chapter brealey, myers, and allen principles of corporate finance 11th global edition the value of...

TRANSCRIPT

Chapter

Brealey, Myers, and Allen

Principles of Corporate Finance

11th Global Edition

THE VALUE OF COMMON STOCKS

4

4-4-22

4-1 HOW COMMON STOCKS ARE TRADED

•Primary Market• New securities

•Secondary Market• Previously-issued securities

•Common Stock• Ownership shares in publicly-held corporation

4-4-33

4-1 HOW COMMON STOCKS ARE TRADED

• Electronic Communication Networks (ECNs)• Computer networks that allow electronic trading

• Exchange-Traded Funds (ETFs)• Stock portfolios bought/sold in single trade

4-4-44

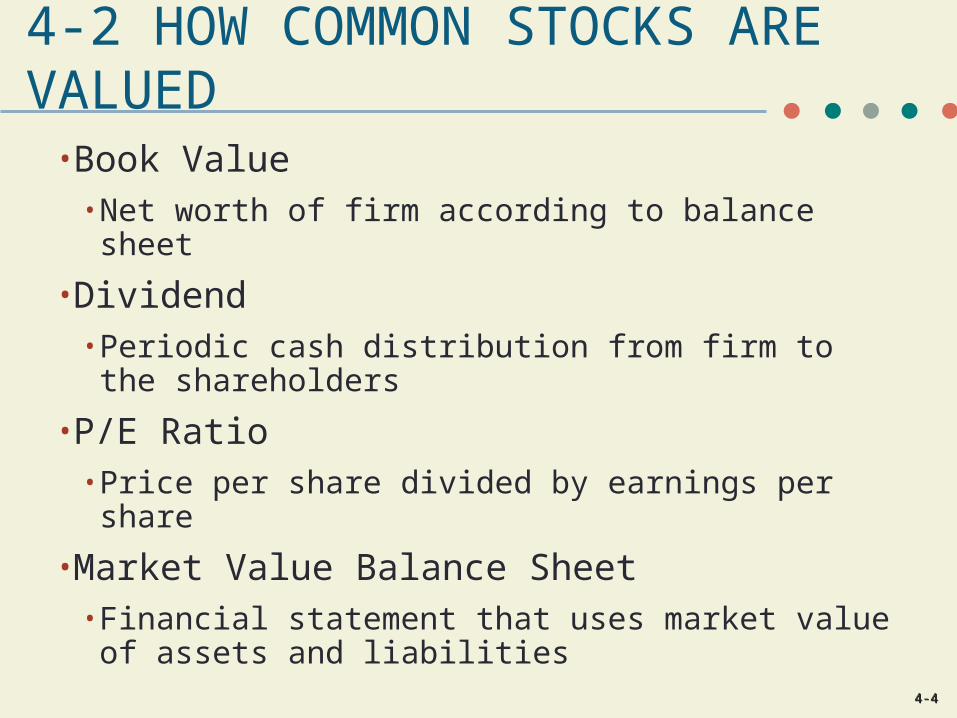

4-2 HOW COMMON STOCKS ARE VALUED

• Book Value• Net worth of firm according to balance sheet

• Dividend• Periodic cash distribution from firm to the shareholders

• P/E Ratio• Price per share divided by earnings per share

• Market Value Balance Sheet• Financial statement that uses market value of assets and liabilities

4-4-55

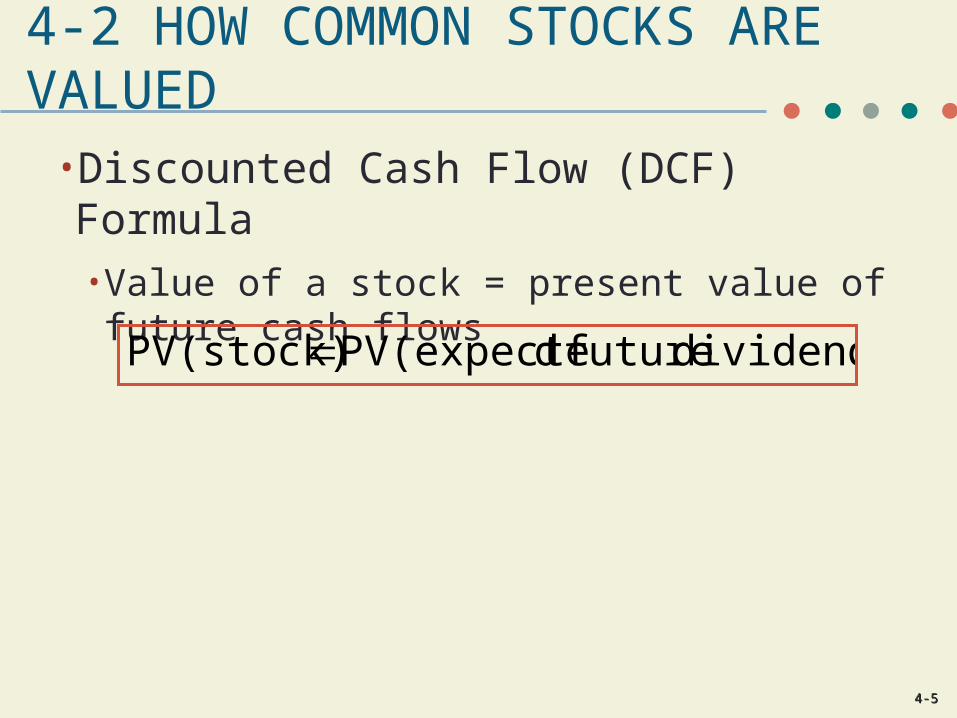

4-2 HOW COMMON STOCKS ARE VALUED

• Discounted Cash Flow (DCF) Formula• Value of a stock = present value of future cash flows

dividends) future dPV(expectePV(stock)

4-4-66

4-2 HOW COMMON STOCKS ARE VALUED

• Expected Return• Percentage yield forecast from specific investment over time period

• Sometimes called market capitalization rate

4-4-77

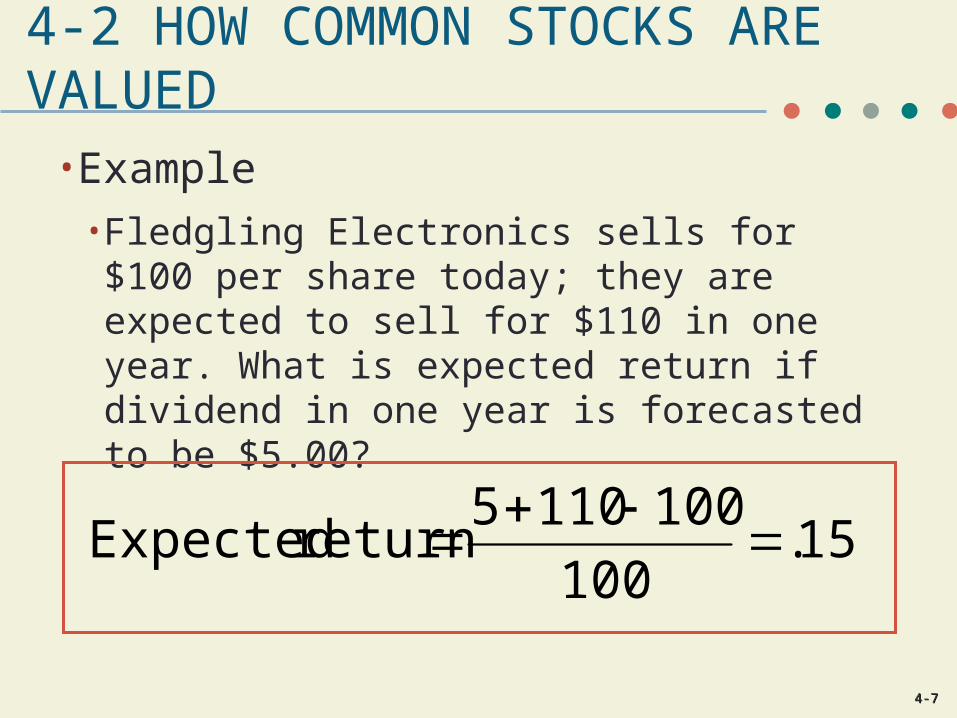

4-2 HOW COMMON STOCKS ARE VALUED

• Example• Fledgling Electronics sells for $100 per share today; they are expected to sell for $110 in one year. What is expected return if dividend in one year is forecasted to be $5.00?

15.100

1001105return Expected

4-4-88

4-2 HOW COMMON STOCKS ARE VALUED

• Price of share of stock is present value of future cash flows

• For a stock, future cash flows are dividends and ultimate sales price

r

PDivP

1

Price 110

4-4-99

4-2 HOW COMMON STOCKS ARE VALUED

•Example• Fledgling Electronics price

10015.1

1105Price 0

P

4-4-1010

4-2 HOW COMMON STOCKS ARE VALUED

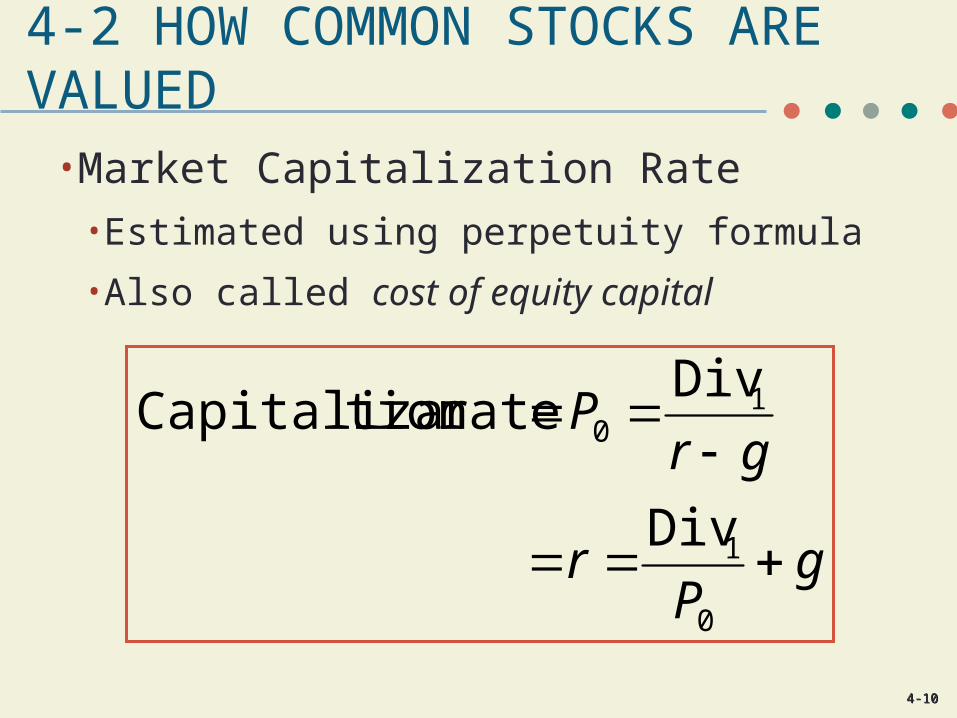

• Market Capitalization Rate• Estimated using perpetuity formula

• Also called cost of equity capital

gP

r

grP

0

1

10

Div

Divratetion Capitaliza

4-4-1111

4-2 HOW COMMON STOCKS ARE VALUED

• Dividend Discount Model• Computation of today’s stock price: share value equals present value of all expected future dividends

• H: Time horizon for investment

HHH

r

PDiv

r

Div

r

DivP

)1(...

)1()1( 22

11

0

4-4-1212

4-2 HOW COMMON STOCKS ARE VALUED

• Modified Formula

HHH

r

PDiv

r

Div

r

DivP

)1(...

)1()1( 22

11

0

HH

H

ttt

r

P

r

DivP

)1()1(10

4-4-1313

4-2 HOW COMMON STOCKS ARE VALUED

• Example• Fledgling Electronics forecasted to pay $5.00 dividend at end of year 1 and $5.50 dividend at end of year 2. End-of-second-year stock will be sold for $121. Discount rate is 15%. What is the price of stock?

00.100$PV

)15.1(

12150.5

)15.1(

00.5PV

21

4-4-1414

4-2 HOW COMMON STOCKS ARE VALUED

• Example• XYZ Company will pay dividends of $3, $3.24, and $3.50 over next three years. After three years, stock sells for $94.48. What is the price of stock given 12% expected return?

00.75$PV

)12.1(

48.9450.3

)12.1(

24.3

)12.1(

00.3PV

321

4-4-1515

4-2 HOW COMMON STOCKS ARE VALUED

4-4-1616

4-3 ESTIMATING COST OF EQUITY CAPITAL

•Dividend Yield• Expected return on stock investment plus expected dividend growth

• Similar to capitalization rate

gP

Divr

gr

DivP

0

1

10

yield Dividend

Price

4-4-1717

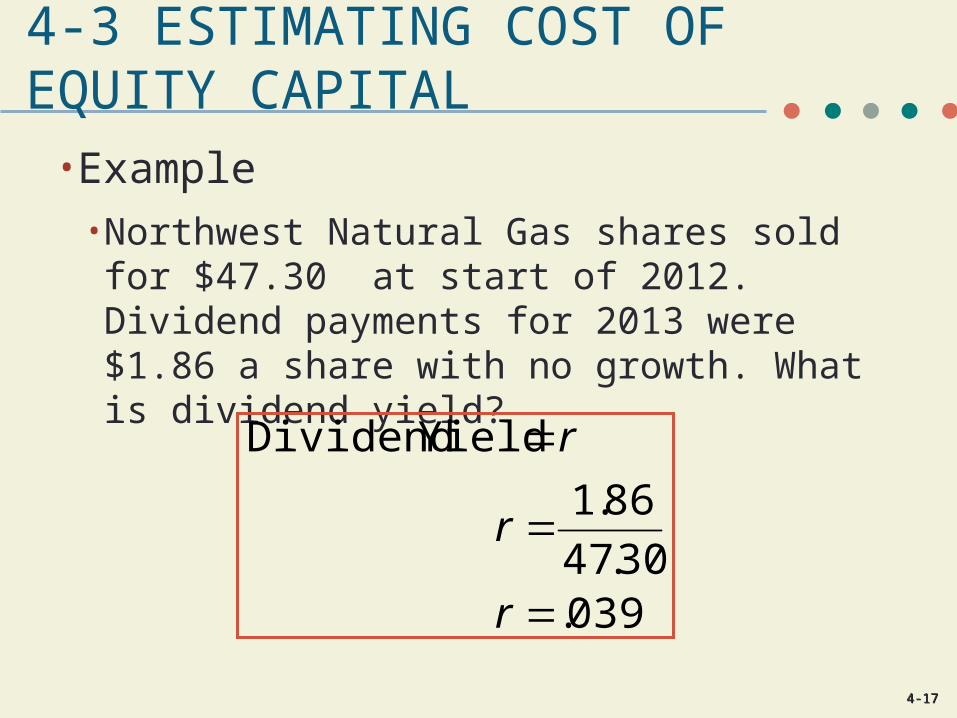

4-3 ESTIMATING COST OF EQUITY CAPITAL

• Example• Northwest Natural Gas shares sold for $47.30 at start of 2012. Dividend payments for 2013 were $1.86 a share with no growth. What is dividend yield?

039.30.47

86.1

Yield Dividend

r

r

r

4-4-1818

4-3 ESTIMATING COST OF EQUITY CAPITAL

• Example• Northwest Natural Gas shares sold for $47.30 at start of 2012. Dividend payments for 2013 were $1.86 a share with 4.6% growth. What is r?

085.

046.30.47

86.1

r

r

4-4-1919

4-3 ESTIMATING COST OF EQUITY CAPITAL

• Return Measurements

0

1yield DividendP

Div

shareper equity Book

EPSROE

ROEEquityon Return

4-4-2020

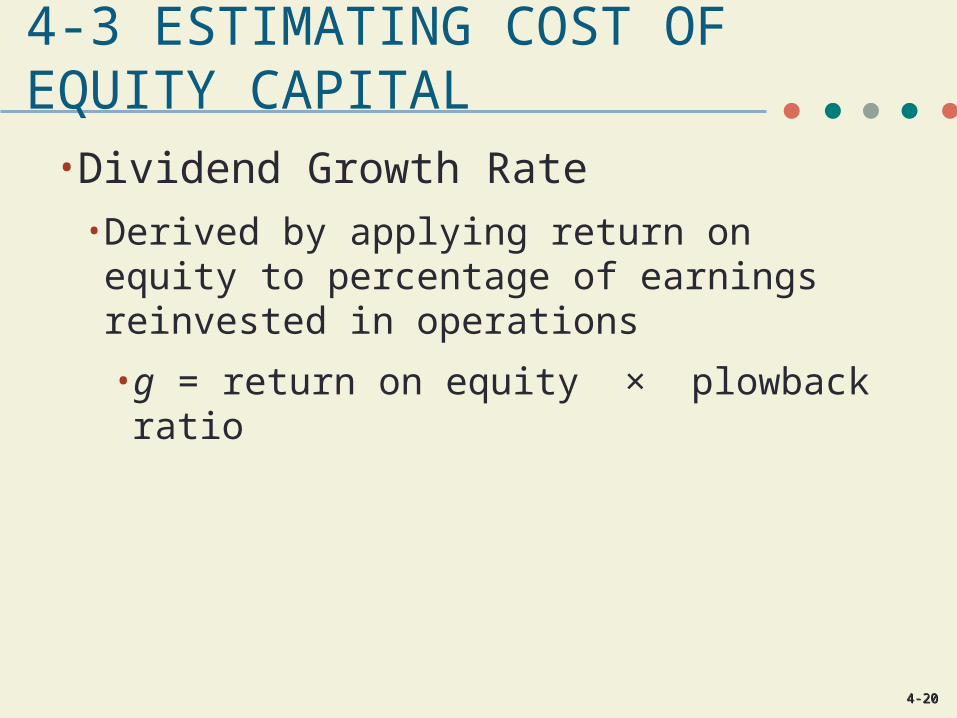

4-3 ESTIMATING COST OF EQUITY CAPITAL

• Dividend Growth Rate• Derived by applying return on equity to percentage of earnings reinvested in operations

• g = return on equity × plowback ratio

4-4-2121

4-3 ESTIMATING COST OF EQUITY CAPITAL

• Valuing Non-Constant Growth

HH

HH

r

P

r

Div

r

Div

r

Div

)1()1(...

)1()1(PV

22

11

gr

DivP HH

1

4-4-2222

4-3 ESTIMATING COST OF EQUITY CAPITAL

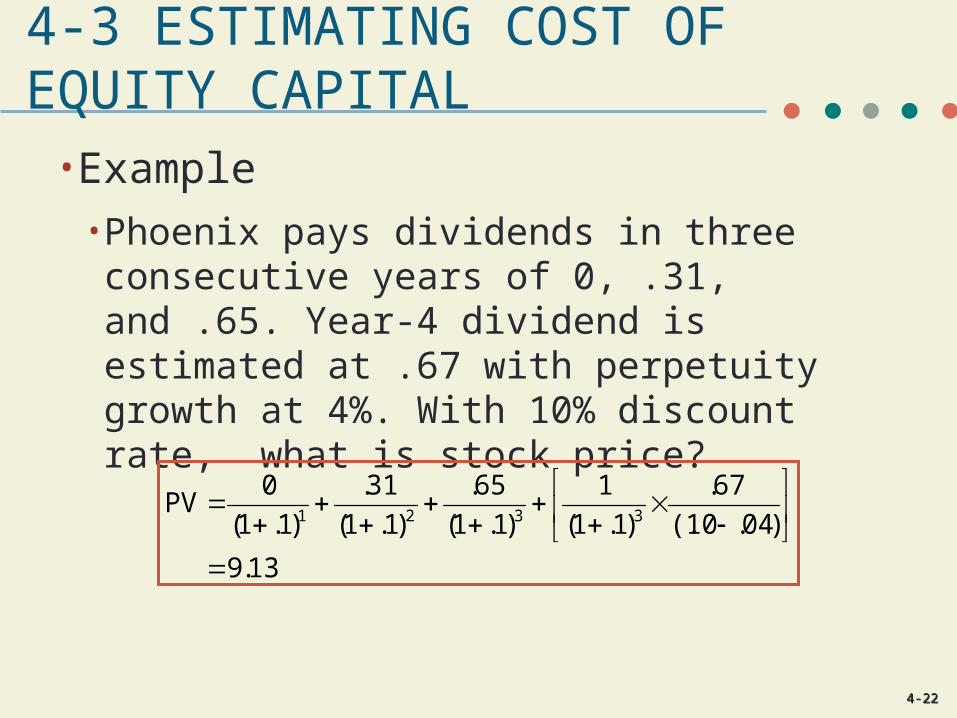

• Example• Phoenix pays dividends in three consecutive years of 0, .31, and .65. Year-4 dividend is estimated at .67 with perpetuity growth at 4%. With 10% discount rate, what is stock price?

13.9

)04.10(.

67.

)1.1(

1

)1.1(

65.

)1.1(

31.

)1.1(

0PV

3321

4-4-2323

4-4 STOCK PRICE AND EARNINGS PER SHARE

• If firm pays lower dividend and reinvests funds, stock price may increase due to higher future dividends

• Payout Ratio• Fraction of earnings paid out as dividends

• Plowback Ratio • Fraction of earnings retained by firm

4-4-2424

4-4 STOCK PRICE AND EARNINGS PER SHARE

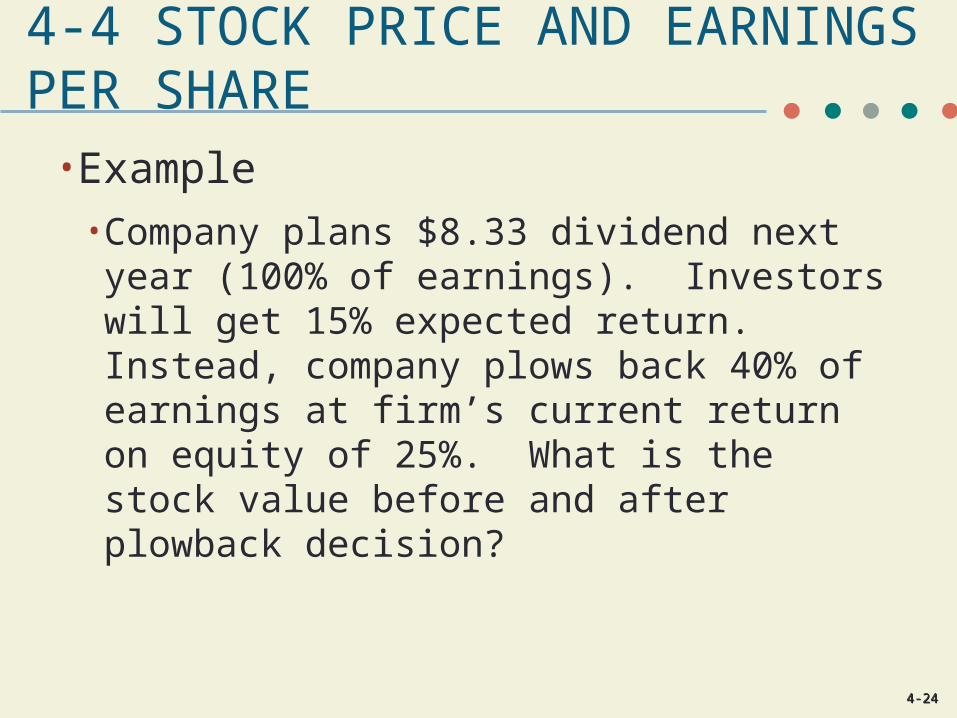

• Example• Company plans $8.33 dividend next year (100% of earnings). Investors will get 15% expected return. Instead, company plows back 40% of earnings at firm’s current return on equity of 25%. What is the stock value before and after plowback decision?

4-4-2525

4-4 STOCK PRICE AND EARNINGS PER SHARE

• Example, continued• No Growth

• With Growth

56.55$15.

33.80 P

00.100$10.15.

00.5

10.40.25.

0

P

g

4-4-2626

4-4 STOCK PRICE AND EARNINGS PER SHARE

• Example, continued• Stock price remains at $55.56 with no earnings plowed back

• With plowback, price is $100.00

• Difference is called present value of growth opportunities (PVGO)

44.44$56.5500.100PVGO

4-4-2727

4-4 STOCK PRICE AND EARNINGS PER SHARE

• Present Value of Growth Opportunities (PVGO)• Net present value of firm’s future investments

• Sustainable Growth Rate• Steady rate at which firm can grow: plowback ratio x return on equity

4-4-2828

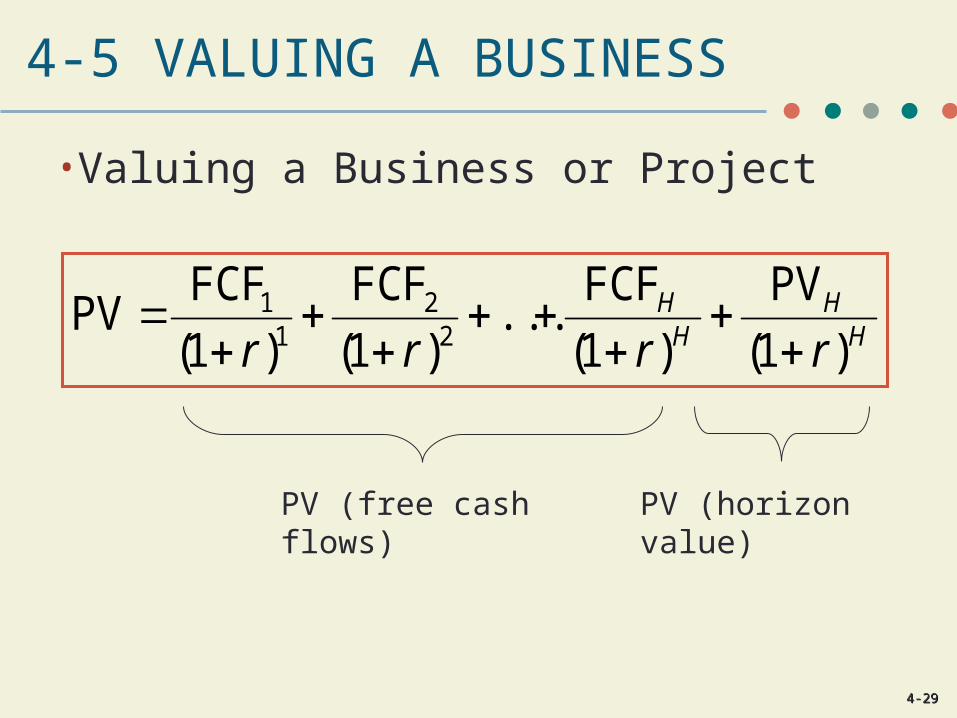

4-5 VALUING A BUSINESS

• Valuing a Business or Project• Usually computed as discounted value of FCF to valuation horizon (H)

• Valuation horizon sometimes called terminal value and calculated like PVGO

HH

HH

rrrr )1(

PV

)1(

FCF...

)1(

FCF

)1(

FCFPV

22

11

4-4-2929

4-5 VALUING A BUSINESS

• Valuing a Business or Project

HH

HH

rrrr )1(

PV

)1(

FCF...

)1(

FCF

)1(

FCFPV

22

11

PV (free cash flows) PV (horizon value)

4-4-3030

4-5 VALUING A BUSINESS

• Example• Given cash flows for Concatenator Manufacturing Division, calculate PV of near-term cash flows, PV (horizon value), and total value of firm; r = 10% and g = 6%

4-4-3131

4-5 VALUING A BUSINESS

• Example, Continued

4.22

06.10.

59.1

1.1

1 value)PV(horizon 6

6.3

1.1

23.

1.1

20.

1.1

39.1

1.1

15.1

1.1

96.

1.1

.80PV(FCF) 65432

4-4-3232

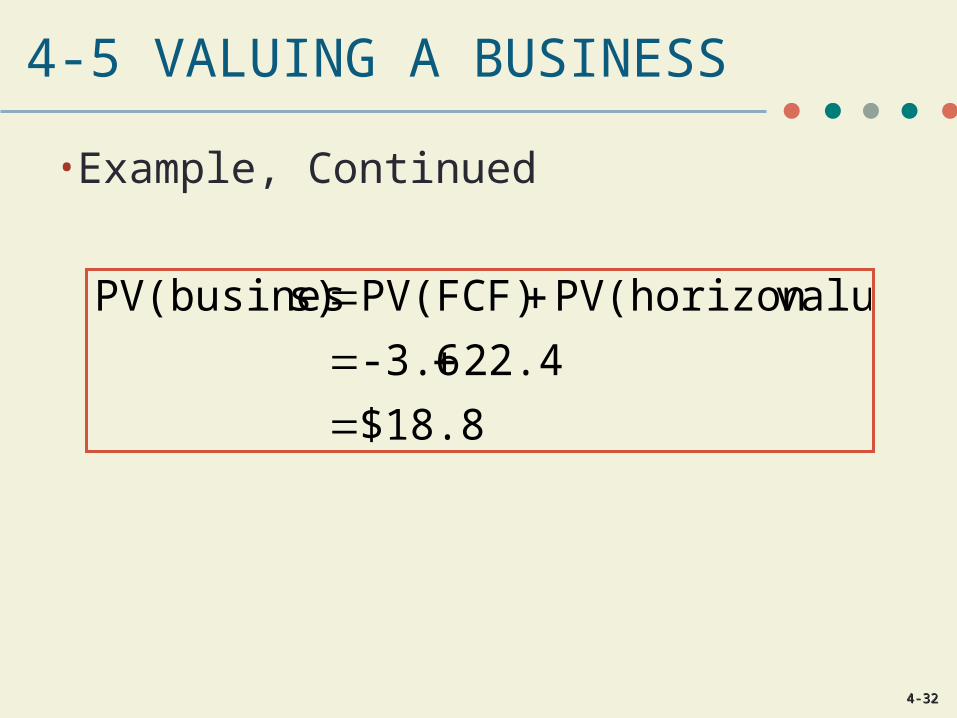

4-5 VALUING A BUSINESS

• Example, Continued

$18.8

22.4-3.6

value)PV(horizonPV(FCF)s)PV(busines