china’s changing net trade position in seafood and … rabobank: globally leading food and...

TRANSCRIPT

China’s changing net trade position in seafood and implications

Dr. Beyhan de JongReykjavik, November 2017

The Dragon’s changing appetite

Toronto

New York

Mexico City

Sao Paulo

Buenos Aires SydneySantiago de Chile

Willemstad

Calgary

Washington DC

Chicago

Atlanta

DallasEl Centro

San Francisco

Tasmania

Melbourne

Wellington

Cedar Falls

St Louis London

Madrid

Milan

AntwerpFrankfurt

Warsaw

Utrecht

Hong Kong

Singapore

Mumbai

Kolkata

Jakarta

Tokyo

Beijing

Delhi

Kuala Lumpur

Moscow

Istanbul

Dublin

Lubuan

Amsterdam

Paris

Bangalore

Shanghai

MaputoChimoio

Beira

Tete

Ulónguè

Malema

Maxixe

Nampula

Kigali

Asuncion

46 Countries Over 600 Offices Over 55,000 Employees

Rabobank: Globally leading food and agribusiness lender and financial services provider

In volume terms China’s seafood consumption dwarfs that of the western countries

Source: OECD-FAO, Rabobank 2017

0

10

20

30

40

50

60

70

80

North America Europe Africa Latin America & Caribbean China Asia excl. China

Million tonnes2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

China has a high seafood consumption, estimated at 44 kg per person, which is forecasted to reach 50 kg in 2026

35% of global consumption

1

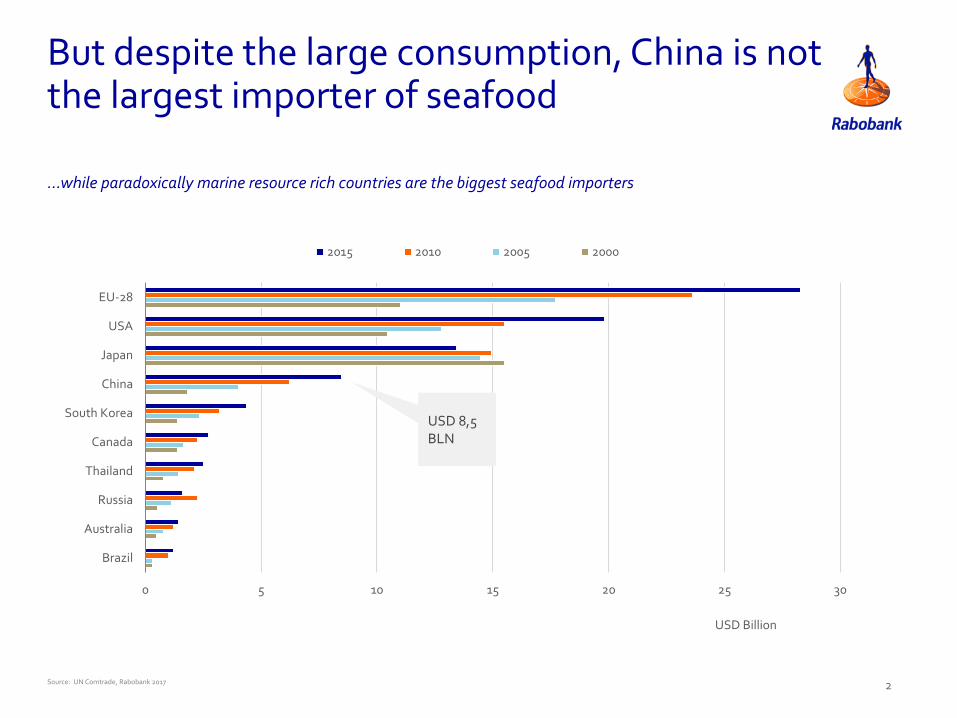

But despite the large consumption, China is not the largest importer of seafood

…while paradoxically marine resource rich countries are the biggest seafood importers

0 5 10 15 20 25 30

Brazil

Australia

Russia

Thailand

Canada

South Korea

China

Japan

USA

EU-28

USD Billion

2015 2010 2005 2000

Source: UN Comtrade, Rabobank 2017

USD 8,5 BLN

2

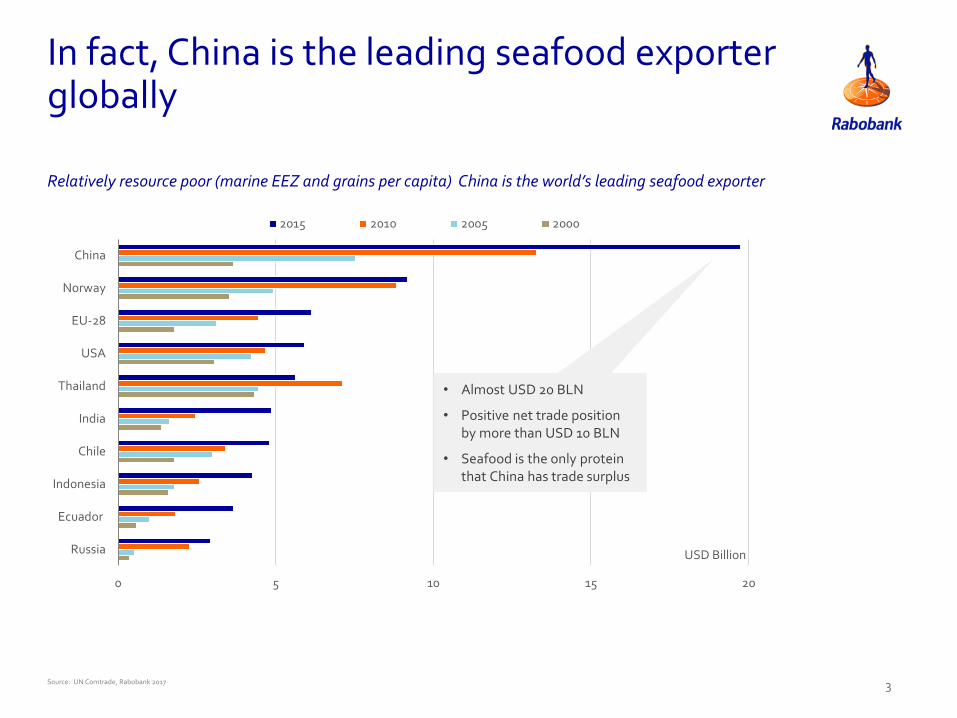

In fact, China is the leading seafood exporter globally

Source: UN Comtrade, Rabobank 2017

Relatively resource poor (marine EEZ and grains per capita) China is the world’s leading seafood exporter

0 5 10 15 20

Russia

Ecuador

Indonesia

Chile

India

Thailand

USA

EU-28

Norway

China

USD Billion

2015 2010 2005 2000

• Almost USD 20 BLN

• Positive net trade position by more than USD 10 BLN

• Seafood is the only protein that China has trade surplus

3

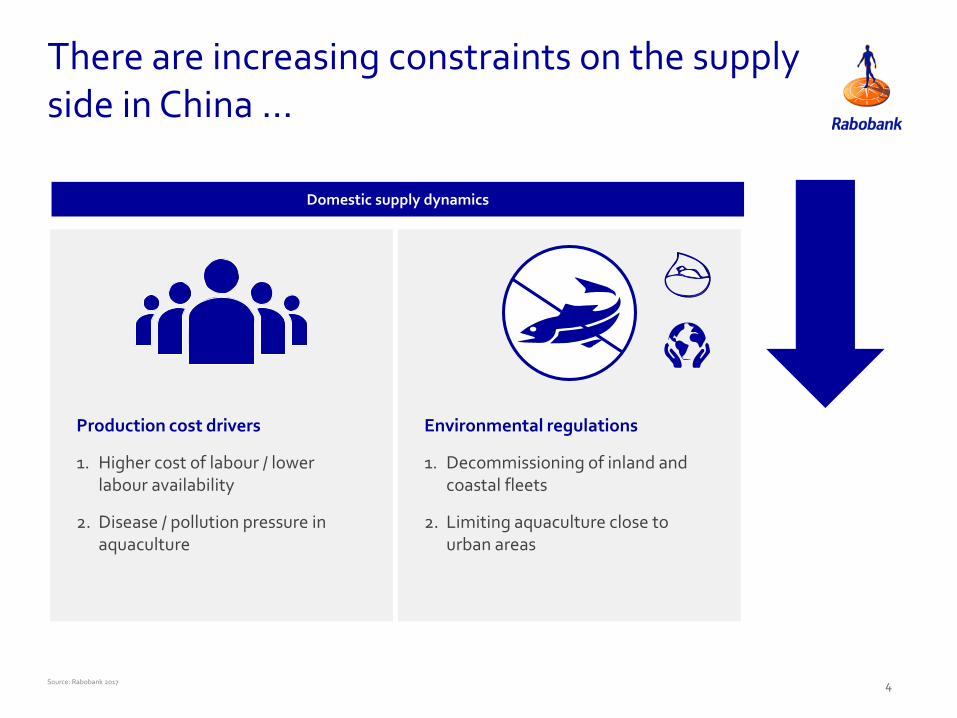

Domestic supply dynamics

Production cost drivers

1. Higher cost of labour / lower labour availability

2. Disease / pollution pressure in aquaculture

Environmental regulations

1. Decommissioning of inland and coastal fleets

2. Limiting aquaculture close to urban areas

There are increasing constraints on the supply side in China …

Source: Rabobank 2017 4

Import demand drivers

1. Income growth and strong currency

2. Distrust of locally produced seafood (due to pollution and scandals)

Import enablers

1. On-line seafood trade

2. Improving logistical infrastructure / urbanisation

Import demand dynamics

…while the drivers on the demand side accelerate import demand

Source: Rabobank 2017 5

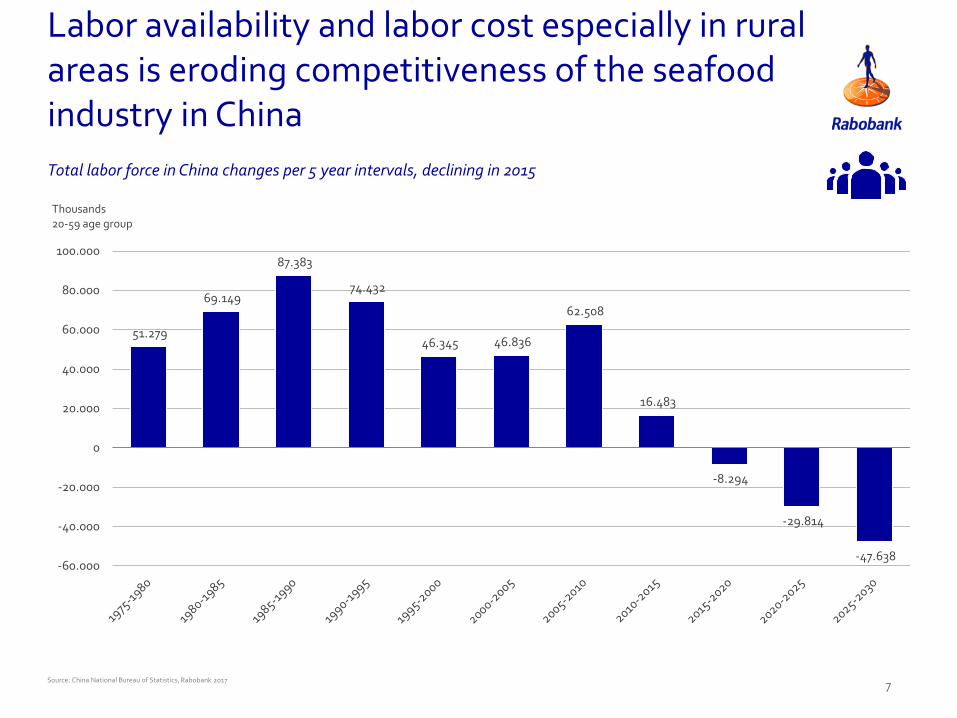

Domestic seafood supply to stagnate or

contract

Source: China National Bureau of Statistics, Rabobank 2017

51.279

69.149

87.383

74.432

46.345 46.836

62.508

16.483

-8.294

-29.814

-47.638 -60.000

-40.000

-20.000

0

20.000

40.000

60.000

80.000

100.000

Thousands20-59 age group

Total labor force in China changes per 5 year intervals, declining in 2015

Labor availability and labor cost especially in rural areas is eroding competitiveness of the seafood industry in China

7

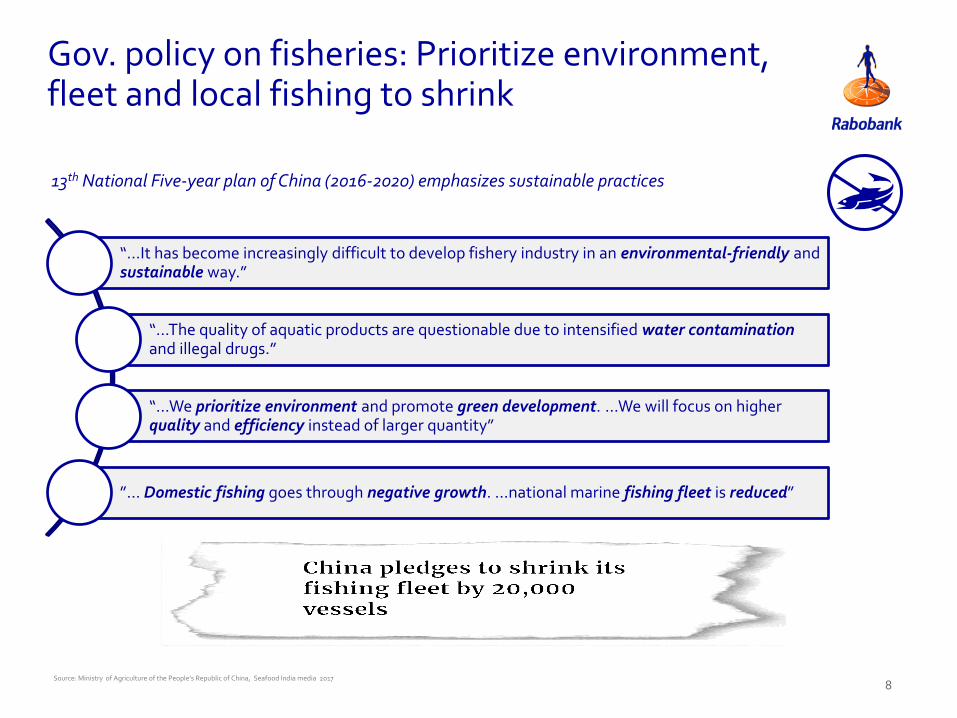

Gov. policy on fisheries: Prioritize environment, fleet and local fishing to shrink

Source: Ministry of Agriculture of the People’s Republic of China, Seafood India media 2017

“…It has become increasingly difficult to develop fishery industry in an environmental-friendly and sustainable way.”

“…The quality of aquatic products are questionable due to intensified water contamination and illegal drugs.”

“…We prioritize environment and promote green development. …We will focus on higher quality and efficiency instead of larger quantity”

”… Domestic fishing goes through negative growth. …national marine fishing fleet is reduced”

13th National Five-year plan of China (2016-2020) emphasizes sustainable practices

8

0

10

20

30

40

50

60

70

80

Million tonnes

Wild catch Marine Farmed Freshwater Farmed

Overall we expect Chinese seafood production to experience a gradual decline, after years of growth

Source: China National Bureau of Statistics, OECD-FAO, Rabobank 2017

China’s wild catch production is expected to decline as targeted in the latest fisheries policy

• Next five year plan targets a decrease in total seafood production from 67 million tonnes to 66 million.

• Domestic wild catch (inland and near coastal areas) to be decreased and aquaculture to be increased.

• By using modern technologies and intensive farming, aquaculture is targeted to be increased.

9

Import demand to grow faster than ever before

-3%

-9%

-24%

-31%

-44%

-22%

-19%

-3%

-50%

-40%

-30%

-20%

-10%

0%

2013-2017 currency change

Thai Baht Indian Rupee Mexican Peso Brazilian Real Russian Ruble Indonesian Rupiah Chilean Peso Vietnamese Dong

Nearly all developing countries have had devaluating currencies vs the Chinese Yuan, impacting competitiveness

Source: Bloomberg, Rabobank 2017

Weak currency is no longer a key gov. policy in China

Value of developing country currencies vs the Chinese Yuan 2013 September vs. 2017 September

11

0%

3%

6%

9%

12%

15%

18%

21%

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Urban Disposable Income per capita (RMB) Growth Rate

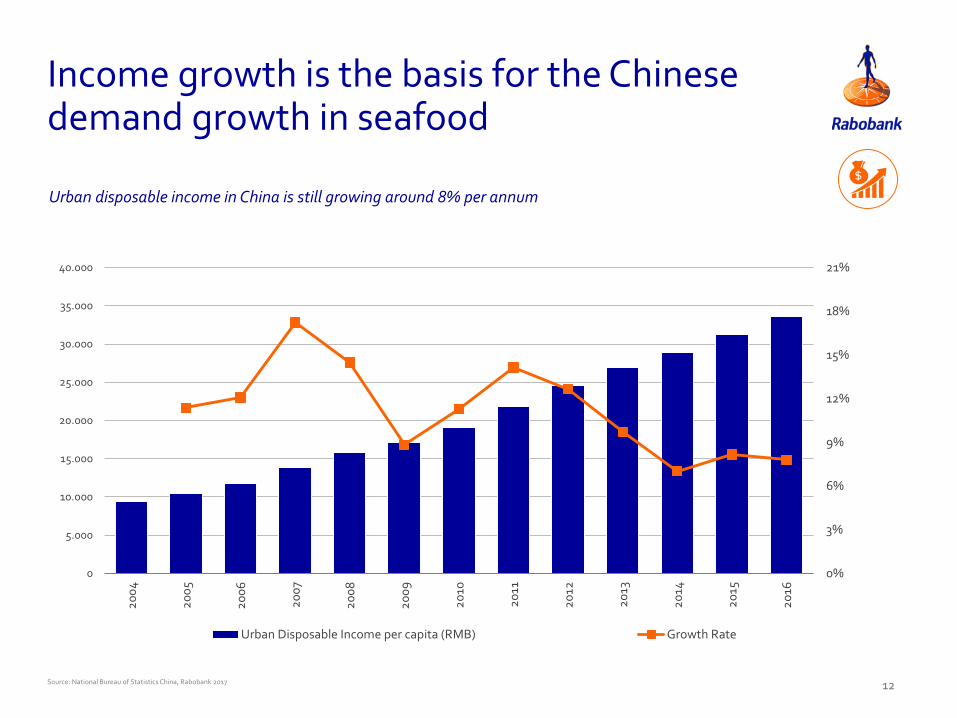

Income growth is the basis for the Chinese demand growth in seafood

Source: National Bureau of Statistics China, Rabobank 2017

Urban disposable income in China is still growing around 8% per annum

12

4%

5%

6%

7%

8%

12%

14%

16%

18%

20%

22%

24%

Lowest Low Lower Middle Middle Upper Middle High Highest

Seafood expenditure shareMeat expenditure share

Meat, Poultry and Processed Products (LHS) Aquatic Products (RHS)

The demand growth is accelerated by a high income elasticity of seafood demand in China

Source: National Bureau of Statistics, Nielsen, BCG, Rabobank 2017

Share of seafood (right) and meat (left) expenditure increases per income group

13

Source: Euromonitor; Iresearchchina, Rabobank 2017

0

1.000

2.000

3.000

4.000

5.000

6.000

2012 2013 2014 2015 2016 2017e 2018f

Retail fresh food sales (RMB bln) Online fresh food sales (RMB bln)

14

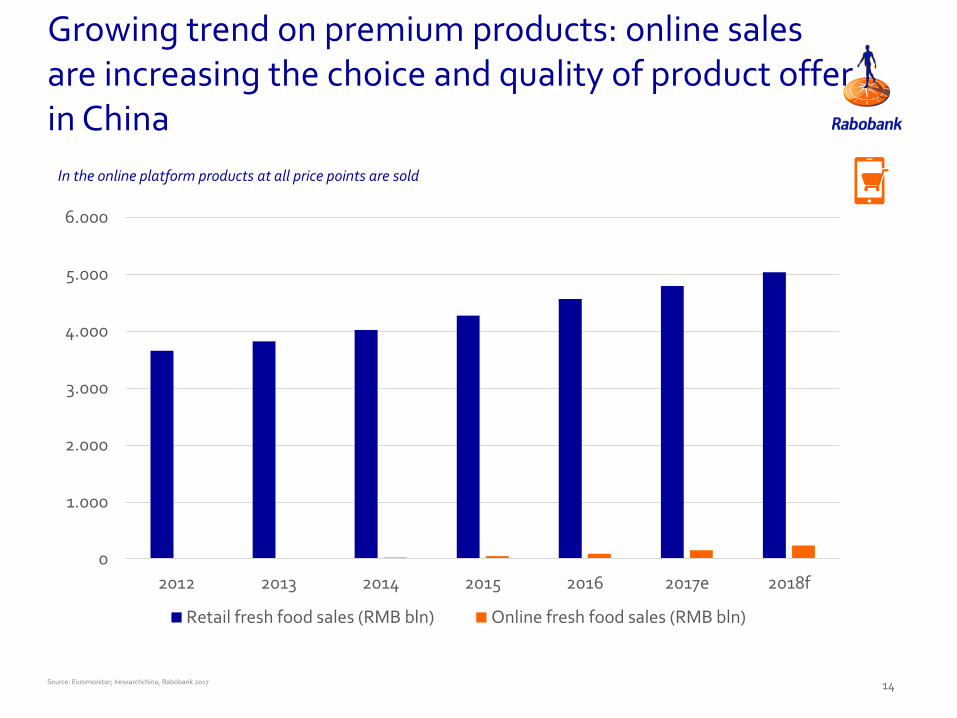

Growing trend on premium products: online sales are increasing the choice and quality of product offer in China

In the online platform products at all price points are sold

Source: Euromonitor; Iresearchchina, Rabobank 2017

0

50

100

150

200

250

2012 2013 2014 2015 2016 2017e 2018f

Online fresh food sales (RMB bln)

Online value proposition of seafood in China:

Variety

Convenience / delivery

Information

No crowds

Food safety

Authenticity

15

Seafood is the second most sold food category on the online market after imported fruits

RMB 237 BLN = USD 35 BLN

+82%

RMB 153 BLN = USD 23 BLN

Imported seafood sales are rapidly increasing through e-commerce

Source: JD, Tmall, Gfresh, Rabobank 2017

Tmall - largest B2C platform in China JD has the largest e-commerce logistics

infrastructure in China • By November 8th, 263 pages with 60 seafood items per page

• New seafood listings everyday

• 198 million active users in 2016

17

0

200

400

600

800

1.000

1.200

1.400

1.600

2015 2016 2017 e 2018 f

Sales in USD million

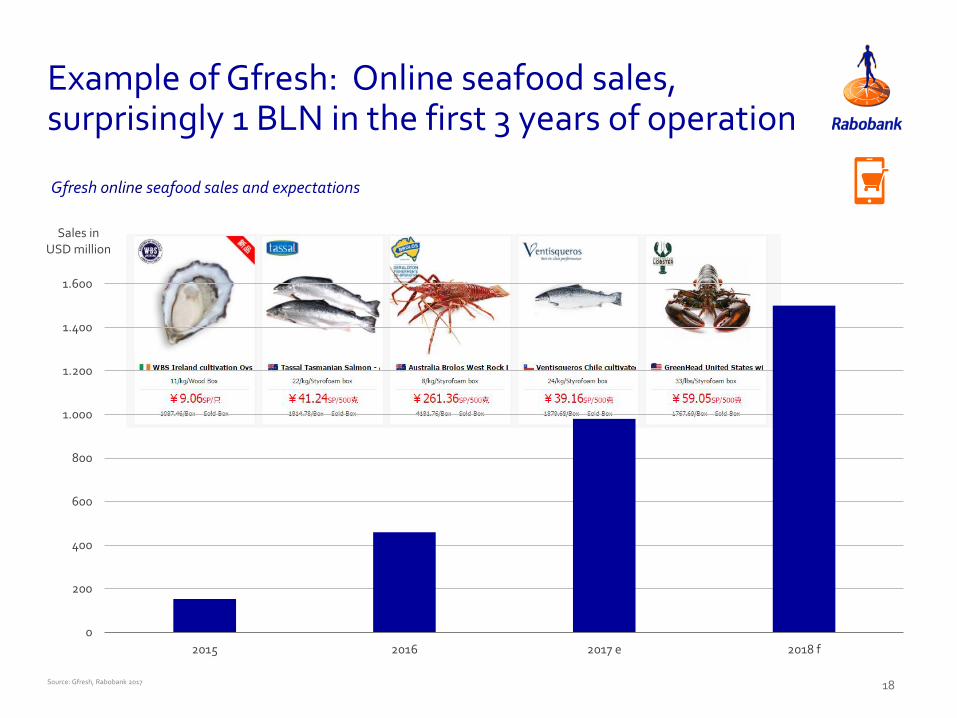

Example of Gfresh: Online seafood sales, surprisingly 1 BLN in the first 3 years of operation

Source: Gfresh, Rabobank 2017

Gfresh online seafood sales and expectations

18

Still China can be very challenging especially for trade of frozen and chilled seafood

Source: China Bureau of Statistics, GCCA, Rabobank, 2017

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e 2017f 2018f 2019f 2020f

Storage capacity in China Number of refrigirated vehicles

Million m3 / ‘000 Vehicles

Cold chain infrastructure is growing by 15-30% p.a. in China – major changes are occurring, partly driven by

online retailers

19

Implications: New seafood consumers in China

and perhaps new East-West partnerships

Having at least one of these features seems to be the recipe for success in the Chinese seafood market (but there are exceptions)

Source: Rabobank 2017

Marine

Crustaceans

Wild Caught

Marine

• Marine fish is perceived as healthier than fresh water fish

• China currently has relatively low availability of marine seafood

Premium

• Especially on-line and in modern retail premium products are ordered and are often imported

• Most locally produced products are sold on wet markets and are not premium

Crustaceans

• Cultural preference for shell fish

• Huge range of products already known to Chinese consumers

Wild Caught

• Wild seafood is perceived as heathier than farmed

• In China far less available thanelsewhere in the world

Premium

21

0

200

400

600

800

1.000

1.200

EU US China

tonnes

Thousands

2010 2011 2012 2013 2014 2015 2016 2017e

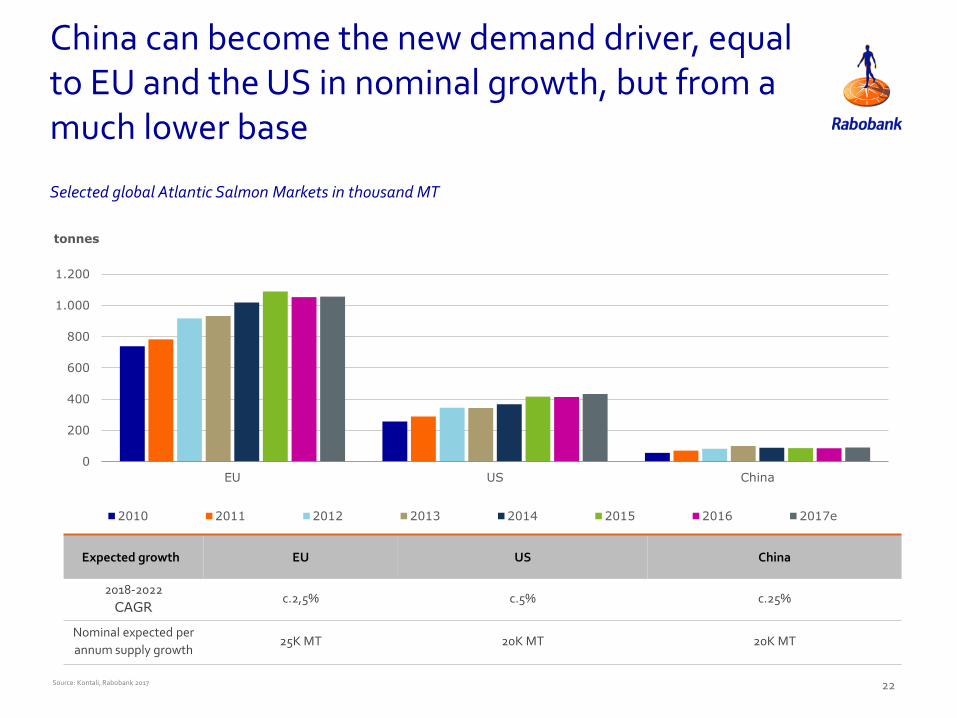

Source: Kontali, Rabobank 2017

Selected global Atlantic Salmon Markets in thousand MT

Expected growth EU US China

2018-2022

CAGRc.2,5% c.5% c.25%

Nominal expected per

annum supply growth25K MT 20K MT 20K MT

China can become the new demand driver, equal to EU and the US in nominal growth, but from a much lower base

22

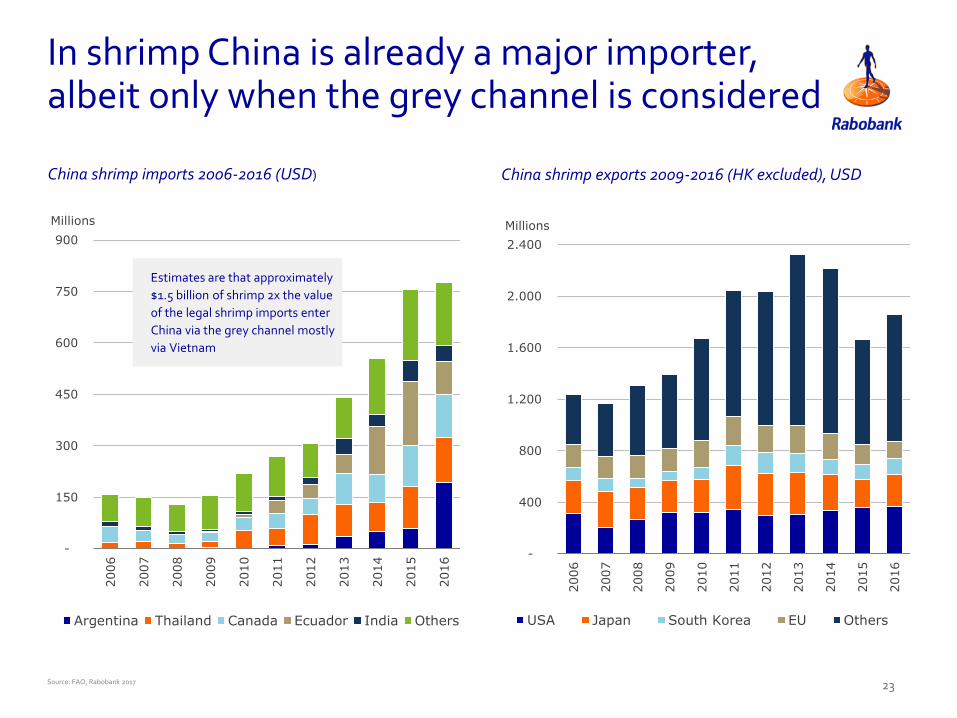

In shrimp China is already a major importer, albeit only when the grey channel is considered

China shrimp exports 2009-2016 (HK excluded), USD

Source: FAO, Rabobank 2017

China shrimp imports 2006-2016 (USD)

-

150

300

450

600

750

900

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Millions

Argentina Thailand Canada Ecuador India Others

-

400

800

1.200

1.600

2.000

2.400

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Millions

USA Japan South Korea EU Others

Estimates are that approximately

$1.5 billion of shrimp 2x the value

of the legal shrimp imports enter

China via the grey channel mostly

via Vietnam

23

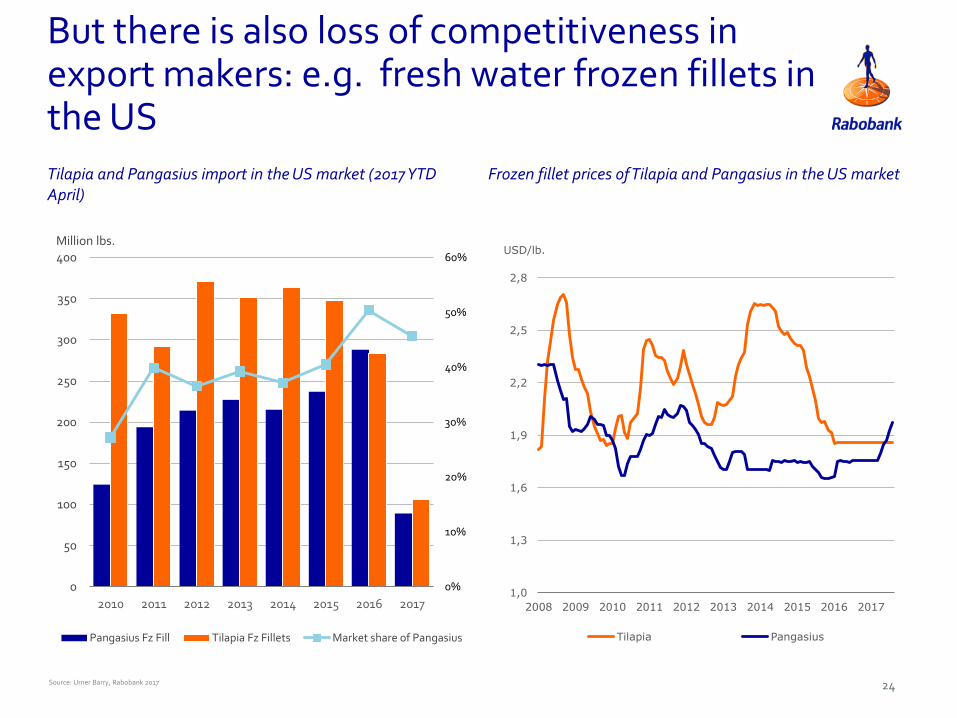

But there is also loss of competitiveness in export makers: e.g. fresh water frozen fillets in the US

Frozen fillet prices of Tilapia and Pangasius in the US marketTilapia and Pangasius import in the US market (2017 YTD April)

Source: Urner Barry, Rabobank 2017

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015 2016 2017

Million lbs.

Pangasius Fz Fill Tilapia Fz Fillets Market share of Pangasius

1,0

1,3

1,6

1,9

2,2

2,5

2,8

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

USD/lb.

Tilapia Pangasius

24

0

50

100

150

200

250

300

350

400

450

2012 2013 2014 2015 2016 2017E

Millions USD

And surpassingly in a few years China has become the No.1 market for Vietnamese pangasius

Source: UN Comtrade, VASEP, Rabobank 2017

Vietnamese pangasius exports to China in value

26

Why West to China M&A is not very likely

• Barriers: language, culture, business environment

• High Chinese value expectations

• Synergies are not always obvious

• JVs` are the current choice for cooperation

• E.g. Western seafood companies and on-line retailers

• E.g. Western and local technology aquaculture companies (e.g. feed)

M&A from West to China is not highly likely

Source: Bloomberg, Rabobank 2017

EV/EBITDA multiples in European and Chinese listed seafood companies

8.5x 8.5x

12.9x

18.0x

8.3x

5.9x

14.8x13.8x

11.5x

21.8x

18.4x

13.1x

36.8x

49.7x

13.2x

39.9x

58.0x

26.0x

7.1x

Europe average: 10.5x China average: 28.4x

7.3x

27

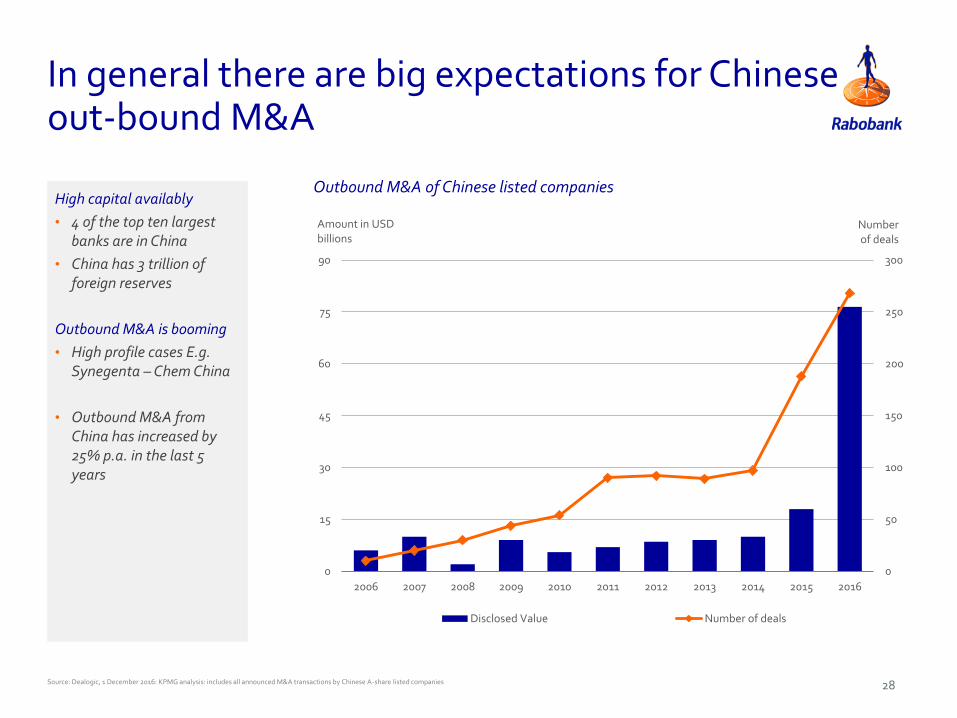

0

50

100

150

200

250

300

0

15

30

45

60

75

90

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Number of deals

Amount in USD billions

Disclosed Value Number of deals

Outbound M&A of Chinese listed companies

Source: Dealogic, 1 December 2016: KPMG analysis: includes all announced M&A transactions by Chinese A-share listed companies

In general there are big expectations for Chinese out-bound M&A

High capital availably

• 4 of the top ten largest banks are in China

• China has 3 trillion of foreign reserves

Outbound M&A is booming

• High profile cases E.g. Synegenta – Chem China

• Outbound M&A from China has increased by 25% p.a. in the last 5 years

28

China Marine Food Group Ltd Frosta

Source: Bloomberg, Rabobank 2017

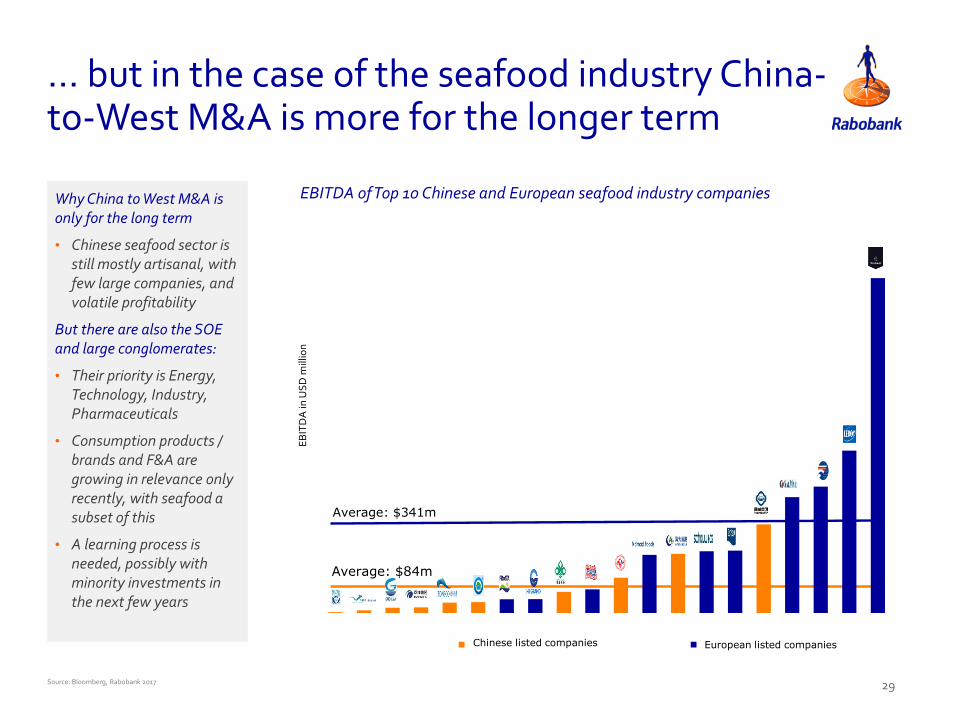

… but in the case of the seafood industry China-to-West M&A is more for the longer term

EBITDA of Top 10 Chinese and European seafood industry companies

Average: $84m

Average: $341m

EB

ITD

A in

US

D m

illio

n

Chinese listed companies European listed companies

Why China to West M&A is only for the long term

• Chinese seafood sector is still mostly artisanal, with few large companies, and volatile profitability

But there are also the SOE and large conglomerates:

• Their priority is Energy, Technology, Industry, Pharmaceuticals

• Consumption products / brands and F&A are growing in relevance only recently, with seafood a subset of this

• A learning process is needed, possibly with minority investments in the next few years

29

30

This document is meant exclusively for you and does not carry any right of publication or disclosure other than to Coöperatieve Rabobank U.A. (“Rabobank”), registered in Amsterdam. Neither this document nor any of its contents may be distributed, reproduced, or used for any other purpose without the prior written consent of Rabobank. The information in this document reflects prevailing market conditions and our judgement as of this date, all of which may be subject to change. This document is based on public information. The information and opinions contained in this document have been compiled or derived from sources believed to be reliable; however, Rabobank does not guarantee the correctness or completeness of this document, and does not accept any liability in this respect. The information and opinions contained in this document are indicative and for discussion purposes only. No rights may be derived from any potential offers, transactions, commercial ideas, et cetera contained in this document. This document does not constitute an offer, invitation, or recommendation. This document shall not form the basis of, or cannot be relied upon in connection with, any contract or commitment whatsoever. The information in this document is not intended, and may not be understood, as an advice (including, without limitation, an advice within the meaning of article 1:1 and article 4:23 of the Dutch Financial Supervision Act). This document is governed by Dutch law. The competent court in Amsterdam, the Netherlands has exclusive jurisdiction to settle any dispute which may arise out of, or in connection with, this document and/or any discussions or negotiations based on it. This report has been published in line with Rabobank’s long-term commitment to international food and agribusiness. It is one of a series of publications undertaken by the global department of RaboResearch Food & Agribusiness. ©2017 - All Rights Reserved.

Dr. Beyhan de JongAssociate Analyst Animal ProteinRabobank, Utrecht, The [email protected]