china: a-step forward what does the msci inclusion … · what does the msci inclusion of china...

TRANSCRIPT

China

September 2017

CHINA: A-STEP FORWARDWHAT DOES THE MSCI INCLUSION OF CHINA A-SHARES REALLY MEAN?

Global investment grade bond universe

MSCI Inclusion of China A-share will make 2018 a key inflection point for China’s Capital Market

According to some measures China is already the largest economy in the world, yet Chinese financial assets have only ever been at the periphery of global investors’ portfolio allocation decisions. This is reflected in China’s low country weighting of only 3.2% in the MSCI All Country World Equity Index and the fact that foreign ownership of Chinese government bonds is only 3.9% of the total1.

However, there have been some changes in recent years indicative of an increase in appetite for Asian assets. For example, from 2006 to July 2017, the market capitalisation of global stock markets grew 57%, with Asian markets growing considerably faster and therefore now accounting for a much larger share of the total. China and India in particular experienced rapid growth rates over this period. China’s share of global stock market capitalisation – excluding Hong Kong – increased from 2.0% in 2006 to 9.1% in July 2017 while India’s share increased from 1.6% to 2.7%. In fact, Chinese equities now constitute a larger share of global stock market capitalisation than the equity markets of Japan, the UK and Germany. This is supportive of the view that the centre of economic and market gravity is slowly shifting east.

A-Step Forward: What does the MSCI inclusion of China A-shares really mean?

Mansfield Mok Senior Portfolio Manager

Mansfield Mok is Senior Portfolio Manager

of the New Capital China Equity Fund. With

more than 25 years’ investing experience,

including 10 years as a sell-side Hong

Kong/China analyst, Mansfield’s award-

winning expertise and insights have earned

him international recognition from the

investment community.

Claudia Ching Senior Equity Research Analyst

Claudia Ching is a Senior Equity Research

Analyst focusing on equity research in

China; assisting Mansfield with company

research for the New Capital China Equity

Fund. Claudia has over 10 years’ experience

as a Research Analyst and contributes

in both the stock selection and portfolio

construction process.

3

World’s Top 10 countries by Market Cap

Mkt Cap (US$ trillion)

Rank Market 2017 2006 % Change

1 US 27.5 17.5 57.2%

2 China 7.1 1.0 618.5%

3 Japan 5.7 4.9 17.8%

4 Hong Kong 4.8 2.3 109.1%

5 UK 3.6 3.8 -6.8%

6 Canada 2.4 2.5 -3.8%

7 France 2.2 1.8 26.9%

8 Germany 2.2 1.5 46%

9 India 2.1 0.8 154.1%

10 Switzerland 1.7 1.2 43.8%

Top 10 59.3 37.2 59.3%

World 78.1 49.9 56.5%

Source: Bloomberg. CEIC data as at July 2017

See “China’s Investor Army is Bracing for More Stock Market Pain” Bloomberg News, 16 May 2017.

China’s overall weighting include China A-shares, HK listed Chinese companies and US listed ADRs.

1Source: CEIC data as of February 2017

A-Step Forward: What does the MSCI inclusion of China A-shares really mean?

4

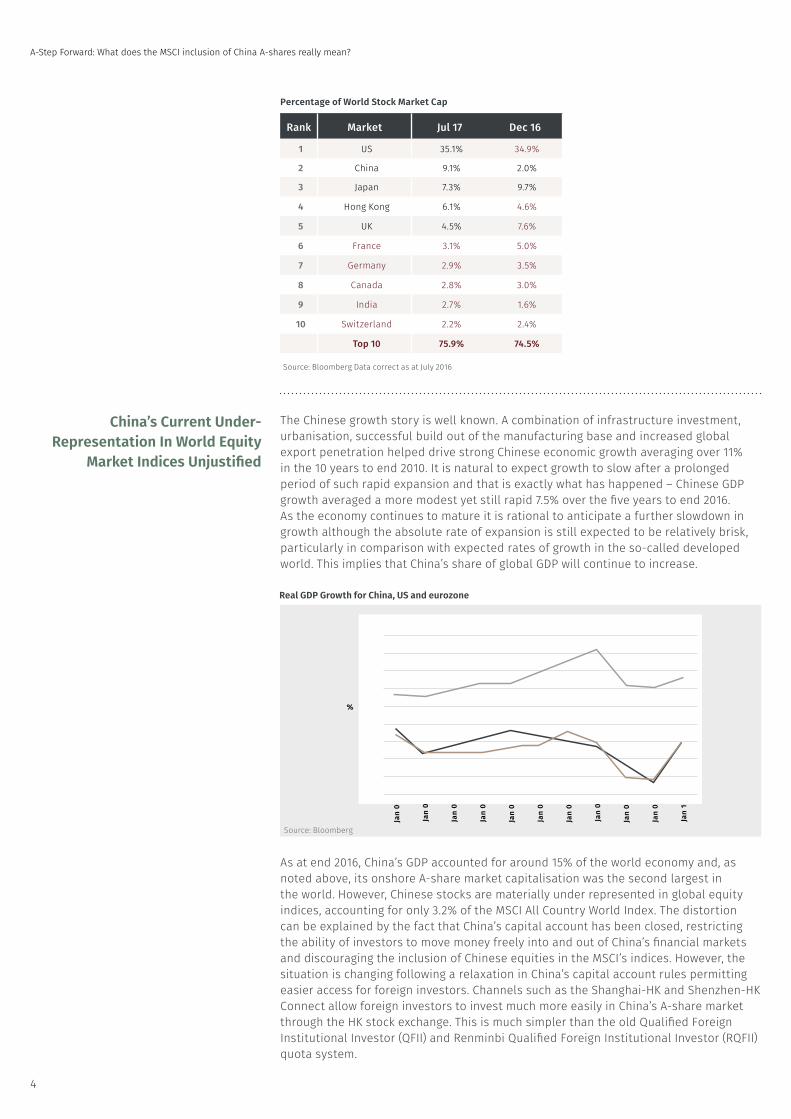

China’s Current Under-Representation In World Equity

Market Indices Unjustified

The Chinese growth story is well known. A combination of infrastructure investment, urbanisation, successful build out of the manufacturing base and increased global export penetration helped drive strong Chinese economic growth averaging over 11% in the 10 years to end 2010. It is natural to expect growth to slow after a prolonged period of such rapid expansion and that is exactly what has happened – Chinese GDP growth averaged a more modest yet still rapid 7.5% over the five years to end 2016. As the economy continues to mature it is rational to anticipate a further slowdown in growth although the absolute rate of expansion is still expected to be relatively brisk, particularly in comparison with expected rates of growth in the so-called developed world. This implies that China’s share of global GDP will continue to increase.

As at end 2016, China’s GDP accounted for around 15% of the world economy and, as noted above, its onshore A-share market capitalisation was the second largest in the world. However, Chinese stocks are materially under represented in global equity indices, accounting for only 3.2% of the MSCI All Country World Index. The distortion can be explained by the fact that China’s capital account has been closed, restricting the ability of investors to move money freely into and out of China’s financial markets and discouraging the inclusion of Chinese equities in the MSCI’s indices. However, the situation is changing following a relaxation in China’s capital account rules permitting easier access for foreign investors. Channels such as the Shanghai-HK and Shenzhen-HK Connect allow foreign investors to invest much more easily in China’s A-share market through the HK stock exchange. This is much simpler than the old Qualified Foreign Institutional Investor (QFII) and Renminbi Qualified Foreign Institutional Investor (RQFII)quota system.

Source: Bloomberg Data correct as at July 2016

Percentage of World Stock Market Cap

Rank Market Jul 17 Dec 16

1 US 35.1% 34.9%

2 China 9.1% 2.0%

3 Japan 7.3% 9.7%

4 Hong Kong 6.1% 4.6%

5 UK 4.5% 7.6%

6 France 3.1% 5.0%

7 Germany 2.9% 3.5%

8 Canada 2.8% 3.0%

9 India 2.7% 1.6%

10 Switzerland 2.2% 2.4%

Top 10 75.9% 74.5%

16

14

12

10

8

% 6

4

2

0

-2

-4

China US eurozone

Jan

10

Jan

09

Jan

08

Jan

07

Jan

06

Jan

05

Jan

04

Jan

03

Jan

02

Jan

01

Jan

00

Real GDP Growth for China, US and eurozone

Source: Bloomberg

As the table below shows, the Stock Connect programs broaden the eligible investor base from only large, qualified institutional investors, to all overseas investors including individuals. More importantly, there will be no lock-up period. The experience of Korea and Taiwan suggests that full inclusion (100% inclusion factor) for Chinese A-shares will take around 5-10 years.

Following introduction of the Stock Connect arrangements, the MSCI now considers Chinese A-shares to be sufficiently investible to be included in its indices for the first time. The MSCI have initiated the index position with only a 5% weight (only 5% of the free float A-share market cap will be included in calculating the index weight) but will expand the weighting ultimately to full inclusion when China opens its capital account further. In view of these developments and as the index weighting of Chinese shares increases over time, so we would expect the market to attract flows from foreign investors who tend to allocate to regional equities based at least in part on country weightings in global indices. Passive investment vehicles, for instance, are obliged to mimic very closely those global weightings. In turn one would expect enhanced foreign flows to push prices higher.

One would expect enhanced foreign flows to push prices higher

Percentage of World GDP vs. MSCI ACWI Index Weighting

Source: BloombergGDP data as at 30 June 2017. MSCI data as at 4 July 2017

US China Japan Germany UK France Canada SouthKorea

0

10

20

30

40

50

60

GDP Weight MSCI ACWI Index Weight

Australia Switzerland Other

55

* Individual investors must have balance of at least 500,000 in their cash and securities accounts.

** Stocks, bonds, warrents, funds, index futures fixed income products in interbank-market; primary market activities such as IPO, convertible bond issuance, additional shares issuance and seasoned equity offerings.

*** Shares acquired as entitlements can only be sold if they are not one of the eligible stocks of the Stock Connect but are SSE-listed and cannot be bought or sold using the Stock Connect scheme if they are not SSE-listed.

Source: Shanghai Stock Exchange (SSE)

Stock Connect QFII RQFII

Eligible Investor

SSE Members, institutional investors

& indiviual investors* in Mainland for HK Stock

Connect trades Selected institutional investors

Selected institutional investors

All Hong Kong and overseas investors for

Shanghai Stock Connect trades

Currency Transactions in RMB Transactions in USD and other foreign currencies Transactions in RMB

Quota Applies to market as a whole

Allocated to each institutional investor

Allocated to offshore regions

Eligible Products Selected A-listed and H-listed Stocks

RMB denominated products approved by

CSRC**

RMB denominated products approved by

CSRC

Regulation of Funds Funds must return to origin; No lock-up period

Funds subject to lock-up period and can stay in mainland afterwards

Funds subject to lock-up period and can stay in mainland afterwards

Investors’ Rights Subject to limitations*** No limitations No limitations

A-Step Forward: What does the MSCI inclusion of China A-shares really mean?

The increase in weighting of Chinese A-shares in the MSCI indices going forward will encourage meaningful flow

6

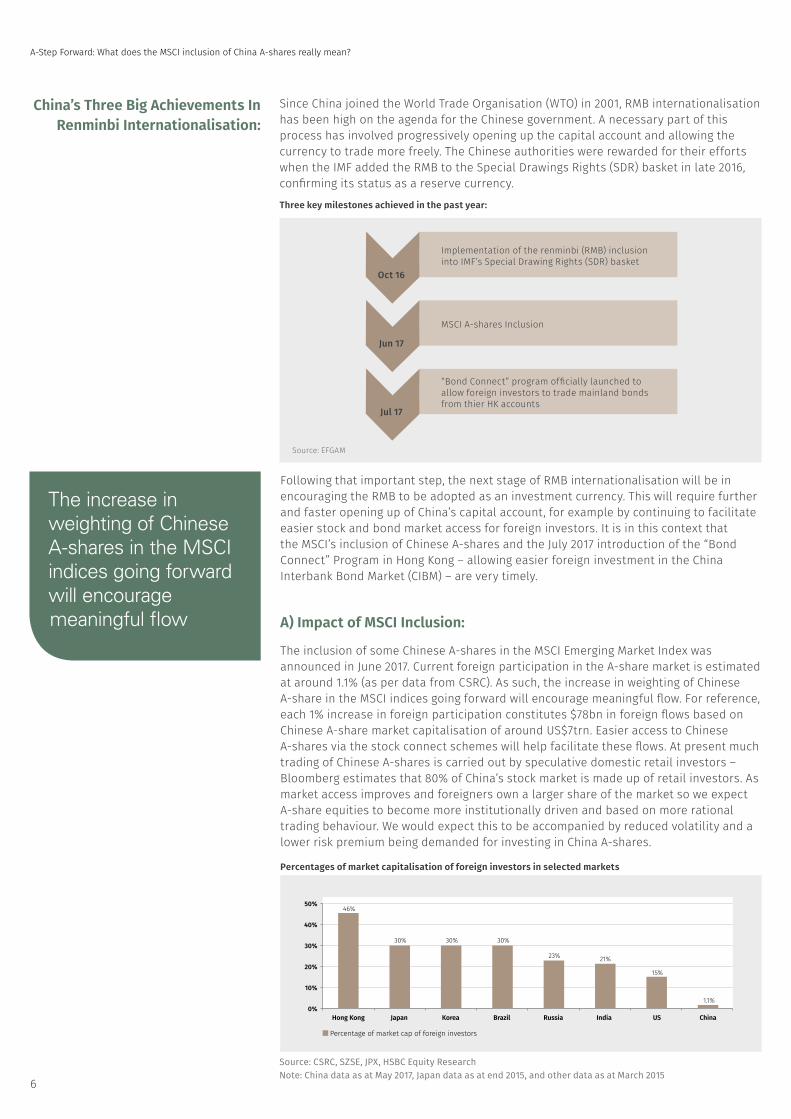

Following that important step, the next stage of RMB internationalisation will be in encouraging the RMB to be adopted as an investment currency. This will require further and faster opening up of China’s capital account, for example by continuing to facilitate easier stock and bond market access for foreign investors. It is in this context that the MSCI’s inclusion of Chinese A-shares and the July 2017 introduction of the “Bond Connect” Program in Hong Kong – allowing easier foreign investment in the China Interbank Bond Market (CIBM) – are very timely.

A) Impact of MSCI Inclusion:

The inclusion of some Chinese A-shares in the MSCI Emerging Market Index was announced in June 2017. Current foreign participation in the A-share market is estimated at around 1.1% (as per data from CSRC). As such, the increase in weighting of Chinese A-share in the MSCI indices going forward will encourage meaningful flow. For reference, each 1% increase in foreign participation constitutes $78bn in foreign flows based on Chinese A-share market capitalisation of around US$7trn. Easier access to Chinese A-shares via the stock connect schemes will help facilitate these flows. At present much trading of Chinese A-shares is carried out by speculative domestic retail investors – Bloomberg estimates that 80% of China’s stock market is made up of retail investors. As market access improves and foreigners own a larger share of the market so we expect A-share equities to become more institutionally driven and based on more rational trading behaviour. We would expect this to be accompanied by reduced volatility and a lower risk premium being demanded for investing in China A-shares.

China’s Three Big Achievements In Renminbi Internationalisation:

Since China joined the World Trade Organisation (WTO) in 2001, RMB internationalisation has been high on the agenda for the Chinese government. A necessary part of this process has involved progressively opening up the capital account and allowing the currency to trade more freely. The Chinese authorities were rewarded for their efforts when the IMF added the RMB to the Special Drawings Rights (SDR) basket in late 2016, confirming its status as a reserve currency.

Source: EFGAM

MSCI A-shares Inclusion

Jun 17

“Bond Connect” program officially launched to allow foreign investors to trade mainland bonds from thier HK accounts

Jul 17

Implementation of the renminbi (RMB) inclusion into IMF’s Special Drawing Rights (SDR) basket

Oct 16

Three key milestones achieved in the past year:

Percentages of market capitalisation of foreign investors in selected markets

Source: CSRC, SZSE, JPX, HSBC Equity ResearchNote: China data as at May 2017, Japan data as at end 2015, and other data as at March 2015

Hong Kong

46%

30% 30% 30%

23% 21%

15%

1.1%

Japan Korea Brazil Russia India US China0%

10%

20%

30%

40%

50%

Percentage of market cap of foreign investors

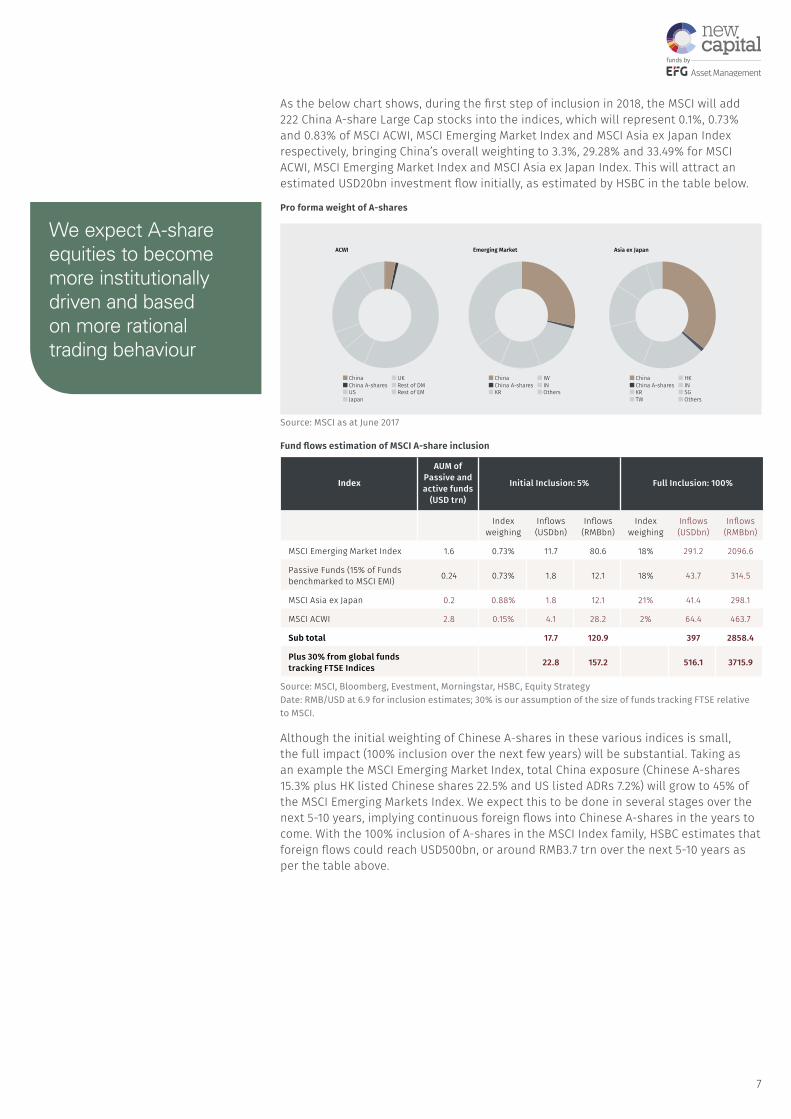

As the below chart shows, during the first step of inclusion in 2018, the MSCI will add 222 China A-share Large Cap stocks into the indices, which will represent 0.1%, 0.73% and 0.83% of MSCI ACWI, MSCI Emerging Market Index and MSCI Asia ex Japan Index respectively, bringing China’s overall weighting to 3.3%, 29.28% and 33.49% for MSCI ACWI, MSCI Emerging Market Index and MSCI Asia ex Japan Index. This will attract an estimated USD20bn investment flow initially, as estimated by HSBC in the table below.

Pro forma weight of A-shares

Source: MSCI as at June 2017

ChinaChina A-sharesUSJapan TW Others

UKRest of DMRest of EM

ChinaChina A-sharesKR

IWINOthers

ChinaChina A-sharesKR

HKINSG

ACWI Emerging Market Asia ex Japan

We expect A-share equities to become more institutionally driven and based on more rational trading behaviour

Although the initial weighting of Chinese A-shares in these various indices is small, the full impact (100% inclusion over the next few years) will be substantial. Taking as an example the MSCI Emerging Market Index, total China exposure (Chinese A-shares 15.3% plus HK listed Chinese shares 22.5% and US listed ADRs 7.2%) will grow to 45% of the MSCI Emerging Markets Index. We expect this to be done in several stages over the next 5-10 years, implying continuous foreign flows into Chinese A-shares in the years to come. With the 100% inclusion of A-shares in the MSCI Index family, HSBC estimates that foreign flows could reach USD500bn, or around RMB3.7 trn over the next 5-10 years as per the table above.

77

Index

AUM of Passive and active funds

(USD trn)

Initial Inclusion: 5% Full Inclusion: 100%

Index weighing

Inflows (USDbn)

Inflows (RMBbn)

Index weighing

Inflows (USDbn)

Inflows (RMBbn)

MSCI Emerging Market Index 1.6 0.73% 11.7 80.6 18% 291.2 2096.6

Passive Funds (15% of Funds benchmarked to MSCI EMI) 0.24 0.73% 1.8 12.1 18% 43.7 314.5

MSCI Asia ex Japan 0.2 0.88% 1.8 12.1 21% 41.4 298.1

MSCI ACWI 2.8 0.15% 4.1 28.2 2% 64.4 463.7

Sub total 17.7 120.9 397 2858.4

Plus 30% from global funds tracking FTSE Indices 22.8 157.2 516.1 3715.9

Fund flows estimation of MSCI A-share inclusion

Source: MSCI, Bloomberg, Evestment, Morningstar, HSBC, Equity Strategy Date: RMB/USD at 6.9 for inclusion estimates; 30% is our assumption of the size of funds tracking FTSE relative to MSCI.

A-Step Forward: What does the MSCI inclusion of China A-shares really mean?

We foresee the valuation gap between A and H-shares narrowing

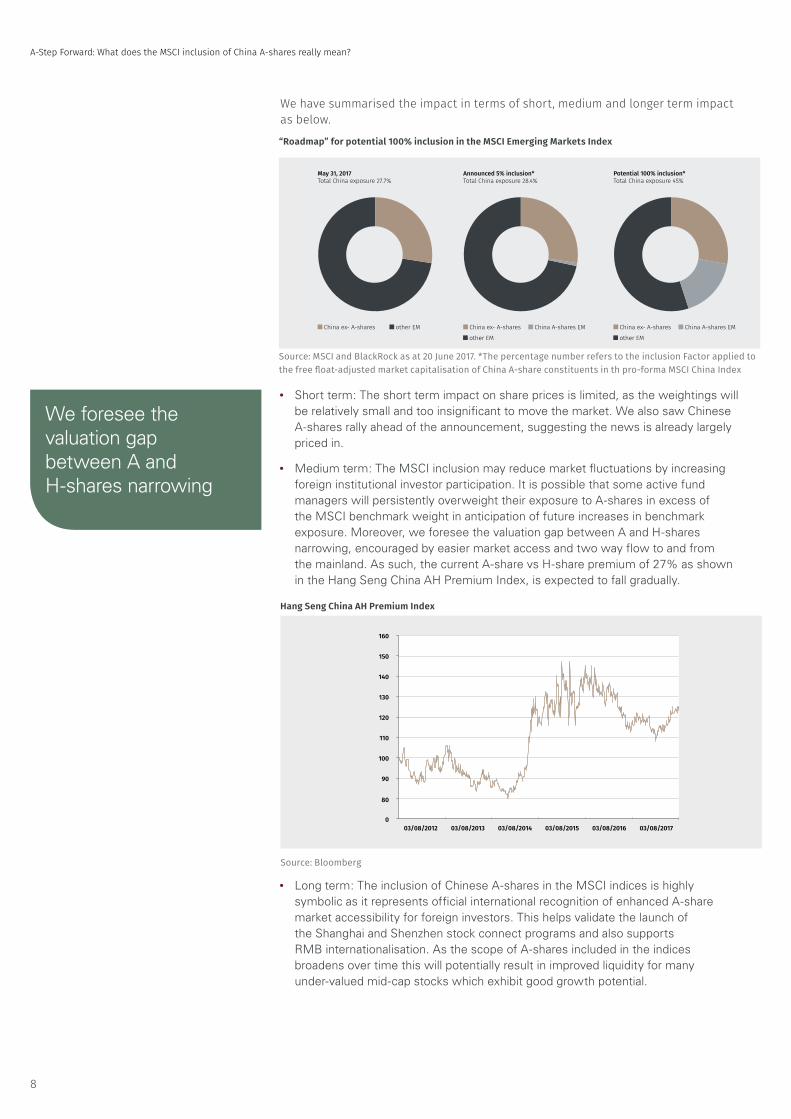

We have summarised the impact in terms of short, medium and longer term impact as below.

• Long term: The inclusion of Chinese A-shares in the MSCI indices is highly symbolic as it represents official international recognition of enhanced A-share market accessibility for foreign investors. This helps validate the launch of the Shanghai and Shenzhen stock connect programs and also supports RMB internationalisation. As the scope of A-shares included in the indices broadens over time this will potentially result in improved liquidity for many under-valued mid-cap stocks which exhibit good growth potential.

• Short term: The short term impact on share prices is limited, as the weightings will be relatively small and too insignificant to move the market. We also saw Chinese A-shares rally ahead of the announcement, suggesting the news is already largely priced in.

• Medium term: The MSCI inclusion may reduce market fluctuations by increasing foreign institutional investor participation. It is possible that some active fund managers will persistently overweight their exposure to A-shares in excess of the MSCI benchmark weight in anticipation of future increases in benchmark exposure. Moreover, we foresee the valuation gap between A and H-shares narrowing, encouraged by easier market access and two way flow to and from the mainland. As such, the current A-share vs H-share premium of 27% as shown in the Hang Seng China AH Premium Index, is expected to fall gradually.

Hang Seng China AH Premium Index

8

“Roadmap” for potential 100% inclusion in the MSCI Emerging Markets Index

Source: MSCI and BlackRock as at 20 June 2017. *The percentage number refers to the inclusion Factor applied to the free float-adjusted market capitalisation of China A-share constituents in th pro-forma MSCI China Index

China ex- A-shares other EM

May 31, 2017Total China exposure 27.7%

China ex- A-shares China A-shares EM

other EM

Announced 5% inclusion*Total China exposure 28.4%

China ex- A-shares China A-shares EM

other EM

Potential 100% inclusion* Total China exposure 45%

Source: Bloomberg

0

90

80

100

110

120

130

140

150

160

Hang Seng China AH Premium Index

03/08/2012 03/08/2013 03/08/2014 03/08/2015 03/08/2016 03/08/2017

1990

0

50

100

150

200

250

300

350

400

450

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

MSCI AP exJ KOSPI Index

50% market cap Tawain stocks

MSCI Inclusion in Sep 1996 Full market cap

Tawain stocks MSCI inclusion in

Jun 2005

1990

0

50

100

150

200

250

300

350

400

450

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

MXASJ Index KOSPI Index

50% market cap Korean stocks

MSCI inclusion in Sep 1996

Full market cap Korean Stocks

MSCI inclusion in Sep 199820% market cap

Korean stocks MSCI inclusion in

Jan 1992

South Korea’s case

Taiwan’s case

B) Experience of Korea and Taiwan Suggests China A-share Full Inclusion Will Take 5-10 Years

How long will it take for full inclusion of Chinese A-shares into MSCI Indices? In South Korea’s case, the process of full inclusion from an initial 20% inclusion factor took from 1992 to 1998. In Taiwan’s case, the process of full inclusion from an initial 50% inclusion factor took almost 10 years, from 1996 to 2005. Applying these rates to the Chinese market suggests it will take 5-10 years before the full market capitalisation is represented in the MSCI’s indices.

Potentially result in improved liquidity for many under-valued mid-cap stocks which exhibit good growth potential

Source: MSCI and Bloomberg

Source: MSCI and Bloomberg

99

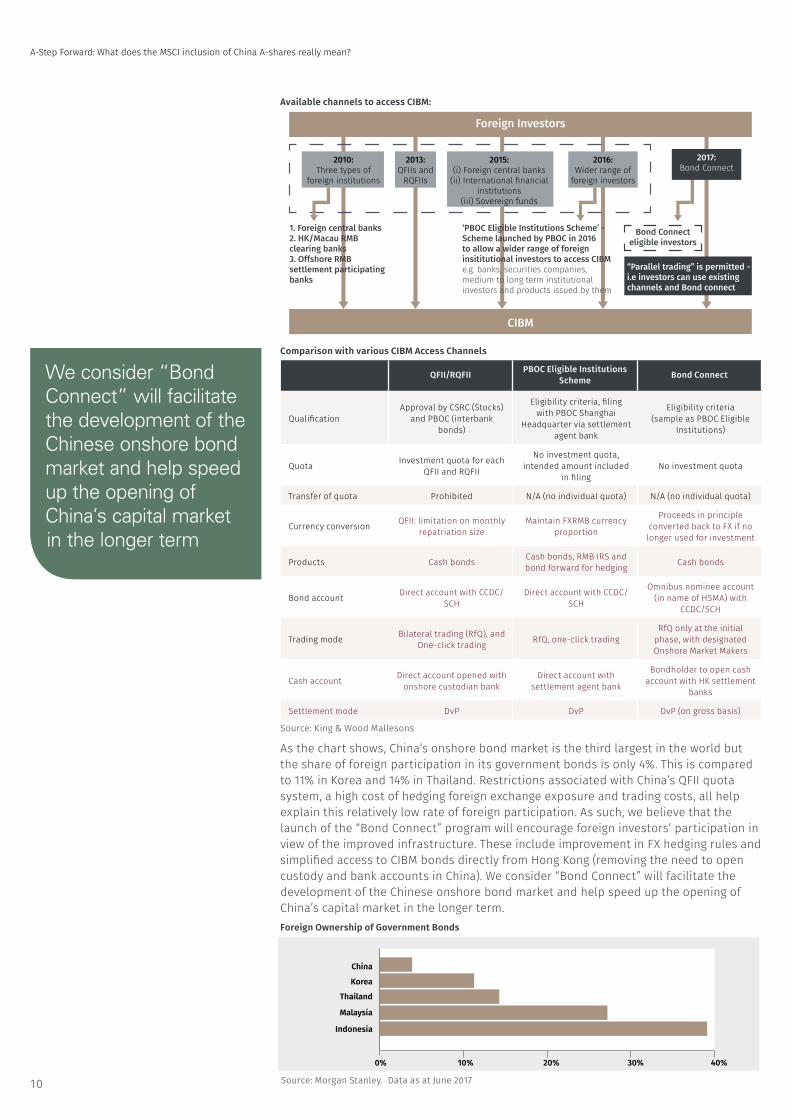

C) Opening Of China Interbank Bond Market (CIBM) via “Bond Connect”

The Bond Connect Program, launched on 1 July 2017, is a new mutual market access scheme which allows Mainland China and overseas investors to trade in each other’s bond markets through a linkage between Mainland China and Hong Kong market infrastructures. Under the new scheme, foreign investor can use offshore electronic trading platforms to execute trades on the CIBM. This is much simpler as foreign investors are no longer required to trade through onshore settlement agents under the existing schemes, namely QFII, RQFII and People’s Bank of China (PBOC) Eligible Institution Scheme.

A-Step Forward: What does the MSCI inclusion of China A-shares really mean?

We consider “Bond Connect” will facilitate the development of the Chinese onshore bond market and help speed up the opening of China’s capital market in the longer term

Available channels to access CIBM:

China

Korea

Thailand

Malaysia

Indonesia

0% 10% 20% 30% 40%

Foreign Ownership of Government Bonds

As the chart shows, China’s onshore bond market is the third largest in the world but the share of foreign participation in its government bonds is only 4%. This is compared to 11% in Korea and 14% in Thailand. Restrictions associated with China’s QFII quota system, a high cost of hedging foreign exchange exposure and trading costs, all help explain this relatively low rate of foreign participation. As such, we believe that the launch of the “Bond Connect” program will encourage foreign investors’ participation in view of the improved infrastructure. These include improvement in FX hedging rules and simplified access to CIBM bonds directly from Hong Kong (removing the need to open custody and bank accounts in China). We consider “Bond Connect” will facilitate the development of the Chinese onshore bond market and help speed up the opening of China’s capital market in the longer term.

Foreign Investors

CIBM

2010:Three types of

foreign institutions

1. Foreign central banks2. HK/Macau RMB clearing banks3. Offshore RMB settlement participating banks

‘PBOC Eligible Institutions Scheme’ - Scheme launched by PBOC in 2016to allow a wider range of foreign insititutional investors to access CIBM e.g. banks, securities companies, medium to long term institutional investors and products issued by them

Bond Connecteligible investors

“Parallel trading” is permitted -i.e investors can use existing channels and Bond connect

2013:QFIIs and

RQFIIs

2015:(i) Foreign central banks

(ii) International financialinstitutions

(iii) Sovereign funds

2016:Wider range of

foreign investors

2017:Bond Connect

Source: Morgan Stanley. Data as at June 201710

QFII/RQFII PBOC Eligible Institutions Scheme Bond Connect

QualificationApproval by CSRC (Stocks)

and PBOC (interbank bonds)

Eligibility criteria, filing with PBOC Shanghai

Headquarter via settlement agent bank

Eligibility criteria (sample as PBOC Eligible

Institutions)

Quota Investment quota for each QFII and RQFII

No investment quota, intended amount included

in filingNo investment quota

Transfer of quota Prohibited N/A (no individual quota) N/A (no individual quota)

Currency conversion QFII: limitation on monthly repatriation size

Maintain FXRMB currency proportion

Proceeds in principle converted back to FX if no longer used for investment

Products Cash bonds Cash bonds, RMB IRS and bond forward for hedging Cash bonds

Bond account Direct account with CCDC/SCH

Direct account with CCDC/SCH

Omnibus nominee account (in name of HSMA) with

CCDC/SCH

Trading mode Bilateral trading (RfQ), and One-click trading RfQ, one-click trading

RfQ only at the initial phase, with designated Onshore Market Makers

Cash account Direct account opened with onshore custodian bank

Direct account with settlement agent bank

Bondholder to open cash account with HK settlement

banks

Settlement mode DvP DvP DvP (on gross basis)

Comparison with various CIBM Access Channels

Source: King & Wood Mallesons

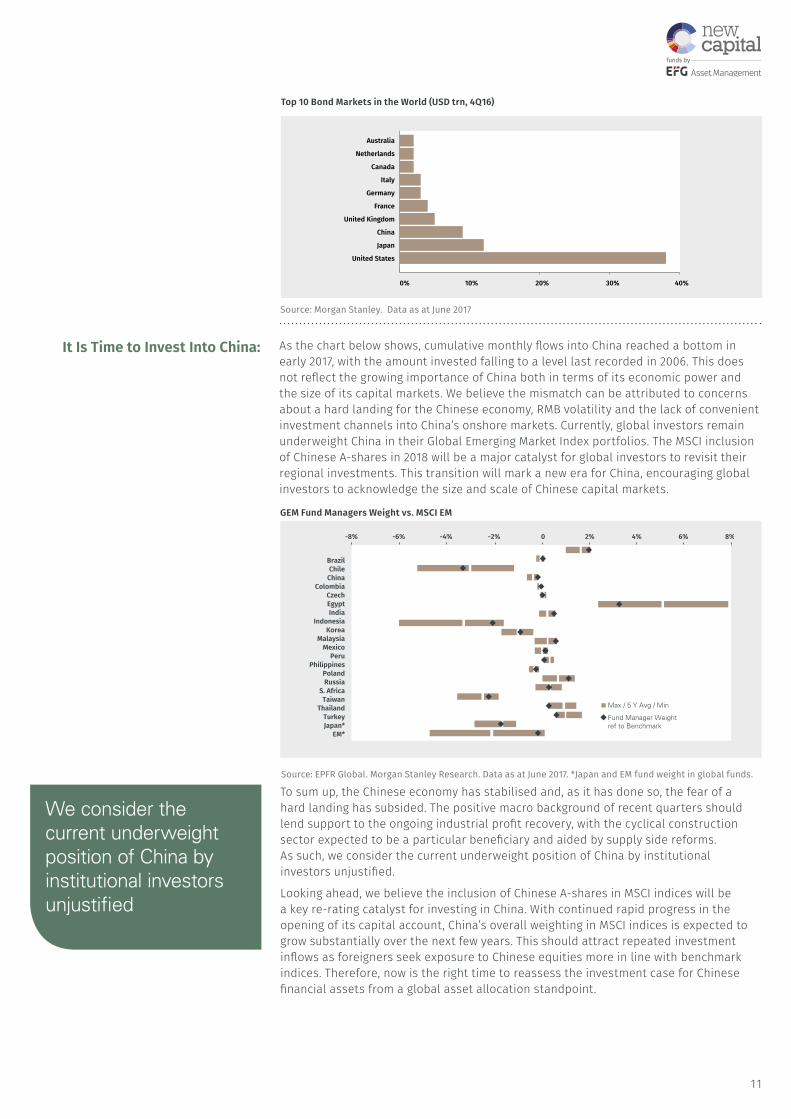

It Is Time to Invest Into China: As the chart below shows, cumulative monthly flows into China reached a bottom in early 2017, with the amount invested falling to a level last recorded in 2006. This does not reflect the growing importance of China both in terms of its economic power and the size of its capital markets. We believe the mismatch can be attributed to concerns about a hard landing for the Chinese economy, RMB volatility and the lack of convenient investment channels into China’s onshore markets. Currently, global investors remain underweight China in their Global Emerging Market Index portfolios. The MSCI inclusion of Chinese A-shares in 2018 will be a major catalyst for global investors to revisit their regional investments. This transition will mark a new era for China, encouraging global investors to acknowledge the size and scale of Chinese capital markets.

-8% -6% -4% -2% 0 2% 4% 6% 8%

BrazilChile

ChinaColombia

CzechEgyptIndia

IndonesiaKorea

MalaysiaMexico

PeruPhilippines

PolandRussia

S. AfricaTaiwan

ThailandTurkeyJapan*

EM*

Fund Manager Weight ref to Benchmark

Max / 5 Y Avg / Min

GEM Fund Managers Weight vs. MSCI EM

We consider the current underweight position of China by institutional investors unjustified

Source: Morgan Stanley. Data as at June 2017

Source: EPFR Global. Morgan Stanley Research. Data as at June 2017. *Japan and EM fund weight in global funds.

Australia

Netherlands

Canada

Italy

Germany

France

United Kingdom

China

Japan

United States

0% 10% 20% 30% 40%

Top 10 Bond Markets in the World (USD trn, 4Q16)

1111

To sum up, the Chinese economy has stabilised and, as it has done so, the fear of a hard landing has subsided. The positive macro background of recent quarters should lend support to the ongoing industrial profit recovery, with the cyclical construction sector expected to be a particular beneficiary and aided by supply side reforms. As such, we consider the current underweight position of China by institutional investors unjustified.

Looking ahead, we believe the inclusion of Chinese A-shares in MSCI indices will be a key re-rating catalyst for investing in China. With continued rapid progress in the opening of its capital account, China’s overall weighting in MSCI indices is expected to grow substantially over the next few years. This should attract repeated investment inflows as foreigners seek exposure to Chinese equities more in line with benchmark indices. Therefore, now is the right time to reassess the investment case for Chinese financial assets from a global asset allocation standpoint.

A-Step Forward: What does the MSCI inclusion of China A-shares really mean?

Important InformationNote: Past performance is not necessarily a guide to the future. Returns may increase or decrease as a result of currency fluctuations. Performance is net of fees. Please refer to the Prospectus for further information on this Fund and prior to any subscription.This document does not constitute and shall not be construed as a prospectus, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any investment, security, other financial instrument or other product or service. This document is for general information only and is not intended as investment advice or any other specific recommendation as to any particular course of action or inaction. The information in this document does not take into account the specific investment objectives, financial situation, tax situation or particular needs of the recipient. You should seek your own professional advice (including tax advice) suitable to your particular circumstances prior to making any investment or if you are in doubt as to the information in this document.This document contains material that may be interpreted in the country in which this document has been communicated as a financial promotion and/or advertisement in relation to investment services, securities or other investments. Accordingly, the information in this document is only intended to be viewed by persons who fall outside the scope of any law that seeks to regulate financial promotions and/or advertisements in the country of your residence or in the country in which this document has been communicated. If you are uncertain about your position under the laws of the country in which this document has been communicated then you should seek clarification by obtaining legal advice.Although information in this document has been obtained from sources believed to be reliable, no member of the EFG group represents or warrants its accuracy, and such information and/or investment research may be inaccurate, incomplete or condensed. Any opinions in this document are subject to change without notice. This document may contain personal opinions which do not necessarily reflect the position of any member of the EFG group. To the fullest extent permissible by law, no member of the EFG group shall be responsible for the consequences of any errors or omissions herein, or reliance upon any opinion or statement contained herein, and each member of the EFG group expressly disclaims any liability, including (without limitation) liability for incidental or consequential damages, arising from the same or resulting from any action or inaction on the part of the recipient in reliance on this document.The value of investments and the income derived from them can fall as well as rise, and any reference to past performance is no indicator of current or future performance. Any past performance data for collective investment schemes may not take account of the commissions and costs incurred on the issue and redemption of shares. Income from an investment may fluctuate. Investment products may be subject to investment risks involving, but not limited to, possible loss of all or part of the principal invested. The risk of loss from investing in commodity and financial futures, foreign exchange contract securities, warrants and index contracts and options can be substantial.The publication or availability of this document in any jurisdiction or country may be contrary to local law or regulation and persons who come into possession of this document should inform themselves of and observe any restrictions. No distribution of this information to anyone other than the designated recipient is intended or authorized. This document may not be reproduced, disclosed or distributed (in whole or in part) to any other person without prior written permission from an authorised member of the EFG group.The information contained in this document is merely a brief summary of key aspects of the New Capital UCITS Fund plc (the “Fund”). More complete information on the Fund can be found in the prospectus or key investor information document, and the most recent audited annual report and the most recent semi-annual report. These documents constitute the sole binding basis for the purchase of Fund units. Copies of these documents are available free of charge and may be obtained at the registered office of the Fund at 5 George’s Dock, IFSC, Dublin 1, Ireland; in the United Kingdom from the facilities agent EFG Asset Management (UK) Limited (“EFGAM”), Leconfield House, Curzon Street, London W1J 5JB, United Kingdom; in Germany from the German information agent, HSBC Trinkaus & Burkhardt AG, Königsallee 21/23, 40212 Düsseldorf, Germany; in France from the French centralizing agent, Societe Generale, 29, boulevard Haussmann – 75009 Paris, France; in Luxembourg from the Luxembourg paying agent, HSBC Securities Services (Luxembourg) S.A., 16 boulevard d’Avranches, L-1160 Luxembourg, R.C.S. Luxembourg, B28531; in Austria from the Austrian paying and information agent, Erste Bank der oesterreichischen Sparkasse AG Graben 21, 1010 Vienna, Austria; in Sweden from the Swedish paying agent, MFEX Mutual Funds Exchange AB, Linnégatan 9-11, 11 447 Stockholm, Sweden; and in Switzerland from the Swiss representative,

CACEIS (Switzerland) SA, Route de Signy 35, CH-1260 Nyon and the paying agent, EFG Bank AG, Bleicherweg 8, 8022 Zurich.Hong Kong: This document does not constitute an offer, solicitation or invitation, publicity or any other advice or recommendation. The information contained within this document has been obtained from sources believed to be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness, accuracy or completeness of the information. Investment involves risk. Past performance is not indicative of future results. Before making any investment decision to invest in the Fund, you should read the Hong Kong offering documents and especially the risk factors therein. An investment in the Fund may not be suitable for everyone. If you are in any doubt about the contents of this document, you should consult your stockbroker, bank manager, solicitor, accountant or other financial adviser for independent professional advice. This document is issued by EFG Asset Management (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission (“SFC”) in Hong Kong. The SFC takes no responsibility for the contents of this statement and makes no representation as to its accuracy or completeness.Singapore: The Fund is not authorised or recognised by the Monetary Authority of Singapore (the “MAS”) and the shares in the Fund (the “Shares”) are not allowed to be offered to the Singapore retail public. Moreover, this presentation, and any other document or material issued in connection with the offer or sale is not a prospectus as defined in the Securities and Futures Act, Chapter 289 of Singapore (“SFA”). Accordingly, statutory liability under the SFA in relation to the content of prospectuses would not apply. You should consider carefully whether the investment is suitable for you. This presentation has not been registered as a prospectus by the MAS, and the offer of the Shares is made pursuant to the exemptions under Sections 304 and 305 of the SFA. Accordingly, the Shares may not be offered or sold, nor may the Shares be the subject of an invitation for subscription or purchase, nor may this presentation or any other document or material in connection with the offer or sale, or invitation for subscription or purchase of the Shares be circulated or distributed, whether directly or indirectly, to any person in Singapore other than under exemptions provided in the SFA for offers made (a) to an institutional investor (as defined in Section 4A of the SFA) pursuant to Section 304 of the SFA, (b) to a relevant person (as defined in Section 305(5) of the SFA), or any person pursuant to an offer referred to in Section 305(2) of the SFA, and in accordance with the conditions specified in Section 305 of the SFA or (c) otherwise pursuant to, and in accordance with, the conditions of any other applicable provision of the SFA. Where the Shares are acquired by persons who are relevant persons specified in Section 305A of the SFA, namely: a) a corporation (which is not an accredited investor (as defined in Section 4A

of the SFA)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or

b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an individual who is an accredited investor,

the shares, debentures and units of shares and debentures of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within six months after that corporation or that trust has acquired the Shares pursuant to an offer made under Section 305 of the SFA except: 1. to an institutional investor or to a relevant person as defined in Section 305(5)

of the SFA, or which arises from an offer referred to in Section 275(1A) of the SFA (in the case of that corporation) or Section 305A(3)(i)(B) of the SFA (in the case of that trust);

2. where no consideration is or will be given for the transfer; 3. where the transfer is by operation of law; 4. as specified in Section 305A(5) of the SFA; or 5. as specified in Regulation 36 of the Securities and Futures (Offers of

Investments) (Collective Investment Schemes) Regulations 2005 of Singapore. The offer, holding and subsequent transfer of Shares are subject to restrictions and conditions under the SFA. You should consider carefully whether you are permitted (under the SFA and any laws or regulations applicable to you) to make an investment in the Shares and whether any such investment is suitable for you and you should consult your legal or professional advisor if in doubt.

This document has been produced by EFG Asset Management (UK) Limited for use by the EFG group and the worldwide subsidiaries and affiliates within the EFG group. EFG Asset Management (UK) Limited is authorised and regulated by the UK Financial Conduct Authority, registered no. 7389746. Registered address: EFG Asset Management (UK) Limited, Leconfield House, Curzon Street, London W1J 5JB, United Kingdom, telephone +44 (0)20 7491 9111.