chapter iv an analysis of level of customers...

TRANSCRIPT

194

CHAPTER IV

AN ANALYSIS OF LEVEL OF CUSTOMERS AWARENESS

IN RETAIL BANKING SERVICES

INRODUCTION

The awareness of customers towards retail banking services would have an

impact on the utilization of these services. The banks render various retail banking

services to their customers. Due to technological advancement, the retail banking

services offered by banks have improved to a greater extent. However, the usage of

these services would depend highly on the awareness of customers towards these

services. In this study, an attempt has been made to analyze the level of awareness

of customers towards various retail banking services offered by banks in Salem

District. In this regard, 25 retail banking services as listed below have been

selected:

1. E – Banking Facility/Core Banking

2. Credit card facility

3. ECS for payment of loan installment

4. Teller facility

5. Housing loan

6. Personal loans

7. Electronic clearance service

8. Educational loans

9. Agency service

10. Inter – bank deposits facility

11. Vehicle loan

195

12. Safety locker facility

13. RTGS/NEFT (Electronic Fund Transfer)

14. Jewel loan

15. Overdraft

16. NRI Deposit

17. Provision of 24 hrs free phone services

18. Services to senior citizens

19. Rates of interest on various deposits

20. Counseling on post retirement services

21. Interest rate option/Fixed and floating rate on loan

22. Conversion of excess balance to time deposit

23. Sunday banking facility

24. Tele-banking and

25. Insurance products

The sample respondents were asked to indicate their level of awareness

towards these retail banking services in a five-point rating scale – Fully aware,

Partially aware, Just aware, Not aware and Not at all aware. The responses given

by the respondents were assigned scores like 5 for fully aware, 4 for partially aware,

3 for just aware, 2 for not aware and 1 for not at all aware. These scores have been

summed up and on the basis of total scores, the level of awareness has been

classified as low, medium and high. The scores between 25 and 41 were considered

as low level, while the scores between 42 and 58 were categorized as medium level

and the scores above 59 but less than or equal to 75 were grouped as high level. On

the basis of these scores and levels, the relationships between demographic

196

variables and level of awareness, ownership pattern of the bank and level of

awareness and frequency of operations and level of awareness have been examined

in this chapter.

TABLE 4.1

GENDER AND AWARENESS ON RETAIL BANKING SERVICES

Gender No. of respondents % Mean Minimum Maximum S.D.

Male 348 69.60 71.20 33 125 14.83

Female 152 30.40 72.61 35 116 15.65

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.1 shows that the average score of awareness of male customers was

found to be 71.20 which ranged between 33 and 125 with a standard deviation of

14.83. The mean score of awareness of female customers was found to be 72.61

which ranged between 35 and 116 with a standard deviation of 15.65. It denotes

that the mean score of awareness of female customers (72.61) was higher than

the mean score of awareness of male customers (71.20). However, the maximum

score of male customers (125) was found to be greater than that of female

customers (116).

TABLE 4.2

GENDER AND AWARENESS ON RETAIL BANKING SERVICES –

TWO WAY TABLE

Gender Level of Awareness

Low Medium High Total

Male 66

(67.35)

259

(70.57)

23

(65.71)

348

Female 32

(32.65)

108

(29.43)

12

(34.29)

152

Total 98 367 35 500

Source: Computed from the Primary Data

197

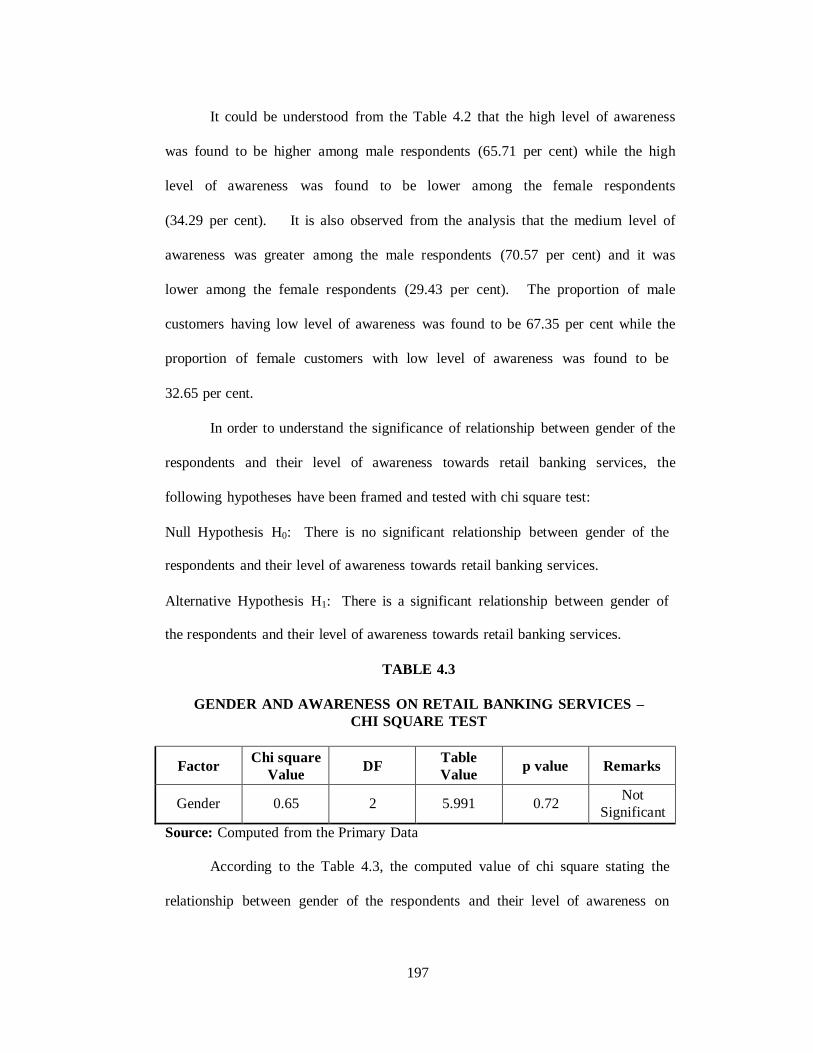

It could be understood from the Table 4.2 that the high level of awareness

was found to be higher among male respondents (65.71 per cent) while the high

level of awareness was found to be lower among the female respondents

(34.29 per cent). It is also observed from the analysis that the medium level of

awareness was greater among the male respondents (70.57 per cent) and it was

lower among the female respondents (29.43 per cent). The proportion of male

customers having low level of awareness was found to be 67.35 per cent while the

proportion of female customers with low level of awareness was found to be

32.65 per cent.

In order to understand the significance of relationship between gender of the

respondents and their level of awareness towards retail banking services, the

following hypotheses have been framed and tested with chi square test:

Null Hypothesis H0: There is no significant relationship between gender of the

respondents and their level of awareness towards retail banking services.

Alternative Hypothesis H1: There is a significant relationship between gender of

the respondents and their level of awareness towards retail banking services.

TABLE 4.3

GENDER AND AWARENESS ON RETAIL BANKING SERVICES –

CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Gender

0.65

2

5.991

0.72 Not

Significant

Source: Computed from the Primary Data

According to the Table 4.3, the computed value of chi square stating the

relationship between gender of the respondents and their level of awareness on

198

retail banking services was 0.65 while the table value at 5% level of significance for

2 degrees of freedom was 5.991 and the p value was 0.72. Since the computed

value was lesser than the table value, it falls in the acceptance region. Hence, the

null hypothesis is accepted and the alternative hypothesis is rejected. The

hypothesis that ‘gender of the respondents and their level of awareness on retail

banking services are not significantly related’ holds good. Thus, it is concluded

that there is no significant relationship between gender of the respondents and their

level of awareness on retail banking services.

TABLE 4.4

AGE AND AWARENESS ON RETAIL BANKING SERVICES

Age

No. of

responde

nts

%

Mean

Minimum

Maximum

S.D.

Up to 20

years

50

10.00

72.52

48

101

11.66

21 to 30

years

284

56.80

72.48

33

125

15.15

31 to 40

years

112

22.40

71.99

35

106

14.56

Above

40 years

54

10.80

65.57

39

100

17.44

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.4 shows that the average score of awareness of customers in the age

group of up to 20 years was found to be 72.52 which ranged between 48 and 101

with a standard deviation of 11.66. The mean score of awareness of customers in

the age group of 21 to 30 years was found to be 72.48 which ranged between 33 and

125 with a standard deviation of 15.15. It is also found that the average score of

awareness of customers in the age group of 31 to 40 years was 71.99 which ranged

between 35 and 106 with a standard deviation of 14.56 while the average score of

199

awareness of customers in the age group of above 40 years was found to be 65.57

which ranged between 39 and 100 with a standard deviation of 17.44.

It denotes that the mean score of awareness of customers in the age group of

up to 20 years (72.52) was higher than the mean score of awareness of all the other

customers. However, the maximum score of customers in the age group of 20 to 40

years (125) was found to be greater than that of the other customers.

TABLE 4.5

AGE AND AWARENESS ON RETAIL BANKING SERVICES –

TWO WAY TABLE

Age Level of Awareness

Low Medium High Total

Up to 20 years 6

(6.12)

42

(11.44)

2

(5.71)

50

21 to 30 years 46

(46.94)

215

(58.58)

23

(65.71)

284

31 to 40 years 23

(23.47)

81

(22.07)

8

(22.86)

112

Above 40 years 23

(23.47)

29

(7.90)

2

(5.71)

54

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.5 that the high level of awareness

was found to be higher among respondents in the age group of up to 20 years

(65.71 per cent) while the high level of awareness was found to be lower among the

respondents in the age group of above 40 years (5.71 per cent). It is also observed

from the analysis that the medium level of awareness was greater among the

respondents in the age group of 21 to 30 years (58.58 per cent) and it was lower

among the respondents in the age group of above 40 years (7.90 per cent). The

proportion of customers in the age group of 21 to 30 years having low level of

200

awareness was found to be 46.94 per cent while the proportion of customers in the

age group of up to 20 years with low level of awareness was found to be

6.12 per cent.

In order to understand the significance of relationship between age group of

the respondents and their level of awareness towards retail banking services, the

following hypotheses have been framed and tested with chi square test:

Null Hypothesis H0: There is no significant relationship between age group of the

respondents and their level of awareness towards retail banking services.

Alternative Hypothesis H1: There is a significant relationship between age group of

the respondents and their level of awareness towards retail banking services.

TABLE 4.6

AGE AND AWARENESS ON RETAIL BANKING SERVICES – CHI

SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Age

23.58

6

16.812

0.00 Significant

@ 1%

Source: Computed from the Primary Data

According to the Table 4.6, the computed value of chi square stating the

relationship between age of the respondents and their level of awareness on retail

banking services was 23.58 while the table value at 1% level of significance for 6

degrees of freedom was 16.812 and the p value was 0.00. Since the computed value

was greater than the table value, it falls in the rejection region. Hence, the null

hypothesis is rejected and the alternative hypothesis is accepted. The hypothesis

that ‘age of the respondents and their level of awareness on retail banking services

are not significantly related’ does not hold good. Thus, it is concluded that there is

201

a significant relationship between age of the respondents and their level of

awareness on retail banking services.

TABLE 4.7

MARITAL STATUS AND AWARENESS ON RETAIL BANKING

SERVICES

Marital

Status

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Married 230 46.00 70.61 35 116 16.34

Unmarri

ed

270

54.00

72.49

33

125

13.89

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.7 shows that the average score of awareness of married customers

was found to be 70.61 which ranged between 35 and 116 with a standard deviation

of 16.34. The mean score of awareness of unmarried customers was found to be

72.49 which ranged between 33 and 125 with a standard deviation of 13.89. It

denotes that the mean score of awareness of unmarried customers (72.49) was

higher than the mean score of awareness of married customers (70.61). Similarly,

the maximum score of unmarried customers (125) was found to be greater than that

of married customers (116).

TABLE 4.8

MARITAL STATUS AND AWARENESS ON RETAIL BANKING

SERVICES – TWO WAY TABLE

Marital Status Level of Awareness

Low Medium High Total

Married 62

(63.27)

151

(41.14)

17

(48.57)

230

Unmarried 36

(36.73)

216

(58.86)

18

(51.43)

270

Total 98 367 35 500

Source: Computed from the Primary Data

202

It could be understood from the Table 4.8 that the high level of awareness

was found to be higher among unmarried respondents (51.43 per cent) while the

high level of awareness was found to be lower among the married respondents

(48.57 per cent). It is also observed from the analysis that the medium level of

awareness was greater among the unmarried respondents (58.86 per cent) and it was

lower among the married respondents (41.14 per cent). On the other hand, the

proportion of married customers having low level of awareness was found to be

63.27 per cent while the proportion of unmarried customers with low level of

awareness was found to be 36.73 per cent.

In order to understand the significance of relationship between marital status

of the respondents and their level of awareness towards retail banking services, the

following hypotheses have been framed and tested with chi square test:

Null Hypothesis H0: There is no significant relationship between marital status of

the respondents and their level of awareness towards retail banking services.

Alternative Hypothesis H1: There is a significant relationship between marital

status of the respondents and their level of awareness towards retail banking

services.

TABLE 4.9

MARITAL STATUS AND AWARENESS ON RETAIL BANKING

SERVICES – CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Marital

Status

15.34

2

9.21

0.00 Significant

@ 1%

Source: Computed from the Primary Data

203

According to the Table 4.9, the computed value of chi square stating the

relationship between marital status of the respondents and their level of awareness

on retail banking services was 15.34 while the table value at 1% level of

significance for 2 degrees of freedom was 9.21 and the p value was 0.00. Since the

computed value was greater than the table value, it falls in the rejection region.

Hence, the null hypothesis is rejected and the alternative hypothesis is accepted.

The hypothesis that ‘marital status of the respondents and their level of awareness

on retail banking services are not significantly related’ does not hold good. Thus, it

is concluded that there is a significant relationship between marital status of the

respondents and their level of awareness on retail banking services.

TABLE 4.10

EDUCATIONAL QUALIFICATION AND AWARENESS ON RETAIL

BANKING SERVICES

Educational

Qualification

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Illiterate 19 3.80 74.47 50 99 16.04

School Level 98 19.60 65.51 35 102 16.50

UG 188 37.60 71.98 33 110 13.70

PG 164 32.80 75.25 35 125 14.78

Others 31 6.20 67.90 46 94 13.25

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.10 shows that the average score of awareness of illiterate customers

was found to be 74.47 which ranged between 50 and 99 with a standard deviation of

16.04. The mean score of awareness of school level educated customers was found

to be 65.51 which ranged between 35 and 102 with a standard deviation of 16.50. It

is also found that the average score of awareness of UG level educated customers

was 71.98 which ranged between 33 and 110 with a standard deviation of 13.70

204

Educational

Qualification

Level of Awareness

Low Medium High Total

Illiterate 5

(5.10)

12

(3.27)

2

(5.71)

19

School Level 37

(37.76)

55

(14.99)

6

(17.14)

98

UG 25

(25.51)

152

(41.42)

11

(31.43)

188

PG 22

(22.45)

127

(34.60)

15

(42.86)

164

Others 9

(9.18)

21

(5.72)

1

(2.86)

31

Total 98 367 35 500

while the average score of awareness of PG level educated customers was found to

be 75.25 which ranged between 35 and 125 with a standard deviation of 14.78. The

average score of awareness of customers with other levels of educational

qualification was found to be 67.90 with a minimum of 46 and a maximum of 94

whose standard deviation was found to be 13.25.

It denotes that the mean score of awareness of PG level educated customers

(75.25) was higher than the mean score of awareness of all the other customers.

Similarly, the maximum score of PG level educated customers (125) was found to

be greater than that of the other customers.

TABLE 4.11

EDUCATIONAL QUALIFICATION AND AWARENESS ON RETAIL

BANKING SERVICES – TWO WAY TABLE

Source: Computed from the Primary Data

It could be understood from the Table 4.11 that the high level of awareness

was found to be higher among PG level educated respondents (42.86 per cent)

while the high level of awareness was found to be lower among the respondents

with other educational qualifications (2.86 per cent). It is also observed from the

analysis that the medium level of awareness was greater among the UG level

205

educated respondents (41.42 per cent) and it was lower among the illiterate

respondents (3.27 per cent). The proportion of school level educated customers

having low level of awareness was found to be 37.76 per cent while the proportion

of illiterate customers with low level of awareness was found to be 5.10 per cent.

In order to understand the significance of relationship between educational

qualification of the respondents and their level of awareness towards retail banking

services, the following hypotheses have been framed and tested with chi square test:

Null Hypothesis H0: There is no significant relationship between educational

qualification of the respondents and their level of awareness towards retail banking

services.

Alternative Hypothesis H1: There is a significant relationship between educational

qualification of the respondents and their level of awareness towards retail banking

services.

TABLE 4.12

EDUCATIONAL QUALIFICATION AND AWARENESS ON RETAIL

BANKING SERVICES – CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Educational

Qualification

34.02

8

20.09

0.00 Significant

@ 1%

Source: Computed from the Primary Data

According to the Table 4.12, the computed value of chi square stating the

relationship between educational qualification of the respondents and their level of

awareness on retail banking services was 34.02 while the table value at 1% level of

significance for 8 degrees of freedom was 20.09 and the p value was 0.00. Since

the computed value was greater than the table value, it falls in the rejection region.

206

Hence, the null hypothesis is rejected and the alternative hypothesis is accepted.

The hypothesis that ‘educational qualification of the respondents and their level of

awareness on retail banking services are not significantly related’ does not hold

good. Thus, it is concluded that there is a significant relationship between

educational qualification of the respondents and their level of awareness on retail

banking services.

TABLE 4.13

OCCUPATION AND AWARENESS ON RETAIL BANKING SERVICES

Occupation No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Agriculture 63 12.60 63.06 37 109 17.37

Business /

Profession

141

28.20

72.83

37

109

14.92

Employed 197 39.40 73.84 33 125 14.22

Others 99 19.80 70.95 35 96 13.61

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.13 shows that the average score of awareness of customers who

were doing agriculture was found to be 63.06 which ranged between 37 and 109

with a standard deviation of 17.37. The mean score of awareness of customers who

were doing business / profession was found to be 72.83 which ranged between 37

and 109 with a standard deviation of 14.92. It is also found that the average score

of awareness of employed customers was 73.84 which ranged between 33 and 125

with a standard deviation of 14.22 while the average score of awareness of

customers involved in other occupations was found to be 70.95 which ranged

between 35 and 96 with a standard deviation of 13.61.

It denotes that the mean score of awareness of employed customers (73.84)

was higher than the mean score of awareness of all the other customers. Similarly,

207

the maximum score of employed customers (125) was found to be greater than that

of the other customers.

TABLE 4.14

OCCUPATION AND AWARENESS ON RETAIL BANKING SERVICES –

TWO WAY TABLE

Occupation Level of Awareness

Low Medium High Total

Agriculture 29

(29.59)

29

(7.90)

5

(14.29)

63

Business / Profession 26

(26.53)

102

(27.79)

13

(37.14)

141

Employed 23

(23.47)

160

(43.60)

14

(40.00)

197

Others 20

(20.41)

76

(20.71)

3

(8.57)

99

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.14 that the high level of awareness

was found to be higher among employed respondents (40.00 per cent) while the

high level of awareness was found to be lower among the respondents who were

engaged in other occupations (8.57 per cent). It is also observed from the analysis

that the medium level of awareness was greater among the employed respondents

(43.60 per cent) and it was lower among the respondents engaged in the agriculture

(7.90 per cent). The proportion of customers engaged in the agriculture having low

level of awareness was found to be 29.59 per cent while the proportion of

customers involved in any other occupation with low level of awareness was found

to be 20.41 per cent.

208

In order to understand the significance of relationship between occupation

of the respondents and their level of awareness towards retail banking services, the

following hypotheses have been framed and tested with chi square test:

Null Hypothesis H0: There is no significant relationship between occupation of the

respondents and their level of awareness towards retail banking services.

Alternative Hypothesis H1: There is a significant relationship between occupation

of the respondents and their level of awareness towards retail banking services.

TABLE 4.15

OCCUPATION AND AWARENESS ON RETAIL BANKING SERVICES –

CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Occupation

40.43

6

16.812

0.00 Significant

@ 1%

Source: Computed from the Primary Data

According to the Table 4.15, the computed value of chi square stating the

relationship between occupation of the respondents and their level of awareness on

retail banking services was 40.43 while the table value at 1% level of significance

for 6 degrees of freedom was 16.812 and the p value was 0.00. Since the computed

value was greater than the table value, it falls in the rejection region. Hence, the

null hypothesis is rejected and the alternative hypothesis is accepted. The

hypothesis that ‘occupation of the respondents and their level of awareness on retail

banking services are not significantly related’ does not hold good. Thus, it is

concluded that there is a significant relationship between occupation of the

respondents and their level of awareness on retail banking services.

209

TABLE 4.16

MONTHLY INCOME AND AWARENESS ON RETAIL BANKING

SERVICES

Monthly

Income

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Up to Rs.

10000

225

45.00

67.48

35

98

14.26

Rs.10001 to

Rs.20000

161

32.20

74.04

37

116

13.98

Rs.20001 to

Rs.30000

86

17.20

75.47

33

125

17.36

Above

Rs.30000

28

5.60

79.25

49

103

11.15

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.16 shows that the average score of awareness of customers in the

income group of up to Rs.10000 was found to be 67.48 which ranged between 35

and 98 with a standard deviation of 14.26. The mean score of awareness of

customers in the income group of Rs.10001 to Rs.20000 was found to be 74.04

which ranged between 37 and 116 with a standard deviation of 13.98. It is also

found that the average score of awareness of customers in the income group of

Rs.20001 to Rs.30000 was 75.47 which ranged between 33 and 125 with a standard

deviation of 17.36 while the average score of awareness of customers in the income

group of above Rs.30000 was found to be 79.25 which ranged between 49 and 103

with a standard deviation of 11.15.

It denotes that the mean score of awareness of customers in the age group of

above 40 years (79.25) was higher than the mean score of awareness of all the other

customers. However, the maximum score of customers in the income group of

Rs.20001 to Rs.30000 (125) was found to be greater than that of the other customers.

210

TABLE 4.17

MONTHLY INCOME AND AWARENESS ON RETAIL BANKING

SERVICES – TWO WAY TABLE

Monthly Income Level of Awareness

Low Medium High Total

Up to Rs. 10000 63

(64.29)

154

(41.96)

8

(22.86)

225

Rs.10001 to Rs.20000 19

(19.39)

128

(34.88)

14

(40.00)

161

Rs.20001 to Rs.30000 14

(14.29)

61

(16.62)

11

(31.43)

86

Above Rs.30000 2

(2.04)

24

(6.54)

2

(5.71)

28

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.17 that the high level of awareness

was found to be higher among respondents in the income group of Rs.10001 to

Rs.20000 (40.00 per cent) while the high level of awareness was found to be lower

among the respondents in the income group of above Rs.30000 (5.71 per cent). It

is also observed from the analysis that the medium level of awareness was greater

among the respondents in the income group of up to Rs.10000 (41.96 per cent) and

it was lower among the respondents in the income group of above Rs.30000

(6.54 per cent). The proportion of customers in the income group of up to Rs.10000

having low level of awareness was found to be 64.29 per cent while the proportion

of customers in the income group of above Rs.30000 with low level of awareness

was found to be 2.04 per cent.

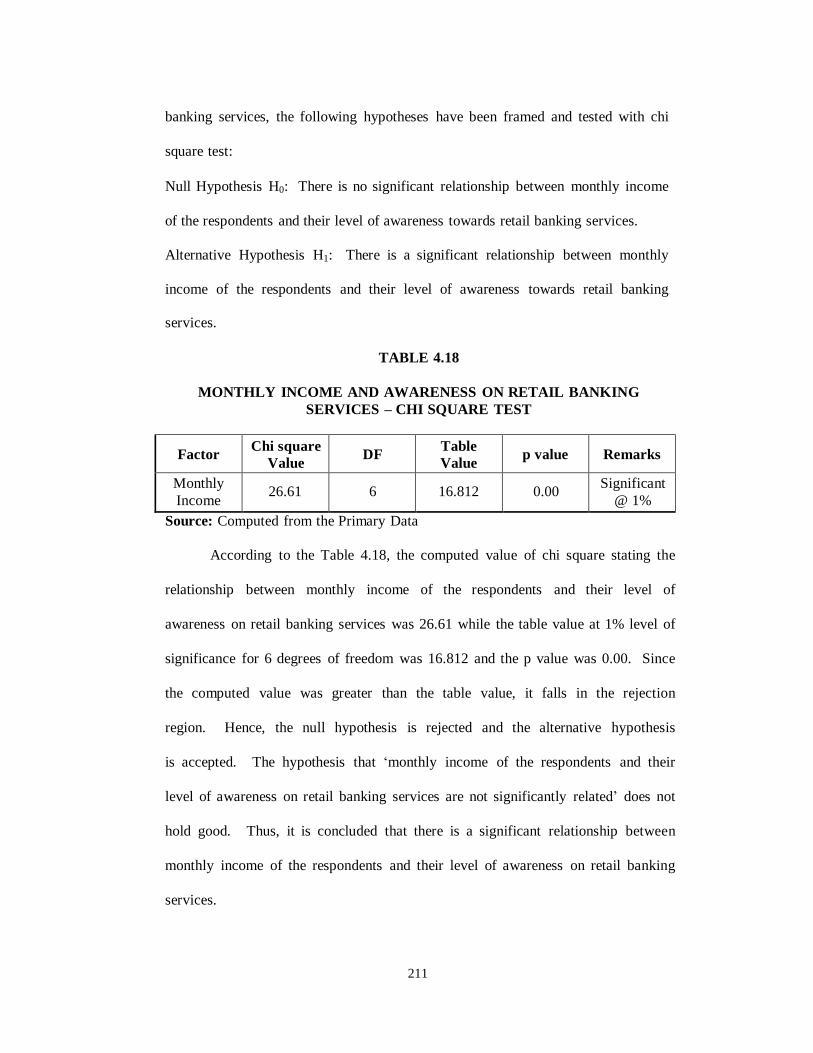

In order to understand the significance of relationship between

monthly income of the respondents and their level of awareness towards retail

211

banking services, the following hypotheses have been framed and tested with chi

square test:

Null Hypothesis H0: There is no significant relationship between monthly income

of the respondents and their level of awareness towards retail banking services.

Alternative Hypothesis H1: There is a significant relationship between monthly

income of the respondents and their level of awareness towards retail banking

services.

TABLE 4.18

MONTHLY INCOME AND AWARENESS ON RETAIL BANKING

SERVICES – CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Monthly

Income

26.61

6

16.812

0.00 Significant

@ 1%

Source: Computed from the Primary Data

According to the Table 4.18, the computed value of chi square stating the

relationship between monthly income of the respondents and their level of

awareness on retail banking services was 26.61 while the table value at 1% level of

significance for 6 degrees of freedom was 16.812 and the p value was 0.00. Since

the computed value was greater than the table value, it falls in the rejection

region. Hence, the null hypothesis is rejected and the alternative hypothesis

is accepted. The hypothesis that ‘monthly income of the respondents and their

level of awareness on retail banking services are not significantly related’ does not

hold good. Thus, it is concluded that there is a significant relationship between

monthly income of the respondents and their level of awareness on retail banking

services.

212

TABLE 4.19

SIZE OF FAMILY AND AWARENESS ON RETAIL BANKING SERVICES

Size of family

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Up to 2 32 6.40 75.56 39 112 16.21

3 to 4 337 67.40 71.80 33 125 14.43

More than 4 131 26.20 70.23 35 110 16.31

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.19 shows that the average score of awareness of customers

in the family size of up to 2 members was found 75.56 which ranged between

39 and 112 with a standard deviation of 16.21. The mean score of awareness

of customers in the family size of 3 to 4 members was found to be 71.80 which

ranged between 33 and 125 with a standard deviation of 14.43. It is also found

that the average score of awareness of customers in the family size of more

than 4 members was 70.23 which ranged between 35 and 110 with a standard

deviation of 16.31.

It denotes that the mean score of awareness of customers in the family

size of up to 2 members (75.56) was higher than the mean score of awareness

of all the other customers. However, the maximum score of customers in the family

size of 3 to 4 members (125) was found to be greater than that of the other

customers.

213

TABLE 4.20

SIZE OF FAMILY AND AWARENESS ON RETAIL BANKING

SERVICES – TWO WAY TABLE

Size of family Level of Awareness

Low Medium High Total

Up to 2 4

(4.08)

23

(6.27)

5

(14.29)

32

3 to 4 63

(64.29)

255

(69.48)

19

(54.29)

337

More than 4 31

(31.63)

89

(24.25)

11

(31.43)

131

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.20 that the high level of awareness

was found to be higher among respondents in the family size of 3 to 4 members

(54.29 per cent) while the high level of awareness was found to be lower among the

respondents in the family size of up to 2 members (14.29 per cent). It is also

observed from the analysis that the medium level of awareness was greater among

the respondents in the family size of 3 to 4 members (69.48 per cent) and it was

lower among the respondents in the family size of up to 2 members (6.27 per cent).

The proportion of customers in the family size of 3 to 4 members having low level

of awareness was found to be 64.29 per cent while the proportion of customers in

the family size of up to 2 members with low level of awareness was found to be

4.08 per cent.

In order to understand the significance of relationship between size of

family of the respondents and their level of awareness towards retail banking

services, the following hypotheses have been framed and tested with chi square test:

Null Hypothesis H0: There is no significant relationship between size of family of

the respondents and their level of awareness towards retail banking services.

214

Alternative Hypothesis H1: There is a significant relationship between size of

family of the respondents and their level of awareness towards retail banking

services.

TABLE 4.21

SIZE OF FAMILY AND AWARENESS ON RETAIL BANKING SERVICES

– CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Size of

family

7.51

4

13.277

0.11 Not

Significant

Source: Computed from the Primary Data

According to the Table 4.21, the computed value of chi square stating the

relationship between size of family of the respondents and their level of awareness

on retail banking services was 7.51 while the table value at 5% level of significance

for 4 degrees of freedom was 13.277 and the p value was 0.11. Since the computed

value was lesser than the table value, it falls in the acceptance region. Hence, the

null hypothesis is accepted and the alternative hypothesis is rejected. The

hypothesis that ‘size of family of the respondents and their level of awareness on

retail banking services are not significantly related’ holds good. Thus, it is

concluded that there is no significant relationship between size of family of the

respondents and their level of awareness on retail banking services.

215

TABLE 4.22

OWNERSHIP PATTERN OF THE BANK AND AWARENESS ON RETAIL

BANKING SERVICES

Ownership

pattern

of the bank

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Nationalized

bank

368

73.60

70.20

33

125

14.80

Private

sector bank

127

25.40

74.93

35

116

14.99

Others 5 1.00 92.40 79 107 11.67

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.22 shows that the average score of awareness of nationalized bank

customers was found to be 70.20 which ranged between 33 and 125 with a standard

deviation of 14.80. The mean score of awareness of private sector bank customers

was found to be 74.93 which ranged between 35 and 116 with a standard deviation

of 14.99. It is also found that the average score of awareness of other

bank customers was 92.40 which ranged between 79 and 107 with a standard

deviation of 11.67.

It denotes that the mean score of awareness of customers of other banks

(92.40) was higher than the mean score of awareness of all the other customers.

However, the maximum score of nationalized bank customers (125) was found to

be greater than that of the other customers.

216

TABLE 4.23

OWNERSHIP PATTERN OF THE BANK AND AWARENESS ON RETAIL

BANKING SERVICES – TWO WAY TABLE

Ownership pattern of the bank Level of Awareness

Low Medium High Total

Nationalized bank 78

(79.59)

272

(74.11)

18

(51.43)

368

Private sector bank 20

(20.41)

93

(25.34)

14

(40.00)

127

Others 0

(0.00)

2

(0.54)

3

(8.57)

5

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.23 that the high level of awareness

was found to be higher among nationalized bank customers (51.43 per cent) while

the high level of awareness was found to be lower among the customers of other

banks (8.57 per cent). It is also observed from the analysis that the medium level

of awareness was greater among the nationalized bank customers (74.11 per cent)

and it was lower among the customers of other banks (0.54 per cent). The

proportion of nationalized bank customers having low level of awareness was found

to be 79.59 per cent while the proportion of private sector bank customers with low

level of awareness was found to be 20.41 per cent.

In order to understand the significance of relationship between ownership

pattern of the banks of the respondents and their level of awareness towards retail

banking services, the following hypotheses have been framed and tested with chi

square test:

217

Null Hypothesis H0: There is no significant relationship between ownership pattern

of the banks of the respondents and their level of awareness towards retail banking

services.

Alternative Hypothesis H1: There is a significant relationship between ownership

pattern of the banks of the respondents and their level of awareness towards retail

banking services.

TABLE 4.24

OWNERSHIP PATTERN OF THE BANK AND AWARENESS ON RETAIL

BANKING SERVICES – CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Ownership pattern

of the bank

28.53

4

13.277

0.00 Significant

@ 1%

Source: Computed from the Primary Data

According to the Table 4.24, the computed value of chi square stating the

relationship between ownership pattern of the bank of the respondents and their

level of awareness on retail banking services was 28.53 while the table value at 1%

level of significance for 4 degrees of freedom was 13.277 and the p value was 0.00.

Since the computed value was greater than the table value, it falls in the rejection

region. Hence, the null hypothesis is rejected and the alternative hypothesis is

accepted. The hypothesis that ‘ownership pattern of the bank of the respondents

and their level of awareness on retail banking services are not significantly related’

does not hold good. Thus, it is concluded that there is a significant relationship

between ownership pattern of the bank of the respondents and their level of

awareness on retail banking services.

218

TABLE 4.25

PERIOD OF CUSTOMERSHIP AND AWARENESS ON RETAIL

BANKING SERVICES

Period of

customer ship

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Less than 5

years

279

55.80

70.00

35

112

12.83

5 to 10 years 192 38.40 73.48 33 125 16.98

More than 10

years

29

5.80

75.00

43

110

19.77

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.25 shows that the average score of awareness of customers in the

period of customership of less than 5 years was found to be 70.00 which ranged

between 35 and 112 with a standard deviation of 12.83. The mean score of

awareness of customers in the period of customership of 5 to 10 years was found to

be 73.48 which ranged between 33 and 125 with a standard deviation of 16.98. It is

also found that the average score of awareness of customers in the period of

customership of more than 10 years was 75.00 which ranged between 43 and 110

with a standard deviation of 19.77.

It denotes that the mean score of awareness of customers in the period of

customership of more than 10 years (75.00) was higher than the mean score of

awareness of all the other customers. However, the maximum score of customers

in the period of customership of 5 to 10 years (125) was found to be greater than

that of the other customers.

219

TABLE 4.26

PERIOD OF CUSTOMERSHIP AND AWARENESS ON RETAIL

BANKING SERVICES – TWO WAY TABLE

Period of customership Level of Awareness

Low Medium High Total

Less than 5 years 54

(55.10)

218

(59.40)

7

(20.00)

279

5 to 10 years 35

(35.71)

136

(37.06)

21

(60.00)

192

More than 10 years 9

(9.18)

13

(3.54)

7

(20.00)

29

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.26 that the high level of awareness

was found to be higher among bank customers for 5 to 10 years (60.00 per cent)

while the high level of awareness was found to be lower among the bank customers

for less than 5 years (20.00 per cent). It is also observed from the analysis that the

medium level of awareness was greater among the bank customers for less than 5

years (59.40 per cent) and it was lower among the bank customers for more than 10

years (3.54 per cent). The proportion of bank customers for less than 5 years

having low level of awareness was found to be 55.10 per cent while the proportion

of bank customers for more than 10 years with low level of awareness was found to

be 9.18 per cent.

In order to understand the significance of relationship between period of

customership of the respondents and their level of awareness towards retail banking

services, the following hypotheses have been framed and tested with chi square test:

220

Null Hypothesis H0: There is no significant relationship between period of

customership of the respondents and their level of awareness towards retail banking

services.

Alternative Hypothesis H1: There is a significant relationship between period of

customership of the respondents and their level of awareness towards retail banking

services.

TABLE 4.27

PERIOD OF CUSTOMERSHIP AND AWARENESS ON RETAIL

BANKING SERVICES – CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p

value

Remarks

Period of

customership

30.84

4

13.277

0.00 Significant @

1%

Source: Computed from the Primary Data

According to the Table 4.27, the computed value of chi square stating the

relationship between period of customership of the respondents and their level of

awareness on retail banking services was 30.84 while the table value at 1% level of

significance for 4 degrees of freedom was 13.277 and the p value was 0.00. Since

the computed value was greater than the table value, it falls in the rejection region.

Hence, the null hypothesis is rejected and the alternative hypothesis is accepted.

The hypothesis that ‘period of customership of the respondents and their level of

awareness on retail banking services are not significantly related’ does not hold

good. Thus, it is concluded that there is a significant relationship between period of

customership of the respondents and their level of awareness on retail banking

services.

221

TABLE 4.28

FREQUENCY OF OPERATIONS AND AWARENESS ON RETAIL

BANKING SERVICES

Frequency of

operations

No. of

respondents

%

Mean

Minimum

Maximum

S.D.

Daily 15 3.00 89.33 66 110 15.45

Frequently 95 19.00 74.35 48 109 12.56

Rarely 113 22.60 70.53 39 103 15.83

As and when

needed

266

53.20

69.73

33

125

14.77

Others 11 2.20 81.18 50 100 13.82

Total 500 100.00 71.63 33 125 15.08

Source: Computed from the Primary Data

Table 4.28 shows that the average score of awareness of daily using

customers was found to be 89.33 which ranged between 66 and 110 with a standard

deviation of 15.45. The mean score of awareness of frequently using customers

was found to be 74.35 which ranged between 48 and 109 with a standard deviation

of 12.56. It is also found that the average score of awareness of rarely using

customers was 70.53 which ranged between 39 and 103 with a standard deviation of

15.83 while the average score of awareness of customers using retail banking

services as and when needed was found to be 69.73 which ranged between 33 and

125 with a standard deviation of 14.77. The average score of awareness of other

customers was found to be 81.18 with a minimum of 50 and a maximum score of

100 while the standard deviation was 13.82.

It denotes that the mean score of awareness of daily using customers (89.33)

was higher than the mean score of awareness of all the other customers. However,

the maximum score of customers using retail banking services as and when needed

(125) was found to be greater than that of the other customers.

222

TABLE 4.29

FREQUENCY OF OPERATIONS AND AWARENESS ON RETAIL

BANKING SERVICES – TWO WAY TABLE

Frequency of

operations

Level of Awareness

Low Medium High Total

Daily 0

(0.00)

7

(1.91)

8

(22.86)

15

Frequently 14

(14.29)

75

(20.44)

6

(17.14)

95

Rarely 26

(26.53)

75

(20.44)

12

(34.29)

113

As and when

needed

57

(58.16)

201

(54.77)

8

(22.86)

266

Others 1

(1.02)

9

(2.45)

1

(2.86)

11

Total 98 367 35 500

Source: Computed from the Primary Data

It could be understood from the Table 4.29 that the high level of awareness

was found to be higher among rarely using customers (34.29 per cent) while the

high level of awareness was found to be lower among the other customers

(2.86 per cent). It is also observed from the analysis that the medium level of

awareness was greater among the bank customers using retail banking services as

and when needed (54.77 per cent) and it was lower among the customers using the

retail banking services daily (1.91 per cent). The proportion of bank customers

using the retail banking services as and when needed having low level of awareness

was found to be 58.16 per cent while the proportion of other customers with low

level of awareness was found to be 1.02 per cent.

In order to understand the significance of association between frequency of

operations of the respondents and their level of awareness towards retail banking

services, the following hypotheses have been framed and tested with chi square test:

223

Null Hypothesis H0: There is no significant association between frequency of

operations of the respondents and their level of awareness towards retail banking

services.

Alternative Hypothesis H1: There is a significant association between frequency of

operations of the respondents and their level of awareness towards retail banking

services.

TABLE 4.30

FREQUENCY OF OPERATIONS AND AWARENESS ON RETAIL

BANKING SERVICES – CHI SQUARE TEST

Factor Chi square

Value

DF Table

Value

p value

Remarks

Frequency of

Operations

63.03

8

20.09

0.00 Significant

@ 1%

Source: Computed from the Primary Data

According to the Table 4.30, the computed value of chi square stating the

association between frequency of operations of the respondents and their level of

awareness on retail banking services was 63.03 while the table value at 1% level of

significance for 8 degrees of freedom was 20.09 and the p value was 0.00. Since

the computed value was greater than the table value, it falls in the rejection region.

Hence, the null hypothesis is rejected and the alternative hypothesis is accepted.

The hypothesis that ‘frequency of operations of the respondents and their level of

awareness on retail banking services are not significantly related’ does not hold

good. Thus, it is concluded that there is a significant association between frequency

of operations of the respondents and their level of awareness on retail banking

services.