Source BZW Equity Gilt Study

Comparison with 40 random shuffled BZW data surrogates

Non-overlapping return runs of length n

1 Y

ea

r Eq

uiv

ale

nt V

ola

tility

y_1

0.06

0.10

0.14

0.18

0.22

0.26

0.30

0.34

bzw sur

y_2

bzw sur

y_4

bzw sur

y_8

bzw sur

y_16

bzw sur

1 year cumulative performance attribution

35 Source: Standard Life Investments GARS SICAV portfolio, 30 June 2014

Quarter Q3 13 Q4 13 Q1 14 Q2 14

Year to Date

Cumulative

contribution over

1 year Number of contributors 31 31 31 31

Security Selection 0.0% 0.4% -0.1% -0.2% -0.3% 0.1%

UK Equity 0.2% 0.2% 0.0% 0.1% 0.0% 0.4%

Global Equity 0.2% 0.4% 0.0% 0.2% 0.2% 0.8%

European Equity -0.1% 0.3% 0.2% 0.1% 0.3% 0.5%

US Equity 0.1% 0.2% 0.0% 0.1% 0.1% 0.4%

Russian Equity 0.0% 0.0% 0.0%

Global Equity Oil Majors 0.0% 0.3% 0.0% 0.3% 0.2% 0.6%

Chinese Equity 0.3% 0.1% -0.3% 0.0% -0.3% 0.1%

Investment Grade Corporate Bonds 0.1% 0.2% 0.1% 0.2% 0.3% 0.6%

High Yield Credit 0.3% 0.3% 0.1% 0.1% 0.2% 0.8%

Global REITs 0.0% 0.1% 0.1% 0.3% 0.5% 0.6%

Cash 0.1% 0.1% 0.1% 0.1% 0.1% 0.2%

Short UK Real Yield -0.1% 0.0% -0.1% -0.1%

Australian Short-term Interest Rates 0.0% 0.1% 0.4% 0.5% 0.5%

European Long-End Curve Steepener 0.0% 0.1% 0.1% 0.0% 0.1% 0.2%

European Duration (Forward Start) 0.1% 0.1% 0.1% 0.0% 0.2% 0.3%

US steepener 0.2% 0.0% 0.2%

Mexican Government Bonds vs Euro -0.1% -0.1% 0.2% 0.3% 0.4% 0.2%

Brazilian Government Bonds -0.1% -0.1% -0.1%

Long Equity Variance -0.3% -0.2% -0.4% -0.5% -0.8%

Suppressed European Interest Rate Volatility 0.0% 0.0% -0.1% -0.1% -0.1%

Long US Dollar vs Japanese Yen 0.1% 0.3% 0.0% 0.0% 0.0% 0.4%

Long US Dollar vs Euro -0.4% -0.2% 0.0% 0.1% 0.0% -0.5%

Long US Dollar vs Canadian Dollar -0.4% 0.4% 0.5% -0.6% -0.1% 0.0%

Long Mexican Peso vs Australian Dollar -0.2% 0.4% -0.2% -0.1% -0.3% -0.2%

Long Indian Rupee vs Singapore Dollar -0.3% 0.0% -0.3%

Other FX -0.1% -0.1% 0.0% 0.0% 0.0% -0.2%

Global Miners vs Swiss Equity -0.2% 0.0% -0.2% -0.2%

US Large vs US Small Cap Equity -0.2% 0.0% -0.2%

US Equity Technology Sector vs US Equity Small

Cap 0.0% 0.1% -0.3% 0.4% 0.2% 0.3%

US Equity Technology vs Taiwan 0.1% 0.2% 0.0% 0.0% 0.3%

German vs French Equity -0.1% 0.4% -0.1% 0.0% -0.1% 0.1%

Japanese vs Korean Equity -0.2% 0.3% -0.2% 0.1% -0.1% 0.0%

European v US and Japanese Duration 0.0% 0.2% 0.2% 0.4% 0.4%

China Equity vs UK Equity Volatility 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Relative Variance Income 0.0% 0.0% 0.0% 0.0%

Hang Seng vs S&P volatility 0.0% 0.0% 0.0% 0.0%

Asian Basket vs US Variance 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Residual 0.5% -0.52% 0.4% 0.0% 0.3% 0.3%

GARS total 0.2% 3.7% 0.6% 1.3% 1.9% 5.8%

-1.0% 0.0% 1.0%

Cumulative performance attribution

36 Source: Standard Life Investments UK GARS portfolio, 30 June 2014

Quarter Q3 06 Q4 06 Q1 07 Q2 07 Q3 07 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14

Number of strategies 13 14 14 15 16 18 22 23 30 34 37 36 35 30 31 35 33 32 34 28 30 29 31 30 31 34 35 34 31 31 31 31

Security Selection -0.2% 1.4% 1.2% 0.7% -0.3% -0.6% 0.0% 0.8% -0.9% -0.5% 1.4% -1.2% -1.0% -0.1% -0.3% -0.6% 0.2% 0.3% -0.5% -0.4% -0.7% 0.3% 0.4% 0.2% 0.1% 0.1% 0.2% 0.2% 0.1% 0.3% -0.1% -0.2%

UK Equity 0.6% 0.7% 0.2% 0.6% -0.1% 0.1% -1.0% -0.3% -0.5% 0.1% -0.4% 0.8% 0.9% 0.2% 0.2% -0.3% 0.6% 0.3% 0.2% 0.1% -0.4% 0.0% 0.0% 0.0% 0.0% 0.0% 0.3% 0.0% 0.2% 0.1% 0.0% 0.1%

Global Equity 0.5% 0.7% 0.2% 0.7% 0.0% -0.4% -1.3% 0.0% -0.8% -1.1% -0.9% 1.4% 1.1% 0.3% 0.4% -0.8% 0.7% 0.8% 0.4% -0.2% -0.5% 0.3% 0.6% -0.4% 0.2% -0.2% 0.6% 0.2% 0.3% 0.3% 0.0% 0.2%

European Equity 0.5% 0.3% 0.7% 1.0% -0.1% -0.2% -1.4% -0.4% -1.1% -1.4% -0.8% 1.2% 1.0% 0.1% 0.1% 0.0% 0.4% 0.4% 0.2% 0.0% -0.6% 0.1% 0.4% -0.2% 0.3% 0.2% 0.2% 0.0% 0.0% 0.3% 0.2% 0.1%

US Equity -0.7% -1.1% -0.9% 1.0% 0.8% 0.3% 0.2% -0.2% 0.3% 0.3% 0.2% 0.0% -0.4% 0.4% 0.3% -0.2% 0.1% -0.1% 0.4% 0.1% 0.1% 0.2% 0.0% 0.1%

Russian Equity -0.2% -0.7% 0.1% 0.4% -0.4% 0.2% 0.2% 0.1% -0.3% 0.1%

Global Equity Oil Majors 0.0% 0.3% 0.0% 0.3%

Korean Equity 0.0% -0.5% 0.2% 0.0% -0.1%

Chinese Equity -0.1% -0.3% 0.4% 0.1% -0.3% 0.0%

Investment Grade Corporate Bonds 0.3% 0.3% 0.1% -0.2% 0.3% 0.2% -0.1% -0.1% -0.4% -0.3% -0.7% 3.0% 2.6% 0.4% 1.1% 0.2% 0.9% -0.4% 0.2% 0.2% -0.3% 0.4% 0.9% 0.1% 0.8% 0.5% 0.1% -0.1% 0.2% 0.1% 0.2% 0.2%

Financial Sector Credit 0.8% 0.4% -0.3% 0.3% -0.9% 0.8% 1.1% -0.1%

High Yield Credit -0.3% 0.2% 0.2% 0.1% 0.0% -0.8% 0.6% 0.6% 0.0% 0.6% 0.3% 0.4% -0.1% 0.3% 0.3% 0.1% 0.1%

Global Inflation-Linked Bonds 0.4% -0.1% 0.1% -0.1% 0.4% 0.4% 0.4% 0.1% 0.0% -0.3% 0.1% 0.2% 0.3% 0.2% 0.1% 0.2% 0.3% -0.1% 0.1% 0.3% 0.3% 0.4% 0.2% -0.2% 0.3% 0.4% 0.3% -0.4%

European Real Estate -0.2% -0.1% -0.7% -0.4%

Japanese Real Estate -0.1% -0.7% -0.3% -0.3% -0.1% -0.2%

Global REITs 0.1% 0.3% 0.0% 0.1% 0.1% 0.1% 0.4%

Cash 0.3% 0.2% 0.3% 0.5% 0.3% 0.3% 0.4% 0.4% 0.4% 0.3% 0.2% 0.1% 0.1% 0.1% 0.0% 0.0% 0.1% 0.0% 0.1% 0.0% 0.1% 0.1% 0.1% 0.1% 0.1% 0.0% 0.0% 0.1% 0.0% 0.1% 0.0% 0.0%

Short UK Inflation 0.2% -0.2% 0.0% -0.3% 0.4% -0.4% 1.2% -0.1% -0.4% -0.1%

UK Inflation Real Yield 0.1% -0.1% 0.0%

Short UK Real Yields -0.1% -0.1%

UK Short-term Interest Rates -0.5% 0.8% 0.4% 0.1% 0.3% 0.8% 0.1% -0.6% 0.2% 0.1% 0.7% 0.4%

European Short-term Interest Rates -0.1% 0.1% -1.1% 0.6% 1.8% 1.0% -0.7% 0.2% 0.0% 0.2% 0.0%

Australian Short-term Interest Rates 0.0% -0.4% 0.1% 0.2% 0.0% 0.3% 0.0% 0.1% 0.0% 0.1% 0.0% 0.1% 0.4%

Swedish Short-term Interest Rates 0.1% 0.0% -0.1% 0.2% 0.4%

Medium-term UK Interest Rates 0.2% -0.3% -0.1%

Medium-term European Interest Rates 2.4% 0.9% -0.1% 0.8%

Medium-term Australian Interest Rates -0.4% 1.1% 0.0%

Long-term European Interest Rates 0.3% -0.3% -0.3% -0.6% 0.1% 0.0% 0.0% -0.7% 0.7% 2.7% -0.9% -0.5% 0.5% -0.2% 0.5% 0.8% 0.3%

Long-term US Interest Rates 0.2% -0.2% -0.6% 0.5% -0.8% 0.1%

Long-term Japanese Interest Rates 1.0% 0.8% 0.3% -0.2% 1.0% 0.5% 0.5% 0.6% 0.9% -0.5% 0.3% 0.4% 0.2%

Japanese Interest Rates -0.2% -0.1%

Australian interest rate flattener 0.0% 0.0%

Credit Curve Steepener 0.0% 0.1% 0.0%

UK Curve Steepener 0.4% 0.3%

European Bond Yield Steepener 0.0% 0.0% 0.0% 0.0% 0.1% 0.1% 0.0% 0.1% 0.1% 0.0% 0.1%

European Long-End Curve Steepener 0.0% -0.2% 0.0% 0.1% 0.1% 0.0%

European Duration (Forward Start) 0.0% 0.1% 0.1% 0.1% 0.0%

US Long Bond Yields (Forward-Start) 0.3% -1.1% -0.1% 0.0% 2.3% 0.2% 0.0% 0.0% 0.1% 0.1%

US steepener 0.0% 0.3% -0.2% 0.1%

Mexican Government Bonds vs Euro -0.2% 0.2% 0.5% 0.3% 0.4% -0.1% 0.6% -0.2% -0.1% -0.1% 0.2% 0.3%

Brazilian Government Bonds 0.0%

UK Inflation Linked Asset Swap 0.5% 0.1%

FTSE 100 Dividends 0.0% -0.3% -0.1% 0.1% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Nikkei Dividends -0.1% 0.0% 0.2% 0.1% 0.1%

UK Equity Volatility 0.3% 0.2% 0.1% 0.2% 0.4% 0.1%

Long Equity Variance -0.1% -0.2% 1.9% -0.1% -0.3% -0.1% -0.3%

Long Equity Volatility 0.1% -0.2% -0.1% -0.1% -0.2%

Suppressed European Interest Rate Volatility 0.0% 0.0% -0.1%

Long Sterling vs Euro 0.1% -3.1% 1.0% 1.3% -0.6% 0.2% 0.2% 0.4% -0.2% -0.1%

Long Sterling vs South African Rand 0.0% -0.1% 0.0% 0.0% 0.0%

Long US Dollar vs Sterling 0.1% -0.2% 0.0% -0.2% -0.1% 0.5% 0.0% 0.0% 0.5%

Long US Dollar vs Japanese Yen -0.2% 0.2% 0.0% -0.8% 0.5% -0.1% -0.3% 0.3% 0.1% -0.2% -0.2% -0.1% 0.1% -0.1% -0.2% 0.1% 0.4% -0.2% -0.1% 0.5% 0.4% 0.2% 0.1% 0.3% 0.0% 0.0%

Long US Dollar vs Euro 0.3% 0.8% 0.8% -0.4% -0.3% 0.2% 0.6% 0.7% -1.0% 0.5% -0.9% -0.3% 0.5% 0.5% -0.3% 0.6% -0.3% -0.3% 0.3% -0.1% -0.4% -0.2% 0.0% 0.1%

Long US Dollar vs South African Rand -0.2%

Long US Dollar vs Canadian Dollar -0.1% -0.1% 0.2% -0.6% 0.1% 0.3% 0.4% -0.3% 0.4% 0.5% -0.5%

Long Swedish Krona vs Euro -0.2% 0.5% 0.0% 0.5% 0.0%

Long Brazilian Real vs Japanese Yen -0.4% 1.0% -0.9% -1.3% 0.5% 0.9% 0.3%

Long Brazilian Real vs Chilean Peso 0.2% -0.1% 0.1% 0.2% -0.2% -0.1%

Long Brazilian Real vs Czech Koruna -0.4% 0.0%

Long Brazilian Real vs Australian Dollar -0.4% 0.0%

Long Turkish Lira vs Sterling 0.2% 0.0%

Long Turkish Lira vs Canadian Dollar -0.2% 0.1% -0.1%

Long Turkish Lira vs South Aftrican Rand -0.6% 0.3%

Long Polish Zloty vs Czech Koruna -0.3% 0.4% 0.2% -0.2% 0.0% 0.2% -0.2% 0.0% -0.2%

Long Norwegian Krone vs Euro -0.3% 0.1% 0.1%

Long Norwegian Krone vs Swiss Franc 0.8%

Long Mexican Peso vs Australian Dollar 0.0% 0.0% 0.2% 0.3% -0.1% 0.3% -0.3% -0.1%

Long Indian Rupee vs Singapore Dollar -0.1% 0.2% -0.2% -0.3%

Other FX 0.1% 0.0% 0.1% 0.0% 0.1% 0.0% 0.2% 0.0% 0.0% -0.5% -0.2% -0.2% 0.1% 0.0% 0.1% 0.1% 0.1% 0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.1% -0.1% -0.1% -0.1% 0.0% 0.0%

UK Large v Mid Cap UK equity -0.4% -0.9% -0.3% 0.6% 0.3% 0.3% -0.5% 0.5% 0.2% 0.5% -0.9% -0.6%

Swiss Equity vs German Equity 0.0% -0.3% 0.2% -0.1% 0.2% 0.0% 0.1% -0.3% -0.1% -0.1% 0.1% -0.6% -0.1% -0.8% -0.3%

Korean Equity vs Japanese Equity 0.0% 0.1%

Korean Equity vs European Equity 0.3% -0.1% 0.0% 0.0% 0.1% -0.5%

US Large vs US Small Cap Equity 0.1% -0.2% 0.0% -0.7% -0.1% 0.1% 0.7% -0.3% -0.1% 0.1% 0.0% -0.2% -0.3% 0.0% -0.3%

US Equity Technology vs US Equity Small Cap 0.1% -0.4% 0.7% -0.3% 0.1% -0.3% -0.2% 0.0% 0.0% 0.1% -0.1% 0.4%

US Equity Technology vs Taiwan -0.1% 0.2% 0.1% 0.1% 0.2% 0.1%

German vs French Equity 0.0% -0.2% 0.4% -0.2% 0.0%

Japanese vs Korean Equity -0.2% 0.3% -0.2% 0.1%

Global Miners vs Swiss Equity -0.1% -0.1%

Financial Sector vs Broad Credit -0.6% -0.4% 1.0% 0.3% 0.2% 0.3% 0.0% 0.2% -1.1% 0.7% -0.2% -0.8% 0.0% 1.0% -0.7%

Broad vs Financial Sector Equity 0.1% 0.3% 0.6% 0.3% 0.0% 0.9%

European Financials Capital Structure 0.1% 0.1% 0.1% -0.4% 0.0%

High Yield vs Equity -0.3% -0.6% 1.2% 0.0% -0.1% -0.3%

European vs Japanese Medium Term Interest Rates -0.4% 0.9% 0.4%

US vs Japanese Medium Term Interest Rates 0.6% 0.9%

Australian vs Japanese Medium Term Interest Rates 0.1% -0.6% 0.2% 0.2% 0.1%

Japanese vs European Forward-Start Interest Rates 0.5% -0.1%

European vs US and Japanese Duration 0.0% 0.2% 0.2%

US Short-term Swap Spread 0.9%

UK vs German Short-rates 0.1% 0.5% 0.2%

Australian vs German Short-rates 0.1% 0.1%

Australian vs US Short-rates -0.2% -0.1% 0.1% 0.0% 0.4% 0.2%

Swedish vs German Short-rates 0.0% 0.0% 0.1% -0.2% 0.0%

Swedish vs US Short-rates -0.2% -0.2%

UK vs European Forward-Start Duration 0.1% 0.0% 0.0% 0.0%

German vs French Interest rates 0.0% -0.1% 0.0% -0.1%

US Inflation vs UK Inflation -0.5% -1.5% 0.0% 0.3%

UK vs European Inflation -0.1%

UK Inflation vs Long Gilts 0.2%

USD vs GBP Volatility Spread 0.1% 0.0% 0.1%

European Equity Volatility 0.2% 0.0% 0.0% -0.1% 0.0%

S&P Call Calendar Spread 0.1%

German Equity vs UK Equity Relative Volatility -0.2% 2.0% -0.1% -0.1% 0.1%

China Equity vs UK Equity Volatility 0.0% 0.1% -0.5% 0.2% 0.0% 0.0% 0.0% 0.1% 0.1% -0.1% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Relative Variance Income -0.2% 1.2% 0.0% 0.2% 0.1% 0.4% -0.3% -0.7% 0.1% 0.5% 0.4% -0.2% -1.0% 0.3% 0.3% -0.3% 0.2% 0.3% 0.2% 0.0% 0.0% 0.0%

Hang Seng vs S&P volatility -0.2% 0.0% -0.1% -0.1% 0.0% 0.0% 0.0%

Chinese vs. Japanese currency volatility 0.0% 0.0% -0.2% 0.0%

Asian Basket vs US Variance 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Residual 0.0% 0.6% -0.5% -0.1% 0.2% 0.4% 0.0% 0.1% 0.0% 0.0% -0.2% -0.2% 0.2% 0.2% 0.0% 0.0% 0.2% 0.0% -0.1% -0.1% 0.2% -0.2% -0.1% -0.1% 0.0% 0.0% 0.0% 0.0% -0.2% -0.1% 0.0% -0.1%

GARS total 3.7% 3.7% 2.0% 2.3% 2.7% 1.7% -3.7% 0.9% -4.2% 3.4% 0.8% 5.5% 11.3% 1.5% 4.6% 2.2% 4.8% -0.7% 0.2% -1.3% 1.2% 3.7% 5.5% -1.7% 3.0% 1.4% 4.0% -0.6% 0.4% 3.6% 0.4% 1.4%

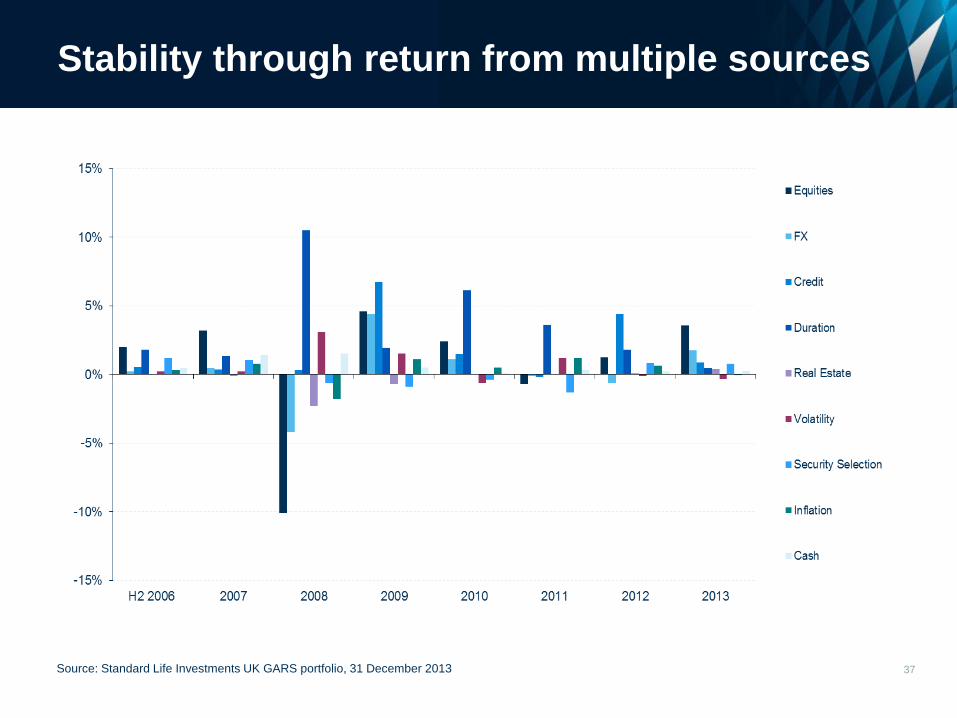

Stability through return from multiple sources

37 Source: Standard Life Investments UK GARS portfolio, 31 December 2013

Monthly GARS SICAV performance

38

Converted € performance of £, institutional pooled pension portfolio to the 26/01/2011. GARS SICAV portfolio performance from the 27/01/2011

Source: Standard Life Investments, 31/08/2014

GROSS Portfolio 6m Euribor Relative NET Portfolio 6m Euribor Relative GROSS Portfolio MCSI World (€) Relative

Sep-13 0.39 0.03 0.36 Sep-13 0.32 0.03 0.29 Sep-13 0.39 2.32 -1.88

Oct-13 1.48 0.03 1.45 Oct-13 1.41 0.03 1.38 Oct-13 1.48 3.49 -1.94

Nov-13 1.46 0.03 1.44 Nov-13 1.39 0.03 1.36 Nov-13 1.46 1.67 -0.21

Dec-13 0.72 0.03 0.69 Dec-13 0.65 0.03 0.62 Dec-13 0.72 2.15 -1.40

Jan-14 0.55 0.03 0.51 Jan-14 0.48 0.03 0.44 Jan-14 0.55 -1.58 2.16

Feb-14 0.39 0.03 0.36 Feb-14 0.33 0.03 0.30 Feb-14 0.39 2.58 -2.13

Mar-14 -0.36 0.03 -0.39 Mar-14 -0.43 0.03 -0.46 Mar-14 -0.36 0.41 -0.76

Apr-14 -0.06 0.04 -0.10 Apr-14 -0.13 0.04 -0.17 Apr-14 -0.06 0.47 -0.53

May-14 1.17 0.03 1.13 May-14 1.09 0.03 1.06 May-14 1.17 3.71 -2.45

Jun-14 0.18 0.03 0.15 Jun-14 0.11 0.03 0.08 Jun-14 0.18 1.49 -1.28

Jul-14 1.83 0.02 1.81 Jul-14 1.76 0.02 1.74 Jul-14 1.83 0.72 1.11

Aug-14 0.19 0.02 0.17 Aug-14 0.12 0.02 0.10 Aug-14 0.19 3.86 -3.53

YTD 3.94 0.25 3.69 YTD 3.36 0.25 3.11 YTD 3.94 12.14 -7.31

1 Year (%) 8.21 0.36 7.82 1 Year (%) 7.30 0.36 6.91 1 Year (%) 8.21 21.86 -11.21

2 Years (% p.a.) 6.57 0.36 6.19 2 Years (% p.a.) 5.67 0.36 5.29 2 Years (% p.a.) 6.57 17.40 -9.23

3 Years (% p.a.) 8.35 0.67 7.63 3 Years (% p.a.) 7.44 0.67 6.72 3 Years (% p.a.) 8.35 19.64 -9.43

4 Years (% p.a.) 5.77 0.88 4.85 4 Years (% p.a.) 4.88 0.88 3.96 4 Years (% p.a.) 5.77 14.84 -7.90

5 Years (% p.a.) 7.89 0.91 6.92 5 Years (% p.a.) 6.98 0.91 6.02 5 Years (% p.a.) 7.89 14.92 -6.12

Q2 07 1.85 1.06 0.78 Q2 07 1.63 1.06 0.57 Q2 07 1.85 5.18 -3.16

Q3 07 2.27 1.16 1.10 Q3 07 2.06 1.16 0.89 Q3 07 2.27 -2.70 5.11

Q4 07 1.29 1.24 0.05 Q4 07 1.07 1.24 -0.16 Q4 07 1.29 -4.99 6.60

Q1 08 -3.99 1.14 -5.07 Q1 08 -4.19 1.14 -5.27 Q1 08 -3.99 -15.99 14.28

Q2 08 0.63 1.25 -0.61 Q2 08 0.42 1.25 -0.82 Q2 08 0.63 -0.86 1.51

Q3 08 -4.37 1.33 -5.62 Q3 08 -4.57 1.33 -5.82 Q3 08 -4.37 -4.83 0.48

Q4 08 3.32 1.10 2.19 Q4 08 3.10 1.10 1.97 Q4 08 3.32 -20.84 30.51

Q1 09 0.74 0.54 0.20 Q1 09 0.53 0.54 -0.01 Q1 09 0.74 -7.64 9.07

Q2 09 5.48 0.38 5.08 Q2 09 5.26 0.38 4.85 Q2 09 5.48 14.58 -7.94

Q3 09 11.30 0.29 10.98 Q3 09 11.06 0.29 10.74 Q3 09 11.30 12.81 -1.34

Q4 09 1.52 0.26 1.26 Q4 09 1.31 0.26 1.05 Q4 09 1.52 6.14 -4.35

Q1 10 4.56 0.24 4.30 Q1 10 4.33 0.24 4.08 Q1 10 4.56 9.58 -4.59

Q2 10 2.30 0.25 2.04 Q2 10 2.08 0.25 1.83 Q2 10 2.30 -3.33 5.82

Q3 10 4.76 0.29 4.46 Q3 10 4.54 0.29 4.24 Q3 10 4.76 2.19 2.52

Q4 10 -0.64 0.32 -0.95 Q4 10 -0.85 0.32 -1.16 Q4 10 -0.64 10.98 -10.47

Q1 11 0.24 0.34 -0.10 Q1 11 0.03 0.34 -0.31 Q1 11 0.24 -0.82 1.07

Q2 11 -1.29 0.43 -1.71 Q2 11 -1.50 0.43 -1.92 Q2 11 -1.29 -1.46 0.17

Q3 11 1.60 0.45 1.15 Q3 11 1.39 0.45 0.93 Q3 11 1.60 -9.79 12.63

Q4 11 3.65 0.44 3.20 Q4 11 3.43 0.44 2.99 Q4 11 3.65 11.34 -6.90

Q1 12 5.52 0.34 5.16 Q1 12 5.30 0.34 4.94 Q1 12 5.52 8.90 -3.10

Q2 12 -1.90 0.25 -2.14 Q2 12 -2.10 0.25 -2.35 Q2 12 -1.90 -0.16 -1.74

Q3 12 3.31 0.16 3.15 Q3 12 3.09 0.16 2.93 Q3 12 3.31 5.39 -1.97

Q4 12 1.34 0.10 1.24 Q4 12 1.12 0.10 1.02 Q4 12 1.34 0.14 1.19

Q1 13 3.78 0.08 3.69 Q1 13 3.56 0.08 3.48 Q1 13 3.78 10.75 -6.30

Q2 13 -0.37 0.08 -0.45 Q2 13 -0.58 0.08 -0.66 Q2 13 -0.37 -0.38 0.00

Q3 13 0.21 0.09 0.12 Q3 13 -0.01 0.09 -0.10 Q3 13 0.21 3.99 -3.64

Q4 13 3.70 0.09 3.60 Q4 13 3.48 0.09 3.38 Q4 13 3.70 6.21 -2.96

Q1 14 0.58 0.10 0.48 Q1 14 0.37 0.10 0.28 Q1 14 0.58 1.37 -0.78

Q2 14 1.28 0.10 1.18 Q2 14 1.07 0.10 0.97 Q2 14 1.28 5.75 -4.23

12/06/06 - 31/08/14 (% p.a.) 7.85 2.07 5.66 12/06/06 - 31/08/14 (% p.a.) 6.94 2.07 4.77 12/06/06 - 31/08/14 (% p.a.) 7.85 6.09 1.66

2007 7.31 4.53 2.66 2007 6.41 4.53 1.80 2007 7.31 -1.18 8.60

2008 -4.53 4.92 -9.01 2008 -5.34 4.92 -9.77 2008 -4.53 -37.24 52.13

2009 20.07 1.47 18.32 2009 19.05 1.47 17.33 2009 20.07 26.72 -5.25

2010 11.33 1.10 10.12 2010 10.40 1.10 9.19 2010 11.33 20.14 -7.33

2011 4.21 1.67 2.50 2011 3.33 1.67 1.64 2011 4.21 -1.84 6.17

2012 8.38 0.85 7.47 2012 7.46 0.85 6.56 2012 8.38 14.75 -5.54

2013 7.44 0.34 7.07 2013 6.53 0.34 6.17 2013 7.44 21.86 -11.84

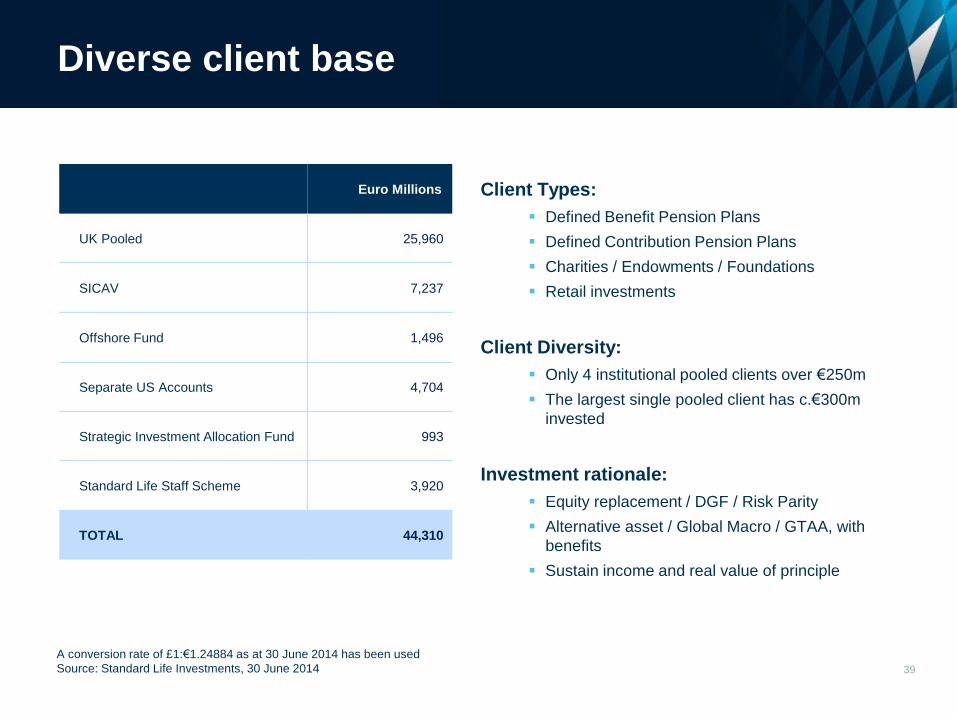

Diverse client base

39

A conversion rate of £1:€1.24884 as at 30 June 2014 has been used

Source: Standard Life Investments, 30 June 2014

Client Types:

Defined Benefit Pension Plans

Defined Contribution Pension Plans

Charities / Endowments / Foundations

Retail investments

Client Diversity:

Only 4 institutional pooled clients over €250m

The largest single pooled client has c.€300m

invested

Investment rationale:

Equity replacement / DGF / Risk Parity

Alternative asset / Global Macro / GTAA, with

benefits

Sustain income and real value of principle

Euro Millions

UK Pooled 25,960

SICAV 7,237

Offshore Fund 1,496

Separate US Accounts 4,704

Strategic Investment Allocation Fund 993

Standard Life Staff Scheme 3,920

TOTAL 44,310

40

Global Absolute Return Strategies Fund SICAV

Launch Date

Benchmark

Performance target

Robust risk control

Charges

ISIN Codes

Bloomberg

• 26th January 2011

• 6 month Euribor

• 6 month Euribor + 5 % (Gross of fees) over a 3 year rolling basis

• Expected volatility range: 4% to 8%

• Sophisticated portfolio

• Retail (Share Class A) 1.60% AMC, Expected TER 1.70%

• Institutional (Share Class D) 0.85% AMC, Expected TER 0.90%

• Retail (Share Class A)

Acc LU0548153104

Dist LU0548153443

• Institutional (Share Class D)

Acc LU0548153799

Dist LU0548153955

• Retail (Share Class A)

Acc SLGLARA LX

Dist SLGLARI LX

• Institutional (Share Class D)

Acc SLGLDIA LX

Dist SLGLDII LX

Euro GARS

Firm Disclosures

A complete list and description of all of the firm's composites are available from Standard Life Investments. There are no minimum asset levels set below which portfolios are not included in a composite. All

performance calculations and returns have been calculated gross of management fees. All returns are presented on an all-inclusive basis and as such all capital gains interest income and withholding taxes

have been taken into account in market valuations and returns. All indices are on a gross of tax basis apart from FTSE UK indices which are net of Withholding Tax. There are no Non-Fee-Paying portfolios

included in any composite. The Daily True Time Weighted Rate of Return methodology has been used from 2001 apart from unitised Cash Property GARS and MyFolio products where NAV performance is

used. Prior to this NAV performance was used for all products.

Additional information regarding policies for calculating and reporting returns is available upon request. Dispersion is calculated using high/low difference. Standard Life Investments 'The Firm' consists of all

fee-paying funds managed by Standard Life Investments and its Subsidiaries which include Standard Life Investments (Mutual Funds) Limited SLTM Limited Standard Life Investments (Corporate Funds)

Limited Standard Life Investments (USA) Limited and Standard Life Investments (Asia) Limited. Past performance results from Standard Life Investments Limited UK Firm and Standard Life Investments

Limited Irish Firm have been linked to form the performance record of the new firm Standard Life Investments. The new firm was created on 01/01/2008. Standard Life Investments claims compliance with the

Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Standard Life Investments has been independently verified by

PricewaterhouseCoopers LLP for the periods 1996 to 2013. The verification report is available upon request. Verification assesses whether (1) the firm has complied with all the composite construction

requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification

does not ensure the accuracy of any specific composite presentation

Composite Disclosures

Derivatives may be used to vary exposure to markets and express views on the direction of currencies, interest rates, sectors and securities to enhance capital return, limit downside volatility and preserve

capital

Includes part period return for 2006 from 01/07

The composite includes funds that invest in a highly diversified strategy including equities, bonds, property and cash with a derivative overlay in options, futures, swaps and currency forwards to deliver a

positive absolute return. The fund is benchmarked against 6 month Euribor

This composite includes GBP denominated funds that are converted into EUR using 3 month EUR Libor and 3 month GBP Libor rates

The standard annual fee applicable to the composite is 0.85%, but individual fees are negotiated on an account basis

41

Composite Name Euro GARS

Creation Date 01-07-2006

Firm Standard Life Investments

Currency EUR

Report End Date 31-12-2013

Composite Group Converted GARS

Benchmark 6 Month Euribor

Anlzd Return

(Composite)

Anlzd Return

(Benchmark)

3 Year Anzld StdDev

(Composite)

3 Year Anzld StdDev

(Benchmark) Dispersion Market Value Total Firm Assets

% of Firm

Assets

Number of

Portfolios

Dec 2006 6.88 1.82 NA NA NA 46,559,943 189,614,161,508 0.02 1

Dec 2007 7.31 4.53 NA NA NA 328,936,430 186,833,049,375 0.18 1

Dec 2008 -4.79 4.92 NA NA NA 858,822,210 122,024,692,127 0.70 1

Dec 2009 19.90 1.47 7.13 0.45 NA 2,424,300,230 142,954,997,814 1.70 1

Dec 2010 11.25 1.10 7.25 0.50 NA 8,013,954,428 153,735,850,524 5.21 1

Dec 2011 4.03 1.67 5.73 0.11 NA 1,421,412,636 147,648,287,247 0.96 1

Dec 2012 8.38 0.85 4.75 0.12 NA 3,310,696,559 165,118,070,004 2.01 1

Dec 2013 7.44 0.34 4.67 0.17 NA 6,166,575,083 180,260,162,963 3.42 1

42

The information shown relates to the past. Past performance is not a guide to the future. The value of investment can go down as well as up. Any data contained herein which is attributed to a third party ("Third Party Data") is the property of (a) third party supplier(s) (the “Owner”) and is licensed for use by Standard Life**. Third Party Data may not be copied or distributed. Third Party Data is provided “as is” and is not warranted to be accurate, complete or timely. To the extent permitted by applicable law, none of the Owner, Standard Life** or any other third party (including any third party involved in providing and/or compiling Third Party Data) shall have any liability for Third Party Data or for any use made of Third Party Data. Past performance is no guarantee of future results. Neither the Owner nor any other third party sponsors, endorses or promotes the fund or product to which Third Party Data relates. ** Standard Life means the relevant member of the Standard Life group, being Standard Life plc together with its subsidiaries, subsidiary undertakings and associated companies (whether direct or indirect) from time to time." Standard Life Investments Limited is registered in Scotland (SC123321) at 1 George Street, Edinburgh EH2 2LL. Standard Life Investments Limited is authorised and regulated by the Financial Conduct Authority. Calls may be monitored and/or recorded to protect both you and us and help with our training. www.standardlifeinvestments.com © 2014 Standard Life, images reproduced under licence