christopher mcbride, v.p., trg - hfma...

TRANSCRIPT

1

“Bundled Payments—Getting it Right!”

Christopher McBride, V.P., TRG

2

TRG Overview

• Founded in 2001, Located in Denver, CO (Division

of Vizient)

• Clients include Physician Practices, Hospitals, and

Health Systems

• Key Focus is Physician-Hospital Alignment Higher Quality

Lower Cost

Better Patient Experience

• Have Been Involved in Every Medicare Bundled

Payment- Related Effort Since the “Participating

Centers of Excellence” in the 1990s

• Currently Working with Over 30 Hospitals and

60 Physician Groups in Models 2 and 4 of BPCI

as well as CJR

3

Today’s Topics

1. “Bundled Payments 101”

2. Payors and Bundled Payments—The 20+ Year Tango

3. BPCI—Bigger and Bolder than Anything Before

4. CJR—The Choice Isn’t Yours

5. The Future and Some Wise Words

4

• The Antithesis of “Per-Click”, “Fee-for-Service” Medicine

• A Method of Creating Transparency and Price Predictability

through Shifting Risk from Payer to Provider

Bundled Payments—Who, What, How?

Q: Average # of Claims

for a Total Joint

Surgery (MS DRG

#470) over a 90 day

episode?

Answer: 25

5

Air Travel in the Unbundled Age…

• Ticketing Fees

• Change Fees

• Checked Bag Fees

• Carry-On Fees

• Lavatory Fees (!!)

“What were once habits are now vices…”(with apologies to The Doobie Brothers)

“The study named United as the top

airline for producing ancillary revenue

in the world, estimating its annual haul

at $5.86 billion.”

6

Bundled Payment Success Story

“Fee Free”(40+ Years of Profitability—ONLY

Major US Airline to NEVER File for

Bankruptcy)

6

7

What’s the Magic Word?

8

At a Minimum, Bundled Payments Look to:

Create a Fixed and Predictable—Transparent— Reimbursement

per MS-DRG

Include all Hospital and Physician Services Rendered During an

MS-DRG LOS—including 72 Hours Prior for the Hospital and,

Increasingly, 90 Days Post-Discharge Inclusive of Many

Components

Eliminate Outlier Payments

Shift Risk for the Good, Bad, and Ugly to Providers

Payers

RISKProviders

Key Objectives of Bundled Payments

9

Volume to Value: CMS Announces Goals

Medicare move towards Alternate

Payment Models (ACO and

Bundles)

Year

30% 2016

50% 2018

Medicare payments tied to quality

or valueYear

85% 2016

90% 2018

10

What percent of system

revenue will be in value-

based agreements by 2020?

Source: 2015 Survey, MedAssets Healthcare Executive Forum

“Our first goal is for 30% of all Medicare provider

payments to be in alternative payment models that are

tied to how well providers care for their patients, instead

of how much care they provide – and to do it by 2016.

Our goal would then be to get to 50% by 2018.”

—Sylvia Mathews Burwell, HHS Secretary, January 26, 2015

>75%

<25%

26–49%

50–75%

Bye-Bye Fee-for-Service—It’s So ‘90s…

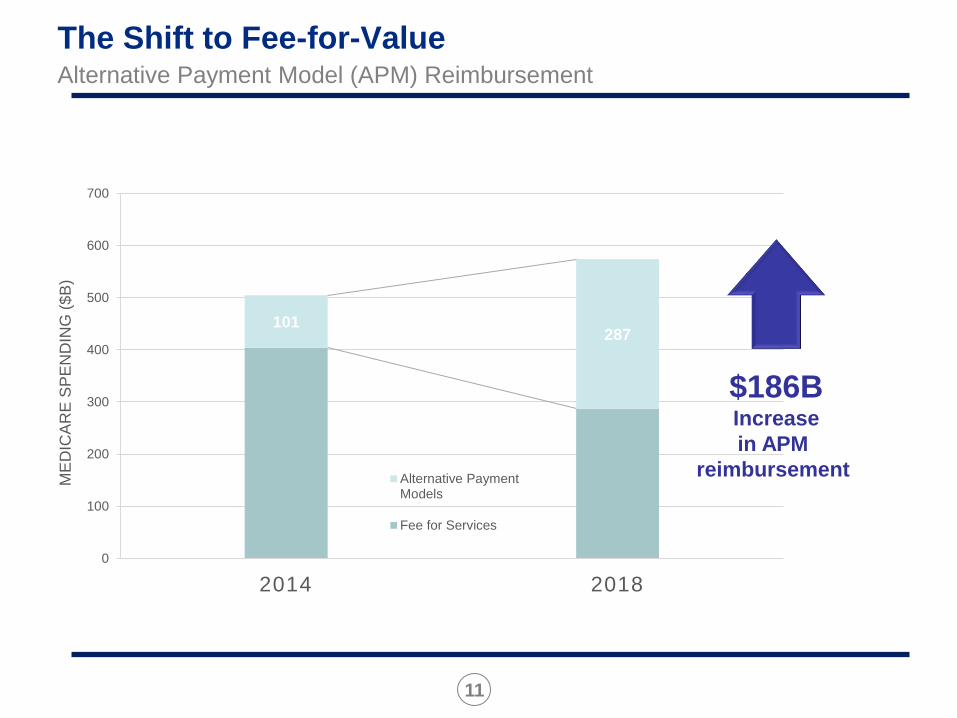

11

101287

0

100

200

300

400

500

600

700

2014 2018

ME

DIC

AR

E S

PE

ND

ING

($

B)

Alternative PaymentModels

Fee for Services

The Shift to Fee-for-ValueAlternative Payment Model (APM) Reimbursement

$186BIncrease

in APM

reimbursement

12

PAYORS AND BUNDLED PAYMENTS

The 20+ Year Tango

Then Why Haven’t

You Married Me?

Bundled

Payments…

¡Te Adoro!

13

The Father of Bundled Payments

14

“Of the many 'firsts' with which I have been involved at the Texas

Heart Institute —including the first successful human heart transplant

in the United States and the first total artificial heart transplant in the

world—the achievement that may have the greatest impact on health

care did not occur in the operating room or in the research

laboratory. It happened on a piece of paper... when we created the

first-ever packaged pricing plan for cardiovascular surgical

procedures.”

― Denton Cooley

You Heard It Here First

15

1991—Medicare Participating Heart Bypass Demonstration—Implemented

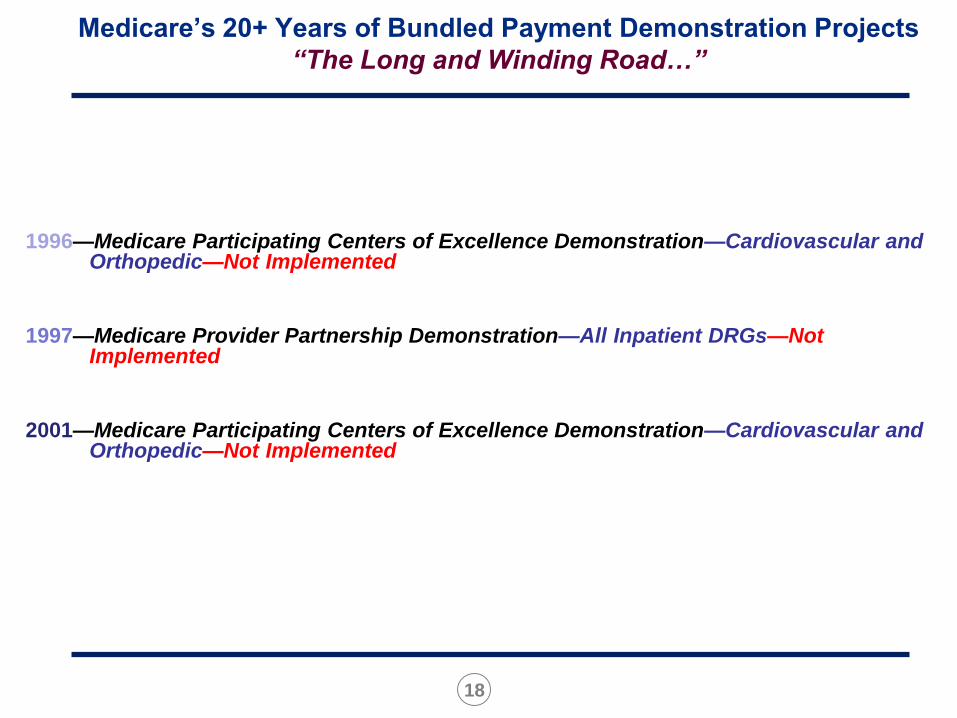

Medicare’s 20+ Years of Bundled Payment Demonstration Projects

“In the Beginning…”

16

St. Joseph’s Hospital of Atlanta

Methodist Hospital, Indianapolis

St. Luke’s Episcopal Hospital/THI, Houston

University Hospital, Boston

The Ohio State University Hospital, Columbus

St. Joseph Mercy Hospital, Ann Arbor

St. Vincent’s Hospital, Portland

Medicare’s 20+ Years of Bundled Payment Demonstration Projects

“In the Beginning…”

Medicare Participating Heart Bypass Demonstration Sites

17

Early Private Payor Bundled Initiatives

18

1996—Medicare Participating Centers of Excellence Demonstration—Cardiovascular and Orthopedic—Not Implemented

1997—Medicare Provider Partnership Demonstration—All Inpatient DRGs—Not Implemented

2001—Medicare Participating Centers of Excellence Demonstration—Cardiovascular and Orthopedic—Not Implemented

Medicare’s 20+ Years of Bundled Payment Demonstration Projects

“The Long and Winding Road…”

19

SOURCE: U.S. Department of Health and Human Services

“The Case for ACE”—National Health Expenditure Growth

Period of initial

demonstrations

20

2008—Acute Care Episode (“ACE”) Demonstration—Cardiovascular and Orthopedic—Implemented

• 4 State Focus: Colorado, New Mexico, Oklahoma and Texas

Ortho—90 Medicare Hip and Knee; 125 Total

Cardiac—100 Medicare CABG / VALVE; 200 Total All-Payor

200 Medicare PTCAs; 400 Total All-Payor

• Hospitals Submitted Bundled Pricing Bids for 28 Cardiovascular and/or 9 Orthopedic DRGs –

Inclusive of Medicare Discount (Discount not Prescribed)

• Bundled Bid was Inclusive of ALL Part A, Part B, Outliers, and Capital Pass-Through

Reimbursements for IP Episode

• Medicare Shared 50% of Savings with Medicare Beneficiaries

• Physicians Could Make Up to 25% Above Medicare FFS through Gainsharing

• All Claims Adjudication and Payment Facilitated by a Single Fiscal Intermediary (TrailBlazer)

Then Along Came ACE…

21

AlabamaAlabamaAlabamaAlabamaAlabama

ArizonaArizonaArizonaArizonaArizona

ArkansasArkansasArkansasArkansasArkansasCaliforniaCaliforniaCaliforniaCaliforniaCalifornia

ColoradoColoradoColoradoColoradoColorado

FloridaFloridaFloridaFloridaFlorida

IdahoIdahoIdahoIdahoIdaho

IllinoisIllinoisIllinoisIllinoisIllinois IndianaIndianaIndianaIndianaIndiana

IowaIowaIowaIowaIowa

KansasKansasKansasKansasKansas

KentuckyKentuckyKentuckyKentuckyKentucky

LouisianaLouisianaLouisianaLouisianaLouisiana

MichiganMichiganMichiganMichiganMichigan

MinnesotaMinnesotaMinnesotaMinnesotaMinnesota

MissouriMissouriMissouriMissouriMissouri

MontanaMontanaMontanaMontanaMontana

NebraskaNebraskaNebraskaNebraskaNebraska

Nev adaNev adaNev adaNev adaNev ada

New MexicoNew MexicoNew MexicoNew MexicoNew Mexico

OklahomaOklahomaOklahomaOklahomaOklahoma

OregonOregonOregonOregonOregonSouth DakotaSouth DakotaSouth DakotaSouth DakotaSouth Dakota

TennesseeTennesseeTennesseeTennesseeTennessee

TexasTexasTexasTexasTexas

UtahUtahUtahUtahUtah

WisconsinWisconsinWisconsinWisconsinWisconsin

WyomingWyomingWyomingWyomingWyoming

Exempla Saint Joseph Hospital, Denver

Lovelace Health System, Albuquerque

Oklahoma Heart Hospital, Oklahoma City

Hillcrest Medical Center, Tulsa

Baptist Health System, San Antonio

2008… Then Along Came “ACE”

22

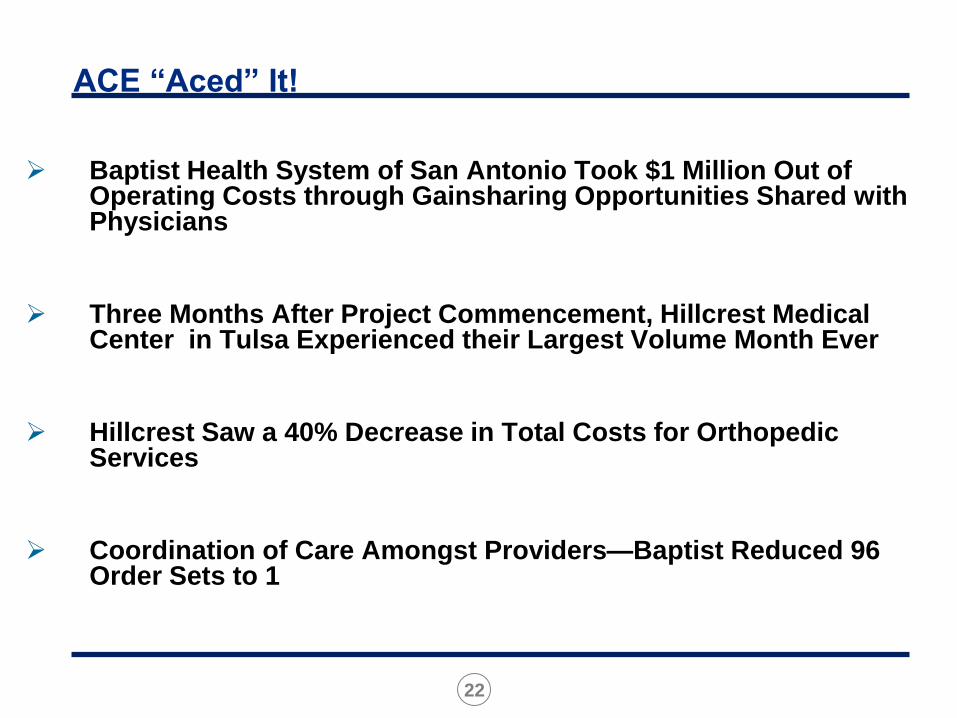

ACE “Aced” It!

Baptist Health System of San Antonio Took $1 Million Out of Operating Costs through Gainsharing Opportunities Shared with Physicians

Three Months After Project Commencement, Hillcrest Medical Center in Tulsa Experienced their Largest Volume Month Ever

Hillcrest Saw a 40% Decrease in Total Costs for Orthopedic Services

Coordination of Care Amongst Providers—Baptist Reduced 96 Order Sets to 1

23

Hospital

A

Hospital

B

Hospital

C

Hospital

D

CMS

Volume/Market

Share

Cost Reduction

Physician

Alignment

Quality

Would you do

it again?

Yes Yes Yes Yes Yes

23

Source: TRG interpretations of verbal and written surveys and CMS publications

Overall Positive ACE Results

24

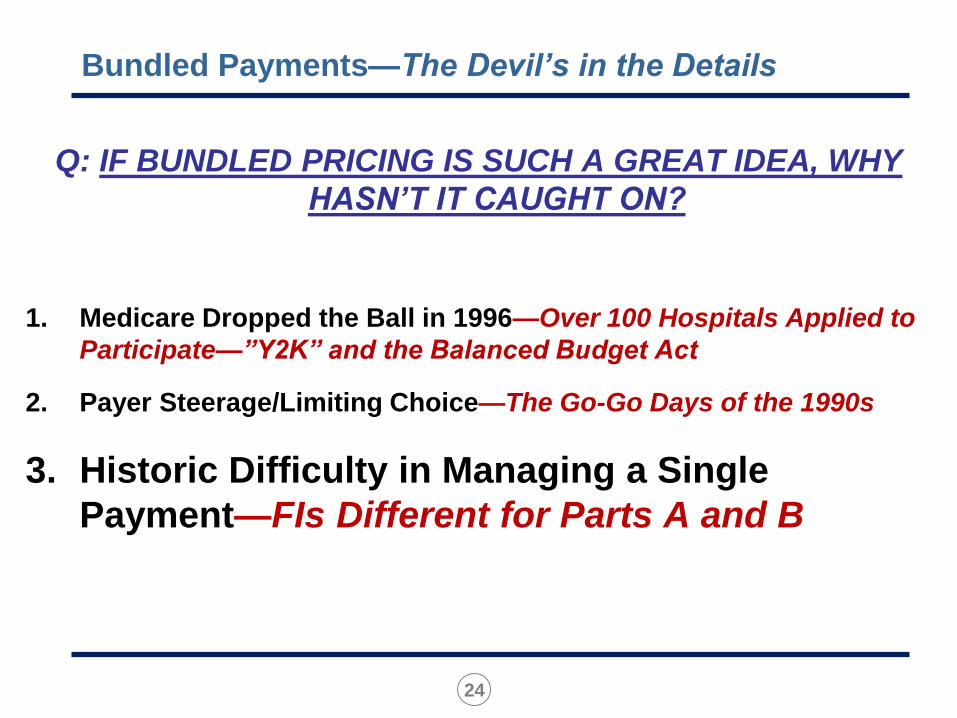

Q: IF BUNDLED PRICING IS SUCH A GREAT IDEA, WHY

HASN’T IT CAUGHT ON?

1. Medicare Dropped the Ball in 1996—Over 100 Hospitals Applied to

Participate—”Y2K” and the Balanced Budget Act

2. Payer Steerage/Limiting Choice—The Go-Go Days of the 1990s

3. Historic Difficulty in Managing a Single

Payment—FIs Different for Parts A and B

Bundled Payments—The Devil’s in the Details

25

BUNDLED PRICE

ALL“CONSULTING” PHYSICIAN

REIMBURSEMENT

$$$

HOSPITAL REIMBURSEMENT

$$$

“CORE” PHYSICIAN REIMBURSEMENT

$$$

Bundled Payments—Traditional “Prospective” Model

26

Medicare “Cracks the Code” on Bundled Payment Methodology

27

2011- Bundled Payments for Care Improvement (BPCI)

Open to ALL Hospitals Across the Country

Enabled Non-Hospital Entities to participate (e.g. Physicians, Remedy, naviHealth, etc.)

Select from 48 “Episodes” Consisting of 181 MS-DRGs

Four Possible Participation Models; 3 of Which Include Significant Post-Operative Care

Common Discount Percentage

No Market Exclusivity

No Savings Payment to Beneficiaries but Physicians Eligible to Earn 50% Above Medicare FFS through Gainsharing

3 of 4 Models are RETROSPECTIVE with Spend Reconciliation—i.e. All Providers Bill and Collect as Normal

28

2011- Bundled Payments for Care Improvement (BPCI)

3 Year Voluntary Program—4 Models; Over 1500 Participants

Model 2 is the Most Inclusive BPCI Model

Includes Acute A&B, 90-Day Post-Discharge “Related Readmissions” and Virtually All Post-Acute Expenditures Except Hospice

Participants Agree to Reduce Medicare’s Historical Spend by 2% Overall

If Successful in Reducing Below the 2% Discounted Target Price, Participants Retain Savings

If Unsuccessful, Participants Owe CMS the 2% Plus Any Overages

BPCI Model 2 Gave Impetus and Birth to CJR

29

Bundled Payments for Care Improvement (BPCI) Initiative

BPCI Initiative: Model 1

Total number of Participants:11

BPCI Initiative: Model 2

Total number of Participants: 628

BPCI Initiative: Model 3

Total number of Participants:859

BPCI Initiative: Model 4

Total number of Participants:9

30

BPCI Model 2 Target Pricing…The Black Box

31

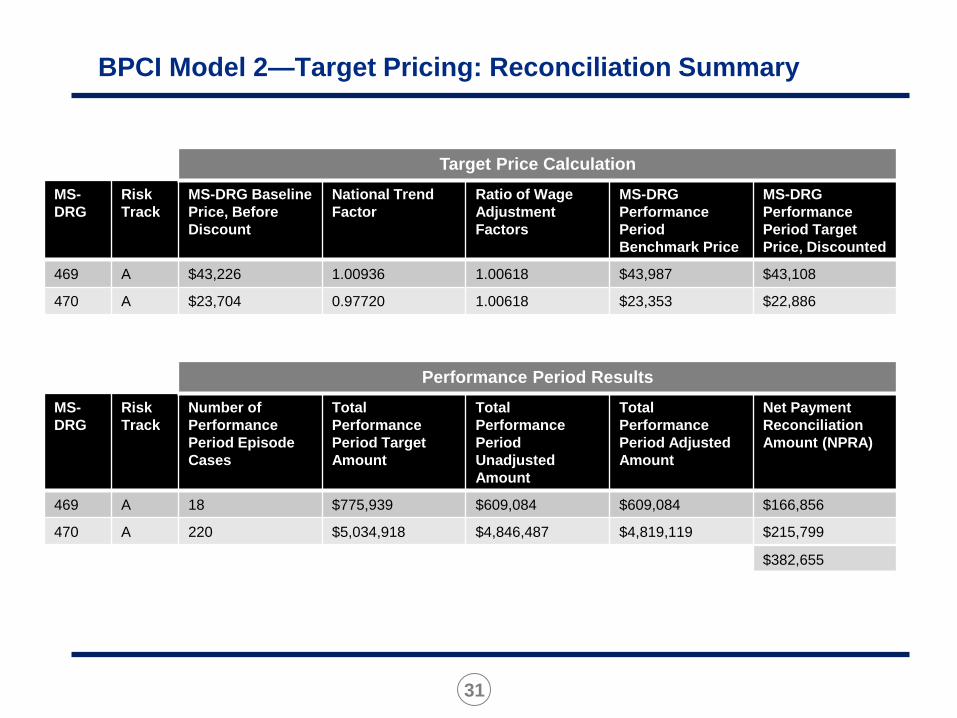

BPCI Model 2—Target Pricing: Reconciliation Summary

MS-

DRG

Risk

Track

MS-DRG Baseline

Price, Before

Discount

National Trend

Factor

Ratio of Wage

Adjustment

Factors

MS-DRG

Performance

Period

Benchmark Price

MS-DRG

Performance

Period Target

Price, Discounted

469 A $43,226 1.00936 1.00618 $43,987 $43,108

470 A $23,704 0.97720 1.00618 $23,353 $22,886

MS-

DRG

Risk

Track

Number of

Performance

Period Episode

Cases

Total

Performance

Period Target

Amount

Total

Performance

Period

Unadjusted

Amount

Total

Performance

Period Adjusted

Amount

Net Payment

Reconciliation

Amount (NPRA)

469 A 18 $775,939 $609,084 $609,084 $166,856

470 A 220 $5,034,918 $4,846,487 $4,819,119 $215,799

Target Price Calculation

Performance Period Results

$382,655

32

BPCI Model 2: Target Price Construction: Baseline Trending

• Historical claims data captures admissions from July 2009 – June

2012 for eligible* BPCI patients

Eligible BPCI patients are traditional Medicare Fee-for-service beneficiaries that must

be enrolled in both Parts A and B, must not be enrolled in a Medicare Advantage plan,

must not have End Stage Renal Disease, and must not have Medicare as a secondary

payer

• Trend earlier two years of data to be in terms of 2012 dollars

• Winsorize payments using trim points for the selected Risk Track

• Apply low volume adjustments

• Apply national case mix indices

MS-

DRG

Risk

Track

MS-DRG Baseline

Price, Before

Discount

National Trend

Factor

Ratio of Wage

Adjustment

Factors

MS-DRG

Performance

Period Benchmark

Price

MS-DRG

Performance

Period Target

Price, Discounted

469 A $43,226 1.00936 1.00618 $43,987 $43,108

470 A $23,704 0.97720 1.00618 $23,353 $22,886

Target Price Calculation

33

BPCI Model 2: Target Price Construction: National Trend Factor

• National Trend Factor, as defined by CMS:

“i.e. changes in MS-DRG mean episode payments for all episodes nationally between

the performance quarter and the baseline period, which capture health care market

basket changes1, policy changes2, and secular trends3 that affect service volume and

prices nationally”

For Example…

1. MS-DRG Payment Changes

2. Sequestration

3. National Utilization Changes

MS-

DRG

Risk

Track

MS-DRG Baseline

Price, Before

Discount

National Trend

Factor

Ratio of Wage

Adjustment

Factors

MS-DRG

Performance

Period Benchmark

Price

MS-DRG

Performance

Period Target

Price, Discounted

469 A $43,226 1.00936 1.00618 $43,987 $43,108

470 A $23,704 0.97720 1.00618 $23,353 $22,886

Target Price Calculation

34

BPCI Model 2: Target Price Construction: Wage Adjustment Factors

• Ratio of Wage Adjustment Factors

The baseline price gets adjusted either up or down depending on what has happened

to the wage indices at the hospitals that you practice at; CMS does not want to

artificially penalize/reward you for changes in area wages.

MS-

DRG

Risk

Track

MS-DRG Baseline

Price, Before

Discount

National Trend

Factor

Ratio of Wage

Adjustment

Factors

MS-DRG

Performance

Period Benchmark

Price

MS-DRG

Performance

Period Target

Price, Discounted

469 A $43,226 1.00936 1.00618 $43,987 $43,108

470 A $23,704 0.97720 1.00618 $23,353 $22,886

Target Price Calculation

Performance

Period Wage

Factor

0.99662

2012 Wage Factor

0.99050

Ratio of Wage

Adjustment

Factors

1.00618

35

BPCI Model 2: Target Price Calculation: Winsorization

How Medicare Adjusts for Risk

• Participants selected from three risk tracks, each having a unique lower and upper

threshold

• Threshold values are established utilizing the distribution of episode payments

nationally

• Payments below the lower threshold will be brought up to equal the lower threshold

for calculation purposes

• Payments above the upper threshold will be brought down to equal the upper

threshold, plus 20% of the difference between the threshold and the actual payment

• Both the baseline and the performance period episode payments are adjusted

1st %tile

99th %tile

5th %tile

95th %tile

5th %tile

75th %tile

Highest Risk/Opportunity ------------------------- Lowest Risk/Opportunity

A B C

36

BPCI Model 2: Target Price Construction: The True-Up Process

When does it occur?

• Each quarter is “trued-up” three times after the originally released

reconciliation; quarterly results are not considered final until the third true-up

What can change?

• Trend factors, winsorization trim points, and performance period total spend

are all recalculated

• Episodes can potentially fall out of the program (e.g. if a patient enrolls in a

Medicare Advantage plan)

• Additional claims can be processed

Performance

Period Quarter

Original

ReconciliationFirst True-Up

Second True-

UpFinal True-up

Q2 2015 January 2016 April 2016 July 2016 October 2016

Q3 2015 April 2016 July 2016 October 2016 January 2017

Q4 2015 July 2016 October 2016 January 2017 April 2017

37

• All IPPS hospitals within the 67

selected MSAs (approx. 800 hospitals)

• The selection process utilized a

stratified random sampling

methodology of all MSAs with the

following exclusions:

1. MSAs with less than 400 LEJR

episodes

2. MSAs with less than 400 non-BPCI

LEJR episodes

3. MSAs with greater than 50% of eligible

CJR episodes currently in Phase 2 of

BPCI

4. MSAs with greater than 50% of eligible

CJR episodes not paid under IPPS

2016: CJR: Required—i.e. MANDATED—Participants

38

The Basics of CJR

Defining CJR • CJR is a mandatory bundled payment program for

Lower Extremity Joint Replacement episodes, as

initiated by MS-DRGs 469-470 (unlike BPCI,

consideration is given for patients with fractures)

Program Timeframe • The program begins on April 1, 2016 and runs for

almost five years until December 31, 2020

Included Services • Services that occur during the anchor

hospitalization and spanning through 90 days

post-discharge

• Inpatient Hospital Services, Professional Services,

Readmissions, Skilled Nursing Facility, Inpatient

Rehab Facility, Long Term Care, Home Health,

Outpatient, Durable Medical Equipment, Hospice

Reconciliation • Annual retrospective reconciliation of Medicare’s

actual spend versus the target price

• Does not impact provider payments

39

The Basics of CJR

Target Price • Based on 3 year historical spend that blends

hospital-specific performance with a regional

average

• Discount between 1.5% - 3.0% depending on a

hospital’s quality composite score

• Hospitals will know the Target Price in advance—

unlike BPCI

Quality • Quality performance is required to be eligible for a

reconciliation payment

• Includes 2 mandatory metrics:

THA/TKA Complication Rate

HCAHPS

Risk Protection • CMS has implemented stop-loss and stop-gain

limits on aggregate NPRA to minimize risk

Stop Gain: 5%, 5%, 10%, 20%, 20%

Stop Loss: 0%, 5%, 10%, 20%, 20%

Waivers • Allow for gainsharing arrangements with

physicians and other providers

40

“We propose to calculate (CJR) episode target prices using a blend of hospital-specific and regional historical average (CJR) episode payments, including (CJR) episode payments for all (CJR) eligible hospitals in the same U.S. Census division…”

Page 119, CMS-5516-P

The Big Difference Between BPCI and CJR

If a hospital has historically been lower than the region, the hospital will be rewarded as they are measured against a target price that has been inflated by the regional experience.

If a hospital has historically been higher than the region, the hospital will be penalized as they are measured against a target price that has been deflated by the regional experience.

Years 1 and 2: 2/3 Hospital, 1/3 Regional

Year 3: 1/3 Hospital, 2/3 Regional

Years 4 and 5: 100% Regional

…and the Target Price baseline will be

updated every two years to a more recent

3-year period (i.e. 3 baselines throughout CJR)

41

Are Bundled Payments the Future?

COPD?

CHF?

CABG?Fee-for-

Service?

42

Are Bundled Payments the Future?

“Being an ally of the United States is like

living on the banks of an enormous river. The soil

is wonderfully fertile but every four or eight years

the river changes course and you may find yourself

alone in a desert.”

—Muhammad Zia-ul-Haq

President of Pakistan 1978-1988

43

Are Bundled Payments the Future?

CMS Pays the Bills for 1 out of Every 3 People in the United States

44

Providers Unable to Successfully Manage the Episode Will Be

Pushed Out of the Game

CMMI Initiatives Commercial Direct to Employer Future PredictionACE = Acute Care Episode; BCBS = Blue Cross and Blue Shield; CalPERS = California Public Employees’ Retirement System;

CJR = Comprehensive Care for Joint Replacement; CJRI = Connecticut Joint Replacement Institute; TJR = total joint replacement.

Kroger designates 19

hospitals for total joint

replacement

Walmart

partners with

hospitals for

spine surgery

General Electric

pursues direct

contracting

strategy. 4 Centers

designated for TJR

National

Orthopaedic &

Spine Alliance

CalPERS

reference pricing

Bundled

Payments

for Care

Improvement

initiative

CMS

proposes and

finalizes CJR rule

Bundles are

the default

reimbursement for

Medicare TJR.

ACE

demonstration

Anthem BCBS of MO

and SSM Health Care

Duke and

BCBS of NC

CJRI and

ConnectiCare

NC Specialty

Hospital and

BCBS of NC

Florida Ortho Institute

and Florida Blue

2011 2012 2013 2014 20192015 2016 2017 2018201020092008

Innovation Escalates

CCF Creates National Heart

Network. Targets 24 sites for

bundled pmt contracting

BPCI is extended for

2 add’l years

45

Current Private Payor Bundled Payment Initiatives

46

How to Prepare for a Bundled Future

• Begin Changing Mindset and Focus—No Longer Volume per se

• Participate in any Bundled Opportunities—Look Local!

• Look Beyond the Four Walls of the Hospital to Establish Relationships with

High Quality, Efficient Providers

• If You Have Employed or Contracted Physicians on a wRVU Model, Evaluate

Other Structures

• Begin Sharing Relevant Data with Physicians

• Determine Who Efficient, High Quality Physicians Are

• ENGAGE YOUR PHYSICIANS!!

47

CASE STUDY: BPCI Model 2: SIGNATURE MEDICAL GROUP

Awardee Convener CMS Bundled Payments for Care Improvement (BPCI)

Convener for Largest Orthopedic Bundled Payment Initiative

48

CASE STUDY: BPCI MODEL 2; SIGNATURE MEDICAL GROUP

49

CASE STUDY: BPCI MODEL 2; SIGNATURE MEDICAL GROUP

PARTICIPATING ORTHOPEDIC GROUPS IN 26 STATES & OVER 60 CITIES

50

CASE STUDY: BPCI MODEL 2; SIGNATURE MEDICAL GROUP—

RESULTS Q1 and Q2 of 2015

• Readmissions Reduced – 12 to 70%

• SNF Unnecessary Utilization Reduced – 10 to 50%

• IRF Unnecessary Utilization Reduced – 30 to 80%

• Average Patient Satisfaction Scores over 97%

• Selected Quality measures achieved and frequently surpassed

• Average ICS Savings (Implant Costs BPCI Cases Only) : $887 per

Case

– Note: Physician Gainsharing Maximum Approximately $700 per Case

• Top Performing SMG Groups Have Reduced Episode PAC

Spend Between $2750 and $3750 per Case

51

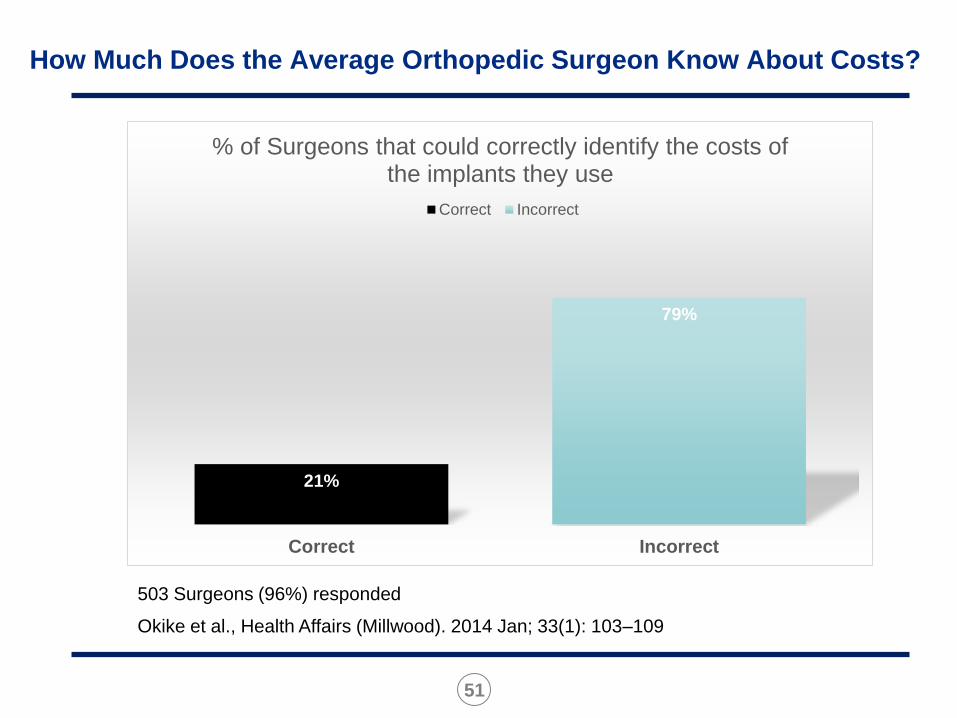

Okike et al., Health Affairs (Millwood). 2014 Jan; 33(1): 103–109

503 Surgeons (96%) responded

21%

79%

Correct Incorrect

% of Surgeons that could correctly identify the costs of the implants they use

Correct Incorrect

How Much Does the Average Orthopedic Surgeon Know About Costs?

52

The Art of Anticipation

53

“I skate to where the

puck is going to be,

not to where it is.”

--Wayne GretzkyAll-Time NHL Point Leader

The Art of Anticipation