chapter 7 banking system: a price-theoretic model … ii, prof. dr. t. wollmershäuser, slide 15...

TRANSCRIPT

ME II, Prof. Dr. T. Wollmershäuser

Chapter 7Banking System: A

Price-theoretic Model of Loan Supply

Version: 08.07.2010

ME II, Prof. Dr. T. Wollmershäuser, Slide 2

The demand for money of firms or private households is identical with the demand for credit

Credit supply of a bankleads to a demand for central bank money

Supply of central bank money by other banks via

the interbank money market

Supply of central bank money by the ECB via open

market operations

Control over the refinancing costs (i.e. the costs of central bank money) via monetary policy instruments of the ECB

Structure of the money supply / credit supply process

The Role of Banks

ME II, Prof. Dr. T. Wollmershäuser, Slide 3

ECB has control over money market interest rates and refinancing costs

ECB is able to influence the interest rates set by commercial banks for credits to the private sector

Purpose of monetary policy

The Role of Banks

ME II, Prof. Dr. T. Wollmershäuser, Slide 4

The Role of Banks

So far: Money = Currency / Cash (M = CU)The central bank has direct control over the amount of cash in the hands of the private sector.

Now: Money = Cash + Checkable Deposits (M = CU + D)Money is held for transaction purposes

• Checkable deposits D are above all demand deposit accountsBanks are institutions that receive funds from people and firms,and use these funds to buy bonds or stocks, or to make loans to other people and firms.

• Banks receive funds from people and firms who either deposit funds directly or have funds sent to their checking accounts.

• The liabilities of the banks are therefore equal to the value of these checkable deposits D.

• Banks are subject to reserve requirements: a fraction θ of the deposits D is held as reserves R at the central bank (R = θ⋅D)

ME II, Prof. Dr. T. Wollmershäuser, Slide 5

The Role of Banks

Central banks are monopolistic suppliers of central bank money H

• Central bank money = Currency + Reserves (H = CU + R)• Central bank money = Money used for both, transactions

between the central bank and commercial banks, and transactions among commercial banks

Giving a new credit is creation of money (increase in the money supply), since a new credit to the private sector either leads to deposits (in case it is booked to the people’s account) or to cash (in case it is disbursed)

• In both cases the new credit has to be refinanced by new centralbank money (due to minimum reserve or cash requirements).

ME II, Prof. Dr. T. Wollmershäuser, Slide 6

Balance Sheets

Central Bank

Assets Liabilities

Credits to domestic banks

Currency

Reserves

Commercial Bank

Assets Liabilities

Reserves

Credits todomestic

non-banks

Deposits

Liab. againstcentral bank

Capital

Central bank m

oney

ME II, Prof. Dr. T. Wollmershäuser, Slide 7

Consolidated Balance Sheets

Banking System

Assets Liabilities

Currency

Deposits

Capital

Money M

1

Non-banking System

Assets Liabilities

DebtCurrency

Deposits

Capital

Tangible assets

Credits todomestic

non-banks

ME II, Prof. Dr. T. Wollmershäuser, Slide 8

Consolidated Balance Sheet of Euro Area MFIs

(in EUR billions; outstanding amounts at end of period)

ME II, Prof. Dr. T. Wollmershäuser, Slide 9

The Supply and the Demand for Central Bank Money

P

P

Credit demand of private households

and firms

ME II, Prof. Dr. T. Wollmershäuser, Slide 10

The Supply and the Demand for Central Bank Money

Demand for currency/cash: c … Cash holding ratiod dCU cM=

Demand for checkable deposits: (1 )d dD c M= −

Relation between deposits (D) and reserves (R):θ … Reserve coefficient

Demand for reserves by banks:

Demand for central bank money: d d dH CU R= +

Then:

R Dθ=

( )1d dR c Mθ= −

( ) ( )1 1d d d dH cM c M c c Mθ θ⎡ ⎤= + − = + −⎣ ⎦

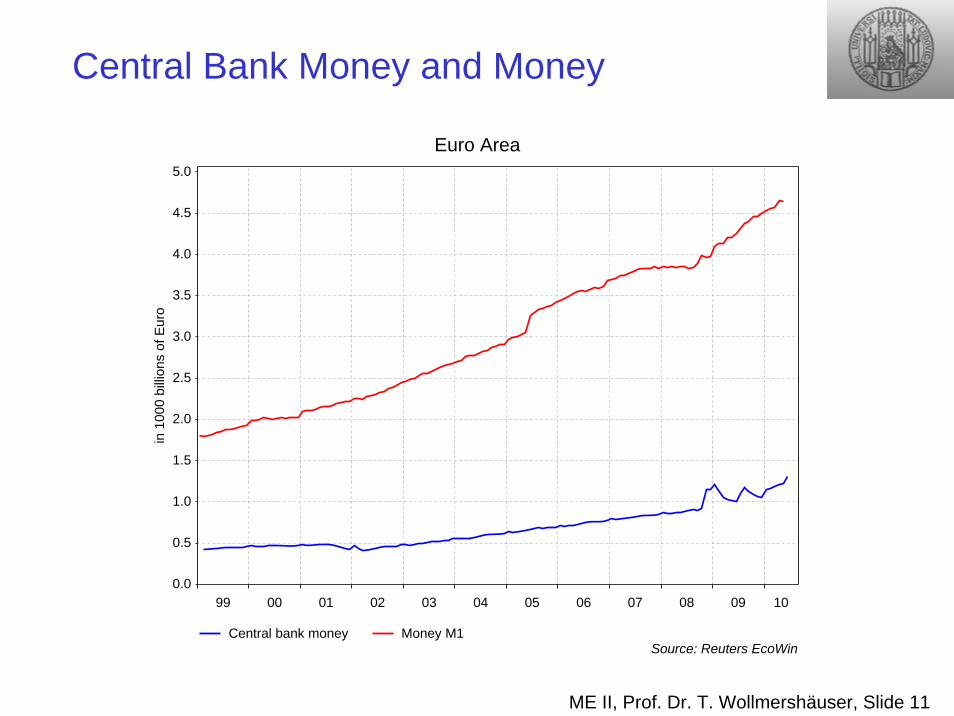

ME II, Prof. Dr. T. Wollmershäuser, Slide 11

Central Bank Money and Money

Euro Area

Central bank money Money M1Source: Reuters EcoWin

99 00 01 02 03 04 05 06 07 08 09 10

in 1

000

billi

ons

of E

uro

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

ME II, Prof. Dr. T. Wollmershäuser, Slide 12

Central Bank Money and Money

Euro Area

MultiplierSource: Reuters EcoWin

99 00 01 02 03 04 05 06 07 08 09 100

1

2

3

4

5

6

7

8

Multiplier:

( )θ= =

+ −11

MmH c c

ME II, Prof. Dr. T. Wollmershäuser, Slide 13

Market for Central Bank Money

In equilibrium, the supply of central bank money (H) is equal to the demand for central bank money (Hd):

dH H=

Or restated as:

[ ] 1(1 )θ= + − =H c c M Mm

Special cases: c = 1 and c = 0θ = 1 (100% reserves)

ME II, Prof. Dr. T. Wollmershäuser, Slide 14

Market for Central Bank Money

The equilibrium interest rate is such that the supply of central bank money is equal to the demand for central bank money.

Equilibrium in the Market for Central Bank Money and the Determination of the Interest Rate

ME II, Prof. Dr. T. Wollmershäuser, Slide 15

Price-theoretic Model of Loan Supply

Equilibrium on the credit market is not only determined by the demand for credits (which is equal to the demand for money), but also by the supply of credits and hence by the behavior of banks.The price-theoretic model of the credit market comprises:

Market for money M1 / for credits from banks to non-banks• Money / credit demand of non-banks• Money / credit supply of banks

Market for central bank money / for credits from the central bank to banks

• Banks’ demand for central bank mony• Central bank as monopolistic supplier

Multiplier as link

ME II, Prof. Dr. T. Wollmershäuser, Slide 16

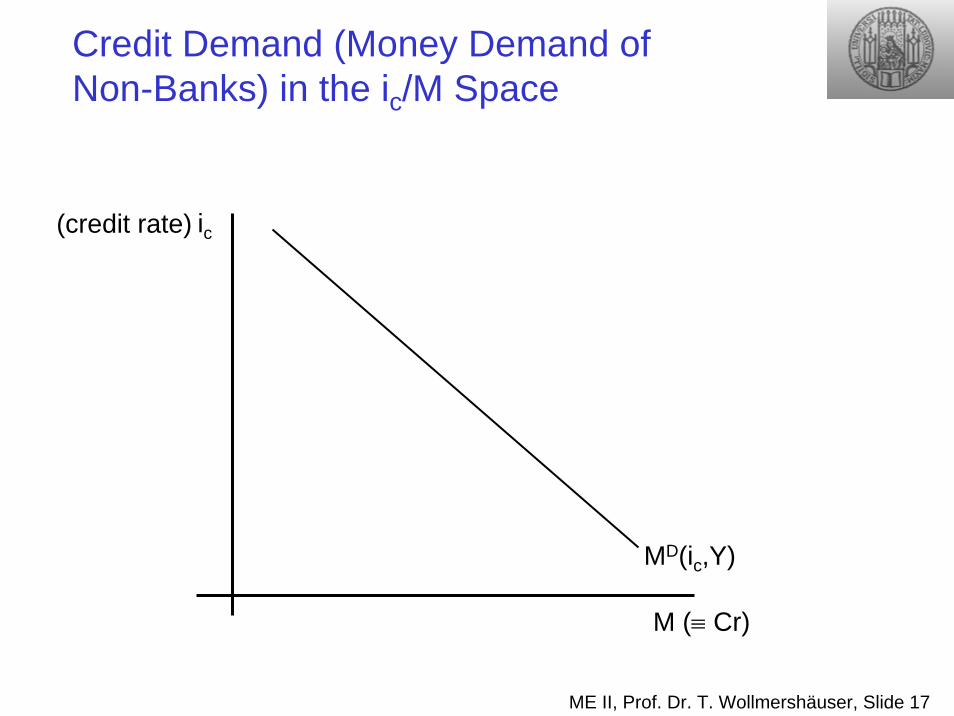

Credit Demand of Non-Banks

Starting point:Money demand ≡ credit demandMoney demand function as in the IS-LM modelCrD ≡ MD = MD(ic,Y)

∂MD / ∂ic < 0 (opportunity costs of holding money) ∂MD / ∂Y > 0 (transaction motive)

ME II, Prof. Dr. T. Wollmershäuser, Slide 17

MD(ic,Y)

ic(credit rate)

Credit Demand (Money Demand of Non-Banks) in the ic/M Space

M (≡ Cr)

ME II, Prof. Dr. T. Wollmershäuser, Slide 18

Credit Supply of an Individual Bank j

Revenues from credit business: iC⋅Crj

Refinancing costsprivate sector deposits: iD⋅Dj

central bank credits: iR⋅CrjECB

Minimum reserves Rj (which depend on the level of deposits) are remunerated at iR: iR⋅Rj

Default costs: β⋅(Crj)2/Yprobability of a default (β⋅Crj/Y) times the volume of credits (Crj)assumption: credit risks increase more than proportionally with the credit volume

ME II, Prof. Dr. T. Wollmershäuser, Slide 19

Profit function: Π j = iC⋅Cr j – iD⋅Dj – iR⋅(Crj

ECB – Rj) – β (Crj )2 /YBalance sheet identity:Cr j + Rj = Dj + Crj

ECB ⇒ CrjECB – Rj = Cr j – Dj

Profit function: Π j = (iC – iR)⋅Cr j – (iD – iR)⋅Dj – β (Crj )2 /YProfit maximization:∂Π j/ ∂Crj =iC – iR – 2β Crj /Y = 0Optimal supply of credit:Crj = (iC – iR)Y/ 2β

Credit Supply of an Individual Bank j

ME II, Prof. Dr. T. Wollmershäuser, Slide 20

Determinants of Credit Supply

Interest rate spread (mark-up over marginal costs)IncomeCredit risk

⇒aggregate over all banks:

CrS = (iC – iR)nY/2β

n … number of banks

ME II, Prof. Dr. T. Wollmershäuser, Slide 21

Credit Supply and Credit Demand in the ic/M Space

Crs(ic,iR,n,Y,β)ic

ic0

Cr0=M0 M (≡ Cr)

MD (≡ CrD)

ME II, Prof. Dr. T. Wollmershäuser, Slide 22

Effects of Changes in the Refinancing Costs iR on the Credit Market

Initial demand of banks for central bank money: H0 = (1/m)⋅Cr0

What are the effects of changes in iR on the demand for H?An increase in iR shifts the credit supply to the upper left, since the interest rate spread decreases.For a given credit demand credit interest rates increase and the equilibrium credit volume decresesto Cr1.Thus, the demand for central bank money also decreases to H1 = (1/m)⋅Cr1

ME II, Prof. Dr. T. Wollmershäuser, Slide 23

Effects of Changes in the Refinancing Costs iR on the Credit Market

Crs(ic,iR0,n,Y,β)ic

ic0

Cr0=M0 M (≡ Cr)

MD (≡ CrD)

ME II, Prof. Dr. T. Wollmershäuser, Slide 24

Higher Refinancing Costs Shift the Credit Supply to the Upper Left

Crs(ic,iR0,n,Y,β)ic

ic0

Cr0 M (≡ Cr)

MD (≡ CrD)

Cr1

ic1

Crs(iR1)

ME II, Prof. Dr. T. Wollmershäuser, Slide 25

The Complete Model

Money multiplier Market for central bank money

Interest rate relation

MiR M0*H0*iR0

ic0

icCrs(iR0)

CrD

Credit market

=MmH

H

ME II, Prof. Dr. T. Wollmershäuser, Slide 26

Effects of Lower Refinancing Costs

MiR M0*H0*iR0

ic0

icCrs(iR0)

CrD

iR1

H

=MmH

Money multiplier Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 27

...Increase in the Supply of Credit

MiR

CrD

M0*H0*iR0

ic0

iR1

icCrs(iR0)

Crs(iR1)

ic1

H

=MmH

Money multiplier Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 28

Central Bank Money ↑, Money / Credit Volume ↑, Credit Interest Rates ↓

MiR

CrD

M0*H0*iR0

ic0

icCrs(iR0)

iR1

Crs(iR1)

ic1

M1*

H1*

H

=MmH

Money multiplier Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 29

Effects of Higher Refinancing Costs

MiR M0*

H0*

iR0

ic0

icCrs(iR0)

CrD

iR1

H

=MmH

Money multiplier Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 30

MiR

Crs(iR0)

CrD

M0*

H0*

iR0

ic0

ic

ic1

Crs(iR1)

M1*iR1

H

...Decrease of the Supply of Credit

=MmH

Credit market

Money multiplier Market for central bank money

Interest rate relation

ME II, Prof. Dr. T. Wollmershäuser, Slide 31

MiR

Crs(iR0)

CrD

M0*

H0*

iR0

ic0

ic

ic1

Crs(iR1)

H

Central Bank Money ↓, Money / Credit Volume ↓, Credit Interest Rates ↑

=MmH

Credit market

Money multiplier Market for central bank money

Interest rate relation

ME II, Prof. Dr. T. Wollmershäuser, Slide 32

Summary

The ECB is able • to control the refinancing costs of banks (iR) with its

instruments and• to control the credit interest rates (iC) that non-

banks have to pay for getting credits from banks

ME II, Prof. Dr. T. Wollmershäuser, Slide 33

Empirical Evidence

Per

cent

ME II, Prof. Dr. T. Wollmershäuser, Slide 34

MiR

CrD

M0*

H0*

iR0

ic0

ic Crs(iR0)

=MmH

H

iR1

Crs(iR1)

H1*

M1*

Money multiplier

ic1

Graphical Derivation of the Model

Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 35

Massive Reduction of Credit Demand (Recession)

MiR

CrDiR0

ic0

ic Crs(iR0)

=MmH

H

iR1

Crs(iR1)

ic1

H1*

M1*M0*

H0*

Money multiplier Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 36

ECB is Unable to Stabilize Credit Volume with Conventional Interest Rate Cuts

MiR

CrDiR0

ic0

ic Crs(iR0)

=MmH

H

iR1

Crs(iR1)

ic1

H1*

M1*M0*

H0*iR2 = 0

Crs(iR2)

Money multiplier Market for central bank money

Interest rate relation Credit market

ME II, Prof. Dr. T. Wollmershäuser, Slide 37

Unconventional Measures: Direct Supply of Credit to the Private Sector

MiR

CrDiR0

ic0

ic Crs(iR0)

=MmH

H

iR1

Crs(iR1)

ic1

H1*

M1*M0*

H0*iR2 = 0

Crs(iR2)

Crs(iR2) + CrECB/Private

Money multiplier Market for central bank money

Interest rate relation Credit market