china power sector - credit suisse

TRANSCRIPT

KEY CONCLUSIONS

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

Equity Research China&Hong Kong

Utilities (Utilities CN (Asia))

29 April 2015

China Power Sector THEME

The Ideas Engine

series showcases

Credit Suisse’s unique

insights and investment ideas.

Please contact your

Sales person to

access the

supplemental

analysis behind this

report.

Reforms bite!

New game rules. Safety will become Rule No.1 when investing in the power generators

in the coming years amid China's aggressive push for power reforms. Our preliminary

analysis of market-based pricing in the recent primer report is now strengthened by the

four official documents issued in the past month. Without large demand recovery,

electricity will remain a seriously oversupplied commodity, and price war and consolidation

could pull the average ROE of national coal-fired IPPs from 17% in 2014 down to 10%

by 2020E. With 2Q15 earnings likely marking a meaningful inflection, we recommend

investors exit.

A painful process before gain. The IPPs tariffs could go down further after the recent

5% cut and IPPs' tariffs for direct supplied contracts in 2014 (10% lower on average) is a

very strong early signal of what market forces can do. China aims full liberalisation of power

pricing and when it happens, depressed tariffs could force the exit of uncompetitive smaller

units together with a large impairment (before full depreciation). Competitive survivors could

swell after consolidation but the process could take years and could be painful.

Safe waters in the storm. Meanwhile, investors should find much better visibility for

demand and prices in: (1) wind operators; (2) low-cost hydro power generators; and (3)

A-share listed local IPPs with protective schemes. Nuclear operators are no longer

attractive with rising uncertainty on utilisation and technology risks.

SELL the national IPPs. With valuation nearing a five-year high plus major industry

headwinds, we recommend investors to sell the national IPPs. We cut target prices and

ratings (Huadian-H) on lower sustainable ROEs and our top sells are Huaneng (both A/H)

and CR Power. We also downgrade CGN to UNDERPERFORM with an unjustified valuation

and rising nuclear earnings risks. Areas that are worth buying include wind operators, low-

cost hydro power generators and local power utilities (we are initiating on Jingneng and

Mengdian with an Outperform).

Structural ROE trend of the national IPPs

Source: Company data, Credit Suisse estimates

Switch to the safer sectors!

Source: Credit Suisse research

The report follows our China Utilities Reform Primer in March 2015

(click here)

RESEARCH ANALYSTS

Dave Dai, CFA

852 2101 7358

Ran Ma 852 2101 6653

18% 17% 16%

14%

11%

9% 10% 10%

6%

8%

10%

12%

14%

16%

18%

20%

2013 2014 2015E 2016E 2017E 2018E 2019E 2020E

IDEAS ENGINE SERIES

IDEAS ENGINE 2

China Power Sector

Focus charts

Figure 1: Slow demand scenario—utilisation trend would

continue to weaken without power reforms

Figure 2: Slow demand scenario—market reform can make

consolidation possible

Figure 3: IPPs with larger exposure to smaller units could

see greater shut-down risks

Source: CEIC, Credit Suisse estimates Source: CEIC, Credit Suisse estimates Source: Company data

Figure 4: Inner Mongolia enjoys better utilisation hours than the

national average

Figure 5: Forward P/B of national IPPs at five-year high despite

upcoming ROE pressure

Figure 6: Switch to the safer sectors!

Source: CEIC Source: Bloomberg, Credit Suisse estimates, excluding Datang Source: Credit Suisse research

The author of this report wishes to acknowledge the contributions made by Gary Zhou, an employee of Evalueserve Research Hong Kong Ltd, a third-party provider to Credit Suisse of

research support services.

5,031

5,294

4,9655,012

4,706

4,559

5,1025,043 5,085 5,130

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

2010 2011 2012 2013 2014

(Hours)

China Inner Mongolia

0%

4%

8%

12%

16%

20%

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

ROE (RHS)

0.8x Avg-1SD

0.6x Avg-2SD

1.0x Avg

1.2x Avg+1SD

1.4x Avg+2SD

(x)

IDEAS ENGINE 3

China Power Sector

Figure 7: Valuation summary

Name Ticker Rating Price TP Mkt cap P/E (x) P/B (x) Yield (%) ROE (%) %EPS CAGR

(US$ bn) 15E 16E 15E 16E 15E 16E 15E 16E 14-16E

China Wind power sector

Huaneng Renewables 0958.HK O 3.3 4.0 4.1 13.4 9.6 1.5 1.3 1.5 2.1 11.4 14.3 49.2

Longyuan Power 0916.HK O 9.7 11.5 10.0 14.8 11.9 1.7 1.5 1.3 1.7 12.0 13.5 42.7

China Datang Renewables 1798.HK O 1.3 1.5 1.2 17.0 11.5 0.7 0.6 0.6 0.9 4.0 5.6 n.a.

Huadian Fuxin Energy 0816.HK O 4.3 5.5 4.7 10.6 8.7 1.7 1.5 1.8 2.9 17.0 18.1 30.2

China Suntien Green Energy 0956.HK O 2.1 2.5 1.0 12.5 8.6 0.8 0.7 2.7 4.0 6.4 8.8 44.4

Simple average 13.7 10.1 1.3 1.1 1.6 2.3 10.2 12.1 41.6

China Hydro power sector

SDIC Power 600886.SS N 12.5 12.5 13.7 11.7 11.0 3.1 2.6 3.0 3.2 28.5 25.5 17.3

China Yangtze Power Co Ltd 600900.SS O 12.6 14.8 33.6 17.6 18.6 2.3 2.2 2.9 2.7 13.6 12.1 -1.7

Sichuan Chuantou Energy 600674.SS O 26.2 30.0 9.3 11.4 10.9 3.2 2.6 1.3 1.4 32.1 26.3 23.6

Simple average 13.6 13.5 2.9 2.5 2.4 2.4 24.7 21.3 13.0

China IPPs sector - A (Local)

Inner Mongolia Mengdian 600863.SS O 6.1 7.5 5.7 34.2 21.4 3.2 3.0 3.1 2.3 9.4 14.5 10.5

Jingneng Power 600578.SS O 8.1 10.0 6.0 17.6 18.2 2.4 2.2 2.0 1.9 14.1 12.5 -10.3

Simple average 26.0 19.9 2.8 2.6 2.5 2.1 11.8 13.5 0.1

China Nuclear sector

CGN Power 1816.HK U 4.5 3.4 26.3 26.3 22.8 3.0 2.7 1.3 1.5 11.7 12.5 11.9

China IPPs sector - H (National)

Datang International Power 0991.HK O 4.8 4.6 14.9 10.5 8.7 1.1 1.0 3.8 4.6 10.4 11.6 52.1

Huadian Power International 1071.HK U 8.7 6.4 11.9 11.0 12.3 1.7 1.6 3.7 3.3 16.6 13.6 -8.7

China Resources Power 0836.HK U 23.3 16.3 14.4 9.2 9.3 1.4 1.3 3.5 3.8 16.2 14.5 14.4

Huaneng Power International 0902.HK U 11.3 7.3 24.3 10.8 12.0 1.7 1.6 5.1 4.6 16.6 13.8 -0.3

Simple average 10.4 10.6 1.5 1.4 4.0 4.1 14.9 13.4 14.4

China IPPs sector - A (National)

Huadian Power International 600027.SS U 8.7 5.1 11.9 13.8 15.4 2.2 2.0 2.9 2.6 16.6 13.6 -8.7

Datang International Power 601991.SS U 7.9 3.7 14.9 21.6 18.1 2.2 2.0 1.9 2.2 10.4 11.6 52.1

Huaneng Power International 600011.SS U 11.0 5.8 24.3 13.1 14.6 2.1 2.0 4.2 3.8 16.6 13.8 -0.3

Simple average 16.2 16.0 2.1 2.0 3.0 2.9 14.5 13.0 14.4

China City Gas sector

China Gas Holdings Ltd 0384.HK O 14.3 17.5 9.2 18.0 14.3 3.4 2.9 1.3 1.7 20.2 21.6 25.2

Beijing Enterprises Holdings 0392.HK O 72.1 82.0 12.0 15.7 13.7 1.5 1.4 1.9 2.2 10.1 10.7 17.9

China Resources Gas 1193.HK O 27.1 27.0 7.8 19.4 15.4 3.2 2.8 1.1 1.4 17.6 19.2 24.1

ENN Energy Holdings Ltd 2688.HK O 56.7 56.0 7.9 18.3 15.6 3.5 3.0 1.6 1.9 20.6 20.9 15.9

Shenzhen Gas Corporation 601139.SS U 12.3 6.6 3.9 30.6 27.2 4.1 3.8 1.3 1.5 14.0 14.5 11.3

Kunlun Energy 0135.HK N 9.1 8.7 9.4 14.4 12.3 1.3 1.2 2.0 2.3 9.3 10.1 2.8

Hong Kong and China Gas 0003.HK U 18.7 15.0 25.3 26.3 24.9 3.5 3.3 2.3 2.4 13.8 13.8 5.2

Simple average 20.4 17.7 2.9 2.6 1.6 1.9 15.1 15.8 14.6

Source: Company data, Credit Suisse estimates

IDEAS ENGINE 4

China Power Sector

New game rules YTD 2015, the national IPPs have mostly underperformed the broader index and most other

utilities sub-sectors. However, the names showed strength again in April with lower coal prices

and stronger-than-expected 1Q15 results. In our view, the national IPPs are unlikely to enjoy

such high profitability as in 1Q15 over the next few years as: (1) cheaper coal prices are likely

to be offset by another "cost-plus" tariff cut later this year; (2) the recent 5% tariff cut should

reflect legacy costs instead of recent costs; and (3) most importantly, the power reform is likely

to trigger huge dynamic changes in this oversupplied industry. With rising uncertainties on the

operational environment for power generators, we believe safety should replace growth as the

key investment criteria.

Figure 8: YTD sub-sector performance

Source: Bloomberg

Further downgrade of national IPPs

With four separate documents issued in the past month, there is little doubt that China is very

determined to push for a market-based power economy. This is likely to radically change the

dynamics from the current industry structure, whereby every power tariff change has been

regulated by the central authority (National Development and Reform Commission or the

NDRC) and power plants' utilisation ability is largely planned. In an oversupplied industry

(thermal utilisation is nearing a 39-year-low this year), market pricing could pull down sector

ROE from 17% in 2014 to about 10% in 2020E in a slow demand scenario. We reflect our

P/B-based target prices with lower sustainable ROE (average of a stable demand and slow

demand scenario).

Figure 9: China IPPs—target price and rating changes

Company Ticker Prev.

rating

New

rating

Prev.

TP

New

TP

U/D Target

P/B

Underlying

ROE

Prev. ROE

HNP-H 0902.HK U U 7.7 7.3 -35% 1.0 11.3% 13.5%

HDP-H 1071.HK N U 6.6 6.4 -26% 1.2 12.2% 14.0%

CRP 0836.HK U U 17.0 16.3 -30% 1.2 12.6% 14.0%

HNP-A 600011.SS U U 6.2 5.8 -47% 1.0 11.1% 13.5%

HDP-A 600027.SS U U 5.2 5.1 -41% 1.2 12.2% 14.0%

Source: Company data, Credit Suisse estimates

Coal prices are unlikely to impact post-FY15 profits

In 1Q15, some IPPs reported strong profits and the key positive surprises mostly came from

cheaper coal prices. However, the recent tariff cut suggested that China has started to base

regulated tariff calculations on movements in fuel prices, suggesting any weakness in coal

prices could trigger another tariff cut later this year. Therefore, given that it is largely a rule of

90% pass-through, a stronger FY15 net profit would mean more tariff cuts going into FY16.

This is why we now base our target price calculations on FY16E P/B which will largely reduce

any influence of short-term movements in coal prices. Taking a longer-term view, valuation

would become much more stretched vs. history.

Figure 10: Three-year forward P/B history

Source: Bloomberg, Credit Suisse estimates

IDEAS ENGINE 5

China Power Sector

Why is consolidation needed?

In the following sections, we try to reflect on the "consolidation" and "no consolidation" cases in

a "slow demand" scenario. Given the continuing pressure on overall thermal utilisation, the

power reforms may make consolidation possible where power generating units compete with

each other on generation costs. In a nutshell, with utilisation hours likely touching a 39-year low

in 2015 (4,706 in 2014), a large fleet of units need to be phased out for the entire thermal

power industry to restore the optimal level of >5,000 hours. In the consolidation scenario, we

assume utilisation and tariffs to keep weakening in the next three years, phasing smaller units

out but companies that need to shut down before full depreciation may realise impairment

losses; however, a recovery may happen in 2019-20 as smaller units would be out of the fray

and it would be a more orderly industry. If there is no power reform and consolidation, tariffs

may be less destructive but everyone will get hurt with the rising pain of oversupply. Therefore,

without assuming additional asset injections, the key loser would be Huaneng with similar ROE

in both scenarios while the other three companies will be better positioned post consolidation

vs. no consolidation at all. More details are in the following sections.

Figure 11: ROE scenarios in the two cases (slow demand scenario)

2014 ROE 2020E ROE

Huaneng Power Consolidation 16.2% 10.2%

No consolidation 16.2% 10.5%

Datang Power Consolidation 4.0% 11.9%

No consolidation 4.0% 10.2%

Huadian Power Consolidation 21.8% 12.2%

No consolidation 21.8% 9.6%

CR Power Consolidation 13.6% 12.1%

No consolidation 13.6% 9.1%

Source: Company data, Credit Suisse estimates

The reform is moving quicker than expected

In our first primer report published in March 2015, we expected that coal-fired IPPs could face

both near-term and longer-term earnings headwinds. In the short run, we forecast an

asymmetric cut to on-grid power tariffs: coastal and inland provinces to be impacted by 2.5

fen/kWh (6%) and 1.5 fen/kWh (4%) cuts, respectively. Given that the IPPs could deflect

incremental pricing pressure to the coal producers, we expect average unit fuel cost to drop 5%

YoY for the IPPs in FY15. However, the cost-plus formula should remain effective going

forward, which will trigger another possible tariff cut in early FY16 (we assume further cuts by

1.5 fen and 1.0 fen/kWh for coastal and inland provinces ,respectively).

Also, our previous analysis of full-blown power reforms was based more on tariff differences

whereby high-tariff zones could see much larger tariff pressure than low-tariff locations. This

would result in an ROE squeeze of another >100 bp, but this scenario excludes the impact of

further utilisation downside.

Figure 12: The first reform primer report (March 2015)

Source: Credit Suisse estimates

Figure 13: China IPPs ROE (stable demand scenario)

Source: Company data, Credit Suisse estimate

IDEAS ENGINE 6

China Power Sector

A painful process before gain We begin this section by looking at how seriously oversupplied electricity is in China. In 2014,

China recorded thermal utilisation hours of 4,706 (implying a 54% utilisation rate), which is

reportedly the lowest reading in the past 38 years. Utilisation hours of 5,500 are used as a

common industry borderline between shortages and surpluses.

Figure 14: China—power demand/supply/utilisation trend

Source: CEIC

Further downside in utilisation

The power-GDP intensity factor is a way to gauge the amount of electricity inputs required to

support a period of economic activities. Given that the majority of power users in China are

industrial users, power intensity tends to overshoot on either side during sudden changes in

GDP. For example, during 4Q08 and 1Q09, overall power demand was reported as negative

despite quarterly GDP at 7.6% and 6.6%, respectively. Another recent weakness was

recorded in 2Q-3Q12, whereby power demand growth was close to zero as a result of

continuing GDP slowdown that marked the end of the "8%" growth era. Most recently, we saw

a negative growth in power demand in August 2014, the first negative month since 2009.

Figure 15: Power demand vs GDP

Source: CEIC

Figure 16: Monthly power consumption growth (YoY)

Source: CEIC

-5.0%

5.0%

15.0%

25.0%

35.0%

4,000

4,500

5,000

5,500

6,000

6,500

199719981999200020012002200320042005200620072008200920102011201220132014

Thermal power demand Thermal power capacityThermal utilization hours (LHS)

Power shortage

Power oversupply

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

(10)

(5)

0

5

10

15

20

25(x)

(%)

Power gen YoY GDP growth Power-GDP Intensity factor (RHS)

(15)

(10)

(5)

0

5

10

15

20

25

30

Jan-F

eb 0

7

May-

07

Au

g-0

7

Nov-

07

Mar-

08

Jun-0

8

Se

p-0

8

Dec-

08

Ap

r-0

9

Jul-0

9

Oct

-09

Jan-F

eb 1

0

May-

10

Au

g-1

0

Nov-

10

Mar-

11

Jun-1

1

Se

p-1

1

Dec-

11

Ap

r-1

2

Jul-1

2

Oct

-12

Jan-F

eb 1

3

May-

13

Au

g-1

3

Nov-

13

Mar-

14

Jun-1

4

Se

p-1

4

Dec-

14

(%)

IDEAS ENGINE 7

China Power Sector

Stay in safer waters In a "fire and ice" era, we prefer power producers that can offer better visibility either through

government-mandated support or output protection driven by location-specific reasons, coupled

with protection of tariff risks. Therefore, the following groups stand out:

(1) Renewables such as wind power operators are positioned at sweet spots.

(2) Clean energy such as hydro power. Within hydro, we prefer low-cost producers exposed to

lower tariff cut risks.

(3) Local utilities with protective utilisation and potential to enter new power retail markets.

(4) Nuclear operators could face issues of lower utilisation hours with more flexible peak

functions.

The power of priority

Given the high cost and intermittency issues of renewable energy and non-stop features of nuclear

power, they are unlikely to be included in the power pool, in our view. China's current power dispatch

order protects the on-grid purchases of renewable energy and nuclear energy. According to the

policy, power grid companies are required to follow a pecking order of: (1) maximum purchase of

renewable energy (wind, solar, marine energy, hydro and renewables with no flexibility in power

generation adjustments), (2) hydro, biomass, geothermal and other renewables with flexibility of

adjustments, (3) nuclear power, (4) co-generation coal-fired power (power and heat), (5) gas-fired

power and coal gasification power, (6) coal-fired power and (7) oil-fired power.

Given the high cost and reliability issues of renewable energy and non-stop features of nuclear

power, they are unlikely to be included in the power pool, in our view. China's current power

dispatch order protects the on-grid purchases of renewable energy and nuclear energy.

Potential overhang for nuclear and hydro tariffs

Although nuclear and renewables may be free from pooling, tariff risks could emerge with

further downside adjustment of coal-fired tariffs, which are usually the benchmark prices.

1. Nuclear tariff

The on-grid tariffs of CGN's nuclear projects which commenced operation before 2013 were

determined project-by-project in accordance with fixed costs and operating costs. According to

NDRC's Circular on Relevant Issues Concerning Improving the On-grid Tariff Mechanism for

Nuclear, nuclear generating units (Gen-II) that started operations after 1 January 2013, will be

subject to a national benchmark no-grid tariff of Rmb0.43/kWh (including the 17% value-

added tax). However, it is worth noting that the tariff set for Hongyanhe's first two units has

been Rmb0.4142/kWh, which is same as the local benchmark tariff for coal-fired power before

the adjustment in September 2014.

Figure 17: China's electricity purchase priority list

Source: NDRC, Credit Suisse research

2. Hydro tariff

Hydro power tariffs were previously set on a plant-by-plant basis usually based on cost-plus

models (reasonable return based on budgeted capex and opex). However, China is working on

a different pricing option for hydro power designed for outer transmissions. The so-called

retrograde method is calculated by deducting on-grid selling tariff by transmission charges.

CYP's parentco's new plants—Xiluodu and Xiangjiaba—have much higher pricing than the

current Gezhouba and Three Gorges units given that the calculation is now benchmarking to the

new method. Similarly, the Yalong River projects (owned by SDIC and Chuantou) also enjoy this

calculation, although most hydro tariffs are still lower than coal-fired tariff, which is now at

Rmb400/MWh including VAT. The differences are slightly smaller, if we take into consideration

the hydro VAT rebates currently enforced.

Wind, solar, marine energy, hydro and other renewables (with no flexibility in power generation)

Hydro, biomass, geothermal and other renewables (with flexibility in power generation) & waste-to-energy

Nuclear power

Co-generation coal-fired power

Gas-fired power and coal gasification power

Coal-fired power (units with lower energy consumption and emissions have higher dispatch priority)

Oil-fired power

IDEAS ENGINE 8

China Power Sector

Sell the national IPPs In a world of safety for power gencos, we like: (1) Wind operators (top picks: Huaneng

Renewables and Longyuan), (2) Low-cost Hydro (China Yangtze Power) and (3) Local IPPs

protected by policies (top pick: Mengdian). We are negative on National IPPs (top sells:

Huaneng A/H, China Resources Power).

Figure 18: Recommendation summary of China power operators

POSITIVE NEGATIVE

Wind National IPPs

Huaneng Renewables (0958.HK) Huaneng Power-H (0902.HK) – top sell

Longyuan Power (0916.HK) Huaneng Power-A (600011.SS) – top sell

Low-cost hydro CR Power (0836.HK) – top sell

Yangtze Power (600900.SS) Datang Power-A (601991.SS)

Local IPPs Huadian Power-H (1071.HK) – downgrade to U/P

Jingneng (600578.SS) – initiation Huadian Power-A (600027.SS)

Mengdian (600863.SS) – initiation Nuclear

CGN Power (1816.HK) – downgrade to U/P

Source: Credit Suisse estimates

Figure 19: Matrix of volume/tariff visibility going into the power reform

Source: Credit Suisse estimates

Unsustainable valuation ahead of major headwinds

Following the recent share price strength, national IPPs are now trading at stretched multiples

with 12-month forward P/B nearing a five-year high despite likely pressure on future ROE. The

12-month dividend yield is also around 1 standard deviation below the five-year mean at around

4%. The current valuation could weaken the positive thesis of buying these names on the back

of near-term dividends. If we adjust the calculation to look at three-year forward multiples

(where we could see a meaningful downside in ROE), the multiple could become even more

stretched than the 12-month calculation.

Figure 20: National IPPs—one-year forward P/B history

Source: Bloomberg, Credit Suisse estimates, excluding Datang

0%

4%

8%

12%

16%

20%

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

ROE (RHS)

0.8x Avg-1SD

0.6x Avg-2SD

1.0x Avg

1.2x Avg+1SD

1.4x Avg+2SD

(x)

IDEAS ENGINE 9

China Power Sector

Inner Mongolia Mengdian Huaneng (600863.SS / 600863 CH)

Improving earnings with additional transmission

Dave Dai, CFA / 852 2101 7358 / [email protected]

Ran Ma / 852 2101 6653 / [email protected]

■ Initiate coverage with OUTPERFORM. We initiate coverage on Inner Mongolia Mengdian

Huaneng (Mengdian) with an OUTPERFORM rating and a DCF-based target price of

Rmb7.50. With all generation units (>90% is coal-fired power) located in Inner Mongolia

(one of the least oversupplied locations), Mengdian's earnings growth should be driven by:

(1) capacity and utilisation supported by outbound transmission; (2) cheaper tariffs leading

to marginal benefits of direct supplies or competitive bidding; and (3) strong local

background helping it bid in the event of a potential opening-up of local power retail assets.

■ Earnings to improve. While FY15 earnings are likely to be impacted by weak power

demand, additional ultra-high voltage transmission lines should help transmit most of the

output to other provinces, creating utilisation upside in FY16-17E. We forecast the time-

weighted attributable capacity to witness a 13% FY14-16E CAGR with ~4GW capacity

under construction, stronger than most national IPPs. Parentco may also inject other local

projects (~10% upside on FY16E capacity) but there is no firm timeline yet.

■ A power reform winner. Mengdian is well-positioned to protect its utilisation hours with

competitive tariffs for outbound transmission (cheaper than local destination tariff) under

reforms. Meanwhile, as a dominant power generator in Western Inner Mongolia,

participation in the power retail bidding (we estimate potential annual profit of Rmb1.9 bn at

3% net margin) is possible.

■ Resembling renewable energy. Even without injections and power retail, we expect

meaningful earnings turnaround in FY16-17 helped by new transmission. High visibility on

utilisation and supreme ROE (21% by FY17E) resemble characteristics of a renewable

energy player and justifies its higher multiple than national peers. Key downside risks are

lower-than-expected utilisation and tariffs.

Rating OUTPERFORM* Price (24 Apr 15, Rmb) 6.11 Target price (Rmb) 7.50¹ Upside/downside (%) 22.7 Mkt cap (Rmb mn) 35,485 (US$ 5,730) Enterprise value (Rmb mn) 60,501 Number of shares (mn) 5,807.74 Free float (%) 32.3 52-week price range 6.26 - 2.37 ADTO - 6M (US$ mn) 102.9 *Stock ratings are relative to the coverage universe in each

analyst's or each team's respective sector.

¹Target price is for 12 months.

Share price performance

The price relative chart measures performance against the

Shanghai Shenzhen CSI300 index which closed at 4807.59 on

24/04/15

On 24/04/15 the spot exchange rate was Rmb6.19/US$1

Performance over 1M 3M 12M Absolute (%) 32.8 46.5 156.7 Relative (%) 11.6 26.1 113.4

Financial and valuation metrics

Year 12/13A 12/14E 12/15E 12/16E Revenue (Rmb mn) 12,153.0 13,634.0 13,488.1 16,435.8 EBITDA (Rmb mn) 4,363.5 4,604.8 4,574.5 5,892.1 EBIT (Rmb mn) 2,669.3 2,781.5 2,218.6 3,409.9 Net profit (Rmb mn) 1,375.6 1,359.6 1,037.4 1,659.7 EPS (CS adj.) (Rmb) 0.36 0.23 0.18 0.29 Change from previous EPS (%) n.a. Consensus EPS (Rmb) n.a. 0.36 0.37 — EPS growth (%) -29.2 -34.1 -23.7 60.0 P/E (x) 17.2 26.1 34.2 21.4 Dividend yield (%) 2.4 3.3 3.1 2.3 EV/EBITDA (x) 12.0 13.1 13.4 10.0 P/B (x) 2.2 3.2 3.2 3.0 ROE (%) 13.2 12.4 9.4 14.5 Net debt/equity (%) 122.7 170.2 171.4 141.4

Source: Company data, Thomson Reuters, Credit Suisse estimates.

60

80

100

120

0

2

4

6

8

May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15

Price (LHS) Rebased Rel (RHS)

IDEAS ENGINE 10

China Power Sector

Beijing Jingneng Power Co Ltd (600578.SS / 600578 CH)

Strong asset injection theme

Dave Dai, CFA / 852 2101 7358 / [email protected]

Ran Ma / 852 2101 6653 / [email protected]

■ Initiate coverage with OUTPERFORM. We initiate coverage on Beijing Jingneng Power

(Jingneng) with an OUTPERFORM rating and an SOTP-based target price of Rmb10.0

(including asset injections). Jingneng has a portfolio of high quality coal-fired power units

with >60% of attributable capacity located in Inner Mongolia. Similar to Mengdian, Jingneng

should enjoy resilient utilisation hours for Inner Mongolia assets but the asset injection angle

should be more clear with parentco commitment by 2016.

■ Asset injection commitment. The company's output and earnings may be depressed in

FY15 given the scheduled shutdown of the Shijingshan (Beijing) project but capacity growth

should turn positive again with 6% and 11% in FY16 and FY17, respectively. Additionally,

the parentco has committed to inject additional assets before end of FY16 and we believe it

should be of the size of 4-5GW (>50%). The transaction should be supported by the light

balance sheet.

■ Power retail is only possible. Unlike Mengdian with the local government as one of the

indirect shareholders, Jingneng is ultimately controlled by the Beijing SASAC. Therefore,

the probability of acquiring local power retail business may be low despite its large capacity

exposure to Inner Mongolia. Additionally, Jingneng has 12% of its capacity in Ningxia,

which is also listed for the next batch of power reforms.

■ Compared with Mengdian. We have incorporated the injection potential in our SOTP

target price but no earnings contribution is built in considering limited details. We prefer

Jingneng to Mengdian given similar exposure to Inner Mongolia but better asset growth

opportunity with asset injection. Bidding for the power retail business would be a plus. Key

downside risks are lower-than-expected utilisation and tariffs.

Rating OUTPERFORM* Price (24 Apr 15, Rmb) 8.08 Target price (Rmb) 10.00¹ Upside/downside (%) 23.8 Mkt cap (Rmb mn) 37,308 (US$6,024 mn) Enterprise value (Rmb mn) 47,501 Number of shares (mn) 4,617.32 Free float (%) 21.4 52-week price range 8.08–3.23 ADTO - 6M (US$ mn) 68.7 *Stock ratings are relative to the coverage universe in each analyst's or each

team's respective sector.

¹Target price is for 12 months.

Share price performance

The price relative chart measures performance against the Shanghai

Shenzhen CSI300 index which closed at 4702.64 on 24/04/15

On 24/04/15 the spot exchange rate was Rmb6.19/US$1

Performance over 1M 3M 12M Absolute (%) 25.1 46.9 137.6 Relative (%) 6.7 16.6 20.7

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (Rmb mn) 12,964.0 10,962.0 11,371.6 14,054.1 EBITDA (Rmb mn) 4,899.2 4,055.1 4,135.8 5,526.4 EBIT (Rmb mn) 3,233.0 2,271.8 2,255.0 3,364.0 Net profit (Rmb mn) 2,551.0 2,115.5 2,050.4 2,527.9 EPS (CS adj.) (Rmb) 0.55 0.46 0.44 0.55 Change from previous EPS (%) n.a. Consensus EPS (Rmb) n.a. 0.43 — — EPS growth (%) 6.2 -17.1 -3.1 23.3 P/E (x) 14.6 17.6 18.2 14.8 Dividend yield (%) 2.5 2.0 1.9 2.4 EV/EBITDA (x) 9.5 11.7 11.5 8.3 P/B (x) 2.6 2.4 2.2 2.0 ROE (%) 18.5 14.1 12.5 14.2 Net debt/equity (%) 50.5 50.4 45.9 34.6

Source: Company data, Thomson Reuters, Credit Suisse estimates.

80

90

100

110

120

2

4

6

8

10

Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 Dec-14

Price (LHS) Rebased Rel (RHS)

IDEAS ENGINE 11

China Power Sector

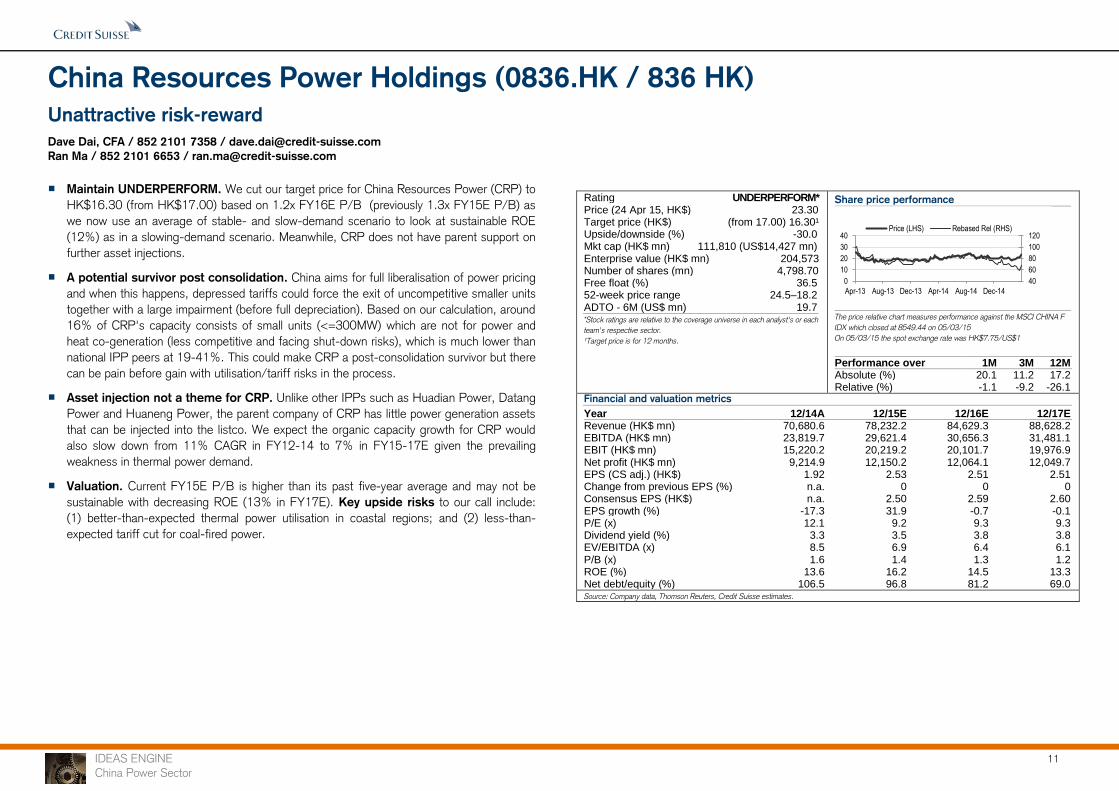

China Resources Power Holdings (0836.HK / 836 HK)

Unattractive risk-reward

Dave Dai, CFA / 852 2101 7358 / [email protected]

Ran Ma / 852 2101 6653 / [email protected]

■ Maintain UNDERPERFORM. We cut our target price for China Resources Power (CRP) to

HK$16.30 (from HK$17.00) based on 1.2x FY16E P/B (previously 1.3x FY15E P/B) as

we now use an average of stable- and slow-demand scenario to look at sustainable ROE

(12%) as in a slowing-demand scenario. Meanwhile, CRP does not have parent support on

further asset injections.

■ A potential survivor post consolidation. China aims for full liberalisation of power pricing

and when this happens, depressed tariffs could force the exit of uncompetitive smaller units

together with a large impairment (before full depreciation). Based on our calculation, around

16% of CRP's capacity consists of small units (<=300MW) which are not for power and

heat co-generation (less competitive and facing shut-down risks), which is much lower than

national IPP peers at 19-41%. This could make CRP a post-consolidation survivor but there

can be pain before gain with utilisation/tariff risks in the process.

■ Asset injection not a theme for CRP. Unlike other IPPs such as Huadian Power, Datang

Power and Huaneng Power, the parent company of CRP has little power generation assets

that can be injected into the listco. We expect the organic capacity growth for CRP would

also slow down from 11% CAGR in FY12-14 to 7% in FY15-17E given the prevailing

weakness in thermal power demand.

■ Valuation. Current FY15E P/B is higher than its past five-year average and may not be

sustainable with decreasing ROE (13% in FY17E). Key upside risks to our call include:

(1) better-than-expected thermal power utilisation in coastal regions; and (2) less-than-

expected tariff cut for coal-fired power.

Rating UNDERPERFORM* Price (24 Apr 15, HK$) 23.30 Target price (HK$) (from 17.00) 16.30¹ Upside/downside (%) -30.0 Mkt cap (HK$ mn) 111,810 (US$14,427 mn) Enterprise value (HK$ mn) 204,573 Number of shares (mn) 4,798.70 Free float (%) 36.5 52-week price range 24.5–18.2 ADTO - 6M (US$ mn) 19.7 *Stock ratings are relative to the coverage universe in each analyst's or each

team's respective sector.

¹Target price is for 12 months.

Share price performance

The price relative chart measures performance against the MSCI CHINA F

IDX which closed at 8549.44 on 05/03/15

On 05/03/15 the spot exchange rate was HK$7.75/US$1

Performance over 1M 3M 12M Absolute (%) 20.1 11.2 17.2 Relative (%) -1.1 -9.2 -26.1

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (HK$ mn) 70,680.6 78,232.2 84,629.3 88,628.2 EBITDA (HK$ mn) 23,819.7 29,621.4 30,656.3 31,481.1 EBIT (HK$ mn) 15,220.2 20,219.2 20,101.7 19,976.9 Net profit (HK$ mn) 9,214.9 12,150.2 12,064.1 12,049.7 EPS (CS adj.) (HK$) 1.92 2.53 2.51 2.51 Change from previous EPS (%) n.a. 0 0 0 Consensus EPS (HK$) n.a. 2.50 2.59 2.60 EPS growth (%) -17.3 31.9 -0.7 -0.1 P/E (x) 12.1 9.2 9.3 9.3 Dividend yield (%) 3.3 3.5 3.8 3.8 EV/EBITDA (x) 8.5 6.9 6.4 6.1 P/B (x) 1.6 1.4 1.3 1.2 ROE (%) 13.6 16.2 14.5 13.3 Net debt/equity (%) 106.5 96.8 81.2 69.0

Source: Company data, Thomson Reuters, Credit Suisse estimates.

40

60

80

100

120

0

10

20

30

40

Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 Dec-14

Price (LHS) Rebased Rel (RHS)

IDEAS ENGINE 12

China Power Sector

Huaneng Power International Inc (0902.HK / 902 HK)

The worst is yet to come

Dave Dai, CFA / 852 2101 7358 / [email protected]

Ran Ma / 852 2101 6653 / [email protected]

■ One of the top sells. We cut our target price for Huaneng Power (HNP) to HK$7.30

(from HK$7.70) based on 1.0x FY16E P/B (previously 1.2x FY15E P/B) as we now use

an average of stable- and slow-demand scenario to look at sustainable ROE (10.5%). In

the slow demand scenario, ROE can average ~8.7% in FY16-20 given HNP's higher

exposure to smaller units (shutdown risks). We have not cut earnings to reflect the slow-

demand scenario but further weak signs could impact valuation ahead of earnings.

■ Painful industry consolidation. China aims for full liberalisation of power pricing and

when this happens, depressed tariffs could force the exit of uncompetitive smaller units

together with a large impairment (before full depreciation). The tariffs for HNP's direct

supplied power in 2014 (8-10% lower on average) is a very strong early signal of what

market forces can do. Based on our calculation, close to 40% of HNP's capacity consists

of small units (<=300MW) and 89% of such units are not for power and heat co-

generation, which may be less competitive and face shutdown risks.

■ Asset injection limited. After the asset injection at end-2014, we expect limited profitable

assets to be injected into HNP in the near term, based on our analysis of the parentco's

unlisted assets. Besides, the total unlisted thermal capacity represents only 58% of HNP's

capacity (2013 data), lower than peers at over 100%.

■ Valuation unattractive. The stock is currently trading at 1.7x 2015E P/B, much higher

than its five-year historical average of 1.1x, unjustified given our projected long-term ROE

of 11%. The key upside risks to our forecasts are better-than-expected utilisation hours

and later-than-expected tariff cuts.

Rating UNDERPERFORM* Price (24 Apr 15, HK$) 11.30 Target price (HK$) (from 7.70) 7.30¹ Upside/downside (%) -35.4 Mkt cap (HK$ mn) 188,313 (US$24,298 mn) Enterprise value (Rmb mn) 316,747 Number of shares (mn) 14,420.38 Free float (%) 48.7 52-week price range 11.66–7.57 ADTO - 6M (US$ mn) 37.5 *Stock ratings are relative to the coverage universe in each analyst's or each

team's respective sector.

¹Target price is for 12 months.

Share price performance

The price relative chart measures performance against the MSCI CHINA F

IDX which closed at 8549.44 on 24/04/15

On 24/04/15 the spot exchange rate was HK$7.75/US$1

Performance over 1M 3M 12M Absolute (%) 28.7 0.5 46.0 Relative (%) 7.5 -19.9 2.7

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (Rmb mn) 125,406.9 137,510.3 137,490.2 143,090.8 EBITDA (Rmb mn) 36,921.3 39,820.2 37,649.0 38,999.2 EBIT (Rmb mn) 25,274.6 26,748.9 23,560.7 24,464.7 Net profit (Rmb mn) 10,672.2 12,067.0 10,816.0 11,558.8 EPS (CS adj.) (Rmb) 0.75 0.84 0.75 0.80 Change from previous EPS (%) n.a. 0 0 0 Consensus EPS (Rmb) n.a. 0.92 0.94 0.91 EPS growth (%) 1.6 11.0 -10.4 6.9 P/E (x) 12.0 10.8 12.0 11.3 Dividend yield (%) 4.2 5.1 4.6 4.9 EV/EBITDA (x) 7.9 8.0 8.2 7.6 P/B (x) 1.8 1.7 1.6 1.5 ROE (%) 16.1 16.6 13.8 13.9 Net debt/equity (%) 167.4 174.3 152.6 132.4

Source: Company data, Thomson Reuters, Credit Suisse estimates.

60

80

100

120

6

8

10

12

14

Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 Dec-14

Price (LHS) Rebased Rel (RHS)

IDEAS ENGINE 13

China Power Sector

Huaneng Power International Inc (600011.SS / 600011 CH)

Stay negative

Dave Dai, CFA / 852 2101 7358 / [email protected]

Ran Ma / 852 2101 6653 / [email protected]

■ Maintain UNDERPERFORM. We cut our target price for Huaneng Power-A (HNP-A) to

Rmb5.80 (from Rmb6.20) based on 1.0x FY16E P/B (previously 1.2x FY15E P/B) as we

now use an average of stable- and slow-demand scenario to look at sustainable ROE

(10.5%). In the slow demand scenario, ROE can average ~8.7% in FY16-20 given HNP's

higher exposure to smaller units (shutdown risks). We have not cut earnings to reflect the

slow-demand scenario but further weak signs could impact valuation ahead of earnings.

■ Painful industry consolidation. China aims for full liberalisation of power pricing and

when this happens, depressed tariffs could force the exit of uncompetitive smaller units

together with a large impairment (before full depreciation). The tariffs for HNP's direct

supplied power in 2014 (8-10% lower on average) is a very strong early signal of what

market forces can do. Based on our calculation, close to 40% of HNP's capacity consists

of small units (<=300MW) and 89% of such units are not for power and heat co-

generation, which may be less competitive and face shut-down risks.

■ Asset injection limited. After the asset injection at end-2014, we expect limited profitable

assets to be injected into HNP in the near term, based on our analysis of the parentco's

unlisted assets. Besides, the total unlisted thermal capacity represents only 58% of HNP's

capacity (2013 data), lower than peers at over 100%.

■ Valuation unattractive. The stock is currently trading at 2.0x 2015E P/B, much higher

than its five-year historical average of 1.1x, unjustified given our projected long-term ROE

of 11%. The key upside risks to our forecasts are better-than-expected utilisation hours

and later-than-expected tariff cuts.

Rating UNDERPERFORM* Price (24 Apr 15, Rmb) 10.96 Target price (Rmb) (from 6.20) 5.80¹ Upside/downside (%) -47.1 Mkt cap (Rmb mn) 150,480 (US$ 24,298) Enterprise value (Rmb mn) 316,747 Number of shares (mn) 14,420.38 Free float (%) 48.7 52-week price range 10.96 - 5.27 ADTO - 6M (US$ mn) 37.5 *Stock ratings are relative to the coverage universe in each analyst's or each

team's respective sector.

¹Target price is for 12 months.

Share price performance

The price relative chart measures performance against the Shanghai

Shenzhen CSI300 index which closed at 4702.64 on 24/04/15

On 24/04/15 the spot exchange rate was Rmb6.19/US$1

Performance over 1M 3M 12M Absolute (%) 34.0 29.4 105.2 Relative (%) 12.8 9.0 62.0

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (Rmb mn) 125,406.9 137,510.3 137,490.2 143,090.8 EBITDA (Rmb mn) 36,921.3 39,820.2 37,649.0 38,999.2 EBIT (Rmb mn) 25,274.6 26,748.9 23,560.7 24,464.7 Net profit (Rmb mn) 10,672.2 12,067.0 10,816.0 11,558.8 EPS (CS adj.) (Rmb) 0.75 0.84 0.75 0.80 Change from previous EPS (%) n.a. 0 0 0 Consensus EPS (Rmb) n.a. 0.92 0.95 0.93 EPS growth (%) 1.6 11.0 -10.4 6.9 P/E (x) 14.5 13.1 14.6 13.7 Dividend yield (%) 3.5 4.2 3.8 4.0 EV/EBITDA (x) 7.9 8.0 8.2 7.6 P/B (x) 2.2 2.1 2.0 1.8 ROE (%) 16.1 16.6 13.8 13.9 Net debt/equity (%) 167.4 174.3 152.6 132.4

Source: Company data, Thomson Reuters, Credit Suisse estimates.

60

80

100

120

4

6

8

10

12

Apr-13 Aug-13 Dec-13 Apr-14 Aug-14 Dec-14

Price (LHS) Rebased Rel (RHS)

IDEAS ENGINE 14

China Power Sector

CGN Power Co., Ltd. (1816.HK / 1816 HK)

Downgrade to UNDERPERFORM with rising risks

Dave Dai, CFA / 852 2101 7358 / [email protected]

Ran Ma / 852 2101 6653 / [email protected]

■ Downgrade rating. We downgrade CGN Power (CGN) to UNDERPERFORM from

Neutral with China's introduction of peaking functions and possible delays in the Taishan

project. The stock is now trading at 26x FY15 P/E with little yield and one of the most

expensive large-cap global utilities names. We incorporated the newly approved Hongyanhe

Phase II project but the revised DCF-based target price of HK$3.40 still implies significant

downside.

■ Expectations are rich. We believe that the market is forecasting stable utilisation hours

across different locations but the recent reform document suggests the possibility of

peaking functions going forward, which implies possible utilisation downside. China has

started to investigate the equipment risks of the Taishan EPR project (10% of FY17E

attributable capacity) after receiving a warning from the French nuclear authority. We cut

our FY16-17 EPS forecasts by 4-6% on lower utilisation for Hongyanhe (very oversupplied)

after FY16 and delayed operation of Taishan by 12 months.

■ Not a lot left for immediate earnings upside. After Taishan, the parentco still owns the

Fangchenggang (Guangxi) project, if the project is injected, it could create ~9% attributable

capacity upside. Any new approval (such as the case of Hongyanhe Phase II) will take 5-6

years of construction time and contribute no earnings in the medium term. If Taishan is

delayed, it could push back the capacity growth beyond our forecast 2H16.

■ Rarity has a price. As the only listed pure nuclear operator in China, CGN is enjoying a

large scarcity premium, which we see as unjustified with rising earnings risks. Upside

investment risks are higher utilisation hours.

Rating (from Neutral) UNDERPERFORM* [V] Price (24 Apr 15, HK$) 4.48 Target price (HK$) (from 3.20) 3.40¹ Upside/downside (%) -24.1 Mkt cap (HK$ mn) 203,610 (US$ 26,272) Enterprise value (Rmb mn) 276,716 Number of shares (mn) 45,448.75 Free float (%) 41.6 52-week price range 4.65 - 3.07 ADTO - 6M (US$ mn) 86.6 *Stock ratings are relative to the coverage universe in each analyst's or each

team's respective sector.

¹Target price is for 12 months.

[V] = Stock considered volatile (see Disclosure Appendix).

Share price performance

The price relative chart measures performance against the MSCI CHINA F

IDX which closed at 8650.86 on 24/04/15

On 24/04/15 the spot exchange rate was HK$7.75/US$1

Performance over 1M 3M 12M Absolute (%) 40.9 43.1 — Relative (%) 20.1 22.7 —

Financial and valuation metrics

Year 12/14A 12/15E 12/16E 12/17E Revenue (Rmb mn) 20,793.3 21,760.8 26,248.4 32,901.2 EBITDA (Rmb mn) 12,446.3 13,402.2 15,786.2 19,452.9 EBIT (Rmb mn) 9,826.3 10,523.1 12,318.5 14,714.1 Net profit (Rmb mn) 5,712.2 6,185.8 7,151.2 8,193.2 EPS (CS adj.) (Rmb) 0.13 0.14 0.16 0.18 Change from previous EPS (%) n.a. -0.4 -5.5 -4.1 Consensus EPS (Rmb) n.a. 0.14 0.17 0.20 EPS growth (%) -18.0 8.3 15.6 14.6 P/E (x) 28.5 26.3 22.8 19.9 Dividend yield (%) 0.1 1.3 1.5 1.7 EV/EBITDA (x) 17.2 20.6 17.9 14.2 P/B (x) 3.2 3.0 2.7 2.5 ROE (%) 15.5 11.7 12.5 13.1 Net debt/equity (%) 85.5 151.7 145.9 127.4

Source: Company data, Thomson Reuters, Credit Suisse estimates.

80

90

100

110

120

2

3

4

5

6

Dec-14 Apr-15

Price (LHS) Rebased Rel (RHS)

IDEAS ENGINE 15

China Power Sector

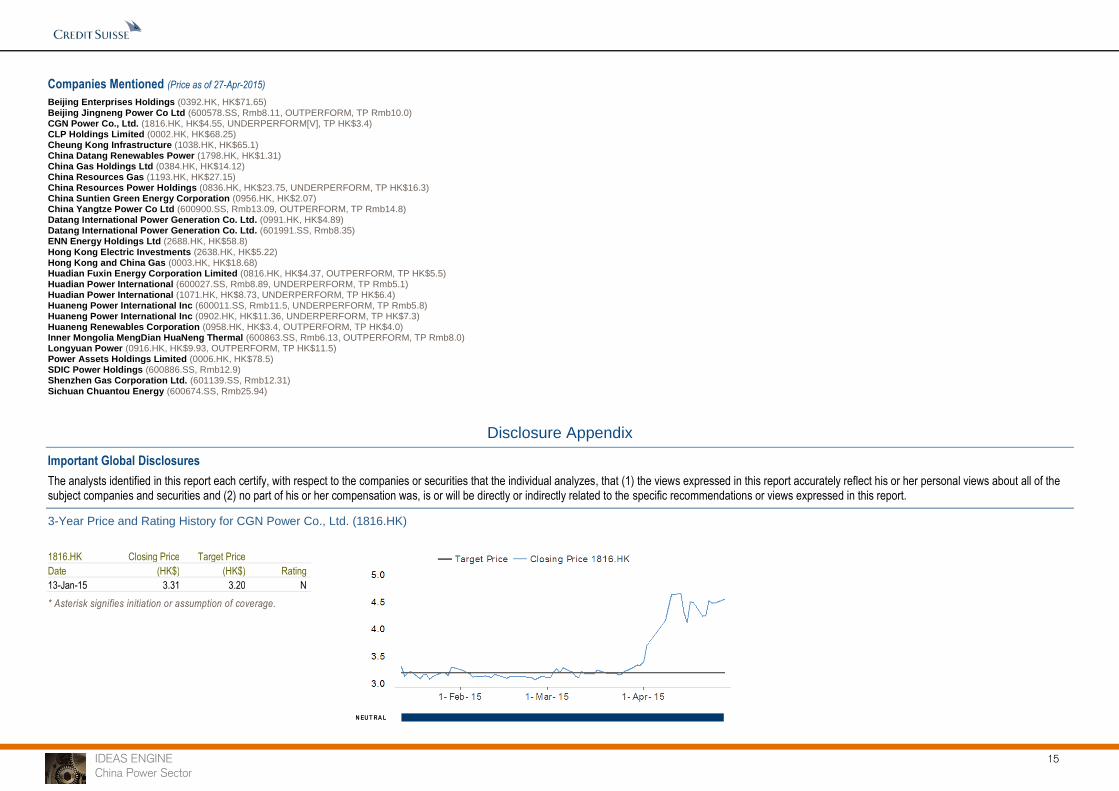

Companies Mentioned (Price as of 27-Apr-2015)

Beijing Enterprises Holdings (0392.HK, HK$71.65) Beijing Jingneng Power Co Ltd (600578.SS, Rmb8.11, OUTPERFORM, TP Rmb10.0) CGN Power Co., Ltd. (1816.HK, HK$4.55, UNDERPERFORM[V], TP HK$3.4) CLP Holdings Limited (0002.HK, HK$68.25) Cheung Kong Infrastructure (1038.HK, HK$65.1) China Datang Renewables Power (1798.HK, HK$1.31) China Gas Holdings Ltd (0384.HK, HK$14.12) China Resources Gas (1193.HK, HK$27.15) China Resources Power Holdings (0836.HK, HK$23.75, UNDERPERFORM, TP HK$16.3) China Suntien Green Energy Corporation (0956.HK, HK$2.07) China Yangtze Power Co Ltd (600900.SS, Rmb13.09, OUTPERFORM, TP Rmb14.8) Datang International Power Generation Co. Ltd. (0991.HK, HK$4.89) Datang International Power Generation Co. Ltd. (601991.SS, Rmb8.35) ENN Energy Holdings Ltd (2688.HK, HK$58.8) Hong Kong Electric Investments (2638.HK, HK$5.22) Hong Kong and China Gas (0003.HK, HK$18.68) Huadian Fuxin Energy Corporation Limited (0816.HK, HK$4.37, OUTPERFORM, TP HK$5.5) Huadian Power International (600027.SS, Rmb8.89, UNDERPERFORM, TP Rmb5.1) Huadian Power International (1071.HK, HK$8.73, UNDERPERFORM, TP HK$6.4) Huaneng Power International Inc (600011.SS, Rmb11.5, UNDERPERFORM, TP Rmb5.8) Huaneng Power International Inc (0902.HK, HK$11.36, UNDERPERFORM, TP HK$7.3) Huaneng Renewables Corporation (0958.HK, HK$3.4, OUTPERFORM, TP HK$4.0) Inner Mongolia MengDian HuaNeng Thermal (600863.SS, Rmb6.13, OUTPERFORM, TP Rmb8.0) Longyuan Power (0916.HK, HK$9.93, OUTPERFORM, TP HK$11.5) Power Assets Holdings Limited (0006.HK, HK$78.5) SDIC Power Holdings (600886.SS, Rmb12.9) Shenzhen Gas Corporation Ltd. (601139.SS, Rmb12.31) Sichuan Chuantou Energy (600674.SS, Rmb25.94)

Disclosure Appendix

Important Global Disclosures

The analysts identified in this report each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for CGN Power Co., Ltd. (1816.HK)

1816.HK Closing Price Target Price

Date (HK$) (HK$) Rating

13-Jan-15 3.31 3.20 N

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

IDEAS ENGINE 16

China Power Sector

3-Year Price and Rating History for China Resources Power Holdings (0836.HK)

0836.HK Closing Price Target Price

Date (HK$) (HK$) Rating

21-Aug-12 17.06 19.00 O

03-Oct-12 16.78 19.70

19-Mar-13 22.65 23.00

11-Apr-13 23.90 28.00

27-Nov-13 18.78 22.00 *

18-Mar-14 19.24 23.50

21-Apr-14 21.00 23.50 N

18-Aug-14 22.20 25.00

14-Oct-14 20.80 22.00

11-Mar-15 19.22 17.00 U

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

U N D ERPERFO RM

3-Year Price and Rating History for China Yangtze Power Co Ltd (600900.SS)

600900.SS Closing Price Target Price

Date (Rmb) (Rmb) Rating

30-Apr-12 6.48 8.30 O

01-Nov-12 6.46 8.50

02-May-13 7.13 8.60

02-Sep-13 6.71 8.30

21-May-14 5.97 7.60

22-May-14 6.04 *

26-Sep-14 7.79 9.50 O

13-Jan-15 10.55 12.20

* Asterisk signifies initiation or assumption of coverage. O U T PERFO RM

IDEAS ENGINE 17

China Power Sector

3-Year Price and Rating History for Huadian Fuxin Energy Corporation Limited (0816.HK)

0816.HK Closing Price Target Price

Date (HK$) (HK$) Rating

03-Mar-14 4.24 5.20 O *

25-Mar-14 3.80 5.30

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

3-Year Price and Rating History for Huadian Power International (600027.SS)

600027.SS Closing Price Target Price

Date (Rmb) (Rmb) Rating

15-Oct-14 3.97 4.92 O

13-Jan-15 6.18 5.70 U

11-Mar-15 5.80 5.10

31-Mar-15 6.80 5.20

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

U N D ERPERFO RM

IDEAS ENGINE 18

China Power Sector

3-Year Price and Rating History for Huadian Power International (1071.HK)

1071.HK Closing Price Target Price

Date (HK$) (HK$) Rating

15-Oct-14 5.49 6.20 O

13-Jan-15 6.45 7.10

11-Mar-15 6.39 6.40 N

31-Mar-15 6.45 6.60

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

3-Year Price and Rating History for Huaneng Power International Inc (600011.SS)

600011.SS Closing Price Target Price

Date (Rmb) (Rmb) Rating

14-Oct-14 6.20 5.95 N *

13-Jan-15 8.25 6.90 U

11-Mar-15 7.58 6.20

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

U N D ERPERFO RM

IDEAS ENGINE 19

China Power Sector

3-Year Price and Rating History for Huaneng Power International Inc (0902.HK)

0902.HK Closing Price Target Price

Date (HK$) (HK$) Rating

02-Aug-12 5.62 5.85 O

03-Oct-12 5.88 7.10

10-Apr-13 8.37 9.00

24-Apr-13 8.80 9.40

27-Nov-13 7.43 6.40 U *

30-Jul-14 8.73 7.40

14-Oct-14 8.90 7.50 *

13-Jan-15 10.84 8.60

11-Mar-15 8.89 7.70

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

U N D ERPERFO RM

3-Year Price and Rating History for Huaneng Renewables Corporation (0958.HK)

0958.HK Closing Price Target Price

Date (HK$) (HK$) Rating

03-Mar-14 3.45 4.05 O *

10-Apr-14 2.63 3.65

19-Mar-15 2.79 3.55

10-Apr-15 3.20 3.80

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

IDEAS ENGINE 20

China Power Sector

3-Year Price and Rating History for Longyuan Power (0916.HK)

0916.HK Closing Price Target Price

Date (HK$) (HK$) Rating

13-May-12 5.84 6.95 O

29-Aug-12 5.08 6.32

05-Nov-12 5.08 6.19

17-Dec-12 5.23 6.10

12-Mar-13 6.51 7.08 N

25-Nov-13 10.10 12.30 O *

03-Mar-14 9.61 12.60

18-Mar-14 7.93 11.90

20-Aug-14 8.57 10.50

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutra ls the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional ben chmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe . For Australian and New Zealand stocks, 12-month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10-15% and -10-15% levels in the Neutral stock rating definition, respectively. Prior to 10th December 2012, Japanese ratings were based on a stock’s total return relative to the average total return of the relevant country or regional benchmark.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

IDEAS ENGINE 21

China Power Sector

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 43% (53% banking clients)

Neutral/Hold* 38% (50% banking clients)

Underperform/Sell* 16% (44% banking clients)

Restricted 3%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, and Underperform most closely correspond to B uy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objective s, current holdings, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Price Target: (12 months) for CGN Power Co., Ltd. (1816.HK)

Method: Our target price of HK$3.40 for CGN Power is based on discounted cash flow method with a WACC of 7% (cost of equity of 11% and cost of debt of 4.5%, debt to equity ratio of 1.5x) as well as zero

terminal growth.

Risk: Key risks to our target price of HK$3.40 for CGN Power includes: (1) drop of utilisaiton hours; (2) change of national nuclear policies; (3) nuclear accidents worldwide; (4) increase in the fuel costs and other costs

as well as (5) delay of construction schedule of nuclear

Price Target: (12 months) for China Yangtze Power Co Ltd (600900.SS)

Method: We arrive at our target price for China Yangtze Power by using DCF model, as we believe operating cash flow best captures the company's mid- to long-term growth profile. Our WACC of 8.3% with

terminal growth of 0% suggest a fair price of Rmb10.7 for the stock (without injection), and a target price of Rmb14.8 (with injection).

Risk: The following are the risks to our target price: (1) volatilities in hydro resources, (2) changes in interest rate (3) a delay in asset injection or no injection would surprise the market negatively.

Price Target: (12 months) for Huaneng Power International Inc (600011.SS)

Method: Our target price of Rmb5.8 for Huaneng Power International Inc (A) is based on a P/B (price-to-book) of 1.0x backed by a sustainable ROE (return on equity) of 10.5%..

Risk: Risks that could cause the share price to diverge from our Rmb5.8 target price for Huaneng Power International Inc include: (1) worse-than-expected thermal utilisation in coastal areas; and (2) coal price rebound.

Price Target: (12 months) for Huadian Power International (600027.SS)

Method: Our target price of Rmb5.1 for Huadian Power International (A) is based on a P/B (price-to-book) of 1.2x backed by a sustainable ROE (return on equity) of 11%.

Risk: Risks that could impede achievement target price of Rmb5.1 for Huadian Power International (A) include: (1) thermal utlisation; and (2) uncertainty on asset injections.

IDEAS ENGINE 22

China Power Sector

Price Target: (12 months) for Huaneng Power International Inc (0902.HK)

Method: We use P/B (price-to-book) valuation to derive our target price of HK$7.30 for Huaneng Power International Inc (H). We assume a long-term ROE (return on equity) of 11.1%, which implies a FY16 P/B of

1.0x.

Risk: Risks to our HK$7.30 target price for Huaneng Power International Inc (H) include: (1) faster-than-expected capacity growth; (2) lower-than-expected coal prices; (3) better-than expected utilisation hours.

Price Target: (12 months) for China Resources Power Holdings (0836.HK)

Method: Our target price of HK$16.30 for CRP is based on the sum-of-the-parts valuation. We use 1.2x FY16 P/B (price-to-book) ratio for the power generation business and DCF (discounted cash flow)

methodology for coal mining.

Risk: Risks to our target price of HK$16.30 for CRP include: (1) Better-than-expected thermal power utilisation in coastal regions; and (2) less-than-expected tariff cuts for coal-fired power.

Price Target: (12 months) for Huadian Power International (1071.HK)

Method: Our target price of HK$6.4 for Huadian Power International (H) is derived from a price-to-book (P/B) methodology with a target P/B of 1.2x backed by a sustainable ROE (return on equity) of 12%.

Risk: Risks that could impede achievement of our target price of HK$6.4 for Huadian Power International include: (1) coal price increase in 2015; (2) worse-than-expected thermal power utlisation in 2015-16; (3)

uncertain details for asset injections.

Price Target: (12 months) for Huaneng Renewables Corporation (0958.HK)

Method: Our HK$ 4.00 target price for Huaneng Renewables is based on discounted cash flow method with a WACC of 7% and terminal growth rate of 2%. We use 12% cost of equity and 5% after tax cost of

debt. The terminal value takes up 90% in our total DCF valuation.

Risk: Key investment risks to our target price of HK$4.00 for Huaneng Renewables include: (1) slower-than-expected capacity growth; (2) volatile wind resources and utilisation hours; and (3) further impairment of

assets.

Price Target: (12 months) for Longyuan Power (0916.HK)

Method: Our HK$11.5 for Longyuan Power Group is based on DCF. Our WACC of 8% is based on a cost of equity of 12% and a post-tax cost of debt of 4%. The terminal growth we assume is 2%.

Risk: Key risks to our target price of HK$11.5 for Longyuan Power include: (1) lower-than-expected capacity growth; (2) worse-than-expected utilisation hours; and (3) potential wind power tariff cut in 2015 or later.

Price Target: (12 months) for Huadian Fuxin Energy Corporation Limited (0816.HK)

Method: Our HK$5.50 target price for Huadian Fuxin Energy Corp. is based on discounted cash flow method with a WACC of 8% and terminal growth rate of 1%. We use 12% cost of equity and 5.5% after tax

cost of debt. The terminal value takes up 80% in our total DCF valuation.

Risk: Key risks to our target price of HK$5.50 for Huadian Fuxin Energy Corp. include: (1) slower-than-expected wind power capacity growth; (2) volatile wind and hydro resources; and (3) more-than-expected cut of

coal-fired tariff.

IDEAS ENGINE 23

China Power Sector

Price Target: (12 months) for Inner Mongolia MengDian HuaNeng Thermal (600863.SS)

Method: The target price of Rmb 8.0 for Inner Mongolia MengDian HuaNeng Thermal is based on discounted cash flow method. We use 8% WACC and zero terminal growth.

Risk: Key risks to our target price of Rmb 8.0 for Inner Mongolia MengDian HuaNeng Thermal includes: (1) lower tariff and (2) lower utilisation hours.

Price Target: (12 months) for Beijing Jingneng Power Co Ltd (600578.SS)

Method: The target price of Rmb 10.0 for Beijing Jingneng Power Co Ltd is based on sum-of-the-parts method. We values existing pipeline at Rmb 8.90/share and asset injection at Rmb 1.00/share.

Risk: Key risks to our SOTP-based target price of Rmb 10.0 for Beijing Jingneng Power Co Ltd includes: (1) lower-than-expected tariff; (2) lower-than-expected utilisation hours; (3) delay of asset injections.

Please refer to the firm's disclosure website at https://rave.credit-suisse.com/disclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names

The subject company (1816.HK, 0902.HK, 0836.HK, 1071.HK, 0958.HK, 0916.HK, 0816.HK, 600863.SS, 0002.HK, 0006.HK, 0392.HK, 0991.HK, 1038.HK, 1798.HK, 601139.SS, 601991.SS) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (1816.HK, 0958.HK, 600863.SS, 0392.HK, 601139.SS) within the past 12 months.

Credit Suisse has managed or co-managed a public offering of securities for the subject company (1816.HK, 0958.HK, 600863.SS) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (1816.HK, 0958.HK, 600863.SS, 0392.HK, 601139.SS) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (1816.HK, 600900.SS, 600027.SS, 0902.HK, 0836.HK, 1071.HK, 0958.HK, 0916.HK, 0816.HK, 600863.SS, 0002.HK, 0003.HK, 0006.HK, 0392.HK, 0991.HK, 1038.HK, 1193.HK, 1798.HK, 2688.HK, 601139.SS) within the next 3 months.

As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (0902.HK, 0916.HK, 0991.HK).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company (1816.HK, 600900.SS, 0902.HK, 0836.HK, 1071.HK, 0958.HK, 0916.HK, 0816.HK, 600863.SS, 600578.SS, 0002.HK, 0003.HK, 0006.HK, 0384.HK, 0392.HK, 0956.HK, 0991.HK, 1038.HK, 1193.HK, 1798.HK, 2638.HK, 2688.HK, 600674.SS, 600886.SS, 601139.SS) within the past 12 months

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html.

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (1816.HK, 600011.SS, 0902.HK, 0958.HK, 600863.SS) within the past 3 years.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

IDEAS ENGINE 24

China Power Sector

Credit Suisse (Hong Kong) Limited ................................................................................................................................... Dave Dai, CFA ; Ran Ma

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

IDEAS ENGINE 25

China Power Sector